GOLD:$1963.75 DOWN $39.65 The quote is London spot price (cash market)

Silver:$27.31 DOWN $0.66 London spot price ( cash market)

Today marks the 4TH day out of the last 7 days that a raid has been orchestrated by the bankers..

DONATE

Closing access prices: London spot

i)Gold : $1928.80 LONDON SPOT 4:30 pm

ii)SILVER: $26.70//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUGUST GOLD: $1960.00 CLOSE 1::30 PM SPREAD SPOT/FUTURE AUG (BACKWARD $3.75//)

OCT GOLD: $1965.10 CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: : $1.35//CONTANGO/$1.55/BELOW NORMAL CONTANGO/

DEC. GOLD $1971.80 CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $8.35 ($3.65 BELOW NORMAL CONTANGO)

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $27.40…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : 9 CENTS PER OZ ( CONTANGO/ 6 CENTS ABOVE NORMAL CONTANGO)

SILVER DECEMBER CLOSE: $27.55 1:30 PM SPREAD SPOT/FUTURE DEC. : 24 CENTS PER OZ ( 12 CENTS ABOVE NORMAL CONTANGO)

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today: 15/334

jpmorgan issued 0//goldman sachs issued: 333

EXCHANGE: COMEX

CONTRACT: AUGUST 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,999.400000000 USD

INTENT DATE: 08/18/2020 DELIVERY DATE: 08/20/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 333 1

072 H GOLDMAN 8

104 C MIZUHO 3

159 C ED&F MAN CAP 1

226 C DIRECT ACCESS 1

323 C HSBC 1

332 H STANDARD CHARTE 2

355 C CREDIT SUISSE 1

365 C ED&F MAN CAPITA 1

657 C MORGAN STANLEY 70

657 H MORGAN STANLEY 8

661 C JP MORGAN 11

661 H JP MORGAN 4

686 C INTL FCSTONE 1

690 C ABN AMRO 25

709 C BARCLAYS 3

709 H BARCLAYS 1

730 C PTG DIVISION SG 1

880 C CITIGROUP 1

880 H CITIGROUP 6

905 C ADM 1 4

991 H CME 180

____________________________________________________________________________________________

TOTAL: 334 334

MONTH TO DATE: 48,498

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 334 NOTICE(S) FOR 33400 OZ (1.038 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 48,498 NOTICES FOR 4,849,800 OZ (150.849 TONNES)

SILVER

0 NOTICE(S) FILED TODAY FOR 0 OZ/

total number of notices filed so far this month: 1274 for 6.370 MILLION oz

BITCOIN MORNING QUOTE $11,837 DOWN 107

BITCOIN AFTERNOON QUOTE.: $11,695 DOWN 248

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $39.65 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/// //

A STRONG PAPER DEPOSIT OF 4.09 TONNES INTO THE GLD///

GLD: 1,252.38 TONNES OF GOLD//

WITH SILVER DOWN $0.66 CENTS TODAY: AND WITH NO SILVER AROUND:

A HUGE CHANGES IN SILVER INVENTORY AT THE SLV//

A DEPOSIT OF: 2.514 MILLION OZ INTO THE SLV

RESTING SLV INVENTORY TONIGHT:

SLV: 576.567 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A TINY SIZED 530 CONTRACTS FROM 195,427 DOWN TO 194,807, AND FURTHER FROM OUR NEW RECORD OF 244,710, (FEB 25/2020. THE LOSS IN OI OCCURRED DESPITE OUR STRONG 44 CENT GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE LOSS IN COMEX OI IS PRIMARILY DUE TO HUGE BANKER SHORT COVERING COUPLED AGAINST A SMALL EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, WITH A SMALL INCREASE IN SILVER OZ. STANDING AT THE COMEX FOR AUGUST. WE HAD A SMALL NET GAIN IN OUR TWO EXCHANGES OF 32 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: SEP 426 DEC: 136 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 562 CONTRACTS. WITH THE TRANSFER OF 562 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 562 EFP CONTRACTS TRANSLATES INTO 2.810 MILLION OZ ACCOMPANYING:

1.THE 44 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

86.470 MILLION OZ FINAL STANDING IN JULY.

6.480 MILLION OZ INITIAL STANDING IN AUGUST

TUESDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 44 CENTS ).. AND, OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY WEAK SILVER LONGS FROM THEIR POSITIONS. THEY ENGAGED IN HUGE BANKER SHORT COVERING. THUS: THE TINY SIZED GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A SMALL INCREASE IN SILVER OZ STANDING FOR AUGUST, BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A SMALL NET GAIN OF 32 CONTRACTS OR 0.160 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKERS ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER..AND THUS THE REASON FOR OUR MASSIVE RAID THIS MORNING!!

SPREADING OPERATIONS/NOW SWITCHING TO SILVER

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN SILVER AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF AUGUST. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

AUGUST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF AUGUST:

13,015 CONTRACTS (FOR 14 TRADING DAY(S) TOTAL 13,015 CONTRACTS) OR 65.075 MILLION OZ: (AVERAGE PER DAY: 9296 CONTRACTS OR 4.648 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 65.075 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 9.29% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,335.37 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 133.95 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

AUGUST EXP 65.075 MILLION OZ (EXCHANGE FOR PHYSICALS INCREASING)

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 530, DESPITE OUR STRONG 44 CENT GAIN IN SILVER PRICING AT THE COMEX ///TUESDAY…THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 562 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A SMALL SIZED 32 OI CONTRACTS ON THE TWO EXCHANGES (DESPITE OUR STRONG 44 CENT RISE IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 562 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A TINY SIZED DECREASE OF 530 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 44 CENT RISE IN PRICE OF SILVER/AND A CLOSING PRICE OF $27.97 // TUESDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.9770 BILLION OZ TO BE EXACT or 139% of annual global silver production (ex Russia & ex China).

FOR THE NEW AUGUST DELIVERY MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR nil OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 WAS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 86.470 million oz//AUGUST 6.480 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1657 CONTRACTS TO 544,010 AND FURTHER FORM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE LOSS OF COMEX OI OCCURRED DESPITE OUR STRONG GAIN IN PRICE OF $14.60 /// COMEX GOLD TRADING// TUESDAY//WE HAD CONSIDERABLE BANKER SHORT COVERING, A SMALL SIZED DECREASE IN GOLD TONNAGE STANDING AT THE COMEX FOR AUGUST, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR STRONG GAIN IN PRICE OF $14.60.

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 158

WE GAINED A SMALL SIZED 74 CONTRACTS (0.23 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 1731 CONTRACTS:

CONTRACT .; AUG 0 AND OCT: 0 DEC: 1731; JUNE: 0 ALL OTHER MONTHS ZERO//TOTAL: 1731. The NEW COMEX OI for the gold complex rests at 544.010. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 74 CONTRACTS: 1657 CONTRACTS DECREASED AT THE COMEX AND 1731 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 74 CONTRACTS OR 0.2301 TONNES. TUESDAY, WE HAD A STRONG GAIN OF $14.60 IN GOLD TRADING..….

AND WITH THAT GAIN IN PRICE, WE HAD A SMALL SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 0.2301 TONNES!!!!!! THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $14.60. HOWEVER WE DID HAVE CONSIDERABLE BANKER SHORT COVERING// BUT AT MUCH HIGHER PRICES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1731) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (1637 OI): TOTAL GAIN IN THE TWO EXCHANGES: 74 CONTRACTS. WE NO DOUBT HAD 1 )CONSIDERABLE BANKER SHORT COVERING LATE IN THE SESSION, 2.)A SMALL DECREASE IN GOLD TONNAGE STANDING AT THE GOLD COMEX FOR THE FRONT AUGUST MONTH, 3) ZERO LONG LIQUIDATION; 4) SMALL COMEX OI LOSS AND 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL AND …ALL OF THIS WAS COUPLED WITH OUR HUGE GAIN IN GOLD PRICE TRADING//TUESDAY//$14.60. WE NO DOUBT HAD BANKER SHORT COVERING BUT AT MUCH HIGHER PRICES AS THE TRADING SESSION WORE ON.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

AUGUST

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAY(S) IN TONNES: 94.79 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 94.79/3550 x 100% TONNES =2.67% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3,354.97 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 313.09 TONNES ..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

AUGUST TOTAL EFP ISSUANCE; 94.79 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A TINY SIZED 530 CONTRACT FROM 195,427 UP TO 194.807 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE TINY GAIN IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) BANKER SHORT COVERING LATE IN THE SESSION , 2) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A SMALL DECREASE IN SILVER OZ STANDING AT THE SILVER COMEX FOR AUGUST, AND 4) ZERO LONG LIQUIDATION,

EFP ISSUANCE 562 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT: 426 AND DEC. 136 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 562 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 530 CONTRACTS TO THE 562 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL GAIN OF 32 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 0.16 MILLION OZ, OCCURRED WITH OUR 44 CENT GAIN IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 42.96 POINTS OR 1.24% //Hang Sang CLOSED DOWN 188.47 POINTS OR 0.74% /The Nikkei closed UP 59.53 POINTS OR 0.26%//Australia’s all ordinaires CLOSED UP .72%

/Chinese yuan (ONSHORE) closed UP at 6.9111 /Oil UP TO 42.54 dollars per barrel for WTI and 45.06 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.9111 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9042 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS PANDEMIC : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total withdrawals; nil oz

We had 1 kilobar transactions +

ADJUSTMENTS: 0 //

The front month of AUGUST registered a total of 535 CONTRACTS as we LOST 46 contracts. We had 34 notices served on TUESDAY so we LOST 12 contracts or an additional 1200 OZ will NOT stand for delivery on this side of the pond as they morphed into London based forwards as well as accepting a fiat bonus for their effort. The boys are scrambling in search of badly needed physical metal as they start to search for metal on the other side of the pond.

After August we have the non active Sept contract month.. Here we saw another LOSS of 62 contracts to stand at 2363. Oct GAINED 380 contracts UP to 70,070

The big December contract lost 3168 contracts down to 400,403 contracts…(it is here where some of our short side bankers bailed)

We had 334 notices filed today for 33400 oz

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2020. contract month, we take the total number of notices filed so far for the month (48,498) x 100 oz , to which we add the difference between the open interest for the front month of AUGUST (535 CONTRACTS ) minus the number of notices served upon today (334 x 100 oz per contract) equals 4,866,900 OZ OR 151.474 TONNES) the number of ounces standing in this active month of JUNE

thus the INITIAL standings for gold for the AUGUST/2020 contract month:

No of notices filed so far (48,498, x 100 oz + (535 OI) for the front month minus the number of notices served upon today (334) x 100 oz which equals 4,866,900 oz standing OR 151.474 TONNES in this active delivery month. This is a HUGE amount for gold standing for a AUGUST delivery month (an active delivery month).

We lost 12 contracts or 1200 oz of gold as these guys morphed into London based forwards.

THE NAME OF THE GAME TODAY IS BANKER SHORT COVERING AS FINALLY FEAR BECAME THEIR CENTRAL FOCUS. THE PRICE OF GOLD ROSE SO WHATEVER THEY COVERED WAS AT HIGHER PRICES.

NEW PLEDGED GOLD: BRINKS

144,088.952 oz NOW PLEDGED JAN 21.2020/HSBC 5.4807 TONNES

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

231,924.295 oz (some deleted august 3) JPM 7.2138 TONNES

611,401.341 oz pledged June 12/2020 Brinks/ july 2/july 21 19.017 tonnes

total pledged gold: 1,029,962.895 oz 32.03 tonnes

total registered, pledged and eligible (customer) gold; 37,297,889.108 oz 1,160.12 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1033.78 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

536,900.510 oz

CNT

Delaware

Scotia

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

451,183.870 oz

Delaware

Malca

|

| No of oz served today (contracts) |

0

CONTRACT(S)

(nil OZ)

|

| No of oz to be served (notices) |

22 contracts

110,000 oz)

|

| Total monthly oz silver served (contracts) | 1274 contracts

6,370,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 2 deposits into the customer account

i)into JPMorgan: nil oz

ii) Into CNT: 2020.600 oz

iii) Into Malca: 449,163.270 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 165.53 million oz of total silver inventory or 48.75% of all official comex silver. (165.53 million/339.453 million

total customer deposits today: 451,183.870 oz

we had 3 withdrawals:

i)Delaware: 2002.950 oz

ii) Out of CNT: 85,734.290 oz

iii) Out of Scotia: 449,163.270 oz

total withdrawals; 536,900.510 oz

We had 0 adjustments

Total dealer(registered) silver: 129.555 million oz

total registered and eligible silver: 339.453 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

the front month of August registered an open interest of 22 contracts and thus we GAINED 4 contracts. We had 2 notices filed on TUESDAY so we GAINED 6 contracts or an additional 30,000 oz will stand for delivery as these guys refused to morph into London based forwards as well as negating a fiat bonus for their efforts…. The bankers are now desperate in their search for badly needed silver whether it is on this side of the pond or the European side.

After August we have the big September contract month and here we see a loss 4998 contracts down to 77,222. November saw another gain of 17 contracts to stand at 283.

SEPT OI IS VERY HIGH AND WE WILL HAVE A DANDY AMOUNT OF SILVER STANDING AT THE COMEX.

The big December contract month saw its OI rise by good 4461 contracts up to 105,462

The total number of notices filed today for the AUGUST 2020. contract month is represented by 0 contract(s) FOR nil, oz

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 1274 x 5,000 oz = 6,370,000 oz to which we add the difference between the open interest for the front month of AUGUST(22) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the AUGUST/2019 contract month: 1274 (notices served so far) x 5000 oz + OI for front month of AUGUST (22)- number of notices served upon today (0) x 5000 oz of silver standing for the AUGUST contract month.equals 6,480,000 oz. ..VERY STRONG FOR A NON ACTIVE MONTH.

We gained 6 contracts or an additional 30,000 oz will stand for delivery as they refused to morph into London based forwards..

TODAY’S ESTIMATED SILVER VOLUME : 211,404 CONTRACTS // volume huge++++++++++++++++++++++++++++++++++++/

FOR YESTERDAY: 249,365. ,CONFIRMED VOLUME//volume huge.++++++++++++++++++++++++++++++++++++++++++++++++++++

YESTERDAY’S CONFIRMED VOLUME OF 249,365 CONTRACTS EQUATES to 1.246 billion OZ 178% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 2.78% ((AUGUST 19/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.61% to NAV: (AUGUST 19/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/2.78%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 20.28 TRADING 20.07///NEGATIVE 1,02

END

And now the Gold inventory at the GLD/

AUGUST 19//WITH GOLD DOWN $39.65 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT XXX TONNES

AUGUST 18/WITH GOLD UP $14.60 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 4.09 TONNES//GLD INVENTORY RESTS TONIGHT AT 1252.38 TONNES

AUGUST 17/WITH GOLD UP $46.30 TODAY: SURPRISINGLY WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 3.8 TONNES//INVENTORY RESTS AT 1248.29 TONNES

AUGUST 14/ WITH GOLD DOWN $19.45 TODAY: SURPRISINGLY, WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.46 TONNES/INVENTORY RESTS AT 1252.63 TONNES.

AUGUST 13/WITH GOLD UP $23.15 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY: SURPRISINGLY A PAPER WITHDRAWAL OF 7.30 TONNES/INVENTORY RESTS AT 1250.63 TONNES

AUGUST 12/ WITH GOLD UP $1.00 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 4.19 TONNES//INVENTORY RESTS AT 1257.93 TONNES

AUGUST 11//WITH GOLD DOWN $92.40 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1262.12 TONNES.

AUGUST 10/WITH GOLD UP $11.35 TODAY, WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.84 TONNES//INVENTORY RESTS AT 1262.12 TONNES

AUGUST 7/WITH GOLD DOWN $38.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1267.96 TONNES

AUGUST 6/WITH GOLD UP $20.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER DEPOSIT OF 10.23 TONNES INTO THE GLD/INVENTORY RESTS AT 1267.96 TONNES//

AUGUST 5/WITH GOLD UP $ 33.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 9.35 TONNES INTO THE GLD//INVENTORY RESTS AT 1257.73 TONNES

AUGUST 4//WITH GOLD UP $31.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 6.48 TONNES/GLD INVENTORY RESTS AT 1248.38 TONNES

AUGUST 3/WITH GOLD UP $2.20 TODAY, WE HAVE NO CHANGES IN THE GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241,96 TONNES

JULY 31/WITH GOLD UP $17.90 TODAY/WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241.96 TONNES.

JULY 30/WITH GOLD DOWN $10.00 TODAY, WE HAVE ANOTHER SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES//INVENTORY RESTS AT 1241.96 TONNES.

JULY 29//WITH GOLD UP $12.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 8.47 TONNES/INVENTORY RESTS AT 1243.12 TONNES

JULY 28///WITH GOLD UP $13.25 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 5.84 TONNES/INVENTORY RESTS AT 1234.65

JULY 27//WITH GOLD UP $35.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF XXX TONNES/INVENTORY RESTS AT 1228.81 TONNES

JULY 24/WITH GOLD UP $8.80 TODAY: WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.80 TONNES//INVENTORY RESTS AT 1228.81 TONNES

JULY 23/WITH GOLD UP $24.90 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 7.26 TONNES/INVENTORY RESTS AT 1225.01 TONNES

JULY 22/WITH GOLD UP $22.00 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 7.89 TONNES/INVENTORY RESTS AT 1219.75 TONNES

JULY 21//WITH GOLD UP $26.00 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.97 TONNES INTO THE GLD// INVENTORY RESTS AT 1211.86 TONNES

JULY 20/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1206.89 TONNES

JULY 17/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1206.89 TONNES

JULY 16/WITH GOLD DOWN $9.80 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: INVENTORY RESTS AT 1206.89 TONNES

JULY 15//WITH GOLD UP $1.55 TODAY/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 2.96 TONNES INTO THE GLD///INVENTORY RESTS AT 1206.89 TONNES

JULY 14//WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 3.51 TONNES/INVENTORY RESTS AT 1203.97 TONNES

JULY 13//WITH GOLD UP $12.50 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1200.46 TONNES

JULY 10/WITH GOLD DOWN $.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD//A STRANGE WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1200.82 TONNES

JULY 9//WITH GOLD DOWN $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OX 3.21 TONNES INTO THE GLD//INVENTORY RESTS AT 1202.57 TONNES

JULY 8/WITH GOLD UP $13.75 TODAY; A BIG CHANGE IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 7.89 TONNES INTO THE GLD//INVENTORY RESTS AT 1199.36 TONNES

JULY 7/WITH GOLD UP $12.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1191.47 TONNES

JULY 6/WITH GOLD UP $6.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1191.47 TONNES

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

AUGUST 19/ GLD INVENTORY 1252.38 tonnes*

LAST; 884 TRADING DAYS: +312.88 NET TONNES HAVE BEEN ADDED THE GLD

LAST 784 TRADING DAYS://+491,41 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

AUGUST 19/WITH SILVER DOWN $.66 TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF XX MILLION OZ//INVENTORY REST AT XXX MILLION

AUGUST 18/WITH SILVER UP $.44 TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.514MILLION OZ//THE SLV INVENTORY RESTS TONIGHT AT 576.567 MILLION OZ//

AUGUST 17/WITH SILVER UP $1.27 TODAY: WE HAD NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 14/WITH SILVER DOWN $1.31 TODAY, WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.984 MILLION OZ// //INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 13//WITH SILVER UP $1.76 TODAY: WE HAVE TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A PAPER DEPOSIT OF 2.421 MILLION OZ INTO THE SLV AT 2 PM AND ANOTHER DEPOSIT OF 6.984 MILLION OZ AT 5 20 PM/INVENTORY RESTS AT 581.037 MILLION OZ//

AUGUST 12/WITH SILVER DOWN 40 CENTS TODAY: WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF XX MILLION OZ//INVENTORY RESTS AT XX MILLION OZ/

AUGUST 11/WITH SILVER DOWN $3.25 CENTS, WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.41 MILLION OZ//INVENTORY RESTS AT 571.632 MILLION OZ//

AUGUST 10/WITH SILVER UP 1.89 TODAY, WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 3.538 MILLION OZ/INVENTORY RESTS AT 569.491 MILLION OZ//

AUGUST 7/WITH SILVER DOWN 69 CENTS TODAY: WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY: A DEPOSIT OF 0.465 MILLION OZ/INVENTORY RESTS AT 573.029 MILLION OZ.

AUGUST 6/WITH SILVER UP $1.52 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 572.564 MILLION OZ///

AUGUST 5/WITH SILVER UP $1.03 TODAY, WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A MONSTROUS DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 572.564 MILLION OZ//

AUGUST 4/WITH SILVER UP $1.45 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 367.161 MILLION OZ//

AUGUST 3/WITH SILVER UP 23 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//SURPRISINGLY ANOTHER WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 367.161 MILLION OZ//

JULY 31/WITH SILVER UP 82 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: SURPRISINGLY A HUGE WITHDRAWAL OF 3.26 MILLION OZ//INVENTORY RESTS AT 368.092 MILLION OZ//

JULY 30//WITH SILVER DOWN 97 CENTS TODAY: WE HAVE A SMALL CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 571.352 MILLION OZ//

JULY 29/WITH SILVER UP 7 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY//A DEPOSIT OF 5.984 MILLION OZ//INVENTORY RESTS AT 572.283 MILLION OZ//

JULY 28 WITH SILVER DOWN 14 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 7.52 MILLION OZ//INVENTORY RESTS AT 566.299 MILLION OZ//

JULY 27/WITH SILVER UP $2.67 TODAY, WE HAD NO CHANGES IN SILVER INVENTORY: A DEPOSIT OF XX MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ//

JULY 24/WITH SILVER DOWN $0.12 TODAY: NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 558.779 MILLION OZ/

JULY 23/WITH SILVER UP $.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A HUMONGOUS PAPER DEPOSIT OF 9.594 MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ///

JULY 22/WITH SILVER UP $1.54 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A HUMONGOUS PAPER DEPOSIT OF 7.218 MILLION OZ//INVENTORY RESTS AT 549.185 MILLION OZ/

JULY 21/WITH SILVER UP $1.38 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUMONGOUS PAPER DEPOSIT OF 15.368 MILLION OZ////INVENTORY RESTS AT 541.967 MILLION OZ//

JULY 20/WITH SILVER UP 40 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 3.819 MILLION OZ ‘ENTERED” THE SLV..INVENTORY RESTS AT 526.599 MILLION OZ/

JULY 17/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 1.583 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 522.780 MILLION OZ//

JULY 16//WITH SILVER DOWN 14 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ//INVENTORY RESTS AT 521.197 MILLION OZ..

JULY 15.WITH SILVER UP 21 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.956 MILLION OZ//INVENTORY RESTS AT 516.074 MILLION OZ//

JULY 14/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 514.118 MILLION OZ//

JULY 13//WITH SILVER UP 67 CENTS TODAY: A HUGE CHANGE IN SILVER: A WITHDRAWAL OF 1.677 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 514.118 MILLION OZ//

JULY 10/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 4.844 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.795 MILLION OZ

WHAT A FRAUD!!

JULY 9/WITH SILVER DOWN 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 8.198 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 510.951 MILLION OZ/

JULY 8/WITH SILVER UP 37 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.118 MILLION OZ FROM THE SLV//VERY SURPRISING.//INVENTORY RESTS AT 502.753 MILLION OZ//

JULY 7/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/INVENTORY RESTS AT 503.871 MILLION OZ///

JULY 6//WITH SILVER UP 24 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.863 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 503.871 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

AUGUST 19.2020:

SLV INVENTORY RESTS TONIGHT AT

576.567 MILLION OZ.

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

There Is No “Gold Bubble” as Retail Investors Are Only Starting To Invest in Gold – Bloomberg Interview GoldCore

GoldCore Research Director Mark O’Byrne speaks on “Bloomberg Surveillance” about the factors behind the recent sharp fall in the gold price and as gold recovers above $2,000 per ounce, the very positive medium and long term outlook.

The outlook is positive due to significant economic uncertainty due to societal and economic lockdowns as the divisive U.S. election and Brexit loom, negative interest rates on deposits and bonds and looming currency devaluations globally.

NEWS and COMMENTARY

Gold Rebounds Above $2,000 Amid Escalating U.S.-China Tensions (Bloomberg)

Gold jumps 1% to surpass $2,000/oz as dollar dips (Reuters)

Barrick Gold Shares Surge After Berkshire Hathaway Stake Purchase

Dollar hovers near two-year low as traders push euro longs to record high

New U.S. curbs to slam Huawei, hurt suppliers in short term

Venezuelan central bank’s gold reserves fall to lowest level in 50 years

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

17-Aug-20 1949.85 1972.85 1488.13 1505.68 1645.87 1661.53

14-Aug-20 1948.30 1944.75 1491.42 1482.09 1653.33 1643.31

13-Aug-20 1931.00 1944.25 1476.06 1482.30 1632.47 1640.17

12-Aug-20 1931.70 1931.90 1479.10 1483.70 1642.14 1640.57

11-Aug-20 1996.60 1939.65 1524.40 1479.57 1694.51 1646.76

10-Aug-20 2030.30 2044.50 1552.98 1561.38 1725.35 1734.96

07-Aug-20 2061.50 2031.15 1574.37 1559.52 1743.82 1726.88

06-Aug-20 2049.15 2067.15 1555.30 1569.59 1728.87 1743.43

05-Aug-20 2034.45 2048.15 1553.30 1558.03 1718.09 1722.90

04-Aug-20 1972.25 1977.90 1508.77 1519.62 1671.09 1686.56

Own gold and silver coins and bars in the safest vaults in Zurich, Singapore, London and Dublin with GoldCore.

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here

end

ii) Important gold commentaries courtesy of GATA/Chris Powell

Gold and silver are not in a speculative bubble..this is just fiction.

Craig Hemke/Sprott/GATA

Craig Hemke at Sprott Money: ‘Speculative bubble’ in gold and silver is fiction

Submitted by cpowell on Wed, 2020-08-19 15:24. Section: Daily Dispatches

11:24a ET Wednesday, August 19, 2020

Dear Friend of GATA and Gold:

While some mainstream financial news organizations are reporting that gold and silver prices are in a “speculative bubble,” the TF Metals Report’s Craig Hemke, writing today at Sprott Money, shows that gold and silver futures contract volumes have been contracting steadily amid the recent price increases.

Hemke’s analysis is headlined “The ‘Speculative Bubble’ in Gold and Silver” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/the-speculative-bubble-in-gold-and-silv…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

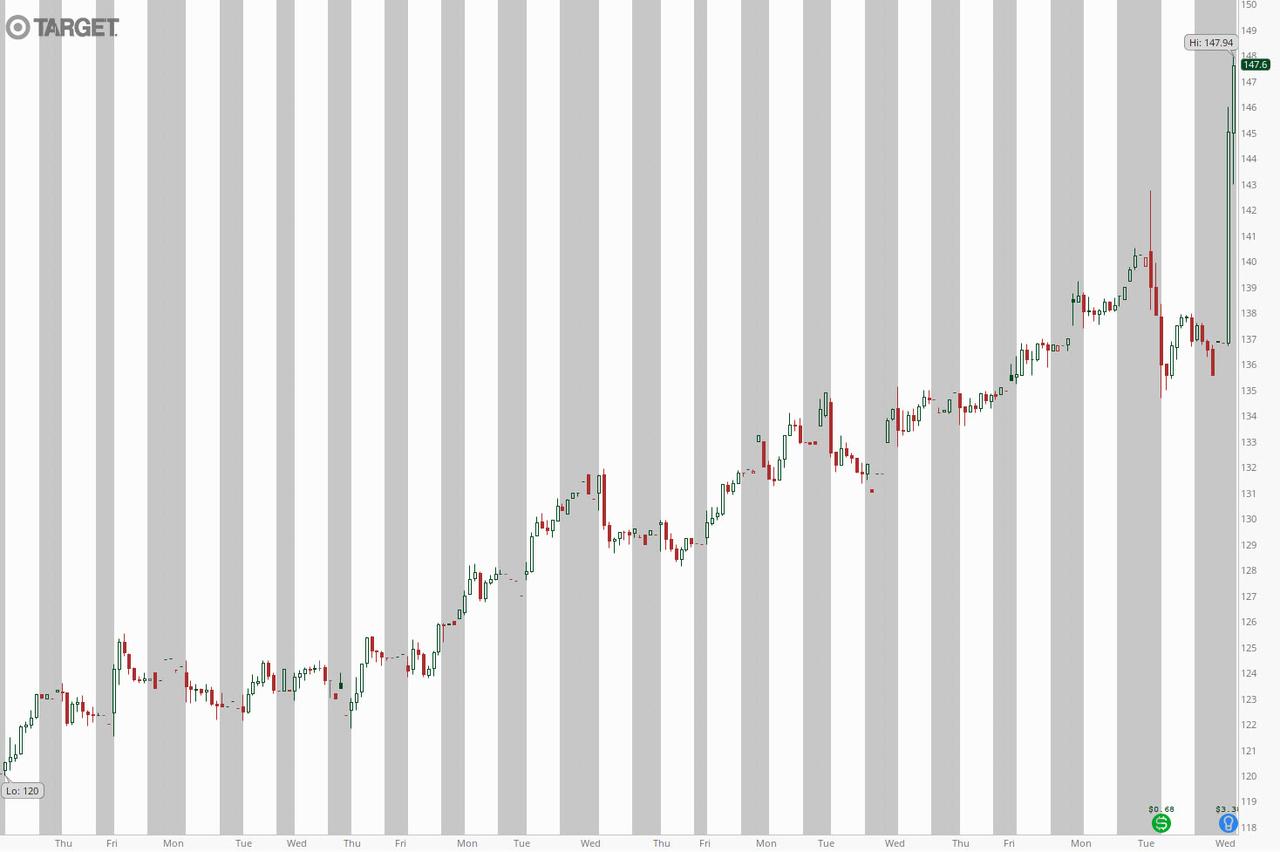

Futures At All Time High As Target Reports Record Quarter

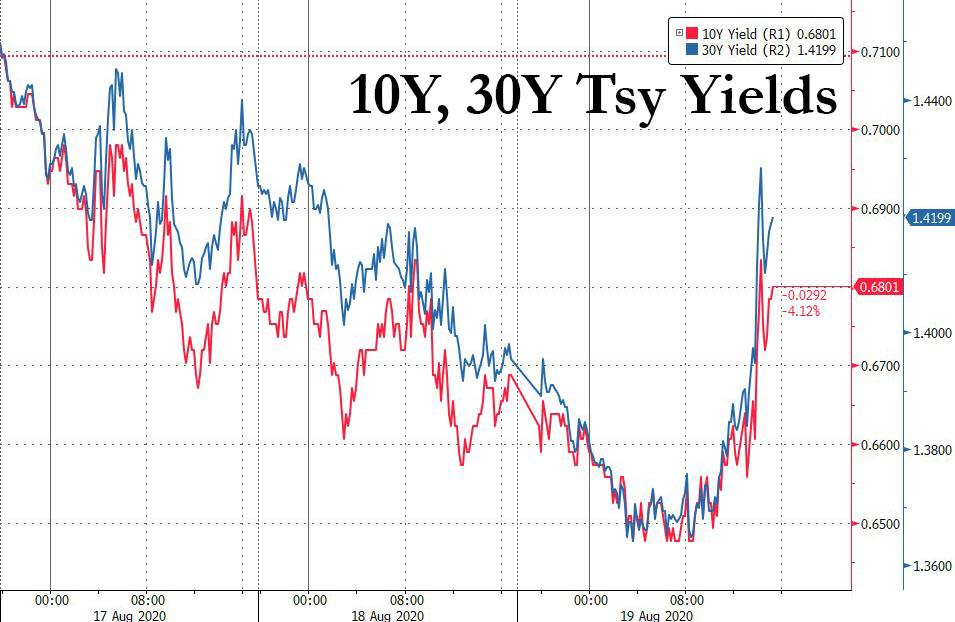

S&P futures edged higher, alongside European stocks, flirting with record highs and just shy of 3,400 following blockbuster earnings from retailers Target and Lowe’s, a day after the S&P 500 completed its fastest recovery from a bear market in history. The dollar headed for a sixth daily drop while Treasuries rose again, the 10Y yield sliding to 0.6477%.

Target Corp soared in premarket trade to a record high of $150 after posting its best quarterly comparable sales growth on record and online revenues that nearly tripled. The supermarket operator reported second-quarter sales that smashed analysts’ expectations, brushing off concerns that demand would ebb after consumers spent their relief checks. Comparable sales rose a record 24% in the three months through Aug. 1, Target said Wednesday – the fastest pace in the retailer’s 58-year history, and almost three times higher than the average estimate of 8.6%. Adjusted earnings per share also touched an all-time high at $3,38, more than double the 1.58 expected, while revenue hit $22.98 billion, beating estimates of $19.82 billion. Additionally, the average Q2 transaction amount rose +18.8% vs. +0.90% y/y, while digital sales as share of total sales rose 17.2% in Q2 vs. 7.30% y/y.

Target CEO Brian Cornell said the retailer attracted consumers’ dollars because they couldn’t go on vacation or spend money on typical summer activities during the pandemic. “We’re not on planes. We’re not spending dollars on lodging, so many of those dollars have been redirected into retail,” he said in an interview with CNBC.

Home improvement chain Lowe’s Companies also jumped 2.7% after beating estimates for quarterly same-store sales as it benefited from a surge in demand for its products from consumers stuck indoors. Its larger rival Home Depot and retail behemoth Walmart reported similar results on Tuesday, although they reversed gains after warning that the Q2 selling frenzy was fading as stimulus payments were cut.

On Tuesday, the S&P 500 closed at a new record high, completing a stunning 50% recovery from a dramatic pandemic-led sell-off. The Nasdaq, the first of the three main indexes to confirm a bull market in June, also closed at an all-time high. Only the Dow remains some 6% below February’s record closing high. Yet while trillions of dollars in fiscal and monetary support and a preference for tech-related stocks have helped the benchmark surge about 55% from its March lows, the battered economy is still far from the pre-pandemic levels.

“We have a Federal Reserve that is all in, keeping rates low probably across the curve for as far as the eye can see,” Katie Nixon, chief investment officer at Northern Trust Wealth Management, said on Bloomberg TV. “That is supportive of higher valuations.”

In a positive signal for equities, Nancy Pelosi suggested that Democrats might be willing to make more cuts to their stimulus proposal to seal a deal with Republicans and speed Covid-19 relief. “The lack of fiscal progress has been a big driver of late and has taken the baton from what was initially a more virus-led story,” strategists including Craig Nicol at Deutsche Bank AG wrote in a note.

In Europe, the Stoxx 600 reversed early losses, gaining as health-care firms including AstraZeneca and Roche Holding led the index higher.

Earlier in the session, Asia stocks were mixed: sentiment was dampened after President Donald Trump said he called off last weekend’s trade talks. The State Department is also asking colleges and universities to divest from Chinese holdings in their endowments. Australia’s S&P/ASX 200 and South Korea’s Kospi Index rose; Japan’s Topix also gained 0.2% with Softbrain and TEMONA rising the most. Meanwhile, the Shanghai Composite Index retreated 1.2% pausing after recent gains, with Haiqi Transportation and Yijiahe Tech posting the biggest slides.

In FX, the Bloomberg Dollar index fell for a sixth consecutive day, but failed to breach its lowest level in over two years reached Tuesday as profit taking on short exposure was quickly offset by momentum and hedge funds looking to sell even the shortest of rallies. The pound edged higher amid firmer-than-expected U.K. inflation in July and managed to erase this year’s drop versus the greenback. U.S. corporate names and institutional accounts were among the main sellers of the euro around $1.1950 and the pound at $1.3260 on a take-profit basis.

The Aussie climbed, supported by higher iron ore prices, though rising tensions between Australia and China likely limited gains; the Kiwi led gains among Group-of-10 peers as short positions versus the Aussie were unwound. Japan’s yen halted a three-day gain to trade little changed after earlier strengthening toward 105 per dollar as offshore banks earlier sent the Japanese yen to day highs around 105.10, according to three traders in Europe.

The Yuan enjoyed a firm session as the recent Dollar weakness prompted the PBoC to set the CNY mid-point at a 7-month high, with today’s USD/CNY setting at 6.9168 vs. yesterday’s 6.9325. USD/CNH was driven lower during the APAC session and briefly traded sub-6.9000 for the first time since January.

In rates, Treasuries are higher across the curve led by the long end, while bunds gained amid record demand for 30-year German bond sale. Yields are lower by as much as 2.8bp at long end, 10-year by 2.1bp at 0.648%, with front-end yields little changed, flattening 2s10s and 5s30s by ~1.5bp; S&P 500 futures are little changed after cash index closed at a record high Tuesday. 10-year and 30-year yields, which climbed into last week’s record-size auctions of those tenors, are lower for a third straight day, both at lower yields (higher prices) than buyers in the auction obtained. On deck today, bond market prepares to digest a $25BN 20-year bond auction at 1pm ET.

An hour later, at 2pm the Fed is slated to release minutes of July 29 FOMC meeting, which will offer clues into the policymaker’s view of the economy and its actions in September, where Average Inflation Targeting is expected to be unveiled. The market’s focus will also shift to U.S. presidential elections, which is about 11 weeks away. Democrats on Tuesday formally nominated Joe Biden for president. The Republican National Convention is slated for next week.

Also on today’s calendar, Analog Devices, TJX and Nvidia are among companies reporting earnings.

Market Snapshot

- S&P 500 futures up 0.1% to 3,391.25

- STOXX Europe 600 up 0.1% to 367.64

- MXAP down 0.04% to 172.34

- MXAPJ down 0.2% to 568.35

- Nikkei up 0.3% to 23,110.61

- Topix up 0.2% to 1,613.73

- Hang Seng Index down 0.7% to 25,178.91

- Shanghai Composite down 1.2% to 3,408.13

- Sensex up 0.6% to 38,759.63

- Australia S&P/ASX 200 up 0.7% to 6,167.64

- Kospi up 0.5% to 2,360.54

- Brent futures down 1% to $45.01/bbl

- Gold spot down 0.6% to $1,989.88

- U.S. Dollar Index down 0.1% to 92.18

- German 10Y yield fell 1.9 bps to -0.482%

- Euro up 0.1% to $1.1943

- Italian 10Y yield fell 0.4 bps to 0.801%

- Spanish 10Y yield fell 0.6 bps to 0.304%

Top Overnight News from Bloomberg

- U.K. inflation accelerated to the fastest in four months in July, an unexpected jump that’s unlikely to last or persuade the Bank of England to ease off the stimulus pedal

- An auction of 30- year German debt saw the highest demand in the record books, which date back to 1997

- The Trump administration sees a possibility for Republicans and Democrats to agree on a smaller round of pandemic relief totaling $500 billion that would omit the biggest areas of disagreement, according to a senior U.S. official

- The $20 trillion U.S. Treasury market is giving the Federal Reserve a thumbs-up for its efforts to revive inflation after the coronavirus pandemic threatened to inflict a damaging bout of deflation on the U.S. economy

- Japanese exports continued to drop steeply in July even as a recovery in shipments to China helped cushion declines to Europe and other key markets where the coronavirus is spreading rapidly

A quick rundown of global markets courtesy of NewsSquawk.

Asian equity markets sustained the mixed lead from their counterparts on Wall St where the S&P 500 and Nasdaq notched fresh record intraday highs shortly after the open, although the tone briefly soured before picking back up again with participants somewhat tentative and volumes thinner due to the lack of data and risk events ahead. Nonetheless, ASX 200 (+0.7%) was positive with the best performing stocks in the index driven by earnings, while Nikkei 225 (+0.3%) was rangebound as participants digested mixed releases including disappointing Machinery Orders and although trade data printed better than expected, there were still substantial contractions to both Exports and Imports. Elsewhere, Shanghai Comp. (-1.2%) weakened alongside the closure of morning trade in Hong Kong due to a typhoon signal, ultimately, Hang Seng (-0.7%); as well as the continued antagonism between US-China as President Trump noted that he postponed talks with China and does not want to talk with China right now, while he responded “we’ll see“ when questioned if he will pull out of the trade agreement. Finally, 10yr JGBs were choppy with mild pressure seen as Japanese stocks just about remained afloat, but with downside also stemmed amid the BoJ presence in the market for JPY 770bln of JGBs with 3yr-10yr maturities.

Top Asian News

- Japan Exports Drop Steeply Again as Virus Continues Spread

- Bank Indonesia Holds Rates Steady to Safeguard Weak Currency

- China Stocks Post Biggest Loss in Three Weeks on U.S. Tensions

European equities trade with little in the way of firm direction (Eurostoxx 50 +0.3%) with ongoing pessimism surrounding US-China relations and stimulus talks in Washington unable to impose any meaningful sway on summer-thinned European markets. Price action thus far has been more of a case of treading water ahead of the US entrance to market, although Europe has seen a modest pick-up in recent trade as indices across the Atlantic continue to eye record highs. From a sectoral standpoint in Europe, energy names are a laggard in-fitting with price action in with some of the modest losses seen in the complex, albeit downside is relatively small in terms of magnitude. Elsewhere, some of the travel & leisure names such as IAG (+2.9%), easyJet (+0.5%) and Ryanair (+0.9%) began the session on a slightly firmer footing amid reports in UK press that Heathrow could expand its testing capabilities in an attempt to replace the imposition of blanket quarantines. Utility names are seen lower in Europe amid losses in RWE (-4.0%) with the DAX-constituent having completed a USD 2bln share issue to support its expansion into renewable energy. Of note for the DAX, investors are awaiting the release of the updated composition of the index at 21:00BST today with reports suggesting that Wirecard could be replaced by Delivery Hero (+0.8%). Maersk (+4.7%) have been a standout outperformer thus far following its Q2 earnings release, in which the Co. beat on estimates for profits and subsequently reinstated guidance at a higher level than indicated previously.

Top European News

- Billionaire Greensill’s German Bank Draws Regulatory Scrutiny

- Galapagos Suffers Biggest Fall Ever as FDA Fails to Approve Drug

- The Best Days May Be Over for Europe’s Stock Rally This Year

- U.K. Is Working on Covid Tests at Airports to Ease Quarantine

In FX, The broader Dollar and index are losing steam as the APAC consolidatory strength, which reverberated into early European hours, fades ahead of the FOMC Minutes (Full preview available in the Research Suite). DXY found an overnight base at 92.150 ahead of the YTD low at 92.124, with the index now residing closer to the middle of the current 92.150-92.388 intraday band.

- NZD, AUD, CAD – The non-US Dollars posted various degrees of resilience vs. the Buck in overnight trade and have since extended on gains as the Dollar wanes. NZD/USD outperforms in the G10 FX space after finding support at the 0.6600 mark before topping its 21 DMA at 0.6621. AUD/USD gains in tandem after breaching mild resistance around 0.7237-43, but market participants eye a sustained break above the 200 WMA at 0.7255 ahead of the Feb 2019 weekly high at 0.7295. Meanwhile, the Loonie ekes mild gains despite losses in the crude complex with potential technical factors at play – USD/CAD drifted below its 200 DMA (1.3169) overnight before dipping under 1.3150 as it eyes the release of Canadian CPI later today.

- GBP, EUR – Both marginally firmer against the USD, although the former saw some fleeting strength on the back of UK CPI metrics notably topping forecasts across the board, mainly due to a less significant decline in clothing prices alongside the easing of lockdown restrictions. Cable meanders around mid-range after printing a post-CPI high of 1.3267 (low 1.3230) ahead of the Dec 31st 2019 high of 1.3283. EUR/USD meanwhile remains within recent ranges and moves in tandem with the USD, having had shrugged off Final CPI figures heading into the European summit on Belarusian sanctions, albeit EU diplomats noted that these are unlikely to be agreed on until the end of this week at the earliest. Note: EUR/USD sees a hefty EUR 1.7bln in options expiring at strike 1.1900 at the NY cut.

- CHF, JPY – Mixed trade between the CHF and the JPY, with the former compliant to USD-action and the latter flat after a choppy APAC session amid mixed data and an absence of clear sentiment. USD/CHF inched closer towards 0.9000 to the downside, with yesterday’s low residing at 0.9008. USD/JPY remains sub-105.50 after rebounding from an overnight base at 105.11, with the pair seeing USD 762mln in options rolling off at 105.00 and USD 800mln scattered between 105.25-30. For the technicians, if 105.00 fails to hold then focus will turn on 104.86 which marks the 76.4% Fib of the Jul-Aug rise.

- Yuan – A firm session for the Yuan as the recent Dollar weakness prompted the PBoC to set the CNY mid-point at a 7-month high, with today’s USD/CNY setting at 6.9168 vs. yesterday’s 6.9325. USD/CNH was driven lower during the APAC session and briefly traded sub-6.9000 for the first time since January.

In commodities, WTI and Brent October futures have been edging lower in early European trade as participants eye the fallout of the JMMC meeting poised to commence from 15:00BST. Although no fireworks are expected from the meeting, market chatter yesterday noted of a possible recommendation of an early taper of the output cut deal, speculations that were dismissed by Russian Energy Minister Novak last week. Focus will likely fall on the laggards’ compliance levels amid pledges to over-comply to make up for their earlier shortfalls, whilst commentary on the JMMC’s outlook will also garner attention given resurging COVID-19 cases. Alongside the meeting, the weekly EIA inventories will be released, with headline crude forecast to have fallen 2.670mln barrels in the past week after private inventories printed a larger than expected draw of 4mln barrels vs. Exp. -2.7mln – with prices shrugging off the release. Elsewhere, Eastern Libyan authorities are to allow limited and temporary exports from the blockaded oil ports in a bid to free up storage to allow fuel production for fire stations. The blockades have resulted in a build-up in condensates and the reduction of gas production used for power stations. In terms of precious metals, spot gold and silver largely move in tandem with the Dollar amidst a lack of fresh catalysts, with the former meandering just under USD 2,000/oz and the latter just north of USD 27.50/oz. UBS remains constructive on gold over the next 6-month, with its base case is at USD 2,000/oz and an upside case of USD 2,200-2,300/oz, whilst UBS’ silver upside case resides around USD 30-40/oz. Over to base metals, Dalian iron ore continued to rise amid firm demand from China as steel mill outputs remain near record levels. However, analysts at ING note that as uncertainties over Brazilian supply subsides, the bank expects prices to ease. Meanwhile, copper prices gain as mining giant Rio Tinto lowered its copper guidance to 135k-175k tons from 165k-205k tons.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 6.8%

- 2pm: FOMC Meeting Minutes

DB’s Craig Nicol concludes the overnight wrap

Much of the focus in markets over the last 24 hours has been on yet another leg lower for the dollar. Indeed the dollar index fell -0.62% yesterday – good for a fifth consecutive daily decline – and to the lowest level since April 2018 with the move fairly broad across most major currency pairs with the euro in particular above $1.19 for the first time since May 2018. The lack of fiscal progress has been a big driver of late and has taken the baton from what was initially a more virus-led story. Mnuchin’s comment yesterday about not knowing why a deal seems so far off didn’t do much to help, as did comments from Walmart’s CFO about potential earnings pressure ahead with the end of stimulus checks.

There was one glimmer of good news on the fiscal front late in the US session though, when House Speaker Pelosi indicated that Democrats could pullback their stimulus demands to cut a deal with Republicans now before introducing additional bills after the November elections. With all that in mind it’ll be interesting to see if the FOMC minutes today change the narrative at all with monetary policymakers recently reiterating the need for further fiscal support.

A reminder that at the meeting, Powell noted that the Committee aims to wrap up the policy review in the “near future”, which would be consistent with our economists’ expectation that the results of this review will be released at the September meeting. The minutes should give a sense as to what kind of issues were discussed at the July meeting and how close the Committee is to announcing any changes to how they conduct monetary policy. So, worth keeping an eye on.

Ahead of that the S&P 500 finally closed at an all-time high last night, finishing up +0.23%. The NASDAQ also hit a fresh record high of its own, following a further +0.73% advance. While the weaker dollar certainly helped, the US housing data for July also played a part. Indeed the number of housing starts rose to an annualised 1.496m (vs. 1.245m expected), while building permits also rose to 1.495m (vs. 1.326m expected), in a move that puts them basically back at their pre-Covid levels. It was a somewhat tentative rally again though, with roughly 67% of the S&P down on the day and the majority of the move was driven by retail and communications stocks.

Of course it wouldn’t be a recap without another round of US-China trade headlines. Late last night, President Trump said that he cancelled last weekend’s talks with China, saying “I don’t want to talk to China right now”. He also said “we’ll see what happens” when addressing whether the US would pull out of the phase one trade deal. Prior to this the US administration said that it wants university endowments to divest Chinese holdings, saying it would be “prudent” to get ahead of potentially more onerous measures on holding the shares including a wholesale de-listing of PRC firms from U.S. exchanges. The State Department letter also warned universities of China’s growing influence on campuses and said the US is accelerating investigations of what it called “illicit PRC funding of research, intellectual property theft and the recruitment of talent”.

The Shanghai Comp -0.30%, Shenzhen Comp -0.86% and CSI -0.54% are all lower in response overnight. In contrast, the Nikkei (+0.37%), Kospi (+0.89%) and ASX (+1.10%) are up while the Hang Seng is yet to reopen as we go to print after scrapping the morning session following a typhoon alert. Futures on the S&P 500 are also up with +0.17% gain while spot gold is back below $2000/oz, and bond markets are a touch stronger.

Back to yesterday, where along with the weaker dollar, treasuries continue to unwind some of last week’s selloff. Indeed 10y yields fell by -2.0bps and measures of the curve including 2s10s and 5s30s have now retraced -3.9bps and -3.4bps of the +12.9bps and +15.0bps respective steepening last week. It was a stronger day for bonds in Europe too where 10y bunds closed -1.2bps lower however equity markets closed at their lows for the session – the STOXX 600 down -0.56% – not helped by the stronger euro and also deteriorating virus news including German Chancellor Merkel warning that the recent increase in cases meant that it wouldn’t be possible to ease restrictions further. German cases doubled in the last 3 weeks and are now seeing the highest daily increases in infections in nearly four months. Elsewhere, Amsterdam has increased scrutiny of bars and restaurants to ensure they adhere to guidelines as the number of new cases is on the rise. In Asia, South Korea reported 297 additional cases in the past 24 hours, marking the biggest daily increase since March.

In other virus news, trackthrecovery.com’s updated small business stats in the US showed a continued downward trend through August 7. Small businesses open are now roughly 20% below pre-virus levels and are near the lowest since mid-May. Job postings, while very volatile, fell to near a low for the recession period being down -36%. These stats lines up well with the NY Fed survey that came out yesterday, which could point to lower ISM service index numbers this month. Cases overall in the US rose 0.8% yesterday, in-line with the 0.9% 7-day average.

To the day ahead now, and the data highlights include the UK’s CPI reading for July, the Euro Area’s current account for June, along with Canada’s CPI for July. From central banks, the Fed will be releasing the minutes from their latest meeting and we’ll hear from Richmond Fed President Barkin. Finally, the Democratic vice presidential nominee Kamala Harris will be speaking at the party’s convention.

3A/ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 42.96 POINTS OR 1.24% //Hang Sang CLOSED DOWN 188.47 POINTS OR 0.74% /The Nikkei closed UP 59.53 POINTS OR 0.26%//Australia’s all ordinaires CLOSED UP .72%

/Chinese yuan (ONSHORE) closed UP at 6.9111 /Oil UP TO 42.54 dollars per barrel for WTI and 45.06 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.9111 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9042 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS PANDEMIC : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

This is telling: Export centric Japan sees its exports tumble as USA demand collapses

(courtesy Reuters)

Japan’s exports tumble as U.S. demand collapses, order books shrink

TOKYO (Reuters) – Japan’s exports extended their double-digit slump into a fifth month in July as the coronavirus pandemic took a heavy toll on auto shipments to the United States, dashing hopes for a trade-led recovery from the deep recession.

FILE PHOTO: A worker walks between shipping containers at a port in Tokyo, Japan, March 22, 2017. REUTERS/Issei Kato