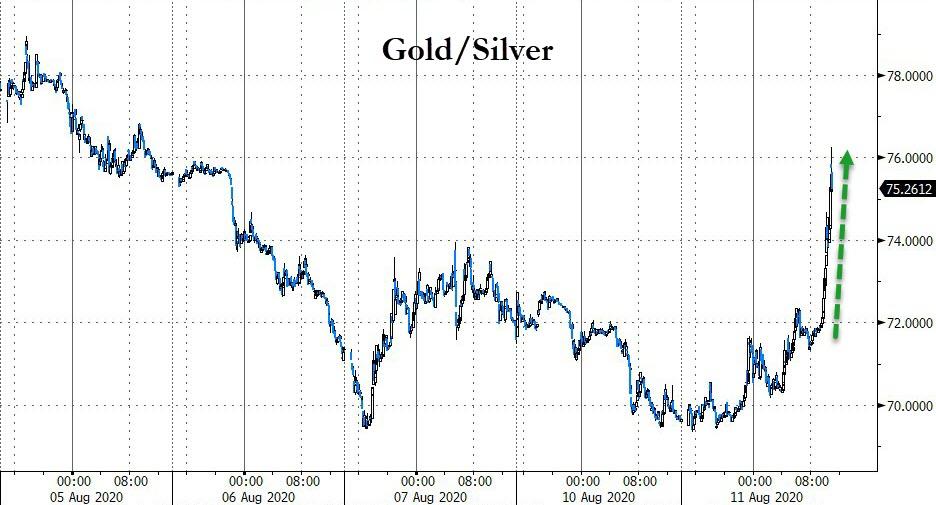

GOLD:$1,937.40 DOWN $92.40 The quote is London spot price (cash market)

Silver:$26.21// DOWN 3.25 London spot price ( cash market)

DONATE

Closing access prices: London spot

i)Gold : $1910.00 LONDON SPOT 4:30 pm

ii)SILVER: $24.78//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUGUST GOLD: $1932.50 CLOSE 1::30 PM SPREAD SPOT/FUTURE AUG (BACKWARD $5.10)

OCT GOLD: $2038.90 CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: : $1.50//CONTANGO//BELOW NORMAL CONTANGO $1.50

DEC. GOLD $2046.20 CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $8.80 ($ BELOW NORMAL CONTANGO)

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $26.20…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : 1 CENT PER OZ ( BACKWARDS)

SILVER DECEMBER CLOSE: $26.38 1:30 PM SPREAD SPOT/FUTURE DEC. : 17 CENTS PER OZ ( 5 CENTS ABOVE NORMAL CONTANGO)

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today: 708/2359

issued: 33

EXCHANGE: COMEX

CONTRACT: AUGUST 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,024.400000000 USD

INTENT DATE: 08/10/2020 DELIVERY DATE: 08/12/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 1333 5

072 H GOLDMAN 383

104 C MIZUHO 167

118 H MACQUARIE FUT 3

132 C SG AMERICAS 573

135 H RAND 2

159 C ED&F MAN CAP 1

226 C DIRECT ACCESS 1

323 C HSBC 12

332 H STANDARD CHARTE 62

355 C CREDIT SUISSE 14

365 C ED&F MAN CAPITA 1

657 C MORGAN STANLEY 56

657 H MORGAN STANLEY 297

661 C JP MORGAN 33 456

661 H JP MORGAN 252

686 C INTL FCSTONE 1 2

690 C ABN AMRO 231 31

700 C UBS 59

709 C BARCLAYS 185

709 H BARCLAYS 5

730 C PTG DIVISION SG 1

732 C RBC CAP MARKETS 6

737 C ADVANTAGE 2 29

800 C MAREX SPEC 183 14

880 C CITIGROUP 8

880 H CITIGROUP 302

905 C ADM 8

____________________________________________________________________________________________

TOTAL: 2,359 2,359

MONTH TO DATE: 46,280

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 2359 NOTICE(S) FOR 235,900 OZ (7.334 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 46,280 NOTICES FOR 4,628,000 OZ (143.95 TONNES)

SILVER

FOR AUGUST

16 NOTICE(S) FILED TODAY FOR 80,000 OZ/

total number of notices filed so far this month: 1147 for 5.735 MILLION oz

BITCOIN MORNING QUOTE $11,686 DOWN 286

BITCOIN AFTERNOON QUOTE.: $11,409 DOWN 483

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $92.40 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

NO CHANGES IN GOLD INVENTORY AT THE GLD/// //

GLD: 1,262/12 TONNES OF GOLD//

WITH SILVER DOWN $3.25 CENTS TODAY: AND WITH NO SILVER AROUND:

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.141 MILLION OZ//

RESTING SLV INVENTORY TONIGHT:

SLV: 571,632 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A STRONG SIZED 1575 CONTRACTS FROM 207,490 DOWN TO 205489, AND FURTHER FROM OUR NEW RECORD OF 244,710, (FEB 25/2020. THE LOSS IN OI OCCURRED DESPITE OUR STRONG $1.87 GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE LOSS IN COMEX OI IS PRIMARILY DUE TO A FAILED BANKER SHORT COVERING PLUS A STRONG EXCHANGE FOR PHYSICAL ISSUANCE, MINIMAL LONG LIQUIDATION, ACCOMPANYING A ZERO DECREASE IN SILVER OZ. STANDING AT THE COMEX FOR AUGUST. WE HAD A TINY NET LOSS IN OUR TWO EXCHANGES OF 575 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: SEP 950 DEC: 50 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1000 CONTRACTS. WITH THE TRANSFER OF 1320 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1000 EFP CONTRACTS TRANSLATES INTO 5.000 MILLION OZ ACCOMPANYING:

1.THE 187 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

86.470 MILLION OZ FINAL STANDING IN JULY.

6.400 MILLION OZ INITIAL STANDING IN AUGUST

MONDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 187 CENTS ).. AND, OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS. THE CONSIDERABLE LOSS AT THE COMEX WAS ACCOMPANIED BY : i) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A ZERO DECREASE IN SILVER OZ STANDING FOR AUGUST, A FAILED BANKER SHORT COVERING AND 4) MINIMAL LONG LIQUIDATION AS WE DID HAVE A SMALL NET LOSS OF 509 CONTRACTS OR 2.875 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKERS ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER..AND THUS THE REASON FOR OUR MASSIVE RAID THIS MORNING!!

SPREADING OPERATIONS/NOW SWITCHING TO SILVER

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN SILVER AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF AUGUST. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

AUGUST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF AUGUST:

8373 CONTRACTS (FOR 7 TRADING DAY(S) TOTAL 8373 CONTRACTS) OR 41.865 MILLION OZ: (AVERAGE PER DAY: 1196 CONTRACTS OR 5.9807 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 41.865 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 4.32% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,313.25 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 133.95 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

AUGUST EXP 41.865 MILLION OZ (EXCHANGE FOR PHYSICALS INCREASING)

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1575, DESPITE OUR STRONG 187 CENT GAIN IN SILVER PRICING AT THE COMEX ///MONDAY…THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1000 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE LOST A SMALL SIZED OI CONTRACTS ON THE TWO EXCHANGES: 575 CONTRACTS (DESPITE OUR $1.87 GAIN IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 1000 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A CONSIDERABLE SIZED DECREASE OF 1575 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED DESPITE A HUGE 187 CENT GAIN IN PRICE OF SILVER/AND A CLOSING PRICE OF $29.44 // MONDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.030 BILLION OZ TO BE EXACT or 147% of annual global silver production (ex Russia & ex China).

FOR THE NEW AUGUST DELIVERY MONTH/ THEY FILED AT THE COMEX: 16 NOTICE(S) FOR 80,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 WAS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 86.470 million oz//AUGUST 6.400 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 509 CONTRACTS TO 551,018 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE TINY GAIN OF COMEX OI OCCURRED DESPITE OUR STRONG RISE IN PRICE OF $11.45 /// COMEX GOLD TRADING// MONDAY//WE HAD A FAILED BANKER SHORT COVERING, A GOOD SIZED INCREASE IN GOLD TONNAGE STANDING AT THE COMEX FOR AUGUST, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR STRONG GAIN IN PRICE OF $11.45.

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 53

WE GAINED A SMALL SIZED 1797 CONTRACTS (5,589 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 1288 CONTRACTS:

CONTRACT .; AUG 0 AND OCT: 0 DEC: 1147; JUNE: 141 ALL OTHER MONTHS ZERO//TOTAL: 6201. The NEW COMEX OI for the gold complex rests at 551,018. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1797 CONTRACTS: 509 CONTRACTS INCREASED AT THE COMEX AND 1288 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 1797 CONTRACTS OR 5.589 TONNES. MONDAY, WE HAD A STRONG GAIN OF $11.45 IN GOLD TRADING……

AND WITH THAT GAIN IN PRICE, WE HAD A SMALL SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 5.589 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE LOATHE TO SUPPLY SHORT GOLD COMEX PAPER. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $11.45) AS IT SEEMS THAT OUR BANKER FRIENDS WERE NOT HAPPY AS WE HAD A FAILED BANKER SHORT COVERING MONDAY//THE BANKERS REGROUPED AND THEN INITIATED ANOTHER MASSIVE RAID ON GOLD/SILVER THIS MORNING AS THE BANKS FRONT RUNNED OUR OFFICIAL SECTOR BOMBING ORCHESTRATED BY THE BIS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1288) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (509 OI): TOTAL GAIN IN THE TWO EXCHANGES: 1797 CONTRACTS. WE NO DOUBT HAD 1 )A FAILED BANKER SHORT COVERING, 2.)A GOOD INCREASE IN GOLD TONNAGE STANDING AT THE GOLD COMEX FOR THE FRONT AUGUST MONTH, 3) ZERO LONG LIQUIDATION; 4) SMALL COMEX OI GAIN AND 5) SMALL EXCHANGE FOR PHYSICAL ISSUANCE AND …ALL OF THIS WAS COUPLED WITH OUR VERY STRONG GAIN IN GOLD PRICE TRADING//MONDAY//$11.45.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

AUGUST

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY(S) IN TONNES: 45.75 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 45.75/3550 x 100% TONNES =1.28% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3,305.93 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 313.09 TONNES ..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

AUGUST TOTAL EFP ISSUANCE; 45.75 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A CONSIDERABLE SIZED 1575 CONTRACTS FROM 207,064 DOWN TO 205,489 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE CONSIDERABLE SIZED LOSS IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) A FAILED BANKER SHORT COVERING , 2) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A ZERO INCREASE IN SILVER OZ STANDING AT THE SILVER COMEX FOR AUGUST, AND 4) MINIMAL LONG LIQUIDATION

EFP ISSUANCE 1000 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT: 950 AND DEC. 50 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1000 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1575 CONTRACTS TO THE 1000 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL LOSS OF 575 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 2.875 MILLION OZ, OCCURRED DESPITE OUR HUGE 187 CENT GAIN IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 38.96 POINTS OR 1.15% //Hang Sang CLOSED UP 513.25 POINTS OR 2.11% /The Nikkei closed UP 420.30 POINTS OR 1.88%//Australia’s all ordinaires CLOSED UP .40%

/Chinese yuan (ONSHORE) closed UP at 6.9447 /Oil UP TO 42,841 dollars per barrel for WTI and 45.60 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.9447 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9380 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED //CORONAVIRUS//PANDEMIC// : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

1639.701 oz

Manfra

51 kilobars

|

| Deposits to the Dealer Inventory in oz | 160,690.700 oz

|

| Deposits to the Customer Inventory, in oz |

547,853.000 OZ BRINKS

17040 1/2 KILOBARS |

| No of oz served (contracts) today |

2359 notice(s)

235900 OZ

(7.337 TONNES)

|

| No of oz to be served (notices) |

2126 contracts

(212,600 oz)

6.610 TONNES

|

| Total monthly oz gold served (contracts) so far this month |

46,280 notices

4628,000 OZ

143.95 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

i) Out of Manfra 1639.701 oz

total withdrawals; 1639.701 oz

We had 2 kilobar transactions +

ADJUSTMENTS: 3 //

: customer to dealer

i) Int Delaware: 24,002.400 oz

ii) Out of JPMorgan: 200,018.646 oz

iii) Out of Loomis: 8005.35 oz (249 kilobars)

The front month of AUGUST registered a total of 4486 CONTRACTS as we lost 105 contracts. We had 156 notices served on MONDAY so we GAINED 51 contracts or an additional 5100 will stand for delivery on this side of the pond as they refused to morph into London based forwards as well as negating a fiat bonus. The boys are scrambling in search of badly needed physical metal.

After August we have the non active Sept contract month.. Here we saw another GAIN of 41 contracts to stand at 2758. Oct GAINED 868 contracts UP to 69,505

The big December contract LOST 1034 contracts down to 404,713 contracts… on a rise in price???.(attempted short covering)

We had 2359 notices filed today for 235,900 oz

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2020. contract month, we take the total number of notices filed so far for the month (46,280) x 100 oz , to which we add the difference between the open interest for the front month of AUGUST (4485 CONTRACTS ) minus the number of notices served upon today (2,359 x 100 oz per contract) equals 4,840,600 OZ OR 150.560 TONNES) the number of ounces standing in this active month of JUNE

thus the INITIAL standings for gold for the AUGUST/2020 contract month:

No of notices filed so far (46,280, x 100 oz + (4485 OI) for the front month minus the number of notices served upon today (2,359) x 100 oz which equals 4,840,600 oz standing OR 150.506 TONNES in this active delivery month. This is a HUGE amount for gold standing for a AUGUST delivery month (an active delivery month).

We gained 51 contracts or 5100 oz of gold as these guys refused to morph into London based forwards.

NEW PLEDGED GOLD: BRINKS

144,088.952 oz NOW PLEDGED JAN 21.2020/HSBC 5.4807 TONNES

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

231,924.295 oz (some deleted august 3) JPM 7.2138 TONNES

611,401.341 oz pledged June 12/2020 Brinks/ july 2/july 21 19.017 tonnes

total pledged gold: 1,029,962.895 oz 32.03 tonnes

total registered, pledged and eligible (customer) gold; 36,660,485.581 oz 1,140.95 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1014.61 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 2 deposits into the customer account

i)into JPMorgan: nil oz

ii) Into CNT: 599,305.160 oz

iii) Into Delaware: 44,417.790 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 164.3 million oz of total silver inventory or 48,79% of all official comex silver. (164.3 million/336.816 million

total customer deposits today: 643,722.950 oz

we had 2 withdrawals:

i) Out of Delaware: 17,217.513 oz

ii) Out of Scotia: 600,083.220 oz

total withdrawals; 617,300.733 oz

We had 1 adjustments

i) Out of CNT: 585,486.19 oz

customer to dealer account of CNT

Total dealer(registered) silver: 128,022 million oz

total registered and eligible silver: 336.816 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

the front month of August registered an open interest of 149 contracts and thus we lost 25 contracts. We had 25 notices filed on Monday so we lost 0 contracts or NIL oz will stand for delivery as these guys refused to morph into London based forwards as well as negating a fiat bonus for their efforts…. The bankers are now desperate in their search for badly needed silver whether it is on this side of the pond or the European side.

After August we have the big September contract month and here we see a lost 6399 contracts down to 117,772. November saw another gain of 29 contracts to stand at 185.

The big December contract month saw its OI rise by strong 4179 contracts up to 76,202

Nobody has left the silver arena despite the vicious attack, Friday.

The total number of notices filed today for the AUGUST 2020. contract month is represented by 16 contract(s) FOR 80,000, oz

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 1147 x 5,000 oz = 5,735,000 oz to which we add the difference between the open interest for the front month of AUGUST(.149) and the number of notices served upon today 16 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the AUGUST/2019 contract month: 1147 (notices served so far) x 5000 oz + OI for front month of AUGUST (149)- number of notices served upon today (16) x 5000 oz of silver standing for the AUGUST contract month.equals 6,400,000 oz. ..VERY STRONG FOR A NON ACTIVE MONTH.

We lost 0 contracts or an additional nil will stand for delivery as they refused to morph into London based forwards..

TODAY’S ESTIMATED SILVER VOLUME : 356,999 CONTRACTS // volume huge++++++++++++++++++/

FOR YESTERDAY: 303,196. ,CONFIRMED VOLUME//volume huge+++++++++++++++++++++++++++++/

YESTERDAY’S CONFIRMED VOLUME OF 303,196 CONTRACTS EQUATES to 1.784 billion OZ 254% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO- 1.39% ((AUGUST 11/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.74% to NAV: (AUGUST 11/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 1,39%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 19.65 TRADING 19,25///NEGATIVE 2,01

END

And now the Gold inventory at the GLD/

AUGUST 11//WITH GOLD DOWN $92.40 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1262.12 TONNES.

AUGUST 10/WITH GOLD UP $11.35 TODAY, WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.84 TONNES//INVENTORY RESTS AT 1262.12 TONNES

AUGUST 7/WITH GOLD DOWN $38.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1267.96 TONNES

AUGUST 6/WITH GOLD UP $20.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER DEPOSIT OF 10.23 TONNES INTO THE GLD/INVENTORY RESTS AT 1267.96 TONNES//

AUGUST 5/WITH GOLD UP $ 33.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 9.35 TONNES INTO THE GLD//INVENTORY RESTS AT 1257.73 TONNES

AUGUST 4//WITH GOLD UP $31.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 6.48 TONNES/GLD INVENTORY RESTS AT 1248.38 TONNES

AUGUST 3/WITH GOLD UP $2.20 TODAY, WE HAVE NO CHANGES IN THE GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241,96 TONNES

JULY 31/WITH GOLD UP $17.90 TODAY/WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241.96 TONNES.

JULY 30/WITH GOLD DOWN $10.00 TODAY, WE HAVE ANOTHER SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES//INVENTORY RESTS AT 1241.96 TONNES.

JULY 29//WITH GOLD UP $12.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 8.47 TONNES/INVENTORY RESTS AT 1243.12 TONNES

JULY 28///WITH GOLD UP $13.25 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 5.84 TONNES/INVENTORY RESTS AT 1234.65

JULY 27//WITH GOLD UP $35.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF XXX TONNES/INVENTORY RESTS AT 1228.81 TONNES

JULY 24/WITH GOLD UP $8.80 TODAY: WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.80 TONNES//INVENTORY RESTS AT 1228.81 TONNES

JULY 23/WITH GOLD UP $24.90 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 7.26 TONNES/INVENTORY RESTS AT 1225.01 TONNES

JULY 22/WITH GOLD UP $22.00 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 7.89 TONNES/INVENTORY RESTS AT 1219.75 TONNES

JULY 21//WITH GOLD UP $26.00 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.97 TONNES INTO THE GLD// INVENTORY RESTS AT 1211.86 TONNES

JULY 20/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1206.89 TONNES

JULY 17/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1206.89 TONNES

JULY 16/WITH GOLD DOWN $9.80 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: INVENTORY RESTS AT 1206.89 TONNES

JULY 15//WITH GOLD UP $1.55 TODAY/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 2.96 TONNES INTO THE GLD///INVENTORY RESTS AT 1206.89 TONNES

JULY 14//WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 3.51 TONNES/INVENTORY RESTS AT 1203.97 TONNES

JULY 13//WITH GOLD UP $12.50 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1200.46 TONNES

JULY 10/WITH GOLD DOWN $.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD//A STRANGE WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1200.82 TONNES

JULY 9//WITH GOLD DOWN $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OX 3.21 TONNES INTO THE GLD//INVENTORY RESTS AT 1202.57 TONNES

JULY 8/WITH GOLD UP $13.75 TODAY; A BIG CHANGE IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 7.89 TONNES INTO THE GLD//INVENTORY RESTS AT 1199.36 TONNES

JULY 7/WITH GOLD UP $12.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1191.47 TONNES

JULY 6/WITH GOLD UP $6.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1191.47 TONNES

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

JUNE 30//WITH GOLD UP $16.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1178.90 TONNES

JUNE 29/WITH GOLD UP $2.90 TODAY: A HUGE DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1178.90 TONNES

JUNE 26/WITH GOLD UP $5.03 TODAY: VERY STRANGE: A PAPER WITHDRAWAL OF 1.46 TONNES//INVENTORY RESTS AT 1175.39 TONNES

JUNE 25//WITH GOLD DOWN $3.30 TODAY//ANOTHER STRONG PAPER DEPOSIT OF 7.6 TONNES///INVENTORY RESTS AT 1176.85 TONNES

JUNE 24/WITH GOLD DOWN $1.50 TODAY; A STRONG 3.21 TONNES ADDED TO THE GLD//INVENTORY RESTS AT 1169.25 TONNES

JUNE 23/WITH GOLD UP $25.50 TODAY/ANOTHER CRIMINAL PAPER DEPOSIT OF 6.73 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1166.04 TONNES

JUNE 22/WITH GOLD UP $14.00 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 23.09 TONNES//INVENTORY RESTS AT 1159.31 TONNES

JUNE 19/WITH GOLD UP$16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//; INVENTORY RESTS AT 1136.22 TONNES

JUNE 18//WITH GOLD DOWN $2.75 TODAY: NO CHANGES IN GOLD INVENTORY: INVENTORY RESTS AT 1136.22 TONNES

JUNE 17/WITH GOLD DOWN $1.05: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1136.22 TONNES

JUNE 16//WITH GOLD UP $6.70 TODAY: NO CHANGES IN GOLD INVENTORY: /INVENTORY RESTS AT 1136.22 TONNES

JUNE 15/WITH GOLD DOWN ANOTHER $8.80 TODAY, NO CHANGES IN GOLD INVENTORY/INVENTORY RESTS AT 1136.22 TONNES

JUNE 12//WITH GOLD DOWN $1.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 1.17 TONNES AT THE GLD//INVENTORY RESTS AT 1136.22 TONNES

JUNE 11//WITH GOLD UP $16.80 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 6.55 TONNES AT THE GLD//INVENTORY RESTS AT 1135.05 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

AUGUST 11/ GLD INVENTORY 1262.12 tonnes*

LAST; 878 TRADING DAYS: +322.68 NET TONNES HAVE BEEN ADDED THE GLD

LAST 778 TRADING DAYS://+501.15 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

AUGUST 11/WITH SILVER DOWN $3.25 CENTS, WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.41 MILLION OZ//INVENTORY RESTS AT 571.632 MILLION OZ//

AUGUST 10/WITH SILVER UP 1.89 TODAY, WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 3.538 MILLION OZ/INVENTORY RESTS AT 569.491 MILLION OZ//

AUGUST 7/WITH SILVER DOWN 69 CENTS TODAY: WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY: A DEPOSIT OF 0.465 MILLION OZ/INVENTORY RESTS AT 573.029 MILLION OZ.

AUGUST 6/WITH SILVER UP $1.52 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 572.564 MILLION OZ///

AUGUST 5/WITH SILVER UP $1.03 TODAY, WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A MONSTROUS DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 572.564 MILLION OZ//

AUGUST 4/WITH SILVER UP $1.45 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 367.161 MILLION OZ//

AUGUST 3/WITH SILVER UP 23 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//SURPRISINGLY ANOTHER WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 367.161 MILLION OZ//

JULY 31/WITH SILVER UP 82 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: SURPRISINGLY A HUGE WITHDRAWAL OF 3.26 MILLION OZ//INVENTORY RESTS AT 368.092 MILLION OZ//

JULY 30//WITH SILVER DOWN 97 CENTS TODAY: WE HAVE A SMALL CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 571.352 MILLION OZ//

JULY 29/WITH SILVER UP 7 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY//A DEPOSIT OF 5.984 MILLION OZ//INVENTORY RESTS AT 572.283 MILLION OZ//

JULY 28 WITH SILVER DOWN 14 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 7.52 MILLION OZ//INVENTORY RESTS AT 566.299 MILLION OZ//

JULY 27/WITH SILVER UP $2.67 TODAY, WE HAD NO CHANGES IN SILVER INVENTORY: A DEPOSIT OF XX MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ//

JULY 24/WITH SILVER DOWN $0.12 TODAY: NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 558.779 MILLION OZ/

JULY 23/WITH SILVER UP $.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A HUMONGOUS PAPER DEPOSIT OF 9.594 MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ///

JULY 22/WITH SILVER UP $1.54 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A HUMONGOUS PAPER DEPOSIT OF 7.218 MILLION OZ//INVENTORY RESTS AT 549.185 MILLION OZ/

JULY 21/WITH SILVER UP $1.38 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUMONGOUS PAPER DEPOSIT OF 15.368 MILLION OZ////INVENTORY RESTS AT 541.967 MILLION OZ//

JULY 20/WITH SILVER UP 40 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 3.819 MILLION OZ ‘ENTERED” THE SLV..INVENTORY RESTS AT 526.599 MILLION OZ/

JULY 17/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 1.583 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 522.780 MILLION OZ//

JULY 16//WITH SILVER DOWN 14 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ//INVENTORY RESTS AT 521.197 MILLION OZ..

JULY 15.WITH SILVER UP 21 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.956 MILLION OZ//INVENTORY RESTS AT 516.074 MILLION OZ//

JULY 14/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 514.118 MILLION OZ//

JULY 13//WITH SILVER UP 67 CENTS TODAY: A HUGE CHANGE IN SILVER: A WITHDRAWAL OF 1.677 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 514.118 MILLION OZ//

JULY 10/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 4.844 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.795 MILLION OZ

WHAT A FRAUD!!

JULY 9/WITH SILVER DOWN 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 8.198 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 510.951 MILLION OZ/

JULY 8/WITH SILVER UP 37 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.118 MILLION OZ FROM THE SLV//VERY SURPRISING.//INVENTORY RESTS AT 502.753 MILLION OZ//

JULY 7/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/INVENTORY RESTS AT 503.871 MILLION OZ///

JULY 6//WITH SILVER UP 24 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.863 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 503.871 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

JUNE 30/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 29/WITH SILVER DOWN ONE CENT TODAY: A TWO CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 466,000 OZ TO PAY FOR STORAGE FEES AND INSURANCE//// AND A LARGE DEPOSIT OF 1.212 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 26/WITH SILVER UP 6 CENTS TODAY: ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ RESTS AT 491.858 MILLION OZ//

JUNE 25/WITH SILVER UP 12 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 931,000 OZ INTO THE SLV////INVENTORY RESTS AT 491.858 MILLION OZ//

JUNE 24///WITH SILVER DOWN 31 CENTS// NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 490.927 MILLION OZ

JUNE 23//WITH SILVER UP 16 CENTS TODAY: A MONSTROUS CHANGE IN INVENTORY: A PAPER DEPOSIT OF 4.473 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 490.927 MILLION OZ//

JUNE 22/WITH SILVER UP 15 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/: INVENTORY/INVENTORY RESTS AT 486/454 MILLION OZ//

JUNE 19//WITH SILVER UP 22 CENTS TODAY: STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 839,000 OZ FROM THE SLV////INVENTORY RESTS AT 486,454 MILLION OZ..

JUNE 18/WITH SILVER DOWN 16 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 932,000 OZ INTO THE SLV////INVENTORY RESTS AT 487.293 MILLION OZ

JUNE 17/WITH SILVER UP 8 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.261 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.361 MILLION OZ

JUNE 16//WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.118 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 483.100 MILLION OZ//

JUNE 15/WITH SILVER DOWN 14 CENTS NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 481.982 MILLION OZ///

JUNE 12/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: TWO DEPOSITS OF 7.269 MILLION OZ AND 1.802 MILLION OZ ADDED TO THE SLV///INVENTORY RESTS THIS WEEKEND AT 481.982 MILLION OZ//

JUNE 11//WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY: ///INVENTORY RESTS AT 472.89 MILLION OZ//

AUGUST 11.2020:

SLV INVENTORY RESTS TONIGHT AT

571,632 MILLION OZ.

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

Biden vows to block Pebble mine project if elected

Submitted by cpowell on Mon, 2020-08-10 14:44. Section: Daily Dispatches

From the Associated Press

via Alaska Public Media, Anchorage

Sunday, August 9, 2020

JUNEAU, Alaska — Democratic presidential candidate Joe Biden said Sunday that if he’s elected, his administration would stop a proposed copper and gold mine in Alaska’s Bristol Bay region.

“It is no place for a mine,” the former vice president said in a statement to news media. “The Obama-Biden administration reached that conclusion when we ran a rigorous, science-based process in 2014, and it is still true today.”

The Environmental Protection Agency under the Obama administration proposed restricting development in the Bristol Bay region but never finalized the restrictions. The agency retains the option to invoke that so-called veto process again if it decides to do so. …

… For the remainder of the report:

https://www.alaskapublic.org/2020/08/09/biden-vows-to-block-pebble-mine-…

end

Turk talks about the huge potential for silver

Kingworldnews/James Turk

In comments to KWN, Turk sees greatest potential for silver

Submitted by cpowell on Mon, 2020-08-10 14:59. Section: Daily Dispatches

10:58a ET Monday, August 10, 2020

Dear Friend of GATA and Gold:

In comments to King World News today, GoldMoney founder and GATA consultant James Turk updates his predictions for the accelerating monetary metals. Turk is most impressed by silver’s prospects because the metal is still trading far below its price 40 years ago when the U.S. dollar was also succumbing to inflation.

The monetary metals, Turk concludes, “are in a long-overdue major bull market.”

His comments can be found at KWN here:

https://kingworldnews.com/man-who-correctly-predicted-silver-would-hit-3…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

bill Murphy talks about gold/silver price suppression

(Bill Murphy/GATA)

GATA Chairman Murphy interviewed about gold price suppression

Submitted by cpowell on Mon, 2020-08-10 15:26. Section: Daily Dispatches

11:25a ET Monday, August 10, 2020

Dear Friend of GATA and Gold:

GATA Chairman Bill Murphy was interviewed yesterday about gold price suppression policy by market observer Bob Unger. The interview is a half hour long and can be seen at YouTube here:

https://www.youtube.com/watch?v=rW977KwhEiM

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

iii) Other physical stories:

Gold and silver bombed! ..official sector

Gold, Silver, Bonds Hit As “Everything Duration”-Momo/Liquidity Trade Unwinds

Precious metals are getting pummeled this morning as real rates rise amid vaccine optimism and hotter than expected inflation data…

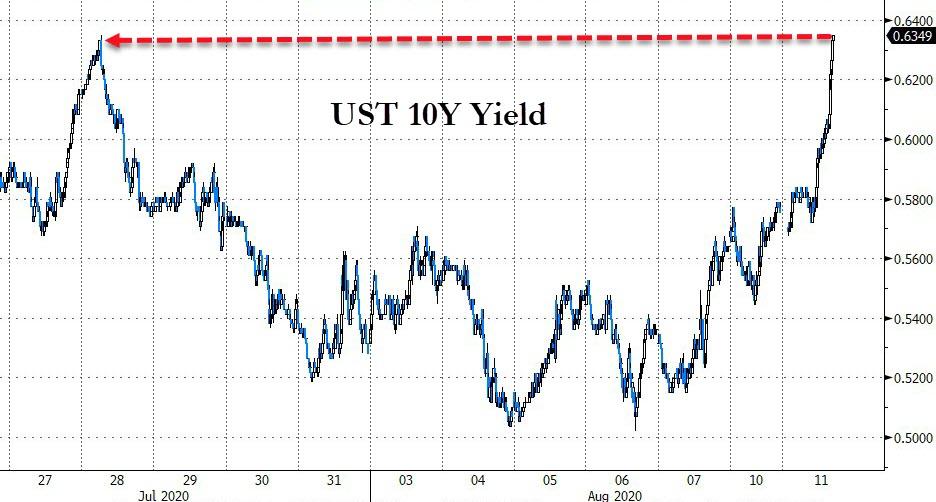

Bonds are also getting slammed with 10Y Yields back above 60bps at 10-day highs…

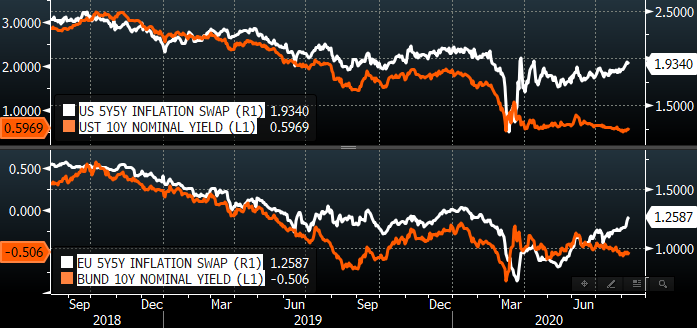

As Nomura’s Charlie McElligott reiterates (from his call last week), “inflation expectations” are beginning to adjust higher – Inflation swaps in U.S. and Europe (fickle traders, no doubt) are beginning to tell a story of nascently accelerating global views towards forward inflation – something that was inconceivable to nearly all just a few months ago and now coinciding with the back-to-back weeks of U.S. M2 decline, showing a decrease in risk-aversion and saving and a “less bad” economic outlook from corporates.

And as real yields rise, gold prices fall…

As the Nomura MD has noted over the past few weeks, the SPX macro factor regime has transitioned from “Liquidity” macro factor measures which led the March Equities recovery:

1. Fed QE Expectations – 1y5y USD Rate Vol,

2. Fed Rate Cut Expectations – ED$ Curve,

3. USD Liquidity – FX Basis Swaps

…now into “Growth” inputs as the largest POSITIVE price-drivers for S&P 500 in the factor PCA model:

1. US and EU GDP NowCasting and

2. Inflation Swaps

But the most dramatic impacts of the reflation trade inflection are evident in the broad equity markets… where Nasdaq (tech – growth focused) is tumbling as Small Caps (financials/energy – value dominant) surge…

And as McElligott notes, US Equities factors are showing the most glaring expression of the market’s flat-footedness in their growth- and inflation- skepticism (and evidencing itself in the crowded “Everything Duration” Momentum-positioning which is evidently being de-grossed by somebody):

The current iteration of this U.S. Equities factor “Value / Momentum” swing (5d aggregate % chg) is a doozy, ranking as in the top six since at least 2010, going hand-in-hand with monster thematic- and sector- reversals.

The question is – how high will The Fed let nominal rate rise before it stomps on this reversal? As Morgan Stanely recently warned:

To be clear, we think that overall equity and credit markets can weather a modest rise in yields, driven by better data. Risk assets have frequently been happy to trade a better growth outlook for a higher discount rate, and we saw this pattern as recently as Monday when global PMIs surprised to the upside. But the rise in duration across asset classes, at its most expensive levels on record, suggests that the transition won’t be smooth.

Whether one is active or passive, August appears to be a good time to evaluate, and be honest about, your cross-asset duration exposure.

end

James McShirley to me

“The Comex raised margins on gold and silver yesterday. That was the trigger for the late day selloff, and now today’s smack down. As I have said whenever there is a margin requirement change it nearly always precedes a cartel attack. Raising margins is one of the few remaining weapons the cartel and their Comex cronies have to slow down this precious metal bull market. Silver leverage now back down to 11.9-1. Gold leverage now 22.4-1. Look for more of the same in the future as it will help the cartel escape their short positions.”

JMc

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

S&P Futures Hit All Time Highs On Stimulus, Vaccine Hopes; Gold, Silver Tumble

S&P 500 futures hit a record high as investors shrugged off continuing U.S.-China tensions and instead focused on news of an approved, if largely unclear, Russian vaccine, and more stimulus optimism as President Donald Trump said he’s considering a tax cut on capital gains. According to Reuters calculations at the current levels, the benchmark index is set to open about 12 points below its Feb. 19 record peak of 3,393.52.

American Airlines and Carnival led a boom in travel shares in the premarket. The S&P 500 closed less than 1% below its record high on Monday as investors extended a rotation into value stocks from heavyweight tech-related names. At 8:00 a.m. ET, S&P 500 e-minis were up 23.25 points, or 0.69%, topping an all-time high of 3,372.25 points last hit on Feb. 20.

A rally in the tech megacaps including Amazon.com, Netflix and Apple that thrived during the shutdowns helped the Nasdaq reclaim its all-time high in June, while the Dow still remains about 6% below its peak.

“Equity has never looked cheaper compared to fixed income and the like,” Jun Bei Liu, portfolio manager at Tribeca Investment Partners, said in a Bloomberg TV interview. “If you want any return, any yield, any income or even any growth you have to go to equities.”

In Europe and Asia, a broad rally from industrial goods to health-care shares set the Stoxx Europe 600 Index headed for its best increase since mid-June. The Stoxx 600 Europe index rose more than 2% , with auto shares leading the way after a surge in Chinese car sales. The Stoxx 600 Travel & Leisure Index jumps as much as 4.8%, to the highest since June 11, amid investor optimism about the development of a vaccine for the coronavirus and after InterContinental Hotels said it is seeing some very early signs of improvement as traveller confidence returns, sending its stock up 6.1%. The subgroup was among the biggest advancers in Europe’s Stoxx 600 Index, which is up 2.1% after President Vladimir Putin said Russia has registered its first Covid-19 vaccine, though some pharmaceutical companies have called Russia’s rushed registration dangerous. Airline stocks also rose: IAG +7.8%, EasyJet +6.5%, Lufthansa +4.7%, Ryanair +4%, Turkish Airlines +8%.

Earlier in the session, Asian shares ex-Japan gained nearly 1%, with Japan’s Nikkei rising 1.9% after a Monday holiday. There were hopes Beijing’s sanctions on 11 U.S. citizens may end this round of tit-for-tat moves between the two powers.

“It has left the White House untouched,” said Vishnu Varathan, head of economics at Mizuho Bank in Singapore. “That gives some relief that China is still giving some priority to the (trade deal) dialogue,” he said.

Elsewhere, the resignation of Lebanon’s government after the devastating explosion in Beirut threatened to upend prospects of a debt restructuring deal in the next few months.

Market participants remain eager to see an agreement on the fifth federal aid bill to help Americans battle with the health crisis was far from over with U.S. cases surpassing 5 million last week. The mood remains cautious as sparring continues in the U.S. Congress over extending fiscal stimulus while economic data such as a steep drop in South Korean exports and a rise in UK jobless rates remain a cause for concern. But upbeat comments by U.S. Treasury Secretary Steven Mnuchin on the prospects for a bipartisan stimulus deal supported Brent crude futures at near five-month highs and kept the dollar index near a one-week peak.

Commerzbank analysts said markets were shrugging off doubts over the legality of Trump’s order and appeared convinced Congress would agree a deal

“Not without good reason, because in the election campaign both parties have an interest in presenting themselves well,” they said. “Who wants to be seen as the stingy bad guy even in times of great need?”

General optimism kept safe haven assets under gentle pressure, with gold falling back under $2000 an ounce, down more than 2%, even as the dollar slumped. Precious metals dropped with spot gold south of $2000 and spot silver just about holding onto a USD 28/oz handle having briefly dipped below the figure. No fundamental news flow coincided with the losses across precious metals but action could merely be a function of tech play alongside some profit taking/stops being triggered. But the most likely reason for the back down in gold prices is that 10Y real rates – which gold has been tracking tick for tick – also dipped from recent record lows.

In FX, the dollar slipped as European stocks follow Asian equities higher, with markets taking encouragement from falling hospitalization rates in California and New York and decreasing new infections in Hong Kong. The euro rose as much as 0.5% after ZEW data revealed investors raised their expectations of a rebound for the German economy in August. Italy’s 10-year yield premium over its German equivalent tightened to its lowest level since February.

In rates, ten-year U.S. Treasury yields were near a two-week high of 0.5870% while German yields likewise rose to two-week highs. Treasury yields were cheaper by 1bp to 2.5bp across the curve led by long end, steepening 2s10s, 5s30s by 1.6bp and 1bp; 10-year yields around 0.60% while bunds, gilts both lag by ~1bp. Ahead of 3-year auction, WI yield is ~0.160%, 3bp richer than July’s record low stop at 0.19%; refunding includes $38b 10-year Wednesday and $26b 30-year Thursday; all sizes are records.

In commodities, WTI and Brent continue to grind higher in early trade, with upside more-so a function of the overall risk tone as opposed to fresh fundamental catalysts, albeit prices remain underpinned by the recent upbeat assessment from Saudi, Iraq and Gulf members alongside the constructive outlook by Saudi Aramco post-earnings. Looking ahead, traders will be eyeing the weekly API inventory release, with expectations for crude stockpiles to decline by almost 4mln barrels, but ahead of the weekly release, participants will pay attention to the EIA Short Term energy Outlook which will include US crude production forecasts for the rest of 2020 and 2021. In terms of base metals, Dalian iron ore futures snapped its two-day losing streak as prices were bolstered by falling portside inventories, whilst LME copper prices saw early downside.

Looking at the day ahead, and data releases out include UK unemployment data for June, the German ZEW survey for August, as well as July’s PPI reading and the NFIB small business optimism index from the US. Otherwise, Fed speakers today include Barkin, Daly and Brainard.

Market Snapshot

- S&P 500 futures up 0.6% to 3,371.75

- STOXX Europe 600 up 1.8% to 371.07

- MXAP up 1.1% to 169.75

- MXAPJ up 0.6% to 562.38

- Nikkei up 1.9% to 22,750.24

- Topix up 2.5% to 1,585.96

- Hang Seng Index up 2.1% to 24,890.68

- Shanghai Composite down 1.2% to 3,340.29

- Sensex up 0.9% to 38,507.25

- Australia S&P/ASX 200 up 0.5% to 6,138.65

- Kospi up 1.4% to 2,418.67

- German 10Y yield rose 1.3 bps to -0.513%

- Euro up 0.3% to $1.1768

- Brent Futures up 0.8% to $45.33/bbl

- Italian 10Y yield fell 0.8 bps to 0.795%

- Spanish 10Y yield fell 0.2 bps to 0.253%

- Brent Futures up 0.8% to $45.33/bbl

- Gold spot down 2.1% to $1,985.04

- U.S. Dollar Index down 0.2% to 93.44

Top Overnight News from Bloomberg

- Britain’s mounting labor market crisis was underscored by a 220,000 slump in employment during the height of the coronavirus lockdown, the worst decline since the global financial crisis

- Even as China continues to hit back at the Trump administration, leaders in Beijing are also signaling they want to ease tensions with the U.S. as the clock ticks down to the presidential election

- Lebanon’s political leaders are expected to launch parliamentary consultations to choose a new prime minister after Hassan Diab’s government resigned on Monday over the devastating explosion at Beirut’s port

- Hong Kong’s worst coronavirus outbreak is showing signs of coming under control as the city reported the lowest number of new local infections since its resurgence began over a month ago

A quick look at global markets courtesy of NewsSquawk:

Asian equity markets traded higher as risk appetite in the region improved on the tepid performance seen on Wall St where most major indices finished in the green but tech underperformed and indecision lingered amid the ongoing stimulus talks stalemate, mixed views on President Trump’s recent executive orders and ongoing US-China tensions. ASX 200 (+0.5%) was positive as top-weighted financials spearheaded the advances and with the broad sector gains offsetting the weakness in gold miners and tech, while Nikkei 225 (+1.8%) was buoyed on return from an extended weekend helped by a predominantly weaker currency and after bank lending increased by its fastest pace on record. Hang Seng (+2.1%) and Shanghai Comp. (-1.2%) conformed to the upbeat mood after the PBoC upped its liquidity efforts with a CNY 50bln reverse repo injection and although China announced sanctions against officials in retaliation to US sanctions on Hong Kong, they refrained from imposing them on Trump administration officials. Furthermore, casino stocks are red-hot after reports China is to remove the quarantine requirement for Macau effective tomorrow and Next Digital shares surged over 400% in an extension of yesterday’s sharp intraday turnaround as activists piled into the shares in a show of support following the founder’s recent arrest and amid speculation it could sell its listed entity as a shell for other firms to acquire for a back-door listing. Finally, 10yr JGBs were lower and approached 152.00 to the downside as they played catch up to the recent weakness in T-notes and as havens were shunned amid gains in riskier assets, while the lack of BoJ presence in the market also added to the dampened mood for JGBs.

Top Asian News

- One of World’s Strongest Rallies Propels Kospi to Two-Year High

- Tough-to-Impress Harvard Grad Molds Fortunes of China’s Rich

- Singapore’s Economy Posts Worse Contraction in Second Quarter

- Iron Ore Futures Gain as China’s Economic Recovery Fuels Demand

European equities trade higher across the board [Euro Stoxx 50 +2.7%], with upside accelerating after the cash open as sentiment improved following an initially bleak APAC handover – prompting DAX cash and Sept futures to gain above 13k, albeit fresh fundamental catalysts remain light throughout the session thus far; some modest impetus coincided with vaccine updates from Russia. Firm gains are also seen across all European sectors, with cyclicals/value clearly outpacing defensives, whilst the breakdown paints a similarly performance, with Travel & Leisure topping the chart, closely followed by Oil & Gas, Autos and Banks, whilst the other side of the spectrum sees Healthcare and Chemicals as the laggards. In terms of individual movers, UK listed Cineworld (+17%) extended on earlier gains and resides at the top of the Stoxx 600 amid reports that the group could go private. BP (+3.7%) coattails on the back of firmer energy prices coupled with source reports the group is said to be mulling the sale of its German chemicals’ unit DHC Solvent Chemie. Mediobanca (+5.9%) extends on opening gains after the ECB gave the green-light for shareholder Del Vecchio to increase his stake in the Co. to 13-14% from 10%.

Top European News

- Hungary Inflation Surges, Putting Rate Policy Back in Focus

- U.K. Jobs Crisis Worsens as Employment Drops Most Since 2009

- Vestas Shares Surge as 2020 Revenue Guidance Reintroduced

- Unilever Warns of Dutch Tax Proposal’s Risk for Plan to Move

In FX, another back up in US Treasury yields and mild steepening along the curve into record refunding has underpinned the Dollar to a degree, but a deeper retracement in spot bullion to test support around the psychological Usd 2000/oz level coincided with the DXY marginally eclipsing Monday’s high at 93.729. However, the Greenback has lost momentum against the backdrop of extended gains in global equities that is keeping high beta/cyclical currencies supported and safe-haven demand suppressed.

- AUD/NZD/CAD/NOK – As noted above, the Aussie is benefiting from bullish risk sentiment to the extent that declines in NAB business sentiment and conditions have not weighed on Aud/Usd unduly, while the Kiwi is just keeping tabs with 0.6600 ahead of Wednesday’s RBNZ policy meeting even though the bias may be skewed towards a more dovish event compared to the prior assessment and guidance, while NZ reports a local outbreak of COVID-19 cases after a 100+ day run of no infections at all. Elsewhere, elevated crude prices are helping the Loonie and Norwegian Crown remain afloat around 1.3300 and 10.5800 vs the Buck and Euro respectively, with the former now looking for some independent impetus via Canadian housing starts.

- EUR/CHF/GBP – All benefiting from the aforementioned Dollar fade, with the index now back under 93.500 again and Euro rebounding between 1.1723-83 parameters following a somewhat mixed ZEW survey, the Franc paring losses within a 0.9168-34 range and Pound maintaining 1.3050+ status, but not quite able to retest yesterday’s best a few pips over 1.3100 in wake of mostly weaker than forecast UK labour and pay data.

- JPY – The Yen is marginally underperforming either side of 106.00 on a loss of safety premium and with Japanese markets back from their long holiday weekend, but little lasting reaction to a wider than anticipated Japanese current account surplus.

- EM – Oil’s ongoing resurgence is helping the Rouble and Mexican Peso supplement gains vs the flagging Greenback. but the SA Rand has not been deterred by Gold’s meltdown or looming data and has breached key technical resistance in the form of the 100 DMA (17.6240) on the way up towards 17.5400. Similarly, the Turkish Lira is back in recovery mode as tighter CBRT funding conditions prompt some short covering, while Brazil’s Real awaits BCB COPOM minutes from the last meeting.

In commodities, WTI and Brent front-month futures continue to grind higher in early trade, with upside more-so a function of the overall risk tone as opposed to fresh fundamental catalysts, albeit prices remain underpinned by the recent upbeat assessment from Saudi, Iraq and Gulf members alongside the constructive outlook by Saudi Aramco post-earnings. The benchmarks experienced modest downside heading into the European cash open, in which prices briefly dipped below 45/bbl for the Brent Oct contract, whilst WTI Sep tested 42/bbl, before recovering lost ground and some more. Looking ahead, traders will be eyeing the weekly Private Inventory release, with expectations for crude stockpiles to decline by almost 4mln barrels, but ahead of the weekly release, participants will pay attention to the EIA Short Term energy Outlook which will include US crude production forecasts for the rest of 2020 and 2021. Elsewhere, precious metals are under pressure this morning with spot gold south of USD 2000/oz and spot silver just about holding onto a USD 28/oz handle having briefly dipped below the figure. No fundamental news flow coincided with the losses across precious metals but action could merely be a function of tech play alongside some profit taking/stops being triggered. In terms of base metals, Dalian iron ore futures snapped its two-day losing streak as prices were bolstered by falling portside inventories, whilst LME copper prices saw early downside amid the firming USD at the time; albeit, has since nursed losses.

US Event Calendar

- 6am: NFIB Small Business Optimism 98.8, est. 100.5, prior 100.6

- 8:30am: PPI Final Demand MoM, est. 0.3%, prior -0.2%; PPI Ex Food and Energy MoM, est. 0.1%, prior -0.3%

- 8:30am: PPI Final Demand YoY, est. -0.7%, prior -0.8%; PPI Ex Food and Energy YoY, est. 0.0%, prior 0.1%

DB’s Jim Reid concludes the overnight wrap

The last 24 hours has pretty much fit the bill as far as slow news days are concerned in markets. That being said there was a somewhat notable milestone reached yesterday as the S&P 500 surpassed the all-time highs from February on a total return basis. This is a fairly astonishing feat when you consider that in late-March the index was down as much as -33.79% from those highs. In price terms it finished +0.27% yesterday which means it’s just -0.76% lower than its all-time closing high. That move also marked the S&P’s 7th consecutive advance for the first time since April 2019.

While the S&P nudged higher, the Dow Jones saw a much larger +1.30% gain, which is somewhat unusual given the strong correlation between the two indices. Indeed, it’s only the 6th time in the last decade that the Dow’s daily move has been more than one percentage point different to the S&P’s (even if 5 of them have been since the pandemic hit). At the other end of the spectrum though, the NASDAQ (-0.39%) slipped for a rare second consecutive session. At the margin the macro news acted as a bit of headwind and included the news of further Chinese sanctions on US officials after similar measures were announced by the US on Friday, with those sanctioned by China including the Republican senators Marco Rubio, Ted Cruz and Tom Cotton. Chinese Foreign Ministry spokesman Zhao Lijan said yesterday that “China has decided to impose sanctions on those individuals who behaved badly on Hong Kong-related issues”. And in a further sign that US-China tensions are showing no sign of abating any time soon, US Secretary of State Mike Pompeo tweeted yesterday that the arrest of Jimmy Lai under Hong Kong’s national security law was “further proof that the CCP has eviscerated Hong Kong’s freedoms and eroded the rights of its people.”