GOLD$: 1969.20 UP $17.90 The quote is London spot price (cash market)

Silver:$24.03// UP 82 CENTS London spot price ( cash market)

Closing access prices: London spot

i)Gold : $1973.00 LONDON SPOT 4:30 pm

ii)SILVER: $24.32//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUGUST GOLD: $1962.00 CLOSE 1::30 PM SPREAD SPOT/FUTURE AUG (BACKWARD $7.20)

OCT GOLD: $1976.10 CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: $6.90 ($ 0/90 ABOVE NORMAL CONTANGO)

DEC. GOLD $1988.30 CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $19.10 ($7.10 ABOVE NORMAL CONTANGO)

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $24.20…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : 17 CENTS PER OZ (14 CENTS ABOVE CONTANGO)

SILVER DECEMBER CLOSE: $24.44 1:30 PM SPREAD SPOT/FUTURE DEC. : 41 CENTS PER OZ ( 29 CENTS ABOVE NORMAL CONTANGO)

DONATE

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today: 11,205/32,732

ISSUED: 7913

EXCHANGE: COMEX

CONTRACT: AUGUST 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,942.300000000 USD

INTENT DATE: 07/30/2020 DELIVERY DATE: 08/03/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 1666 75

072 H GOLDMAN 6220

104 C MIZUHO 2656

132 C SG AMERICAS 412

135 H RAND 7

152 C DORMAN TRADING 49

159 C ED&F MAN CAP 25

167 C MAREX 300 1

226 C DIRECT ACCESS 7

323 H HSBC 1750

332 H STANDARD CHARTE 1026

355 C CREDIT SUISSE 176 228

363 H WELLS FARGO SEC 1062

365 C ED&F MAN CAPITA 3

435 H SCOTIA CAPITAL 800

555 H BNP PARIBAS SEC 6000

624 C BOFA SECURITIES 58

657 C MORGAN STANLEY 2 522

657 H MORGAN STANLEY 4962

661 C JP MORGAN 7913 7111

661 H JP MORGAN 4094

DLV615-T CME CLEARING

BUSINESS DATE: 07/30/2020 DAILY DELIVERY NOTICES RUN DATE: 07/30/2020

PRODUCT GROUP: METALS RUN TIME: 22:13:43

685 C RJ OBRIEN 140 8

686 C INTL FCSTONE 365 41

690 C ABN AMRO 60 950

700 C UBS 968

709 C BARCLAYS 3006

709 H BARCLAYS 71

730 C PTG DIVISION SG 10

732 C RBC CAP MARKETS 23

732 H RBC CAP MARKETS 2427

737 C ADVANTAGE 88

800 C MAREX SPEC 30 265

878 C PHILLIP CAPITAL 15

880 C CITIGROUP 162 111

880 H CITIGROUP 9400

905 C ADM 9 190

____________________________________________________________________________________________

TOTAL: 32,732 32,732

MONTH TO DATE: 32,732

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 32,732 NOTICE(S) FOR 3,273,200 OZ (101.810 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 32732 NOTICES FOR 3,273,200 OZ (101.810 TONNES)

SILVER

FOR AUGUST

475 NOTICE(S) FILED TODAY FOR 2,375,000 OZ/

total number of notices filed so far this month: 475 for 2.375 MILLION oz

BITCOIN MORNING QUOTE $11,146 UP 47

BITCOIN AFTERNOON QUOTE.: $11,409 UP 235

GLD AND SLV INVENTORIES:

WITH GOLD UP $17.90 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

NO CHANGES IN GOLD INVENTORY AT THE GLD///

GLD: 1,241.96 TONNES OF GOLD//

WITH SILVER UP 82 CENTS TODAY: AND WITH NO SILVER AROUND:

A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: SURPRISINGLY:

A WITHDRAWAL OF 3.26 MILLION OZ FROM THE SLV//

RESTING SLV INVENTORY TONIGHT:

SLV: 568.092 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A HUMONGOUS SIZED 3348 CONTRACTS FROM 184,392 UP TO 187,740, AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE HUGE SIZED GAIN IN OI OCCURRED DESPITE OUR $0.97 LOSS IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS PRIMARILY DUE TO HUGE BANKER SHORT COVERING PLUS A GOOD EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A HUGE SILVER STANDING AT THE COMEX FOR AUGUST. WE HAD A GOOD NET GAIN IN OUR TWO EXCHANGES OF 4467 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: SEP 1119 DEC: 0 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1119 CONTRACTS. WITH THE TRANSFER OF 1119 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1119 EFP CONTRACTS TRANSLATES INTO 11.075 MILLION OZ ACCOMPANYING:

1.THE 97 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

86.470 MILLION OZ FINAL STANDING IN JULY.

4.57 MILLION OZ INITIAL STANDING IN AUGUST

THURSDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL 97 CENTS ).. AND,OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS. THE HUGE GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A HUMONGOUS INITIAL STANDING OF SILVER OZ FOR AUGUST, STRONG BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A GOOD NET GAIN OF 4467 CONTRACTS OR 22.33 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

JULY

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF JULY:

26,790 CONTRACTS (FOR 22 TRADING DAY(S) TOTAL 26,790 CONTRACTS) OR 133.950 MILLION OZ: (AVERAGE PER DAY: 1217 CONTRACTS OR 6.088 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 133.95 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 19.13% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,271.365 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 133.95 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3348, DESPITE OUR 97 CENT LOSS IN SILVER PRICING AT THE COMEX ///THURSDAY… THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1119 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A VERY STRONG SIZED OI CONTRACTS ON THE TWO EXCHANGES: 4467 CONTRACTS (DESPITE OUR $0.97 CENT LOSS IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 1119 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A HUGE SIZED INCREASE OF 3348 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 97 CENT LOSS IN PRICE OF SILVER/AND A CLOSING PRICE OF $23.27 // THURSDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.9305 BILLION OZ TO BE EXACT or 132% of annual global silver production (ex Russia & ex China).

FOR THE NEW AUGUST DELIVERY MONTH/ THEY FILED AT THE COMEX: 475 NOTICE(S) FOR 2,375,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 86.470 million oz//AUGUST 4.57 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A CONSIDERABLE SIZED 12,846 CONTRACTS TO 586,484 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE CONSIDERABLE SIZED LOSS OF COMEX OI OCCURRED WITH OUR STRONG FALL IN PRICE OF $10.00 /// COMEX GOLD TRADING// THURSDAY// WE HAD HUGE BANKER SHORT COVERING, A HUMONGOUS SIZED GOLD TONNAGE STANDING AT THE COMEX FOR AUGUST, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE AND A VERY STRONG GOLD SPREADER LIQUIDATION. THIS ALL HAPPENED WITH OUR STRONG LOSS IN PRICE OF $10.00 .

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 58

WE LOST A STRONG SIZED 11,339 CONTRACTS (35.273 TONNES) ON OUR TWO EXCHANGES.

HOWEVER THE MAJORITY OF THE LOSS WAS DOMINATED BY THE LIQUIDATION OF THOSE SPREADERS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 1507 CONTRACTS:

CONTRACT .; AUG 220 AND OCT: 0 DEC: 1287; FEB: 0 ALL OTHER MONTHS ZERO//TOTAL: 1507. The NEW COMEX OI for the gold complex rests at 586,484. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,339 CONTRACTS: 12,846 CONTRACTS DECREASED AT THE COMEX AND 1507 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 11,339 CONTRACTS OR 35.27 TONNES. THURSDAY, WE HAD A LOSS OF $10.00 IN GOLD TRADING…...

AND WITH THAT LOSS IN PRICE, WE HAD A STRONG SIZED LOSS IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 35.27 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT FELL $10.00).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS ALSO UNSUCCESSFUL AS ALMOST ALL OF THE LOSS WAS DUE TO THE SPREADER LIQUIDATION. SPREADER LIQUIDATION WILL COME TO ITS CONCLUSION WITH MONDAY’S REPORT (FRIDAY’S OFFICIAL NUMBERS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1507) ACCOMPANYING THE HUGE SIZED LOSS IN COMEX OI (12,846 OI): TOTAL LOSS IN THE TWO EXCHANGES: 11,339 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)A MONSTROUS INITIAL GOLD TONNAGE STANDING AT THE GOLD COMEX FOR THE FRONT AUGUST MONTH, 3) ZERO LONG LIQUIDATION; 4) HUMONGOUS COMEX OI LOSS AND .5) SMALL EXCHANGE FOR PHYSICAL ISSUANCE 6) CONTINUAL STRONG GOLD SPREADER LIQUIDATION... AND …ALL OF THIS WAS COUPLED WITH OUR STRONG LOSS IN GOLD PRICE TRADING//THURSDAY//$10.00.

THE DOMINANT FACTOR IN THE LOSS OF OI AT THE COMEX WAS DUE TO THE SPREADING LIQUIDATION!!

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

SPREADING OPERATIONS/NOW SWITCHING TO GOLD

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN GOLD AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF AUGUST FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF JULY. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUGUST), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

JULY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 22 TRADING DAY(S) IN TONNES: 313.09 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 313.09/3550 x 100% TONNES =8.81% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3264.12 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 313.09 TONNES SO FAR..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

AUGUST TOTAL EFP ISSUANCE;

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A HUGE SIZED 3348 CONTRACTS FROM 184,392 UP TO 187,740 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE HUGE SIZED GAIN IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) HUGE BANKER SHORT COVERING , 2) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A HUMONGOUS STANDING AT THE SILVER COMEX FOR AUGUST IN AN NON ACTIVE MONTH, AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 1119 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT: 1119 AND DEC. 200 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1119 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3248 CONTRACTS TO THE 1119 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUGE GAIN OF 4467 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 22.33 MILLION OZ, OCCURRED DESPITE OUR 97 CENT LOSS IN PRICE///

NOBODY LEFT THE SILVER ARENA DESPITE THE HUGE WHACK IN PRICE!!

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 23.19 POINTS OR 0.71% //Hang Sang CLOSED DOWN 115.24 POINTS OR 0.47% /The Nikkei closed DOWN 629.23 POINTS OR 2.82%//Australia’s all ordinaires CLOSED DOWN 1.93%

/Chinese yuan (ONSHORE) closed UP at 6.9752 /Oil UP TO 40.30 dollars per barrel for WTI and 43.41 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 6.9752 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9834 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS PANDEMIC : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

i)we had 3 deposits into the customer account

into JPMorgan: nil oz

ii) Into Delaware: 4004.4 oz

iii) Into Scotia: 594,911.100 oz

iv) Into Brinks 20,409.900 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 163.098 million oz of total silver inventory or 48,99% of all official comex silver. (163.677 million/334.544 million

total customer deposits today: 619,325.402 oz

we had 2 withdrawals:

i)Out of CNT: 619,929.550 oz

ii) Out of Delaware: 34,704.666 oz

total withdrawals; 651,634.216 oz

We had 6 adjustments

dealer to customer account

i) Brinks: 867,703.219 oz

ii) CNT: 242,820.287 oz

iii) HSBC: 5119.170 oz

iv) Int Delaware: 4969.605 oz

v) JPMorgan: 34,850.700 o

vi) Manfra: 125,830.790 oz

adjusted totals; 1.28 million oz.

total dealer silver: 131.786 million

total dealer + customer silver: 334,508 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

the front month of August registered an open interest of 914 contracts.

Thus by definition the initial silver oz standing in this non active month of August is as follows:

914 oi x 5000 oz per contract = 4.575 million oz

After August we have the big September contract month and here we see a gain of 57 contracts up to 130,040.

The big December contract month saw its OI rise by 3573 contracts up to 48,192

The total number of notices filed today for the AUGUST 2020. contract month is represented by 475 contract(s) FOR 2,375,000, oz

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 475 x 5,000 oz = 2,375,000 oz to which we add the difference between the open interest for the front month of AUGUST.(914) and the number of notices served upon today 475 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the AUGUST/2019 contract month: 475 (notices served so far) x 5000 oz + OI for front month of AUGUST (914)- number of notices served upon today (475) x 5000 oz of silver standing for the AUGUST contract month.equals 4,570,000 oz. ..VERY STRONG FOR A NON ACTIVE MONTH.

TODAY’S ESTIMATED SILVER VOLUME : 143,921 CONTRACTS // volume huge+++/

FOR YESTERDAY: 175,595.,CONFIRMED VOLUME//volume huge++++++++/

YESTERDAY’S CONFIRMED VOLUME OF 175,595 CONTRACTS EQUATES to 0.715 billion OZ 102% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 3.20% ((JULY 31/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.95% to NAV: (JULY 31/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 3,20%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 19.97 TRADING 19.67///NEGATIVE 1.48

END

And now the Gold inventory at the GLD/

JULY 31/WITH GOLD UP $17.90 TODAY/WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241.96 TONNES.

JULY 30/WITH GOLD DOWN $10.00 TODAY, WE HAVE ANOTHER SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES//INVENTORY RESTS AT 1241.96 TONNES.

JULY 29//WITH GOLD UP $12.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 8.47 TONNES/INVENTORY RESTS AT 1243.12 TONNES

JULY 28///WITH GOLD UP $13.25 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 5.84 TONNES/INVENTORY RESTS AT 1234.65

JULY 27//WITH GOLD UP $35.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF XXX TONNES/INVENTORY RESTS AT 1228.81 TONNES

JULY 24/WITH GOLD UP $8.80 TODAY: WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.80 TONNES//INVENTORY RESTS AT 1228.81 TONNES

JULY 23/WITH GOLD UP $24.90 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 7.26 TONNES/INVENTORY RESTS AT 1225.01 TONNES

JULY 22/WITH GOLD UP $22.00 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 7.89 TONNES/INVENTORY RESTS AT 1219.75 TONNES

JULY 21//WITH GOLD UP $26.00 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.97 TONNES INTO THE GLD// INVENTORY RESTS AT 1211.86 TONNES

JULY 20/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1206.89 TONNES

JULY 17/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1206.89 TONNES

JULY 16/WITH GOLD DOWN $9.80 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: INVENTORY RESTS AT 1206.89 TONNES

JULY 15//WITH GOLD UP $1.55 TODAY/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 2.96 TONNES INTO THE GLD///INVENTORY RESTS AT 1206.89 TONNES

JULY 14//WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 3.51 TONNES/INVENTORY RESTS AT 1203.97 TONNES

JULY 13//WITH GOLD UP $12.50 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1200.46 TONNES

JULY 10/WITH GOLD DOWN $.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD//A STRANGE WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1200.82 TONNES

JULY 9//WITH GOLD DOWN $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OX 3.21 TONNES INTO THE GLD//INVENTORY RESTS AT 1202.57 TONNES

JULY 8/WITH GOLD UP $13.75 TODAY; A BIG CHANGE IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 7.89 TONNES INTO THE GLD//INVENTORY RESTS AT 1199.36 TONNES

JULY 7/WITH GOLD UP $12.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1191.47 TONNES

JULY 6/WITH GOLD UP $6.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1191.47 TONNES

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

JUNE 30//WITH GOLD UP $16.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1178.90 TONNES

JUNE 29/WITH GOLD UP $2.90 TODAY: A HUGE DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1178.90 TONNES

JUNE 26/WITH GOLD UP $5.03 TODAY: VERY STRANGE: A PAPER WITHDRAWAL OF 1.46 TONNES//INVENTORY RESTS AT 1175.39 TONNES

JUNE 25//WITH GOLD DOWN $3.30 TODAY//ANOTHER STRONG PAPER DEPOSIT OF 7.6 TONNES///INVENTORY RESTS AT 1176.85 TONNES

JUNE 24/WITH GOLD DOWN $1.50 TODAY; A STRONG 3.21 TONNES ADDED TO THE GLD//INVENTORY RESTS AT 1169.25 TONNES

JUNE 23/WITH GOLD UP $25.50 TODAY/ANOTHER CRIMINAL PAPER DEPOSIT OF 6.73 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1166.04 TONNES

JUNE 22/WITH GOLD UP $14.00 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 23.09 TONNES//INVENTORY RESTS AT 1159.31 TONNES

JUNE 19/WITH GOLD UP$16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//; INVENTORY RESTS AT 1136.22 TONNES

JUNE 18//WITH GOLD DOWN $2.75 TODAY: NO CHANGES IN GOLD INVENTORY: INVENTORY RESTS AT 1136.22 TONNES

JUNE 17/WITH GOLD DOWN $1.05: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1136.22 TONNES

JUNE 16//WITH GOLD UP $6.70 TODAY: NO CHANGES IN GOLD INVENTORY: /INVENTORY RESTS AT 1136.22 TONNES

JUNE 15/WITH GOLD DOWN ANOTHER $8.80 TODAY, NO CHANGES IN GOLD INVENTORY/INVENTORY RESTS AT 1136.22 TONNES

JUNE 12//WITH GOLD DOWN $1.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 1.17 TONNES AT THE GLD//INVENTORY RESTS AT 1136.22 TONNES

JUNE 11//WITH GOLD UP $16.80 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 6.55 TONNES AT THE GLD//INVENTORY RESTS AT 1135.05 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

JULY 31/ GLD INVENTORY 1241.96 tonnes*

LAST; 871 TRADING DAYS: +302.46 NET TONNES HAVE BEEN ADDED THE GLD

LAST 771 TRADING DAYS://+480.93 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JULY 31/WITH SILVER UP 82 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: SURPRISINGLY A HUGE WITHDRAWAL OF 3.26 MILLION OZ//INVENTORY RESTS AT 368.092 MILLION OZ//

JULY 30//WITH SILVER DOWN 97 CENTS TODAY: WE HAVE A SMALL CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 571.352 MILLION OZ//

JULY 29/WITH SILVER UP 7 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY//A DEPOSIT OF 5.984 MILLION OZ//INVENTORY RESTS AT 572.283 MILLION OZ//

JULY 28 WITH SILVER DOWN 14 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 7.52 MILLION OZ//INVENTORY RESTS AT 566.299 MILLION OZ//

JULY 27/WITH SILVER UP $2.67 TODAY, WE HAD NO CHANGES IN SILVER INVENTORY: A DEPOSIT OF XX MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ//

JULY 24/WITH SILVER DOWN $0.12 TODAY: NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 558.779 MILLION OZ/

JULY 23/WITH SILVER UP $.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A HUMONGOUS PAPER DEPOSIT OF 9.594 MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ///

JULY 22/WITH SILVER UP $1.54 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A HUMONGOUS PAPER DEPOSIT OF 7.218 MILLION OZ//INVENTORY RESTS AT 549.185 MILLION OZ/

JULY 21/WITH SILVER UP $1.38 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUMONGOUS PAPER DEPOSIT OF 15.368 MILLION OZ////INVENTORY RESTS AT 541.967 MILLION OZ//

JULY 20/WITH SILVER UP 40 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 3.819 MILLION OZ ‘ENTERED” THE SLV..INVENTORY RESTS AT 526.599 MILLION OZ/

JULY 17/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 1.583 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 522.780 MILLION OZ//

JULY 16//WITH SILVER DOWN 14 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ//INVENTORY RESTS AT 521.197 MILLION OZ..

JULY 15.WITH SILVER UP 21 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.956 MILLION OZ//INVENTORY RESTS AT 516.074 MILLION OZ//

JULY 14/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 514.118 MILLION OZ//

JULY 13//WITH SILVER UP 67 CENTS TODAY: A HUGE CHANGE IN SILVER: A WITHDRAWAL OF 1.677 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 514.118 MILLION OZ//

JULY 10/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 4.844 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.795 MILLION OZ

WHAT A FRAUD!!

JULY 9/WITH SILVER DOWN 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 8.198 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 510.951 MILLION OZ/

JULY 8/WITH SILVER UP 37 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.118 MILLION OZ FROM THE SLV//VERY SURPRISING.//INVENTORY RESTS AT 502.753 MILLION OZ//

JULY 7/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/INVENTORY RESTS AT 503.871 MILLION OZ///

JULY 6//WITH SILVER UP 24 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.863 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 503.871 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

JUNE 30/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 29/WITH SILVER DOWN ONE CENT TODAY: A TWO CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 466,000 OZ TO PAY FOR STORAGE FEES AND INSURANCE//// AND A LARGE DEPOSIT OF 1.212 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 26/WITH SILVER UP 6 CENTS TODAY: ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ RESTS AT 491.858 MILLION OZ//

JUNE 25/WITH SILVER UP 12 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 931,000 OZ INTO THE SLV////INVENTORY RESTS AT 491.858 MILLION OZ//

JUNE 24///WITH SILVER DOWN 31 CENTS// NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 490.927 MILLION OZ

JUNE 23//WITH SILVER UP 16 CENTS TODAY: A MONSTROUS CHANGE IN INVENTORY: A PAPER DEPOSIT OF 4.473 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 490.927 MILLION OZ//

JUNE 22/WITH SILVER UP 15 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/: INVENTORY/INVENTORY RESTS AT 486/454 MILLION OZ//

JUNE 19//WITH SILVER UP 22 CENTS TODAY: STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 839,000 OZ FROM THE SLV////INVENTORY RESTS AT 486,454 MILLION OZ..

JUNE 18/WITH SILVER DOWN 16 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 932,000 OZ INTO THE SLV////INVENTORY RESTS AT 487.293 MILLION OZ

JUNE 17/WITH SILVER UP 8 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.261 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.361 MILLION OZ

JUNE 16//WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.118 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 483.100 MILLION OZ//

JUNE 15/WITH SILVER DOWN 14 CENTS NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 481.982 MILLION OZ///

JUNE 12/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: TWO DEPOSITS OF 7.269 MILLION OZ AND 1.802 MILLION OZ ADDED TO THE SLV///INVENTORY RESTS THIS WEEKEND AT 481.982 MILLION OZ//

JUNE 11//WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY: ///INVENTORY RESTS AT 472.89 MILLION OZ//

JULY 31.2020:

SLV INVENTORY RESTS TONIGHT AT

568.092 MILLION OZ.

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Short Term Weakness Likely Prior To A “Massive Short Squeeze Propels” Gold and Silver “To Much Higher Levels” – GoldCore

From MarketWatch:

Gold prices ended lower Thursday, with bullion retreating from a record rally that had seen the precious metal notch nine consecutive days of gains.

The precious metal found support Wednesday following the Federal Reserve signaling it planned to keep the low interest rate environment in place for the foreseeable future as the U.S. economy recovers from COVID-19. Benchmark federal-funds futures rates stand at a range between 0% and 0.25%.

However, some analysts make the case that gold prices may be entering a period of consolidation following a historic run-up that has been at least partly prompted by the public-health crisis, but also exacerbated by a recent bout of weakness in the U.S. dollar and the low yields being offered by government debt.

One measure of the dollar, the ICE U.S. Dollar Index is hanging around its lowest level in two years and the yield for the 10-year Treasury note is around 0.55%.

As expected and forecast, gold has reached record highs near $2,000 an ounce and silver reached multi-year highs near $26 an ounce, but prices were “due a sharp correction,” said Mark O’Byrne, research director at GoldCore, based in Dublin.

“Short-term weakness is very likely prior to a massive short squeeze that propels the precious metals to much higher levels,” he told MarketWatch Thursday. Gold is “quite likely” to climb to $3,000 in the next 12 months, and silver could rise to between $50 and $100.

“Focus on value and not price—it is important investors focus on gold and silver’s value as hedging and safe haven assets rather than their nominal price highs in dollars,” said O’Byrne.

Full article via Marketwatch here

NEWS and COMMENTARY

Gold prices decline, on track for first loss in 10 sessions – GoldCore in Marketwatch

Blow for pension savers as bank imposes charges on holding cash (Irish Indepedent)

Oil down nearly 4% as virus surge weighs on demand outlook – Reuters

Wall St. falls after grim data; Trump suggests election delay – Reuters

The Other Reason Silver Is Soaring: Disruptions in Latin America – Bloomberg

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

30-Jul-20 1952.20 1957.65, 1503.00 1502.10 & 1662.30 1662.44

29-Jul-20 1954.35 1950.90, 1506.80 1502.39 & 1663.54 1659.24

28-Jul-20 1931.65 1940.90, 1499.15 1501.48 & 1647.70 1654.23

27-Jul-20 1940.55 1936.65, 1511.30 1504.78 & 1659.56 1647.70

24-Jul-20 1893.85 1902.10, 1486.67 1490.30 & 1631.55 1638.09

23-Jul-20 1882.35 1878.30, 1480.28 1477.47 & 1624.47 1621.54

22-Jul-20 1851.00 1852.40, 1462.85 1456.91 & 1604.82 1598.44

21-Jul-20 1823.20 1842.55, 1436.86 1449.35 & 1594.21 1608.36

20-Jul-20 1810.30 1815.65, 1437.92 1438.18 & 1580.21 1590.87

17-Jul-20 1802.90 1807.35, 1435.47 1442.45 & 1578.98 1581.07

16-Jul-20 1804.60 1807.70, 1438.09 1436.04 & 1583.72 1581.56

15-Jul-20 1809.30 1804.60, 1436.22 1441.31 & 1582.96 1579.57

14-Jul-20 1798.20 1801.90, 1436.58 1440.62 & 1583.14 1581.71

Own gold coins and bars in the safest vaults in Zurich, Switzerland with GoldCore. Learn why Switzerland remains a safe haven jurisdiction for owning precious metals. Access Our Most Popular Guide, the Essential Guide to Storing Gold in Switzerland here

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here

ii) Important gold commentaries courtesy of GATA/Chris Powell

Gold rally is being fueled by unlikely buyers :pension funds, insurance companies, and private wealth specialists

(Bloomberg/GATA)

Gold’s record rally fueled by unlikely buyers

Submitted by cpowell on Thu, 2020-07-30 14:42. Section: Daily Dispatches

By Ranjeetha Pakiam, Jack Farchy, and Anchalee Worrachate

Bloomberg News

Wednesday, July 29, 2020

Gold’s surge to an all-time high is winning over a wider fan base of pension funds, insurance companies, and private wealth specialists.

Managers who run long-term portfolios worth trillions of dollars are taking interest in gold as they search for returns in a yield-starved investing landscape. The broader array of buyers is one of the key dynamics behind the rally to $2,000 an ounce, even as gold’s traditional customers in India and China remain on the sidelines.

In the past, when bonds offered heftier yields, many professional investors had little use for gold. A broad portfolio of stocks and bonds could generate a reliable yield, and the two assets would balance each other out during market downdrafts. Gold, which offers no income, is hard to value and costs money to keep in storage.

But now, the math has shifted. With $15 trillion in debt offering negative yields and the Federal Reserve likely holding rates near zero for the foreseeable future, some on Wall Street are questioning the wisdom of owning bonds and looking elsewhere for assets to hedge against equity volatility. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2020-07-29/from-pensions-to-priv…

* * *

END

A must see interview of Chris Powell by Mr Meir Bank:

Chris gives a thorough analysis of how GATA came to be and the history of gold/silver suppression for the past 20 years

(ChrisPowell/GATA/Meir Bank)

GATA secretary interviewed comprehensively by Meir Bank

Submitted by cpowell on Thu, 2020-07-30 16:58. Section: Daily Dispatches

12:55p ET Thursday, July 30, 2020

Dear Friend of GATA and Gold:

Gold market observer Meir Bank last week interviewed your secretary/treasurer comprehensively for an hour, asking many good questions about GATA’s founding and purposes, gold price suppression history and policy, and the prospects for the monetary metals. The interview can be seen at YouTube here:

https://www.youtube.com/watch?v=IQC84S9JSnY

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

iii) Other physical stories:

What Is Gold Telling Us?

While the trade-weighted dollar has only just begun to breakdown…

Gold has been signaling something very different in the ‘currency’ markets for a few years now, and its recently accelerated dramatically…

So what is that message?

FFTT’s Luke Gromen laid out in a few short tweets his take on what is being priced in (by some assets)…

1/ Let’s pretend the currency system is a human body.

The US says it wants to de-couple from China; 20 yrs ago, we could’ve de-coupled & it would’ve been like amputating a finger or a hand.

2/ Even 10-15 years ago, perhaps “de-coupling from China” would’ve been like amputating an arm, or a leg from our currency system.

However, after 20+ years of $200-400B surpluses (USD exports), & China’s (generally) savvy reinvesting of those USD exports…

3/ “De-coupling from China” is no longer amputating an arm or a leg off the currency system; it is like cutting out some critical organ like heart, the lungs, or the liver out of the currency system…

4/ Yes, we can do it, & it’s probably the right thing to do, but the cold, hard math of the situation is that “US de-coupling from China” means the currency system as we have known it for 50+ yrs will die on the table, shortly after the critical organs are removed,

UNLESS…

Guess what that is? Yup, you guessed it…

6/ This is a take on gold as we have been looking at it for our clients at FFTT for some time.

Schiff: “The Dollar Is Not Just Going Down; It’s Going To Crash”

As gold was closing in on its all-time record price last week, Peter Schiff appeared on the Claman Countdown and warned about the looming dollar crisis.

Claman set up the interview pointing out that Peter predicted this big move up in gold months ago and asked, “What’s your new prediction about the dollar?”

Peter said it’s not really a new prediction, but perhaps it’s more timely.

The dollar’s not just going down. It is going to crash.”

Prior to the interview, Claman mentioned that the Dow was up, but Peter said there is another way to look at it.

Priced in real money, gold and silver, the Dow is actually down. And what gold is telling you, and silver, is that the dollar is losing value. It’s losing purchasing power.”

The dollar had been drifting lower against other fiat currencies over the past several weeks. At the time of the interview, the dollar index was just a few ticks off its March low.

But I think the dollar is going to keep drifting down until it collapses,” Peter said. “And this is going to usher in a real economic crisis in America, unlike something we’ve ever seen. Because it’s going to force the Fed to choose between saving the dollar, and dumping all the bonds its been buying, letting interest rates rise sharply, forcing the US government to slash spending right now and abandon all these stimulus plans, or just let inflation ravage the entire economy and wipe out a generation of Americans.”

Claman asked Peter what is the trade given what’s coming down the pike. Peter said his advice is “to get out of Dodge.”

Get out of dollars. Number one, yeah, own gold and silver. The gold and silver mining stocks are killing it, but they’re just getting started. I mean, these stocks, I think, can go up 10, 20 times in dollar terms.”

Peter also recommended foreign stocks that derive their revenues outside the US and earn them in foreign currencies, not US dollars. They can return those appreciated foreign currencies to you in dividends that avoid the inflation tax.

Forget about the payroll tax. The real tax that’s going to clobber every American is inflation because that’s how the government is now funding its spending is through inflation. And inflation is a tax on anybody who owns US dollars.”

END

J Johnson…

The Resolutes Are Scaring The S**t Out Of The Shorts!

Great and Wonderful Friday Morning Folks,

We start the last day of July off in the positive with December Gold up $25.10 with the trade at $1,991.90, after it made another New Life of Contract High at $2,005.40 with the low at $1,971.40. Silver is leading the rise today with the September contract now at $24.215, up 84.9 cents after hitting $24.53 with the low wayyy down there at $23.67. It’s been over 40 years since Silver made a N-LoCH, maybe it’s time for it to catch up, stay tooned! The US Dollar did get a little jiggy during the FOMC, with the trade now heading lower at 92.94, down 6.9 points and close to the high at 92.965 after it recovered from the low at 92.51. Of course, all this happened before 5 am pst, the Comex open, the London close, and after Ghislaine Maxwell’s unsealed court records were released.

The precious metals gains are also rolling along against the emerging fiats, as the Venezuelan Bolivar will prove Gold gaining 222.72 overnight with the last trade at 19,894.10 Bolivar. Silver under the same currency is now at 244.444 Bolivar, providing the holder at 10.294 Bolivar gain per ounce. Argentina’s Peso now has Gold’s value pegged at 143,813.65, a gain of 1,746.20 A-Peso’s with Silver at 1,767.18 giving the most manipulated metal in the markets a 76.09 A-Peso gain. Turkey’s Lira has given Gold a 152 T-Lira gain with the last trade at 13,886.11 with Silver gaining 7.12 with the last trade at 170.606 T-Lira.

August Silver Delivery Demands have officially begun, with the demand count now at 914 fully paid for contracts and with a trading range for the 3 lot Volume, between $23.59 and $23.565 with the last trade at the low. We need to leave some room for the unaware trader, he/she/they may have one or two positions to clear, but all in all we have a $107,692,050 order now standing for delivery. If the deliveries are as strong as the last several months, there’s gonna be a big problem at the Comex! Silver’s Overall Open Interest is now calculated at 187,817 Overnighters, more than doubling yesterday’s reductions, which may prove the FOMC meeting was simply a 2-day stall, as 3,931 more shorts had to be added into the markets.

August Gold has to be scaring the shit out of the shorts with the Resolutes Delivery Demand count at 47,236 and with a Volume of 1,100 already up on the board with a trading range between $1,981.10 and $1,948 with the last swap at $1,965.90, up $23.90. Let’s see how the rest of Augusts deliveries go, as the first day’s buy orders equal $9,286,124,240. Gold’s Overall Open Interest is proving someone is getting out of the way of the next rally with the Overall count dropping 12,524 leaving 587,560 contracts to go against the physicals.

I have no kind words for what we all have been forced to deal with over the decades as one who represented us as a leader, got continual protection from the Deep State. This one raped many women (and paid to shut them up) and (is accused of having sex with) young girls over his professional years as a government elected. A party was even willing to allow his wife to represent our nation too, and chose to ignore all the wiener laptop evidence and the death of Seth Rich! This same group also attacked anyone who accused both Clintons of wrong doing and that body count of the dead from way back when he represented Arkansas going forward, needs to be reviewed without the FBI/CIA/NSA interferences. All those involved with the Entire Pedo Machine need to be brought into court to answer questions. That is, if they survive their assisted suicides. I believe the promise, that has to be one of the hardest promises any president has ever attempted to do! Root out pedophilia and child trafficking rings, no matter who gets caught or the costs, and that includes the Republican Party!

The future promises to bring out many more stories that link this Pedo-Protect-Group to many others, not only in our country’s government, but many other countries as well! This revelation is either going to be swept under the rug by a bigger story, or it’s going to come out in full blossom. I don’t expect the media to reveal any of these stories because they too are all caught up in the mess with the Weinstein links, however, I do expect the court cases will reveal it all! Need we say, the best place to have one’s retirement while all this comes out, is still Physical Silver and Gold? Probably not, so have a great weekend, keep a smile on your face and a prayer for all, and as always…

Stay Strong!

Jeremiah Johnson

end

Friday was the largest first day notice filing for gold in its history: 102 tonnes

(Farchy/London’s Financial Times)

Gold Traders Issue Largest Delivery Notice on Record at Comex

Jack Farchy and Phoebe Sedgman, Bloomberg News

Gold of various weights and sizes sit at Gold Investments Ltd. bullion dealers in this arranged photograph in London, U.K., on Wednesday, July 29, 2020. Gold held its ground after a record-setting rally as investors awaited the outcome of a Federal Reserve meeting amid expectations policy makers will remain dovish, potentially spurring more gains.

(Bloomberg) — Traders on the main gold futures exchange in New York have issued the largest daily delivery notice on record.

In the latest sign of how the market’s norms have been upended by the price disconnect that struck in March, traders on Thursday declared their intent to deliver 3.27 million ounces of gold against the August Comex contract, the largest daily notice in bourse data going back to 1994.

While millions of ounces of gold trade on the futures market every day, typically only a tiny fraction of that goes to delivery. But in recent months, huge amounts of bullion have flowed into New York and the Comex has seen record deliveries.

That’s the result of a disconnect between prices in the two main markets, London and New York, that began in March as lockdowns grounded flights and shuttered refineries.

Futures, which typically trade in lockstep with the London spot price, soared to a premium of as much as $70 an ounce. Since then, that premium has been smaller, but there have been regular flare-outs.

In response, arbitragers have shipped precious metals to New York to capture the price differential — and the result has been much larger than normal deliveries against Comex futures.

©2020 Bloomberg L.P.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

“It’s Shocking No Matter How You Look At It” – Futures Jump On Blockbuster Tech Earnings; Gold Hits New Record High

S&P futures rose (but faded much of their earlier gains) alongside European shares with Nasdaq futures jumping nearly 1% as stellar earnings from US tech giants lifted sentiment amid dismal economic data and a resurgent virus. Gold climbed to a record even as the dollar rebounded from two year lows.

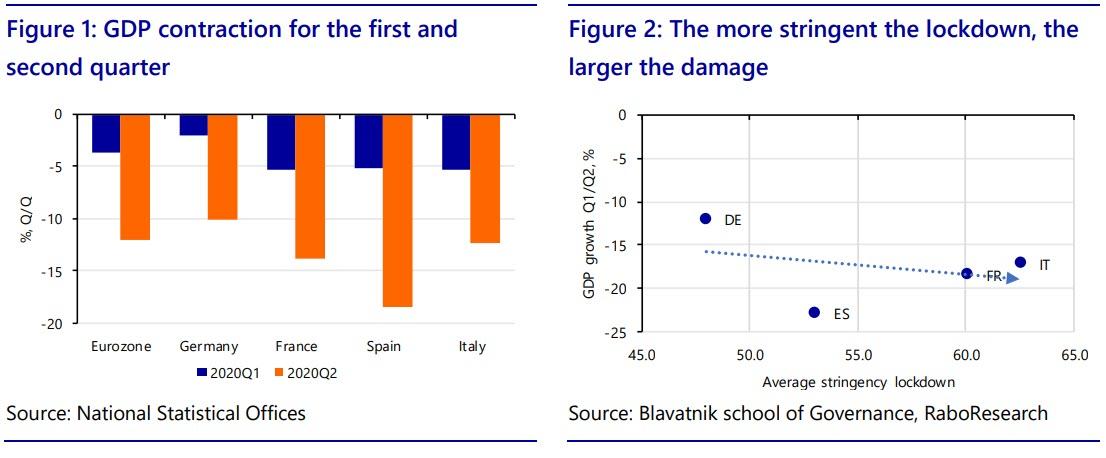

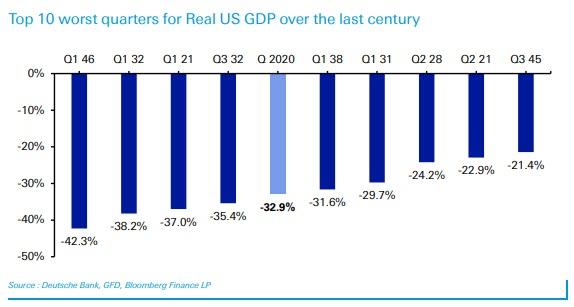

The Tech Tsunami helped lifted European shares, with the Stoxx Europe 600 Index rising, even after France and Spain posted record economic contractions. Nokia Oyj soared after earnings beat estimates, while BNP Paribas SA jumped on a blowout performance in fixed-income trading. Following the dismal US GDP print, the Euro Area reported that in Q2, its GDP contracted sharply by 12.1%qoq, in line with expectations, and corresponding to by far the sharpest decline in quarterly GDP growth since records began in 1995. French and Italian GDP both contracted by less than expected—by -13.8% and -12.4%, respectively—whereas Spanish GDP contracted most sharply (-18.5%) across the Euro area countries that have so far reported Q2 GDP. The unprecedented contractions in GDP were primarily attributable to weak domestic demand in both France and Spain, with a comparatively smaller drag from net trade as both exports and imports collapsed. The weakness was broad-based across sectors, with industry and services both registering record quarterly declines.

Asian stocks fell, led by industrials and energy, after falling in the last session. Most markets in the region were down, with Japan’s Topix Index dropping 2.8% and Australia’s S&P/ASX 200 falling 2%, while Shanghai Composite gained 0.7% on widespread retail buying as margin debt increased once again. The Topix declined 2.8%, with SoldOut and DTS falling the most. The Shanghai Composite Index rose 0.7%, with Xi’an Bright Laser and Anji Micro posting the biggest advances.

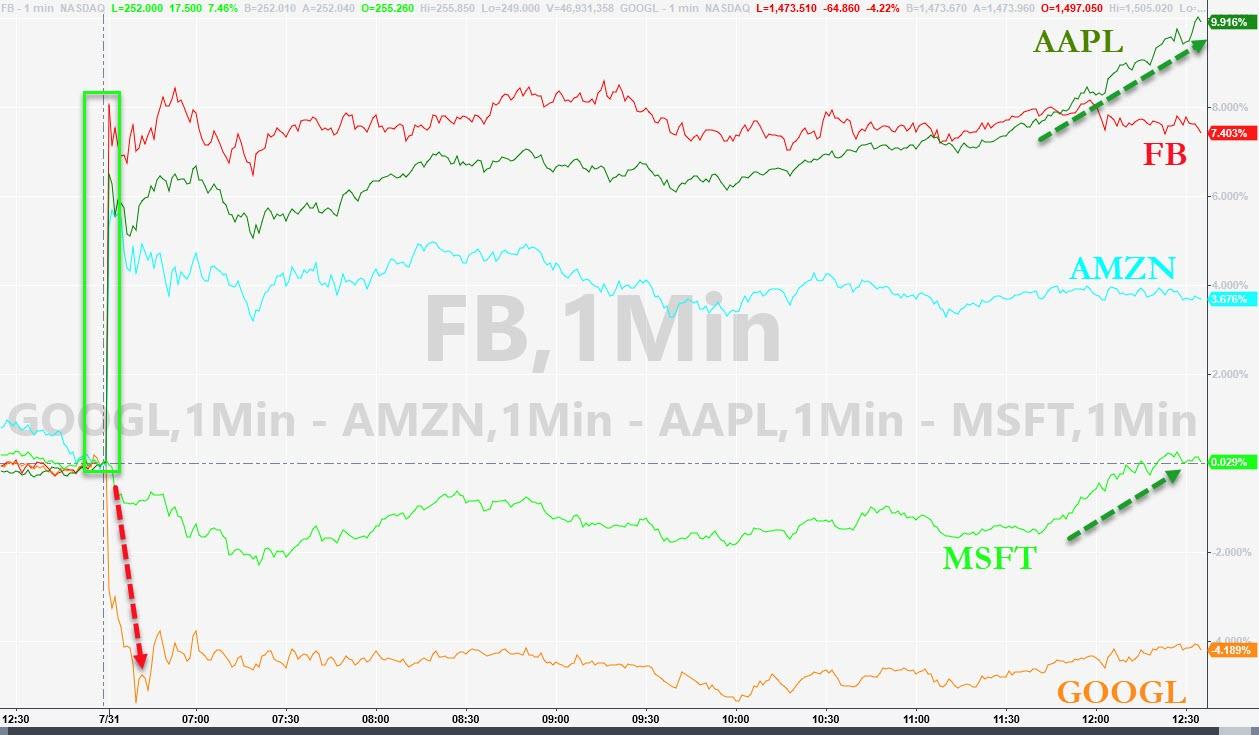

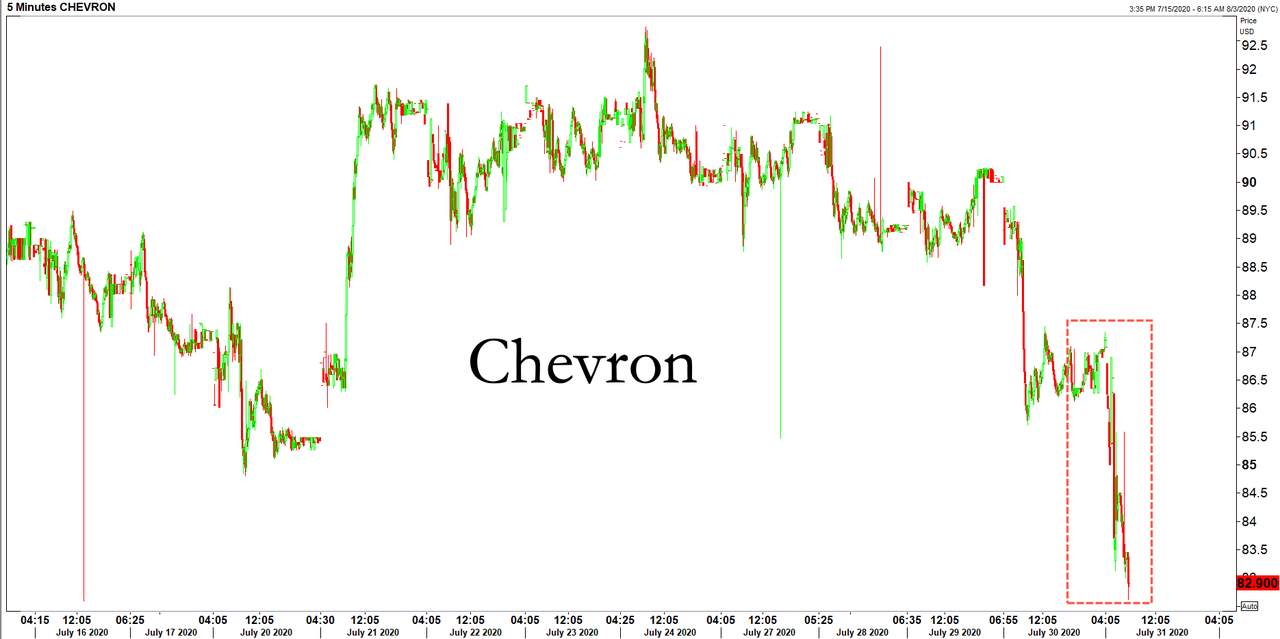

Apple surged 6% in premarket trading, setting the stock on course to open at a record high, as it delivered year-on-year revenue gains across every category and in every geography. Amazon.com also jumped 5.4% after posting the biggest profit in its 26-year history, while Facebook gained 6% as it reported better-than-expected revenue. Trading in Alphabet was more subdued as quarterly sales fell for the first time in its 16 years as a public company (for a response to tech earnings from some Wall Street analysts see here). Elsewhere, Ford rose 2.7% after signaling ample cash-on-hand for the year even as it forecast a full-year loss. Gilead Sciences fell 3.5% as it posted worse-than-expected quarterly results, hurt by weak sales of its hepatitis C drugs and flagship HIV treatments. Caterpillar Inc. gained after reporting higher-than-expected profit. Bucking the trend, U.S. oil giant Chevron Corp. posted its worst quarterly loss in at least three decades, sending the shares lower.

“It’s shocking no matter how you look at it,” said Randy Frederick, vice president of trading and derivatives for Schwab Center for Financial Research.

“The virus is getting worse in a lot of areas, and some places have started to shut back down again. If you look at earnings in terms of beat rates, the results have actually been pretty good, granted the expectations bar has been set very low.”

A surge in the stock price of the four companies, which make up nearly a fifth of the S&P 500’s value, as well as aggressive fiscal and monetary stimulus have sent the tech-heavy Nasdaq to record highs and set the S&P 500 on course for its fourth straight monthly gain. The S&P is now about 4% shy of its February all-time high, but faltering macroeconomic data and rising COVID-19 cases are making investors cautious again.

The GDP number on Thursday confirmed the sharpest contraction in the US economy since the Great Depression, while rising jobless weekly claims suggested a nascent recovery in the labor market was stalling. Investors betting on more U.S. government stimulus, before an extra $600-per-week federal jobless benefit expires on Friday, have also been disappointed as the Senate adjourned for the weekend and will return on Monday.

In FX, a gauge of the dollar’s strength weakened to its lowest since May 2018, heading for its sixth week of losses, before rebounding sharply as the EUR slumped. The pound advanced against the dollar, while the euro trimmed its gains following data showing an unprecedented euro-area slump. The two currencies are heading for their best monthly performance for a decade.

The Aussie dollar declined against the greenback as a risk-off mood persisted on reports of surges of the virus across the world, including Australia’s Melbourne.

In rates, Treasuries bull flattened as yields ticked lower, outperforming German bunds; the two-year yield hovered near May’s record low. The 10-year TSY dropped as low as 0.519%, supported by month-end flows. Yields were lower by 0.5bp to 2bp across the curve with long-end-led gains flattening 2s10s, 5s30s by ~0.5bp; 10-year at 0.535% has breached the 0.54% level where convexity trigger is thought to lie and is also its record low closing level on March 9 Bunds, gilts trade broadly in line with Treasuries; S&P 500 E-minis have pared an 0.8% gain to 0.3% with Euro Stoxx 50 higher by 0.6%.

China’s 10-year government bond yield rose after official data showed manufacturing activity expanded at a faster rate this month, suggesting the country’s economic recovery has gained momentum to start the year’s second half. The yield on 10Y Chinese bonds rose 4bps to 2.98% and is on pace to climb 12 basis points for July, the third straight monthly gain. The official manufacturing purchasing managers’ index rose to 51.1 in July from 50.9 a month earlier, as government-led investment gained traction and global demand recovered. Economists have revised up their forecasts for full-year growth, and now see China’s economy expanding 2% this year. Building strength could further reduce the prospects of more monetary easing and add downward pressure on China’s bonds.

In commodities, WTI and Brent have been rangebound throughout the morning as sentiment more broadly remains modestly elevated, while Gold futures stormed back to its all time high just shy of $2,000.

Looking ahead, on the economic front, core personal consumption expenditures data due at 830am, the Fed’s preferred measure of inflation, is likely to have edged higher by 0.2% in June.

Market Snapshot

- S&P 500 futures up 0.3% to 3,257.00

- STOXX Europe 600 up 0.7% to 362.11

- MXAP down 1% to 165.19

- MXAPJ down 0.3% to 551.51

- Nikkei down 2.8% to 21,710.00

- Topix down 2.8% to 1,496.06

- Hang Seng Index down 0.5% to 24,595.35

- Shanghai Composite up 0.7% to 3,310.01

- Sensex down 0.3% to 37,628.16

- Australia S&P/ASX 200 down 2% to 5,927.78

- Kospi down 0.8% to 2,249.37

- German 10Y yield fell 0.7 bps to -0.549%

- Euro up 0.2% to $1.1866

- Brent Futures up 0.8% to $43.26/bbl

- Italian 10Y yield fell 2.1 bps to 0.845%

- Spanish 10Y yield fell 0.8 bps to 0.309%

- Brent Futures up 0.8% to $43.26/bbl

- Gold spot up 1% to $1,975.84

- U.S. Dollar Index down 0.2% to 92.82

Top Overnight News from Bloomberg

- The euro-area economy plunged into an unprecedented slump in the second quarter, putting it in a deep hole from which it may take years to fully recover. Spain took the biggest hit in the period, shrinking 18.5%, while French and Italian output also dropped by double digits

- Gold rose to another record high on Friday, setting it on track for its strongest monthly performance in eight years, fueled by a weaker dollar and low interest rates

- An uptick in virus infections are stoking fears of a resurgence in Europe, with Spain seeing particularly high numbers of new cases and the British government re-imposing lockdown measures in part of the U.K. New York City has kept its Covid-19 infection rates low, but the risk of a resurgence looms over the Big Apple as fall approaches

- The Senate left Washington for the weekend after a fourth day of negotiations yielded little substantial progress on narrowing differences between Republicans and Democrats on a plan to bolster the coronavirus- ravaged U.S. economy

- The largest U.S. technology companies are thriving in a pandemic that has increased dependence on their products and services, while hammering much of the rest of the economy

Asian equity markets traded lacklustre heading into month-end after somewhat mixed Chinese PMI data with the region failing to take advantage of the momentum from US, where futures were boosted after-hours following big tech earnings in which Apple, Alphabet, Amazon and Facebook all beat on top and bottom lines. ASX 200 (-2.0%) was dragged lower by underperformance in the commodity related sectors and with the top-weighted financials also heavily pressured, while there were reports that Australian PM Morrison recently held emergency discussions with the Victoria state Premier which included possible further restrictions for movement within Melbourne and a shutdown of non-essential businesses. Nikkei 225 (-2.8%) was hampered by unfavourable currency flows and although Industrial Production data beat expectations for June, quarterly output was at a decline of 16.7% which was the largest drop according to comparable data since 2015. Furthermore, the biggest movers were driven by earnings including Panasonic, while SoftBank shares also suffered due to the currency effects despite a share repurchase announcement of up to 12.3% of shares for JPY 1tln. Hang Seng (-0.5%) and Shanghai Comp. (+0.7%) were both initially positive with outperformance in the mainland after the PBoC’s liquidity efforts resulted to a net weekly injection of CNY 120bln, although this eventually faded following the latest mixed data releases in which Chinese Official Manufacturing PMI topped estimates but Non-Manufacturing PMI missed and Composite PMI slowed although all figures remained in expansionary territory. Finally, 10yr JGBs eked mild gains amid the soured risk appetite in the region and with the BoJ present in the market for JPY 450bln of JGBs predominantly concentrated in the belly of the curve.

Top Asian News

- Japan Factory Production Rises for First Time in Five Months

- China Stocks Will Only Get Wilder After July Whipsaws Investors

- Facebook, Google Told They Must Pay Australia Media For News

European equities (Eurostoxx 50 +0.6%) trade modestly firmer across the board in what has been another busy morning of corporate updates whilst incremental macro newsflow remains relatively light since yesterday’s close. Although stocks are attempting to recoup some of yesterday’s heavy losses, the extent of the recovery is relatively mild with the Eurostoxx still lower by some 2.5% on the week heading into month-end. Some of the positivity in Europe is a by-product of the fallout from US mega-cap stocks earnings’ in which Apple, Alphabet, Amazon and Facebook all beat on top and bottom lines and were seen higher in after-market trade, prompting outperformance in Nasdaq 100 futures and the tech sector in Europe this morning. Also supporting the tech sector in Europe today is Nokia (+12.2%) post-earnings in which the Co. raised its guidance. Banking names have posted a strong performance in Europe following earnings from BNP Paribas (+2.1%) and Natwest Group (+1.1%), although gains for the sector have been capped by performance in the periphery following disappointing earnings from Spanish-listed Caixabank (-2.6%) and Sabadell (-2.0%). Elsewhere, travel & leisure names have been unable to join in on the mild positivity seen in Europe this far following earnings IAG (-9.1%) in which the Co. announced a EUR 1.37bln operating loss and proposed a capital increase of EUR 2.75bln; easyJet (-3.0%), Ryanair (-3.2%) and Deutsche Lufthansa (-2.2%) are seen lower in sympathy. Performance for telecom names has been hampered by BT (-3.4%) with the Co. warning over the impact of coronavirus on its revenues and earnings after posting a decline in profits. Looking ahead, asides from US participants continuing to digest the latest updates from Apple, Alphabet, Amazon and Facebook, focus will also be on pre-market updates from Exxon, Chevron, Phillips 66, Caterpillar, Merck and Colgate.

Top European News

- NatWest Adds $2.8 Billion Provision for Pandemic Loan Losses

- He Built It But No One Came: China Chills the Next Canary Wharf

- Fortiana Buys Out Abramovich in Bid for Russian Gold Miner

- Spanish-Led Outbreaks Fuel Concerns About Further Economic Pain

In FX, it seemed to start with a tweet, but Dollar losses accumulated after Thursday’s plunge in Q2 GDP and IJC data into the NY close and as APAC participants entered the fray for their final trading day of July to push the index further below 93.000 where it remains. The latest rise in unemployment benefit claims is especially worrying as Congress remains at odds over the next fiscal support package that looks certain to leave an overhang when the current jobless insurance measures expire, and with White House Chief of Staff Meadows not confident about reaching a deal next week. All this on top of the ongoing resurgence of COVID-19 across many US states plus the prospect of even more Greenback selling for month end, especially around the 4 pm London fix, amidst a growing number of bank models flagging bearish portfolio rebalancing signals. However, the DXY is holding between 92.539-969 parameters as the Buck pares some declines across the board.