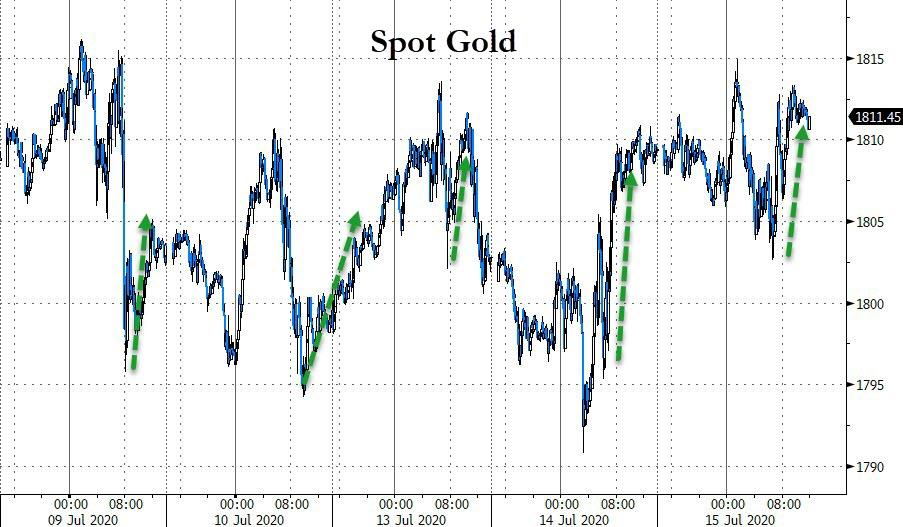

GOLD:$1811.30 UP $1.65 The quote is London spot price (cash market)

Silver:$19.36// UP 21 CENTS London spot price ( cash market)

Closing access prices: London spot

i)Gold : $1810.40 LONDON SPOT 4:30 pm

ii)SILVER: $19.42//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUG GOLD: $1813.90 CLOSE 1.30 PM// SPREAD SPOT/FUTURE AUG /: $2.60

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $19.76…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : 40 CENTS PER OZ

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today: 0/86

issued 22

EXCHANGE: COMEX

CONTRACT: JULY 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,810.600000000 USD

INTENT DATE: 07/14/2020 DELIVERY DATE: 07/16/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

332 H STANDARD CHARTE 8

355 C CREDIT SUISSE 11

657 H MORGAN STANLEY 59

661 C JP MORGAN 22

690 C ABN AMRO 20

737 C ADVANTAGE 20 7

800 C MAREX SPEC 24 1

____________________________________________________________________________________________

TOTAL: 86 86

MONTH TO DATE: 7,211

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 86 NOTICE(S) FOR 86000 OZ ( tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 7211 NOTICES FOR 721100 OZ (22.429 TONNES)

SILVER

FOR JULY

16 NOTICE(S) FILED TODAY FOR 80 OZ/

total number of notices filed so far this month: 13,919 for 69.595 MILLION oz

BITCOIN MORNING QUOTE $9226 DOWN 29

BITCOIN AFTERNOON QUOTE.: $9194 DOWN $64

GLD AND SLV INVENTORIES:

WITH GOLD UP $1.65 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.92 TONNES WAS ADDED TO GLD.

GLD: 1,206.89 TONNES OF GOLD//

WITH SILVER UP 21 CENTS TODAY: AND WITH NO SILVER AROUND:

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUGE PAPER DEPOSIT OF 1.956 MILLION OZ//

WHAT A FRAUD!!

RESTING SLV INVENTORY TONIGHT:

SLV: 516.074 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A TINY SIZED 226 CONTRACTS FROM 178,141 UP TO 178,367, AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE TINY SIZED GAIN IN OI OCCURRED DESPITE OUR HUGE 21 CENT LOSS IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE SMALL GAIN IN COMEX OI IS PRIMARILY DUE TO HUGE BANKER SHORT COVERING PLUS A SMALL EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A SMALL DECREASE IN SILVER STANDING AT THE COMEX FOR JULY. WE HAD A NET GAIN IN OUR TWO EXCHANGES OF 948 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: JULY: 0 AND SEP 658 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 658 CONTRACTS. WITH THE TRANSFER OF 658 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 658 EFP CONTRACTS TRANSLATES INTO 4.125 MILLION OZ ACCOMPANYING:

1.THE 21 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

81.605 MILLION OZ INITIALLY IN JULY.

TUESDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL 21 CENTS).. AND,OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS. THE STRONG GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A SMALL DECREASE IN STANDING OF SILVER OZ STANDING FOR JULY, STRONG BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A NET GAIN OF 948 CONTRACTS OR 4,42 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

JULY

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF JULY:

6869 CONTRACTS (FOR 10 TRADING DAY(S) TOTAL 6869 CONTRACTS) OR 34.345 MILLION OZ: (AVERAGE PER DAY: 687 CONTRACTS OR 3.4345 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 34.345 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 4.90% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,171,76 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 34.345 MILLION OZ/

EXCHANGE FOR PHYSICAL ISSUANCE FOR THE PAST 60 DAYS IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD A TINY SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 226, DESPITE OUR 21 CENT LOSS IN SILVER PRICING AT THE COMEX ///TUESDAY… THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 658 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A GOOD SIZED OI CONTRACTS ON THE TWO EXCHANGES: 884 CONTRACTS (WITH OUR 21 CENT LOSS IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 648 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A TINY SIZED INCREASE OF 226 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED DESPITE A 21 CENT GAIN IN PRICE OF SILVER/AND A CLOSING PRICE OF $19.15 // TUESDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.892 BILLION OZ TO BE EXACT or 127% of annual global silver production (ex Russia & ex China).

FOR THE NEW JULY DELIVERY MONTH/ THEY FILED AT THE COMEX: 16 NOTICE(S) FOR 80,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 81.640 million oz

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 8492 CONTRACTS TO 580,175 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE STRONG SIZED GAIN OF COMEX OI OCCURRED DESPITE OUR TINY LOSS IN PRICE OF $1.65 /// COMEX GOLD TRADING// TUESDAY// WE HAD HUGE BANKER SHORT COVERING, ANOTHER HUMONGOUS SIZED GOLD OZ STANDING AT THE COMEX FOR JULY, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A GOOD EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR LOSS IN PRICE OF $1.65 .

WE HAD A VOLUME OF 1 4 -GC CONTRACTS//OPEN INTEREST 64

WE GAINED A STRONG SIZED 15,847 CONTRACTS (49.29 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 7355 CONTRACTS:

CONTRACT .; AUG 5727 AND OCT: 0 DEC: 1628 ALL OTHER MONTHS ZERO//TOTAL: 7355. The NEW COMEX OI for the gold complex rests at 580,175. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 15,847 CONTRACTS: 8492 CONTRACTS INCREASED AT THE COMEX AND 7355 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 15,847 CONTRACTS OR 49.29 TONNES. TUESDAY, WE HAD A LOSS OF $1.65 IN GOLD TRADING……

AND WITH THAT LOSS IN PRICE, WE HAD A STRONG SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 49.29 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT FELL $1.65).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS ALSO UNSUCCESSFUL (SEE BELOW).

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (7355) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (8492 OI): TOTAL GAIN IN THE TWO EXCHANGES: 16985 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)ANOTHER HUMONGOUS INCREASE IN GOLD STANDING AT THE GOLD COMEX FOR THE FRONT JULY MONTH, 3) ZERO LONG LIQUIDATION; 4) STRONG COMEX OI GAIN.5) GOOD EXCHANGE FOR PHYSICAL ISSUANCE… AND …ALL OF THIS WAS COUPLED WITH OUR TINY LOSS IN GOLD PRICE TRADING//TUESDAY//$1.65.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

SPREADING OPERATIONS/NOW SWITCHING TO GOLD

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN GOLD AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF AUGUST FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF JULY. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUGUST), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

JULY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAY(S) IN TONNES: 123.35 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 123.35/3550 x 100% TONNES =3.47% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3141.55 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 123.35 TONNES SO FAR..

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A TINY SIZED 226 CONTRACTS FROM 178,141 UP TO 178,367 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE TINY GAIN IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) HUGE BANKER SHORT COVERING , 2) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A SMALL DECREASE STANDING AT THE SILVER COMEX FOR JULY AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 658 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY: 0 CONTRACTS AND SEPT: 658 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 658 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 226 CONTRACTS TO THE 658 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 884 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 4.74 MILLION OZ, OCCURRED WITH OUR STRONG 21 CENT LOSS IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 53.31 POINTS OR 1.56% //Hang Sang CLOSED UP 3.69 POINTS OR 0.01% /The Nikkei closed UP 358.49 POINTS OR 1.59%//Australia’s all ordinaires CLOSED UP 1.90%

/Chinese yuan (ONSHORE) closed DOWN at 6.9855 /Oil UP TO 40.83 dollars per barrel for WTI and 43.36 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.9855 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9881 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS//PANDEMIC: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

i)we had 1 deposits into the customer account

into JPMorgan: 0

ii) Into Delaware: 19,728.740 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.744 million oz of total silver inventory or 49.66% of all official comex silver. (160.819 million/323.787 million

total customer deposits today: nil oz

we had 3 withdrawals:

ii) Out of Loomis: 600,002.100

iii) Out of HSBC: 55,282.690 oz

total withdrawals; 874,146.69 oz

We had 0 adjustments

total dealer silver: 126.708 million

total dealer + customer silver: 323.787 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The front month of July has an open interest of 2418 contracts, as we lost 7 contracts. We had 0 notices served on TUESDAY, so we lost a tiny 7 contracts or an additional 35,000 oz will not stand in this active delivery month of July as they morphed into a London based forwards. It seems that we have little silver over on this side of the pond.

The next month after July is the non active month of August and here sees its open interest fell by 47 contracts down to 810

The big September contract month sees a loss of 295 contracts down to 140,245.

The total number of notices filed today for the JULY 2020. contract month is represented by 16 contract(s) FOR 80,000, oz

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 13,919 x 5,000 oz = 69,595,000 oz to which we add the difference between the open interest for the front month of JULY.(2418) and the number of notices served upon today 16 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the JULY/2019 contract month: 13,919 (notices served so far) x 5000 oz + OI for front month of JULY (2418)- number of notices served upon today (16) x 5000 oz of silver standing for the JULY contract month.equals 81,605,000 oz. (A WHOPPER )

WE LOST 7 CONTRACTS OR 35,000 OZ WILL NOT STAND FOR DELIVERY. SILVER IS STILL VERY SCARCE ON THIS SIDE OF THE POND AND THE REASON FOR MORPHING OVER TO LONDON.

TODAY’S ESTIMATED SILVER VOLUME : 54,674 CONTRACTS // volume fair/

FOR YESTERDAY: 79,234.,CONFIRMED VOLUME//volume very good/

YESTERDAY’S CONFIRMED VOLUME OF 79,234 CONTRACTS EQUATES to 396 million OZ 56.5% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 0.12% ((JULY 15/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -.12% to NAV: (JULY 15/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 0.12%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 17.48 TRADING 17.44///NEGATIVE 0.25

END

And now the Gold inventory at the GLD/

JULY 15//WITH GOLD UP $1.55 TODAY/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 2.96 TONNES INTO THE GLD///INVENTORY RESTS AT 1206.89 TONNES

JULY 14//WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 3.51 TONNES/INVENTORY RESTS AT 1203.97 TONNES

JULY 13//WITH GOLD UP $12.50 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1200.46 TONNES

JULY 10/WITH GOLD DOWN $.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD//A STRANGE WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1200.82 TONNES

JULY 9//WITH GOLD DOWN $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OX 3.21 TONNES INTO THE GLD//INVENTORY RESTS AT 1202.57 TONNES

JULY 8/WITH GOLD UP $13.75 TODAY; A BIG CHANGE IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 7.89 TONNES INTO THE GLD//INVENTORY RESTS AT 1199.36 TONNES

JULY 7/WITH GOLD UP $12.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1191.47 TONNES

JULY 6/WITH GOLD UP $6.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1191.47 TONNES

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

JUNE 30//WITH GOLD UP $16.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1178.90 TONNES

JUNE 29/WITH GOLD UP $2.90 TODAY: A HUGE DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1178.90 TONNES

JUNE 26/WITH GOLD UP $5.03 TODAY: VERY STRANGE: A PAPER WITHDRAWAL OF 1.46 TONNES//INVENTORY RESTS AT 1175.39 TONNES

JUNE 25//WITH GOLD DOWN $3.30 TODAY//ANOTHER STRONG PAPER DEPOSIT OF 7.6 TONNES///INVENTORY RESTS AT 1176.85 TONNES

JUNE 24/WITH GOLD DOWN $1.50 TODAY; A STRONG 3.21 TONNES ADDED TO THE GLD//INVENTORY RESTS AT 1169.25 TONNES

JUNE 23/WITH GOLD UP $25.50 TODAY/ANOTHER CRIMINAL PAPER DEPOSIT OF 6.73 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1166.04 TONNES

JUNE 22/WITH GOLD UP $14.00 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 23.09 TONNES//INVENTORY RESTS AT 1159.31 TONNES

JUNE 19/WITH GOLD UP$16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//; INVENTORY RESTS AT 1136.22 TONNES

JUNE 18//WITH GOLD DOWN $2.75 TODAY: NO CHANGES IN GOLD INVENTORY: INVENTORY RESTS AT 1136.22 TONNES

JUNE 17/WITH GOLD DOWN $1.05: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1136.22 TONNES

JUNE 16//WITH GOLD UP $6.70 TODAY: NO CHANGES IN GOLD INVENTORY: /INVENTORY RESTS AT 1136.22 TONNES

JUNE 15/WITH GOLD DOWN ANOTHER $8.80 TODAY, NO CHANGES IN GOLD INVENTORY/INVENTORY RESTS AT 1136.22 TONNES

JUNE 12//WITH GOLD DOWN $1.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 1.17 TONNES AT THE GLD//INVENTORY RESTS AT 1136.22 TONNES

JUNE 11//WITH GOLD UP $16.80 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 6.55 TONNES AT THE GLD//INVENTORY RESTS AT 1135.05 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

JULY 15/ GLD INVENTORY 1206.89 tonnes*

LAST; 861 TRADING DAYS: +263.07 NET TONNES HAVE BEEN ADDED THE GLD

LAST 761 TRADING DAYS://+441.18 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JULY 15.WITH SILVER UP 21 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.956 MILLION OZ//INVENTORY RESTS AT 516.074 MILLION OZ//

JULY 14/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 514.118 MILLION OZ//

JULY 13//WITH SILVER UP 67 CENTS TODAY: A HUGE CHANGE IN SILVER: A WITHDRAWAL OF 1.677 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 514.118 MILLION OZ//

JULY 10/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 4.844 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.795 MILLION OZ

WHAT A FRAUD!!

JULY 9/WITH SILVER DOWN 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 8.198 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 510.951 MILLION OZ/

JULY 8/WITH SILVER UP 37 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.118 MILLION OZ FROM THE SLV//VERY SURPRISING.//INVENTORY RESTS AT 502.753 MILLION OZ//

JULY 7/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/INVENTORY RESTS AT 503.871 MILLION OZ///

JULY 6//WITH SILVER UP 24 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.863 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 503.871 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

JUNE 30/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 29/WITH SILVER DOWN ONE CENT TODAY: A TWO CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 466,000 OZ TO PAY FOR STORAGE FEES AND INSURANCE//// AND A LARGE DEPOSIT OF 1.212 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 26/WITH SILVER UP 6 CENTS TODAY: ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ RESTS AT 491.858 MILLION OZ//

JUNE 25/WITH SILVER UP 12 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 931,000 OZ INTO THE SLV////INVENTORY RESTS AT 491.858 MILLION OZ//

JUNE 24///WITH SILVER DOWN 31 CENTS// NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 490.927 MILLION OZ

JUNE 23//WITH SILVER UP 16 CENTS TODAY: A MONSTROUS CHANGE IN INVENTORY: A PAPER DEPOSIT OF 4.473 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 490.927 MILLION OZ//

JUNE 22/WITH SILVER UP 15 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/: INVENTORY/INVENTORY RESTS AT 486/454 MILLION OZ//

JUNE 19//WITH SILVER UP 22 CENTS TODAY: STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 839,000 OZ FROM THE SLV////INVENTORY RESTS AT 486,454 MILLION OZ..

JUNE 18/WITH SILVER DOWN 16 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 932,000 OZ INTO THE SLV////INVENTORY RESTS AT 487.293 MILLION OZ

JUNE 17/WITH SILVER UP 8 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.261 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.361 MILLION OZ

JUNE 16//WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.118 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 483.100 MILLION OZ//

JUNE 15/WITH SILVER DOWN 14 CENTS NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 481.982 MILLION OZ///

JUNE 12/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: TWO DEPOSITS OF 7.269 MILLION OZ AND 1.802 MILLION OZ ADDED TO THE SLV///INVENTORY RESTS THIS WEEKEND AT 481.982 MILLION OZ//

JUNE 11//WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY: ///INVENTORY RESTS AT 472.89 MILLION OZ//

JULY 15.2020:

SLV INVENTORY RESTS TONIGHT AT

516.074 MILLION OZ.

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

What a joke: the biggest manipulators of them all, the uSA is accusing Switzerland for allegedly manipulating its currency exchange rate. Switzerland defends its intervention as essential.

If we are on a gold standard, this entire episode is moot.

Bloomberg

Swiss central bank defends currency intervention as ‘essential’

Submitted by cpowell on Tue, 2020-07-14 15:03. Section: Daily Dispatches

By Catherine Bosley

Bloomberg News

Tuesday, July 14, 2020

Currency intervention is an “essential” policy tool for Switzerland, its central bank chief said, in a riposte to the United States, which has the country on a watchlist for allegedly manipulating its exchange rate.

“Even though we still have scope for further interest-rate cuts, the fact remains that one cannot lower interest rates indefinitely,” Swiss National Bank President Thomas Jordan said today in a lecture for the International Monetary Fund. “For this reason, interventions in the foreign exchange market, in which we buy foreign currencies and sell Swiss francs, also play a central role in our policy mix.”

…

The U.S. Treasury earlier this year put Switzerland back on a list of countries that it believes are manipulating their exchange rates for competitive gain, citing the nation’s high current-account surplus and bilateral trade balance as evidence.

Yet Swiss policy makers have long relied on interventions to prevent too much strength in the franc, which investors tend to flock to at times of stress. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2020-07-14/swiss-central-bank-de…

end

The outlook for the value of the dollar shows mounting risks…and sure enough it has been falling badly as of late…

London’s financial times/GATA

Mounting risks in U.S. will weigh on the dollar, analysts predict

Submitted by cpowell on Tue, 2020-07-14 15:12. Section: Daily Dispatches

By Eva Szalay and Colby Smith

Financial Times, London

Monday, July 13, 2020

Escalating political and health risks in the United States and rising optimism about the global economic recovery should keep the dollar sliding over the next few months, according to analysts.

Large banks turned bearish on the greenback in late May, citing drastic cuts in interest rates and a flood of liquidity unleashed by the Federal Reserve, as it tried to alleviate the economic effects of the pandemic.

…

Since then, the outlook for the dollar has deteriorated further, strategists say. They cite growing concerns over the reopening of the world’s largest economy in the face of a steady increase in Covid-19 cases, as well as increased political threats and a hit from investors exiting safety-seeking bets in the dollar.

…

… For the remainder of the report:

https://www.ft.com/content/e6352387-5704-4e44-9b79-22ae87039e59

end

The 5 factors responsible for gold’s rise: Craig Hemke

(Craig Hemke/Sprott/GATA)

Craig Hemke at Sprott Money: Explosive debt is one of many props for gold

Submitted by cpowell on Tue, 2020-07-14 21:38. Section: Daily Dispatches

5:37p ET Tuesday, July 14, 2020

Dear Friend of GATA and Gold:

The explosive increase in U.S. government debt is joining five other developments creating an outstanding environment for the monetary metals, the TF Metals Report’s Craig Hemke notes today at Sprott Money:

— Infinite fiat currency creation.

— Economic contraction and stagflation.

— Central bank yield curve control.

— Increasingly negative real interest rates.

— Record global physical demand for the metals.

Hemke’s analysis is headlined “Total U.S. Debt Soars” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/total-us-debt-soars-craig-hemke-july-14…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

GATA’s Ed Steer interviewed by talk-show host Dave Janda

Submitted by cpowell on Tue, 2020-07-14 21:46. Section: Daily Dispatches

5:45p ET Tuesday, July 14, 2020

Dear Friend of GATA and Gold:

Gold price suppression is longstanding government policy, GATA board member Ed Steer tells talk show host Dave Janda of “Operation Freedom” on WAAM-AM1600 in Ann Arbor, Michigan, in an interview conducted Sunday. But, Steer adds, the world financial system is unraveling and monetary metals prices are showing it.

The interview is 23 minutes long and can be heard here:

https://operation-freedom-shows.s3.amazonaws.com/JUL12_2020/EdSteer07122…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Are Western banks also involved in spoofing gold trading in Shanghai?

(Kim/GATA)

John Kim: Did China foil Western banks’ spoofing of Shanghai gold market?

Submitted by cpowell on Tue, 2020-07-14 22:04. Section: Daily Dispatches

6p ET Tuesday, July 14, 2020

Dear Friend of GATA and Gold:

Market analyst John Kim today reports a recent statement by the Shanghai Futures Exchange that the exchange has caught attempts to “spoof” trading, and Kim wonders if the perpetrators are Western banks that often have “spoofed” Western gold markets.

Kim’s analysis is headlined “Did China Foil Western Banking Spoofing of Gold Markets in Shanghai This Month?” and it’s posted at his internet site here:

https://maalamalama.com/wordpress/did-china-foil-western-banking-spoofin…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

GATA) Lawrence Lepard: Fed, Treasury are now ‘sort of’ on gold’s side

Submitted by cpowell on 04:24PM ET Wednesday, July 15, 2020. Section: Daily Dispatches

12:27p Wednesday, July 15, 2020

Dear Friend of GATA and Gold:

Equity Management Associates Managing Partner Lawrence Lepard’s second-quarter report for the firm’s gold fund, published this week, brilliantly itemizes the circumstances working in favor of the monetary metal and the companies that mine it.

But the report may be most interesting for its speculation that the U.S. government’s Federal Reserve and Treasury Department are attempting a controlled retreat with gold and now are “sort of” on the side of gold investors.

Lepard writes: “It all comes down to faith in the stewards of the currency — the Federal Reserve and by extension the U.S. Treasury. If faith in them increases, gold will fall in price. If faith in them diminishes, gold will accelerate in price.

“Because they are in a sovereign debt crisis/trap, I believe the Fed knows that the only way out is to inflate. The alternative is a deflationary collapse that they would view as infinitely worse.

“I believe that they will attempt to have a managed retreat. That is, they know they need inflation and a higher gold price. They just don’t want it to happen too quickly or in a disorderly fashion, because if that occurs, Gresham’s Law will kick in and the dollar will fail.

“So as investors in gold and gold mining equities, I believe we now have the government on our side — sort of. We have to be prepared for them to take actions to attack gold if its price begins to accelerate too dramatically.”

With Lepard’s kind permission, his report is posted at GATA’s internet site here:

http://gata.org/files/EMA-GARP-Fund- Q2-2020-Report.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Professor Altman…a good read as to what is going to happen to corporations this year: big bankruptcies!

Professor Whose Formula Predicts Bankruptcies Has a Big Warning

Bankruptcies have not only been rising quickly — they have been rising in scale as “mega” firms go bust. “More than 30 American companies with liabilities exceeding $1 billion have already filed for Chapter 11” this year. https://bloomberg.com/news/articles/2020- 07-15/father-of-the-z-score-pr

edicts-a-surge-in-mega- bankruptcies

end

***

iii) Other physical stories:

Central Banks Buy Another 40 Tons Of Gold In May

Central banks added a net of 39.8 tons of gold in May,according to the latest data from the World Gold Council. May purchases maintained the pace we’ve seen through the first four months of the yearand was slightly above the four-month average of 35 tons.

So far in 2020, central banks have added a net of 181 tons of gold to their reserves. That’s about 31% lower than the total through the same period last year. The lower rate of purchases in 2020 was entirely expected given the strength of central bank buying both in 2018 and 2019.

Central bank demand came in at 650.3 tons last year.That was the second-highest level of annual purchases for 50 years, just slightly below the 2018 net purchases of 656.2 tons. According to the WGC, 2018 marked the highest level of annual net central bank gold purchases since the suspension of dollar convertibility into gold in 1971, and the second-highest annual total on record.

The World Gold Council bases its data on information submitted to the International Monetary Fund.

Continuing a trend we’ve seen throughout 2020, Turkey drove central bank gold-buying in May, adding 36.8 tons. That brings its total reserves to roughly 561 tons. The Turkish lira dropped to all-time lows in early May. Analysts told CNBC that rapidly shrinking foreign reserves, inflation and currency devaluation are showing no signs of abating. The Turkish central bank is frantically trying to backstop its currency. Meanwhile, Turkey is selling dollars. According to Bloomberg, state banks sold roughly $1.1 billion of foreign currency in just two days in May.

Uzbekistan was the other major buyer of gold in May, adding 6.8 tons of gold to its reserves. The Uzbeks were big buyers in 2019, but have primarily been sellers this year.

Russia bought a half-ton of gold in May. In March, the Central Bank of Russia announced a plan to suspend gold-purchases for the time being, effective April 1. But there was immediate pressure on the bank to resume purchases. In early April, Russian banks asked the Central Bank of Russia to resume buying gold for its reserves as gold exports were hobbled by the coronavirus pandemic. In a letter released on April 29, the Russian central bank said it did not see any need to resume buying gold at the time, but added it would continue to monitor the situation in both the global gold market and the banking sector.

Mongolia was the only big seller in May, shrinking its gold reserves by 3.3 tons. Columbia sold 0.9 tons of the yellow metal.

For the eighth straight month, the People’s Bank of China did not report any gold purchases. It’s not uncommon for China to go silent and then suddenly announce a large increase in reserves.

Many analysts believe China holds far more gold than it officially reveals. As Jim Rickards pointed out on Mises Daily back in 2015, many people speculate that China keeps several thousand tons of gold “off the books” in a separate entity called the State Administration for Foreign Exchange (SAFE). Given the political dynamics and the ongoing trade war, it seems unlikely the Chinese suddenly stopped increasing their gold reserves in 2016.

.

The World Gold Council says it expects central bank demand for gold to continue in the near-term.

As we noted in our Q1 2020 Gold Demand Trends report, the case for central banks holding gold remains strong. Especially considering the economic uncertainty caused by the COVID-19 pandemic.”

The WGC 2020 Central Bank Survey found that 20% of central banks globally plan to expand their gold holdings in the next 12 months.

Factors related to the economic environment – such as negative interest rates – were overwhelming drivers of these planned purchases.This was supported by gold’s role as a safe haven in times of crisis, as well as its lack of default risk.”

end

Von Greyerz: The ‘Humpty-Dumpty’ System Is Irreparable

Authored by Egon von Grezerz via GoldSwitzerland.com,

What does it take to break the global financial system? Well, we obviously know what it takes since the system is already broken. Broken by debts, broken by deficits, broken by a fractured financial system, and broken by false markets as well as fake money.

So just like Humpty Dumpty, the system has already had a big fall. But the world still believes that this is all a fairytale with a happy ending. No one wants to recognise that Humpty is totally broken and irreparable.

NO ONE CAN PUT HUMPTY TOGETHER AGAIN

All the king’s men, in the shape of the Fed and other central banks plus governments, are desperately trying to put Humpty back together again. The problem is that the glue just won’t stick. Already back in 2007-9 and thereafter, massive amounts of glue were applied in the form of unlimited money printing and credit creation. The problem was that a remedy in big quantities serves no purpose if the quality is poor.

Fortunately for the king’s men, nobody realised that they worked with inferior material. Equity markets only care about quantity and there certainly was enough glue or printed money. So it has been all about quantity or printing a lot of worthless money. Why else would it be called QE or quantitative easing?

HOCUS POCUS ACTIONS

QE is one of these Hocus Pocus words, invented by TPTB (the powers that be), which sounds important and mysterious. But for us normal mortals it should be called MP or money printing. That’s all it is, but since money printing sounds quite crude, the Fed and Co think they can get away with a posh word which nobody understands. All QE stands for is printing money in great quantities.

But let’s just understand that the glue or printed money which is supposed to fix the financial system is fake. There is no chance that all the king’s horses and all the king’s men can put the system together again.

A world which has got used to a rising living standards based on debt and fake money is under the illusion that this is all that is required to create wealth. A fake world and an illusory financial system cannot survive without creating real values based on hard work with the production of goods and services. Sustainable wealth can never be achieved by financial wizardry and hocus pocus money.

A DUMBFOUNDED SYSTEM HAS DUG ITS OWN GRAVE

A few of us have understood that the end game would consist of unlimited creation of debt and fake money. Not because anyone believes that the biggest debt bubble in the world will disappear by issuing more debt. But this is the only remedy left to a totally dumbfounded system which has for years dug its own grave.

It is into this grave that Humpty has fallen. The king’s men believe that they can pull him out like they have for decades but this time it won’t work.

WORLD ECONOMIC FORUM PLANNING THE GREAT RESET

TPTB are desperately working on solutions. For example, the WEF (World Economic Forum) in Davos are calling the next Forum in early 2021 “The Great Reset”.

They have created a Strategic Intelligence Platform which will help the members to control the world. Strategic Partners of the WEF will be members of a number of platforms from which they intend to orchestrate the Great Reset. These platforms include “Shaping the future of: Technology, Blockchain, New Economy & Society, Future Consumption, Digital Economy, Financial and Monetary Systems, Trade, Cities & Infrastructure, Energy, Media & Culture etc.

Well, it sounds like they plan to control everything.

Central bankers, bankers, industrialists incl. Bill Gates, IMF MD, ECB President Lagarde, Mark Carney former Bank of England governor etc are all members.

The WEF has developed the Fourth Industrial Revolution (4IR) which “will leave no aspect of global society unchanged”.

ORWELL’S 1984 IS HERE

All this sounds quite frightening but that is clearly the intention too. George Orwell’s 1984 is not just approaching at great speed but also becoming more realistic by the day.

There is only one major problem. Whatever wizardry and however much glue TPTB apply, there is just no way that a system that is totally broken can be repaired. The world has reached the end of the road and will need a reset.

But even if TPTB attempt an orderly reset with debt moratoria and a new artificial reserve currency like a crypto dollar, it can at best only fool the world for a very brief period.

A DISORDERLY RESET

The real reset, which will be disorderly, will inevitably happen thereafter. This will involve an implosion of the financial system including debt, stock and property markets. Sadly Humpty will be totally buried in the rubble of this collapse.

As I have pointed out many times, the world can only attain real growth in a system which has eliminated a mega debt which can never be serviced or repaid. What must also implode are fake bubble markets and false money.

The transition to a sound system will clearly be very painful for the world, but sadly totally necessary.

A DANGEROUS INTERCONNECTED WORLD

Before we get there, we will see more of the same, namely unlimited money printing which has already started. But we have only seen the mere beginning. The danger with a global financial system is that nobody can escape. Everything is totally interconnected and interlocking. A serious problem in a Hong Kong bank will instantaneously reverberate around the world and within minutes affect the whole financial system.

Take Deutsche Bank (DB) which many observers have for many years expected to fall. It has equity of €57B which is only 4% of their total balance sheet. In addition, their gross derivative exposure is €44 trillion. The market cap is just €18B, well below the equity. So the market clearly doesn’t believe the net asset value is real.

A 5% bad debt write-off or a 0.13% loss in derivatives would be enough to wipe out DB. It would be surprising if the losses on the debt portfolio were less than 25% or derivative losses less than say 5%. Still, these magnitudes of losses would bankrupt DB.

DERIVATIVES – A NUCLEAR BOMB

Derivatives is a nuclear bomb and when a counterparty fails, the $1.5+ quadrillion bubble will burst in one fell swoop.

In a fractured global financial system where every single entity is under-capitalised. It will take very little to bring everything down at once. And that is not an improbable outcome in the next few years.

This brings us back to gold which stands as La Grande Resistance against the broken Humpty or financial system.

It is no coincidence that gold is the only money that has survived every single financial crisis in history. For 5,000 years, there has been no permanent replacement for gold. And whatever alternative governments and central bankers come up with to solve the current crisis, it can never replace nature’s money. Gold is eternal money and the only reserve currency that has stood the test of time.

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

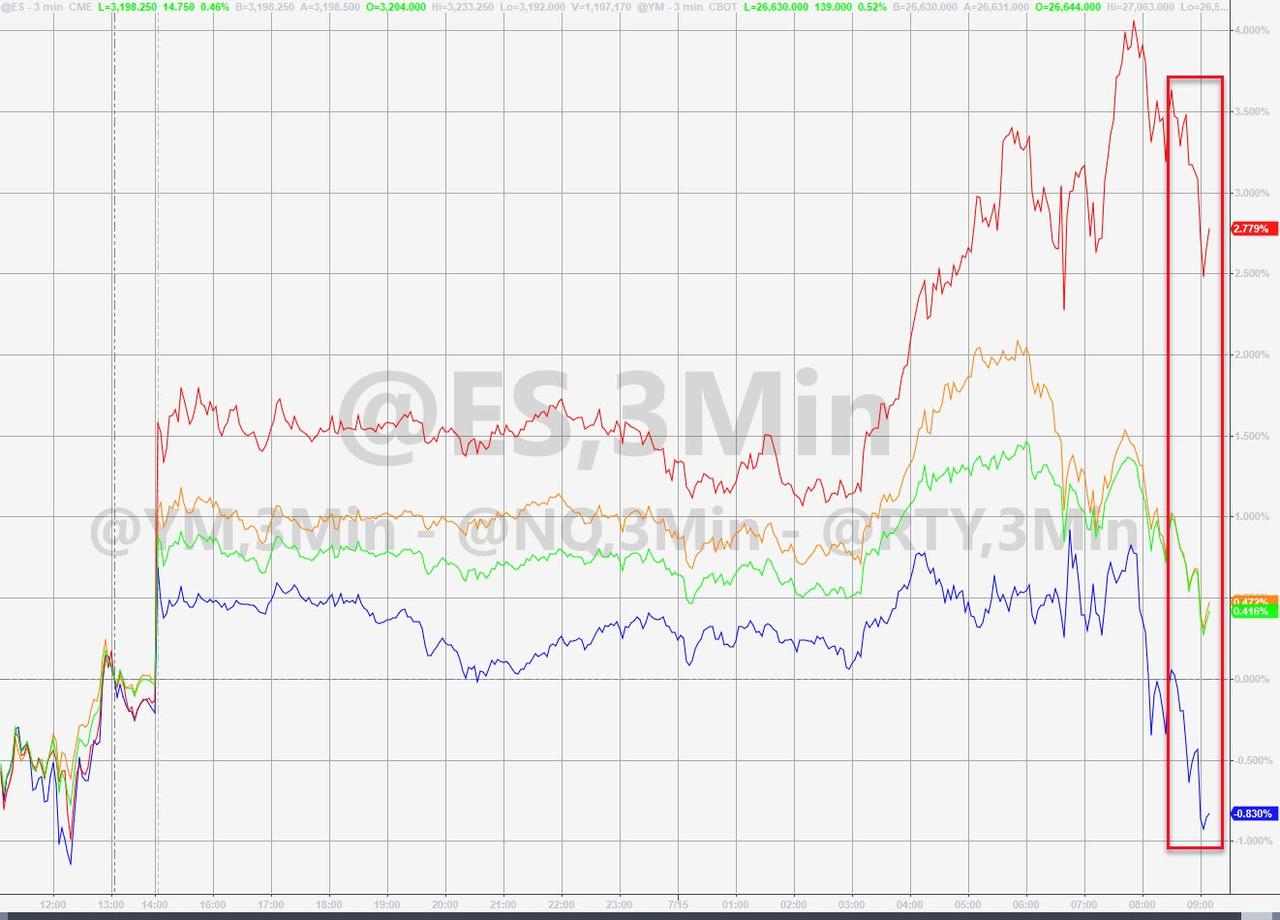

Global Stocks Soar On Vaccine Optimism

Global stocks surged, and US equity futures jumped rising to the Monday pre-dump highs, on coronavirus vaccine optimism (with headlines now conveniently appearing every time stocks appear poised for a selloff) and looking past record daily death rates in some states and brewing tensions between Washington and Beijing. Yields rose and the dollar slumped to a one month low.

US stocks staged a late session surge on Tuesday after news that Moderna’s coronavirus vaccine produced antibodies to the coronavirus in all patients tested in an initial safety trial. The vaccine developments brought optimism to financial markets that have been struggled to make headway recently in the face of new outbreaks across the U.S. and Asia.

Moderna shares surged 18% in pre-market trading following late Tuesday news that it was safe and provoked immune responses in all 45 healthy volunteers in an ongoing early-stage study, while AstraZeneca rose after a report that a medical journal will release positive news on the coronavirus vaccine the company is developing with University of Oxford researchers. American Airlines, United Airlines Holdings, Carnival Corp, Royal Caribbean Cruises Ltd and Norwegian Cruise Line Holdings Ltd rose between 6% and 6.8%.

“The vaccine news is clearly a positive development,” said Mark Nash, head of global fixed income at Merian Global Investors. “But it’s still long way off. The fear of the W-shaped recovery is probably very high at the moment. Good news is that markets still have a chance to ride it out because the Fed has bought time, so financial conditions can stay easy until growth kicks in.”

Europe’s Stoxx 600 Index extended gains to 1.3% shortly before noon in London, with travel leading among sectors, amid positive sentiment in markets on the back of progress in developing a coronavirus vaccine. European index heads for a third day of gains in four sessions The Travel & Leisure sector rose 2.7%, led by Carnival while the Stoxx Europe 600 Industrial Goods & Services +2.5%, boosted by Schneider Electric, Adyen. Banks and telecom gauges are the only two trading lower. Atlantia SpA surged 22% as Italy’s government moved to resolve a long-running dispute linked to a 2018 bridge collapse.

Earlier in the session, Asian stocks gained, led by industrials and materials, after falling in the last session. Most markets in the region were up, with India’s S&P BSE Sensex Index gaining 1.9% and Australia’s S&P/ASX 200 rising 1.9%, while Shanghai Composite dropped 1.6%. Trading volume for MSCI Asia Pacific Index members was 17% above the monthly average for this time of the day. The Topix gained 1.6%, with Danto and SERAKU rising the most.

Surprisingly, Chinese markets underperformed with the Hang Seng and Shanghai Comp. (-1.6%) both negative after US President Trump signed legislation and an executive order to hold China accountable for actions in Hong Kong, with the executive order to remove preferential treatment for Hong Kong and which will now be treated the same as China. Furthermore, China later responded that it strongly opposes US signing the sanctions bill and that it will implement its own sanctions on US officials and entities. Reports of China state funds continuing to sell shares also did not help in which a pension fund was said to have offloaded 42.3mln BoCom A-shares on Tuesday.Qianjiang Water Resources Development and Shanghai LongYun Media Group Co Ltd posting the biggest drops.

In FX, the Bloomberg Dollar Spot Index fell to a one-month low as Norway’s Krone led G-10 gains followed by the pound; the krone was also supported by higher oil prices, while sterling got a boost after U.K. inflation surprisingly accelerated last month. The euro rose a fourth day against the dollar to a four- month high of 1.1445, and the cost to hedge one-day fluctuations in euro-dollar suggests market makers see a good chance that year-to-date highs may come to test as Thursday’s European Central Bank meeting comes into focus. Sweden’s krona touched its strongest level in 17 months against the euro as risk sentiment improved and following a report that showed Swedish inflation expectations didn’t drop further.

In rates, Treasury yields moved higher with gilt yields also rising after a debt sale. US Treasury yields were higher by 2bp-3bp at long end, remaining inside weekly ranges, 10-year by ~2bp at 0.643; U.K. 10-year yield higher by 2.6bp, gilts leading declines for sovereign bond markets. UST 5s30s steeper for first day in five, approaching 104bp.

In commodities, oil gained after a report pointed to a drop in U.S. crude stockpiles; gold remained well above $1800.

Looking at the day ahead, the focus will be on corporate earnings with highlights including UnitedHealth Group, Goldman Sachs, US Bancorp, BNY Mellon and Infosys. Otherwise, there’ll be a rate decision from the Bank of Canada, the release of the Fed’s Beige book, as well as remarks from the BoE’s Tenreyro and the Fed’s Harker. Finally, data highlights include June industrial production and capacity utilisation numbers, along with July’s Empire State manufacturing survey.

Top Overnight News from Bloomberg

- German Chancellor Angela Merkel said she’s prepared to compromise in difficult talks on assembling a European recovery plan this weekend in Brussels, as Spanish Prime Minister Pedro Sanchez urged leaders to reach an accord at the meeting

- The EU Council needs to make a decision on a European recovery plan by the end of July, Italy’s Prime Minister Giuseppe Conte tells lawmakers on Wednesday

- Bank of Japan Governor Haruhiko Kuroda said Japan’s economy was past the worst, but warned the recovery would be slow, adding that he remains ready to take further action if needed; said that excessively low super-long yields could cause problems

- The U.K. will sell nearly twice as many bonds than it did during the height of the financial crisis, according to estimates of primary dealers

- Bank of England policy maker Silvana Tenreyro says current pace of recovery will be slowed by social distancing, restrictions in some sectors and higher unemployment

- U.K. levels of Covid-19 infection fell faster than previously reported in May, according to a study of 120,000 people that took place before the country’s lockdown was eased

- OPEC+ is seeking extra production cuts from members that have missed their targets again in June, potentially tempering the impact of the supply resumption planned by the wider coalition next month.

Market Snapshot

- S&P 500 futures up 0.8% to 3,208.00

- STOXX Europe 600 up 0.9% to 370.81

- MXAP up 1.1% to 166.57

- MXAPJ up 0.8% to 548.07

- Nikkei up 1.6% to 22,945.50

- Topix up 1.6% to 1,589.51

- Hang Seng Index up 0.01% to 25,481.58

- Shanghai Composite down 1.6% to 3,361.30

- Sensex up 1.9% to 36,710.28

- Australia S&P/ASX 200 up 1.9% to 6,052.92

- Kospi up 0.8% to 2,201.88

- German 10Y yield fell 1.1 bps to -0.458%

- Euro up 0.3% to $1.1438

- Italian 10Y yield fell 2.4 bps to 1.085%

- Spanish 10Y yield fell 1.4 bps to 0.394%

- Brent futures up 1.5% to $43.54/bbl

- Gold spot little changed at $1,810.36

- U.S. Dollar Index down 0.4% to 95.91

Asian equity markets were mostly positive as the regional bourses tracked the cyclical-led gains in US peers and on vaccine hopes after Moderna’s COVID-19 vaccine produced antibodies in all 45 patients tested in an initial study. ASX 200 (+1.9%) and Nikkei 225 (+1.6%) were lifted from the open with Australia’s tech sector and gold miners front-running the broad advances in the index which surpassed the 6000 milestone, while the Japanese benchmark printed its highest level in over a month and withstood the ongoing virus concerns in Tokyo which prompted the city to switch to its highest COVID-19 alert status. Chinese markets underperformed with the Hang Seng (U/C) and Shanghai Comp. (-1.6%) both negative after US President Trump signed legislation and an executive order to hold China accountable for actions in Hong Kong, with the executive order to remove preferential treatment for Hong Kong and which will now be treated the same as China. Furthermore, China later responded that it strongly opposes US signing the sanctions bill and that it will implement its own sanctions on US officials and entities. Reports of China state funds continuing to sell shares also did not help in which a pension fund was said to have offloaded 42.3mln BoCom A-shares on Tuesday. Indian markets were also notable gainers with the NIFTY up 0.2% and the NIFTY IT index gaining around 3% in early trade alongside Wipro shares which hit 10% upper circuit following a beat on earnings. Finally, 10yr JGBs were lacklustre amid the gains in stocks and unsurprising BoJ policy hold, while there was notable corporate supply with Nissan pricing a JPY 70bln 3-tranche in its first JPY-denominated bond offering since 2016.

Top Asian News

- Hong Kong’s Beaten Down Stocks Face Yet Another Blow from Trump

- Central Banker Urges Israel to Seize Cheap Debt Opportunity

- Hillhouse Invested About $1 Billion In Beigene’s Share Sale

- ChemChina, State Funds Said in Talks for Syngenta’s Pre-IPO

European equities trade higher across the board (Eurostoxx 50 +1.1%) following the recovery in the latter half of yesterday’s session for US equities. As has been the case throughout the week, there wasn’t a great deal of narrative-altering newsflow for the majority of the session with many of the same macro factors that are in focus having been present for some time now. Some of the positivity late doors emanated from a COVID-19 drug update from Moderna, however, the latest update doesn’t necessarily mark a breakthrough from the data already published in May with the latest findings instead from a larger sample group than prior. More recently, global bourses took another leg higher and moved back into proximity to session highs on reports via ITV’s Peston that positive news is on the way, perhaps as soon as tomorrow, for AstraZeneca’s (+2.9%) COVID-19 vaccine – which is seeing a rare ‘twin effect’ in terms of the response for both antibodies and T-cells. In terms of sectoral performance for Europe, travel & leisure names are the clear outperformer with the sector noted as one of the purest reopening plays. Carnival (+5.3%), Ryanair (+5.1%), Tui (+3.2%) and easyJet (+2.9%) all trade with notable gains, however, there has been little in the way of sector-specific newsflow in the past 24 hours for European airline names. Elsewhere, Auto names are also trading firmer today with Renault the outperformer in the sector after reports that Nissan is to start selling an EV. To the downside, Telecom names lag peers in a potential pullback from some of the upside seen yesterday in the wake of the UK’s decision to bar Huawei from the UK’s 5G network by 2027. In terms of individual movers, Atlantia (+24.2%) sit at the top of the Stoxx 600 as the company appears to be making progress in striking a deal with the Italian government, whilst Burberry (-6.9%) are a notable underperformer after its latest trading update in which it expects a potential 50% decline in H1 sales.

Top European News

- The 700 Billion-Euro Man Counting Each Cent to Keep Italy Afloat

- Kremlin Plots Pullback from Stimulus Despite Rising Infections

- Sunak Orders Review of U.K. Capital Gain Tax After Virus Splurge

- BOE’s Tenreyro Is Ready to Boost Stimulus Again If Needed

In FX, it was a woeful start to Wednesday’s EU session for the Greenback as losses accumulate across the board on various fundamental and technical factors, including a rebound in broad risk sentiment due to more positive COVID-19 vaccine reports and somewhat contradictory persistent/latent concerns about the resurgence of the virus in US states. The index has fallen below 96.000 and close to June lows (95.716) at 95.866 as several Dollar/major pairs extend beyond or breach round number levels that have been providing some support for the Buck and resistance in terms of G10 counterparts. Ahead, a busy midweek US data docket and more Fed speak from Harker before the latest Beige Book.

- GBP – Sterling has benefited most from the Greenback’s ongoing travails, with Cable back above 1.2600, but the Pound also reclaiming losses vs the Euro from sub-0.9100 lows yesterday on a technical retracement rather than anything specifically Gbp supportive. On that note, UK CPI data was a tad firmer than expected, but still benign and BoE’s Tenreyro subsequently countered with a disinflationary outlook, while adding that NIRP is a live issue for the MPC currently under review.

- AUD/NZD/EUR/JPY/CAD/CHF – All firmer against the US Dollar as noted above, with the Aussie hitting fresh 1+ month highs with the aid of momentum buying when 0.7005 was breached, but meeting offers into 0.7020 ahead of jobs data on Thursday. Meanwhile, the Kiwi continues to lag around 0.6550 and 1.0680 in Aud/Nzd cross terms awaiting Q2 CPI tonight in contrast to the Euro that has extended gains on the 1.1400 handle to circa 1.1445 and surpassing June 10’s 1.1422 best along the way pre-ECB tomorrow. Elsewhere, the Yen has rebounded from 107.30 to 106.90 and the Loonie is pivoting 1.3600 in the run up to the BoC with options pricing in a 57 pip break-even on the event, while the Franc remains mixed either side of 0.9400 vs the Buck and down to 1 month lows against the single currency near 1.0740.

- SCANDI/EM – The Norwegian and Swedish Crowns are both nudging key markers vs the Euro at 10.6500 and 10.3500 respectively, with the former buoyed by firm crude prices and latter maintaining post-inflation data impetus even though June’s trade deficit widened significantly and almost all CPI/CPIF projections from Prospera were unchanged. Similarly, the Rand has taken weaker than forecast SA inflation in stride on overall Dollar weakness and despite potential implications for the SARB policy meeting next week given a relatively reserved -25 bp consensus vs -1/2 point last time.

In commodities, WTI and Brent remain bolstered ahead of the JMMC meeting, with sentiment generally positive this morning and after last nights larger than expected draw in private inventories. Firstly, the JMMC, which energy correspondents note is expected to commence from around 13:00BST/08:00ET but as with any OPEC related event the timing should be taken as guidance only. Indications heading into the JMMC meeting point towards the committee recommending that the level of production cuts is reduced, which would be in-line with the original plan. As a reminder, the JTC committee met yesterday to discuss the planned easing of cuts to 7.7mln BPD; note, Saudi is said to be looking to keep export figures steady for the month of August. JMMC aside, much of the upside price action follows on from yesterday’s private inventories where crude stocks printed a larger than expected draw of 8.3mln vs. Exp. draw of 2.1mln; focus turns to today’s EIA stocks for confirmation of this reading with expectations pointing to a draw of 2.09mln. Turning to metals, spot gold has been choppy this morning with the upside just after the European cash open derived from further USD downside as well as resistance levels lying in proximity to the current high. Elsewhere, Antofagasta is calling for further negotiations to resolve the strike action in Chile; but, the strike action has not been sufficient to bolster copper prices thus far.

US Event Calendar

- 8:30am: Export Price Index MoM, est. 0.8%, prior 0.5%; Import Price Index MoM, est. 1.0%, prior 1.0%

- 8:30am: Empire Manufacturing, est. 10, prior -0.2

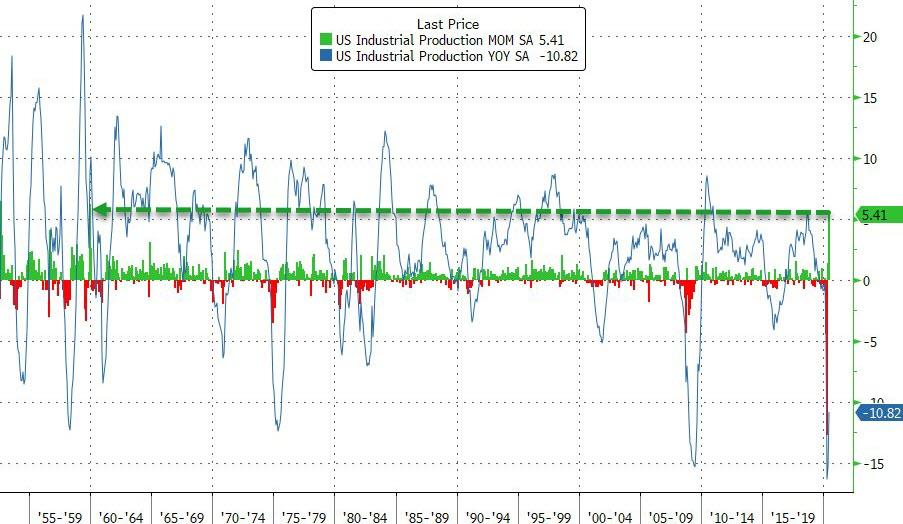

- 9:15am: Industrial Production MoM, est. 4.3%, prior 1.4%; Manufacturing (SIC) Production, est. 5.65%, prior 3.8%

- 2pm: U.S. Federal Reserve Releases Beige Book

DB’s Jim Reid concludes the overnight wrap

Unless I’m forgetting a random trip, I drove a car yesterday for the first time since lockdown and also wore a mask for the first time. Luckily I didn’t do the two together as my glasses kept on steaming up wearing it. Watch that mobility data climb in the U.K.. It was only 4 minutes to a local physio as I’ve hurt my hip and back over the last month and it won’t go away, especially when my wife asks me to do something. The physio has managed to diagnose it. It’s got quite a complicated name so bear with me. She said it’s likely “middleagemanovergolfingintheeveningsinlockdownitis”. In short I’m having spasms all over my lower back. Interestingly she said that since she reopened she is seeing a surge in patients as people have either done too little exercise in lockdown or too much.