GOLD:$1799.10 DOWN $11.75 The quote is London spot price

Silver:$18.62// DOWN 8 CENTS London spot price

Closing access prices: London spot

i)Gold : $1803.10 LONDON SPOT 4:30 pm

ii)SILVER: $18.67//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUG GOLD: $1806.40 CLOSE 1.30 PM// SPREAD SPOT/FUTURE AUG /: $7.70

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $18.97…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : 35 CENTS PER OZ

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2600. usa per oz

and silver; $29.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 10/129

EXCHANGE: COMEX

CONTRACT: JULY 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,815.500000000 USD

INTENT DATE: 07/08/2020 DELIVERY DATE: 07/10/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 H GOLDMAN 2

118 H MACQUARIE FUT 26

152 C DORMAN TRADING 4

159 C ED&F MAN CAP 2

657 C MORGAN STANLEY 11

657 H MORGAN STANLEY 4

661 C JP MORGAN 10

690 C ABN AMRO 2

737 C ADVANTAGE 46 17

800 C MAREX SPEC 76 41

878 C PHILLIP CAPITAL 3 3

905 C ADM 11

____________________________________________________________________________________________

TOTAL: 129 129

MONTH TO DATE: 6,107

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 129 NOTICE(S) FOR 12900 OZ (0.401 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 6107 NOTICES FOR 610700 OZ (18.99 TONNES)

SILVER

FOR JULY

27 NOTICE(S) FILED TODAY FOR 185,000 OZ/

total number of notices filed so far this month: 13,493 for 67.465 MILLION oz

BITCOIN MORNING QUOTE $9287 UP 30

BITCOIN AFTERNOON QUOTE.: $9390 DOWN $90

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $11.75 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES

GLD: 1,202.57 TONNES OF GOLD//

WITH SILVER DOWN 8 CENTS TODAY: AND WITH NO SILVER AROUND:

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTROUS PAPER DEPOSIT OF 8.198 MILLION OZ//

THIS IS A MASSIVE FRAUD

RESTING SLV INVENTORY TONIGHT:

SLV: 510.951 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A HUMONGOUS SIZED 6612 CONTRACTS FROM 169,513 UP TO 176,125, AND CLOSER T0 OUR NEW RECORD OF 244,710, (FEB 25/2020. THE HUGE SIZED GAIN IN OI OCCURRED WITH OUR 37 CENT GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS PRIMARILY DUE TO HUGE BANKER SHORT COVERING PLUS A FAIR EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A SMALL DECREASE IN SILVER STANDING AT THE COMEX FOR JULY. WE HAD A NET GAIN IN OUR TWO EXCHANGES OF 7790 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: JULY: 0 AND SEP 1178 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1178 CONTRACTS. WITH THE TRANSFER OF 1178 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1178 EFP CONTRACTS TRANSLATES INTO 5.890 MILLION OZ ACCOMPANYING:

1.THE 37 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

81.695 MILLION OZ INITIALLY IN JULY.

WEDNESDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 37 CENTS).. AND,OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS. THE HUGE GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A SMALL DECLINE IN STANDING OF SILVER OZ STANDING FOR JULY, STRONG BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A STRONG NET GAIN OF 7790 CONTRACTS OR 38.90 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

JULY

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF JULY:

4267 CONTRACTS (FOR 6 TRADING DAY(S) TOTAL 4267 CONTRACTS) OR 21.335 MILLION OZ: (AVERAGE PER DAY: 711 CONTRACTS OR 3.558 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 21.335 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 2.206% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,158.75 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 21,355 MILLION OZ/

EXCHANGE FOR PHYSICAL ISSUANCE FOR THE PAST 60 DAYS IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 6612, WITH OUR 37 GAIN IN SILVER PRICING AT THE COMEX ///WEDNESDAY… THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 1178 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A HUMONGOUS SIZED OI CONTRACTS ON THE TWO EXCHANGES: 7790 CONTRACTS (WITH OUR 37 CENT GAIN IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 1178 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A HUGE SIZED INCREASE OF 6,612 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED DESPITE A 37 CENT GAIN IN PRICE OF SILVER/AND A CLOSING PRICE OF $18.70 // WEDNESDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.8475 BILLION OZ TO BE EXACT or 121% of annual global silver production (ex Russia & ex China).

FOR THE NEW JULY DELIVERY MONTH/ THEY FILED AT THE COMEX: 27 NOTICE(S) FOR 135,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 81.695 million oz

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 3096 CONTRACTS TO 575,872 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE CONSIDERABLE SIZED GAIN OF COMEX OI OCCURRED WITH OUR STRONG GAIN IN PRICE OF $13.75 /// COMEX GOLD TRADING// WEDNESDAY// WE HAD HUGE BANKER SHORT COVERING, ANOTHER HUMONGOUS SIZED GOLD OZ STANDING AT THE COMEX FOR JULY, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR GAIN IN PRICE OF $13.75 .

WE HAD A VOLUME OF 8 4 -GC CONTRACTS//OPEN INTEREST 60

WE GAINED A STRONG SIZED 7188 CONTRACTS (22.36 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 4092 CONTRACTS:

CONTRACT .; AUG 2452 AND OCT: 1680 ALL OTHER MONTHS ZERO//TOTAL: 4092. The NEW COMEX OI for the gold complex rests at 575,872. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7188 CONTRACTS: 3096 CONTRACTS INCREASED AT THE COMEX AND 4092 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 8347 CONTRACTS OR 22.36 TONNES. WEDNESDAY, WE HAD A GAIN OF $13,75 IN GOLD TRADING……

AND WITH THAT GAIN IN PRICE, WE HAD A GOOD SIZED LOSS IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 22.36 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $13.75).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS ALSO UNSUCCESSFUL (SEE BELOW).

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4092) ACCOMPANYING THE CONSIDERABLE SIZED GAIN IN COMEX OI (3096 OI): TOTAL GAIN IN THE TWO EXCHANGES: 7188 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)ANOTHER HUMONGOUS INCREASE IN GOLD STANDING AT THE GOLD COMEX FOR THE FRONT JULY MONTH, 3) ZERO LONG LIQUIDATION; 4) CONSIDERABLE COMEX OI GAIN.. AND …ALL OF THIS WAS COUPLED WITH OUR STRONG GAIN IN GOLD PRICE TRADING//WEDNESDAY//$13.75.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

SPREADING OPERATIONS/NOW SWITCHING TO GOLD

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN GOLD AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF AUGUST FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF JULY. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUGUST), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

JULY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAY(S) IN TONNES: 53.85 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 53.85/3550 x 100% TONNES =1.51% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3081.58 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 53.85 TONNES SO FAR..

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A HUMONGOUS SIZED 6612 CONTRACTS FROM 169,513 UP TO 176,125 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE GIGANTIC OI GAIN IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) HUGE BANKER SHORT COVERING , 2) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A SMALL DECREASE STANDING AT THE SILVER COMEX FOR JULY AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 1178 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY: 0 CONTRACTS AND SEPT: 1178 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1178 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 6612 CONTRACTS TO THE 1178 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 7790 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 38.90 MILLION OZ, OCCURRED WITH THE 37 CENT GAIN IN PRICE///

RESULT: A HUGE SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 37 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// WEDNESDAY. WE ALSO HAD A FAIR SIZED 1178 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON PLUS HUGE FUTURE PREMIUMS OVER SPOT.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 47.15 POINTS OR 1.39% //Hang Sang CLOSED UP 80.98 POINTS OR 0.31% /The Nikkei closed UP 90.67 POINTS OR 0.40%//Australia’s all ordinaires CLOSED UP .67%

/Chinese yuan (ONSHORE) closed UP at 6.9857 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 6.9857 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9855 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS//PANDEMIC// : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

i)we had 0 deposits into the customer account

into JPMorgan: 0

ii) Into everybody else: 0

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.744 million oz of total silver inventory or 49.53% of all official comex silver. (160.819 million/324.954 million

total customer deposits today: nil oz

we had 2 withdrawals:

ii) Out of Brinks: 4299.500 oz

iii) Out of HSBC: 3035.65 oz

total withdrawals; 7335.15 oz

We had 0 adjustments

total dealer silver: 126.641 million

total dealer + customer silver: 324.954 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The front month of July has an open interest of 2882 contracts, as we lost 227 contracts. We had 203 notices served on WEDNESDAY, so we LOST a tiny 24 contracts or an additional 120,000 oz will NOT stand in this active delivery month of July as they received a London based forward and a fiat bonus for their effort.. They boys seem to have a problem serving upon our longs at the comex

The next month after July is the non active month of August and here sees its open interest rose by 110 contracts UP to 812

The big September contract month sees a GAIN of 5585 contracts UP to 139,314.

The total number of notices filed today for the JULY 2020. contract month is represented by 37 contract(s) FOR 185,000, oz

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 13,493 x 5,000 oz = 67,465,000 oz to which we add the difference between the open interest for the front month of JULY.(2882) and the number of notices served upon today 37 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the JULY/2019 contract month: 13,493 (notices served so far) x 5000 oz + OI for front month of JULY (2882)- number of notices served upon today (37) x 5000 oz of silver standing for the JULY contract month.equals 81,690,000 oz. (A WHOPPER )

WE LOST 24 CONTRACTS OR 120,000 OZ WILL NOT STAND FOR DELIVERY AS THERE SEEMS TO BE SCARCITY OF SILVER.

TODAY’S ESTIMATED SILVER VOLUME : 102,420 CONTRACTS // volume excellent/

FOR YESTERDAY: 92,179.,CONFIRMED VOLUME//volume very good/

YESTERDAY’S CONFIRMED VOLUME OF 92,179 CONTRACTS EQUATES to 460 million OZ 65.8% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO+ 0.12% ((JULY 9/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO +21% to NAV: (JULY 9/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into POSITIVE/ 0.12%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 17.22 TRADING 17.18///NEGATIVE 0.25

END

And now the Gold inventory at the GLD/

JULY 9//WITH GOLD DOWN $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OX 3.21 TONNES INTO THE GLD//INVENTORY RESTS AT 1202.57 TONNES

JULY 8/WITH GOLD UP $13.75 TODAY; A BIG CHANGE IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 7.89 TONNES INTO THE GLD//INVENTORY RESTS AT 1199.36 TONNES

JULY 7/WITH GOLD UP $12.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1191.47 TONNES

JULY 6/WITH GOLD UP $6.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1191.47 TONNES

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

JUNE 30//WITH GOLD UP $16.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1178.90 TONNES

JUNE 29/WITH GOLD UP $2.90 TODAY: A HUGE DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1178.90 TONNES

JUNE 26/WITH GOLD UP $5.03 TODAY: VERY STRANGE: A PAPER WITHDRAWAL OF 1.46 TONNES//INVENTORY RESTS AT 1175.39 TONNES

JUNE 25//WITH GOLD DOWN $3.30 TODAY//ANOTHER STRONG PAPER DEPOSIT OF 7.6 TONNES///INVENTORY RESTS AT 1176.85 TONNES

JUNE 24/WITH GOLD DOWN $1.50 TODAY; A STRONG 3.21 TONNES ADDED TO THE GLD//INVENTORY RESTS AT 1169.25 TONNES

JUNE 23/WITH GOLD UP $25.50 TODAY/ANOTHER CRIMINAL PAPER DEPOSIT OF 6.73 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1166.04 TONNES

JUNE 22/WITH GOLD UP $14.00 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 23.09 TONNES//INVENTORY RESTS AT 1159.31 TONNES

JUNE 19/WITH GOLD UP$16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//; INVENTORY RESTS AT 1136.22 TONNES

JUNE 18//WITH GOLD DOWN $2.75 TODAY: NO CHANGES IN GOLD INVENTORY: INVENTORY RESTS AT 1136.22 TONNES

JUNE 17/WITH GOLD DOWN $1.05: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1136.22 TONNES

JUNE 16//WITH GOLD UP $6.70 TODAY: NO CHANGES IN GOLD INVENTORY: /INVENTORY RESTS AT 1136.22 TONNES

JUNE 15/WITH GOLD DOWN ANOTHER $8.80 TODAY, NO CHANGES IN GOLD INVENTORY/INVENTORY RESTS AT 1136.22 TONNES

JUNE 12//WITH GOLD DOWN $1.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 1.17 TONNES AT THE GLD//INVENTORY RESTS AT 1136.22 TONNES

JUNE 11//WITH GOLD UP $16.80 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 6.55 TONNES AT THE GLD//INVENTORY RESTS AT 1135.05 TONNES

JUNE 10/WITH GOLD DOWN $.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 4.02 TONNES AT THE GLD/INVENTORY RESTS AT 1129.50 TONNES

JUNE 9//WITH GOLD UP $16.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 2.63 TONNES OF GOLD AT THE GLD//INVENTORY RESTS AT 1125.48 TONNES

JUNE 8//WITH GOLD UP $18.70 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 4.10 TONNES AT THE GLD//INVENTORY RESTS AT 1128.11 TONNES

JUNE 5//WITH GOLD DOWN $40.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A PAPER WITHDRAWAL OF 1.16 TONNES OUT OF THE GLD//INVENTORY RESTS AT 1132.21 TONNES

JUNE 4//WITH GOLD UP $20.60: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD…A DEPOSIT OF 4.09 TONNES INTO THE GLD//INVENTORY RESTS AT 1133.37 TONNES

JUNE 3//WITH GOLD DOWN $26.15//A SMALL CHANGE IN GOLD INVENTORY//A DEPOSIT OF 0.78 TONNES OF GLD INTO THE GLD//INVENTORY RESTS AT 1129.28 TONNES

JUNE 2//WITH GOLD DOWN $11.20 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1128.40 TONNES

JUNE 1//WITH GOLD UP $1.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES OF GOLD//GLD INVENTORY RESTS TONIGHT AT 1123.14 TONNES

MAY 29/WITH GOLD UP $19.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///GLD INVENTORY RESTS THIS WEEKEND AT 1119.05 TONNES

MAY 28//WITH GOLD UP $4.00 TODAY/NO CHANGES IN GOLD INVENTORY TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

MAY 27/WITH GOLD UP $.10 TODAY: A STRONG 2.34 TONNES OF GOLD ADDED TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

JULY 9/ GLD INVENTORY 1202.57 tonnes*

LAST; 856 TRADING DAYS: +258.75 NET TONNES HAVE BEEN ADDED THE GLD

LAST 756 TRADING DAYS://+436.86 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JULY 9/WITH SILVER DOWN 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 8.198 MILLION OZ INTO THE SLV/INVENTORY RESTS AT510.951 MILLION OZ/

JULY 8/WITH SILVER UP 37 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.118 MILLION OZ FROM THE SLV//VERY SURPRISING.//INVENTORY RESTS AT 502.753 MILLION OZ//

JULY 7/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/INVENTORY RESTS AT 503.871 MILLION OZ///

JULY 6//WITH SILVER UP 24 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.863 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 503.871 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

JUNE 30/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 29/WITH SILVER DOWN ONE CENT TODAY: A TWO CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 466,000 OZ TO PAY FOR STORAGE FEES AND INSURANCE//// AND A LARGE DEPOSIT OF 1.212 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 26/WITH SILVER UP 6 CENTS TODAY: ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ RESTS AT 491.858 MILLION OZ//

JUNE 25/WITH SILVER UP 12 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 931,000 OZ INTO THE SLV////INVENTORY RESTS AT 491.858 MILLION OZ//

JUNE 24///WITH SILVER DOWN 31 CENTS// NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 490.927 MILLION OZ

JUNE 23//WITH SILVER UP 16 CENTS TODAY: A MONSTROUS CHANGE IN INVENTORY: A PAPER DEPOSIT OF 4.473 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 490.927 MILLION OZ//

JUNE 22/WITH SILVER UP 15 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/: INVENTORY/INVENTORY RESTS AT 486/454 MILLION OZ//

JUNE 19//WITH SILVER UP 22 CENTS TODAY: STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 839,000 OZ FROM THE SLV////INVENTORY RESTS AT 486,454 MILLION OZ..

JUNE 18/WITH SILVER DOWN 16 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 932,000 OZ INTO THE SLV////INVENTORY RESTS AT 487.293 MILLION OZ

JUNE 17/WITH SILVER UP 8 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.261 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.361 MILLION OZ

JUNE 16//WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.118 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 483.100 MILLION OZ//

JUNE 15/WITH SILVER DOWN 14 CENTS NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 481.982 MILLION OZ///

JUNE 12/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: TWO DEPOSITS OF 7.269 MILLION OZ AND 1.802 MILLION OZ ADDED TO THE SLV///INVENTORY RESTS THIS WEEKEND AT 481.982 MILLION OZ//

JUNE 11//WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY: ///INVENTORY RESTS AT 472.89 MILLION OZ//

JUNE 10/WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.849 MILLION OZ//

JUNE 9/WITH SILVER DOWN 6 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.605 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 422.849 MILLION OZ//

JUNE 8/WITH SILVER UP 36 CENTS TODAY: TWO HUGE WITHDRAWALS OF 932,000 MILLION OZ AND 1.491 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 470.240 MILLION OZ//

JUNE 5/WITH SILVER DOWN 46 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 648,000 OZ FROM THE SLV////INVENTORY RESTS AT 472.663 MILLION OZ

JUNE 4//WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV.//INVENTORY RESTS AT 473.315 MILLION OZ//

JUNE 3//WITH SILVER DOWN 23 CENTS TODAY//NO CHANGES IN SILVER INVENTORY AT THE SLV//

INVENTORY RESTS AT 473.315 MILLION OZ//

JUNE 2//WITH SILVER DOWN 31 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUMONGOUS 6.686 MILLION OZ ADDED TO THE SLV////INVENTORY RESTS TONIGHT AT 473.315 MILLION OZ//

JUNE 1//WITH SILVER UP 38 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.56 MILLION OZ INTO THE SLV////INVENTORY RESTS TONIGHT AT 466.629 MILLION OZ//

MAY 29//WITH SILVER UP 52 CENTS TODAY: A MASSIVE DEPOSIT OF 2.796 MILLION OZ INTO THE SLV//INVENTORY RESTS THIS WEEKEND AT 463.273 MILLION OZ//

MAY 28//WITH SILVER UP 9 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.660 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 460.477 MILLION OZ//

MAY 27/WITH SILVER UP 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 455.817 MILLION OZ//

JULY 9.2020:

SLV INVENTORY RESTS TONIGHT AT

510.951 MILLION OZ.

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

in the dollar trading we have now experienced the “death cross” whereby the 50 day moving average crosses over the long term 200 day moving average. This is bad for the dollar

(Reuters/GATA)

‘Death Cross’ strikes U.S. dollar as virus cases grow

Submitted by cpowell on Thu, 2020-07-09 03:04. Section: Daily Dispatches

By Saqib Iqbal Ahmed

Reuters

Wednesday, July 8, 2020

NEW YORK — A resurgent coronavirus pandemic in the United States and the prospect of improving growth abroad are souring some investors on the dollar, threatening a years-long rally in the currency.

The dollar index is off 6% from its recent highs, while net bets against the currency in futures markets stand near their highest level since 2018.

…

A decline in the dollar earlier this week set off a technical formation known as a “Death Cross,” which occurs when the 50-day moving average crosses below the 200-day moving average, according to analysts at BofA Global Research.

Past occurrences of the Death Cross have been followed by a period of dollar weakness eight out of nine times since 1980 when the 200-day moving average has been declining, as it is now, analysts at the bank said.

The U.S. currency’s weakness comes amid criticism over the government’s response to the coronavirus pandemic and protests over racial inequality that has eroded support for President Donald Trump months before the Nov. 3 presidential election. At the same time, investors increasingly expect growth to accelerate in Europe, threatening to narrow an economic performance gap that has boosted the dollar for years. …

… For the remainder of the report:

https://www.reuters.com/article/us-health-coronavirus-dollar-analysis/de…

END

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

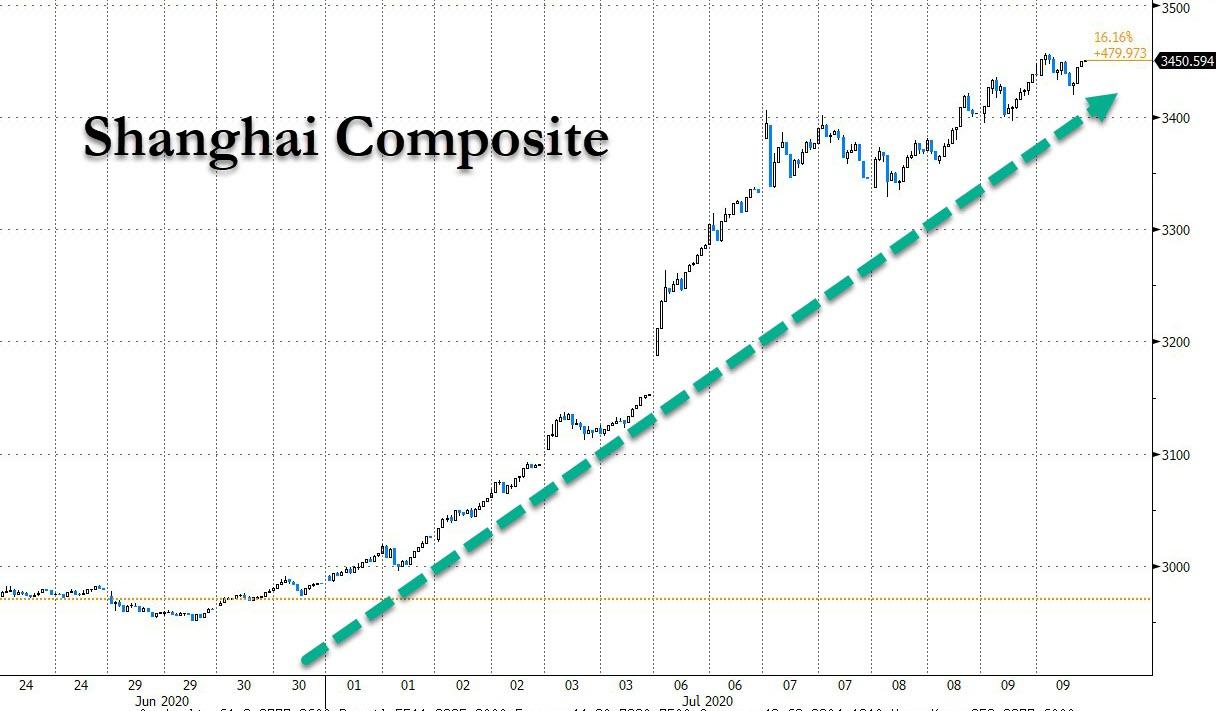

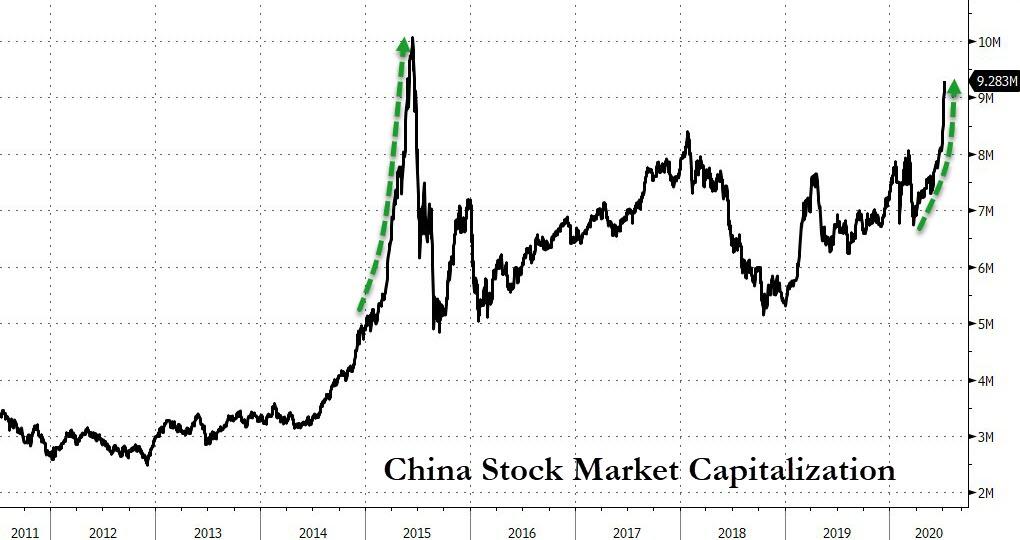

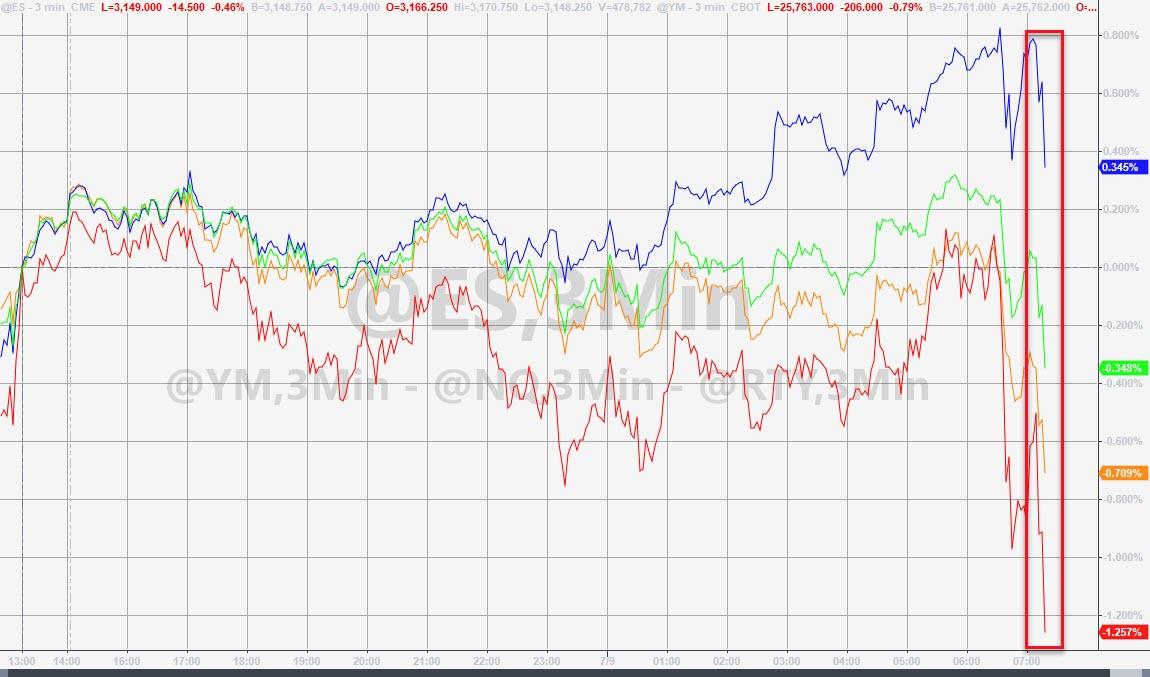

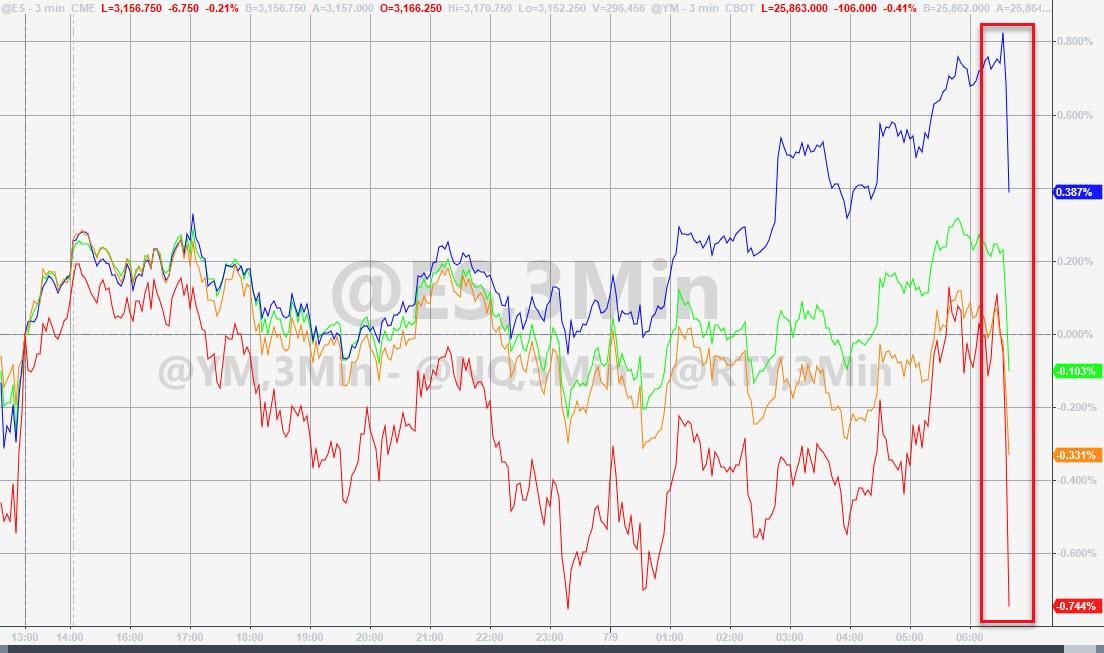

S&P Futures Flat As China’s Bubblemania Storms Higher For 8th Day

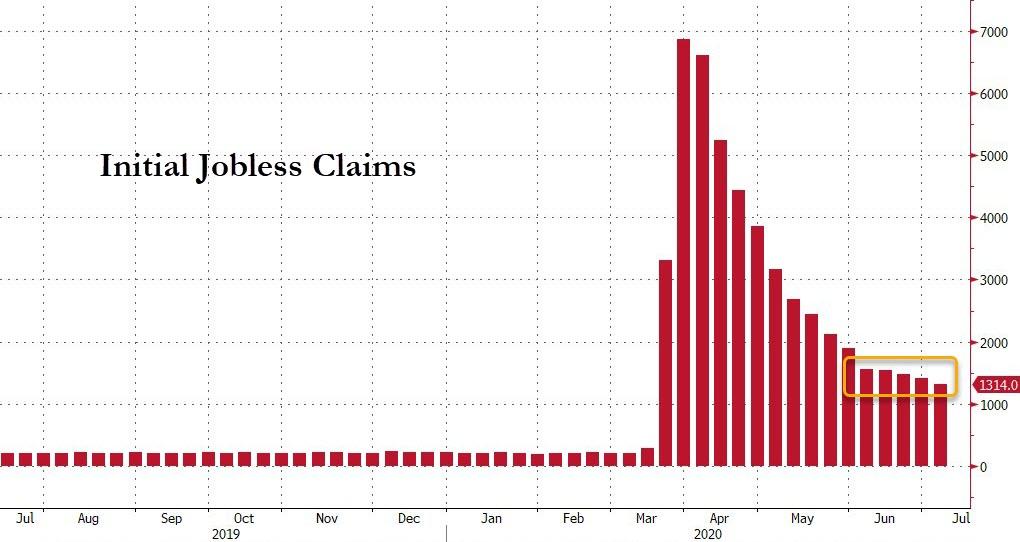

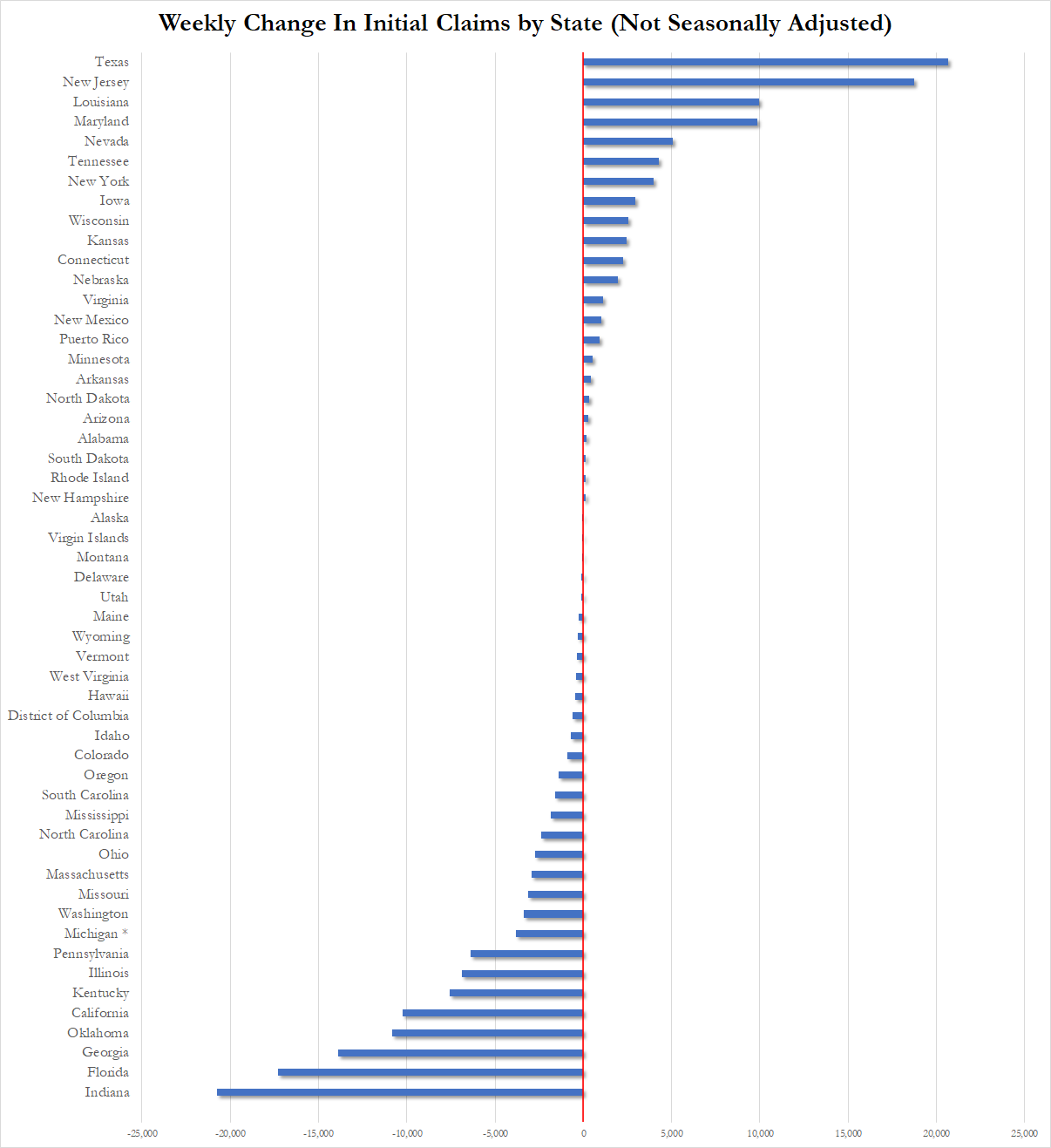

S&P futures were flat on Thursday, rebounded from an earlier dip in a low-volume session ahead of the closely watched weekly jobless claims report, with investors weighing the risk of another business shutdown amid soaring U.S. COVID-19 cases.

Despite the muted overnight session, the S&P 500 has now risen more than 40% from its March lows and is now about 7% below its February record high. The Labor Department’s most timely data on the economy is expected to show 1.38 million Americans filed for state unemployment benefits in the latest week, down from 1.43 million claims in the prior week. Cisco Systems rose 2% in premarket trading as Morgan Stanley upgraded its rating on the network gear maker’s stock to “overweight”. Walgreen’s slumped 3% after the company reported disappointing results with sales hit by the pandemic, announced it would suspend its buyback and cut 4,000 jobs. Best Buy was down 8.8% also as a result of sales and margin hits due to the pandemic.

The United States reported more than 60,000 new COVID-19 infections on Wednesday, setting a single day global record. And yet, investors continue to look past news of rising virus infections, concentrating on the continued reopening of economies. Confidence in policy support measures has mostly held firm, even as Hong Kong reported its biggest jump in cases since the start of the pandemic. The number of U.S. infections topped 3 million, more than a quarter of the global total.

“Risk is bouncing back broadly in equities but the real show is in Chinese equities, U.S. technology stocks and then gold,” said Saxo Bank CIO Steen Jakobsen. “U.S. Covid-19 cases rose yesterday to a new record and signs are now emerging that daily deaths are on the rise nationally which could suddenly become a new risk factor for the market.”

European stocks rose for the first time in three days, with shares in the region’s largest technology company, SAP SE, jumping over 7% after it reported better-than-expected second quarter revenue on returning demand for software in Asia.

Halfway across the world, the Chinese stock rally continued for an eighth day as margin debt soared to the highest level since 2015, even after authorities cracked down on margin financing platforms and state media warns of risks. The Shanghai Composite Index  rose 1.4%, with Xining Special Steel and Shanghai Sanmao Enterprise Group posting the biggest advances.

rose 1.4%, with Xining Special Steel and Shanghai Sanmao Enterprise Group posting the biggest advances.

Elsewhere in Asia, stocks gained led by communications and materials, after rising in the last session. Markets in the region were mixed, with Shanghai Composite and India’s S&P BSE Sensex Index rising, and Jakarta Composite and Singapore’s Straits Times Index falling. Trading volume for MSCI Asia Pacific Index members was 70% above the monthly average for this time of the day. The Topix was little changed, with FamilyMart rising and Aeon Financial falling the most. Hong Kong’s Hang Seng Index erased a gain after the news site HK01 reported that at least 16 new local virus cases were found Thursday.

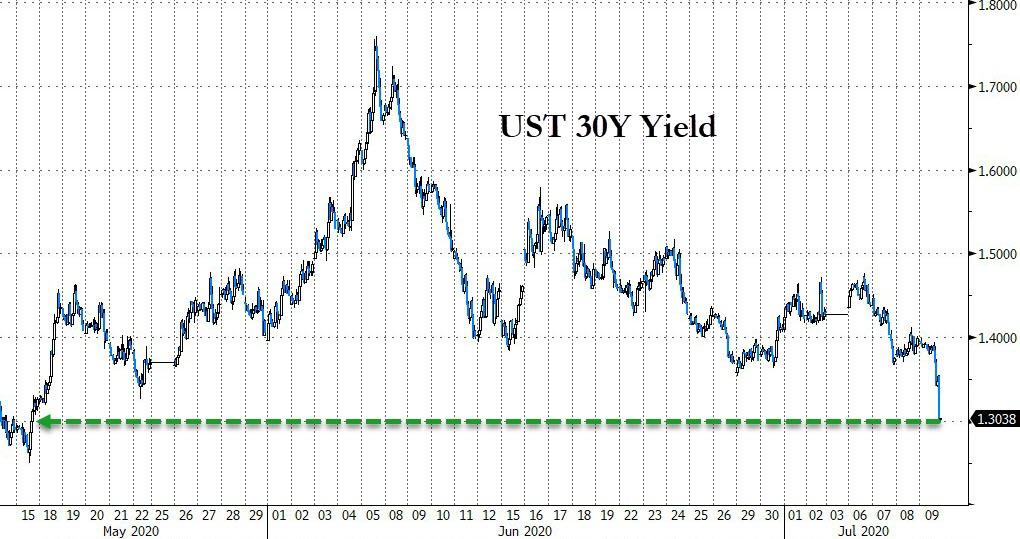

In rates, treasuries edged higher on low volume, with the 30Y auction at 1pm today. Yields from 5- to 30-year sectors lower on the day by 1bp-1.5bp, 10-year to ~0.65%, flattening 2s10s by ~1bp; bunds, gilts ~0.5bp cheaper on the day vs U.S. 10-year. Treasury yields richened slightly from belly to long end during Asia session and European morning in lackluster trading; front end little changed. Bunds, gilts lag. The week’s Treasury auction cycle concludes with $19BN 30-year reopening at 1pm ET; Wednesday’s 10-year reopening was well-bid, stopping 1bp below the WI yield at the bidding deadline at a record low yield.

In FX, the Bloomberg Dollar Index inched down to a three-week low as risk assets mostly held firm, dampening demand for the world’s reserve currency ahead of U.S. jobs data. Weaker-than-expected data on jobless claims would add to market concerns that the coronavirus outbreak is impacting the U.S. labor market recovery, according to Commonwealth Bank of Australia in note. EUR/USD climbed to a four-week high as investors bought the euro against the dollar and the yen, according to one FX trader. Chinese stocks led a rally in Asian equities after U.S. shares climbed on Wednesday.

“Amidst the improvement in economic data of late and the relatively buoyant market sentiment, a bearish consensus with the greenback seems to have been the case,” said Jingyi Pan, market strategist at IG Asia.

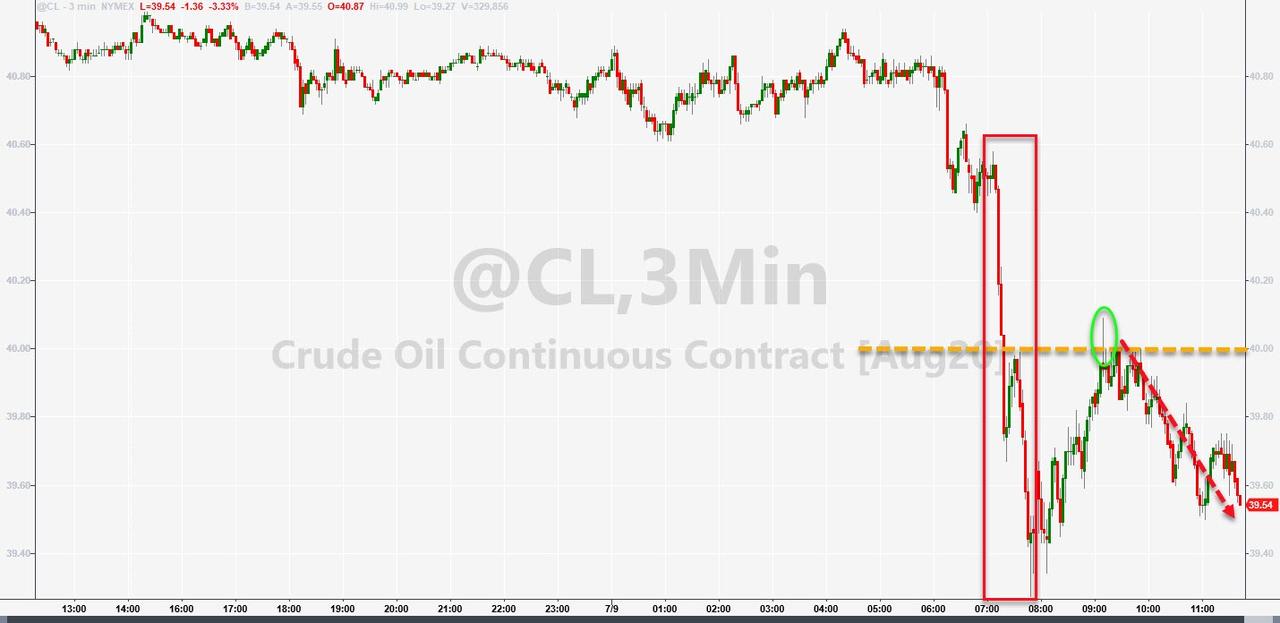

In commodities, oil was steady around $41 a barrel in New York after swelling U.S. crude stockpiles raised fresh concerns about oversupply. Silver rose above $19/oz with gold trading above $1800.

To the day ahead now, and the data highlights will include the weekly initial jobless claims from the US, along with Germany’s trade balance for May, Canadian housing starts for June. Elsewhere, we’ll hear from the Fed’s Bostic and the ECB’s Hernandez de Cos.

Market snapshot

- S&P 500 futures down 0.1% to 3,160.00

- MXAP up 0.6% to 166.19

- STOXX Europe 600 up 0.3% to 367.63

- German 10Y yield fell 0.6 bps to -0.446%

- Euro up 0.04% to $1.1335

- Italian 10Y yield fell 0.2 bps to 1.075%

- Spanish 10Y yield fell 0.6 bps to 0.404%

- MXAPJ up 0.7% to 552.43

- Nikkei up 0.4% to 22,529.29

- Topix unchanged at 1,557.24

- Hang Seng Index up 0.3% to 26,210.16

- Shanghai Composite up 1.4% to 3,450.59

- Sensex up 0.9% to 36,669.43

- Australia S&P/ASX 200 up 0.6% to 5,955.46

- Kospi up 0.4% to 2,167.90

- Brent futures up 0.1% to $43.35/bbl

- Gold spot up 0.3% to $1,814.94

- U.S. Dollar Index little changed at at 96.43

Top Overnight News

- Gold’s allure in 2020 continues to strengthen, with spot prices surpassing $1,800 an ounce and inflows into bullion-backed ETFs already topping the record full-year total set in 2009.

- European policy makers who frantically assembled plans to help their economies weather the coronavirus lockdowns are starting to focus on how to prevent cascading bankruptcies that could derail the rebound.

- Asian stocks pushed higher Thursday as investors continued to place faith in policy support and shrugged off simmering tensions between Washington and Beijing.

Asian equity markets traded mostly higher as the region took its cue from the positive rollover from US, where a late tech-led push helped all major indices finish in the green and lifted the Nasdaq to another record close on what had otherwise been predominantly indecisive session amid COVID-19 concerns. ASX 200 (+0.6%) and Nikkei 225 (+0.4%) were positive with gains in Australia led by tech as the sector found inspiration from its counterparts stateside and with gold miners euphoric after spot prices of the precious metal rose above USD 1800/oz for the first time since 2011, while stocks in Tokyo remained afloat after better than expected Machinery Orders data which showed a surprise expansion of 1.7% M/M although upside was initially capped amid virus fears. Hang Seng (+0.3%) and Shanghai Comp. (+1.4%) began indecisive after the PBoC continued to refrain from liquidity operations and with Chinese press calling for investors to manage risks, but gradually advanced amid a more amicable tone from China as Foreign Minister Wang stated that US-China relations need a more positive message and that China is willing to develop ties with US based on sincerity, despite noting that relations face serious challenges. Furthermore, Alibaba shares were among today’s stellar performers to track the upside in its US listing following reports its unit Ant Financial plans a Hong Kong IPO despite a denial by the unit. Finally, 10yr JGBs were indecisive as gains in stocks saw prices stall around the 152.00 level and with participants side-lined ahead of today’s 5yr auction. Finally, 10yr JGBs were indecisive as gains in stocks saw prices stall around the 152.00 level but later eked mild gains following firm demand at the 5yr JGB auction result.

Top Asian News

- Australia Suspends Hong Kong Extradition Deal in Swipe at China

- India Plans to Raise $2.7 Billion Selling Stakes in Two Firms

- Top Hong Kong Official Says Pan-Dem Primary May Break New Law

European equities have somewhat diverged to trade mixed [Euro Stoxx 50 +0.5%] as the optimism seen during the APAC session, which initially reverberated across Europe, petered out for some indices. Sentiment overnight was more-so a function of the tech-led gains seen on Wall Street and rally among miners, whilst Chinese press called on investors to manage risks accordingly amid the recent gains seen in the Mainland and Hong Kong. On that front, and more-so from a technical standpoint, reports note that over 70% of the CSI300 have a 14-day RSI over 70 – i.e. an overbought signal. Back to Europe, the FTSE 100 (-0.1%) is the only core bourse in the red amid unfavourable currency dynamics coupled with some large-cap movers to the downside. Sectors are mixed with a cyclical bias, with the detailed breakdown also painting a similar picture. The IT sector heavily outperforms peers and the broader market amid SAP’s (+7.7%) prelim earnings in which it reiterated guidance and stated that business recovered more than expected in Q2, while its flagship cloud revenue rose 21% YY. SAP carries an almost-10% weighting in the DAX and as such, the German index outperforms regional peers. Elsewhere, Rolls-Royce (-7.0%) immediately reversed course after opening higher by 3%, originally stemming from a positive trading update at face-value, as the breakdown warned of a significant revenue drop over the next seven years. Elsewhere, Siemens (+1.0%) hold onto gains after reports shareholders will vote on its proposal to spin off 55% of Siemens Energy to them. Finally, Atlantia (-9.0%) shares were halted to the downside after Italy’s 5-Star Leader Di Maio said the Co’s motorway concessions need to be withdrawn.

Top European News

- Siemens CEO Says Spinoff Is Best Way to Boost Share Price

- Commerzbank Power Vacuum Set to Last as Board Extends Search

- WeWork Rival Workspace Is Losing More London Office Tenants

- ECB Should Examine Targeting Average Inflation, Villeroy Says

- Bulgarian Police Raid President Radev’s Offices

In FX, cable is consolidating gains on the 1.2600 handle in wake of Wednesday’s fiscal support measures from UK Chancellor Sunak, while Eur/Gbp probes stops and support said to be sitting sub-0.8970 on positive Brexit vibes following EU chief negotiator Barnier conceding some ground on post-transition zonal arrangements, prompting more short covering of oversold Sterling positions. However, resistance looms ahead of the next round number in the form of a Fib retracement level at 1.2680 and then the 200 DMA at 1.2698.

- NZD/AUD – The Kiwi and Aussie continue to benefit from Greenback weakness alongside upturns in broad risk sentiment that are compensating/offsetting negatives for the latter via the COVID-19 related problems in Melbourne, Victoria that has now prompted Tasmania to extend its state of emergency. Nzd/Usd has advanced closer to 0.6600 with independent impetus coming from an improvement in ANZ business sentiment and even more pronounced rebound in the activity outlook, while Aud/Usd has retested 0.7000 as the Aud/Nzd cross hovers above 1.0600. Conversely, the DXY is struggling to retain sight of 96.500 having dipped below support to 96.233 in the run up to the latest US initial claims data and wholesale inventories, as the Buck remains prone to safe haven unwinding and the ongoing spiral in coronavirus infections/deaths in several hotspots.

- CAD/CHF/EUR/JPY – All narrowly mixed and still eyeing Usd moves alongside the general market tone, but the Loonie also conscious of decent option expiry interest between 1.3495-1.3500 (1 bn) and the 200 DMA (bang on 1.3500) ahead of Canada’s June leading index that follow’s yesterday’s economic and fiscal snapshot. Meanwhile, the Franc is meandering around 0.9375 and 1.0635 vs the Euro that pivots 1.1350 against the Dollar amidst expiries extending from 1.1300 (1.8 bn) through 1.1350-60 (1 bn) to 1.1375 (1.1 bn). Elsewhere, the Yen has eked gains towards 107.00 having been confined to a relatively tight range either side of 107.50, but could yet gravitate back given 1.1 bn option expiry for the NY cut, and with Jpy crosses firmer in line with the overall risk tone.

- SCANDI/EM – Indecisive and choppy trade across the board, but currencies mostly on the up and especially the Yuan that has made a more concerted 7.0000+ break following a PBoC midpoint fixing very close to the level and yet more strength in Chinese stock indices overnight.

In commodities, WTI and Brent front month futures trade choppy within tight ranges with price action somewhat lacklustre amid a lack of newsflow for the complex coupled with a number of bearish factors including this week’s inventory releases. News-flow for the complex has been light in early trade, although on the geopolitical front, one to keep on the radar would be the escalating tensions between Saudi and the Houthis, with the latest reports nothing that a Saudi-led coalition in Yemen have reportedly struck and destroyed two explosive laden-boats south of the port of Al Salif, according to Saudi TV. Nonetheless, crude prices remain flat/modestly softer with WTI Aug just above USD 40.50/bbl and Brent Sep keeps its head above USD 43/bbl. Elsewhere, spot gold retains at USD 1800/oz+ status having touched a recent high of USD 1816/oz. Shanghai copper hit a 16-month high on supply woes coupled with a firm performance in Chinese markets, whilst Dalian iron ore extended gains for a fifth straight day as steel mills replenish inventories on higher demand hopes.

US Event Calendar

- 8:30am: Initial Jobless Claims, est. 1.38m, prior 1.43m

- 8:30am: Continuing Claims, est. 18.8m, prior 19.3m

- 9:45am: Bloomberg Consumer Comfort, prior 43.3

- 10am: Wholesale Trade Sales MoM, est. 4.5%, prior -16.9%; Wholesale Inventories MoM, est. -1.2%, prior -1.2%

DB’s Jim Reid concludes the overnight wrap

In terms of yesterday’s market moves, one of the major headlines was the continued rally in gold, with the precious metal surpassing $1800/oz yesterday for the first time since 2011, before closing at a fresh 8-year high of $1809/oz. As we’ve written about in our monthly performance reviews, gold has been one of the strongest performing assets on a YTD basis in 2020 – up +19.22%. In many ways this isn’t surprising given central banks are printing money like it is going out of fashion. See Tuesday’s CoTD here showing that US money supply is up 25% yoy – only the 10th time above 20% in last 190 years of data.

Other metals continued to perform strongly too yesterday, with silver advancing by +2.45% yesterday to its own 4-month high, with the industrial bellwether of copper (+0.71%) up for a 7th straight session and to a new 5-month high. For more on the outlook for commodities see our strategists’ new note linked here. Notably our team has upgraded their 2021 gold target to $2000/oz, while shifting to a bullish Crude bias.

As gold and other metals advanced, US equity markets had a tough early session falling over 1% as several US states again announced elevated case counts. However, a steady recovery to just above flat was given a late boost in the last couple of hours of the day. It is possible that the late rally was partly due to Fed Reserve Bank of Atlanta President Bostic saying that the current pace of virus infections may warrant further policy action by either the central bank or Congress. With that the S&P 500 ended the session up +0.78% with another strong performance from tech stocks which saw the NASDAQ rise a further +1.44% and to a new record. Europe underperformed significantly however having been long closed before sentiment got a boost. The STOXX 600 ending the session down -0.67%, as other bourses experienced even larger declines, including the DAX (-0.97%) and the CAC 40 (-1.24%). Banks were among the laggards once again with the STOXX Banks index falling a further -2.12%. It was the reverse picture in fixed income though, with US Treasuries losing ground as European sovereign bonds advanced. By the close, 10yr Treasury yields had risen +2.5bps, in contrast to bunds which fell -1.1bps. BTPs were fairly flat to bunds.

Asian markets are trading higher this morning following Wall Street’s lead with the Nikkei (+0.59%), Hang Seng (+0.47%), Shanghai Comp (+1.03%; marking 8 days of consecutive gains), Kospi (+0.78%) and ASX (+1.07%) all posting gains. In Fx, the US dollar index is down a further -0.13% after yesterday’s -0.47% decline. Meanwhile, futures on the S&P 500 are trading flat. In terms of data out overnight, China’s June CPI printed in line with consensus at +2.5% yoy while PPI came in at -3.0% yoy (vs. -3.2% yoy expected).

In other news, Bloomberg reported overnight that Joe Biden will call for a moderate approach toward reviving the U.S. economy if elected President that includes spurring manufacturing and encouraging innovation, shelving for now the more ambitious proposals pushed by progressive Democrats. He is likely to deliver an economic speech today framing his argument for the rest of the campaign. As an aside the challenges going forward were further highlighted yesterday as United Airlines notified 45% of its workforce (36,000 employees in total) that their jobs are at risk after federal payroll aid expires at the end of September.

On the coronavirus, there weren’t a great deal of fresh headlines yesterday, though we saw yet further case increases in the US, with Florida and Arizona rising by 4.7% and 3.3% respectively. The country overall has now passed 3 million cases, with daily cases now increasing by over 50,000 per day for the first time. For context, the peak in April saw 31,500 average cases per day. Texas posted its second record day of fatalities with a further 97 yesterday. The 7 day average rise in fatalities is now 1.9% per day, after being in a range between 1.3% and 1.5% for the last 3 weeks, so this bears paying attention to even if the lagged ratio of deaths to cases is still well below that of the first wave. Citing backlogs in some counties, the Governor of California announced that cases in the state rose by over 11,000, the largest one day rise yet. Positive test rates in the state are now up to 7% after being at 5% just 2 weeks ago. With caseloads rising, the New Jersey Governor said that he would issue an order for the public to wear masks outside where crowds are congregating, whilst here in the UK, one hospital in west London closed for emergencies following a Covid-19 outbreak there. Globally, cases have now crossed the 12 million mark and even in areas with a low number of cases there are still fears. Indeed Hong Kong’s government has expressed worries that the city might be in the early days of a wider outbreak. Hong Kong has seen 118 new cases since June 30 and reported 19 new community transmissions yesterday.

Elsewhere disputes emerged in the US over school reopenings, with President Trump tweeting that he disagreed with the CDC’s school reopening guidelines, referring to them as “very tough & expensive”. Meanwhile NYC mayor de Blasio said on schools that he anticipated a “blended” learning program that would see students in class 2-3 days each week once school restarts in September, though Governor Cuomo announced he will be making a final decision on NY schools in early August.

Back to the U.K., Chancellor Sunak announced a fresh package of fiscal stimulus measures to bolster the recovery, which could be worth up to £30bn in total. In terms of the main announcements, the biggest is potentially the job retention bonus, whereby employers who bring back furloughed workers can qualify for a £1,000 bonus per employee, provided certain conditions are met. In theory, if all 9.4m furloughed jobs were retained, then this could be worth £9.4bn. The other main highlights include a temporary 9-month VAT cut from 20% to 5% for hospitality, accommodation and attractions, as well as a temporary Stamp Duty cut (the tax paid on home purchases) that will see the threshold rise to from £125k to £500k up to the end of March. And finally, though it was far from the costliest measure announced, one of the most headline-grabbing was an “Eat Out to Help Out” scheme whereby diners will get a 50% discount of up to £10 per head when eating out, valid Monday to Wednesday throughout August. The Early Morning Reid will come live from the terrace at my golf course opposite my house early in the week in August. For more on the Chancellor’s announcement see out UK economists note here.

On the longer term implications, it’s worth noting that in spite of the fiscal largesse yesterday, Sunak said that “over the medium term, we must, and we will, put out public finances back on a sustainable footing.” So clearly a nod towards future fiscal tightening now that the national debt is over 100% of GDP for the first time since 1963. Furthermore, there was also the acknowledgement that the furlough scheme “cannot and should not go on forever.” We should hear more this autumn when we get the next Budget and Spending Review from the UK government. For what it’s worth I suspect governments (including the U.K.) will talk a tough game on fiscal discipline going forward but the reality is that the fiscal genie is now out of the bottle and we’re set for a decade of MMT and helicopter money type policies. We will see.

To the day ahead now, and the data highlights will include the weekly initial jobless claims from the US, along with Germany’s trade balance for May, Canadian housing starts for June, and Japan’s preliminary machine tool orders reading for June. Elsewhere, we’ll hear from the Fed’s Bostic and the ECB’s Hernandez de Cos.

3A/ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 47.15 POINTS OR 1.39% //Hang Sang CLOSED UP 80.98 POINTS OR 0.31% /The Nikkei closed UP 90.67 POINTS OR 0.40%//Australia’s all ordinaires CLOSED UP .67%

/Chinese yuan (ONSHORE) closed UP at 6.9857 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 6.9857 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9855 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS//PANDEMIC// : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

CHINA VS USA

The war escalates; USA sanctions 4 Chinese nationals under the “Magnitsky Act”

(zerohedge)

US Sanctions 4 Chinese Nationals Under ‘Magnitsky Act’

Following a series of reports claiming that the White House was weighing sanctions against Chinese officials under the “Magnitsky Act”, ironically a law passed to target corruption in Russia.

The sanctions affected 4 individuals, and one company.

Here’s the statement from Treasury, which is responsible for implementing economic sanctions:

CHEN, Quanguo (Chinese Simplified: 陈全国), Xinjiang, China; DOB 1955; POB Pingyu, Henan, China; Gender Male (individual) [GLOMAG].

HUO, Liujun (Chinese Simplified: 霍留军), Xinjiang, China; DOB 1952; Gender Male (individual) [GLOMAG].

WANG, Mingshan (Chinese Simplified: 王明山), Xinjiang, China; DOB Jan 1964; POB Wuwei, Gansu, China; Gender Male (individual) [GLOMAG].

ZHU, Hailun (Chinese Simplified: 朱海仑), Xinjiang, China; DOB Jan 1958; POB Lianshui, Jiangsu, China; Gender Male (individual) [GLOMAG].

The following entity has been added to OFAC’s SDN List:

XINJIANG PUBLIC SECURITY BUREAU (Chinese Simplified: 新疆公安局) (a.k.a. PUBLIC SECURITY DEPARTMENT OF THE AUTONOMOUS REGION; a.k.a. PUBLIC SECURITY DEPARTMENT OF XINJIANG UYGAR AUTONOMOUS REGION; a.k.a. PUBLIC SECURITY DEPARTMENT OF XUAR; a.k.a. XINJIANG BUREAU OF PUBLIC SECURITY), Xinjiang, China [GLOMAG].

* * *

Source: Treasury

According to Secretary of State Mike Pompeo, the sanctions make the individuals “ineligible” for entry into the US.

The decision will likely provoke a response from Beijing beyond just the angry rhetoric they often employ, as President Xi and top Communist Party officials have specifically denounced American economic sanctions on individuals and Chinese companies as “politically motivated” attempts to undercut the Chinese economy.

Notably, the move follows the UK’s decision to use new “Magnitsky” powers adopted by the British government to impose sanctions on individuals involved in “human rights abuses” from Russia, Saudi Arabia, North Korea and Myanmar. Those targeted include senior Saudi intelligence officials believed to have been involved in the Khashoggi murder, as well as Russian officials implicated in the death of Sergei Magnitsky, a lawyer who died in a Moscow prison after purportedly uncovering a massive fraud.

Both President Xi and President Putin have criticized the US for abusing its sanction powers, claiming that the end result will be more countries shying away from the greenback and using other currencies (the ruble, perhaps. or just straight gold) to store foreign reserves.

One twitter user offered some insight into who these men are. All of them, it seems, are senior CCP officials; one is a chief of police in Xinjiang, where nearly a million Muslims are believed to be held in captivity.

Sec Chen is being cited as the biggest name on the list, since he’s the senior CCP official in Xinjiang.

The decision comes two days after FBI director Christopher Wray revealed that half of the bureau’s investigations involved Chinese entities. The FBI director, who has taken flack for not kowtowing to Trump, also described China as America’s “greatest threat”.

CORONAVIRUS UPDATE/HONG KONG/TOKYO/THE GLOBE

Hong Kong, Tokyo Report New Single-Day Coronavirus Records; US Deaths Are Starting To Climb: Live Updates

Summary:

- US single-day tally tops 60k again

- Global total tops 12 million

- 7-day average death rate creeps higher

- Tokyo, Hong Kong report single-day highs of new cases

- India reported 22.7k new cases

- Victoria reports another 165 new cases

- Beijing slams US over WHO pullout

* * *

Wednesday was another brutal day for the US during the global coronavirus outbreak as all of the worst hit states in the sunbelt produced new single-day records ranging from the highest 7-day positivity rate (Florida) to new records for deaths (Texas), single-day cases (California) and hospitalizations (Arizona, Florida, Texas etc).

After the US reported more than 60k new cases on Tuesday for the first time, the country repeated that feat on Wednesday, essentially tying its record number from the prior day.

But as the COVID tracking project points out, the 7-day average for deaths is “creeping back up” after two days of deaths near 1,000 (on Monday, the US reported fewer than 500 deaths for the entire country).

As deaths continue falling in New England, the sun belt has more than compensated for it.

As we noted, the US also topped 3 million cases yesterday.

So far on Thursday, the bad news out of the US has apparently carried over to Asia, as Hong Kong and Tokyo both reported new single-day records of new cases, as new outbreaks in both territories have come roaring back in recent weeks. Both areas are closely watched bellwethers of the outbreak in East Asia.

Tokyo confirmed 224 new infections on Thursday, its largest single-day tally yet. While Tokyo has focused its virus suppression efforts on nightlife districts, more mundane places like diners and – of course – nursing homes have seen several outbreaks.

The city’s mayor has said there are no plans to reinstate the state of emergency that was lifted in Tokyo last month.

Hong Kong health officials have warned of a third wave of coronavirus infections after the city recorded 23 new cases in two days. Social distancing measures in HK were largely lifted over the past two months as the city’s cases dwindled. An outbreak at a nursing home in Kowloon has contributed 8 infections to today’s total – four residents and four staff tested positive, on top of one resident who tested positive yesterday.

India reported 22,752 new cases, up slightly from 22,252 yesterday, bringing India’s virus total to 742,417. The death toll has jumped to 20,642, up 482.

Meanwhile, as tensions with Beijing intensify, with the White House mulling new retaliatory measures ranging from an assault on the HKD currency peg to barring the popular social media app TikTok, Beijing hurled a few rhetorical rocks Thursday morning when Foreign Ministry spokesperson Zhao Lijian slammed the Trump Administration’s decision to withdraw was “another demonstration of the US pursuing unilateralism, withdrawing from groups and breaking contracts.”

The WHO is “the most authoritative and professional international institution in the field of global public health security,” Zhao said at a briefing Wednesday, adding that the US departure would hurt the developing world, the AP reports – contrasting America’s WHO withdrawal with President Xi’s promises of forgivable or zero-interest loans and bundles while supplying the developing world with the vaccine.

In Australia, Victoria, the worst-hit Australian state, recorded another 165 case, as an outbreak at a Melbourne high school emerged as the largest cluster in the country. Queensland state also closed its border to people fleeing a six-week lockdown in Melbourne. In addition to the lockdown, Victoria has effectively sealed its borders, while neighboring New South Wales has also shut its border with Victoria.

END

China has played the game of debt building it’s growth without giving time for equity creation. While such strategy works when income growth is faster than debt service to allow projection of success. The opposite is true when income growth becomes negative as debt service overwhelms cash availability.

China’ problems are augmented by having built worthless monuments of glory in empty cities which have become non performing assets causing cash removal and a lessened velocity in internal cash movements. The building of major infrastructure assets in foreign lands have become worthless non performing assets to unbridled ambitions of hegemony.

What is not well reported is that not all is well with the China Russia relationship as China is actively leveraging its’ friendship with Russia to ride decades of Russian diplomacy to build debt slaves in the Baltic countries and in Eurasia having become the largest investor in Kazakhstan in only the last 2 years.