GOLD:$1939.90 DOWN $0.40 The quote is London spot price

Silver:$26.75 DOWN $0.30 London spot price ( cash market)

Today marks the 6TH day out of the last 9 days that a raid has been orchestrated by the bankers..

DEFINITION OF INSANITY:

DONATE

Closing access prices: London spot

i)Gold : $1938.40 LONDON SPOT 4:30 pm

ii)SILVER: $26.83//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUGUST GOLD: $1931.40 CLOSE 1::30 PM SPREAD SPOT/FUTURE AUG (BACKWARD $8.70//)

OCT GOLD: $1937.90 CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: : $2.00//BACKWARD/

DEC. GOLD $1946.50 CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $6.60/ CONTANGO ($5.40 BELOW NORMAL CONTANGO)

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $26.78…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : ( 3 cent contango//correct contango)

SILVER DECEMBER CLOSE: $27.92 1:30 PM SPREAD SPOT/FUTURE DEC. : 17 CENTS PER OZ ( 5 CENTS ABOVE NORMAL CONTANGO)

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today: enhanced 24/24

issued: jpmorgan 24

EXCHANGE: COMEX

CONTRACT: AUGUST 2020 GOLD (ENHANCED DELIVERY) FUTURES

SETTLEMENT: 1,933.800000000 USD

INTENT DATE: 08/20/2020 DELIVERY DATE: 08/24/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 H MORGAN STANLEY 24

661 C JP MORGAN 24

____________________________________________________________________________________________

TOTAL: 24 24

MONTH TO DATE: 24

and

34/172

issued 89

EXCHANGE: COMEX

CONTRACT: AUGUST 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,933.800000000 USD

INTENT DATE: 08/20/2020 DELIVERY DATE: 08/24/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

135 H RAND 5

657 C MORGAN STANLEY 7 11

661 C JP MORGAN 89 34

690 C ABN AMRO 2 98

737 C ADVANTAGE 66 22

905 C ADM 3 7

____________________________________________________________________________________________

TOTAL: 172 172

MONTH TO DATE: 48,710

total notices: 48,734 or 4873400 oz or 151.579 tonnes

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 196 NOTICE(S) FOR 19600 OZ (0.60966 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 48,710 NOTICES FOR 4,8710,000 OZ (151.579 TONNES)

SILVER

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 1278 for 6.390 MILLION oz

BITCOIN MORNING QUOTE $11,732 DOWN 150

BITCOIN AFTERNOON QUOTE.: $11,695 DOWN 162

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $0.40 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

NO CHANGES IN GOLD INVENTORY AT THE GLD/// //

GLD: 1,252.38 TONNES OF GOLD//

WITH SILVER DOWN $0.26 CENTS TODAY: AND WITH NO SILVER AROUND:

A HUGE CHANGES IN SILVER INVENTORY AT THE SLV//

SURPRISINGLY: A DEPOSIT OF 838,000 OZ INTO THE SLV//

RESTING SLV INVENTORY TONIGHT:

SLV: 573.681 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A SMALL SIZED 915 CONTRACTS FROM 192,857 DOWN TO 191,942, AND FURTHER FROM OUR NEW RECORD OF 244,710, (FEB 25/2020. THE TINY LOSS IN OI OCCURRED DESPITE OUR STRONG 26 CENT LOSS IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE LOSS IN COMEX OI IS PRIMARILY DUE TO TINY BANKER SHORT COVERING (IF ANY) COUPLED AGAINST A STRONG EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, WITH A ZERO DECREASE IN SILVER OZ. STANDING AT THE COMEX FOR AUGUST. WE HAD A STRONG NET GAIN IN OUR TWO EXCHANGES OF 1314 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: SEP 2149 DEC: 100 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 2249 CONTRACTS. WITH THE TRANSFER OF 562 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2249 EFP CONTRACTS TRANSLATES INTO 11.245 MILLION OZ ACCOMPANYING:

1.THE 26 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

86.470 MILLION OZ FINAL STANDING IN JULY.

6.465 MILLION OZ INITIAL STANDING IN AUGUST

THURSDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL 26 CENTS ).. AND, OUR OFFICIAL SECTOR/BANKERS WERE BASICALLY UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS. THEY ENGAGED IN MINOR BANKER SHORT COVERING BUT JUDGING FROM THE HUGE GAIN ON THE TWO EXCHANGES, THEY COULD NOT COVER MUCH… THUS: THE TINY SIZED LOSS AT THE COMEX WAS ACCOMPANIED BY : i) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A ZERO INCREASE IN SILVER OZ STANDING FOR AUGUST, MINOR BANKER SHORT COVERING (IF ANY) AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A STRONG NET GAIN OF 1314 CONTRACTS OR 6.67 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKERS ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER..AND THUS THE REASON FOR OUR MASSIVE RAID THIS MORNING!!

SPREADING OPERATIONS/NOW SWITCHING TO SILVER

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN SILVER AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF AUGUST. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

AUGUST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF AUGUST:

16,434 CONTRACTS (FOR 16 TRADING DAY(S) TOTAL 16,434 CONTRACTS) OR 82.170 MILLION OZ: (AVERAGE PER DAY: 1027 CONTRACTS OR 5.1356 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 82.170 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 11.73% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,352.46 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 133.95 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

AUGUST EXP 82.170 MILLION OZ (EXCHANGE FOR PHYSICALS STARTING TO DECREASE AGAIN)

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 915, DESPITE OUR STRONG 26 CENT LOSS IN SILVER PRICING AT THE COMEX ///THURSDAY AS ONE A NET BASIS, NOT TOO MANY LEFT THE SILVER ARENA..…THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2249 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A STRONG SIZED 1334 OI CONTRACTS ON THE TWO EXCHANGES (DESPITE OUR HUGE 26 CENT FALL IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 2249 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A SMALL SIZED DECREASE OF 915 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 26 CENT FALL IN PRICE OF SILVER/AND A CLOSING PRICE OF $27.05 // THURSDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.9640 BILLION OZ TO BE EXACT or 138% of annual global silver production (ex Russia & ex China).

FOR THE NEW AUGUST DELIVERY MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR nil OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 WAS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 86.470 million oz//AUGUST 6.465 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A TINY SIZED 233 CONTRACTS TO 546,461 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE TINY LOSS IN COMEX OI OCCURRED DESPITE OUR STRONG LOSS IN PRICE OF $23.45 /// COMEX GOLD TRADING// THURSDAY//WE HAD MINIMAL BANKER SHORT COVERING(IF ANY), A STRONG SIZED INCREASE IN GOLD TONNAGE STANDING AT THE COMEX FOR AUGUST, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR STRONG LOSS IN PRICE OF $23.45.

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 158

WE GAINED A GOOD SIZED 1669 CONTRACTS (5.191 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 1748 CONTRACTS:

CONTRACT .; AUG 0 AND OCT: 0 DEC: 1902; JUNE: 0 ALL OTHER MONTHS ZERO//TOTAL: 1748. The NEW COMEX OI for the gold complex rests at 546,461. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1669 CONTRACTS: 233 CONTRACTS DECREASED AT THE COMEX AND 1902 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 1669 CONTRACTS OR 5.191 TONNES. THURSDAY, WE HAD A STRONG LOSS OF $23.45 IN GOLD TRADING..….

AND WITH THAT LOSS IN PRICE, WE HAD A GOOD SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 5.191 TONNES!!!!!! THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT FELL $23.45). WE DID HAVE MINOR BANKER SHORT COVERING (IF ANY) OPERATION BUT JUDGING FROM THE GAIN IN COMEX OI AND THE GAIN IN EXCHANGES FOR PHYSICAL THEY COULD NOT FLEECE ON A NET BASIS ANY OF OUR SPECULATOR LONGS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1902) ACCOMPANYING THE SURPRISINGLY SMALL SIZED LOSS IN COMEX OI (233 OI): TOTAL GAIN IN THE TWO EXCHANGES: 1669 CONTRACTS. WE NO DOUBT HAD 1 )TINY BANKER SHORT COVERING (IF ANY), 2.)A STRONG INCREASE IN GOLD TONNAGE STANDING AT THE GOLD COMEX FOR THE FRONT AUGUST MONTH, 3) ZERO LONG LIQUIDATION; 4) SMALL COMEX OI LOSS AND 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL AND …ALL OF THIS WAS COUPLED WITH OUR HUGE LOSS IN GOLD PRICE TRADING//THURSDAY//$23.45.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

AUGUST

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES: 106.15 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 106.15/3550 x 100% TONNES =2.99% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3,366.32 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 313.09 TONNES ..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

AUGUST TOTAL EFP ISSUANCE; 106.15 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A SMALL SIZED 915 CONTRACTS FROM 192,857 DOWN TO 191,942 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE SMALL SIZED LOSS IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) MINIMAL BANKER SHORT COVERING , 2) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A ZERO DECREASE IN SILVER OZ STANDING AT THE SILVER COMEX FOR AUGUST, AND 4) SOME WEAK LONG LIQUIDATION, BUT ON NET ZERO LONG LIQUIDATION.

EFP ISSUANCE 2249 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT: 2149 AND DEC. 100 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2249 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 915 CONTRACTS TO THE 2249 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 1334 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 6.67 MILLION OZ, OCCURRED WITH OUR 26 CENT LOSS IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 16.78 POINTS OR 0.50% //Hang Sang CLOSED DOWN 322.45 POINTS OR 1.30% /The Nikkei closed UP 39.68 POINTS OR 0.17%//Australia’s all ordinaires CLOSED DOWN .02%

/Chinese yuan (ONSHORE) closed DOWN at 6.92230 /Oil UP TO 42.28 dollars per barrel for WTI and 44.21 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.92230 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9191 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS//PANDEMIC : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

i) Out of Brinks: 151,971.031

ii) Out of jPMorgan: 225,057.000 oz (7000 kilobars)

total withdrawals; 377,510.301 oz

We had 1 kilobar transactions +

ADJUSTMENTS: 0 //

The front month of AUGUST registered a total of 290 CONTRACTS as we GAINED 1 contracts. We had 40 notices served on THURSDAY so we GAINED A STRONG 41 AND 24 ENHANCED contracts or an additional 6500 OZ will stand for delivery on this side of the pond as they refused to morph into London based forwards as well as negating a fiat bonus. The boys are scrambling in search of badly needed physical metal as they start to search for metal on the other side of the pond.

After August we have the non active Sept contract month.. Here we saw another GAIN of 56 contracts to stand at 2452. Oct LOST 551 contracts UP to 71,280

The big December contract LOST 1217 contracts down to 398,578 contracts…(it is here where some of our short side bankers tried to bail and failed)

We had 172 notices filed today for 17200 oz REGULAR INVENTORY

AND 24 NOTICES OR 2400 OZ ENHANCED INVENTORY.

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2020. contract month, we take the total number of notices filed so far for the month (48,734) x 100 oz , to which we add the difference between the open interest for the front month of AUGUST (314 CONTRACTS ) minus the number of notices served upon today (196 x 100 oz per contract) equals 4,885,200 OZ OR 151.950 TONNES) the number of ounces standing in this active month of JUNE

thus the INITIAL standings for gold for the AUGUST/2020 contract month:

No of notices filed so far (48,734, x 100 oz + (314 OI) for the front month minus the number of notices served upon today (196) x 100 oz which equals 4,885,200 oz standing OR 151.950 TONNES in this active delivery month. This is a HUGE amount for gold standing for a AUGUST delivery month (an active delivery month).

We gained 65 contracts or 6500 oz of gold as these guys refused to morph into London based forwards.

THE NAME OF THE GAME TODAY IS BANKER SHORT COVERING AS FINALLY FEAR BECAME THEIR CENTRAL FOCUS. THEY ORCHESTRATED A RAID TODAY SO AS TO CAUSE MANY SPECULATORS TO FLEE THE GOLD ARENA. IT LOOKS LIKE THEY FAILED.

NEW PLEDGED GOLD: BRINKS

144,088.952 oz NOW PLEDGED JAN 21.2020/HSBC 5.4807 TONNES

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

231,924.295 oz (some deleted august 3) JPM 7.2138 TONNES

611,401.341 oz pledged June 12/2020 Brinks/ july 2/july 21 19.017 tonnes

25,078.004 oz Pledged August 21/regular account .7800 tonnes

total pledged gold: 1,055,040.900 oz 32.81 tonnes

total registered, pledged and eligible (customer) gold; 37,003,517.208 oz 1,150.96 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1024.42 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

492,447.430 oz

Brinks

Delaware

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

1,319,570.215 oz

Malca

Scotia

|

| No of oz served today (contracts) |

0

CONTRACT(S)

(nil OZ)

|

| No of oz to be served (notices) |

15 contracts

75,000 oz)

|

| Total monthly oz silver served (contracts) | 1278 contracts

6,390,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 2 deposits into the customer account

i)into JPMorgan: nil oz

ii) Into Malca: 110,732.755 oz

iii) Into Scotia: 1,208,837.460

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 165.53 million oz of total silver inventory or 48.64% of all official comex silver. (165.53 million/340.279 million

total customer deposits today: 2,319,570.215 oz

we had 2 withdrawals:

ii) Out of Brinks: 490,478.930 oz

iii) Out of Delaware: 1968.560 oz

total withdrawals; 492,447.430 oz

We had 0 adjustments

Total dealer(registered) silver: 129.555 million oz

total registered and eligible silver: 340,279 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

the front month of August registered an open interest of 15 contracts and thus we LOST 4 contracts. We had 4 notices filed on THURSDAY so we LOST 0 contracts or an additional NIL oz will stand for delivery as these guys refused to morph into London based forwards as well as negating a fiat bonus for their efforts…. The bankers are now desperate in their search for badly needed silver whether it is on this side of the pond or the European side.

After August we have the big September contract month and here we see a loss 4601 contracts down to 66,517. November saw another gain of 1 contract to stand at 306.

SEPT OI IS VERY HIGH AND WE WILL HAVE A DANDY AMOUNT OF SILVER STANDING AT THE COMEX.

The big December contract month saw its OI rise by good 3653 contracts up to 113,172

The total number of notices filed today for the AUGUST 2020. contract month is represented by 0 contract(s) FOR nil, oz

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 1278 x 5,000 oz = 6,390,000 oz to which we add the difference between the open interest for the front month of AUGUST(15) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the AUGUST/2019 contract month: 1278 (notices served so far) x 5000 oz + OI for front month of AUGUST (15)- number of notices served upon today (0) x 5000 oz of silver standing for the AUGUST contract month.equals 6,465,000 oz. ..VERY STRONG FOR A NON ACTIVE MONTH.

We lost 0 contracts or an additional nil oz will not stand for delivery as they morphed into London based forwards..

TODAY’S ESTIMATED SILVER VOLUME : 190,591 CONTRACTS // volume huge++++++++++++++++++++++++++++++++++++++/

FOR YESTERDAY: 181,832. ,CONFIRMED VOLUME//volume huge.++++++++++++++++++++++++++++++++++++++++++++++++++++

YESTERDAY’S CONFIRMED VOLUME OF 181,832 CONTRACTS EQUATES to 0.909 billion OZ 129% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 4.13% ((AUGUST 21/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.59% to NAV: (AUGUST 21/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/4.13%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 20.38 TRADING 19.79///NEGATIVE 2.88

END

And now the Gold inventory at the GLD/

AUGUST 21//WITH GOLD DOWN $.40 TODAY: WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1252.38 TONNES

AUGUST 20/WITH GOLD DOWN $23.45 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD: .//INVENTORY REST AT 1252.38 TONNES

AUGUST 19//WITH GOLD DOWN $39.65 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1252.38 TONNES

AUGUST 18/WITH GOLD UP $14.60 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 4.09 TONNES//GLD INVENTORY RESTS TONIGHT AT 1252.38 TONNES

AUGUST 17/WITH GOLD UP $46.30 TODAY: SURPRISINGLY WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 3.8 TONNES//INVENTORY RESTS AT 1248.29 TONNES

AUGUST 14/ WITH GOLD DOWN $19.45 TODAY: SURPRISINGLY, WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.46 TONNES/INVENTORY RESTS AT 1252.63 TONNES.

AUGUST 13/WITH GOLD UP $23.15 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY: SURPRISINGLY A PAPER WITHDRAWAL OF 7.30 TONNES/INVENTORY RESTS AT 1250.63 TONNES

AUGUST 12/ WITH GOLD UP $1.00 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 4.19 TONNES//INVENTORY RESTS AT 1257.93 TONNES

AUGUST 11//WITH GOLD DOWN $92.40 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1262.12 TONNES.

AUGUST 10/WITH GOLD UP $11.35 TODAY, WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.84 TONNES//INVENTORY RESTS AT 1262.12 TONNES

AUGUST 7/WITH GOLD DOWN $38.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1267.96 TONNES

AUGUST 6/WITH GOLD UP $20.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER DEPOSIT OF 10.23 TONNES INTO THE GLD/INVENTORY RESTS AT 1267.96 TONNES//

AUGUST 5/WITH GOLD UP $ 33.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 9.35 TONNES INTO THE GLD//INVENTORY RESTS AT 1257.73 TONNES

AUGUST 4//WITH GOLD UP $31.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 6.48 TONNES/GLD INVENTORY RESTS AT 1248.38 TONNES

AUGUST 3/WITH GOLD UP $2.20 TODAY, WE HAVE NO CHANGES IN THE GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241,96 TONNES

JULY 31/WITH GOLD UP $17.90 TODAY/WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241.96 TONNES.

JULY 30/WITH GOLD DOWN $10.00 TODAY, WE HAVE ANOTHER SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES//INVENTORY RESTS AT 1241.96 TONNES.

JULY 29//WITH GOLD UP $12.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 8.47 TONNES/INVENTORY RESTS AT 1243.12 TONNES

JULY 28///WITH GOLD UP $13.25 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 5.84 TONNES/INVENTORY RESTS AT 1234.65

JULY 27//WITH GOLD UP $35.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF XXX TONNES/INVENTORY RESTS AT 1228.81 TONNES

JULY 24/WITH GOLD UP $8.80 TODAY: WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.80 TONNES//INVENTORY RESTS AT 1228.81 TONNES

JULY 23/WITH GOLD UP $24.90 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 7.26 TONNES/INVENTORY RESTS AT 1225.01 TONNES

JULY 22/WITH GOLD UP $22.00 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 7.89 TONNES/INVENTORY RESTS AT 1219.75 TONNES

JULY 21//WITH GOLD UP $26.00 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.97 TONNES INTO THE GLD// INVENTORY RESTS AT 1211.86 TONNES

JULY 20/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1206.89 TONNES

JULY 17/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1206.89 TONNES

JULY 16/WITH GOLD DOWN $9.80 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: INVENTORY RESTS AT 1206.89 TONNES

JULY 15//WITH GOLD UP $1.55 TODAY/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 2.96 TONNES INTO THE GLD///INVENTORY RESTS AT 1206.89 TONNES

JULY 14//WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 3.51 TONNES/INVENTORY RESTS AT 1203.97 TONNES

JULY 13//WITH GOLD UP $12.50 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1200.46 TONNES

JULY 10/WITH GOLD DOWN $.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD//A STRANGE WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1200.82 TONNES

JULY 9//WITH GOLD DOWN $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OX 3.21 TONNES INTO THE GLD//INVENTORY RESTS AT 1202.57 TONNES

JULY 8/WITH GOLD UP $13.75 TODAY; A BIG CHANGE IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 7.89 TONNES INTO THE GLD//INVENTORY RESTS AT 1199.36 TONNES

JULY 7/WITH GOLD UP $12.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1191.47 TONNES

JULY 6/WITH GOLD UP $6.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1191.47 TONNES

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

AUGUST 21/ GLD INVENTORY 1252.38 tonnes*

LAST; 886 TRADING DAYS: +312.88 NET TONNES HAVE BEEN ADDED THE GLD

LAST 786 TRADING DAYS://+491,41 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

AUGUST 21//WITH SILVER DOWN 30 CENTS TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.838 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 573.843 MILLION OZ..

AUGUST 20/WITH SILVER DOWN $.26 TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 3.724 MILLION OZ FROM THE SLV..//INVENTORY REST AT 572.843 MILLION OZ

AUGUST 18/WITH SILVER UP $.44 TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.514 MILLION OZ//THE SLV INVENTORY RESTS TONIGHT AT 576.567 MILLION OZ//

AUGUST 17/WITH SILVER UP $1.27 TODAY: WE HAD NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 14/WITH SILVER DOWN $1.31 TODAY, WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.984 MILLION OZ// //INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 13//WITH SILVER UP $1.76 TODAY: WE HAVE TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A PAPER DEPOSIT OF 2.421 MILLION OZ INTO THE SLV AT 2 PM AND ANOTHER DEPOSIT OF 6.984 MILLION OZ AT 5 20 PM/INVENTORY RESTS AT 581.037 MILLION OZ//

AUGUST 12/WITH SILVER DOWN 40 CENTS TODAY: WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF XX MILLION OZ//INVENTORY RESTS AT XX MILLION OZ/

AUGUST 11/WITH SILVER DOWN $3.25 CENTS, WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.41 MILLION OZ//INVENTORY RESTS AT 571.632 MILLION OZ//

AUGUST 10/WITH SILVER UP 1.89 TODAY, WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 3.538 MILLION OZ/INVENTORY RESTS AT 569.491 MILLION OZ//

AUGUST 7/WITH SILVER DOWN 69 CENTS TODAY: WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY: A DEPOSIT OF 0.465 MILLION OZ/INVENTORY RESTS AT 573.029 MILLION OZ.

AUGUST 6/WITH SILVER UP $1.52 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 572.564 MILLION OZ///

AUGUST 5/WITH SILVER UP $1.03 TODAY, WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A MONSTROUS DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 572.564 MILLION OZ//

AUGUST 4/WITH SILVER UP $1.45 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 367.161 MILLION OZ//

AUGUST 3/WITH SILVER UP 23 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//SURPRISINGLY ANOTHER WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 367.161 MILLION OZ//

JULY 31/WITH SILVER UP 82 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: SURPRISINGLY A HUGE WITHDRAWAL OF 3.26 MILLION OZ//INVENTORY RESTS AT 368.092 MILLION OZ//

JULY 30//WITH SILVER DOWN 97 CENTS TODAY: WE HAVE A SMALL CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 571.352 MILLION OZ//

JULY 29/WITH SILVER UP 7 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY//A DEPOSIT OF 5.984 MILLION OZ//INVENTORY RESTS AT 572.283 MILLION OZ//

JULY 28 WITH SILVER DOWN 14 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 7.52 MILLION OZ//INVENTORY RESTS AT 566.299 MILLION OZ//

JULY 27/WITH SILVER UP $2.67 TODAY, WE HAD NO CHANGES IN SILVER INVENTORY: A DEPOSIT OF XX MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ//

JULY 24/WITH SILVER DOWN $0.12 TODAY: NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 558.779 MILLION OZ/

JULY 23/WITH SILVER UP $.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A HUMONGOUS PAPER DEPOSIT OF 9.594 MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ///

JULY 22/WITH SILVER UP $1.54 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A HUMONGOUS PAPER DEPOSIT OF 7.218 MILLION OZ//INVENTORY RESTS AT 549.185 MILLION OZ/

JULY 21/WITH SILVER UP $1.38 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUMONGOUS PAPER DEPOSIT OF 15.368 MILLION OZ////INVENTORY RESTS AT 541.967 MILLION OZ//

JULY 20/WITH SILVER UP 40 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 3.819 MILLION OZ ‘ENTERED” THE SLV..INVENTORY RESTS AT 526.599 MILLION OZ/

JULY 17/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 1.583 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 522.780 MILLION OZ//

JULY 16//WITH SILVER DOWN 14 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ//INVENTORY RESTS AT 521.197 MILLION OZ..

JULY 15.WITH SILVER UP 21 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.956 MILLION OZ//INVENTORY RESTS AT 516.074 MILLION OZ//

JULY 14/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 514.118 MILLION OZ//

JULY 13//WITH SILVER UP 67 CENTS TODAY: A HUGE CHANGE IN SILVER: A WITHDRAWAL OF 1.677 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 514.118 MILLION OZ//

JULY 10/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 4.844 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.795 MILLION OZ

WHAT A FRAUD!!

JULY 9/WITH SILVER DOWN 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 8.198 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 510.951 MILLION OZ/

JULY 8/WITH SILVER UP 37 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.118 MILLION OZ FROM THE SLV//VERY SURPRISING.//INVENTORY RESTS AT 502.753 MILLION OZ//

JULY 7/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/INVENTORY RESTS AT 503.871 MILLION OZ///

JULY 6//WITH SILVER UP 24 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.863 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 503.871 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

AUGUST 21.2020:

SLV INVENTORY RESTS TONIGHT AT

573.681 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

Central banks scale back their dollar lending as demand for dollars continue to wane

(London’s Financial Times/GATA)

Central banks scale back dollar lending operation as demand drops

Submitted by cpowell on Thu, 2020-08-20 14:36. Section: Daily Dispatches

By Martin Arnold and Eva Szalay

Financial Times, London

Thursday, August 20, 2020

Four leading central banks have further scaled back the U.S. dollar liquidity they offer via emergency swap lines with the Federal Reserve, in the latest illustration of the global financial system’s recovery from the market panic caused by coronavirus earlier this year.

The European Central Bank, the Bank of England, the Bank of Japan, and the Swiss National Bank said Thursday that they would offer short-term dollar funding via the Fed’s swap lines only once a week, instead of three times, because of “continuing improvements in U.S. dollar funding conditions and the low demand” at recent auctions.

This is the second time central banks have scaled back their efforts to channel dollars cheaply into their domestic economies. In June they cut back the auctions from every day to three times a week. …

… For the remainder of the report:

https://www.ft.com/content/210ef737-2628-4431-bd6b-456aa65b2024

* * *

END

A must ..

Chris Powell being interviewed by Claudio Grass. Chris talks about recent changes in the gold market and what is in store for us\(Chris Powell/Claudio Grass

(zerohedge)

GATA secretary reviews prospects for monetary metals in interview with Claudio Grass

Submitted by cpowell on Thu, 2020-08-20 15:13. Section: Daily Dispatches

11:12a ET Thursday, August 20, 2020

Dear Friend of GATA and Gold:

Major recent changes in the gold market and what they may foretell are discussed in an interview with your secretary/treasurer conducted by market analyst and financial adviser Claudio Grass.

There are many positive signs for monetary metals prices, your secretary/treasurer says, but the rise in assets claimed by gold and silver exchange-traded funds is probably not one of them.

The interview is headlined “Central Banks, Not Elected Governments, Run the World” and it’s posted at ProAurum.com here:

https://proaurum.ch/aktuellwichtig/interview-with-chris-powell-central-b…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

For your interest..

Two giant gold nuggets worth US$250,000 found in Australia

Submitted by cpowell on Thu, 2020-08-20 15:42. Section: Daily Dispatches

By Jack Guy

Cable News Network, Atlanta

Thursday, August 20, 2020

Gold diggers in southern Australia have found two huge nuggets worth A$350,000 (US$250,000) in historic goldfields.

The pair of nuggets weigh in at a combined 3.5 kilograms (7.7 pounds) and were found on the same day near Tarnagulla in Victoria state, as shown on today’s episode of “Aussie Gold Hunters: on the Discovery Channel.

…

..Prospectors Brent Shannon and his brother-in-law Ethan West found the nuggets in a matter of hours with the help of West’s father, Paul West, according to a Discovery Channel press release. …

… For the remainder of the report and some spectacular photos:

https://www.cnn.com/2020/08/20/asia/australia-gold-nuggets-scli-intl/ind…

end

iii) Other physical stories:

https://www.jsmineset.com/2020/08/21/fedbugs-vs-goldbugs/

FedBugs Vs. GoldBugs

Posted August 21st, 2020 at 9:02 AM (CST) by J. Johnson & filed under General Editorial.

Great and Wonderful Friday Morning Folks,

20 minutes before I started writing, Gold began the London Dip to $1,932.70 with the trade now at $1,934.60, down $12 with the high to beat at $1,963.10. Silver is doing the London thing as well with its trade at $27.035, down 26.6 cents after hitting the nearby low at $27.01 with the high to beat at $27.75. The US Dollar, is still getting support with its value pegged at 93.17 up 39.2 points, recovering from yesterday’s 10.2-point drop, and after hitting the London high of 93.24 with the low we expect to eventually be blown out at 92.565. Of course, all this happened before 5 am pst, the Comex open, the London close, and after the Chicago Mayor Lightfoot, tells protestors they are welcome to peacefully burn, loot, and riot, in the city, where taxes are made and drawn, by businesses that are supposed to be protected by the defunded police, that are paid with tax dollars, but not allowed to riot, burn, or loot, on her own homes block. Oh Yeah! and its Trumps fault.

Venezuela’s price for Gold now sits at 19,321.82 Bolivar, down 91.88 since yesterday with Silver price at 270.012 losing 2.197 Bolivars. Gold in Argentina is now valued at 142,143.31 Peso’s dropping 561.21 A-Peso’s with Silver price getting another 14.35 A-Peso shave with the trade at 1,986.55. Turkey’s Lira now has Gold’s value pegged at 13,958.50 showing another 322.54 T-Lira reduction with Silver’s price at 195.103 T-Lira, pulling back another 5.165.

August Silver’s Delivery Demands now sit at 15 contracts and with a Volume of 22 already up on the board (Mr. Resolute, is that you?) and there’s a trading range to boot! Between $27.475 and $27.055 with the last swap at $27.125, up 3/10th’s of a penny so far while the London paper swing – does its thing. Yesterday’s Comex deliveries had zero trades but did have 4 contracts finally getting their receipts, reducing the count from 19. Silver’s Overall Open Interest continues to shave the shorts as another 916 pieces of paper exited the scene leaving 192,422 in Open Interest to go against the physicals.

August Gold’s Delivery Demands now show 290 fully paid for contracts waiting for receipts and with a Volume of 25 up on the board with a trading range between $1,945 and $1,940, until the last London swap “hit the tape” at $1,908.90, now down $24.90, so far today. London’s pull has to be noted here! Just before these 2 sell trades hit the tape, the last Delivered Gold price was at $1,943.40. A positive price proving a gain of $9.40 before the 2 lot sell order hit and after the 23 contracts traded in the positive. The game London plays is taking away their marbles and in time, they will have no choice but to allow the markets to trade freely, in order to find the physicals. Gold’s shorts are continuing to drop out as well as another 892 pieces of paper left the playground leaving a total of 547,112 Overnighters still in play to go against the physicals.

Our Federal Reserve has now decided to go on the attack during the 2020 presidential campaign, many months after Trump nominated Judy Sheldon to chair one of the open spots on the “reserve”. Of note; whenever our beloved former Congressman Ron Paul brought up a US Silver and Gold backed currency (like we had before the Federal Reserve was created, 12/23/1913) during the many many televised hearings over the decades he was on the committee, we would see our socialist media services go to commercial, or pop in with a “just in news story” about a cow that crossed the road in an Amish village. We have witnessed the Fed game for too long to believe anything they say because they cannot compete against anyone who understands what came out of that middle of the night illegal act by Congress. IMO, now it appears the Federal Reserve “specialists” are fighting for their jobs (control), by any means possible, as we see the Sheldon nomination aiming to remove the Reserve and place the responsibilities back into the hands of the US Treasury, where it belongs!

The present story is no different than Andrew Jackson’s, when he too was running for his second term when London’s own Nicholas Biddle, head of the Second Bank of the United States, did anything and everything possible to get Jackson out of office, including threatening to destroy the economy. G. Edward Griffin, who authored the book, The Creature From Jekyll Island, and was interviewed here on JSMineSet, last October, after the September Bond Event, helps clarify what happened back then and it is ironically the same now. After her nomination, Judy Sheldon was called a GoldBug. All she did was laugh hard after being labeled that, and said those that support the Federal Reserve are FedBugs. So now we have a great labeled clarification; FedBugs Vs. GoldBugs, and once again we’re in the fight for control of our countries money that has been taken away from the US Treasury.

History proves; Paper loses to Rock, Always! So, get as many precious metals rocks in hand and hold them close. We haven’t seen volatility like those in the emerging markets yet, but we will, and when that happens, you will be thankful to be well rocked. So have a great weekend, have a smile on your face and a prayer for all, and as always …

Stay Strong!

Jeremiah Johnson

More J.Johnson content is available with purchase of a JSMineset subscription.

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Futures Tumble, Dollar Soars After European PMIs Slump, Putting Recovery In Doubt

US stock index futures dropped, tracking European markets a day after the tech-heavy Nasdaq closed at a record high, as optimism in a virus-vaccine breakthrough and faith in the record tech rally was challenged by concerns over an unexpected frop in Eurozone PMIs which put the biggest recovery narrative in recent months in doubt.

Among US stocks, Deere & Co rose 4.5% premarket after it revised up its full-year earnings forecast and reported a smaller-than-expected decline in quarterly profit. Pfizer rose 1.5% after reporting positive additional data from an early-stage study of its experimental coronavirus vaccine being developed in collaboration with German biotech firm BioNTech. U.S.-listed shares of BioNTech jumped 8.1%. Tesla gained another 1.8% after surging past the $2,000 mark on Thursday for the first time and extending its rally ahead of an upcoming share split.

US stocks finished higher on Thursday as investors continued to bet on tech heavyweights including Apple and Amazon.com to ride out the pandemic as U.S. data painted a picture of a wobbly economic recovery. However the market’s bad breadth is getting extremely narrow: yesterday stocks closed green even though 70% of all companies closed in the red.

U.S. tech darlings “continue to mask the broader concerns spearheading an end-of-week rally,” said Nema Ramkhelawan-Bhana, head of research at Johannesburg-based Rand Merchant Bank. “Wider credit spreads and bond bidding suggest an air of nervousness is starting to creep in.”

Joe Biden accepted his party’s nomination Thursday to challenge President Donald Trump in a speech that cast November’s election as not merely the choice of a president but a fundamental referendum on the nation’s character.

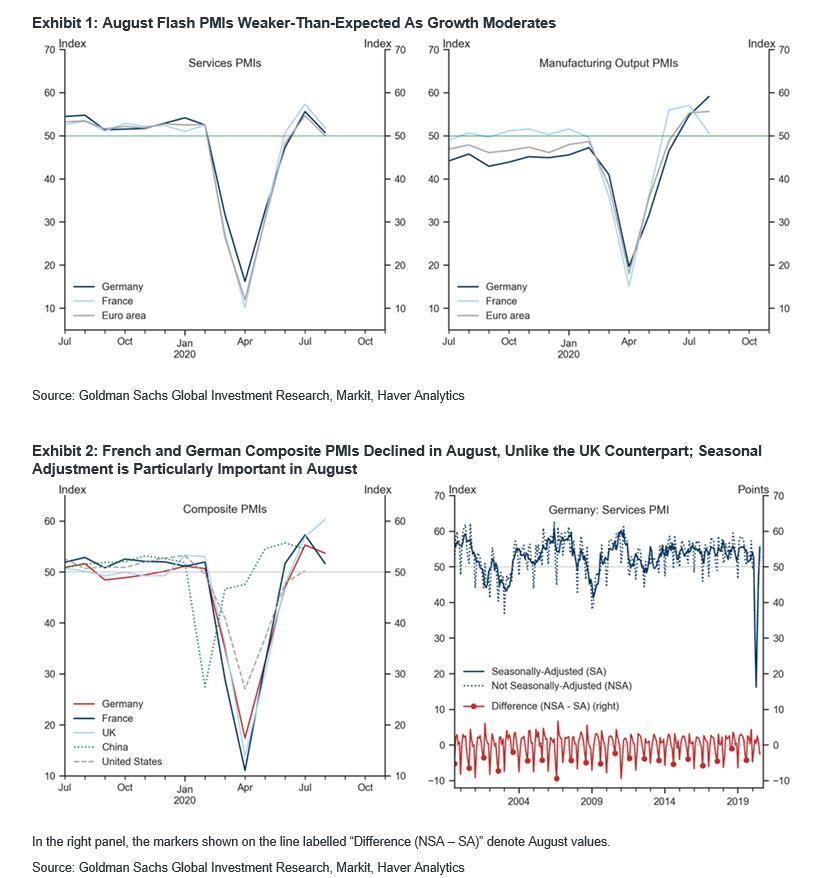

European stocks and the euro slumped after European PMI composite readings unexpectedly declined in August from July, missing expectations even as U.K. data was materially stronger (UK flash composite PMI 60.3 vs 57; est. 56.9). Job losses were a notable feature of the surveys.

As Goldman writes, after a record, better-than-expected cumulative improvement of 41.2pt over May-July, the Euro area composite PMI declined by 3.3pt to 51.6 in August, notably below expectations. The overall decline was heavily skewed towards the service sector, with the manufacturing PMI little changed from July. Across countries, the German and French composite PMIs were also weaker than expected, with the sequential weakening in France broad-based across sectors but solely concentrated in services in Germany. The implicit decline in the composite PMI outside of France and Germany was only marginally smaller than the decline in the Franco-German composite PMI. The weakening in the PMIs suggests that the pace of sequential growth has moderated as the gap in the level of activity relative to pre-Covid narrows (consistent with high-frequency activity indicators):

- Euro Area Composite PMI (August, Flash): 51.6, consensus 55.0, last 54.9.

- Euro Area Manufacturing PMI (August, Flash): 51.7, consensus 52.7, last 51.8.

- Euro Area Services PMI (August, Flash): 50.1, consensus 54.5, last 54.7.

- Germany Composite PMI (August, Flash): 53.7, consensus 55.0, last 55.3.

- France Composite PMI (August, Flash): 51.7, consensus 57.0, last 57.3.

The broader miss was led by France whose manufacturing PMI unexpectedly dropped in August after a two-month rebound. The sharp fall put in doubt the country’s recovery and led to a decline in the euro. Meanwhile Germany’s recovery also lost momentum, with mixed PMI figures. PMI for services declined while manufacturing continued to improve

Earlier in the session, Asian stocks gained, led by communications and IT, after falling in the last session. Most markets in the region were up, with Taiwan’s Taiex Index gaining 2% and South Korea’s Kospi Index rising 1.3%, while Australia’s S&P/ASX 200 dropped 0.1%. The Topix gained 0.3%, with Fujikyu and TSUNAGU GROUP HOLDINGS I rising the most. The Shanghai Composite Index rose 0.5%, with Whirlpool China and Ningbo Jifeng Auto Parts posting the biggest advances.

Earlier this week, the S&P 500 clinched a record high, recouping the last of its losses caused by the coronavirus-driven slump and joining the Nasdaq in notching new highs even as investors remained on edge over a stalemate in talks between House Democrats and the White House over the next coronavirus aid bill as about 28 million Americans continued to collect unemployment checks. There was some hope that a deal would be reached tomorrow when a $25BN post office spending proposal is considered.

In FX, the dollar gained against a basket of its peers largely thanks to a sharp drop in the Euro which reversed an early gain that came at the back of hopes over a coronavirus vaccine after the latest PMI data challenged the narrative that euro area growth will outperform the US; the EURUSD slumped after data showed French manufacturing unexpectedly contracted in August after a two- month rebound; German and euro area data also missed expectations. The common currency retreated as much as 0.6% to 1.1780.

The euro poised for first weekly drop in nine; interbank desks fade the dip given Thursday’s rebound after 21-DMA support held, yet short-term traders look for a move toward 1.1750, three traders in Europe said.

The offshore yuan rose to its strongest level in seven months against the dollar, as China’s economic and market rebound from the pandemic has proved one of the world’s fastest.

Elsewhere, Turkey’s lira gained amid speculation President Recep Tayyip Erdogan will announce a major Turkish energy discovery in the Black Sea later Friday.

In rates, Treasuries advanced while European bond yields were flat to 1bp lower across the curves; the 10Y Treasury yield dropped -3bp to 0.6282%, flattening the 2s-10s curve. German 2-yr, 10-yr yields 1bp lower.

In commodities, Brent ($44.72) and WTI ($42.57) traded lower but were on track for a third weekly gain in New York trading. Gold slumped to $1920 as the dollar surged.

Looking ahead, expected data include PMIs and existing home sales. Deere is reporting earnings

Market Snapshot

- S&P 500 futures little changed at 3,380.00

- MXAP up 0.8% to 170.76

- MXAPJ up 0.9% to 562.42

- Nikkei up 0.2% to 22,920.30

- Topix up 0.3% to 1,604.06

- Hang Seng Index up 1.3% to 25,113.84

- Shanghai Composite up 0.5% to 3,380.68

- Sensex up 0.8% to 38,515.19

- Australia S&P/ASX 200 down 0.1% to 6,111.18

- Kospi up 1.3% to 2,304.59

- STOXX Europe 600 up 0.3% to 366.72

- German 10Y yield fell 1.1 bps to -0.507%

- Euro down 0.4% to $1.1813

- Italian 10Y yield unchanged at 0.789%

- Spanish 10Y yield fell 0.2 bps to 0.289%

- Brent futures down 0.7% to $44.59/bbl

- Gold spot down 0.8% to $1,932.61

- U.S. Dollar Index up 0.2% to 92.98

Top US News from Bloomberg

- France’s manufacturing PMI unexpectedly dropped in August after a two-month rebound. The sharp fall put in doubt the country’s recovery and led to a decline in the euro. Meanwhile Germany’s recovery lost momentum, with mixed PMI figures. PMI for services declined while manufacturing continued to improve

- Composite PMI fell below estimates in the euro-area.

- The U.K. economy rebounded to a seven-year high, with composite PMI performing better than expected, while retail sales for July beat estimates, pushing the pound upwards momentarily

Global market snapshot courtesy of NewsSquawk:

Asian equity markets traded mostly positive as the region benefitted from the tech-led gains on Wall St where Apple prodded above the USD 2tln market cap status and as firm gains in Tesla, Microsoft, Intel and Facebook also fuelled the big tech resurgence resulting to outperformance in the Nasdaq, although upside was capped in the broader market amid mixed data releases including higher than expected Initial Jobless Claims. ASX 200 (-0.1%) and Nikkei 225 (+0.2%) both initially took impetus from the constructive handover from US peers but with upside in Australia later retraced following soft PMI data and with weakness seen in defensives as well as the top-weighted financials sector, while the Japanese benchmark contended with the effects of a mixed currency and resistance at the 23,000 level. Hang Seng (+1.3%) and Shanghai Comp. (+0.5%) were underpinned amid the continued PBoC liquidity efforts in which it injected CNY 150bln through 7-day reverse repos and CNY 50bln in 14-day reverse repos. This was the first occasion the central bank utilized the latter instrument in around 2 months, and there was also recent confirmation from China’s MOFCOM that the US and China will be conducting the delayed trade discussions in the approaching days. Finally, 10yr JGBs were flat and continue to eye the 152.00 level to the upside despite the gains in Japanese stocks, with mild support provided by the BoJ’s presence in the market for JPY 870bln of JGBs and the central bank also offered to purchase JPY 200bln in corporate bonds from 25th August with a remaining 3-5yrs to maturity.

Top Asian News

- Pressure Grows on Hong Kong to Re-Open Economy as Cases Drop

- Hong Kong to Start Virus Testing Blitz of Whole City on Sept. 1

- India Slaps New Curbs on Visas, Schools to Stem China Influence

- Millions Escaped Caste Discrimination. Covid-19 Brought It Back

European equities (Eurostoxx 50 +0.3%) have held onto opening gains despite a brief dip lower in the wake of French PMI metrics. However, the pessimism surrounding the August outturn for France was short-lived for broader European assets with equities paring declines ahead of the German release. The German release painted a slightly less downbeat picture with a firmer manufacturing outturn alongside a softer than expected services, with the eventual EZ-wide release posting a miss on expectations for both sectors but ultimately remaining in expansionary territory. IHS Markit noted “the eurozone stands at a crossroads, with growth either set to pick back up in coming months or continue to falter following the initial post-lockdown rebound”. Nonetheless, sentiment for European equities remains afloat in what has been a relatively choppy week in terms of price action for the region. Sectoral performance in Europe is broadly firmer with the exception of energy names which are tracking crude prices lower. Travel & Leisure names are faring the best thus far with some reprieve been granted to the likes of Ryanair (+1.6%) and easyJet (+1.4%), however, with the UK continuing to add more countries to its quarantine list (albeit, has removed Portugal), it’s difficult to see how much conviction will be placed upon a recovery in the sector. Elsewhere, individual movers include Kingspan (+7.4%) post-earnings, Wirecard (+5.4%) amid reports that it has found a suitor for its UK assets, whilst Accor (+2.6%) shares continue to remain supported alongside talk of a potential bid for InterContinental Hotels. To the downside, laggards are relatively sparse with Maersk (-2.8%) and Saipem (-2%) lower on the day following downgrades at JP Morgan Chase and Bernstein respectively.

Top European News

- Europe’s Economic Recovery Stumbles After Initial Bounceback

- U.K. Economy Rebounds With Activity Rising to Seven-Year High

- Pessimism Returns to Brexit Talks as Hopes for Deal Slip Away

- Advent Said to Mull Over $1.2 Billion Sale of Health Firm Mediq

In FX, sub-par French Flash PMIs triggered the losses in the Single Currency, with the French manufacturing metric surprisingly falling back into contraction, whilst Germany and EZ held their heads above the 50 threshold, but largely missed forecasts. EUR/USD has receded from its 1.1882 high and took out an interim support area around 1.1840-45 to test 1.1800 to the downside. Participants will now be eyeing any updates on the Belarus front in regard to sanctions, with little on the docket in terms of scheduled events. Conversely, UK Retail Sales and PMIs topped forecasts across the board but gains Sterling were short-lived as the currency succumbs to the Buck, whilst Brexit talks remain in limbo as officials suggest no progress has been made on outstanding points in the latest round of negotiations. Cable has given up its 1.3200 status (vs. high 1.3255) and continues declining in light of pessimistic comments from both the EU and UK Chief Brexit negotiators, with the former nothing that at this stage, a deal seems unlikely and both sides highlight the little progress mate. EUR/GBP has recovered off lows amid the latest Brexit headlines, with the cross initially dipping below the Aug 13th low ~0.8948 before rebounding to session high at 0.8980.

- DXY – Propped up by the post-PMI Euro – the index is back around 93.000 from an overnight base of 92.570 , with the highs from Wednesday (93.059) and Monday (93.124) the next points of resistance ahead of yesterday’s peak at 93.248. Looking ahead to today, the calendar remains light with US Markit PMIs and Existing Home Sales the only scheduled events.

- JPY – USD/JPY had been ebbing overnight in light of the weaker Dollar during APAC hours, but the JPY holds onto gains in early EU hours despite the Dollar rebound as PMI-related haven flows keeps the Japanese currency buoyed. USD/JPY dipped below 105.50 from 105.80 at best ahead of the weekly base at 105.104. Note: USD/JPY sees around USD 550mln in options rolling off at 105.00 at the NY cut.

- AUD, CAD, NZD – All narrowly softer in what is a Dollar story. AUD/USD as dipped back below 0.7200 (vs. high 0.7215), whilst Westpac raised its year-end forecast to 0.7500 from 0.7200 as their case of a momentum stall is still not convincing. NZD/USD remains contained within a tight current range of 0.6525-0.6550, with overnight comments from the RBNZ Chief economy noting that the Central Bank has scope to act aggressively if needed. Similarly, the revival of the Dollar and declines in the crude complex sees the Loonie yield, with USD/CAD testing resistance at 1.3200 (vs. low 1.3159) ahead of Canadian Retail Sales, with today’s option expiries seeing USD 505mln at 1.3225 alongside a sizeable USD 1.7bln between 1.3250-60.

- EM – Mixed trade across EMs but the Lira stands out as the outperformer after the CBRT lifted the TRY interest rate on swap transactions from 8.25% to 9.75% yesterday to match the lending rate. Furthermore, the Turkish President is expected to announce “good news” today in regard to an energy discover in the black sea, most likely natural gas. USD/TRY has trades sub-7.2500 from a high of 7.3380.

In commodities, WTI and Brent October futures have waned off overnight highs, albeit with the magnitude of price action relatively small thus far. Crude-specific news flow has remained light, but the contracts saw a sentiment-driven leg lower amid the overall down-beat flash PMIs from the EU. Both contracts trade lower by some USD 0.20/bbl apiece, with WTI testing USD 42.50/bbl to the downside (vs. high 42.96./bbl) whilst its Brent counterpart dipped below USD 44.75/bbl from around USD 45/bbl at best, with only the weekly Baker Hughes rig count slated on the calendar. Elsewhere, spot gold and spot silver yield to the post-PMI Dollar strength, with the former losing further ground below USD 1950/oz (vs. high 1956/oz) whilst latter briefly dipped below USD 27.00 from 27.54 at best. In terms of base metals, copper continued to grind lower with the Shanghai inventories again posting another rise in stocks. Dalian iron ore prices fell overnight as the steel-demand-driven rally somewhat fizzled whilst China’s iron ore portside stockpile rose to four-month highs.

US Event Calendar

- 9:45am: Markit US Manufacturing PMI, est. 52, prior 50.9

- 9:45am: Markit US Services PMI, est. 51, prior 50

- 9:45am: Markit US Composite PMI, prior 50.3

- 10am: Existing Home Sales, est. 5.41m, prior 4.72m; MoM, est. 14.62%, prior 20.7%

DB’s Jim Reid concludes the overnight wrap