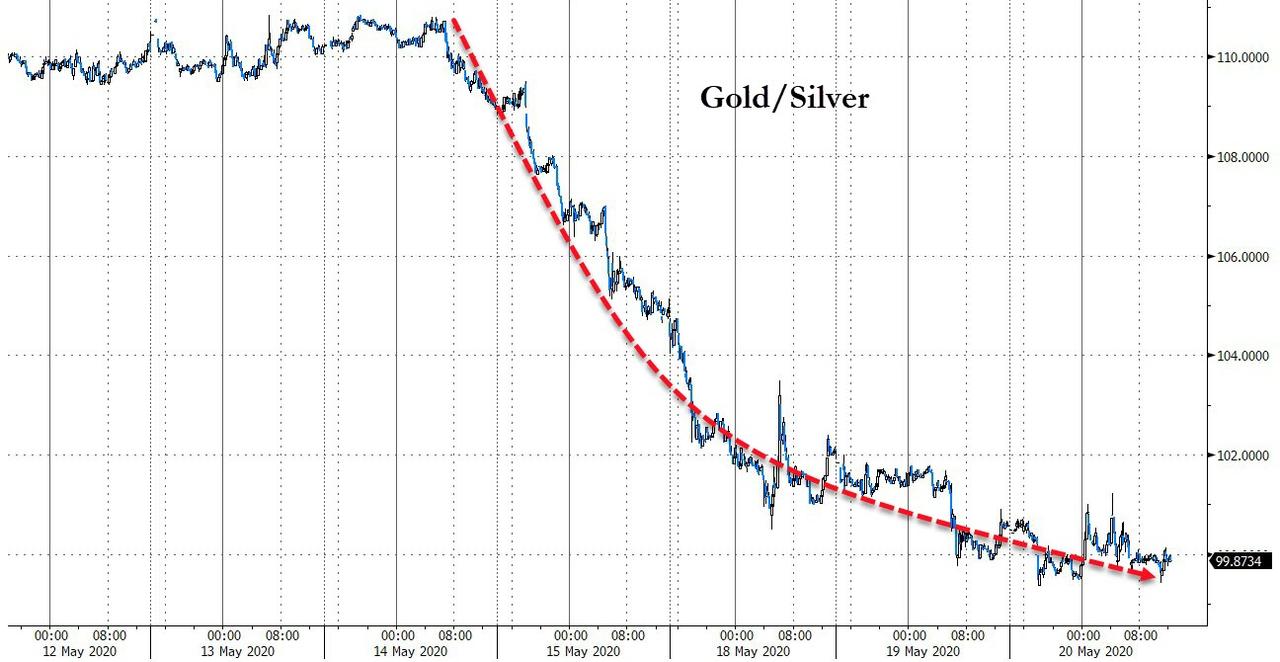

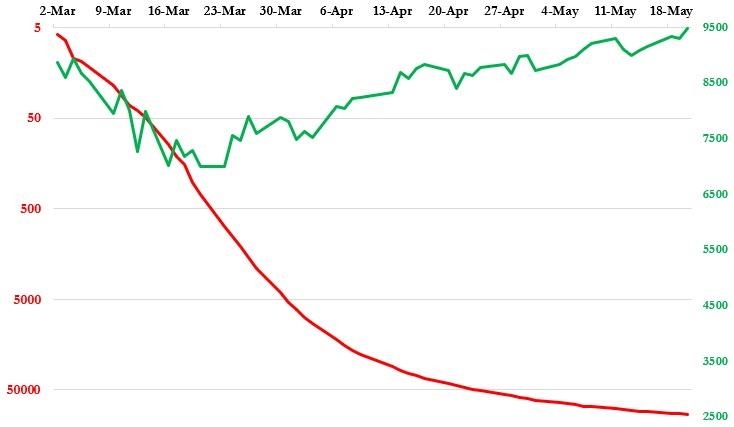

GOLD:$1723.20 DOWN $26.40 The quote is London spot price

Silver:$17.01 DOWN 50 CENTS (London spot closing price

COMEX OPTIONS EXPIRY TUESDAY MAY 26

OTC/LBMA OPTIONS EXPIRY FRIDAY MAY 29

The reason for the raid today is the comex expiry this coming Tuesday.

Expect gold/silver to be subdued in price until after first day notice.

Closing access prices: London spot

i)Gold : $1727.00 LONDON SPOT 4:30 pm

ii)SILVER: $17.11//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

MAY COMEX GOLD: XXX

JUNE GOLD: $1723.20 CLOSE 1.30 PM// SPREAD SPOT (LONDON) VS/FUTURE JUNE: $0.//PREMIUMS WENT UP AGAIN

CLOSING SILVER FUTURE MONTH

SILVER JUNE COMEX CLOSE; $17.32…1:30 PM.//SPREAD SPOT/(LONDON) VS FUTURE JUNE: 31 CENTS PER OZ//PREMIUMS UP AGAIN//HUGE DIFFERENCE

JULY: 1:30 PM: $1738//1:30 PM //SPREAD SPOT LONDON VS FUTURE JULY: 38 CENTS PER OZ//

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2800. usa per oz

and silver; $31.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

DO NOT PAY ANY ATTENTION TO WHAT THE CROOKS ARE DOING AT THE COMEX AND LONDON LBMA..PHYSICAL IS THE NAME OF THE GAME AND NOTHING ELSE

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 1/13

EXCHANGE: COMEX

CONTRACT: MAY 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,750.600000000 USD

INTENT DATE: 05/20/2020 DELIVERY DATE: 05/22/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

118 H MACQUARIE FUT 6

661 C JP MORGAN 1

690 C ABN AMRO 4

737 C ADVANTAGE 6 2

800 C MAREX SPEC 7

____________________________________________________________________________________________

TOTAL: 13 13

MONTH TO DATE: 9,822

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 13 NOTICE(S) FOR 1300 OZ (0.0404 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 9822 NOTICES FOR 982200 OZ (30.550 TONNES)

SILVER

FOR MAY

2 NOTICE(S) FILED TODAY FOR 10,000 OZ/

total number of notices filed so far this month: 8910 for 44,550,000 oz

BITCOIN MORNING QUOTE $9087 DOWN 444

BITCOIN AFTERNOON QUOTE.: $9515 DOWN 258

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $26.70 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

NO CHANGES IN GOLD INVENTORY AT THE GLD:

GLD: 1,112.78 TONNES OF GOLD//

WITH SILVER DOWN 50 CENTS TODAY: AND WITH NO SILVER AROUND

ANOTHER HUGE 7.923 MILLION OZ DEPOSIT//WHAT FRAUDSTERS!!

RESTING SLV INVENTORY TONIGHT:

SLV: 457.681 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A STRONG SIZED 3364 CONTRACTS FROM 151,890 UP TO 155,360 AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE STRONG SIZED GAIN IN OI OCCURRED WITH OUR VERY GOOD 11 CENT GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS DUE TO STRONG BANKER SHORT COVERING PLUS A FAIR EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A SMALL DECREASE IN SILVER OZ STANDING AT THE COMEX FOR MAY. WE HAD A NET GAIN IN OUR TWO EXCHANGES OF 4130 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUMONGOUS AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: MARCH: 00 AND MAY: 0 AND JULY: 660 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 660 CONTRACTS. WITH THE TRANSFER OF 660 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 660 EFP CONTRACTS TRANSLATES INTO 3.30 MILLION OZ ACCOMPANYING:

1.THE 11 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.330 MILLION OZ INITIALLY STANDING FOR MAY

WEDNESDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 11 CENTS).. AND, OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY AMOUNT OF SILVER LONGS FROM THEIR POSITIONS. THE GOOD GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A SMALL LOSS IN SILVER OZ STANDING FOR MAY,3) CONSIDERABLE BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A NET GAIN OF 4024 CONTRACTS OR 20.120 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF MAY:

10,908 CONTRACTS (FOR 15 TRADING DAYS TOTAL 10,908 CONTRACTS) OR 54.54 MILLION OZ: (AVERAGE PER DAY: 727 CONTRACTS OR 3.636 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 54.54 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 7.79% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,043.40 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP SO FAR: 54.54 MILLION OZ

EXCHANGE FOR PHYSICAL ISSUANCE FOR THE PAST 30 DAYS IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3364, WITH OUR GOOD 11 CENT GAIN IN SILVER PRICING AT THE COMEX ///WEDNESDAY… THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 660 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A STRONG SIZED OI CONTRACTS ON THE TWO EXCHANGES: 4024 CONTRACTS (WITH OUR 11 CENT GAIN IN PRICE)

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 660 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A STRONG SIZED INCREASE OF 3364 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A HUGE 11 CENT GAIN IN PRICE OF SILVER/AND A CLOSING PRICE OF $17.52 // WEDNESDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.7050 BILLION OZ TO BE EXACT or 100.7% of annual global silver production (ex Russia & ex China).

FOR THE NEW MAR DELIVERY MONTH/ THEY FILED AT THE COMEX: 2 NOTICE(S) FOR 10,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.330 MILLION OZ

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 4808 CONTRACTS TO 533,013 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE CONSIDERABLE SIZED GAIN OF COMEX OI OCCURRED WITH OUR STRONG COMEX GAIN IN PRICE OF $7.20 /// COMEX GOLD TRADING// WEDNESDAY// WE HAD STRONG BANKER SHORT COVERING , A STRONG SIZED INCREASE IN GOLD OZ STANDING AT THE COMEX, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A GOOD EX. FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR LARGE GAIN IN THE PAPER PRICE OF GOLD.

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 10

WE GAINED A GOOD SIZED 5378 CONTRACTS (16.73 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 570 CONTRACTS:

CONTRACTS, FEB> 0 CONTRACTS; MARCH 00 APRIL: 0. MAY: 0, AND JUNE 570.; AUG 0 AND ALL OTHER MONTHS ZERO//TOTAL: 570. The NEW COMEX OI for the gold complex rests at 533,013. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5378 CONTRACTS: 4808 CONTRACTS INCREASED AT THE COMEXAND 570 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 5378 CONTRACTS OR 16.73 TONNES. WEDNESDAY, WE HAD A GAIN OF $7.20 IN GOLD TRADING……

AND WITH THAT GAIN IN PRICE, WE HAD A VERY STRONG SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 16.73 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $7.20).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS UNSUCCESSFUL (SEE BELOW).

4 GC VOLUME: 0 // open interest 10

END

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (570) ACCOMPANYING THE CONSIDERABLE SIZED GAIN IN COMEX OI (4808 OI): TOTAL GAIN IN THE TWO EXCHANGES: 5378 CONTRACTS. WE NO DOUBT HAD 1 )CONSIDERABLE BANKER SHORT COVERING, 2.)A GOOD INCREASE IN OUNCES STANDING AT THE GOLD COMEX FOR THE FRONT MAY MONTH, 3) ZERO LONG LIQUIDATION; 4) CONSIDERABLE COMEX OI GAIN, AND …ALL OF THIS WAS COUPLED WITH OUR STRONG GAIN IN GOLD PRICE TRADING//WEDNESDAY

SPREADING OPERATIONS

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

WE HAVE NOW COMMENCED IN SILVER THE ILLEGAL SPREADING OPERATION \ FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW STOPPED IN SILVER AS THEY NOW BEGIN TO MORPH INTO GOLD AS WE HEAD TOWARDS THE NEW FRONT MONTH WILL BE JUNE.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF MAY. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 43,691 CONTRACTS OR 4,369,100 oz OR 135.89 TONNES (15 TRADING DAYS AND THUS AVERAGING: 2912 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAY(S) IN TONNES: 135.89 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 135.90/3550 x 100% TONNES =3.95% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 2702.24 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 140.33 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 3364 CONTRACTS FROM 151,890 UP TO 155,254 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

ALL OF THE GAIN IN COMEX OI WAS DUE TO 1) CONSIDERABLE BANKER SHORT COVERING , 2) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A TINY DECREASE IN SILVER OZ STANDING AT THE COMEX FOR MAY AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 660 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR FEB. 0; FOR MAR 0: AND MAY: 0 JULY: 660 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 660 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3364 CONTRACTS TO THE 660 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 4024 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 20.12 MILLION OZ!!! OCCURRED WITH THE 11 CENT GAIN IN PRICE///

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 11 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// WEDNESDAY. WE ALSO HAD A SMALL SIZED 660 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 15.81 POINTS OR 0.35% //Hang Sang CLOSED DOWN 119.92 POINTS OR 0.49% /The Nikkei closed DOWN 42.84 POINTS OR 0.21%//Australia’s all ordinaires CLOSED DOWN .34%

/Chinese yuan (ONSHORE) closed DOWN at 7.1039 /Oil UP TO 34.26 dollars per barrel for WTI and 36.49 for Brent. Stocks in Europe OPENED MOSTLY RED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1039 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1119 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

i)we had 1 deposits into the customer account

into JPMorgan: 0

ii)into Scotia; 600,911.450 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.819 million oz of total silver inventory or 51.22% of all official comex silver. (160.819 million/314.220 million

total customer deposits today: 600,911.450 oz

we had 2 withdrawals:

i) Out of CNT: 608,531.860 oz

ii) Out of Delaware: 1000.917 oz

total withdrawals; 609,532.777 oz

We had 1 adjustments

i) Out of JPMorgan: 74,740.200 oz was adjusted out of the dealer account and this lands into the customer account

total dealer silver: 91.117 million

total dealer + customer silver: 311.713 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The total number of notices filed today for the MAY 2020. contract month is represented by 2 contract(s) FOR 10,000 oz

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 8910 x 5,000 oz = 44,550,000 oz to which we add the difference between the open interest for the front month of MAY.(158) and the number of notices served upon today 2 x (5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the MAY/2019 contract month: 8910 (notices served so far) x 5000 oz + OI for front month of MAY (158)- number of notices served upon today (2) x 5000 oz of silver standing for the MAY contract month.equals 45,330,000 oz.

We LOST 8 or an additional 40,000 oz will seek out metal on the London side of the pond as they ACCEPTED a London based forward contract..

TODAY’S ESTIMATED SILVER VOLUME: 75,716 CONTRACTS //volume very high

FOR YESTERDAY: 70,445 CONTRACTS..,CONFIRMED VOLUME//

YESTERDAY’S CONFIRMED VOLUME OF 70,445 CONTRACTS EQUATES to 352 million OZ 50.3% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO- 0.24% ((MAY 21/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO +0.09% to NAV: (MAY 21/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 0.24%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 16.29 TRADING 16.25///NEGATIVE 0.25

END

And now the Gold inventory at the GLD/

MAY 21//WITH GOLD DOWN $26.70//NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1112.32 TONNES

MAY 20/WITH GOLD UP $7.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 1.46 TONNES FROM THE GLD////INVENTORY RESTS TONIGHT AT 1112.32 TONNES

MAY 19//WITH GOLD UP $10.60//NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1113.78 TONNES

MAY 18/WITH GOLD DOWN $15.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A PAPER DEPOSIT OF 9.06 TONNES./INVENTORY RESTS AT 1113.78 TONNES

MAY 15.WITH GOLD UP $16.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 12.58 TONNES/ INVENTORY RESTS AT 1104.72 TONNES

MAY 14//WITH GOLD UP $19.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1092.14 TONNES

MAY 13//WITH GOLD UP $9.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 11.07 TONNES/INVENTORY RESTS AT 1092.14 TONNES

MAY 12//WITH GOLD UP $6.60 TODAY; A SMALL CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 1081.07 TONNES

MAY 11/WITH GOLD DOWN $12.65 TODAY: NO CHANGES IN GOLD INVENTORY: //INVENTORY RESTS AT 1081.65 TONES..

MAY 8/WITH GOLD DOWN $7.00 TODAY; A BIG CHANGE IN GOLD INVENTORY: A PAPER ADDITION OF 5.85 TONNES/INVENTORY RESTS AT 1081.65 TONNES

MAY 7/WITH GOLD UP $29.65 TODAY : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER ADDITION OF .41 TONNES/INVENTORY RESTS AT 1075.80 TONNES

MAY 6//WITH GOLD DOWN $17.00 TODAY/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER ADDITION OF 3.68 TONNES/INVENTORY RESTS AT 1075.39 TONES

MAY 5/WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER ADDITION OF 3.81 TONNES//INVENTORY RESTS AT 1071.71 TONNES

MAY 4//WITH GOLD UP $12.00 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE PAPER DEPOSIT OF 11.4 TONNES INTO THE GLD////GOLD INVENTORY RESTS AT 1067.90 TONNES

MAY 1/WITH GOLD UP $8.45 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1056.50 TONNES

APRIL 30/WITH GOLD DOWN $15.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1056.50 TONNES

APRIL 29/WITH GOLD DOWN $7.65/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 8.19 TONNES OF GOLD INTO THE GLD////INVENTORY REST AT 1056.50 TONNES//

APRIL 28/WITH GOLD DOWN $4.50//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1048.31 TONNES

APRIL 27/WITH GOLD DOWN $12.75//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 5.85 TONNES INTO THE GLD////INVENTORY RESTS TONIGHT AT 1048.31 TONNES

APRIL 24/WITH GOLD DOWN $4.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS TONIGHT AT 1042.46 TONNES

APRIL 23/WITH GOLD UP $10.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS TONIGHT AT 1042.46 TONNES

APRIL 22/WITH GOLD UP $40.75 TODAY:; TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A)A MONSTROUS 3.8 PAPER TONNES WERE ADDED TO THE GLD INVENTORY AND B) ANOTHER HUGE 9.07 TONNES OF PAPER GOLD ADDED LATE IN THE DAY//INVENTORY RESTS AT 1042.46 TONNES

APRIL 21/WITH GOLD DOWN $21.60 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTROUS ADDITION OF 7.9 PAPER TONNES TO THE GLD INVENTORY//INVENTORY RESTS AT 1029.59 TONNES

APRIL 20//WITH GOLD UP $10.00 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1021.69 TONNES

APRIL 17/WITH GOLD DOWN $27.80 TODAY: SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1021.69 TONNES TONNES..THE STRING OF 12 STRAIGHT STRONG DEPOSITS ENDS..

APRIL 16/WITH GOLD DOWN $4.50 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG DEPOSIT OF 4.10 TONNES WAS ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 1021.69 TONNES/12TH STRAIGHT STRONG DEPOSIT

APRIL 15//WITH GOLD DOWN $19.10 TODAY; ANOTHER HUGE CHANGE IN GOLD INVENTORY; A STRONG 7.89 TONNES WAS ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 1117.59 TONNES.//11TH STRAIGHT STRONG DEPOSIT

APRIL 14/WITH GOLD UP $23.55 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 15.51 TONNES WAS ADDED TO THE GLD INVENTORY/INVENTORY RESTS AT 1009.70 TONNES//THIS IS THE 10TH STRAIGHT STRONG DEPOSIT//THIS IS A FRAUDULENT VEHICLE..THEY HAVE NO PHYSICAL GOLD IN THE TRUST..

APRIL 13//WITH GOLD UP $27.65 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 5.36 TONNES WAS ADDED TO THE GLD//INVENTORY RESTS AT 994.19 TONNES

APRIL 9 WITH GOLD UP $37.30 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 2.92 TONNES WAS ADDED TO THE GLD//GOLD INVENTORY RESTS TONIGHT AT..988.63 TONNES

APRIL 8/WITH GOLD DOWN $.60//ANOTHER HUGE CHANGE IN GOLD INVENTORY/;; A STRONG 1.45 TONNES WAS ADDED TO THE GLD/GOLD INVENTORY RESTS AT 985.71 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

MAY 21/ GLD INVENTORY 1112.32 tonnes*

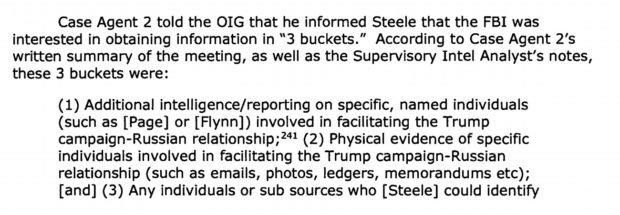

LAST; 825 TRADING DAYS: +166.01 NET TONNES HAVE BEEN REMOVED FROM THE GLD

LAST 725 TRADING DAYS://+341.16 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

MAY 21/WITH SILVER DOWN 50 CENTS TODAY: A HUGE PAPER DEPOSIT OF 7.923 MILLION OZ///INVENTORY RESTS AT 449.758 MILLION OZ//

MAY 20//WITH SILVER UP ANOTHER 11 CENTS TODAY: A HUGE CHANGE IN SLV INVENTORY: A HUGE PAPER DEPOSIT OF 9.601 MILLION OZ INTO THE SLV// //INVENTORY RESTS AT 449.758 MILLION OZ

MAY 19/WITH SILVER UP ANOTHER 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 440.157 MILLION OZ//

MAY 18/WITH SILVER UP ANOTHER 48 CENTS TODAY: TWO BIG CHANGES IN SILVER INVENTORY AT THE SLV I.E. 2 PAPER DEPOSIT OF ( I) 8.39 MILLION OZ AND THEN ( 2) 8.109 MILLION OZ//INVENTORY RESTS AT 432.048 MILLION OZ// (TOTAL DEPOSITS 16.500 MILLION OZ///)

MAY 15/WITH SILVER UP 81 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV: /INVENTORY RESTS AT 423.65 MILLION OZ.

MAY 14//WITH SILVER UP 33 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV.//INVENTORY RESTS AT 423.65 MILLION OZ

MAY 13/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.79 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 423.65 MILLION OZ//

MAY 12/WITH SILVER UP 5 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.076 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 420.861 MILLION OZ//

MAY 11.WITH SILVER DOWN 5 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 417.785 MILLION OZ//

MAY 8/WITH SILVER UP 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTER DEPOSIT OF 4.661 MILLION OZ OF SILVER INTO THE SLV..///INVENTORY RESTS AT 417.785 MILLION OZ//

MAY 7/WITH SILVER UP 45 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 5/WITH SILVER UP 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ///

MAY 4//WITH SILVER DOWN 5 CENTS TODAY:2 HUGE PAPER CHANGES IN SILVER INVENTORY AT THE SLV.i).A LARGE 1.399 MILLION OZ OF PAPER SILVER REMOVED FROM THE SLV//..//INVENTORY RESTS AT 411.427 MILLION OZ and ii) A LARGE 1.647 MILLION OZ OF PAPER SILVER ADDED TO THE SLV// INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 1/WITH SILVER FLAT IN PRICE: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 412.826 MILLION OZ///

APRIL 30/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 412.826 MILLION OZ//

APRIL 29/WITH SILVER DOWN ONE CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 412.826 MILLION OZ//

APRIL 28 /WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 412.826 MILLION OZ..

APRIL 27/WITH SILVER UP ONE CENT TODAY: TWO SMALL CHANGE IN SILVER INVENTORY AT THE SLV: a) A WITHDRAWAL OF 373,000 OZ FORM THE SLV// b) A SECOND WITHDRAWAL OF 466,000: ////INVENTORY RESTS AT 412.826 MILLION OZ//

APRIL 24//WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.665 MILLION OZ

APRIL 23/WITH SILVER UP 0 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.891 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 413.665 MILLION OZ//

APRIL 22/WITH SILVER UP 42 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY: A PAPER WITHDRAWAL OF 1.865 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 410.774 MILLION OZ//

APRIL 21//WITH SILVER DOWN 60 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER ADDITION OF 1.398 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 412.639 MILLION OZ//

APRIL 20//WITH SILVER UP 16 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.797 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 414.038 MILLION OZ//

APRIL 17/WITH SILVER DOWN 24 CENTS TODAY; A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.3999 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 16/WITH SILVER UP 5 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 15//WITH SILVER DOWN 45 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV TWO HUGE DEPOSITS: A DEPOSIT OF 1.679 MILLION OZ AND ANOTHER 5.222 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 14./WITH SILVER UP 51 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A MASSIVE PAPER DEPOSIT OF XXX MILLION OZ//INVENTORY RESTS AT 408.536 MILLION OZ//

APRIL 13//WITH SILVER DOWN 29 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 6.155 MILLION OZ////INVENTORY RESTS AT 408.536 MILLION OZ//

APRIL 9/WITH SILVER UP 60 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUGE DEPOSIT OF 1.84 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 402.381 MILLION OZ.

MAY 21.2020:

SLV INVENTORY RESTS TONIGHT AT

457.681 MILLION OZ.

END

LIBOR SCHEDULE AND GOFO RATES// GOLD LEASE RATES

YOUR DATA…..

6 Month MM GOFO 3.22/ and libor 6 month duration 0.59

Indicative gold forward offer rate for a 6 month duration/calculation:

GOLD LENDING RATE: -2.63%

NEGATIVE GOLD LEASING RATES INCREASING//GOLD SCARCITY AND CENTRAL BANKS CALLING IN ALL OF THEIR GOLD LEASES

XXXXXXXX

12 Month MM GOFO

+ 2.19%

LIBOR FOR 12 MONTH DURATION: 0.71

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -1.48%

NEGATIVE GOLD LEASING RATES INCREASING//GOLD SCARCITY AND CENTRAL BANKS CALLING IN ALL OF THEIR GOLD LEASES

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Gold Is The Best Performing Asset In 2020 YTD With 15% Gain in USD

Gold Is The Best Performing Asset In 2020 YTD: +15% in USD, +18% in EUR and +23% in GBP

◆ Gold is 15% higher in dollars, 18% higher in euros and 23% higher in sterling year to date as safe haven demand sees gold act as a hedge again.

◆ Silver has under-performed gold in the short and medium term and is only 1% higher year to date in dollars, 4% in euros and 9% higher in British pounds.

◆ The gold silver ratio has fallen from 125 to 100 as silver starts to outperform gold again as it does in gold and silver bull markets. Silver remains very undervalued versus gold, versus property markets and versus risk assets in general.

◆ Gold is now outperforming the 30 year US bond and is the best performing asset in 2020 year to date in all currencies. It is even outperforming the tech giants with the Nasdaq 100 only 6.8% higher year to date.

◆ Stock markets have fallen sharply and risk assets in general including the tech monopolies and property markets are vulnerable as the global economy contracts massively.

◆ Government bonds including U.S. Treasuries are also vulnerable given the strong possibility of a sovereign debt crisis in the increasingly bankrupt U.S. and increasingly bankrupt world.

NEWS and COMMENTARY

Gold steady, firm dollar offsets recession support

Venezuela files claim to force Bank of England to hand over gold

S&P stumbles as Moderna sinks on report questioning trial results

C.B.O. now forecasting 38% decline in GDP in Q2, with 26 million fewer people employed

Euro rallies on Franco-German proposal for recovery fund: 500 billion euros

‘We are fully prepared to take losses’ on coronavirus bailouts, Mnuchin says

G7 finance ministers discuss accelerating economies as countries reopen: U.S. Treasury

What matters most in gold and silver – Butler

GATA asks CFTC if it has ever audited Comex gold

Gold Price Analysis: Probes $1,750 as US dollar stays sluggish

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

19-May-20 1735.25 1737.95, 1416.14 1418.34 & 1584.11 1589.01

15-May-20 1734.85 1735.35, 1422.06 1427.67 & 1604.39 1602.60

14-May-20 1716.40 1731.60, 1403.67 1420.09 & 1587.84 1603.98

13-May-20 1699.85 1708.40, 1383.85 1394.74 & 1568.11 1573.09

12-May-20 1703.45 1702.40, 1381.84 1379.80 & 1574.50 1565.87

11-May-20 1698.80 1702.75, 1375.35 1378.55 & 1570.20 1571.81

07-May-20 1688.65 1704.05, 1366.29 1387.78 & 1565.21 1582.38

06-May-20 1698.90 1691.50, 1373.56 1366.73 & 1574.71 1564.13

05-May-20 1696.30 1699.55, 1363.83 1363.72 & 1566.36 1562.91

04-May-20 1703.70 1709.10, 1371.14 1374.63 & 1558.72 1563.83

01-May-20 1673.05 1686.25, 1332.08 1347.15 & 1523.14 1536.68

30-Apr-20 1716.75 1702.75, 1373.92 1361.69 & 1577.86 1568.91

29-Apr-20 1706.00 1703.35, 1371.97 1368.64 & 1569.69 1568.10

28-Apr-20 1708.10 1691.55, 1367.68 1357.98 & 1571.11 1559.27

27-Apr-20 1717.25 1714.95, 1381.36 1380.19 & 1582.96 1581.18

NOTE: Inbound deliveries to our Loomis and Brink’s vaults in Zurich, Singapore, London and Dublin have resumed and to ensure liquidity, investors can move their assets to our vaults from safe deposit box companies, bullion stored with banks or digital gold platforms or ETFs.

We have resumed buying non stored bullion again and are buying gold and silver coins and bars at attractive premiums. Please email us for shipping instructions to vaults: support@goldcore.com

ii) Important gold commentaries courtesy of GATA/Chris Powell

iii) Other physical stories:

Global Investors Demand Gold As Protection Against Financial Repression

Disconnect between markets and economic reality:

“There is a huge disconnect between markets and the economic reality, and it’s fundamentally based on the view that 2020 is a lost year and therefore what investors need to think about is 2021 is a recovery year. It looks a very dangerous bet to me because if there’s anything that we have learned from this crisis is that estimates for 2021 remain excessively optimistic, and that the V-shaped recovery is more than elusive.”

Reaction to liquidity injections:

“The reaction of markets has been very aggressive to the liquidity injections coming from the Federal Reserve and the European central banks. But I think that at the same time that level of risk-taking is too high considering the challenges both on the economic growth recovery, but more importantly, because it’s been driven by the most cyclical sectors, the recovery in earnings cash flow and balance sheets.”

Gold miners/ BANG stocks:

“I personally always say that if you want to look at the world of metals or commodities, and you want to invest in the fundamentals of those metals or those commodities, the best way to play it is through the commodity itself, or the macro, not through equities, because cost of capital is also rising and there are challenges of financing.”

Covid-19 vaccine/implications for gold:

“There are two things that we know about Covid viruses.

One is that there has never been a vaccine for a coronavirus. That’s something that we need to pay a lot of attention to when we get these levels of optimism in the market about the vaccine. When 18 previous types of viruses have never seen a vaccine, you cannot expect it to happen or at least happen as quickly as markets would want.

The second is there is likely to be a treatment, there is likely to be a way to live with Covid-19.

What is the outlook for gold in that environment? Well if anything gold is proven in 2019 that in an environment in which markets remain positive and remain attracted to a certain level of expectation of economic growth, gold and the dollar do and can rise in tandem.”

“Gold is currently working as an alternative and as a de-correlated asset to a downturn. But we must remember as well that it is a pretty good inflation hedge. So, in general I think that the outlook for gold even in and in a recovery is actually pretty good.”

Gold/silver ratio

“I always tell my clients that if you like gold you certainly have to like silver. I don’t understand why you would be long silver short gold or have it as a pair. I think that you need to have both. But I don’t believe in the debate about the ratio of gold to silver. Reminds me of the debate about the ratio of oil to natural gas. And I think that that was a mistake in the past.”

“Silver has its own fundamentals. They’re pretty good fundamentals in supply and demand. Silver is a precious metal that has numerous positive elements in order to be comfortably bullish. However, it is not money. This is the important thing in a monetary debasement craziness like the one that we’re living is that the only asset that has been proven for centuries to be money is gold. And I think that will maintain the ratio high.

Will gold continue to be bullish?

“I don’t think that gold is going to be as bullish relative to the dollar because of the high shortage of US dollars that exists in the economy right now, which is about between 13 to 20 trillion.

However, global investors are likely to look for opportunities to find a good investment relative to their currency now.

So Brazilian investors, Turkish investors, Chinese investors, Japanese investors, European investors are likely to see a much better return of gold relative to their currencies than relative to the US.”

A good one:

an email from Robert to me:

With nearly 80% of the civil workforce employed in the service sector, these schemes of keeping the economy locked down are extremely dangerous. And this is not only in America. Every country faces the same realities to similar extents. And this is why the service sector will likely see a 50% reduction in jobs by yearend. People fail to realize that this is undermining society in a major way so that it is not going to return to normal even with Gates’ certificates to prove you have been vaccinated. Mind you the latest information on Moderna and its’ testing is a disaster. So that plan is already in the toilet.

In the US the Democratic states are refusing to open up when there is no real justification to keep their economies closed. What is really going on behind the curtain is a clever trick. The $1 trillion that Pelosi was stuffing in the Democratic Bill is money to bail out state and municipal governments which have been going broke because of their unfunded pensions.

The scheme is to crash their economies and then blame everything on the virus and then blame Trump for not bailing them out for the 2020 election. This is a very clever scheme being relayed in whispers from behind the curtain. They are using this virus as cover to bail out 70 years of fiscal mismanagement. It is why Trump also let the Governors decide when to open to sidestep the blame. This whole mess is political.

Why would anyone want to spend capital in a Democrat state where the agenda is so clear? What will become clear in another month or two is that the states that went back to work are the ones with an economy, while those who remain shut will see rapid erosion of social fabric. The divide will only widen going into the fall. And regardless of what happens in November the chaos from this folly will last a long time.

And one can assume that China is gleefully watching and waiting as the west destroys itself, hoping its’ own financial problems do not overwhelm it first.

It really would be a bunch simpler if we all simply worked and forgot about political agendas to fracture and remake society and let society mold itself.

Cheers

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

US Futures Drop On Renewed US-China Tensions

S&P futures drifted lower alongside European and Asian stocks on Thursday as Trump ramped up his criticism of China and Xi Jinping, amid rapidly deteriorating Sino-US relations, souring the mood on the the recent rally in risk assets. Safe havens such as Treasuries edged up with the dollar. As reported here last night, in a rare outburst that went so far as to accuse the “very top” of China’s government of a “massive disinformation campaign”, Trump slammed China again just days before the biggest Chinese political gathering of the year, with traders betting that it was now just a matter of time before China retaliated in deed instead of just in word.

As a result, contracts on the three main equity index futures dropped after the S&P closed at the highest level in two months, a day after the Senate overwhelmingly passed a bill that could bar some Chinese companies from listing on U.S. exchanges, with the Emini flirting on either side of the critical 2,950 level.

“Markets may be pricing in far too much complacency as the U.S.-China ‘phase one’ trade deal could be at risk,” said market strategist Stephen Innes. “The pandemic and resulting acute economic downturn have made China’s trade commitment to the U.S. much more challenging to fulfill.”

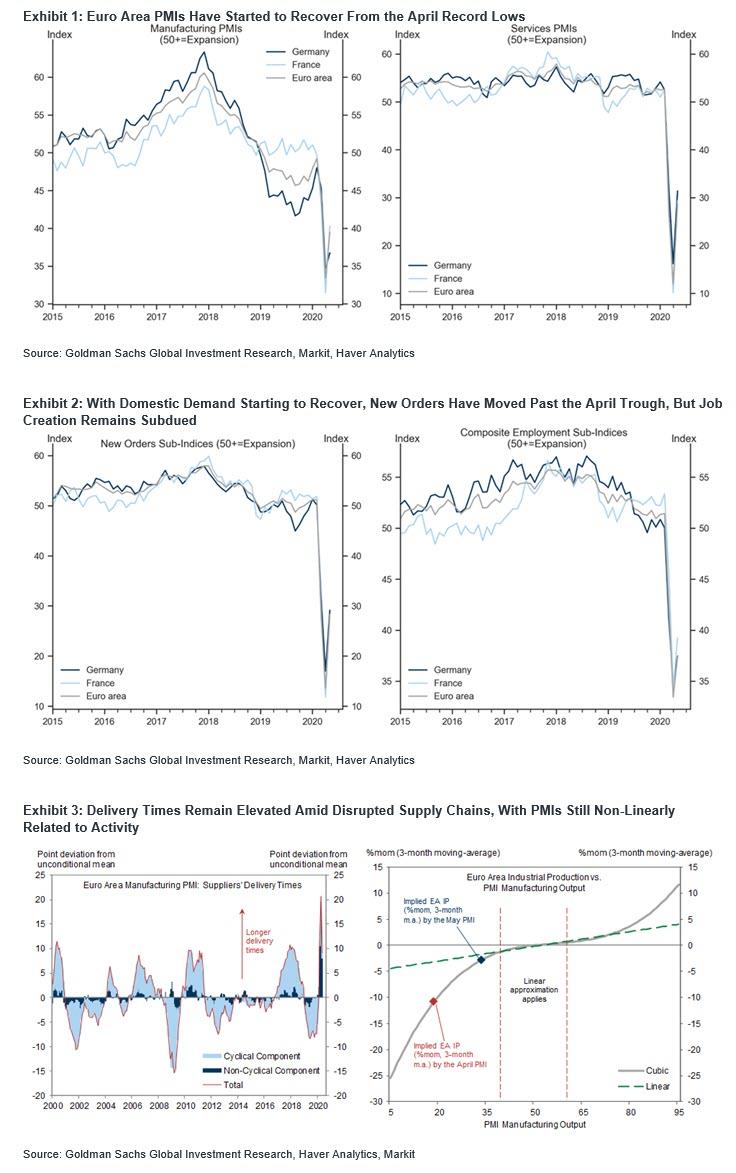

Europe’s Stoxx 600 Index fell, with nearly all 19 sector groups in the red. Deutsche Lufthansa AG shares bucked the trend after the carrier said it was close to a multibillion-euro bailout deal from the German government. There was some good news out of Europe, where May flash PMIs (even though there is still ten days in the month) rebounded solidly from April’s lows. As Goldman notes, after reaching a historical low in April at the height of the coronacrisis, the Euro area flash composite PMI rebounded by 16.9pt in May (to 30.5), and above consensus. The increase was broad-based across sectors—with manufacturing output rising by slightly more than services activity—consistent with the gradual lifting of containment measures from early May.

Yet there was some continued weakness with German manufacturing PMI printing at 36.8, below the 39.2 expected.

Earlier in the session, Asian stocks also fell, led by utilities and communications, after rising in the last session. Markets in the region were mixed, with Shanghai Composite and Hong Kong’s Hang Seng Index falling, and India’s S&P BSE Sensex Index and Taiwan’s Taiex Index rising. The Topix declined 0.2%, with Funai Soken and Marudai Food falling the most. The Shanghai Composite Index retreated 0.5%, with Xinjiang Korla Pear and Nanjing Chervon Auto Precision posting the biggest slides.

Concerns over the growing stress between the US and China and global coronavirus cases reaching 5 million are vying for investor attention with optimism over reopening economies and progress on thwarting the pandemic. AstraZeneca received more than $1 billion in American funding to develop a Covid-19 vaccine. Meanwhile, the U.S. legislation could lead to Chinese mega-companies such as Alibaba Group Holding and Baidu being barred from exchanges. Both slipped in early trading, with Baidu going so far as declaring it may delist first before it is kicked out:

- EXCLUSIVE-CHINA’S BAIDU CONSIDERS DELISTING FROM NASDAQ TO BOOST VALUATION – RTRS

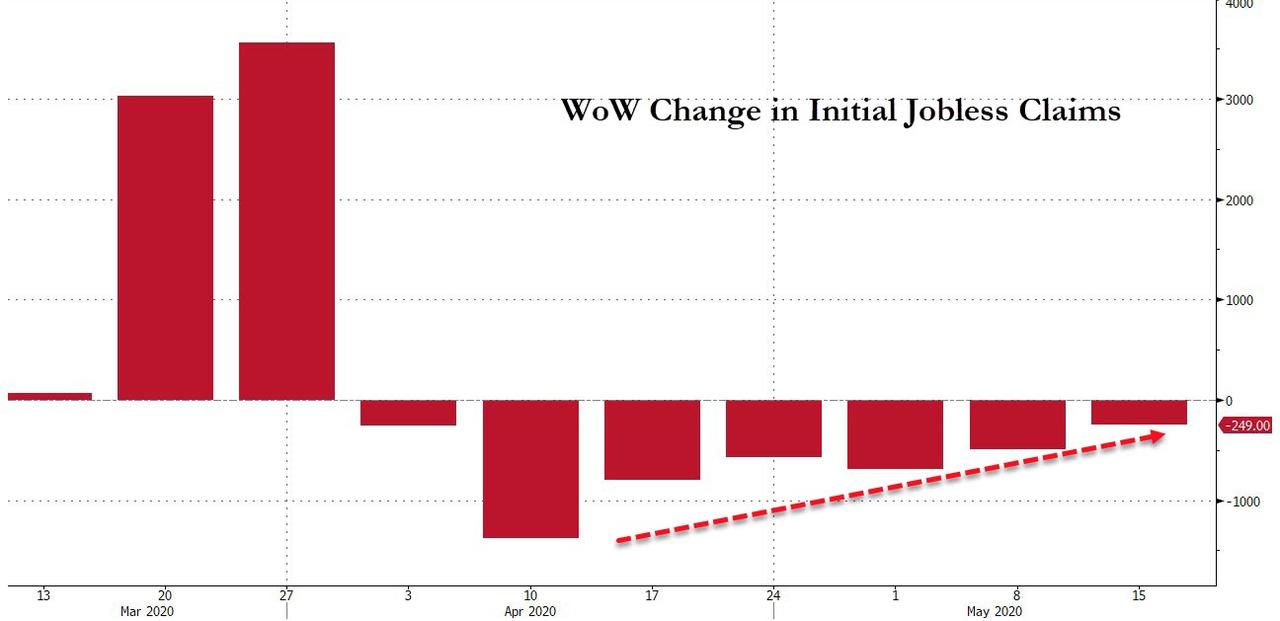

Investors are also awaiting the latest weekly jobless claims data, which is due at 8:30 a.m. ET and is expected to show millions more Americans filing for unemployment benefits due to layoffs and mass furloughs as a result of the lockdown. Still, claims have gradually declined since hitting a record 6.867 million in the week ended March 28 and Thursday’s report could offer early clues on how quickly businesses re-hire as they reopen.

In rates, Treasuries were flat into early U.S. trading after paring Asia-session gains that were paced by demand for longer-dated tenors after Wednesday’s well-received 20-year auction, the first in decades. Yields remain lower by about 1bp across the curve, 10-year around 0.67%, with 5s30s, 2s10s flatter by around 0.5bp each. Gilts outperformed, richer by 2bp vs. Treasuries; BOE conducted buybacks via three operations Thursday, totaling GBP4.5b. Treasuries also drew support during Asia session from rising U.S.-China tensions. The new 20-year, priced at 1.22% Wednesday, improved to about 1.16%.

Market Snapshot

- S&P 500 futures down 0.8% to 2,945.50

- STOXX Europe 600 down 0.9% to 339.81

- MXAP down 0.3% to 148.47

- MXAPJ down 0.2% to 479.40

- Nikkei down 0.2% to 20,552.31

- Topix down 0.2% to 1,491.21

- Hang Seng Index down 0.5% to 24,280.03

- Shanghai Composite down 0.6% to 2,867.92

- Sensex up 0.8% to 31,058.54

- Australia S&P/ASX 200 down 0.4% to 5,550.43

- Kospi up 0.4% to 1,998.31

- German 10Y yield fell 1.1 bps to -0.479%

- Euro down 0.1% to $1.0967

- Italian 10Y yield fell 0.2 bps to 1.46%

- Spanish 10Y yield rose 2.2 bps to 0.662%

- Brent futures up 2% to $36.47/bbl

- Gold spot down 0.8% to $1,734.25

- U.S. Dollar Index up 0.2% to 99.31

Top Overnight News

- U.S. and European futures retreated and the dollar advanced with Treasuries as deteriorating Sino-American ties cast a cloud over the recent rally in risk assets

- The euro-area economy started to claw its way out of its deepest downturn ever as the relaxing of coronavirus lockdowns allows thousands of businesses to reopen. Markit’s headline gauge of private-sector activity rose in May, though it continued to signal contraction in both manufacturing and services

- The U.K.’s economic slump eased this month as some companies resumed trading amid a lockdown that has brought most activity to a halt. IHS Markit’s Purchasing Managers Index for the whole economy rose to 28.9 from 13.8 in April in a preliminary estimate

- The U.S. threw its weight behind one of the fastest-moving experimental solutions to the coronavirus pandemic, pledging as much as $1.2 billion to AstraZeneca Plc to help make the University of Oxford’s Covid vaccine

- British banks are confronting the European import of sub-zero interest rates that could damage profits already weakened by the coronavirus pandemic, and the Brexit divorce rumbling towards its rocky end

Asian equity markets struggled to sustain the impetus from the rebound on Wall St where stocks were underpinned by hopes of a pick-up in economic activity after all US states were said to have at least partially reopened and as the continued recovery in oil prices also supported the risk tone, with sentiment in Asia eventually clouded by ongoing US-China tensions. ASX 200 (-0.4%) was initially led higher by strength in energy names although the index later reversed the moves after its top weighted financials sector dipped into the red and amid the souring ties with China. Nikkei 225 (-0.2%) also failed to hold on to opening gains despite reports Japan is set to lift the emergency declarations in Osaka, Kyoto and Hyogo, but with Tokyo not included in the status lifting, while participants digested mixed trade data that showed Exports at a narrower than expected contraction, which was still the worst decline since 2009. Hang Seng (-0.5%) and Shanghai Comp. (-0.5%) were subdued as the war of words between US and China persisted with US President Trump alleging the incompetence of China was behind the mass worldwide killing and that China’s disinformation and propaganda attack on the US and Europe is a disgrace. Furthermore, the White House released a report blasting China for its actions ranging from predatory economic policies to human rights abuses, and the US Senate recently passed the bill aimed at increasing oversight of Chinese companies that could see them delisted from US exchanges. Finally, 10yr JGBs were higher as they tracked the upside seen in T-notes following the hostile US-China rhetoric and decent results at the new US 20-year auction which disproved the naysayers that had anticipated a lacklustre auction, while the BoJ presence in the market and mild deterioration in risk tone also added to the upside for JGBs.

Top Asian News

- China Simplifies Iron Ore Import Rules Amid Australia Spat

- Chinese Port Operator Xinghua’s Owner Said to Explore Sale

- Fiscal Nightmare Ties Up Kuwait’s Stimulus With 40% Deficit

- Airlines Caught Off Guard as India Suddenly Allows Flights

European stocks see losses across most major bourses [Euro Stoxx 50 -1.4%], as the negative APAC sentiment reverberated into the region. Bourses see broad-based losses amid the escalating rhetoric between US and China as sentiment between the nations hit a low – with Spain faring slightly better after earlier underperformance on account of its extended State of Emergency, while Switzerland and Scandi markets are closed amid holidays. Broader sectors are all in the red with defensives faring better than cyclicals – suggesting risk aversion across the market, whilst the breakdown pains a similar picture with banks and Travel & Leisure among the laggards. In terms of individual movers, easyJet (+6.3%) holds onto gains after announcing the resumption of flights from 15th June. Co. believes there is sufficient customer demand to support profitable flying. Initial schedule will comprise mainly of domestic flights in UK and France, Further routes will be announced in the coming weeks as customer demand increases. Sticking with the airline sector, Lufthansa (+4.8%) confirmed it is in advanced talks with the German Govt’s Economic Stabilisation Fund (WSF) on a stabilisation package comprising of measures amounting up to EUR 9bln, with the package subject to approval by the European Commission. On the flip side, Altice (-12%) shares tumble post earnings.

Top European News

- EasyJet Among First Carriers in Europe to Plan Restart

- Swissport Seeks Support to Raise up to $417 Million of Loans

- British Lenders Brace for Sub-Zero Rates Floated by Central Bank

- U.K. Grid Struggles as Renewables Overtake Fossil Fuels

In FX, mixed to weaker than forecast French and German PMIs were rather misleading, as the preliminary survey for the bloc as a whole beat on all counts to keep the Euro elevated and more resistant than other majors against a broad Dollar revival. Indeed, Eur/Usd remains underpinned above 1.0950 even though the DXY has pared some losses from Wednesday’s 99.001 low to sit a bit more comfortably within a 99.183-434 range ahead of US PMIs and the latest weekly jobless claims data. Similarly, albeit to a lesser extent, the Pound has regained composure in wake of UK services, manufacturing and composite readings all surpassing consensus, with Cable back above the 1.2200 handle and Eur/Gbp just holding below 0.9000. However, the former still looks bearish from a technical standpoint after breaching one side of an inverse head and shoulders chart formation at 1.2225, while a softer than forecast CBI trends metric did little to spur any action.

- AUD/NZD – Renewed risk aversion and further assurances from RBA Governor Lowe about turning up the QE dial again if needed have prompted a pull-back in the Aussie and Kiwi from midweek peaks vs their US counterpart, as Aud/Usd reverses from 0.6600+ and Nzd/Usd is back under 0.6150. Note much in the way of additional impetus gleaned from CBA PMIs overnight, but NZ retail sales could be more pivotal later.

- CAD/CHF/JPY – Firm crude prices continue to cushion the Loonie from downturns in broader risk sentiment, but Usd/Cad has further from sub-1.3900 lows into a band up to 1.3946, while the Franc is pivoting 0.9650 and Yen is consolidating between 107.49-84 parameters following a much wider than expected Japanese trade deficit due to exports plunging around 3 times more than imports.

- SCANDI/EM – The Scandi Crowns have both lost momentum amidst the aforementioned risk-off mood, with Eur/Sek and Eur/Nok rebounding after forays to fresh multi-month lows towards 10.5000 and 10.8500 respectively, but the overall trend remains bearish in cross terms. Meanwhile, EMs have also handed back some of their recent gains as the clock ticks down to CBRT and SARB rate verdicts that are predicted to reveal matching 50 bp benchmark reductions, but could conceivably culminate in more aggressive easing moves. Usd/Try is straddling 6.7900 at present and Usd/Zar has reversed through 18.0000 after crossing the psychological mark on Wednesday.

- RBA Governor Lowe said the future remains unusually uncertain in which one uncertainty is the pace of which restrictions are eased and another source is the level of confidence people have about their future, while he added the RBA remain prepared to scale up bond purchases again if necessary but noted there is a limit to what can be achieved with monetary policy. Furthermore, RBA Governor Lowe added there is no change to thinking on negative rates which are still extraordinarily unlikely and that the costs of negative rates exceed the benefits. (Newswires)

In commodities, WTI and Brent front month futures eke mild gains in what is another new-flow light European session. Rising US-Sino frictions weigh on the stock markets but caps gains in the energy market, as the complex still prices in demand from reopening economy alongside lower supply from producers. Regarding OPEC, Russian oil and condensate between May 1-19 was reported to have averaged 9.42mln BPD – although condensate is not part of the OPEC+ deal – its output was reportedly between 700-800mln BPD, meaning Russian oil output was modestly above the agreed cap of 8.5mln BPD, according to ING. WTI July resides just south of USD 34/bbl whilst its Brent counterpart trades on either side of USD 36/bbl – with both benchmarks within a USD 1/bbl or so intraday band. In terms of bank commentary, Citi sees Brent prices averaging USD 39/bbl in Q2 and USD 48/bbl in Q4, expects oil market to move into a deficit from June through Q3 2020 onward. Meanwhile, spot gold remains weighed on by a firmer USD as President Trump ramped up rhetoric against China – with the yellow metal around USD 1735/oz having printed a high of USD 1749.50 thus far. Copper prices have receded in tandem with stocks and the overall protectionism-hit sentiment, but downside action remains limited as the demand prospect from opening economies underpin demand for the red metal.

US Event Calendar

- 8:30am: Philadelphia Fed Business Outlook, est. -40, prior -56.6

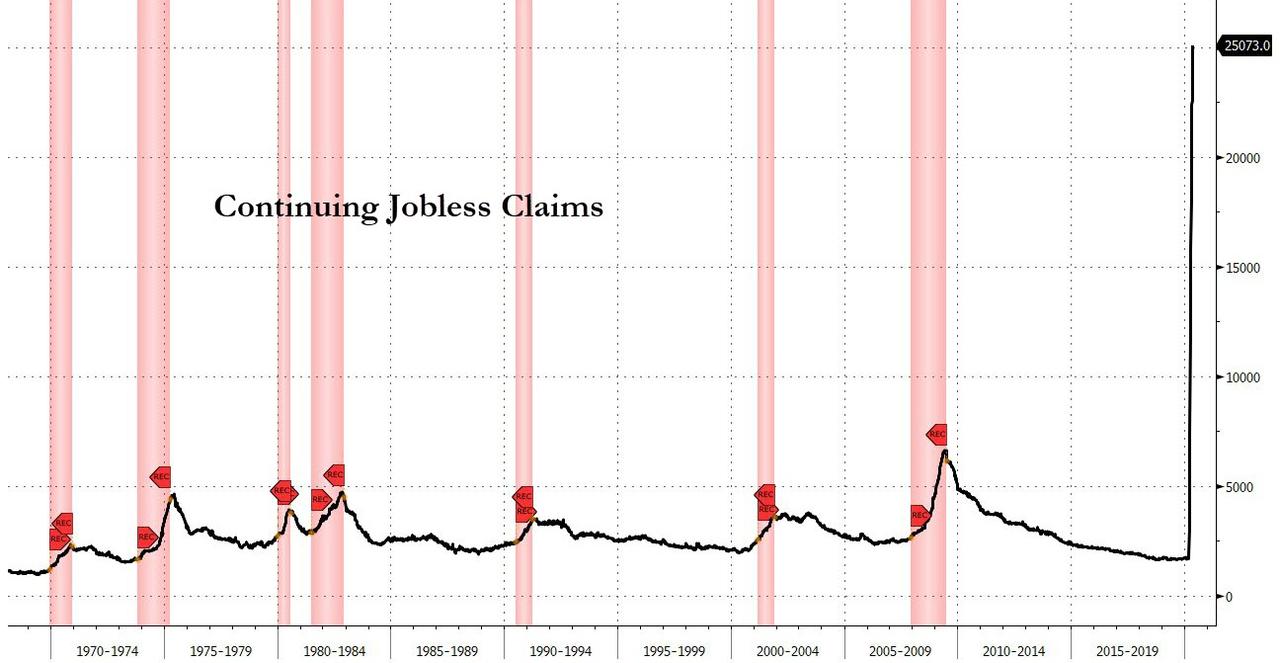

- 8:30am: Continuing Claims, est. 24.3m, prior 22.8m; Initial Jobless Claims, est. 2.4m, prior 2.98m

- 9:45am: Bloomberg Economic Expectations, prior 29; Bloomberg Consumer Comfort, prior 35.8

- 9:45am: Markit US Manufacturing PMI, est. 39.5, prior 36.1

- 9:45am: Markit US Services PMI, est. 32.3, prior 26.7

- 9:45am: Markit US Composite PMI, prior 27

- 10am: Existing Home Sales, est. 4.22m, prior 5.27m; Existing Home Sales MoM, est. -19.92%, prior -8.5%

DB’s Jim Reid concludes the overnight wrap

One interesting stat that we’ve included in our penultimate CCD today is that in the US state of Pennsylvania (12.8m pop.) more people have died of covid-19 aged over 100 years old than below the age of 45. In total it is 41 deaths under the age of 45 vs. 72 over the age of 100. In fact more people have died in the 105-109 year old age bucket (six people) than in any 5 year buckets up to the age of 30. Eight people under 30 have died in total in the state out of 4493. We show the graph in the CCD today. It is perhaps the most granular age data we’ve seen so far and goes up to those 110 years old.

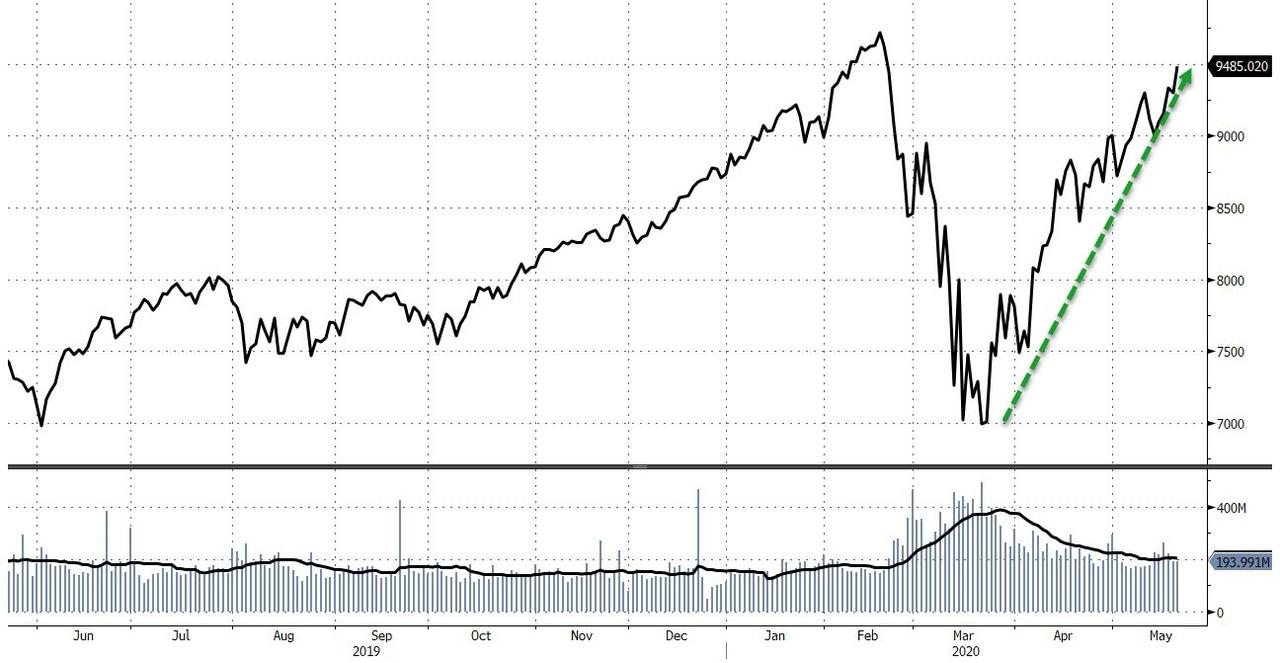

Onto markets now and it was yet another strong day for risk assets yesterday, with the S&P 500 climbing a further +1.67% to reach its highest closing level since the crisis was in full-swing. Indeed, the index now stands at an astonishing +32.82% higher since its closing low less than 2 months ago, as abundant liquidity, the continually slowing rates of infection and possible signs of hope on a vaccine have seen equities make one of their fastest moves upwards in many years. The question is whether this can sustain itself given that the very live risk of a second wave remains, as well as the fact that a vaccine is far from certain.

In terms of the details, 23 of 24 industry groups in the S&P moved higher, with energy leading the way on the back of higher oil prices. Europe also made gains as the STOXX 600 rose +0.98%, led partially by oil and gas stocks. The DAX was also up +1.34% and at a 2-month high. As mentioned, oil’s rally helped the covid laggards lead the day’s rally with both WTI (+3.05%) and Brent crude (+3.71%) making significant advances as both reached their own 2-month highs. It was not all positive for the commodity as data out of the US showed that there was an increase in gasoline storage thus showing the ongoing demand weakness. Markets continue to look beyond this at the moment with hopes that reopening of large parts of the US will see demand return.

The positive moves yesterday actually came in spite of a further escalation in rhetoric between the US and China. Secretary of State Pompeo said that China was ruled by a brutal, authoritarian regime, and that Beijing was hostile to free nations, which follows warnings from China after Pompeo congratulated the new Taiwanese President on her inauguration, since China claims Taiwan as part of its “one China” principle. Lastly, the US Senate passed by unanimous consent, legislation yesterday which require companies certify that they are not under the control of a foreign government for them to be listed on US exchanges. This was pointed at China with the Senator introducing the bill, John Kennedy (Republican from Louisiana), saying that “I do not want to get into a new Cold War,” but he wants “China to play by the rules.”

In terms of markets this morning, momentum has faded somewhat as that trade rhetoric weighs on sentiment. The Nikkei (-0.16%) is down, Hang Seng and Shanghai Comp both flat and Kospi (+0.33%) has posted a modest gain. Futures on the S&P 500 are also down -0.62%. Elsewhere, the US dollar index is trading up +0.24% while yields on 10y USTs are down -2.1bps.

We’ve also had the preliminary May PMIs for Japan and Australia overnight. Japan’s manufacturing PMI printed at 38.4 (vs. 41.9 last month), the lowest reading since March 2009 while the services print came in at 25.3 (vs. 21.5 last month) thereby putting the composite at 27.4 (vs. 25.8 last month). For Australia, the manufacturing PMI came in at 42.8 (vs. 44.1 last month) and services reading improved to 25.5 (vs. 19.5 last month) which put the composite at 26.4 (vs. 21.7 last month). In addition to that, Japan’s April trade data revealed that exports fell by -21.9% yoy (vs. -22.2% yoy expected), the largest decline since 2009 while the decline in imports was -7.2% yoy (vs. -13.2% yoy expected). In other overnight news, President Trump said that he may hold the June G-7 meeting at Maryland’s Camp David after previously planning a video conference.

Here in the UK, Bloomberg reported overnight that the government is considering an option of asking businesses to take over paying national insurance and employer pension contributions for furloughed staff as it weighs up winding down its spending on the program. Separately, the Financial Times has reported that Chancellor Sunak is drawing up plans to extend the holiday on mortgage payments that banks have to give 1.7 million homeowners suffering financial stress due to the virus. The holiday is currently set to finish at the end of June.

There were two noteworthy items out of central banks yesterday. Later in the day the Fed’s minutes from the 28-29 April meeting were released. The highlight was the level of concern the committee felt the virus posed to the US economy and the need to stem the fallout. “Members agreed that the Federal Reserve was committed to using its full range of tools to support the U.S. economy in this challenging time.” There was ample discussion into how forward guidance should be determined in the upcoming months, two suggestions were an outcome-based approach specifying macroeconomic indicators that needed to be reached or a date-based approach with the target range for the benchmark rate only rising after a specific amount of time had passed. The topic of negative rates were only brought up once, as “respondents to Desk surveys attached almost no probability to the FOMC implementing negative policy rates.” One of the issues with determining the best approach to forward guidance is the uncertainty around the path of the virus itself. Many Fed officials judged that there was a “substantial likelihood of additional waves of outbreak in the near or medium term. In such scenarios, it was believed likely that there would be further economic disruptions.” See our US economists recap for further details. Link here.

The cautionary tone of the FOMC minutes did not help the dollar as it fell against other major currencies on the day. The Bloomberg dollar index was down -0.25% to levels last seen on 1 May. The Euro rose 0.52%, trading higher for the fourth straight day, the longest such streak since the last week of March.

Back here in the UK, we got a few headlines from the Bank of England, as Governor Bailey said that “we’re keeping the tools under active review in the current situation”. He continued to not rule out negative rates, in line with the recent rhetoric we’ve been hearing, but he also acknowledged that there’ve been pretty mixed reviews on their use elsewhere, so it doesn’t obviously look as though these are going to be on the table anytime soon. The comments came as the UK’s debt management office actually sold bonds at a negative yield for the first time yesterday, raising £3.75bn at a yield of -0.003%. Our economists’ view is that the next policy move will be £125bn of extra QE next month, rather than negative rates.

Meanwhile, we got reports from MNI that the ECB would soon announce details on the reinvestment of principal payments on the bonds it’s bought under their Pandemic Emergency Purchase Programme launched in March. It was also said to be likely to add junk debt to its purchases. Credit had a good day yesterday with IG cash spreads 5bps tighter in USD and 3bps tighter in EUR, and HY cash spreads 19bps tighter in USD and 11bps tighter in EUR.

Looking at sovereign bonds yesterday, they were mostly treading water on both sides of the Atlantic, with no big moves in either direction. This was even as the US government sold 20-year bonds for the first time since 1986, and at a yield (1.220%) only marginally above the pre-auction levels. 10yr US Treasury yields ended the session mostly unchanged, down -0.8bps at 0.68%, while those on bunds fell by -0.4bps. One of the bigger moves was seen in Greece, where the country’s spread over 10yr bunds came down by -4.7bps to their lowest level in over a month.