GOLD:$1798.80 DOWN $0.50 The quote is London spot price

Silver:$18.69// UP 7 CENTS London spot price

FRIDAY’S ARE GOOD DAYS FOR OUR BANKERS TO RAID ESPECIALLY AFTER 12 PM AS OUR STRONG PHYSICAL MARKETS IN LONDON ARE PUT TO BED.

Closing access prices: London spot

i)Gold : $1798.50 LONDON SPOT 4:30 pm

ii)SILVER: $18.72//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUG GOLD: $1802.60 CLOSE 1.30 PM// SPREAD SPOT/FUTURE AUG /: $3.80

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $19.06…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : 37 CENTS PER OZ

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2600. usa per oz

and silver; $29.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 70/564

issued 500

EXCHANGE: COMEX

CONTRACT: JULY 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,799.200000000 USD

INTENT DATE: 07/09/2020 DELIVERY DATE: 07/13/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 H GOLDMAN 5

118 H MACQUARIE FUT 102

135 H RAND 3

152 C DORMAN TRADING 11

226 C DIRECT ACCESS 1

355 C CREDIT SUISSE 92

555 C BNP PARIBAS SEC 1

624 C BOFA SECURITIES 4

657 C MORGAN STANLEY 44

657 H MORGAN STANLEY 13

661 C JP MORGAN 500 70

686 C INTL FCSTONE 1

690 C ABN AMRO 2 2

732 C RBC CAP MARKETS 1

737 C ADVANTAGE 17 62

800 C MAREX SPEC 41 102

878 C PHILLIP CAPITAL 3 18

905 C ADM 33

____________________________________________________________________________________________

TOTAL: 564 564

MONTH TO DATE: 6,671

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 564 NOTICE(S) FOR 56400 OZ (1.751 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 6671 NOTICES FOR 667100 OZ (20.714 TONNES)

SILVER

FOR JULY

165 NOTICE(S) FILED TODAY FOR 825,000 OZ/

total number of notices filed so far this month: 13,658 for 68.290 MILLION oz

BITCOIN MORNING QUOTE $9287 UP 30

BITCOIN AFTERNOON QUOTE.: $9238 DOWN $5

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $0.50 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

STRANGE: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES

(AND NO DOUBT USED IN THE RAID TODAY)

GLD: 1,200.82 TONNES OF GOLD//

WITH SILVER UP 7 CENTS TODAY: AND WITH NO SILVER AROUND:

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTROUS PAPER DEPOSIT OF 4.844 MILLION OZ//

THIS IS A MASSIVE FRAUD

RESTING SLV INVENTORY TONIGHT:

SLV: 515.795 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A SMALL SIZED 324 CONTRACTS FROM 176,125 DOWN TO 175,801, AND FURTHER FROM OUR NEW RECORD OF 244,710, (FEB 25/2020. THE TINY SIZED LOSS IN OI OCCURRED WITH OUR 8 CENT LOSS IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE LOSS IN COMEX OI IS PRIMARILY DUE TO HUGE BANKER SHORT COVERING PLUS A GOOD EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A SMALL INCREASE IN SILVER STANDING AT THE COMEX FOR JULY. WE HAD A NET GAIN IN OUR TWO EXCHANGES OF 244 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: JULY: 0 AND SEP 553 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 553 CONTRACTS. WITH THE TRANSFER OF 553 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 553 EFP CONTRACTS TRANSLATES INTO 2.765 MILLION OZ ACCOMPANYING:

1.THE 8 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

81.75 MILLION OZ INITIALLY IN JULY.

THURSDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL 8 CENTS).. AND,OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS. THE SMALL LOSS AT THE COMEX WAS ACCOMPANIED BY : i) A TINY ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A SMALL INCREASE IN STANDING OF SILVER OZ STANDING FOR JULY, STRONG BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A NET GAIN OF 229 CONTRACTS OR 1.145 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

JULY

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF JULY:

4820 CONTRACTS (FOR 7 TRADING DAY(S) TOTAL 4820 CONTRACTS) OR 23.232 MILLION OZ: (AVERAGE PER DAY: 688 CONTRACTS OR 3.442 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 23.232 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 3.32% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,161.51 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 23,232 MILLION OZ/

EXCHANGE FOR PHYSICAL ISSUANCE FOR THE PAST 60 DAYS IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 324, WITH OUR 8 LOSS IN SILVER PRICING AT THE COMEX ///THURSDAY… THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 553 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A SMALL SIZED OI CONTRACTS ON THE TWO EXCHANGES: 229 CONTRACTS (DESPITE OUR 8 CENT LOSS IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 553 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A SMALL SIZED DECREASE OF 324 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED DESPITE A 8 CENT LOSS IN PRICE OF SILVER/AND A CLOSING PRICE OF $18.62 // THURSDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.8475 BILLION OZ TO BE EXACT or 121% of annual global silver production (ex Russia & ex China).

FOR THE NEW JULY DELIVERY MONTH/ THEY FILED AT THE COMEX: 165 NOTICE(S) FOR 825,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 81.695 million oz

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 3540 CONTRACTS TO 572,332 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE SMALL SIZED LOSS OF COMEX OI OCCURRED DESPITE OUR STRONG LOSS IN PRICE OF $11.75 /// COMEX GOLD TRADING// THURSDAY// WE HAD HUGE BANKER SHORT COVERING, ANOTHER HUMONGOUS SIZED GOLD OZ STANDING AT THE COMEX FOR JULY, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A GOOD EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR LOSS IN PRICE OF $11.75 .

WE HAD A VOLUME OF 3 4 -GC CONTRACTS//OPEN INTEREST 63

WE GAINED A GOOD SIZED 4969 CONTRACTS (15.46 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 8509 CONTRACTS:

CONTRACT .; AUG 6559 AND DEC: 1950 ALL OTHER MONTHS ZERO//TOTAL: 8509. The NEW COMEX OI for the gold complex rests at 572,332. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4969 CONTRACTS: 3540 CONTRACTS DECREASED AT THE COMEX AND 8509 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 4969 CONTRACTS OR 15.46 TONNES. THURSDAY, WE HAD A LOSS OF $11,75 IN GOLD TRADING……

AND WITH THAT LOSS IN PRICE, WE HAD A GOOD SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 15.46 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT FELL $11.75).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS UNSUCCESSFUL (SEE BELOW).

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (8509) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (3540 OI): TOTAL GAIN IN THE TWO EXCHANGES: 5725 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)ANOTHER HUMONGOUS INCREASE IN GOLD STANDING AT THE GOLD COMEX FOR THE FRONT JULY MONTH, 3) ZERO LONG LIQUIDATION; 4) SMALL COMEX OI LOSS.. AND …ALL OF THIS WAS COUPLED WITH OUR STRONG LOSS IN GOLD PRICE TRADING//THURSDAY//$11.75.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

SPREADING OPERATIONS/NOW SWITCHING TO GOLD

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN GOLD AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF AUGUST FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF JULY. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUGUST), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

JULY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY(S) IN TONNES: 80.63 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 80.63/3550 x 100% TONNES =1.51% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3108.05 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 80.63 TONNES SO FAR..

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A SMALL SIZED 324 CONTRACTS FROM 175,180 DOWN TO 175,816 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE TINY OI LOSS IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) HUGE BANKER SHORT COVERING , 2) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A SMALL INCREASE STANDING AT THE SILVER COMEX FOR JULY AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 553 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY: 0 CONTRACTS AND SEPT: 553 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 553 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 324 CONTRACTS TO THE 553 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 229 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 1.220 MILLION OZ, OCCURRED DESPITE THE 8 CENT LOSS IN PRICE///

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 8 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// THURSDAY. WE ALSO HAD A SMALL SIZED 553 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON PLUS HUGE FUTURE PREMIUMS OVER SPOT.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 67.27 POINTS OR 1.95% //Hang Sang CLOSED DOWN 482.75 POINTS OR 1.84% /The Nikkei closed DOWN 238.48 POINTS OR 1.06%//Australia’s all ordinaires CLOSED DOWN .64%

/Chinese yuan (ONSHORE) closed DOWN at 7.0017 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0017 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0034 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED///CORONAVIRUS//PANDEMIC : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

i)we had 2 deposits into the customer account

into JPMorgan: 0

ii) Into CNT: 600,247.299 oz

iii) Into Delaware: 40,563.600 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.744 million oz of total silver inventory or 49.47% of all official comex silver. (160.819 million/324.985 million

total customer deposits today: nil oz

we had 2 withdrawals:

ii) Out of CNT 605,351.350 oz

iii) Out of Delaware: 4983.482 oz

total withdrawals; 60,334.832 oz

We had 2 adjustments

dealer to customer:

Brinks: 397,048.250 oz

Scotia: 15,143.000 oz ???

total dealer silver: 126.229 million

total dealer + customer silver: 324.985 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The front month of July has an open interest of 2857 contracts, as we lost 25 contracts. We had 37 notices served on THURSDAY, so we FINALLY GAINED a tiny 12 contracts or an additional 60,000 oz will stand in this active delivery month of July as they refused to morph into a London based forwards. Our banker boys will now be busy trying to find some scarce silver to put out fires elsewhere.

The next month after July is the non active month of August and here sees its open interest rose by 1 contracts UP to 813

The big September contract month sees a loss of 757 contracts down to 138,557.

The total number of notices filed today for the JULY 2020. contract month is represented by 165 contract(s) FOR 825,000, oz

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 13,658 x 5,000 oz = 68,290,000 oz to which we add the difference between the open interest for the front month of JULY.(2857) and the number of notices served upon today 165 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the JULY/2019 contract month: 13,658 (notices served so far) x 5000 oz + OI for front month of JULY (2857)- number of notices served upon today (165) x 5000 oz of silver standing for the JULY contract month.equals 81,750,000 oz. (A WHOPPER )

WE GAINED 12 CONTRACTS OR 60,000 OZ WILL STAND FOR DELIVERY. SILVER IS STILL VERY SCARCE ON THIS SIDE OF THE POND.

TODAY’S ESTIMATED SILVER VOLUME : 61,828 CONTRACTS // volume good/

FOR YESTERDAY: 108,856.,CONFIRMED VOLUME//volume excellent/

YESTERDAY’S CONFIRMED VOLUME OF 108,856 CONTRACTS EQUATES to 544 million OZ 77.75% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 0.25% ((JULY 10/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO +.34% to NAV: (JULY 10/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 0.25%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 17.21 TRADING 17.19///NEGATIVE 0.12

END

And now the Gold inventory at the GLD/

JULY 10/WITH GOLD DOWN $.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD//A STRANGE WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1200.82 TONNES

JULY 9//WITH GOLD DOWN $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OX 3.21 TONNES INTO THE GLD//INVENTORY RESTS AT 1202.57 TONNES

JULY 8/WITH GOLD UP $13.75 TODAY; A BIG CHANGE IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 7.89 TONNES INTO THE GLD//INVENTORY RESTS AT 1199.36 TONNES

JULY 7/WITH GOLD UP $12.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1191.47 TONNES

JULY 6/WITH GOLD UP $6.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1191.47 TONNES

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

JUNE 30//WITH GOLD UP $16.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1178.90 TONNES

JUNE 29/WITH GOLD UP $2.90 TODAY: A HUGE DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1178.90 TONNES

JUNE 26/WITH GOLD UP $5.03 TODAY: VERY STRANGE: A PAPER WITHDRAWAL OF 1.46 TONNES//INVENTORY RESTS AT 1175.39 TONNES

JUNE 25//WITH GOLD DOWN $3.30 TODAY//ANOTHER STRONG PAPER DEPOSIT OF 7.6 TONNES///INVENTORY RESTS AT 1176.85 TONNES

JUNE 24/WITH GOLD DOWN $1.50 TODAY; A STRONG 3.21 TONNES ADDED TO THE GLD//INVENTORY RESTS AT 1169.25 TONNES

JUNE 23/WITH GOLD UP $25.50 TODAY/ANOTHER CRIMINAL PAPER DEPOSIT OF 6.73 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1166.04 TONNES

JUNE 22/WITH GOLD UP $14.00 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 23.09 TONNES//INVENTORY RESTS AT 1159.31 TONNES

JUNE 19/WITH GOLD UP$16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//; INVENTORY RESTS AT 1136.22 TONNES

JUNE 18//WITH GOLD DOWN $2.75 TODAY: NO CHANGES IN GOLD INVENTORY: INVENTORY RESTS AT 1136.22 TONNES

JUNE 17/WITH GOLD DOWN $1.05: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1136.22 TONNES

JUNE 16//WITH GOLD UP $6.70 TODAY: NO CHANGES IN GOLD INVENTORY: /INVENTORY RESTS AT 1136.22 TONNES

JUNE 15/WITH GOLD DOWN ANOTHER $8.80 TODAY, NO CHANGES IN GOLD INVENTORY/INVENTORY RESTS AT 1136.22 TONNES

JUNE 12//WITH GOLD DOWN $1.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 1.17 TONNES AT THE GLD//INVENTORY RESTS AT 1136.22 TONNES

JUNE 11//WITH GOLD UP $16.80 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 6.55 TONNES AT THE GLD//INVENTORY RESTS AT 1135.05 TONNES

JUNE 10/WITH GOLD DOWN $.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 4.02 TONNES AT THE GLD/INVENTORY RESTS AT 1129.50 TONNES

JUNE 9//WITH GOLD UP $16.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 2.63 TONNES OF GOLD AT THE GLD//INVENTORY RESTS AT 1125.48 TONNES

JUNE 8//WITH GOLD UP $18.70 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 4.10 TONNES AT THE GLD//INVENTORY RESTS AT 1128.11 TONNES

JUNE 5//WITH GOLD DOWN $40.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A PAPER WITHDRAWAL OF 1.16 TONNES OUT OF THE GLD//INVENTORY RESTS AT 1132.21 TONNES

JUNE 4//WITH GOLD UP $20.60: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD…A DEPOSIT OF 4.09 TONNES INTO THE GLD//INVENTORY RESTS AT 1133.37 TONNES

JUNE 3//WITH GOLD DOWN $26.15//A SMALL CHANGE IN GOLD INVENTORY//A DEPOSIT OF 0.78 TONNES OF GLD INTO THE GLD//INVENTORY RESTS AT 1129.28 TONNES

JUNE 2//WITH GOLD DOWN $11.20 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1128.40 TONNES

JUNE 1//WITH GOLD UP $1.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES OF GOLD//GLD INVENTORY RESTS TONIGHT AT 1123.14 TONNES

MAY 29/WITH GOLD UP $19.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///GLD INVENTORY RESTS THIS WEEKEND AT 1119.05 TONNES

MAY 28//WITH GOLD UP $4.00 TODAY/NO CHANGES IN GOLD INVENTORY TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

MAY 27/WITH GOLD UP $.10 TODAY: A STRONG 2.34 TONNES OF GOLD ADDED TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

JULY 10/ GLD INVENTORY 1200.52 tonnes*

LAST; 857 TRADING DAYS: +257.00 NET TONNES HAVE BEEN ADDED THE GLD

LAST 757 TRADING DAYS://+435.11 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JULY 10/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 4.844 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.795 MILLION OZ

WHAT A FRAUD!!

JULY 9/WITH SILVER DOWN 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 8.198 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 510.951 MILLION OZ/

JULY 8/WITH SILVER UP 37 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.118 MILLION OZ FROM THE SLV//VERY SURPRISING.//INVENTORY RESTS AT 502.753 MILLION OZ//

JULY 7/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/INVENTORY RESTS AT 503.871 MILLION OZ///

JULY 6//WITH SILVER UP 24 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.863 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 503.871 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

JUNE 30/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 29/WITH SILVER DOWN ONE CENT TODAY: A TWO CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 466,000 OZ TO PAY FOR STORAGE FEES AND INSURANCE//// AND A LARGE DEPOSIT OF 1.212 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 26/WITH SILVER UP 6 CENTS TODAY: ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ RESTS AT 491.858 MILLION OZ//

JUNE 25/WITH SILVER UP 12 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 931,000 OZ INTO THE SLV////INVENTORY RESTS AT 491.858 MILLION OZ//

JUNE 24///WITH SILVER DOWN 31 CENTS// NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 490.927 MILLION OZ

JUNE 23//WITH SILVER UP 16 CENTS TODAY: A MONSTROUS CHANGE IN INVENTORY: A PAPER DEPOSIT OF 4.473 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 490.927 MILLION OZ//

JUNE 22/WITH SILVER UP 15 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/: INVENTORY/INVENTORY RESTS AT 486/454 MILLION OZ//

JUNE 19//WITH SILVER UP 22 CENTS TODAY: STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 839,000 OZ FROM THE SLV////INVENTORY RESTS AT 486,454 MILLION OZ..

JUNE 18/WITH SILVER DOWN 16 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 932,000 OZ INTO THE SLV////INVENTORY RESTS AT 487.293 MILLION OZ

JUNE 17/WITH SILVER UP 8 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.261 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.361 MILLION OZ

JUNE 16//WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.118 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 483.100 MILLION OZ//

JUNE 15/WITH SILVER DOWN 14 CENTS NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 481.982 MILLION OZ///

JUNE 12/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: TWO DEPOSITS OF 7.269 MILLION OZ AND 1.802 MILLION OZ ADDED TO THE SLV///INVENTORY RESTS THIS WEEKEND AT 481.982 MILLION OZ//

JUNE 11//WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY: ///INVENTORY RESTS AT 472.89 MILLION OZ//

JUNE 10/WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.849 MILLION OZ//

JUNE 9/WITH SILVER DOWN 6 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.605 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 422.849 MILLION OZ//

JUNE 8/WITH SILVER UP 36 CENTS TODAY: TWO HUGE WITHDRAWALS OF 932,000 MILLION OZ AND 1.491 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 470.240 MILLION OZ//

JUNE 5/WITH SILVER DOWN 46 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 648,000 OZ FROM THE SLV////INVENTORY RESTS AT 472.663 MILLION OZ

JUNE 4//WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV.//INVENTORY RESTS AT 473.315 MILLION OZ//

JUNE 3//WITH SILVER DOWN 23 CENTS TODAY//NO CHANGES IN SILVER INVENTORY AT THE SLV//

INVENTORY RESTS AT 473.315 MILLION OZ//

JUNE 2//WITH SILVER DOWN 31 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUMONGOUS 6.686 MILLION OZ ADDED TO THE SLV////INVENTORY RESTS TONIGHT AT 473.315 MILLION OZ//

JUNE 1//WITH SILVER UP 38 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.56 MILLION OZ INTO THE SLV////INVENTORY RESTS TONIGHT AT 466.629 MILLION OZ//

MAY 29//WITH SILVER UP 52 CENTS TODAY: A MASSIVE DEPOSIT OF 2.796 MILLION OZ INTO THE SLV//INVENTORY RESTS THIS WEEKEND AT 463.273 MILLION OZ//

MAY 28//WITH SILVER UP 9 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.660 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 460.477 MILLION OZ//

MAY 27/WITH SILVER UP 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 455.817 MILLION OZ//

JULY 10.2020:

SLV INVENTORY RESTS TONIGHT AT

515.795 MILLION OZ.

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

Market Watch’s Watts explains why safe haven gold and the stock market are now moving northbound

Watts/Market Watch/GATA)

Why ‘safe haven’ gold and the stock market are now moving the same direction

Submitted by cpowell on Fri, 2020-07-10 02:00. Section: Daily Dispatches

By William Watts

MarketWatch.com, New York

Thursday, July 9, 2020

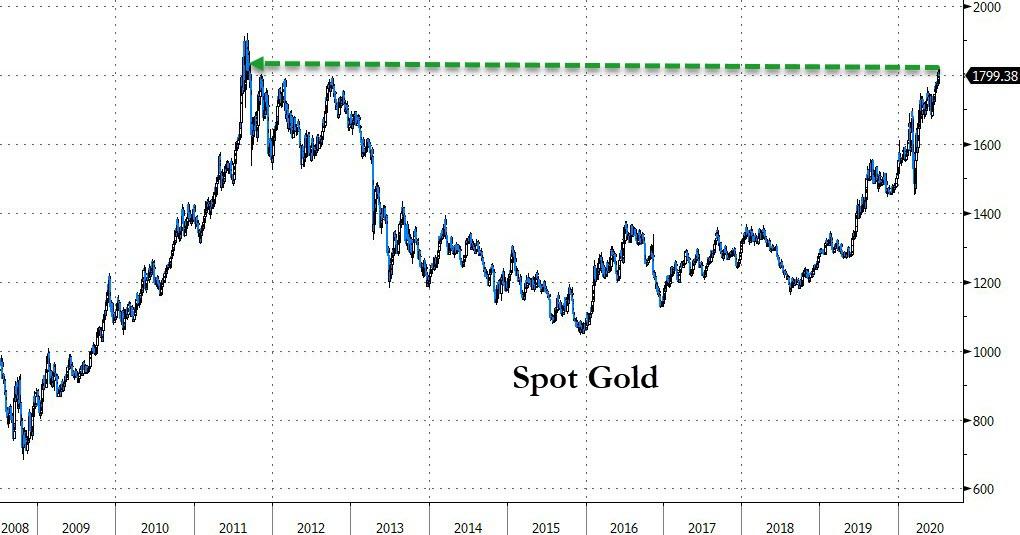

Gold is traditionally thought of as a haven asset — a safe port in a storm. But that hasn’t stopped it from rising to a near nine-year high, and within striking distance of its record, even as equities and other assets traditionally viewed as risky remain buoyant as they rebound from the pandemic-inspired selloff suffered earlier this year.

Chalk it up, in part, to opportunity costs. Efforts by global central banks to push down interest rates, which have fallen into negative territory in real, or inflation-adjusted terms, in the U.S. and are outright negative in many parts of the world, mean that investors who hold gold aren’t missing out on the yield they would earn from holding bonds in more usual circumstances.

…

As real yields turn negative, opportunity costs for holding non-yielding assets essentially vanish, particularly when viewed through the historical lens of fiat currencies and their purchasing power,” wrote Jeff deGraaf, chairman of Renaissance Macro Research, in a note today.

“This provides a continued tailwind for gold,” he said referring to the chart below, which shows the gold price inverted versus the real Treasury yield curve. …

… For the remainder of the report:

https://www.marketwatch.com/story/why-safe-haven-gold-is-acting-like-a-r…

END

iii) Other physical stories:

Only with Venezuelan gold? Other countries will find out soon enough that much of sovereign gold held in England has been leased out and never to be returned

(Ross/Infobric.org)

UK Commits “Highway Robbery” Of Venezuelan Gold, Says Academic

Authored by Johanna Ross via InfoBrics.org,

When it comes to Venezuela, Britain is suffering from split personality disorder. While the UK Foreign Office reportedly maintains ‘full, normal and reciprocal diplomatic relations’ with legitimately elected President Maduro’s government, and with Maduro’s UK ambassador, the British government has been actively supporting the self-appointed US-backed ‘leader’ Juan Guaido, who led the coup against Maduro in 2019.

Last week the High Court in London ruled that Juan Guaido was ‘unequivocally’ recognised as the President of Venezuela.

There’s just one problem with the ruling however: Juan Guaido isn’t the President.

He may have tried hard; he talked the talk, and walked the walk (clearly modelling himself on a cross between Justin Trudeau and Emmanuel Macron, with sleeves rolled up like Barack Obama). He had just the right youthful, liberal image to front the US led regime change campaign in the South American nation. But last year’s coup, supported by the US and Colombia, dramatically backfired after the Venezuelan military refused to back him.

Nevertheless, it has been in the British government’s interest to prop up the would-be Venezuelan leader. The High Court’s verdict was in a case brought to the court by Maduro’s government, which is trying to access $1bn of its gold currently held by the Bank of England. It’s pretty straightforward – the bank doesn’t want to pay out, and is using Maduro’s ‘contested’ leadership as a reason not to do so. Suddenly it matters that Maduro’s presidency is questionable, never mind the fact that he was democratically re-elected in 2018.

Juan Guaido claims that the funds from the Bank of England gold would be used to ‘prop up the regime’, while the Venezuelan government has insisted that the money would go towards managing the coronavirus pandemic. Maduro has even said that once the gold is sold the money will be transferred to the UN Development Programme. In any case, the reason seems irrelevant; when was the last time you or I had to justify a withdrawal from our own bank accounts?

I spoke recently to the National Secretary of the Venezuela Solidarity Campaign and senior lecturer at the University of Middlesex, Dr Francisco Dominguez, who said to me that the move by the High Court to block the transfer of Venezuelan gold constituted nothing more than ‘highway robbery’ and he condemned the UK’s use of Guaido in this case as a ‘legal device to steal Venezuela’s assets’. He stated:

“It is abundantly clear the UK’s recognition of Guaido’s farcical ‘interim presidency’ has nothing to do with ‘democracy’ or ‘human rights’ but with ‘colonial pillage’.

After all, there is nothing democratic or decent about Guaido: he colludes with Colombian narco-traffickers; he attempted a violent coup d’etat’; contracted US mercenaries to assassinate President Maduro and several Venezulean government high officials, vigorously promotes sanctions and aggression against his own nation, and he reeks of corruption.”

Dr Dominguez also pointed to direct collusion of the UK government with Guaido, as was recently uncovered by a British journalist. Newly obtained documents, exposed by John McEvoy, have recently shed light on the murky connection between the British government and the aspiring Venezuelan president. It was uncovered that a Foreign & Commonwealth Office (FCO) Unit named the Venezuela Reconstruction Unit has been created which has not been officially acknowledged by either country. In the documents it was revealed that Juan Guaidó’s representative in the UK, Vanessa Neumann, had spoken with FCO officials about the sustenance of British business interests in Venezuela’s ‘reconstruction’. A conversation of this nature obviously stinks of regime change, given the fact Venezuela sits on the largest proven oil reserves in the world, and that Neumann has previously links to oil companies. Britain is placing its stake in Venezuela’s demise.

Formally the UK government has a different position. In relation to Venezuela’s gold, former Treasury Minister Robert Jenrick said back in 2019 in response to the parliamentary question ‘what the legal basis was for the Bank of England’s decision to freeze approximately 1125 gold bars stored by the Venezuelan central bank in November 2018.’, that it was a ‘matter for the Bank of England’. Jenrick maintained that HM Treasury only has direct control over the UK government’s own holdings of gold within its official reserves, which are held at the Bank of England.’

However the facts paint a different picture.

John Bolton’s White House memoir The Room Where It Happened’ reveals that UK Foreign Secretary at the time, Jeremy Hunt ‘was delighted to freeze Venezuelan gold deposits in the Bank of England so the regime could not sell the gold to keep itself going.’

As Bolton unashamedly admitted:

“These were the sort of steps we were already applying to pressure Maduro financially.”

The former National Security Advisor relates in his book how proud he was to have been the driving force behind the 2019 power grab:

“I was heartened that Maduro’s government promptly accused me of leading a coup.”

Bolton openly describes how they discussed ways of delegitimizing the Venezuelan government as Trump reportedly said “Maybe it’s time to put Maduro out of business.”

The evidence suggests that the UK complied fully in Bolton’s masterplan to unseat Maduro, and is continuing to work with the US to undermine the Venezuelan leadership; only in truly subtle British fashion, surreptitiously, hoping no-one would notice. Who knows, when, if ever, the Venezuelans will see their gold. But you can be sure they won’t be investing with the Bank of England any time soon.

end

Andrew Maguire talks with Chris Marcus on the shenanigans being played out by JPMorgan.

Andrew Maguire: DOJ Told JP Morgan To Reduce Silver Position

Last week the shocking news was that on the first day of the COMEX July silver delivery period, JPMorgan posted 30 million ounces of silver for delivery. Now, Andrew Maguire of Kinesis Money, who’s been a key witness in the Department of Justice investigation, reports that JP Morgan was told to by the DOJ to reduce its silver position as they negotiate a settlement.

(Harvey: spoiler alert..it did not happen)

Andrew also talked about the stunning recent silver inflows to SLV and the silver trusts, and explained how the number just simply don’t add up.

Especially with the silver price experiencing another sharp jolt to the upside, this is a timely interview you are going to want to see, so click to watch what Andrew had to say now!

Chris Marcus

July 9, 2020

JULY 10, 2020

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

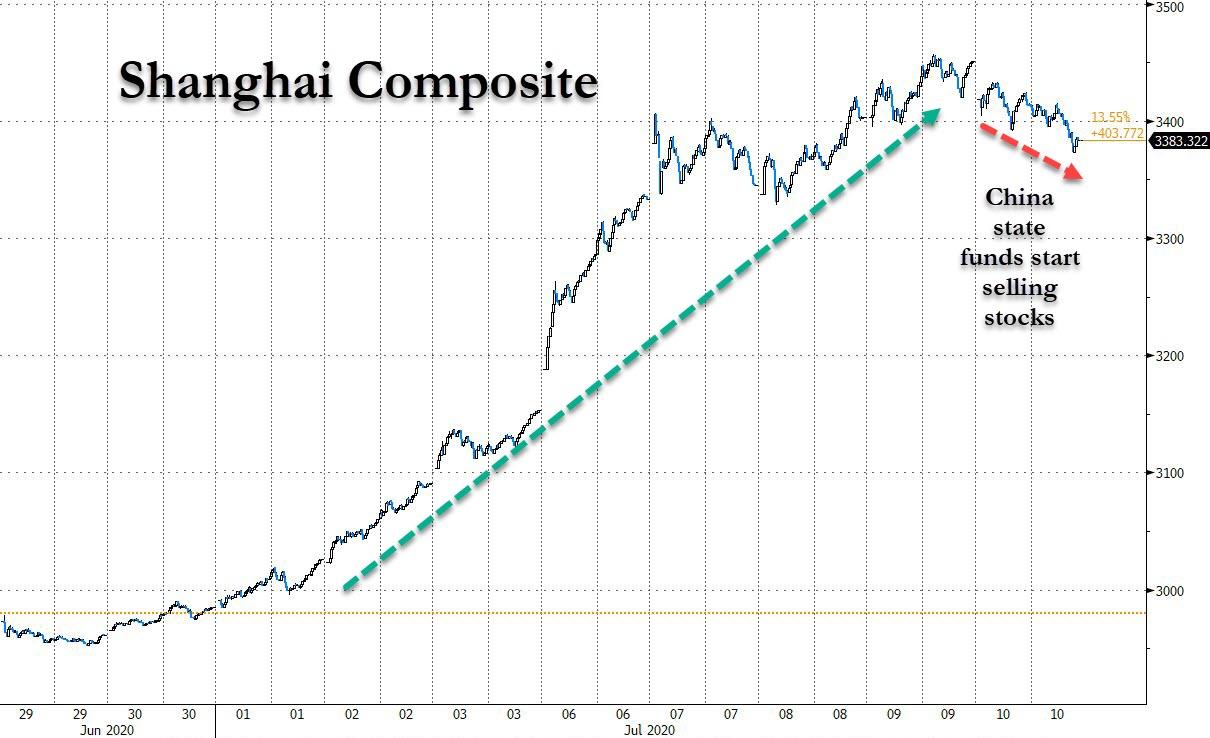

Futures Slide, Follow China Lower After Beijing-Owned Funds Start Selling Stocks

US stock futures slipped on Friday as the buying frenzy in China fizzled and fears re-emerged that record increase in coronavirus cases could lead to another hit to Corporate America with several states delaying the easing of business restrictions. Treasuries jumped, sending five-year yields near a record low.

Chinese stocks slumped for the first time in over a week after Beijing acted to cool the speculative frenzy in its $9.5 trillion stock market, ending a euphoric eight-day surge that had fueled worries of a new bubble in the making. The selling in the Shanghai Composite started after Bloomberg reported that two government-owned funds announced plans to trim holdings of stocks that soared this week.

China’s National Council for Social Security Fund – the country’s national pension fund – said Thursday it intends to sell a stake of as much as 2% in People’s Insurance Company (Group) of China Ltd. The fund, which oversees about 2.2 trillion yuan ($314 billion) in assets, said the sale was part of its “regular divesting activities.” The stock dropped 7.4% in Shanghai, the most in five months. Additionally, the National Integrated Circuit Industry Investment Fund Co. – a smaller state-backed semiconductor fund aimed at fostering China’s homegrown chipmakers – announced plans to offload shares in three firms. Textile maker Wuxi Taiji Industry Co., Shenzhen Goodix Technology Co., and Beijing BDStar Navigation Co. fell at least 3.8%.

Separately, on Friday the state-run China Economic Times warned about the dangers of a “crazy” bull market, while Caixin reported that regulators had asked mutual fund companies to cap the size of new products. Meanwhile, foreign-based funds turned net sellers of Chinese shares for the first time this month on Friday, dumping a net 4.4 billion yuan, the most since late March. They had pumped a net 63 billion yuan across the border via exchange links in July.

“The signal could not be clearer — stocks have just become too hot for the regulators’ liking,” said Niu Chunbao, a fund manager at Shanghai Wanji Asset Management Co. “A slight dip or so may put their minds more at ease at this point.”

As a result, the Shanghai Composite closed down 2% and the SSE 50 Index of Shanghai’s largest stocks ended the day 2.6% lower. The index had closed Thursday within 2% of its intraday peak in 2015.

The end of China’s rally sent a shockwave around the globe sending US index futures modestly in the red and almost wiping out all of the week’s gains, while traders also focused on record deaths in Florida, Texas and California from the virus. 41 of the 50 U.S. states have reported an increase in COVID-19 cases over the last two weeks, while the country registered the largest single-day increase in new infections globally for the second day in a row on Thursday. The surge has forced Americans to take new precautions, with several states backpedaling on reopening plans but likelihood of a lockdown similar to February and March seems unlikely, according to market experts.

“We’re going to see intermittent periods of shutdowns over the next year or so while we’re still grappling with this virus,” Erin Browne, a multi-asset portfolio manager at Pacific Investment Management Co. said on Bloomberg TV. “But I wouldn’t expect we’re likely to see a wholesale shutdown of the U.S. economy like we saw earlier this year.”

At 7:45 a.m. ET, Dow e-minis were down 89 points, S&P 500 e-minis were down 9.25 points, and Nasdaq 100 e-minis were down 21.50 points. Energy stocks Occidental Petroleum and Exxon Mobil dropped 1.7% and 1% respectively in premarket trading, as oil prices retreated on concern about the pace of economic recovery and fuel demand.

In Europe, tech shares helped the Stoxx Europe 600 Index erase an earlier decline after Apple chipmaker TSMC posted revenue just above estimates for the June quarter. Carlsberg A/S climbed after it said the slump in western European beer sales has moderated. European stocks climbed to a session high, rising 0.7% as of noon London as all industry sectors turned positive. Autos lead gains, up 1.6%, with technology, chemicals and real estate among other subgroups rising 1% or more.

As noted above, Asian stocks fell, led by finance and materials, after rising in the last session. Trading volume for MSCI Asia Pacific Index members was 47% above the monthly average for this time of the day. The Topix declined 1.4%, with Voltage and Nomura falling the most. The Shanghai Composite Index retreated 1.95%, with Zheshang Bank and Genuine New posting the biggest slides

Attention now shifts to the second-quarter earnings season, which will begin with reports from big banks on Tuesday. Overall profits for S&P 500 firms are expected to plunge the most since the financial crisis.

In FX, the Dollar remains elevated after yesterday’s swift and sudden rebound on deteriorating sentiment surrounding fresh coronavirus outbreaks in the US and elsewhere, with the DXY getting very close to 97.000 again having fallen to a 96.233 low and failing to derive any initial momentum from encouraging weekly jobless claims data. However, the Greenback is paring some gains vs major counterparts ahead of PPI and the weekend as crude prices bounce on an upgrade in the IEA’s 2020 global oil demand forecast due to a smaller Q2 drop than previously envisaged. The yen rose versus all G-10 peers followed by the Swedish krona and Danish krone as the interbank market cleared out long positioning into the weekend, according to Asia-based FX traders. “The resurgence of the coronavirus, especially increased death tolls, is seen as a risk-off catalyst,” said David Lu, director at NBC Financial Markets Asia in Hong Kong. “That’s leading to yen buying.”

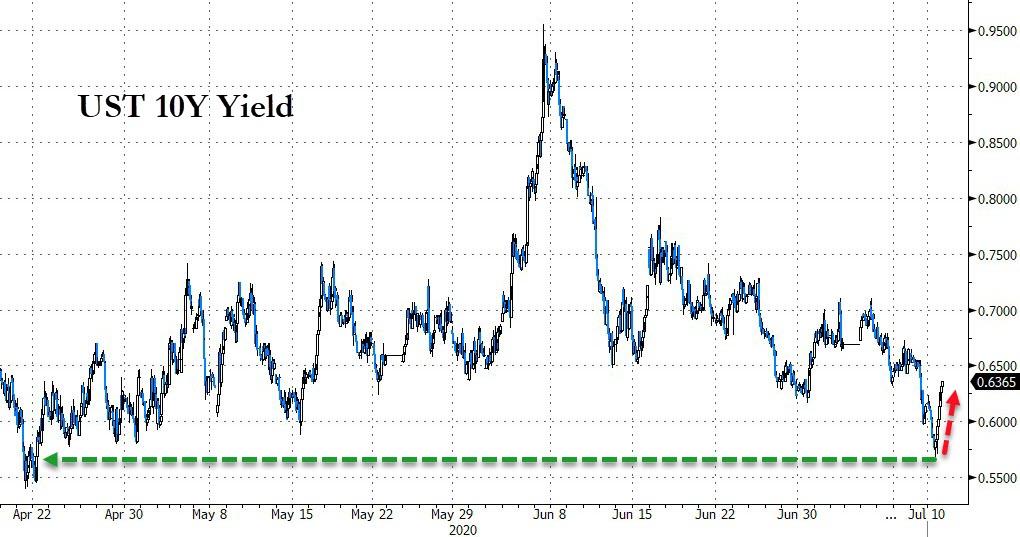

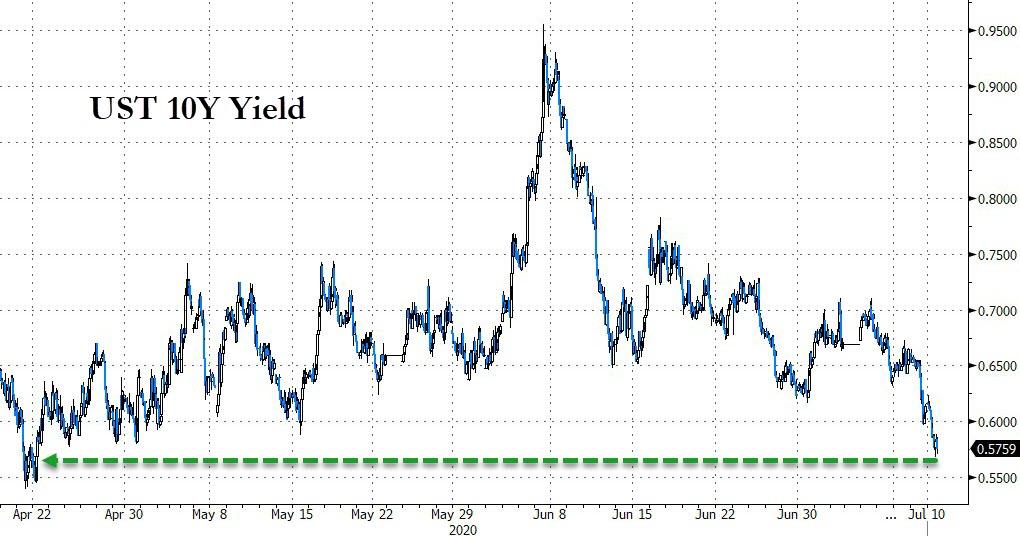

In rates, Treasuries resumed bull-flattening Friday as S&P 500 E-mini futures followed Asian equities lower weighing on risk sentiment. Even as 5-year yield touched a record low 0.256%, long-end outperformance sent 5s30s curve below 100bp for first time since May 15, approaching 100-DMA, support since mid-March. Treasury yields were lower by 1bp to 5bp across the curve, 10-year 0.586% after touching 0.568%, lowest since April 22 and within 3bp of a presumed convexity trigger level; it’s ~8bp lower on the week.

Elsewhere, oil traded around $39 a barrel in New York. In the U.K., yields on two- and five-year notes hovered near all-time lows amid speculation that the Bank of England may further ease monetary policy.

Looking at the day ahead, the data highlights include French and Italian industrial production for May, along with the Canadian jobs report for June and the June PPI reading from the US. We will also hear from the ECB’s Hernandez de Cos, while Singapore is holding a general election. Finally we could get more commentary on the Recovery Fund in Europe from the ECOFIN meeting press conference due at 13.15 CET.

Market Snapshot

- S&P 500 futures down 0.6% to 3,122.75

- STOXX Europe 600 up 0.2% to 364.52

- MXAP down 1% to 164.70

- MXAPJ down 1.1% to 547.53

- Nikkei down 1.1% to 22,290.81

- Topix down 1.4% to 1,535.20

- Hang Seng Index down 1.8% to 25,727.41

- Shanghai Composite down 2% to 3,383.32

- Sensex down 0.5% to 36,542.83

- Australia S&P/ASX 200 down 0.6% to 5,919.22

- Kospi down 0.8% to 2,150.25

- German 10Y yield fell 1.5 bps to -0.478%

- Euro up 0.02% to $1.1287

- Italian 10Y yield rose 2.2 bps to 1.097%

- Spanish 10Y yield unchanged at 0.408%

- Brent futures down 2.3% to $41.37/bbl

- Gold spot up 0.2% to $1,806.42

- U.S. Dollar Index little changed at 96.72

Top Overnight News

- China acted to cool the speculative frenzy in its $9.5 trillion stock market, ending a euphoric eight-day surge that had fueled worries of a new bubble in the making.

- The European Central Bank isn’t done expanding its bond-buying program yet, according to economists, despite recent remarks by policy makers that the outlook has brightened slightly.

- Oil fell as the International Energy Agency said a jump in Covid-19 cases could derail the market recovery, while Libya signaled the potential restart of crude exports.

Asian stock markets were negative following a lacklustre performance across global peers amid lingering coronavirus concerns and as US-China tensions were stoked by several escalatory reportssuch as the US enacting sanctions on 4 Chinese individuals for human rights abuses including the Xinjiang security bureau director and a top member of the Chinese Communist Party. ASX 200 (-0.6%) was led lower by underperformance in the energy sector after the recent pullback in oil prices and amid ongoing lockdown headwinds, with the Victoria state Treasurer anticipating GDP to decline 14%, although the downside for the index was stemmed by resilience in the tech sector which continued to ride on the work from home bandwagon. Nikkei 225 (-1.1%) was subdued by the weight of the haven currency inflows and with some large retailers pressured including Fast Retailing, Seven & I and Lawson after weaker earnings. Hang Seng (-1.8%) and Shanghai Comp. (-2.0%) underperformed after PBoC inaction resulted to a total CNY 290bln liquidity drain this week and as anti-China sentiment persisted with the Trump administration said to be finalising regulations this week that will bar US government from purchasing goods and services from several Chinese tech firms including Huawei and ZTE. Furthermore, it was also reported that China state funds were also said to plan cutting holdings in some companies including PICC. Finally, 10yr JGBs were slightly higher due to the weakness in stocks and following the bull flattening stateside in the aftermath of a blockbuster 30yr auction, while the BoJ were also present in the market today for JPY 870bln on JGBs with an emphasis on 1-3yr and 5-10yr maturities. China state funds are said to be planning to cut holdings in PICC and other China-listed firms, with China’s National Council for Social Security Fund planning to sell up to 884.5mln A-shares in PICC or a 2% stake valued around USD 1bln during the next 6 months, citing the need for asset allocation and investment.

Top Asian News

- China Points to Shrimp as Covid-19 Carrier After Salmon Debacle (Harvey: a joke!!)

- Tencent Is Said in Talks for Hong Kong-Listed Gaming Firm Leyou

- Philippine Lawmakers Deny TV Giant ABS-CBN’s Franchise Bid

- Empty Offices Growing in Tokyo as Virus Gives Tenants Pause

A choppy session for European equities as the region swings between gains and losses [Euro Stoxx 50 +0.2%] as sentiment somewhat improves from the downbeat APAC session in early hours. Europe opened with broad-based losses of some 0.5% but the upside coincided with the IEA oil market reported which raised its global oil demand growth forecasts which noted that demand decline in Q2 was less severe than expected. Furthermore, the unveiling of the compromise EU recovery fund underpinned benchmarks amid attempts to narrow the rift among EU members, whilst unanimous backing is not needed, thus decreasing chances of a veto. Nonetheless, major bourses are mixed with no stand-out out/underperformer. Sectors are also mixed with little by way of a risk-tone to be derived, with the detailed breakdown providing no further meat on the bone. The IT sector outperforms following numbers from chip giant TSMC which topped revenue estimates; thus propping up fellow chip names such as STMicroelectronics (+5.0%), Infineon (+2%). The energy sector meanwhile remains the underperformer. Energy names meanwhile remain subdued amid price action in the complex with Shell (-0.7%) and BP (-0.3%). In terms of individual movers, LVMH (-0.7%) and Kering (-0.2%) are subdued amid source reports US may release a French tariff list targeting French wine, cheese and handbags, however, Pernod Ricard (+0.1%) holds its ground, potentially due to the recent announcement of French aid for the wine sector.

Top European News

- England Eases Virus Rules to Open Gyms, Allow Outdoor Arts

- ECB Seen Boosting Stimulus by December to Aid Fledgling Recovery

- Italy Is Said to Be In Talks to Buy Into Telecom Italia Network

- Dufry Retreats as MainFirst Cuts to Sell, Slaps on Street-Low PT

In FX, the Dollar remains elevated after yesterday’s swift and sudden rebound on deteriorating sentiment surrounding fresh coronavirus outbreaks in the US and elsewhere, with the DXY getting very close to 97.000 again having fallen to a 96.233 low and failing to derive any initial momentum from encouraging weekly jobless claims data. However, the Greenback is paring some gains vs major counterparts ahead of PPI and the weekend as crude prices bounce on an upgrade in the IEA’s 2020 global oil demand forecast due to a smaller Q2 drop than previously envisaged.

- JPY – Notwithstanding the Buck’s renaissance, demand for the Yen has pushed Usd/Jpy down through 107.00 and a multi-month bull level at 106.90 to expose 106.75 and deeper lows, while Jpy crosses are also depressed on the aforementioned renewed risk aversion.

- AUD/CAD/NZD – Hardly a surprise to see the activity/cyclical/commodity bloc underperforming, with the Aussie back around 0.6950, Loonie pivoting 1.3600 and Kiwi straddling 0.6550 having hit peaks around 0.7000, 1.3500+ and 0.6600 respectively on Thursday. Ahead for the Cad, jobs data for June will be watched closely for more signs of recovery following a rather downbeat Canadian economic and fiscal update.

- EUR/GBP – Both narrowly mixed vs the Dollar, but struggling to keep sight of round numbers relinquished when the Usd took flight late in the EU session yesterday, and with the Euro also capped by decent option expiry interest between 1.1300-10 (1 bn) and bearish Eur/Gbp impulses. On that note, Eur/Usd is also eyeing some technical levels in the form of the 200 HMA (1.1272) and a Fib retracement (1.1262).

- CHF/NOK/SEK – The Franc is softer across the board with any sign of safe haven positioning more than offset by the fact that SNB will be on the offer, while the Norwegian Crown is lagging due to the recoil in oil rather than inflation data that was somewhat mixed vs consensus. Conversely, the Swedish Krona is bucking risk-off leanings after Riksbank minutes reaffirming a high bar for reverting to a sub-zero repo rate and more likelihood of further stimulus via QE if required

In commodities, IEA raises 2020 oil demand forecast by 400k BPD to 92.1mln BPD; demand decline in Q2 was less severe than expected; 2021 demand rise is lower than previously expected due to improved 2020 recovery view; outlook skewed to the downside. Additionally, Global oil supply fell by 2.4mln BPD in June to a 9yr low. US production in May fell 1.3mln BPD MM and June fell by 500k BPD. Highlights that Libya’s oil production by end 2020 could be as much as 900k BPD higher than today.

US Event Calendar

- 8:30am: PPI Final Demand MoM, est. 0.4%, prior 0.4%; Final Demand YoY, est. -0.2%, prior -0.8%

- 8:30am: PPI Ex Food and Energy MoM, est. 0.1%, prior -0.1%; PPI Ex Food and Energy YoY, est. 0.4%, prior 0.3%

DB’s Jim Reid concludes the overnight wrap

“Back” and “hit” were needed by the market yesterday to restore rhythm after a choppy session of rising coronavirus cases, associated fears of further economic slowdowns, and potential political volatility. By the close, the S&P 500 was down by -0.56%. However following a Supreme court ruling concerning Mr Trump and also record fatalities being announced in some heavily affected US states, the index was down as much as -1.71% just prior to European markets closing. Following Europe closing their laptops, US stocks ground higher primarily on the strength of Technology and Consumer Discretionary stocks – the latter of which was primarily driven by Amazon (+3.29% yesterday). Once again that stark outperformance of tech stocks saw the NASDAQ as one of the few global indices positive on the day, up +0.53%. Over in Europe, the STOXX 600 gave up its weekly gains with a -0.77% decline, as other bourses including the FTSE 100 (-1.73%) and the CAC 40 (-1.21%) suffered losses too. The DAX (-0.04%) was almost the exception thanks to a +3.99% advance from SAP after the company reported stronger than expected preliminary results for Q2 revenue.

Overnight markets in Asia are trading down with the Nikkei (-0.25%), Hang Seng (-1.17%), Shanghai Comp (-1.05%), Kospi (-0.67%) and Asx (-0.33%) all seeing losses. Declines for Chinese markets came with news that two state-backed funds have said that they plan to trim holdings in a sign that the government wants to slow down the rally. In FX, the US dollar is up +0.17%. Futures on the S&P 500 are also down -0.23% while WTI crude oil prices are down c. -1%.

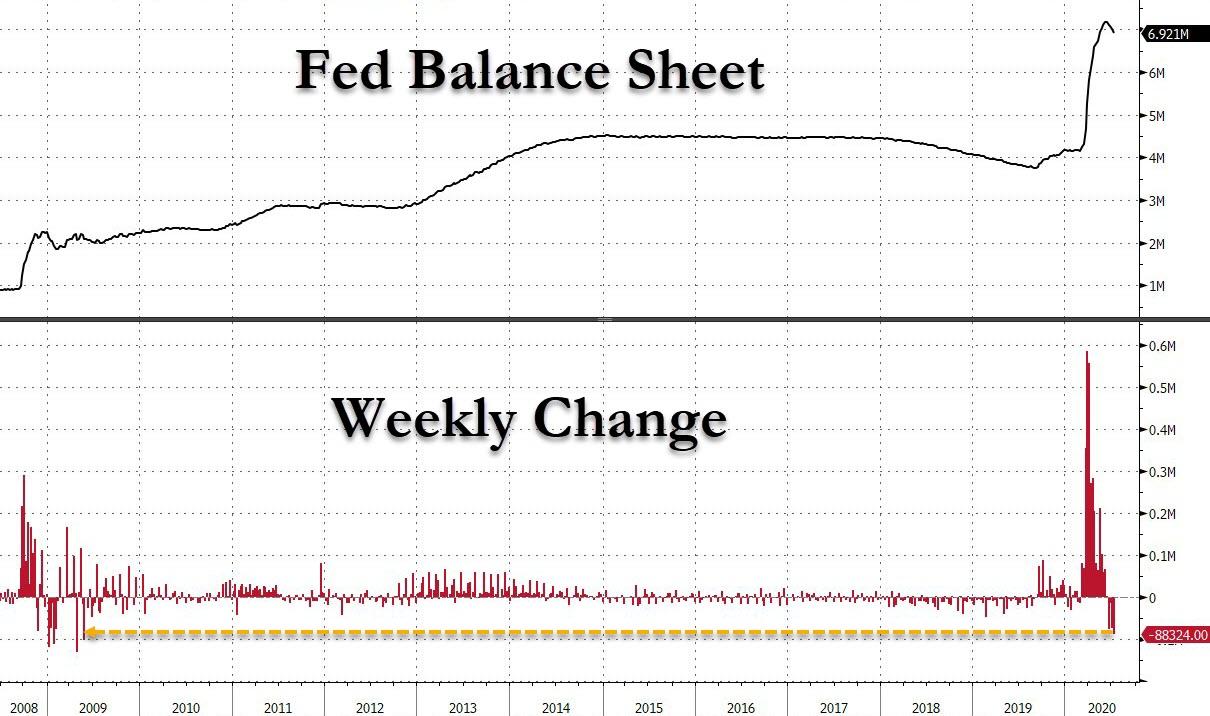

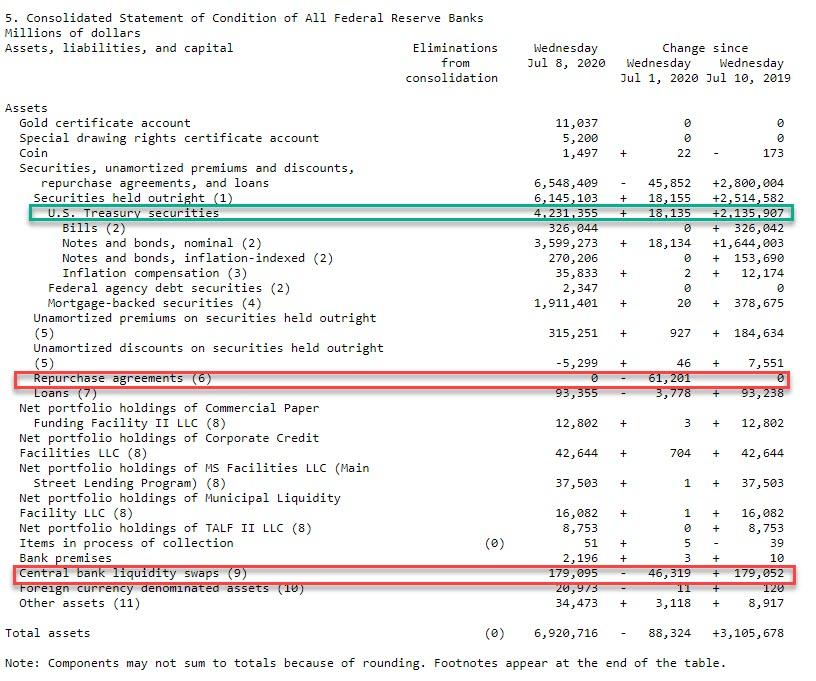

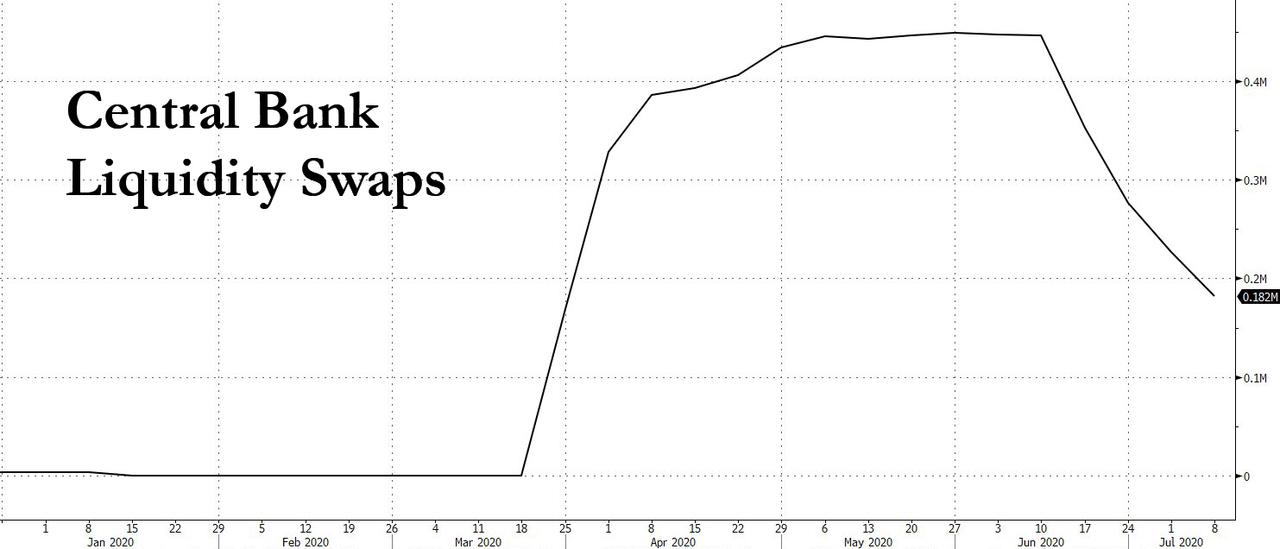

In other news, the Fed’s balance sheet shrank for a fourth week, with the total size back below $7 tn, as emergency loans extended to primary dealers and foreign central banks to shore up dollar liquidity at the depth of the COVID-19 crisis matured. Short-term cash loans to dealers and foreign central banks repurchase agreements, fell to 0 (vs. $442bn at peak in mid-March) in the week through July 8 while Foreign-exchange swaps with the US central bank’s counterparts abroad dropped to $179 bn (from $449bn at peak in end of May). The decline underscores some normalisation in the working of the financial markets since the peak of the crisis.

Yesterday brought further negative news on the coronavirus pandemic as the case numbers continued to rise across the world. In the US, new cases were over 80,000 for the first time, rising by +2.8%, the highest daily increase since May. Fatalities are starting to rise slowly as well but still not at the pace of the first wave. Florida reported a further 120 deaths in what was a daily record, while the number of cases rose by a further 4%, compared to the average weekly rise of 5%. California recorded a record one day rise in fatalities as well, however the Governor cautioned that the data included some delayed reporting. Cases in the state rose by over 11,000, above the 8040 7-day average. In Arizona, there was a further 3.7% rise or just over 4000 cases. This was the highest daily rise in a week, while the percentage increase was in-line with the 7-day average. Hopefully the somewhat slowing caseloads in these heavily affected states means that the recent acceleration of cases is slowing somewhat following some health measures being reinstituted over a week ago.

Here in the UK, we got the news that indoor gyms and swimming pools will be reopening from July 25. While some recreational team sports can begin as soon as this weekend, starting with cricket tomorrow. The club I am the President of (I’ve kinda retired) are playing their first matches tomorrow. They are very excited. Outdoor swimming pools can reopen tomorrow as well, with beauticians, salons and spas reopening Monday. However, in spite of Chancellor Sunak’s fresh economic support package the previous day, further retail job losses were announced, including 4,000 at Boots and another 1,300 at John Lewis. That’s 30,000 retail jobs lost over the last 2-3 weeks according to Sanjay Raja in our U.K. economics team.

One piece of more positive news yesterday came thanks to a better-than-expected reading from the US initial weekly jobless claims, which fell to 1.314m in the week through July 4 (vs. 1.375m expected). That’s the 14th consecutive week of falls since the peak of 6.867m back at the end of March, and the -99k reduction on the previous week is the biggest in 4 weeks. Furthermore, the continuing claims number for the previous week through June 27 was also better-than-expected at 18.062m (vs. 18.8m expected), with the insured unemployment rate falling to 12.4%, easing fears that the labour market recovery could be at risk of stalling. Nevertheless, it’s worth noting that the 1.314m initial claims figure is still well above the pre-Covid record of 695k, so there’s still a long way to go before a return to labour market normality.

Staying with the US, yesterday saw Democratic presidential nominee and former Vice President Joe Biden unveil the first part of his economic plan, with the tagline “Build Back Better”. The message was delivered in the swing state of Pennsylvania, not far from his childhood hometown of Scranton. Former VP Biden called for stricter new rules to “Buy American”, while leveraging tax and investment policy to create manufacturing jobs in the US, and reduce reliance on foreign supply chains. Mr. Biden’s plan specifically proposed a $300bn increase in government spending on research and development for new technologies like electric vehicles and 5G cellular networks, as well as an additional $400 billion in federal spending on US manufactured products. On the topic of paying for his economic plan as well as the recovery from the coronavirus, Mr. Biden has proposed to offset much of spending plans with nearly $4tr in tax raises. These would largely be done by reversing some of President Trump’s tax cuts.

Markets are likely to pay increasing attention to the former VP over the coming weeks, since his continued strong performance in the polls has forced investors to consider the implications of a Biden presidency, not just on domestic policy but also on what it could mean for global trade and the USA’s relations with China and the EU. Biden now leads President Trump by 9.5pts according to the FiveThirtyEight polling average, and this frontrunner status has been increasingly reflected in betting and prediction markets too, with both PredictIt (60%) and the Betfair Exchange (63%) now putting him in pole position for the White House. Meanwhile, the President got news that he will most likely be able to keep his personal financial records out of public record until after the November election, after the Supreme Court ruling blocked Congress from subpoenaing his records. The court ruled that federal appeals courts needed to close scrutinise Trump’s contentions that the document demands are unnecessary and would be too intrusive. In the other case, the Supreme Court ruled that a New York grand jury could receive President Donald Trump’s financial records, with the Chief Justice Roberts saying, “No citizen, not even the president, is categorically above the common duty to produce evidence when called upon in a criminal proceeding.” Regardless it is unlikely, Mr. Trump will see those documents unsealed prior to November. As noted above, the S&P fell -0.5% following the initial ruling, before the losses accelerated as elevated cases numbers were announced. The latter continues to be the potentially more damaging factor for the President’s reelection odds.

Turning elsewhere, core sovereign bonds rallied yesterday as investors sought out safe assets, with 10yr Treasury yields falling -5.1bps to close at 0.614%, their lowest level in over 2 months, just as the dollar strengthened by +0.28% in its biggest move up in 2 weeks. Bund yields saw their own -2.3bps move lower, while in the UK 5yr gilt yields fell by -1.9bps to a fresh record low of -0.06%. While we’re on the UK, we should mention that once again there seemed to be little progress in the Brexit negotiations, with the EU’s chief negotiator Michel Barnier tweeting yesterday that the latest discussions this week “confirm that significant divergences remain”.