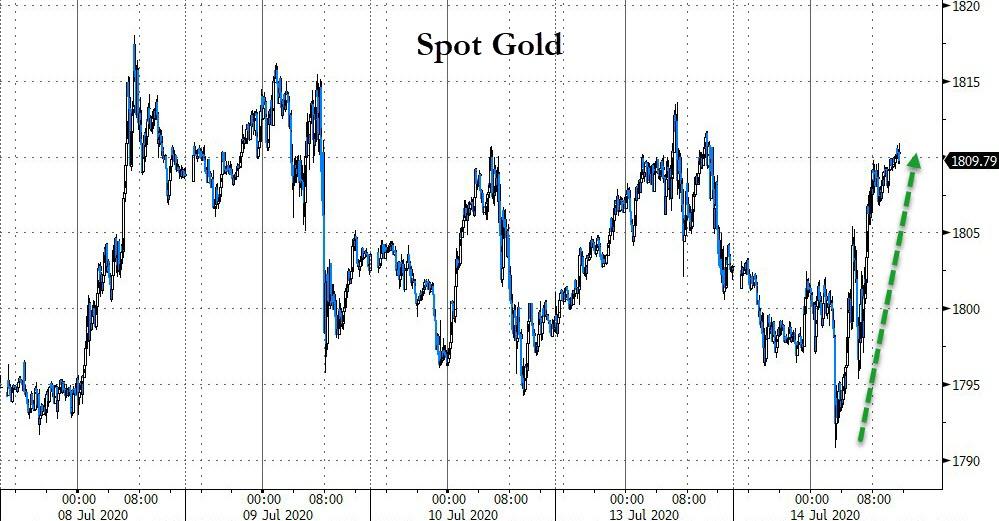

GOLD:$1809.75 DOWN $1.65 The quote is London spot price (cash market)

Silver:$19.15// DOWN 21 CENTS London spot price ( cash market)

Closing access prices: London spot

i)Gold : $1809.10 LONDON SPOT 4:30 pm

ii)SILVER: $19.25//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUG GOLD: $1813.70 CLOSE 1.30 PM// SPREAD SPOT/FUTURE AUG /: $3.95

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $19.55…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : 40 CENTS PER OZ

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today: 3/151

issued 0

EXCHANGE: COMEX

CONTRACT: JULY 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,811.000000000 USD

INTENT DATE: 07/13/2020 DELIVERY DATE: 07/15/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 H GOLDMAN 1

118 H MACQUARIE FUT 3

135 C RAND 1

135 H RAND 2

152 C DORMAN TRADING 67

332 H STANDARD CHARTE 76

355 C CREDIT SUISSE 48

657 C MORGAN STANLEY 11 2

657 H MORGAN STANLEY 1

661 C JP MORGAN 3

686 C INTL FCSTONE 1

690 C ABN AMRO 17

737 C ADVANTAGE 25 7

800 C MAREX SPEC 25 9

905 C ADM 3

____________________________________________________________________________________________

TOTAL: 151 151

MONTH TO DATE: 7,125

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 151 NOTICE(S) FOR 15100 OZ (.4696 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 7125 NOTICES FOR 712500 OZ (22.161 TONNES)

SILVER

FOR JULY

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 13,903 for 69.515 MILLION oz

BITCOIN MORNING QUOTE $9188 DOWN 54

BITCOIN AFTERNOON QUOTE.: $9256 UP $14

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $1.65 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.51 TONNES WAS ADDED TO GLD.

GLD: 1,203.97 TONNES OF GOLD//

WITH SILVER DOWN 21 CENTS TODAY: AND WITH NO SILVER AROUND:

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUGE PAPER WITHDRAWAL OF 1.677 MILLION OZ//

WHAT A FRAUD!!

RESTING SLV INVENTORY TONIGHT:

SLV: 514.118 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A STRONG SIZED 2416 CONTRACTS FROM 175,725 UP TO 178,141, AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE STRONG SIZED GAIN IN OI OCCURRED WITH OUR HUGE 67 CENT GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS PRIMARILY DUE TO HUGE BANKER SHORT COVERING PLUS A SMALL EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A SMALL INCREASE IN SILVER STANDING AT THE COMEX FOR JULY. WE HAD A NET GAIN IN OUR TWO EXCHANGES OF 2913 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: JULY: 0 AND SEP 497 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 497 CONTRACTS. WITH THE TRANSFER OF 497 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 497 EFP CONTRACTS TRANSLATES INTO 4.125 MILLION OZ ACCOMPANYING:

1.THE 67 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

81.645 MILLION OZ INITIALLY IN JULY.

MONDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 67 CENTS).. AND,OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS. THE STRONG GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A SMALL INCREASE IN STANDING OF SILVER OZ STANDING FOR JULY, STRONG BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A NET GAIN OF 2913 CONTRACTS OR 14,57 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

JULY

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF JULY:

6211 CONTRACTS (FOR 9 TRADING DAY(S) TOTAL 6211 CONTRACTS) OR 31.055 MILLION OZ: (AVERAGE PER DAY: 819 CONTRACTS OR 4.099 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 31.055 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 4.43% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,168.47 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 31.055 MILLION OZ/

EXCHANGE FOR PHYSICAL ISSUANCE FOR THE PAST 60 DAYS IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2416, WITH OUR 67 CENT GAIN IN SILVER PRICING AT THE COMEX ///MONDAY… THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 497 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A GOOD SIZED OI CONTRACTS ON THE TWO EXCHANGES: 2913 CONTRACTS (WITH OUR 67 CENT GAIN IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 497 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A STRONG SIZED INCREASE OF 2416 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED DESPITE A 67 CENT GAIN IN PRICE OF SILVER/AND A CLOSING PRICE OF $19.36 // FRIDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.891 BILLION OZ TO BE EXACT or 127% of annual global silver production (ex Russia & ex China).

FOR THE NEW JULY DELIVERY MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR nil OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 81.640 million oz

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 3262 CONTRACTS TO 571,683 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE SMALL SIZED GAIN OF COMEX OI OCCURRED WITH OUR STRONG GAIN IN PRICE OF $12.50 /// COMEX GOLD TRADING// MONDAY// WE HAD HUGE BANKER SHORT COVERING, ANOTHER HUMONGOUS SIZED GOLD OZ STANDING AT THE COMEX FOR JULY, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR GAIN IN PRICE OF $12.50 .

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 63

WE GAINED A STRONG SIZED 6227 CONTRACTS (19.37 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2965 CONTRACTS:

CONTRACT .; AUG 2265 AND OCT: 160 DEC: 300 ALL OTHER MONTHS ZERO//TOTAL: 2965. The NEW COMEX OI for the gold complex rests at 571,683. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6,227 CONTRACTS: 3262 CONTRACTS INCREASED AT THE COMEX AND 2965 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 6227 CONTRACTS OR 19.37 TONNES. MONDAY, WE HAD A GAIN OF $12.50 IN GOLD TRADING…...

AND WITH THAT GAIN IN PRICE, WE HAD A STRONG SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 19.37 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $12.50).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS ALSO UNSUCCESSFUL (SEE BELOW).

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2965) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (3262 OI): TOTAL GAIN IN THE TWO EXCHANGES: 6227 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)ANOTHER HUMONGOUS INCREASE IN GOLD STANDING AT THE GOLD COMEX FOR THE FRONT JULY MONTH, 3) ZERO LONG LIQUIDATION; 4) SMALL COMEX OI GAIN.. AND …ALL OF THIS WAS COUPLED WITH OUR STRONG GAIN IN GOLD PRICE TRADING//MONDAY//$12.50.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

SPREADING OPERATIONS/NOW SWITCHING TO GOLD

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN GOLD AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF AUGUST FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF JULY. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUGUST), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

JULY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES: 100.475 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 100.475/3550 x 100% TONNES =2.83% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3118.67 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 100.475 TONNES SO FAR..

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 2416 CONTRACTS FROM 175,725 UP TO 178,141 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE STRONG GAIN IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) HUGE BANKER SHORT COVERING , 2) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A SMALL INCREASE STANDING AT THE SILVER COMEX FOR JULY AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 497 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY: 0 CONTRACTS AND SEPT: 497 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 497 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2416 CONTRACTS TO THE 497 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 2913 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 14.57 MILLION OZ, OCCURRED WITH OUR HUGE 67 CENT GAIN IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 28.67 POINTS OR 0.83% //Hang Sang CLOSED DOWN 294.23 POINTS OR 1.14% /The Nikkei closed DOWN 197.73 POINTS OR 0.87%//Australia’s all ordinaires CLOSED DOWN .72%

/Chinese yuan (ONSHORE) closed DOWN at 6.9951 /Oil UP TO 39.73 dollars per barrel for WTI and 342.37 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9951 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0181 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS//PANDEMIC : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

i)we had 1 deposits into the customer account

into JPMorgan: 0

ii) Into Delaware: 3618.244 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.744 million oz of total silver inventory or 49.47% of all official comex silver. (160.819 million/324.624 million

total customer deposits today: nil oz

we had 2 withdrawals:

ii) Out of Loomis: 613,200.670 oz

iii) Out of Delaware: 4023.100 oz

total withdrawals; 617,223.770 oz

We had 5 adjustments

ALL dealer to customer:

Brinks 25,679.927 oz

CNT: 543,493.198 oz

Delaware: 53,250.270 oz

HSBC 39,316.210 oz

Scotia; 9,068.420 oz

total dealer silver: 126.708 million

total dealer + customer silver: 324.640 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The front month of July has an open interest of 2425 contracts, as we lost 238 contracts. We had 245 notices served on MONDAY, so we GAINED a tiny 7 contracts or an additional 35,000 oz will stand in this active delivery month of July as they refused to morph into a London based forwards. It seems that we have little silver over here.

The next month after July is the non active month of August and here sees its open interest rose by 18 contracts UP to 857

The big September contract month sees a gain of 2092 contracts up to 140,540.

The total number of notices filed today for the JULY 2020. contract month is represented by 0 contract(s) FOR nil, oz

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 13,903 x 5,000 oz = 69,515,000 oz to which we add the difference between the open interest for the front month of JULY.(2425) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the JULY/2019 contract month: 13,903 (notices served so far) x 5000 oz + OI for front month of JULY (2245)- number of notices served upon today (0) x 5000 oz of silver standing for the JULY contract month.equals 81,640,000 oz. (A WHOPPER )

WE GAINED 7 CONTRACTS OR 35,000 OZ WILL STAND FOR DELIVERY. SILVER IS STILL VERY SCARCE ON THIS SIDE OF THE POND AND THE REASON FOR MORPHING OVER TO LONDON.

TODAY’S ESTIMATED SILVER VOLUME : 72,517 CONTRACTS // volume good/

FOR YESTERDAY: 92,931.,CONFIRMED VOLUME//volume excellent/

YESTERDAY’S CONFIRMED VOLUME OF 92,931 CONTRACTS EQUATES to 464 million OZ 66.3% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO- 0.09% ((JULY 14/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -.18% to NAV: (JULY 14/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 0.09%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 17.42 TRADING 17.36///NEGATIVE 0.35

END

And now the Gold inventory at the GLD/

JULY 14//WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 3.51 TONNES/INVENTORY RESTS AT 1203.97 TONNES

JULY 13//WITH GOLD UP $12.50 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1200.46 TONNES

JULY 10/WITH GOLD DOWN $.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD//A STRANGE WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1200.82 TONNES

JULY 9//WITH GOLD DOWN $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OX 3.21 TONNES INTO THE GLD//INVENTORY RESTS AT 1202.57 TONNES

JULY 8/WITH GOLD UP $13.75 TODAY; A BIG CHANGE IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 7.89 TONNES INTO THE GLD//INVENTORY RESTS AT 1199.36 TONNES

JULY 7/WITH GOLD UP $12.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1191.47 TONNES

JULY 6/WITH GOLD UP $6.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1191.47 TONNES

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

JUNE 30//WITH GOLD UP $16.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1178.90 TONNES

JUNE 29/WITH GOLD UP $2.90 TODAY: A HUGE DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1178.90 TONNES

JUNE 26/WITH GOLD UP $5.03 TODAY: VERY STRANGE: A PAPER WITHDRAWAL OF 1.46 TONNES//INVENTORY RESTS AT 1175.39 TONNES

JUNE 25//WITH GOLD DOWN $3.30 TODAY//ANOTHER STRONG PAPER DEPOSIT OF 7.6 TONNES///INVENTORY RESTS AT 1176.85 TONNES

JUNE 24/WITH GOLD DOWN $1.50 TODAY; A STRONG 3.21 TONNES ADDED TO THE GLD//INVENTORY RESTS AT 1169.25 TONNES

JUNE 23/WITH GOLD UP $25.50 TODAY/ANOTHER CRIMINAL PAPER DEPOSIT OF 6.73 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1166.04 TONNES

JUNE 22/WITH GOLD UP $14.00 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 23.09 TONNES//INVENTORY RESTS AT 1159.31 TONNES

JUNE 19/WITH GOLD UP$16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//; INVENTORY RESTS AT 1136.22 TONNES

JUNE 18//WITH GOLD DOWN $2.75 TODAY: NO CHANGES IN GOLD INVENTORY: INVENTORY RESTS AT 1136.22 TONNES

JUNE 17/WITH GOLD DOWN $1.05: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1136.22 TONNES

JUNE 16//WITH GOLD UP $6.70 TODAY: NO CHANGES IN GOLD INVENTORY: /INVENTORY RESTS AT 1136.22 TONNES

JUNE 15/WITH GOLD DOWN ANOTHER $8.80 TODAY, NO CHANGES IN GOLD INVENTORY/INVENTORY RESTS AT 1136.22 TONNES

JUNE 12//WITH GOLD DOWN $1.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 1.17 TONNES AT THE GLD//INVENTORY RESTS AT 1136.22 TONNES

JUNE 11//WITH GOLD UP $16.80 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 6.55 TONNES AT THE GLD//INVENTORY RESTS AT 1135.05 TONNES

JUNE 10/WITH GOLD DOWN $.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 4.02 TONNES AT THE GLD/INVENTORY RESTS AT 1129.50 TONNES

JUNE 9//WITH GOLD UP $16.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 2.63 TONNES OF GOLD AT THE GLD//INVENTORY RESTS AT 1125.48 TONNES

JUNE 8//WITH GOLD UP $18.70 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 4.10 TONNES AT THE GLD//INVENTORY RESTS AT 1128.11 TONNES

JUNE 5//WITH GOLD DOWN $40.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A PAPER WITHDRAWAL OF 1.16 TONNES OUT OF THE GLD//INVENTORY RESTS AT 1132.21 TONNES

JUNE 4//WITH GOLD UP $20.60: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD…A DEPOSIT OF 4.09 TONNES INTO THE GLD//INVENTORY RESTS AT 1133.37 TONNES

JUNE 3//WITH GOLD DOWN $26.15//A SMALL CHANGE IN GOLD INVENTORY//A DEPOSIT OF 0.78 TONNES OF GLD INTO THE GLD//INVENTORY RESTS AT 1129.28 TONNES

JUNE 2//WITH GOLD DOWN $11.20 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1128.40 TONNES

JUNE 1//WITH GOLD UP $1.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES OF GOLD//GLD INVENTORY RESTS TONIGHT AT 1123.14 TONNES

MAY 29/WITH GOLD UP $19.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///GLD INVENTORY RESTS THIS WEEKEND AT 1119.05 TONNES

MAY 28//WITH GOLD UP $4.00 TODAY/NO CHANGES IN GOLD INVENTORY TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

MAY 27/WITH GOLD UP $.10 TODAY: A STRONG 2.34 TONNES OF GOLD ADDED TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

JULY 14/ GLD INVENTORY 1203.97 tonnes*

LAST; 860 TRADING DAYS: +260.15 NET TONNES HAVE BEEN ADDED THE GLD

LAST 760 TRADING DAYS://+438.26 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JULY 14/WITH SILVER DOWN 21 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 514.118 MILLION OZ//

JULY 13//WITH SILVER UP 67 CENTS TODAY: A HUGE CHANGE IN SILVER: A WITHDRAWAL OF 1.677 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 514.118 MILLION OZ//

JULY 10/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 4.844 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.795 MILLION OZ

WHAT A FRAUD!!

JULY 9/WITH SILVER DOWN 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 8.198 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 510.951 MILLION OZ/

JULY 8/WITH SILVER UP 37 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.118 MILLION OZ FROM THE SLV//VERY SURPRISING.//INVENTORY RESTS AT 502.753 MILLION OZ//

JULY 7/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/INVENTORY RESTS AT 503.871 MILLION OZ///

JULY 6//WITH SILVER UP 24 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.863 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 503.871 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

JUNE 30/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 29/WITH SILVER DOWN ONE CENT TODAY: A TWO CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 466,000 OZ TO PAY FOR STORAGE FEES AND INSURANCE//// AND A LARGE DEPOSIT OF 1.212 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 26/WITH SILVER UP 6 CENTS TODAY: ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ RESTS AT 491.858 MILLION OZ//

JUNE 25/WITH SILVER UP 12 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 931,000 OZ INTO THE SLV////INVENTORY RESTS AT 491.858 MILLION OZ//

JUNE 24///WITH SILVER DOWN 31 CENTS// NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 490.927 MILLION OZ

JUNE 23//WITH SILVER UP 16 CENTS TODAY: A MONSTROUS CHANGE IN INVENTORY: A PAPER DEPOSIT OF 4.473 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 490.927 MILLION OZ//

JUNE 22/WITH SILVER UP 15 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/: INVENTORY/INVENTORY RESTS AT 486/454 MILLION OZ//

JUNE 19//WITH SILVER UP 22 CENTS TODAY: STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 839,000 OZ FROM THE SLV////INVENTORY RESTS AT 486,454 MILLION OZ..

JUNE 18/WITH SILVER DOWN 16 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 932,000 OZ INTO THE SLV////INVENTORY RESTS AT 487.293 MILLION OZ

JUNE 17/WITH SILVER UP 8 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.261 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.361 MILLION OZ

JUNE 16//WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.118 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 483.100 MILLION OZ//

JUNE 15/WITH SILVER DOWN 14 CENTS NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 481.982 MILLION OZ///

JUNE 12/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: TWO DEPOSITS OF 7.269 MILLION OZ AND 1.802 MILLION OZ ADDED TO THE SLV///INVENTORY RESTS THIS WEEKEND AT 481.982 MILLION OZ//

JUNE 11//WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY: ///INVENTORY RESTS AT 472.89 MILLION OZ//

JUNE 10/WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.849 MILLION OZ//

JUNE 9/WITH SILVER DOWN 6 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.605 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 422.849 MILLION OZ//

JUNE 8/WITH SILVER UP 36 CENTS TODAY: TWO HUGE WITHDRAWALS OF 932,000 MILLION OZ AND 1.491 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 470.240 MILLION OZ//

JUNE 5/WITH SILVER DOWN 46 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 648,000 OZ FROM THE SLV////INVENTORY RESTS AT 472.663 MILLION OZ

JUNE 4//WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV.//INVENTORY RESTS AT 473.315 MILLION OZ//

JUNE 3//WITH SILVER DOWN 23 CENTS TODAY//NO CHANGES IN SILVER INVENTORY AT THE SLV//

INVENTORY RESTS AT 473.315 MILLION OZ//

JUNE 2//WITH SILVER DOWN 31 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUMONGOUS 6.686 MILLION OZ ADDED TO THE SLV////INVENTORY RESTS TONIGHT AT 473.315 MILLION OZ//

JUNE 1//WITH SILVER UP 38 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.56 MILLION OZ INTO THE SLV////INVENTORY RESTS TONIGHT AT 466.629 MILLION OZ//

MAY 29//WITH SILVER UP 52 CENTS TODAY: A MASSIVE DEPOSIT OF 2.796 MILLION OZ INTO THE SLV//INVENTORY RESTS THIS WEEKEND AT 463.273 MILLION OZ//

MAY 28//WITH SILVER UP 9 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.660 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 460.477 MILLION OZ//

MAY 27/WITH SILVER UP 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 455.817 MILLION OZ//

JULY 14.2020:

SLV INVENTORY RESTS TONIGHT AT

514.118 MILLION OZ.

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

The Fed’s 3 trillion rescue pkg inflates all market bubbles

(Reuters)

Fed’s $3 trillion virus rescue inflates market bubbles

Submitted by cpowell on Mon, 2020-07-13 15:02. Section: Daily Dispatches

By Kate Duguid

Reuters

Monday, July 13, 2020

The Federal Reserve’s $3 trillion bid to stave off an economic crisis in the wake of the coronavirus outbreak is fuelling excesses across U.S. capital markets.

The U.S. central bank has pledged unlimited financial asset purchases to sustain market liquidity, increasing its balance sheet from $4.2 trillion in February to $7 trillion today.

…

While the vast majority of these purchases has been limited to U.S. Treasuries and mortgage-backed securities, the Fed’s pledge to bolster the corporate bond market has been enough to spur a frenzy among investors for bonds and stocks.

“COVID-19 is now inversely related to the markets. The worse that COVID-19 gets, the better the markets do because the Fed will bring in stimulus. That is what has been driving markets,” said Andrew Brenner, head of international fixed income at NatAlliance. …

… For the remainder of the report:

https://www.reuters.com/article/us-health-coronavirus-federalreserve-mar…

end

GATA board member Ed Steer’s Saturday letter posted at SilverSeek

Submitted by cpowell on Mon, 2020-07-13 15:08. Section: Daily Dispatches

11:10a ET Monday, July 13, 2020

Dear Friend of GATA and Gold:

The Saturday edition of GATA board member Ed Steer’s letter, Ed Steer’s Gold and Silver Digest, is posted in the clear at GoldSeek’s companion site, SilverSeek, here:

https://silverseek.com/article/ted-butler-silver-pressure-cooker-hefty-d…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Global Stocks Slide, Futures Flat As China Sanctions Lockheed, Virus Fears Grow

European and Asian stocks slumped following Monday’s dramatic Nasdaq reversal, following a fresh escalation in the US-China cold war, and as investors weighed the risks of the upcoming earnings season even as rising virus cases prompted more states to resume shutdowns. Treasuries were flat and the dollar was modestly higher.

S&P 500 and Nasdaq futures were generally flat after yesterday’s freak late day selloff, even as Tesla climbed in pre-market trading following yet another ridiculous upgrade, this time from some bucket shop which sees the stock rising above $2,300.

“We are marginally risk-off today, driven by the dive into the close in the U.S.,” said Charles Diebel, head of fixed income at Mediolanum International Funds. “The real worrying aspect for the market really is that the rise in U.S. infections will make people behave like a lockdown even if they are opening up.”

Market sentiment took a hit from signs the virus is throttling reopening plans in states like California, and concern that equity valuations are stretched with global stocks trading near pre-pandemic highs according to Bloomberg.

Tensions between Washington and Beijing also escalated further after the United States rejected China’s disputed claims to offshore resources in most of the South China Sea. Meanwhile, in a surprisingly sharp escalation in tensions, China said it would impose sanctions on Lockheed Martin after the U.S. approved a possible $620 million deal for Taiwan to buy parts to refurbish defensive missiles made by the company. Chinese Foreign Ministry spokesman Zhao Lijian made the announcement at a briefing in Beijing on Tuesday. He called on the U.S. to cut military ties with Taiwan – which China considers part of its territory – to avoid “further harm to bilateral relations.”

“China firmly opposes U.S. arms sales to Taiwan,” Zhao said. “We will impose sanctions on the main contractor of this arms sale, Lockheed Martin.”

The news sent the offshore Yuan, which had risen sharply in recent weeks, to session lows and back under 7.00.

Meanwhile, traders are braced for earnings reports this week that will provides clues on the outlook for corporate profits. Q2 earnings season is set to officially begin in a few minutes, when JPMorgan Chase and Citigroup, which have substantial lending businesses, report Q2 earnings and could see a sharp plunge in net income in the April-June quarter that witnessed the biggest blow to businesses activity. JPM and CITI shares edged higher in premarket trading, while Wells Fargo which is expected to swing to a loss, was flat.

Earlier in the session, Asian stocks fell, led by communications and health care, after rising in the last session. Most markets in the region were down, with India’s S&P BSE Sensex Index dropping 1.6% and Hong Kong’s Hang Seng Index falling 1.1%, while Jakarta Composite gained 0.3%. Trading volume for MSCI Asia Pacific Index members was 31% above the monthly average for this time of the day. The Topix declined 0.5%, with Niitaka and Chuco falling the most. Even the Shanghai Composite Index retreated 0.8%, ending its stunning rally over the past two weeks, with Inzone Group Co Ltd and Sino-Platinum posting the biggest slides.

In the latest US-Sino escalation, the Trump administration rejected China’s expansive maritime claims in the South China Sea, reversing a previous policy of not taking sides in such disputes. The Trump administration also plans to scrap a 2013 auditing agreement that could foreshadow a broader crackdown on U.S.-listed Chinese firms

In FX, the Bloomberg Dollar Spot Index inched up after the euro rose in early European hours, with options traders seeing scope for more gains. The Swedish krona led G-10 gains after data showed inflation beat estimates last month.

In rates, the 10Y Treasury was modestly lower with the yield rising to 0.6283% after tumbling yesterday during the sharp Nasdaq selloff. The yield on the U.K.’s two- year bonds declined to an all-time low of minus 0.129% amid weaker global sentiment; the yield is for the first time lower than its Japanese peer.

In commodities, West Texas Intermediate crude rebounded 0.7% to $39.83 a barrel, while Brent crude gained 0.7% to $42.48 a barrel. Copper ended a six-day winning streak amid renewed tensions between Beijing and Washington.

To the day ahead now, and the data highlights from Europe include the May readings of UK GDP and Euro Area industrial production, as well as July’s ZEW survey from Germany. Over in the US, there’ll be the June CPI reading, along with the NFIB small business optimism index. Earnings releases feature a number of US financials, including JPMorgan, Citigroup and Wells Fargo, while we’ll also hear from the Fed’s Brainard and Bullard.

Market Snapshot

- S&P 500 futures up 0.3% to 3,157.50

- STOXX Europe 600 down 1.3% to 365.69

- MXAP down 0.8% to 164.77

- MXAPJ down 1% to 544.23

- Nikkei down 0.9% to 22,587.01

- Topix down 0.5% to 1,565.15

- Hang Seng Index down 1.1% to 25,477.89

- Shanghai Composite down 0.8% to 3,414.62

- Sensex down 1.6% to 36,094.68

- Australia S&P/ASX 200 down 0.6% to 5,941.08

- Kospi down 0.1% to 2,183.61

- German 10Y yield fell 1.5 bps to -0.432%

- Euro down 0.04% to $1.1340

- Italian 10Y yield rose 1.0 bps to 1.109%

- Spanish 10Y yield fell 1.4 bps to 0.43%

- Brent futures down 0.7% to $42.41/bbl

- Gold spot down 0.2% to $1,798.98

- U.S. Dollar Index little changed at 96.52

Top Overnight News from Bloomberg

- Investors dampened their expectations about the rebound in Germany, adding to signs that it still has a long road ahead as it recovers from the coronavirus lockdowns in the first half of the year

- WHO Director-General Tedros Adhanom Ghebreyesus said “there will be no return to the old normal for the foreseeable future”

- German Chancellor Angela Merkel showed a united front with Italy’s Giuseppe Conte days ahead of a crucial European Union summit, warning that EU leaders need to deliver a “massive” response to the economic fallout of the pandemic

- China said it would impose sanctions on Lockheed Martin Corp. after the U.S. approved a possible $620 million deal for Taiwan to buy parts to refurbish defensive missiles

- Saudi Arabia commended Iraq for implementing almost all its pledged oil-production cuts and Nigeria told the kingdom it was committed to hitting its target, in further signs that disputes among OPEC+ members over cheating of quotas are being resolved

Asian equity markets traded negatively with sentiment dampened following choppy performance stateside owing to a temperamental tech sector and ongoing US-China tensions after the US denounced China’s claims to the South China Sea as unlawful. Furthermore, sentiment was also subdued by the latest developments on the coronavirus front in which California Governor Newsom ordered a shutdown of indoor restaurants, bars, movie theatres and other businesses across the state. ASX 200 (-0.6%) and Nikkei 225 (-0.9%) were lower with Australia pressured by underperformance in the tech sector but with downside restricted by the improvement in Business Survey data, while Tokyo shares suffered the ill-effects of the recent currency inflows and despite reports that Softbank was exploring options for its Arm Holdings unit such as a potential sale or IPO. Hang Seng (-1.1%) and Shanghai Comp. (-0.8%) adhered to the downbeat picture due to the increased tensions after the US departed from its policy of not taking sides in the South China Sea dispute in which it denounced China’s claims, while China’s Foreign Ministry said it will impose sanctions on US lawmakers in response to sanctions over Xinjiang. Focus was also on the latest trade data from China which printed mostly better than expected, although this failed to inspire a turnaround for Chinese stocks with Hong Kong underperforming after the local government’s recent announcement of coronavirus related restrictions. Finally, 10yr JGBs were marginally higher as the risk averse tone favoured haven assets and after stronger demand at the enhanced liquidity auction for longer-dated JGBs, but with upside limited as the BoJ kicked off its 2-day policy meeting.

Top Asian News

- Modi’s Fuel-Tax Hikes Are Putting Brakes on India’s Recovery

- Korea Looking Into H.K. Hedge Fund That Halted Some Withdrawals

- Morgan Stanley’s Head of Asia Flow Credit Trading Leaves Firm

- China Posts Surprise Trade Gains as Economies Try to Reopen

European equities have pulled back from yesterday’s advances (Eurostoxx 50 -1.5%) as indices catch-up to the declines seen on Wall St. yesterday after the EU close. No one individual catalyst was attributed to the sell-off seen in the latter half of the US session yesterday with many of the bearish factors cited already present at the time of the initial rally. However, one feature of the selling pressure yesterday was an emphasis on tech names; a theme which has been replicated today in Europe with the IT sector the clear underperformer thus far as the likes on Infineon (-4.8%), STMicroelectronics (-4.5%) and SAP (-3.9%) all lag peers. Macro newsflow from a European perspective has been relatively light thus far with focus for the equity complex likely to fall on upcoming pre-market US earnings reports from JP Morgan, Well Fargo, Citi and Delta Airlines (previews of key metrics can be found on the newsquawk headline feed). Elsewhere, stateside, focus could fall on defense names after reports the Chinese Foreign Ministry intends to apply sanctions to Lockheed Martin (-1.1% in pre-market) over arms sales to Taiwan. Elsewhere in Europe, sectors trade broadly lower with no real clear theme seen in the focus of selling asides from the IT sector with individual equity stories on the light side this morning. Notable corporate updates have included Ocado (-0.8%), who trade lower despite reporting a 27% increase in revenues with the Co. unable to provide guidance and announcing the search for a new Chairman & CEO to replace “retail veteran” Lord Rose.

Top European News

- Merkel and Conte Show Common Front in Push for Recovery Fund

- Italy’s Conte Keeps Investors Guessing on Autostrade’s Fate

- ECB Says Loan Standards to Tighten as Government Protections End

- Lotos Soars in Warsaw on Fresh Hopes of Improved Orlen Offer

In FX, the Dollar continues to track broad risk sentiment and has benefited from renewed aversion on latest COVID-19 developments coupled with a further deterioration in US-Chinese relations centring on the South China Sea. As such, the DXY has regrouped to trade back around the 96.500 level within a 96.472-707 band ahead of US CPI data and a raft of Fed speakers awaiting the next daily update from states that are seeing a resurgence in the number of virus infections and fatalities.

- CHF/JPY/EUR/AUD – All narrowly mixed vs the Greenback, as the Franc and Yen retain an element of safe haven demand near 0.9400 and 107.00 respectively, while the former has pared some of Monday’s relatively heavy declines against the Euro from sub-1.0700 towards 1.0650 even though SNB head Jordan is highly likely to reiterate the importance of direct intervention and NIRP later today. However, the single currency is holding up well in its own right as Eur/Usd consolidates above 1.1300 and eyes hefty option expiry interest at the round number (2.1 bn), between 1.1320-25 (2 bn) and from 1.1350 to 1.1355 (1.3 bn). Similarly, the Aussie is gleaning some underlying traction circa 0.6945 from encouraging Chines trade data plus a firm rebound in NAB business sentiment and conditions to compensate for another incremental rise in pandemic cases in Victoria. Next up for the Jpy and Aud, the end of the 2-day BoJ convene and July consumer sentiment.

- CAD/NOK/NZD/GBP – The Loonie and Norwegian Krona have both been knocked out of stride by the aforementioned turnaround in tone from bullish to bearish that is also weighing on crude prices, as Usd/Cad rebounds through 1.3600 in advance of Wednesday’s BoC policy meeting and Eur/Nok pivots 10.7300 from sub-10.6000 mtd lows. Similarly, the Kiwi is back on the defensive within a 0.6545-10 range heading into NZ Q2 CPI tonight and Sterling is losing more momentum across the board on a mix of negative factors, as Cable fails to derive any traction from tame improvements in UK activity data and Eur/Gbp remains elevated on ongoing Brexit divisions having reversed/rebounded through 1.2600 and 0.9000 yesterday. Note, market contacts report big buy orders in the cross when 0.9075 was breached, but 0.9100 has capped advances beyond 0.9080 for now.

- SEK – In contrast to its Scandinavian peer, the Swedish Crown has been inflated by firmer than forecast CPI readings to remain close to 10.4000 and recent highs vs the Euro.

In commodities, WTI & Brent have succumbed to the broader risk-off moves overnight and in Europe this morning, with little fresh for the complex fundamentally out this morning as we await the OPEC monthly oil report. Benchmarks are posting losses just shy of 1% at present as sentiment modestly picks-up in the approach to US hours, with equity futures stateside marginally positive ahead of US earnings season’s full commencement. Returning to the aforementioned OPEC monthly report, aside from their demand outlooks for this year and next, attention will be on any insight into compliance figures for June. As, while we know compliance overall exceeded 100% this was largely due to efforts from Saudi Arabia, UAE & Kuwait and as the likes of Nigeria & Iraq having agreed to over-comply ahead to make up for their shortcomings in recent months this report will be looked at as an indication of just how much overcompliance will be required; and, of course, ahead of tomorrow’s JMMC where further insight into this and guidance on easing production cuts for the immediate period is expected. Further ahead, the weekly private inventory report is expected to print a headline draw of 1.8mln. Turning to metals, spot gold is very much rangebound around the USD 1800/oz handle as the USD has been relatively steady since the volatility around the European equity open & China Foreign Ministry updates. Copper prices remain supported by the strike action commencing in multiple Antofagasta mines over the weekend as reports note the final wage offers have been rejected by supervisors.

US Event Calendar

- 6am: NFIB Small Business Optimism, est. 97.8, prior 94.4

- 8:30am: Real Avg Weekly Earnings YoY, prior 7.4%; Real Avg Hourly Earning YoY, prior 6.5%

- 8:30am: US CPI MoM, est. 0.5%, prior -0.1%; CPI YoY, est. 0.6%, prior 0.1%

- 8:30am: US CPI Ex Food and Energy MoM, est. 0.1%, prior -0.1%; CPI Ex Food and Energy YoY, est. 1.1%, prior 1.2%

DB’s Jim Reid concludes the overnight wrap

Yesterday was the end of an era and the start of a more difficult 15 years to come – at least until the twins leave home. After bedtime has increasingly become an elongated and tortuous nightmare of late we decided that we should abandon their daily 2 hour lunchtime sleep for good. It doesn’t impact me in the week but at weekends this double dose of two hours is a godsend. Makes playing golf a bit easier on the rest of the family for starters. Now those days are gone and negotiations will get tougher.

Markets threw their toys out of the cot before bedtime last night as a strong day turned sour in the last 2.5 hours of trading on the back of renewed US / China tensions and more concerns about the virus spread in the US.

The S&P 500 initially rose roughly +1.5% and briefly reached post-pandemic highs before finishing down -0.94%. The drop came following the dual headlines of record covid-19 hospitalisations and shutdowns in California and the US denouncing China’s claim to the South China Sea. The VIX volatility index rose +4.9pts, the largest one day rise since 11 Jun. It looked like tech outperformance would continue as the NASDAQ had advanced +1.95% to yet another record high in early trading, but then the index saw a roughly -4% turnaround within the last 2 hours of the session to finish at -2.13%. European stocks outperformed having closed well before the reversal in the US, with the STOXX 600 (+1.00%), the DAX (+1.32%) and the CAC 40 (+1.73%) all moving higher. We didn’t get an awful lot of earnings releases yesterday though PepsiCo rose +0.33% on the back of a stronger than expected report, with core EPS of $1.32 (vs. $1.25 expected). We’ll get a lot more results today though, particularly from US financials including JPMorgan, Citigroup and Wells Fargo.

On that, with US Q2 earnings starting in earnest today it was interesting to see our equity strategists report last night that they are set up to notably beat expectations. Their rationale was that earnings expectations flatlined in June in the face of substantial improvements in US macro surprises. The two are well correlated so even with the recent case growth rise, earnings should have had a much better last month of the quarter than analysts were prepared to reflect. See their report here for more.

Overnight Asian markets have tracked Wall Street with the Nikkei (-1.04%), Hang Seng (-1.69%), Shanghai Comp (-1.10%), Kospi (-0.57%) and Asx (-0.83%) all losing ground. Amidst the risk off, the Japanese yen is up +0.11% this morning while the US dollar is up +0.10%. Meanwhile, futures on the S&P 500 are trading flat and crude oil prices are down c. -2%. In terms of overnight data releases, Singapore’s Q2 GDP printed at an annualized -41.2% qoq (vs. -35.9% qoq expected) as peak lockdown took its toll. China also released its June trade data with exports rising by +0.5% yoy (vs. -2.0% yoy expected) while imports came in at +2.7% yoy (vs. -9.7% expected). In terms of trade with the US, YtD June exports were down -11% yoy while imports were down -4.2% yoy bringing the trade balance to USD 121bn (-13.8% yoy).

In other overnight news, Akira Amari, Japan’s ruling party’s tax policy chief, has said that PM Shinzo Abe might call an election this year after putting together another extra budget. He added that “While there’s debate over the timing of a third extra budget, I don’t think we’ll get to the end of the year without doing something.” Elsewhere, top advisers to President Trump have ruled out undermining the Hong Kong dollar’s peg to the greenback as a retaliation to China’s imposition of new security law over the city.

Back to the ongoing rise in new virus cases. Florida saw a further 4.7% rise yesterday, slightly above the previous 7-day average of 4.4%, though in the state’s most populous county of Miami-Dade, the mayor said they weren’t yet planning another lockdown. California reported a record number of people hospitalised with coronavirus with nearly 6,500 on Sunday, as cases continue to trend higher in the state. The state’s largest school districts, Los Angeles and San Diego, will remain fully remote in the autumn. California Governor Newsom rolled back reopenings and ordered all indoor dining, wineries, movie theatres and entertainment to close. Bars and breweries statewide must close all indoor and outdoor operations, while fitness centres, worship services and salons must shut in counties that have been on a monitoring list for three straight days. Meanwhile, here in the UK, face masks will likely be compulsory in all shops in England from July 24 and the move will be enforced by fines of GBP 100 for non-compliance.

We continue to see rises in coronavirus cases in various countries, as well as the imposition of further restrictions. In Hong Kong, there was a noticeably tightening as public gatherings were limited to just 4 people, while gyms and bars were ordered to close for a week with restaurants allowed to offer only takeout from 6 pm to 5 am; and the number of patrons at a table at other times is limited to four. The city also mandated a $645 fine for not wearing a mask, as they reported a further 41 cases yesterday, of which 21 were related to previous clusters and the other 20 were of unknown origins. The city will also require inbound travellers who have been to high-risk regions in the last 14 days to pass a virus test before boarding their flights.

As mentioned above, there was also a further escalation in US-China tensions yesterday. Early in the day, China announced that they were placing sanctions on 4 US individuals, including the Republican Senators and former 2016 presidential candidates Marco Rubio and Ted Cruz. It comes after the US placed sanctions on a number of Chinese individuals last week, including Politburo member Chen Quanguo, over Xinjiang. A Chinese Foreign Ministry spokeswoman said yesterday that “Xinjiang is China’s internal affairs and U.S has no right to interfere”. Then last night, the US denounced China’s claim to the South China Sea, reversing a long-held policy of not taking sides in the disputes in the region. Secretary of State Michael Pompeo said, “Beijing’s claims to offshore resources across most of the South China Sea are completely unlawful, as is its campaign of bullying to control them.” Elsewhere, Reuters reported overnight that the Trump administration is planning to abandon a 2013 agreement between US and China auditing authorities. US watchdog PCAOB was already at an impasse with China on inspections.

In some positive market news out of the US, Senate Majority Leader Mitch McConnell said that his caucus planned to have a draft of the next round of stimulus ready by next week. The plan will be done in conjunction with the White House and will serve as a rebuttal of sorts to the Democrats’ $3.5tr plan that was passed in the House back in May.

Staying on politics, one other dampener yesterday were remarks from Chancellor Merkel, who said that EU positions were still far apart ahead of this Friday’s European Council summit on the recovery fund. She said that “bridges still need to be built” and started to adjust expectations for the outcome by saying a further meeting may be required if no consensus is achieved. The Chancellor, along with Italian Prime Minister Conte, touted the need for the EUR750bn recovery plan to combat the economic fallout of the pandemic. Conte noted that his government is willing to accept tighter criteria for the grants and loans package. This seems to be a concession to the more fiscally conservative nations that have demanded that any funding was attached to a set of conditions.

Back to markets yesterday and the US dollar fell -0.19% to a one-month low, while 10yr Treasuries saw yields down by -2.6bps to 0.618% on the sharp reversal in US equities. Over in Europe, where risk closed higher, the sovereign bonds of core countries were among the biggest losers, with 10yr bunds (+4.8bps), as well as Swiss (+5.9bps) and Dutch (+4.7bps) debt all seeing rising yields. The periphery outperformed however, with Italian (+1.1bps) and Greek (+0.1bps) witnessing smaller increases.

Elsewhere, in the commodities sphere, silver provided the main headline up +1.90% to a 10-month high and within striking distance of a 4 year high. Other metals also had strong performances, with palladium up +1.32% in its best day in nearly 2 weeks, even if gold experienced a more modest +0.23% rise. Copper (+1.91%) rose for a tenth consecutive gain and to its highest level since April 2019. It could be supported further by the possibility of production strikes in Chile. With risk assets under pressure, Brent crude (-1.20%) and WTI (-1.11%) pulled back ahead of OPEC+’s Joint Ministerial Monitoring Committee meeting tomorrow where the group is expected to adhere to a plan of tapering the production cuts from August on.

To the day ahead now, and the data highlights from Europe include the May readings of UK GDP and Euro Area industrial production, as well as July’s ZEW survey from Germany. Over in the US, there’ll be the June CPI reading, along with the NFIB small business optimism index. Earnings releases feature a number of US financials, including JPMorgan, Citigroup and Wells Fargo, while we’ll also hear from the Fed’s Brainard and Bullard.

3A/ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 28.67 POINTS OR 0.83% //Hang Sang CLOSED DOWN 294.23 POINTS OR 1.14% /The Nikkei closed DOWN 197.73 POINTS OR 0.87%//Australia’s all ordinaires CLOSED DOWN .72%

/Chinese yuan (ONSHORE) closed DOWN at 6.9951 /Oil UP TO 39.73 dollars per barrel for WTI and 342.37 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9951 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0181 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS//PANDEMIC : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

Asia,Europe/Globe/Coronavirus update

Asian, European Countries Roll Back Economic Reopenings As COVID-19 Makes Global Comeback: Live Updates

Summary:

- US daily cases below 60k

- Global daily cases below 200k

- Hong Kong imposes new restrictions

- France makes mask wearing mandatory in public

- Australia cases top 10k.

- Iran closes mosques, schools

- WHO warns: “there will be no return to normal”

* * *

The number of new coronavirus cases reported yesterday in the US remained below the critical 60k threshold, but from Asia to Europe, economies that only recently appeared to have beaten the coronavirus are now imposing new restrictions to try and prevent a resurgence.

But globally, the number of new cases remained near a recently hit record high, pushing the worldwide total to 13,238,121 as of Tuesday morning. Though crucially, the number of cases reported yesterday came in just below 200k, roughly 30k shy of the record.

The death toll from the deadly virus has reached 575,543 globally, according to Worldometer. Of the currently infected 4,964,306 patients, 4,905,425 were in mild condition, while 58,881 were in serious or critical condition.

Last night (Tuesday morning in HK), Hong Kong announced plans to impose a new lockdown that appears to be even more restrictive than the measures it imposed during the opening weeks of the outbreak. While HK had previously relied on closing borders with the mainland, the new measures focus on suppressing domestic transmission. They include: that face masks will be mandatory for people using public transport and restaurants will no longer provide dine-in services, instead only offering takeaway service.

We teased the new measures in our report from yesterday, when a top HK epidemiologist warned that a mutated strain of the virus circulating in HK is even more infectious than its predecessor.

If an individual doesn’t wear a mask on public transport, they face a fine of HK$5,000 ($645). Gatherings would be limited to 4 people from 50. Gyms, places of amusement and other establishments must shut for a week.

“The recent emergence of local cases of unknown infection source indicates the existence of sustained silent transmission in the community,” the government said in a statement late on Monday.

The Chinese-ruled city recorded 52 new cases of coronavirus on Tuesday, including 41 that were locally transmitted, health authorities said, bringing its total outbreak to 224 people over the past week.

In Australia, Melbourne remains on lockdown while the number of new cases being reported continues to climb, the Australian state of Victoria has recorded 270 new cases of coronavirus, while New South Wales recorded 13, bringing the national total to about 10,250.

As the US outbreak in the Sun Belt nears its peak, the EU is reportedly set to recommend keeping its external borders shut to Americans and most other foreigners for at least two more weeks as fears grow of a second coronavirus wave.

As fears about a resurgence in Asia intensify, the WHO raised concerns over the Philippines’ rising number of new cases, which have swamped some local hospitals as the number of new cases being reported daily hits record after new record.

The proportion of positive cases in the country is gradually increasing from about 6.5% two weeks ago to about 7.8% on Monday, WHO representative in the Philippines Rabindra Abeyasinghe warned.

“This is worrying as it shows that there is continuing transmission. This is also reflected by the increased number of admissions into hospitals,” he said.

Similarly, after recording a record jump in deaths a few days ago, Iran is reeling from its own resurgence, prompting Tehran to close schools, universities, Shia seminaries, mosques and other sites of religious gatherings for at least a week, local state news reported. Iran reported 2,521 new cases and 179 deaths overnight, bringing the total figures to 262,173 cases and 13,211 deaths.

As Catalonian government imposes new restrictions on local hot spots, across the border in France, President Macron warned that the virus “is coming back a little bit” and that starting next week, France will make mask wearing compulsory in public spaces.

During a press briefing Tuesday in Geneva, the WHO warned the pandemic could get far worse if countries around the world do not follow basic healthcare precautions.

“The virus remains public enemy number one,” WHO Director-General Dr. Tedros Adhanom Ghebreyesus told a virtual briefing from WHO headquarters in Geneva.

“There will be no return to the old normal for the foreseeable future,” Tedros said.

end

3 C CHINA

Where do all of China\s unsold cars go to die? Answer Wuhan!

(zerohedge)

Where China’s Unsold Cars Go To Die

While every effort has been made in China to paint a picture of a recovering ‘back to normal’ economy with production rebounding dramatically, it appears, as we noted earlier, that the demand side of the equation is not keeping pace with supply.

Case in point, China’s passenger car sales broke the v-shaped recovery narrative in June, slumping back 6.5%, despite soaring auto production data.

So what happened to all those cars?

We have the answer…

Wuhan, the epicenter of the CCP virus, is one of the major automaking towns in China. Dongfeng Motor Group, China’s third-biggest state-owned automaker, is headquartered in the city.

On June 30, a woman was shocked to see thousands and thousands of unsold new cars sitting idle on Dongfeng Motor land.

She shot the video from an overpass above Dongfeng’s car lots…