GOLD:$1,938.40 UP $1.00 The quote is London spot price (cash market)

Silver:$25.81// DOWN $0.40 London spot price ( cash market)

shockingly the open interest at the comex (as well as comex + London) rose despite our wicked raid Tuesday. Nobody left the gold arena

In silver: a net 6,000 contracts departed despite our huge $3.25 loss in price.

Billions were of non backed paper in each precious metal were sold short by our bankers. Without a question, this operation was the work of our official sector (BIS)

and this was front- runned by our crooked bankers.

The crooks are also aware that we are going to have a physical exchange in London through the LME. Once set, you will see a physical price of say 2500.00 dollars per oz.

All paper contracts must be converted to real metal. This must be scaring our bankers to no end

Expect another raid tonight/tomorrow

DONATE

Closing access prices: London spot

i)Gold : $1919.20 LONDON SPOT 4:30 pm

ii)SILVER: $25.50//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUGUST GOLD: $1941.70 CLOSE 1::30 PM SPREAD SPOT/FUTURE AUG (CONTANGO $3.40//ABOVE NORMAL)

OCT GOLD: $1937.70 CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: : $0.70//BACKWARD/

DEC. GOLD $2046.70 CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $8.30 ($ BELOW NORMAL CONTANGO)

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $25.86…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : 5 CENT PER OZ ( CONTANGO/NORMAL)

SILVER DECEMBER CLOSE: $26.07 1:30 PM SPREAD SPOT/FUTURE DEC. : 26 CENTS PER OZ ( 14 CENTS ABOVE NORMAL CONTANGO)

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today: 408/1471

ISSUED 74

EXCHANGE: COMEX

CONTRACT: AUGUST 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,932.600000000 USD

INTENT DATE: 08/11/2020 DELIVERY DATE: 08/13/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 333 4

072 H GOLDMAN 221

104 C MIZUHO 96

135 H RAND 4

226 C DIRECT ACCESS 1

323 C HSBC 6

332 H STANDARD CHARTE 36

355 C CREDIT SUISSE 8

363 H WELLS FARGO SEC 1000

657 C MORGAN STANLEY 63

657 H MORGAN STANLEY 141

661 C JP MORGAN 74 263

661 H JP MORGAN 145

685 C RJ OBRIEN 1

686 C INTL FCSTONE 21 1

690 C ABN AMRO 1 93

700 C UBS 42

709 C BARCLAYS 107

709 H BARCLAYS 4

730 C PTG DIVISION SG 1

732 C RBC CAP MARKETS 5

737 C ADVANTAGE 29 23

800 C MAREX SPEC 13 15

880 C CITIGROUP 4

880 H CITIGROUP 174

905 C ADM 13

____________________________________________________________________________________________

TOTAL: 1,471 1,471

MONTH TO DATE: 47,751

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 1471 NOTICE(S) FOR 147,100 OZ (4.5773 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 47,751 NOTICES FOR 477,5100 OZ (148.52 TONNES)

SILVER

FOR AUGUST

32 NOTICE(S) FILED TODAY FOR 160,000 OZ/

total number of notices filed so far this month: 1179 for 5.895 MILLION oz

BITCOIN MORNING QUOTE $11,511 UP 118

BITCOIN AFTERNOON QUOTE.: $11,573 UP 182

GLD AND SLV INVENTORIES:

WITH GOLD UP $1.00 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/// //

A PAPER WITHDRAWAL OF 4.19 TONNES FROM THE GLD///

GLD: 1,257.93 TONNES OF GOLD//

WITH SILVER DOWN $0.40 CENTS TODAY: AND WITH NO SILVER AROUND:

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.141 MILLION OZ//

RESTING SLV INVENTORY TONIGHT:

SLV: 571,632 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A STRONG SIZED 7420 CONTRACTS FROM 205,489 DOWN TO 198,069, AND FURTHER FROM OUR NEW RECORD OF 244,710, (FEB 25/2020. THE LOSS IN OI OCCURRED WITH OUR STRONG $3,25 LOSS IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE LOSS IN COMEX OI IS PRIMARILY DUE TO A SOME BANKER SHORT COVERING PLUS A GOOD EXCHANGE FOR PHYSICAL ISSUANCE, SOME FLUFF LONG LIQUIDATION, ACCOMPANYING A SMALL INCREASE IN SILVER OZ. STANDING AT THE COMEX FOR AUGUST. WE HAD A STRONG NET LOSS IN OUR TWO EXCHANGES OF 6605 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: SEP 815 DEC: 0 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 815 CONTRACTS. WITH THE TRANSFER OF 1320 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 815 EFP CONTRACTS TRANSLATES INTO 4.075 MILLION OZ ACCOMPANYING:

1.THE $3,25 LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

86.470 MILLION OZ FINAL STANDING IN JULY.

6.420 MILLION OZ INITIAL STANDING IN AUGUST

TUESDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL $3,25 ).. AND, OUR OFFICIAL SECTOR/BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO FLEECE SOME SILVER LONGS FROM THEIR POSITIONS. THE CONSIDERABLE LOSS AT THE COMEX WAS ACCOMPANIED BY : i) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A SMALL INCREASE IN SILVER OZ STANDING FOR AUGUST, SOME BANKER SHORT COVERING AND 4) MINIMAL LONG LIQUIDATION AS WE DID HAVE A STRONG NET LOSS OF 6605 CONTRACTS OR 33.025 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKERS ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER..AND THUS THE REASON FOR OUR MASSIVE RAID THIS MORNING!!

SPREADING OPERATIONS/NOW SWITCHING TO SILVER

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN SILVER AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF AUGUST. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

AUGUST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF AUGUST:

9188 CONTRACTS (FOR 8 TRADING DAY(S) TOTAL 9188 CONTRACTS) OR 45.940 MILLION OZ: (AVERAGE PER DAY: 1148 CONTRACTS OR 5.7434 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 45.940 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 4.32% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,317.32 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 133.95 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

AUGUST EXP 45.940 MILLION OZ (EXCHANGE FOR PHYSICALS INCREASING)

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 7420, WITH OUR HUGE $3.25 LOSS IN SILVER PRICING AT THE COMEX ///TUESDAY…THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 815 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE LOST A HUGE SIZED OI CONTRACTS ON THE TWO EXCHANGES: 6605 CONTRACTS (WITH OUR $3.25 LOSS IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 815 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A STRONG SIZED DECREASE OF 7420 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A $3.25 LOSS IN PRICE OF SILVER/AND A CLOSING PRICE OF $26,19 // TUESDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.9925 BILLION OZ TO BE EXACT or 141% of annual global silver production (ex Russia & ex China).

FOR THE NEW AUGUST DELIVERY MONTH/ THEY FILED AT THE COMEX: 32 NOTICE(S) FOR 160,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 WAS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 86.470 million oz//AUGUST 6.420 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 2327 CONTRACTS TO 553,345 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE GOOD GAIN OF COMEX OI OCCURRED DESPITE OUR HUGE FALL IN PRICE OF $92.40 /// COMEX GOLD TRADING// TUESDAY//WE HAD A FAILED BANKER SHORT COVERING, A GOOD SIZED INCREASE IN GOLD TONNAGE STANDING AT THE COMEX FOR AUGUST, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR HUGE LOSS IN PRICE OF $92.40.

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 53

WE GAINED A STRONG SIZED 6032 CONTRACTS (18.76 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3705 CONTRACTS:

CONTRACT .; AUG 0 AND OCT: 100 DEC: 3605; JUNE: 0 ALL OTHER MONTHS ZERO//TOTAL: 3705. The NEW COMEX OI for the gold complex rests at 553,345. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6032 CONTRACTS: 2,327 CONTRACTS INCREASED AT THE COMEX AND 3705 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 6032 CONTRACTS OR 18.76 TONNES. TUESDAY, WE HAD A HUGE LOSS OF $92,40 IN GOLD TRADING…...

AND WITH THAT LOSS IN PRICE, WE HAD A STRONG SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 18.76 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE LOATHE TO SUPPLY SHORT GOLD COMEX PAPER. THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT FELL $92.40). HOWEVER IT SEEMS THAT OUR BANKER FRIENDS WERE NOT HAPPY WITH YESTERDAY’S PERFORMANCE AS WE HAD ANOTHER FAILED BANKER SHORT COVERING TUESDAY//THE BANKERS (OFFICIAL SECTOR) HAVE REGROUPED AND ARE INITIATING ANOTHER MASSIVE RAID ON GOLD/SILVER TUESDAY EVENING. AS WE WITNESSED TODAY, THAT FAILED AS WELL!!

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3705) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI (2327 OI): TOTAL GAIN IN THE TWO EXCHANGES: 6032 CONTRACTS. WE NO DOUBT HAD 1 )A FAILED BANKER SHORT COVERING, 2.)A GOOD INCREASE IN GOLD TONNAGE STANDING AT THE GOLD COMEX FOR THE FRONT AUGUST MONTH, 3) ZERO LONG LIQUIDATION; 4) GOOD COMEX OI GAIN AND 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL AND …ALL OF THIS WAS COUPLED WITH OUR HUGE LOSS IN GOLD PRICE TRADING//TUESDAY//$92,40.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

AUGUST

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES: 57.27 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 57.27/3550 x 100% TONNES =1.63% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3,317.45 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 313.09 TONNES ..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

AUGUST TOTAL EFP ISSUANCE; 57.27 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 7420 CONTRACTS FROM 205,489 DOWN TO 198,069 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE STRONG SIZED LOSS IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) SOME BANKER SHORT COVERING , 2) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A SMALL INCREASE IN SILVER OZ STANDING AT THE SILVER COMEX FOR AUGUST, AND 4) SOME FLUFF MARGINAL LONG LIQUIDATION

EFP ISSUANCE 815 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT: 950 AND DEC. 50 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 815 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 7420 CONTRACTS TO THE 815 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG LOSS OF 6605 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 33.025 MILLION OZ, OCCURRED WITH OUR HUGE $3.25 LOSS IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 21.02 POINTS OR 0.63% //Hang Sang CLOSED UP 353.34 POINTS OR 1.42% /The Nikkei closed UP 93.72 POINTS OR 0.41%//Australia’s all ordinaires CLOSED DOWN .24%

/Chinese yuan (ONSHORE) closed UP at 6.9460 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 6.9460 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9459 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED/CORONAVIRUS /PANDEMIC : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

i) Out of HSBC: 16,160.75 oz

total withdrawals; 16,160.75 oz

We had 1 kilobar transactions +

ADJUSTMENTS: 1 //

customer to dealer

i) Brinks: 96,453.000 oz (3, 000 kilobars)

The front month of AUGUST registered a total of 2259 CONTRACTS as we lost 2226 contracts. We had 2359 notices served on TUESDAY so we GAINED 133 contracts or an additional 13,300 will stand for delivery on this side of the pond as they refused to morph into London based forwards as well as negating a fiat bonus. The boys are scrambling in search of badly needed physical metal.

After August we have the non active Sept contract month.. Here we saw another GAIN of 64 contracts to stand at 2822. Oct GAINED 836 contracts UP to 70,341

The big December contract GAINED 3249 contracts UP to 407,962 contracts… on a HUGE FALL in price???.(FAILED short covering??)

We had 1471 notices filed today for 147,100 oz

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2020. contract month, we take the total number of notices filed so far for the month (47,751) x 100 oz , to which we add the difference between the open interest for the front month of AUGUST (2259 CONTRACTS ) minus the number of notices served upon today (1471 x 100 oz per contract) equals 4,853,900 OZ OR 150.976 TONNES) the number of ounces standing in this active month of JUNE

thus the INITIAL standings for gold for the AUGUST/2020 contract month:

No of notices filed so far (47,751, x 100 oz + (2260 OI) for the front month minus the number of notices served upon today (1471) x 100 oz which equals 4,853,900 oz standing OR 150.9760 TONNES in this active delivery month. This is a HUGE amount for gold standing for a AUGUST delivery month (an active delivery month).

We gained 133 contracts or 13,300 oz of gold as these guys refused to morph into London based forwards.

NEW PLEDGED GOLD: BRINKS

144,088.952 oz NOW PLEDGED JAN 21.2020/HSBC 5.4807 TONNES

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

231,924.295 oz (some deleted august 3) JPM 7.2138 TONNES

611,401.341 oz pledged June 12/2020 Brinks/ july 2/july 21 19.017 tonnes

total pledged gold: 1,029,962.895 oz 32.03 tonnes

total registered, pledged and eligible (customer) gold; 36,741,756.055 oz 1,142.82 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1016.48 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

1,648,127.219 oz

Delaware

Scotia

HSBC

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

1,409,101.386 oz

Brinks

Delaware

JPM

Malca

|

| No of oz served today (contracts) |

32

CONTRACT(S)

(160,000 OZ)

|

| No of oz to be served (notices) |

105 contracts

525,000 oz)

|

| Total monthly oz silver served (contracts) | 1179 contracts

5,895,,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 4 deposits into the customer account

i)into JPMorgan: 1,194,723.050 oz

ii) Into Brinks: 12,569.840 oz

iii) Into Delaware: 992.686 oz

iv) Into Malca: 200,815.810 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 165.57 million oz of total silver inventory or 49.15% of all official comex silver. (165.57 million/336.8577 million

total customer deposits today: 1,409,101.386 oz

we had 3 withdrawals:

i) Out of CNT: 1,546,676.648 oz

ii) Out of Delaware: 17,718.981

iii) Out of HSBC: 83,731.590 oz

total withdrawals; 1,648,127.219 oz

We had 0 adjustments

Total dealer(registered) silver: 128,022 million oz

total registered and eligible silver: 336.577 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

the front month of August registered an open interest of 137 contracts and thus we lost 12 contracts. We had 16 notices filed on TUESDAY so we GAINED 4 contracts or an additional 20,000 oz will stand for delivery as these guys refused to morph into London based forwards as well as negating a fiat bonus for their efforts…. The bankers are now desperate in their search for badly needed silver whether it is on this side of the pond or the European side.

After August we have the big September contract month and here we see a lost 11,742 contracts down to 106,030. November saw another gain of 68 contracts to stand at 253.

The big December contract month saw its OI rise by strong 3900 contracts up to 80,102

We lost some fluff marginal longs but silver in strong hands refuse to leave the silver arena despite the vicious attack, yesterday and today..

The total number of notices filed today for the AUGUST 2020. contract month is represented by 32 contract(s) FOR 160,000, oz

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 1179 x 5,000 oz = 5,895,000 oz to which we add the difference between the open interest for the front month of AUGUST(137) and the number of notices served upon today 32 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the AUGUST/2019 contract month: 1179 (notices served so far) x 5000 oz + OI for front month of AUGUST (137)- number of notices served upon today (32) x 5000 oz of silver standing for the AUGUST contract month.equals 6,420,000 oz. ..VERY STRONG FOR A NON ACTIVE MONTH.

We gained 4 contracts or an additional 20,000 oz will stand for delivery as they refused to morph into London based forwards..

TODAY’S ESTIMATED SILVER VOLUME : 266,857 CONTRACTS // volume huge++++++++++++++++++/

FOR YESTERDAY: 408,323. ,CONFIRMED VOLUME//volume all time record/huge/criminal/

YESTERDAY’S CONFIRMED VOLUME OF 408,323 CONTRACTS EQUATES to 2.041 billion OZ 291% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 4.12% ((AUGUST 12/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1 .39% to NAV: (AUGUST 11/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/4.12%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 19.87 TRADING 19.31///NEGATIVE 2,82

END

And now the Gold inventory at the GLD/

AUGUST 12/ WITH GOLD UP $1.00 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 4.19 TONNES//INVENTORY RESTS AT 1257.93 TONNES

AUGUST 11//WITH GOLD DOWN $92.40 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1262.12 TONNES.

AUGUST 10/WITH GOLD UP $11.35 TODAY, WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.84 TONNES//INVENTORY RESTS AT 1262.12 TONNES

AUGUST 7/WITH GOLD DOWN $38.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1267.96 TONNES

AUGUST 6/WITH GOLD UP $20.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER DEPOSIT OF 10.23 TONNES INTO THE GLD/INVENTORY RESTS AT 1267.96 TONNES//

AUGUST 5/WITH GOLD UP $ 33.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 9.35 TONNES INTO THE GLD//INVENTORY RESTS AT 1257.73 TONNES

AUGUST 4//WITH GOLD UP $31.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 6.48 TONNES/GLD INVENTORY RESTS AT 1248.38 TONNES

AUGUST 3/WITH GOLD UP $2.20 TODAY, WE HAVE NO CHANGES IN THE GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241,96 TONNES

JULY 31/WITH GOLD UP $17.90 TODAY/WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241.96 TONNES.

JULY 30/WITH GOLD DOWN $10.00 TODAY, WE HAVE ANOTHER SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES//INVENTORY RESTS AT 1241.96 TONNES.

JULY 29//WITH GOLD UP $12.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 8.47 TONNES/INVENTORY RESTS AT 1243.12 TONNES

JULY 28///WITH GOLD UP $13.25 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 5.84 TONNES/INVENTORY RESTS AT 1234.65

JULY 27//WITH GOLD UP $35.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF XXX TONNES/INVENTORY RESTS AT 1228.81 TONNES

JULY 24/WITH GOLD UP $8.80 TODAY: WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.80 TONNES//INVENTORY RESTS AT 1228.81 TONNES

JULY 23/WITH GOLD UP $24.90 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 7.26 TONNES/INVENTORY RESTS AT 1225.01 TONNES

JULY 22/WITH GOLD UP $22.00 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 7.89 TONNES/INVENTORY RESTS AT 1219.75 TONNES

JULY 21//WITH GOLD UP $26.00 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.97 TONNES INTO THE GLD// INVENTORY RESTS AT 1211.86 TONNES

JULY 20/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1206.89 TONNES

JULY 17/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1206.89 TONNES

JULY 16/WITH GOLD DOWN $9.80 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: INVENTORY RESTS AT 1206.89 TONNES

JULY 15//WITH GOLD UP $1.55 TODAY/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 2.96 TONNES INTO THE GLD///INVENTORY RESTS AT 1206.89 TONNES

JULY 14//WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 3.51 TONNES/INVENTORY RESTS AT 1203.97 TONNES

JULY 13//WITH GOLD UP $12.50 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1200.46 TONNES

JULY 10/WITH GOLD DOWN $.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD//A STRANGE WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1200.82 TONNES

JULY 9//WITH GOLD DOWN $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OX 3.21 TONNES INTO THE GLD//INVENTORY RESTS AT 1202.57 TONNES

JULY 8/WITH GOLD UP $13.75 TODAY; A BIG CHANGE IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 7.89 TONNES INTO THE GLD//INVENTORY RESTS AT 1199.36 TONNES

JULY 7/WITH GOLD UP $12.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1191.47 TONNES

JULY 6/WITH GOLD UP $6.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1191.47 TONNES

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

AUGUST 12/ GLD INVENTORY 1257.93 tonnes*

LAST; 879 TRADING DAYS: +318.43 NET TONNES HAVE BEEN ADDED THE GLD

LAST 779 TRADING DAYS://+496.96 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

AUGUST 12/WITH SILVER DOWN 40 CENTS TODAY: WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF XX MILLION OZ//INVENTORY RESTS AT XX MILLION OZ/

AUGUST 11/WITH SILVER DOWN $3.25 CENTS, WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.41 MILLION OZ//INVENTORY RESTS AT 571.632 MILLION OZ//

AUGUST 10/WITH SILVER UP 1.89 TODAY, WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 3.538 MILLION OZ/INVENTORY RESTS AT 569.491 MILLION OZ//

AUGUST 7/WITH SILVER DOWN 69 CENTS TODAY: WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY: A DEPOSIT OF 0.465 MILLION OZ/INVENTORY RESTS AT 573.029 MILLION OZ.

AUGUST 6/WITH SILVER UP $1.52 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 572.564 MILLION OZ///

AUGUST 5/WITH SILVER UP $1.03 TODAY, WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A MONSTROUS DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 572.564 MILLION OZ//

AUGUST 4/WITH SILVER UP $1.45 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 367.161 MILLION OZ//

AUGUST 3/WITH SILVER UP 23 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//SURPRISINGLY ANOTHER WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 367.161 MILLION OZ//

JULY 31/WITH SILVER UP 82 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: SURPRISINGLY A HUGE WITHDRAWAL OF 3.26 MILLION OZ//INVENTORY RESTS AT 368.092 MILLION OZ//

JULY 30//WITH SILVER DOWN 97 CENTS TODAY: WE HAVE A SMALL CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 571.352 MILLION OZ//

JULY 29/WITH SILVER UP 7 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY//A DEPOSIT OF 5.984 MILLION OZ//INVENTORY RESTS AT 572.283 MILLION OZ//

JULY 28 WITH SILVER DOWN 14 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 7.52 MILLION OZ//INVENTORY RESTS AT 566.299 MILLION OZ//

JULY 27/WITH SILVER UP $2.67 TODAY, WE HAD NO CHANGES IN SILVER INVENTORY: A DEPOSIT OF XX MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ//

JULY 24/WITH SILVER DOWN $0.12 TODAY: NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 558.779 MILLION OZ/

JULY 23/WITH SILVER UP $.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A HUMONGOUS PAPER DEPOSIT OF 9.594 MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ///

JULY 22/WITH SILVER UP $1.54 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A HUMONGOUS PAPER DEPOSIT OF 7.218 MILLION OZ//INVENTORY RESTS AT 549.185 MILLION OZ/

JULY 21/WITH SILVER UP $1.38 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUMONGOUS PAPER DEPOSIT OF 15.368 MILLION OZ////INVENTORY RESTS AT 541.967 MILLION OZ//

JULY 20/WITH SILVER UP 40 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 3.819 MILLION OZ ‘ENTERED” THE SLV..INVENTORY RESTS AT 526.599 MILLION OZ/

JULY 17/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 1.583 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 522.780 MILLION OZ//

JULY 16//WITH SILVER DOWN 14 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ//INVENTORY RESTS AT 521.197 MILLION OZ..

JULY 15.WITH SILVER UP 21 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.956 MILLION OZ//INVENTORY RESTS AT 516.074 MILLION OZ//

JULY 14/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 514.118 MILLION OZ//

JULY 13//WITH SILVER UP 67 CENTS TODAY: A HUGE CHANGE IN SILVER: A WITHDRAWAL OF 1.677 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 514.118 MILLION OZ//

JULY 10/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 4.844 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.795 MILLION OZ

WHAT A FRAUD!!

JULY 9/WITH SILVER DOWN 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 8.198 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 510.951 MILLION OZ/

JULY 8/WITH SILVER UP 37 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.118 MILLION OZ FROM THE SLV//VERY SURPRISING.//INVENTORY RESTS AT 502.753 MILLION OZ//

JULY 7/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/INVENTORY RESTS AT 503.871 MILLION OZ///

JULY 6//WITH SILVER UP 24 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.863 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 503.871 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

AUGUST 12.2020:

SLV INVENTORY RESTS TONIGHT AT

571,632 MILLION OZ.

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Value of gold stored by Irish metals broker GoldCore surges past €100m

The value of gold coins and bars stored for clients by Irish precious metals broker GoldCore has surged 68pc so far this year to more than €100m.

Gold prices last week topped the $2,000-per-ounce level for the first time as investors seek havens from the pandemic.

“We are seeing demand on a scale which has not been seen since the early stages of the global financial crisis in 2009 and we expect that to continue in the coming months,” said GoldCore CEO Stephen Flood.

NEWS and COMMENTARY

Gold loses ground as dollar firms; investors eye U.S. stimulus

Silver rallies over 6%; Gold ends higher as China-U.S. tensions seen escalating

Why Is Everyone Buying Gold?

Yields hold near historic lows on economic slowdown fears

Dollar rises vs euro, Swiss franc as investors focus on aid package

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

10-Aug-20 2030.30 2044.50 1552.98 1561.38 1725.35 1734.96

07-Aug-20 2061.50 2031.15 1574.37 1559.52 1743.82 1726.88

06-Aug-20 2049.15 2067.15 1555.30 1569.59 1728.87 1743.43

05-Aug-20 2034.45 2048.15 1553.30 1558.03 1718.09 1722.90

04-Aug-20 1972.25 1977.90 1508.77 1519.62 1671.09 1686.56

03-Aug-20 1972.95 1958.55 1509.50 1504.56 1678.39 1670.45

31-Jul-20 1974.70 1964.90 1505.91 1492.54 1666.84 1661.72

30-Jul-20 1952.20 1957.65, 1503.00 1502.10 & 1662.30 1662.44

29-Jul-20 1954.35 1950.90, 1506.80 1502.39 & 1663.54 1659.24

28-Jul-20 1931.65 1940.90, 1499.15 1501.48 & 1647.70 1654.23

27-Jul-20 1940.55 1936.65, 1511.30 1504.78 & 1659.56 1647.70

24-Jul-20 1893.85 1902.10, 1486.67 1490.30 & 1631.55 1638.09

23-Jul-20 1882.35 1878.30, 1480.28 1477.47 & 1624.47 1621.54

22-Jul-20 1851.00 1852.40, 1462.85 1456.91 & 1604.82 1598.44

21-Jul-20 1823.20 1842.55, 1436.86 1449.35 & 1594.21 1608.36

20-Jul-20 1810.30 1815.65, 1437.92 1438.18 & 1580.21 1590.87

17-Jul-20 1802.90 1807.35, 1435.47 1442.45 & 1578.98 1581.07

Own gold and silver coins and bars in the safest vaults in Zurich, Singapore, London and Dublin with GoldCore.

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here

ii) Important gold commentaries courtesy of GATA/Chris Powell

For all of our coin collectors out there…..

First U.S. silver coin, minted in 1794, offered at auction

Submitted by cpowell on Tue, 2020-08-11 14:50. Section: Daily Dispatches

1794 Silver Dollar, Worth $10 Million, for Sale by New Jersey Dealer; ‘This Coin Is the Holy Grail’

By David P. Willis

Asbury Park Press, Asbury Park, New Jersey

Tuesday, Augustd 11, 2020

A rare 1794 U.S. silver dollar, believed to be the first ever silver dollar minted by a newborn United States, is going up for sale by a Middletown coin dealer.

“This coin is the Holy Grail of all dollars,” said Laura Sperber, president of Legend Numismatics in Middletown’s Lincroft section. The sale, by Legend Auctions, will be held Oct. 8 at The Venetian Hotel in Las Vegas and online

Bruce Morelan, a Las Vegas collector, purchased the coin, nicknamed the “Flowing Hair Silver Dollar,” in 2013 for $10 million, the most ever paid for a rare coin. It features Lady Liberty ringed with stars on one side and an eagle on the other.

“Of the 1,758 silver dollars the Mint delivered in October 1794, perhaps fewer than 130 are known to survive, and this particular coin is the finest known,” said Brett Charville, president of Professional Coin Grading Service, a rare coin authentication company, in a statement.

“It is believed to the very first one struck,” Sperber said. It is “extremely significant.”

It was presented to then-U.S. Secretary of State Edmund Jennings Randolph, who referred to it with a letter to President George Washington. …

… For the remainder of the report and photographs of the coin:

https://www.app.com/story/money/business/main-street/2020/08/11/1794-flo…

* * *

END

Alasdair Macleod states that dips in gold and silver will be bought because both metals are so scarce

(Kingworldnews/Alasdair Macleod)

Dips in gold, silver will be bought because metal is so scarce, GoldMoney’s Macleod tells KWN

Submitted by cpowell on Tue, 2020-08-11 15:12. Section: Daily Dispatches

11:12a ET Tuesday, August 11, 2020

Dear Friend of GATA and Gold:

11:10a ET Tuesday, August 11, 2020

Dear Friend of GATA and Gold:

In comments to King World News, GoldMoney research director Alasdair Macleod explains why he thinks a collapse of gold and silver prices isn’t likely. Foremost among his reasons is simply that real metal is in short supply and declines in futures prices will continue to be bought in expectation of standing for delivery.

Macleod’s comments are posted at KWN here:

https://kingworldnews.com/exclusive-alasdair-macleod-why-a-big-correctio…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

The Fed allows the big banks to rig their own stress tests!!

crooks!

(Pam and Russ Martens/Wall Street on Parade)

Pam and Russ Martens: Fed lets big banks rig their stress tests

Submitted by cpowell on Tue, 2020-08-11 15:25. Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Tuesday, August 11, 2020

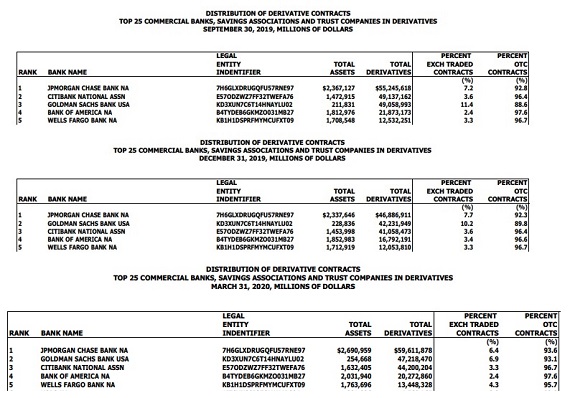

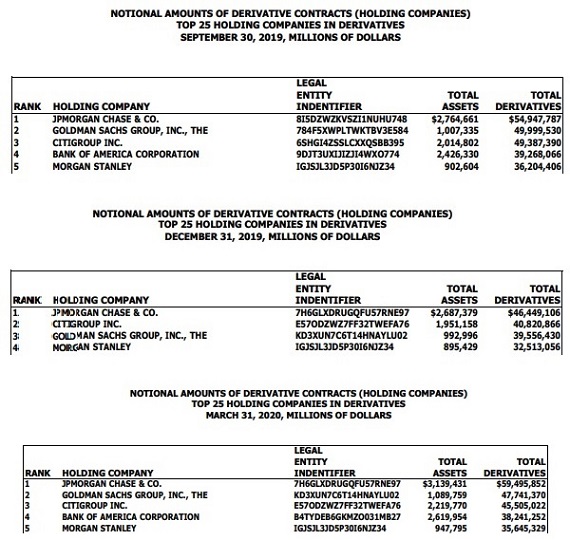

On January 31 this year, researchers for the Federal Reserve released a study that showed that the largest banks operating in the United States have been gaming their stress test results by intentionally dropping their exposure to over-the-counter derivatives in the fourth quarter. The fourth quarter data is the information used by the Federal Reserve to determine surcharges on capital for Global Systemically Important Banks, or G-SIBs.

The report, “How Do U.S. Global Systemically Important Banks Lower Their Capital Surcharges?,” was written by Jared Berry, Akber Khan, and Marcelo Rezende.

…

We decided to evaluate this claim for ourselves, using the quarterly derivative reports provided by the Office of the Comptroller of the Currency, the regulator of national banks.

The data was appalling.

The largest Wall Street banks not only dropped their level of derivatives by trillions of dollars in the fourth quarter, but they restored those derivatives by the end of the following first quarter.

In the case of JPMorgan Chase, the bank dropped its total derivatives from $55 trillion notional (face amount) in the third quarter to $46.9 trillion in the fourth quarter of 2019, a decline of $8 trillion in one quarter or 15 percent. But by the end of the first quarter of 2020, JPMorgan had pushed those derivatives back up to $59.6 trillion. …

… For the remainder of the report:

https://wallstreetonparade.com/2020/08/bombshell-report-fed-is-aware-tha…

* * *

Bombshell Report: Fed Is Aware that Big Banks Are Rigging their Stress Tests and Letting Them Get Away with It

By Pam Martens and Russ Martens: August 11, 2020 ~

On January 31 of this year, researchers for the Federal Reserve released a study that showed that the largest banks operating in the U.S. have been gaming their stress test results by intentionally dropping their exposure to over-the-counter derivatives in the fourth quarter. The fourth quarter data is the information used by the Federal Reserve to determine surcharges on capital for Global Systemically Important Banks, or G-SIBs.

The report, “How Do U.S. Global Systemically Important Banks Lower Their Capital Surcharges?,” was written by Jared Berry, Akber Khan, and Marcelo Rezende.

We decided to evaluate this claim for ourselves, using the quarterly derivative reports provided by the Office of the Comptroller of the Currency (OCC), the regulator of national banks. The data was appalling. The largest Wall Street banks not only dropped their level of derivatives by trillions of dollars in the fourth quarter, but they restored those derivatives by the end of the following first quarter. (See first OCC chart below which shows the largest of the top 25 banks by derivative exposure.)

In the case of JPMorgan Chase, it dropped its total derivatives from $55 trillion notional (face amount) in the third quarter to $46.9 trillion in the fourth quarter of 2019, a decline of $8 trillion in one quarter or 15 percent. But by the end of the first quarter of 2020, JPMorgan had pushed those derivatives back up to $59.6 trillion.

The Federal Reserve seems to be accepting this behavior from JPMorgan Chase as a legitimate means of reducing its capital requirements. Yesterday, the Federal Reserve announced the new capital requirements for the largest, Global Systemically Important Banks, or G-SIBs. We fully expected JPMorgan Chase to be slapped with the highest capital requirement since its Systemic Risk Report last year showed it to be the riskiest bank in the U.S. and, clearly, based on the above research that appears on the Fed’s own website, it’s aware of JPMorgan’s “window dressing,” the term used by its own researchers.

But instead of JPMorgan Chase getting slapped with the highest Common Equity Tier 1 (CET1) capital requirement of all 34 banks that underwent the stress test, it was given a relatively tame 11.3 percent CET1. The banks hit with the highest CET1 capital requirements were Goldman Sachs at 13.7 percent and Morgan Stanley at 13.4 percent. (See the Fed’s full chart of capital requirements here.)

Morgan Stanley does not show up on the first OCC chart below because it holds its huge derivatives book at its bank holding company, rather than at its federally-insured commercial banks. The second OCC chart below suggests that Morgan Stanley was also window-dressing its derivatives book, dropping it from $36.2 trillion in the third quarter of 2019 to $32.5 trillion in the fourth quarter; then back to $35.6 trillion in the first quarter of 2020.

Goldman Sachs and Morgan Stanley came away with a higher CET1 capital requirement than even Deutsche Bank’s U.S. entity, DB USA, which was assigned a CET1 capital requirement of 12.3 percent. That’s really saying something. Deutsche Bank has lost money in four of the last five years, including a whopping $5.8 billion last year. Its stock price has evaporated 90 percent of its value since 2007 and it has been repeatedly hit with large fines by regulators for money laundering.

All of this is just further evidence that Congress needs to take away the supervisory powers over banks from the Federal Reserve; strip it of its ability to bail them out; and restrict the Fed to setting monetary policy. Those restrictions can’t arrive soon enough.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

iii) Other physical stories:

TUESDAY NIGHT/GOLD AND SILVER EARLY EVENING TRADING:

Precious Metal Pummeling Continues In Early Asia Trading

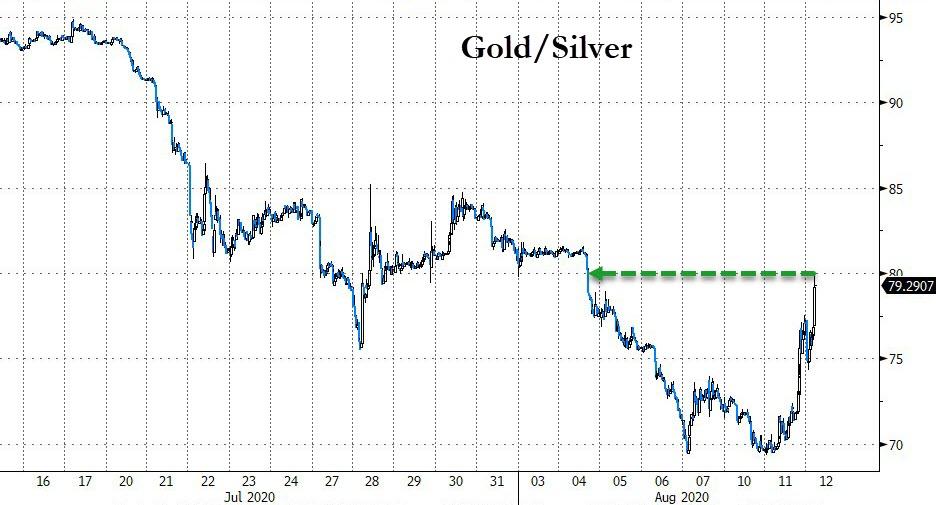

As Bloomberg’s Mark Cranfield noted this evening, small reversals are just not gold’s style after a major advance (typically somewhere between a 15% and 20% drop is more common), and the selling pressure on precious metals has continued as Japan and then China opens this evening with Silver futures back at a $23 handle and Gold futures back below $1900.

Sending the gold/silver ratio soaring…

After finding support at 2017 lows…

As Peter Schiff noted earlier:

Nothing goes up every single day, and gold and silver are not going to be the exception to that rule. There are no bull markets that are up every day. You’re always going to have down days.”

Peter said the fundamentals are better than any he’s ever seen.

The Federal Reserve is printing trillions of dollars. Fed Chair Jerome Powell has said it isn’t even thinking about thinking about raising interest rates. And there are reports that the central bank is set to make a commitment to ramping up inflation. All of this is extremely bullish for gold.

In a CNBC interview, US Global Investors CEO Frank Holmes said he can see $4,000 gold in the relatively near future with G-20 finance ministers and central banks “working together like a cartel and they’re all printing trillions of dollars.”

We’ve not seen this level where central banks are printing money at a zero interest rate. At zero interest rates, gold becomes a very, very attractive asset class,” Holmes said.

You have to focus on the fundamentals. A lot of investors aren’t doing that.

They’re not looking into the future and realizing the monetary fiscal policies that have already driven gold past $2,000 are going to continue and drive it past $3,000, $4,000, $5,000… And therein lies the opportunity.”

Finally, we note that Central banks added another net 18.1 tons of gold to their reserves in June, according to the latest data from the World Gold Council, who also found that 20% of central banks globally plan to expand their gold holdings in 2020.

Factors related to the economic environment – such as negative interest rates – were overwhelming drivers of these planned purchases. This was supported by gold’s role as a safe haven in times of crisis, as well as its lack of default risk.”

This year’s surge in precious metals, as Peter Schiff warns, is not a happy occasion because it really portends some real big problems on the horizon. I mean, most Americans don’t have any gold. There is severe economic hardship that the vast majority of Americans are going to be enduring, and gold is basically letting you know that that hardship is on the way.”

END

Bill Holter…

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Futures Rebound Back Near All Time Highs, Precious Metals Bounce After Crash

Reversing yesterday’s sharp Nasdaq and precious metals-led selloff, S&P futures rebounded from Tuesday’s drop ignoring the continuing deadlock in Washington on more stimulus spending which could significantly delay the U.S. virus rescue package, and pushing the Emini to within inches of the all time high.

Energy stocks Exxon Mobil gained 1.1% and Chevron Corp added 1.5% in premarket trading, alongside gains in ConocoPhillips, Marathon Oil Corp. and other oil drillers all of which rose pre-market as crude futures approached a five-month high. Nasdaq 100 contracts also climbed after the index dropped for three days, an unheard of event. Tesla rose 5.7% as it announced a five-for-one stock split in an attempt to make its shares more accessible to employees and investors. The fact that a stock split has added billions to a company’s market cap just shows how broken everything in this “market” truly is.

On Tuesday, the S&P 500 Index fell for the first time in eight sessions after the benchmark index came within 0.15% of its closing record high, powered by historic fiscal and monetary stimulus and signs of a nascent economic recovery, and sparking speculation that a rotation out of the tech stocks may happen soon.

“The bias at moment is probably to fade the S&P 500 and fade risk generally,” said Societe Generale strategist Kit Juckes. “What happens next probably depends on what happens in U.S. equity markets (which are focused on stimulus)… That might be the decisive factor for short-term sentiment.”

Barring a bipartisan deal on stimulus, the U.S. economy could be left with measures U.S. President Donald Trump called for on Saturday through executive orders to bypass Congress.

“We have enormous uncertainty. It appears it’s getting harder for both sides to compromise as the election is nearing… Trump’s proposals would be smaller than markets have expected. There’s question over whether they are viable, too,” said Junpei Tanaka, strategist at Pictet.

Europe’s Stoxx 600 Index edged up thanks to gains in telecom and bank shares. Advances in ABN Amro Bank NV and HSBC Holdings Plc and drugmakers Novartis AG and GlaxoSmithKline Plc offset declines in tech, aviation and real estate shares. Elsewhere, Europe’s corporate bond spreads narrowed to their tightest since early March, just a few basis points off pre-virus levels, according to a Bloomberg Barclays index.

Earlier in the session, mixed sentiment dragged on Asian stocks as sniping continued between China and the United States. Beijing also reported weaker-than-expected loan growth, while the U.S. Senate’s majority leader described stimulus talks there overnight as “at a bit of a stalemate”.

Investors are weighing whether a rotation in equities is playing out as pandemic high-flyers including AMD and Zoom Video tumbled on Tuesday. There’s some portfolio switching “given the constant flurry of concerns about crowded positioning and stretched valuations in growth sectors such as tech and communication services,” said Matthew Sherwood, head of investment strategy for multi-asset at Perpetual Investment. “Value and cyclicals continue to be supported by positive economic surprise momentum.”

With a better-than-feared (but still down over 30% Y/Y) second-quarter earnings season largely over, attention will turn to the upcoming U.S. presidential elections. Democratic candidate Joe Biden on Tuesday picked Senator Kamala Harris as his choice for vice president.

In FX, the Bloomberg Dollar Spot Index was unchanged after earlier declining for the first time in four days, which the euro reversed an early decline to rise for a second day. The Norwegian krone and the Swedish krona led gains among Group-of-10 currencies as oil and regional equities advanced. NZD/USD fell for a fourth day, sliding as much as 0.8%, as the Reserve Bank of New Zealand boosted its Large Scale Asset Program to as much as NZ$100 billion ($65 billion) and said negative rates remained in “active preparation.” Turkey’s volatile lira took another 1.5% pounding as concerns about its economic health and policy making took hold again, while New Zealand dollar’s dropped 0.4% after its central bank signalled it would stay highly supportive.

In rates, U.S. Treasuries yield climbed a couple of basis points to 0.67% in Europe to stay at a one-month high. The 10-year yield (+6.6bps) and 30-year (+7.5bps) yields saw their biggest increases in over a month on Tuesday, while the 2s10s curve steepened 4.6 basis points, the most since June 5th. The gap between U.S. two-year and 10-year Treasury yields is a metric closely watched for signs of a slowdown. On Wednesday, yields were cheaper by 1bp to 4bp across the curve with 20-year sector faring worst; long-end underperformance steepens 2s10s by more than 2bp to 51.3bp, 5s30s to 106.8bp, both highest since early July. 10-year yield at 0.671% is highest since July 7 and above its 50- and 100-DMAs. In Europe, bunds lagged by 1bp while 30-year German bond yield turns positive for first time since July. Refunding auctions resume with $38b 10-year at 1pm ET, conclude with $26b 30-year Thursday, both all-time high sizes. The WI 10-year yield ~0.69% is cheaper than July’s record low stop at 0.653%, which was ~1bp lower than WI yield at the bidding deadline.

In commodities, oil prices edged up after bigger-than-expected drop in U.S. inventories, with Brent up 0.6% at $44.75 a barrel. U.S. crude was up 0.5% at $41.80. Silver halted its selloff with gold, as investors decided the flight from precious metals amid advancing bond yields had gone too far.

Expected data include inflation. Royalty Pharma, Cisco, Lyft and Trulieve Cannabis are among companies reporting earnings

Market Snapshot

- S&P 500 futures up 0.7% to 3,352.75

- STOXX Europe 600 up 0.1% to 371.20

- MXAP up 0.2% to 169.90

- MXAPJ down 0.09% to 561.67

- Nikkei up 0.4% to 22,843.96

- Topix up 1.2% to 1,605.53

- Hang Seng Index up 1.4% to 25,244.02

- Shanghai Composite down 0.6% to 3,319.27

- Sensex down 0.1% to 38,351.33

- Australia S&P/ASX 200 down 0.1

- German 10Y yield rose 3.0 bps to -0.448%

- Euro up 0.1% to $1.1755

- Italian 10Y yield rose 2.2 bps to 0.817%

- Spanish 10Y yield rose 2.1 bps to 0.3%

- Brent futures up 1% to $44.95/bbl

- Gold spot up 1.2% to $1,934.56

- U.S. Dollar Index little changed at 93.60

Top Overnight News from Bloomberg

- The U.K. suffered the worst economic downturn in Europe, with a 20.4% contraction in the second quarter, pushing the country in its first recession since 2009

- China is to bring up the recent measures brought by President Donald Trump against the WeChat and TikTok apps during upcoming trade talks with the U.S. this week. The trade review, for which an exact date hasn’t been released yet, comes in a context of growing hostility between the two superpowers

- California reported a surge in coronavirus cases, nations in Asia are struggling to contain new waves of infections, and European countries report new increases, a reminder that the battle against the virus is far from over. But there are encouraging vaccine news, including Russian President Vladimir Putin’s announcement that his government has cleared the first Covid vaccine before clinical tests are finished

A quick look at global markets courtesy of RanSquawk:

Asian equity markets traded with a lacklustre tone following on from a weak lead from US where the major indices faltered in late trade after comments from US Senate Majority Leader McConnell dashed some stimulus hopes and saw the S&P 500 retrace its earlier gains which had initially pushed the index to within 1% of its all-time high. ASX 200 (-0.1%) was subdued with underperformance seen in gold miners following the aggressive pullback in the precious metal which retreated firmly below the USD 2000/oz level. Furthermore, nearly all its sectors languished in the red aside from financials which showed some resilience despite CBA posting an 11.3% decline in FY cash profits, while recent data releases contributed to the dampened mood after a further deterioration in Westpac Consumer Sentiment and with Wage Growth at its slowest pace in 27 years. Nikkei 225 (+0.4%) was choppy as participants digested earnings including SoftBank which was pressured following a drop in Q1 pre-tax profits, and NZX 50 (-1.3%) suffered from lockdown restrictions following reports of the country’s first COVID-19 cases after having gone 102 days without any locally-transmitted spread of the virus, although some of the losses were stemmed following the RBNZ announcement to expand its QE program. Elsewhere, Hang Seng (+1.4%) and Shanghai Comp. (-0.6%) initially conformed to the glum mood despite a strong liquidity effort by the PBoC which injected CNY 140bln through 7-day reverse repos as participants also react to weaker than expected lending data from China and as US-China tensions lingered. Finally, 10yr JGBs are weaker in the aftermath of yesterday’s extended retreat and following recent losses in T-notes, while participants were also kept sidelined amid the enhanced liquidity auction for longer dated JGBs which attracted weaker interest than prior.

Top Asian News

- Abu Dhabi Is Said to Seek Local Investors for Gas Pipelines

- Alibaba-Backed Best to List Delivery Business in H.K.: Reuters

- Softbank-Backed KE Poised to Raise $2.1 Billion in U.S. IPO

- Singapore Regulator Warns of More Bank Job Losses in Second Half

European equities trade flat/firmer after an uninspiring cash open [Euro Stoxx 50 +0.1%] as sentiment somewhat improved from a downbeat APAC handover. News flow has again been light in early hours with little by way of fresh fundamental catalysts to shift the dials. That being said, the DAX (-0.2%) holds its position as the laggard as heavyweight SAP (-0.9%) fails to trim losses amid the broad tech underperformance seen Wall St and Asia-Pac, whilst the FTSE 100 (+0.6%) trades on the other side of the spectrum bolstered by its heavy energy and financials exposure. Sectors are mixed with no clear risk profile to be derived, with the breakdown seeing banking names among the gainers after ABN AMRO (+5.3%) reported lower than expected loan loss provisions whilst Q2 operating income was more-or-less in-line with forecasts. The energy sector meanwhile is propped up by price action in the oil complex, whilst Travel & Leisure remains pressured amid fears of the impact of resurging cases in the sector. In terms of individual movers, Sunrise Communications (+26%) soared at the open and held onto gains as Liberty is to acquire Co. for CHF 110/shr for a total of CHF 6.8bln. Note, shares closed at CHF 86.20 yesterday. E.ON (-1.6%) remains in the red after cutting its FY adj. net guidance and EBIT guidance. Asos (+4.6%) remains firmer, albeit off highs, after the group noted that profit before tax for the FY is expected to be significantly ahead of market forecasts.

Top European News

- M&G Commits to Dividend in Face of Retail Investor Fund Exodus

- ABN Amro Cuts a Third of Investment Bank After Virus Losses

- Just Eat Takeaway’s 1H Orders Jumped 32% During Pandemic

In FX, the Kiwi has fallen further from recent highs on renewed 2nd wave pandemic concerns following an outbreak in Auckland and reports that up to 4 more people may have contracted the virus, while latest negative OCR vibes via the RBNZ have also undermined sentiment more so than the LSAP extension and increase to Nzd 100 bn from Nzd 60 bn that was widely expected. Nzd/Usd is now hovering below 0.6550 and Aud/Nzd fading from 1.0900+ peaks overnight, as the Aussie drifts back towards 0.7100 in wake of Westpac’s August consumer sentiment showing a downturn in morale and Q2 wages sub-consensus for the weakest y/y rate of growth in 27 years.

- USD – More real yield appreciation and associated GOLD depreciation (Xau down through Usd 1900/oz at one stage) boosted the Buck across the board, with the DXY hitting 93.909 before waning ahead of 94.000 and last week’s 93.997 apex after a late swoon on Wall Street amidst the ongoing fiscal relief stalemate. Ahead, US CPI comes hot on the heels of firmer than forecast PPI reads, but unlikely to impact much in the current less data-centric mood.

- JPY – Another victim of relative Dollar strength and US Treasury curve concessions for Quarterly Refunding, as Usd/Jpy shifts into a loftier range in the upper 106.00 region and Eur/Jpy rebounds from just shy of 125.00 to around 125.55.

- SEK/NOK/CHF/EUR/GBP/CAD – The tide has turned somewhat in Scandinavia where the Swedish Crown has been inflated by firmer CPI prints to an extent, while the Norwegian Krona has lost momentum alongside crude prices, but both are still outperforming vs the Euro circa 10.2600 and 10.5500 respectively as the single currency tops out against the Greenback following unsuccessful attempts to clear 1.1800 and the 200 HMA near the round number. Elsewhere, the Franc is paring declines from 0.9200, but respecting resistance at 0.9150 and Sterling has recoiled from 1.3100+ on Tuesday to test support into 1.3000, largely shrugging off not quite as bad as feared, though still pretty abject UK GDP along the way. Similarly, the Loonie handed back more gains vs its US counterpart as oil slipped and broad risk sentiment/appetite dipped before bouncing circa 1.3350.

- EM – Payback after yesterday’s strong recovery rallies, and perhaps a few signs of Cny/Cnh caution in the run up to Saturday’s US-Sino Summit as China’s Foreign Ministry warns against the danger of playing with fire in reference to US Health Chief Azar’s trip to Taiwan.