GOLD::$1,942.10 DOWN $19.45 The quote is London spot price (cash market)

Silver:$26.26 DOWN $1.31 London spot price ( cash market)

DONATE

Closing access prices: London spot

i)Gold : $1944.50 LONDON SPOT 4:30 pm

ii)SILVER: $26.45//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUGUST GOLD: $1937.70 CLOSE 1::30 PM SPREAD SPOT/FUTURE AUG (BACKWARD $4.60//)

OCT GOLD: $1943.30 CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: : $1,20//SLIGHT CONTANGO//BELOW NORMAL CONTANGO/

DEC. GOLD $1952.80 CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $10.70 ($ BELOW NORMAL CONTANGO)

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $26.35…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : 11 CENT PER OZ ( CONTANGO/NORMAL)

SILVER DECEMBER CLOSE: $26.51 1:30 PM SPREAD SPOT/FUTURE DEC. : 25 CENTS PER OZ ( 13 ABOVE NORMAL CONTANGO)

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today: 9/31

issued: 0

EXCHANGE: COMEX

CONTRACT: AUGUST 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,956.700000000 USD

INTENT DATE: 08/13/2020 DELIVERY DATE: 08/17/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 H GOLDMAN 4

104 C MIZUHO 2

657 C MORGAN STANLEY 4

657 H MORGAN STANLEY 5

661 C JP MORGAN 6

661 H JP MORGAN 3

690 C ABN AMRO 21

709 C BARCLAYS 2

732 C RBC CAP MARKETS 1

737 C ADVANTAGE 5

800 C MAREX SPEC 5 1

880 H CITIGROUP 3

____________________________________________________________________________________________

TOTAL: 31 31

MONTH TO DATE: 48,035

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 31 NOTICE(S) FOR 3100 OZ (0.0984 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 48,035 NOTICES FOR 4,803,500 OZ (149.409 TONNES)

SILVER

FOR AUGUST

3 NOTICE(S) FILED TODAY FOR 15,000 OZ/

total number of notices filed so far this month: 1270 for 6.350 MILLION oz

BITCOIN MORNING QUOTE $11,747 DOWN 20

BITCOIN AFTERNOON QUOTE.: $11,810 UP 35

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $19.45 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/// //

A STRONG PAPER DEPOSIT OF 1.46 TONNES INTO THE GLD///

GLD: 1,252.09 TONNES OF GOLD//

WITH SILVER DOWN $1.31 CENTS TODAY: AND WITH NO SILVER AROUND:

A HUGE CHANGES IN SILVER INVENTORY AT THE SLV//

A WITHDRAWAL OF 6.894 MILLION OZ

RESTING SLV INVENTORY TONIGHT:

SLV: 574.053 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A GOOD SIZED 957 CONTRACTS FROM 196,666 UP TO 197,623, AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE GAIN IN OI OCCURRED WITH OUR STRONG $1.76 GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS PRIMARILY DUE TO A MASSIVE BANKER SHORT COVERING PLUS A SMALL EXCHANGE FOR PHYSICAL ISSUANCE, NO LONG LIQUIDATION, ACCOMPANYING A SMALL INCREASE IN SILVER OZ. STANDING AT THE COMEX FOR AUGUST. WE HAD A STRONG NET GAIN IN OUR TWO EXCHANGES OF 1259 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: SEP 152 DEC: 150 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 302 CONTRACTS. WITH THE TRANSFER OF 302 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 302 EFP CONTRACTS TRANSLATES INTO 4.700 MILLION OZ ACCOMPANYING:

1.THE $1.87 GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

86.470 MILLION OZ FINAL STANDING IN JULY.

6.430 MILLION OZ INITIAL STANDING IN AUGUST

THURSDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE $1.76 ).. AND, OUR OFFICIAL SECTOR/BANKERS WERE NOT ONLY UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS BUT THEY ALSO ENGAGED IN A MASSIVE BANKER SHORT COVERING. THE GOOD SIZED GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A SMALL INCREASE IN SILVER OZ STANDING FOR AUGUST, MASSIVE BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A GOOD NET GAIN OF 1259 CONTRACTS OR 6.295 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKERS ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER..AND THUS THE REASON FOR OUR MASSIVE RAID THIS MORNING!!

SPREADING OPERATIONS/NOW SWITCHING TO SILVER

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN SILVER AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF AUGUST. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

AUGUST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF AUGUST:

10,703 CONTRACTS (FOR 10 TRADING DAY(S) TOTAL 10,703 CONTRACTS) OR 53.515 MILLION OZ: (AVERAGE PER DAY: 1070 CONTRACTS OR 5.3515 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 53.515 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 4.32% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,323.81 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 133.95 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

AUGUST EXP 53.51 MILLION OZ (EXCHANGE FOR PHYSICALS INCREASING)

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 957, WITH OUR $1.87 GAIN IN SILVER PRICING AT THE COMEX ///THURSDAY…THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 575 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A STRONG SIZED 1259 OI CONTRACTS ON THE TWO EXCHANGES (WITH OUR $1.87 RISE IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 322 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A GOOD SIZED INCREASE OF 957 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A $1.87 GAIN IN PRICE OF SILVER/AND A CLOSING PRICE OF $27.66 // THURSDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.9925 BILLION OZ TO BE EXACT or 141% of annual global silver production (ex Russia & ex China).

FOR THE NEW AUGUST DELIVERY MONTH/ THEY FILED AT THE COMEX: 3 NOTICE(S) FOR 15,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 WAS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 86.470 million oz//AUGUST 6.445 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A TINY SIZED 768 CONTRACTS TO 548,726 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE SMALL SIZED LOSS OF COMEX OI OCCURRED DESPITE OUR STRONG GAIN IN PRICE OF $23.15 /// COMEX GOLD TRADING// THURSDAY//WE HAD A MASSIVE BANKER SHORT COVERING, A SMALL SIZED INCREASE IN GOLD TONNAGE STANDING AT THE COMEX FOR AUGUST, ALONG WITH MINIMAL LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR STRONG GAIN IN PRICE OF $23.15.

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 138

WE LOST A TINY SIZED 193 CONTRACTS (0.600 TONNES) ON OUR TWO EXCHANGES.(MASSIVE BANKER SHORT COVERING)

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 575 CONTRACTS:

CONTRACT .; AUG 0 AND OCT: 0 DEC: 575; JUNE: 0 ALL OTHER MONTHS ZERO//TOTAL: 575. The NEW COMEX OI for the gold complex rests at 548,726. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A TINY SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 193 CONTRACTS: 769 CONTRACTS DECREASED AT THE COMEX AND 575 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 193 CONTRACTS OR 0.600 TONNES. THURSDAY, WE HAD A STRONG GAIN OF $23.15 IN GOLD TRADING.…..

AND DESPITE THAT GAIN IN PRICE, WE HAD A TINY SIZED LOSS IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 0.60 TONNES!!!!!! THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $23.15). HOWEVER WE DID HAVE A MASSIVE BANKER SHORT COVERING SESSION ON THURSDAY//

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (575) ACCOMPANYING THE TINY SIZED LOSS IN COMEX OI (769 OI): TOTAL LOSS IN THE TWO EXCHANGES: 193 CONTRACTS. WE NO DOUBT HAD 1 )A MASSIVE BANKER SHORT COVERING, 2.)A SMALL INCREASE IN GOLD TONNAGE STANDING AT THE GOLD COMEX FOR THE FRONT AUGUST MONTH, 3) ZERO LONG LIQUIDATION; 4) SMALL COMEX OI LOSS AND 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL AND …ALL OF THIS WAS COUPLED WITH OUR HUGE GAIN IN GOLD PRICE TRADING//THURSDAY//$23.15.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

AUGUST

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAY(S) IN TONNES: 79.00 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 77.21/3550 x 100% TONNES =2.17% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3,339.19 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 313.09 TONNES ..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

AUGUST TOTAL EFP ISSUANCE; 79.00 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GOOD SIZED 957 CONTRACTS FROM 196,666 UP TO 197,623 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE GAIN IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) MASSIVE BANKER SHORT COVERING , 2) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A SMALL INCREASE IN SILVER OZ STANDING AT THE SILVER COMEX FOR AUGUST, AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 302 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT: 252 AND DEC. 50 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 302 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 957 CONTRACTS TO THE 302 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 1259 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 6.295 MILLION OZ, OCCURRED WITH OUR $1.87 GAIN IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 39.37 POINTS OR 1.19% //Hang Sang CLOSED DOWN 47.66 POINTS OR 0.19% /The Nikkei closed UP 39.75 POINTS OR 0.10%//Australia’s all ordinaires CLOSED DOWN .61%

/Chinese yuan (ONSHORE) closed DOWN at 6.9500 /Oil UP TO 42.16 dollars per barrel for WTI and 44.91 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9500 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9498 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED //CORONAVIRUS/PANDEMIC : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

i) Out of Malca: 32151.000 oz 1000 kilobars

ii) Out of Manfra: 482.265 oz

total withdrawals; 32,633.265 oz

We had 02 kilobar transactions +

ADJUSTMENTS: 0 //

The front month of AUGUST registered a total of 613 CONTRACTS as we lost 251 contracts. We had 253 notices served on THURSDAY so we GAINED 2 contracts or an additional 200 will stand for delivery on this side of the pond as they refused to morph into London based forwards as well as negating a fiat bonus. The boys are scrambling in search of badly needed physical metal.

After August we have the non active Sept contract month.. Here we saw another LOSS of 43 contracts to stand at 2451. Oct GAINED 687 contracts UP to 70,421

The big December contract LOST 1325 contracts DOWN to 405,157 contracts…

We had 31 notices filed today for 3100 oz

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2020. contract month, we take the total number of notices filed so far for the month (48,035) x 100 oz , to which we add the difference between the open interest for the front month of AUGUST (613 CONTRACTS ) minus the number of notices served upon today (31 x 100 oz per contract) equals 4,861,700 OZ OR 151.219 TONNES) the number of ounces standing in this active month of JUNE

thus the INITIAL standings for gold for the AUGUST/2020 contract month:

No of notices filed so far (48,035, x 100 oz + (613 OI) for the front month minus the number of notices served upon today (31) x 100 oz which equals 4,861,700 oz standing OR 151.219 TONNES in this active delivery month. This is a HUGE amount for gold standing for a AUGUST delivery month (an active delivery month).

We gained 2 contracts or 200 oz of gold as these guys refused to morph into London based forwards.

THE NAME OF THE GAME TODAY IS A MASSIVE BANK SHORT COVERING AS FINALLY FEAR BECAME THEIR CENTRAL FOCUS

NEW PLEDGED GOLD: BRINKS

144,088.952 oz NOW PLEDGED JAN 21.2020/HSBC 5.4807 TONNES

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

231,924.295 oz (some deleted august 3) JPM 7.2138 TONNES

611,401.341 oz pledged June 12/2020 Brinks/ july 2/july 21 19.017 tonnes

total pledged gold: 1,029,962.895 oz 32.03 tonnes

total registered, pledged and eligible (customer) gold; 36,963,022.861 oz 1,149.70 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1023,36 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

301,895.740 oz

CNT

Scotia

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

1,134,863.019 oz

CNT

Delaware

Scotia

|

| No of oz served today (contracts) |

3

CONTRACT(S)

(14,000 OZ)

|

| No of oz to be served (notices) |

19 contracts

195,000 oz)

|

| Total monthly oz silver served (contracts) | 1270 contracts

6,350,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 4 deposits into the customer account

i)into JPMorgan: 1,194,723.050 oz

ii) Into Brinks: 12,569.840 oz

iii) Into Delaware: 992.686 oz

iv) Into Malca: 200,815.810 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 165.53 million oz of total silver inventory or 49.15% of all official comex silver. (165.53 million/335.614 million

total customer deposits today: 1,409,101.386 oz

we had 3 withdrawals:

i) Out of CNT: 1,546,676.648 oz

ii) Out of Delaware: 17,718.981

iii) Out of HSBC: 83,731.590 oz

total withdrawals; 1,648,127.219 oz

We had 0 adjustments

Total dealer(registered) silver: 128,470 million oz

total registered and eligible silver: 335.614 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

the front month of August registered an open interest of 22 contracts and thus we lost 85 contracts. We had 88 notices filed on THURSDAY so we GAINED 3 contracts or an additional 15,000 oz will stand for delivery as these guys refused to morph into London based forwards as well as negating a fiat bonus for their efforts…. The bankers are now desperate in their search for badly needed silver whether it is on this side of the pond or the European side.

After August we have the big September contract month and here we see a lost 91,009 contracts down to 91,009. November saw another gain of 3 contracts to stand at 256.

The big December contract month saw its OI rise by strong 8393 contracts up to 94,501

The total number of notices filed today for the AUGUST 2020. contract month is represented by 3 contract(s) FOR 15,000, oz

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 1270 x 5,000 oz = 6,350,000 oz to which we add the difference between the open interest for the front month of AUGUST(22) and the number of notices served upon today 3 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the AUGUST/2019 contract month: 1270 (notices served so far) x 5000 oz + OI for front month of AUGUST (22)- number of notices served upon today (3) x 5000 oz of silver standing for the AUGUST contract month.equals 6,445,000 oz. ..VERY STRONG FOR A NON ACTIVE MONTH.

We gained 3 contracts or an additional 15,000 oz will stand for delivery as they refused to morph into London based forwards..

TODAY’S ESTIMATED SILVER VOLUME : 197,623 CONTRACTS // volume huge++++++++++++++++++/

FOR YESTERDAY: 196,666. ,CONFIRMED VOLUME//volume huge.++++++++++++++++++++++++

YESTERDAY’S CONFIRMED VOLUME OF 196,666 CONTRACTS EQUATES to 0.983 billion OZ 140% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO- 3.53% ((AUGUST 14/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.39% to NAV: (AUGUST 14/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/3.53%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 20.32 TRADING 19.77///NEGATIVE 2,70

END

And now the Gold inventory at the GLD/

AUGUST 14/ WITH GOLD DOWN $19.45 TODAY: SURPRISINGLY, WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.46 TONNES/INVENTORY RESTS AT 1252.63 TONNES.

AUGUST 13/WITH GOLD UP $23.15 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY: SURPRISINGLY A PAPER WITHDRAWAL OF 7.30 TONNES/INVENTORY RESTS AT 1250.63 TONNES

AUGUST 12/ WITH GOLD UP $1.00 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 4.19 TONNES//INVENTORY RESTS AT 1257.93 TONNES

AUGUST 11//WITH GOLD DOWN $92.40 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1262.12 TONNES.

AUGUST 10/WITH GOLD UP $11.35 TODAY, WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.84 TONNES//INVENTORY RESTS AT 1262.12 TONNES

AUGUST 7/WITH GOLD DOWN $38.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1267.96 TONNES

AUGUST 6/WITH GOLD UP $20.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER DEPOSIT OF 10.23 TONNES INTO THE GLD/INVENTORY RESTS AT 1267.96 TONNES//

AUGUST 5/WITH GOLD UP $ 33.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 9.35 TONNES INTO THE GLD//INVENTORY RESTS AT 1257.73 TONNES

AUGUST 4//WITH GOLD UP $31.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 6.48 TONNES/GLD INVENTORY RESTS AT 1248.38 TONNES

AUGUST 3/WITH GOLD UP $2.20 TODAY, WE HAVE NO CHANGES IN THE GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241,96 TONNES

JULY 31/WITH GOLD UP $17.90 TODAY/WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241.96 TONNES.

JULY 30/WITH GOLD DOWN $10.00 TODAY, WE HAVE ANOTHER SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES//INVENTORY RESTS AT 1241.96 TONNES.

JULY 29//WITH GOLD UP $12.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 8.47 TONNES/INVENTORY RESTS AT 1243.12 TONNES

JULY 28///WITH GOLD UP $13.25 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 5.84 TONNES/INVENTORY RESTS AT 1234.65

JULY 27//WITH GOLD UP $35.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF XXX TONNES/INVENTORY RESTS AT 1228.81 TONNES

JULY 24/WITH GOLD UP $8.80 TODAY: WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.80 TONNES//INVENTORY RESTS AT 1228.81 TONNES

JULY 23/WITH GOLD UP $24.90 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 7.26 TONNES/INVENTORY RESTS AT 1225.01 TONNES

JULY 22/WITH GOLD UP $22.00 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 7.89 TONNES/INVENTORY RESTS AT 1219.75 TONNES

JULY 21//WITH GOLD UP $26.00 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.97 TONNES INTO THE GLD// INVENTORY RESTS AT 1211.86 TONNES

JULY 20/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1206.89 TONNES

JULY 17/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1206.89 TONNES

JULY 16/WITH GOLD DOWN $9.80 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: INVENTORY RESTS AT 1206.89 TONNES

JULY 15//WITH GOLD UP $1.55 TODAY/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 2.96 TONNES INTO THE GLD///INVENTORY RESTS AT 1206.89 TONNES

JULY 14//WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 3.51 TONNES/INVENTORY RESTS AT 1203.97 TONNES

JULY 13//WITH GOLD UP $12.50 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1200.46 TONNES

JULY 10/WITH GOLD DOWN $.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD//A STRANGE WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1200.82 TONNES

JULY 9//WITH GOLD DOWN $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OX 3.21 TONNES INTO THE GLD//INVENTORY RESTS AT 1202.57 TONNES

JULY 8/WITH GOLD UP $13.75 TODAY; A BIG CHANGE IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 7.89 TONNES INTO THE GLD//INVENTORY RESTS AT 1199.36 TONNES

JULY 7/WITH GOLD UP $12.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1191.47 TONNES

JULY 6/WITH GOLD UP $6.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1191.47 TONNES

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

AUGUST 14/ GLD INVENTORY 1252.09 tonnes*

LAST; 881 TRADING DAYS: +312.59 NET TONNES HAVE BEEN ADDED THE GLD

LAST 781 TRADING DAYS://+491.12 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

AUGUST 14/WITH SILVER DOWN $1.31 TODAY, WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.984 MILLION OZ// //INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 13//WITH SILVER UP $1.76 TODAY: WE HAVE TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A PAPER DEPOSIT OF 2.421 MILLION OZ INTO THE SLV AT 2 PM AND ANOTHER DEPOSIT OF 6.984 MILLION OZ AT 5 20 PM/INVENTORY RESTS AT 581.037 MILLION OZ//

AUGUST 12/WITH SILVER DOWN 40 CENTS TODAY: WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF XX MILLION OZ//INVENTORY RESTS AT XX MILLION OZ/

AUGUST 11/WITH SILVER DOWN $3.25 CENTS, WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.41 MILLION OZ//INVENTORY RESTS AT 571.632 MILLION OZ//

AUGUST 10/WITH SILVER UP 1.89 TODAY, WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 3.538 MILLION OZ/INVENTORY RESTS AT 569.491 MILLION OZ//

AUGUST 7/WITH SILVER DOWN 69 CENTS TODAY: WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY: A DEPOSIT OF 0.465 MILLION OZ/INVENTORY RESTS AT 573.029 MILLION OZ.

AUGUST 6/WITH SILVER UP $1.52 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 572.564 MILLION OZ///

AUGUST 5/WITH SILVER UP $1.03 TODAY, WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A MONSTROUS DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 572.564 MILLION OZ//

AUGUST 4/WITH SILVER UP $1.45 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 367.161 MILLION OZ//

AUGUST 3/WITH SILVER UP 23 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//SURPRISINGLY ANOTHER WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 367.161 MILLION OZ//

JULY 31/WITH SILVER UP 82 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: SURPRISINGLY A HUGE WITHDRAWAL OF 3.26 MILLION OZ//INVENTORY RESTS AT 368.092 MILLION OZ//

JULY 30//WITH SILVER DOWN 97 CENTS TODAY: WE HAVE A SMALL CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 571.352 MILLION OZ//

JULY 29/WITH SILVER UP 7 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY//A DEPOSIT OF 5.984 MILLION OZ//INVENTORY RESTS AT 572.283 MILLION OZ//

JULY 28 WITH SILVER DOWN 14 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 7.52 MILLION OZ//INVENTORY RESTS AT 566.299 MILLION OZ//

JULY 27/WITH SILVER UP $2.67 TODAY, WE HAD NO CHANGES IN SILVER INVENTORY: A DEPOSIT OF XX MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ//

JULY 24/WITH SILVER DOWN $0.12 TODAY: NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 558.779 MILLION OZ/

JULY 23/WITH SILVER UP $.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A HUMONGOUS PAPER DEPOSIT OF 9.594 MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ///

JULY 22/WITH SILVER UP $1.54 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A HUMONGOUS PAPER DEPOSIT OF 7.218 MILLION OZ//INVENTORY RESTS AT 549.185 MILLION OZ/

JULY 21/WITH SILVER UP $1.38 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUMONGOUS PAPER DEPOSIT OF 15.368 MILLION OZ////INVENTORY RESTS AT 541.967 MILLION OZ//

JULY 20/WITH SILVER UP 40 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 3.819 MILLION OZ ‘ENTERED” THE SLV..INVENTORY RESTS AT 526.599 MILLION OZ/

JULY 17/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 1.583 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 522.780 MILLION OZ//

JULY 16//WITH SILVER DOWN 14 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ//INVENTORY RESTS AT 521.197 MILLION OZ..

JULY 15.WITH SILVER UP 21 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.956 MILLION OZ//INVENTORY RESTS AT 516.074 MILLION OZ//

JULY 14/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 514.118 MILLION OZ//

JULY 13//WITH SILVER UP 67 CENTS TODAY: A HUGE CHANGE IN SILVER: A WITHDRAWAL OF 1.677 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 514.118 MILLION OZ//

JULY 10/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 4.844 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.795 MILLION OZ

WHAT A FRAUD!!

JULY 9/WITH SILVER DOWN 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 8.198 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 510.951 MILLION OZ/

JULY 8/WITH SILVER UP 37 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.118 MILLION OZ FROM THE SLV//VERY SURPRISING.//INVENTORY RESTS AT 502.753 MILLION OZ//

JULY 7/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/INVENTORY RESTS AT 503.871 MILLION OZ///

JULY 6//WITH SILVER UP 24 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.863 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 503.871 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

AUGUST 14.2020:

SLV INVENTORY RESTS TONIGHT AT

574.053 MILLION OZ.

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Gold, Silver Jump After Swings Amid Weak Dollar and Economic Woe

(Bloomberg) Spot gold headed for back-to-back gains as investors weighed the outlook for the metal’s record-setting rally after this week’s dramatic price swings. Silver climbed the most in more than five years.

Rising U.S. bond yields helped spark a sharp selloff in gold and silver Tuesday and early Wednesday, followed by a rebound. Both metals have resumed their uptrend as the dollar falls a second straight day. They remain among the best-performing commodities this year, aided by negative real yields and vast stimulus to combat the fallout from the pandemic.

Gold gained as much as 2.6% on Thursday as concerns over the outlook for economic recovery persist and central banks and governments signal further support for their economies. Two senior Federal Reserve officials said Wednesday that the U.S. failure to control the coronavirus pandemic has undermined the nation’s economic recovery, further bolstering support for precious metals as haven assets.

“We’re not out of this crisis yet,” Jeffrey Currie, global head of commodities research at Goldman Sachs Group Inc., said by phone. “Even if a vaccine is rolled out in November it won’t be rolled out until at best the first quarter of next year, which means you still need to provide stimulus to the global economy. More stimulus means more downside risk in real rates. That’s what drives the upside in gold.”

Spot gold rose 2.4% to $1,962.22 an ounce by 1:46 p.m. in New York. On Tuesday, prices dropped 5.7%, the most in seven years, following a rally to an all-time high last week. Futures for December delivery advanced 1.1% to settle at $1,970.40 on the Comex in New York.

Silver for immediate delivery climbed as much as 8.7% to $27.7207 an ounce, the biggest intraday increase since December 2014. The metal rose 2.9% on Wednesday and slumped 15% on Tuesday.

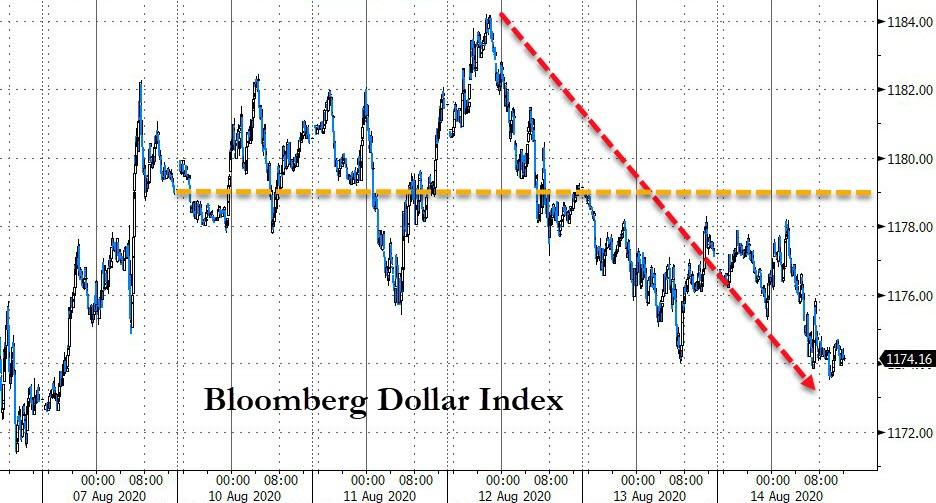

The Bloomberg Dollar Spot Index headed for a second straight decline.

“The dollar index broke down a bit today, but there’s a lot of people that are on the sidelines that are looking to get back in and are chasing back into gold and silver right now,” Phil Streible, chief market strategist at Blue Line Futures in Chicago, said by phone.

“We still hold a positive view on gold, targeting a retest of the level of $2,000 an ounce by the end of this year,” said Giovanni Staunovo, an analyst at UBS Group AG. “The Fed should reiterate its dovish message and U.S. real yields and the broad U.S. dollar will likely fall further.”

The death toll from the virus continued to climb, with India’s total surpassing the U.K.’s, according to the latest data collated by Johns Hopkins University. There were signs of resilience to the economic harm wrought by the pandemic though. Australia added four times as many jobs as forecast in July, withstanding a fresh lockdown in Victoria and concerns about infection spreading.

Read More: Gold Consumers in India Hug Sidelines Ignoring Steep Price Drop

The scope of the drop in gold prices earlier this week may limit the pace of recovery, some analysts said.

“The extent of this selloff was so severe that I think it’s caused jitteriness about longs getting back in so quickly,” Edward Meir, an analyst at ED&F Man Capital Markets in New York, said by phone. “I think the more likely scenario is we will start a consolidation range. So we might bounce around between $1,850 and $2,050 for the next six weeks or so. Things don’t go up forever.”

You can read the full article at Bloomberg.com

NEWS and COMMENTARY

Gold Fever Spurs Dollar Oddity Not Seen Since Erdogan Took Power

Gold prices set for first weekly decline in 10

Gold Price Is Set To Record Its First Weekly Loss Since June, What Now?

A faltering U.S.-China trade deal is now the nations’ strongest link

U.S. hits fiscal cliff with jobs, economic recovery in the balance

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

13-Aug-20 1931.00 1944.25 1476.06 1482.30 1632.47 1640.17

12-Aug-20 1931.70 1931.90 1479.10 1483.70 1642.14 1640.57

11-Aug-20 1996.60 1939.65 1524.40 1479.57 1694.51 1646.76

10-Aug-20 2030.30 2044.50 1552.98 1561.38 1725.35 1734.96

07-Aug-20 2061.50 2031.15 1574.37 1559.52 1743.82 1726.88

06-Aug-20 2049.15 2067.15 1555.30 1569.59 1728.87 1743.43

05-Aug-20 2034.45 2048.15 1553.30 1558.03 1718.09 1722.90

04-Aug-20 1972.25 1977.90 1508.77 1519.62 1671.09 1686.56

03-Aug-20 1972.95 1958.55 1509.50 1504.56 1678.39 1670.45

31-Jul-20 1974.70 1964.90 1505.91 1492.54 1666.84 1661.72

30-Jul-20 1952.20 1957.65 1503.00 1502.10 1662.30 1662.44

29-Jul-20 1954.35 1950.90 1506.80 1502.39 1663.54 1659.24

Own gold and silver coins and bars in the safest vaults in Zurich, Singapore, London and Dublin with GoldCore.

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here

ii) Important gold commentaries courtesy of GATA/Chris Powell

We have highlighted this interview yesterday but in case you missed it, I am repeating it:

(courtesy Andrew Maguire/Kinesis/GATA)

Raid on gold and silver had ‘surgical precision’ but won’t stop their rise, Maguire says

Submitted by cpowell on Thu, 2020-08-13 18:10. Section: Daily Dispatches

2:09p ET Thursday, August 12, 2020

Dear Friend of GATA and Gold:

Tuesday’s attack on gold and silver futures prices was a “rigged selloff” aimed at speculative longs with “surgical precision,” London metals trader Andrew Maguire said yesterday in an interview with Kinesis Money’s Shane Morand, but it won’t change the trajectory of the monetary metals.

The instigators of the raid violated futures position limits, Maguire adds, and the CME Group, operator of the New York Commodities Exchange, is “pandering” to the big bullion bank shorts that can’t deliver metal.

…

Maguire adds that the Bank for International Settlements is trading real metal for unallocated — imaginary — metal to help bullion banks meet the delivery claims giving them trouble.

Central banks and bullion banks, Maguire says, are aiming to move gold prices up to $2,500 and silver prices up to $35 soon but had to strike the market on Tuesday because prices were rising too fast for them.

The interview is 24 minutes long and can be viewed at YouTube here:

https://www.youtube.com/watch?v=kZcrB489LSc&feature=youtu.be

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

iii) Other physical stories:

J Johnson’s commodity report!

https://www.jsmineset.com/2020/08/14/these-markers-help-prove-the-desperation-at-the-comex/

These Markers Help Prove The Desperation At The Comex

Posted August 14th, 2020 at 9:09 AM (CST) by J. Johnson & filed under General Editorial.

Great and Wonderful Friday Morning Folks,

The Precious Metals are trading lower this morning, after another surprise hike in margins was applied, with Gold now at $1,956, down only $14.40 and recovering from the low at $1,945.30 with the high at $1,970. December Silver is trading at $27.085 down 84.4 cents and is recovering from the low at $26.59 with the high so far at $28.03. We’ll be quoting the December Contract from now on because the Open Interest blew past Septembers as the roll overs are occurring faster than normal. The US Dollar is still flat as can be with the trade at 93.19, down 12.7 points after hitting a low of 93.135 with the high at 93.41. Of course, all this happened before 5 am pst, the Comex open, the London close, and after the DOJ found out that Yale illegally and intentionally discriminated against Whites and Asians. What part of Equal Rights requires pigment?

Even though the margins were raised at the Comex, the precious metals inside the emerging markets continue to trek higher as their currencies increase in quantity, not quality. In Venezuela, Gold is now priced at 19,535.55, showing an increase of 134.83 Bolivars with Silver gaining 5.393 with the current priced at 270.511 Bolivars. Argentina’s currency now has Gold’s value at 142,857.19 Peso’s providing the holder a 1,045.09 gain with Silver now priced at 1,977.90 A-Peso’s, popping in an additional 40.18 overnight. The Turkish Lira’s price for Gold now rests at 14,437.67, showing a gain of 188.58 Lira’s with Silver’s last trade adding 5.211 with the price at 199.920 T-Lira’s.

August Silver’s Delivery Demands now shows a post of 22 fully paid for contracts waiting for receipts with a Volume of 12 already up on the board with a trading range between $27.685 and $27.205 with the last trade at $27.23, down 45.4 cents while the futures markets, attempt to pump and dump, the prices lower. Yesterday’s delivery activity happened in between $27.525 and $26.38 with the last purchase at $27.38 with the calculated close at $27.694, a gain of $1.739 that included a Volume of 30, reducing the previous days count by 85 contracts that supposedly got receipts somewhere. Silver’s Overall Open Interest lost another round of shorts as 1,289 contracts jumped ship during yesterday’s rally leaving a total of 196,043 Overnighters to go against the physicals. To me, the raising of the margins within 7 trading days, pumping up the Option values, and the adjustments in the delivery price close’s, are all proving to be markers of desperation at the Comex, as the physicals become harder and harder to find everywhere.

August Gold’s Delivery Demands now shows 613 fully paid for contracts waiting for receipts and with a Volume of 53 up on the board with a trading range between $1,934.40 and $1,938.70 with the last trade at $1,941.90, down $14.80 so far today. Yesterday’s physical trades happened in between $1,957.40 and $1,916.90 with the last registered trade at $1,947 with the higher close at $1,956.70, providing a gain of $21.80 which also reduced the demand count by 251 contracts that got receipts. Adding more to the above paragraphs point, it seems the closing delivery prices are adjusted higher in order to make the next day’s dip look bigger, but if one simply focuses on the purchases and ignoring the closing prices, things really don’t seem to be moving as much as the papers. Gold’s Overall Open Interest is really showing the fear in deliveries as the count dropped 7,682 short contracts leaving 543,918 Overnighters going against a product in heavy demand.

Things have already been interesting inside the Comex Precious Metals and it appears to be increasing. Comex already replaced those Time Outs (circuit breakers) with a percentage limit (in March, 2020), and that too was totally removed before it could be used. Now they are raising margins quickly, and we expect many more increases (and decreases to create the illusion) to come, as the margins eventually go to 100%. Basically, it’s a wide-open infestation of activity in order to find physicals at all costs to meet the demands. First, they have to reduce the investors count from profitting off the demands. Second, they have to get out of their shorts, and third, Comex is required to find product no matter what the price. It is the last place to get product and many are certain the Comex will default. Will they? Imo, nowhere near these prices, maybe 100’s or 1,000’s of percentage points from here. Reminder; Jim said in one of the weekly interviews, that he was surprised that the Hunt Brothers didn’t sue the Comex back at the Life of Contract High when they no longer allowed the buying of physical! He felt they had a big chance of winning. Will they attempt to do it again and if so, how will the Comex defend their actions when they claim to be physical deliverers of the last resort? How about those inside the governing bodies that support the system?

Regardless of the future responses coming from Comex, sitting tight with physicals, trumps all the papers. So, keep things real and in hand, have a smile on your face and a prayer for all. Have a Great and Wonderful Weekend and, As Always …

Stay Strong!

Jeremiah Johnson

More J.Johnson content is available with purchase of a JSMineset subscription.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Futures Drop Ahead Of Key Retail Sales Report

After again briefly hitting a new all time high on Thursday, S&P500 futures retreated on Friday after the latest Chinese econ data pointed to a wobbly economic recovery from the COVID-19 pandemic as two out of three key Chinese metrics missed…

… coupled while new quarantine rules in the UK sent European stocks sliding.

And as attention now turns to retail sales, where BofA warned that a miss is virtually assured based on its own internal card spending data, it may explain why both the dollar and Treasury yields are also sliding on the last day of the week.

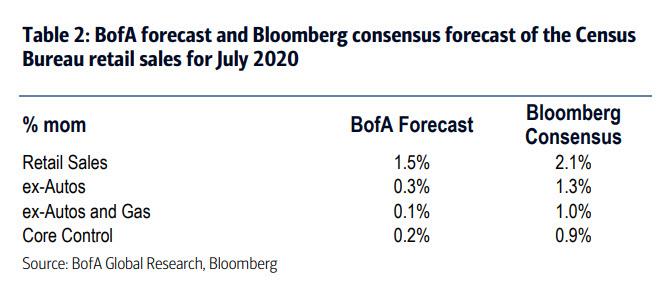

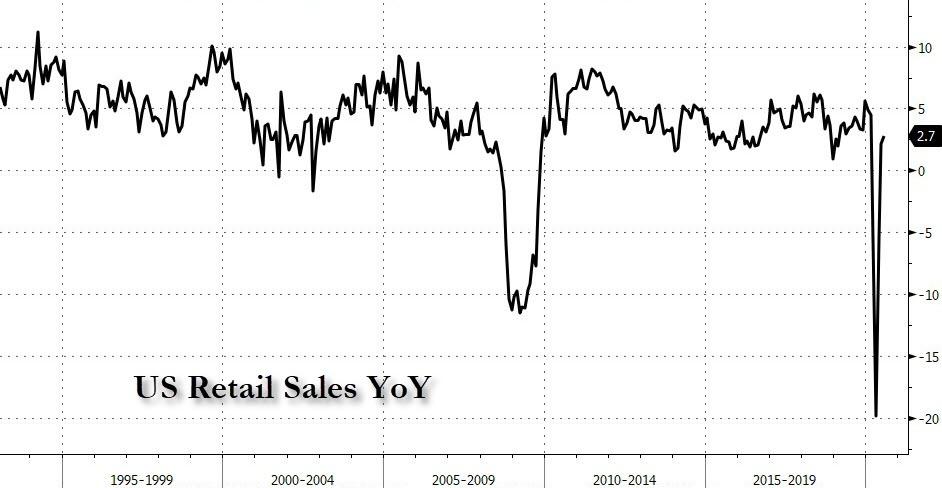

The S&P has struggled to top its all-time high of 3,393.52, also set on Feb. 19, on growing evidence of a faltering labor market rebound. Data at 8:30 a.m. ET is expected to show retail sales increased 2.1% last month after jumping 7.5% in June, but as we explained last night, the reported number is likely to be well lower.

Also weighing on sentiment are ongoing negotiations between top Democrats and the White House over more stimulus measures to support the economy, which have hopelessly stalled and with Senate now out until September, it appears that a resolution is weeks if not months away. Nonetheless, Bloomberg notes, that traders continue to bank on further fiscal stimulus to help the nascent recovery, after U.S. and Asian stocks erased most of their pandemic-related losses.

On the virus front, Joe Biden said U.S. governors should require masks for the next three months, while New Zealand recorded 12 new confirmed local cases of the coronavirus. Germany added the most new cases since May, while the head of the French Health Agency Jerome Salomon said the situation in his country is worsening.

The Stoxx Europe 600 Index sank after Britain added France, the Netherlands and Malta to its list of countries from which people arriving have to quarantine for 14 days. The Eurostoxx 50 dropped 1.7%, Spain’s IBEX underperformed peers on tourism concerns, dropping over 2.25%. All sectors are in the red with travel, banks and oil & gas names declining the most. The UK’s FTSE 100 drops over 2% to trade back near Monday’s opening levels. EasyJet Plc fell as much as 8% and British Airways owner IAG SA by as much as 7%.

The latest euro area jobs data reflected the scale of the damage the coronavirus crisis has done to the bloc’s economy. The number of people employed fell by 2.8% in the second quarter. Governments now face difficult choices as to how to wind down the furlough programs that have kept the rise in unemployment below that of other countries such as the U.S.

Earlier in the session, Asian stocks were little changed, with energy and materials falling, after rising in the last session. Most markets in the region were down, with Thailand’s SET dropping 1.5% and South Korea’s Kospi Index falling 1.2%, while Shanghai Composite gained 1.2% as margin debt posted its first increase in three days. The Shanghai Composite Index rose 1.2%, with Harbin Xinguang and Haohua Chemical posting the biggest advances. News of China’s unexpected economic disappointment led to stocks rising in Hong Kong and China, on hopes of more stimulus. Japan’s Topix was little changed, with Mynet rising and DS falling the most.

In rates, Bund and Treasuries curves bull flattened slightly. Gilts steepen at the margin with 5s30s the steepest in a year. Treasury futures are higher as U.S. trading gets under way after falling every day this week, leaving yields lower by 1bp-2bp on the day. Treasury 10-year yields hover around 0.70%, 2bp lower on thee day; gilts lag by 3bp, bunds by 2bp; UST 30-year yields around 1.415%, still around 1bp cheaper than Thursday’s auction stop. Gains during Asia session stalled as gilts underperformed, extending move spurred earlier this week by stronger-than-forecast U.K. growth data and reduced expectations for additional BOE QE. Peripheral spreads widen, BTP futures bounce off Thursday’s worst levels.

In FX, the dollar faded a modest earlier gain even as the euro slipped 0.1%, ending a three-session positive run, after news of the sharp drop in employment for the second quarter. U.K. gilts edged lower led by the long-end, pushing the curve to its steepest in a year. The New Zealand dollar fell against most of its Group-of-10 peers as a coronavirus outbreak widened and amid indications that the central bank is seeking to slow gains in the currency.

In commodities, gold edged lower following two days of gains, while oil headed for a second weekly advance. Gold was set to post its first weekly drop after 9 consecutive weeks of increases.

Looking at the day ahead, retail sales figures on Friday will offer clues about the health of the consumer recovery following a report that showed weekly jobless claims in the U.S. dropped below 1 million for the first time since March. Other expected data include industrial production, and University of Michigan Consumer Sentiment Index. DraftKings is reporting earnings

Market Snapshot

- S&P 500 futures down 0.5% to 3,351.00

- STOXX Europe 600 down 1.7% to 366.20

- MXAP down 0.09% to 170.90

- MXAPJ down 0.2% to 563.14

- Nikkei up 0.2% to 23,289.36

- Topix down 0.05% to 1,623.38

- Hang Seng Index down 0.2% to 25,183.01

- Shanghai Composite up 1.2% to 3,360.10

- Sensex down 1% to 37,919.13

- Australia S&P/ASX 200 up 0.6% to 6,126.25

- Kospi down 1.2% to 2,407.49

- Brent futures down 1% to $44.50/bbl

- Gold spot down 0.3% to $1,947.55

- U.S. Dollar Index down 0.1% to 93.25

- German 10Y yield fell 0.7 bps to -0.419%

- Euro down 0.07% to $1.1806

- Italian 10Y yield rose 4.9 bps to 0.885%

- Spanish 10Y yield rose 1.2 bps to 0.382%

Top Overnight News From Bloomberg

- The euro area jobs data reflects the scale of the damage the coronavirus crisis has done to the bloc’s economy. The number of people employed fell by 2.8% in the second quarter. Governments now face difficult choices as to how to wind down the furlough programs that have kept the rise in unemployment below that of other countries such as the U.S.

- The virus resurgence is gaining momentum in Europe, with Germany recording the highest number of new cases in more than three months while worrying infections figures are recorded in France, which the led the U.K. to impose a quarantine for travelers coming back from France as well as Malta and the Netherlands.

- The U.K. signed two more deals to expand its vaccine supply, ordering 60 million doses from Novarax Inc. and 30 million from Johnson and Johnson’s Janssen. That brings the total number of potential vaccine doses secured by Britain to 300 million.

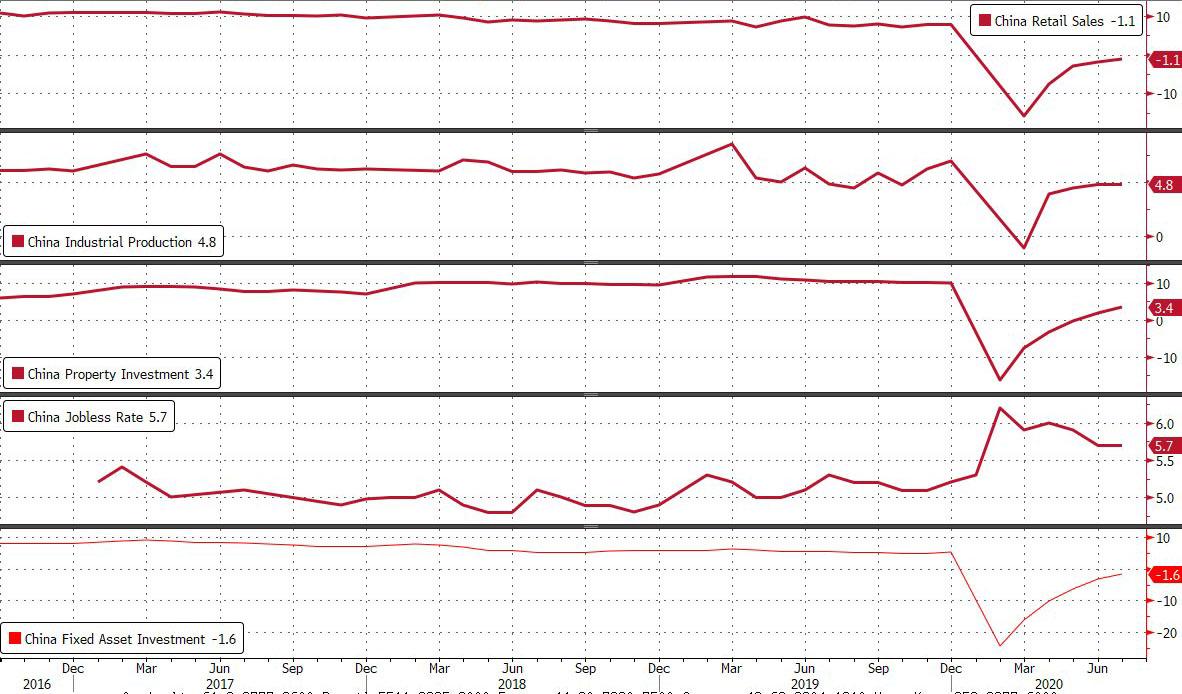

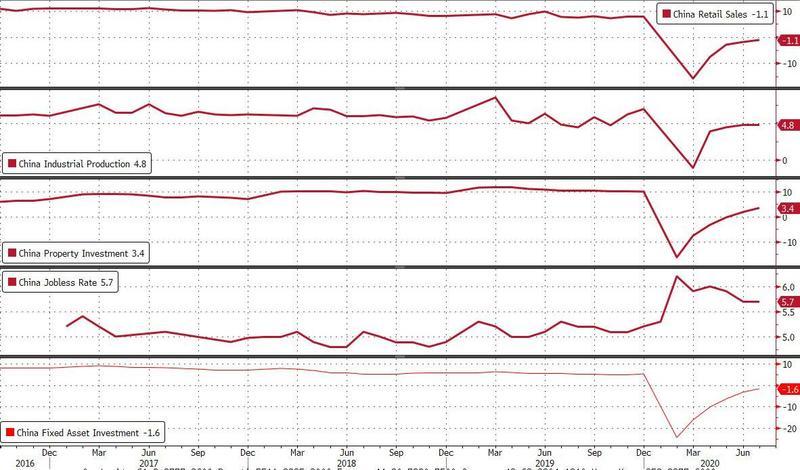

- China’s industrial output for July grew as much as the previous month but didn’t beat estimates. Retail sales fell, reflecting an uneven economic recovery with demand unable to keep up with the factory output rebound.

Asian equity markets head into the weekend mixed as the region took its cue from the lackadaisical performance in global peers after both the S&P 500 and Nasdaq failed to carve out fresh record levels in the US but where downside was stemmed by encouraging initial jobless claims data, while participants also digested disappointing Industrial Production and Retail Sales data from China. ASX 200 (+0.6%) was underpinned by outperformance in tech and healthcare, while the largest weighted financials sector was dragged following a 7% decline in NAB’s cash profit for Q3 although shares in the Big 4 bank itself were kept afloat after its revenue rose 10% for the quarter and as it explores a sale of its MLC wealth business. Nikkei 225 (+0.2%) traded indecisively amid an uneventful currency and the KOSPI (-1.2%) was the worst performer following a flare up of virus cases in which the country posted its largest daily increase in cases since March. Hang Seng (-0.2%) and Shanghai Comp. (+1.2%) were choppy after both Industrial Production and Retail Sales missed expectations, although PBoC efforts resulted to a net weekly injection of CNY 490bln and it announced to conduct a medium-term lending facility operation on Monday, while focus also shifts to the US-China talks set for tomorrow. Finally, 10yr JGBs were lower amid spillover selling from USTs in the aftermath of an abysmal 30yr auction, with prices also dampened by weaker demand at the enhanced liquidity auction for longer-dated JGBs.

Top Asian News

- Malaysia’s Economy Shrinks Most Since 1998 Asia Financial Crisis

- Singapore Oil Legend and Hin Leong Founder Charged With Forgery

- China’s Pouring More Steel Than Ever to Power Virus Rebound

- China’s Industry-Led Recovery Continues But Retail Stays Weak

European stocks continue to bleed in early trade [Euro Stoxx 50 -1.7%] despite a mostly positive APAC handover, with little by way of fresh catalysts to spur the sell-off, although participants note of possible squaring ahead of the weekend following this week’s rally alongside some positioning ahead of US retail sales. Broad-based losses are seen across major bourses, with DAX cash and Sept futures back below the 13,000-mark, Euro Stoxx 50 cash under 3,300 and CAC cash sub-5,000. Sectors are firmly in the red with energy underperforming, whilst the detailed breakdown sees Travel & Leisure the clear laggard after the UK imposed the 14-day quarantine rule to travelers from France and Netherlands – a move France said will see reciprocal action. As such, pronounced losses are seen across easyJet (-7%), IAG (-6.2%), Tui (-5.2%), Air France-KLM (-5.7%), Ryanair (-4.7%), and Lufthansa (-3.5%). Upside movers are scarce with only some 9 stocks within the Stoxx 600 in positive territory at the time of writing; Qiagen (+3.2%) are the top mover, supported by a broker upgrade. Some smaller earnings-related movers include Hapag-Lloyd (+11%), Maersk Drilling (-8.4%) and Clas Ohlson (-0.2%). Finally, Atlantia (-3.0%) is pressured after Italian PM Conte noted that there are still details that need ironing out in Autostrade’s agreement with the government. The PM also noted that any deal will not prevent the government from launching legal action against the Co. in the case of “serious negligence”.

Top European News

- U.K. Expands Covid Vaccine Supplies With Novavax, J&J Deals

- Spain’s Business Leaders Fear Second Lockdown as Virus Surges

- Spike in Cigar Use During Lockdown Triggers STG Upgrade

- East EU Sees Worst Slump Since Communism But Finds Positives

In FX, the 2 renowned safe haven currencies remain in lock-step, but Usd/Jpy continues to respect and reject triple-top resistance around the 107.00 level where Japanese exporters are reported to have selling/hedging interests. This could also be a top line for the MoF and BoJ in similar vein to defences of 105.00 fairly recently, and 104.00 not that long ago. However, the Greenback has survived another test of its own with assistance from significantly higher US Treasury yields, a steeper curve and signs that global stock markets are losing momentum amidst the ongoing spread and re-emergence of COVID-19. Indeed, the DXY is back above 93.000 following Thursday’s fall to 92.922, albeit tentatively heading into more top tier data (retail sales, ip and Michigan sentiment) and Saturday’s US-Sino showdown, while the Yen holds a relatively firm line between 107.03-106.68 parameters.

- AUD – A very marginal ‘outperformer’ and straddling 0.7150 vs its US counterpart in wake of supportive Aussie jobs data in contrast to Chinese retail sales and ip missing consensus overnight. Resilience also coming after rhetoric from RBA Governor Lowe reaffirming no willingness to intervene directly to weaken the Aud even if he and the Bank would like to see it depreciate, or desire to devalue via negative rates.

- GBP/EUR/CHF – All marginally weaker against the Buck in comparatively quiet, consolidative trade, as Sterling retreats from 1.3100+ again, the Euro retests bids around 1.1800 and the 200 HMA and the Franc pivots 0.9100. Note, hefty option expiry interest may also be weighing on the single currency given 1.1 bn at 1.1825 and 1.1850 ahead of almost double that size at the 1.1900 strike, though 1.1 bn at 1.1750 should provide some underlying support.

- CAD/NZD/SEK/NOK – The Loonie also looks bound by big expiries in the absence of any inertia from oil ahead of Canadian manufacturing sales, with 1.5 bn running off at the NY cut very close to the top of the range (1.3250 vs 1.3248) and 1.1 bn below the base (at 1.3175 vs 1.3206). Meanwhile, the Kiwi continues to lag on the back of dovish RBNZ policy guidance and the pandemic resurgence, as Nzd/Usd pulls back further from 0.6600 and under 0.6550, while Aud/Nzd picks up pace beyond 1.0900.

- EM – No major adverse reaction to the aforementioned disappointing Chinese macro releases as attention is trained on the upcoming US-China meeting and the Yuan hovers around 6.9500, but other EMs are feeling the effects of the mini-Usd revival and a downturn in risk sentiment. In fact the Try has slipped to a new, albeit slender, record low circa 7.3765 after weaker than expected Turkish ip, the Rub has reversed through 73.0000 against the backdrop of softer Brent crude prices and the Mxn is sub-22.0000 following the latest Banxico rate cut, shrugging off 1 dissenter voting for a 25 bp ease rather than -1/2 point.

In commodities, WTI and Brent front month futures see a session of losses thus far, with the benchmarks pressured on a number of fronts – including the Israel/UAE deal providing some stability in the region, whilst the UK quarantine rule on France and Netherlands further dampens jet fuel demand as flagged by the IEA oil market report yesterday. Furthermore, participants will also be keeping stock of US-Sino sentiment heading into the weekend meeting, which comes against the backdrop of heightened tensions, although very little is expected to develop on the trade front. WTI Sept and Brent October are down some USD 0.50/bbl apiece and trade below 42/bbl and 45/bbl respectively, with eyes on retail sales for a possible sentiment-driven move ahead of the weekly Baker Hughes rig count. Elsewhere, spot gold is uneventful on either side of USD 1950/oz as the yellow metal trades in lockstep with the USD ahead of Tier 1 US data, albeit prices are set for the first weekly decline in ten weeks, whilst spot silver oscillates on either side of USD 26/oz. In terms of base metals, Shanghai copper closed lower amid sub-par Chinese retail sales and industrial output data, coupled with Shanghai warehouse copper stocks rising. Conversely, Dalian iron ore futures closed higher by almost 2% as the metal remains underpinned by steel producers’ demand alongside supply woes. Reports also note that China produced record amounts of crude steel last month amid infrastructure boosts. Finally, China’s aluminium output hit a record high last month as smelters were incentivized to restart production and launch new capacity by the rally in prices.

US Event Calendar

- 8:30am: Retail Sales Advance MoM, est. 2.05%, prior 7.5%; Retail Sales Ex Auto MoM, est. 1.3%, prior 7.3%

- Retail Sales Control Group, est. 0.8%, prior 5.6%

- 8:30am: Nonfarm Productivity, est. 1.5%, prior -0.9%; Unit Labor Costs, est. 6.85%, prior 5.1%

- 9:15am: Industrial Production MoM, est. 3.0%, prior 5.4%; Capacity Utilization, est. 70.3%, prior 68.6%; Manufacturing (SIC) Production, est. 3.0%, prior 7.2%

- 9:45am: Bloomberg Aug. United States Economic Survey

- 10am: Business Inventories, est. -1.1%, prior -2.3%

- 10am: U. of Mich. Sentiment, est. 72, prior 72.5; Current Conditions, est. 82.3, prior 82.8; Expectations, est. 65.5, prior 65.9

DB’s Jim Reid concludes the overnight wrap