GOLD:$1715.10 UP $16.00 The quote is London spot price

Silver:$17.64 DOWN 6 CENTS//LONDON SPOT PRICE

Closing access prices: London spot

i)Gold : $1716.00 LONDON SPOT 4:30 pm

ii)SILVER: $17.58//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUG GOLD: $1722.10 CLOSE 1.30 PM// SPREAD SPOT (LONDON) VS/FUTURE JUNE: $+7.00

CLOSING SILVER FUTURE MONTH

JULY: 1:30 PM: $17.81//1:30 PM //SPREAD SPOT LONDON VS FUTURE JULY: 17 CENTS PER OZ//

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2800. usa per oz

and silver; $31.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

DO NOT PAY ANY ATTENTION TO WHAT THE CROOKS ARE DOING AT THE COMEX AND LONDON LBMA..PHYSICAL IS THE NAME OF THE GAME AND NOTHING ELSE

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 272/352

ISSUED: 70

EXCHANGE: COMEX

CONTRACT: JUNE 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,698.300000000 USD

INTENT DATE: 06/08/2020 DELIVERY DATE: 06/10/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 7

072 H GOLDMAN 34

099 H DB AG 50

118 H MACQUARIE FUT 8

152 C DORMAN TRADING 9

190 H BMO CAPITAL 4

323 H HSBC 1

355 C CREDIT SUISSE 78 4

357 C WEDBUSH 9

624 C BOFA SECURITIES 3

657 C MORGAN STANLEY 3 11

657 H MORGAN STANLEY 46

661 C JP MORGAN 70 248

661 H JP MORGAN 24

686 C INTL FCSTONE 50

690 C ABN AMRO 27 5

737 C ADVANTAGE 7

800 C MAREX SPEC 3 3

____________________________________________________________________________________________

TOTAL: 352 352

MONTH TO DATE: 47,475

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT: 352 NOTICE(S) FOR 35,200 OZ (1.0948 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 47,475 NOTICES FOR 4,747,500 OZ (147.667 TONNES)

SILVER

FOR JUNE

14 NOTICE(S) FILED TODAY FOR 70,000 OZ/

total number of notices filed so far this month: 418 for 2,090,000 oz

BITCOIN MORNING QUOTE $9734 DOWN $49

BITCOIN AFTERNOON QUOTE.: $9708 DOWN 73

GLD AND SLV INVENTORIES:

WITH GOLD UP $16.00 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

TODAY WE HAD A HUGE WITHDRAWAL OF 2.63 TONNES OF GOLD FROM THE GLD//

GLD: 1,125.48 TONNES OF GOLD//

WITH SILVER DOWN 6 CENTS TODAY: AND WITH NO SILVER AROUND

A HUGE DEPOSIT OF 2.605 MILLION OZ INTO THE SLV

RESTING SLV INVENTORY TONIGHT:

SLV: 472.849 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A STRONG SIZED 2220 CONTRACTS FROM 169,232 UP TO 171,452 AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE STRONG SIZED GAIN IN OI OCCURRED WITH OUR HUGE 36 CENT GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS DUE TO STRONG BANKER SHORT COVERING PLUS A SMALL EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A GOOD INCREASE IN SILVER OZ STANDING AT THE COMEX FOR JUNE. WE HAD A NET GAIN IN OUR TWO EXCHANGES OF 2441 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUMONGOUS AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: MAY: 0 AND JULY: 225 AND SEPT 0 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 225 CONTRACTS. WITH THE TRANSFER OF 225 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 225 EFP CONTRACTS TRANSLATES INTO 1.125 MILLION OZ ACCOMPANYING:

1.THE 36 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.145 MILLION OF INITIALLY STANDING FOR JUNE

MONDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 36 CENTS).. AND,OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS. THE CONSIDERABLE GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A GOOD INCREASE IN SILVER OZ STANDING FOR JUNE,3) CONSIDERABLE BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A STRONG NET GAIN OF 2441 CONTRACTS OR 12.205 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

SPREADING OPERATIONS

OUR SPREADING OPERATION HAS NOW SWITCHED INTO SILVER…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN SILVER AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JULY.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF JUNE. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

JUNE

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF JUNE:

3732 CONTRACTS (FOR 8 TRADING DAY(S) TOTAL 3732 CONTRACTS) OR 18.660 MILLION OZ: (AVERAGE PER DAY: 467 CONTRACTS OR 2.335 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 18.660 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 2.66% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,084.60 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP SO FAR 18.660 MILLION OZ.

EXCHANGE FOR PHYSICAL ISSUANCE FOR THE PAST 60 DAYS IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD AN EXTREMELY LARGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2220, WITH OUR STRONG 36 CENT GAIN IN SILVER PRICING AT THE COMEX ///FRIDAY… THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 225 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE LOST A STRONG SIZED OI CONTRACTS ON THE TWO EXCHANGES: 2445 CONTRACTS (WITH OUR 36 CENT GAIN IN PRICE)

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 225 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A LARGE SIZED INCREASE OF 2,220 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED DESPITE A HUGE 36 CENT LOSS IN PRICE OF SILVER/AND A CLOSING PRICE OF $17.70 // MONDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.846 BILLION OZ TO BE EXACT or 121% of annual global silver production (ex Russia & ex China).

FOR THE NEW JUNE DELIVERY MONTH/ THEY FILED AT THE COMEX: 6 NOTICE(S) FOR 30,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.145 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A UNEXPECTED 1252 CONTRACTS TO 469,893 AND SLIGHTLY FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE CONSIDERABLE SIZED LOSS OF COMEX OI OCCURRED DESPITE OUR STRONG GAIN IN PRICE OF $18.70 /// COMEX GOLD TRADING// MONDAY// WE HAD STRONG BANKER SHORT COVERING,ANOTHER HUMONGOUS SIZED INCREASE IN GOLD OZ STANDING AT THE COMEX, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A SMALL EX. FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR STRONG GAIN IN PRICE OF $18.70 .

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 8

WE GAINED A TINY SIZED 163 CONTRACTS (0.506 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 1415 CONTRACTS:

CONTRACT JUNE 0.; AUG 1415 AND ALL OTHER MONTHS ZERO//TOTAL: 1415. The NEW COMEX OI for the gold complex rests at 469,893. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A TINY SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 163 CONTRACTS: 1252 CONTRACTS DECREASED AT THE COMEX AND 1415 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 163 CONTRACTS OR 0.506 TONNES. MONDAY, WE HAD A STRONG GAIN OF $18.70 IN GOLD TRADING……

AND WITH THAT GAIN IN PRICE, WE HAD A SMALL SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 0.505 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $18.70).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS UNSUCCESSFUL (SEE BELOW).

4 GC VOLUME: 0 // open interest 8

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1415) ACCOMPANYING THE CONSIDERABLE SIZED LOSS IN COMEX OI (1252 OI): TOTAL GAIN IN THE TWO EXCHANGES: 163 CONTRACTS. WE NO DOUBT HAD 1 )CONSIDERABLE BANKER SHORT COVERING, 2.)ANOTHER HUMONGOUS INCREASE IN GOLD OUNCES STANDING AT THE GOLD COMEX FOR THE FRONT JUNE MONTH, 3) ZERO LONG LIQUIDATION; 4) CONSIDERABLE COMEX OI LOSS.. AND …ALL OF THIS WAS COUPLED WITH OUR STRONG GAIN IN GOLD PRICE TRADING//MONDAY//$18.70.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

JUNE

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES: 62.86 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 62.86/3550 x 100% TONNES =1.77% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 2879.97 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 62.86 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 2220 CONTRACTS FROM 169,232 UP TO 171,452 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE STRONG GAIN IN OI SILVER COMEX WAS DUE TO; 1) CONSIDERABLE BANKER SHORT COVERING , 2) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A GOOD INCREASE IN SILVER OZ STANDING AT THE COMEX FOR JUNE AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 225 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY: 727 CONTRACTS AND SEPT: 14 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 225 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2220 CONTRACTS TO THE 225 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 2445 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 12.225 MILLION OZ!!! OCCURRED WITH THE 36 CENT gain IN PRICE///

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 36 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// MONDAY. WE ALSO HAD A SMALL SIZED 225 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 18.54 POINTS OR 0.62% //Hang Sang CLOSED UP 280.45 POINTS OR 1.13% /The Nikkei closed DOWN 87.07 POINTS OR 0.38%//Australia’s all ordinaires CLOSED UP 2.39%

/Chinese yuan (ONSHORE) closed DOWN at 7.0857 /Oil DOWN TO 38.19 dollars per barrel for WTI and 40.65 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0857 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0803 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

i)we had 2 deposits into the customer account

into JPMorgan: 0

ii)into Scotia 232,913.700 oz

III) Into CNT: 55,372.980 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.819 million oz of total silver inventory or 51.22% of all official comex silver. (160.819 million/314.220 million

total customer deposits today: 288,286.680 oz

we had 1 withdrawals:

i) Out of CNT 768,141.159 oz

ii) Out of Delaware: 8042.51 oz

total withdrawals; 776,183.669 oz

We had 0 adjustments

total dealer silver: 85.401 million

total dealer + customer silver: 314.106 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The total number of notices filed today for the JUNE 2020. contract month is represented by 14 contract(s) FOR 70,000 oz

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 418 x 5,000 oz = 2,090,,000 oz to which we add the difference between the open interest for the front month of JUNE.(25) and the number of notices served upon today 14 x (5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JUNE/2019 contract month: 418 (notices served so far) x 5000 oz + OI for front month of JUNE (25)- number of notices served upon today 14) x 5000 oz of silver standing for the JUNE contract month.equals 2,145,000 oz.

We GAINED 12 contracts or an additional 60,000 oz will stand for delivery as they refused to morphed into London based forwards as well as negating a fiat bonus

TODAY’S ESTIMATED SILVER VOLUME: 69,324 CONTRACTS // volume low/

FOR YESTERDAY: 89,834..,CONFIRMED VOLUME//volume good/

YESTERDAY’S CONFIRMED VOLUME OF 89,834 CONTRACTS EQUATES to 449 million OZ 64.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO- 0.54% ((JUNE 9/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.72% to NAV: (JUNE 9/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 0.54%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 16.33 TRADING 16.22///NEGATIVE 0.54

END

And now the Gold inventory at the GLD/

JUNE 9//WITH GOLD UP $16.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 2.63 TONNES OF GOLD AT THE GLD//INVENTORY RESTS AT 1125.48 TONNES

JUNE 8//WITH GOLD UP $18.70 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 4.10 TONNES AT THE GLD//INVENTORY RESTS AT 1128.11 TONNES

JUNE 5//WITH GOLD DOWN $40.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A PAPER WITHDRAWAL OF 1.16 TONNES OUT OF THE GLD//INVENTORY RESTS AT 1132.21 TONNES

JUNE 4//WITH GOLD UP $20.60: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD…A DEPOSIT OF 4.09 TONNES INTO THE GLD//INVENTORY RESTS AT 1133.37 TONNES

JUNE 3//WITH GOLD DOWN $26.15//A SMALL CHANGE IN GOLD INVENTORY//A DEPOSIT OF 0.78 TONNES OF GLD INTO THE GLD//INVENTORY RESTS AT 1129.28 TONNES

JUNE 2//WITH GOLD DOWN $11.20 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1128.40 TONNES

JUNE 1//WITH GOLD UP $1.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES OF GOLD//GLD INVENTORY RESTS TONIGHT AT 1123.14 TONNES

MAY 29/WITH GOLD UP $19.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///GLD INVENTORY RESTS THIS WEEKEND AT 1119.05 TONNES

MAY 28//WITH GOLD UP $4.00 TODAY/NO CHANGES IN GOLD INVENTORY TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

MAY 27/WITH GOLD UP $.10 TODAY: A STRONG 2.34 TONNES OF GOLD ADDED TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

MAY 26//WITH GOLD DOWN $23.05//NO CHANGES IN GOLD INVENTORY://RESTS TONIGHT AT 1116.71 TONNES

MAY 22//WITH GOLD UP $13.05//A BIG CHANGE IN GOLD INVENTORY:: A PAPER ADDITION OF 3.93 TONNES//INVENTORY RESTS THIS WEEKEND AT: 1116.71 TONNES

MAY 21//WITH GOLD DOWN $26.70//NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1112.32 TONNES

MAY 20/WITH GOLD UP $7.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 1.46 TONNES FROM THE GLD////INVENTORY RESTS TONIGHT AT 1112.32 TONNES

MAY 19//WITH GOLD UP $10.60//NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1113.78 TONNES

MAY 18/WITH GOLD DOWN $15.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A PAPER DEPOSIT OF 9.06 TONNES./INVENTORY RESTS AT 1113.78 TONNES

MAY 15.WITH GOLD UP $16.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 12.58 TONNES/ INVENTORY RESTS AT 1104.72 TONNES

MAY 14//WITH GOLD UP $19.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1092.14 TONNES

MAY 13//WITH GOLD UP $9.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 11.07 TONNES/INVENTORY RESTS AT 1092.14 TONNES

MAY 12//WITH GOLD UP $6.60 TODAY; A SMALL CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 1081.07 TONNES

MAY 11/WITH GOLD DOWN $12.65 TODAY: NO CHANGES IN GOLD INVENTORY: //INVENTORY RESTS AT 1081.65 TONES..

MAY 8/WITH GOLD DOWN $7.00 TODAY; A BIG CHANGE IN GOLD INVENTORY: A PAPER ADDITION OF 5.85 TONNES/INVENTORY RESTS AT 1081.65 TONNES

MAY 7/WITH GOLD UP $29.65 TODAY : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER ADDITION OF .41 TONNES/INVENTORY RESTS AT 1075.80 TONNES

MAY 6//WITH GOLD DOWN $17.00 TODAY/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER ADDITION OF 3.68 TONNES/INVENTORY RESTS AT 1075.39 TONES

MAY 5/WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER ADDITION OF 3.81 TONNES//INVENTORY RESTS AT 1071.71 TONNES

MAY 4//WITH GOLD UP $12.00 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE PAPER DEPOSIT OF 11.4 TONNES INTO THE GLD////GOLD INVENTORY RESTS AT 1067.90 TONNES

MAY 1/WITH GOLD UP $8.45 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1056.50 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

JUNE 9/ GLD INVENTORY 1125.48 tonnes*

LAST; 837 TRADING DAYS: +180.56 NET TONNES HAVE BEEN REMOVED FROM THE GLD

LAST 737 TRADING DAYS://+355.74 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JUNE 9/WITH SILVER DOWN 6 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.605 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 422.849 MILLION OZ//

JUNE 8/WITH SILVER UP 36 CENTS TODAY: TWO HUGE WITHDRAWALS OF 932,000 MILLION OZ AND 1.491 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 470.240 MILLION OZ//

JUNE 5/WITH SILVER DOWN 46 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 648,000 OZ FROM THE SLV////INVENTORY RESTS AT 472.663 MILLION OZ

JUNE 4//WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV.//INVENTORY RESTS AT 473.315 MILLION OZ//

JUNE 3//WITH SILVER DOWN 23 CENTS TODAY//NO CHANGES IN SILVER INVENTORY AT THE SLV//

INVENTORY RESTS AT 473.315 MILLION OZ//

JUNE 2//WITH SILVER DOWN 31 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUMONGOUS 6.686 MILLION OZ ADDED TO THE SLV////INVENTORY RESTS TONIGHT AT 473.315 MILLION OZ//

JUNE 1//WITH SILVER UP 38 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.56 MILLION OZ INTO THE SLV////INVENTORY RESTS TONIGHT AT 466.629 MILLION OZ//

MAY 29//WITH SILVER UP 52 CENTS TODAY: A MASSIVE DEPOSIT OF 2.796 MILLION OZ INTO THE SLV//INVENTORY RESTS THIS WEEKEND AT 463.273 MILLION OZ//

MAY 28//WITH SILVER UP 9 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.660 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 460.477 MILLION OZ//

MAY 27/WITH SILVER UP 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 455.817 MILLION OZ//

MAY 26//WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/// INVENTORY RESTS AT 455.817 MILLION OZ//

MAY 22/WITH SILVER UP 22 CENTS TODAY/ A HUGE PAPER WITHDRAWAL OF 1.864 MILLION OZ//INVENTORY RESTS AT 455.817 MILLION OZ/

LAST 5 DAYS: SILVER UP 60 CENTS: INVENTORY UP A WHOOPING 23.767 MILLION OZ///

MAY 21/WITH SILVER DOWN 50 CENTS TODAY: A HUGE PAPER DEPOSIT OF 7.923 MILLION OZ///INVENTORY RESTS AT 457.681 MILLION OZ//

MAY 20//WITH SILVER UP ANOTHER 11 CENTS TODAY: A HUGE CHANGE IN SLV INVENTORY: A HUGE PAPER DEPOSIT OF 9.601 MILLION OZ INTO THE SLV// //INVENTORY RESTS AT 449.758 MILLION OZ

MAY 19/WITH SILVER UP ANOTHER 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 440.157 MILLION OZ//

MAY 18/WITH SILVER UP ANOTHER 48 CENTS TODAY: TWO BIG CHANGES IN SILVER INVENTORY AT THE SLV I.E. 2 PAPER DEPOSIT OF ( I) 8.39 MILLION OZ AND THEN ( 2) 8.109 MILLION OZ//INVENTORY RESTS AT 432.048 MILLION OZ// (TOTAL DEPOSITS 16.500 MILLION OZ///)

MAY 15/WITH SILVER UP 81 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV: /INVENTORY RESTS AT 423.65 MILLION OZ.

MAY 14//WITH SILVER UP 33 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV.//INVENTORY RESTS AT 423.65 MILLION OZ

MAY 13/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.79 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 423.65 MILLION OZ//

MAY 12/WITH SILVER UP 5 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.076 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 420.861 MILLION OZ//

MAY 11.WITH SILVER DOWN 5 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 417.785 MILLION OZ//

MAY 8/WITH SILVER UP 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTER DEPOSIT OF 4.661 MILLION OZ OF SILVER INTO THE SLV..///INVENTORY RESTS AT 417.785 MILLION OZ//

MAY 7/WITH SILVER UP 45 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 5/WITH SILVER UP 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.124 MILLION OZ///

MAY 4//WITH SILVER DOWN 5 CENTS TODAY:2 HUGE PAPER CHANGES IN SILVER INVENTORY AT THE SLV.i).A LARGE 1.399 MILLION OZ OF PAPER SILVER REMOVED FROM THE SLV//..//INVENTORY RESTS AT 411.427 MILLION OZ and ii) A LARGE 1.647 MILLION OZ OF PAPER SILVER ADDED TO THE SLV// INVENTORY RESTS AT 413.124 MILLION OZ//

MAY 1/WITH SILVER FLAT IN PRICE: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 412.826 MILLION OZ///

JUNE 9.2020:

SLV INVENTORY RESTS TONIGHT AT

472.849 MILLION OZ.

END

LIBOR SCHEDULE AND GOFO RATES// GOLD LEASE RATES

YOUR DATA…..

6 Month MM GOFO 2.34/ and libor 6 month duration 0.48

Indicative gold forward offer rate for a 6 month duration/calculation:

GOLD LENDING RATE: -1.86%

NEGATIVE GOLD LEASING RATES INCREASING BY A HUGE AMOUNT//GOLD SCARCITY AND CENTRAL BANKS CALLING IN ALL OF THEIR GOLD LEASES

XXXXXXXX

12 Month MM GOFO

+ 2.06%

LIBOR FOR 12 MONTH DURATION: 0.63

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -1.43%

NEGATIVE GOLD LEASING RATES INCREASING BY A HUGE AMOUNT//GOLD SCARCITY AND CENTRAL BANKS CALLING IN ALL OF THEIR GOLD LEASES

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

USAGold’s ‘News & Views’: Inflation may not be dead; gold demand strong

Submitted by cpowell on Mon, 2020-06-08 14:24. Section: Daily Dispatches

10:25a ET Monday, June 8, 2020

Dear Friend of GATA and Gold:

USAGold’s June “News & Views” newsletter challenges the prevailing market opinion that deflation will be ruling the world and that inflation is finished.

The letter also notes that gold demand is strong among financial institutions, central banks, and individual investors, and that the monetary metals have performed better than the Dow Jones Industrial Average so far this year.

USAGold’s June “News & Views” letter is posted in the clear here:

https://www.usagold.com/cpmforum/nv1019june2020/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Stephen Roach now is banging the table that the crash on the dollar is coming

(Bloomberg/Stephen Roach/GATA)

Stephen Roach: A crash in the dollar is coming

Submitted by cpowell on Tue, 2020-06-09 04:21. Section: Daily Dispatches

The author is an economist, senior fellow at Yale University’s Jackson Institute for Global Affairs, and a senior lecturer at the Yale School of Management. He was formerly chairman of Morgan Stanley Asia and chief economist at Morgan Stanley, the New York-based investment bank.

* * *

By Stephen Roach

Bloomberg News

Monday, June 8, 2020

The era of the U.S. dollar’s “exorbitant privilege” as the world’s primary reserve currency is coming to an end. In the 1960s French Finance Minister Valery Giscard d’Estaing coined that phrase largely out of frustration, bemoaning a United States that drew freely on the rest of the world to support its overextended standard of living.

For almost 60 years, the world complained but did nothing about it. Those days are over.

already stressed by the impact of the Covid-19 pandemic, U.S. living standards are about to be squeezed as never before. At the same time, the world is having serious doubts about the once widely accepted presumption of American exceptionalism.

Currencies set the equilibrium between these two forces — domestic economic fundamentals and foreign perceptions of a nation’s strength or weakness. The balance is shifting, and a crash in the dollar could well be in the offing. …

… For the remainder of the commentary:

https://www.bloomberg.com/opinion/articles/2020-06-08/a-crash-in-the-dol…

end

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

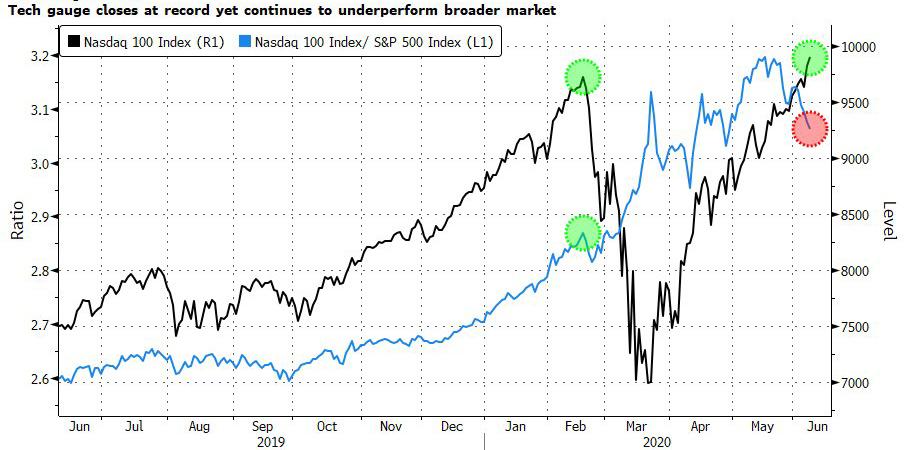

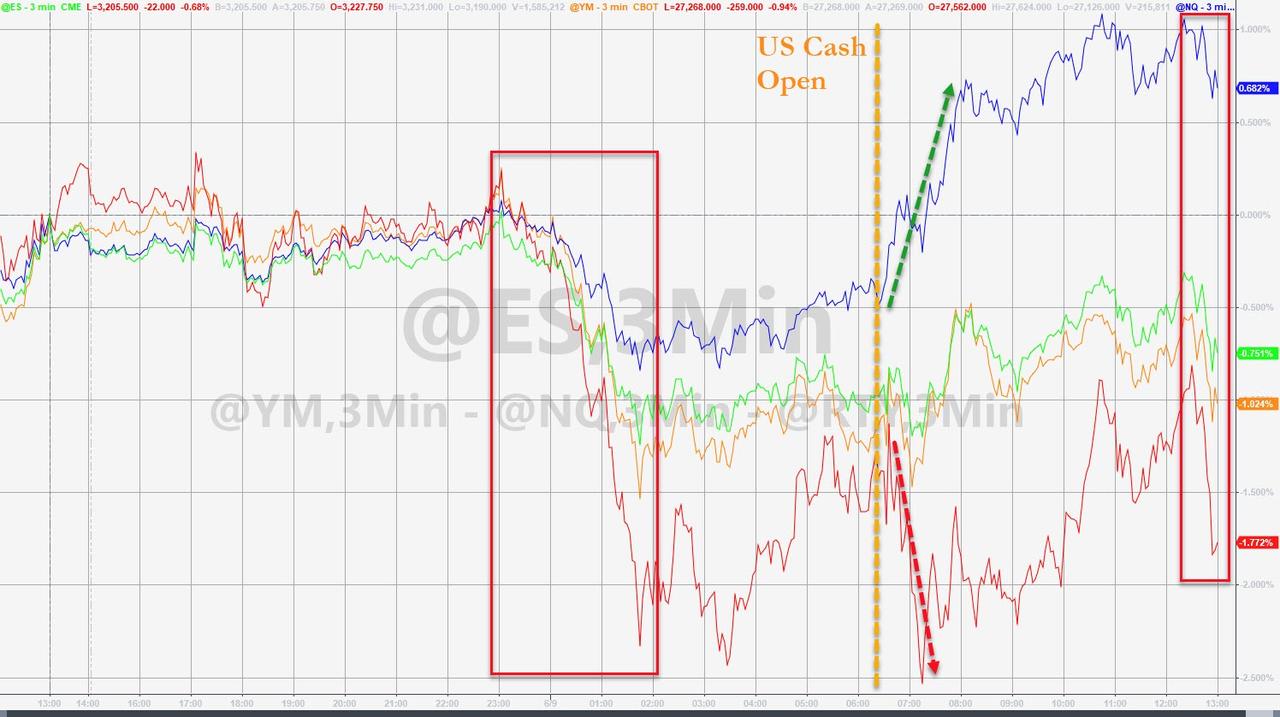

Futures Tumble As Historic Rally Fizzles; Treasurys, Dollar Jump

After hanging around at 3-month highs well into the overnight session, U.S. equity futures took a sharp leg lower around the time Europe opened, sliding back under 3,200 along with European stocks on worries that the historic rally in risk assets has overshot the economic recovery giving back some of the gains from the recent historic rally after the Nasdaq notched a record closing high in the previous session, with focus now on the Federal Reserve’s two-day policy meeting. Treasuries advanced with gold and the yen.

The drop comes one day after the Nasdaq hit a fresh record closing high on Monday, while the S&P 500, which is about 5% below its own all-time high, also erased its year-to-date losses.

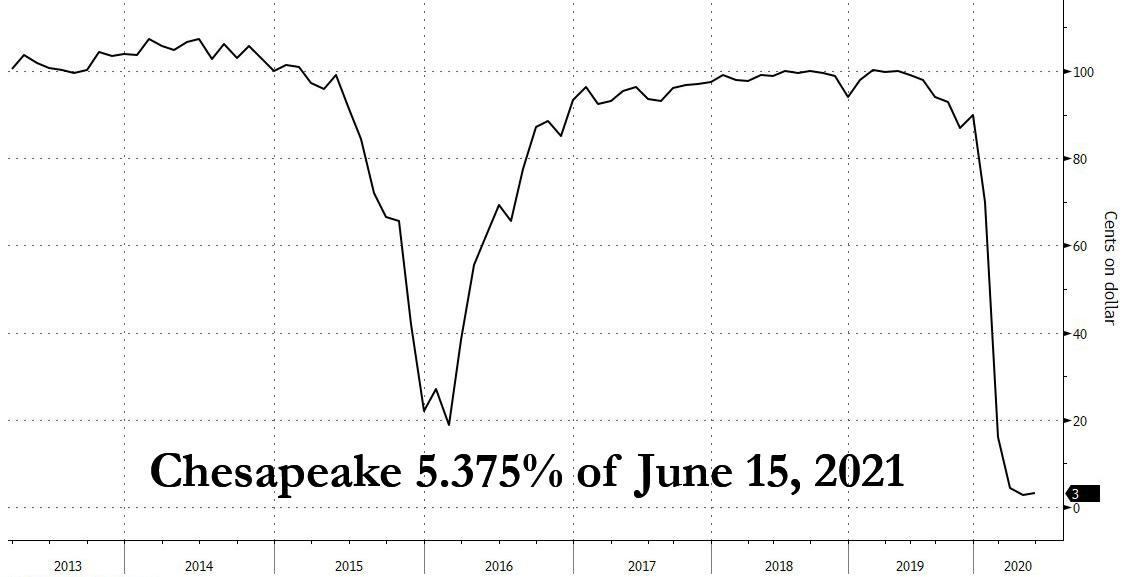

Declines in the U.S. premarket were broad, hitting many of the “value” stocks that had soared in recent days, ranging from cruise lines to oil drillers: American Airlines, United Airlines Holdings, Alaska Air and Marriott International all dropped between 4.5% and 9.0% in early trading after surging on Monday following another retail rush. Soon to be bankrupt Chesapeake tumbled by more than 50% following a Bloomberg reported it was preparing to file for Chapter 11; even bankrupt Hertz dropped and now sports a market cap of only $700 million or so. Macy’s rose 5.8% after raising $4.5 billion in financing, as it tries to navigate through the fallout from the COVID-19 pandemic.

In Europe, the Eurostoxx 50 dropped as much as 1.8%, with FTSE MIB and IBEX underperforming peers. The Stoxx 600 Banks Index slumped as much as 5.1% on Tuesday, the biggest drop in two months. Losses were broad, as cyclical sectors all dropped with banks, autos, oil and construction among the weakest sectors, while health care and food outperform. The decline comes after strong gains over the past two weeks that pushed the banking index up 24%.

Asian stocks gained, pushed higher by Monday’s US momentum, led by finance and consumer staples. Markets in the region were mixed, with Australia’s S&P/ASX 200 and Hong Kong’s Hang Seng Index rising, and Thailand’s SET and Jakarta Composite falling. The Topix declined 0.1%, with Asahi Broadcasting Group and Mynet falling the most. The Shanghai Composite Index rose 0.6%, with Chengdu B-Ray Media and Hangzhou Jiebai Group posting the biggest advances

As Bloomberg notes, “after a record-breaking rally that added $21 trillion to global stock markets, valuations look now stretched and technical indicators suggest a pullback is overdue. The World Bank warned the economy will contract the most since World War II this year, reducing incomes and sending millions of people into poverty in emerging and developing nations.”

“There are a lot of unknowns that we are dealing with despite the fact that normalizations of economic activities are still on track,” said Value Partners manager Frank Tsui. “There are still a lot of unknown factors.”

While no major policy announcements are expected when the U.S. central bank wraps up its meeting on Wednesday, policymakers will issue economic projections for the first time since December, before a decade-long economic expansion was brought to a grinding halt due to coronavirus-induced lockdowns. Last week’s strikingly strong employment data for May strengthened views that the worst of the economic fallout from the pandemic was over, and is also expected to be discussed at the meeting. On Monday, the Fed expanded its Main Street Lending Program, allowing more companies to participate and lessening the burden on banks that create the loans, confirming that America’s small businesses are getting crushed.

In rates, Treasuries jumped with yields falling 1-6 basis points across the curve, the 10Y sliding just above 0.80%, bull-flattening for second consecutive session. Cash volumes have been light, however, especially in long maturities. According to Bloomberg, the bull-flattening eroded profit in curve steepeners, a popular trade ahead of Wednesday’s FOMC meeting. Yields richer by 1bp to 7bp across the curve led by 20- and 30- year sectors, flattening 5s30s by 3.2bp and 2s10s by 3.5bp; 10- year yields lower by 4.4bp at ~0.83% with bunds, gilts both cheaper by around 4bp. Treasury auction cycle resumes with $29b 10-year reopening at 1pm ET, concludes with $19b 30-year reopening Thursday, with FOMC meeting intervening on Wednesday. A gauge of European junk-grade credit risk increased the most since April.

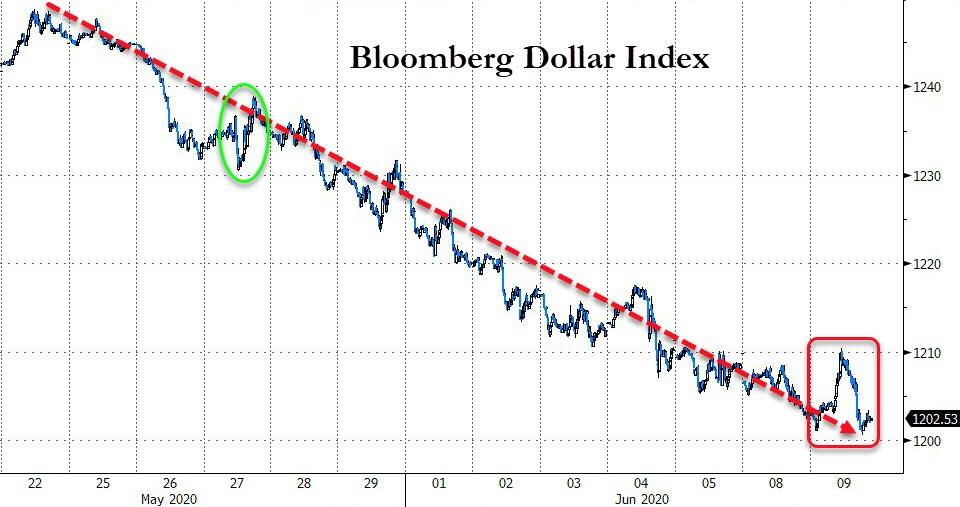

In FX, the dollar rose against a basket of currencies for the first time in nine days. The Bloomberg Dollar Spot Index ended its longest losing streak since 2011 as the greenback rose against most Group-of-10 peers ; the euro edged lower, to trade below 1.13 per euro dollar and bunds edged higher. The pound fell against the dollar after an eight-day winning streak for the currency looked to have taken it far enough, and wider risk appetite faded on global markets. Norway’s krone plunged as oil prices slumped. Japan’s currency rose against all its Group-of-10 peers and staged its biggest 2-day rally against the greenback in more than two months after a decline in stocks in Tokyo prompted traders to cover short yen positions. The Australian dollar swung to a deep loss against the greenback after climbing to the highest level this year, dragged lower by the yen’s surge.

In commodities, the energy complex continued to leak in the aftermath of the OPEC+ meeting as players question the enforcement (or not) of the agreed upon output cuts with laggards such as Iraq already hinting as difficulties on overcompliance. Further, some traders also cite a “buy the rumour, sell the fact” playbook given the rally in the complex heading into the meeting. Meanwhile, BP’s demand-driven job cuts yesterday added further weighed on prices. Elsewhere, in Libya, source reports noted that El-Sharara’s production has again been shuttered by armed men ordering employees to stop working – which comes just two days after the restart and lift of force majeure on exports (now reimposed), albeit the oilfield was only producing at a tenth of its 300k BPD full capacity – which was expected to be reached within 90 days

Expected data include wholesale inventories. Tiffany and Chewy are reporting earnings

Market Snapshot

- S&P 500 futures down 1% to 3,196.25

- STOXX Europe 600 down 1.2% to 369.75

- MXAP up 0.4% to 161.06

- MXAPJ up 0.5% to 517.26

- Nikkei down 0.4% to 23,091.03

- Topix down 0.1% to 1,628.43

- Hang Seng Index up 1.1% to 25,057.22

- Shanghai Composite up 0.6% to 2,956.11

- Sensex down 0.4% to 34,228.05

- Australia S&P/ASX 200 up 2.4% to 6,144.95

- Kospi up 0.2% to 2,188.92

- German 10Y yield fell 1.9 bps to -0.338%

- Euro down 0.4% to $1.1247

- Italian 10Y yield fell 0.7 bps to 1.234%

- Spanish 10Y yield rose 0.8 bps to 0.556%

- Brent futures down 1.8% to $40.07/bbl

- Gold spot up 0.5% to $1,706.57

- U.S. Dollar Index up 0.5% to 97.06

Top Overnight News from Bloomberg

- Demand for government bonds is showing no signs of letup, with Ireland securing record investor demand despite a host of countries, including the U.K., selling debt

- Prime Minister Boris Johnson will talk his cabinet through his plans for easing the U.K.’s lockdown on Tuesday after officials reported the lowest number of daily deaths since restrictions were imposed

- German exports plunged at a record pace in April when economies around the world shut down to contain the coronavirus

- French economic output will take two years to recover from the virus-related slump that that will inflict even longer lasting damage on the labor market, the country’s central bank said

- Deflation is back on the minds of European Central Bank officials, presaging battles for President Christine Lagarde over whether the euro zone needs yet more monetary stimulus.

- Japan’s famously low- yielding bonds hold surprising appeal for Australian investors, thanks to how cheap the yen is in funding markets. Investors holding Australian dollars can generate healthy returns on 10- year and 30-year JGBs using cross-currency basis swaps

The risk tone across the Asia-Pac region was mostly positive with the regional bourses spurred by the firm handover from Wall St where the DJIA led the respectable gains across the major indices and the Nasdaq printed a fresh record high as there wasn’t much to derail the ongoing reopening and recovery narrative. Furthermore, the S&P 500 turned positive YTD and all sectors closed in the green with substantial gains seen in energy names following the OPEC+ output cut extension, despite an actual pullback in oil prices that was attributed to participants selling the news and concerns regarding compliance issues. ASX 200 (+2.4%) and Nikkei 225 (-0.4%) traded mixed with Australia the outperformer as it played catch up on return from the holiday closure and with gains spearheaded by financials and energy, while the Japanese benchmark lagged as exporters suffered from the ill effects of a stronger currency. The KOSPI (+0.2%) was subdued after North Korea announced to sever communication with South Korea completely from today and with index heavyweight Samsung Electronics failing to hold on to most the opening gains despite the court ruling to reject the arrest of de facto head Jay Y. Lee. Elsewhere, Hang Seng (+1.1%) climbed back above the 25k milestone with the government planning to bailout Cathay Pacific through a HKD 30bln loan and the Shanghai Comp. (+0.6%) conformed to the predominantly upbeat tone after the PBoC resumed its liquidity efforts, albeit with a reserved CNY 60bln injection. Finally, 10yr JGBs extended on this week’s rebound amid a similar recovery in USTs and underperformance of Japanese stocks, but with upside capped amid the lack of BoJ presence in the market today.

Top Asian News

- Japan Low-Yield Bonds Have Surprise Appeal for Aussie Funds

- China Urges Students to Assess Risks of Studying in Australia

- How Covid Upended 20 Million Lives in India’s Finance Hub

European stocks continue to deteriorate with downside exacerbated since the European cash open [Euro Stoxx 50 -2.0%] as investors side-line the recent Central bank/reopen-induced rally and fixate on the backdrop of skittish US-Sino rhetoric, potential second wave as lockdown measures ease and amid Western protests/riots. An argument could also be built for profit-taking at near pre-COVID highs ahead of immediate risk events such as the FOMC meeting and the Eurogroup summit. Sectors are mostly in the red with underperformance in energy and financials amid the deterioration in energy prices and yields, whilst broader sectors point to a more risk averse session and defensives fare better – particularly healthcare. The detailed breakdown paints a similar picture Travel & Leisure also bearing the brunt of risk aversion. In terms of individual movers, the session kicked off with the French aerospace sector significantly higher amid France unveiling a EUR 15bln package for the sector vs. Exp. EUR 10bln, albeit the likes of Airbus (-6.6%), Thales (-2.9%) and Safran (-3.5%) have since conformed to the broader risk tone. Meanwhile, British American Tobacco (-4.5%) extended on losses after trimming its FY guidance and pointing to low growth.

Top European News

- VW Board Infighting Rocks Carmaker Struggling With Virus Crisis

- Deflation Fears at ECB Mean Stimulus Battles Ahead for Lagarde

- Ireland Gets Record 50 Billion Euros of Orders in Bond Sale

- SocGen Signals Mixed Second Quarter as Tough Market Endures

In FX, not the biggest G10 move today, but Usd/Jpy has now reversed in excess of 2 big figures from post-NFP highs alongside similar pronounced retracements in Eur/Jpy and other Yen crosses as risk appetite evaporates amidst further re-flattening in debt markets. The headline pair is back down below 108.00 and a key technical level (200 DMA at 108.44), with the 50 DMA (107.65) exposed ahead of last Tuesday’s 107.51 low as safe-haven demand picks up generally to the benefit of Gold (over Usd 1700/oz again) and the Swiss Franc (Usd/Chf testing 0.9550 and Eur/Chf 1.0750 after breaching its 200 DMA – 1.0769). Back to the Yen, no adverse reaction to S&P cutting Japan’s A+ ratings outlook to stable from positive.

- AUD/NZD/CAD – The aforementioned deterioration in risk sentiment on rising Chinese-US/Australian tensions, NK terminating official lines of communication with SK and crude prices unwinding more OPEC+ extension gains, has hit the high beta Aussie and Kiwi particularly hard, even though independent impulses via improvements in NAB and ANZ business surveys overnight may otherwise be supportive. Indeed, Aud/Usd has pulled back around 150 pips to sub-0.6900 and Nzd/Usd is losing grip of 0.6500 after extending gains on the handle to around 0.6580, albeit Aud/Nzd still trending lower towards 1.0750 in the run up to NZ Q1 manufacturing sales. Meanwhile, the Loonie has handed back a chunk of its recent oil-powered upside vs the Greenback with Usd/Cad rebounding from circa 1.3359 to 1.3487 ahead of the FOMC on Wednesday, and this along with an element of broader risk-off positioning is keeping the DXY afloat near 97.000.

- NOK/GBP/SEK/EUR – All weaker, albeit to varying degrees, as the Norwegian Krona underperforms in wake of another bleak Norges Bank regional survey and the correction in crude, while Sterling and the Swedish Crown are undermined by cross selling against the Yen and the overall bearish tone, but the Euro holds up bit better vs the Dollar in consolidative trade. Eur/Nok has bounced firmly following a more concerted test of the 200 DMA, Cable is back under 1.2650 after failing to sustain 1.2750+ status, Eur/Sek is back above 10.4000 and Eur/Usd is trying to keep afloat within a 1.1314-1.1242 range.

- EM – In contrast to widespread reversals vs the Usd, the Try is just staying north of 6.8000 by virtue of Turkey finally ending years of isolation from Euroclear for bond settlements and joining the international platform.

In commodities, the energy complex continues to leak in the aftermath of the OPEC+ meeting as players question the enforcement (or not) of the agreed upon output cuts with laggards such as Iraq already hinting as difficulties on overcompliance. Further, some traders also cite a “buy the rumour, sell the fact” playbook given the rally in the complex heading into the meeting. Meanwhile, BP’s demand-driven job cuts yesterday added further weighed on prices. Elsewhere, in Libya, source reports noted that El-Sharara’s production has again been shuttered by armed men ordering employees to stop working – which comes just two days after the restart and lift of force majeure on exports (now reimposed), albeit the oilfield was only producing at a tenth of its 300k BPD full capacity – which was expected to be reached within 90 days. All-in-all, the OPEC fallout and deteriorating risk sentiment sees WTI July back below USD 38/bbl and closer to USD 37/bbl (vs. high USD 38.86/bbl) , whilst Brent suffers and has breached USD 40/bbl to the downside (vs. high 41.45/bbl). Participants today will be eyeing the monthly EIO STEO – with focus on their estimates for US oil production – the prior report estimated an average output of 11.7mln BPD in 2020 and 10.9mln BPD in 2021. Meanwhile, the weekly Private Inventory data could also offer some short-term volatility in prices. Turning to metals, spot gold continues to gain ground above USD 1700/oz amid risk aversion despite the firmer Buck as investors flee to the safe haven metal, with geopolitical tensions between North Korea/South Korea coupled with Aussie-Sino strains also underpinning the yellow metal. Copper prices are pulling back in tandem with the stock markets and broader sentiment, but prices remain comfortably north of USD 2.5/lb at present.

US Event Calendar

- 6am: NFIB Small Business Optimism, est. 92.5, prior 90.9

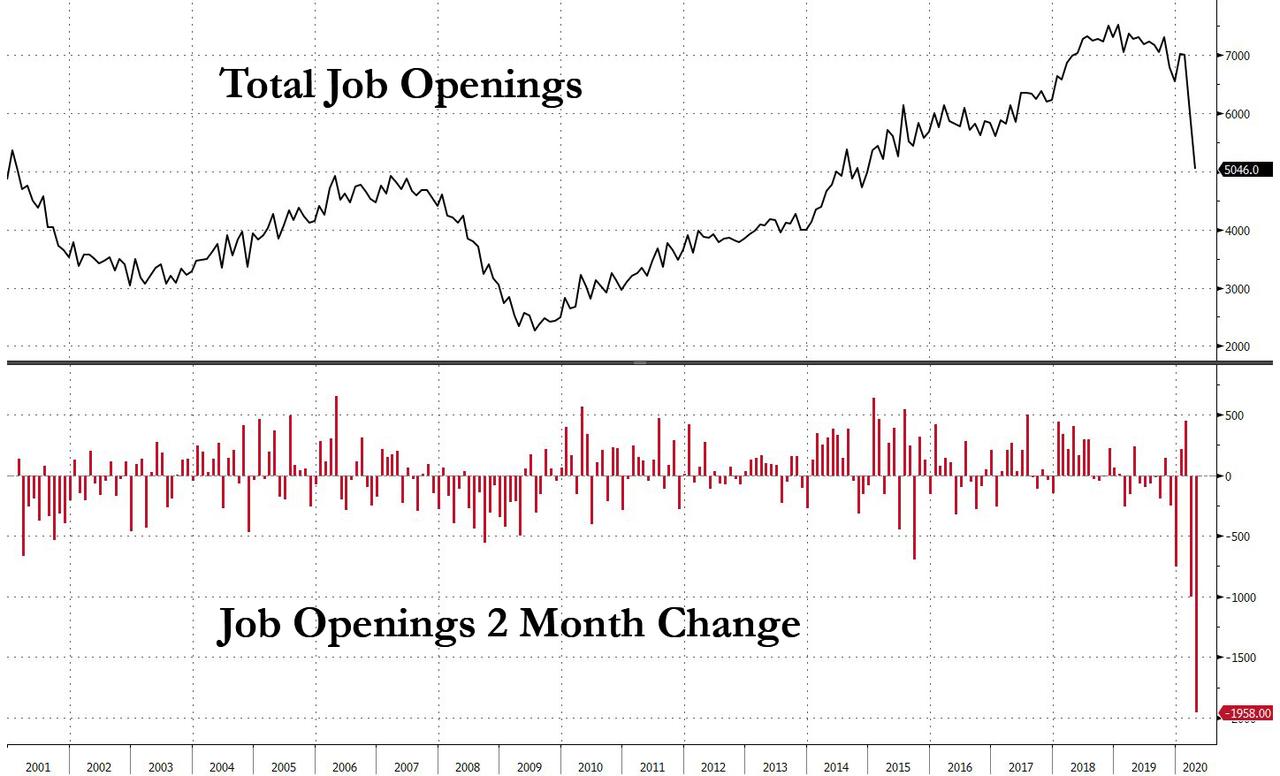

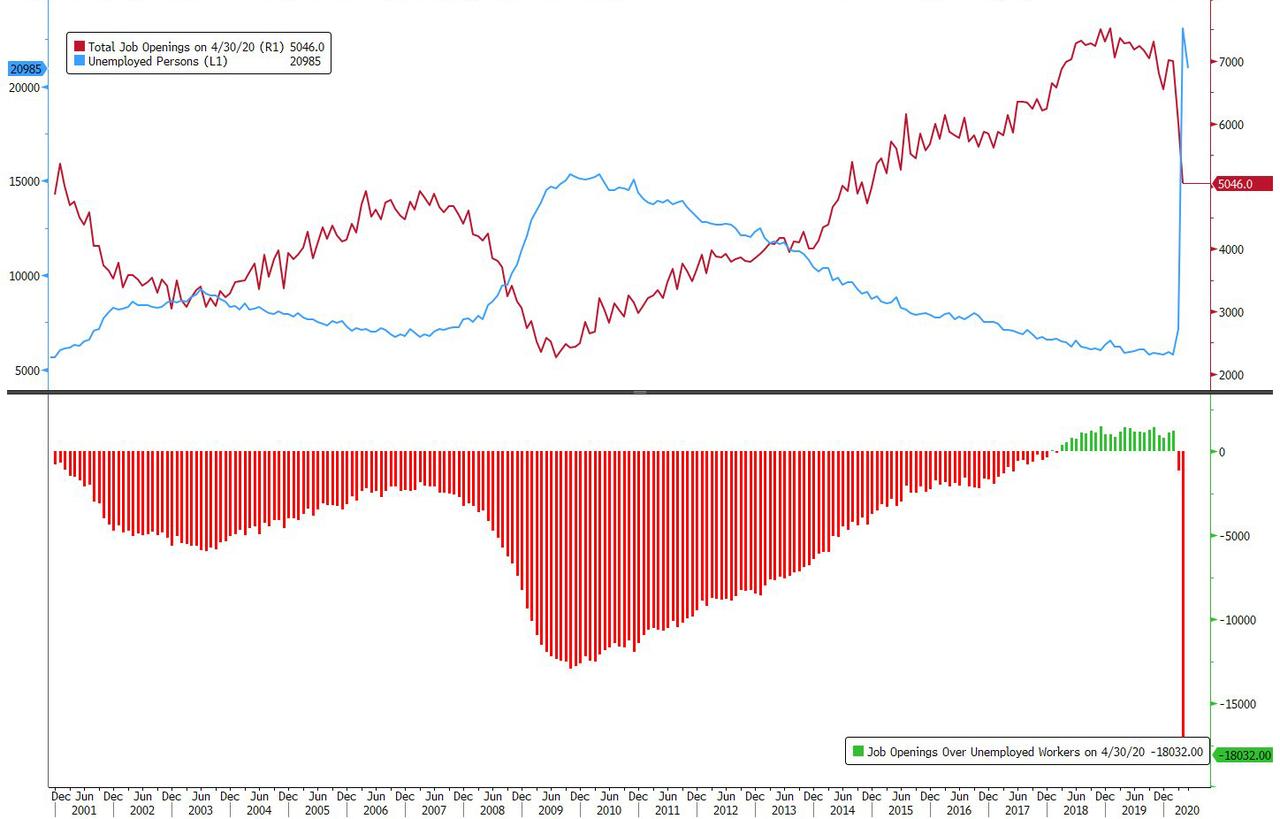

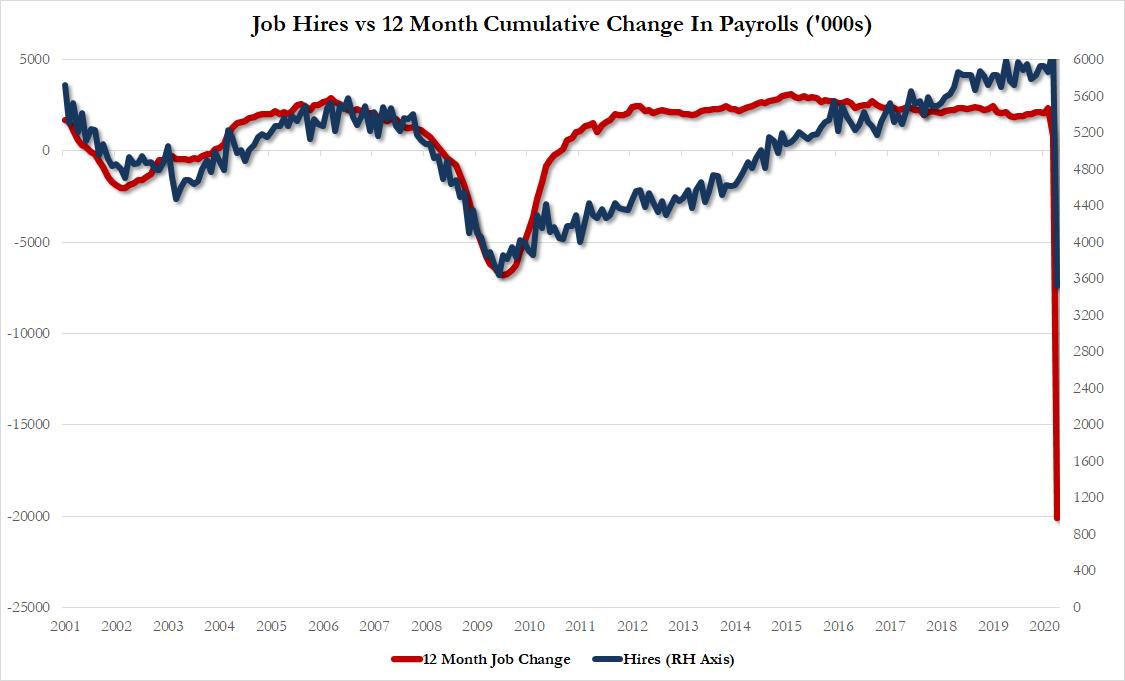

- 10am: JOLTS Job Openings, est. 5,750, prior 6,191

- 10am: Wholesale Inventories MoM, est. 0.4%, prior 0.4%; Wholesale Trade Sales MoM, est. -2.0%, prior -5.2%

DB’s Jim Reid concludes the overnight wrap

Yesterday we officially waved goodbye to the longest US cycle in history as the National Bureau of Economic Research declared that the US has been in a recession since February, thus ending a 128 month expansion. Whilst we’ll never know what would have happened if Covid-19 had not occurred, it’s fascinating that the best predictor of recessions, namely the US yield curve, has struck again. More by luck than judgement this time but the cycle did look increasingly stretched beforehand so this cycle may not have had much life left in it anyway. However it sums the current financial world up perfectly at the moment when on the day we get the official recession word, the NASDAQ hit a new record high and the S&P 500 erased all its declines for 2020. Looking at these indices you’d be forgiven for wondering what all the fuss has been about in 2020.

Looking at the moves in more depth, the S&P 500 closed up +1.20% (+0.05% YTD now), while the NASDAQ climbed +1.13% on the day. The Dow Jones was a big out-performer with a +1.70% advance, driven by Boeing’s +12.20% move. The rotation of recent days was in full effect as cyclicals like Energy (+4.32%) and Banks (+2.78%) were among the best performing industries, while semiconductors (-0.26%) were the only industry group lower yesterday.

About a half hour before US markets closed, the Fed announced that their “Main Street” program, which will open soon to eligible lenders, would be available to more businesses. This seemed to drive the last half percentage point of the rally last night. In terms of details, the central bank lowered loan minimums to $250,000 from $500,000 while extending the loan term to five years from four. Also businesses in the program will be able to defer principal payments on their loans for two years, up from the previously announced one. And finally, in a step meant to incentivize greater participation from banks, lenders will only be required to hold 5% of the loans on their balance sheet, while previously it had been 15%. As a reminder, the Main Street facilities are backed by a $75 billion investment from the Treasury, which is part of the $454bn allocated by Congress in the CARES Act for the Fed’s emergency-lending programs.

Over in Europe there was a bit more of a subdued picture after an impressive run. The STOXX 600 was down -0.32%, with the DAX (-0.22%), CAC 40 (-0.43%) and the FTSE 100 (-0.18%) all losing ground yesterday. European banks were the best performing sector in the index though, up +1.97%, as cyclicals continued to outperform on both sides of the Atlantic.

Markets are a bit more mixed in Asia overnight with the Nikkei (-0.68%) and Kospi (-0.30%) down while the Hang Seng (+1.30%) and Shanghai Comp (+0.47%) are up. Not helping sentiment is news that North Korea will shut down a liaison office it shares with South Korea and sever other official communication including a leaders’ hotline. The country cited that South Korean authorities have “connived” to carry out “hostile acts” against the country. The KCNA also reported that “this measure is the first step of the determination to completely shut down all contact means with South Korea and get rid of unnecessary things.”

That seems to have helped fuel a bid for the Yen (+0.32%) while all other G-10 currencies are trading weak against the greenback. Meanwhile, yields on 10y USTs are down -3.3bps to 0.843% and futures on the S&P 500 are down -0.17%. Elsewhere, WTI crude oil prices are up 1% this morning to $38.58. In terms of overnight data releases the UK’s May BRC like for like sales surprised to the upside with print at +7.9% yoy (vs. +3.0% yoy expected and +5.7% yoy last month).

Back in Europe, we also got some headlines from ECB President Lagarde’s appearance before the European Parliament’s economic and monetary affairs committee. Perhaps the main news was on the German constitutional court though, which as you’ll know has asked the ECB to carry out a proportionality assessment of their public sector purchase programme. In her introductory statement, it was notable that Lagarde explicitly echoed this language, saying that the ECB’s “crisis-related measures are temporary, targeted and proportionate”, and also that “the ECB continually monitors the proportionality of its instruments.” Lagarde also called the net effects of last week’s expansion of the PEPP by a further €600bn “overwhelmingly positive.”

Against this backdrop, market inflation expectations for the Euro Area hit a 3-month high yesterday, with five-year forward five-year inflation swaps rising to 1.09%. Similarly, inflation expectations in the US rose +3.9 bps yesterday to 1.89%. Our US economics team published a report yesterday, where they see the Covid-19 shock generating severe disinflationary pressure in the near-term, but then recovering to near the Fed’s 2% target. See their paper here for more

Meanwhile, sovereign debt advanced both in Europe and the US yesterday after the recent sell-off, with yields on 10yr bunds falling by -4.2bps to -0.32% and US treasury yields down -2.0bps to 0.875%. There was a slight widening in peripheral bond spreads, with the spreads of 10yr yields on both Italian (+3.4bps) and Spanish (+3.2bps) debt over bunds widening marginally following the big tightening seen last week.

One of the big moves yesterday came from oil, where Brent crude snapped a run of 7 successive advances to fall -3.55% following an announcement from Saudi Arabia that they wouldn’t maintain their deeper cuts on output after this month, as well as a move from Libya to resume exports from their largest oil field. Brent now stands at $40.80/bbl, while WTI also declined -3.44% to $38.19/bbl.

There wasn’t a great deal of data out yesterday, though German industrial production fell by -17.9% in April (vs. -16.5% expected), following a revised -8.9% decline in March. The move puts the year-on-year decline for April at -25.3%, which to put that in perspective is above the peak -21.8% annual decline following the GFC in April 2009. Meanwhile in Canada, May’s housing starts rose to 193.5k on an annualised basis (vs. 160.0k expected).

To the day ahead, and data highlights in Europe include the German and French trade balance for April, as well as the final estimate of the Euro Area’s GDP in Q1. Over in the US, there’s also the NFIB small business optimism index for May, and April job openings. Separately, we’ll hear from the ECB’s Rehn, and the BoE’s Cunliffe.

3A/ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 18.54 POINTS OR 0.62% //Hang Sang CLOSED UP 280.45 POINTS OR 1.13% /The Nikkei closed DOWN 87.07 POINTS OR 0.38%//Australia’s all ordinaires CLOSED UP 2.39%

/Chinese yuan (ONSHORE) closed DOWN at 7.0857 /Oil DOWN TO 38.19 dollars per barrel for WTI and 40.65 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0857 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0803 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

North Korea

Seems that North Korea is under what pressure whether they have been hit with the COVID 19 or sanctions against them. They need some help from the west.

(zerohedge)

North Korea Assumes ‘Warlike’ Posture, Cuts Off All Contact With South

Virtually overnight, the thaw in inter-Korea relations apparently ended, and hostility reemerged, as the North Korean leadership announced plans to cut off all communications, including an emergency hotline, in retaliation against South Korea allowing defectors to send propaganda leaflets back across the border.

For several days, North Korea has lashed out at the South Korea over the defector leaflets, which have been a semi-permanent feature of inter-Korea relations, and have long angered Pyongyang.

Over the past few days, the North threatened to close an inter-Korean liaison office and other projects if the South does not stop defectors from sending leaflets and other material into the North. Several leaders quoted in the North Korean press said the “work” toward the south should change into “one against an enemy.”

Top government officials in North Korea, including leader Kim Jong Un’s sister, Kim Yo Jong, and Kim Yong Chol, vice-chairman of the Central Committee of the ruling Workers’ Party of Korea, determined “that the work towards the South should thoroughly turn into the one against an enemy,” KCNA said.

Officials began cutting communication lines at noon Tuesday (about 7 hours ago).

As a first step, at noon on Tuesday, North Korea will close lines of communication at an inter-Korean liaison office, and hotlines between the two militaries and presidential offices, the report said.

On Tuesday morning, North Korean officials did not answer a routine daily call to the liaison office, nor calls on military hotlines, a South Korean defence ministry spokeswoman told a briefing.

The routine calls between South and North Korea should be maintained as they are basic means of communication, said the South’s unification ministry, responsible for inter-Korean affairs.

The ministry said it will continue to follow the agreed principles and strive for peace and prosperity on the Korean Peninsula.

On Monday morning, North Korea did not answer the liaison phone call for the first time since 2018, though it later answered an afternoon call.

Though the North hasn’t confirmed a single COVID-19 case, many suspect that the outbreak has ravaged the North Korean economy while international sanctions continued to bite. One expert says the decision to cut off communication – “a well-worn tactic” – is a sign the North is trying to extract some relief from its neighbor.

Analysts said the move is likely about more than the defectors, as North Korea is under increasing economic pressure as the coronavirus crisis and international sanctions take their toll.

“North Korea is in a much more dire situation than we think,” said Choo Jae-woo, a professor at Kyung Hee University “I think they are trying to squeeze something out of the South.”

“Cutting communications is “a well-worn play for Pyongyang,” but one that can be dangerous, Daniel Wertz, of the U.S.-based National Committee on North Korea, said on Twitter.

“Regular communication channels are needed most during a crisis, and for that reason North Korea cuts them off to create an atmosphere of heightened risk,” he said.

The people of North Korea have “been angered by the treacherous and cunning behaviour of the South Korean authorities, with whom we still have lots of accounts to settle,” KCNA said.

The report accused South Korean authorities of irresponsibly allowing defectors to hurt the dignity of North Korea’s supreme leadership.

“We have reached a conclusion that there is no need to sit face to face with the South Korean authorities and there is no issue to discuss with them, as they have only aroused our dismay,” KCNA said.

The decision follows a recent incident where Kim Jong Un, the supreme leader of North Korea, disappeared for weeks, prompting speculation that he was deathly ill.

b) REPORT ON JAPAN

3 C CHINA

China/USA

China warns the USA not to engage in nuke testing

(zerohedge)

China Warns US: “Abandon Plans” For Nuke Testing Or Risk “Undermining Global Stability”

Just over two weeks ago The Washington Post revealed that “the Trump administration has discussed whether to conduct the first US nuclear test explosion since 1992.”

It was said to have been under serious discussion during a May 15 “deputies meeting” of senior national security officials at the White House – and though doesn’t appear to currently be something seriously pursued – the possibility remains “very much an ongoing conversation,” according to a senior admin official.

While all eyes were initially on Russia’s reaction, the Chinese Foreign Ministry has belatedly issued a response, warning Washington in a press briefing on Monday that it must abide by its international obligations and abandon any possible plans to carry out nuclear tests.

“We insist that the United States should strictly abide by its obligations to end nuclear testing… and we hope that it will listen to the international community,” ministry spokesperson Hua Chunying said. “The US should abandon plans that could undermine global stability and strategic order,” she added.

Emphasizing Beijing has repeatedly urged the US to honor its commitments, the top diplomat continued: “The US needs to contribute to international cooperation to ensure disarmament and the non-proliferation of weapons of mass destruction.”

However, the administration is sure to shrug off these words and hit back, given it’s lately repeatedly accused China and Russia of ‘illegally’ conducting low-yield nuclear tests, which both countries have denied. In Beijing’s case it’s believed China’s military is able to conceal such provocative tests at an elaborate underground testing facility.

There hasn’t been an American nuclear test (that’s officially known about at least) since 1992, upon the end of the Cold War and collapse of the USSR in the year prior. But there are signs we could all soon witness a new provocative test given landmark weapons treaties with Moscow are fast being shed, also as Trump might entertain using nuke tests as powerful “leverage” for desired negotiations “for a better deal” – as he’s said in the past.

The Japan Times

✔@japantimes

Trump envisions a three-way nuclear pact. China has other ideas http://jtim.es/GDQh30qLSfw

Trump envisions a three-way nuclear pact. China has other ideas | The Japan Times

Washington takes aim at Beijing’s atomic ambitions as Trump administration vows to craft ‘new era of arms control’

japantimes.co.jp

All of this leaves the potential for a new global arms race centered on nukes, given at this point Beijing, Moscow, and Washington are already trading warnings to step back from the brink of nuclear testing.

Meanwhile Beijing has shown itself resistant to Trump’s floating the idea of a new nuclear weapons pact involving China. He dumped the INF in part because it failed to take into a account developing Chinese missile technology and capabilities, according to admin officials.

4/EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6.Global Issues

This is very worrisome: a locust plague has put millions on the brink of famine

(Michael Snyder)

A ‘Biblical’ Locust Plague Has Put Millions On Brink Of Famine

Authored by Michael Snyder via The Economic Collapse blog,