GOLD:$1801.50 DOWN $9.80 The quote is London spot price (cash market)

Silver:$19.22// DOWN 14 CENTS London spot price ( cash market)

Closing access prices: London spot

i)Gold : $1797.25 LONDON SPOT 4:30 pm

ii)SILVER: $19.16//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUG GOLD: $1797.80 CLOSE 1.30 PM// SPREAD SPOT/FUTURE AUG /:- $2.20

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $19.57…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : 35 CENTS PER OZ

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today:0/317

issued: 210

EXCHANGE: COMEX

CONTRACT: JULY 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,811.400000000 USD

INTENT DATE: 07/15/2020 DELIVERY DATE: 07/17/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

152 C DORMAN TRADING 42

332 H STANDARD CHARTE 17

355 C CREDIT SUISSE 24

657 C MORGAN STANLEY 8

657 H MORGAN STANLEY 140

661 C JP MORGAN 210

686 C INTL FCSTONE 87

690 C ABN AMRO 36

737 C ADVANTAGE 8 25

800 C MAREX SPEC 13 9

878 C PHILLIP CAPITAL 15

____________________________________________________________________________________________

TOTAL: 317 317

MONTH TO DATE: 7,528

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 317 NOTICE(S) FOR 317,000 OZ (.9860 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 7528 NOTICES FOR 752,800 OZ (23.415 TONNES)

SILVER

FOR JULY

752 NOTICE(S) FILED TODAY FOR 3,760,000 OZ/

total number of notices filed so far this month: 14,671 for 73.355 MILLION oz

BITCOIN MORNING QUOTE $9116 DOWN 80

BITCOIN AFTERNOON QUOTE.: $9127 DOWN $74

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $9.80 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

NO CHANGES IN GOLD INVENTORY AT THE GLD:

GLD: 1,206.89 TONNES OF GOLD//

WITH SILVER DOWN 14 CENTS TODAY: AND WITH NO SILVER AROUND:

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUGE PAPER DEPOSIT OF 5.123 MILLION OZ//

WHAT A FRAUD!!

RESTING SLV INVENTORY TONIGHT:

SLV: 521.197 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A TINY SIZED 172 CONTRACTS FROM 178,367 UP TO 178,539, AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE TINY SIZED GAIN IN OI OCCURRED DESPITE OUR STRONG 21 CENT GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE SMALL GAIN IN COMEX OI IS PRIMARILY DUE TO HUGE BANKER SHORT COVERING PLUS A STRONG EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A SMALL DECREASE IN SILVER STANDING AT THE COMEX FOR JULY. WE HAD A NET GAIN IN OUR TWO EXCHANGES OF 2902 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: JULY: 0 AND SEP 2730 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 2730 CONTRACTS. WITH THE TRANSFER OF 2730 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2730 EFP CONTRACTS TRANSLATES INTO 13.65 MILLION OZ ACCOMPANYING:

1.THE 21 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

81.550 MILLION OZ INITIALLY IN JULY.

WEDNESDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 21 CENTS).. AND,OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS. THE SMALL GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A SMALL DECREASE IN STANDING OF SILVER OZ STANDING FOR JULY, STRONG BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A NET GAIN OF 2902 CONTRACTS OR 14,51 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

JULY

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF JULY:

9599 CONTRACTS (FOR 11 TRADING DAY(S) TOTAL 9599 CONTRACTS) OR 47.99 MILLION OZ: (AVERAGE PER DAY: 873 CONTRACTS OR 4.363 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 47.99 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 6.85% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,185.41 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 47.99 MILLION OZ/

EXCHANGE FOR PHYSICAL ISSUANCE FOR THE PAST 60 DAYS IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD A TINY SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 172, DESPITE OUR 21 CENT GAIN IN SILVER PRICING AT THE COMEX ///WEDNESDAY… THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2730 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A STRONG SIZED OI CONTRACTS ON THE TWO EXCHANGES: 2902 CONTRACTS (WITH OUR 21 CENT GAIN IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 2730 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A TINY SIZED INCREASE OF 172 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED DESPITE A 21 CENT GAIN IN PRICE OF SILVER/AND A CLOSING PRICE OF $19.36 // THURSDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.892 BILLION OZ TO BE EXACT or 127% of annual global silver production (ex Russia & ex China).

FOR THE NEW JULY DELIVERY MONTH/ THEY FILED AT THE COMEX: 752 NOTICE(S) FOR 3,760,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 81.550 million oz

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1322 CONTRACTS TO 578,853 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE SMALL SIZED LOSS OF COMEX OI OCCURRED DESPITE OUR TINY GAIN IN PRICE OF $1.65 /// COMEX GOLD TRADING// WEDNESDAY// WE HAD HUGE BANKER SHORT COVERING, ANOTHER HUMONGOUS SIZED GOLD OZ STANDING AT THE COMEX FOR JULY, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR TINY GAIN IN PRICE OF $1.65 .

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 64

WE GAINED A GOOD SIZED 1130 CONTRACTS (3.514 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 2425 CONTRACTS:

CONTRACT .; AUG 2045 AND OCT: 380 DEC: 0 ALL OTHER MONTHS ZERO//TOTAL: 2425. The NEW COMEX OI for the gold complex rests at 578.853. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1130 CONTRACTS: 1322 CONTRACTS DECREASED AT THE COMEX AND 2425 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 1130 CONTRACTS OR 3.514 TONNES. WEDNESDAY, WE HAD A GAIN OF $1.65 IN GOLD TRADING……

AND WITH THAT GAIN IN PRICE, WE HAD A STRONG SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 4.416 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $1.65).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS ALSO UNSUCCESSFUL (SEE BELOW).

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2425) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (1005 OI): TOTAL GAIN IN THE TWO EXCHANGES: 1130 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)ANOTHER HUMONGOUS INCREASE IN GOLD STANDING AT THE GOLD COMEX FOR THE FRONT JULY MONTH, 3) ZERO LONG LIQUIDATION; 4) SMALL COMEX OI LOSS.5) SMALL EXCHANGE FOR PHYSICAL ISSUANCE… AND …ALL OF THIS WAS COUPLED WITH OUR TINY GAIN IN GOLD PRICE TRADING//WEDNESDAY//$1.65.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

SPREADING OPERATIONS/NOW SWITCHING TO GOLD

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN GOLD AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF AUGUST FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF JULY. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUGUST), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

JULY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY(S) IN TONNES: 130.89 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 130.89/3550 x 100% TONNES =3.68% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3149.09 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 130.89 TONNES SO FAR..

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A TINY SIZED 172 CONTRACTS FROM 178,367 UP TO 178,551 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE TINY GAIN IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) HUGE BANKER SHORT COVERING , 2) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A SMALL DECREASE STANDING AT THE SILVER COMEX FOR JULY AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 2730 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY: 0 CONTRACTS AND SEPT: 2730 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2730 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 172 CONTRACTS TO THE 2730 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 2902 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 14.720 MILLION OZ, OCCURRED WITH OUR STRONG 21 CENT GAIN IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 151.21 POINTS OR 4.50% //Hang Sang CLOSED DOWN 510.89 POINTS OR 2.00% /The Nikkei closed DOWN 175.13 POINTS OR 0.76%//Australia’s all ordinaires CLOSED DOWN .61%

/Chinese yuan (ONSHORE) closed DOWN at 6.9936 /Oil UP TO 40.21 dollars per barrel for WTI and 43.55 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9936 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9920 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

i)we had 1 deposits into the customer account

into JPMorgan: 0

ii) Into CNT: 603,883.100 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.744 million oz of total silver inventory or 49.67% of all official comex silver. (160.819 million/323.767 million

total customer deposits today: 603,883.100 oz

we had 1 withdrawals:

ii) Out of CNT: 624,826.880 oz

total withdrawals; 624,826.880 oz

We had 0 adjustments

total dealer silver: 127.311 million

total dealer + customer silver: 323.767 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The front month of July has an open interest of 2391 contracts, as we lost 27 contracts. We had 16 notices served on WEDNESDAY, so we lost a tiny 11 contracts or an additional 55,000 oz will not stand in this active delivery month of July as they morphed into a London based forwards. It seems that we have little silver over on this side of the pond.

The next month after July is the non active month of August and here sees its open interest ROSE by 7 contracts UP to 817

The big September contract month sees a loss of 247 contracts down to 139,998.

The total number of notices filed today for the JULY 2020. contract month is represented by 752 contract(s) FOR 3,760,000, oz

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 14,671 x 5,000 oz = 73,355,000 oz to which we add the difference between the open interest for the front month of JULY.(2391) and the number of notices served upon today 752 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the JULY/2019 contract month: 14,671 (notices served so far) x 5000 oz + OI for front month of JULY (2391)- number of notices served upon today (752) x 5000 oz of silver standing for the JULY contract month.equals 81,550,000 oz. (A WHOPPER )

WE LOST 11 CONTRACTS OR 55,000 OZ WILL NOT STAND FOR DELIVERY. SILVER IS STILL VERY SCARCE ON THIS SIDE OF THE POND AND THE REASON FOR MORPHING OVER TO LONDON.

TODAY’S ESTIMATED SILVER VOLUME : 50,865 CONTRACTS // volume fair/

FOR YESTERDAY:61,961.,CONFIRMED VOLUME//volume fair/

YESTERDAY’S CONFIRMED VOLUME OF 61,961 CONTRACTS EQUATES to 309 million OZ 44.1% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 0.33% ((JULY 16/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -+.16% to NAV: (JULY 16/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 0.33%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 17.32 TRADING 17.25///NEGATIVE 0.42

END

And now the Gold inventory at the GLD/

JULY 16/WITH GOLD DOWN $9.80 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: INVENTORY RESTS AT 1206.89 TONNES

JULY 15//WITH GOLD UP $1.55 TODAY/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 2.96 TONNES INTO THE GLD///INVENTORY RESTS AT 1206.89 TONNES

JULY 14//WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 3.51 TONNES/INVENTORY RESTS AT 1203.97 TONNES

JULY 13//WITH GOLD UP $12.50 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1200.46 TONNES

JULY 10/WITH GOLD DOWN $.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD//A STRANGE WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1200.82 TONNES

JULY 9//WITH GOLD DOWN $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OX 3.21 TONNES INTO THE GLD//INVENTORY RESTS AT 1202.57 TONNES

JULY 8/WITH GOLD UP $13.75 TODAY; A BIG CHANGE IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 7.89 TONNES INTO THE GLD//INVENTORY RESTS AT 1199.36 TONNES

JULY 7/WITH GOLD UP $12.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1191.47 TONNES

JULY 6/WITH GOLD UP $6.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1191.47 TONNES

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

JUNE 30//WITH GOLD UP $16.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1178.90 TONNES

JUNE 29/WITH GOLD UP $2.90 TODAY: A HUGE DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1178.90 TONNES

JUNE 26/WITH GOLD UP $5.03 TODAY: VERY STRANGE: A PAPER WITHDRAWAL OF 1.46 TONNES//INVENTORY RESTS AT 1175.39 TONNES

JUNE 25//WITH GOLD DOWN $3.30 TODAY//ANOTHER STRONG PAPER DEPOSIT OF 7.6 TONNES///INVENTORY RESTS AT 1176.85 TONNES

JUNE 24/WITH GOLD DOWN $1.50 TODAY; A STRONG 3.21 TONNES ADDED TO THE GLD//INVENTORY RESTS AT 1169.25 TONNES

JUNE 23/WITH GOLD UP $25.50 TODAY/ANOTHER CRIMINAL PAPER DEPOSIT OF 6.73 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1166.04 TONNES

JUNE 22/WITH GOLD UP $14.00 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 23.09 TONNES//INVENTORY RESTS AT 1159.31 TONNES

JUNE 19/WITH GOLD UP$16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//; INVENTORY RESTS AT 1136.22 TONNES

JUNE 18//WITH GOLD DOWN $2.75 TODAY: NO CHANGES IN GOLD INVENTORY: INVENTORY RESTS AT 1136.22 TONNES

JUNE 17/WITH GOLD DOWN $1.05: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1136.22 TONNES

JUNE 16//WITH GOLD UP $6.70 TODAY: NO CHANGES IN GOLD INVENTORY: /INVENTORY RESTS AT 1136.22 TONNES

JUNE 15/WITH GOLD DOWN ANOTHER $8.80 TODAY, NO CHANGES IN GOLD INVENTORY/INVENTORY RESTS AT 1136.22 TONNES

JUNE 12//WITH GOLD DOWN $1.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 1.17 TONNES AT THE GLD//INVENTORY RESTS AT 1136.22 TONNES

JUNE 11//WITH GOLD UP $16.80 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 6.55 TONNES AT THE GLD//INVENTORY RESTS AT 1135.05 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

JULY 16/ GLD INVENTORY 1206.89 tonnes*

LAST; 862 TRADING DAYS: +263.07 NET TONNES HAVE BEEN ADDED THE GLD

LAST 762 TRADING DAYS://+441.18 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JULY 16//WITH SILVER DOWN 14 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ//INVENTORY RESTS AT 521.197 MILLION OZ..

JULY 15.WITH SILVER UP 21 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.956 MILLION OZ//INVENTORY RESTS AT 516.074 MILLION OZ//

JULY 14/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 514.118 MILLION OZ//

JULY 13//WITH SILVER UP 67 CENTS TODAY: A HUGE CHANGE IN SILVER: A WITHDRAWAL OF 1.677 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 514.118 MILLION OZ//

JULY 10/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 4.844 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.795 MILLION OZ

WHAT A FRAUD!!

JULY 9/WITH SILVER DOWN 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 8.198 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 510.951 MILLION OZ/

JULY 8/WITH SILVER UP 37 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.118 MILLION OZ FROM THE SLV//VERY SURPRISING.//INVENTORY RESTS AT 502.753 MILLION OZ//

JULY 7/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/INVENTORY RESTS AT 503.871 MILLION OZ///

JULY 6//WITH SILVER UP 24 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.863 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 503.871 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

JUNE 30/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 29/WITH SILVER DOWN ONE CENT TODAY: A TWO CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 466,000 OZ TO PAY FOR STORAGE FEES AND INSURANCE//// AND A LARGE DEPOSIT OF 1.212 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 26/WITH SILVER UP 6 CENTS TODAY: ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ RESTS AT 491.858 MILLION OZ//

JUNE 25/WITH SILVER UP 12 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 931,000 OZ INTO THE SLV////INVENTORY RESTS AT 491.858 MILLION OZ//

JUNE 24///WITH SILVER DOWN 31 CENTS// NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 490.927 MILLION OZ

JUNE 23//WITH SILVER UP 16 CENTS TODAY: A MONSTROUS CHANGE IN INVENTORY: A PAPER DEPOSIT OF 4.473 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 490.927 MILLION OZ//

JUNE 22/WITH SILVER UP 15 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/: INVENTORY/INVENTORY RESTS AT 486/454 MILLION OZ//

JUNE 19//WITH SILVER UP 22 CENTS TODAY: STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 839,000 OZ FROM THE SLV////INVENTORY RESTS AT 486,454 MILLION OZ..

JUNE 18/WITH SILVER DOWN 16 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 932,000 OZ INTO THE SLV////INVENTORY RESTS AT 487.293 MILLION OZ

JUNE 17/WITH SILVER UP 8 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.261 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.361 MILLION OZ

JUNE 16//WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.118 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 483.100 MILLION OZ//

JUNE 15/WITH SILVER DOWN 14 CENTS NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 481.982 MILLION OZ///

JUNE 12/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: TWO DEPOSITS OF 7.269 MILLION OZ AND 1.802 MILLION OZ ADDED TO THE SLV///INVENTORY RESTS THIS WEEKEND AT 481.982 MILLION OZ//

JUNE 11//WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY: ///INVENTORY RESTS AT 472.89 MILLION OZ//

JULY 16.2020:

SLV INVENTORY RESTS TONIGHT AT

521.197 MILLION OZ.

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

‘Death Cross’ Strikes U.S. Dollar As Virus Cases Grow

(Reuters)

A resurgent coronavirus pandemic in the United States and the prospect of improving growth abroad are souring some investors on the dollar, threatening a years-long rally in the currency.

The dollar index is off 6% from its recent highs, while net bets against the currency in futures markets stand near their highest level since 2018.

A decline in the dollar earlier this week set off a technical formation known as a “Death Cross,” which occurs when the 50-day moving average crosses below the 200-day moving average, according to analysts at BofA Global Research.

Past occurrences of the Death Cross have been followed by a period of dollar weakness eight out of nine times since 1980 when the 200-day moving average has been declining, as it is now, analysts at the bank said.

The U.S. currency’s weakness comes amid criticism over the government’s response to the coronavirus pandemic and protests over racial inequality that has eroded support for President Donald Trump months before the Nov. 3 presidential election

You can read the full article here

NEWS and COMMENTARY

Gold hits 1-week peak as U.S.-China row adds to safe-haven demand

Gold ends with a modest loss, holding ground above $1,800 an ounce

Trump says he is ‘not interested’ in trade talks with China

Fed officials warn on ‘thick fog’ ahead for U.S. economy as recovery concerns deepen

Treasury yields move higher ahead of Fed’s Beige Book report

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

14-Jul-20 1798.20 1801.90, 1436.58 1440.62 & 1583.14 1581.71

13-Jul-20 1808.05 1807.50, 1435.23 1432.26 & 1598.32 1591.68

10-Jul-20 1805.75 1803.10, 1433.40 1427.33 & 1599.35 1594.84

09-Jul-20 1812.45 1812.10, 1434.01 1431.74 & 1600.57 1600.08

08-Jul-20 1799.35 1811.10, 1438.40 1438.74 & 1596.38 1598.48

07-Jul-20 1775.50 1789.55, 1423.77 1424.84 & 1576.11 1585.00

06-Jul-20 1774.40 1787.90, 1420.76 1429.43 & 1572.12 1578.36

03-Jul-20 1774.65 1772.90, 1426.29 1422.40 & 1580.33 1577.70

02-Jul-20 1771.85 1777.45, 1415.00 1421.60 & 1568.97 1577.13

01-Jul-20 1787.40 1771.15, 1444.90 1424.63 & 1592.93 1574.82

Own gold coins and bars in the safest vaults in Zurich, Switzerland with GoldCore. Learn why Switzerland remains a safe haven jurisdiction for owning precious metals. Access Our Most Popular Guide, the Essential Guide to Storing Gold in Switzerland here

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here

ii) Important gold commentaries courtesy of GATA/Chris Powell

iii) Other physical stories:

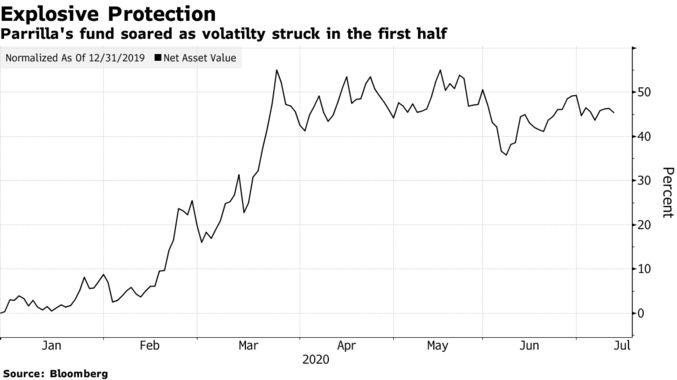

Soaring Inflation To Send Gold To $5000 “Doomsday” Fund Predicts

Picking up on what Russell Napier said recently, when the formerly iconic deflationist threw in the towel and now expects inflation because “control of money supply has permanently left the hands of central bankers”, a fund manager who returned 47% this year by betting heavily on gold and Treasuries says the next decade is going to be marked by inflation that central banks are powerless to control.

Diego Parrilla, who heads the $450 million Quadriga Igneo fund dubbed “Doomsday” by Bloomberg, perhaps because unlike most of his peers he refused to buy into the biggest groupthink trade ever namely FAAMG stocks, said unprecedented monetary stimulus is fueling asset bubbles and corporate debt addiction, which renders rate hikes impossible without an economic crash. In the ensuing market mania, the manager whose portfolio is loaded up with cross-asset hedges says gold could rise as high as $5,000 an ounce in the next three to five years, more than doubling from its current price of $1,800 which is just shy of all time highs.

“What you’re going to see in the next decade is this desperate effort, which is already very obvious, where banks and government just print money and borrow, and bail everyone out, whatever it takes, just to prevent the entire system from collapsing,” Parrilla told Bloomberg in an interview from Madrid.

Actually, we get why Quadriga Igneo was called “Doomsday”: it does not shy away from the truth that the Fed has pushed the financial system into a corner where any deviation from massive money injections would lead to catastrophe. Also, unlike most hedge funds – which as we noted earlier no longer function as they should due to central bank interventions – and whose job is to compound steady returns over time, Parrilla’s fund is similar to a “black swan” fund in that it tends to hedge the next big crash while generating capital over time. Managers with a tail-risk bias position for extreme market events, typically bucking mainstream views on Wall Street.

While calls for surging inflation have been often made in the past decade, yet were confined to financial assets while the broader economy suffered from lack of aggregate demand, Parrilla believes that the stimulus packages have exacerbated deeper issues within the financial system, “such as central banks who have kept interest-rates near zero for more than a decade and are willing to re-write the policy rulebook in a crisis.”

While the jury is still out on if and when soaring inflation will hit – although we should note that in recent weeks such prominent deflationists as Albert Edwards, Russell Napier and Horseman’s Russell Clark have all shifted to expecting runaway inflation in the coming year – Parrilla may be on to something if only based on the soaring value of his asset portfolio which soared as virus-fueled fear ripped through markets in February and March. The fund is about 50% invested in gold and precious metals, 25% in Treasuries and the rest in options strategies that profit from market chaos, such as calls on gold and the U.S. dollar.

“This is the part that makes us super explosive,” he said.

Quoted by Bloomberg, Parrilla, who previously ran the commodities department for Old Mutual Global Investors, described his investment process as search for anti-bubbles: unusually cheap assets that do well when bubbles burst. It had to wait patiently until its moment came: the Quadriga Igneo fund was launched in 2018 and had returned 10% by the end of the year. Performance was flat in 2019 before exploding by 50% in 2020.

“What we’ve seen over the last decade is the transformation from risk-free interest to interest-free risk, and what this has created is a global series of parallel synchronous bubbles,” said the fund manager, who is also the author of a book called “The Anti-Bubbles: Opportunities Heading into Lehman Squared and Gold’s Perfect Storm.”

“One of the key bubbles is fiat currency, and one clear anti-bubble in this system is gold,” he said, adding that other examples are volatility, correlations and inflation. “It’s a case of when, not if, they will reprice significantly higher.” We, and many others agree.

Parrilla is on a good start: gold has rallied 19% this year and captivated some of the world’s most prominent investors this year, who argue that the rapid expansion of central bank balance sheets will reduce fiat currency values and drive demand for hard assets.

“The bubbles are too big to fail and mommy and daddy will do whatever it takes to prevent this,” said Parrilla, referring to central banks who now step in and prop up capital markets after even a modest drop.

The 2018 Realvision clip below captures some of Parrilla’s core views.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

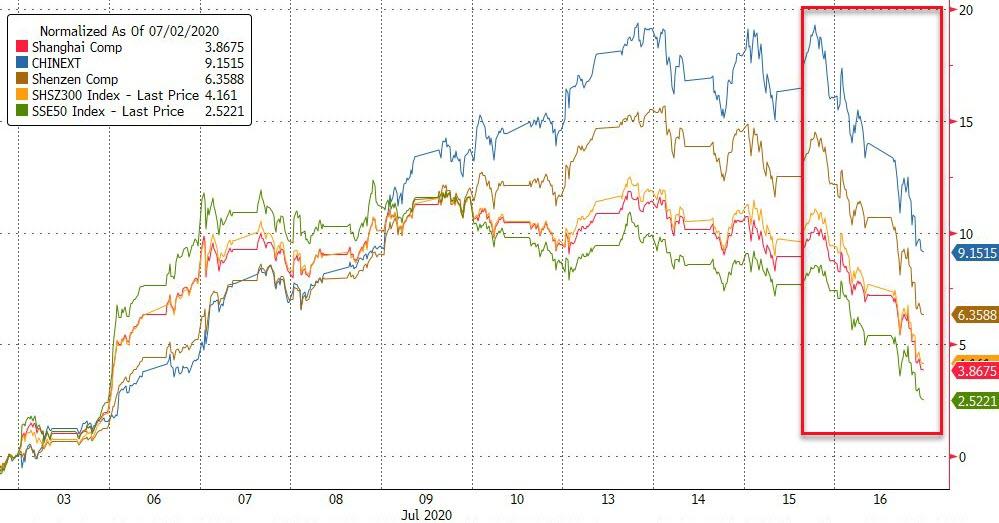

US Futures Slide As Chinese Stocks Crash

S&P futures slipped back under 3,200 and Chinese stocks finally cracked overnight, after a surprise drop in China’s retail sales signaled a bumpy economic recovery, with investors now turning to for guidance from the ECB on on its massive stimulus program. The dollar jumped and Treasury yields drifted lower.

Nasdaq futures led declines among the main American equity benchmarks, with Twitter plunging 6.6% in the premarket as hackers accessed its internal systems to hijack some of the platform’s top voices including U.S. presidential candidate Joe Biden, reality TV star Kim Kardashian West, former U.S. President Barack Obama and billionaire Elon Musk and used them to solicit digital currency. Tesla dropped 4.9% as its vehicle registrations nearly halved in the U.S. state of California during the second quarter, according to data from a marketing research firm.

Bank of America Corp shares edged lower after it reported a more than 50% decline in second-quarter profit, setting aside $4 billion for potential loan losses tied to the coronavirus pandemic. Morgan Stanley is due to report quarterly results later in the day, wrapping up what has been a mixed bag of quarterly earnings updates from the top six U.S. lenders. Johnson & Johnson was flat as it posted a 35.3% fall in quarterly profit as demand for its medical devices was hammered by hospitals putting off non-urgent procedures such as knee and hip replacement. Diversified manufacturer Honeywell and medical device maker Abbott Laboratories (ABT.N) are also slated to report their quarterly results on Thursday.

Stock markets in Asia and Europe also fell earlier in the day after data showed China’s retail sales fell 1.8% in June.

Asian stocks fell, led by communications and health care, after rising in the last session. Most markets in the region were down, with Shanghai Composite dropping 4.5% and Hong Kong’s Hang Seng Index falling 2%, while India’s S&P BSE Sensex Index gained 0.5%. Trading volume for MSCI Asia Pacific Index members was 20% above the monthly average for this time of the day. The Topix declined 0.7%, with Yoshimura Food Holdings and ITmedia falling the most. The Shanghai Composite Index retreated 4.5%, with China Life and Nacity Property Service posting the biggest slides.

The slump in tech shares and the reminder of the long road ahead to a full global recovery is quashing optimism seen earlier in the week spurred by progress in developing a coronavirus vaccine. While China is experiencing a modest domestic recovery, it remains vulnerable to setbacks as shutdowns continue to hamper activity across the globe.

“The problem is, this is still uneven,” Helen Qiao, chief greater China economist at Bank of America Corp., said on Bloomberg TV, referring to the latest data. “It is hard to see how China can remain on a firm footing at a time when the rest of the world is still coping with a very deep recession.”

In macro, the dollar rose against all Group-of-10 peers and the euro fell to a two-day low in European hours as risk sentiment worsened and given positioning ahead of the ECB. The central bank is widely expected to keep its QE program unchanged at 1.35 trillion euros, supplemented by negative interest rates and generous long-term loans to banks. The Swiss franc and the yen held up well, in line with familiar risk-off patterns; the Norwegian krone was the worst Group-of-10 performer as oil prices edged lower after closing at a four-month high; the OPEC+ alliance confirmed it would start tapering output cuts from next month. The Australian dollar fell as traders focused on the upward revision of job losses in May and a record spike in coronavirus cases in the nation’s second-most populous state.

In rates, 10Y Treasurues were modestly higher, with 10Y yields at 0.62% last. Gilts edged higher after Britain ramped up its bond sale plan by another 110 billion pounds, which was less than the 115 billion pounds estimated in a Bloomberg survey of primary dealers. Most regional bonds climbed ahead of the ECB’s policy decision, where it’s expected to keep its emergency bond-buying program unchanged. President Christine Lagarde will likely face questions over whether the current level of support is sufficient.

Looking at the day ahead now, the ECB meeting and President Lagarde’s subsequent press conference are likely to be the highlights. Other central bank speakers today include the Fed’s Williams, Bostic and Evans. Data releases include June’s retail sales, the weekly initial jobless claims, the Philadelphia Fed’s business outlook survey for July, and the NAHB housing market index for July. Earnings releases will include Johnson & Johnson, Netflix, Bank of America, Abbott Laboratories and Morgan Stanley.

Market Snapshot

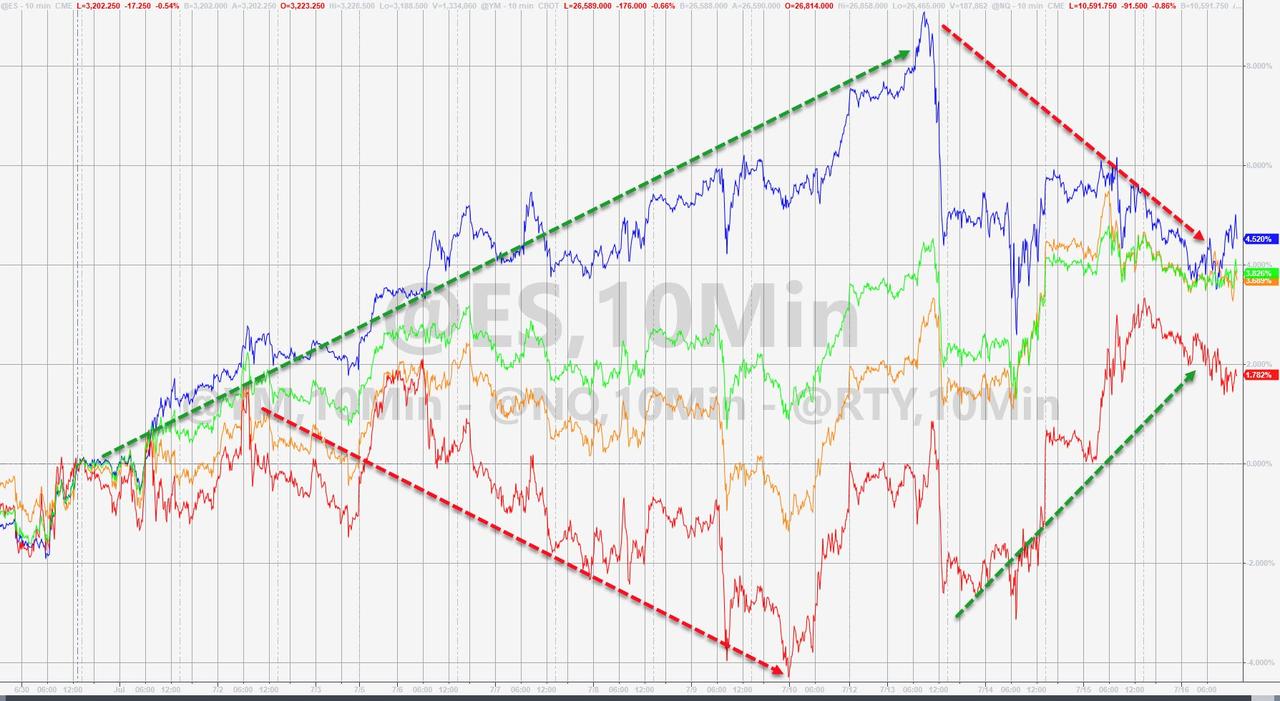

- S&P 500 futures down 0.8% to 3,194.50

- STOXX Europe 600 down 1% to 370.26

- German 10Y yield fell 0.6 bps to -0.45%

- Euro down 0.07% to $1.1404

- Italian 10Y yield fell 1.1 bps to 1.074%

- Spanish 10Y yield rose 0.4 bps to 0.426%

- MXAP down 1.5% to 164.16

- MXAPJ down 1.8% to 538.13

- Nikkei down 0.8% to 22,770.36

- Topix down 0.7% to 1,579.06

- Hang Seng Index down 2% to 24,970.69

- Shanghai Composite down 4.5% to 3,210.10

- Sensex up 0.5% to 36,212.32

- Australia S&P/ASX 200 down 0.7% to 6,010.86

- Kospi down 0.8% to 2,183.76

- Brent futures down 0.9% to $43.38/bbl

- Gold spot down 0.3% to $1,805.32

- U.S. Dollar Index up 0.1% to 96.18

Top Overnight News from Bloomberg

- Tokyo joined Australia’s second-biggest state in posting record coronavirus cases as second waves spread in several hotspots

- The Chinese economy expanded 3.2% in the second quarter from a year ago as the nation returned to growth, but the economy remains 1.6% smaller than a year ago and details showed the recovery was uneven, with a contraction in retail sales continuing in June

- As countries across Asia Pacific struggle with resurgences of the coronavirus, one data point is steering government responses: the share of cases with no clear indication of how infection occurred

- For all the pressure on U.K. Chancellor of the Exchequer Rishi Sunak to explain how he’ll repair public finances ravaged by the coronavirus, investors are lending the money with very few questions

- A relentlessly expanding physical hoard of bullion stored in London and New York means exchange-traded funds have usurped managed money in the futures market as the key driver of the price of the shiny metal

- The number of hours worked in the U.K. economy fell the most on the record in the coronavirus lockdown, underlining the risk facing the labor market as government income support is phased out

Asian stocks traded negatively as the recent vaccine optimism that underpinned global stocks took a back seat to the slew of tier-1 releases in the region including Australian Employment numbers, as well as Chinese GDP, Industrial Production and Retail Sales data. ASX 200 (-0.7%) was subdued with underperformance seen in commodity names and amid rumours of a potential Stage 4 lockdown surrounding Victoria state where its capital Melbourne is currently under stage 3 restrictions. Nikkei 225 (-0.8%) was pressured by recent detrimental currency flows and after falling short of the 23K status, while KOSPI (-0.6%) also declined after the BoK kept rates unchanged at 0.5% as expected and provided a grim tone on the economy. Elsewhere, Hang Seng (-2.0%) and Shanghai Comp. (-4.5%) failed to benefit from the mostly better than expected Chinese data in which GDP and Industrial Production topped estimates but Retail Sales disappointed and showed a surprise contraction which led to concerns related to consumer demand and an uneven recovery. Finally, 10yr JGBs were higher amid the negative mood across stocks and improved demand at the enhanced liquidity auction for 2yr-20yr JGBs.

Top Asian News

- Apple Supplier JDI Surges as CEO Reveals Mobile OLED Talks

- Worst China Stocks Selloff Since February Caps Brutal Reversal

- Hong Kong Sees Record 63 Local Virus Cases in Swelling Wave

- Thai Finance Minister Quits in Cabinet Shake-Up Amid Slump

European equities have started the session on the backfoot (Eurostoxx 50 -0.7%) as markets take a breather from some of the recent vaccine-inspired gains. Macro newsflow from a European perspective has been light as markets look ahead to the latest policy announcement from the ECB today and perhaps more importantly the upcoming negotiations on the EU recovery fund and budget. In terms of the composition of losses in Europe, all sectors trade lower with the exception of oil & gas names which trade closer to the unchanged mark post-yesterday’s JMMC agreement while telecom names are erring higher as well. The laggard in Europe is Food & Beverage with Heineken (-2.5%) a noteworthy underperformer after the Co. reported a 16% decline in H1 sales. Elsewhere, for the luxury sector, Richemont (-5.3%) sit near the foot of the Stoxx 600 after posting a near 50% decline in Q1 trading revenue in what was a particularly bleak earnings report. Other movers include Zalando (+2.1%) and Atos (-1.7%) post-earnings, whilst Deutsche Lufthansa (-3.0%) lag other travel & leisure names despite noting that it hopes to get around 90% of its short haul flights back up and running by the end of October.

Top European News

- Analysts Wary After Biggest Swedish Bank Has Tiny Impairment

- U.K. Bond-Sale Plan Is Now Equal to 18% of GDP to Fund Recovery

- Risky Debt Threatens U.K. Recovery, Finance Lobby Says

- Johnson Battles U.K. Spy Watchdog Ahead of Key Russia Report

In FX, the Dollar has clawed back more lost ground vs G10 and EM rivals on renewed safe haven demand as euphoria over COVID-19 vaccines fades somewhat and markets look ahead to key events, like the ECB, US retail sales data and weekly initial claims. However, the DXY still looks precarious just above 96.000 after Wednesday’s bearish break below the round number (to 95.770 and just off the June low), as coronavirus cases and deaths continue to rise in several states and reach fresh record peaks in some areas, such as Texas yesterday.

- GBP/NZD/AUD – The major victims of a reversal in broad risk sentiment and associated Greenback revival, but with Cable also undermined by negative technical factors having lost grip of the 1.2600 handle and a series of shorter term MA levels, including the 50, 100 and 200 markers, on the way down through 1.2550. Note, conflicting UK jobs data has not really impacted, but the Pound may be taking heed of NIRP expectations in Short Sterling futures that been brought forward by some 6 months in wake of BoE’s Tenreyro’s ‘live’ revelation yesterday. Meanwhile, benign NZ CPI and a mixed Aussie employment report have not helped the Nzd or Aud retain gains vs the Usd, with the former back under 0.6550 and the latter retreating through 0.7000.

- EUR/CAD/JPY/CHF – Also unwinding outperformance relative to the Buck, as the Euro relinquishes 1.1400+ status ahead of the ECB policy meeting and press conference amidst another heavy spread of option expiries descending from just shy of Wednesday’s high (circa 1.1452) at 1.1440-30 (1 bn) through 1.1380-75 (1 bn) down to 1.1350 (2 bn). Note, a full preview of the upcoming July ECB convene and presser is available on our Research Suite and will be reposted via the headline feed in the run up to the event. Similarly, the Loonie is paring back post-BoC between 1.3502-29 parameters against the backdrop of softer crude prices, while the Yen has pulled back from over 107.00, albeit some distance from 1.5 bn expiry interest at 107.25-35, and the Franc is straddling 0.9450.

- SCANDI/EM – General weakness, or payback after midweek session strength with few exceptions and the oil/commodity bloc bearing the brunt of the general deterioration in temperament. However, the Cnh is holding around 7.0000 following another firm PBoC Cny fix and a slew of Chinese data overnight that was either side of expectations, but comfortably above consensus in terms of Q2 GDP.

In commodities, WTI and Brent are once again subdued following the modest pullback in sentiment more broadly before today’s key central bank event. For the crude complex itself, since yesterday’s JMMC meeting where they confirmed OPEC+ will begin easing production cuts to 7.7mln BPD (~8.3mln BPD when taking compensation into account) there has been very little in the way of fundamental updates. As attention now returns more so to the demand side of the equation and the impact of any further COVID-19 induced headwinds; for the supply side, attention will be on whether OPEC+ members who are required to over-compensate do so as well as the situation in areas including Libya. Elsewhere, spot gold has had a somewhat more rangebound session but has most recently erred lower as European equity bourses attempt to rise from their session lows. Saudi Energy Minister said the effective oil cuts in August will be around 8.1-8.2mln BPD and reportedly commented that it is too late to change August quotas at this JMMC since term lifters’ nominations are already set for the month. (Newswires)

US Event Calendar

- 8:30am: Initial Jobless Claims, est. 1.25m, prior 1.31m; Continuing Claims, est. 17.5m, prior 18.1m

- 8:30am: Retail Sales Advance MoM, est. 5.0%, prior 17.7%; Retail Sales Ex Auto and Gas, est. 5.0%, prior 12.4%

- Retail Sales Ex Auto MoM, est. 5.0%, prior 12.4%; Retail Sales Control Group, est. 4.0%, prior 11.0%

- 8:30am: Philadelphia Fed Business Outlook, est. 20, prior 27.5

- 9:45am: Bloomberg Consumer Comfort, prior 42.9

- 10am: Business Inventories, est. -2.3%, prior -1.3%

- 10am: NAHB Housing Market Index, est. 61, prior 58

- 4pm: Net Long-term TIC Flows, prior $128.4b deficit; Total Net TIC Flows, prior $125.3b

DB’s Jim Reid concludes the overnight wrap

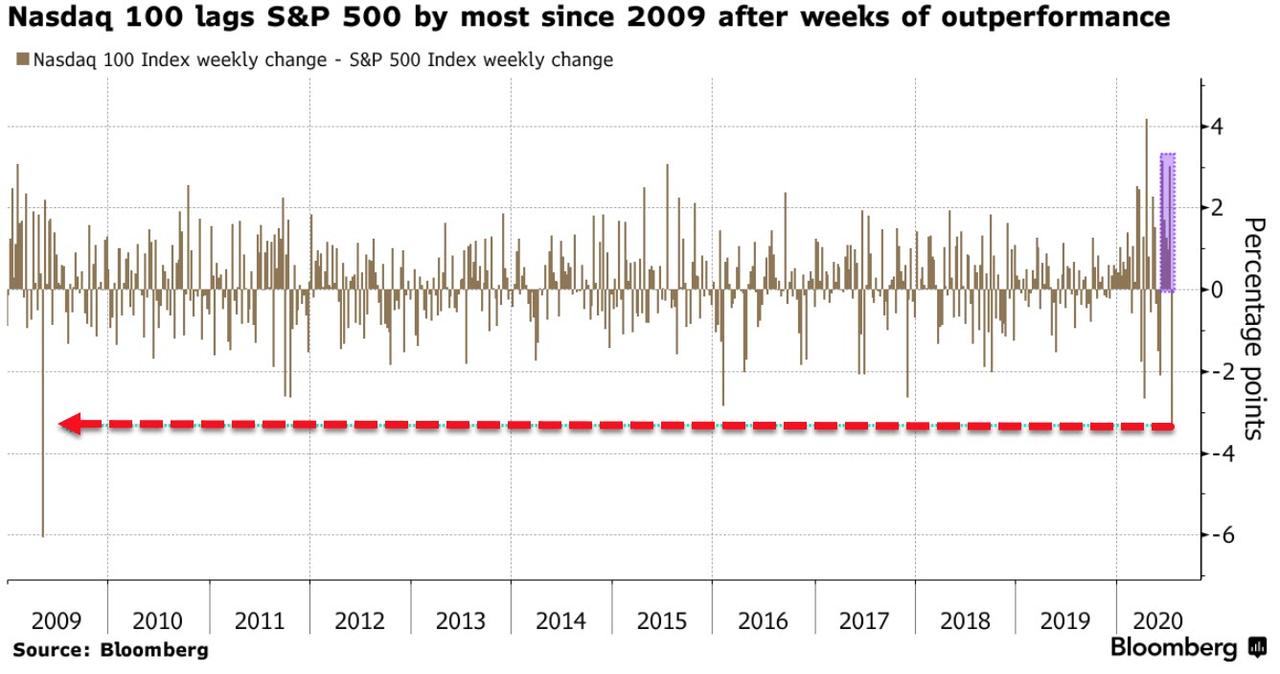

Risk assets were positive but volatile yesterday. It looked like a decent session was going to fizzle out as stocks dipped from their peaks 45 minutes before the European close as US/China tensions hit the headlines again and tech stocks came under some pressure after a dizzying run. However by the end of the session the S&P 500 reversed its downward course to finish just shy of its post-pandemic high. The reversal seemed driven by headlines that President Trump has told aides that he does not want to escalate tensions with China and also that Senate Majority Leader McConnell reiterated his plans to release a fiscal stimulus bill early next week. By the close the S&P 500 had advanced a further +0.91%, but was up as much as +1.27% at the day’s high and had briefly erased its YTD losses. The Nasdaq was up a lesser +0.59%, having been up over 1% earlier in the session but in negative territory after Europe closed. The best performing stocks were some of the most affected by the pandemic and the shutdowns. In the US, Airlines were among the leading industries, up over +10%, while Norwegian Cruise Line (+20.68%), Carnival (+16.22%), and Royal Caribbean Cruises (+21.20%) were among the best performing stocks in the S&P.

It was a similar story in Europe, where the Travel and Leisure sector (+6.06%) led the STOXX 600 higher, however the sector is still over -33% down from pre-pandemic highs compared to the broad index which is down -13.83%. The rise of cruise lines, airlines and other hospitality stocks in both the US and Europe was likely tied in parts to the positive vaccine stories over the last 36 hours. Europe managed to survive the aforementioned dip in risk sentiment with most of the bourses up by around 2%, including the STOXX 600 (+1.76%), the DAX (+1.84%) and the CAC 40 (+2.03%).

In terms of earnings, Goldman Sachs rose +1.4% yesterday as they announced, like their American peers, a large jump in fixed incoming trading. FICC sales and trading revenue of $4.24 billion beat an estimate of $2.64 billion. Also in-line with peers was the large Q2 provision for credit losses, up $1.59 billion from the prior year. Alcoa slightly beat after the close, but most importantly on the earnings call CEO Harvey said, “if the number of virus cases increases substantially in a prolonged first or potential second wave, a new round of strict lockdown orders would likely cause the current demand recovery to reverse course.”

Asian markets are trading lower this morning with the Nikkei (-0.71%), Hang Seng (-1.17%), Shanghai Comp (-1.41%), Kospi (-0.52%) and Asx (-0.97%) all down. A miss on retail sales data seems to be weighing on Chinese bourses even as Q2 GDP surprised on the upside (more below). The jump in COVID-19 infections in the region seems to also be acting as an overhang. Futures on the S&P 500 are also trading down -0.40%.

In more detail on the data, China’s Q2 GDP surprised on the upside with a reading of +3.2% yoy (vs. +2.4% yoy expected). Only 2 out of 28 economists on Bloomberg had pencilled in an above +3% print. Bloomberg highlighted that public investment swung to growth of +2.1% yoy in 1H, after contracting in the first 5 months. China’s 1H GDP growth now stands at -1.6% yoy (vs. -2.4% yoy expected). Alongside GDP we saw the other main data releases for June with industrial production rising in line with expectations at +4.8% yoy while YtD fixed asset investment came in at -3.1% yoy (vs. -3.3% yoy expected). Retail sales disappointed with a print of -1.8% yoy (vs. +0.5% yoy expected). The surveyed jobless rate for the month fell to 5.7% (vs. 5.9% last month). Elsewhere, Chinese President Xi Jinping wrote in a brief letter to a group of global chief executives that “We will continue efforts to deepen reform and opening, and provide a more sound business environment for Chinese and overseas investors.”

On the coronavirus, markets were initially reacting to the previous night’s news from the Moderna’s trial, in which their vaccine produced antibodies in all the patients tested. In response the company’s share price was up by +6.90% yesterday. The other news came through from UK ITV’s Robert Peston, who tweeted that “Positive news is coming on Oxford Covid-19 vaccine. The vaccine is generating the kind of antibody and T-cell (killer cell) response that the researchers would hope to see, I understand.” AstraZeneca shares surged following that tweet, ending the day up +5.23%, and Peston’s report on the ITV website said that the news could come as soon as today. Sky News also reported that the Lancet medical journal will publish data on the potential AstraZeneca Plc vaccine on Monday, so one to look out for.

There are some signs that the virus’ continued spread throughout the US may be slightly slowing in states that showed sharp increases in mid-June. Florida reported a 3.5% increase in cases yesterday, below the 4.5% weekly average. Still deaths continue to rise in the state, a further 112 reported yesterday compared to the average of 90 per day over the last week. Meanwhile Arizona saw a 2.5% increase that is also lower than its weekly average of 2.9%, however positive tests in the state remain very high at 23.4%, indicating that the official count may be missing a large number of cases. Deaths in the state rose by 97, the 5th increase in the last 6 days, and well above the 7 day average of 68. We would expect case growth to slow down this week as activity has dropped in these regions. Overall cases in the US rose by 2.0%, in-line with the last week’s average. According to rtlive’s model, only 6 states currently have an Rt under 1.0 and so there is very real concern of cases rising throughout the country even as the majority of the northeast sees limited case growth.

In Asia, after Tokyo raised their alert level to the highest point on a 4-point scale yesterday, they reported a record 280 confirmed cases today. The 7-day average of new cases in the city is now above its April peak. Tokyo‘s governor has urged residents to avoid stores that don’t meet guidelines designed to reduce the spread, but hasn’t called on businesses to close their doors yet. Australia’s second most populous state, Victoria recorded 317 new cases in the past 24 hours, the largest single-day increase for any of Australia’s states and territories.

On another note, the use of masks continued to become more widespread, with Walmart announcing that it would require all customers to wear them in its US stores from July 20. This comes as more US states have adopted mask mandates in recent days, the most recent of which was Alabama yesterday. The state borders recent hotspot Florida and has seen daily new cases rise by over 1,500 for 4 days in a row for the first time. In Europe, both Ireland and Serbia announced that the use of masks would become mandatory. The former also announced that they will delay the latest phase of reopening, which included bars and nightclubs, after the effective transmission rate rose over 1.0 in the country.

Attention today will turn to the ECB’s latest monetary policy decision, along with President Lagarde’s subsequent press conference. Our European economists write in their preview (link here ) that they expect the policy statement to remain unchanged, following the decision at the last meeting to expand the envelope for their Pandemic Emergency Purchase Programme by a further €600bn, bringing the total up to €1.35tn. Though recent comments from ECB officials have shown signs of an emerging optimism, our economists don’t believe these signal a change in the policy stance, and expect the commitment to “substantial monetary policy stimulus” to be repeated. Other issues to look out for include any comments from President Lagarde on the German Constitutional Court, now that the German Bundestag has passed a motion on proportionality.

Staying on Europe, our economists have written a fresh blog post on the proposed EU recovery fund ahead of the special European Council summit that commences tomorrow in Brussels (link here ). Their view is that although an agreement is still possible this weekend, it would now be a positive surprise, with the political messaging having shifted away from expecting a (full) agreement on Friday and Saturday. This could simply be expectations management, but so far there is no indication of the differences of opinion between member states having been bridged yet. That said, if agreement is not reached this weekend, then they still expect an agreement within weeks. The question of how the market will respond to the lack of an agreement will ultimately depend on the post-summit statements on how close or far the EU is from an agreement.

Ahead of that and the ECB later today, the euro actually strengthened to a 4-month high against the US dollar yesterday, at $1.1412. Indeed, if it surpasses the $1.145 it reached at the height of the market’s pandemic fears in early March, that’ll take the euro to its strongest level against the dollar in over a year. Meanwhile in fixed income, yields on 10yr Italian debt fell by -1.1bps to close at their lowest level in over 3 months, but bunds held steady, with just a +0.3bps rise. Over in the US, yields on 10yr Treasuries similarly rose by just +0.7bps.

Looking at yesterday’s data, the main news came from the US, where industrial production rose by a stronger-than-expected +5.4% in June (vs. +4.3% expected), though this still left IP -10.9% below its level in February before the pandemic hit. Further positive news came from the New York Fed’s Empire State manufacturing survey, with the headline general business conditions index rising to 17.2 (vs. 10.0 expected), the first positive reading since February. Finally here in the UK, the June CPI reading rose by a tenth to +0.6% (vs. +0.4% expected),which is the first time that the inflation rate has risen since January.

To the day ahead now, and as mentioned the ECB meeting and President Lagarde’s subsequent press conference are likely to be the highlights. Other central bank speakers today include BoE Governor Bailey, along with the Fed’s Williams, Bostic and Evans. Data releases include May’s UK unemployment and the Euro Area trade balance, while over in the US, we’ll get June’s retail sales, the weekly initial jobless claims, the Philadelphia Fed’s business outlook survey for July, and the NAHB housing market index for July. Earnings releases will include Johnson & Johnson, Netflix, Bank of America, Abbott Laboratories and Morgan Stanley.

3A/ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 151.21 POINTS OR 4.50% //Hang Sang CLOSED DOWN 510.89 POINTS OR 2.00% /The Nikkei closed DOWN 175.13 POINTS OR 0.76%//Australia’s all ordinaires CLOSED DOWN .61%

/Chinese yuan (ONSHORE) closed DOWN at 6.9936 /Oil UP TO 40.21 dollars per barrel for WTI and 43.55 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9936 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9920 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

CHINA

Collapse in confidence is surging a surge in Chinese bank runs

(zerohedge)

China Rocked By “Unprecedented” Surge In Bank Runs

At first, it was an unthinkable taboo – after all with a banking system that’s twice as large as that of the US, the last thing Beijing wanted (or could afford) was doubts that the people’s trillions in savings were safe as the alternative was not just a collapse of the financial sector but a breach of China’s capital controls firewall as tens of millions scrambled to move their savings abroad, in the process obliterating the yuan. Then, starting in early 2019 after several banks quietly failed or were not so quietly nationalized…

… most notably the inner-Mongolia-based Baoshang Bank which was seized in the first state takeover since 1998, domestic confidence in China’s banking system was suddenly – and perhaps irreparably – shaken, leading to scattered scenes such as these as depositor runs hammered several Chinese banks , forcing Beijing to unleash unprecedented damage control (and internet censorship) to keep the illusion that all is well.

Fast forward to today, when a confluence of the adverse trends that emerged in 2018 and 2019, coupled with the historic economic slowdown in China’s economy, and accelerated by social media-fueled rumors about collapsing banks have sparked what Bloomberg called an “unprecedented” surge of bank runs, forcing regulators and even the police to step in to calm depositors.

According to Bloomberg, in just the past few weeks, worried savers have descended on three banks to withdraw funds amid rumors of cash shortages that were later dismissed as false.

Over the weekend customers rushed to a bank in the northern Hebei province to take out money, prompting local regulators to publicly vouch for the soundness of its lenders as the police halted the run.

Indeed, as Bloomberg adds, “after several bailouts and the first bank seizure in more than two decades last year, the coronavirus outbreak and its economic fallout have exacerbated an already shaky situation in the world’s largest banking system” leading to a sharp erosion of confidence in the $43 trillion banking system among the nation’s more than 1 billion account holders, threatening a cornerstone of China’s rise into an economic powerhouse.

“The perception Chinese savers had of banks being risk free is changing even though in nearly all recent cases their deposits have been protected,” said China International Capital Corp analyst Zhang Shuaishuai.

“Once a rumor like this spreads, it brings immediate liquidity risk to a bank.”

There is probably a reason for why these “rumors” have led to such a dramatic response: they merely bring to the surface whatever most already know, namely that behind its sterling facade, China’s banking system is rotten to the core, with lies upon lies about trillions in non-performing loans…