GOLD:$1714.80 DOWN $0.30 The quote is London spot price

Silver:$17.67 UP 3 CENTS//LONDON SPOT PRICE

Closing access prices: London spot

i)Gold : $1738.00 LONDON SPOT 4:30 pm

ii)SILVER: $18.10//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUG GOLD: $1720.70 CLOSE 1.30 PM// SPREAD SPOT (LONDON) VS/FUTURE JUNE: $+5.90

CLOSING SILVER FUTURE MONTH

JULY: 1:30 PM: $17.79//1:30 PM //SPREAD SPOT LONDON VS FUTURE JULY: 12 CENTS PER OZ//

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2800. usa per oz

and silver; $31.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

DO NOT PAY ANY ATTENTION TO WHAT THE CROOKS ARE DOING AT THE COMEX AND LONDON LBMA..PHYSICAL IS THE NAME OF THE GAME AND NOTHING ELSE

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 845/1282

issued 276

EXCHANGE: COMEX

CONTRACT: JUNE 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,714.700000000 USD

INTENT DATE: 06/09/2020 DELIVERY DATE: 06/11/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 21

072 H GOLDMAN 115

104 C MIZUHO 2

118 H MACQUARIE FUT 25

132 C SG AMERICAS 3

167 C MAREX 1

190 H BMO CAPITAL 12

323 H HSBC 3

355 C CREDIT SUISSE 12

357 C WEDBUSH 1 2

555 C BNP PARIBAS SEC 1

555 H BNP PARIBAS SEC 800

624 C BOFA SECURITIES 31

657 C MORGAN STANLEY 55

657 H MORGAN STANLEY 57

661 C JP MORGAN 276 813

661 H JP MORGAN 82

685 C RJ OBRIEN 1

686 C INTL FCSTONE 89 1

690 C ABN AMRO 66 16

732 C RBC CAP MARKETS 2

737 C ADVANTAGE 2

800 C MAREX SPEC 7 10

845 C GOLDMAN SACHS C 1

880 C CITIGROUP 1

905 C ADM 43 13

____________________________________________________________________________________________

TOTAL: 1,282 1,282

MONTH TO DATE: 48,757

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT: 1282 NOTICE(S) FOR 128,200 OZ (3.987 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 48,757 NOTICES FOR 4,875,700 OZ (151.657 TONNES)

SILVER

FOR JUNE

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 418 for 2,090,000 oz

BITCOIN MORNING QUOTE $9724 DOWN $51

BITCOIN AFTERNOON QUOTE.: $9862 UP 90

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $.30 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

A HUGE 4.02 TONNES OF GOLD DEPOSITED INTO THE GLD/

GLD: 1,129.50 TONNES OF GOLD//

WITH SILVER UP 3 CENTS TODAY: AND WITH NO SILVER AROUND

RESTING SLV INVENTORY TONIGHT:

SLV: 472.849 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A STRONG SIZED 3788 CONTRACTS FROM 171,452 UP TO 175,240 AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE STRONG SIZED GAIN IN OI OCCURRED WITH OUR SMALL 6 CENT LOSS IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS DUE TO STRONG BANKER SHORT COVERING PLUS A FAIR EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A ZERO INCREASE IN SILVER OZ STANDING AT THE COMEX FOR JUNE. WE HAD A NET GAIN IN OUR TWO EXCHANGES OF 4284 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUMONGOUS AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: MAY: 0 AND JULY: 500 AND SEPT 0 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 500 CONTRACTS. WITH THE TRANSFER OF 500 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 225 EFP CONTRACTS TRANSLATES INTO 2.500 MILLION OZ ACCOMPANYING:

1.THE 6 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.145 MILLION OF INITIALLY STANDING FOR JUNE

TUESDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL 6 CENTS).. AND,OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS. THE CONSIDERABLE GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A ZERO INCREASE IN SILVER OZ STANDING CONSIDERABLE BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A STRONG NET GAIN OF 3918 CONTRACTS OR 19.590 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

SPREADING OPERATIONS

OUR SPREADING OPERATION HAS NOW SWITCHED INTO SILVER…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN SILVER AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JULY.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF JUNE. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

JUNE

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF JUNE:

3862 CONTRACTS (FOR 9 TRADING DAY(S) TOTAL 3862CONTRACTS) OR 19.310 MILLION OZ: (AVERAGE PER DAY: 429 CONTRACTS OR 2.155 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 19.310 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 3.08% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,085.42 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP SO FAR 19.310 MILLION OZ.

EXCHANGE FOR PHYSICAL ISSUANCE FOR THE PAST 60 DAYS IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD AN EXTREMELY LARGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3788, DESPITE OUR 6 CENT GAIN IN SILVER PRICING AT THE COMEX ///TUESDAY… THE CME NOTIFIED US THAT WE HAD A TINY SIZED EFP ISSUANCE OF 130 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A STRONG SIZED OI CONTRACTS ON THE TWO EXCHANGES: 3918 CONTRACTS (DESPITE OUR 6 CENT LOSS IN PRICE)

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 130 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A LARGE SIZED INCREASE OF 3788 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED DESPITE A 6 CENT LOSS IN PRICE OF SILVER/AND A CLOSING PRICE OF $17.64 // TUESDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.846 BILLION OZ TO BE EXACT or 121% of annual global silver production (ex Russia & ex China).

FOR THE NEW JUNE DELIVERY MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR nil OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.145 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD 5768CONTRACTS TO 475,661 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE CONSIDERABLE SIZED GAIN OF COMEX OI OCCURRED WITH OUR STRONG GAIN IN PRICE OF $16.00 /// COMEX GOLD TRADING// TUESDAY// WE HAD STRONG BANKER SHORT COVERING, ANOTHER HUMONGOUS SIZED INCREASE IN GOLD OZ STANDING AT THE COMEX, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A FAIR EX. FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR STRONG GAIN IN PRICE OF $16.00 .

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 8

WE GAINED A STRONG SIZED 9455 CONTRACTS (29.40 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3687 CONTRACTS:

CONTRACT JUNE 0.; AUG 3687 AND ALL OTHER MONTHS ZERO//TOTAL: 3687. The NEW COMEX OI for the gold complex rests at 475,661. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 9455 CONTRACTS: 5768 CONTRACTS INCREASED AT THE COMEX AND 3687 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 9455 CONTRACTS OR 29.40 TONNES. TUESDAY, WE HAD A STRONG GAIN OF $16.00 IN GOLD TRADING……

AND WITH THAT GAIN IN PRICE, WE HAD A STRONG SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 29.40 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $16.00).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS UNSUCCESSFUL (SEE BELOW).

4 GC VOLUME: 0 // open interest 8

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3687) ACCOMPANYING THE CONSIDERABLE SIZED GAIN IN COMEX OI (5768 OI): TOTAL GAIN IN THE TWO EXCHANGES: 9455 CONTRACTS. WE NO DOUBT HAD 1 )CONSIDERABLE BANKER SHORT COVERING, 2.)ANOTHER HUMONGOUS INCREASE IN GOLD OUNCES STANDING AT THE GOLD COMEX FOR THE FRONT JUNE MONTH, 3) ZERO LONG LIQUIDATION; 4) CONSIDERABLE COMEX OI GAIN.. AND …ALL OF THIS WAS COUPLED WITH OUR STRONG GAIN IN GOLD PRICE TRADING//TUESDAY//$16.00.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

JUNE

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES: 76.41 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 76.41/3550 x 100% TONNES =2.15% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 2891.34 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 76.41 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 3788 CONTRACTS FROM 171,452 UP TO 175,240 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE STRONG GAIN IN OI SILVER COMEX WAS DUE TO; 1) CONSIDERABLE BANKER SHORT COVERING , 2) A TINY ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A GOOD INCREASE IN SILVER OZ STANDING AT THE COMEX FOR JUNE AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 130 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY: 500 CONTRACTS AND SEPT: 00 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 130 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3784 CONTRACTS TO THE 130 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 3918 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 19.590 MILLION OZ!!! OCCURRED WITH THE 6 CENT LOSS IN PRICE///

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 6 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// TUESDAY. WE ALSO HAD A FAIR SIZED 500 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 12.36 POINTS OR 0.42% //Hang Sang CLOSED DOWN 7.49 POINTS OR 0.03% /The Nikkei closed UP 33.92 POINTS OR 0,15%//Australia’s all ordinaires CLOSED UP .10%

/Chinese yuan (ONSHORE) closed UP at 7.0606 /Oil DOWN TO 38.10 dollars per barrel for WTI and 40.47 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0606 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.0544 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/USA RIOTS : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

i)we had 1 deposits into the customer account

into JPMorgan: 0

ii)into Delaware: 172,986.355 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.819 million oz of total silver inventory or 51.22% of all official comex silver. (160.819 million/313.078 million

total customer deposits today: 172,986,355 oz

we had 1 withdrawals:

i) Out of CNT: 1,200,293.180 oz

total withdrawals; 1200,293.180 oz

We had 1 adjustments

i ) Out of CNT: 76,329.600 oz was adjusted out of dealer CNT into the customer CNT

total dealer silver: 85.324 million

total dealer + customer silver: 313.078 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The total number of notices filed today for the JUNE 2020. contract month is represented by 0 contract(s) FOR nil, oz

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 418 x 5,000 oz = 2,090,,000 oz to which we add the difference between the open interest for the front month of JUNE.(11) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JUNE/2019 contract month: 418 (notices served so far) x 5000 oz + OI for front month of JUNE (11)- number of notices served upon today 14) x 5000 oz of silver standing for the JUNE contract month.equals 2,145,000 oz.

We GAINED 0 contracts or an additional nil oz will stand for delivery as they refused to morphed into London based forwards as well as negating a fiat bonus

TODAY’S ESTIMATED SILVER VOLUME: 87,642 CONTRACTS // volume good/

FOR YESTERDAY: 78,770..,CONFIRMED VOLUME//volume good/

YESTERDAY’S CONFIRMED VOLUME OF 78,770 CONTRACTS EQUATES to 393 million OZ 56.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 1.62% ((JUNE 10/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.12% to NAV: (JUNE 10/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 1.62%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 16.55 TRADING 16.49///NEGATIVE 0.98

END

And now the Gold inventory at the GLD/

JUNE 10/WITH GOLD DOWN $.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 4.02 TONNES AT THE GLD/INVENTORY RESTS AT 1129.50 TONNES

JUNE 9//WITH GOLD UP $16.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 2.63 TONNES OF GOLD AT THE GLD//INVENTORY RESTS AT 1125.48 TONNES

JUNE 8//WITH GOLD UP $18.70 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 4.10 TONNES AT THE GLD//INVENTORY RESTS AT 1128.11 TONNES

JUNE 5//WITH GOLD DOWN $40.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A PAPER WITHDRAWAL OF 1.16 TONNES OUT OF THE GLD//INVENTORY RESTS AT 1132.21 TONNES

JUNE 4//WITH GOLD UP $20.60: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD…A DEPOSIT OF 4.09 TONNES INTO THE GLD//INVENTORY RESTS AT 1133.37 TONNES

JUNE 3//WITH GOLD DOWN $26.15//A SMALL CHANGE IN GOLD INVENTORY//A DEPOSIT OF 0.78 TONNES OF GLD INTO THE GLD//INVENTORY RESTS AT 1129.28 TONNES

JUNE 2//WITH GOLD DOWN $11.20 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1128.40 TONNES

JUNE 1//WITH GOLD UP $1.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES OF GOLD//GLD INVENTORY RESTS TONIGHT AT 1123.14 TONNES

MAY 29/WITH GOLD UP $19.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///GLD INVENTORY RESTS THIS WEEKEND AT 1119.05 TONNES

MAY 28//WITH GOLD UP $4.00 TODAY/NO CHANGES IN GOLD INVENTORY TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

MAY 27/WITH GOLD UP $.10 TODAY: A STRONG 2.34 TONNES OF GOLD ADDED TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

MAY 26//WITH GOLD DOWN $23.05//NO CHANGES IN GOLD INVENTORY://RESTS TONIGHT AT 1116.71 TONNES

MAY 22//WITH GOLD UP $13.05//A BIG CHANGE IN GOLD INVENTORY:: A PAPER ADDITION OF 3.93 TONNES//INVENTORY RESTS THIS WEEKEND AT: 1116.71 TONNES

MAY 21//WITH GOLD DOWN $26.70//NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1112.32 TONNES

MAY 20/WITH GOLD UP $7.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 1.46 TONNES FROM THE GLD////INVENTORY RESTS TONIGHT AT 1112.32 TONNES

MAY 19//WITH GOLD UP $10.60//NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1113.78 TONNES

MAY 18/WITH GOLD DOWN $15.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A PAPER DEPOSIT OF 9.06 TONNES./INVENTORY RESTS AT 1113.78 TONNES

MAY 15.WITH GOLD UP $16.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 12.58 TONNES/ INVENTORY RESTS AT 1104.72 TONNES

MAY 14//WITH GOLD UP $19.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1092.14 TONNES

MAY 13//WITH GOLD UP $9.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 11.07 TONNES/INVENTORY RESTS AT 1092.14 TONNES

MAY 12//WITH GOLD UP $6.60 TODAY; A SMALL CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 1081.07 TONNES

MAY 11/WITH GOLD DOWN $12.65 TODAY: NO CHANGES IN GOLD INVENTORY: //INVENTORY RESTS AT 1081.65 TONES..

MAY 8/WITH GOLD DOWN $7.00 TODAY; A BIG CHANGE IN GOLD INVENTORY: A PAPER ADDITION OF 5.85 TONNES/INVENTORY RESTS AT 1081.65 TONNES

MAY 7/WITH GOLD UP $29.65 TODAY : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER ADDITION OF .41 TONNES/INVENTORY RESTS AT 1075.80 TONNES

MAY 6//WITH GOLD DOWN $17.00 TODAY/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER ADDITION OF 3.68 TONNES/INVENTORY RESTS AT 1075.39 TONES

MAY 5/WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER ADDITION OF 3.81 TONNES//INVENTORY RESTS AT 1071.71 TONNES

MAY 4//WITH GOLD UP $12.00 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE PAPER DEPOSIT OF 11.4 TONNES INTO THE GLD////GOLD INVENTORY RESTS AT 1067.90 TONNES

MAY 1/WITH GOLD UP $8.45 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1056.50 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

JUNE 10/ GLD INVENTORY 1129.50 tonnes*

LAST; 838 TRADING DAYS: +184.58 NET TONNES HAVE BEEN REMOVED FROM THE GLD

LAST 738 TRADING DAYS://+359.76 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JUNE 10/WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.849 MILLION OZ//

JUNE 9/WITH SILVER DOWN 6 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.605 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 422.849 MILLION OZ//

JUNE 8/WITH SILVER UP 36 CENTS TODAY: TWO HUGE WITHDRAWALS OF 932,000 MILLION OZ AND 1.491 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 470.240 MILLION OZ//

JUNE 5/WITH SILVER DOWN 46 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 648,000 OZ FROM THE SLV////INVENTORY RESTS AT 472.663 MILLION OZ

JUNE 4//WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV.//INVENTORY RESTS AT 473.315 MILLION OZ//

JUNE 3//WITH SILVER DOWN 23 CENTS TODAY//NO CHANGES IN SILVER INVENTORY AT THE SLV//

INVENTORY RESTS AT 473.315 MILLION OZ//

JUNE 2//WITH SILVER DOWN 31 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUMONGOUS 6.686 MILLION OZ ADDED TO THE SLV////INVENTORY RESTS TONIGHT AT 473.315 MILLION OZ//

JUNE 1//WITH SILVER UP 38 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.56 MILLION OZ INTO THE SLV////INVENTORY RESTS TONIGHT AT 466.629 MILLION OZ//

MAY 29//WITH SILVER UP 52 CENTS TODAY: A MASSIVE DEPOSIT OF 2.796 MILLION OZ INTO THE SLV//INVENTORY RESTS THIS WEEKEND AT 463.273 MILLION OZ//

MAY 28//WITH SILVER UP 9 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.660 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 460.477 MILLION OZ//

MAY 27/WITH SILVER UP 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 455.817 MILLION OZ//

MAY 26//WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/// INVENTORY RESTS AT 455.817 MILLION OZ//

MAY 22/WITH SILVER UP 22 CENTS TODAY/ A HUGE PAPER WITHDRAWAL OF 1.864 MILLION OZ//INVENTORY RESTS AT 455.817 MILLION OZ/

LAST 5 DAYS: SILVER UP 60 CENTS: INVENTORY UP A WHOOPING 23.767 MILLION OZ///

MAY 21/WITH SILVER DOWN 50 CENTS TODAY: A HUGE PAPER DEPOSIT OF 7.923 MILLION OZ///INVENTORY RESTS AT 457.681 MILLION OZ//

MAY 20//WITH SILVER UP ANOTHER 11 CENTS TODAY: A HUGE CHANGE IN SLV INVENTORY: A HUGE PAPER DEPOSIT OF 9.601 MILLION OZ INTO THE SLV// //INVENTORY RESTS AT 449.758 MILLION OZ

MAY 19/WITH SILVER UP ANOTHER 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 440.157 MILLION OZ//

MAY 18/WITH SILVER UP ANOTHER 48 CENTS TODAY: TWO BIG CHANGES IN SILVER INVENTORY AT THE SLV I.E. 2 PAPER DEPOSIT OF ( I) 8.39 MILLION OZ AND THEN ( 2) 8.109 MILLION OZ//INVENTORY RESTS AT 432.048 MILLION OZ// (TOTAL DEPOSITS 16.500 MILLION OZ///)

MAY 15/WITH SILVER UP 81 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV: /INVENTORY RESTS AT 423.65 MILLION OZ.

MAY 14//WITH SILVER UP 33 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV.//INVENTORY RESTS AT 423.65 MILLION OZ

MAY 13/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.79 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 423.65 MILLION OZ//

MAY 12/WITH SILVER UP 5 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.076 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 420.861 MILLION OZ//

MAY 11.WITH SILVER DOWN 5 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 417.785 MILLION OZ//

MAY 8/WITH SILVER UP 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTER DEPOSIT OF 4.661 MILLION OZ OF SILVER INTO THE SLV..///INVENTORY RESTS AT 417.785 MILLION OZ//

MAY 7/WITH SILVER UP 45 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 5/WITH SILVER UP 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ///

MAY 4//WITH SILVER DOWN 5 CENTS TODAY:2 HUGE PAPER CHANGES IN SILVER INVENTORY AT THE SLV.i).A LARGE 1.399 MILLION OZ OF PAPER SILVER REMOVED FROM THE SLV//..//INVENTORY RESTS AT 411.427 MILLION OZ and ii) A LARGE 1.647 MILLION OZ OF PAPER SILVER ADDED TO THE SLV// INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 1/WITH SILVER FLAT IN PRICE: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 412.826 MILLION OZ///

JUNE 10.2020:

SLV INVENTORY RESTS TONIGHT AT

472.849 MILLION OZ.

END

LIBOR SCHEDULE AND GOFO RATES// GOLD LEASE RATES

YOUR DATA…..

6 Month MM GOFO 2.70/ and libor 6 month duration 0.46

Indicative gold forward offer rate for a 6 month duration/calculation:

GOLD LENDING RATE: -2.24%

NEGATIVE GOLD LEASING RATES INCREASING BY A HUGE AMOUNT//GOLD SCARCITY AND CENTRAL BANKS CALLING IN ALL OF THEIR GOLD LEASES

XXXXXXXX

12 Month MM GOFO

+ 2.25%

LIBOR FOR 12 MONTH DURATION: 0.63

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -1.62%

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

Does China vault any gold at the New York Fed: totally unlikely

(Jan Nieuwenhuijs/GATA)

Jan Nieuwenhuijs: It’s unlikely China vaults gold at the New York Fed

Submitted by cpowell on Tue, 2020-06-09 15:41. Section: Daily Dispatches

11:40a ET Tuesday, June 9, 2020

Dear Friend of GATA and Gold:

Does China store gold at the Federal Reserve Bank of New York?

Voima Gold researcher Jan Nieuwenhuijs today addresses the question and concludes that such storage is highly unlikely.

But Nieuwenhuijs reprints the brief memoir of a former Bank of China official who handled gold and foreign exchange transactions for the Chinese government in the 1980s and in 1983 accompanied government gold flown from Beijing for vaulting at the Bank of England in London.

…

The memoir may be most interesting for suggesting that China’s government back then was interested in earning money by leasing its gold from the Bank of England.

Nieuwenhuijs’ report is headlined “Does the People’s Bank of China Store Gold at the Fed in New York?” and it’s posted at Voima Gold here:

https://www.voimagold.com/insight/does-the-pboc-store-gold-at-the-fed-in…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Pam and Russ talks about the financial crisis that has started well before the Covid 19.

(Pam and Russ Martens/Wall Street on Parade/GATA)

Pam and Russ Martens: Investors were blocked from fund withdrawals months before virus pandemic

Submitted by cpowell on Tue, 2020-06-09 15:50. Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Monday, June 8, 2020

Wall Street On Parade has previously written that a financial crisis was already well under way before the first case of Covid-19 was reported anywhere in the world. This should matter greatly to Americans because the Federal Reserve is attempting to blame the financial crisis on the virus to avoid congressional investigations of its second epic failure in a dozen years at regulating the behemoth Wall Street banks.

America needs a comprehensive investigation of what really triggered this financial crisis in order to restructure the U.S. financial system away from a casino culture into one that doesn’t regularly need massive Federal Reserve and government bailouts.

These bailouts are piling more and more debt on the shoulders of taxpayers and becoming a crushing drag on the U.S. economy, notwithstanding Fed Chairman Jerome Powell’s dismissive remark to Congress that we’ll worry about the debt later.

Today we’re expanding our financial crisis timeline to include pre-Covid-19 announcements of big job cuts at global banks; mutual funds and hedge funds taking the desperate measure of locking out investors from access to their money; and the massive sums investors were pulling from mutual funds and hedge funds throughout 2019 — all prior to the first case of Covid-19 anywhere in the world. …

… For the remainder of the analysis:

https://wallstreetonparade.com/2020/06/investors-were-being-blocked-from…

* * *

END

Gold’s rise is causing bullion banks to cover their shorts in a big way

(Craig Hemke/Sprott/GATA)

Craig Hemke at Sprott Money: Clearing the Comex decks

Submitted by cpowell on Wed, 2020-06-10 02:39. Section: Daily Dispatches

10:40p ET Tuesday, June 9, 2020

Dear Friend of GATA and Gold:

Positions of both speculators and bullion banks in gold futures contracts on the New York Commodities Exchange have been steadily declining, the TF Metals Report’s Craig Hemke writes tonight at Sprott Money.

This, Hemke writes, suggests that there is no speculative bubble and that the banks are getting out of the way of an imminent rally.

Hemke’s analysis is headlined “Clearing the Comex Decks” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/clearing-the-comex-decks-craig-hemke-ju…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

iii) Other physical stories:

A good commentary tonight from Peter Schiff: Central banks added 32 tonnes of gold in April despite the lockdowns. Even bankrupt Turkey led the way

(Peter Schiff)

Central Banks Added Nearly 32 Tons Of Gold To Reserves In April, Led By Turkey

The pace has slowed somewhat this year, but central banks are still buying gold, and the World Gold Council expects central bank demand to continue over the next 12 months.

In April, central banks globally added another net 31.6 tons of gold to their reserves, despite Russia following through on its commitment to suspend its buying program.

According to the World Gold Council, the lower rate of purchases was entirely expected given the strength of central bank buying both in 2018 and 2019.

On the year, central banks have added a net 142 tons of gold to their reserves. This is off the near-record pace of purchases last year.

Central bank demand came in at 650.3 tons in 2019. That was the second-highest level of annual purchases for 50 years, just slightly below the 2018 net purchases of 656.2 tons. According to the WGC, 2018 marked the highest level of annual net central bank gold purchases since the suspension of dollar convertibility into gold in 1971, and the second-highest annual total on record.

The World Gold Council bases its data on information submitted to the International Monetary Fund.

Turkey drove purchases yet again in April. The Turks added 38.8 tons of gold to its hoard, bringing its total reserves to 524 tons. The Turkish lira dropped to near all-time lows in March and the Turkish central bank is frantically trying to backstop its currency. Meanwhile, Turkey is selling dollars. According to Bloomberg, state banks sold roughly $1.1 billion of foreign currency in just two days last month.

Serbia continued to buy small amounts of gold, adding another 0.1 ton. The Serbs bought 9 tons of the yellow metal back in October 2019 and have added at least 0.1 ton to its reserves every month since.

We saw a little bit of selling in April as well. Kazakhstan reduced its gold reserves by 4.1 tons and Uzbekistan’s holdings declined by 2.2 tons. Russia saw a modest drop of 0.4 tons in its reserves.

In March, the Central Bank of Russia announced it planned to suspend gold-purchases for the time being, effective April 1. But there is already pressure on the bank to resume purchases. In early April, Russian banks asked the Central Bank of Russia to resume buying gold for its reserves as gold exports were hobbled by the coronavirus pandemic. In a letter released on April 29, the Russian central bank said it did not see any need to resume buying gold at the time, but added it would continue to monitor the situation in both the global gold market and the banking sector.

For the seventh straight month, the People’s Bank of China did not report any gold purchases. It’s not uncommon for China to go silent and then suddenly announce a large increase in reserves.

Many analysts believe China holds far more gold than it officially reveals. As Jim Rickards pointed out on Mises Daily back in 2015, many people speculate that China keeps several thousand tons of gold “off the books” in a separate entity called the State Administration for Foreign Exchange (SAFE). Given the political dynamics and the ongoing trade war, it seems unlikely the Chinese suddenly stopped increasing their gold reserves in 2016.

Does the slowdown in purchases in recent months signal an absence of central bank demand going forward? The World Gold Council doesn’t think so.

As we noted in our Q1 2020 Gold Demand Trends report, the case for central banks holding gold remains strong. Especially considering the economic uncertainty caused by the COVID-19 pandemic.”

The WGC 2020 Central Bank Survey found that 20% of central banks globally plan to expand their gold holdings in the next 12 months.

Factors related to the economic environment – such as negative interest rates – were overwhelming drivers of these planned purchases. This was supported by gold’s role as a safe haven in times of crisis, as well as its lack of default risk.”

One thing is clear, the trend towards precious metals reserves continues…

https://www.jsmineset.com/2020/06/10/precious-metals-open-interest-is-showing-the-fear/

Precious Metals Open Interest Is Showing The Fear!

Posted June 10th, 2020 at 9:03 AM (CST) by J. Johnson & filed under General Editorial.

Great and Wonderful Wednesday Morning Folks,

It’s the final day of the FOMC meetings and Gold is inside a $10 trading range at $1,728.10, up $6.20 and right close to the high at $1,728.40 with the low at $1,718.70. Silver is leading again, in its choppy and sporadic way as it attempts to break free from all that applied calm, with the trade at $17.945, up 15.6 cents with the high – ½ penny away and the low at $17.715. The US Dollar, the topic of today’s FOMC meeting (it’s really about the set calculations against Silver and Gold), is valued at 96.020, down 30.1 points and near its low of 95.975 with the high up at 96.465. Of course, all this happened already, before 5 am pst, the Comex open, the London close, and after the FBI started looking and scooping up the idiots who used social media to brag about the stuff they stole while protesting a wrongful death.

Precious Metals are gaining across the board today. Venezuela’s Bolivar is getting weaker, continuing to make Gold more valuable with the trade at 17,259.40, gaining 110.86 Bolivar since yesterday with Silver now at 179.226 Bolivar finally gaining 1.049 after several days of applied calm. Argentinians are now paying 119,413.93 Peso’s for 1 ounce of Gold proving a gain of 1,164.14 with Silver also showing a 10.87 A-Peso gain with the trade at 1,239.99. The Turkish Lira’s price for Gold now sits at 11,734.46, proving a gain of 53.32 Lira with Silver also gaining 0.49 of a T-Lira with the last trade at 121.854.

June Silver’s Demand Count now sits at 11 fully paid for contracts and with no purchases made in the early morning as we wait for Mr. Resolute to make his mark once again. Hopefully he’ll be here just before the Gods of Print bless their own against the mass of investors they could not beat if they didn’t have control of the print. Yesterday’s delivery activity occurred at one price, $17.83 with a Volume of 1 with that adjusted price settled down at $17.774 as 14 buyers finally got their receipts. The fear is showing up behind the price as the Overall Open Interest continues to climb in order to keep the calm with the short trades adding another 3,788 contracts bringing the count to 175,237 Overnighters.

June Gold’s Delivery Requests now sit at 3,970 fully paid for contracts and with a Volume of 35 already posted up on the board inside a trading range between $1,724.80 and $1,716.10 with the last trade, of course, at the high. Yesterday’s final trading range occurred between $1,720.90 and $1,692 with the last trade (I could see) at $1,712 with the adjusted close higher at $1,714.70 with a final Volume of 690. Only 100 buyers got receipts during all that activity. The fear behind the price finally popped into Gold yesterday as 5,845 short contracts had to be added or Gold would have a much higher value than it is now with the total Short Vs Long reaching 475,987 Overnighters (buyers and sellers holding their positions overnight) on the first day of the FOMC.

As time rolls by, we continue to see the intrusion against truth in reporting as the Chinese Propaganda outlet called “China Watch”, paid millions to the Washington Post and the Wall Street Journal over the years, to run advertisements made to look like news reports. Then we have something very interesting, if true it’s a huge WOW, about ANTIFA management being picked up on the streets as they are walking, leaving the underlings in absolute fear as we once again state, how difficult is it to understand “we have the servers”? It may be time to Q the videos. Those that follow and believe in law and order, may be finally seeing it occur, but don’t expect the media to tell you about it, they are commercially compromised to not be truthful.

More and more people are bypassing all proclaimed media and are going directly to the sources, such as the White House Press meetings to hear the Scorched Earth Tongue of Kayleigh McEnany. It’s amazing to see how the presstitutes act now after trying their best to ask loaded and stupid questions. Many are also going directly to the president’s tweets as well in order to get what our legally elected is trying to do while the press proves it’s been on the side of foreign nations against our country and its people.

We sit with physicals, outside the financial mess called the markets, controlled by a (not really federal) Fed Reserve, that may have been swallowed up by the US Treasury. Then the compromising media, which is advertising pure bias claiming its news when many of us remember what news used to be, just the facts presented without bias. Have a great day! After all it’s all up to you to do so. Keep the faith, and a smile no matter what, because we are still right here, keeping watch, we believe higher prices in Silver and Gold are coming, because it’s a real product that fiat was made to trade against ….

Stay Strong!

Jeremiah Johnson

More J.Johnson content is available with purchase of a JSMineset subscription.

Top Primary Silver Mining Industry Production Yield Falls To The Lowest Ever

The era of high-grade silver mines may be coming to an end. Remarkably, the top primary silver miners’ average yield fell to the lowest ever in 2019. Which begs the question, will high-grade silver mines become extinct in the not-so-distant future? Well, if we look at the data, it seems to be already happening.

Since I started researching the primary silver mining industry, the yields at many high-grade silver mines have fallen drastically. For example, Fresnillo PLC’s Flagship mine, the Fresnillo Mine, had seen its average yield decline from 15 oz/t (ounce per tonne) in 2005 to only 5.3 oz/t last year. That is one hell of a reduction in just 14 years… nearly 10 oz/t of silver yield evaporated.

Take a look at how much more silver the Fresnillo Mine was producing in 2005 compared to 2019… processing LESS ORE!!

- Fresnillo Mine 2005 Production = 33.4 million oz

- Fresnillo Mine 2005 Processed Ore = 2.2 million tons

- Fresnillo Mine 2005 Average Yield = 15.2 oz/t

- Fresnillo Mine 2019 Production = 13.0 million oz

- Fresnillo Mine 2019 Processed Ore = 2.5 million tons

- Fresnillo Mine 2019 Average Yield = 5.3 oz/t

As we can see, workers at the Fresnillo Mine processed more ore in 2019 to produce 20 million fewer ounces of silver. No wonder the cost to produce silver has risen from $4-5 per ounce back in 2005 to over $15+ an ounce presently.

Now, if we combine the top seven primary silver miners in my group, the average yield fell to a record low of 6.0 oz/t in 2019:

The top primary silver mining companies’ average yield fell from 13 oz/t in 2005 to 6.0 oz/t last year. That’s a 54% decline in average yield from the top primary silver mining industry. This means these silver mining companies have to extract, transport, and process more than twice the amount of ore than they did in 2005 to produce the same amount of metal.

The companies that impacted the group’s average yield the most were from Peru. Peru’s Hochschild average yield declined from 7.5 oz/t in 2018 to 5.9 oz/t last year, while Buenaventura’s average yield fell from 10.6 oz/t to 7.5 oz/t during the same period. Mexico’s Fresnillo PLC’s average yield from its primary silver mines (Fresnillo, Saucito & San Julian) fell from 5.7 oz/t in 2018 to 5.0 oz/t in 2019.

Also, Russia’s Polymetal International, Dukat Operations, saw its average yield fall to 7.7 oz/t last year down from 8.5 oz/t in 2018. The only primary silver miner that saw an increase in yield was Hecla. Mainly due to Hecla’s Greens Creek Mine, the company’s average silver yield increased from 10 to 11.5 oz/t during the same period.

The world is running out of its HIGH-GRADE, easy to get to silver deposits. While there are still some high-grade silver deposits still remaining in the world, the primary mining industry continues to BURN through its better quality reserves. At some point, production from these top seven silver mines will no longer be able to offset the declines from falling ore grades.

Investors have no idea what a deal they are getting in acquiring silver for such a great deal when we compare it to most of the over-valued financial paper assets and real estate. The few silver miners in the world may just surprise the market when investors begin to move into them in a BIG WAY.

THANK YOU ALL FOR THE SUPPORT: I just wanted to thank all the individuals who continue to support the SRSrocco Report website and youtube channel. I know some of you have canceled memberships as times are tough. I understand. If you are new to the site and find the information valuable, please consider supporting the website, if you have the means to do so, at Paypal or Patreon below.

If you are new to the SRSrocco Report, please consider subscribing to my: SRSrocco Report Youtube Channel.

HOW TO SUPPORT THE SRSROCCO REPORT SITE:

I would also like to thank those foundation supporters, who have chosen to become a member by making donations through PayPal to further the research and publishing work at the SRSrocco Report.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

S&P Futures Jittery, Nasdaq Surge Continues Ahead Of Fed Decision

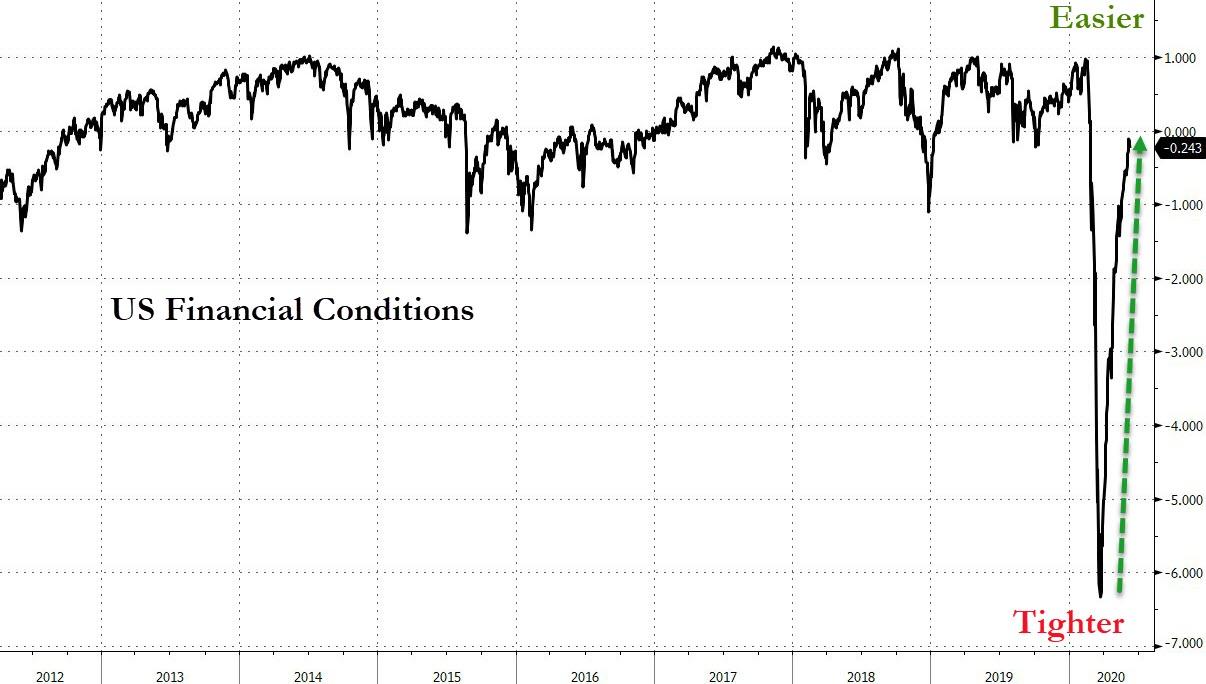

For the second night in a row, US equity futures peaked overnight then slumped around the time Europe opened, sliding along European stocks as investors were spooked by a grim economic forecast by the OECD (it is unclear why bad news isn’t good news in this case) ahead of what is expected to be another very dovish statement by the Fed, which pushed the dollar to the most oversold level since 2007.

The Fed will publish its first economic projections since the coronavirus pandemic set off a recession in February that ended a decade-long expansion. Investors will also look for any hints on yield curve control measures amid a recent surge in U.S. Treasury yields. Investors will be looking for reassurance on the central bank’s willingness to keep providing extraordinary support for the economy. Policy makers may also comment on potentially targeting yields for some Treasury maturities. Markets are balancing that with the OECD’s assessment that the economic hit from the pandemic may be deeper than anticipated.

The Fed is also expected to mark the first step away from a complete focus on crisis prevention towards more traditional goals of providing accommodation to support the recovery. As part of this, economists expect that the Fed will announce an open-ended QE program consistent with monthly Treasury purchases of between $65bn and $85bn, while the statement should slightly enhance the commitment to keep rates low by stating that the FOMC will keep rates at current levels until the economy is “close to achieving the Fed’s dual mandate goals of full employment and price stability”.

“Markets have been cautious before the Fed meeting and technical indicators are stretched after the recent powerful rally,” Credit Agricole strategist Jean-Francois Paren wrote in a client note. “For now, it sounds like yield-curve control is the necessary condition for markets to further rally, but it may not be sufficient by itself as it also highlights the fragility of the system we are now living in.”

Some speculate that the Fed may even step in to tame the insane retail investor froth that has gripped the market, but we find that unlikely.

Prospects of even more Fed stimulus, together with optimism about a rebound in the economy, have driven stocks higher in recent weeks, with the Nasdaq notching a record closing high for the second straight session on Tuesday and the S&P 500 ending about 5% below its all-time peak. Of course, the untouchable Nasdaq 100 futures traded in the green all morning, with Apple, Facebook and Amazon.com all rising about 0.5% in premarket trading. Meanwhile as the momentum-to-value rotation reverses, oil majors Exxon Mobil and Chevron dropped about 1.5% each, as oil prices weakened after a rise in U.S. crude inventories raised concerns of oversupply. AMC Entertainment Holdings rose about 4% after the world’s largest theater operator said it expected to reopen its theaters globally in July.

Shortly after 5am ET, Europe’s STOXX 600 Europe turned negative after climbing as much as 0.9% earlier, with travel and leisure and automakers leading losses among sectors. The Index dropped 0.1%, poised for the third consecutive session of declines. Sub-index tracking travel and leisure shares falls 1.3%, automakers down 1%. On the opposite end, personal and household goods advance 0.6%.

Earlier in the session, Asian stocks gained, led by health care and communications, after rising in the last session. Markets in the region were mixed, with Taiwan’s Taiex Index and India’s S&P BSE Sensex Index rising, and Jakarta Composite and Shanghai Composite falling. The Topix declined 0.2%, with Land Co and Besterra falling the most. The Shanghai Composite Index retreated 0.4%, with Shanghai Fengyuzhu Culture and Technology Co Ltd and Beijing Wantai Biological Pharmacy Enterprise posting the biggest slides.

In rates, Treasury futures traded near highs of the day in early US session as stock futures pare gains; the long end was leading, continuing this week’s bull-flattening trend ahead of the FOMC decision, with futures volume about 60% of the 5-day average. Yields are lower by 1bp to 3bp across the curve with 2s10s flatter by 2bp, 5s30s by 0.5bp; 10-year yields richer by 3bp at 0.795%, with bunds cheaper by 2bp ahead of expected syndicated 30- and 20-year deals from Germany and Finland.

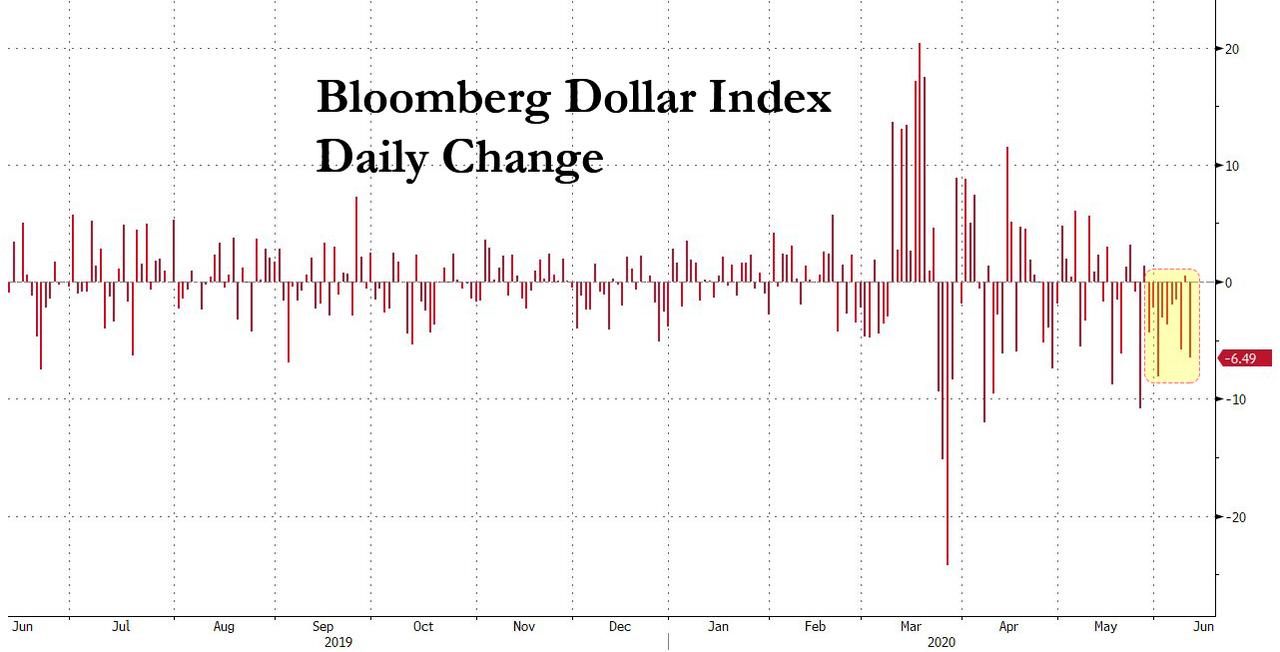

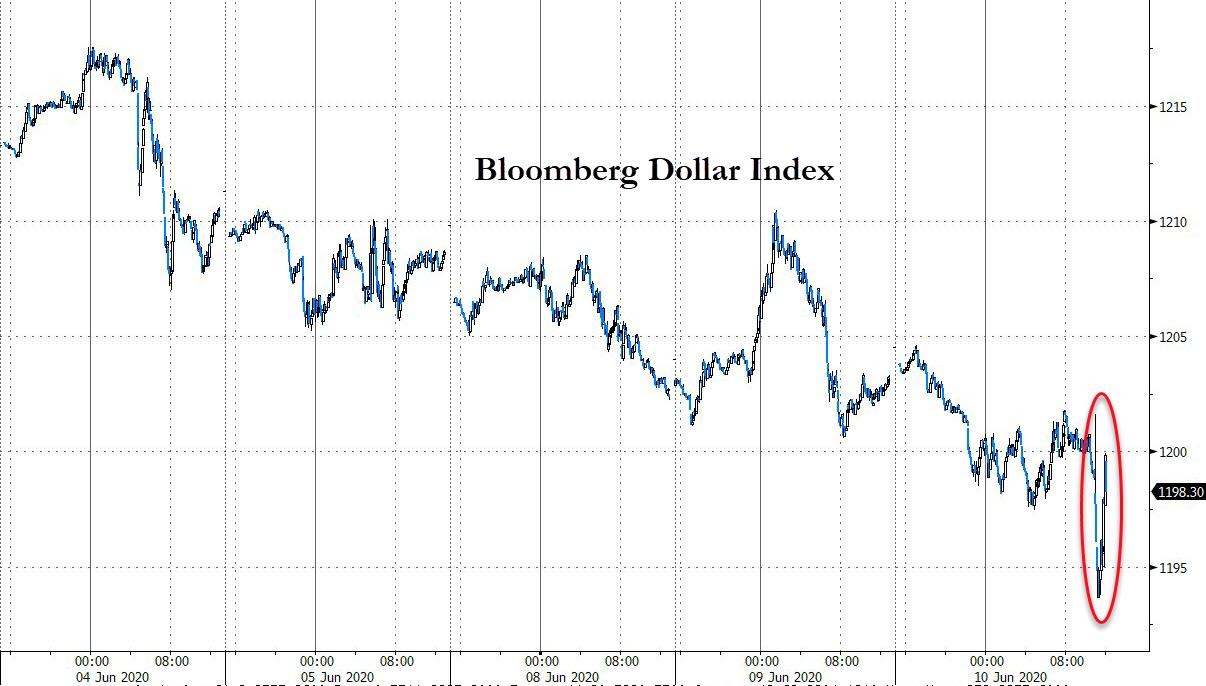

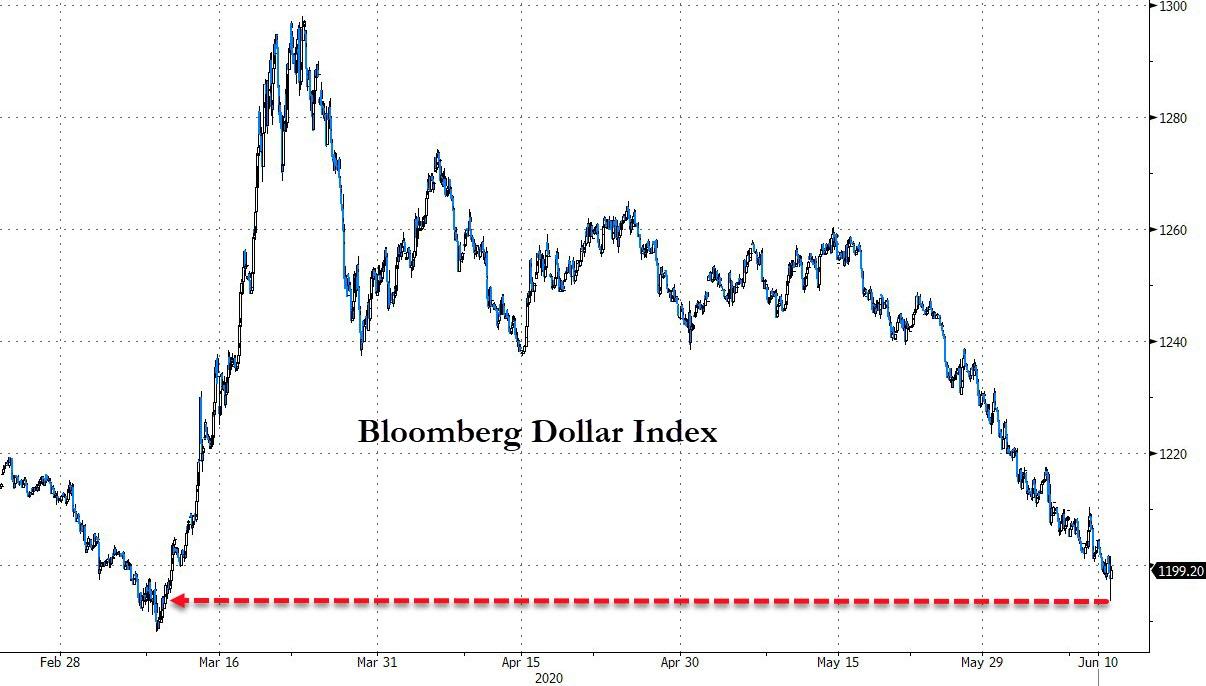

In FX, the dollar resumed its recent decline, dropping to the most oversold level since 2007. The Bloomberg Dollar Spot Index fell to a three-month low and the greenback slumped against all of its Group-of-10 peers ahead of the Federal Reserve’s policy meeting.

The euro resumed its March toward $1.14; the Bund curve bull flattened modestly as bunds underperformed Treasuries. The pound continued its lengthy ascent over the dollar thanks to a broad improvement in risk sentiment and plans to raise the pace of reopening the U.K. economy, while short-covering pushed it to modest gains on the euro. The Aussie rose and the yen was set for its biggest three- day gain since March against the dollar into the FOMC meeting.

WTI and Brent futures remain subdued in early mid-week trade as sentiment across the market erodes alongside a number of bearish narratives for the complex. Yesterday’s EIA STEO report cut 2020 world oil demand growth forecast by 120k BPD to 8.34mln BPD but noted it sees US crude output declining 670k BPD (vs. Prev. 540k BPD) this year. In-fitting with the global 2020 contraction viewpoint, OECD forecasts a 2020 contraction of 6.0%, whilst the scenario with a second wave sees global GDP -11.5%. Elsewhere, the weekly Private Inventory data also proved to add to the bearish bias with the headline having printed a surprise build of 8.4mln barrels vs.

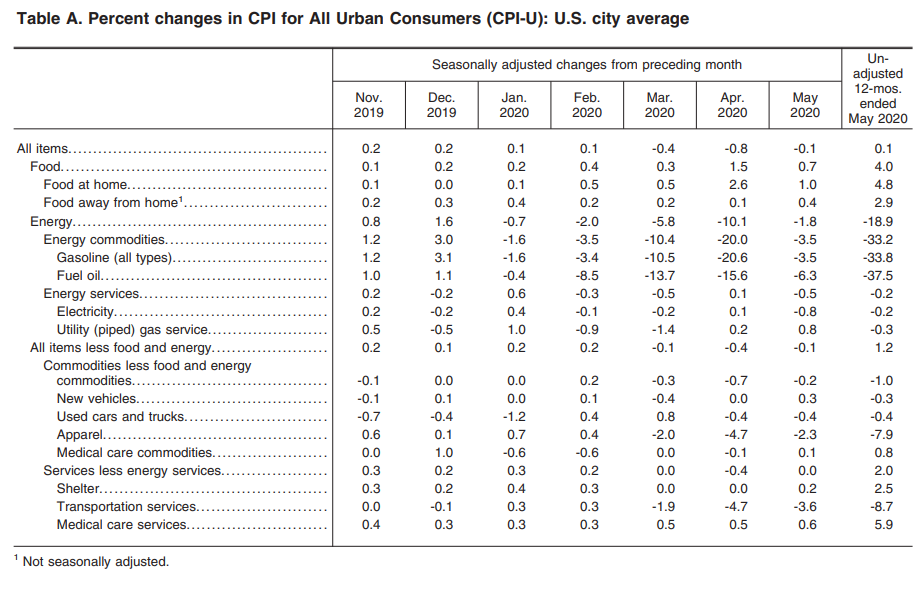

Looking at the day ahead, the highlight is the aforementioned Fed decision. Otherwise, data releases include the US CPI reading for May and French industrial production for April. We’ll also hear from the ECB’s de Guindos, Schnabel, Muller and Knot, while the OECD will also be publishing their Economic Outlook.

Market Snapshot

- S&P 500 futures up 0.5% to 3,221.00

- STOXX Europe 600 up 0.6% to 371.62

- MXAP up 0.4% to 162.10

- MXAPJ up 0.5% to 521.14

- Nikkei up 0.2% to 23,124.95

- Topix down 0.2% to 1,624.71

- Hang Seng Index down 0.03% to 25,049.73

- Shanghai Composite down 0.4% to 2,943.75

- Sensex up 0.7% to 34,183.19

- Australia S&P/ASX 200 up 0.06% to 6,148.43

- Kospi up 0.3% to 2,195.69

- German 10Y yield fell 1.0 bps to -0.319%

- Euro up 0.3% to $1.1372

- Brent Futures down 1.6% to $40.52/bbl

- Italian 10Y yield rose 13.8 bps to 1.372%

- Spanish 10Y yield rose 0.9 bps to 0.646%

- Brent Futures down 1.6% to $40.52/bbl

- Gold spot up 0.3% to $1,720.21

- U.S. Dollar Index down 0.3% to 96.08

Top Overnight News

- Investors are waiting to see if Fed officials discuss a possible return to the 1940s-era policy of yield-curve control

- The top U.S. specilaist in infectious diseases called the coronavirus pandemic his “worst nightmare” and warned that the deadly outbreak is far from over

- The ECB’s first three-month dollar swap allotment for $75.8 billion is set to mature on Thursday, making Wednesday’s operation the time to rollover. This accounts for over half of the total outstanding ECB swap lines

- U.K. Chancellor of the Exchequer Rishi Sunak is being asked by members of the ruling Conservative party to take decades to pay off the record debt the country is racking up as it tries to weather the coronavirus pandemic

- The global iron ore market may flip to a deficit if a virus-driven mine halt in Brazil persists and prices are now “on a knife edge,” UBS Group AG said in a warning that reflects a rising tide of concern over the suspension’s potential implications. Futures held above $100 a ton

- China’s factory deflation deepened in May and consumer price gains slowed, signaling that the recovery isn’t yet strong enough to produce inflation pressures

Asian equity markets traded somewhat indecisively after the mostly negative lead from global peers amid cautiousness heading into the FOMC, which saw all major indices on Wall St stall aside from the Nasdaq as tech resilience boosted it briefly above the historic 10K milestone. ASX 200 (+0.1) declined at the open with Australia dragged by weakness in financials and energy but with the losses gradually pared amid gains in defensives and improved consumer sentiment, while Nikkei 225 (+0.1%) was also initially pressured due to a firmer currency and larger than expected contraction in Machine Orders before staging a rebound to take back the 23K level. Hang Seng (U/C) and Shanghai Comp. (-0.4%) were varied with Hong Kong lifted at the open after the government’s bailout of Cathay Pacific which saw the airline’s shares take-off at the open, while the mainland lagged from the get-go as participants digested a somewhat tepid PBoC liquidity operation and softer than expected Chinese inflation data. Furthermore, tensions also lingered in the background as the Global Times suggested China could restrict the use of Qualcomm chips in government entities and key sectors related to national security, while it may also conduct anti-monopoly investigations and impose tariffs on US firms. Finally, 10yr JGBs were choppy around 152.00 amid similar indecision seen in the regional stock markets and with prices failing to benefit from today’s Rinban announcement in which the BoJ were present in the market for JPY 800bln of JGBs heavily concentrated in the belly.

Top Asian News

- Indonesian Stocks Slump Most in Five Weeks on Pandemic Concern

- Architect of Japan’s Virus Strategy Sees Flaw in West’s Approach

- China Protests Japan’s Plan For a G-7 Statement on Hong Kong

European equities have given up earlier gains and fall deeper into negative territory [Euro Stoxx 50 -0.8%] as stocks market failed to sustain the mostly positive APAC lead as players take some chips off the table ahead of some key risk events including the latest FOMC decision (full preview available on the newsquawk research suite) alongside the Eurogroup meeting later this week. News-flow has been light for the session but nonetheless bourses broadly post mild losses. Sectors are mostly in negative territory with more of an anti-cyclical bias and thus pointing to a more risk averse session. The detailed breakdown paints a picture in a similar vein and sees Travel & Leisure underperforming the region. In terms of individual movers, Spanish giant Inditex (+2.8%) erased earlier earning-induced downside of around 3% amid a jump in online sales. Commerzbank (+0.3%) holds its head above water but has waned off prior highs of c.3% which initially emanated from reports its second largest shareholder Cerberus (5% holding) demanded a fix-up of the group’s board. Shares thereafter drifted lower in tandem with yields. Elsewhere, Julius Baer (-1.5%) extended on losses amid reports the firm is facing another enforcement proceeding by FINMA over proper anti-money-laundering procedures.

Top European News

- Swedes Finally Learn Who Shot Their Prime Minister Olof Palme

- Frankie and Benny’s Owner to Close About 125 Restaurants

- KKR Considers Minority Investment in Italy’s Open Fiber: MF

In FX, the Dollar continues to depreciate amidst increasingly bearish price action as the index falls further from early June recovery highs in a declining pattern of daily ranges. Indeed, after a couple of attempts to revisit 97.000+ post-NFP peaks, the DXY has faded on each occasion, and the latest effort to bounce fell short of 96.500 to leave the index precarious above the round number below and eyeing the FOMC for fresh direction. However, Fed expectations do not suggest much in the way of a reprieve for the Greenback even though the aforementioned US jobs data was encouraging in terms of hopes for a relatively speedy rebound from the deep COVID-19 depths of unemployment, with the economic outlook still shrouded in uncertainty and hardly helped by violent protests or renewed global trade tensions. From a technical perspective, nearest support for the DXY comes in at 95.914 (March 11 low), while resistance remains at 97.069 (Monday’s apex) and the current range is 96.460-057.

- NZD/CHF/AUD – All vying for top G10 ranking, with the Kiwi firmly back above 0.6500 and not far from Tuesday’s best, while the Aussie is testing 0.7000 amidst reports of bids under the big figure from exporters and leverage accounts. Elsewhere, the Franc has forged more gains towards 0.9450 and 1.0750 vs the Euro, albeit still not cleanly or convincingly through the 200 DMA as the single currency maintains its bullish momentum against the Buck.

- JPY/GBP/EUR/CAD – The next best majors in descending order, with Usd/Jpy extending its marked retreat from circa 109.85 last Friday through more apparent supports, including the 30 DMA (107.54) to expose the only real downside chart level left before 107.00, at 107.09 (May 29 reaction low). Similarly, if Cable can sustain a break above Fib resistance around 1.2778 then 1.2800 beckons ahead of 1.2849 (March 12 high) and a more meaningful technical trendline at 1.2860, while Eur/Usd is inching closer to its post-NFP pinnacle (1.1384), but may find 1.1400 protected by decent option expiry interest between 1.1390-95 (1.2 bn). Turning to Usd/Cad, 1.3400 is still proving pivotal as crude prices consolidate off post-OPEC+ peaks and the pair looks to US CPI data before the Fed for additional impetus in the absence of anything scheduled on the Canadian front.

- SCANDI/EM – Waning risk sentiment and softer oil has thwarted another sub-10.5000 Eur/Nok move aided by firmer than expected Norwegian inflation metrics, while Eur/Sek has bounced from just shy of 10.4100 following further declines in Swedish household consumption and awaiting commentary from Riksbank Governor Ingves. Conversely, ongoing Dollar weakness has kept the HKMA active in defence of the currency peg and the Turkish Lira has derived traction from closer FX position monitoring by the CBRT rather than a fall in the jobless rate.

In commodities, WTI and Brent futures remain subdued in early mid-week trade as sentiment across the market erodes alongside a number of bearish narratives for the complex. Yesterday’s EIA STEO report cut 2020 world oil demand growth forecast by 120k BPD to 8.34mln BPD but noted it sees US crude output declining 670k BPD (vs. Prev. 540k BPD) this year. In-fitting with the global 2020 contraction viewpoint, OECD forecasts a 2020 contraction of 6.0%, whilst the scenario with a second wave sees global GDP -11.5%. Elsewhere, the weekly Private Inventory data also proved to add to the bearish bias with the headline having printed a surprise build of 8.4mln barrels vs. Expectations for a draw of 1.7mln. Meanwhile in Libya, production at the El-Sharara oil field (300k BPD) was reportedly shut-off again and the NOC later confirmed the continuation of a force majeure at the Sharara oil field. WTI July extends losses below USD 38/bbl (vs. high) and Brent August moves in tandem below USD 40.50/bbl (vs. high) as traders await the weekly EIA inventory data ahead of the FOMC rate decision. In terms of metals, spot gold ekes mild gains amid the risk-reversal from the APAC session coupled with a softer USD, but price action remains somewhat muted in anticipation of the Fed policy decision. Copper prices are underpinned by a weaker USD despite the deteriorating sentiment – Shanghai copper rose to near 20-week highs amid strong demand from China. Dalian iron meanwhile failed to benefit from the China demand as rising shipments from miners pressure prices.

US Event Calendar

- 8:30am: US CPI Ex Food and Energy MoM, est. 0.0%, prior -0.4%; CPI Ex Food and Energy YoY, est. 1.3%, prior 1.4%