GOLD:$: 1951.30 DOWN $10.00 The quote is London spot price (cash market)

Silver:$23.27// DOWN 97 CENTS London spot price ( cash market)

Options expiry on the big London LBMA/OTC is scheduled for July 31. at exactly 10 am est// 3pm London time

The bankers will do everything in their power to keep gold/silver from rising. They are hurt very badly as huge number of options are now in the money

stay tune…

Closing access prices: London spot

i)Gold : $1955.70 LONDON SPOT 4:30 pm

ii)SILVER: $23.47//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUGUST GOLD: XXX CLOSE 1::30 PM SPREAD SPOT/FUTURE AUG (BACKWARD $XX)

OCT GOLD: $XX CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: $XX ($ NORMAL CONTANGO)

DEC. GOLD $XX CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $XX ($XX ABOVE NORMAL CONTANGO) OR .03% ABOVE CONTANGO OR EXCESS CONTANGO)

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $XX…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : XX CENTS PER OZ (8 CENTS ABOVE CONTANGO)

SILVER DECEMBER CLOSE: $XX 1:30 PM SPREAD SPOT/FUTURE DEC. : XX CENTS PER OZ ( 28 CENTS ABOVE NORMAL CONTANGO)

DONATE

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today:1/1

issued 0

EXCHANGE: COMEX

CONTRACT: JULY 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,953.500000000 USD

INTENT DATE: 07/29/2020 DELIVERY DATE: 07/31/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 H JP MORGAN 1

690 C ABN AMRO 1

____________________________________________________________________________________________

TOTAL: 1 1

MONTH TO DATE: 9,607

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 1 NOTICE(S) FOR 100 OZ (0.0031 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 9607 NOTICES FOR 960700 OZ (29.881 TONNES)

SILVER

FOR JULY

596 NOTICE(S) FILED TODAY FOR 2,980,000 OZ/

total number of notices filed so far this month: 17,294 for 86.470 MILLION oz

BITCOIN MORNING QUOTE $10,925 DOWN 177

BITCOIN AFTERNOON QUOTE.: $11,095 DOWN 5

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $10.00 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

A SMALL CHANGE IN GOLD INVENTORY AT THE GLD/// A WITHDRAWAL OF 1.16 TONNES OF GOLD WITHDRAWN FROM THE GLD//

GLD: 1,241.96 TONNES OF GOLD//

WITH SILVER DOWN 97 CENTS TODAY: AND WITH NO SILVER AROUND:

A SMALL CHANGES IN SILVER INVENTORY AT THE SLV:

A WITHDRAWAL OF 931,000 OZ FROM THE SLV//

RESTING SLV INVENTORY TONIGHT:

SLV: 571.352 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A SMALL SIZED 372 CONTRACTS FROM 184,020 UP TO 184,392, AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE SMALL SIZED GAIN IN OI OCCURRED WITH OUR $0.07 GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS PRIMARILY DUE TO HUGE BANKER SHORT COVERING PLUS A SMALL EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A HUGE INCREASE IN SILVER STANDING AT THE COMEX FOR JULY. WE HAD A GOOD NET GAIN IN OUR TWO EXCHANGES OF 1062 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: JULY: 0 AND SEP 601 DEC: 0 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 601 CONTRACTS. WITH THE TRANSFER OF 601 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 601 EFP CONTRACTS TRANSLATES INTO 11.075 MILLION OZ ACCOMPANYING:

1.THE 7 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

86.470 MILLION OZ INITIALLY IN JULY.

WEDNESDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 7 CENTS ).. AND,OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS. THE SMALL GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A HUMONGOUS INCREASE IN STANDING OF SILVER OZ STANDING FOR JULY, STRONG BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A GOOD NET GAIN OF 1062 CONTRACTS OR 5.310 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

JULY

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF JULY:

25,671 CONTRACTS (FOR 21 TRADING DAY(S) TOTAL 25,671 CONTRACTS) OR 128.355 MILLION OZ: (AVERAGE PER DAY: 1222 CONTRACTS OR 6.112 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 128.355 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 18.33% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,265.77 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 128.355 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 372, WITH OUR 7 CENT GAIN IN SILVER PRICING AT THE COMEX ///WEDNESDAY… THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 601 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A GOOD SIZED OI CONTRACTS ON THE TWO EXCHANGES: 973 CONTRACTS (WITH OUR $0.07 CENT GAIN IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 601 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A SMALL SIZED INCREASE OF 372 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 7 CENT GAIN IN PRICE OF SILVER/AND A CLOSING PRICE OF $24.34 // WEDNESDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.9305 BILLION OZ TO BE EXACT or 132% of annual global silver production (ex Russia & ex China).

FOR THE NEW JULY DELIVERY MONTH/ THEY FILED AT THE COMEX: 596 NOTICE(S) FOR 2,980,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 86.470 million oz

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 701 CONTRACTS TO 599,330 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE SMALL SIZED GAIN OF COMEX OI OCCURRED WITH OUR STRONG RISE IN PRICE OF $12,45 /// COMEX GOLD TRADING// WEDNESDAY// WE HAD HUGE BANKER SHORT COVERING, A TINY SIZED INCREASE IN GOLD OZ STANDING AT THE COMEX FOR JULY, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE AND A STRONG GOLD SPREADER LIQUIDATION. THIS ALL HAPPENED WITH OUR STRONG GAIN IN PRICE OF $12.45 .

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 58

WE GAINED A GOOD SIZED 4489 CONTRACTS (13.97 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3788 CONTRACTS:

CONTRACT .; AUG 2576 AND OCT: 20 DEC: 1192; FEB: 0 ALL OTHER MONTHS ZERO//TOTAL: 3788. The NEW COMEX OI for the gold complex rests at 600,085. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4489 CONTRACTS: 701 CONTRACTS INCREASED AT THE COMEX AND 3788 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 4489 CONTRACTS OR 16.31 TONNES. WEDNESDAY, WE HAD A GAIN OF $12.45 IN GOLD TRADING……

AND WITH THAT GAIN IN PRICE, WE HAD A GOOD SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 13.97 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $12.45).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS ALSO UNSUCCESSFUL (SEE BELOW).

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3788) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (701 OI): TOTAL GAIN IN THE TWO EXCHANGES: 5244 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)A TINY INCREASE IN GOLD STANDING AT THE GOLD COMEX FOR THE FRONT JULY MONTH, 3) ZERO LONG LIQUIDATION; 4) SMALL COMEX OI GAIN AND .5) FAIR EXCHANGE FOR PHYSICAL ISSUANCE 6) CONTINUAL STRONG GOLD SPREADER LIQUIDATION... AND …ALL OF THIS WAS COUPLED WITH OUR STRONG GAIN IN GOLD PRICE TRADING//WEDNESDAY//$12.45.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

SPREADING OPERATIONS/NOW SWITCHING TO GOLD

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN GOLD AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF AUGUST FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF JULY. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUGUST), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

JULY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAY(S) IN TONNES: 308.41 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 308.41/3550 x 100% TONNES =8.68% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3259.43 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 308.41 TONNES SO FAR..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A SMALL SIZED 372 CONTRACTS FROM 184,020 UP TO 184,392 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE SMALL SIZED GAIN IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) HUGE BANKER SHORT COVERING , 2) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A HUMONGOUS INCREASE STANDING AT THE SILVER COMEX FOR JULY AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 601 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY: 0 CONTRACTS AND SEPT: 2692 AND DEC. 200 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 601 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 372 CONTRACTS TO THE 601 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD GAIN OF 973 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 5.310 MILLION OZ, OCCURRED WITH OUR 7 CENT GAIN IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 7.73 POINTS OR 0.23% //Hang Sang CLOSED DOWN 172.55 POINTS OR 0.69% /The Nikkei closed DOWN 57.88 POINTS OR 0.26%//Australia’s all ordinaires CLOSED UP .81%

/Chinese yuan (ONSHORE) closed DOWN at 7.0032 /Oil UP TO 40.50 dollars per barrel for WTI and 43.16 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0032 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0035 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: 1,837,513.0000 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

i)we had 2 deposits into the customer account

into JPMorgan: nil oz

ii) Into Delaware: 1001.200 oz

iii) Into Scotia: 788,787,170 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 163.098 million oz of total silver inventory or 48,99% of all official comex silver. (163.677 million/334.544 million

total customer deposits today: 789,788.370 oz

we had 2 withdrawals:

i)Out of CNT: 613,257.550 oz

ii) Out of Delaware: 5027.803 oz

total withdrawals; 618,285.350 oz

We had 1 adjustments

out of Brinks: dealer to customer account

4758.50 oz dealer to customer

total dealer silver: 133.067 million

total dealer + customer silver: 334,544 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The front month of July has an open interest of 596 contracts, as we LOST 230 contracts. We had 459 notices served on WEDNESDAY, so we GAINED 229 contracts or an additional 1,145,000 oz will stand in this active delivery month of July as they REFUSED TO morph into a London based forwards. Somebody was in urgent need of silver on this side of the pond.

The next month after July is the non active month of August and here sees its open interest FELL by 99 contracts to 820

The big September contract month sees a LOSS of 1109 contracts down to 129,983.

The total number of notices filed today for the JULY 2020. contract month is represented by 596 contract(s) FOR 2,980,000, oz

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 17,294 x 5,000 oz = 86,470,000 oz to which we add the difference between the open interest for the front month of JULY.(596) and the number of notices served upon today 596 x (5000 oz) equals the number of ounces standing.

Thus the FINAL standings for silver for the JULY/2019 contract month: 17,294 (notices served so far) x 5000 oz + OI for front month of JULY (596)- number of notices served upon today (596) x 5000 oz of silver standing for the JULY contract month.equals 86,470,000 oz. (A WHOPPER )//ALL TIME RECORD FOR ONE DELIVERY MONTH

WE GAINED 229 CONTRACTS OR 1,145,000 OZ WILL STAND FOR DELIVERY. SILVER IS STILL VERY SCARCE ON THIS SIDE OF THE POND AND THE REASON FOR CONSIDERABLE MORPHING OVER TO LONDON DURING THIS DELIVERY MONTH OF JULY.

TODAY’S ESTIMATED SILVER VOLUME : 163,035 CONTRACTS // volume huge+++/

FOR YESTERDAY: 184,020.,CONFIRMED VOLUME//volume huge++++++++/

YESTERDAY’S CONFIRMED VOLUME OF 184,020 CONTRACTS EQUATES to 0.920 million OZ 131% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 2.13% ((JULY 30/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.00% to NAV: (JULY 39/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 2.13%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 19.59 TRADING 19.42///NEGATIVE 0.87

END

And now the Gold inventory at the GLD/

JULY 30/WITH GOLD DOWN $10.00 TODAY, WE HAVE ANOTHER SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES//INVENTORY RESTS AT 1241.96 TONNES.

JULY 29//WITH GOLD UP $12.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 8.47 TONNES/INVENTORY RESTS AT 1243.12 TONNES

JULY 28///WITH GOLD UP $13.25 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 5.84 TONNES/INVENTORY RESTS AT 1234.65

JULY 27//WITH GOLD UP $35.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF XXX TONNES/INVENTORY RESTS AT 1228.81 TONNES

JULY 24/WITH GOLD UP $8.80 TODAY: WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.80 TONNES//INVENTORY RESTS AT 1228.81 TONNES

JULY 23/WITH GOLD UP $24.90 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 7.26 TONNES/INVENTORY RESTS AT 1225.01 TONNES

JULY 22/WITH GOLD UP $22.00 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 7.89 TONNES/INVENTORY RESTS AT 1219.75 TONNES

JULY 21//WITH GOLD UP $26.00 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.97 TONNES INTO THE GLD// INVENTORY RESTS AT 1211.86 TONNES

JULY 20/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1206.89 TONNES

JULY 17/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1206.89 TONNES

JULY 16/WITH GOLD DOWN $9.80 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: INVENTORY RESTS AT 1206.89 TONNES

JULY 15//WITH GOLD UP $1.55 TODAY/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 2.96 TONNES INTO THE GLD///INVENTORY RESTS AT 1206.89 TONNES

JULY 14//WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 3.51 TONNES/INVENTORY RESTS AT 1203.97 TONNES

JULY 13//WITH GOLD UP $12.50 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1200.46 TONNES

JULY 10/WITH GOLD DOWN $.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD//A STRANGE WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1200.82 TONNES

JULY 9//WITH GOLD DOWN $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OX 3.21 TONNES INTO THE GLD//INVENTORY RESTS AT 1202.57 TONNES

JULY 8/WITH GOLD UP $13.75 TODAY; A BIG CHANGE IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 7.89 TONNES INTO THE GLD//INVENTORY RESTS AT 1199.36 TONNES

JULY 7/WITH GOLD UP $12.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1191.47 TONNES

JULY 6/WITH GOLD UP $6.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1191.47 TONNES

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

JUNE 30//WITH GOLD UP $16.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1178.90 TONNES

JUNE 29/WITH GOLD UP $2.90 TODAY: A HUGE DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1178.90 TONNES

JUNE 26/WITH GOLD UP $5.03 TODAY: VERY STRANGE: A PAPER WITHDRAWAL OF 1.46 TONNES//INVENTORY RESTS AT 1175.39 TONNES

JUNE 25//WITH GOLD DOWN $3.30 TODAY//ANOTHER STRONG PAPER DEPOSIT OF 7.6 TONNES///INVENTORY RESTS AT 1176.85 TONNES

JUNE 24/WITH GOLD DOWN $1.50 TODAY; A STRONG 3.21 TONNES ADDED TO THE GLD//INVENTORY RESTS AT 1169.25 TONNES

JUNE 23/WITH GOLD UP $25.50 TODAY/ANOTHER CRIMINAL PAPER DEPOSIT OF 6.73 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1166.04 TONNES

JUNE 22/WITH GOLD UP $14.00 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 23.09 TONNES//INVENTORY RESTS AT 1159.31 TONNES

JUNE 19/WITH GOLD UP$16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//; INVENTORY RESTS AT 1136.22 TONNES

JUNE 18//WITH GOLD DOWN $2.75 TODAY: NO CHANGES IN GOLD INVENTORY: INVENTORY RESTS AT 1136.22 TONNES

JUNE 17/WITH GOLD DOWN $1.05: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1136.22 TONNES

JUNE 16//WITH GOLD UP $6.70 TODAY: NO CHANGES IN GOLD INVENTORY: /INVENTORY RESTS AT 1136.22 TONNES

JUNE 15/WITH GOLD DOWN ANOTHER $8.80 TODAY, NO CHANGES IN GOLD INVENTORY/INVENTORY RESTS AT 1136.22 TONNES

JUNE 12//WITH GOLD DOWN $1.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 1.17 TONNES AT THE GLD//INVENTORY RESTS AT 1136.22 TONNES

JUNE 11//WITH GOLD UP $16.80 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 6.55 TONNES AT THE GLD//INVENTORY RESTS AT 1135.05 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

JULY 30/ GLD INVENTORY 1241.96 tonnes*

LAST; 870 TRADING DAYS: +302.46 NET TONNES HAVE BEEN ADDED THE GLD

LAST 770 TRADING DAYS://+480.93 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JULY 30//WITH SILVER DOWN 97 CENTS TODAY: WE HAVE A SMALL CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 571.352 MILLION OZ//

JULY 29/WITH SILVER UP 7 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY//A DEPOSIT OF 5.984 MILLION OZ//INVENTORY RESTS AT 572.283 MILLION OZ//

JULY 28 WITH SILVER DOWN 14 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 7.52 MILLION OZ//INVENTORY RESTS AT 566.299 MILLION OZ//

JULY 27/WITH SILVER UP $2.67 TODAY, WE HAD NO CHANGES IN SILVER INVENTORY: A DEPOSIT OF XX MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ//

JULY 24/WITH SILVER DOWN $0.12 TODAY: NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 558.779 MILLION OZ/

JULY 23/WITH SILVER UP $.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A HUMONGOUS PAPER DEPOSIT OF 9.594 MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ///

JULY 22/WITH SILVER UP $1.54 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A HUMONGOUS PAPER DEPOSIT OF 7.218 MILLION OZ//INVENTORY RESTS AT 549.185 MILLION OZ/

JULY 21/WITH SILVER UP $1.38 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUMONGOUS PAPER DEPOSIT OF 15.368 MILLION OZ////INVENTORY RESTS AT 541.967 MILLION OZ//

JULY 20/WITH SILVER UP 40 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 3.819 MILLION OZ ‘ENTERED” THE SLV..INVENTORY RESTS AT 526.599 MILLION OZ/

JULY 17/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 1.583 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 522.780 MILLION OZ//

JULY 16//WITH SILVER DOWN 14 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ//INVENTORY RESTS AT 521.197 MILLION OZ..

JULY 15.WITH SILVER UP 21 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.956 MILLION OZ//INVENTORY RESTS AT 516.074 MILLION OZ//

JULY 14/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 514.118 MILLION OZ//

JULY 13//WITH SILVER UP 67 CENTS TODAY: A HUGE CHANGE IN SILVER: A WITHDRAWAL OF 1.677 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 514.118 MILLION OZ//

JULY 10/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 4.844 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.795 MILLION OZ

WHAT A FRAUD!!

JULY 9/WITH SILVER DOWN 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 8.198 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 510.951 MILLION OZ/

JULY 8/WITH SILVER UP 37 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.118 MILLION OZ FROM THE SLV//VERY SURPRISING.//INVENTORY RESTS AT 502.753 MILLION OZ//

JULY 7/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/INVENTORY RESTS AT 503.871 MILLION OZ///

JULY 6//WITH SILVER UP 24 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.863 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 503.871 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

JUNE 30/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 29/WITH SILVER DOWN ONE CENT TODAY: A TWO CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 466,000 OZ TO PAY FOR STORAGE FEES AND INSURANCE//// AND A LARGE DEPOSIT OF 1.212 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 26/WITH SILVER UP 6 CENTS TODAY: ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ RESTS AT 491.858 MILLION OZ//

JUNE 25/WITH SILVER UP 12 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 931,000 OZ INTO THE SLV////INVENTORY RESTS AT 491.858 MILLION OZ//

JUNE 24///WITH SILVER DOWN 31 CENTS// NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 490.927 MILLION OZ

JUNE 23//WITH SILVER UP 16 CENTS TODAY: A MONSTROUS CHANGE IN INVENTORY: A PAPER DEPOSIT OF 4.473 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 490.927 MILLION OZ//

JUNE 22/WITH SILVER UP 15 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/: INVENTORY/INVENTORY RESTS AT 486/454 MILLION OZ//

JUNE 19//WITH SILVER UP 22 CENTS TODAY: STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 839,000 OZ FROM THE SLV////INVENTORY RESTS AT 486,454 MILLION OZ..

JUNE 18/WITH SILVER DOWN 16 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 932,000 OZ INTO THE SLV////INVENTORY RESTS AT 487.293 MILLION OZ

JUNE 17/WITH SILVER UP 8 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.261 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.361 MILLION OZ

JUNE 16//WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.118 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 483.100 MILLION OZ//

JUNE 15/WITH SILVER DOWN 14 CENTS NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 481.982 MILLION OZ///

JUNE 12/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: TWO DEPOSITS OF 7.269 MILLION OZ AND 1.802 MILLION OZ ADDED TO THE SLV///INVENTORY RESTS THIS WEEKEND AT 481.982 MILLION OZ//

JUNE 11//WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY: ///INVENTORY RESTS AT 472.89 MILLION OZ//

JULY 30.2020:

SLV INVENTORY RESTS TONIGHT AT

571.352 MILLION OZ.

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

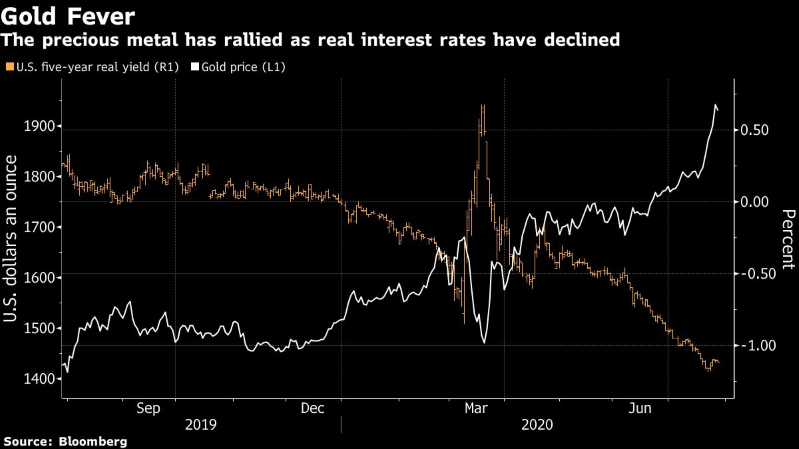

COVID Pandemic Will Support Gold In Long Term as Highlights Strong Fundamental Reasons To Invest In Gold

Gold Hits Record High: Sprint Or Marathon? (Investment Update from the World Gold Council – 30 July, 2020)

COVID-19 pandemic may bring structural shifts to asset allocation and there are strong fundamental reasons supporting gold investment longer term.

Gold has been on a generally positive trend for the past few years and the onset of the global COVID-19 pandemic has made gold’s relevance as a hedge even more apparent and accelerated its price performance.

Gold increased by 17% during the first half of 2020, moving up by an additional 10% in July.

The most recent price move has come fast which, combined with markedly weak consumer demand, may result in higher gold price volatility in the near term. However, we believe the COVID-19 pandemic may bring structural shifts to asset allocation and that there are strong fundamental reasons supporting gold investment longer term.

Gold broke a new high on 28th July, reaching US$1,940.9/oz on the LBMA Gold Price PM (PM Price) and topping US$1,981.3/oz intra-day.

On the heels of this milestone, investors are asking two key questions, which we explore in this report: ‘How does this compare to previous highs?’ and ‘Is the price rally sustainable?’

Full Report from World Gold Council here

NEWS and COMMENTARY

Gold slips as Fed’s continuing ultra low rates whets risk appetite

China Banks, Regulators Move to Cool Gold Rush

Anxious investors are pushing gold prices to all-time highs

The Other Reason Silver Is Soaring: Disruptions in Latin America

Where did the gold and silver for Britain’s coins come from?

India’s banks are racing to lend against a $1.5 trillion hoard of gold

India Considers Amnesty for Citizens Hoarding Gold Illegally

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

29-Jul-20 1954.35 1950.90, 1506.80 1502.39 & 1663.54 1659.24

28-Jul-20 1931.65 1940.90, 1499.15 1501.48 & 1647.70 1654.23

27-Jul-20 1940.55 1936.65, 1511.30 1504.78 & 1659.56 1647.70

24-Jul-20 1893.85 1902.10, 1486.67 1490.30 & 1631.55 1638.09

23-Jul-20 1882.35 1878.30, 1480.28 1477.47 & 1624.47 1621.54

22-Jul-20 1851.00 1852.40, 1462.85 1456.91 & 1604.82 1598.44

21-Jul-20 1823.20 1842.55, 1436.86 1449.35 & 1594.21 1608.36

20-Jul-20 1810.30 1815.65, 1437.92 1438.18 & 1580.21 1590.87

17-Jul-20 1802.90 1807.35, 1435.47 1442.45 & 1578.98 1581.07

16-Jul-20 1804.60 1807.70, 1438.09 1436.04 & 1583.72 1581.56

15-Jul-20 1809.30 1804.60, 1436.22 1441.31 & 1582.96 1579.57

14-Jul-20 1798.20 1801.90, 1436.58 1440.62 & 1583.14 1581.71

13-Jul-20 1808.05 1807.50, 1435.23 1432.26 & 1598.32 1591.68

Own gold coins and bars in the safest vaults in Zurich, Switzerland with GoldCore. Learn why Switzerland remains a safe haven jurisdiction for owning precious metals. Access Our Most Popular Guide, the Essential Guide to Storing Gold in Switzerland here

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here

ii) Important gold commentaries courtesy of GATA/Chris Powell

Pam and Russ Martens: U.S. GDP seen collapsing by record rate in Q2

As outlined before from the Atlanta Fed 2nd quarter GDP is set to drop 32.1%

(Pam and Russ Martens/Wall Street on Parade)

Submitted by cpowell on Wed, 2020-07-29 16:16. Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Wednesday, July 29, 2020

The very reliable GDPNow forecasting model provided by researchers at the Atlanta Fed was updated this morning and predicts that gross domestic product in the United States contracted by a jaw-dropping 32.1 percent on a seasonally-adjusted, annualized rate in the second quarter.

The public will get the official number from the Bureau of Economic Analysis at the U.S. Department of Commerce at 8:30 a.m. tomorrow morning.

…

It’s expected that the second-quarter GDP number will be the largest decline since quarterly GDP records began being compiled by the BEA in 1947. It is also expected that the number will be exponentially worse than any quarter during the Great Recession of 2007 to 2009. …

… For the remainder of the report:

https://wallstreetonparade.com/2020/07/u-s-gdp-number-tomorrow-expected-…

END

China gets it: they are now terrified by the risks posed by paper gold (silver)

(Reuters/GATA)

Even China now is terrified by risks of paper gold

Submitted by cpowell on Wed, 2020-07-29 17:06. Section: Daily Dispatches

China Banks, Regulators Move to Cool Gold Rush

By Andrew Galbraith, Winni Zhou, Samuel Shen, and Arpan Varghese

Reuters

Wednesday, July 29, 2020

SHANGHAI — Chinese regulators and major banks are rushing to curb precious metal trading by domestic investors to temper speculation that some fear could cause a repeat of this year’s oil trading mishaps.

The scramble to limit risks comes as gold prices hit record highs this week, spurred by investors hunting for safe-haven assets in markets rattled by worries of rising coronavirus cases, lofty equity valuations and a falling U.S. dollar.

A deepening rift between the United States and China has also become a factor drawing mainland investors to gold.

Industrial and Commercial Bank of China, the country’s biggest lender, said today that from Friday it would bar its clients from opening new trading positions for platinum, palladium, and index products linked to precious metal. That directive, according to the lender’s customer service department, was in response to “violent price volatility” and “the need to control risks.”

Agricultural Bank of China said it had recently suspended new businesses related to gold, while Bank of China said it halted new account openings for platinum and palladium trading.

The Shanghai Gold Exchange said on Tuesday gold and silver holdings were high, and it would take risk-control measures if warranted to protect investors.

The Shanghai Futures Exchange, where gold and silver futures contracts are traded, also urged its members to strengthen risk-management efforts and invest rationally.

“Gold remains a niche investment in China due to limited investment channels,” said Frank Hao, an analyst at Hywin Wealth Management in Shanghai. “Investors mainly rely on purchasing paper gold products at commercial banks as a way to counteract risks.” …

… For the remainder of the report:

https://www.reuters.com/article/us-china-gold-rush/china-banks-regulator…

END

Goldseek is now making plans for major improvements in its site.

(Goldseek/GATA)

GoldSeek plans major improvements to start soon

Submitted by cpowell on Thu, 2020-07-30 02:11. Section: Daily Dispatches

10:10p ET Wednesday, July 29, 2020

Dear Friend of GATA and Gold:

Monetary metals internet site GoldSeek today announced plans to make wide-ranging additions and improvements in the near future.

GoldSeek’s new features will include:

— Live gold prices, including streaming live prices and charts.

— A format designed for mobile device

Increased coverage of the gold-mining industry.

— Virtual conferences about gold and silver.

— Higher downloading speed.

— A weekly gold stock review.

The full announcement can be read at GoldSeek here:

http://news.goldseek.com/GoldSeek/1596085199.php

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

India’s banks are now racing to lend against citizens huge hoard of $1.5 trillion in gold.

(Bloomberg/GATA)

India’s banks are racing to lend against a $1.5 trillion hoard of gold

Submitted by cpowell on Thu, 2020-07-30 02:20. Section: Daily Dispatches

By Swansy Afonso and Ankika Biswas

Bloomberg News

Wednesday, July 30, 2020

Indian families, sitting on the world’s biggest private stash of gold, are rushing to borrow against their jewelry as the precious metal rallies to records and the coronavirus pandemic fuels an economic downturn. Now financial firms and banks are using that demand to lure more customers from pawnbrokers and money lenders.

The added competition could lower borrowing costs for Indian consumers, who in desperate moments of financial stress often pay exorbitant rates to informal lenders to use gold as collateral. Firms like HDFC Bank Ltd. and Federal Bank Ltd. are expanding the loans they make against the precious metal. India’s gold lenders, such as Muthoot Finance Ltd. and Manappuram Finance Ltd., are making it easier for their clients to borrow.

…

Manappuram is offering gold-backed loans at the customer’s doorsteps via a 24-hour bank network since people are reluctant to leave their homes while coronavirus cases are surging in India. And it has staff and vehicles on standby to service client requests. HDFC Bank is boosting the number of branches offering such loans in rural India, where money lenders remain the norm. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2020-07-29/banks-are-racing-to-l…

END

For your interest….where did the gold and silver come from for Britain to coin?

Answer international trade.

(Sprott/GATA)

Where did the gold and silver for Britain’s coins come from?

Submitted by cpowell on Thu, 2020-07-30 04:13. Section: Daily Dispatches

12:35a ET Thursday, July 30, 2020

Dear Friend of GATA and Gold:

Anyone hanging around the gold sector for the last 20 years knows where much of Britain’s gold went.

Chancellor Gordon Brown sold half of it between 1999 and 2002, supposedly to diversify the country’s foreign exchange reserves but more likely to rescue London bullion banks from their short positions as the gold market turned upward and broke the gold carry trade of the preceding decade.

With the gold price having increased about eight times, from L180 to L1,500 per ounce, since the “Brown’s Bottom” sale began, the operation turns out to have cost the British government something like a trillion bazillion pounds. But what the heck — the banks were saved.

Since Britain does not have extensive gold deposits, where did the gold for its coins come from? Geologist and mining equity analyst Graham Birch, a member of the Board of Directors of Canadian financial house Sprott Inc., has written a book on the subject, “The Metal in Britain’s Coins — Where Did It Come from and How Did It Get Here?,” a fascinating excerpt from which was posted this week on Sprott’s internet site.

Birch reports that much of Britain’s first gold and silver came from international trade (including the African slave trade) and piracy, the gold being stamped into the sovereign coins that built an empire, only to be extracted from the population by the government to finance wars and similar necessities, leaving the population with paper cash that has devalued by nearly 100 percent in a century.

Birch concludes: “We can have no confidence that the pattern is going to change. Gold seems certain to outperform sterling and any other paper currency. And now there is no offsetting interest to make holding currency any more palatable.”

Since gold remains both the supreme money and the mechanism of escape from a corrupt and unfair financial system, monetary gold and silver in private hands are much resented by many governments and always vulnerable to more of their expropriation. So monetary metals investors may do well to learn some of the history Birch relates. The excerpt from his book is here:

https://sprott.com/insights/the-metal-in-britains-coins-where-did-it-com…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

iii) Other physical stories:

China is trying to curb paper gold trading

(zerohedge)

Chinese Banks Bar Clients From Buying Precious Metals

In an attempt to avoid another retail-driven momentum meltup similar to what happened with Chinese stocks earlier this month when government-media first encouraged Chinese investors to buy stocks only to backtrack days later when local markets soared sparking fears of another stock bubble on the mainland, Reuters reported that Chinese regulators and major banks have been rushing to curb precious metal trading by domestic investors to temper speculation that could send prices explosively higher, something we hinted at just last week.

The scramble to limit risks comes as gold prices hit record highs this week, spurred by investors hunting for safe haven assets in markets rattled by worries of rising coronavirus cases, lofty equity valuations, and a plunge in the U.S. dollar which prompted Goldman to contemplate if the days of the world’s reserve currency are numbered.

Industrial and Commercial Bank of China (ICBC), the country’s largest bank said on Wednesday it would bar its clients from opening new trading positions for platinum, palladium and index products linked to precious metal from Friday. That directive, according to the lender’s customer service department, was in response to “violent price volatility” and “the need to control risks.” The reality? It is neither in China’s, nor any other government’s interest, to see gold prices soaring as they likely would if tens of millions of Chinese speculators rushed to bid up the precious metal.

Similarly, Agricultural Bank of China said it had recently suspended new businesses related to gold, while Bank of China also said it halted new account openings for platinum and palladium trading.

Meanwhile, the Shanghai Gold Exchange said on Tuesday that gold and silver holdings were high, and it would take risk-control measures if warranted to protect investors.

It’s odd how investors are never “protected” when stock prices soar… but only when gold and silver do.

The Shanghai Futures Exchange, where gold and silver futures contracts are traded, also urged its members to strengthen risk-management efforts and invest rationally.

“Gold remains a niche investment in China due to limited investment channels,” said Frank Hao, an analyst at Hywin Wealth Management in Shanghai. “Investors mainly rely on purchasing paper gold products at commercial banks as a way to counteract risks.”

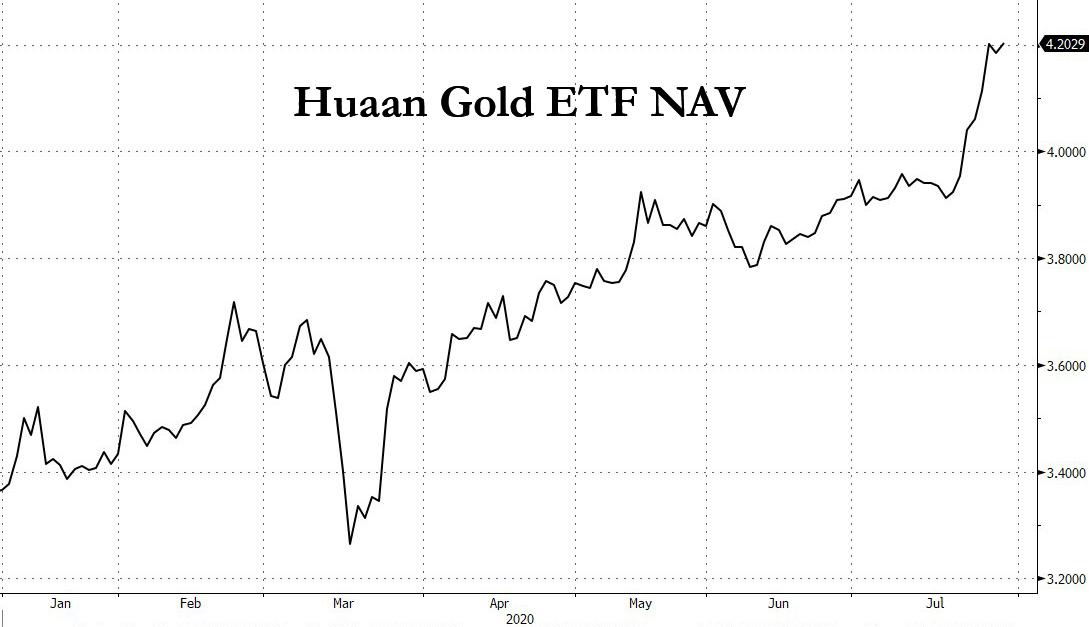

Chinese investors have also been actively buying up gold ETFs, whose turnover has jumped in recent weeks. Huaan Gold ETF, Asia’s biggest gold exchange-traded fund, has seen its assets under management soar more than 68% to over 11.8 billion yuan ($1.69 billion) since end-2019.

Hao said any further gains in gold may spur more speculation, despite regulatory attempts to tamp it down.

“If the gold price rises past $2,000, some more hot money will certainly flow into the market, and some investors will divert their stock investments to gold,” he said.

Which really says all one needs to know: when it comes to stocks, nobody is worried about the “hot money” flowing into the market, in fact it is encouraged. But when gold explodes higher and it may “divert” stock investment to gold the authorities start to panic and do everything in their power to limit its ascent.

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

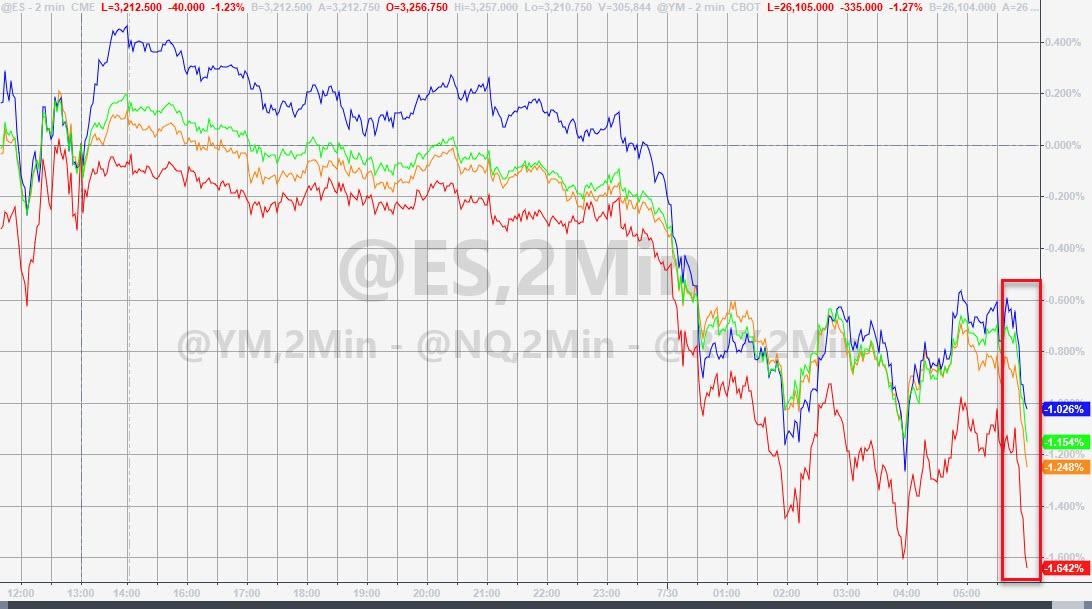

“Markets Are Nearing Their Limits”: Futures Falls, European Markets Tumble After German GDP Crashes

S&P futures tumbled, European stocks slumped to a three week low, 10Y Treasury yields dropped near all time lows (where the 5Y already was at 0.2374%, the lowest yield on record), and the EUR slid from near a 22-month high after the market reassessed that Powell’s message could have been even more dovish, and as German GDP crashed the most on record, alongside a surge in Covid-19 cases. Meanwhile, today’s US GDP report is expected to show shortly that the US economy contracted by a record 34.5%. The dollar strengthened against most Group-of-10 peers, with Scandinavian currencies leading losses.

German GDP contracted by 10.1% Q/Q in the second quarter of 2020, the biggest drop on record and worse than the 9% expected drop.The good news: this print is consistent with a relatively fast rebound of both the industrial and services sectors through May and June. That said, the below-consensus performance of Germany points to downside risks to consensus expectations for the Euro area Q2 release published tomorrow. It also means that the narrative of a faster European recovery than the US has just come to a screeching halt.

In US pre-market trading, UPS jumped on a surge in delivery demand during the pandemic. Qualcomm jumped 11.5% after forecasting fourth-quarter revenue largely above expectations, powered by sales of its chips used in 5G devices and reaching a settlement with Huawei Technologies Co Ltd. Eastman Kodak extended yesterday’s 319% surge from winning a government loan to assist in the production of a coronavirus treatment.

European stocks tumbled as much as 1.7%, dropping to the lowest since July 1, as the prospects for stimulus is weighed against the quickening spread of the coronavirus. Among the biggest decliners, SAP fell 2.6%, HSBC loses 3.4%, Allianz retreats 3.6%. Danone was down 5.6% after sales fell more than expected last quarter, dragged down by its water business. Lloyds Banking Group Plc slumped as much as 9% after profit was wiped out by bad loans charges. Volkswagen tumbled 5.6% after posting 2Q figures that included what MainFirst called a “clear miss” at the heavy- trucks division and worse-than-expected performance at some car brands.

“A vacuum on EU positive news could now be in store as the recovery fund ratification process begins” and European equities start to struggle, Dankse Bank strategists write in a note. Meanwhile, Germany’s covid infection rate remains above the threshold of 1.0, and recorded the highest number of new cases in around six weeks.

Asian stocks also fell, wiping out earlier gains, with shares in Japan and China under pressure even as the Kospi stayed modestly firmer following upbeat Samsung outlook. The drop was led by finance and utilities; markets in the region were mixed, with Singapore’s Straits Times Index and Thailand’s SET falling, and Taiwan’s Taiex Index and Jakarta Composite rising. The Topix declined 0.6%, with Gurunavi and Kushikatsu Tanaka falling the most. The Shanghai Composite Index reversed Wednesday’s rally and retreated 0.2%, with Hangzhou Electronic Soul Network and Shanghai Material Trading posting the biggest slides.

“Markets are nearing their limits without further stimulus and a much stronger recovery,” said Andrew McCaffery, the global CIO of asset management at Fidelity International, citing the failure to get the outbreak under control in some countries. “The third quarter is likely to be much more challenging and markets could see renewed volatility.”

While markets are bracing for a slew of earnings from the tech giants, they will also get economic data that’s will show the biggest contraction in U.S. GDP on record. Thursday marks the first time the four of the biggest U.S. tech companies — Apple, Amazon.com, Alphabet and Facebook — will post financial results on the same day, with expectations running high as their valuations soared over the past three months. Shares of the companies, which have a combined market value of about $5 trillion, fell between 0.6% and 0.9% premarket. On Wednesday, the CEOs of the four companies took jabs from lawmakers for antitrust issues.

“Tonight could be a pivot for markets with four of the big tech companies reporting earnings,” said Berndt Maisch, a senior portfolio manager at Tresides Asset Management. “Their stocks are so super expensive and hence offer very little room for any disappointment. Should they miss the high expectations that could lead to a significant market shake up. We can already see that nervousness within European markets today.”

While signs of a pickup in activity have fueled a stellar rally in U.S. stocks, the momentum of economic has slowed recently amid a resurgence in new infections, especially in southern and western U.S. states, leading to a pause in reopening plans. The S&P 500 is about 4% below its Feb. 19 record high after coming within 3% of that level last week. The backward looking GDP print is due at 8:30 a.m. ET when we will also get the Labor Department’s latest jobless claims data which is expected to show another ominous an uptick in newly fired workers.

On Wednesday, the Federal Reserve acknowledged the surge in COVID-19 cases is likely stalling economic recovery. The central bank also pledged to support the economy as long as necessary, lifting Wall Street’s three main indexes at the end of the session. Also dampening the mood was a deadlock in negotiations in the U.S. Congress over a pandemic relief plan, before a $600-per-week unemployment benefit lapses on Friday.

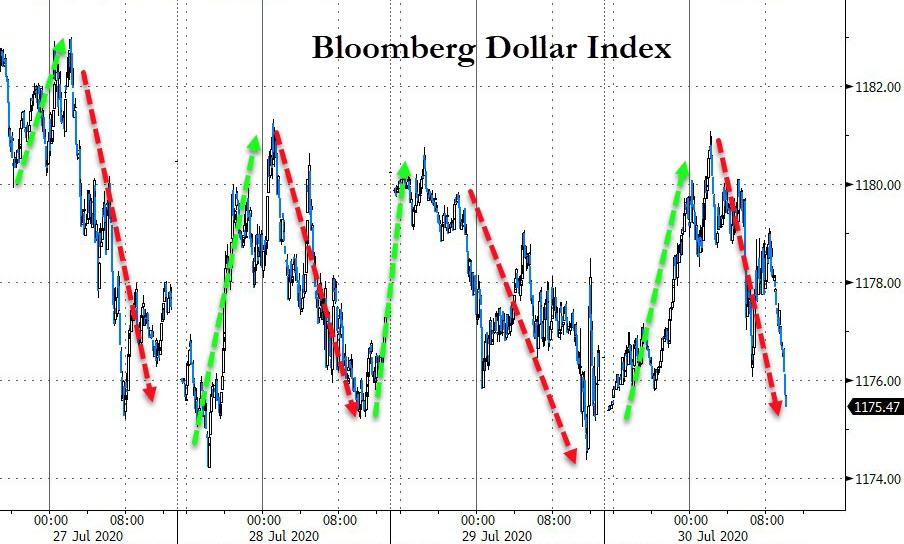

In FX, the dollar reversed Wednesday’s losses and climbed from the lowest since September 2018 as rising coronavirus cases worldwide supported demand for haven assets; the euro retreated against the dollar from the high it touched on Wednesday after news that Germany’s economy fell the most since records began in the second quarter. Investors sought refuge in the greenback after nations from Australia to Vietnam reported a fresh spike in infections and Federal Reserve Chair Jerome Powell warned of the most severe economic downturn “in our lifetime.”

Among the G-10, the Norwegian krone saw the biggest losses, making it this year’s worst performer; it was followed by the krona and kiwi, which also extended declines versus the Aussie as data showed a further drop in New Zealand’s consumer confidence. Sterling snapped a nine-day rally against the dollar, yet outperformed the euro.

The Australian dollar slipped as leveraged funds initiated short positions after Victoria state registered a record number of cases, according to a trader. The yen halted a five-day gain as traders weighed Japan’s tally of infections which rose to an all-time high.

“The virus story is shifting away from being just a U.S. story with now many hot spots around the globe,”said Rodrigo Catril, a currency strategist at National Australia Bank Ltd. “The dollar’s decline is starting to look stretched, particularly if more containment measures are reintroduced in other parts of the world”

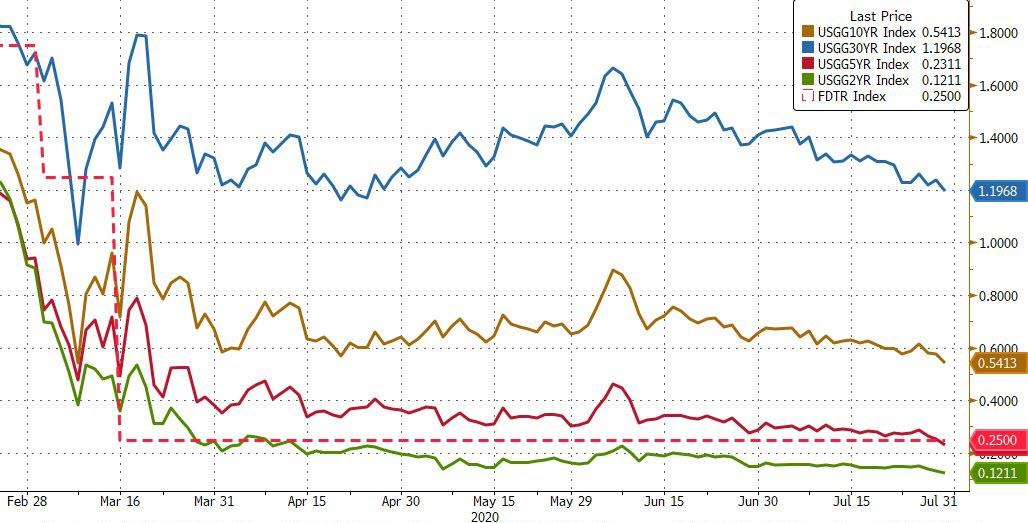

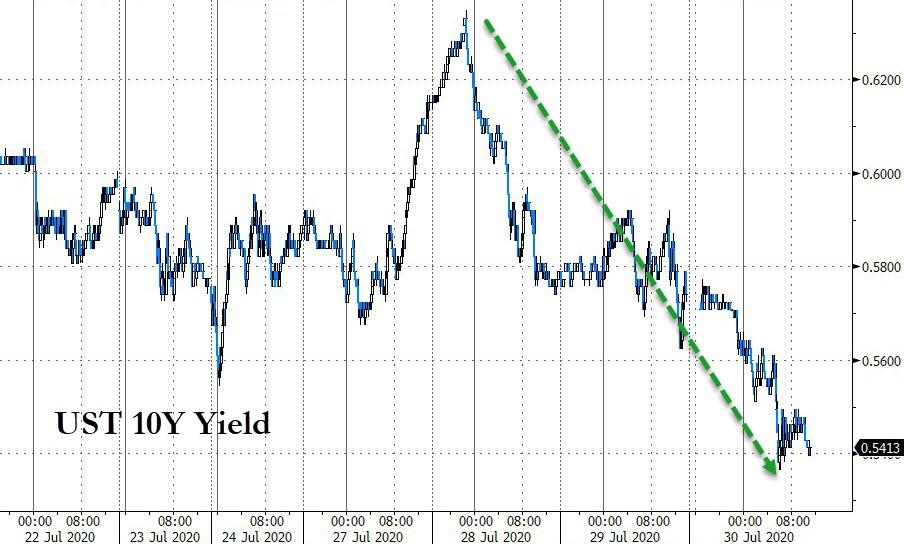

In rates, two-year Treasury yields are two basis points away from falling below the record set in May and the 5-year yield fell to a record low 0.2374%. The US Treasury curve bull-flattened, extending a move that followed Wednesday’s FOMC meeting and anticipating month-end index-extension flows Friday that may further support long end. U.S yields were lower by 1bp to 3bp across the curve with long-end- led gains flattening 2s10s by ~1bp, 5s30s by ~2bp; 10-year yields around 0.555%, richer by 2bp vs Wednesday’s close and within 2bp of its record low close on March 9. German bonds rallied on demand for the safety of sovereign debt, driving benchmark yields to a two-month low and widening the differential with Italian equivalents.

In commodities, gold fell for the first time in 10 days as the dollar rebounded.

Looking at the day ahead, the focus for data will be the advanced Q2 GDP reading for the US which is expected to show an annualized contraction of -34.5% qoq. Other data includes weekly jobless claims while in Europe we’ve got preliminary July CPI and Q2 GDP in Germany. As highlighted earlier, expect earnings to be a big focus with Alphabet, Amazon, Facebook and Apple reporting along with Nestle, P&G, Shell, MasterCard, Total, ABInBev and Volkswagen.

Market Snapshot

- S&P 500 futures down 0.9% to 3,222.50

- STOXX Europe 600 down 0.8% to 364.50

- German 10Y yield fell 2.7 bps to -0.525%

- Euro down 0.3% to $1.1754

- Italian 10Y yield fell 1.6 bps to 0.866%

- Spanish 10Y yield fell 1.6 bps to 0.332%

- Brent futures down 1.4% to $43.12/bbl

- Gold spot down 0.8% to $1,955.55

- U.S. Dollar Index up 0.2% to 93.61

- MXAP down 0.2% to 166.87

- MXAPJ down 0.01% to 553.40

- Nikkei down 0.3% to 22,339.23

- Topix down 0.6% to 1,539.47

- Hang Seng Index down 0.7% to 24,710.59

- Shanghai Composite down 0.2% to 3,286.82

- Sensex down 0.4% to 37,915.38

- Australia S&P/ASX 200 up 0.7% to 6,051.08

- Kospi up 0.2% to 2,267.01

Top Overnight News from Bloomberg

- Germany’s economy plunged into a record slump in the second quarter, when virus restrictions slammed businesses and households across Europe, destroying jobs and prompting an unprecedented policy response

- Germany also reported the highest number of new coronavirus cases in about six weeks. In the U.K., almost 10,000 people have been given an experimental Covid-19 vaccine, a key step toward finding a shot that will help control the pandemic

- Hong Kong’s government barred 12 pro-democracy activists including Joshua Wong from running in September elections

- The early signs are that bond investors agree with Federal Reserve Chairman Jerome Powell that the coronavirus still warrants extreme caution from policy makers

Asian equity markets were mostly kept afloat as the region took advantage of the post-FOMC tailwinds from Wall Street and as focus was centred on a deluge of earnings releases. ASX 200 (+0.7%) was led by outperformance in the tech sector and with mining names underpinned by Rio Tinto earnings. Nikkei 225 (-0.2%) also began positively although gains were later reversed amid recent currency strength and after Retail Sales Y/Y topped estimates but remained in contractionary territory. Furthermore, notable movers have been driven by corporate updates with Nomura Holdings the biggest gainer, while Isetan Mitsukoshi, TEPCO and Sumitomo Mitsui Financial Group are at the other side of the spectrum on dismal results. KOSPI (+0.3%) began the session on the front foot to print its best level since October 2018 after encouraging earnings from Samsung Electronics although some of the gains were later pared after shares of the tech and index behemoth stalled around the KRW 60,000 level. Elsewhere, Hang Seng (+1.1%) and Shanghai Comp. (+0.1%) were varied with indecision seen in the mainland following the prior day’s outperformance and after the PBoC opted for a neutral position in its latest liquidity operations. Finally, 10yr JGBs were subdued amid the flimsy sentiment in Tokyo and mostly weaker results at the 2yr JGB auction.

Top Asian News

- Herd Immunity May Be Developing in Mumbai’s Poorest Areas

- Thailand Sees 8.5% GDP Contraction as Virus Ravages Economy

- Hong Kong’s Dollar Peg Is ‘Unassailable’, StanChart CEO Says

European equities (Eurostoxx 50 -1.7%) trade lower across the board with selling pressure continuing to pick up throughout the session amid a backdrop of light macro newsflow and a particularly busy earnings slate. Despite selling pressure in equity index futures becoming more prominent throughout the session, equity-specific focus has largely been centred around individual pre-market earnings reports from a vast number of large-cap names from across the region. Sector-wise, auto names are a notable laggard amid earnings from Volkswagen (-5.7%) and Renault (-5.7%) with the former reporting a H1 loss of EUR 1.4bln (prev. profit of EUR 9.6bln) and the latter posting a EUR 7.4bln loss; Renault CEO noting that results have acted as a “disturbing wake up call”. For the banking sector, Lloyds (-7.4%) trade lower after posting a GBP 602mln loss (prev. profit of GBP 2.9bln), Standard Chartered (-3.6%) and BBVA (-7.9%) are also down on the day post-earnings, whilst some reprieve for the sector has been presented by Credit Suisse (+0.2) after the Co. posted a 24% increase in net income whilst also announcing some structural changes in its operations. Large-cap energy names Shell (-1.7%) and Total (+1.3%) have both come to market with Q2 earnings today in which the former posting a USD 16.8bln writedown on its assets and the latter managing to avoid entering the red after recording a net income figure of USD 126mln during the quarter. Elsewhere, AstraZeneca (+2.8%) are a notable outperformer after reporting an increase in H1 profits and revenues with performance boosted by new medicines with the Co. continuing to focus on developing a vaccine for COVID-19. Swiss heavyweight Nestle (+0.4%) are firmer this morning after H1 organic sales rose 2.8% vs. Exp. 2.3% despite the fallout from the pandemic. Airbus (+3.0%) are another outperformer post-earnings despite posting a H1 loss of EUR 1.9bln with the Co. vowing to stem its sizable cash outflows. AB InBev (+5.4%) sit near the top of the Stoxx 600 after Q2 sales figures exceeded expectations during the pandemic. To the downside, Casino (-15.8%) reside at the bottom of the Stoxx 600 after posting a drop in sales and trading profits

Top European News

- Euronext Rejects Shorter Hours After Some Investors Resist

- Lazard Banker Among Suspects in German Insider Trading Probe

- BBVA’s Miss in Mexico Overshadows Quick Return to Profit

- Casino Shares Collapse to 24-Year Low as 1H Seen as ‘A Disaster’

In FX, the Greenback continues to regroup after a knee-jerk slide in wake of the dovish/downbeat FOMC, as broad risk sentiment sours on heightened 2nd wave COVID-19 prompted by the latest daily updates showing increases in infections and deaths to new record levels in several cases. As such, the Buck has bounced across the board with the DXY pivoting 93.500 within 93.308-685 bounds compared to a low of 93.169 at one stage on Wednesday and now eyeing 2 top-tier US data points for near term direction (weekly initial claims and Q2 GDP) before remaining month end rebalancing kicks in.

- AUD/NZD/CAD/NOK – No big surprise that the high beta, cyclical and commodity currencies have been hit hardest by renewed aversion and the mini or partial US Dollar revival, as the Aussie also laments another rise in virus cases in Victoria and retreats further nigh on 0.7200 peaks towards 0.7125, while the Kiwi fails to glean any lasting traction from improvements in ANZ business sentiment or an even bigger rebound in the outlook, with 0.6600 more tangible than 0.6700 that seemed reachable at one stage. Similarly, the Loonie has reversed sharply from multi-week highs around 1.3330 to sub-1.3400 against the backdrop of waning crude prices and the Norwegian Krona is back below 10.7000 vs the Euro even though the latter has unwound gains elsewhere.

- EUR/SEK/CHF/JPY/GBP – All backing off amidst the downturn in risk appetite and Greenback recovery, with the single currency testing bids under 1.1750 having rallied just above 1.1800 late yesterday, but not quite far enough to probe the bottom end of a resistance zone stretching from 1.1815 to 1.1851 that includes a key Fib retracement (1.1822). However, the Swedish Crown has slipped through 10.3000 against the Euro in contrast to the Franc that is straddling 1.0750 and only handing back a portion of its gains vs the Buck between 0.9151-21 parameters in keeping with the safe-haven Yen that is holding a tight range either side of 105.00. Last, but not least, the Pound is actually confounding normal conventions, to a degree, and retaining sight of 1.3000, albeit capped ahead of Wednesday’s 1.3014 pinnacle and a chart hurdle just a few pips above (1.3018).

- EM – General depreciation on overall risk factors, but the Rand also losing ground with GOLD, Rouble alongside Brent, Lira on a lack of Turkish reserves to arrest the slide and Mexican Peso ahead of Q2 GDP that is expected to extend the recessionary run to 5 quarters and by record margins.