GOLD:$1940.30 DOWN $23.45 The quote is London spot price

Silver::$27.05 DOWN $0.26 London spot price ( cash market)

Today marks the 5TH day out of the last 8 days that a raid has been orchestrated by the bankers..

DONATE

Closing access prices: London spot

i)Gold : $1946.20 LONDON SPOT 4:30 pm

ii)SILVER: $27.23//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUGUST GOLD: $1938.70 CLOSE 1::30 PM SPREAD SPOT/FUTURE AUG (BACKWARD $1.60//)

OCT GOLD: $1938.00 CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: : $2.30//BACKWARD/

DEC. GOLD $1946.20 CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $6.10/ CONTANGO ($6.00 BELOW NORMAL CONTANGO)

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $27.15…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : ( BACKWARD)

SILVER DECEMBER CLOSE: $27.30 1:30 PM SPREAD SPOT/FUTURE DEC. : 01 CENTS PER OZ ( WELL BELOW NORMAL CONTANGO)

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today: 10/40

issued: JPMorgan 1//Goldman Sachs 1

EXCHANGE: COMEX

CONTRACT: AUGUST 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,958.700000000 USD

INTENT DATE: 08/19/2020 DELIVERY DATE: 08/21/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 1

624 C BOFA SECURITIES 5

661 C JP MORGAN 1 10

685 C RJ OBRIEN 17

690 C ABN AMRO 29

732 C RBC CAP MARKETS 6

905 C ADM 10 1

____________________________________________________________________________________________

TOTAL: 40 40

MONTH TO DATE: 48,538

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 40 NOTICE(S) FOR 400 OZ (0.1244 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 48,538 NOTICES FOR 4,853,800 OZ (150.973 TONNES)

SILVER

4 NOTICE(S) FILED TODAY FOR 20,000 OZ/

total number of notices filed so far this month: 1278 for 6.390 MILLION oz

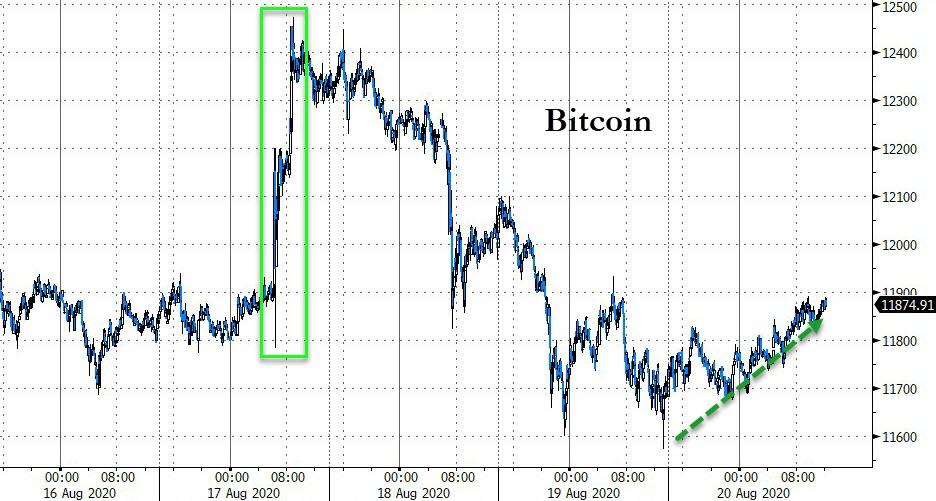

BITCOIN MORNING QUOTE $11,766 UP 15

BITCOIN AFTERNOON QUOTE.: $11,863 UP 112

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $23.45 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

NO CHANGES IN GOLD INVENTORY AT THE GLD/// //

GLD: 1,252.38 TONNES OF GOLD//

WITH SILVER DOWN $0.26 CENTS TODAY: AND WITH NO SILVER AROUND:

A HUGE CHANGES IN SILVER INVENTORY AT THE SLV//

A WITHDRAWAL OF 3.724 MILLION OZ FROM THE SLV//

RESTING SLV INVENTORY TONIGHT:

SLV: 572.843 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A CONSIDERABLE SIZED 2040 CONTRACTS FROM 194,807 DOWN TO 192,857, AND FURTHER FROM OUR NEW RECORD OF 244,710, (FEB 25/2020. THE LOSS IN OI OCCURRED WITH OUR STRONG 66 CENT LOSS IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE LOSS IN COMEX OI IS PRIMARILY DUE TO SOME BANKER SHORT COVERING COUPLED AGAINST A GOOD EXCHANGE FOR PHYSICAL ISSUANCE, TINY LONG LIQUIDATION, WITH A TINY DECREASE IN SILVER OZ. STANDING AT THE COMEX FOR AUGUST. WE HAD A SMALL NET LOSS IN OUR TWO EXCHANGES OF 870 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: SEP 1170 DEC: 0 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1170 CONTRACTS. WITH THE TRANSFER OF 562 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1170 EFP CONTRACTS TRANSLATES INTO 5.85 MILLION OZ ACCOMPANYING:

1.THE 44 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

86.470 MILLION OZ FINAL STANDING IN JULY.

6.465 MILLION OZ INITIAL STANDING IN AUGUST

WEDNESDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL 66 CENTS ).. AND, OUR OFFICIAL SECTOR/BANKERS WERE SOMEWHAT SUCCESSFUL IN THEIR ATTEMPT TO FLEECE SOME WEAK SILVER LONGS FROM THEIR POSITIONS. THEY ENGAGED IN SOME BANKER SHORT COVERING BUT JUDGING FROM THE SMALL LOSS ON THE TWO EXCHANGES, THEY COULD NOT COVER MUCH… THUS: THE CONSIDERABLE SIZED LOSS AT THE COMEX WAS ACCOMPANIED BY : i) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A SMALL DECREASE IN SILVER OZ STANDING FOR AUGUST, SOME BANKER SHORT COVERING AND 4) SOME LONG LIQUIDATION AS WE DID HAVE A SMALL NET LOSS OF 870 CONTRACTS OR 1.95 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKERS ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER..AND THUS THE REASON FOR OUR MASSIVE RAID THIS MORNING!!

SPREADING OPERATIONS/NOW SWITCHING TO SILVER

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN SILVER AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF AUGUST. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

AUGUST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF AUGUST:

14,185 CONTRACTS (FOR 15 TRADING DAY(S) TOTAL 14,185 CONTRACTS) OR 70.925 MILLION OZ: (AVERAGE PER DAY: 9456 CONTRACTS OR 4.728 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 70.925 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 9.29% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,341.22 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 133.95 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

AUGUST EXP 70.925 MILLION OZ (EXCHANGE FOR PHYSICALS STARTING TO DECREASE AGAIN)

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2040, DESPITE OUR STRONG 66 CENT LOSS IN SILVER PRICING AT THE COMEX ///WEDNESDAY AS ONE A NET BASIS, NOT TOO MANY LEFT THE SILVER ARENA..…THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1170 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE LOST A SMALL SIZED 2040 OI CONTRACTS ON THE TWO EXCHANGES (DESPITE OUR STRONG 66 CENT FALL IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 1170 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A GOOD SIZED DECREASE OF 2040 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 66 CENT FALL IN PRICE OF SILVER/AND A CLOSING PRICE OF $27.31 // WEDNESDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.9640 BILLION OZ TO BE EXACT or 138% of annual global silver production (ex Russia & ex China).

FOR THE NEW AUGUST DELIVERY MONTH/ THEY FILED AT THE COMEX: 4 NOTICE(S) FOR 20,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 WAS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 86.470 million oz//AUGUST 6.465 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 2684 CONTRACTS TO 546,694 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE SURPRISING GAIN IN COMEX OI OCCURRED DESPITE OUR STRONG LOSS IN PRICE OF $39.65 /// COMEX GOLD TRADING// WEDNESDAY//WE HAD SOME BANKER SHORT COVERING, A STRONG SIZED INCREASE IN GOLD TONNAGE STANDING AT THE COMEX FOR AUGUST, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR STRONG LOSS IN PRICE OF $39.65.

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 158

WE GAINED A GOOD SIZED 4432 CONTRACTS (13.784 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 1748 CONTRACTS:

CONTRACT .; AUG 0 AND OCT: 0 DEC: 1748; JUNE: 0 ALL OTHER MONTHS ZERO//TOTAL: 1748. The NEW COMEX OI for the gold complex rests at 546,694. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4432 CONTRACTS: 2684 CONTRACTS INCREASED AT THE COMEX AND 1748 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 4432 CONTRACTS OR 17.86 TONNES. WEDNESDAY, WE HAD A STRONG LOSS OF $39.65 IN GOLD TRADING..….

AND WITH THAT LOSS IN PRICE, WE HAD A GOOD SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 13.785 TONNES!!!!!! THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT FELL $39.65. WE DID HAVE A TINY BANKER SHORT COVERING OPERATION BUT JUDGING FROM THE GAIN IN COMEX OI AND THE GAIN IN EXCHANGES FOR PHYSICAL THEY COULD NOT FLEECE OUR SPECULATOR LONGS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1748) ACCOMPANYING THE SURPRISINGLY GOOD SIZED GAIN IN COMEX OI (2684 OI): TOTAL GAIN IN THE TWO EXCHANGES: 4432 CONTRACTS. WE NO DOUBT HAD 1 )TINY BANKER SHORT COVERING , 2.)A GOOD INCREASE IN GOLD TONNAGE STANDING AT THE GOLD COMEX FOR THE FRONT AUGUST MONTH, 3) ZERO LONG LIQUIDATION; 4) GOOD COMEX OI GAIN AND 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL AND …ALL OF THIS WAS COUPLED WITH OUR HUGE LOSS IN GOLD PRICE TRADING//WEDNESDAY//$39.65.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

AUGUST

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAY(S) IN TONNES: 100.23 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 100.23/3550 x 100% TONNES =2.67% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3,360.41 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 313.09 TONNES ..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

AUGUST TOTAL EFP ISSUANCE; 100.23 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A CONSIDERABLE SIZED 2040 CONTRACTS FROM 194,807 DOWN TO 192,857 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE CONSIDERABLE SIZED LOSS IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) SOME BANKER SHORT COVERING , 2) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A SMALL DECREASE IN SILVER OZ STANDING AT THE SILVER COMEX FOR AUGUST, AND 4) SOME WEAK LONG LIQUIDATION,

EFP ISSUANCE 1170 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT: 1170 AND DEC. 0 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1170 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2684 CONTRACTS TO THE 1170 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL LOSS OF 870 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 4.35 MILLION OZ, OCCURRED WITH OUR 66 CENT LOSS IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 44.23 POINTS OR 1.30% //Hang Sang CLOSED DOWN 387.52 POINTS OR 1.54% /The Nikkei closed DOWN 229.99 POINTS OR 1.00%//Australia’s all ordinaires CLOSED DOWN .67%

/Chinese yuan (ONSHORE) closed UP at 6.9166 /Oil UP TO 42.50 dollars per barrel for WTI and 44.58 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED UP // LAST AT 6.9166 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9129 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS //PANDEMIC// : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

i) Out of Manfra: 4822.65 oz

150 kilobars

total withdrawals; nil oz

We had 3 kilobar transactions +

ADJUSTMENTS: 0 //

i) Out of JPMorgan: 14,467.809.006 oz

The front month of AUGUST registered a total of 289 CONTRACTS as we LOST 246 contracts. We had 334 notices served on WEDNESDAY so we GAINED A STRONG 88 contracts or an additional 8800 OZ will stand for delivery on this side of the pond as they refused to morph into London based forwards as well as negating a fiat bonus. The boys are scrambling in search of badly needed physical metal as they start to search for metal on the other side of the pond.

After August we have the non active Sept contract month.. Here we saw another GAIN of 33 contracts to stand at 2396. Oct GAINED 2309 contracts UP to 72,379

The big December contract GAINED 608 contracts down to 399,795 contracts…(it is here where some of our short side bankers tried to bail and failed)

We had 40 notices filed today for 4000 oz

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2020. contract month, we take the total number of notices filed so far for the month (48,538) x 100 oz , to which we add the difference between the open interest for the front month of AUGUST (289 CONTRACTS ) minus the number of notices served upon today (40 x 100 oz per contract) equals 4,878,700 OZ OR 151.748 TONNES) the number of ounces standing in this active month of JUNE

thus the INITIAL standings for gold for the AUGUST/2020 contract month:

No of notices filed so far (48,538, x 100 oz + (289 OI) for the front month minus the number of notices served upon today (40) x 100 oz which equals 4,878,700 oz standing OR 151.748 TONNES in this active delivery month. This is a HUGE amount for gold standing for a AUGUST delivery month (an active delivery month).

We gained 88 contracts or 800 oz of gold as these guys refused to morph into London based forwards.

THE NAME OF THE GAME TODAY IS BANKER SHORT COVERING AS FINALLY FEAR BECAME THEIR CENTRAL FOCUS. THEY ORCHESTRATED A RAID TODAY SO AS TO CAUSE MANY SPECULATORS TO FLEE THE GOLD ARENA. IT LOOKS LIKE THEY FAILED.

NEW PLEDGED GOLD: BRINKS

144,088.952 oz NOW PLEDGED JAN 21.2020/HSBC 5.4807 TONNES

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

231,924.295 oz (some deleted august 3) JPM 7.2138 TONNES

611,401.341 oz pledged June 12/2020 Brinks/ july 2/july 21 19.017 tonnes

total pledged gold: 1,029,962.895 oz 32.03 tonnes

total registered, pledged and eligible (customer) gold; 37,337,506.8.11 oz 1,161.35 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1035.01 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

998.79

CNT

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

nil

|

| No of oz served today (contracts) |

4

CONTRACT(S)

(20,000 OZ)

|

| No of oz to be served (notices) |

15 contracts

75,000 oz)

|

| Total monthly oz silver served (contracts) | 1278 contracts

6,390,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 0 deposits into the customer account

i)into JPMorgan: nil oz

ii) Into everybody else: 0

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 165.53 million oz of total silver inventory or 48.75% of all official comex silver. (165.53 million/339.452 million

total customer deposits today: nil oz

we had 1 withdrawals:

ii) Out of CNT: 85,734.290 oz

total withdrawals; 536,900.510 oz

We had 0 adjustments

Total dealer(registered) silver: 129.555 million oz

total registered and eligible silver: 339.453 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

the front month of August registered an open interest of 19 contracts and thus we LOST 3 contracts. We had 0 notices filed on WEDNESDAY so we LOST 3 contracts or an additional 15,000 oz will NOT stand for delivery as these guys morphed into London based forwards as well as accepting a fiat bonus for their efforts…. The bankers are now desperate in their search for badly needed silver whether it is on this side of the pond or the European side.

After August we have the big September contract month and here we see a loss 6104 contracts down to 71,118. November saw another gain of 22 contracts to stand at 305.

SEPT OI IS VERY HIGH AND WE WILL HAVE A DANDY AMOUNT OF SILVER STANDING AT THE COMEX.

The big December contract month saw its OI rise by good 4057 contracts up to 109,519

The total number of notices filed today for the AUGUST 2020. contract month is represented by 4 contract(s) FOR 20,000, oz

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 1278 x 5,000 oz = 6,390,000 oz to which we add the difference between the open interest for the front month of AUGUST(19) and the number of notices served upon today 4 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the AUGUST/2019 contract month: 1278 (notices served so far) x 5000 oz + OI for front month of AUGUST (19)- number of notices served upon today (4) x 5000 oz of silver standing for the AUGUST contract month.equals 6,465,000 oz. ..VERY STRONG FOR A NON ACTIVE MONTH.

We lost 3 contracts or an additional 15,000 oz will not stand for delivery as they morphed into London based forwards..

TODAY’S ESTIMATED SILVER VOLUME : 92,524 CONTRACTS // volume excellent+++++/

FOR YESTERDAY: 248,883. ,CONFIRMED VOLUME//volume huge.++++++++++++++++++++++++++++++++++++++++++++++++++++

YESTERDAY’S CONFIRMED VOLUME OF 248883 CONTRACTS EQUATES to 1.244 billion OZ 178% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO- 2.51% ((AUGUST 20/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.10% to NAV: (AUGUST 19/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/2.51%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 20.55 TRADING 20.27///NEGATIVE 1,35

END

And now the Gold inventory at the GLD/

AUGUST 20/WITH GOLD DOWN $23.45 TODAY: WE HAD NO CHANGED IN GOLD INVENTORY AT THE GLD: .//INVENTORY REST AT 1252.38 TONNES

AUGUST 19//WITH GOLD DOWN $39.65 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1252.38 TONNES

AUGUST 18/WITH GOLD UP $14.60 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 4.09 TONNES//GLD INVENTORY RESTS TONIGHT AT 1252.38 TONNES

AUGUST 17/WITH GOLD UP $46.30 TODAY: SURPRISINGLY WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 3.8 TONNES//INVENTORY RESTS AT 1248.29 TONNES

AUGUST 14/ WITH GOLD DOWN $19.45 TODAY: SURPRISINGLY, WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.46 TONNES/INVENTORY RESTS AT 1252.63 TONNES.

AUGUST 13/WITH GOLD UP $23.15 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY: SURPRISINGLY A PAPER WITHDRAWAL OF 7.30 TONNES/INVENTORY RESTS AT 1250.63 TONNES

AUGUST 12/ WITH GOLD UP $1.00 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 4.19 TONNES//INVENTORY RESTS AT 1257.93 TONNES

AUGUST 11//WITH GOLD DOWN $92.40 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1262.12 TONNES.

AUGUST 10/WITH GOLD UP $11.35 TODAY, WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.84 TONNES//INVENTORY RESTS AT 1262.12 TONNES

AUGUST 7/WITH GOLD DOWN $38.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1267.96 TONNES

AUGUST 6/WITH GOLD UP $20.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER DEPOSIT OF 10.23 TONNES INTO THE GLD/INVENTORY RESTS AT 1267.96 TONNES//

AUGUST 5/WITH GOLD UP $ 33.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 9.35 TONNES INTO THE GLD//INVENTORY RESTS AT 1257.73 TONNES

AUGUST 4//WITH GOLD UP $31.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 6.48 TONNES/GLD INVENTORY RESTS AT 1248.38 TONNES

AUGUST 3/WITH GOLD UP $2.20 TODAY, WE HAVE NO CHANGES IN THE GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241,96 TONNES

JULY 31/WITH GOLD UP $17.90 TODAY/WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241.96 TONNES.

JULY 30/WITH GOLD DOWN $10.00 TODAY, WE HAVE ANOTHER SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES//INVENTORY RESTS AT 1241.96 TONNES.

JULY 29//WITH GOLD UP $12.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 8.47 TONNES/INVENTORY RESTS AT 1243.12 TONNES

JULY 28///WITH GOLD UP $13.25 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 5.84 TONNES/INVENTORY RESTS AT 1234.65

JULY 27//WITH GOLD UP $35.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF XXX TONNES/INVENTORY RESTS AT 1228.81 TONNES

JULY 24/WITH GOLD UP $8.80 TODAY: WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.80 TONNES//INVENTORY RESTS AT 1228.81 TONNES

JULY 23/WITH GOLD UP $24.90 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 7.26 TONNES/INVENTORY RESTS AT 1225.01 TONNES

JULY 22/WITH GOLD UP $22.00 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 7.89 TONNES/INVENTORY RESTS AT 1219.75 TONNES

JULY 21//WITH GOLD UP $26.00 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.97 TONNES INTO THE GLD// INVENTORY RESTS AT 1211.86 TONNES

JULY 20/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1206.89 TONNES

JULY 17/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1206.89 TONNES

JULY 16/WITH GOLD DOWN $9.80 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: INVENTORY RESTS AT 1206.89 TONNES

JULY 15//WITH GOLD UP $1.55 TODAY/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 2.96 TONNES INTO THE GLD///INVENTORY RESTS AT 1206.89 TONNES

JULY 14//WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 3.51 TONNES/INVENTORY RESTS AT 1203.97 TONNES

JULY 13//WITH GOLD UP $12.50 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1200.46 TONNES

JULY 10/WITH GOLD DOWN $.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD//A STRANGE WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1200.82 TONNES

JULY 9//WITH GOLD DOWN $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OX 3.21 TONNES INTO THE GLD//INVENTORY RESTS AT 1202.57 TONNES

JULY 8/WITH GOLD UP $13.75 TODAY; A BIG CHANGE IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 7.89 TONNES INTO THE GLD//INVENTORY RESTS AT 1199.36 TONNES

JULY 7/WITH GOLD UP $12.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1191.47 TONNES

JULY 6/WITH GOLD UP $6.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1191.47 TONNES

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

AUGUST 20/ GLD INVENTORY 1252.38 tonnes*

LAST; 885 TRADING DAYS: +312.88 NET TONNES HAVE BEEN ADDED THE GLD

LAST 785 TRADING DAYS://+491,41 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

AUGUST 20/WITH SILVER DOWN $.26 TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 3.724 MILLION OZ FROM THE SLV..//INVENTORY REST AT 572.843 MILLION OZ

AUGUST 18/WITH SILVER UP $.44 TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.514 MILLION OZ//THE SLV INVENTORY RESTS TONIGHT AT 576.567 MILLION OZ//

AUGUST 17/WITH SILVER UP $1.27 TODAY: WE HAD NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 14/WITH SILVER DOWN $1.31 TODAY, WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.984 MILLION OZ// //INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 13//WITH SILVER UP $1.76 TODAY: WE HAVE TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A PAPER DEPOSIT OF 2.421 MILLION OZ INTO THE SLV AT 2 PM AND ANOTHER DEPOSIT OF 6.984 MILLION OZ AT 5 20 PM/INVENTORY RESTS AT 581.037 MILLION OZ//

AUGUST 12/WITH SILVER DOWN 40 CENTS TODAY: WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF XX MILLION OZ//INVENTORY RESTS AT XX MILLION OZ/

AUGUST 11/WITH SILVER DOWN $3.25 CENTS, WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.41 MILLION OZ//INVENTORY RESTS AT 571.632 MILLION OZ//

AUGUST 10/WITH SILVER UP 1.89 TODAY, WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 3.538 MILLION OZ/INVENTORY RESTS AT 569.491 MILLION OZ//

AUGUST 7/WITH SILVER DOWN 69 CENTS TODAY: WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY: A DEPOSIT OF 0.465 MILLION OZ/INVENTORY RESTS AT 573.029 MILLION OZ.

AUGUST 6/WITH SILVER UP $1.52 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 572.564 MILLION OZ///

AUGUST 5/WITH SILVER UP $1.03 TODAY, WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A MONSTROUS DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 572.564 MILLION OZ//

AUGUST 4/WITH SILVER UP $1.45 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 367.161 MILLION OZ//

AUGUST 3/WITH SILVER UP 23 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//SURPRISINGLY ANOTHER WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 367.161 MILLION OZ//

JULY 31/WITH SILVER UP 82 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: SURPRISINGLY A HUGE WITHDRAWAL OF 3.26 MILLION OZ//INVENTORY RESTS AT 368.092 MILLION OZ//

JULY 30//WITH SILVER DOWN 97 CENTS TODAY: WE HAVE A SMALL CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 571.352 MILLION OZ//

JULY 29/WITH SILVER UP 7 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY//A DEPOSIT OF 5.984 MILLION OZ//INVENTORY RESTS AT 572.283 MILLION OZ//

JULY 28 WITH SILVER DOWN 14 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 7.52 MILLION OZ//INVENTORY RESTS AT 566.299 MILLION OZ//

JULY 27/WITH SILVER UP $2.67 TODAY, WE HAD NO CHANGES IN SILVER INVENTORY: A DEPOSIT OF XX MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ//

JULY 24/WITH SILVER DOWN $0.12 TODAY: NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 558.779 MILLION OZ/

JULY 23/WITH SILVER UP $.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A HUMONGOUS PAPER DEPOSIT OF 9.594 MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ///

JULY 22/WITH SILVER UP $1.54 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A HUMONGOUS PAPER DEPOSIT OF 7.218 MILLION OZ//INVENTORY RESTS AT 549.185 MILLION OZ/

JULY 21/WITH SILVER UP $1.38 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUMONGOUS PAPER DEPOSIT OF 15.368 MILLION OZ////INVENTORY RESTS AT 541.967 MILLION OZ//

JULY 20/WITH SILVER UP 40 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 3.819 MILLION OZ ‘ENTERED” THE SLV..INVENTORY RESTS AT 526.599 MILLION OZ/

JULY 17/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 1.583 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 522.780 MILLION OZ//

JULY 16//WITH SILVER DOWN 14 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ//INVENTORY RESTS AT 521.197 MILLION OZ..

JULY 15.WITH SILVER UP 21 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.956 MILLION OZ//INVENTORY RESTS AT 516.074 MILLION OZ//

JULY 14/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 514.118 MILLION OZ//

JULY 13//WITH SILVER UP 67 CENTS TODAY: A HUGE CHANGE IN SILVER: A WITHDRAWAL OF 1.677 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 514.118 MILLION OZ//

JULY 10/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 4.844 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.795 MILLION OZ

WHAT A FRAUD!!

JULY 9/WITH SILVER DOWN 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 8.198 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 510.951 MILLION OZ/

JULY 8/WITH SILVER UP 37 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.118 MILLION OZ FROM THE SLV//VERY SURPRISING.//INVENTORY RESTS AT 502.753 MILLION OZ//

JULY 7/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/INVENTORY RESTS AT 503.871 MILLION OZ///

JULY 6//WITH SILVER UP 24 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.863 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 503.871 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

AUGUST 20.2020:

SLV INVENTORY RESTS TONIGHT AT

572.843 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

Big news but just the tip of the iceberg: Scotia bank pays 127 million dollars to settle gold and silver manipulating claims

(zerohedge/GATA)

Scotiabank pays $127.4 million to settle gold and silver spoofing claims

Submitted by cpowell on Thu, 2020-08-20 01:05. Section: Daily Dispatches

By Matt Robinson

Bloomberg News

Wednesday, August 19, 2020

Bank of Nova Scotia agreed to pay $127.4 million to settle U.S. allegations that the company engaged in spoofing of gold and silver futures contracts, and made false statements to the government.

As part of the accord, Bank of Nova Scotia will pay a $17 million fine on Commodity Futures Trading Commission claims that it dramatically misrepresented the scope of the alleged wrongdoing.

…

..The bank made multiple false statements during the CFTC’s investigation of a spoofing case that was resolved in 2018 for $800,000, the agency said. The regulator said the new punishment reflects Bank of Nova Scotia’s lack of cooperation in the earlier probe and actions it took to conceal its misconduct.

“Entities seeking to cooperate with the CFTC, like all others that interact with the commission, must tell the truth,” James McDonald, the agency’s enforcement chief said in a statement. “When entities are not completely truthful, they will be penalized.”

Bank of Nova Scotia also agreed to a deferred prosecution agreement with the Justice Department tied to criminal charges of attempted price manipulation and wire fraud. Under the agreement, the Toronto-based lender will pay $60.4 million in fines, forfeiture, and restitution, which will be offset by the CFTC order. The bank also agreed to hire an independent monitor for three years. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2020-08-19/scotiabank-to-pay-127…

Bank Of Nova Scotia Pays $127 Million In Fines Over Criminal Precious Metal Manipulation

Back in April, we reported that one of the pillars in the gold-trading business, Bank of Nova Scotia’s ScotiaMocatta business was closing after failing to find a buyer in a sale process that had started in late 2017. As we further reported, Scotia was for years the world’s biggest lender to the physical precious metals industry, with a history stretching to the founding in 1684 of London gold dealer Mocatta Bullion, which it bought in 1997. Once a global player with more than 100 staff in offices from New York and London to India and Hong Kong, the bank effectively exited the business in 2018 following the above mentioned strategic review and unsuccessful attempt to find a buyer.

The sudden exit of one of the core precious metal traders left many wondering if some big news was about to hit. Well, that’s precisely what happened, because earlier today the Department of Justice announced that Bank of Nova Scotia has agreed to pay more than $127 million in fines to settle criminal investigations into a price manipulation scheme in the price of precious metals that saw the participation of at least four of itw traders.

The fines consist of $60.4 million to the Department of Justice with the remainder going to the CFTC in the form of two monetary penalties of $42 million and $17 million.

“Today, Scotiabank has admitted to their role in a massive price manipulation scheme aimed at falsely manufacturing the prices of precious metals futures contracts to serve the bank’s best interests,” said Assistant Director in Charge William F. Sweeney Jr. of the FBI’s New York Field Office.

“The bank’s actions were designed to lead others to trade in ways they never would have without what was believed to be legitimate market activity. Scotiabank’s agreement to surrender more than $60 million in criminal fines, disgorgement and victim compensation underscores the severe penalties that can be levied against those who wish to engage in similar, illegal business tactics.”

The Canadian bank agreed to a deferred prosecution agreement (DPA) to settle separate probes by the Department of Justice and the U.S. commodities regulator, the Commodity Futures Trading Commission (CFTC).

According to an agreed upon statement of facts, between January 2008 and July 2016, four precious metals traders employed by Scotia in New York, London and Hong Kong made bogus trades to try to manipulate the price of gold, silver, platinum and palladium futures contracts by engaging in manipulative spoofing of the type demonstrated repeatedly on this website and elsewhere.

“For over eight years, Scotiabank traders placed thousands of orders for precious metals futures contracts in an attempt to manipulate prices for their own and the bank’s benefit and to deceive other market participants,” said Chief Robert A. Zink of the Justice Department’s Criminal Division, Fraud Section. “This deferred prosecution agreement—which includes a criminal monetary penalty at the top of the United States Sentencing Guidelines range, money to compensate victims, and an independent compliance monitor—reflects the seriousness of the offense and the state of Scotiabank’s compliance program, and further helps to promote the integrity of our public markets.”

According to the settlement, “four Scotiabank traders attempted to rig precious metals futures prices in their favor by placing thousands of orders they knew they would cancel before the trades were executed,” U.S. Attorney Craig Carpenito said, describing a financial practice known as “spoofing.”

“In this way, they sought to illegally manipulate the market to their own advantage and to the disadvantage of other traders.”

The bank is also being punished because its compliance department “failed to detect or prevent the four traders’ unlawful trading practices,” the DOJ said.

“Between August 2013 and February 2016, three Scotiabank compliance officers possessed information regarding unlawful trading by one of the traders … but failed to prevent further unlawful conduct by this same trader,” the Department said.

While it was previously reported that Scotiabank, along with other banks such as JPMorgan and Merrill Lynch had participated in illegal spoofing for the better part of a decade, and was already forced to pay $800,000 in 2018 for the matter, the kicker is that according to the CFTC, the bank made false statements during the organization’s investigation necessitating another $77.4 million in payments.

According to admissions and court documents, between approximately January 2008 and July 2016, four precious metals traders located in New York, London and Hong Kong engaged in fraudulent and manipulative trading practices in the markets for gold, silver, platinum, and palladium futures contracts (collectively, precious metals futures contracts) that traded on the New York Mercantile Exchange Inc. (NYMEX) and Commodity Exchange Inc. (COMEX), which are commodities exchanges operated by the CME Group, Inc. One of the traders, Corey Flaum, 42, of Delray Beach, Florida, pleaded guilty on July 25, 2019, to one count of attempted price manipulation in connection with his precious metals futures contracts trading at Scotiabank and another financial services firm, and his sentencing is scheduled for Jan. 27, 2021, before U.S. District Judge Brian M. Cogan of the Eastern District of New York.

Scotiabank did not receive voluntary disclosure credit because it did not voluntarily and timely disclose the offense conduct to the department. In 2016, after one of its futures commission merchants flagged trading by Flaum for possible spoofing, Scotiabank made a voluntary disclosure regarding Flaum to the CFTC. As a result of recordkeeping failures, however, Scotiabank’s disclosure to the CFTC was materially incomplete. As a result, the CFTC was impaired in its ability to fully investigate Flaum’s unlawful trading and discover the true extent of the misconduct. The CFTC, relying on Scotiabank’s incomplete and, ultimately, inaccurate disclosure, entered into a resolution with Scotiabank in 2018 that did not reflect the full extent of Flaum’s conduct (2018 CFTC Resolution). In the 2018 CFTC resolution, Scotiabank received a substantially reduced penalty in recognition of, among other things, its purported self-reporting.

As part of the DPA, Scotiabank has agreed to continue to cooperate with the department in any ongoing investigations and prosecutions relating to the underlying misconduct, to modify its compliance program where necessary and appropriate, and to retain an independent compliance monitor for a period of three years.

“At Scotiabank, we understand that in order to maintain the trust of our stakeholders, we must adhere to trading-related regulatory requirements and compliance policies,” the bank said in a statement Wednesday. “We are committed to adhering to these standards.”

Sadly, the only thing that Scotia is truly committed to is making sure it does not get caught the next time it is rigging the price of gold.

iii) Other physical stories:

The U.S. Mint Sells Another Million Silver Eagles In One Day

By SRSroccoin News, Precious Metals on

With Silver Eagle demand continuing to be RED HOT, the U.S. Mint sold another million of the coins yesterday. This is the biggest one-day sales increase in six months. It seems as if the U.S. Mint is now able to ramp up production of both Gold and Silver Eagles.

In my last update, After Months Of Supply Issues, U.S. Mint Silver Eagle Sales Jump In August, I stated that sales for Silver Eagles reached the highest level at 1,593,000 on Monday since March. I thought we might see a slow and steady rise in Silver Eagle sales out of the U.S. Mint, but when they updated their website, it jumped another one million yesterday. Total sales of Silver Eagles are now 2,593,000.

I have to tell you; this is quite amazing as the average premium for many of the larger online dealers is running more than $10 per coin (based on sales of 1-19 coins). Actually, the best prices I have seen from the leading online dealers is $9+ per coin (based on sales of 500+ coins). So, the high premiums don’t seem to be curtailing Silver Eagle investment demand.

Total Silver Eagle sales for 2020 are already 16.3 million versus 14.8 million for 2019 and 15.7 million for 2018. So, with four more months remaining in the year, it looks like Silver Eagle sales are quickly going to surpass 20 million, and quite possibly 25 million.

Lastly, the U.S. Mint is now providing the lower denomination Gold Eagles. Here are the sales of Gold Eagles as of Tuesday, August 17th:

Gold Eagle Sales For August 2020 (coin amounts)

1/10 oz = 20,000 coins

1/4 oz = 12,000 coins

1/2 oz = 5,000 coins

1 oz = 84,000 coins

When I posted the update on Monday, the U.S. Mint didn’t show any sales of the smaller denomination Gold Eagle coins. Thus, in one day, the U.S. Mint sold an additional 22,000 oz of Gold Eagle coins, mainly the 1 oz coins (14,500).

I believe we are just now seeing a glimpse of the enormous demand to come for silver and gold bullion products over the next several years as the Fed and central banks continue to prop up the global economy with massive monetary stimulus and liquidity.

-END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

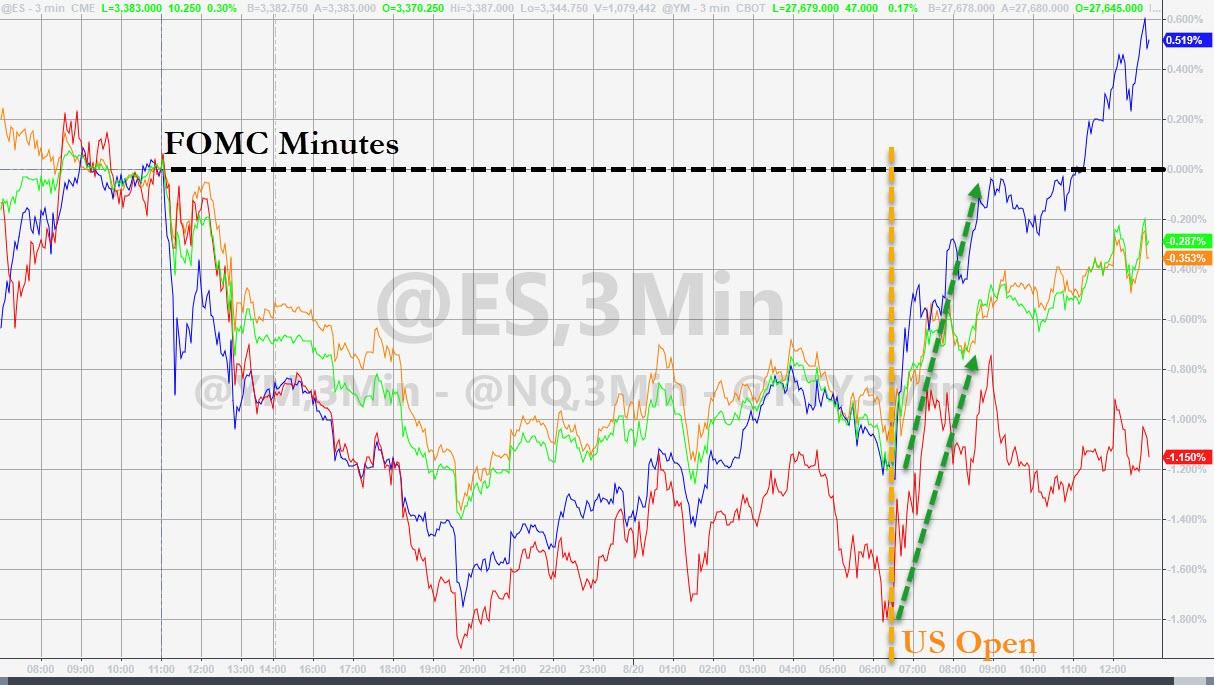

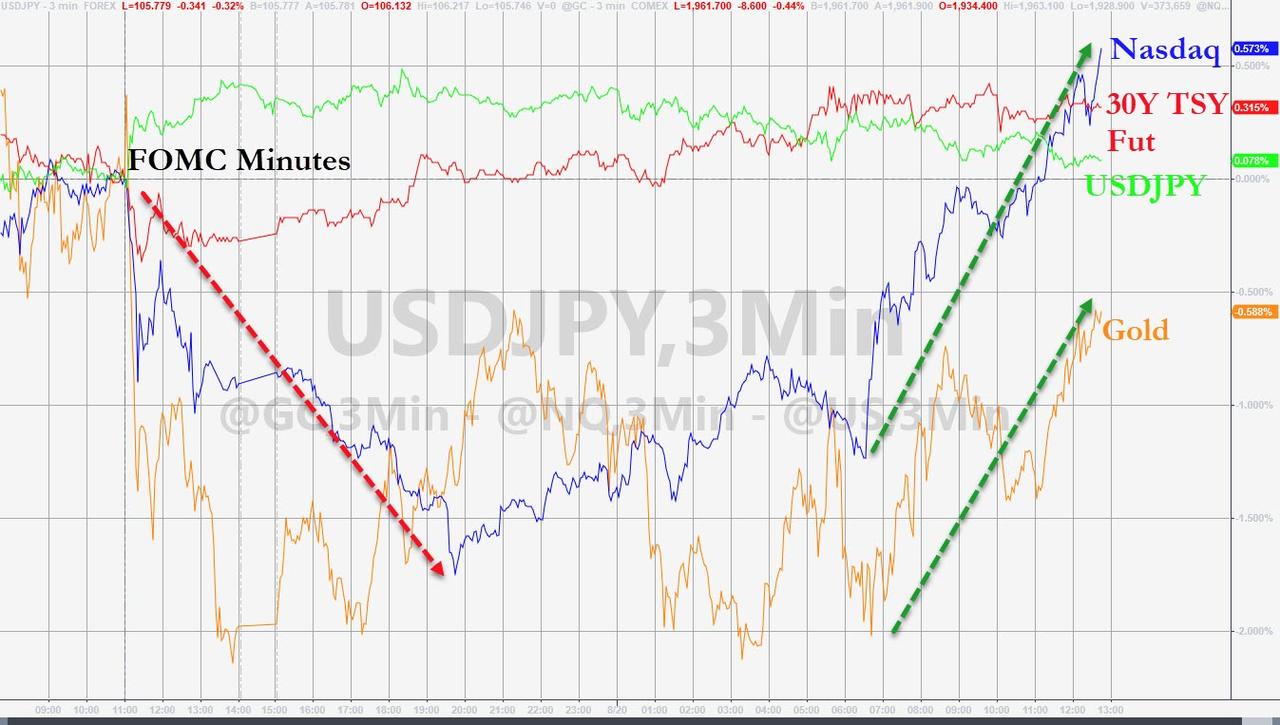

Global Stocks Slide After Fed Minutes Disappoint

US equity futures, Asian and European markets fell on Thursday after the U.S. Federal Reserve’s latest meeting minutes did not guide to more easing or hint at yield curve control while highlighting doubts about the recovery of the world’s largest economy which knocked the S&P500 from its record highs, although sentiment got a modest boost overnight after China announced it had agreed with the US to resume trade talks “in the coming days” to evaluate the progress of their Phase 1 trade deal.

Among early movers, Nvidia Corp slipped 1.1% in premarket trade after results from the data center business of the rising semiconductor industry star disappointed some investors. Intel Corp rose 4% after announcing an accelerated $10-billion share buyback plan. L Brands rose 1.3% after reporting a surprise quarterly profit, boosted by strong demand for Bath & Body Works’ products as well as higher online sales of Victoria’s Secret lingerie.

Markets stumbled after the Fed’s minutes from its July meeting highlighted doubts about the U.S. economic recovery, showing that the swift labor market rebound seen in May and June had likely slowed. “Of course, the Fed agreed that the virus is weighing heavily on the economy: is that some kind of surprise? Apparently it was,” Rabobank’s global strategist Michael Every wrote in a note to clients.

Yet despite the overall dovish sentiment, U.S. Treasury yields and the dollar surged with investors focusing on parts of the minutes that showed policymakers downplaying the need for yield caps and targets, nor did they hint at any additional QE.

“There is still a fair amount of uncertainty around the path of the coronavirus, through the flu season, and what that may mean for economic growth,” Jim McDonald, chief investment strategist at Northern Trust, said on Bloomberg TV. “Stocks are somewhat expensive here – we struggle to get to a meaningful positive return on stocks over the next year just because we’ve priced in so much of a recovery already.”

As Bloomberg notes, equities in several continents are seeing fresh weakness as investors debate whether momentum that pushed the S&P 500 to a record high this week can be sustained amid lofty valuations and delays in further stimulus to counter the pandemic. While France, Spain and Austria reported the highest daily infections in months, cases have subsided in a few populous U.S. states. Weekly unemployment figures are due in Washington later Thursday.

“The key question for investors is whether the policy responses are enough to mitigate the economic damage,” hedge fund firm Brevan Howard said in an interim report published on Thursday. “Many businesses face solvency risks that are not addressed by borrowing; a debt overhang cannot be cured by more borrowing no matter how cheap it may be,” the fund’s report added.

“Improved financial conditions are narrowly focused on a handful of large companies and benefiting stakeholders who need relatively little economic assistance. The result is that financial assets are expensive by many standard metrics. So long as a V-shaped recovery in risky assets fails to create a V-shaped recovery in economic activity, this tension is a recipe for increased volatility.”

The MSCI world equity index was also impacted, sliding 0.6% early on Thursday. The pan-European STOXX 600 was down 0.9% and London’s FTSE 100 fell 0.8%. European equities slumped following a downbeat Asian session. Eurostoxx 50 dropped as much as 1.5%, with the CAC lagging peers. Miners, banking names and financial services are the worst performing sectors; real estate manages small gains

Earlier in the session, MSCI’s index of Asia-Pacific shares outside Japan had its biggest daily decline in five weeks. All markets in the region were down, with South Korea’s Kospi Index dropping 3.7% and Taiwan’s Taiex Index falling 3.3%. The Topix declined 0.9%, with Carta Holdings Inc and Mitani Sekisan falling the most. The Shanghai Composite Index retreated 1.3%, with Junzheng Energy and Yijiahe Tech posting the biggest slides. Hong Kong stocks fell for a second session as the U.S. suspended its extradition treaty with Hong Kong and ended reciprocal tax treatment with the former British colony.

In FX, the dollar index was choppy overnight after yesterday’s sharp spike but appeared to resume rolling over following the news the US and China had agreed to resume trade talks.

Elsewhere, the euro fluctuated ahead of the release of the ECB meeting’s minutes, and the Norwegian Krone slipped after Norges Bank announced it will probably keep interest rates at a record low for “some time ahead.” The Turkish lira tumbled after the central bank kept rates on hold. The CBRT also increased required FX reserves ratio for banks that meet growth target by 700bps for all maturities for precious metal repo accounts; all other RRR for FX raised by 200bps.

Treasuries reversed their Wednesady slump and were higher across the curve, led by the long end, amid gains for most developed sovereign bond markets and declines for equities globally. Yields are lower by about 4bp at long end, 10-year by ~3bp at 0.65%, flattening 2s10s and 5s30s curves by ~2bp; S&P 500 futures are lower after cash index Wednesday declined from a record high. 20-year yield is lower by 3bp at 1.165%. The new 20-year bond, which got a cool reception at Wednesday’s auction, is trading at a profit, as are the new 10-year and 30-year issues sold last week. This week’s final auction, a $7b 30-year TIPS reopening, is ahead at 1pm ET.

Germany’s benchmark 10-year Bund yield was at -0.473%, little changed after falling for the past four days in a row. Three-month Euribor fell to a record low, less than four months after rising to a four-year high, helped by the ECB’s policy to provide lenders with cheap loans in response to the economic damage of the pandemic.

In commodities, spot gold rebounded overnight, after declining to a near one-week low on Wednesday, when markets were more bullish. It was up 0.6% at $1,940.4478 per ounce. Oil prices fell, as major producers warned of a risk to demand recovery. OPEC and its allies pressed oil nations that are pumping above output targets to cut more in August to September. Brent crude was down 32 cents, or 0.7%, at $45.05 a barrel while WTI was down 38 cents, or 0.9%, at $42.55 a barrel.

Overnight, U.S. Congressional leaders hinted they were looking for a path toward reviving stalled talks on the next round of pandemic relief – even as both sides remain far from a deal. Any accord is still likely to wait until September despite the fact that the U.S. economy is limping along with many businesses still struggling and millions of Americans out of work.

On the day’s calendar, data from the Labor Department, due at 8:30 a.m. ET (1230 GMT), is expected to show the number of Americans seeking jobless benefits dipped to 925,000 in the week ended Aug. 15.

Market Snapshot

- S&P 500 futures down 0.4% to 3,360.00

- Brent futures down 0.8% to $45.00/bbl

- Gold spot up 0.3% to $1,934.33

- U.S. Dollar Index up 0.3% to 93.16

- Stoxx Europe 600 down 1.4% to 364.59

- MXAP down 1.6% to 169.27

- MXAPJ down 1.8% to 557.36

- Nikkei down 1% to 22,880.62

- Topix down 0.9% to 1,599.20

- Hang Seng Index down 1.5% to 24,791.39

- Shanghai Composite down 1.3% to 3,363.90

- Sensex down 1.2% to 38,160.20

- Australia S&P/ASX 200 down 0.8% to 6,120.02

- Kospi down 3.7% to 2,274.22

- German 10Y yield fell 1.2 bps to -0.484%

- Euro down 0.2% to $1.1818

- Italian 10Y yield fell 1.3 bps to 0.788%

- Spanish 10Y yield rose 1.1 bps to 0.303%

Top Overnight News from Bloomberg

- U.S. central bankers backed off in July from an earlier readiness to set a clearer bar for raising interest rates, a step that would underscore their commitment to an extended period of ultra-loose monetary policy

- Coronavirus infections flared in Europe, with France and Spain reporting their biggest increases in months. South Korea confirmed 288 more cases, while Hong Kong’s outbreak showed signs of easing

- French president Emmanuel Macron ruled out shutting down the country once again even as the virus resurges across several European nations. He said the “collateral damage of confinement is considerable”. Cases in France were up 3,776, the most in three months, while Spain recorded 3,715 new infections. Germany recorded more than 1,000 new infections for the third day in a row.

- Russia’s opposition leader Alexey Navalny is in intensive care in “serious condition” with suspected poisoning. Navalny is Russia’s most prominent opponent to Vladimir Putin.

- As Brexit trade talks approach their deadline, the European Union’s top markets regulator called for rule changes that could limit firms’ ability to manage money in the bloc from London.

- China and the U.S. will hold talks in the near term to discuss the progress of their trade deal, Beijing said, without mentioning a precise date, after last week’s call was postponed.

- Three-month Euribor fell to a record low, less than four months after rising to a four-year high, helped by the ECB’s policy to provide lenders with cheap loans in response to the economic damage of the pandemic.

- The U.S. suspended its extradition treaty with Hong Kong and ended reciprocal tax treatment on shipping with the former British colony, the latest salvo in escalating tensions between Washington and Beijing

- President Donald Trump said he would call on the United Nations Security Council to restore all nuclear- related sanctions on Iran, an attempt to kill off the 2015 nuclear agreement and force Tehran back to the negotiating table

- OPEC+ kept up the pressure on Nigeria and Iraq to stop cheating on their crude-production targets, emphasizing the need for all members to stick closely to their agreement because the market recovery remains fragile

- Kamala Harris, the California senator Joe Biden selected as his running mate, opened the third night of the Democrats’ virtual convention by urging the party to defy what she called a Republican effort to suppress their votes

Asian equity markets traded lower across the board amid headwinds from Wall St where stocks faltered in the aftermath of the less accommodative than expected FOMC Minutes which triggered a pullback in the S&P 500 and the Nasdaq from record highs, while Apple shares also retraced the majority of the early gains that had briefly pushed the tech giant to the unprecedented USD 2tln market cap status. ASX 200 (-0.8%) was pressured by a slate of weak earnings and with underperformance seen in energy names, while Nikkei 225 (-1.0%) retreated below the 23,000 level with Tokyo exporters dragged by a predominantly firmer currency. Hang Seng (-1.5%) and Shanghai Comp. (-1.3%) conformed to the downbeat tone after the US State Department either suspended or terminated three bilateral agreements with Hong Kong and reports also suggested the likelihood of a RRR cut this year has declined with the central bank expected to inject liquidity through reverse repos and MLF operations instead. In addition, the PBoC maintained the 1-year and 5-year Loan Prime Rates at 3.85% and 4.65% as expected, while there were reports US and Chinese trade negotiators plan to confer by video in the coming days regarding the Phase 1 trade deal progress and US actions against Chinese tech firms, although this failed to provide any support for stocks. Finally, 10yr JGBs were initially kept afloat by the risk averse tone but with the upside restricted following the post-FOMC pressure in T-notes and with participants sidelined heading into the 5yr JGB auction which turned out to a be a weaker than previous auction and subsequently weighed on prices.

Top Asian News

- Saudi Support for 2002 Plan Shows It Won’t Copy UAE-Israel Pact

- RBL Bank to Raise $209 Million With Preference Share Sale

- Thailand Arrests Leaders of Protests Challenging the Monarchy

- Philippines Central Bank Pauses After Series of Rate Cuts

European equities trade lower across the board (Eurostoxx 50 -1.3%) as market participants digest the fallout of the FOMC minutes which were judged to be less dovish than some had hoped for. Furthermore, geopolitical tensions have been ratcheted up once again in the wake of comments from US Secretary of State Pompeo who warned that the US will hold China and Russia accountable if they attempt to block sanctions snapback on Iran. Separate reports have noted that US and Chinese trade negotiators plan to confer by video in the coming days over Phase One progress, however, no date has been set yet and expectations for the call, should it take place, will likely be relatively low. In terms of the tone of the market in Europe, all sectors trade in the red, with some of the more defensive sectors such as health care and utilities faring slightly better than peers, but ultimately still lower on the day. Basic resources are a laggard in the region following recent declines in both precious and base metals and post-Antofagasta (-4.8%) earnings with the Co. reporting a 22.4% decline in H1 core earnings amid the COVID-19 crisis; note, the Co. will nonetheless pay an interim dividend. Somewhat of a divergence has been seen in the travel & leisure sector with airlines such as IAG (-4.8%), Ryanair (-3.1%) and easyJet (-2.3%) lower as the UK is set to further expand its list of countries which will force travelers to self-isolate upon return. Conversely, hotel names are faring slightly better with Accor (+0.7%) and InterContinental Hotels (+1.0%) supported by reports in French media suggesting that the former could put in a bid for the latter. Elsewhere, as part of a more anti-cyclical bias, banks and auto names are faring relatively poorly this morning, for banks-specifically, some of the laggards are predominantly Spanish names, which could be a reflection of mounting COVID-19 cases in the nation.

Top European News

- Schaeffler Looks to Raise $1.5 Billion Amid Pandemic Fallout

- Swedish Match Misrepresented Oral Nicotine, Lawmakers Say

- Macron Rules Out Shutdown as Europe Grapples With Virus Upsurge

- Adyen Clinches Wirecard Clients During Online Shopping Boom

In FX, the DXY index oscillates on either side of 93.000 in the aftermath of the FOMC minutes – which pushed back on expectations that further policy action will arrive soon as it indicated that members are not inclined to a forward guidance change and YCC. The release propped up the broader Dollar and index back above the 93.000 mark to a high (yesterday) at 93.059, but thereafter trickled back below the figure as the dust settled in early European hours. The index has since regained traction and printed a fresh intraday peak just under 93.200. with the 21 DMA in proximity at 93.336. US stimulus talks will likely regain focus alongside US-Sino developments, whilst US Philly Fed and the weekly initial and continuing jobless claims, and Fed non-voter Daly are on today’s docket.