GOLD:$1680.40 DOWN $40.40 The quote is London spot price

Silver:$17.34 DOWN 46 CENTS//LONDON SPOT PRICE

Closing access prices: London spot

i)Gold : $1584.60 LONDON SPOT 4:30 pm

ii)SILVER: $17.41//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUG GOLD: $1683.10 CLOSE 1.30 PM// SPREAD SPOT (LONDON) VS/FUTURE JUNE: $+2.70

CLOSING SILVER FUTURE MONTH

JULY: 1:30 PM: $17.48//1:30 PM //SPREAD SPOT LONDON VS FUTURE JULY: 16 CENTS PER OZ//

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2800. usa per oz

and silver; $31.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

DO NOT PAY ANY ATTENTION TO WHAT THE CROOKS ARE DOING AT THE COMEX AND LONDON LBMA..PHYSICAL IS THE NAME OF THE GAME AND NOTHING ELSE

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 392/543

EXCHANGE: COMEX

CONTRACT: JUNE 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,718.900000000 USD

INTENT DATE: 06/04/2020 DELIVERY DATE: 06/08/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 12

072 H GOLDMAN 63

104 C MIZUHO 1

118 H MACQUARIE FUT 14

132 C SG AMERICAS 1

190 H BMO CAPITAL 7

323 H HSBC 1

357 C WEDBUSH 8

624 C BOFA SECURITIES 6

657 C MORGAN STANLEY 20

657 H MORGAN STANLEY 281

661 C JP MORGAN 347

661 H JP MORGAN 45

686 C INTL FCSTONE 132

690 C ABN AMRO 105 13

732 C RBC CAP MARKETS 1

737 C ADVANTAGE 14 6

800 C MAREX SPEC 3 2

905 C ADM 4

____________________________________________________________________________________________

TOTAL: 543 543

MONTH TO DATE: 45,802

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT: 543 NOTICE(S) FOR 54,300 OZ (1.688 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 45,802 NOTICES FOR 4,580,200 OZ (142.43 TONNES)

SILVER

FOR JUNE

4 NOTICE(S) FILED TODAY FOR 29,000 OZ/

total number of notices filed so far this month: 398 for 1,990,000 oz

BITCOIN MORNING QUOTE $9685 DOWN $102

BITCOIN AFTERNOON QUOTE.: $9723 DOWN 66

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $40.40 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

A SMALL CHANGE IN GOLD INVENTORY AT THE GLD// A PAPER WITHDRAWAL OF 1.16 TONNES OF GOLD INTO THE GLD//

GLD: 1,132.21 TONNES OF GOLD//

WITH SILVER DOWN 46 CENTS TODAY: AND WITH NO SILVER AROUND

A SMALL PAPER WITHDRAWAL 648,000 OZ

RESTING SLV INVENTORY TONIGHT:

SLV: 472.663 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A STRONG SIZED 2664 CONTRACTS FROM 168,156 UP TO 170,820 AND FURTHER FROM OUR NEW RECORD OF 244,710, (FEB 25/2020. THE STRONG SIZED GAIN IN OI OCCURRED WITH OUR VERY GOOD 8 CENT GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS DUE TO STRONG BANKER SHORT COVERING PLUS A GOOD EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A TINY DECREASE IN SILVER OZ STANDING AT THE COMEX FOR JUNE. WE HAD A NET GAIN IN OUR TWO EXCHANGES OF 3419 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUMONGOUS AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: MAY: 0 AND JULY: 755 AND SEPT 0 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 755 CONTRACTS. WITH THE TRANSFER OF 755 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 735 EFP CONTRACTS TRANSLATES INTO 3.775 MILLION OZ ACCOMPANYING:

1.THE 8 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.045 MILLION OF INITIALLY STANDING FOR JUNE

THURSDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 8 CENTS).. AND,OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS. THE CONSIDERABLE GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A TINY DECREASE IN SILVER OZ STANDING FOR JUNE,3) CONSIDERABLE BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A NET GAIN OF 3419 CONTRACTS OR 17.095 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

SPREADING OPERATIONS

OUR SPREADING OPERATION HAS NOW SWITCHED INTO SILVER…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN SILVER AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JULY.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF JUNE. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

JUNE

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF JUNE:

2766 CONTRACTS (FOR 6 TRADING DAY(S) TOTAL 2766 CONTRACTS) OR 13.830 MILLION OZ: (AVERAGE PER DAY: 461 CONTRACTS OR 2.305 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 13.830 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 1.609% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,079.94 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP SO FAR 13.830 MILLION OZ.

EXCHANGE FOR PHYSICAL ISSUANCE FOR THE PAST 60 DAYS IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD AN EXTREMELY LARGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2664, WITH OUR VERY GOOD 8 CENT GAIN IN SILVER PRICING AT THE COMEX ///THURSDAY… THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 755 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A STRONG SIZED OI CONTRACTS ON THE TWO EXCHANGES: 3365 CONTRACTS (WITH OUR 8 CENT GAIN IN PRICE)

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 755 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A LARGE SIZED INCREASE OF 2664 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED DESPITE A GOOD 8 CENT GAIN IN PRICE OF SILVER/AND A CLOSING PRICE OF $17.80 // THURSDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.856 BILLION OZ TO BE EXACT or 122% of annual global silver production (ex Russia & ex China).

FOR THE NEW JUNE DELIVERY MONTH/ THEY FILED AT THE COMEX: 4 NOTICE(S) FOR 20,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.045 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A CONSIDERABLE SIZED 1711 CONTRACTS TO 471,358 AND FURTHER FORM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE CONSIDERABLE SIZED LOSS OF COMEX OI OCCURRED DESPITEOUR STRONG GAIN IN PRICE OF $20.60 /// COMEX GOLD TRADING// THURSDAY// WE HAD STRONG BANKER SHORT COVERING,ANOTHER HUMONGOUS SIZED INCREASE IN GOLD OZ STANDING AT THE COMEX, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A GOOD EX. FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR STRONG GAIN IN PRICE OF $20.60 .

WE HAD A VOLUME OF 2 4 -GC CONTRACTS//OPEN INTEREST 13

WE GAINED A GOOD SIZED 1886 CONTRACTS (5.8666 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3365 CONTRACTS:

CONTRACT JUNE 0.; AUG 3365 AND ALL OTHER MONTHS ZERO//TOTAL: 3365. The NEW COMEX OI for the gold complex rests at 471,358. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1654 CONTRACTS: 1479 CONTRACTS DECREASED AT THE COMEX AND 3365 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 1654 CONTRACTS OR 5.1446 TONNES. THURSDAY, WE HAD A GAIN OF $20.60 IN GOLD TRADING.…..

AND WITH THAT GAIN IN PRICE, WE HAD A GOOD SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 5.1446 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $20.60).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS UNSUCCESSFUL (SEE BELOW).

4 GC VOLUME: 2 // open interest 13

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3365) ACCOMPANYING THE CONSIDERABLE SIZED LOSS IN COMEX OI (1711 OI): TOTAL GAIN IN THE TWO EXCHANGES: 1886 CONTRACTS. WE NO DOUBT HAD 1 )CONSIDERABLE BANKER SHORT COVERING, 2.)ANOTHER HUMONGOUS INCREASE IN GOLD OUNCES STANDING AT THE GOLD COMEX FOR THE FRONT JUNE MONTH, 3) ZERO LONG LIQUIDATION; 4) CONSIDERABLE COMEX OI LOSS.. AND …ALL OF THIS WAS COUPLED WITH OUR STRONG GAIN IN GOLD PRICE TRADING//THURSDAY//$20.60

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

JUNE

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAY(S) IN TONNES: 34.98 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 45.45/3550 x 100% TONNES =12.80% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 2861.12 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 45.45 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 2664 CONTRACTS FROM 168,156 UP TO 170,820 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE STRONG GAIN IN OI SILVER COMEX WAS DUE TO; 1) CONSIDERABLE BANKER SHORT COVERING , 2) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A TINY DECREASE IN SILVER OZ STANDING AT THE COMEX FOR JUNE AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 755 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY: 755 CONTRACTS AND SEPT: 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 755 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2664 CONTRACTS TO THE 755 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 3419 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 17.095 MILLION OZ!!! OCCURRED WITH THE 8 CENT GAIN IN PRICE///

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 8 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// THURSDAY. WE ALSO HAD A GOOD SIZED 755 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 11.55 POINTS OR 0.40% //Hang Sang CLOSED UP 404.11 POINTS OR 1.66% /The Nikkei closed UP 167.99 POINTS OR 0.74%//Australia’s all ordinaires CLOSED UP .07%

/Chinese yuan (ONSHORE) closed UP at 7.0945 /Oil UP TO 38.32 dollars per barrel for WTI and 41.30 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 7.0945 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.0924 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY [PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC USA RIOTS// : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

i)we had 1 deposits into the customer account

into JPMorgan: 0

ii)into Scotia 598,328.000 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.819 million oz of total silver inventory or 51.22% of all official comex silver. (160.819 million/314.220 million

total customer deposits today: 598,328.000 oz

we had 2 withdrawals:

i) Out of Delaware: 6093.700 oz

iii) Out of CNT 30,237.000 oz

total withdrawals; 36,330.74 oz

We had 0 adjustments

total dealer silver: 85.401 million

total dealer + customer silver: 313.700 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The total number of notices filed today for the JUNE 2020. contract month is represented by 4 contract(s) FOR 20,000 oz

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 398 x 5,000 oz = 1,990,,000 oz to which we add the difference between the open interest for the front month of JUNE.(15) and the number of notices served upon today 4 x (5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JUNE/2019 contract month: 398 (notices served so far) x 5000 oz + OI for front month of JUNE (15)- number of notices served upon today 4) x 5000 oz of silver standing for the JUNE contract month.equals 2,045,000 oz.

We LOST 1 contracts or an additional 5,000 oz will NOT stand for delivery as they morphed into London based forwards as well as accepting a fiat bonus for their effort..

TODAY’S ESTIMATED SILVER VOLUME: 101,059 CONTRACTS // volume high/raid

FOR YESTERDAY: 69,042 CONTRACTS..,CONFIRMED VOLUME//low

YESTERDAY’S CONFIRMED VOLUME OF 69,042 CONTRACTS EQUATES to 345 million OZ 49.3% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO- 1.09% ((JUNE 5/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.58% to NAV: (JUNE 5/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 1.09%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 16.38 TRADING 16.30///NEGATIVE 0.47

END

And now the Gold inventory at the GLD/

JUNE 5//WITH GOLD DOWN $40.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A PAPER WITHDRAWAL OF 1.16 TONNES OUT OF THE GLD//INVENTORY RESTS AT 1132.21 TONNES

JUNE 4//WITH GOLD UP $20.60: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD…A DEPOSIT OF 4.09 TONNES INTO THE GLD//INVENTORY RESTS AT 1133.37 TONNES

JUNE 3//WITH GOLD DOWN $26.15//A SMALL CHANGE IN GOLD INVENTORY//A DEPOSIT OF 0.78 TONNES OF GLD INTO THE GLD//INVENTORY RESTS AT 1129.28 TONNES

JUNE 2//WITH GOLD DOWN $11.20 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1128.40 TONNES

JUNE 1//WITH GOLD UP $1.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES OF GOLD//GLD INVENTORY RESTS TONIGHT AT 1123.14 TONNES

MAY 29/WITH GOLD UP $19.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///GLD INVENTORY RESTS THIS WEEKEND AT 1119.05 TONNES

MAY 28//WITH GOLD UP $4.00 TODAY/NO CHANGES IN GOLD INVENTORY TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

MAY 27/WITH GOLD UP $.10 TODAY: A STRONG 2.34 TONNES OF GOLD ADDED TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

MAY 26//WITH GOLD DOWN $23.05//NO CHANGES IN GOLD INVENTORY://RESTS TONIGHT AT 1116.71 TONNES

MAY 22//WITH GOLD UP $13.05//A BIG CHANGE IN GOLD INVENTORY:: A PAPER ADDITION OF 3.93 TONNES//INVENTORY RESTS THIS WEEKEND AT: 1116.71 TONNES

MAY 21//WITH GOLD DOWN $26.70//NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1112.32 TONNES

MAY 20/WITH GOLD UP $7.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 1.46 TONNES FROM THE GLD////INVENTORY RESTS TONIGHT AT 1112.32 TONNES

MAY 19//WITH GOLD UP $10.60//NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1113.78 TONNES

MAY 18/WITH GOLD DOWN $15.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A PAPER DEPOSIT OF 9.06 TONNES./INVENTORY RESTS AT 1113.78 TONNES

MAY 15.WITH GOLD UP $16.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 12.58 TONNES/ INVENTORY RESTS AT 1104.72 TONNES

MAY 14//WITH GOLD UP $19.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1092.14 TONNES

MAY 13//WITH GOLD UP $9.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 11.07 TONNES/INVENTORY RESTS AT 1092.14 TONNES

MAY 12//WITH GOLD UP $6.60 TODAY; A SMALL CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 1081.07 TONNES

MAY 11/WITH GOLD DOWN $12.65 TODAY: NO CHANGES IN GOLD INVENTORY: //INVENTORY RESTS AT 1081.65 TONES..

MAY 8/WITH GOLD DOWN $7.00 TODAY; A BIG CHANGE IN GOLD INVENTORY: A PAPER ADDITION OF 5.85 TONNES/INVENTORY RESTS AT 1081.65 TONNES

MAY 7/WITH GOLD UP $29.65 TODAY : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER ADDITION OF .41 TONNES/INVENTORY RESTS AT 1075.80 TONNES

MAY 6//WITH GOLD DOWN $17.00 TODAY/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER ADDITION OF 3.68 TONNES/INVENTORY RESTS AT 1075.39 TONES

MAY 5/WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER ADDITION OF 3.81 TONNES//INVENTORY RESTS AT 1071.71 TONNES

MAY 4//WITH GOLD UP $12.00 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE PAPER DEPOSIT OF 11.4 TONNES INTO THE GLD////GOLD INVENTORY RESTS AT 1067.90 TONNES

MAY 1/WITH GOLD UP $8.45 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1056.50 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

JUNE 5/ GLD INVENTORY 1132.21 tonnes*

LAST; 835 TRADING DAYS: +187.29 NET TONNES HAVE BEEN REMOVED FROM THE GLD

LAST 735 TRADING DAYS://+362.49 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JUNE 5/WITH SILVER DOWN 46 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 648,000 OZ FROM THE SLV////INVENTORY RESTS AT 472.663 MILLION OZ

JUNE 4//WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV.//INVENTORY RESTS AT 473.315 MILLION OZ//

JUNE 3//WITH SILVER DOWN 23 CENTS TODAY//NO CHANGES IN SILVER INVENTORY AT THE SLV//

INVENTORY RESTS AT 473.315 MILLION OZ//

JUNE 2//WITH SILVER DOWN 31 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUMONGOUS 6.686 MILLION OZ ADDED TO THE SLV////INVENTORY RESTS TONIGHT AT 473.315 MILLION OZ//

JUNE 1//WITH SILVER UP 38 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.56 MILLION OZ INTO THE SLV////INVENTORY RESTS TONIGHT AT 466.629 MILLION OZ//

MAY 29//WITH SILVER UP 52 CENTS TODAY: A MASSIVE DEPOSIT OF 2.796 MILLION OZ INTO THE SLV//INVENTORY RESTS THIS WEEKEND AT 463.273 MILLION OZ//

MAY 28//WITH SILVER UP 9 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.660 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 460.477 MILLION OZ//

MAY 27/WITH SILVER UP 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 455.817 MILLION OZ//

MAY 26//WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/// INVENTORY RESTS AT 455.817 MILLION OZ//

MAY 22/WITH SILVER UP 22 CENTS TODAY/ A HUGE PAPER WITHDRAWAL OF 1.864 MILLION OZ//INVENTORY RESTS AT 455.817 MILLION OZ/

LAST 5 DAYS: SILVER UP 60 CENTS: INVENTORY UP A WHOOPING 23.767 MILLION OZ///

MAY 21/WITH SILVER DOWN 50 CENTS TODAY: A HUGE PAPER DEPOSIT OF 7.923 MILLION OZ///INVENTORY RESTS AT 457.681 MILLION OZ//

MAY 20//WITH SILVER UP ANOTHER 11 CENTS TODAY: A HUGE CHANGE IN SLV INVENTORY: A HUGE PAPER DEPOSIT OF 9.601 MILLION OZ INTO THE SLV// //INVENTORY RESTS AT 449.758 MILLION OZ

MAY 19/WITH SILVER UP ANOTHER 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 440.157 MILLION OZ//

MAY 18/WITH SILVER UP ANOTHER 48 CENTS TODAY: TWO BIG CHANGES IN SILVER INVENTORY AT THE SLV I.E. 2 PAPER DEPOSIT OF ( I) 8.39 MILLION OZ AND THEN ( 2) 8.109 MILLION OZ//INVENTORY RESTS AT 432.048 MILLION OZ// (TOTAL DEPOSITS 16.500 MILLION OZ///)

MAY 15/WITH SILVER UP 81 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV: /INVENTORY RESTS AT 423.65 MILLION OZ.

MAY 14//WITH SILVER UP 33 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV.//INVENTORY RESTS AT 423.65 MILLION OZ

MAY 13/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.79 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 423.65 MILLION OZ//

MAY 12/WITH SILVER UP 5 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.076 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 420.861 MILLION OZ//

MAY 11.WITH SILVER DOWN 5 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 417.785 MILLION OZ//

MAY 8/WITH SILVER UP 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTER DEPOSIT OF 4.661 MILLION OZ OF SILVER INTO THE SLV..///INVENTORY RESTS AT 417.785 MILLION OZ//

MAY 7/WITH SILVER UP 45 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 5/WITH SILVER UP 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ///

MAY 4//WITH SILVER DOWN 5 CENTS TODAY:2 HUGE PAPER CHANGES IN SILVER INVENTORY AT THE SLV.i).A LARGE 1.399 MILLION OZ OF PAPER SILVER REMOVED FROM THE SLV//..//INVENTORY RESTS AT 411.427 MILLION OZ and ii) A LARGE 1.647 MILLION OZ OF PAPER SILVER ADDED TO THE SLV// INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 1/WITH SILVER FLAT IN PRICE: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 412.826 MILLION OZ///

JUNE 5.2020:

SLV INVENTORY RESTS TONIGHT AT

472.663 MILLION OZ.

END

LIBOR SCHEDULE AND GOFO RATES// GOLD LEASE RATES

YOUR DATA…..

6 Month MM GOFO 2.35/ and libor 6 month duration 0.48

Indicative gold forward offer rate for a 6 month duration/calculation:

GOLD LENDING RATE: -1.87%

NEGATIVE GOLD LEASING RATES INCREASING BY A HUGE AMOUNT//GOLD SCARCITY AND CENTRAL BANKS CALLING IN ALL OF THEIR GOLD LEASES

XXXXXXXX

12 Month MM GOFO

+ 1.92%

LIBOR FOR 12 MONTH DURATION: 0.63

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -1.29%

NEGATIVE GOLD LEASING RATES INCREASING BY A HUGE AMOUNT//GOLD SCARCITY AND CENTRAL BANKS CALLING IN ALL OF THEIR GOLD LEASES

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

Mish Shedlock totally misrepresents GATA

(Chris Powell/GATA)

Mish Shedlock misrepresents GATA

Submitted by cpowell on Thu, 2020-06-04 17:04. Section: Daily Dispatches

1:07p ET Thursday, June 4, 2020

Dear Friend of GATA and Gold:

In his June 1 commentary, “Speculators Dump Gold But Price Goes Up Anyway” —

https://www.thestreet.com/mishtalk/economics/speculators-dump-gold-but-p…

— market analyst and money manager Mish Shedlock grossly misrepresents GATA with this assertion:

“Many gold analysts, from the mainstream to fringe groups such as the Gold Anti-Trust Action Committee, claim that they can predict what the gold price will do by adding up annual fabrication and investment demand (as well as de-hedging demand by miners) and contrasting the resulting total with annual supply (mine supply, central bank selling, disinvestment and scrap). In short, they analyze the gold market in the same manner as they would analyze the copper market.”

This is completely false and Shedlock provides no evidence for his assertion.

GATA does not claim that we can predict the gold price by calculating and integrating the variables Shedlock cites.

Rather, GATA exposes, documents, and challenges the government-instigated and underwritten manipulations of and interventions in the monetary metals markets, manipulations and interventions Shedlock never dares to acknowledge.

GATA’s documentation is archived here —

http://gata.org/taxonomy/term/21

— and much of it is summarized here:

If he ever gains any intellectual honesty, Shedlock is welcome to address it, document by document.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

In case you missed this yesterday, I am repeating this important interview for you

(Andrew Maguire/Bill Murphy/GATA)

London metals trader Andrew Maguire interviews GATA chairman on market manipulation

Submitted by cpowell on Thu, 2020-06-04 16:40. Section: Daily Dispatches

12:40p ET Thursday, June 4, 2020

Dear Friend of GATA and Gold:

On behalf of Kinesis Money, London metals trader Andrew Maguire today interviews GATA Chairman Bill Murphy about gold and silver market manipulation, the heavy involvement of JPMorganChase & Co., the diminishing effectiveness of the usual smashdowns in the market, and the growing tightness in the physical market for the monetary metals, which foreshadows big surges in prices. The interview is 46 minutes long and an be viewed at YouTube here:

https://www.youtube.com/watch?v=qSWd48VU7PQ

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

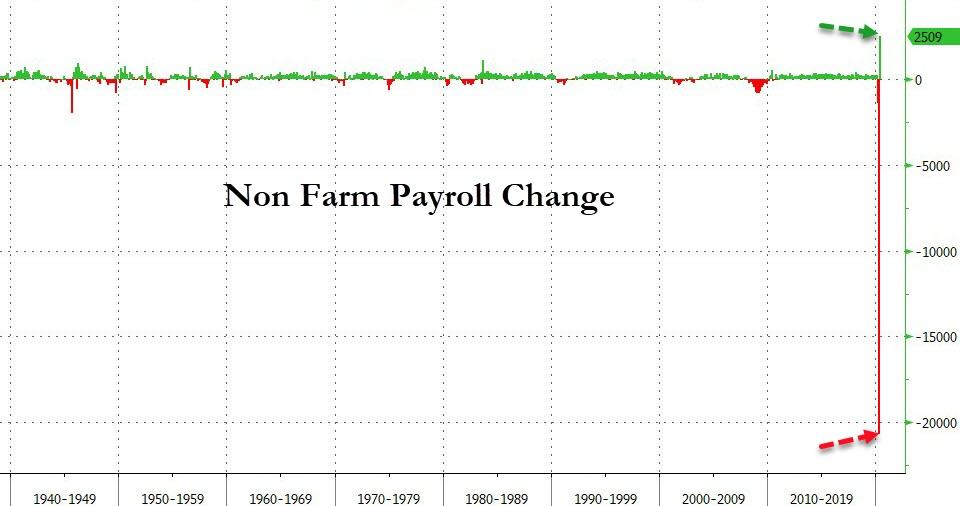

Stocks Soar On Fresh Stimulus Flood Ahead Of Worst Unemployment Print In US History

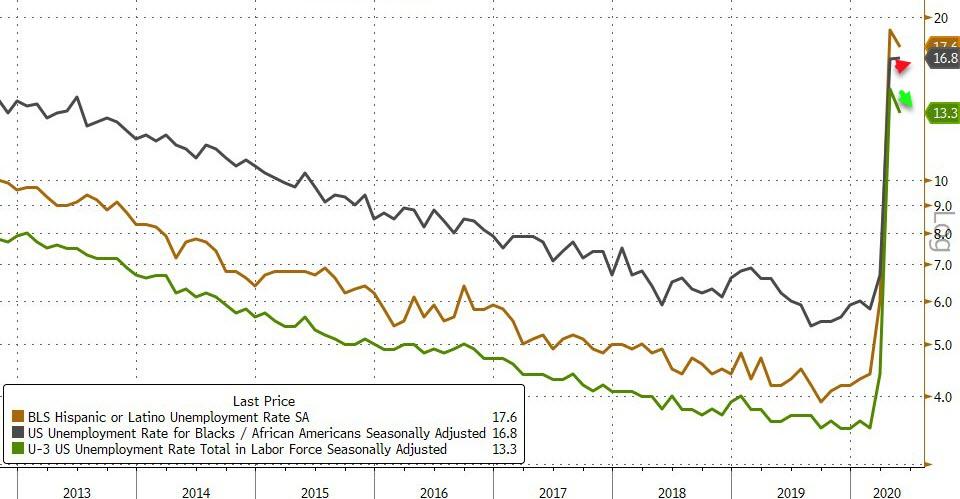

Just when it seemed that the record 40% rally from the March lows was coming to an end, as Treasury yields blew out and tech names rolled over on record volume, the euphoria came back with a vengeance, sending stocks around the globe and US futures surging as the delivery of both monetary and fiscal stimulus in Europe supplanted virus concerns and trade fears on the day the US is expected to report a record 19.1% unemployment rate (luckily, in “Jay’s market” trivia such as fundamentals does not matter).

On Thursday, the Nasdaq 100 became the first U.S. equity index to reclaim its all-time high, with the rebound driven partly by tech-related firms including Amazon.com Inc and Netflix. The broader Nasdaq Composite which is more closely watched than the Nasdaq 100, is just about 2% below its own record high, while the S&P 500 and Dow Jones indexes are 8% and 11% below their respective all-time highs. The S&P 500 is on track for a third week of gains as VIX and V2X returned to the week’s lows, and the sliding dollar has fallen to the lowest since March, while Treasury yields jumped to 0.87%, rising above a key level of 0.84% that sees CTA turn short on Treasurys.

Boeing gained 4% premarket on continued optimism about a pickup in air travel a day after American Airlines Group Inc said it would boost its U.S. flight schedule next month. Vaccine maker Novavax jumped 14.9% after saying it would receive up to $60 million from the U.S. Department of Defense to fund manufacturing of its COVID-19 vaccine candidate.

European equities rallied, with the Spanish IBEX outperforming peers, rising over 2%. Banks, autos and energy names lad broad based gains across sectors, after monetary stimulus from the ECB and fiscal stimulus from Frankfurt and Berlin exceeded expectations, and reports showed that Trump administration officials increasingly expect to spend up to $1 trillion in the next round of stimulus, even as Germany reported a record -25.8% drop in Industrial Orders.

Earlier in the session, Asian stocks gained, led by energy and finance, after rising in the last session. The Topix gained 0.5%, with Fujikyu and DLE rising the most. The Shanghai Composite Index rose 0.4%, with Hunan Corun New Energy and Shangying Global posting the biggest advances.

Markets are riding a wave of enthusiasm as investors bet on a global economy awash with stimulus, while fears of more disruptions from social unrest have also reduced in the past two days, with the largely peaceful protests against the killing of a black man in police custody waning into Friday morning and emergency curfews in many cities being lifted.

“We probably have a window of maybe three months where data are going to be continuing to improve,” Peter Chatwell, head of multi-asset strategy at Mizuho International, told Bloomberg TV. “That is going to drive a very supportive backdrop for credit spreads to keep tightening and for equities to be rallying.”

In rates, the sharp bear-steepening continued in Treasuries ahead of May employment report, with 10- to 30-year yields cheaper by 5bp to 6bp, front-end yields by about 1bp. 5s30s spread topped 125bp for first time since December 2016. Treasury 10-year yields around 0.87%, near cheapest levels of the day and highest since end of March; Thursday’s breach of top of narrow range in place since late March led to CTA accounts shedding long positions, which has added momentum to this week’s bear-steepening trend.

In Europe, yield curves also bear steepened with several ECB speakers commenting on the appropriateness of Thursday’s policy boost. Peripheral spreads continued Thursday’s tightening to core; Bund and Gilt futures rise off the lows with Treasuries sidelined ahead of today’s payroll report.

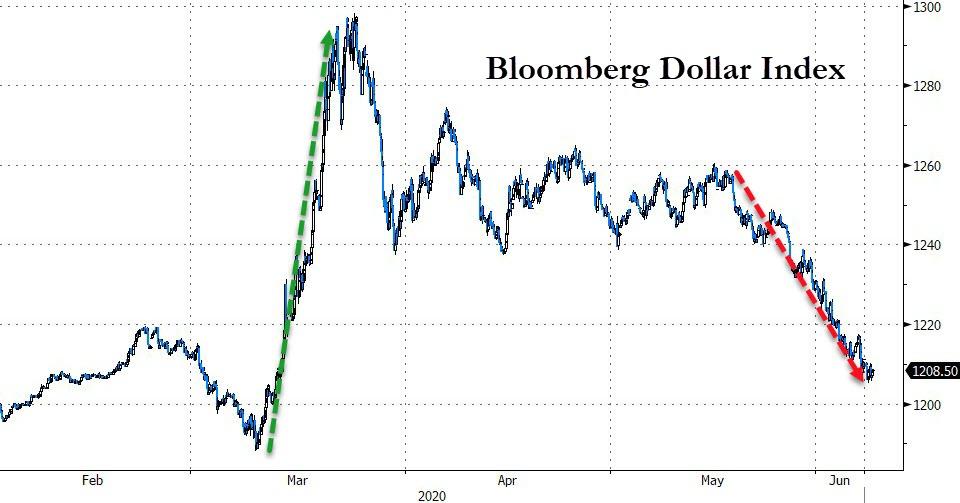

In FX, Bloomberg dollar index extended Asia’s decline. AUD leads G-10 peers, regaining a 0.70-handle for the first time in five months. Havens currencies including CHF and JPY lag.

In commodities, Crude futures rallied with front-month Brent rising through $41 to fresh highs for the week after OPEC+ reached a tentative agreement to extend record production cuts. Spot gold grinds sideways near $1,710/oz, base metals rally with LME lead outperforming.

The focus for traders this morning will be the U.S. jobs report, which is likely to reflect a deepening recession across the country. But despite the grim economic news, markets are continuing to a historic rally. Friday’s report from the Labor Department is likely to show the U.S. unemployment rate shooting up to almost 20% in May, a new post-World War Two record, but investors have so far shrugged off dire data on hopes that an easing of coronavirus-led lockdowns would revive business activity.

Market Snapshot

- S&P 500 futures up 1% to 3,142.00

- MXAP up 0.7% to 158.88

- MXAPJ up 1% to 512.71

- Nikkei up 0.7% to 22,863.73

- Topix up 0.5% to 1,612.48

- Hang Seng Index up 1.7% to 24,770.41

- Shanghai Composite up 0.4% to 2,930.80

- Sensex up 0.9% to 34,288.23

- Australia S&P/ASX 200 up 0.1% to 5,998.72

- Kospi up 1.4% to 2,181.87

- STOXX Europe 600 up 1.3% to 370.98

- German 10Y yield rose 1.3 bps to -0.307%

- Euro up 0.08% to $1.1347

- Italian 10Y yield fell 13.2 bps to 1.25%

- Spanish 10Y yield rose 0.3 bps to 0.559%

- Brent futures up 2.8% to $41.11/bbl

- Gold spot down 0.3% to $1,709.41

- U.S. Dollar Index little changed at 96.64

Top Overnight News from Bloomberg

- Traders are having another look at market pricing for the outlook for Federal Reserve rates. The latest improvement in risk sentiment has damped chatter about negative rates and some investors seem willing to bet on when to expect a rate hike premium appearing

- OPEC+ is set to extend production cuts to prop up the oil market after a breakthrough in high-stakes negotiations, with the alliance meeting on Saturday to sign off on the deal

- The latest round of talks between the U.K. and European Union over their future relationship is set to finish without a breakthrough, with both sides stuck after another week of difficult negotiations

- Fears of deflation justified the European Central Bank’s decision to ramp up its emergency bond- buying program, according to policy maker Pablo Hernandez de Cos

- The German economy has passed the trough of its coronavirus recession and is starting to grow again, the Bundesbank said, endorsing the government’s sweeping fiscal stimulus that should underpin the rebound. Output this year is forecast to shrink 7.1%, before bouncing back in the subsequent two years

- Austria has nearly doubled its borrowing plans in order to help cushion its economy from the worst of the coronavirus crisis. The country will now raise about 60 billion euros ($68 billion) from debt operations in 2020, an all-time high, according to the Treasury. At least 35 billion euros will be by way of government bond offerings

- The Swiss National Bank’s holdings of foreign exchange rose by a double-digit billion franc figure for a second month running, evidence of the heavy interventions to limit pressure on the currency

Asian equity markets were choppy with the region cautious as participants awaited the looming NFP jobs data and after the rally in stocks petered out for its global peers which saw Wall Street end a choppy session mixed albeit with a negative bias. ASX 200 (+0.1%) was dragged by notable weakness in tech and healthcare names but with downside in the index stemmed by resilience in financials. Furthermore, the government announced to increase rules on foreign investment into key industries which raised some questions regarding the ramifications its protectionism could have on its ties with its largest trading partner China although PM Morrison suggested the investment reforms are unlikely to increase ongoing tensions. Nikkei 225 (+0.7%) was initially lower but gradually reversed the downside amid currency weakness, while Hang Seng (+1.7%) and Shanghai Comp. (+0.4%) traded indecisively after the PBoC’s operations resulted to a CNY 450bln weekly net liquidity drain and following mixed US-China rhetoric including USTR Lighthizer expressing confidence regarding the Phase 1 deal and with the US to continue permitting Chinese passenger flights in reciprocation to a similar gesture by China, although plenty of criticism remained following the anniversary of the Tiananmen Square massacre and Hong Kong’s passage of the national anthem bill. Finally, 10yr JGBs were subdued following the resumption of the bear steepening seen in USTs, but with some of the losses in 10yr JGBs briefly retraced after prices rebounded off a floor at 151.55 and with the BoJ present in the market for nearly 1.1tln of JGBs in which it boosted purchase amounts in 5yr-10yr maturities.

Top Asian News

- Japan Household Spending Falls Most on Record Amid Pandemic

- NetEase Is Said to Raise $2.7 Billion in Hong Kong Listing

- Lawmakers in Eight Countries Form New Alliance to Counter China

- Hong Kong Dollar Sees Inflow Surge, Staring Down Capital Flight

European equity futures are on course for respectable weekly gains with Eurostoxx 50 eyeing double-digit weekly gains as we stand. The morning has seen the core bourses extending on the upside with sentiment potentially underpinned amid comments from USTR who said he feels “very good” about the Phase 1 US-China trade deal and that the report that China was not honouring the soybean purchases was false. That being said, more recent headlines from China vowed to retaliate against the US’ 33 Chinese entity list in relation to the Uygur minority population. However, details remain light – the news prompted some losses in equities, but nonetheless, Euro Stoxx 50 (+1.7%) holds onto gains of almost 2%. Desks also note that there is a significant cyclical/value bias as sectors such as autos, banks and energy all post substantial gains – with the SX7E European banking index poised to end the with over 13% higher W/W. The sectorial breakdown sees banks (+3.5%) topping the charts amid the higher yield environment and with Oil and & Gas closely following amid gains in the oil complex. Travel & Leisure meanwhile surges with some pointing to impetus form the America Air update yesterday – Air France (+12.3%), Carnival (+10.9%) trade at the top of the Stoxx 600. Broader sectors are mostly higher with cyclicals clearly outpacing defensives, while Staples and Healthcare reside in the red. In terms of individual movers – Deutsche Wohnen (+1.5%) holds onto opening gains after being tipped to replace Lufthansa (+6.0%) – whose shares see tailwind from the broader sector performance. Telefonica (+3.8%) meanwhile is underpinned amid talks of an imminent sale of its German Towers unit.

Top European News

- SNB Reserves Rose in May Reflecting Bigger Interventions

- Austria Doubles 2020 Borrowing to $68 Billion on Virus Fallout

- Billionaire-Owned Firms Tap State Aid In U.K. Loan Program

- ECB’s De Cos Says Rising Deflation Risk Warranted More Stimulus

In FX, the Antipodean Dollars have both overcome several wobbles on the way to fresh highs against their rival, with the Kiwi and Aussie now trying to establish footholds above new big figures, at 0.6500 and 0.7000 respectively. A firm rebound in risk sentiment has helped the Nzd and Aud extend their winning streaks, but the former has also gleaned impetus from upbeat comments overnight via NZ Finance Minister Robinson noting a faster recovery in the domestic economy and pick up in retail sales. Hence, the cross remains well off post-RBA peaks and pivoting 1.0750, with some mild hindrance for the Aud on strained relations with its main global trading partner and investment reforms designed to tighten the criteria for foreign entities.

- NOK/GBP – The next best majors, as the Norwegian Crown continues its bull run irrespective of more bleak data in the form of manufacturing output and GDP while perhaps drawing more encouragement from accompanying remarks from the Stats Office that economic activity appears to be improving. Eur/Nok has dipped below 10.5400 even though the Euro remains relatively strong in its own right post-ECB, and another rise in oil prices on reports that OPEC and OPEC+ are now set to meet tomorrow is no doubt keep the cross on a downward trajectory. Meanwhile, the Pound forged more gains at the expense of the Buck in Cable terms when stops were tripped at resistance just ahead of 1.2650 and more when the 200 DMA (1.2678) was breached, but hit buffers before 1.2700 despite Eur/Gbp remaining much nearer the bottom of 0.9009-0.8954 parameters awaiting a speech from EU’s Barnier after latest Brexit trade talks with the UK that are expected to end with no breakthrough, albeit apparently more constructive and useful this week per EU sources.

- CAD/EUR/JPY/CHF – All more narrowly mixed vs their US counterpart as the DXY bounces from a deeper 96.438 low to 96.849 in wake of latest Chinese warnings about countermeasures against US sanctions on firms, but with the Loonie supported by the aforementioned upturn in crude and also mega option expiry interest at 1.3500 (2.3 bn). Elsewhere, the Euro extended ECB inspired advances to circa 1.1384, ignoring more weak Eurozone data and mixed GC rhetoric, though taking heed of the China headlines, as did the Yen and Franc to various degrees when paring some declines from around 109.40 and 0.9580, though still undermined by overall safe-haven unwinding and technical impulses as Usd/Jpy breached another upside chart level (109.38 was the April 6 lower high) and Eur/Chf straddles 1.0850 after breaking back above the 200 DMA.

- EM – Mixed starts to Friday’s session and in the run up to potentially pivotal US jobs data, as the Yuan maintains bullish momentum and petro-currencies derive more traction from crude in contrast to the Lira that displays some nerves ahead of Turkey’s next ratings review at the hands of Moody’s and President Erdogan’s decision to reimpose lockdown over the coming weekend due a rise in COVID-19 cases..

In commodities, WTI and Brent front month future continue to grind higher on the final trading session of the week with a few factors at play in the energy complex. On the OPEC front, a meeting has reportedly scheduled for 13:00BST and OPEC+ for 15:00BST on June 6th, according to delegates – Russian Energy Minister Novak confirmed the date. However, early signs indicating that Mexico might have objections to extending the current OPEC+ pact – which may prove to be somewhat of a deja-vu from the April meeting. In terms of the agreement, aside from the pledge for full compliance, Saudi Arabia and Russia reportedly agreed on a preliminary 1-month extension on existing OPEC+ oil cuts, according to sources. Meanwhile, Gulf OPEC members (Saudi, UAE and Kuwait) are reportedly not discussing deeper cuts than the voluntary over-compliance of 1.18mln BPD in June. Sources also added that Saudi Arabia is set wind down on voluntary over-compliance to bring 1mln BPD of production back online. In terms of other factors – with US hurricane season looming, Tropical depression Cristobal is set to strengthen and head over to the Gulf of Mexico over the weekend – potentially shuttering the several oil refineries as it makes landfall. The upside in oil prices is also underpinned by the current risk appetite across the marketplace as prices also tracked stocks higher early-doors. WTI July reclaimed a USD 38/bbl (vs. low 37.05/bbl) while Brent breached USD 41/bbl having printed an intraday base at 39.72/bbl. Elsewhere, spot gold remains lacklustre just above USD 1700/oz and with little action ahead of the US labour market report. Copper prices meanwhile extend on upside in-line with the risk sentiment and stocks as it overlooks US-Sino difficulties for now.

US Event Calendar

- 8:30am: Average Weekly Hours All Employees, est. 34.3, prior 34.2

- 8:30am: Change in Nonfarm Payrolls, est. -7.5m, prior -20.5m

- 8:30am: Change in Private Payrolls, est. -6.75m, prior -19.6m

- 8:30am: Change in Manufact. Payrolls, est. -400,000, prior -1.33m

- 8:30am: Unemployment Rate, est. 19.1%, prior 14.7%

- 8:30am: Two-Month Payroll Net Revision

- 8:30am: Average Hourly Earnings MoM, est. 1.0%, prior 4.7%

- 8:30am: Average Hourly Earnings YoY, est. 8.5%, prior 7.9%

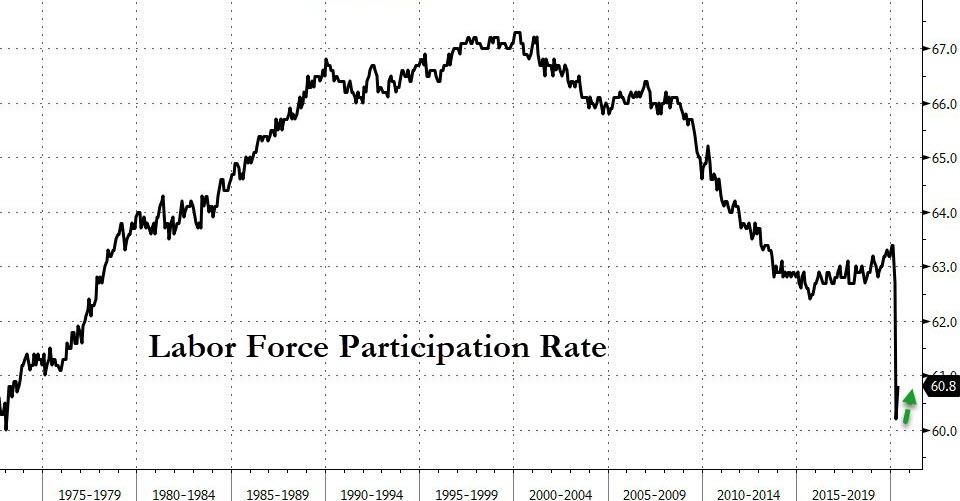

- 8:30am: Labor Force Participation Rate, est. 60.1%, prior 60.2%

- 8:30am: Underemployment Rate, prior 22.8%

- 3pm: Consumer Credit, est. $20.0b deficit, prior $12.0b deficit

DB’s Jim Reid concludes the overnight wrap

Following the remarkable recent rally for risk assets, the advance ran out of a little steam yesterday as economic data and news on the coronavirus acted as a reminder of the difficulties investors are still likely to face over the coming weeks and months, even in the face of yet more stimulus. On that the main news yesterday came from the ECB, who announced that they would be increasing the size of their Pandemic Emergency Purchase Programme (PEPP) by a further €600bn, which with the original €750bn announced back in March brings the total quantity of potential purchases up to €1.35tn. In addition, they announced that the horizon for net purchases will be extended from the end of 2020 until at least the end of June 2021, while maturing principal payments from securities purchased under the PEPP will be reinvested until at least the end of 2022. All-in-all this is actually a bit more than was expected by the consensus, with a majority of respondents to Bloomberg’s survey pointing to a smaller €500bn boost to purchases. DB were at €750bn.

In terms of the market response, sovereign debt rallied strongly in southern European countries. The spread of Italian 10yr yields over bunds fell by -16.7bps to 174bps, its tightest level in over 2 months, while the Spanish spread fell by -8.8bps to its tightest level in 3 months. The euro also rallied strongly, up by +0.93% against the US dollar to its highest level in nearly 3 months. That marked the 8th consecutive daily advance for the single currency, which is its longest streak of gains since 2011. Inflation expectations moved higher as well after the announcements, with five-year forward five-year inflation swaps for the Euro Area increasing +5.5bps to 1.07%, their highest level since early March.

Our European economists have more to say on the ECB (link here), but one thing they had a positive interpretation of was President Lagarde’s comments on the German constitutional court ruling. Lagarde said that she was “confident that a good solution will be found”, and noted it was up to the German government and parliament to come up with that. As far as the ECB is concerned, they’re under the jurisdiction of the ECJ rather than national courts. But Lagarde also said that the minutes of their latest meeting would show that the Governing Council debated the effectiveness, efficiency and cost/benefits of the “package of measures together”, something our European economists interpreted as referring to the entire monetary policy stance, including the PSPP that the German court ruled on. So this could be interpreted as the ECB indirectly satisfying the requirement from the German court for a new decision on the PSPP, which puts the pressure on the Bundesbank to ensure that the Bundestag’s review of proportionality is successful.

On the topic of stimulus, the Trump administration expects to spend another $1 trillion in a further round of spending to boost the economy. While Senate Majority leader McConnell has been trying to slow government expenditure in recent weeks, he has conceded that another stimulus bill may be needed of that amount, but that there are no plans to do so before the 3 July two-week recess. This would put any action at least 7 weeks away.

Today, attention will turn to the US jobs report for May, where we are once again expecting some historic milestones to be reached, albeit not in a good way. Following a record -20.537m decline in nonfarm payrolls for April, DB’s US economists write in their preview (link here) that they’re expecting a further -5.1m decline in May, with the unemployment rate soaring to 18.1%, its highest since the Great Depression in the 1930s. It is worth noting that there are substantial risks around this, and indeed the data is still likely to be messy when it comes to how to classify those affected by the coronavirus. Last month’s report saw the BLS note that many workers had been classified as employed but “not at work for other reasons”, when they probably should have been in the “unemployed on temporary layoff” category. So that could affect where the numbers come out.

Going into the jobs report, the good news is that the ADP’s report of private payrolls on Wednesday saw a far smaller decline than expected of -2.76m, rather than the -9m decline anticipated. On the other hand, yesterday’s jobless claims weren’t quite as good as hoped for, with the number of initial claims in the week through May 30 at 1.877m (vs. 1.833m expected). That’s the 9th consecutive weekly decline though, but the number still remains at nearly triple the pre-Covid record for weekly claims, which was at “only” 695k. Furthermore, the continuing claims number rose to 21.487m (vs. 20m expected), suggesting that the improvement seen the previous week didn’t mark the turning point that many had hoped for.

Overnight, it’s been another fairly mixed session for markets in the absence of any fresh newsflow. The biggest gain has been reserved for the Kospi (+0.89%) while the Nikkei (+0.20%) is also up. The Hang Seng is flat, while bourses in China are broadly down -0.25%. Futures on the S&P 500 are trading up +0.48% as we type. Elsewhere, WTI oil prices are little changed despite the news yesterday that Saudi Arabia and Russia have clinched a deal with Iraq and the cartel could meet as soon as this weekend to ratify it.

Yesterday we heard from US Trade Representative Robert Lighthizer, who said that he feels “very good” about the phase 1 trade deal with China, which was agreed to in January. He believes that China is doing enough to honour the pact during the pandemic. He cited the more than $100m of soybeans purchased by China this week, during a virtual event held by the Economic Club of New York. This refutes reports that Beijing had not been keeping up with its commitments on commodity purchases. When asked about the President’s recent remarks on the World Trade Organisation, Lighthizer said he does not favour the US pulling out of the WTO. The remarks as a whole broke from the recent war of words between the two countries over the past 3 weeks and struck a more conciliatory tone. This is good for risk assets broadly, even if it did not prop them up yesterday.

Back to markets and yesterday’s other moves, the S&P 500 fell back by -0.34% to end its run of 4 successive gains, and just its second daily loss in the last 10 sessions. In Europe the STOXX 600 also fell back -0.72%. Banks outperformed on both sides of the Atlantic however as sovereign bond yields in core countries continued to rise, while American Airlines led the S&P with a +41.10% move higher after they announced they’d be flying 55% of their July 2019 domestic capacity next month. Asian airline stocks have also rallied this morning on the back of American Airlines news. In fixed income, 10yr US Treasury yields were up +7.8bps, climbing above 0.8% for the first time since late March, and 10yr bund yields were also up +3.4bps. The dollar continued to lose ground though, falling -0.62% to be down for a 6th session running.

Finally, there wasn’t a great deal of economic data out yesterday, but the construction PMIs from Germany (40.1) and the UK (28.9) both saw a rebound from their April readings. We also had April’s Euro Area retail sales, which fell by a smaller-than-expected -11.7% (vs. -15.0% expected). From the US, the trade deficit in April came in at $49.4bn, but notably the combined value of US exports and imports was down to $352bn, its lowest since May 2010.

To the day ahead now, as previously mentioned the US jobs report for May is likely to be the main highlight. Other data out includes the Canadian employment report for May, along with German factory orders and Italian retail sales for April. It’s also the last day in the current round of post-Brexit negotiations between the UK and the EU.

3A/ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 11.55 POINTS OR 0.40% //Hang Sang CLOSED UP 404.11 POINTS OR 1.66% /The Nikkei closed UP 167.99 POINTS OR 0.74%//Australia’s all ordinaires CLOSED UP .07%

/Chinese yuan (ONSHORE) closed UP at 7.0945 /Oil UP TO 38.32 dollars per barrel for WTI and 41.30 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 7.0945 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.0924 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY [PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC USA RIOTS// : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

CHINA

China adopts for the first time personal bankruptcy laws as many face financial ruin. Before this, you just carried your debt to the grave

(zerohedge)

Shenzen Adopts China’s First Personal Bankruptcy Laws As Small Businesses, Freelancers Face Financial Ruin

Surprisingly enough, considering that it’s a Communist State founded – at least, in theory – on the principles of social justice and equality, China doesn’t have personal bankruptcy laws, and individuals who are saddled with debt, medical or otherwise, are typically held liable for these debts until death.

However, back in 2007, as Beijing shifted its drift toward ‘economic liberalization’ into hyperdrive, the country adopted corporate bankruptcy laws. Corporate bankruptcies have surged in recent years, and earlier this year, we discussed expectations that the number for 2020 would be even higher, as the coronavirus upends the Chinese economy.

Now, Shenzhen, known as the “Silicon Valley” of the mainland, has drafted China’s first personal bankruptcy laws as the southern city prepares for what’s expected to be a wave of bankruptcies, particularly among the freelancers and smaller contractors common in China’s tech sector. The rules are intended to give “honest and unfortunate” debtors the chance to escape the mire of debt and make a comeback.

Despite corporate bankruptcy laws nationwide since 2007, individuals are still held personally liable for business debts, which makes it virtually impossible for entrepreneurs to be ‘okay’ with failure, like American entrepreneur gurus have advised.

China’s personal bankruptcy process bears certain – shall we say – “Chinese characteristics”. For example, the state will monitor the finances of those who file for personal bankruptcy for three years.

The draft rules, open for public comment until June 18, allow Shenzhen residents who cannot pay their debts to apply for personal bankruptcy if they have paid social insurance in the city for at least three years.

Once approved, applicants will spend at least three years in a supervised “probation” period before all or part of their debts are wiped clean. During this time their expenditure will be supervised, the draft rules said.

Other major Chinese cities are expected to follow in Shenzen’s footsteps as Beijing cranks up the stimulus and hastily reopens its economy. To prevent a second wave, it has embraced dramatic tactics like mass surveillance testing, which were used to test every citizen of Wuhan, something China purportedly finished doing last week (affording to state media).

Reuters claimed 76 companies filed for bankruptcy with the Shenzhen Intermediate People’s Court in May, up 85% from a year earlier. So-called individual businesses (in many cases freelancers) making up 3.3 million of the province’s commercial entities, and accounted for a large share of those filing.

“After the epidemic, it’s unclear just how many business owners will be forced on to the country’s defaulter list if they fail,” said Yin Yanrong, a partner in the Guangdong Baocheng law firm.

On the other hand, creditors who owe more than 500,000 yuan ($70,228.66) will also be able to petition for liquidation of debtor companies.

China has built its explosive growth on a mountain of bad debt. What’s going to happen when investors in the country are forced to take losses on “safe” securities for the first time?

Blain: The Tragedy Of HSBC

Authored by Bill Blain via MorningPorridge.com,

“A waiter, again unbidden, brought the chessboard and the current issue of The Times, with the page turned down at the chess problem.”

While America burns, the dollar tumbles, stock markets soar, Germany announces a massive bailout programme which dwarfs the pennies Italy desperately needs, the ECB gets ready for another money dump, and UK politicians grumble about queues… life goes on…

There is something deeply tragic about yesterday’s announcements from HSBC and Standard Chartered supporting the imposition of China’s Security Law in Hong Kong. We can all act shocked and damn them for supping with the devil, but neither bank had any real choice but to make the unpalatable decision to support the unsupportable. Both know their futures depend too much on China’s patronage to survive without kow-towing.

Yesterday, they each wrote the first lines of the final few paragraphs of their own obituaries.

10-years ago I wrote in the Porridge why HSBC was my top bank stock. I said something along the lines of while other banks will remain vulnerable, HSBC had the franchise, strength and depth to survive and thrive. Its dividend policy was strong and would provide dull, boring, predictable returns for the long-term. The Long-term is so over.

Read the comments following any article about the two Hong Kong banks this morning and are they full of earnest virtue signalling from angry clients who say they will close their accounts. I will probably switch mine.. but only because now there is zero chance the service will get any better.

Timing is everything. I laughed out loud at a post on Linked-In from HSBC claiming leadership in ESG matters and Green funding. Really… this is not the time for HSBC to be bragging about its ethical credentials.

The sad reality is HSBC has become a patron of the Chestnut Tree Café – the bar where the purged characters from 1984 spend their last few months in isolation, irrelevancy and waiting for the axe to fall. HSBC and Standard Chartered’ future is window dressing the new Hong Kong. HSBC has become as yesterday as Deutsche Bank.

It could have been so different.

In the early 2000s HSBC’s tag line was The World’s Local Bank. The Hexagon Logo dominated airports and appeared everywhere. Its ambition was to generate one third of its profits from each of the main global markets; Asia, Europe and North America. By market capitalisation it was the largest bank on the planet. When it bought US sub-prime credit lender Household in 2002, it was a clear signal the bank was on the move with expansion plans everywhere.

I joined HSBC in 2002. It was a bit of a shock after 10 years at an aggressive but highly innovative US investment bank.