GOLD:$1699.10 UP $18.70 The quote is London spot price

Silver:$17.70 UP 36 CENTS//LONDON SPOT PRICE

Closing access prices: London spot

i)Gold : $1698.00 LONDON SPOT 4:30 pm

ii)SILVER: $17.76//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUG GOLD: $1705.50 CLOSE 1.30 PM// SPREAD SPOT (LONDON) VS/FUTURE JUNE: $+6.40

CLOSING SILVER FUTURE MONTH

JULY: 1:30 PM: $17.91//1:30 PM //SPREAD SPOT LONDON VS FUTURE JULY: 21 CENTS PER OZ//

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2800. usa per oz

and silver; $31.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

DO NOT PAY ANY ATTENTION TO WHAT THE CROOKS ARE DOING AT THE COMEX AND LONDON LBMA..PHYSICAL IS THE NAME OF THE GAME AND NOTHING ELSE

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 987/1321

EXCHANGE: COMEX

CONTRACT: JUNE 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,676.200000000 USD

INTENT DATE: 06/05/2020 DELIVERY DATE: 06/09/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 24

072 H GOLDMAN 133

099 H DB AG 212

104 C MIZUHO 7 2

118 H MACQUARIE FUT 29

132 C SG AMERICAS 3

167 C MAREX 1

190 H BMO CAPITAL 14

323 H HSBC 3

355 C CREDIT SUISSE 15

357 C WEDBUSH 29

624 C BOFA SECURITIES 12

657 C MORGAN STANLEY 45

657 H MORGAN STANLEY 714

661 C JP MORGAN 894

661 H JP MORGAN 93

685 C RJ OBRIEN 2

686 C INTL FCSTONE 311

690 C ABN AMRO 26 25

732 C RBC CAP MARKETS 2

737 C ADVANTAGE 6 7

800 C MAREX SPEC 6 6

905 C ADM 10 11

____________________________________________________________________________________________

TOTAL: 1,321 1,321

MONTH TO DATE: 47,123

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT: 1321 NOTICE(S) FOR 132,100 OZ (4.108 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 47,123 NOTICES FOR 4,712,300 OZ (146.57 TONNES)

SILVER

FOR JUNE

6 NOTICE(S) FILED TODAY FOR 30,000 OZ/

total number of notices filed so far this month: 404 for 2,0200,000 oz

BITCOIN MORNING QUOTE $9728 DOWN $16

BITCOIN AFTERNOON QUOTE.: $9702 DOWN 12

GLD AND SLV INVENTORIES:

WITH GOLD UP $18.70 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

A HUGE PAPER WITHDRAWAL OF: 4.10 TONNES FROM THE GLD

GLD: 1,128.11 TONNES OF GOLD//

WITH SILVER UP 36 CENTS TODAY: AND WITH NO SILVER AROUND

TWO CONSIDERABLE PAPER WITHDRAWALS: 1) 932,000 OZ

ii ) 1.491 million oz

RESTING SLV INVENTORY TONIGHT:

SLV: 471.731 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A STRONG SIZED 1588 CONTRACTS FROM 170,820 DOWN TO 169,232 AND FURTHER FROM OUR NEW RECORD OF 244,710, (FEB 25/2020. THE STRONG SIZED LOSS IN OI OCCURRED WITH OUR VERY HUGE 46 CENT LOSS IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE LOSS IN COMEX OI IS DUE TO STRONG BANKER SHORT COVERING PLUS A GOOD EXCHANGE FOR PHYSICAL ISSUANCE, SOME LONG LIQUIDATION, ACCOMPANYING A GOOD INCREASE IN SILVER OZ STANDING AT THE COMEX FOR JUNE. WE HAD A NET LOSS IN OUR TWO EXCHANGES OF 847 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUMONGOUS AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: MAY: 0 AND JULY: 727 AND SEPT 14 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 741 CONTRACTS. WITH THE TRANSFER OF 741 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 741 EFP CONTRACTS TRANSLATES INTO 3.705 MILLION OZ ACCOMPANYING:

1.THE 46 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.085 MILLION OF INITIALLY STANDING FOR JUNE

FRIDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL 46 CENTS).. AND,OUR OFFICIAL SECTOR/BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO FLEECE SOME SILVER LONGS FROM THEIR POSITIONS. THE CONSIDERABLE LOSS AT THE COMEX WAS ACCOMPANIED BY : i) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A GOOD INCREASE IN SILVER OZ STANDING FOR JUNE,3) CONSIDERABLE BANKER SHORT COVERING AND 4) SOME LONG LIQUIDATION AS WE DID HAVE A NET LOSS OF 847CONTRACTS OR 4.235 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

SPREADING OPERATIONS

OUR SPREADING OPERATION HAS NOW SWITCHED INTO SILVER…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN SILVER AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JULY.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF JUNE. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

JUNE

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF JUNE:

3507 CONTRACTS (FOR 7 TRADING DAY(S) TOTAL 3507 CONTRACTS) OR 17.535 MILLION OZ: (AVERAGE PER DAY: 501 CONTRACTS OR 2.505 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 17.535 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 1.609% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,083.47 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP SO FAR 17.535 MILLION OZ.

EXCHANGE FOR PHYSICAL ISSUANCE FOR THE PAST 60 DAYS IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD AN EXTREMELY LARGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1588, WITH OUR HUGE 46 CENT LOSS IN SILVER PRICING AT THE COMEX ///FRIDAY… THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 741 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE LOST A STRONG SIZED OI CONTRACTS ON THE TWO EXCHANGES: 847 CONTRACTS (WITH OUR 46 CENT LOSS IN PRICE)

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 741 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A LARGE SIZED DECREASE OF 1,588 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED DESPITE A HUGE 46 CENT LOSS IN PRICE OF SILVER/AND A CLOSING PRICE OF $17.34 // FRIDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.856 BILLION OZ TO BE EXACT or 122% of annual global silver production (ex Russia & ex China).

FOR THE NEW JUNE DELIVERY MONTH/ THEY FILED AT THE COMEX: 6 NOTICE(S) FOR 30,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.085 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A UNEXPECTED SMALL SIZED 213 CONTRACTS TO 471,145 AND SLIGHTLY FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE TINY SIZED LOSS OF COMEX OI OCCURRED DESPITE OUR STRONG LOSS IN PRICE OF $40.40 /// COMEX GOLD TRADING// FRIDAY// WE HAD STRONG BANKER SHORT COVERING,ANOTHER HUMONGOUS SIZED INCREASE IN GOLD OZ STANDING AT THE COMEX, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A GOOD EX. FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR STRONG LOSS IN PRICE OF $40.40 .

WE HAD A VOLUME OF 5 4 -GC CONTRACTS//OPEN INTEREST 8

WE GAINED A GOOD SIZED 4640 CONTRACTS (14.43 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4853 CONTRACTS:

CONTRACT JUNE 0.; AUG 4835 AND ALL OTHER MONTHS ZERO//TOTAL: 4835. The NEW COMEX OI for the gold complex rests at 471,145. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4640 CONTRACTS: 213 CONTRACTS INCREASED AT THE COMEX AND 4853 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 4640 CONTRACTS OR 14.43 TONNES. FRIDAY, WE HAD A HUGE LOSS OF $40.40 IN GOLD TRADING……

AND WITH THAT LOSS IN PRICE, WE HAD A STRONG SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 14.43 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT FELL $40.40).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS UNSUCCESSFUL (SEE BELOW).

4 GC VOLUME: 5 // open interest 8

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4853) ACCOMPANYING THE TINY SIZED LOSS IN COMEX OI (213 OI): TOTAL GAIN IN THE TWO EXCHANGES: 5008 CONTRACTS. WE NO DOUBT HAD 1 )CONSIDERABLE BANKER SHORT COVERING, 2.)ANOTHER HUMONGOUS INCREASE IN GOLD OUNCES STANDING AT THE GOLD COMEX FOR THE FRONT JUNE MONTH, 3) ZERO LONG LIQUIDATION; 4) TINY COMEX OI GAIN.. AND …ALL OF THIS WAS COUPLED WITH OUR STRONG LOSS IN GOLD PRICE TRADING//FRIDAY//$40.40.

SEEMS THAT NOBODY LEFT THE GOLD ARENA DESPITE THE VICIOUS ATTACK!! NO DOUBT THAT THE NEWBIE TRANSFERS TO LONDON WILL EXERCISE FOR PHYSICAL METAL.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

JUNE

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY(S) IN TONNES: 60.54 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 60.54/3550 x 100% TONNES =1.69% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 2875.57 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 60.54 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 1588 CONTRACTS FROM 170,820 DOWN TO 169,232 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE STRONG LOSS IN OI SILVER COMEX WAS DUE TO; 1) CONSIDERABLE BANKER SHORT COVERING , 2) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A GOOD INCREASE IN SILVER OZ STANDING AT THE COMEX FOR JUNE AND 4) SOME LONG LIQUIDATION

EFP ISSUANCE 741 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY: 727 CONTRACTS AND SEPT: 14 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 741 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1566 CONTRACTSTO THE 741 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD LOSS OF 847 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 4.235 MILLION OZ!!! OCCURRED WITH THE 46 CENT LOSS IN PRICE///

RESULT: A STRONG SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 46 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// FRIDAY. WE ALSO HAD A GOOD SIZED 741 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED DOWN 6.97 POINTS OR 0.24% //Hang Sang CLOSED UP 6.36 POINTS OR 0.03% /The Nikkei closed UP 314.97 POINTS OR 1.38%//Australia’s all ordinaires CLOSED UP .07%

/Chinese yuan (ONSHORE) closed UP at 7.0744 /Oil UP TO 39.15 dollars per barrel for WTI and 42.27 for Brent. Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN CLOSED UP // LAST AT 7.0774 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.0688 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC SPREAD : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

i)we had 2 deposits into the customer account

into JPMorgan: 0

ii)into Scotia 459,958.780 oz

III) Into CNT: 600,666.880 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.819 million oz of total silver inventory or 51.22% of all official comex silver. (160.819 million/314.220 million

total customer deposits today: 1,060,625.660 oz

we had 1 withdrawals:

i) Out of Scotia: 167,080.500 oz

total withdrawals; 167,080.500 oz

We had 0 adjustments

total dealer silver: 85.401 million

total dealer + customer silver: 314.596 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The total number of notices filed today for the JUNE 2020. contract month is represented by 6 contract(s) FOR 30,000 oz

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 404 x 5,000 oz = 2,020,,000 oz to which we add the difference between the open interest for the front month of JUNE.(19) and the number of notices served upon today 6 x (5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JUNE/2019 contract month: 404 (notices served so far) x 5000 oz + OI for front month of JUNE (19)- number of notices served upon today 6) x 5000 oz of silver standing for the JUNE contract month.equals 2,085,000 oz.

We GAINED 8 contracts or an additional 40,000 oz will stand for delivery as they refused to morphed into London based forwards as well as negating a fiat bonus

TODAY’S ESTIMATED SILVER VOLUME: 34,155 CONTRACTS // volume low/

FOR YESTERDAY: 112,239..,CONFIRMED VOLUME//volume high/with raid

YESTERDAY’S CONFIRMED VOLUME OF 112,239 CONTRACTS EQUATES to 561 million OZ 80.17% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO- 1.09% ((JUNE 8/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.58% to NAV: (JUNE 8/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 1.09%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 16.38 TRADING 16.30///NEGATIVE 0.47

END

And now the Gold inventory at the GLD/

JUNE 8//WITH GOLD UP $18.70 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 4.10 TONNES AT THE GLD//INVENTORY RESTS AT 1128.11 TONNES

JUNE 5//WITH GOLD DOWN $40.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A PAPER WITHDRAWAL OF 1.16 TONNES OUT OF THE GLD//INVENTORY RESTS AT 1132.21 TONNES

JUNE 4//WITH GOLD UP $20.60: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD…A DEPOSIT OF 4.09 TONNES INTO THE GLD//INVENTORY RESTS AT 1133.37 TONNES

JUNE 3//WITH GOLD DOWN $26.15//A SMALL CHANGE IN GOLD INVENTORY//A DEPOSIT OF 0.78 TONNES OF GLD INTO THE GLD//INVENTORY RESTS AT 1129.28 TONNES

JUNE 2//WITH GOLD DOWN $11.20 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1128.40 TONNES

JUNE 1//WITH GOLD UP $1.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES OF GOLD//GLD INVENTORY RESTS TONIGHT AT 1123.14 TONNES

MAY 29/WITH GOLD UP $19.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///GLD INVENTORY RESTS THIS WEEKEND AT 1119.05 TONNES

MAY 28//WITH GOLD UP $4.00 TODAY/NO CHANGES IN GOLD INVENTORY TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

MAY 27/WITH GOLD UP $.10 TODAY: A STRONG 2.34 TONNES OF GOLD ADDED TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

MAY 26//WITH GOLD DOWN $23.05//NO CHANGES IN GOLD INVENTORY://RESTS TONIGHT AT 1116.71 TONNES

MAY 22//WITH GOLD UP $13.05//A BIG CHANGE IN GOLD INVENTORY:: A PAPER ADDITION OF 3.93 TONNES//INVENTORY RESTS THIS WEEKEND AT: 1116.71 TONNES

MAY 21//WITH GOLD DOWN $26.70//NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1112.32 TONNES

MAY 20/WITH GOLD UP $7.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 1.46 TONNES FROM THE GLD////INVENTORY RESTS TONIGHT AT 1112.32 TONNES

MAY 19//WITH GOLD UP $10.60//NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1113.78 TONNES

MAY 18/WITH GOLD DOWN $15.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A PAPER DEPOSIT OF 9.06 TONNES./INVENTORY RESTS AT 1113.78 TONNES

MAY 15.WITH GOLD UP $16.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 12.58 TONNES/ INVENTORY RESTS AT 1104.72 TONNES

MAY 14//WITH GOLD UP $19.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1092.14 TONNES

MAY 13//WITH GOLD UP $9.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 11.07 TONNES/INVENTORY RESTS AT 1092.14 TONNES

MAY 12//WITH GOLD UP $6.60 TODAY; A SMALL CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 1081.07 TONNES

MAY 11/WITH GOLD DOWN $12.65 TODAY: NO CHANGES IN GOLD INVENTORY: //INVENTORY RESTS AT 1081.65 TONES..

MAY 8/WITH GOLD DOWN $7.00 TODAY; A BIG CHANGE IN GOLD INVENTORY: A PAPER ADDITION OF 5.85 TONNES/INVENTORY RESTS AT 1081.65 TONNES

MAY 7/WITH GOLD UP $29.65 TODAY : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER ADDITION OF .41 TONNES/INVENTORY RESTS AT 1075.80 TONNES

MAY 6//WITH GOLD DOWN $17.00 TODAY/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER ADDITION OF 3.68 TONNES/INVENTORY RESTS AT 1075.39 TONES

MAY 5/WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER ADDITION OF 3.81 TONNES//INVENTORY RESTS AT 1071.71 TONNES

MAY 4//WITH GOLD UP $12.00 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE PAPER DEPOSIT OF 11.4 TONNES INTO THE GLD////GOLD INVENTORY RESTS AT 1067.90 TONNES

MAY 1/WITH GOLD UP $8.45 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1056.50 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

JUNE 8/ GLD INVENTORY 1128.11 tonnes*

LAST; 836 TRADING DAYS: +183.19 NET TONNES HAVE BEEN REMOVED FROM THE GLD

LAST 738 TRADING DAYS://+358.39 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JUNE 8/WITH SILVER UP 36 CENTS TODAY: TWO HUGE WITHDRAWALS OF 932,000 MILLION OZ AND 1.491 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 470.240 MILLION OZ//

JUNE 5/WITH SILVER DOWN 46 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 648,000 OZ FROM THE SLV////INVENTORY RESTS AT 472.663 MILLION OZ

JUNE 4//WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV.//INVENTORY RESTS AT 473.315 MILLION OZ//

JUNE 3//WITH SILVER DOWN 23 CENTS TODAY//NO CHANGES IN SILVER INVENTORY AT THE SLV//

INVENTORY RESTS AT 473.315 MILLION OZ//

JUNE 2//WITH SILVER DOWN 31 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUMONGOUS 6.686 MILLION OZ ADDED TO THE SLV////INVENTORY RESTS TONIGHT AT 473.315 MILLION OZ//

JUNE 1//WITH SILVER UP 38 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.56 MILLION OZ INTO THE SLV////INVENTORY RESTS TONIGHT AT 466.629 MILLION OZ//

MAY 29//WITH SILVER UP 52 CENTS TODAY: A MASSIVE DEPOSIT OF 2.796 MILLION OZ INTO THE SLV//INVENTORY RESTS THIS WEEKEND AT 463.273 MILLION OZ//

MAY 28//WITH SILVER UP 9 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.660 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 460.477 MILLION OZ//

MAY 27/WITH SILVER UP 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 455.817 MILLION OZ//

MAY 26//WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/// INVENTORY RESTS AT 455.817 MILLION OZ//

MAY 22/WITH SILVER UP 22 CENTS TODAY/ A HUGE PAPER WITHDRAWAL OF 1.864 MILLION OZ//INVENTORY RESTS AT 455.817 MILLION OZ/

LAST 5 DAYS: SILVER UP 60 CENTS: INVENTORY UP A WHOOPING 23.767 MILLION OZ///

MAY 21/WITH SILVER DOWN 50 CENTS TODAY: A HUGE PAPER DEPOSIT OF 7.923 MILLION OZ///INVENTORY RESTS AT 457.681 MILLION OZ//

MAY 20//WITH SILVER UP ANOTHER 11 CENTS TODAY: A HUGE CHANGE IN SLV INVENTORY: A HUGE PAPER DEPOSIT OF 9.601 MILLION OZ INTO THE SLV// //INVENTORY RESTS AT 449.758 MILLION OZ

MAY 19/WITH SILVER UP ANOTHER 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 440.157 MILLION OZ//

MAY 18/WITH SILVER UP ANOTHER 48 CENTS TODAY: TWO BIG CHANGES IN SILVER INVENTORY AT THE SLV I.E. 2 PAPER DEPOSIT OF ( I) 8.39 MILLION OZ AND THEN ( 2) 8.109 MILLION OZ//INVENTORY RESTS AT 432.048 MILLION OZ// (TOTAL DEPOSITS 16.500 MILLION OZ///)

MAY 15/WITH SILVER UP 81 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV: /INVENTORY RESTS AT 423.65 MILLION OZ.

MAY 14//WITH SILVER UP 33 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV.//INVENTORY RESTS AT 423.65 MILLION OZ

MAY 13/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.79 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 423.65 MILLION OZ//

MAY 12/WITH SILVER UP 5 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.076 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 420.861 MILLION OZ//

MAY 11.WITH SILVER DOWN 5 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 417.785 MILLION OZ//

MAY 8/WITH SILVER UP 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTER DEPOSIT OF 4.661 MILLION OZ OF SILVER INTO THE SLV..///INVENTORY RESTS AT 417.785 MILLION OZ//

MAY 7/WITH SILVER UP 45 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 5/WITH SILVER UP 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ///

MAY 4//WITH SILVER DOWN 5 CENTS TODAY:2 HUGE PAPER CHANGES IN SILVER INVENTORY AT THE SLV.i).A LARGE 1.399 MILLION OZ OF PAPER SILVER REMOVED FROM THE SLV//..//INVENTORY RESTS AT 411.427 MILLION OZ and ii) A LARGE 1.647 MILLION OZ OF PAPER SILVER ADDED TO THE SLV// INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 1/WITH SILVER FLAT IN PRICE: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 412.826 MILLION OZ///

JUNE 8.2020:

SLV INVENTORY RESTS TONIGHT AT

470.240 MILLION OZ.

END

LIBOR SCHEDULE AND GOFO RATES// GOLD LEASE RATES

YOUR DATA…..

6 Month MM GOFO 2.36/ and libor 6 month duration 0.48

Indicative gold forward offer rate for a 6 month duration/calculation:

GOLD LENDING RATE: -1.88%

NEGATIVE GOLD LEASING RATES INCREASING BY A HUGE AMOUNT//GOLD SCARCITY AND CENTRAL BANKS CALLING IN ALL OF THEIR GOLD LEASES

XXXXXXXX

12 Month MM GOFO

+ 2.03%

LIBOR FOR 12 MONTH DURATION: 0.63

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -1.40%

NEGATIVE GOLD LEASING RATES INCREASING BY A HUGE AMOUNT//GOLD SCARCITY AND CENTRAL BANKS CALLING IN ALL OF THEIR GOLD LEASES

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

Alasdair Macleod writes that bankers are having trouble closing their short positions due to longs demanding delivery of 140 tonnes last week.

He claims that the Federal reserve is about to sacrifice the dollar in an attempt to preserve asset values

(Kingworldnews/Macleod/GATA)

Alasdair Macleod at KWN: Bullion banks still have a problem despite gold and silver pullback

Submitted by cpowell on Sat, 2020-06-06 02:48. Section: Daily Dispatches

10:50p ET Friday, June 5, 2020

Dear Friend of GATA and Gold:

Bullion banks, GoldMoney research director Alasdair Macleod writes at King World News tonight, are desperately trying to close their short gold futures positions in New York because metal just isn’t available. But, Macleod adds, they are failing as longs have demanded delivery of more than 140 tonnes in the last week.

The Federal Reserve, Macleod concludes, is about to sacrifice the dollar in an attempt to preserve asset values.

Macleod’s analysis is headlined “Bullion Banks Still Have a Problem Despite Gold and Silver Pullback” and it’s posted at KWN here:

https://kingworldnews.com/bullion-banks-still-have-a-problem-despite-gol…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Jim Rickards discusses the value of gold

(Jim Rickards/GATA)

Jim Rickards: Why gold, even though it’s taboo?

Submitted by cpowell on Sat, 2020-06-06 15:31. Section: Daily Dispatches

By James G. Rickards

The Daily Reckoning, Baltimore, Maryland

Tuesday, June 2, 2020

Why gold?

That’s a question I’m asked frequently. It’s usually followed by a comment along the lines of “I don’t get it. It’s just a shiny rock. People dig it out of the ground and then put it back in the ground. What’s the point?”

I usually begin my reply by saying, “It’s not a rock. It’s a metal,” and then go from there.

I have a lot of sympathy in these conversations. That people don’t know much about gold today is not exactly their fault. The economics establishment of policymakers, academics, and central bankers have closed ranks around the idea that gold is a taboo subject.

You can teach it in mining colleges but don’t dare teach it in economics departments. If you have a kind word for gold in a monetary context, you are immediately labeled a “gold nut,” “gold bug,” “Neanderthal,” or something worse. You are excluded from the conversation. Case closed. …

… For the remainder of the commentary:

end

James Turk gives his reasoning for our continual attacks by our banker friends

(Kingworldnews/Turk GATA

James Turk at KWN: What just happened in the gold market is no accident

Submitted by cpowell on Mon, 2020-06-08 15:44. Section: Daily Dispatches

11:45a ET Monday, June 8, 2020

Dear Friend of GATA and Gold:

GoldMoney founder James Turk notes today in commentary at King World News that the price of gold was pushed down to $1,680 just prior to the April and June meetings of the Federal Reserve’s Open Market Committee, and he thinks this is no coincidence.

» So it looks to me that taking the gold price down a second time to $1,680 was done on purpose. It gives a green light to the Federal Open Market Committee that they can keep printing.”Turk also makes several suggestions to gold investors for defeating this market rigging.

His remarks are headlined “What Just Happened in the Gold Market is No Accident” and it’s posted at KWN here:

https://kingworldnews.com/james-turk-what-just-happened-in-the-gold-mark…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

iii) Other physical stories:

Schiff: A Soaring Stock Market Is Not A Sell Signal For Gold

US stock markets continued their inexplicable rally despite the economic destruction wrought by the coronavirus-induced shutdown. The S&P500 is only down about 3.5% on the year and the NASDAQ is actually up. As a result, a lot of investors seem to be getting out of safe havens, including gold. But in his podcast, Peter Schiff explains why selling gold is a mistake if you understand what’s really going on. In a nutshell, stocks are rising because the Fed is printing money. And no matter what the mainstream says, money printing matters.

Think about what has happened over the last year and ask yourself: does this make any sense?

Looking back at the end of 2019, people were optimistic. The stock market was booming. There was no sign of a recession in sight. But since then, the US economy has plunged into the worst recession since the Great Depression sparked by a global pandemic. Over 40 million people have filed for unemployment. The Federal Reserve is printing dollars at breakneck speed. The federal government has run up trillions of dollars in new debt through borrowing for stimulus and bailouts. And we’ve seen major civil unrest with looting and destruction in many major American cities.

If you were told all of this was going to happen back in January, would have believed the S&P 500 would barely be down and that the NASDAQ would be up some 8%?

There is only one explanation.

The only reason the market is rallying is because of the Fed. I mean, people can try to say, ‘Well no, the market is anticipating a recovery.’ This is a lot more than the anticipation of a recovery. This is the Fed driving the narrative, driving the market higher.”

There was a bit of data that came out Wednesday that injected some optimism about a recovery into the markets and helped boost stocks. The ADP private payroll report came out. The expectation was for another 8.6 million jobs lost, but the number came in at just below 2.7 million jobs.

Peter said that number doesn’t even look possible given that we’ve seen 2 to 3 million people file for unemployment every week. Nevertheless, as soon as the number came out, the market rallied and gold sold off. The sentiment seemed to be that the economy isn’t as bad as we thought.

The economy is as bad as they thought. In fact, it’s probably worse. But when the number came out, the market rallied on it because of, I think, the momentum that has been created by the Fed.”

Peter said stocks are way overpriced even if the economy was much better than people thought.

Remember, the US stock market was overpriced at the end of 2019, before any of this bad stuff had happened. And now we have all this bad stuff, which is much worse than anybody could have possibly envisioned, and the market is barely down in the case of the S&P500. And in the case of the NASDAQ, the market is actually higher. Even though it was already expensive and priced for perfection, we got the antithesis of perfection, yet the market went up anyway.”

Meanwhile, the dollar is getting pounded and the bond market is also feeling pressure. The yield on the 30-year appears to be pushing toward 2%. That is still low, but keep in mind, not too long ago that yield was below 1%.

Incidentally, this is a problem for the Federal Reserve. The central bank bought a lot of Treasuries when the yield was under 1%. One of the reasons the market went up was because of all the money the central bank printed to buy up those bonds. Now, as rates rise, the Fed is losing money because it has taken on a lot of interest rate risk. As interest rates rise, bond prices fall. That means the Fed’s balance sheet is losing money.

Ultimately, we’re seeing the market move away from safe havens and that includes gold and silver. This is due to unwarranted optimism about an economic rebound. But Peter said he thinks it’s just the rise in the market itself that is creating the optimism.

People are thinking that the market is rising because people are optimistic about the recovery. I think people are optimistic about the recovery because the market is rising. And the market is not rising because of the recovery. The market is rising because of the Fed – because of all the money the Fed is printing. And even though a lot of people think printing money doesn’t matter, printing money matters a lot. And people are about to find out the hard way just how much it really matters.”

This is why investors should buy gold. It’s not primarily a hedge for your stock portfolio. It’s to hedge for your currency.

Whether they live in the US and have dollars, or they live in Europe and have euros, or they live in Japan and they have Japanese yen, central banks are creating tremendous inflation. And central banks have told everybody that we are intentionally destroying the value of our money. That is our goal. We want prices to go up more. We want more inflation. We want the dollars, or the euros, or the yen that you’re keeping in the bank or in your mattress somewhere – we want them to lose value. The longer you hold on to them, the more value they are going to lose. This is on purpose. This is by design. So, once the central banks have told you that’s the plan, you would be a fool to cooperate.”

Gold is a hedge against central banks creating inflation. It’s a hedge against debasing currency. Instead of selling gold because the stock market is going up, investors need to understand why the stock market is rising.

It’s rising because the Fed is printing all this money because the Fed is creating inflation and debasing the value of currency. That is going to drive the value of gold. Gold becomes more valuable because of what the government is doing to prop up the stock market and prop up the economy. So, a strong stock market is not a sell signal for gold.”

An excellent history on how silver was priced relative to gold

(Alasdair Macleod)

Orphaned Silver Is Finding Its Parent

Authored by Alasdair Macleod via GoldMoney.com,

This article examines the prospects for silver, which has been overlooked in favour of gold. Due to the economic and monetary consequences of the coronavirus lockdowns and the earlier turning of the credit cycle, there is an increasing likelihood of a severe and sustained downturn that will require far more monetary expansion to deal with, favouring the prospects of both gold and silver returning to their former monetary roles.

To understand the consequences for silver, this article draws on history, principally of silver standards in America and Britain, in order to appreciate the issues involved and the prospects for silver to regain its former monetary role.

Introduction

So far this year, the story in precious metals markets has been all about gold. Speculators have this idea that gold is a hedge against inflation. They don’t question it, don’t theorise; they just assume. And when every central bank issuing a respectable currency says they will print like billy-ho, the punters buy gold derivatives.

These normally tameable punters are now breaking the establishment’s control system. On Comex, the bullion establishment does not regard gold and silver as money, just an idea to suck in the punters. The punters are no longer the suckers. With their newly promised infinite monetary expansion, central banks are confirming their inflationary fears.

What makes it worse for bullion bank trading desks is that the banking system is now teetering on the edge of the greatest contraction of bank credit experienced at least since the 1930s, and banks are determined to rein in their balance sheets. We normally think of bank credit contraction crashing the real economy: this time, banks are reining in market making activities as well, and that includes out-of-control gold and silver trading desks, foreign exchange trading, fx swaps and other derivatives —anything that is not a matched arbitrage or an agency deal on behalf of a genuine customer.

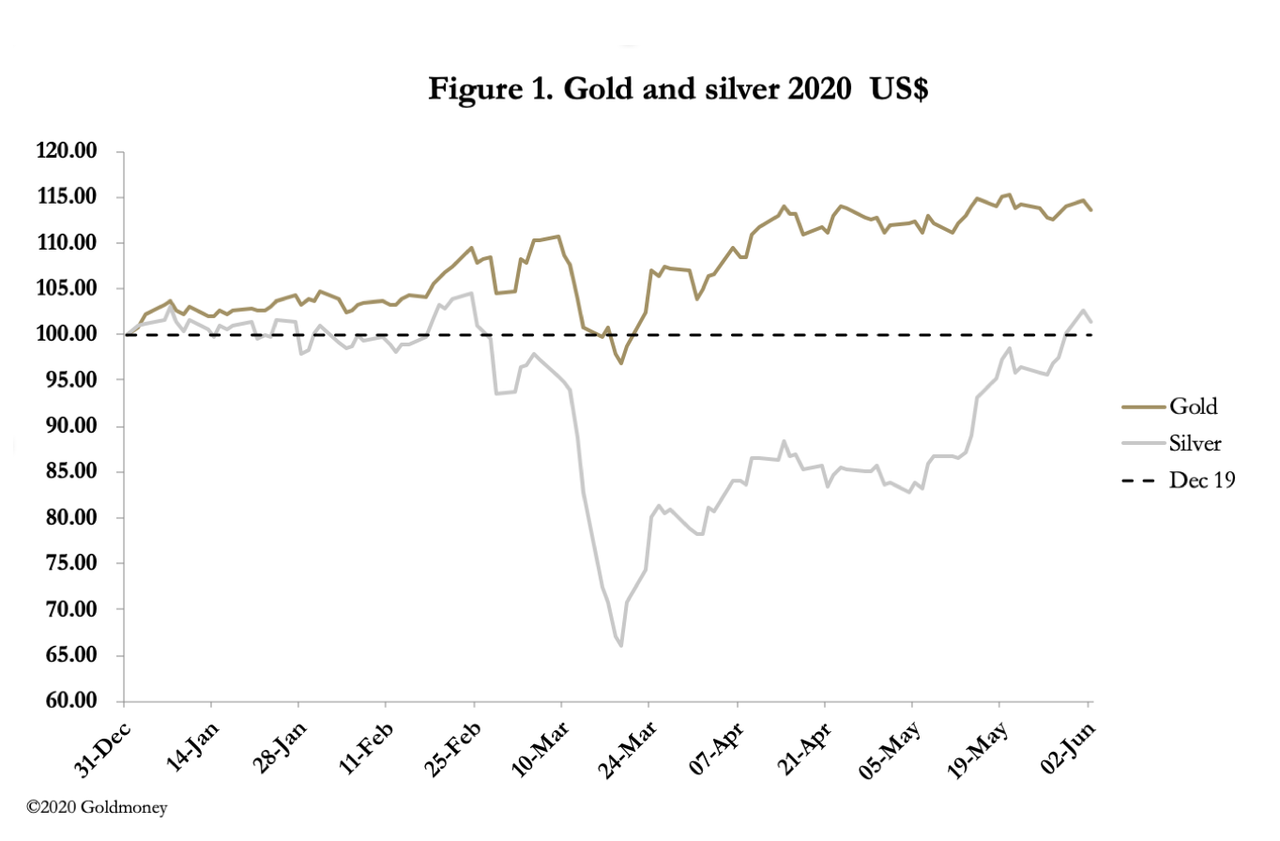

Initially, the focus on gold left silver vulnerable. Figure 1 shows how the two metals have performed in dollar terms so far this year, indexed to 31 December 2019. When the bullion banking establishment tried one of its periodic smashes in mid-February, it reduced Comex gold futures’ open interest from just under 800,000 contracts to about 480,000. The price of gold bounced back strongly to be up 14% on the year and the bullion banks are still horribly net short. But silver crashed, losing 34% and has only just recovered to be level on the year so far.

For the punters, in a proper gold bull market silver is seen as just a leveraged bet on gold. They are less interested in the dynamics that cause a relationship to exist than they are on the momentum behind the price. For now, active traders are looking for entry points in both metals to build or add to their positions in a bullish but overbought market.

This is just short-term stuff, and much has been written on it about gold. We are generally unaware today that silver has been money for ordinary people more so than gold and in that sense still has the greater claim as a circulating medium. It is therefore time to devote our attention to silver.

A brief history of monetary silver

Silver has a similar history to gold of being money. Following the ending of barter, communities worldwide adopted durable metals – gold, silver or copper, depending on local availability — as the principal medium of exchange. And until the 1960s this heritage, with respect to copper and silver, was still reflected in the coinage used in most nations. The British currency is still known as sterling because since the reign of Henry II (1154–1189) money was silver coinage of sterling alloy, comprised of 92.5% silver, the balance being mainly copper.

Silver was the sole monetary standard, sometimes with gold on a bimetallic standard, for most regions from medieval times until the nineteenth century. Sir Isaac Newton reset the silver standard against gold in 1717, and it was because the British government overpriced gold and failed to adjust to the consequences of changing mine supplies, principally the subsequent expansion of gold supply from Brazil, that British commerce moved towards a gold standard during the eighteenth century.

We look in greater detail at these events later in this article.

As international trade developed, gold for trading nations assumed greater significance, leading eventually to the adoption of the British sovereign coin as the gold standard in the early nineteenth century.

In colonial America, silver was the principal circulating currency in common with that of Britain at the time, but following Newton’s introduction of a silver standard for the pricing of gold, similar practical relationships between the two metals existed for trade in nearly all Britain’s colonies; in America’s case at least until independence was formally gained by the Treaty of Paris in 1783.

When Alexander Hamilton was Treasury Secretary, the US introduced a bimetallic standard with the first coinage act in 1792 when the dollar was fixed at 371.25 grains of pure silver, minted with alloy into coins of 416 grains. Gold coins were also authorised in denominations of $10 (eagles) and $2.50 (quarter eagles). The ratio of silver to gold was set at fifteen to one. All these coins were declared legal tender, along with some foreign coins, notably the Spanish milled silver dollar, which had 373 grains of pure silver making them a reasonable approximation for the US silver dollar.

However, not long after Hamilton’s coinage act was passed, the international market rate for the gold/silver ratio rose to 15.5:1, which led to gold being drained from domestic circulation, leaving silver as the common coinage. Effectively, the dollar was on a silver standard until 1834, when Congress approved a change in the ratio to 16:1 by reducing the gold in the eagle from 246.5 to 232 grains, or 258 grains at about nine-tenths fine. An additional adjustment to 232.2 grains was made in 1834. After a few years, gold coins then dominated in circulation over silver, the circulation of which declined as it became more valuable relative to gold. Gold discoveries in California and Australia then increased the quantity of gold mined relative to silver, making silver even more valuable relative to gold coinage thereby driving it almost totally out of circulation. This was remedied by an act of 1853 authorising subsidiary silver coins of less than $1 to be debased with less silver than called for by the official mint ratio and less than indicated by the world market price.

Under financial pressure from the civil war, in 1862 the government issued notes that were not convertible either on demand or at a specific future date. These greenbacks were legal tender for everything but customs duties, which still had to be paid in gold or silver. The government had abandoned the metallic standards. Greenbacks were issued in large quantities and the United States experienced a substantial inflation.

After the war was over Congress determined to return to the metallic standard at the same parity that existed before the war. It was accomplished by slowly removing greenbacks from circulation. The bimetallic standard, measuring the dollar primarily in silver, was finally replaced with a gold standard in 1879, reaffirmed in 1900 when silver was officially relegated to small denomination money.

In Europe, most countries on a silver standard moved to gold after the Franco-Prussian war (1870–1), when Germany imposed substantial reparations from France which were paid in gold, and Germany was then able to migrate from a silver to a gold standard. Other European nations followed suit.

More recently, silver circulated as money in Arab lands in the form of Maria Theresa dollars, which had circulated widely in the Middle East and East Africa from the mid-nineteenth century and were still being used in Muscat and Oman in the 1970s.

These are just some examples of silver’s use as money in the past. It lives on in base metal coins today, made to look like silver. Now imagine a world where fiat currencies are discredited: gold or gold substitutes will almost certainly return as the money for larger transactions, and silver will equally certainly return as money for everyday transactions. Bimetallism might not return as official policy due to the frequent adjustments required, but history has shown that a relatively stable market rate between gold and silver is likely to ensue, and silver more than gold will ensure widespread distribution of circulating metallic money.

Supply and demand factors

Analysts are currently grappling with the effects of the coronavirus on supply and demand in their forecasts for the rest of this year. Silver mines have been affected by changes in grades and production shutdowns. According to the Silver Institute, in 2019 less than 30% of mine supply was from mines classified as primarily silver, the rest coming from lead/zinc, copper, gold mines and “others” in that order of importance. Miners of lead/zinc, copper and others made up about 56% of global silver mine supply, so that a decline in global economic activity automatically leads to a decline in silver output from base metal miners.

At the same time, falling industrial demand for silver throws a greater emphasis on investment to sustain demand overall. Last year, non-investment demand was 806 million ounces, while investment was estimated at 186 million, a relationship which in a deep recession will require a significant increase in investment demand to absorb the combination of mine, scrap and available above-ground stocks. Identifiable above-ground stocks are estimated at 1,651 million, a multiple of 1.67 times 2019 demand, and 8.9 times 2019 investment demand.

For 2020 and beyond, I am very bearish for the global economy for reasons stated elsewhere. If I am right, current estimates for mine supply, of which over half is dependent on base metal mines, will prove optimistic. But silver demand for non-investment usage is likely to decline even more, in which case investment demand will probably need to at least double if silver prices are to rise in real terms.

An interesting point is found in the comparison with gold, where above-ground stocks are many multiples of mine and scrap supply. Stock-to-flow comparisons have been popularised recently by the cryptocurrency community as a measure of future monetary stability, compared with that of infinitely expandable fiat currencies. A high stock-to-flow signals a low rate of inflationary supply. Silver has a very low stock to flow ratio due to the low level of above-ground stocks. But it is a mistake is to rely on this measure of monetary stability for a metallic money when the lack of physical liquidity should be the main consideration.

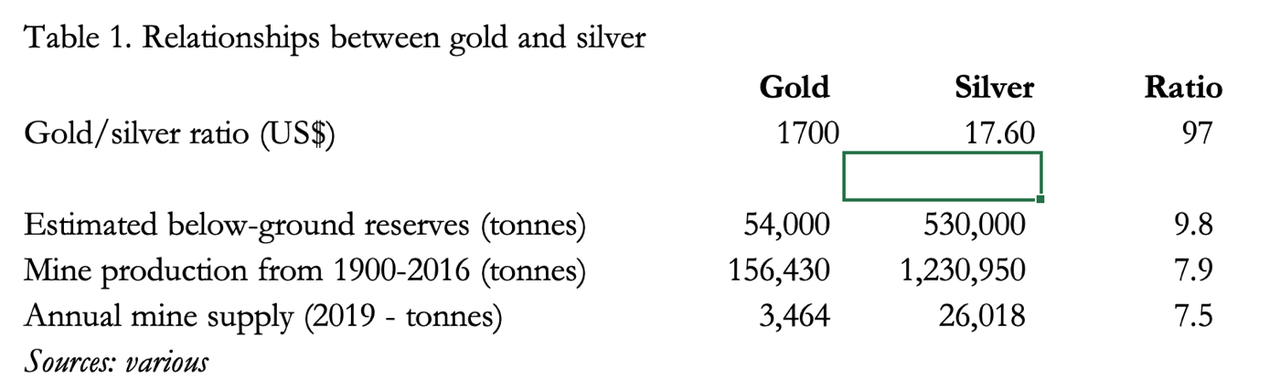

At current prices, silver’s above-ground stock is worth only $31bn, compared with gold’s at over $10 trillion. With this relationship of 323 times of gold to silver’s above-ground stock values and an annual mine supply ratio of only 8 times as many silver ounces to that of gold, it appears that if gold returns to its traditional monetary role, silver will turn out to be substantially undervalued. “If” is a little word for a very big assumption; but given the unprecedented and coordinated acceleration of monetary expansion currently proposed, an ending of the current fiat currency regime and a return to gold and silver as monies is becoming increasingly likely.

The relationship with gold in the numbers above suggest that a bimetallic standard today on mine supply considerations alone would be at almost half Isaac Newton’s 1717 exchange rate. Obviously, the issue is not so simple and will be settled by markets. But looking at some other facts suggest the gold/silver relationship is due for a radical rethink. Table 1 below lists some of the relevant ones.

The clear outlier is the gold/silver ratio.

How Newton decided the gold to silver ratio

It is natural to assume that the greatest scientific genius of the day derived a clever means to settle the gold/silver ratio when he was Master of the Royal Mint in 1717. Not so. He looked at existing exchange rates, how silver was disappearing from circulation in favour of gold at that time and set an initial rate to stop it. Furthermore, he recommended the rate be revised, most probably downwards, in the light of how trade developed. The point was that Britain operated a silver standard of money and both Newton and Parliament wished to retain it. It was, after all, the established money for day-to-day transactions.

To understand the monetary debates at the time, it will be helpful to commence with a guide to the composition of pre-decimal British money and coinage. There were 20 shillings to the pound (£), and twelve pence to the shilling. Silver coins were crowns (5 shillings) and half crowns, being 2 shillings and 6 pence, written 2s. 6d. There were silver coins of lesser value, but they are not relevant to this discussion.

Over a century before Newton, in 1601 a pound weight of old standard silver was coined into £3. 2s. 0d. in crowns and fractions thereof and remained the mint price of silver until 1816, a period lasting over two centuries. In 1670, a pound in weight of gold was coined into £44. 10s. 0d., represented by gold pieces of ten and twenty shillings. That was the equivalent of 14.35 times the value of silver. A monetary pound of twenty shillings was called a guinea, because when they were first struck in 1663 the gold came from the Guinea Coast of Africa, and it was set at 44 ½ to a pound of silver in weight because it was thought that it would be a stable rate of exchange.

There were some adjustments to the price of gold until it was finally fixed in 1717 at the new ratio of £46. 14s. 6d. to the silver standard of £3. 2s.0d. This moved the guinea from £1 in silver to £1. 1s. 0d, or 21 shillings. The crude ratio was now 15.07 to 1; but allowing for the differences in fineness between the slightly purer sterling silver (92.5%) compared with Crown gold coinage at 22 carats (91.67%), the actual ratio was 15.21 to 1.

This rate of exchange was introduced during Isaac Newton’s tenure as Master of the Royal Mint from 1699. In 1696 he had been previously appointed Warden of the Royal Mint to improve the state of silver coinage, and he organised the Great Recoinage in 1696–9.

In setting the price of gold, Newton found that gold, having been fixed as high as 22s. in 1699, had been too expensive compared with its silver value in Europe, particularly Holland, Germany, the Baltic States, France and Italy. Not only did he recommend setting the gold guinea at 21s, but he also recommended the rate be kept under review for a possible change to 20s 6d. That review did not take place.

Trade between Britain and the Continent was increasing, and whatever the rate, merchants had a preference for gold over silver because it was more practical for large payments when they were made in specie, which was normal practice at the time. While Britain remained on a silver standard, for commercial purposes it had increasingly moved to gold, silver being relatively expensive at the rate set and therefore progressively driven from active circulation relative to inflows of gold. The problem was that neither Newton nor Parliament accepted there was more than one currency: silver was the money and gold just a commodity whose price was to be set.

Because silver was valued about 5% more relative to gold in the European countries mentioned in the penultimate paragraph above, silver flowed abroad despite the ban on the export of coinage, and conversely gold flowed into Britain. Furthermore, gold mining output from Brazil began to have an impact on Britain’s monetary system following Newton’s 1717 conversion, due to diplomatic and commercial ties between Britain and Portugal. The bulk of this Brazilian gold, estimated by Fay at about 23 million ounces between 1720–1750, ended up being shipped to London, helping it to become the European monetary centre, taking that mantle from Amsterdam.

We can conclude that it was a combination of Newton overpricing gold, thereby driving silver into Europe and gold into London, and the discovery of Brazilian gold that turned Britain onto a commercial gold standard, even though officially it remained on a silver monetary standard for ninety-nine years after Newton’s fixing. And finally, in 1816, gold was declared the sole standard measure of value, and no tender of silver coin was legal for transactions valued at over forty shillings. By 1821, Britain was on a gold standard in law as well as fact.

From 1601–1816 we learn that silver’s role as money gradually evolved towards a subsidiary role to gold. Gold was the money of merchants and goldsmiths. The latter acting as custodians of gold evolved into banks, so high finance was almost exclusively gold. But silver was always there as money, be it for lesser transactions. And if today’s state-issued unbacked fiat currencies disappear, silver is bound to have a monetary role again alongside gold, because having a lower value and greater abundance of supply it can be more widely circulated.

The current market position for silver

Since the price of gold began to increase from August 2018, silver has lagged, its moneyness broadly ignored. Figure 2 shows how this has been reflected in the gold/silver ratio.

On 19 March a ratio of 125 was the highest ever seen, marking the most extreme undervaluation for silver. Since then, the ratio has fallen rapidly to its current level of 97. For it to fall further a continuing advance in the gold price may be required, because in current financial markets higher gold prices would be associated with economic conditions and monetary policies heading to a substantial, if not catastrophic deterioration in the purchasing power of fiat currencies.

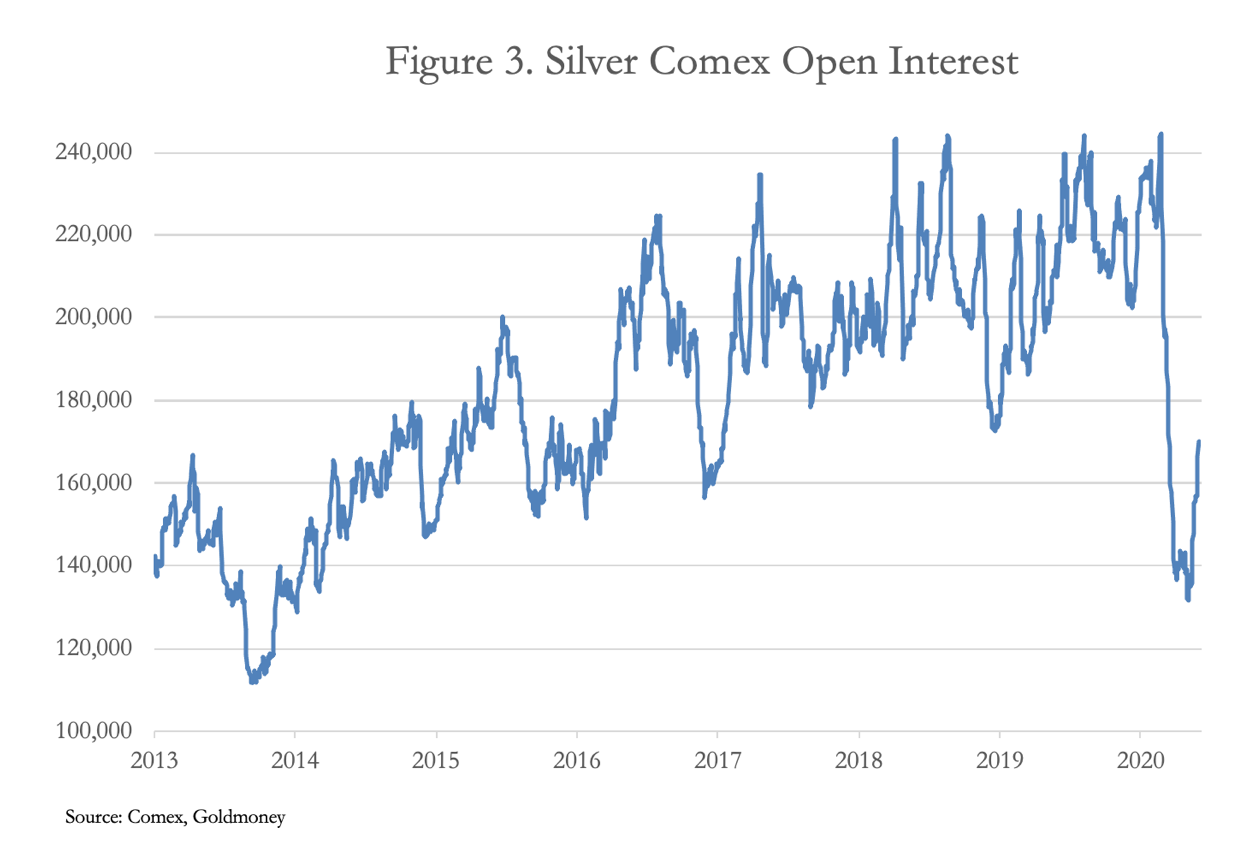

Additionally, traders manning bullion bank desks are generally finding their trading limits being reduced due to a combination of unfavourable trading conditions and pressure from their superiors limiting bank credit expansion generally. When the coronavirus paralysed China and was going to do the same to other nations, and the inflationary response became obvious, it led to a concerted bear raid by the bullion banks to balance their gold and silver positions on Comex before matters got even further beyond their control. The effect on silver’s open interest is shown in Figure 3.

Open interest was driven down to levels not seen for nearly seven years, after the silver price had fallen from a high of nearly $50 an ounce in 2011 to $18 in 2013, a price level only just now being reclaimed. From open interest’s height at 244,705 contracts on 24 February to its low at 181,830 on 4 May, contracts for 314,375,000 ounces of silver have been closed down, which compares with investment demand for the whole of last year estimated by the Silver Institute at 186,000,000 ounces. This contraction amounts to the synthetic equivalent of 20% of the Institute’s estimate of above-ground silver stocks.

Vaulted silver in LBMA vaults was 1,170 million ounces in February, the bulk of the 1.651 million recorded by the Silver Institute. The ownership of that silver is not declared but is likely to be a mixture of industrial users, investors (including ETFs) and bank dealers’ liquidity. In practice, banks keep liquidity at a minimum level consistent with the desk’s trading limits, and we know from developments in other derivative markets that trading limits are tending to contract.

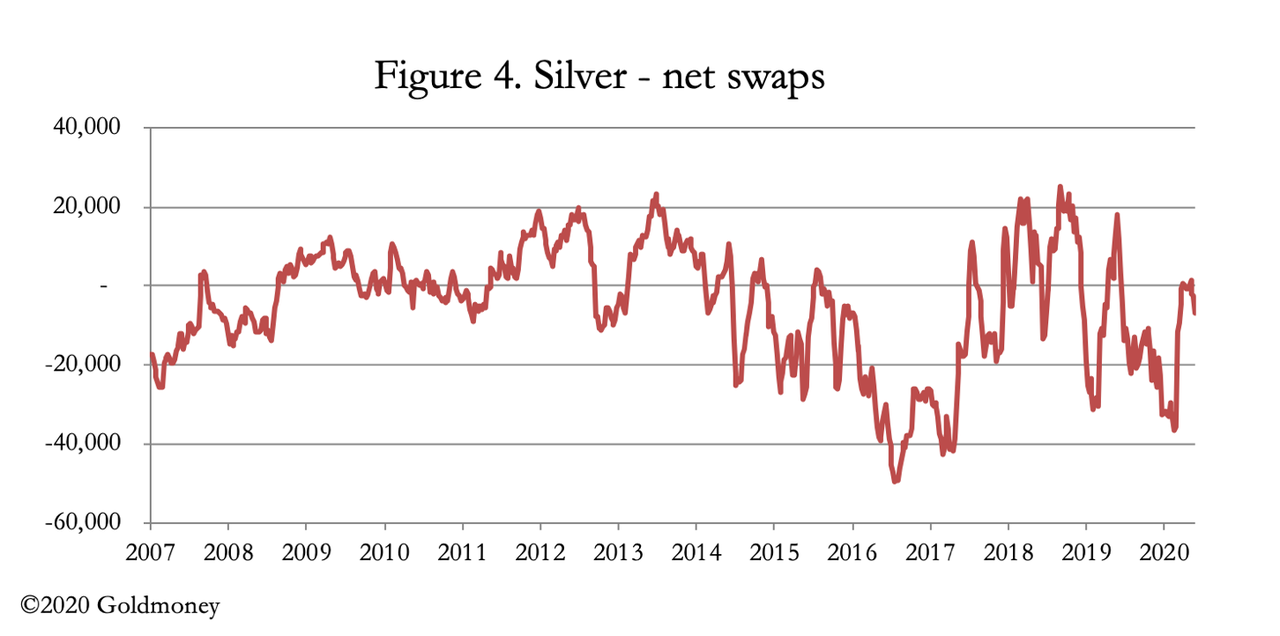

Figure 4 shows the latest available data for the net position of swap dealers, effectively the bullion banks trading desks.

The last commitment of traders’ figures, for 26 May, shows a net short position of only 6,652 contracts; therefor swap dealers positions are almost level. This is a different situation from the gold futures contract where the swaps are currently short a net 182,864 contracts representing the equivalent of 569 tonnes worth $31 billion, almost a record and a major headache for the bullion banks.

In conclusion, having been left behind while monetary events have been focusing on the gold price, silver is now beginning to catch up. The spike to a gold/silver ratio of 125 appears to have marked a major turning point in the relationship, and silver can therefore be expected to continue to outperform gold as the fiat money situation deteriorates. Traders at the bullion banks appear to be avoiding short positions in silver futures, in which case a rising price will see them withdrawing liquidity instead of supplying additional contracts to the buyers.

The global economic and monetary situation is dire, due to both the coronavirus and because the credit cycle was already turning down in late-2019. The amount of monetary debasement deployed by central banks in an attempt to save their economies promises to be unprecedented to the point where total monetary destruction will be an increasingly likely outcome.

That being the case, the attraction of silver over gold is to be found in a substantial fall of the gold/silver ratio, as it dawns on markets that the end of fiat money is nigh.

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

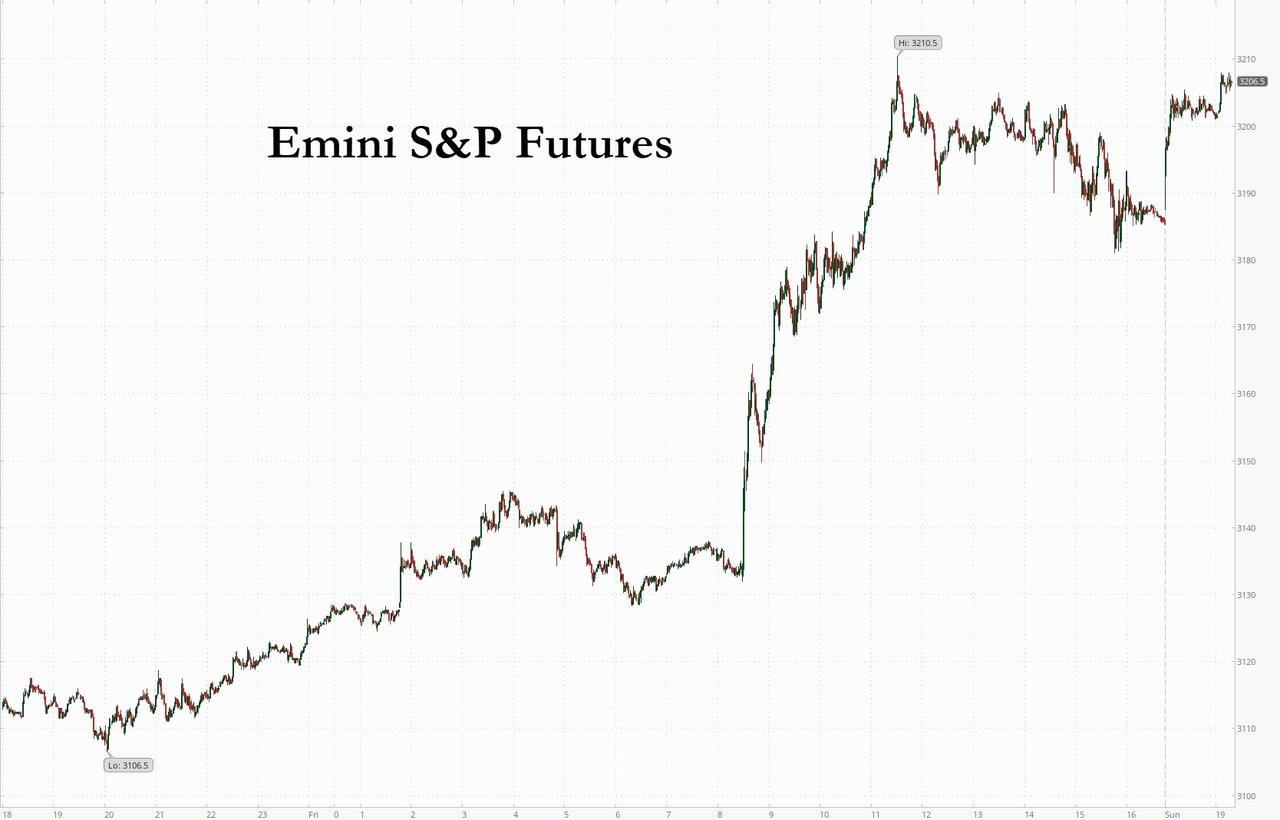

Global Stocks Rise, S&P Futures Above 3,200 As Melt-Up Continues

One day after a record surge in Nasdaq trading volumes on Friday, which was coupled with a record spike in call option activity as both retail and hedge fund investors rush into stocks, global stocks inched higher again on Monday, adding to a 42% surge from their March lows, as the unexpectedly strong US jobs report data fuelled hopes of a quicker global economic recovery from the coronavirus pandemic. Emini futures jumped in early trading overnight then drifted in a range between 3,185 and 3,210.

In stock-specific news, Bloomberg over the weekend reported that AstraZeneca approached Gilead regarding a potential merger which would mark the largest healthcare deal on record. However, sources via The Times downplayed the prospect of any AstraZeneca interest, stating that it has abandoned a tentative interest, while Wall Street analysts puked on the prospects of the deal. Gilead was 3.3% higher in pre-market.

The MSCI all-country world stocks index was 0.1% higher and just 7% away from a fresh record high, while the benchmark S&P 500 is within striking distance of turning positive for the year.

In Europe, a surge in travel and leisure stocks helped cap losses on the pan-regional index, which traded 0.2% lower after poor German and Chinese economic data. The Eurostoxx 50 was weighed down by tech and healthcare names while the FTSE MIB and IBEX bucked the trend, rising over 0.5% supported by banks and autos.

Europe’s fundamentals remain dismal with German industrial output slumping a record 17.9% in April and firms now expect a bumpy road ahead despite a massive stimulus package.

“European stocks are probably under pressure following weak China data overnight. However, we do not think this marks the end of the rally,” said Marija Vertimane, senior strategist at State Street Global Markets. “We are beginning to see evidence of economic data improving gradually and thankfully no major secondary spikes in infections. We expect that to encourage investors to come back to the market.”

Asia shares rose in a catch-up rally following Friday’s U.S. jobs data but were again capped by the Chinese data, published on Sunday, which showed exports contracted in May although an even bigger drop in imports resulted in a record trade surplus. All markets in the region were up, with Jakarta Composite gaining 2.5% and Singapore’s Straits Times Index rising 1.4%. Trading volume for MSCI Asia Pacific Index members was 25% above the monthly average for this time of the day. The Topix gained 1.1%, with Asahi Broadcasting Group and Gumi rising the most. The Shanghai Composite Index rose 0.2%, with Fujian Start Group and Changshu Fengfan Power Equipment posting the biggest advances.