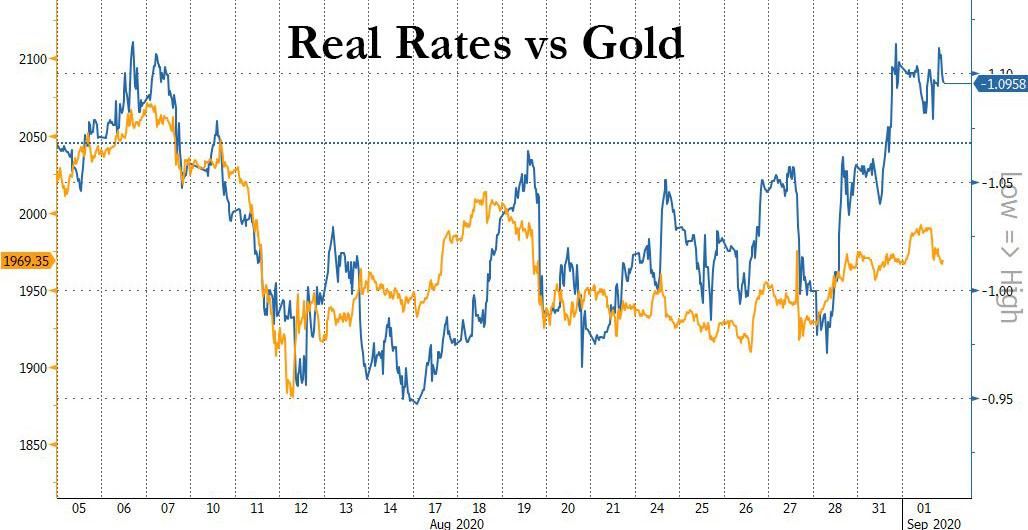

GOLD:$1972.70 UP $7.10 The quote is London spot price

Silver:$28.28 UP$0.09 London spot price ( cash market)

DONATE

Closing access prices: London spot

i)Gold : $1971.00 LONDON SPOT 4:30 pm

ii)SILVER: $28.15//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

SEPT GOLD: $1968.40 CLOSE 1::30 PM SPREAD SPOT/FUTURE AUG (BACKWARD $4,30//) SCARCITY//

OCT GOLD: $1971.00 CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: : $1.70//BACKWARD//

DEC. GOLD $1978.50 CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $5.80/ CONTANGO ($6.20 BELOW NORMAL CONTANGO)

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $28.50…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : ( 13 cents contango//12 CENTS ABOVE NORMAL contango)

SILVER DECEMBER CLOSE: $28.64 1:30 PM SPREAD SPOT/FUTURE DEC. : 27 CENTS PER OZ CONTANGO ( 15 CENTS ABOVE NORMAL CONTANGO)

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today: 3/287

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,967.600000000 USD

INTENT DATE: 08/31/2020 DELIVERY DATE: 09/02/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

118 H MACQUARIE FUT 3

355 C CREDIT SUISSE 7

435 H SCOTIA CAPITAL 207

624 C BOFA SECURITIES 24

657 C MORGAN STANLEY 56

657 H MORGAN STANLEY 83

661 C JP MORGAN 3

690 C ABN AMRO 1

709 C BARCLAYS 134

709 H BARCLAYS 18

732 C RBC CAP MARKETS 3 5

737 C ADVANTAGE 3 3

800 C MAREX SPEC 16 6

905 C ADM 2

____________________________________________________________________________________________

TOTAL: 287 287

MONTH TO DATE: 2,215

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 287 NOTICE(S) FOR 28700 OZ (0.8926 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 2215 NOTICES FOR 221,500 OZ (6.889 tonnes)

SILVER

708 NOTICE(S) FILED TODAY FOR 3,540,000 OZ/

total number of notices filed so far this month: 7253 for 36.265 MILLION oz

BITCOIN MORNING QUOTE $11,886 UP 241

BITCOIN AFTERNOON QUOTE.: $11,957 UP 308

GLD AND SLV INVENTORIES:

WITH GOLD UP $7.10 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

GLD: 1,251.50 TONNES OF GOLD//

WITH SILVER UP 9 CENTS TODAY: AND WITH NO SILVER AROUND:

NO CHANGE IN INVENTORY AT THE SLV///

RESTING SLV INVENTORY TONIGHT:

SLV: 574.053 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A STRONG SIZED 2825 CONTRACTS FROM 168,368 DOWN TO 165,543, AND FURTHER FROM OUR NEW RECORD OF 244,710, (FEB 25/2020. THE LOSS IN OI OCCURRED DESPITE OUR STRONG 80 CENT RISE IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE ENTIRE LOSS IN COMEX OI IS PRIMARILY DUE TO OUR MASSIVE BANKER SILVER SHORT COVERING.. COUPLED AGAINST A STRONG EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, WITH A POWERFUL INITIAL STANDING IN SILVER AT THE COMEX FOR SEPT.. WE HAD A CONSIDERABLE NET LOSS IN OUR TWO EXCHANGES OF 1636 CONTRACTS, WITH THE MAJORITY OF THE COMEX LOSS DUE TO OUR BANKER SHORT COVERING… (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A STRONG AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: SEP 0; DEC: 1189, MARCH 0 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1189 CONTRACTS. WITH THE TRANSFER OF 1189 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1189 EFP CONTRACTS TRANSLATES INTO 5.945 MILLION OZ ACCOMPANYING:

1.THE 80 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

86.470 MILLION OZ FINAL STANDING IN JULY.

6.475 MILLION OZ FINAL STANDING IN AUGUST

52.600 MILLION OZ INITIALLY STANDING IN SEPT

MONDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 80 CENTS) ).. AND, OUR OFFICIAL SECTOR/BANKERS WERE BASICALLY UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS AS FEAR STRUCK AS BANKERS AS THE RATS ARE STARTING TO FLEE A SINKING SHIP. WE ALSO HAD ii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A HUGE INITIAL SILVER OZ STANDING FOR SEPTEMBER, AND 3) ZERO LONG LIQUIDATION. YOU CAN BET THE FARM THAT OUR BANKERS ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER..

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

SEPT.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF SEPT:

1189 CONTRACTS (FOR 1 TRADING DAY(S) TOTAL 1189 CONTRACTS) OR 5.945 MILLION OZ: (AVERAGE PER DAY: 1189 CONTRACTS OR 5.945 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 5.945 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 0.849% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,392.03 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EFP 71.15 MILLION OZ.

JULY EFP 133.95 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

AUGUST EFP 127.46 MILLION OZ (EXCHANGE FOR PHYSICALS STARTING TO DECREASE AGAIN)

SEPT EFP 5.945 MILLION OZ

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2,825, DESPITE OUR STRONG 80 CENT RISE IN SILVER PRICING AT THE COMEX ///MONDAY AS ONE A NET BASIS, NOBODY REALLY LEFT THE SILVER ARENA..AS ALL OF THE LOSS WAS DUE TO BANKER SHORT COVERING…THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1189 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE LOST A STRONG SIZED 1457 OI CONTRACTS ON THE TWO EXCHANGES (DESPITE OUR STRONG 80 CENT GAIN IN PRICE)//AND AS MENTIONED ABOVE, ALL OF THE COMEX LOSS WAS DUE TO BANKER SHORT COVERING.

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 1189 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A CONSIDERABLE SIZED DECREASE OF 2,646 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH OUR 80 CENT RISE IN PRICE OF SILVER/AND A CLOSING PRICE OF $28.29 // MONDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.843 BILLION OZ TO BE EXACT or 120% of annual global silver production (ex Russia & ex China).

FOR THE NEW AUGUST DELIVERY MONTH/ THEY FILED AT THE COMEX: 708 NOTICE(S) FOR 3,540,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 WAS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 86.470 million oz//AUGUST 6.475 MILLION OZ//SEPT. 52.600 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 3806 CONTRACTS TO 544,006 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE FAIR SIZED LOSS IN COMEX OI OCCURRED DESPITE OUR GOOD RISE IN PRICE OF $5.90 /// COMEX GOLD TRADING// MONDAY//WE HAD HUMONGOUS BANKER SHORT COVERING, A STRONG ADVANCE IN STANDING AT THE GOLD COMEX FOR SEPT, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR GOOD GAIN IN PRICE OF $5.90.

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 134// (2400 OZ WAS DELIVERED ON FRIDAY FROM THE ENHANCED GOLD INVENTORY)…

WE LOST A STRONG SIZED 2926 CONTRACTS (9.101 TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 880 CONTRACTS:

CONTRACT .; AUG 0 AND OCT: 0 DEC: 880; JUNE: 0 ALL OTHER MONTHS ZERO//TOTAL: 880. The NEW COMEX OI for the gold complex rests at 544,006. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2926 CONTRACTS: 3806 CONTRACTS DECREASED AT THE COMEX AND 880 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 2926 CONTRACTS OR 9.101 TONNES. MONDAY, WE HAD A GOOD GAIN OF $5.90 IN GOLD TRADING……

AND WITH THAT GAIN IN PRICE, WE HAD A STRONG SIZED LOSS IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 9.101 TONNES!!!!!! THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $5.90). WE HAD HUMONGOUS BANKER SHORT COVERING OPERATION WITH SMALL ISSUANCE IN EXCHANGES FOR PHYSICAL. THEY BANKERS COULD NOT FLEECE ANY OF OUR SPECULATOR LONGS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (880) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (3806 OI): TOTAL LOSS IN THE TWO EXCHANGES: 2926 CONTRACTS. WE NO DOUBT HAD 1 )HUMONGOUS BANKER SHORT COVERING ,2.)A STRONG ADVANCE IN STANDING AT THE GOLD COMEX FOR THE FRONT SEPT. MONTH, 3) ZERO NET LONG LIQUIDATION; 4) FAIR COMEX OI GAINAND 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL AND …ALL OF THIS WAS COUPLED WITH OUR GOOD GAIN IN GOLD PRICE TRADING//MONDAY//$5.90.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

EXCHANGE FOR PHYSICALS//OUTLINE

SPREADING OPERATIONS/NOW SWITCHING TO GOLD (WE SWITCH OVER TO SILVER ON OCT 1)

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN GOLD AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT. HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCT FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

SEPT.

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES: 2.737 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 2.737/3550 x 100% TONNES =0.07% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3,413.56 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 313.09 TONNES ..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

AUGUST TOTAL EFP ISSUANCE; 150.78 TONNES FINAL (AGAIN: RETREATING IN NUMBERS)

SEPT TOTAL EFP ISSUANCE: 2.737 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

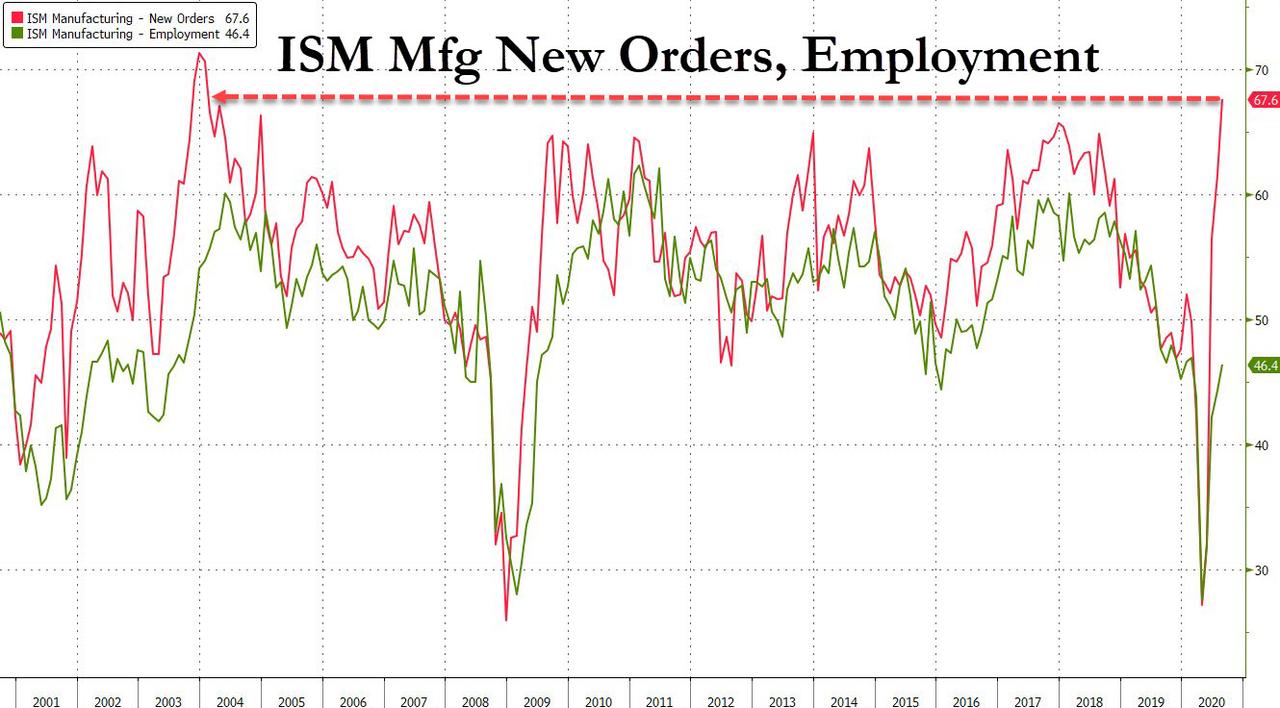

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 2825 CONTRACTS FROM 168,368, DOWN TO 165,543 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE CONSIDERABLE SIZED LOSS IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) HUMONGOUS BANKER SHORT COVERING , 2) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A HUGE INITIAL STANDING FOR SILVER AT THE COMEX FOR SEPT., AND 4) ZERO LONG LIQUIDATION,

EFP ISSUANCE 1189 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT: 0 AND DEC. 1189 AND MARCH: 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1189 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2825 CONTRACTS TO THE 1189 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG SIZED LOSS OF 1636 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 8.180 MILLION OZ, OCCURRED DESPITE OUR STRONG 80 CENT GAIN IN PRICE///

HOWEVER IT MUST BE POINTED OUT THAT THE ENTIRE LOSS IN OI ON THE COMEX WAS DUE TO HUMONGOUS BANKER SHORT COVERING.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 14.93 POINTS OR 0.44% //Hang Sang CLOSED UP 7.80 POINTS OR 0.03% /The Nikkei closed DOWN 1.69 POINTS OR 0.01%//Australia’s all ordinaires CLOSED DOWN 1.64%

/Chinese yuan (ONSHORE) closed UP at 6.8191 /Oil UP TO 43.06 dollars per barrel for WTI and 45.87 for Brent. Stocks in Europe OPENED MOSTLY GREEN EXCEPT LONDON// ONSHORE YUAN CLOSED UP // LAST AT 6.8191 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8213 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total withdrawals; nil oz

We had 0 kilobar transactions +

ADJUSTMENTS: 2 //

dealer to customer

i) Out of BRINKS 1736.154 oz

i

customer to dealer:

Scotia: 20,993.880 oz

The front month of SEPT registered a total of 1182 contracts for a loss of 1888 contracts. We had 1928 notices filed on Monday, so we gained 40 contracts or an additional 4,000 oz will stand for delivery in this non active month of Sept.

Oct LOST 636 contracts DOWN to 62,836. November gained its first contract to stand at l.

The big December contract lost 1202 contracts down to 402,774 contracts…(it is here where we have a huge amount of banker short accompanied by a strong newbie longs entering the gold arena. Bankers leaving far outshined newbies coming in.

We had 287 notices filed today for 28700 oz

To calculate the INITIAL total number of gold ounces standing for the SEPT /2020. contract month, we take the total number of notices filed so far for the month (2215) x 100 oz , to which we add the difference between the open interest for the front month of SEPT (1182 CONTRACTS ) minus the number of notices served upon today (287 x 100 oz per contract) equals 311,000 OZ OR 9.673 TONNES) the number of ounces standing in this active month of JUNE

thus the INITIAL standings for gold for the SEPT/2020 contract month:

No of notices filed so far (2215, x 100 oz + (1182 OI) for the front month minus the number of notices served upon today (287) x 100 oz which equals 311,000 oz standing OR 9.673 TONNES in this active delivery month. This is a HUGE amount for gold standing for a SEPT delivery month (a NON active delivery month).

THE NAME OF THE GAME TODAY IS BANKER SHORT COVERING AS FINALLY FEAR BECAME THEIR CENTRAL FOCUS. YOU CAN VISUALIZE THIS LAST NIGHT AND TODAY WITH GOLD’S STRONG ADVANCE IN TUESDAY’S COMEX.

NEW PLEDGED GOLD: BRINKS

144,088.952 oz NOW PLEDGED JAN 21.2020/HSBC 5.4807 TONNES

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

261,955.892 oz (some deleted august 3) JPM 8.1479 TONNES

611,401.341 oz pledged June 12/2020 Brinks/ july 2/july 21 19.017 tonnes

51,084.609 oz Pledged August 21/regular account 1.588 tonnes jpm

total pledged gold: 1,111,079.092 oz 34.55 tonnes

total registered, pledged and eligible (customer) gold; 37,144,285.895 oz 1,155.34 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1029,00 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

END

And now for the wild silver comex results

INITIAL STANDINGS

SEPT. SILVER COMEX CONTRACT MONTH//INITIAL STANDINGS

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

661,157.680 oz

CNT

Delaware

HSBC

Manfra

|

| Deposits to the Dealer Inventory |

152,099.600 oz

Manfra

|

| Deposits to the Customer Inventory |

1,007,024.353 oz

CNT

Delaware

|

| No of oz served today (contracts) |

708

CONTRACT(S)

(3,540,000 OZ)

|

| No of oz to be served (notices) |

24 contracts

120,000 oz)

|

| Total monthly oz silver served (contracts) | 7253 contracts

36,265,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

total dealer deposits: 152,099.600 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 2 deposits into the customer account

i)into JPMorgan: nil

ii) Into CNT: 933,546.800 oz

iii) into Delaware: 73,477.553

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 167.320 million oz of total silver inventory or 48.42% of all official comex silver. (167.320 million/345.468 million

total customer deposits today: 1,007,024.353 oz

we had 4 withdrawals:

i) Out of Delaware; 2910.600 oz

ii) Out of CNT; 349,963.300 oz

iii) out of HSBC 293,113.200 oz

iv) Out of Manfra; 15,170.000 oz

total withdrawals; 661,157.680 oz

We had 0 adjustments first two: dealer to customer

l

Total dealer(registered) silver: 138.250 million oz

total registered and eligible silver: 345.468 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

the front month of SEPTEMBER registered an open interest of 3978 contracts thus losing 6570 contracts. We had 6545 notices filed on Monday so we LOST A TINY 25 contracts or an additional 125,000 oz will NOT stand in this active delivery month of September as they morphed into London based forwards and received a fiat bonus for their efforts. However this time our London boys are ready to exercise these EFP’s and they will turn them into real physical metal as we now have a full frontal attack on both of our two precious metals.

Oct saw another gain of 22 contracts to stand at 694.November gained its first initial contract to stand at 1,

The big December contract month saw its OI rise by good 3160 contracts up to 144,034

The total number of notices filed today for the SEPT 2020. contract month is represented by 708 contract(s) FOR 3,540,000, oz

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 7253 x 5,000 oz = 36,7265,000 oz to which we add the difference between the open interest for the front month of SEPT(3978) and the number of notices served upon today 708 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the SEPT/2019 contract month: 7253 (notices served so far) x 5000 oz + OI for front month of AUGUST (3978)- number of notices served upon today (708) x 5000 oz of silver standing for the SEPT contract month.equals 52,600,000 oz. ..VERY STRONG FOR AN ACTIVE MONTH.

We lost a small 25 contracts or 125,000 oz.

TODAY’S ESTIMATED SILVER VOLUME : 49,950 CONTRACTS // volume fair

FOR YESTERDAY: 98,831. ,CONFIRMED VOLUME//volume large

YESTERDAY’S CONFIRMED VOLUME OF 98,831 CONTRACTS EQUATES to 0.494 billion OZ 49.4% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 2.43% ((SEPT 1/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.65% to NAV: (SEPT 1/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/2.43%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 20.93 TRADING 20.60///NEGATIVE 1.59

END

And now the Gold inventory at the GLD/

SEPT 1/WITH GOLD UP $7.10 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1251.50 TONNES

AUGUST 31//WITH GOLD UP $5.90 TODAY/WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD..//INVENTORY RESTS AT 1251.50 TONNES/

AUGUST 28/WITH GOLD UP $38.20 TODAY, WE SURPRISINGLY HAD A .59 TONNE WITHDRAWAL//INVENTORY RESTS AT 1251.50 TONNES

AUGUST 27/WITH GOLD DOWN 17.50 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 3.24 TONNES INTO THE GLD//INVENTORY REST AT 1252.09 TONNES

AUGUST 26/WITH GOLD UP $26.70 TODAY/ WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.53 TONNES FROM THE GLD//RESTS AT 1248.85 TONNES

AUGUST 25/WITH GOLD DOWN $14.60 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//RESTS AT 1252.38 TONNES

AUGUST 24//WITH GOLD DOWN $7.20 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1258.38 TONNES

AUGUST 21//WITH GOLD DOWN $.40 TODAY: WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1252.38 TONNES

AUGUST 20/WITH GOLD DOWN $23.45 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD: .//INVENTORY REST AT 1252.38 TONNES

AUGUST 19//WITH GOLD DOWN $39.65 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1252.38 TONNES

AUGUST 18/WITH GOLD UP $14.60 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 4.09 TONNES//GLD INVENTORY RESTS TONIGHT AT 1252.38 TONNES

AUGUST 17/WITH GOLD UP $46.30 TODAY: SURPRISINGLY WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 3.8 TONNES//INVENTORY RESTS AT 1248.29 TONNES

AUGUST 14/ WITH GOLD DOWN $19.45 TODAY: SURPRISINGLY, WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.46 TONNES/INVENTORY RESTS AT 1252.63 TONNES.

AUGUST 13/WITH GOLD UP $23.15 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY: SURPRISINGLY A PAPER WITHDRAWAL OF 7.30 TONNES/INVENTORY RESTS AT 1250.63 TONNES

AUGUST 12/ WITH GOLD UP $1.00 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 4.19 TONNES//INVENTORY RESTS AT 1257.93 TONNES

AUGUST 11//WITH GOLD DOWN $92.40 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1262.12 TONNES.

AUGUST 10/WITH GOLD UP $11.35 TODAY, WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.84 TONNES//INVENTORY RESTS AT 1262.12 TONNES

AUGUST 7/WITH GOLD DOWN $38.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1267.96 TONNES

AUGUST 6/WITH GOLD UP $20.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A PAPER DEPOSIT OF 10.23 TONNES INTO THE GLD/INVENTORY RESTS AT 1267.96 TONNES//

AUGUST 5/WITH GOLD UP $ 33.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 9.35 TONNES INTO THE GLD//INVENTORY RESTS AT 1257.73 TONNES

AUGUST 4//WITH GOLD UP $31.75 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 6.48 TONNES/GLD INVENTORY RESTS AT 1248.38 TONNES

AUGUST 3/WITH GOLD UP $2.20 TODAY, WE HAVE NO CHANGES IN THE GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241,96 TONNES

JULY 31/WITH GOLD UP $17.90 TODAY/WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1241.96 TONNES.

JULY 30/WITH GOLD DOWN $10.00 TODAY, WE HAVE ANOTHER SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES//INVENTORY RESTS AT 1241.96 TONNES.

JULY 29//WITH GOLD UP $12.45 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 8.47 TONNES/INVENTORY RESTS AT 1243.12 TONNES

JULY 28///WITH GOLD UP $13.25 TODAY, WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A HUGE DEPOSIT OF 5.84 TONNES/INVENTORY RESTS AT 1234.65

JULY 27//WITH GOLD UP $35.30 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF XXX TONNES/INVENTORY RESTS AT 1228.81 TONNES

JULY 24/WITH GOLD UP $8.80 TODAY: WE HAVE ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.80 TONNES//INVENTORY RESTS AT 1228.81 TONNES

JULY 23/WITH GOLD UP $24.90 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 7.26 TONNES/INVENTORY RESTS AT 1225.01 TONNES

JULY 22/WITH GOLD UP $22.00 TODAY: WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 7.89 TONNES/INVENTORY RESTS AT 1219.75 TONNES

JULY 21//WITH GOLD UP $26.00 TODAY, WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.97 TONNES INTO THE GLD// INVENTORY RESTS AT 1211.86 TONNES

JULY 20/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1206.89 TONNES

JULY 17/WITH GOLD UP $7.70 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1206.89 TONNES

JULY 16/WITH GOLD DOWN $9.80 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD: INVENTORY RESTS AT 1206.89 TONNES

JULY 15//WITH GOLD UP $1.55 TODAY/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 2.96 TONNES INTO THE GLD///INVENTORY RESTS AT 1206.89 TONNES

JULY 14//WITH GOLD DOWN $1.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 3.51 TONNES/INVENTORY RESTS AT 1203.97 TONNES

JULY 13//WITH GOLD UP $12.50 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1200.46 TONNES

JULY 10/WITH GOLD DOWN $.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD//A STRANGE WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1200.82 TONNES

JULY 9//WITH GOLD DOWN $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OX 3.21 TONNES INTO THE GLD//INVENTORY RESTS AT 1202.57 TONNES

JULY 8/WITH GOLD UP $13.75 TODAY; A BIG CHANGE IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 7.89 TONNES INTO THE GLD//INVENTORY RESTS AT 1199.36 TONNES

JULY 7/WITH GOLD UP $12.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1191.47 TONNES

JULY 6/WITH GOLD UP $6.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1191.47 TONNES

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

SEPT 1/ GLD INVENTORY 1251.50 tonnes*

LAST; 893 TRADING DAYS: +312.00 NET TONNES HAVE BEEN ADDED THE GLD

LAST 793 TRADING DAYS://+490.53 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 1//WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 31/WITH SILVER UP 80 CENTS TODAY: A HUGE CHANGE IN THE SLV//A DEPOSIT OF 2.982 MILLION OZ ENTERS THE SLV/INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 28/WITH SILVER UP 48 CENTS TODAY: A MASSIVE PAPER DEPOSIT OF 4.652 MILLION OZ ENTERS THE SLV//INVENTORY RESTS AT 571.071 MILLION OZ

AUGUST 27/WITH SILVER DOWN 28 CENTS TODAY// NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.419 MILLION OZ

AUGUST 26//WITH SILVER UP $1.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.65 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 566.419 MILLION OZ..

AUGUST 25/WITH SILVER DOWN 21 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.607 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 571.074 MILLION OZ//

AUGUST 24//WITH SILVER DOWN 18 CENTS TODAY: WE HAD A NO CHANGES//INVENTORY RESTS AT 573.843 MILLION OZ//

AUGUST 21//WITH SILVER DOWN 30 CENTS TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.838 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 573.843 MILLION OZ..

AUGUST 20/WITH SILVER DOWN $.26 TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 3.724 MILLION OZ FROM THE SLV..//INVENTORY REST AT 572.843 MILLION OZ

AUGUST 18/WITH SILVER UP $.44 TODAY: WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.514 MILLION OZ//THE SLV INVENTORY RESTS TONIGHT AT 576.567 MILLION OZ//

AUGUST 17/WITH SILVER UP $1.27 TODAY: WE HAD NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 14/WITH SILVER DOWN $1.31 TODAY, WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.984 MILLION OZ// //INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 13//WITH SILVER UP $1.76 TODAY: WE HAVE TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A PAPER DEPOSIT OF 2.421 MILLION OZ INTO THE SLV AT 2 PM AND ANOTHER DEPOSIT OF 6.984 MILLION OZ AT 5 20 PM/INVENTORY RESTS AT 581.037 MILLION OZ//

AUGUST 12/WITH SILVER DOWN 40 CENTS TODAY: WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF XX MILLION OZ//INVENTORY RESTS AT XX MILLION OZ/

AUGUST 11/WITH SILVER DOWN $3.25 CENTS, WE HAVE ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.41 MILLION OZ//INVENTORY RESTS AT 571.632 MILLION OZ//

AUGUST 10/WITH SILVER UP 1.89 TODAY, WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 3.538 MILLION OZ/INVENTORY RESTS AT 569.491 MILLION OZ//

AUGUST 7/WITH SILVER DOWN 69 CENTS TODAY: WE HAVE ANOTHER HUGE CHANGE IN SILVER INVENTORY: A DEPOSIT OF 0.465 MILLION OZ/INVENTORY RESTS AT 573.029 MILLION OZ.

AUGUST 6/WITH SILVER UP $1.52 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 572.564 MILLION OZ///

AUGUST 5/WITH SILVER UP $1.03 TODAY, WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A MONSTROUS DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 572.564 MILLION OZ//

AUGUST 4/WITH SILVER UP $1.45 TODAY, WE HAVE NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 367.161 MILLION OZ//

AUGUST 3/WITH SILVER UP 23 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//SURPRISINGLY ANOTHER WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 367.161 MILLION OZ//

JULY 31/WITH SILVER UP 82 CENTS TODAY: WE HAVE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: SURPRISINGLY A HUGE WITHDRAWAL OF 3.26 MILLION OZ//INVENTORY RESTS AT 368.092 MILLION OZ//

JULY 30//WITH SILVER DOWN 97 CENTS TODAY: WE HAVE A SMALL CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 0.931 MILLION OZ//INVENTORY RESTS AT 571.352 MILLION OZ//

JULY 29/WITH SILVER UP 7 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY//A DEPOSIT OF 5.984 MILLION OZ//INVENTORY RESTS AT 572.283 MILLION OZ//

JULY 28 WITH SILVER DOWN 14 CENTS TODAY, WE HAD A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 7.52 MILLION OZ//INVENTORY RESTS AT 566.299 MILLION OZ//

JULY 27/WITH SILVER UP $2.67 TODAY, WE HAD NO CHANGES IN SILVER INVENTORY: A DEPOSIT OF XX MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ//

JULY 24/WITH SILVER DOWN $0.12 TODAY: NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 558.779 MILLION OZ/

JULY 23/WITH SILVER UP $.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A HUMONGOUS PAPER DEPOSIT OF 9.594 MILLION OZ//INVENTORY RESTS AT 558.779 MILLION OZ///

JULY 22/WITH SILVER UP $1.54 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A HUMONGOUS PAPER DEPOSIT OF 7.218 MILLION OZ//INVENTORY RESTS AT 549.185 MILLION OZ/

JULY 21/WITH SILVER UP $1.38 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUMONGOUS PAPER DEPOSIT OF 15.368 MILLION OZ////INVENTORY RESTS AT 541.967 MILLION OZ//

JULY 20/WITH SILVER UP 40 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 3.819 MILLION OZ ‘ENTERED” THE SLV..INVENTORY RESTS AT 526.599 MILLION OZ/

JULY 17/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 1.583 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 522.780 MILLION OZ//

JULY 16//WITH SILVER DOWN 14 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ//INVENTORY RESTS AT 521.197 MILLION OZ..

JULY 15.WITH SILVER UP 21 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.956 MILLION OZ//INVENTORY RESTS AT 516.074 MILLION OZ//

JULY 14/WITH SILVER DOWN 21 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 514.118 MILLION OZ//

JULY 13//WITH SILVER UP 67 CENTS TODAY: A HUGE CHANGE IN SILVER: A WITHDRAWAL OF 1.677 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 514.118 MILLION OZ//

JULY 10/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 4.844 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 515.795 MILLION OZ

WHAT A FRAUD!!

JULY 9/WITH SILVER DOWN 8 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 8.198 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 510.951 MILLION OZ/

JULY 8/WITH SILVER UP 37 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.118 MILLION OZ FROM THE SLV//VERY SURPRISING.//INVENTORY RESTS AT 502.753 MILLION OZ//

JULY 7/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:/INVENTORY RESTS AT 503.871 MILLION OZ///

JULY 6//WITH SILVER UP 24 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.863 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 503.871 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

SEPT 1.2020:

SLV INVENTORY RESTS TONIGHT AT

574.053 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

Interesting: Refinitiv Lipper is reporting that stocks have been having a negative outflow of cash. If the stock market is rising how can this be possible? Where is the money going? Pam and Russ discuss this

(Pam and Russ Martens/Wall Street on Parade/Gata)

Pam and Russ Martens: How is stock market rising as investors stampede out?

Submitted by cpowell on Mon, 2020-08-31 15:18. Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Monday, August 31, 2020

The S&P 500 stock index set a new record high on Friday, closing at 3508.01 – the first time it has ever closed above 3500. In fact, the S&P 500 set a record high close every single day last week. …

Refinitiv Lipper has been reporting fund flows into and out of the stock market for the past 18 years. According to Refinitiv Lipper, for the week ending Wednesday, August 26, stock (aka equity) mutual funds and stock ETFs had a combined negative outflow of -$7.8 billion. For the week ending Wednesday, August 19, stock mutual funds and stock ETFs had a negative outflow of -$6.6 billion.

…

Put the two weeks together and you have investors yanking a net $14.4 billion out of stock funds. Where was the money going? For the most part, it was going into taxable bond funds.

So exactly how can a stock market index be setting new record highs when investors are cashing out and the majority of the stock components in the S&P 500 are far from their record highs?

The S&P 500 is made up of approximately 500 companies at any one time. The index is market-capitalization weighted, a system that divides the market cap of a company by the index’s total market capitalization to determine its influence in the index.

When you have six companies that have been dramatically outperforming other stocks this year, and just five of them — Alphabet (parent of Google), Amazon, Apple, Facebook, and Microsoft — make up more than 20 percent of the S&P 500’s total market capitalization, you can get an aberration in the pricing of the broader index.

To put it simply, were it not for these six stocks, the whole S&P 500 index would be negative for the year. DoubleLine’s Jeffrey Gundlach, a veteran market watcher, calls this “classic bear-market-rally activity.”

It is also known as “distribution” on Wall Street. That’s when the little guy is seduced into the stock market on the illusion that it is rocketing to one all-time high after another. This gives the knowledgeable insiders who want out the necessary dumb money on which to dump their shares. …

… For the remainder of the report:

https://wallstreetonparade.com/2020/08/investors-have-stampeded-out-of-s…

END

Two smart gold bugs talking about our precious metal: Ned Naylor Leyland interviewed by Ronan Manly

(Bullionstar)

Gold fund manager Ned Naylor-Leyland interviewed by Bullion Star’s Ronan Manly

Submitted by cpowell on Mon, 2020-08-31 15:46. Section: Daily Dispatches

11:45a ET Monday, August 31, 2020

Dear Friend of GATA and Gold:

Bullion Star gold researcher Ronan Manly last week interviewed gold fund manager Ned Naylor-Leyland, discussing prospects for the monetary metals and the possibility of structural changes in the world financial system. The interview is 40 minutes long and can be seen at YouTube here:

https://www.youtube.com/watch?v=oCos4vJ5794

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

He is right about New York..but not London. With the new physical London LME gold/silver exchange, that will become the premier gold trading vehicle in the world and it will all be physical.

(Keller/GATA)

Gold refining veteran dares to say it: ‘GATA has it right’

Submitted by cpowell on Mon, 2020-08-31 16:20. Section: Daily Dispatches

12:21p ET Monday, August 31, 2020

Dear Friend of GATA and Gold:

Interviewed today by a consulting company in Singapore, a guy who has spent more than 30 years in the gold refining industry made an encouraging comment about GATA while admitting that it wouldn’t do him any good.

The comment was made by gold refinery designer and builder Corey Keller of Keller Gold Consulting in remarks to Southeast Asia Consulting Pte. Ltd.

…

Keller was asked: “Are you seeing any developments in the industry that you think are worth discussing?”

He replied: “Absolutely! But like most people in this industry, we are demonized by old-school traditions, institutions, and general intimidation, so I will take a pass on that question. I will say: GATA has it right and the future of physical does not live in New York or London. I guess my job interview with JP Morgan will now be canceled.”

The interview is headlined “Corey Keller — the Canadian Guy Who Builds Gold Refineries” and it’s posted at Southeast Asia Consulting’s internet site here:

https://seasia-consulting.com/corey-keller-the-canadian-guy-that-builds-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Futures Coiled Near All Time High As Dollar Tumbles To Fresh Two Year Low

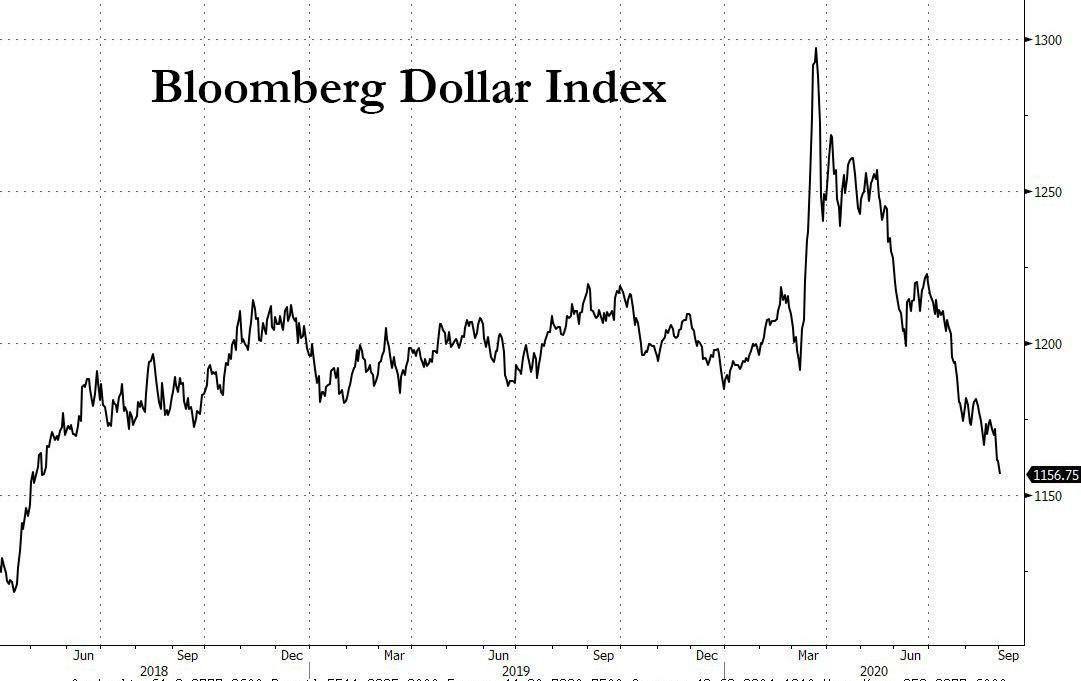

Stocks started September on a positive note on Tuesday, with S&P futures flat after fading earlier gains alongside shares in Europe as global indexes close to all-time highs as data in China and Europe showed manufacturing demand rebounding from coronavirus-induced lows. The dollar tumbled to a two-year low and the Yuan jumped after Chinese manufacturing data indicated that exports are underpinning a recovery.

The MSCI world equity index, which tracks shares in 49 countries, was close to recent highs, while the pan-European Stoxx 600 rose 0.3% in early trading with technology and basic resources climbing the most among sectors. France’s Cac 40 was up 0.2% and Germany’s Dax was up 0.7%. Britain’s FTSE 100 lagged, down 1.4%, hurt by a rising pound. Euro zone manufacturing activity grew last month, though factory managers remained wary about investing and hiring more workers. The French Mfg PMI beat expectations coming at 49.8, above the 49.0 consensus if down from 52.4, while Germany output grew at its fastest pace since February 2018, while in France it contracted.

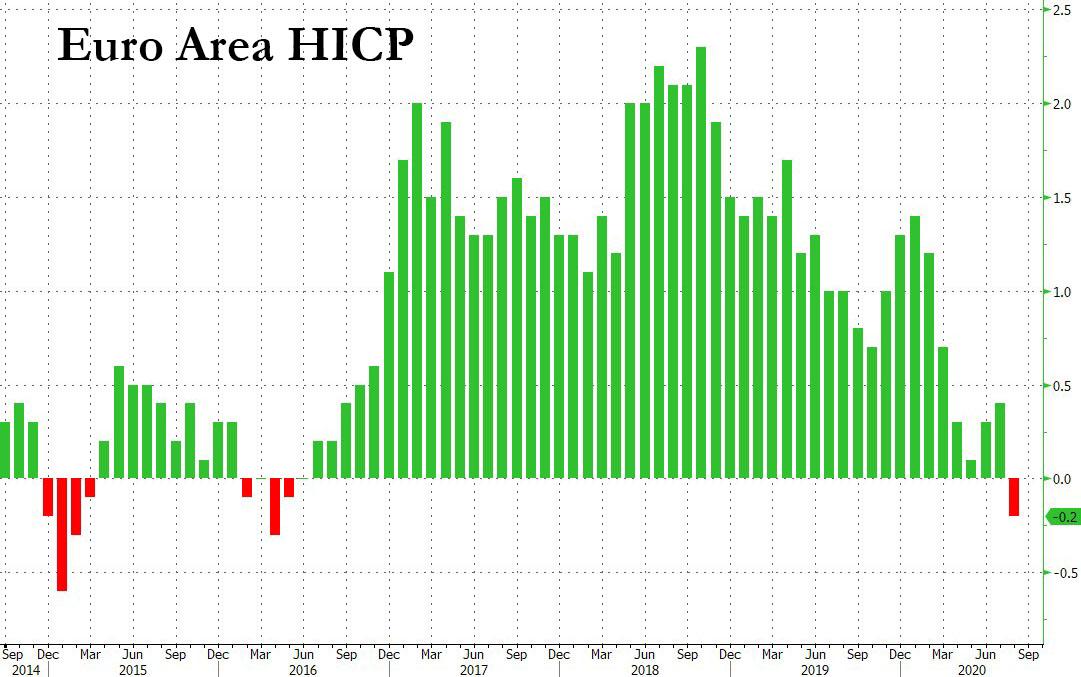

European stocks had opened even higher but pared gains after Germany cut its GDP forecast for 2021. Both shares and the euro, which rose to a two-year high of $1.19975 overnight in New York, were little changed after data showed annual euro zone inflation fell well below expectations in August, turning negative for the first time since May 2016, and a far cry from the European Central Bank’s inflation target of just under 2% (some have mused if the ECB will follow the Fed in announcing AIT as well).

“These numbers are clearly inconsistent with the ECB’s target,” said George Buckley, chief European economist at Nomura, who said the low reading will raise questions about whether the ECB should, like the Fed, adopt average inflation targeting. There were however credibility issues with such an approach, if the bank was unable to raise inflation to balance out the periods of lower inflation.

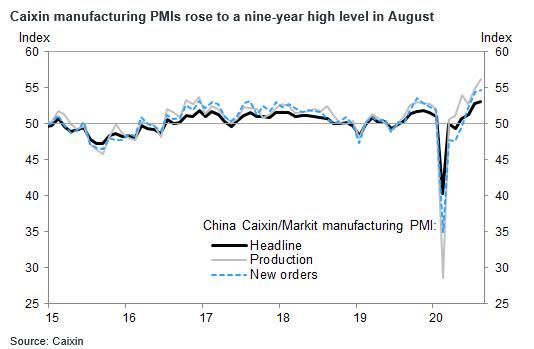

In Asia, China’s yuan touched the highest since 2019 and equities benchmarks in Hong Kong, Shanghai, Taipei and Seoul climbed. The Caixin PMI survey of China’s factory activity rose at the fastest pace in August since January 2011, helped by improving exports and continued domestic recovery, and boosted market sentiment overnight and into the European market open.

In rates, 10Y yields rose to 0.72% , up 2bps on the day with treasuries trading heavy led by the long end as month-end bid unwound. Yields were cheaper by up to 3bp at long end of the curve, steepening 2s10s, 5s30s by 1.6bp and 2.7bp; 10-year yields around 0.725%, cheaper by 1.8bp vs Monday’s close while gilts lag by ~1.5bp across the sector. Gilts underperformed, weighing on Treasuries along with a sharp selloff in Aussie bonds during Asia session. Core euro zone bond yields were up around 1 to 2 basis points, with the benchmark German 10-year yield at -0.387%.

In FX, the dollar continued to drop to a fresh two-year low and was down 0.4% at 91.826, dropping below 92 for the first time since May 2018 after a purchasing managers index for China beat estimates to raise optimism over Asia’s economic recovery.

“The weakness in the dollar is likely to continue and I suspect it will be substantially weaker from where it is against the euro by the end of the year,” said Savvas Savouri, chief economist at Toscafund Asset Management. “We’ve got the Fed chairman clearly telling us he wants inflation to ratchet upwards, and the only reliable way to achieve this is through the channel of a weaker currency.”

The euro climbed after German unemployment eased for a second month, though gains fell short of reaching $1.20 following the abovementioned deflationary print. At 1025 GMT, the single currency traded at $1.19835, up 0.4% since New York’s close as a dollar sell-off continued. Sterling rose to eight-month highs against the dollar, strengthening to as much as $1.3465 at 1028 GMT, and was up around 0.3% versus the euro.

In commodities, oil prices gained, reversing overnight losses. Brent climbed 56 cents to $45.84 a barrel while WTI futures rose 47 cents to $43.08 a barrel. Gold prices also rose, to their highest in two weeks.

Market Snapshot

- S&P 500 futures up 0.3% to 3,510.75

- STOXX Europe 600 up 0.2% to 367.28

- MXAP up 0.4% to 173.35

- MXAPJ up 0.5% to 574.03

- Nikkei down 0.01% to 23,138.07

- Topix down 0.2% to 1,615.81

- Hang Seng Index up 0.03% to 25,184.85

- Shanghai Composite up 0.4% to 3,410.61

- Sensex up 0.8% to 38,948.09

- Australia S&P/ASX 200 down 1.8% to 5,953.41

- Kospi up 1% to 2,349.55

- German 10Y yield rose 0.9 bps to -0.388%

- Euro up 0.3% to $1.1971

- Italian 10Y yield rose 5.0 bps to 0.968%

- Spanish 10Y yield rose 0.8 bps to 0.417%

- Brent futures up 1.2% to $45.82/bbl

- Gold spot up 1.1% to $1,989.57

- U.S. Dollar Index down 0.3% to 91.91

Top Overnight News from Bloomberg

- A private gauge of China’s factory activity grew at the fastest rate in August since January 2011, helped by exports and domestic recovery

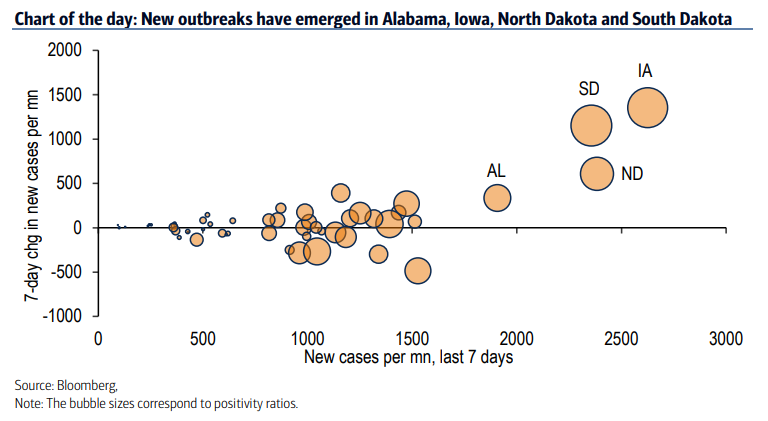

- Global trade is expected to rebound faster than after the 2008 financial crisis, according to Germany’s Kiel Institute for the World Economy. The number of coronavirus cases approaches 25.5 million worldwide, while deaths surpass 850,000

- The euro zone’s inflation rate went negative for the first time since 2016. Meanwhile Germany’s hit from the coronavirus will be less severe than feared, as the government’s efforts to kick start Europe’s largest economy show signs of bearing fruit

- A closely-watched euro-area interbank borrowing rate fell to a record, dragged down by all the money sloshing around the economy

A quick look at global markets courtesy of NewsSquawk:

Asian equities traded cautiously as the region took its cue from the losses seen across most global counterparts despite Wall St. notching its biggest monthly gain since April and its best August performance in more than 3 decades, while participants also digested encouraging Chinese Caixin Manufacturing PMI data. ASX 200 (-1.8%) underperformed and briefly wiped out all of the prior month’s gains on a collapse below the 6,000 level with the downturn led by hefty losses in tech and energy, while the detention of a Chinese-Australian television anchor further highlighted the souring bilateral relations with China. Nikkei 225 (-0.1%) was indecisive but with downside stemmed by recent currency weakness and political continuity hopes with Chief Cabinet Secretary Suga said to be supported by the largest faction of the ruling LDP and is set to announce an intention to continue with Abenomics and the pandemic response when declaring his candidacy on Wednesday. Elsewhere, Hang Seng (U/C) and Shanghai Comp. (+0.4%) swung between gains and losses as mild support was seen following the strongest Caixin Manufacturing PMI reading since January 2011, but with upside also capped after the PBoC drained CNY 230bln from the interbank market and due to lingering US-China tensions after White House trade adviser Navarro stated the US will go after others not just TikTok and WeChat. Finally, 10yr JGBs were higher following the recent gains in T-notes and indecisive risk tone in the region, although some of the gains were reversed after all metrics pointed showed weaker results at the 10yr JGB auction.

Top Asian News

- Total Enters Giant Korean Floating Wind Projects in Green Push

- Samsung’s Heir Jay Y. Lee Indicted in Succession Probe

- Supreme Court Approves 10-Year Rescue Plan for Indian Telcos

- SoftBank Corp. Is ‘Surprise’ Addition to Japan’s Nikkei 225

Earlier gains across European equities have somewhat faded (Euro Stoxx 50 +0.4%) despite a lack of fresh macro catalysts, with the region now ultimately mixed, whilst losses in UK’s FTSE 100 (-1.3%) persist amid a catch-up play from its long weekend Bank holiday. Sectors performance is also varied with no clear risk profile to be derived: the IT sector outperforms as chip-makers cheer reports that Apple is aiming to launch four new iPhone models next month, with volumes in the 75mln region. Thus, the likes of STMicroelectronics (+1.1%), Dialog Semiconductor (+3.3%), Infineon (+1.2%) remain propped up. On the other side of the spectrum resides Travel & Leisure, alongside Banks and Oil & Gas. In terms of individual movers, Novartis (+3.0%) keeps the healthcare sector afloat on the back of a broker upgrade at Morgan Stanley coupled with an announcement that it has developed new ESG targets in order to ramp up access to medicines and achieve full carbon neutrality. Sticking with the healthcare sector, Sanofi (+0.6%) has largely brushed off its COVID-19 Kevzara vaccine failing to meet primary and key secondary endpoints in its Phase III trials. Meanwhile, AstraZeneca (-0.5%) succumbs to the weakness in the post-bank holiday UK markets but with downside somewhat cushioned by a positive update for its Farxiga, Imfinzi and COVID-19 vaccine deal with Canada. Elsewhere, Shell (-2.0%) and BP (-2.1%) are subdued despite higher oil prices, and with losses more pronounced that its cross-border counterparts amid catch-up play alongside reports UK Chancellor Sunak could increase fuel duty by 5p to help pay for the coronavirus in the Autumn budget.

Top European News

- U.K. Manufacturing Output Expands at Fastest Pace in Six Years

- European Factories Brace for Economic Rebound to Falter

- Russia Passes 1 Million Covid-19 Cases as Epidemic Simmers

- German Joblessness Falls Again Amid Revival of Economic Activity

In FX, the Dollar is suffering from a post-month end hangover as the DXY slips to a new 2020 low of 91.741 amidst broad losses vs G10 peers and most EM currencies. Confirmation of a firm US manufacturing PMI via the final release and ISM matching expectations for a pick-up in headline activity could conceivably provide the Greenback some respite, but the index remains toppy on rebounds over 92.000 as buoyant risk sentiment counters renewed bear-steepening along the Treasury curve.

- NZD/CAD/GBP/EUR – The major beneficiaries of ongoing Buck weakness as the Kiwi pivots either side of 0.6750 awaiting NZ terms of trade for Q2 and the Loonie extends through the psychological 1.3000 level with some assistance from firm crude oil. Meanwhile, the Pound has scaled another big figure and briefly breached a mid-December 2019 peak (1.3422), as Eur/Gbp unwinds modest RHS demand for the August/September turn from circa 0.8950 towards 0.8900 irrespective of more negative sounding Brexit news (EU chief negotiator Barnier reportedly unwilling to discuss new UK fishing proposals unless Britain compromises on other contentious issues). Elsewhere, the Euro has tested round number resistance at 1.2000 vs the Dollar, but market contacts note heavy offers related to option expiries and on that note 1.1 bn rolling off between 1.1895-1.1900 at today’s NY cut may keep the headline pair supported given little net reaction to mixed Eurozone manufacturing PMIs and even weak, deflationary inflation.

- JPY/AUD/CHF – Also firmer against the Greenback, albeit mildly as the Yen hovers midway within a 106.03-105.60 range, the Aussie fades after another 0.7400+ foray and Franc fails to breach 0.9000. For the record, the RBA stuck to the script overnight, though did extend and expand its Term Funding Facility, while July building approvals smashed estimates and the Q2 current account surplus was wider than forecast. However, relations with China are going from bad to worse as barley imports from Australia’s CBH Grain company are suspended.

- SCANDI/EM – Not much response to rises in Swedish and Norwegian manufacturing PMIs, but China’s stronger than expected Caixin reading has helped the Yuan appreciate further vs the Dollar in contrast to a decline in the Turkish headline index that is weighing on the already lagging Try.

In commodities, WTI and Brent front month futures continue to ebb higher in early European trade, in what is a continuation of price action seen overnight as a function of the weakening Dollar, whilst the complex also remains underpinned by overall risk sentiment. Aside from that, pertinent news flow has been on the light side, although sources reported that UAE’s ADNOC pumped some 2.693mln BPD of crude in August in order to meet domestic demand – above its quota under the OPEC+ pact. That being said, sources added that the country will compensate for the undercompliance in the months ahead, whilst Iraq submitted a plan to OPEC that proposes additional cuts of 400k BPD in August and September and Kazakhstan plans additional cuts of 95k BPD over the same two-month period, according to sources. Further, Goldman Sachs raised 2020 Brent crude price forecast to USD 43.63/bbl from USD 40.51/bbl and raised 2021 forecast to USD 59.38/bbl from USD 55.63/bbl. WTI October holds its head above USD 43.00/bbl having found an overnight base around USD 42.75/bbl, whilst its Brent counterpart inches higher towards 46/bbl from a low of 45.47/bbl. Elsewhere, the weaker Buck keeps precious metals afloat with spot gold inching higher towards the USD 2000/oz mark (vs. low 1965/oz) whilst spot silver extends gains above USD 28.75/oz (vs. low 28.04/oz). Meanwhile, LME copper prices climbed to levels last seen over two years ago – bolstered by the Chinese Caixin Manufacturing beat coupled with the softer Dollar, whilst Dalian iron ore saw mild gains due to the same factors.

US Event Calendar

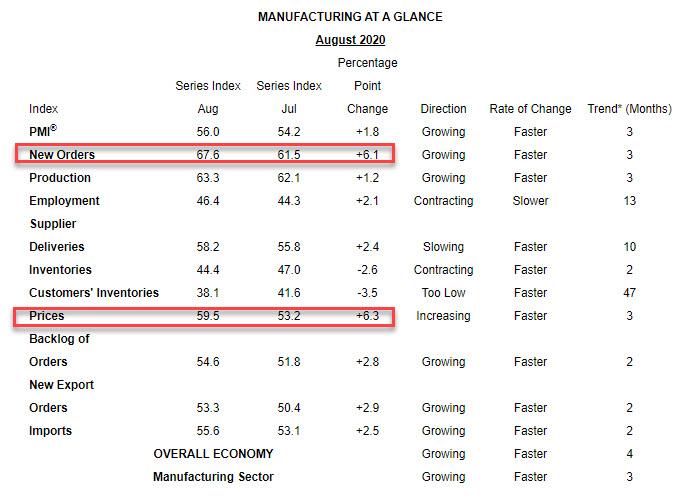

- 9:45am: Markit US Manufacturing PMI, est. 53.6, prior 53.6

- 10am: ISM Manufacturing, est. 54.8, prior 54.2

- 10am: Construction Spending MoM, est. 1.0%, prior -0.7%

- Wards Total Vehicle Sales, est. 15m, prior 14.5m

DB’s Jim Reid concludes the overnight wrap

Never has the restrictions of social distancing felt so liberating. As of today I can break the shackles of two weeks in quarantine. It’s been tedious, tiresome and ponderous. As least during full lockdown we went out for a nice walk once a day and I had heaps of work to occupy me. Of these past 14 days, 10 were spent on holiday at home (or weekends) and 4 at work in my home office. The latter were infinitely more enjoyable and less stressful for me. Much less for my wife. Every morning the twins repeatedly say “Go Mummy car”. They can’t work out why we don’t go out and are very confused. Hopefully they’ll squeal with delight when they realise their wish is finally going to come true.

So with a dull second half of August behind me we welcome in September today. To mark this we are launching our monthly survey this morning as a back to school special. This month’s includes plenty of questions about life around the virus including some questions on whether you will be first up volunteering to take any vaccine, whether you think they should be compulsory and how your understanding is on the effectiveness of vaccines generally. Also a number of other questions. It only takes 3 mins to fill in and results will come in the days ahead. Here is the link. All help filling in the survey very much appreciated.

This morning Henry is publishing the monthly performance review. It was another good month for risk especially for Silver (+15.39%) and the Nasdaq (+9.59%). It was also the best August for the S&P (+7.01%) since 1986 and the best individual month since April – just after the pandemic lows. See the full review in your inboxes soon for more.

Even with the good month, August ended with the S&P 500 slipping slightly, falling -0.16%, as even large gains in tech stocks were unable to keep the index in the green. Roughly 70% of the index was lower on the day after stocks dipped mid-session on reports of China blocking US companies from buying social media company TikTok. In a story that speaks to the power of retail investing in the current market, Apple and Tesla powered the Nasdaq +0.68% higher to another record after their pre-announced stock splits were enacted. The two stocks added +3.39% and +12.57% of value respectively by just lowering the sticker price.

In Europe with the UK markets closed, the Stoxx 600 fell -0.62% during the last session of August, reversing a gain of as much as +0.7% early in the session. This left the index up +2.86% on the month for its best August performance since 2009. Core sovereign bonds diverged much like equities with US 10yr Treasury yields down -1.6bps to finish at 0.705%, while 10yr Bund yields rose +1.2bps to -0.40%. The dollar resumed its slide as well (-0.25%), falling for the fifth session in a row.

Overnight Asian markets are a little directionless with the Nikkei (-0.07%) and Hang Seng (-0.02%) trading flat while the CSI (+0.12%) and Shanghai Comp (+0.04%) are posting modest advances. The Kospi (+1.06%) is leading the way on news that the government is preparing to boost its 2021 budget by 8.5%. In FX, all G-10 currencies are up (0.2-0.6%) against the greenback with the Euro trading closer to the 1.20 handle at 1.1992. Meanwhile the onshore Chinese yuan is up +0.42% to 6.8202, the highest level in over a year. Futures on the S&P 500 are up +0.11% while those on the Nasdaq are up +0.40%. Elsewhere, crude oil prices are trading up c.1% this morning while gold and silver are up +0.91% and +1.81% respectively.

It’s another round of global PMIs today and we’ve already kicked things off in Asia with China’s Caixin manufacturing PMI printing at 53.1 (vs. 52.5 expected and 52.8 last month), the highest reading since Jan 2011 and further emphasising the China recovery story. Yesterday, we saw China’s official August PMIs with manufacturing printing 0.2pts lower than expectations at 51.0 while services were at 55.2 (vs. 54.2 expected). Back to today and Japan’s final manufacturing PMI reading was confirmed at 47.2 (vs. 46.6 in flash). South Korea also showed an improvement at 48.5 (vs. 46.9 last month) while for Taiwan it was at 52.2 (vs. 50.6 last month), the highest reading in 2 years. However, readings for Vietnam (at 45.7 vs. 47.6 last month) and Australia (at 53.6 vs. 53.9 in flash and 54.0 last month) retreated on account of renewed lockdowns during the past month.

Following the policy framework changes laid out by Fed Chair Powell last week, yesterday Federal Reserve Vice Chair Clarida spoke to the possibility of using Treasury yield caps at some point, but suggested that it is not currently in the plans. He also noted that it is appropriate in many circumstances for inflation to overshoot the 2% goal. Markets also heard from the Fed’s Bostic, who said that he was ‘very worried’ about the drop in fiscal support for economy. Given that several participants argued for more accommodation in July, a lack of fiscal response and further gridlock may cause more committee members to opt for additional easing. With the next FOMC in two weeks this meeting will slowly come into the market’s view.