GOLD:$1865.00 DOWN $28.00 The quote is London spot price

Silver:$23.00 DOWN $1.41 London spot price ( cash market)

Today there is no doubt that the official sector came into the fray assisted by the soon to be criminal JPMorgan et al. Generally one week prior to first day notice the spreaders begin their criminal liquidation with the CFTC continually turning a blind eye to this activity. However on the positive side of things, October comex refuses to buckle in numbers and no doubt that a major entity is standing for delivery. You can also bet the farm that options in the money on the October contract month will also be exercised and they will also turn that option into real metal.

comex option expiry FRIDAY: Sept 25

LBMA/OTC options expiry: Sept 30

It is going to be an interesting week…

your data…

Closing access prices: London spot

i)Gold : $1861.40 LONDON SPOT 4:30 pm

ii)SILVER: $22,80//LONDON SPOT 4:30 pm

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 5.41 POINTS OR 0.17% //Hang Sang CLOSED UP 25.66 POINTS OR 0.11% /The Nikkei closed DOWN 13.81 POINTS OR 0.06%//Australia’s all ordinaires CLOSED UP 2.3142%

/Chinese yuan (ONSHORE) closed DOWN at 6.7913 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.7913 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7962 TRADE TALKS STALL////TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS //PANDEMIC : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total withdrawals; 11,599.475 oz (.36 tonnes)

We had 0 kilobar transactions +

ADJUSTMENTS: 1 //

i) Out of HSBC: 104,555.052 adjusted out of the customer and this lands into the dealer account

The front month of SEPT registered a total of 348 contracts for a GAIN of 277 contracts. We had 50 notices filed on Tuesday, so we gained 327 contracts or an additional 32,700 oz will stand for delivery in this non active month of Sept. Remember that we have been adding to our gold deliveries despite the raid these past 9 days.

Oct LOST A TINY 612 contracts DOWN to 61,021. Two major points on this:

a) nobody wants to leave the gold arena

b) we can now safely confirm that a major entity is behind October’s numbers.

Probably Goldman Sachs who has been identified as the major player in the new physical platform at the LME is the one who is accumulating gold in a similar fashion to JPMorgan’s accumulation of silver. Goldman Sachs needs gold to provide liquidity for that new physical exchange.

November gained 64 contracts to stand at 311.

The big December contract GAINED 1182 contracts UP to 427,240 contracts..

THE BIG STORY AGAIN TODAY IS THE HIGH OI FOR OCTOBER AND ITS REFUSAL TO CONTRACT (ROLL TO ANOTHER MONTH). GENERALLY OCTOBER IS A POOR DELIVERY MONTH AS MOST INVESTORS PREFER TO SKIP THIS MONTH AND MOVE STRAIGHT TO DECEMBER. IT LOOKS LIKE SOME MAJOR ENTITY JUST CANNOT WAIT FOR DECEMBER AS THEY ARE MAKING THEIR MOVE ON OCTOBER FOR PHYSICAL METAL. THE REASON FOR THE RAID WAS GOLD AND OCTOBER’S HIGH OI…THE AIM WAS TO FORCE THESE GUYS FROM TAKING DELIVERY BUT TO NO AVAIL!!

We had 298 notices filed today for 29,800 oz

To calculate the INITIAL total number of gold ounces standing for the SEPT /2020. contract month, we take the total number of notices filed so far for the month (4797) x 100 oz , to which we add the difference between the open interest for the front month of SEPT (348 CONTRACTS ) minus the number of notices served upon today (298 x 100 oz per contract) equals 475,700 OZ OR 14.796 TONNES) the number of ounces standing in this active month of JUNE

thus the INITIAL standings for gold for the SEPT/2020 contract month:

No of notices filed so far (4797, x 100 oz +348 OI) for the front month minus the number of notices served upon today (298) x 100 oz which equals 475,700 oz standing OR 14.796 TONNES in this active delivery month. This is a HUGE amount for gold standing for a SEPT delivery month (a NON active delivery month).

We gained 327 contracts or an additional 32,700 oz will try their luck searching for metal on this side of the pond. Somebody today again was in urgent need of physical gold.

NEW PLEDGED GOLD: BRINKS

334,494.256 oz NOW PLEDGED SEPT 15.2020/HSBC 10.389 TONNES

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

261,958.320 oz (some deleted august 3) JPM 8.14 TONNES

610,238.285 oz pledged June 12/2020 Brinks/ july 2/july 21 19.017 tonnes

51,084.609 oz Pledged August 21/regular account 1.588 tonnes jpm

total pledged gold: 1,300,323.778 oz 40.44 tonnes

total registered, pledged and eligible (customer) gold 36,606,348.538 oz 1,138,611 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1012,26 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

END

And now for the wild silver comex results

And now for the wild silver comex results

INITIAL STANDINGS

SEPT. SILVER COMEX CONTRACT MONTH//INITIAL STANDING

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

301,895.740 oz

CNT

Scotia

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

1,212,593.600 oz

JPMorgan

Delaware

Manfra

|

| No of oz served today (contracts) |

193

CONTRACT(S)

(965,000 OZ)

|

| No of oz to be served (notices) |

67 contracts

335,000 oz)

|

| Total monthly oz silver served (contracts) | 10,901 contracts

54,505,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 3 deposits into the customer account (ELIGIBLE ACCOUNT)

i)into JPMorgan: 1,174,824.000 oz

ii) Into Delaware: 2,988.200 oz

iii) Into Manfra: 34,781.400 oz

JPMorgan now has 181.363 million oz of total silver inventory or 49.17% of all official comex silver. (181,363 million/368.829 million

total customer deposits today: 1,212,595.600 oz

we had 0 withdrawals:

total withdrawals; nil oz

We had 0 adjustments/

Total dealer(registered) silver: 142.579 million oz

total registered and eligible silver: 368.829 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

the front month of SEPTEMBER registered an open interest of 260 contracts thus losing 362 contracts. We had 439 notices filed on TUESDAY so we GAINED a strong 77 contracts or an additional 385,000 oz will stand in this active delivery month of September as they refused to morph into London based forwards and thus they also negated a fiat bonus. Not only are longs standing for delivery over here but also our London boys exercising serial forward EFP’s circulating over there and turning them into real physical metal as we now have a full frontal attack on both of our two precious metals.

We thus gained in silver oz standing and in gold despite the vicious raid.

Oct saw another GAIN of 35 contracts to stand at 1997.November gained 1 contract to stand at 39,

The big December contract month saw its OI contract by 727 contracts down to 134,936

The total number of notices filed today for the SEPT 2020. contract month is represented by 193 contract(s) FOR 965,000 oz

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 10,901 x 5,000 oz = 54,505,000 oz to which we add the difference between the open interest for the front month of SEPT( 260) and the number of notices served upon today 193 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the SEPT/2019 contract month: 10,901` (notices served so far) x 5000 oz + OI for front month of SEPT (260)- number of notices served upon today (193) x 5000 oz of silver standing for the SEPT contract month .equals 54,840,000 oz. ..VERY STRONG FOR AN ACTIVE MONTH.

We GAINED 77 contracts or AN ADDITIONAL 385,000 oz. WILL STAND FOR DELIVERY IN THIS ACTIVE DELIVERY MONTH, AS COMEX LONGS LOOK FOR METAL ON THE THIS SIDE OF THE POND!

TODAY’S ESTIMATED SILVER VOLUME : 140,848 CONTRACTS // volume strong// raid volume

FOR YESTERDAY 114,432. ,CONFIRMED VOLUME// strong/raid

YESTERDAY’S CONFIRMED VOLUME OF 114,432 CONTRACTS EQUATES to 0.572 billion OZ 81.71% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 2.71% ((SEPT 23/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.09% to NAV: (SEPT 23/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/2.71%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 18.76 TRADING 18.11///NEGATIVE 3.44

END

And now the Gold inventory at the GLD/

SEPT 23//WITH GOLD DOWN $28.00 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 11.68 TONNES FROM THE GLD////INVENTORY RESTS AT 1267.14 TONNES

SEPT 22/WITH GOLD DOWN $4.50 TODAY, A MONSTROUS CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 18.98 TONNES OF PAPER GOLD ENTER THE GLD///// INVENTORY RESTS AT 1278.62TONNES

SEPT 21/WITH GOLD DOWN $47.20 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 12.94 TONNES INTO THE GLD///INVENTORY RESTS AT 1259.64TONNES

SEPT 18/WITH GOLD UP $10.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS THIS WEEKEND AT: 1246.99 TONNES

SEPT 17/WITH GOLD DOWN $18.05 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD//INVENTORY RESTS AT 1246.99 TONNES

SEPT 16.WITH GOLD UP $4.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1247.57 TONNES

SEPT 15//WITH GOLD UP $2.25 TODAY: A SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .43 TONNES FROM THE GLD//INVENTORY RESTS AT 1247.57 TONNES

SEPT 14/WITH GOLD DOWN 90 CENTS TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.96 TONNES FROM THE GLD////INVENTORY RESTS AT 1248.00 TONNES

SEPT 11/WITH GOLD DOWN $14.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1252.96 TONNES

SEPT 10/WITH GOLD UP $8.85 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.92 TONNES INTO THE GLD////INVENTORY RESTS AT 1252.96 TONNES

SEPT 9/WITH GOLD UP $19.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1250.04 TONNES

SEPT 8/WITH GOLD UP $8.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1250.04 TONNES

SEPT 4//WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1250.04 TONNES

SEPT 3/WITH GOLD DOWN $7.50 ON THIS 2ND DAY OF A 3 DAY RAID: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1250.04 TONNES

SEPT 2/WITH GOLD DOWN $34.00 TODAY, WE HAVE 2 SMALL CHANGES IN GOLD INVENTORY AT THE GLD: 2 WITHDRAWALS OF .87 TONNES AND.59 TONNES FROM THE GLD////INVENTORY RESTS AT 1250.04 TONNES

SEPT 1/WITH GOLD UP $7.10 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1251.50 TONNES

AUGUST 31//WITH GOLD UP $5.90 TODAY/WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD..//INVENTORY RESTS AT 1251.50 TONNES/

AUGUST 28/WITH GOLD UP $38.20 TODAY, WE SURPRISINGLY HAD A .59 TONNE WITHDRAWAL//INVENTORY RESTS AT 1251.50 TONNES

AUGUST 27/WITH GOLD DOWN 17.50 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 3.24 TONNES INTO THE GLD//INVENTORY REST AT 1252.09 TONNES

AUGUST 26/WITH GOLD UP $26.70 TODAY/ WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.53 TONNES FROM THE GLD//RESTS AT 1248.85 TONNES

AUGUST 25/WITH GOLD DOWN $14.60 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//RESTS AT 1252.38 TONNES

AUGUST 24//WITH GOLD DOWN $7.20 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1258.38 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

SEPT 23/ GLD INVENTORY 1267.14 tonnes*

LAST; 907 TRADING DAYS: +327.73 NET TONNES HAVE BEEN ADDED THE GLD

LAST 807 TRADING DAYS://+506.26 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 23//WITH SILVER DOWN $1.41: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.048 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 553.443 MILLION OZ///

SEPT 22/WITH SILVER DOWN ONE CENT TODAY: A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.141 MILLION OZ////INVENTORY RESTS AT 555.491 MILLION OZ..

SEPT 21/WITH SILVER DOWN $2.43 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV A PAPER WITHDRAWAL OF 1.862 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 553.350MILLION OZ//

SEPT 18. WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 555.212 MILLION OZ/

SEPT 17/WITH SILVER DOWN 31 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.537 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 555.212 MILLION OZ/

SEPT 16//WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.749 MILLION OZ//

SEPT 15/WITH SILVER UP 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.793 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 558.749 MILLION OZ..

SEPT 14/WITH SILVER UP 47 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS A) 1.675 MILLION OZ AND ANOTHER B) 0.931 MILLION OZ/ FROM THE SLV////INVENTORY RESTS AT 555.956 MILLION OZ//

SEPT 11/WITH SILVER DOWN 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.562 MILLION OZ//

SEPT 10/WITH SILVER UP 16 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.607 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 558.562 MILLION OZ.

SEPT 9/WITH SILVER UP 6 CENTS TODAY: STRANGE: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.63 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 561.169 MILLION OZ

SEPT 8/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 564.799 MILLION OZ

SEPT 4//WITH SILVER DOWN 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 3.631 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 564.799 MILLION OZ//

SEPT 3//WITH SILVER DOWN 50 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.258 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.430 MILLION OZ/./

SEPT 2.WITH SILVER DOWN $1.04 TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.365 MILLION OZ FROM THE SLV///INVENTORY REST AT 571.688 MILLION OZ.

SEPT 1//WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 31/WITH SILVER UP 80 CENTS TODAY: A HUGE CHANGE IN THE SLV//A DEPOSIT OF 2.982 MILLION OZ ENTERS THE SLV/INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 28/WITH SILVER UP 48 CENTS TODAY: A MASSIVE PAPER DEPOSIT OF 4.652 MILLION OZ ENTERS THE SLV//INVENTORY RESTS AT 571.071 MILLION OZ

AUGUST 27/WITH SILVER DOWN 28 CENTS TODAY// NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.419 MILLION OZ

AUGUST 26//WITH SILVER UP $1.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.65 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 566.419 MILLION OZ..

AUGUST 25/WITH SILVER DOWN 21 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.607 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 571.074 MILLION OZ//

AUGUST 24//WITH SILVER DOWN 18 CENTS TODAY: WE HAD A NO CHANGES//INVENTORY RESTS AT 573.843 MILLION OZ//

SEPT 23.2020:

SLV INVENTORY RESTS TONIGHT AT

553.443 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Heavy Metal Selling [Charts]

Anxiety about an increase in Covid19 cases and fears of a second wave coupled with revelations of historic money laundering practices of major global banks weighed heavily on financial markets yesterday.

Precious metals were not immune to the sell off which saw gold below $1,900 and silver off a whopping 12% during intraday trading.

The following charts show the short term support that halted the rout in precious metals by the end of the day.

With the negative news pushing gold through the 50 day moving average and previous short term support at $1,925 (Support #1) it continued the sell off falling as low as $1,880. As with most markets the daily close is significant for traders and gold closed just above the previous support of $1,910 (Support #2).

Gold remains vulnerable in the short term to a further pull back, particularly with a close below $1,910 which could target the next major support level at $1,810

However, the long term the bull trend still remains intact and the fundamentals are extremely supportive of gold. These pull backs present a major opportunity for long term investors to either get invested or add to their gold holdings.

The sell of in silver was much deeper than gold with the white metal being down over 12% at one stage intraday.

Again a breach of short term support triggered by a weakness in the broader markets saw the start of the sell off. Momentum selling took silver through the support at the 50 day moving average and it didn’t find support until just above the previous major support level at $24.65. Similar to gold, close below this support level could pave the way for a further pull ack to the next major support level close o $23.00.

A resumption of the uptrend short term would require a close above $26.65.

Silver is always the more volatile of the precious metals and one day pullbacks by their nature tend to be larger than one day rallies. However, like gold the long term uptrend in silver remains intact and the fundamentals that underpin silver are stronger than ever.

Precious metals will always be vulnerable to the sell offs in the broader markets in the short term but this can present opportunities for the shrewd investor.

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

22-Sep-20 1903.10 1906.00 1487.46 1493.16 1621.63 1625.25

21-Sep-20 1930.90 1909.35 1503.21 1489.48 1638.18 1624.47

18-Sep-20 1954.75 1950.85 1505.16 1508.01 1647.85 1648.66

17-Sep-20 1936.10 1936.25 1494.67 1499.82 1642.78 1640.20

16-Sep-20 1964.80 1961.80 1521.15 1512.55 1654.56 1656.74

15-Sep-20 1963.55 1949.35 1523.13 1513.09 1652.13 1644.67

14-Sep-20 1942.30 1958.70 1511.69 1518.97 1638.14 1648.83

11-Sep-20 1944.50 1947.40 1519.82 1523.06 1639.41 1644.38

10-Sep-20 1944.80 1966.25 1493.41 1519.71 1643.74 1651.26

09-Sep-20 1928.40 1947.20 1489.69 1496.62 1638.56 1647.14

08-Sep-20 1920.60 1910.95 1467.72 1466.27 1626.17 1622.40

07-Sep-20 1928.40 1928.45 1463.08 1465.43 1629.88 1631.47

04-Sep-20 1937.60 1926.30 1456.49 1459.56 1634.75 1633.12

03-Sep-20 1934.10 1940.45 1453.86 1459.99 1635.28 1637.74

02-Sep-20 1969.00 1947.05 1475.17 1462.43 1659.47 1645.45

Own gold coins and bars in the safest vaults in Zurich, Switzerland with GoldCore. Learn why Switzerland remains a safe haven jurisdiction for owning precious metals. Access Our Most Popular Guide, the Essential Guide to Storing Gold in Switzerland here

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here

ii) Important gold commentaries courtesy of GATA/Chris Powell

A good read:

the corruption of Wall Street banks as the Fed shovels tirllions of dollars of loans at less than 1%

(Pam and Russ Martens)

Pam and Russ Martens: Corporate news organizations conceal crimes of Wall Street banks

Submitted by cpowell on Tue, 2020-09-22 15:31. Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Tuesday, September 22, 2020

There are two opposing narratives living side by side in the United States: independent journalists and researchers have documented how the behemoth banks on Wall Street are as crooked as ever, while the Federal Reserve chairman, Jerome Powell, repeatedly tells Congress and the press that these banks are a “source of strength” in this economic crisis.

Never mind that the Fed is flooding these banks with trillions of dollars in cumulative loans at less than 1 percent interest.

…

Corporate-owned mainstream media that are dependent on financing from these same banks prefer the Fed’s alternative version of reality.

Wall Street On Parade has repeatedly written about critical reports showing serial corruption at these banks that have been censored by those Pulitzer Prize-winning media outlets.

Yesterday provided another example: The New York Times refused to cover the International Consortium of Investigative Journalists’ stunning report on how five of the biggest banks on Wall Street have continued to launder dirty money for fugitives and suspected criminals.

The Wall Street Journal, whose name suggests that perhaps its focus should be Wall Street, failed to put the story on its front page, opting instead to bury it under an innocuous headline about HSBC’s stock hitting a new low. …

… For the remainder of the commentary:

https://wallstreetonparade.com/2020/09/theres-a-pattern-of-corporate-med…

end

iii) Other physical stories:

This is just the beginning

(zerohedge)

JPMorgan To Pay Record $1 Billion Settlement Over Precious Metals, Treasury Manipulation

Last week, we reported that as Deutsche Bank’s infamous gold manipulator and spoofer – and currently star witness for the prosecution in a massive case targinet precious metal manipulation – David Liew, admitted “spoofing was so commonplace I figured it was ok.” Well, it wasn’t ok, but since everyone else was doing it, we can see why Liew was confused.

And speaking of everyone else also manipulating and spoofing gold, we go from Deutsche Bank straight to JPMorgan, which according to Bloomberg is set to pay a record $1 billion settlement to resolve market manipulation investigations by U.S. authorities into its trading of metals futures and Treasury securities.

A penalty approaching $1 billion would far exceed previous spoofing-related fines. It would also be on par with sanctions in many prior manipulation cases, including some brought several years ago against banks for allegedly rigging benchmark interest rates and foreign exchange markets.

The settlement amount, the highest in history of its kind, may be announced as soon as this week said anonymous Bloomberg sources. Its payment would also end probes by the DOJ, CFTC and SEC into whether traders on JPMorgan’s precious metals and treasuries desks rigged markets. Which, of course, they did. In fact, a cynical take would suggest that JPM is merely paying a kickback to the various regulators for the mistake of having been caught rigging various markets.

And since JPM is about to pay a small fraction of the profits it made from manipulating gold and rates markets, said rigging and manipulation with tremendous IRR will resume shortly, only this time JPM’s traders will be far more careful not to get caught, which in retrospect was their only crime.

According to the report, it’s unclear if the largest US commercial bank will face additional DOJ penalties in court:

Previous spoofing cases have been resolved without banks or trading firms pleading guilty to criminal charges. However, when prosecutors filed cases last year against individual JPMorgan traders they painted a grave picture of its precious metals desk, saying it operated as an illicit enterprise within the bank for almost a decade.

What we do know is that once JPM pays the fee – which it may well have funded from one of the numerous bank bailout schemes unleashed by the Fed in recent months – the government’s settlement with JPMorgan is not expected to result in any restrictions on its business practices.

And in what will come as a shock to many, unlike most settlements which are resolved with the guilty party neither admitting nor denying guilt, in this case it is anticipated that JPMorgan will admit to wrongdoing. Just wonderful: the bank made billions rigging rates and gold, and as punishment ends up paying a small portion of the profits and admitting what it did was wrong.

Surely that will teach it a lesson.

And just so we are clear on why Jamie Dimon is “richer than you“, in 2015 JPMorgan pled guilty to massive currency manipulation, paying a $550 million fine to the Justice Department. The bank also paid penalties to U.S. regulators.

It can now add treasurys and precious metals manipulation.

The record JPMorgan settlement follows criminal charges filed last year against several of its employees, including former head of the precious metals desk, Michael Nowak, when the DOJ used racketeering laws more commonly used in mafia and drug gang prosecutions, alleging the precious metals desk effectively became a criminal enterprise for eight years.

Nowak and three others accused in the case pleaded not guilty and are seeking to have the charges dismissed. Two other former traders have pleaded guilty to conspiracy claims and are cooperating. Shortly after Nowak was charged, JPMorgan learned it was the focus of a separate but related criminal investigation into the bank’s trading of Treasury securities and futures, according to another person familiar with the matter. JPMorgan, which disclosed that investigation earlier this year, said it’s cooperating with authorities.

So much for that RICO case: JPM pays $1 billion and all is forgiven.

- How long can it possibly take for John Edmonds to divulge everything he knows?

- Has Jamie Demon, JP Morgan CEO, or former head of JP Morgan Commodities Group Blythe Masters, been questioned about their possible roles in the gold spoofing operation of their bank?

- Given that the feds have gone after JP Morgan bankers under the RICO act, this implies that JP Morgan was running a systemically criminal gold spoofing operation that, by nature, would imply the involvement of much higher level JP Morgan executives in this scheme than even the head of their Metals Trading desk.

- What is the identity of these higher level JP Morgan executives, if true? At least two of the interrogated and arrested JP Morgan has admitted that the gold price manipulation scheme went very high up the corporate hierarchy at JP Morgan.

- What is Mr. Edmonds response to this drawn out inquisition? Does he feel like he is possibly being set-up to be “Epsteined” to keep knowledge of this criminal scheme at the highest echelons of JP Morgan from coming to light?

- Since Edmonds’s arrest, the feds have charged at least four more JP Morgan bankers, Michael Nowak, Gregg Smith, and Christopher Jordan with racketeering charges under the federal RICO act normally reserved for prosecuting low-life gangsters, drug dealers, and mafia members. For example, the US Justice Department invoked the RICO act in 1984 to convict Florida Deputy Police Chief Raymond Cassamayor for running a cocaine smuggling operation and in 1992, to convict John Gotti and Frank Locascio of the infamous Gambino crime family. Both Christopher Jordan and Michael Nowak could face up to 30-years in prison if convicted. JP Morgan Metals Desk Executive Director Jeffrey Ruffo was charged in December 2019. John Edmonds was originally reported upon his arrest in 2018 as facing the same prison time. Has his squealing resulted in the arrest of his three colleagues mentioned above and if so, has he gained a significant reduction in prison time for his cooperation?

- JP Morgan banker have testified that they learned how to effectively spoof gold prices lower in futures markets from Bear Stearns, which makes absolute sense, since Bear Stearns bankers, for decades, were alleged to have been at the head of the class in artificially manufacturing waterfall like type price declines in silver futures markets. It was no surprise, that after the 2008 financial collapse of Bear Stearns, JP Morgan agreed to step in and keep the silver price manipulation scheme going with the assumption of Bear Stearn’s massive short positions in the silver futures markets. Since John Edmonds was arrested, the US Justice Department has brought cases against 16 more bankers employed by Deutsche Bank and United Bank of Switzerland. Is this a result, again, of John Edmonds’s cooperation with the Feds?

- With the Feds bringing cases against bankers from many different global banking institutions for gold and silver price manipulation, what is their end goal in this RICO sting operation? Is it all a smoke and mirrors game executed to deceive the public into thinking justice, for the first time in decades, will actually be enforced? Will bankers actually receive the long prison sentences they deserve, or will all strike a deal and be slapped only with fines that amount to a fraction of the billions they stole from investors through their executed price suppression scheme in the gold and silver futures markets and will they all walk?

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Futures Extend Rebound As Nike Soars, Tesla Tumbles; Powell On Deck For 2nd Day

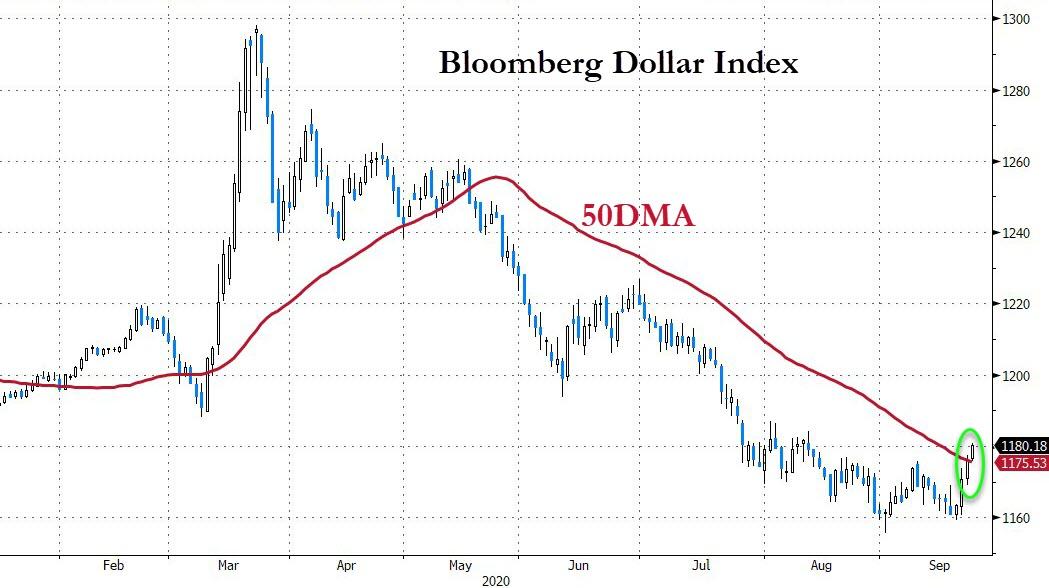

S&P futures and global stocks rose on Wednesday for the second day as Tuesday’s global rebound extended after the recent correction, ahead of data that would throw light on the pace of an economic recovery from a coronavirus-driven recession. Investors also waited for a second speech from Fed Chair Jerome Powell who will appear before the House Select Subcommittee on the coronavirus to discuss the central bank’s response. The dollar extended its impressive Tuesday gains while 10Y yields were fractionally higher.

Nike was set for a record open after a stunning quarterly earnings report. Shares of the world’s largest athletic shoe maker surged 13.2% in premarket trading as its digital sales, especially in North America, helped offset a fall in sales at traditional brick-and-mortar stores. The Dow constituent was set to drive the blue-chip index higher for a second straight day, clawing back more of the sharp declines from Monday that were driven by fears of another round of lockdowns to contain a global surge in COVID-19 cases.

On the other end, Tesla fell 4.8% in premarket trading as the goals announced at Tuesday’s “Battery Day” event was a dud and Musk failed to impress with his promise to cut electric vehicle costs. Oracle headed lower after a report by a state-backed Chinese newspaper said Beijing was unlikely to approve a proposed deal by the software maker and Walmart for ByteDance’s TikTok.

Meanwhile, Russia’s largest internet company Yandex surged 9.2% in premarket after it said it’s in talks to buy TCS Group Holding Plc for about $5.48 billion. Elsewhere, the FAANGs edged higher before the bell. The group has borne the brunt of the declines this month after fuelling a Wall Street rally since March.

Overall sentiment remains skittish as doubts about more U.S. fiscal stimulus and growing political uncertainty in the run-up to the Nov. 3 presidential elections have kept investors from making big stock market bets.

“We are seeing a solid bounce, but it’s in the context of a very sharp pullback on Monday, which was a reset,” said Neil Wilson, chief market analyst in London for Markets.com. “We had bulls just tipping their toes back in the water, and the higher closes — as small as they were — seems to have been enough to cue today’s gains.”

“If we get a second (COVID-19) wave, it could have a significant impact on the election itself and that’s why markets have been wobbly in the last few days,” said Andrea Cicione, head of strategy at TS Lombard in London.

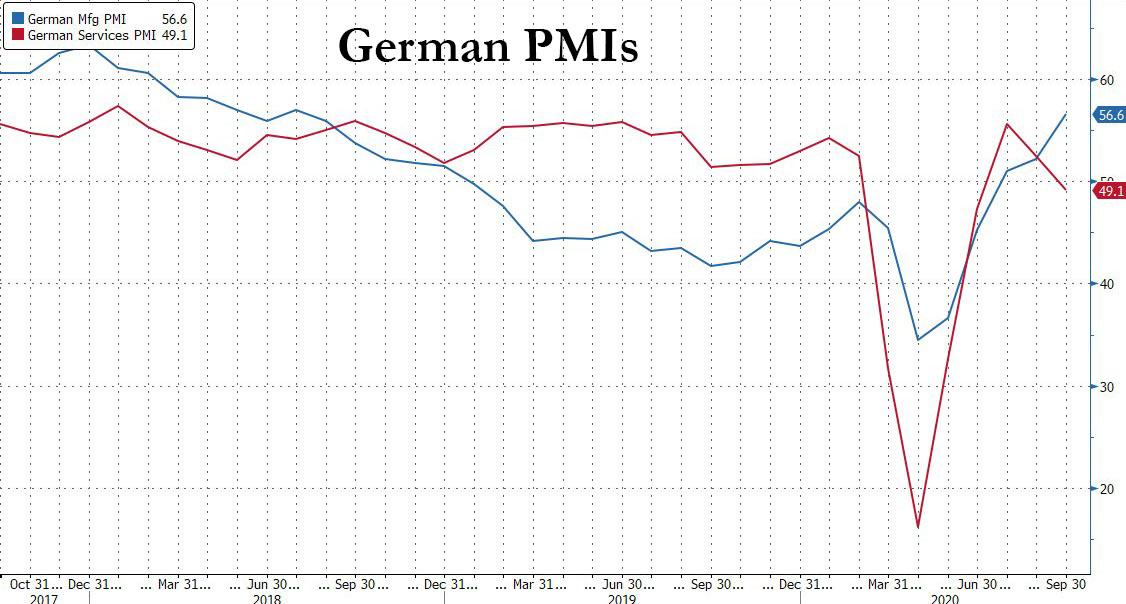

In Europe, the Stoxx 600 Index climbed 1.5%, the biggest gain in two weeks, helped by a jump German stocks after manufacturing data rose to a two-year high. Auto companies and travel stocks led the advance in Europe, with gains of 2.8% for both. Despite stronger German mfg PMI, the service sector stumbled and broader Eurozone data showed eurozone business growth ground to a halt this month with the post-Covid economic recovery stumbling this month, as the latest Euro area composite PMI declined by 1.8pt to 50.1 in September, notably below expectations. Across sectors, the overall decline was concentrated in the service sector, with the pace of recovery in manufacturing reaccelerating from August:

- Euro Area Composite PMI: 50.1, consensus 51.9, last 51.9.

- Euro Area Manufacturing PMI: 53.7, consensus 51.9, last 51.7.

- Euro Area Services PMI: 47.6, consensus 50.6, last 50.5.

And the sharp divergence in Germany:

- Germany Composite PMI: 53.7, consensus 54.0, last 54.4.

- German Services PMI: 49.1, consensus 53.0, last 52.5

- German Manufacturing PMI: 56.6, consensus 52.5

Earlier in the session, Asian stocks were fractionally higher, with health care rising and energy falling, after falling in the last. Markets in the region were mixed, with Australia’s S&P/ASX 200 and Singapore’s Straits Times Index rising, and India’s S&P BSE Sensex Index and Taiwan’s Taiex Index falling. The Topix declined 0.1%, with Daiichi Kigenso and Land Co falling the most. The Shanghai Composite Index rose 0.2%, with EGing Photovoltaic Technology and Jinko Power Technology posting the biggest advances

Chinese state-run media decounced the TikTok deal as “an American trap” and a “dirty and underhanded trick” as sentiment in Beijing swings against the proposal. TikTok owner ByteDance said it would remain in control of the new entity that would be created in the agreement, pushing back on President Donald Trump’s assertions that Oracle Corp. would be in control. The wider context of resistance from China is that the country’s leaders do not want to be seen to be pushed around by unilateral U.S. actions.

Looking at today’s main event in markets, Fed Chair Powell is in Congress again testifying to a House select subcommittee on the coronavirus response from 10:00 a.m. Yesterday he said the U.S. economy has a long way to go before it is fully recovered and that more support will be needed.

In other overnight news, while there is still very little progress on reaching a new stimulus deal, there was some relief late yesterday when an agreement to keep the government funded through Dec. 11 was reached, avoiding a shutdown just before the election. More importantly, Republican moves to get a confirmation hearing for Trump’s Supreme Court nominee in the coming weeks now seem unstoppable, after Democrats gained little support in the Senate for a delay.

In FX, the dollar advanced a fourth day after breaking above a key technical resistance level. The Bloomberg Dollar Spot Index was set for its longest run of gains since June as the greenback continued its rebound and advanced versus most Group-of-10 peers. The euro erased losses, after falling to 1.1672 in early London trading, despite weaker- than-forecast European services PMI data. The pound also steadied after dropping following comments by Foreign Secretary Dominic Raab on not being able to rule out a nationwide shutdown. The Australian dollar led declines after influential Westpac Banking Corp. economist Bill Evans predicted the central bank would cut interest rates at its Oct. 6 meeting; the New Zealand dollar also slipped, with the central bank maintaining the size of its quantitative easing program and keeping rates unchanged.

In rates, treasury yields are slightly cheaper in early U.S. trading as Asia-session gains – led by steep gains for Aussie bonds – eroded ahead of 5-year note auction. Yields are cheaper by about 0.5bp from intermediates to long end with 10-year around 0.675%, trading broadly in line with bunds; gilts outperform slightly, about 0.5bp richer vs. Treasuries. Treasury auction cycle resumes with $53b 5-year note at 1pm ET, concludes with 7-year Thursday. Italian bonds rallied to send 30-year yields to an all-time low with investors continuing to snap up the securities on fading domestic political risk and support from European institutions. Elsewhere, Zambia became the first African country to ask bondholders for relief since the onset of the coronavirus.

In commodities oil was unchanged after fluctuating earlier, while gold continues to slide, dropping below $1,900 earlier and sliding below the 50DMA.

Looking at the day ahead, in addition to Powell speaking in the House, there is a slew of Fed speakers today, including Cleveland Fed President Loretta Mester, Chicago Fed President Charles Evans, Boston Fed President Eric Rosengren, Minneapolis Fed President Neel Kashkari, Atlanta Fed President Raphael Bostic, Fed Vice Chair for Supervision Randal Quarles and San Francisco Fed President Mary Daly. Latest U.S. government crude stockpile data is at 10:30 a.m. President Trump is due to speak to state attorneys general on social media abuses. The UN General Assembly continues.

Market Snapshot

- S&P 500 futures up 0.5% to 3,314.00

- STOXX Europe 600 up 1.3% to 362.11

- MXAP up 0.09% to 171.12

- MXAPJ up 0.2% to 557.55

- Nikkei down 0.06% to 23,346.49

- Topix down 0.1% to 1,644.25

- Hang Seng Index up 0.1% to 23,742.51

- Shanghai Composite up 0.2% to 3,279.71

- Sensex down 1% to 37,353.04

- Australia S&P/ASX 200 up 2.4% to 5,923.93

- Kospi up 0.03% to 2,333.24

- German 10Y yield fell 0.8 bps to -0.513%

- Euro down 0.2% to $1.1689

- Italian 10Y yield fell 5.2 bps to 0.661%

- Spanish 10Y yield fell 1.8 bps to 0.217%

- Brent futures up 0.4% to $41.87/bbl

- Gold spot down 1.1% to $1,879.89

- U.S. Dollar Index little changed at 93.94

Top Overnight News from Bloomberg

- The European Central Bank risks legal trouble if it tries to extend the “emergency powers” of its pandemic bond-buying plan to its other asset-purchase program, according to Executive Board member Yves Mersch

- SNB President Thomas Jordan has taken his foot off the pedal after the most aggressive currency intervention in five years early in the outbreak of the coronavirus pandemic

- The euro area’s economic recovery stalled this month as consumers fretted about a resurgence of the coronavirus and governments reinstated restrictions to control the spread of the disease

- Banks from Goldman Sachs Group Inc. to HSBC Holdings Plc have hit pause on plans to return workers in London after Prime Minister Boris Johnson appealed to Britons to work from home to help tame a resurgent coronavirus

- JPMorgan Chase & Co. is moving about 200 billion euros ($230 billion) from the U.K. to Frankfurt as a result of Britain’s exit from the European Union

A quick look at global markets courtesy of NewsSquawk

Asian equity markets traded mixed and failed to take full impetus from the rebound across their global peers, with the region tentative amid ongoing US-China tensions and with Japan suffering post-holiday blues on return from the extended weekend. Nonetheless, ASX 200 (+2.4%) outperformed and is on track for its best day in seven weeks as tech names led the broad advances after they found inspiration from the resurgence of the sector stateside, with sentiment also buoyed by increasing calls for the RBA to cut rates at next month’s meeting after RBA Deputy Governor Debelle recently outlined policy options. Nikkei 225 (U/C) was subdued as it played catch up to the recent days’ weakness and with Panasonic shares pressured alongside fellow Tesla supplier LG Chem after the EV-maker’s Battery Day Event fell flat where Elon Musk announced plans for a reduction in costs and to manufacture its own batteries, while he also showcased the Model S Plaid which is to be available next year. Conversely, Fujifilm Holdings was at the other side of the spectrum after announcing its Avigan drug met the primary endpoint in Phase 3 COVID trials. Hang Seng (+0.1%) and Shanghai Comp. (+0.2%) were indecisive as the continued PBoC liquidity efforts were offset by ongoing US-China tensions after US President Trump put China on blast for the spread of the coronavirus at the virtual UN meeting, while Beijing later criticized President Trump of spreading “political virus”. In addition, the uncertainty regarding the TikTok deal persists and the US House also overwhelmingly passed the forced labour bill which would ban imports from China’s Xinjiang region that were produced using forced labour. Finally, 10yr JGBs were higher amid the risk averse tone in Japan and with the BoJ also in the market for nearly JPY 1.3tln of JGBs in up to 10yr maturities, while it also offered to purchase 3yr-5yr corporate bonds.

Top Asian News

- Hong Kong’s BEA Is Said to Press Ahead With Life Insurance Sale

- Richard Li’s FWD Said to Plan Up to $3 Billion Hong Kong IPO

- Malaysia Leader Calls for Stability After Anwar Claims Majority

- Hong Kong Traders Chased 1,600-1 Odds to Buy IPO That Flopped

European equities are back on the grind higher (Euro Stoxx 50 +1.7%) after experience a fleeting blip lower on the back of French Services PMI dipping back into contractionary territory on second wave woes. The region picked up the baton from a mixed APAC handover, with reports also noting that the ECB as called upon Brussels to make the EU Recovery Fund a permanent measure. Bourses in the EU are seeing broad-based gains, whilst UK’s FTSE (+2.2%) ploughs ahead initially with the aid of a softer Sterling. Meanwhile UBS Wealth Management sees UK domestic banks falling 15-20% and insurance stocks decline by 7-10% in a no-deal Brexit scenario, but expects double digit positive returns from UK equities over the next 9-12 months in the event of a deal. Sectors in Europe are higher across the board with a slight cyclical/value bias, although material names do not fare so well amid the USD-induced declines across the metals complex. Consumer Discretionary meanwhile tops the charts with the aid of Nike (+13% pre-mkt) post-earnings, who beat on both top and bottom lines whilst reporting digital sales +82% YY – thus bolstering the likes of Adidas (+5.7%), Puma (+4.6%) and JD Sports (+5.1%). In terms of the breakdown, Travel & Leisure leads the gains, closely followed by Autos and Banks. Turning to individual movers, Osram Licht (+14.6%) is the top Stoxx 600 gainer after ASM (+1.4%) has signed a denomination and profit and loss transfer agreement with Osram as part of the takeover process.

Top European News

- Europe’s Economic Revival Put on Hold by Virus Resurgence

- U.K. Recovery Slows as Households Start to Rein In Spending

- Sunak Urged to Save U.K. Firms From ‘Ruin’ of Covid Curbs

- Merkel Resists Full Ban on Huawei, Making Germany an Outlier

In FX, the Dollar has extended its impressive recovery rally, partly in relief that the House finally passed the stopgap spending bill to avert a Government shutdown, but mainly as the Greenback continues to regain its global safe-haven and reserve status amidst the ongoing resurgence in COVID-19 that is accelerating outside the US and notably across Europe again. As a result, the index breached 94.000 and topped out just above 94.250, with several Buck/major pairings looking very vulnerable near or through psychological/round number levels.

- AUD/NZD – Dovish RBA calls via Westpac and NAB both looking for 15 bp cuts at the October meeting, plus a dovish RBNZ hold overnight, leaving the door wide open for more easing and in the offing or in the pipeline, an FLP by the end of 2020, according to the accompanying statement, have all added further pressure on the Aussie and Kiwi, with the former struggling to stay above 0.7100 and latter even less assured around 0.6600 ahead of NZ trade data.

- CAD – Some solace for the Loonie from relative stability in oil prices, but not enough momentum to convincingly reclaim 1.3300+ status within a 1.3345-1.3294 range awaiting the reopening of Canadian Parliament by PM Trudeau.

- CHF/EUR/GBP/JPY – All narrowly mixed vs the Dollar, but not before losing grip of 0.9200, 1.1700, 1.2700 and 105.00 handles respectively in advance of Thursday’s quarterly SNB policy review and following mixed Eurozone/UK prelim PMIs where services sector weakness outweighed manufacturing strength to keep the composite readings compressed. However, Sterling was undermined by domestic factors related to the coronavirus and warnings from Foreign Minister Raab about latest restrictions not going far enough to rule out the risk of reverting to full lockdown. Cable plumbed fresh lows around 1.2677 and Eur/Gbp retested recent peaks circa 0.9220 in response, but the Pound has subsequently received a reprieve from EU’s Barnier expressing determination to strike a Brexit trade deal. Elsewhere, pretty standard commentary from BoJ Governor Kuroda has marked the return of Japanese markets from their 4-day break, but not really the Yen between 104.91-105.19 parameters eyeing mega option expiries for tomorrow that span 105.00 in an even tighter band (104.90-105.10).

- SCANDI/EM – The Norwegian Crown continues to slip closer towards the sentimental if not technically significant 11.0000 level vs the Euro regardless of crude finding a base as noted above, but the Swedish Krona is still benefiting from Riksbank rigidity on the repo staying at the zero lower bound until this time in 2023. On that note, the Turkish Lira will be looking for continuity and some much needed support from the CBRT on Thursday via a form of indirect tightening as it plumbs almost daily record lows, and more immediately the Czech Koruna has the CNB to provide direction, albeit with no change in rates expected.

In commodities, WTI and Brent front month futures have nursed the losses seen in APAC hours, as sentiment in Europe picks back up after the EZ Services PMI fell back contraction but manufacturing topped estimates across the board. The initial weakness in the crude markets stemmed from a surprise build in the Private Inventory data (+0.7mln vs. Exp. -2.3mln), whilst concern remains over the demand implications from the reimposition of lockdowns and quarantine travel rules, with the Gazprom CEO also noting that we are seeing global oil demand recovery slowing down due to pandemic, and expects global oil consumption to return to pre-crisis level in H2 2021. In terms of the reopening supply from Libya, reports yesterday noted that next week could see output of some 260k BPD (vs. 1mln BPD pre-blockade), although analysts at ING downplay the relevance, noting that “In the current environment, where there are clear concerns over demand, additional supply will do little to help rebalance the market.” Something else to be aware of: reports noted that Chinese refiners are requesting additional import quotas for the fourth quota, having had taken advantage of the lower oil prices earlier this year. Desks note that further quota allocation could support the physical market. Aside from that, news-flow has remained relatively light for the complex thus far, WTI Nov meanders around USD 39.85/bbl (vs. low USD 39.26/bbl), while its Brent counterpart resides around 41.85/bbl (vs. low 41.21/bbl), awaiting the weekly EIA inventory data – with headline crude stocks seen drawing 2.325mln barrels. Elsewhere, precious metals initially succumb to the firmer Dollar and broader gains in stocks. Spot gold moves further below the USD 1900/oz mark to find support at USD 1875/oz, and has picked up given the most recent slip in the USD, whilst spot silver found a current base around the USD 23/oz level. Base metals are also mostly lower – with LME copper weighed on by the firmer Buck and lackluster China performance, whilst Dalian iron ore futures fell for a third straight days as higher shipments from mainstream miners weighed on prices.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -2.5%

- 9am: FHFA House Price Index MoM, est. 0.45%, prior 0.9%

- 9:45am: Markit US Manufacturing PMI, est. 53.5, prior 53.1; Services PMI, est. 54.5, prior 55; Composite PMI, prior 54.6

Fed Speakers:

- 9am: Fed’s Mester Discusses Payments and the Pandemic

- 10am: Powell Appears before House Panel on Covid-19

- 11am: Fed’s Evans Discusses the U.S. Economy and Monetary Policy

- 12pm: Fed’s Rosengren Discusses U.S. Economy

- 1pm: Fed’s Kashkari Discusses Public Health

- 1pm: Fed’s Bostic Speaks to Hale County Chamber of Commerce

- 2pm: Fed’s Quarles Gives Speech on the Economic Outlook

- 3pm: Fed’s Daly Discusses Labor Force Implications of Covid-19

DB’s Jim Reid concludes the overnight wrap

I suspect this won’t be the last Zoom call I do from home after the U.K. yesterday effectively encouraged those who can work from home to do so – and possibly for the next 6 months. Today also sees a big change in the weather here as the Indian Summer has come to an abrupt end. Winter is coming in more ways than one. On the virus we’ve revamped our daily cases and fatality tables that appear in the PDF (click view report above) and given they are sorted worst to best they show that the U.K. is certainly not at the top of the second wave, but restrictions are nonetheless being tightened as case numbers build (4,926 yesterday and the highest since early May). In addition to WFH guidance, all hospitality venues must now close at 10pm daily from Thursday. In a nationwide address Johnson stressed the desire to avoid a full lockdown scenarios saying, “we must do all we can to avoid going down that road again.” Though if the infections continue to rise the government naturally left the option on the table. Meanwhile in Scotland, First Minister Nicola Sturgeon went even further, with a ban on households visiting other households indoors.

The virus news flow has been a difficult backdrop for markets this week but US markets started to gather some momentum after Europe went home last night. There was a particular reversal in US technology stocks, which continued to outperform after the late-session rally on Monday. The S&P 500 broke a four-day slide and gained +1.05%, however cyclicals sectors like Banks (-1.89%), Autos (-1.13%) and Energy (-1.03%) continued to lag. Retail (+3.64%), Media (+2.24%) and Software (+1.94%) all the led the S&P higher as the tech gains saw the NASDAQ rally +1.71%. This could again signal that the stay-at-home trade is coming back into vogue with further restrictions being seen in Europe. Europe still saw a slight recovery from Monday’s worst day for three months as the STOXX 600 climbed +0.20% higher.

Asian markets are mixed this morning with the Nikkei (-0.36%) and Kospi (-0.25%) both down while the Hang Seng (-0.01%) and Shanghai Comp (+0.02%) are trading broadly flat and the Asx (+2.15%) is up partly helped by stronger preliminary PMIs (more below). Japanese markets have reopened post 2 days of holiday. In overnight news, Tesla’s “Battery Day” event came short of expectations for a blockbuster leap forward as the company laid out a roadmap to build a $25,000 car only by 2023 which disappointed some. The stock was down -7% in aftermarket trading. This is also weighing on Nasdaq futures (-0.38%) while those on the S&P 500 are trading broadly flat.In fx, the US dollar index is up a further +0.25% this morning after yesterday’s +0.47% advance.

In other news, the US House passed a stopgap funding bill to keep the government operating through Dec. 11 after both parties in Congress and officials at the White House struck a deal to provide aid to farmers and food assistance for low-income families. The temporary spending bill will now move to the Senate for a vote.

Today, investors will be watching out for the flash PMIs for September, which will give us an early indication of how the global economy has fared this month. Overnight we’ve already had readings from Japan and Australia, with Japan struggling to recover further as manufacturing PMI rose by just 0.1 pt to 47.3 while the services reading improved to 45.6 (vs. 45.0 last month). Australia’s readings were a bit more robust with manufacturing PMI climbing to 55.5 (vs. 53.6 last month) and the services reading printing at 50.0 (vs. 49.0 last month). Australia’s reading seem to be helped partly by the easing of lockdown in Victoria, the second largest state. With infections rising again in Europe, not least in the UK, France and Spain, the question is to what extent this will impact on economic activity there as well. DB’s Peter Sidorov put out a piece yesterday (link here) in which he writes that his analysis points to a slight upside risk to the Euro Area PMI because of mobility trends, which has been rising in September. We’ll get those releases this morning.

Back to yesterday, and Fed Chair Powell appeared before the House Financial Services panel, where he again stressed the need to keep the virus under control and for further policy actions from “all levels of government.” Secretary Mnuchin who testified alongside the Fed Chair said that he and the President he would continue to seek Congressional agreement on further fiscal stimulus. Though now Congress seems like it will be more focused on a supreme court confirmation than fiscal stimulus in the short term. The Fed Chair said the Fed has only purchased $1.5 billion in loans so far through its Main Street Lending Program. The program is a $600 billion facility backed by Treasury funds, which aims to provide credit to small-mid sized companies. Mnuchin did bring up the idea of reallocating some of the unused money in Fed facilities to other uses, though it would require congressional approval.

There were a few other central bank headlines. From the ECB, we had Fabio Panetta of the Executive Board saying that “the risks of a policy overreaction are much smaller than the risks of policy being too slow or too shy to react and the worst-case scenarios materialising.” And over in the UK, Bank of England Governor Bailey downplayed the prospect of an imminent move to negative rates after last week’s MPC minutes showed that they were exploring the operational considerations of such a move.

In fixed income, there was a sharp narrowing of sovereign bond spreads in Europe, particularly following the regional election results in Italy that were regarded as positive for the government’s stability. Yields on 10yr BTPs fell -5.2bps to their lowest levels in almost a year, moving below the levels they were at before the pandemic hit the country in late February. And with the selloff for bunds, that sent the BTP-bund spread down -7.7bps to 1.37%, its lowest level in 7 months. Elsewhere, US Treasury yields saw a slight +0.5bps move higher, as the dollar index climbed a further +0.35% to reach its highest level in nearly 2 months.

Staying on the US, and with less than 6 weeks now until the election, President Trump said that he’d announce his choice this Saturday at 5pm (Washington Time) on who would replace Justice Ruth Bader Ginsburg on the Supreme Court. In a positive development for Trump, Senator Mitt Romney said that he’s in favour of moving forward with a confirmation vote on Trump’s choice, which leaves just 2 Republican senators out of the 53-member caucus who have opposed going ahead with a vote. With Trump’s choice on Saturday and the first debate between himself and Biden this Tuesday, the coming week will be one of the most important yet ahead of election day on November 3rd.

Looking at yesterday’s data, existing home sales in the US rose to an annualised rate of 6.00m in August, in line with expectations, and the most since 2006. Meanwhile the Richmond Fed’s manufacturing survey rose to 21 (vs. 12 expected). Finally, the advance consumer confidence reading from the Euro Area in September rose to -13.9 (vs. -14.7 expected). This was its highest level since March, but still some way below the -6.6 reading back in February before the full impact of the pandemic became apparent.

To the day ahead now, and the aforementioned flash PMIs will be one of the key highlights. Otherwise, there are an array of Fed speakers, including Chair Powell before the House Select Subcommittee on the Coronavirus Crisis, as well as the Vice Chair Quarles, Mester, Evans, Rosengren, Kashkari, Bostic and Daly. The ECB’s Hernandez de Cos will also be speaking.

3A/ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 5.41 POINTS OR 0.17% //Hang Sang CLOSED UP 25.66 POINTS OR 0.11% /The Nikkei closed DOWN 13.81 POINTS OR 0.06%//Australia’s all ordinaires CLOSED UP 2.3142%

/Chinese yuan (ONSHORE) closed DOWN at 6.7913 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.7913 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7962 TRADE TALKS STALL////TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS //PANDEMIC : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

CHINA

So much for freedom of speech in China

(zerohedge)

Chinese Property Tycoon Sentenced To 18 Years In Prison After Calling President Xi A “Clown”

President Xi’s intolerance for criticism is widely known to the outside world – and feared within China.

The Chinese internet was scrubbed of practically all references to the children’s cartoon “Winnie the Pooh” because some Chinese dissidents mocked Xi over his alleged ‘resemblance’ to the character, even using it as a code word (for the record, they call Hong Kong Chief Executive Carrie Lam “piglet”).

And in the latest example of the heavy handed punishments that await anybody who dares criticize the ‘dear leader’, a former Chinese property tycoon who openly mocked Beijing’s handling of the coronavirus pandemic has just been sentenced to 18 years in prison on corruption charges.

The sentence was handed down after Ren Zhiqiang, former chairman of the state-owned real estate group, disappeared in March after publishing an essay where he apparently called President Xi “a clown”. It was published after Xi unveiled plans for combating the virus.

Of course, the official charges against Ren included embezzlement and accepting bribes, since Xi typically removes his detractors under the auspices of his anti-corruption drive.

The Beijing No. 2 Intermediate Court found 69-year-old Ren guilty of embezzlement, bribery, misuse of public funds and abuse of power at a state-owned business, according to a notice released on Tuesday by the court. A real-estate developer for most of his career, he was known as a “big cannon” for his outspokenness and even earned the nickname “China’s Donald Trump.”

The court accused Ren of embezzling $7.3 million in public money, and accused him of accepting bribes of more than $180,000, while misusing around $9 million. He also alleged abused his power and caused losses of more than $17 million at the state-owned enterprise, while he personally profited.

China Slams TikTok Deal As “American Trap”, CCP Won’t Kowtow To “Bullying And Robber Logic”

Despite President Trump claiming he had given the TikTok-Oracle/Wal-Mart deal “his blessing” over the weekend, it looks like the deal will fall apart now that the administration has abandoned its Sunday deadline, while Beijing has sent word through the state-controlled press that it simply won’t allow the White House to ‘steal’ TikTok from ByteDance (a company that is 40% owned by American investors).

On Wednesday morning, more state-backed newspapers slammed the deal, adding their voices to the chorus started by the GT.

The People’s Daily warned the so-called “cooperation agreement” with TikTok is “a trap” – an attempt by the US to ‘take advantage’ of ByteDance under the auspices of “commercial cooperation”.

Trump’s “national security” claims are “just an excuse”, the PD argued…

The US is absolutely good at playing routines. Sometimes it looks like a step back, but in fact it is pressing harder. In this “hunting” against Tik Tok, the United States has always used national security as an excuse, but it is in fact untenable. Security is just an excuse. The real approach in the United States is to exert extreme pressure and public opinion, to break through the moral bottom line, to constantly dig traps and bring rhythm. In the depths of the trap, the great rod of power has already been prepared. Aiming at a technology company, the world’s number one power actually used its full power, using the President’s Executive Order and the Ministry of Commerce’s ban.

…and if ByteDance falls for this trickery, Washington will destroy ByteDance and TikTok, just like it did to Alstom, to Toshiba and to Huawei, the paper argued.

“Commercial competition no longer relies on honesty and bottom line,” the paper continued. “The superiority of technological hegemony needs to be maintained by political cards.”

This deal is only the “starting point” for “bullying and robber logic.”

How familiar is this technique. Because of the “American trap”, Toshiba, a Japanese company that once led the world in the semiconductor industry, has difficulty finding a chance to make a comeback. Because of the “American trap”, the French business giant Alstom, which once spanned the global electric energy and rail transit industries, has been “dismembered” by the Americans. If these lessons are not enough, the Chinese people understand Huawei’s bloody struggle in the US in the past two years.

For a country that is trying to dominate forever, this is not a fuss, but a “precision strike.” All opponents stronger than it in a certain aspect are targets of strike. Commercial competition no longer relies on honesty and bottom line, and the superiority of technological hegemony needs to be maintained by political cards. “America first” has become a stark declaration of hegemony. As long as the United States is no longer dominant in any aspect, it will use political tools. This trick has been tried and tested repeatedly, and it is the starting point for bullying and robber logic.

The Trump Administration’s skullduggery in trying to crush a competitor isn’t just a problem for China. “A hegemonic country…cannot tolerate any country above it.”

Kyle Bass reminded us on Tuesday that China’s claims are simply more ‘pot calling the kettle black’. By giving ByteDance a hard time, the Trump administration is essentially giving China a taste of its own medicine (foreign companies operating in Beijing are subjected to a host of controls, including forced partnerships with domestic entities), Bass argued

Still, the editorial continued: “China, which has gone through ups and downs, will not hide or turn a blind eye to difficulties and challenges, obstacles and variables, and will not panic or get confused. After the wind and rain, it is a rainbow.It has withstood the test again and again, and we will finally go through the wind and rain and usher in a better tomorrow.”

Gao Zhikai, a prominent former diplomat and translator, warned that the saga has sparked “complete disbelief” among Chinese leaders: “China wants to emphasize that the Chinese companies’ legitimate rights cannot be violated without consequences.” Others reminded the US of threats, leaked over the weekend, that Beijing might respond to the US’s latest aggression by restricting trade, investment and visas for certain American companies by adding them to an “unreliable entities” list that Beijing used as a cudgel during the trade talks with Washington. This just further cements the impression that the TikTok-Oracle deal was just another “for show” agreement, like the ‘Phase 1’ trade deal.

Another Chinese source told Bloomberg that a deal could still get done, but China can’t “play in favor” of the Trump Administration, since that would anger hard-core nationalists who still hold a lot of sway within the party. The deal is technically still in flux, though most expect Beijing to reject the deal over Trump’s insistence that ByteDance give up more of its control over the newly independent TikTok.

According to media reports, current deal terms allow ByteDance to retain control of the TikTok content-recommendation algorithm, while Oracle steps in to handle all of the user data. It’s still not exactly clear how China would overtly ‘kill’ the deal, though Bloomberg said it expects a statement from the Ministry of Commerce would just about do it.

end

As expected, the deal is falling apart so TikTok files a new injunction against the White House

(zerohedge)

TikTok Files New Injunction Against White House Amid Reports Deal Is “Falling Apart”

As Fox Business publishes rumors that the TikTok-Oracle deal is falling apart, TikTok-owner ByteDance has filed a petition for an injunction Wednesday afternoon, asking a federal court in Washington DC to intervene and quash President Trump’s threatened ban of TikTok on national security grounds.

The injunction, filed Wednesday afternoon, comes after a California court shut down Trump’s attempt to ban Tencent’s WeChat just a few days ago. It follows another lawsuit filed by TikTok and its parent back in August targeting the administration and its leaders, including Commerce Secretary Wilbur Ross.