GOLD:$: 1961.30 UP $12.45 The quote is London spot price (cash market)

This is an all time high!!

Silver:$24.24// UP 7 CENTS London spot price ( cash market)

Options expiry on the big London LBMA/OTC is scheduled for July 31. at exactly 10 am est// 3pm London time

The bankers will do everything in their power to keep gold/silver from rising. They are hurt very badly as huge number of options are now in the money

stay tune…

Closing access prices: London spot

i)Gold : $1968.50 LONDON SPOT 4:30 pm

ii)SILVER: $24.22//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUGUST GOLD: 1953.90 CLOSE 1::30 PM SPREAD SPOT/FUTURE AUG (BACKWARD $7,40)

OCT GOLD: $1965.70 CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: $4.40 ($ NORMAL CONTANGO)

DEC. GOLD $1975.70 CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $14.40 ($2.40 ABOVE NORMAL CONTANGO) OR .03% ABOVE CONTANGO OR EXCESS CONTANGO)

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $24.38…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : 14 CENTS PER OZ (8 CENTS ABOVE CONTANGO)

SILVER DECEMBER CLOSE: $24.64 1:30 PM SPREAD SPOT/FUTURE DEC. : 40 CENTS PER OZ ( 28 CENTS ABOVE NORMAL CONTANGO)

DONATE

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today: 498/825

issued 15

EXCHANGE: COMEX

CONTRACT: JULY 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,944.700000000 USD

INTENT DATE: 07/28/2020 DELIVERY DATE: 07/30/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

159 C ED&F MAN CAP 48

363 H WELLS FARGO SEC 300

657 C MORGAN STANLEY 43

657 H MORGAN STANLEY 326

661 C JP MORGAN 15

661 H JP MORGAN 498

690 C ABN AMRO 389

800 C MAREX SPEC 1

905 C ADM 30

____________________________________________________________________________________________

TOTAL: 825 825

MONTH TO DATE: 9,606

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 825 NOTICE(S) FOR 82500 OZ (2.566 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 9606 NOTICES FOR 960600 OZ (29.878 TONNES)

SILVER

FOR JULY

459 NOTICE(S) FILED TODAY FOR 2,295,000 OZ/

total number of notices filed so far this month: 16,698 for 83.490 MILLION oz

BITCOIN MORNING QUOTE $11,222 UP 312

BITCOIN AFTERNOON QUOTE.: $10,991 DOWN 39

GLD AND SLV INVENTORIES:

WITH GOLD UP $12.45 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/// A DEPOSIT OF 8.47 TONNES OF GOLD ADDED TO THE GLD//

GLD: 1,243.12 TONNES OF GOLD//

WITH SILVER UP 7 CENTS TODAY: AND WITH NO SILVER AROUND:

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV:

A MASSIVE DEPOSIT 5.984 MILLION OZ//

RESTING SLV INVENTORY TONIGHT:

SLV: 572.283 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A FELL BY A STRONG SIZED 2568 CONTRACTS FROM 186,588 DOWN TO 184,020, AND FURTHER FROM OUR NEW RECORD OF 244,710, (FEB 25/2020. THE CONSIDERABLE SIZED LOSS IN OI OCCURRED WITH OUR $0.14 LOSS IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE LOSS IN COMEX OI IS PRIMARILY DUE TO HUGE BANKER SHORT COVERING PLUS A STRONG EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A STRONG INCREASE IN SILVER STANDING AT THE COMEX FOR JULY. WE HAD A TINY NET LOSS IN OUR TWO EXCHANGES OF 353 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: JULY: 0 AND SEP 2215′ DEC: 0 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 2215 CONTRACTS. WITH THE TRANSFER OF 2215 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2215 EFP CONTRACTS TRANSLATES INTO 11.075 MILLION OZ ACCOMPANYING:

1.THE 14 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

85.325 MILLION OZ INITIALLY IN JULY.

TUESDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL 14 CENTS ).. AND,OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS. THE SMALL GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A STRONG INCREASE IN STANDING OF SILVER OZ STANDING FOR JULY, HUGE BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A TINY NET LOSS OF 353 CONTRACTS OR 1.765 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

JULY

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF JULY:

25,070 CONTRACTS (FOR 20 TRADING DAY(S) TOTAL 25,070 CONTRACTS) OR 125.350 MILLION OZ: (AVERAGE PER DAY: 1254 CONTRACTS OR 6.2675 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 125.350 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 16.32% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,262.77 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 125.350 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2568, WITH A 14 CENT LOSS IN SILVER PRICING AT THE COMEX ///TUESDAY… THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2215 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE LOST A VERY TINY SIZED OI CONTRACTS ON THE TWO EXCHANGES: 353 CONTRACTS (WITH OUR $0.14 CENT LOSS IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 2215 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A CONSIDERABLE SIZED DECREASE OF 2568 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED DESPITE A $0.14 CENT LOSS IN PRICE OF SILVER/AND A CLOSING PRICE OF $24.17 // TUESDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.9305 BILLION OZ TO BE EXACT or 132% of annual global silver production (ex Russia & ex China).

FOR THE NEW JULY DELIVERY MONTH/ THEY FILED AT THE COMEX: 459 NOTICE(S) FOR 2,295,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 85.325 million oz

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A HUGE SIZED 12,093 CONTRACTS TO 598,629 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE HUGE SIZED LOSS OF COMEX OI OCCURRED DESPITE OUR STRONG RISE IN PRICE OF $13.25 /// COMEX GOLD TRADING// TUESDAY// WE HAD HUGE BANKER SHORT COVERING, ANOTHER HUGE SIZED INCREASE IN GOLD OZ STANDING AT THE COMEX FOR JULY, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A STRONG EXCHANGE FOR PHYSICAL ISSUANCE AND A HUGE GOLD SPREADER LIQUIDATION. THIS ALL HAPPENED WITH OUR STRONG GAIN IN PRICE OF $13.25 .

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 58

WE LOST A SMALL SIZED 4225 CONTRACTS (13.14 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 7868 CONTRACTS:

CONTRACT .; AUG 6443 AND OCT: 400 DEC: 1025; FEB: 0 ALL OTHER MONTHS ZERO//TOTAL: 7868. The NEW COMEX OI for the gold complex rests at 598,629. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4225 CONTRACTS: 12,093 CONTRACTS DECREASED AT THE COMEX AND 7868 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 4225 CONTRACTS OR 13.14 TONNES. TUESDAY, WE HAD A GAIN OF $13.25 IN GOLD TRADING……

AND WITH THAT LOSS IN PRICE, WE HAD A SMALL SIZED LOSS IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 13.14 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $13.25).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS ALSO UNSUCCESSFUL (SEE BELOW).

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (7868) ACCOMPANYING THE HUGE SIZED LOSS IN COMEX OI (12,093 OI): TOTAL LOSS IN THE TWO EXCHANGES: 4225 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)ANOTHER STRONG INCREASE IN GOLD STANDING AT THE GOLD COMEX FOR THE FRONT JULY MONTH, 3) ZERO LONG LIQUIDATION; 4) CONSIDERABLE COMEX OI LOSS AND .5) STRONG EXCHANGE FOR PHYSICAL ISSUANCE 6) CONTINUAL STRONG GOLD SPREADER LIQUIDATION... AND …ALL OF THIS WAS COUPLED WITH OUR STRONG GAIN IN GOLD PRICE TRADING//TUESDAY//$13.25.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

SPREADING OPERATIONS/NOW SWITCHING TO GOLD

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN GOLD AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF AUGUST FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF JULY. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUGUST), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

JULY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAY(S) IN TONNES: 296.62 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 296.20/3550 x 100% TONNES =8.34% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3247.65 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 296.20 TONNES SO FAR..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A CONSIDERABLE SIZED 2568 CONTRACTS FROM 186,588 DOWN TO 184,020 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE CONSIDERABLE SIZED LOSS IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) HUGE BANKER SHORT COVERING , 2) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A STRONG INCREASE STANDING AT THE SILVER COMEX FOR JULY AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 2215 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY: 0 CONTRACTS AND SEPT: 2692 AND DEC. 200 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2215 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2568 CONTRACTS TO THE 2215 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL LOSS OF 353 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 1,765 MILLION OZ, OCCURRED WITH OUR 14 CENT LOSS IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 66.59 POINTS OR 2.06% //Hang Sang CLOSED UP 110.38 POINTS OR 0.45% /The Nikkei closed DOWN 260.27 POINTS OR 1.15%//Australia’s all ordinaires CLOSED DOWN .31%

/Chinese yuan (ONSHORE) closed DOWN at 7.0001 /Oil UP TO 41.49 dollars per barrel for WTI and 43.70 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 7.0001 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.0049 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: 942,767.700 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

i)we had 2 deposits into the customer account

into JPMorgan: nil oz

ii) Into Brinks: 450,000.000 oz ????

iii) Into Scotia: 597,302.100 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 163.098 million oz of total silver inventory or 49.22% of all official comex silver. (163.677 million/332.531 million

total customer deposits today: 1,047,302.100 oz

we had 3 withdrawals:

i)Out of CNT: 604,971.85 oz

ii) Out of Delaware: 9783.003 oz

iii) Out of Scotia; 599,332.740 oz

total withdrawals; 1,214,087.393 oz

We had 1 adjustments

]out of CNT: dealer to customer account

1,193,479.226 oz dealer to customer

total dealer silver: 131.235 million

total dealer + customer silver: 332.531 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The front month of July has an open interest of 826 contracts, as we LOST 438 contracts. We had 469 notices served on TUESDAY, so we GAINED 31 contracts or an additional 155,000 oz will stand in this active delivery month of July as they REFUSED TO morph into a London based forwards. It seems that we have little silver over on this side of the pond. We still have a huge amount of contracts still outstanding to be served upon in July.

The next month after July is the non active month of August and here sees its open interest ROSE by 80 contracts RISING to 826

The big September contract month sees a LOSS of 4583 contracts down to 131,092.

The total number of notices filed today for the JULY 2020. contract month is represented by 459 contract(s) FOR 2,295,000, oz

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 16,698 x 5,000 oz = 83,490,000 oz to which we add the difference between the open interest for the front month of JULY.(826) and the number of notices served upon today 459 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the JULY/2019 contract month: 16,698 (notices served so far) x 5000 oz + OI for front month of JULY (826)- number of notices served upon today (459) x 5000 oz of silver standing for the JULY contract month.equals 85,325,000 oz. (A WHOPPER )//ALL TIME RECORD FOR ONE DELIVERY MONTH (corrected totals from yesterday)

WE GAINED 31 CONTRACTS OR 155,000 OZ WILL STAND FOR DELIVERY. SILVER IS STILL VERY SCARCE ON THIS SIDE OF THE POND AND THE REASON FOR CONSIDERABLE MORPHING OVER TO LONDON.

TODAY’S ESTIMATED SILVER VOLUME : 105,660 CONTRACTS // volume huge/

FOR YESTERDAY: 271,863.,CONFIRMED VOLUME//volume huge++++++++/

YESTERDAY’S CONFIRMED VOLUME OF 271,863 CONTRACTS EQUATES to 1,559 million OZ 194% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 1.45% ((JULY 29/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.83% to NAV: (JULY 29/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 1.45%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 19.91 TRADING 19.74///NEGATIVE 0.86

END

And now the Gold inventory at the GLD/

JULY 29//WITH GOLD UP $12.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 8.47 TONNES/INVENTORY RESTS AT 1243.12 TONNES OZ

JULY 28///WITH GOLD UP $13.25 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 5.84 TONNES/INVENTORY RESTS AT 1234.65

JULY 27//WITH GOLD UP $35.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF XXX TONNES/INVENTORY RESTS AT 1228.81 TONNES

JULY 24/WITH GOLD UP $8.80 TODAY: WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.80 TONNES//INVENTORY RESTS AT 1228.81 TONNES

JULY 23/WITH GOLD UP $24.90 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 7.26 TONNES/INVENTORY RESTS AT 1225.01 TONNES

JULY 22/WITH GOLD UP $22.00 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 7.89 TONNES/INVENTORY RESTS AT 1219.75 TONNES

JULY 21//WITH GOLD UP $26.00 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.97 TONNES INTO THE GLD// INVENTORY RESTS AT 1211.86 TONNES

JULY 20/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1206.89 TONNES

JULY 17/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1206.89 TONNES

JULY 16/WITH GOLD DOWN $9.80 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: INVENTORY RESTS AT 1206.89 TONNES

JULY 15//WITH GOLD UP $1.55 TODAY/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 2.96 TONNES INTO THE GLD///INVENTORY RESTS AT 1206.89 TONNES

JULY 14//WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 3.51 TONNES/INVENTORY RESTS AT 1203.97 TONNES

JULY 13//WITH GOLD UP $12.50 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1200.46 TONNES

JULY 10/WITH GOLD DOWN $.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD//A STRANGE WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1200.82 TONNES

JULY 9//WITH GOLD DOWN $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OX 3.21 TONNES INTO THE GLD//INVENTORY RESTS AT 1202.57 TONNES

JULY 8/WITH GOLD UP $13.75 TODAY; A BIG CHANGE IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 7.89 TONNES INTO THE GLD//INVENTORY RESTS AT 1199.36 TONNES

JULY 7/WITH GOLD UP $12.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1191.47 TONNES

JULY 6/WITH GOLD UP $6.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1191.47 TONNES

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

JUNE 30//WITH GOLD UP $16.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1178.90 TONNES

JUNE 29/WITH GOLD UP $2.90 TODAY: A HUGE DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1178.90 TONNES

JUNE 26/WITH GOLD UP $5.03 TODAY: VERY STRANGE: A PAPER WITHDRAWAL OF 1.46 TONNES//INVENTORY RESTS AT 1175.39 TONNES

JUNE 25//WITH GOLD DOWN $3.30 TODAY//ANOTHER STRONG PAPER DEPOSIT OF 7.6 TONNES///INVENTORY RESTS AT 1176.85 TONNES

JUNE 24/WITH GOLD DOWN $1.50 TODAY; A STRONG 3.21 TONNES ADDED TO THE GLD//INVENTORY RESTS AT 1169.25 TONNES

JUNE 23/WITH GOLD UP $25.50 TODAY/ANOTHER CRIMINAL PAPER DEPOSIT OF 6.73 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1166.04 TONNES

JUNE 22/WITH GOLD UP $14.00 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 23.09 TONNES//INVENTORY RESTS AT 1159.31 TONNES

JUNE 19/WITH GOLD UP$16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//; INVENTORY RESTS AT 1136.22 TONNES

JUNE 18//WITH GOLD DOWN $2.75 TODAY: NO CHANGES IN GOLD INVENTORY: INVENTORY RESTS AT 1136.22 TONNES

JUNE 17/WITH GOLD DOWN $1.05: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1136.22 TONNES

JUNE 16//WITH GOLD UP $6.70 TODAY: NO CHANGES IN GOLD INVENTORY: /INVENTORY RESTS AT 1136.22 TONNES

JUNE 15/WITH GOLD DOWN ANOTHER $8.80 TODAY, NO CHANGES IN GOLD INVENTORY/INVENTORY RESTS AT 1136.22 TONNES

JUNE 12//WITH GOLD DOWN $1.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 1.17 TONNES AT THE GLD//INVENTORY RESTS AT 1136.22 TONNES

JUNE 11//WITH GOLD UP $16.80 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 6.55 TONNES AT THE GLD//INVENTORY RESTS AT 1135.05 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

JULY 29/ GLD INVENTORY 1234.65 tonnes*

LAST; 869 TRADING DAYS: +301.30 NET TONNES HAVE BEEN ADDED THE GLD

LAST 769 TRADING DAYS://+479.77 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JULY 29/WITH SILVER UP 7 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY//A DEPOSIT OF 5.984 MILLION OZ//INVENTORY RESTS AT 572.283 MILLION OZ//

JULY 28 WITH SILVER DOWN 14 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 7.52 MILLION OZ//INVENTORY RESTS AT 566.299 MILLION OZ//

JULY 27/WITH SILVER UP $2.67 TODAY, WE HAD NO CHANGES IN SILVER INVENTORY: A DEPOSIT OF XX MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ//

JULY 24/WITH SILVER DOWN $0.12 TODAY: NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 558.779 MILLION OZ/

JULY 23/WITH SILVER UP $.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A HUMONGOUS PAPER DEPOSIT OF 9.594 MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ///

JULY 22/WITH SILVER UP $1.54 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A HUMONGOUS PAPER DEPOSIT OF 7.218 MILLION OZ//INVENTORY RESTS AT 549.185 MILLION OZ/

JULY 21/WITH SILVER UP $1.38 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUMONGOUS PAPER DEPOSIT OF 15.368 MILLION OZ////INVENTORY RESTS AT 541.967 MILLION OZ//

JULY 20/WITH SILVER UP 40 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 3.819 MILLION OZ ‘ENTERED” THE SLV..INVENTORY RESTS AT 526.599 MILLION OZ/

JULY 17/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 1.583 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 522.780 MILLION OZ//

JULY 16//WITH SILVER DOWN 14 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ//INVENTORY RESTS AT 521.197 MILLION OZ..

JULY 15.WITH SILVER UP 21 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.956 MILLION OZ//INVENTORY RESTS AT 516.074 MILLION OZ//

JULY 14/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 514.118 MILLION OZ//

JULY 13//WITH SILVER UP 67 CENTS TODAY: A HUGE CHANGE IN SILVER: A WITHDRAWAL OF 1.677 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 514.118 MILLION OZ//

JULY 10/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 4.844 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.795 MILLION OZ

WHAT A FRAUD!!

JULY 9/WITH SILVER DOWN 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 8.198 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 510.951 MILLION OZ/

JULY 8/WITH SILVER UP 37 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.118 MILLION OZ FROM THE SLV//VERY SURPRISING.//INVENTORY RESTS AT 502.753 MILLION OZ//

JULY 7/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/INVENTORY RESTS AT 503.871 MILLION OZ///

JULY 6//WITH SILVER UP 24 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.863 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 503.871 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

JUNE 30/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 29/WITH SILVER DOWN ONE CENT TODAY: A TWO CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 466,000 OZ TO PAY FOR STORAGE FEES AND INSURANCE//// AND A LARGE DEPOSIT OF 1.212 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 26/WITH SILVER UP 6 CENTS TODAY: ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ RESTS AT 491.858 MILLION OZ//

JUNE 25/WITH SILVER UP 12 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 931,000 OZ INTO THE SLV////INVENTORY RESTS AT 491.858 MILLION OZ//

JUNE 24///WITH SILVER DOWN 31 CENTS// NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 490.927 MILLION OZ

JUNE 23//WITH SILVER UP 16 CENTS TODAY: A MONSTROUS CHANGE IN INVENTORY: A PAPER DEPOSIT OF 4.473 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 490.927 MILLION OZ//

JUNE 22/WITH SILVER UP 15 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/: INVENTORY/INVENTORY RESTS AT 486/454 MILLION OZ//

JUNE 19//WITH SILVER UP 22 CENTS TODAY: STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 839,000 OZ FROM THE SLV////INVENTORY RESTS AT 486,454 MILLION OZ..

JUNE 18/WITH SILVER DOWN 16 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 932,000 OZ INTO THE SLV////INVENTORY RESTS AT 487.293 MILLION OZ

JUNE 17/WITH SILVER UP 8 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.261 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.361 MILLION OZ

JUNE 16//WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.118 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 483.100 MILLION OZ//

JUNE 15/WITH SILVER DOWN 14 CENTS NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 481.982 MILLION OZ///

JUNE 12/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: TWO DEPOSITS OF 7.269 MILLION OZ AND 1.802 MILLION OZ ADDED TO THE SLV///INVENTORY RESTS THIS WEEKEND AT 481.982 MILLION OZ//

JUNE 11//WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY: ///INVENTORY RESTS AT 472.89 MILLION OZ//

JULY 29.2020:

SLV INVENTORY RESTS TONIGHT AT

566.299 MILLION OZ.

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

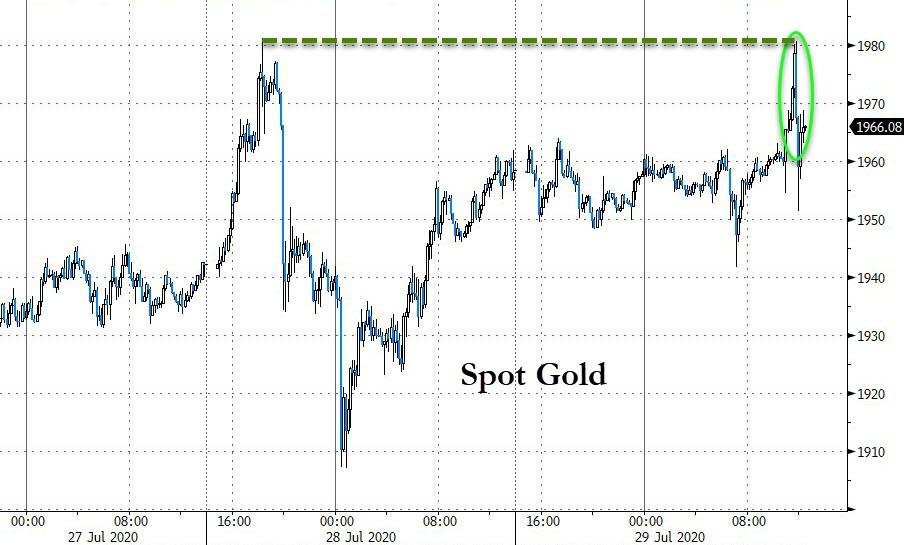

Gold Reaches $2,000/oz Prior to Two “Concerted Attacks” In Futures Market

The King Report

“Anyone that’s been around the block a few times with gold knows that at some point ‘they’ will stage a concerted effort to drive gold lower.”

December gold hit $2,000 at 21:19 ET Monday. It then retreated and traded sideways until 22:50 ET. Then someone slammed gold down to $1,955 in 20 minutes. This is obvious “impact trading.” Gold then traded sideways for over four hours. (see red line above).

At 3:27 ET another attack on gold commenced. December gold finally bottomed at $1,927.50 at 3:51 ET.

Gold rebounded sharply after Goldman hiked its target price to $2,300.

The duo concerted attacks on gold suggest that someone with stature has transitioned from being alarmed about gold to being afraid of gold. …

Today the July gold contract expires, so gold could be volatile. Physical gold is in short supply, so entities that are short July gold better have the stuff. Perhaps this is why gold was attacked on Tuesday. …

[Warren] Buffett and many others have proclaimed that owning “good” common stocks is a far better inflation hedge than gold.

This is mostly true as long as the business is domiciled in a country that has a solid belief in the rule of law and justice as practiced by constitutional oversight.

However, gold is a far better and safer option in a banana republic or totalitarian regime. Common stocks owners, especially private equity, should be very, very alarmed at where the United States is heading.

NEWS and COMMENTARY

Gold’s Record Rally Fuelled by Unlikely Buyers – Bloomberg

Gold pauses as markets seek confirmation on Fed policy – Reuters

Currencies ease on virus worries ahead of Fed – Reuters

Chinese banks urged to switch away from SWIFT as U.S. sanctions loom – Reuters

It Is Time to Abandon Dollar Hegemony – Foreign Affairs

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

28-Jul-20 1931.65 1940.90, 1499.15 1501.48 & 1647.70 1654.23

27-Jul-20 1940.55 1936.65, 1511.30 1504.78 & 1659.56 1647.70

24-Jul-20 1893.85 1902.10, 1486.67 1490.30 & 1631.55 1638.09

23-Jul-20 1882.35 1878.30, 1480.28 1477.47 & 1624.47 1621.54

22-Jul-20 1851.00 1852.40, 1462.85 1456.91 & 1604.82 1598.44

21-Jul-20 1823.20 1842.55, 1436.86 1449.35 & 1594.21 1608.36

20-Jul-20 1810.30 1815.65, 1437.92 1438.18 & 1580.21 1590.87

17-Jul-20 1802.90 1807.35, 1435.47 1442.45 & 1578.98 1581.07

16-Jul-20 1804.60 1807.70, 1438.09 1436.04 & 1583.72 1581.56

15-Jul-20 1809.30 1804.60, 1436.22 1441.31 & 1582.96 1579.57

14-Jul-20 1798.20 1801.90, 1436.58 1440.62 & 1583.14 1581.71

13-Jul-20 1808.05 1807.50, 1435.23 1432.26 & 1598.32 1591.68

10-Jul-20 1805.75 1803.10, 1433.40 1427.33 & 1599.35 1594.84

Own gold coins and bars in the safest vaults in Zurich, Switzerland with GoldCore. Learn why Switzerland remains a safe haven jurisdiction for owning precious metals. Access Our Most Popular Guide, the Essential Guide to Storing Gold in Switzerland here

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here

ii) Important gold commentaries courtesy of GATA/Chris Powell

A must read Financial Times article on gold as they sulk at gold’s rise to almost 2,000 dollars

(London’s Financial Times/GATA)

Gold’s sharp rise throws Financial Times into an erroneous sulk

Submitted by cpowell on Wed, 2020-07-29 02:01. Section: Daily Dispatches

10:14p ET Tuesday, July 29, 2020

Dear Friend of GATA and Gold:

Appended is tomorrow’s editorial in the Financial Times, which, taking note of gold’s sharp rise in price, begins with a factual error, goes on to sulk for six paragraphs, and concludes with the hope and expectation that gold will go back in the dumpster eventually.

The error beginning the editorial is the assertion that gold doesn’t pay interest. Gold doesn’t automatically pay interest like a bond because it doesn’t have to, since holding gold incurs no risk. An ounce of gold today will be an ounce of gold tomorrow, whatever happens in the world, even as many borrowers have failed and even currencies have failed as the regimes issuing them have collapsed.

Gold is money in itself and no one else’s liability. But gold can pay interest if its owner wants to lend it, just as fiat currency cash can pay interest and just as central banks themselves have charged interest in lending their gold to investment banks for hypothecation and price suppression.

The FT attributes gold’s rise to “uncertain times” — geopolitical tensions and the failure of the U.S. government to get the virus epidemic under control. The FT offers not a word about what is likely a bigger cause — the implosion of the fractional-reserve gold banking system built in part on the central bank gold leasing the FT also fails to acknowledge.

If the FT thinks the gold price is unpleasantly high now, what will the price be if the world ever realizes that most of the gold it thought it owned doesn’t exist and never did? If the world ever finds out, it may fairly ask why the FT never reported it, though documentation of central bank gold price suppression policy has been delivered to the newspaper many times over the last 20 years without prompting the newspaper to put a single critical question to any central bank.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

Gold’s Rise Is a Sign of Uncertain Times

From the Financial Times, London

Tuesday, July 28, 2020

https://www.ft.com/content/51db2a1f-6e94-4c5f-9ce0-507ebf41835c

Gold is not a particularly good investment. It yields no interest and pays no dividend. The only way its owners can earn a return is if other investors value the shiny metal more tomorrow than they did today. For a “haven” asset, which investors can use to preserve capital in times of crisis, it is remarkably speculative; aside from some niche industrial uses, most of the permanent demand comes from jewellery. Its rise in value this week to a near-record high of $2,000 per troy ounce reflects that many other options are even less attractive, rather than any intrinsic merits.

Many traditional “safe assets,” such as government bonds, similarly either yield nothing or will gradually lose their value thanks to inflation and negative interest rates. As with gold, earning a return on U.S. Treasuries relies on speculating that prices of the bonds can continue to increase. With interest rates already at virtually zero in the United States and little indication that the Fed intends to drop them into negative territory, that does not strike many as a good bet. In that situation, some investors see gold, which is less vulnerable to inflation, as more attractive.

The current rise in gold is also an indication of fear. What gold primarily offers investors is an alternative to the dollar. Adjusting for changes in overall prices, the metal has been more expensive only twice before: during 2011, when a congressional standoff over the U.S. debt ceiling and the potential for the eurozone to break up drove demand; and in the early 1980s, when a new Islamic revolutionary regime in Iran contributed to concerns that the partly oil-driven inflation of the 1970s would erode the value of the greenback. Gold’s rise today once again reflects worries over the safety of investing in the world’s largest economy.

The dollar has likewise lost value this week against the euro, the British pound, and the Japanese yen. Not only are geopolitical tensions with China rising — gold’s value also rose this year during a standoff between the US and Iran — but the U.S. government continues to mishandle the pandemic. A congressional stalemate over a second stimulus package has also prompted investors to look for alternatives to the international reserve currency.

The dollar’s premier status owes as much to the fact there are few good alternatives to the currency as to the greenback’s own advantages. The euro, the only currency with similar standing, lacks the liquidity and depth of the greenback — though the launch of mutual bonds to pay for the bloc’s post-coronavirus recovery fund may help to change that. For some, gold is also a means to bet against fiat currencies and unrestrained money printing in general.

This is the backdrop against which the Federal Reserve, currently in an interest-rate meeting that will end on Wednesday, will announce its latest decision. The members of its rate-setting committee should ignore the decline in the dollar, which, if anything, provides relief to U.S. exporters and a bit of extra monetary stimulus. There is little, however, they can do to help the American economy at the moment. Market trading is orderly and, until the virus is contained, even cheaper money — whether through negative interest rates or yield-curve control — will do little to boost growth.

Gold’s rise may be overdone. History suggests that it rarely maintains these sorts of levels, and the wave of fear over the future of the U.S. and world economy that propels it eventually breaks. For the moment those fears are grounded, but gold’s disadvantages may soon become clear again.

* * *

END

A good article on the dollar, its pros and cons

(Foreign Affairs/New York GATA/Tolford/Kundnani)

Foreign Affairs: It is time to abandon dollar hegemony

Submitted by cpowell on Wed, 2020-07-29 02:35. Section: Daily Dispatches

Issuing the World’s Reserve Currency Comes at Too High a Price

By Simon Tilford and Hans Kundnani

Foreign Affairs, New York

Tuesday, July 28, 2020

In the 1960s, French Finance Minister Valéry Giscard d’Estaing complained that the dominance of the U.S. dollar gave the United States an “exorbitant privilege” to borrow cheaply from the rest of the world and live beyond its means.

U.S. allies and adversaries alike have often echoed the gripe since. But the exorbitant privilege also entails exorbitant burdens that weigh on U.S. trade competitiveness and employment and that are likely to grow heavier and more destabilizing as the United States’ share of the global economy shrinks.

The benefits of dollar primacy accrue mainly to financial institutions and big businesses, but the costs are generally borne by workers. For this reason, continued dollar hegemony threatens to deepen inequality as well as political polarization in the United States.

Dollar hegemony isn’t foreordained. For years, analysts have warned that China and other powers might decide to abandon the dollar and diversify their currency reserves for economic or strategic reasons. To date, there is little reason to think that global demand for dollars is drying up.

But there is another way the United States could lose its status as issuer of the world’s dominant reserve currency: It could voluntarily abandon dollar hegemony because the domestic economic and political costs have grown too high. …

… For the remainder of the essay:

https://www.foreignaffairs.com/articles/americas/2020-07-28/it-time-aban…

end

The big question: where do people store all the new gold that they bought

New York Times/GATA

Where is all that gold being stored?

Submitted by cpowell on Wed, 2020-07-29 02:40. Section: Daily Dispatches

By Danielle Braff

The New York Times

Tuesday, July 28, 2020

We’re in the midst of a modern-day gold rush.

The precious metal has reached record high prices in recent days. A survey of 1,000 people by Magnify Money found that one out of six have invested in gold or other precious metals since May, and about half of Americans are seriously thinking about buying gold. (This after Gallup reported in April that Americans had cooled somewhat on stocks as a long-term investment.)

Whether these people are stocking up on gold because they’re worried about a pending apocalypse or simply convinced that it’s a fabulous investment, they do have one major issue: storage. Bars and coins are bulky. (And let’s not get started on jewelry, which can be complicated emotionally.)

With anxiety about the economy increasing — which tends to rise any time there’s political or world turmoil — the need for storage is growing, too, and options are expanding to meet it.

“Gold and silver bullion storage options have simply grown more in location diversity, pricing — with even some offering short-term collateral loan options,” said James Anderson, a research executive at SD Bullion in Toledo, Ohio. “When I began in this industry pre-2008 financial crisis, there were perhaps 10 to 20 domestic bullion storage depositories. Now, there are hundreds in the U.S.A. and abroad.”

… For the remainder of the report:

https://www.nytimes.com/2020/07/28/style/gold-storage.html

end

The Thai central bank has a somewhat link to gold/baht. This has caused the baht to rise because citizens there believe that their baht is backed by gold. Now the government want to severe that link and lower the baht balue

Bloomberg./GATA

Thai central bank would push local gold trade out of baht and into dollars

Submitted by cpowell on Wed, 2020-07-29 03:06. Section: Daily Dispatches

Thailand’s Gold Plan May Curb Baht Without Incurring U.S. Anger

By Lilian Karunungan and Suttinee Yuvejwattana

Bloomberg News

Tuesday, July 28, 2020

The Bank of Thailand’s plan to sever the link between gold trading and the baht may be a way to limit the currency’s gains without incurring the wrath of the U.S. over foreign-exchange manipulation.

The Thai central bank says it’s in talks with market participants about converting local gold trading to U.S. dollars, including futures, to reduce the baht’s strength. Policy makers have long complained the appreciating currency threatens to damage the country’s exports.

The baht fell at the start of the Covid-19 outbreak but has since gathered strength amid the gold fervor. The surge in the precious metal has convinced many Thais to cut their holdings, forcing local shops to sell in the international market. The step of exchanging dollars into baht as part of the process has been one of the factors helping the Thai currency gain about 5% from its March low. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2020-07-28/thailand-s-gold-plan-…

end

Tuesday: when gold touched 2,000 dollars on the futures, it triggered two attacks.

King Report

King Report: Gold’s touch of $2,000 triggers two attacks

Submitted by cpowell on Wed, 2020-07-29 05:06. Section: Daily Dispatches

By Bill King

The King Report

Burr Ridge, Illinois

Wednesday, July 29, 2020

http://thekingreport.com/

From Tuesday’s King Report: “Anyone that’s been around the block a few times with gold knows that at some point ‘they’ will stage a concerted effort to drive gold lower. …”

December gold hit $2,000 at 21:19 ET Monday. It then retreated and traded sideways until 22:50 ET. Then someone slammed gold down to %1,955 in 20 minutes. This is obvious “impact trading.” Gold then traded sideways for over four hours.

At 3:27 ET another attack on gold commenced. December gold finally bottomed at $1,927.50 at 3:51 ET. Gold rebounded sharply after Goldman hiked its target price to $2,300.

…The duo concerted attacks on gold suggest that someone with stature has transitioned from being alarmed about gold to being afraid of gold. …

Today the July gold contract expires, so gold could be volatile. Physical gold is in short supply, so entities that are short July gold better have the stuff. Perhaps this is why gold was attacked on Tuesday. …

[Warren] Buffett and many others have proclaimed that owning “good” common stocks is a far better inflation hedge than gold. This is mostly true as long as the business is domiciled in a country that has a solid belief in the rule of law and justice as practiced by constitutional oversight. However, gold is a far better and safer option in a banana republic or totalitarian regime. Common stocks owners, especially private equity, should be very, very alarmed at where the United States is heading.

end

iii) Other physical stories:

Peter Schiff on gold:

Peter Schiff: The Fed Doesn’t Have Another Rabbit In Its Hat

Gold has rallied above its previous all-time record high this week. But can it sustain this bull run? Peter Schiff thinks it can and will.

It’s not about the coronavirus, as many mainstream analysts seem to think. It’s the government and central bank response to the pandemic — the borrowing, the spending, and the money printing. Peter believes that ultimately the Fed’s monetary policy is going to collapse the dollar and it will lose its reserve status. In this podcast, he talked about what this portends. He also explained why he doesn’t think the Fed can kick the can down the road again.

Peter has been talking about a looming dollar collapse for years. He admits he was wrong on the timing. He thought it would happen a lot sooner than this. But he doesn’t think he is wrong now just because he was wrong back then.

The problems are so much bigger now than they were a decade ago, and therefore, I think our ability to kick the can down the road again, I think is gone. I mean, yes, I underestimated that ability before, but at this point, it’s impossible. And so I don’t really see how the US government, the Federal Reserve, is going to stop gold from going up.”

Looking back, gold’s first major rally was in the 1970s when the price went from around $35 to over $800. At the time, Fed Chair Paul Volker’s willingness to get out of the way and allow interest rates to rise sharply to wherever the market was going to take them stopped that rally and kicked off a 20-year bear market in gold. “The Fed did what it took,” Peter said. “They did the right thing.”

The second gold rally started after the dot-com bubble popped and ended after gold set its previous record high just over $1,900 back in 2011. What stopped that? What caused gold to pull back from $1,900?

Somehow, they were able to convince the world and everybody who was worried that QE would end in disaster and that zero percent interest rates would be a failure – the Fed was able to convince everybody that the programs worked, and because they worked, they were temporary and would be ended, and that the Fed was going to start normalizing interest rates and shrink the balance sheet back down to pre-2008 crisis levels. And the market actually believed it.”

In effect, the Fed never had to raise rates to stop the gold rally. It just had to convince the world that it would raise rates.

Of course, the Fed never did normalize because it couldn’t normalize. When the central bank finally tried to slowly notch rates up, it broke the stock market in the fall of 2018. That led to the “Powell Pause” followed by three rate cuts in 2019 and the launch of a quantitative easing program that the Fed refused to call quantitative easing.

The other thing that kept the dollar propped up was the rest of the world slashing interest rates and running their own quantitative easing programs. The dollar got a lot of help from bad monetary policy abroad that made US policy look not as bad in comparison. As Peter put it, “We were the cleanest dirty shirt in the hamper.”

I think the hat’s empty. There are no more rabbits in there.”

Peter said that the Fed can’t raise rates like it did in 1980. The country can’t afford it. There is too much debt. There isn’t enough savings. And the Fed can’t pretend it’s going to raise rates like it did in 2008. Nobody will believe it.

So what are they going to do? Nothing. There is nothing they can do. Now, is there something that I haven’t thought of? I don’t know. Maybe. But obviously, since I can’t think of it, I can’t discuss it. So, is it possible that there’s a rabbit in there that I can’t see? Maybe. And so that’s why we’re not going to go all in. Because you don’t know what you don’t know. So, it is possible that there is a way to kick this can down the road again. I just can’t see it. But the bottom line is we don’t have to go all in. There is so much opportunity in the foreign markets, in the emerging markets, that just having an allocation in gold and gold stocks is all you need.”

Peter went on to talk about the mainstream talking points about this gold rally and the fact that people are actually starting to talk about the dollar losing its reserve status

end

Agnico Eagle EPS beats by $0.01, beats on revenue

Agnico Eagle (NYSE:AEM): Q2 Non-GAAP EPS of $0.18 beats by $0.01; GAAP EPS of $0.43 beats by $0.28.

Revenue of $557.18M (+5.8% Y/Y) beats by $11.36M.

Gold production for the quarter was down ~20% to 74,317 ounces, as a result of the suspension of operations in April.

Raised Gold production guidance for 2020 to 1.68-1.73M ounces (versus previous guidance of 1.63-1.73M ounces).

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

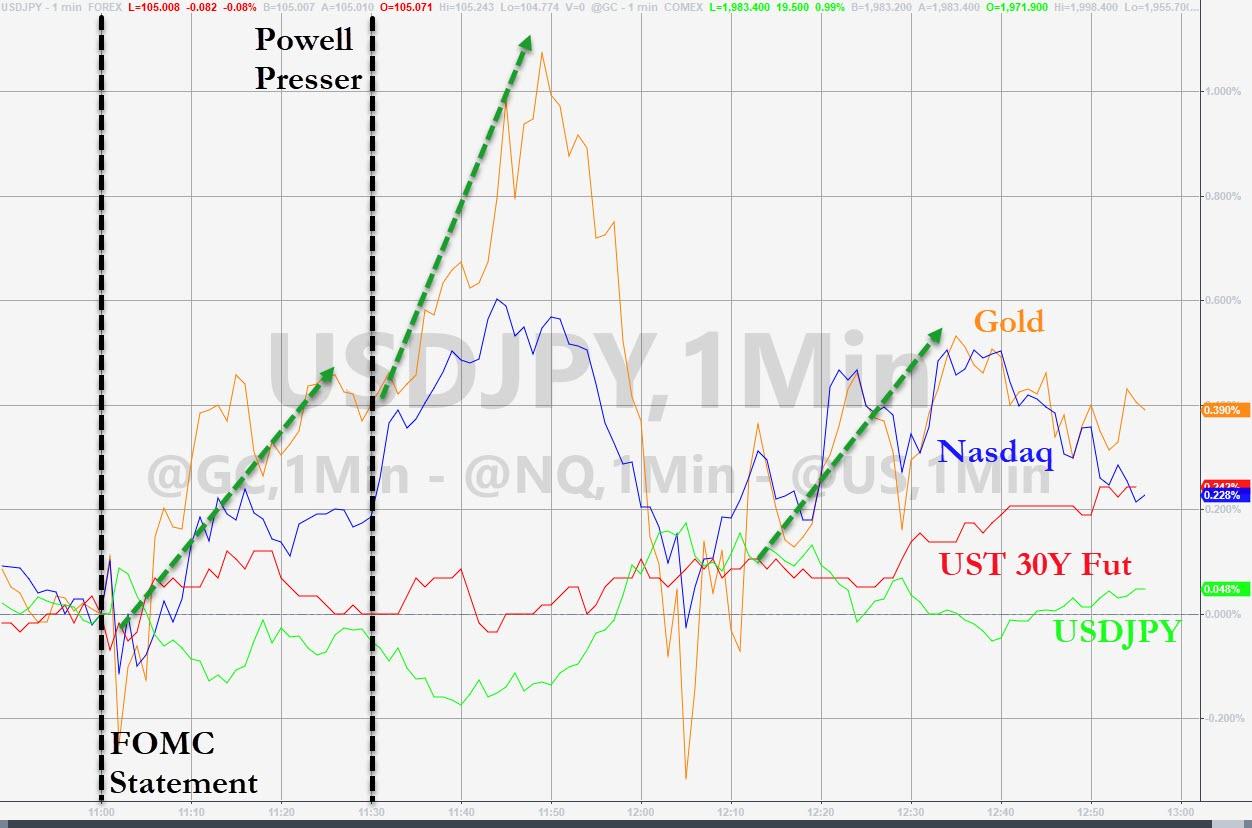

“Wobbly” Markets Tread Water Ahead Of FOMC As Asian Covid Cases Surge

US equity futures and European shares fluctuated on Wednesday, treading water and generally unchanged ahead of the latest FOMC meeting at 2pm today, while a resurgence of COVID-19 cases in Asia (especially China, Japan and Hong Kong) kept investors cautious. The dollar slipped in the run-up to Wednesday’s decision from the Federal Reserve’s policy meeting.

Wall Street closed lower on Tuesday and the negative sentiment continued through the Asian session, with Japan’s Nikkei falling on a rising yen and a weak start to the corporate earnings season. The MSCI world equity index was flat in early trading while mixed corporate earnings sent MSCI’s main European Index down by a quarter of a point.

Deaths from coronavirus in the United States registered their biggest one-day increase since May on Tuesday, with this month’s spike in infections having forced some states to make a U-turn on the reopening of their economies. Asia and Europe have also been hit by new surges in COVID-19 infections, with several countries imposing new restrictions and Britain imposing 14-day quarantines on travellers from Spain. Global airlines cut their coronavirus recovery forecasts on Tuesday, saying it would take until 2024 – a year longer than previously expected – for passenger traffic to return to pre-crisis levels.

“It should be clear to investors that the virus itself is not going away,” said David Riley, chief investment strategist at BlueBay Asset Management. “It’s something that’s going to be there having an impact on behaviour, having an impact on economic activity through the remainder of this year and into much of next year.”

U.S. futures and European equities swung from losses to modest gains as major earnings streamed in. AMD jumped about 10% in the premarket after increasing its guidance and Starbucks advanced on a sales rebound. Seagate Technology tumbled after an earnings miss.

Europe’s STOXX 600 was up 0.1%, Germany’s DAX was down 0.1% and France’s CAC 40 gained 0.7% on the back of a flurry of better than feared results, including from heavyweight luxury group Kering. Spanish bank Santander reported a record second-quarter loss while Germany’s Deutsche Bank gave a slightly improved outlook. Barclays fell on bad loan provisions.

Asian stocks fell, led by energy and industrials, after rising in the last session. Markets in the region were mixed, with Japan’s Topix Index and India’s S&P BSE Sensex Index falling, and Shanghai Composite and Hong Kong’s Hang Seng Index rising. The Topix declined 1.3%, with Melco Holdings and SB Technology Corp falling the most. The Shanghai Composite Index countered the broader Asian weakness, rising 2.1%, with Xi’an Bright Laser Technologies and Anji Micro posting the biggest advances.

In Asian economic news, the Hong Kong recession turned into a depression, with the preliminary reading of Q2 Hong Kong GDP growth coming in at an all time low -9.0% yoy, while in quarter-over-quarter non-annualized terms, real GDP contracted by 0.1% in Q2, vs. a 5.5% decline in Q1 2020. Private consumption, fixed investment and services trade fell further on a year-over-year basis while goods trade growth turned less negative in Q2 compared with Q1, helped by the recovery of the mainland China economy. Looking ahead, external demand might recover in Q3 but the recent surge of local coronavirus cases and the related tightening of social distancing requirements could weigh on domestic activity.

“Global stock markets appear to be starting to get a little wobbly as the latest earnings numbers start to paint a picture of a global economy that could start to face a challenging time in the weeks and months ahead,” wrote Michael Hewson, chief market analyst at CMC Markets UK. “The resurgence of coronavirus cases starting to get reported across the world is prompting the realisation that hopes of a V-shaped recovery are starting to look like pie in the sky.”

Investors will be keeping a close eye on the U.S. Federal Reserve which concludes its two-day meeting. The Fed is expected to sound reassuringly accommodative at its policy review later in the day and perhaps open the door to a higher tolerance for inflation – something dollar bears think could squash real yields and sink the currency even further. With data from unemployment claims to credit-card spending and air travel plateauing in July, Fed Chairman Powell is expected to reinforce his message that it will do whatever it can to support the recovery, while repeating a call for fiscal aid from Congress.

Investors are also focused on U.S. Congress and White House as they clash over new measures to replace enhanced coronavirus unemployment benefits that are due to expire on Friday. BlueBay’s Riley said the market consensus was that a $1 trillion support package will be agreed. “I think that’s a kind of bare minimum and that won’t be the last that will be needed,” he said.

“The Fed may not announce anything new but there is an assumption that monetary and fiscal policy will be there to bridge the gap,” said Chris Chapman, a portfolio manager at Manulife Investment. “Plus, there is a lot of optimism about potential vaccines, given how many are in the works. The combination of those factors gives people reason to look at risk.”

After today’s Fed announcement, investors will keep an eye on earnings this week from Amazon.Com, Apple and Alphabet for clues on whether the resurgence of Covid-19 is affecting tech companies and a recovery in the global economy. A drop in U.S. consumer confidence added to evidence that the pace of the rebound is cooling as the virus interrupts reopenings in several states.

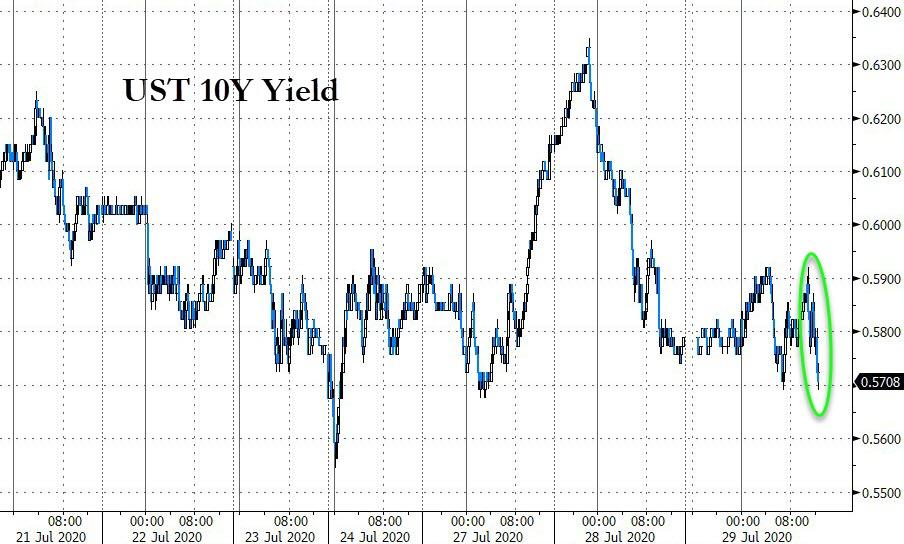

In rates, Treasuries drifted lower into early U.S. session as S&P 500 E-minis pare losses, weighing on long end of the curve. Broadly calm price action was evident in Asia, early Europe on low volumes ahead of Fed decision where no policy move is expected but some strategists have suggested an extension in duration of bond purchases is a possibility in the near-term. U.S yields were cheaper by 1bp-2bp at long with 2s10s, 5s30s steeper by ~1bp; 10-year yields ~0.59%, higher by 1.2bp vs Tuesday’s close. Asia session UST futures volumes dropped back to 60% of 20-day average levels as looming FOMC decision curbed risk-taking. High-grade euro zone bond yields dropped to their lowest in more than two months. The German 10-year yield was at -0.505%, having hit as low as -0.521%.

In FX, a gauge of the dollar fell to the lowest level since mid-2018 amid gloomy sentiment on virus recovery and a drop in U.S. consumer confidence, heading toward its worst monthly performance against peers in almost one decade. The euro resumed its advance, rising 0.5% toward the $1.18 mark while the pound advanced for a ninth day to the strongest level since March. The Norwegian krone leads gains among G-10 currencies as crude prices rally; the Aussie dollar outperforms its Kiwi peer after Australian CPI data beat estimates.

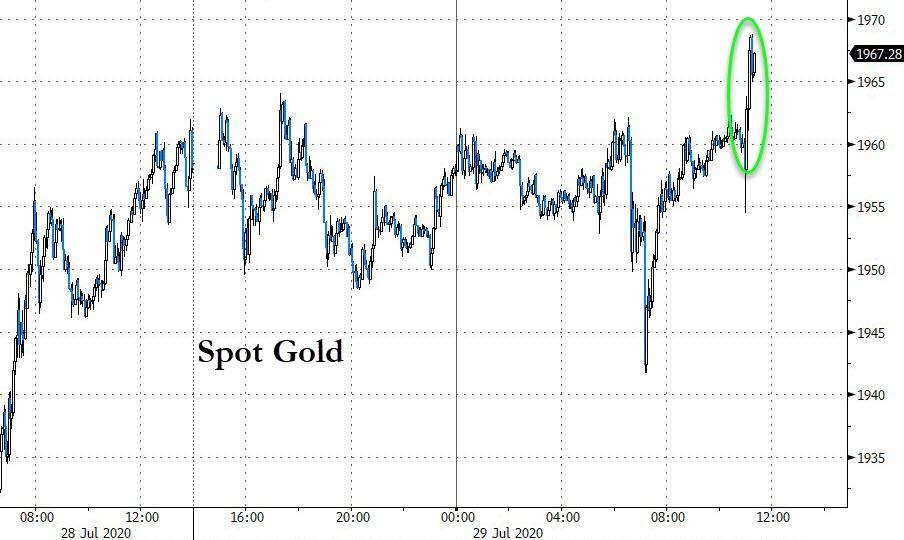

In commodities, gold hovered just below its record $2,000 an ounce and Bitcoin was steady just above $11,000 as the two assets took a breather after eight-day rallies. Gold was down 0.2% at $1,957.32 an ounce. Oil prices climbed after a surprise drop in U.S. crude inventories was enough to offset concerns about U.S. fuel demand, though concerns about the record increases in COVID-19 infections kept gains in check.

Lastly to the day ahead, where the big event is the Federal Reserve meeting in the US and Chair Powell’s press conference. On the data front we will get weekly MBA mortgage applications, June advance goods trade balance, pending home sales and preliminary June wholesale inventories. Also it is a large earnings day with Sanofi, Rio into, GlaxoSmithKline, Qualcomm, PayPal, Boeing, Santander, General Electric, General Motors, Barclays and Nomura all reporting.

Market Snapshot

- S&P 500 futures up 0.2% to 3,220.50

- STOXX Europe 600 up 0.2% to 368.31

- MXAP down 0.3% to 167.20

- MXAPJ up 0.2% to 553.03

- Nikkei down 1.2% to 22,397.11

- Topix down 1.3% to 1,549.04

- Hang Seng Index up 0.5% to 24,883.14

- Shanghai Composite up 2.1% to 3,294.55

- Sensex down 0.6% to 38,281.38

- Australia S&P/ASX 200 down 0.2% to 6,006.39

- Kospi up 0.3% to 2,263.16

- Brent futures up 1.2% to $43.72/bbl

- Gold spot little changed at $1,959.01

- U.S. Dollar Index down 0.2% to 93.52

- German 10Y yield fell 0.3 bps to -0.511%

- Euro up 0.3% to $1.1749

- Italian 10Y yield rose 2.0 bps to 0.882%

- Spanish 10Y yield fell 0.5 bps to 0.351%

Top Overnight News

- The ECB will look at inflation in deciding when to unwind its pandemic stimulus program, said policy maker Yannis Stournaras, suggesting the plan may continue longer than anticipated

- The U.K. is signing a deal with GlaxoSmithKline Plc and Sanofi to secure as many as 60 million doses of their experimental shot for a coronavirus vaccine

- Traders are betting central bankers will pin down global borrowing costs to historic lows for years to come

- The damage to European jobs from virus lockdowns may only be temporarily held at bay by furlough programs, ECB researchers say

- Credit Suisse Group AG is set to announce a sweeping overhaul of its business, merging its investment bank and capital-markets unit