GOLD:$1944.90 UP $26.70 The quote is London spot price

Silver:$27.28 UP $1.04 London spot price ( cash market)

Today marks the 9TH day out of the last 12 days that a raid has been orchestrated by the bankers.. However this time, major players were waiting in the weeds ready for their huge short

paper offering which was all gobbled up. The noose is around bankers’ necks. The bankers will regroup and we await Friday:

Friday is options expiry OTC /London LBMA 10 am.. not Monday, as the 31st is a UK banking holiday. First day notice is still the 31st of August.

DONATE

Closing access prices: London spot

i)Gold : $1954.50 LONDON SPOT 4:30 pm

ii)SILVER: $27.46//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUGUST GOLD: $1912.00 CLOSE 1::30 PM SPREAD SPOT/FUTURE AUG (BACKWARD $18.80//) SCARCITY//ERROR?

OCT GOLD: $1943.50 CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: : $1.40//BACKWARD/SCARCITY

DEC. GOLD $1952.60 CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $7.70/ CONTANGO ($4.30 BELOW NORMAL CONTANGO)

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $27.35…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : ( 11 cent contango//8 CENTS ABOVE NORMAL contango)

SILVER DECEMBER CLOSE: $27.77 1:30 PM SPREAD SPOT/FUTURE DEC. : 29 CENTS PER OZ ( 17 CENTS ABOVE NORMAL CONTANGO)

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today: 1/66

issued 0

EXCHANGE: COMEX

CONTRACT: AUGUST 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,911.800000000 USD

INTENT DATE: 08/25/2020 DELIVERY DATE: 08/27/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 15 52

657 H MORGAN STANLEY 49

661 C JP MORGAN 1

685 C RJ OBRIEN 1

686 C INTL FCSTONE 5

690 C ABN AMRO 4

905 C ADM 2 3

____________________________________________________________________________________________

TOTAL: 66 66

MONTH TO DATE: 48,851

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT:66 NOTICE(S) FOR 6600 OZ (0.2052 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 48,861 NOTICES FOR 4,886100 OZ + 2400 oz enhanced standing = 48875 notices or 4887500 oz (152.021 tonnes

SILVER

3 NOTICE(S) FILED TODAY FOR 15,000 OZ/

total number of notices filed so far this month: 1282 for 6.410 MILLION oz

BITCOIN MORNING QUOTE $11,388 UP 67

BITCOIN AFTERNOON QUOTE.: $11,463 UP 144

GLD AND SLV INVENTORIES:

WITH GOLD UP $26.70 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/// // A WITHDRAWAL OF 3.53 TONNES FROM THE GLD

GLD: 1,248.85 TONNES OF GOLD//

WITH SILVER UP $1.04 CENTS TODAY: AND WITH NO SILVER AROUND:

A HUGE CHANGES IN INVENTORY AT THE SLV/// A WITHDRAWAL OF 3.53 MILLION OZ FROM THE SLV

RESTING SLV INVENTORY TONIGHT:

SLV: 566.419 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A CONSIDERABLE SIZED 1090 CONTRACTS FROM 188,721 DOWN TO 187,631, AND FURTHER FROM OUR NEW RECORD OF 244,710, (FEB 25/2020. THE TINY LOSS IN OI OCCURRED DESPITE OUR STRONG 21 CENT FALL IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE LOSS IN COMEX OI IS PRIMARILY DUE TO A SMALLER SILVER SPREADER LIQUIDATION THAN YESTERDAY, TINY BANKER SHORT COVERING (IF ANY) COUPLED AGAINST A GOOD EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, WITH A GOOD INCREASE IN SILVER OZ. STANDING AT THE COMEX FOR AUGUST. WE HAD A CONSIDERABLE NET GAIN IN OUR TWO EXCHANGES OF 2 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: SEP 1082 DEC: 0 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1082 CONTRACTS. WITH THE TRANSFER OF 1082 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1082 EFP CONTRACTS TRANSLATES INTO 5.410 MILLION OZ ACCOMPANYING:

1.THE 21 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

86.470 MILLION OZ FINAL STANDING IN JULY.

6.475 MILLION OZ INITIAL STANDING IN AUGUST

TUESDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL 21 CENTS ).. AND, OUR OFFICIAL SECTOR/BANKERS WERE BASICALLY UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS AS WE HAD A STRONG GAIN ON OUR TWO EXCHANGES. WE ALSO WITNESSED NO APPRECIABLE SILVER SPREADER LIQUIDATION. THE BANKERS ENGAGED IN MINOR BANKER SHORT COVERING (IF ANY) ON THE TWO EXCHANGES, THEY COULD NOT COVER MUCH… THUS: THE CONSIDERABLE SIZED GAIN AT THE COMEX WAS ACCOMPANIED BY : i)NEGLIGIBLE SPREADER LIQUIDATION ii) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A GOOD INCREASE IN SILVER OZ STANDING FOR AUGUST, MINOR BANKER SHORT COVERING (IF ANY) AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A CONSIDERABLE NET GAIN OF 2 CONTRACTS OR 0.01 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKERS ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER..AND THUS THE REASON FOR OUR MASSIVE RAID THIS MORNING AND ALL LAST WEEK

SPREADING OPERATIONS/NOW SWITCHING TO SILVER

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN SILVER AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF AUGUST. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

AUGUST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF AUGUST:

18,798 CONTRACTS (FOR 19 TRADING DAY(S) TOTAL 18,798 CONTRACTS) OR 93.990 MILLION OZ: (AVERAGE PER DAY: 989 CONTRACTS OR 4.9468 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 93.990 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 13.42% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,364.27 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 133.95 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

AUGUST EXP 93.99 MILLION OZ (EXCHANGE FOR PHYSICALS STARTING TO DECREASE AGAIN)

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 286, DESPITE OUR STRONG 21 CENT LOSS IN SILVER PRICING AT THE COMEX ///TUESDAY AS ONE A NET BASIS, NOBODY LEFT THE SILVER ARENA..…THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1082 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A CONSIDERABLE SIZED 796 OI CONTRACTS ON THE TWO EXCHANGES (WITH OUR 21 CENT FALL IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 1082 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A CONSIDERABLE SIZED DECREASE OF 1090 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 21 CENT FALL IN PRICE OF SILVER/AND A CLOSING PRICE OF $26.24 // TUESDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.9460 BILLION OZ TO BE EXACT or 135% of annual global silver production (ex Russia & ex China).

FOR THE NEW AUGUST DELIVERY MONTH/ THEY FILED AT THE COMEX: 3 NOTICE(S) FOR 15,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 WAS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 86.470 million oz//AUGUST 6.475 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 2367 CONTRACTS TO 549,282 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE SMALL LOSS IN COMEX OI OCCURRED DESPITE OUR STRONG FALL IN PRICE OF $14.60 /// COMEX GOLD TRADING// TUESDAY//WE HAD MINIMAL BANKER SHORT COVERING(IF ANY), A GOOD SIZED INCREASE IN GOLD TONNAGE STANDING AT THE COMEX FOR AUGUST, ALONG WITH MINIMAL LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR LOSS IN PRICE OF $14.60.

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 134// (2400 OZ WAS DELIVERED ON FRIDAY FROM THE ENHANCED GOLD INVENTORY)…

WE LOST A SMALL SIZED 186 CONTRACTS (0.5785 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 2181 CONTRACTS:

CONTRACT .; AUG 0 AND OCT: 0 DEC: 2181; JUNE: 0 ALL OTHER MONTHS ZERO//TOTAL: 2181. The NEW COMEX OI for the gold complex rests at 549,282. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A TINY SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 186 CONTRACTS: 2367 CONTRACTS DECREASED AT THE COMEX AND 2181 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 186 CONTRACTS OR 0.5785 TONNES. TUESDAY, WE HAD A LOSS OF $14.60 IN GOLD TRADING……

AND WITH THAT LOSS IN PRICE, WE HAD A TINY SIZED LOSS IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 0.5785 TONNES!!!!!! THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT FELL $14.60). WE MAY HAVE HAD A MINOR BANKER SHORT COVERING (IF ANY) OPERATION BUT JUDGING FROM THE SLIGHT LOSS IN TOTAL OI DESPITE THE HEAVY LOSS IN PRICE AND THE SMALL ISSUANCE IN EXCHANGES FOR PHYSICAL THEY COULD NOT FLEECE ON A NET BASIS ANY OF OUR SPECULATOR LONGS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2181) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (2367 OI): TOTAL LOSS IN THE TWO EXCHANGES: 186 CONTRACTS. WE NO DOUBT HAD 1 )TINY BANKER SHORT COVERING (IF ANY), 2.)A SMALL INCREASE IN GOLD TONNAGE STANDING AT THE GOLD COMEX FOR THE FRONT AUGUST MONTH, 3) ZERO NET LONG LIQUIDATION; 4) SMALL COMEX OI LOSS AND 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL AND …ALL OF THIS WAS COUPLED WITH OUR STRONG LOSS IN GOLD PRICE TRADING//TUESDAY//$14.60.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

AUGUST

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAY(S) IN TONNES: 120.49 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 120.49/3550 x 100% TONNES =3.39% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3,380.55 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 313.09 TONNES ..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

AUGUST TOTAL EFP ISSUANCE; 120.49 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A CONSIDERABLE SIZED 1090 CONTRACTS FROM 188,721 DOWN TO 187,631 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE CONSIDERABLE SIZED LOSS IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1)NEGLIGIBLE SPREADER LIQUIDATION 2) MINIMAL BANKER SHORT COVERING (IF ANY) , 2) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A GOOD INCREASE IN SILVER OZ STANDING AT THE SILVER COMEX FOR AUGUST, AND 4) MINOR WEAK LONG LIQUIDATION, BUT ON NET, ZERO LONG LIQUIDATION.

EFP ISSUANCE 1082 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT: 1082 AND DEC. 0 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1092 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1090 CONTRACTS TO THE 1092 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A TINY SIZED GAIN OF 2 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 0.01 MILLION OZ, OCCURRED DESPITE OUR 21 CENT LOSS IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 43.84 POINTS OR 1.30% //Hang Sang CLOSED UP 5.57 POINTS OR 0.02% /The Nikkei closed UP 0.75 POINTS OR 0.01%//Australia’s all ordinaires CLOSED DOWN .49%

/Chinese yuan (ONSHORE) closed DOWN at 6.8909 /Oil UP TO 43.16 dollars per barrel for WTI and 45.74 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 6.8909 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8847 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total withdrawals; 106,214.411 oz

We had 2 kilobar transactions +

ADJUSTMENTS: 1 //

customer to dealer

i) Out of JPMorgan; 30,031.587 oz

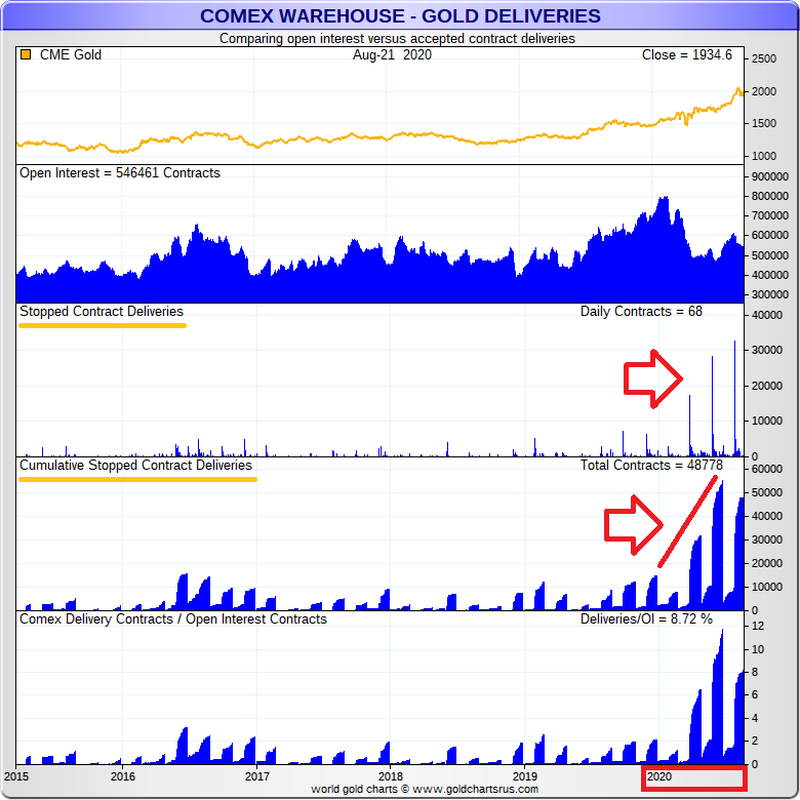

The front month of AUGUST registered a total of 161 CONTRACTS as we GAINED 23 contracts. We had 7 notices served on TUESDAY so we GAINED A STRONG 30 contracts or an additional 3000 OZ will stand for delivery on this side of the pond as they refused to morph into London based forwards as well as negating a fiat bonus for their effort. The boys are scrambling in search of badly needed physical metal as they start to search for metal on the other side of the pond. (the CME is now allowing other refiners as official facilities to supply metal…our regular guys just cannot that which is needed..see report on that below)

After August we have the non active Sept contract month.. Here we saw another GAIN of 62 contracts to stand at 2507. Oct LOST 195 contracts DOWN to 71,792

The big December contract LOST 2023 contracts DOWN to 400,382 contracts…(it is here where some of our short side bankers tried to bail and failed//and some weak hand longs)

We had 66 notices filed today for 6600 oz

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2020. contract month, we take the total number of notices filed so far for the month (48,875) x 100 oz , to which we add the difference between the open interest for the front month of AUGUST (161 CONTRACTS ) minus the number of notices served upon today (66 x 100 oz per contract) equals 4,897,000 OZ OR 152.317 TONNES) the number of ounces standing in this active month of JUNE

thus the INITIAL standings for gold for the AUGUST/2020 contract month:

No of notices filed so far (48,875, x 100 oz + 161 OI) for the front month minus the number of notices served upon today (66) x 100 oz which equals 4,897,000 oz standing OR 152.317 TONNES in this active delivery month. This is a HUGE amount for gold standing for a AUGUST delivery month (an active delivery month). The figures include the 2400 oz delivered upon in the enhanced gold section.

We gained 30 contracts or 3000 oz of gold as these guys refused to morph into London based forwards.

THE NAME OF THE GAME TODAY IS BANKER SHORT COVERING AS FINALLY FEAR BECAME THEIR CENTRAL FOCUS. THEY ORCHESTRATED ANOTHER RAID TODAY SO AS TO CAUSE SOME WEAK HAND SPECULATORS TO FLEE THE GOLD ARENA. THEY SUCCEEDED SLIGHTLY.

NEW PLEDGED GOLD: BRINKS

144,088.952 oz NOW PLEDGED JAN 21.2020/HSBC 5.4807 TONNES

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

261,955.892 oz (some deleted august 3) JPM 8.1479 TONNES

611,401.341 oz pledged June 12/2020 Brinks/ july 2/july 21 19.017 tonnes

25,078.004 oz Pledged August 21/regular account .7800 tonnes jpm

total pledged gold: 1,085,072.487 oz 33.75 tonnes

total registered, pledged and eligible (customer) gold; 37,153,088.527 oz 1,155.61 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1029,27 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

20,000.000 oz

HSBC

???? exact???

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

nil

oz

|

| No of oz served today (contracts) |

3

CONTRACT(S)

(15,000 OZ)

|

| No of oz to be served (notices) |

13 contracts

65,000 oz)

|

| Total monthly oz silver served (contracts) | 1282 contracts

6,410,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 0 deposits into the customer account

i)into JPMorgan: nil oz

ii) Into everybody else: 0

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 165.53 million oz of total silver inventory or 48.71% of all official comex silver. (165.53 million/339.845 million

total customer deposits today: nil oz

we had 1 withdrawals:

i) Out of HSBC: 20,000.000000 oz ???? exact!

total withdrawals; 20,000.000 oz

We had 0 adjustments

Total dealer(registered) silver: 130.403 million oz

total registered and eligible silver: 339.845 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

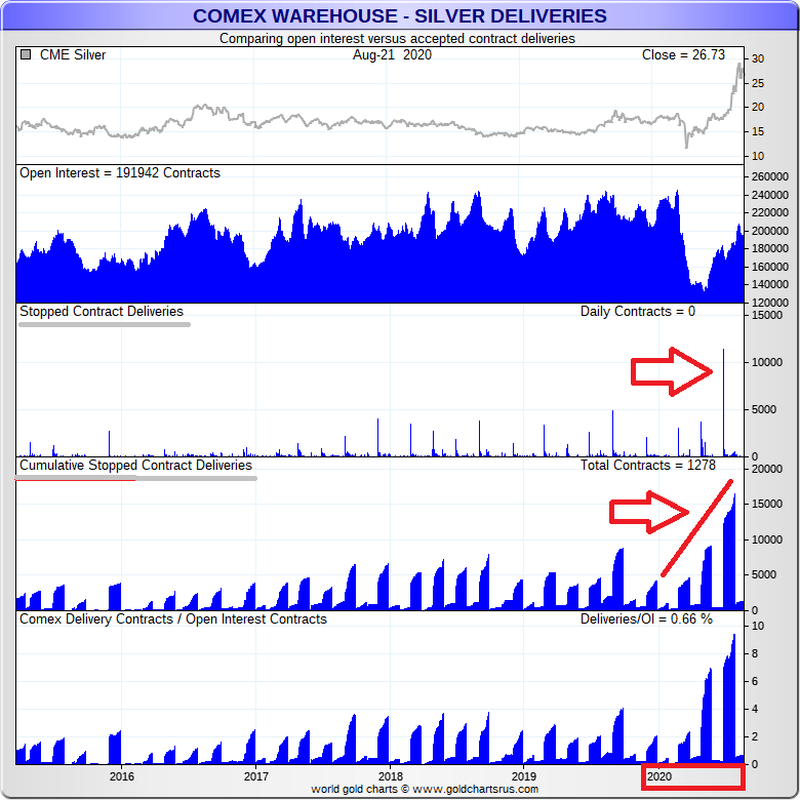

the front month of August registered an open interest of 16 contracts and thus we GAINED 2 contracts. We had 1 notices filed on TUESDAY so we GAINED 3 contracts or an additional 15,000 oz will stand for delivery as these guys REFUSED TO morph into London based forwards as well as NEGATING a fiat bonus…. The bankers are now desperate in their search for badly needed silver whether it is on this side of the pond or the European side.

After August we have the big September contract month and here we see a loss of only 6272 contracts down to 43,375. November saw another gain of 32 contracts to stand at 467.

SEPT OI IS VERY HIGH AND WE WILL HAVE A DANDY AMOUNT OF SILVER STANDING AT THE COMEX. WE HAVE 4 MORE READING DAYS BEFORE FIRST DAY NOTICE AUGUST 31/2020 (MONDAY)

THE BANKERS MUST HAVE BEEN NOT OVERJOYED TONIGHT WHEN THEY SAW THE HIGH OPEN INTEREST FOR THE FRONT MONTH OF SEPT…AND NOT CONTRACTING MUCH!!

The big December contract month saw its OI rise by good 5227 contracts up to 131,844

The total number of notices filed today for the AUGUST 2020. contract month is represented by 3 contract(s) FOR 15,000, oz

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 1282 x 5,000 oz = 6,410,000 oz to which we add the difference between the open interest for the front month of AUGUST(16) and the number of notices served upon today 3 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the AUGUST/2019 contract month: 1282 (notices served so far) x 5000 oz + OI for front month of AUGUST (x)- number of notices served upon today (3) x 5000 oz of silver standing for the AUGUST contract month.equals 6,475,000 oz. ..VERY STRONG FOR A NON ACTIVE MONTH.

We GAINED 3 contracts or an additional 15,000 oz will stand for delivery as they refused to morph into London based forwards..

TODAY’S ESTIMATED SILVER VOLUME : 182,376 CONTRACTS // volume huge++++++++++++++++++++++++++++++++++++++++++++++++/

FOR YESTERDAY: 139,508. ,CONFIRMED VOLUME//volume huge.++++++++

YESTERDAY’S CONFIRMED VOLUME OF 139,508 CONTRACTS EQUATES to 0.697 billion OZ 99.44% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO- 2.70% ((AUGUST 26/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.83% to NAV: (AUGUST 26/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/2,70%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 20.66 TRADING 20.24///NEGATIVE 2.05

END

And now the Gold inventory at the GLD/

AUGUST 26/WITH GOLD UP $26.70 TODAY/ WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.53 TONNES FROM THE GLD//RESTS AT 1248.85 TONNES

AUGUST 25/WITH GOLD DOWN $14.60 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//RESTS AT 1252.38 TONNES

AUGUST 24//WITH GOLD DOWN $7.20 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1258.38 TONNES

AUGUST 21//WITH GOLD DOWN $.40 TODAY: WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1252.38 TONNES

AUGUST 20/WITH GOLD DOWN $23.45 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD: .//INVENTORY REST AT 1252.38 TONNES

AUGUST 19//WITH GOLD DOWN $39.65 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1252.38 TONNES

AUGUST 18/WITH GOLD UP $14.60 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 4.09 TONNES//GLD INVENTORY RESTS TONIGHT AT 1252.38 TONNES

AUGUST 17/WITH GOLD UP $46.30 TODAY: SURPRISINGLY WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 3.8 TONNES//INVENTORY RESTS AT 1248.29 TONNES

AUGUST 14/ WITH GOLD DOWN $19.45 TODAY: SURPRISINGLY, WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.46 TONNES/INVENTORY RESTS AT 1252.63 TONNES.

AUGUST 13/WITH GOLD UP $23.15 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY: SURPRISINGLY A PAPER WITHDRAWAL OF 7.30 TONNES/INVENTORY RESTS AT 1250.63 TONNES

AUGUST 12/ WITH GOLD UP $1.00 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 4.19 TONNES//INVENTORY RESTS AT 1257.93 TONNES

AUGUST 11//WITH GOLD DOWN $92.40 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1262.12 TONNES.

AUGUST 10/WITH GOLD UP $11.35 TODAY, WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.84 TONNES//INVENTORY RESTS AT 1262.12 TONNES

AUGUST 7/WITH GOLD DOWN $38.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1267.96 TONNES

AUGUST 6/WITH GOLD UP $20.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER DEPOSIT OF 10.23 TONNES INTO THE GLD/INVENTORY RESTS AT 1267.96 TONNES//

AUGUST 5/WITH GOLD UP $ 33.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 9.35 TONNES INTO THE GLD//INVENTORY RESTS AT 1257.73 TONNES

AUGUST 4//WITH GOLD UP $31.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 6.48 TONNES/GLD INVENTORY RESTS AT 1248.38 TONNES

AUGUST 3/WITH GOLD UP $2.20 TODAY, WE HAVE NO CHANGES IN THE GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241,96 TONNES

JULY 31/WITH GOLD UP $17.90 TODAY/WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241.96 TONNES.

JULY 30/WITH GOLD DOWN $10.00 TODAY, WE HAVE ANOTHER SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES//INVENTORY RESTS AT 1241.96 TONNES.

JULY 29//WITH GOLD UP $12.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 8.47 TONNES/INVENTORY RESTS AT 1243.12 TONNES

JULY 28///WITH GOLD UP $13.25 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 5.84 TONNES/INVENTORY RESTS AT 1234.65

JULY 27//WITH GOLD UP $35.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF XXX TONNES/INVENTORY RESTS AT 1228.81 TONNES

JULY 24/WITH GOLD UP $8.80 TODAY: WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.80 TONNES//INVENTORY RESTS AT 1228.81 TONNES

JULY 23/WITH GOLD UP $24.90 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 7.26 TONNES/INVENTORY RESTS AT 1225.01 TONNES

JULY 22/WITH GOLD UP $22.00 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 7.89 TONNES/INVENTORY RESTS AT 1219.75 TONNES

JULY 21//WITH GOLD UP $26.00 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.97 TONNES INTO THE GLD// INVENTORY RESTS AT 1211.86 TONNES

JULY 20/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1206.89 TONNES

JULY 17/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1206.89 TONNES

JULY 16/WITH GOLD DOWN $9.80 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: INVENTORY RESTS AT 1206.89 TONNES

JULY 15//WITH GOLD UP $1.55 TODAY/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 2.96 TONNES INTO THE GLD///INVENTORY RESTS AT 1206.89 TONNES

JULY 14//WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 3.51 TONNES/INVENTORY RESTS AT 1203.97 TONNES

JULY 13//WITH GOLD UP $12.50 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1200.46 TONNES

JULY 10/WITH GOLD DOWN $.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD//A STRANGE WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1200.82 TONNES

JULY 9//WITH GOLD DOWN $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OX 3.21 TONNES INTO THE GLD//INVENTORY RESTS AT 1202.57 TONNES

JULY 8/WITH GOLD UP $13.75 TODAY; A BIG CHANGE IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 7.89 TONNES INTO THE GLD//INVENTORY RESTS AT 1199.36 TONNES

JULY 7/WITH GOLD UP $12.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1191.47 TONNES

JULY 6/WITH GOLD UP $6.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1191.47 TONNES

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

AUGUST 26/ GLD INVENTORY 1248.85 tonnes*

LAST; 889 TRADING DAYS: +309.35 NET TONNES HAVE BEEN ADDED THE GLD

LAST 789 TRADING DAYS://+487.88 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

AUGUST 26//WITH SILVER UP $1.04 TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.65 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 566.419 MILLION OZ..

AUGUST 25/WITH SILVER DOWN 21 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.607 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 571.074 MILLION OZ//

AUGUST 24//WITH SILVER DOWN 18 CENTS TODAY: WE HAD A NO CHANGES//INVENTORY RESTS AT 573.843 MILLION OZ//

AUGUST 21//WITH SILVER DOWN 30 CENTS TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.838 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 573.843 MILLION OZ..

AUGUST 20/WITH SILVER DOWN $.26 TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 3.724 MILLION OZ FROM THE SLV..//INVENTORY REST AT 572.843 MILLION OZ

AUGUST 18/WITH SILVER UP $.44 TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.514 MILLION OZ//THE SLV INVENTORY RESTS TONIGHT AT 576.567 MILLION OZ//

AUGUST 17/WITH SILVER UP $1.27 TODAY: WE HAD NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 14/WITH SILVER DOWN $1.31 TODAY, WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.984 MILLION OZ// //INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 13//WITH SILVER UP $1.76 TODAY: WE HAVE TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A PAPER DEPOSIT OF 2.421 MILLION OZ INTO THE SLV AT 2 PM AND ANOTHER DEPOSIT OF 6.984 MILLION OZ AT 5 20 PM/INVENTORY RESTS AT 581.037 MILLION OZ//

AUGUST 12/WITH SILVER DOWN 40 CENTS TODAY: WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF XX MILLION OZ//INVENTORY RESTS AT XX MILLION OZ/

AUGUST 11/WITH SILVER DOWN $3.25 CENTS, WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.41 MILLION OZ//INVENTORY RESTS AT 571.632 MILLION OZ//

AUGUST 10/WITH SILVER UP 1.89 TODAY, WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 3.538 MILLION OZ/INVENTORY RESTS AT 569.491 MILLION OZ//

AUGUST 7/WITH SILVER DOWN 69 CENTS TODAY: WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY: A DEPOSIT OF 0.465 MILLION OZ/INVENTORY RESTS AT 573.029 MILLION OZ.

AUGUST 6/WITH SILVER UP $1.52 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 572.564 MILLION OZ///

AUGUST 5/WITH SILVER UP $1.03 TODAY, WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A MONSTROUS DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 572.564 MILLION OZ//

AUGUST 4/WITH SILVER UP $1.45 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 367.161 MILLION OZ//

AUGUST 3/WITH SILVER UP 23 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//SURPRISINGLY ANOTHER WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 367.161 MILLION OZ//

JULY 31/WITH SILVER UP 82 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: SURPRISINGLY A HUGE WITHDRAWAL OF 3.26 MILLION OZ//INVENTORY RESTS AT 368.092 MILLION OZ//

JULY 30//WITH SILVER DOWN 97 CENTS TODAY: WE HAVE A SMALL CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 571.352 MILLION OZ//

JULY 29/WITH SILVER UP 7 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY//A DEPOSIT OF 5.984 MILLION OZ//INVENTORY RESTS AT 572.283 MILLION OZ//

JULY 28 WITH SILVER DOWN 14 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 7.52 MILLION OZ//INVENTORY RESTS AT 566.299 MILLION OZ//

JULY 27/WITH SILVER UP $2.67 TODAY, WE HAD NO CHANGES IN SILVER INVENTORY: A DEPOSIT OF XX MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ//

JULY 24/WITH SILVER DOWN $0.12 TODAY: NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 558.779 MILLION OZ/

JULY 23/WITH SILVER UP $.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A HUMONGOUS PAPER DEPOSIT OF 9.594 MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ///

JULY 22/WITH SILVER UP $1.54 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A HUMONGOUS PAPER DEPOSIT OF 7.218 MILLION OZ//INVENTORY RESTS AT 549.185 MILLION OZ/

JULY 21/WITH SILVER UP $1.38 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUMONGOUS PAPER DEPOSIT OF 15.368 MILLION OZ////INVENTORY RESTS AT 541.967 MILLION OZ//

JULY 20/WITH SILVER UP 40 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 3.819 MILLION OZ ‘ENTERED” THE SLV..INVENTORY RESTS AT 526.599 MILLION OZ/

JULY 17/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 1.583 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 522.780 MILLION OZ//

JULY 16//WITH SILVER DOWN 14 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ//INVENTORY RESTS AT 521.197 MILLION OZ..

JULY 15.WITH SILVER UP 21 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.956 MILLION OZ//INVENTORY RESTS AT 516.074 MILLION OZ//

JULY 14/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 514.118 MILLION OZ//

JULY 13//WITH SILVER UP 67 CENTS TODAY: A HUGE CHANGE IN SILVER: A WITHDRAWAL OF 1.677 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 514.118 MILLION OZ//

JULY 10/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 4.844 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.795 MILLION OZ

WHAT A FRAUD!!

JULY 9/WITH SILVER DOWN 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 8.198 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 510.951 MILLION OZ/

JULY 8/WITH SILVER UP 37 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.118 MILLION OZ FROM THE SLV//VERY SURPRISING.//INVENTORY RESTS AT 502.753 MILLION OZ//

JULY 7/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/INVENTORY RESTS AT 503.871 MILLION OZ///

JULY 6//WITH SILVER UP 24 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.863 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 503.871 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

AUGUST 26.2020:

SLV INVENTORY RESTS TONIGHT AT

566.419 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

A very important commentary from Ted butler. He is noticing what I have been telling you: huge amounts of silver coming into the comex but an equal amount of silver leaving. He is of the opinion that it is the users of silver that are stockpiling the metal\

\(zerohedge)

Ted Butler: A silver mystery in full view

Submitted by cpowell on Tue, 2020-08-25 15:33. Section: Daily Dispatches

11:36a ET Tuesday, August 25, 2020

Dear Friend of GATA and Gold:

What explains the furious turnover in silver inventory in the vaults associated with the New York Commodities Exchange, a turnover that vastly exceeds levels in any other commodity market?

Silver market analyst Ted Butler ponders the question this week, concluding that the turnover is probably a matter of enormous industrial demand, which, he writes, underlies the bullish case for the metal when combined with rising investment demand.

Butler’s analysis is headlined “A Silver Mystery in Full View” and it’s posted at GoldSeek’s companion site, SilverSeek, here:

https://silverseek.com/article/silver-mystery-full-view

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

A Silver Mystery in Full View

For those who have come to be convinced of the silver price manipulation, as well as those who remain unconvinced, I ask you to put aside all thoughts about derivatives trading, concentrated short positions and epic double crosses and think about something completely different. Please accept this as an open invitation in which no prior experience in matters related to sophisticated financial transactions is required and in which all that is needed is common sense and logical thinking.

In essence, I’ll lay out a series of documented facts which at their core present a silver mystery that cries out for explanation. Remarkably, the facts are beyond dispute and freely available to all, yet for some reason the data have been virtually ignored by everyone in the analytical community. While I’ll provide my explanation for the mystery, my main point is to solicit any reasonable alternative explanations. This is very much a debate open to all to help solve a mystery that deserves an answer.

For more than 9 years, starting in April 2011, I have been observing and reporting on a highly unusual development that has continued to this day. Basically, out of nowhere, the physical movement or turnover of 1000 oz bars of silver being brought into and removed from the COMEX-approved silver warehouses erupted from what had occurred prior to April 2011. Please understand that I am referring to physical metal arriving on trucks and being deposited into the various COMEX warehouses as well as physical metal being taken out of these same warehouses and put on trucks and taken elsewhere.

While there is, obviously, some connection to paper futures trading and deliveries on futures, put that aside and focus on the actual physical metal being brought into and removed from the COMEX silver warehouses because that’s at the heart of the mystery. Just for clarity – if one million oz of silver were brought in and deposited into the COMEX warehouses and another one million oz were taken out that same day, I would count that as a two million oz turnover. For purposes of daily physical silver movement, I exclude changes involving changes in category classification between eligible and registered, as such changes don’t involve physical movement. Just focus on actual amounts received and withdrawn. Detailed physical movement is provided (for free) on the CME Group’s website daily – click on silver stocks

https://www.cmegroup.com/clearing/operations-and-deliveries/nymex-delivery-notices.html

Using these metrics, over the past 9 years there has been an average weekly physical turnover of some 5 million oz, or an annual turnover of more than 250 million oz. In recent years, the annual physical turnover, including that for the most recent 52 weeks, has been 300 million oz. Over the more than 9 years since the highly unusual and unprecedented extreme turnover of physical silver in 1000 oz bar form started to rush into and out from the COMEX-approved silver warehouses, more than 2.5 billion ounces have been physically moved. I would ask you to think about that for a moment.

Here we have conclusive and indisputable evidence that more than 2.5 billion oz of silver have been moved into and out from a small number (10) of warehouses in and around the New York metropolitan area over the past 9 years. I’ve recorded the turnover daily and reported on it weekly for all that time. That total physical movement over this time is equal to or greater than all the silver in 1000 oz bar form that exists in the world. That should astound you and everyone with the slightest interest in silver.

Over this same 9+ years, there has been an increase in total COMEX silver warehouse inventories from around 100 million oz in April 2011 to 340 million oz today, but that only accounts for less than 10% of the total turnover. And much of the increase in total COMEX inventories can be traced to the JPMorgan COMEX warehouse, which started out at zero ounces in 2011 and now holds 166 million oz. Over the past 52 weeks, total COMEX silver inventories grew by 27 million oz, while the physical turnover amounted to 300 million oz. Silver investment demand is not the explanation for the extreme physical turnover in the COMEX silver warehouses. Investor accumulation wouldn’t account for the extreme turnover.

In fact, I’m surprised that total investment holdings at the COMEX haven’t grown more than they have. After all, this is the source of physical silver bought by both the Hunt Bros up through 1980 and by Warren Buffett in 1997. And COMEX physical silver was always the main form in which my departed mentor, Izzy Friedman, owned his silver.

Back in the year 2000, long before the introduction of SLV and other silver ETFs, I wrote an article explaining how COMEX silver receipts (backed by physical silver in the COMEX warehouses) were the very best method for buying and holding silver in size. At the time of the article, silver was trading for $5 an ounce and while it has been higher and lower than it is today ($27), I would point this out to those critics who insist that everything I say is bogus.

https://www.gold-eagle.com/article/best-silver-investment

Over the years (decades), millions of silver ounces have been bought and held, at my urging, in the form of COMEX warehouse silver inventories. I raise this issue to make another, separate point, namely that this privately-owned investment silver is part of the total COMEX warehouse inventories, even though it is not available for delivery currently. And there are countless other millions of ounces in the COMEX warehouses held by investors which haven’t been bought at my urging, but simply because this is a great way to hold investment silver. In a very real sense, this investment silver artificially inflates the total COMEX inventories to levels not indicative of working inventories.

What prompts this thought is the recent refusal by the COMEX and BlackRock, sponsor of the SLV, to comment on whether the 103 million oz held on behalf of the SLV by JPMorgan in New York is part of the 340 million oz in total COMEX silver “inventories”. I believe the refusal by either to confirm or deny the 103 million oz is being “double counted’ means that is likely the case. If my suspicions are correct about investor holdings being included in total COMEX silver inventories that means the true actual amount of working inventories in much less than the 340 million oz being reported. Why does this matter?

It matters because when compared to the actual documented physical turnover, it makes a big difference whether the 300 million oz annual turnover is occurring on a 340 million oz inventory or an inventory much less – say 100 or 150 million oz. Please don’t misunderstand what I’m saying – there is no commodity in the world that has or ever will experience the type of physical turnover that has existed in the COMEX silver warehouses these past 9 years – with no exceptions. But there is a big difference between whether the total inventories are 340 million oz or some much smaller amount. And when it comes to the COMEX, it’s wise to assume the most devious explanation.

OK, so the open question is why, among all commodities, has the physical turnover in COMEX silver been so extraordinarily large and persistent for all these years and not in any other commodity? You don’t need to be a commodities or derivatives expert or other professional with years of hands-on experience to venture an answer to a very simple question – why just silver? This is a debate open to all and no pre-qualifications are required – just something that makes sense.

Since I’m the one raising this issue, I’ve obviously thought about it a lot. My take is that the incredible physical silver turnover has very little to do with silver investors and that leaves only one other source for the physical demand that is driving the extreme turnover. That source is the industrial silver users. There is such large and persistent demand for physical silver by industrial and fabrication consumers that it is both flying into and out from the COMEX warehouses. You may recall I recently wrote about the silver users, both privately (in the archives dated July 29) and publicly on Aug 7 – https://silverseek.com/article/dont-forget-silver-users

I believe there is such strong and persistent demand for physical silver by industrial consumers of every type draining metal from the COMEX that it has been necessary for new silver to be brought into the COMEX warehouses to meet the demand. I don’t think the reverse can possibly be true, namely, that so much silver is coming into the COMEX warehouses that someone needs to withdraw it aggressively to keep total inventories from exploding.

If I am correct in my take, what I’m describing is persistent near white-hot industrial demand that might be on the verge of panic if the physical flow of silver is interrupted for any reason. One thing I’m not sure of is whether the industrial users of silver may have started to build up physical inventories in anticipation of a developing silver shortage. Whereas I always agreed with Izzy that it would take actual delays in physical deliveries to set off a user inventory buying panic, it dawns on me that the industrial silver users today are much different from the users of 35 years ago.

Companies like Apple Computer and Tesla Motors were in their infancy or years from being born in 1985 and it would be hard to argue that these companies aren’t smart and keenly aware of what’s going on in the world. It’s not difficult to imagine that some of today’s industrial silver users may have figured out that silver is likely to be in short supply in the future and it would be wise to secure future supplies now.

Further, it’s quite possible the recent increases in COMEX silver warehouse inventories reflect user inventory building, as there’s no way of knowing exactly who holds the metal – investors or users. Recently, JPMorgan issued (delivered) 40 million oz in its house account, yet none of that metal has been shipped out of its COMEX warehouse, even though ownership changed hands. As much as I condemn the COMEX for price manipulation, the fact is that its approved warehouses are a great place to store silver. A user taking delivery of that silver would have no compelling reason to move it out from the COMEX until needed. Same with an investor taking delivery.

Where this distinction is important, however, is in future silver delivery demands. Some have speculated that delivery demands in the fast-approaching September COMEX futures contract would be extremely large and bullish for the price. That may or may not be the case, but I can attest to something far more certain. If it develops that purely speculative demand gets lined up to take delivery and there is anything that suggests those speculators are interested in “goosing” the price by taking delivery, the regulators are sure to intercede (as they should). But when the day comes that legitimate silver users are demanding delivery, then there is little the regulators can do.

One final point. Imagine if you would that instead of the physical turnover of silver exploding in the COMEX warehouses out of nowhere 9 years ago that the physical turnover occurred in some other industrial metal, like copper or zinc or nickel. Would that not become the talk of the analytical world in those commodities? Would not the conclusion quickly turn to sharply increased industrial demand as causing the sudden burst of physical warehouse movement? Why is that not the case in silver?

I am hard-pressed to construct a more bullish price set up than what I just described. How it is not at the forefront of every silver commentator’s list of reasons to be bullish is a puzzle to me. Be assured it is at the very top of my list of factors that could and should send silver prices soaring. If you have any thoughts on this matter, please let me hear from you. Something is responsible for the unprecedented physical metal turnover in the COMEX silver warehouses and it is high time it be examined.

Ted Butler

August 24, 2020

END

Craig Hemke is seeing what I am seeing; we are going to have a dandy delivery in September; maybe north of 90 million oz//

(Craig Hemke)

Craig Hemke at Sprott Money: Biggest monthly Comex silver offtake is about to happen

Submitted by cpowell on Tue, 2020-08-25 23:36. Section: Daily Dispatches

7:35p ET Tuedsay, August 25, 2020

Dear Friend of GATA and Gold:

More huge delivery demands are likely in Comex September silver, more than the huge demands made in the last three delivery months, the TF Metals Report’s Craig Hemke writes today at Sprott Money.

Hemke writes: “Total delivery demands for Comex silver in September are on track to meet or exceed what was seen in July. Could we see upwards of 90 million ounces of silver ‘delivered’ over the next 30 days? Yes, we sure could. What would this mean? Again, not likely the end of the Comex and its digital derivative pricing scheme. However, maybe we’ll move a few steps closer to the end — and that’s what we’re all anxiously awaiting.”

Hemke’s analysis is headlined “Comex Silver in September” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/COMEX-Silver-in-September-craig-hemke-a…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

The BIS footprint into gold trading is evidenced by the huge number of gold swaps orchestrated by them

(Robert Lambourne/)GATA)

Robert Lambourne BIS gold swaps soared in July, may be at highest level ever

Submitted by cpowell on Wed, 2020-08-26 16:21. Section: Documentation

By Robert Lambourne

Wednesday, August 26, 2020

The recently reported July statement of account of the Bank for International Settlements discloses that the bank’s use of gold swaps increased strongly that month to an estimated 474 tonnes, up 21 percent from 391 tonnes in June.

The swaps are used to gain access to gold supplies from bullion banks and the gold is then deposited in BIS gold sight accounts at major central banks, such as the Federal Reserve.

…

The BIS’ use of gold swaps and derivatives has been extensive so far this year, with July’s level being the highest since August 2018. By contrast, in May 2019 the bank was carrying only 78 tonnes in swaps.

The July estimate of the bank’s gold swaps is also higher than any swaps reported by the BIS at the March year-end since March 2010. Hence it is possible that the gold swaps as of July are highest ever for the bank.

The swap transactions create a mismatch at the BIS, which ends up being long unallocated gold (the gold held in BIS sight accounts at major central banks) and short allocated gold (gold required to be returned to swap counterparties).

This mismatch has not yet been reported as such in the bank’s annual reports.

The table below reports the estimated swap levels since August 2018. It can be seen that the BIS is actively involved in trading gold swaps and other gold derivatives with changes from month to month in excess of 100 tonnes in this period.

———-

Month ….. Swaps

& year … in tonnes

Jul-20 ….. / 474

Jun-20 …. / 391

May-20 …. / 412

Apr-20 …. / 328

Mar-20 …. / 326*

Feb-20 …. / 326

Jan-20 …. / 320

Dec-19 …. / 313

Nov-19 …. / 250

Oct-19 …. / 186

Sep-19 …. / 128

Aug-19 …. / 162

Jul-19 ….. / 95

Jun-19 …. / 126

May-19 …. / 78

Apr-19 ….. / 88

Mar-19 …. / 175

Feb-19 …. / 303

Jan-19 …. / 247

Dec-18 …. / 275

Nov-18 …. / 308

Oct-18 …. / 372

Sep-18 …. / 238

Aug-18 …. / 370

* The estimate originally reported by GATA was 332 tonnes, but the BIS Annual Report states 326 tonnes. It is believed that this difference arose because the gold price used to calculate the GATA estimate was lower than the price used by the BIS. GATA uses gold prices quoted by USAGold.com to estimate the level of gold swaps held by the BIS at month-ends.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults with GATA about the involvement of the Bank for International Settlements in the gold market.

* * *

iii) Other physical stories:

We brought this to your attention yesterday but due to its significance we are repeating the story. As a matter of record, the enhanced inventory section (4 GC) has so far been rarely used and only one delivery of 2400 oz

This is a huge story: the comex is running out of metal

Ronan Manly

LBMA-COMEX Collusion Intensifies As CME Mass Approves 267 LBMA Gold And Silver Bar Brands

Submitted by Ronan Manly of BullionStar.com

In a move which has gone entirely unnoticed in the precious metals markets, but which signals gold and silver bar delivery constraints for the COMEX gold and silver futures contracts, Chicago Mercantile Exchange Group (CME), operator of the New York based COMEX, has quietly and under the radar, hugely expanded its lists of eligible refinery gold and silver bar brands that can be delivered against the massively traded flagship GC 100 (100 oz gold) and SI (5000 oz silver) contracts.

These changes, which were implemented on 27 July and which are detailed below, also look to be serving an even bigger agenda of preparing for a radical change in the delivery procedures of these two famous contracts so as to facilitate gold and silver stored in London Bullion Market Association (LBMA) vaults in London, England, to be used in settlement against the GC 100 oz and the SI 5000 oz COMEX contracts. Note that the COMEX 100 oz gold futures contract is currently deliverable as either one 100 troy ounce gold bar, or three 1 kilo gold bars, while the COMEX 5000 oz silver futures contract is currently deliverable as five 1,000 troy ounce cast silver bars (with a weight tolerance of 10% either higher or lower).

To reiterate, these changes are to the gold and silver refiner brand lists of the big boy contracts GC 100 and SI. You may recall something similar happening for a new 4GC contract when it was rushed out in late March, but that was just a trial run. This is the main event.

From New York to London

As a reminder and as some background, CME (COMEX) and the LBMA began explicitly colluding on 24 March this year in an attempt to try to reign in the global precious metals markets following an Exchange for Physical (EFP) gold delivery failure in London which caused both a blow out between gold futures and gold spot spreads, as well as a bid-ask spread blowout in London spot gold, and which prompted the LBMA in a public statement to say that it had:

“offered its support to CME Group to facilitate physical delivery in New York”

On the same day, 24 March, Reuters, the embedded LBMA mouthpiece, reported that:

“The LBMA and executives at major gold-trading banks asked CME to allow 400-ounce bars to be used to settle Comex contracts, said the two sources, both of whom were involved in the discussions.”

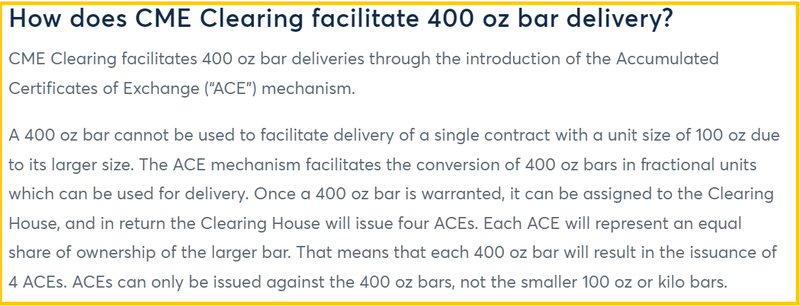

Again, on the same day, 24 March, the CME Group hurriedly launched a new gold futures contract called the “Gold (Enhanced Delivery) futures contract” (ticker 4GC), a contract which is structured to allow delivery via 100 oz gold bars, or kilo gold bars, or 400 oz gold bars.

Notably, in the 4GC contract, a 400 oz gold bar can be delivered via “Accumulated Certificates of Exchange” (ACEs), a fractional paper construct created by the CME to, in its words, “facilitate the conversion of 400 oz bars in fractional units which can be used for delivery” where “the Clearing House will issue four ACEs. Each ACE will represent an equal share of ownership of the larger bar.”

Importantly, in late March, CME created an entirely new and huge list of eligible gold refiner brands whose bars would be acceptable for delivery against this new ‘Enhanced Delivery’ 4GC futures contract, a list which comprised every gold refiner brand on both the current and former LBMA Good Delivery lists of gold refiners, and every gold refiner brand already on the GC 100 contract eligible gold refiner list at that time.

Whatever it Takes – Add the whole Goddam List

As the CME said in its 24 March press release for the 4GC contract:

“The approved brand list for this product will have complete convergence with the approved brand list for CME Group’s existing gold futures and the LBMA gold good delivery list.”

While this 400 oz 4GC contract launched in late March has hardly traded since then, its primary purpose now looks to have been a trial run to test out linking COMEX precious metals contracts to the London vaults and to the LBMA Good Delivery refiners lists, and to test implement the construction technique for the expanded eligible gold and silver bar brand lists of the GC 100 gold and SI (5000) silver contracts.

As the CME and the LBMA said in another joint statement on 1 April, they “will continue to coordinate efforts as market circumstances evolve”. And continue to coordinate they have.

For those who might not be familiar, the COMEX approved brand list for gold and the LBMA Good Delivery lists for gold were (up until recently) two entirely unrelated lists and concepts. The same was true of the COMEX approved brand list for silver and the LBMA Good Delivery lists for silver – they were two entirely unrelated lists and concepts.

The COMEX approved gold refiner brand list (up until 27 July) was a list of refiners which produced either 100 oz gold bars or 1 kilo gold bars which COMEX judged to be of a sufficient standard to be physically deliverable against the GC 100 gold contract. On the other hand, the LBMA Good Delivery List for gold lists those gold refineries around the world which produce the far larger 400 oz gold bars (central bank gold bars) and whose gold bars are deemed by the LBMA Good Delivery referees to be of a high enough quality for inclusion.

Likewise, the COMEX approved silver refiner brand list (up until 27 July) was a list of silver refiners which produced 1000 oz silver bars, bars which COMEX deemed worthy to be deliverable against the SI silver contract. In contrast, the LBMA Good Delivery List for silver is a far larger list of silver refineries which produce 1000 oz silver bars, including many CHinese refineries, that have been accredited by the LBMA Good Delivery referees.

When at the end of March, CME rushed to create a new gold bar refiner list for the 4GC (400 oz) gold contract, there were 68 gold bar brands listed on the existing GC 100 approved gold bar brand, and this list had not changed in any material way for a long time save for a few additions and deletions of refineries along the way.

In late March for the new 4GC contract, CME took this existing COMEX GC 100 refiner list and merged it with the LBMA Good Delivery List for gold, adding in all the gold refinery brands that were on the LBMA Good Delivery list that had not already been on the GC 100 list. This was a whopping 51 bar brands on the LBMA Good Delivery gold list that were not on the GC 100 refiner list. When these two lists were added together and merged, it resulted in a combined list of 119 approved bar brands, an exact 75% increase over the 68 refineries which were on the GC 100 COMEX gold bar brand list.

4GC Test Run

Next, and this too is very important, the CME also added to the 4GC list all of the gold refineries that are listed on the former LBMA Good Delivery List for gold. For those who don’t know, the LBMA maintains two refiner bar brand lists for gold as well as another two refiner bar brand lists for silver. The current LBMA Good Delivery List for gold lists gold refiners which currently produce 400 oz gold bars which have been accredited by the LBMA.

The former LBMA Good Delivery List for gold lists gold refiners which at some point in the past produced 400 oz gold bars which had been accredited by the London Gold Market referees, such as the Royal Mint’s refinery and Johnson Matthey, which previously administered the London Good Delivery list. This former list is a list of refineries, including historic and long gone refiners, which don’t currently make Good Delivery gold bars (400 oz gold bars) but whose gold bars, before they stopped making them or were taken off the list, are still accepted as London Good Delivery. Note that the history of the Good Delivery list stretches back all the way to 1750. The LBMA has only been in existence since 1987.

There are, wait for it, 111 additional refiners on the former LBMA Good Delivery List for gold that are not on the current LBMA Good Delivery list for gold. This means, in total, when the COMEX 4GC contract went live in early April this year, its approved refiner list of gold bar brands contained the names of a massive 230 refiner bar brands, 68 + 51 + 111 = 230. That’s a 238% increase in the number of refineries compared to the 68 refiners which were on the pre-April GC 100 approved refiner gold list. Ironically, the new 4GC contract has never traded, but was it ever meant to, or was it a red herring to set up the 400 oz London deliverable infrastructure for the GC 100 contract?

GC 100 and SI 5000 – A Live Exercise, Conjob-27

Now fast forward to 27 July, and what do we find? Well on 27 July, the CME (COMEX) in a very low key way and without any media announcements or press releases, quietly slipped in a market regulation filing (MKR) on its website titled “Regularity Approvals for Gold and Silver Brands”, with a short statement as follows:

“From Registrar’s Office

# MKR07-27-20

Notice Date 27 July 2020

Effective Date 27 July 2020

The Commodity Exchange, Inc. (“COMEX” or “Exchange”) has approved certain London Bullion Market Association (“LBMA”) good delivery brands for delivery against the Exchange’s Gold Futures (GC) and Silver Futures (SI) contracts. The list of brands are located in the “Gold (GC) Brands” and “Silver (SI) Brands” tabs in the service providers table at the end of Chapter 7 of the COMEX Rulebook.

These approvals will increase the brands of available material that can be used to satisfy delivery requirements of the Gold Futures (GC) and Silver Futures (SI) contractsand will afford market participants expanded delivery options.

These approvals are effective immediately.”

When one consults the said “Gold (GC) Brands” and “Silver (SI) Brands” tabs of the latest CME service providers table (which is published as a spreadsheet in XLS format here), one sees the following.

On the Gold (GC) Brands worksheet for the flagship GC 100 oz contract, we now find that:

- 51 LBMA approved gold refineries have been added to the eligible brand list for the COMEX 100 (GC 100) gold futures contract. These 51 additional refinery brands are listed directly under the existing refiner list with a subheading of “(Added as of 27 July, 2020)” There were 69 brands on this list prior to 27 July. There are now 120 current brands on the GC 100 gold list. 69 + 51 = 120

- Of the 51 refiner brands, the top three countries represented are 12 refineries are from China, 10 from Japan, and 7 from Russia.

- An additional 111 gold bars brands from the LBMA ‘former’ Good Delivery List for gold have been added to the Gold (GC) brands tab as a separate list beside and to the right of the first list. In total 162 LBMA approved gold bar brands have been added to the COMEX approved gold bar brand list.

- Overall, there are now 231 brands on the COMEX approved gold bar brand list. That’s a 235% increase in the number of gold bar brands that are now on the GC 100 list compared to the 69 that were listed before the 27 July change.

Note that the current LBMA Good Delivery List for gold lists 71 refiner gold bar brands. The former LBMA Good Delivery List lists 115 refiner bar brands.

Silver Panic – Under the Radar

An even bigger bombshell arguably is that the CME and LBMA’s actions are now signaling panic about future physical silver delivery. Turning to the Silver Futures (SI) Brands worksheet, we find that on 27 July, the COMEX SI eligible silver refiner brand list, which up until then had listed 75 silver bar refiner brands, has also been hugely expanded.

On the Silver (SI) Brands worksheet tab of the same service providers XLS, we now find that:

- 65 LBMA approved silver refineries have been added to the eligible brand list for the COMEX SI (5000 oz) silver futures contract. These 65 additional refinery brands are listed directly under the existing refiner list with a subheading of “(Added as of 27 July, 2020)”

- There were 75 brands on this list prior to 27 July. There are now 140 current brands on the current SI silver refiner list. 75 + 65 = 140

- Of the 65 silver refiner brands added, the top three countries represented are 26 silver refineries from China, 11 from Japan, and 5 from Russia.

- An additional 40 silver bars brands from the LBMA ‘former’ Good Delivery List for silver have also been added to the Silver (SI) Brands tab as a separate list beside and to the right of the first list.

In total, 105 LBMA silver bar brands were added by COMEX on 27 July, taking the COMEX SI silver list to a total of 180 eligible silver bar brands. That’s a 140% increase in the number of silver bar brands compared to prior to 27 July, or in other words, 2.4 times more brands on the SI silver brand list than there had been prior to 27 July.

Note that the current LBMA Good Delivery List for Silver lists 84 refiner silver bar brands. The former LBMA Good Delivery List lists 82 refiner bar brands.

In summary, on 27 July, across the GC 100 contract and SI contract refiner lists, COMEX stealthily added 267 LBMA gold and silver refiner brands to the COMEX approved refiner lists using one small paragraph in an obscure hidden filing on its website. Critically, these changes were approved and ‘effective immediately’ on 27 July, the same day that they were announced. How’s that for covert behind the scenes dealings? With COMEX and LBMA hoping no one would notice.

The Old Normal

Previously, CME always announced each addition or removal of an approved gold or silver refiner brand separately in a distinct filing, for example, when the ABC Refinery (Australia) brand was added to the GC 100 gold approved refiner list on 5 June this year, or when, CME removed the approval of the gold bar brand of the North Korean central bank from the 4GC approved brand list on July 23 July (the Pyongyang gold bar brand had slipped through the cracks in COMEX’s rush to blanket list all former LBMA brands, this obviously did not go down well in New York, or perhaps in Washington DC).

Another example is the tragicomic addition and subsequent removal of Dubai DMCC’s Al Ethihad Refinery from the GC 100 gold brand list in July, approved and added by CME on 9 July, and then mysteriously removed by CME three weeks later on 31 July without explanation, but market rumor has it that Al Ethihad was kicked off the COMEX gold refiner list due to intervention by JP Morgan.

In contrast to all of these individual additions and deletions, now COMEX has added 267 gold and silver bar brands to its approved in one fell swoop. Nothing like this has ever happened before. So why now?

New Normal – We’re Going to Need A Bigger List

Traditionally, the COMEX futures markets in New York has been known around the world as a venue which trades gargantuan volumes of futures contracts (GC 100 oz gold and SI 5000 silver) that while deliverable, were rarely delivered. This therefore gave the COMEX the reputation of being a relative backwater for physical gold and silver activity. But with contract holders now demanding physical delivery of both gold and silver, that is increasingly less the case.

Since late March 2020, a net 879 tonnes of gold has arrived into COMEX approved New York vaults, with total gold stocks more than quadrupling from 271 tonnes to 1151 tonnes. Of these net additions, 461 tonnes have ended up as registered gold inventories, the eligible gold inventories have swelled by other 418 tonnes.

Since April inclusive, a massive 155,430 GC 100 gold contracts have been delivered (warrants changing hands), predominantly across the April, June and August contracts, representing 483 tonnes of gold.

Silver net inflows into COMEX vaults since 23 March have been more subdued, both in terms of size and a percentage of existing stocks, with the net additions totaling about 16.8 million ozs of silver, which has raised total COMEX silver holdings from 323.4 million ozs to the current 340.3 million ozs. But within that, there has been a marked increase in registered silver stocks from less than 3000 tonnes to currently over 4000 tonnes.

Silver SI 5000 oz contracts moving to delivery have also increased massively in the last few months, with vault warrants 9,044 contracts changing hands in May and 17,294 contracts in July. Between April and August to date, 28989 SI contracts, each for 5000 oz of silver have gone to warrant delivery, that’s 144.95 million ozs of silver, or 4500 tonnes. The next active delivery month in SI silver is September, followed by December. Both months currently have huge Open Interest, 59,000 contracts and 120,000 contracts respectively, far larger than available COMEX silver stocks.

Kilo Bars Do Not Explain the Changes

The billion dollar question now is why, on 27 July, did CME blanketly and surreptitiously add 162 LBMA gold bar brands to the COMEX GC 100 eligible gold refiner list and 105 LBMA silver bar brands to the COMEX SI 5000 eligible silver refiner list?

For the GC 100 gold futures contract, the deliverable unit of the 100 oz gold bar is not only not common, it is not usually a gold bar size produced by gold refineries around the world. While the 1 kilobar unit is popular, many of the gold refinery brands added to the GC 100 approved list on 27 July, not to mention those on the former gold LBMA Good Delivery gold list, don’t and never did produce kilo gold bars, let alone 100 oz gold bars.