GOLD:$1878.10 UP $14.30 The quote is London spot price

Silver:$23.49 UP $0.48 London spot price ( cash market)

Comex options expiry is now over and the bankers made out like bandits again. We still have to deal with the bigger options expiry on Wednesday Sept 30 at 10 am-11 am est

October is going to be a dandy delivery month. October OI is extremely high at 37,521

We will keep you abreast on that.

A huge 361,455.25 oz of gold left all comex vaults. .No doubt that a lot of this gold will head to London .

comex option expiry FRIDAY: Sept 25

LBMA/OTC options expiry: Sept 30

With gold/silver shares down today with the huge rise in price of metals, we are 100% certain of a raid tomorrow

It is going to be an interesting week…

your data…

Closing access prices: London spot

i)Gold : $1882.70 LONDON SPOT 4:30 pm

ii)SILVER: $23.66//LONDON SPOT 4:30 pm

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURDAY NIGHT:

SHANGHAI CLOSED DOWN 3.76 POINTS OR 1.04% //Hang Sang CLOSED DOWN 75.65 POINTS OR 0.32% /The Nikkei closed UP 116.80 POINTS OR 1.97%//Australia’s all ordinaires CLOSED UP 1.39%

/Chinese yuan (ONSHORE) closed DOWN at 6.8305 /Oil UP TO 39.84 dollars per barrel for WTI and 41.66 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8305 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8373 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS//PANDEMIC : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total withdrawals; 361,455.245 oz

We had 1 kilobar transactions +

ADJUSTMENTS: 3 // first two customer into the dealer

i) Out of Brinks: 31,733.037 oz customer into dealer

ii) Loomis: 57870.000 oz 1800 kilobars

iii) Malca: 80,345.839 oz adjusted out of the dealer and this lands into the customer account

The front month of SEPT registered a total of 48 contracts for a LOSS of 180 contracts. We had 180 notices filed on Friday, so we gained 0 contracts or an additional NIL oz will stand for delivery in this non active month of Sept. Remember that we have been adding to our gold deliveries despite the raid these past 12 days. The boys have now switched to October as the assault on the comex gold commences in earnest!!

Oct LOST ONLY 2918 contracts DOWN to 37,521. October witnessed three events:

- more spreader liquidation

- some minor rollover to December

- huge purchases of October and these guys will stand for delivery.

If I were to be a betting man, I would guess we will end up with 35,000 contracts standing for delivery or 3.5 million oz (108 tonnes)

June 2020 saw a huge 152.56 tonnes finally stand for delivery

August 2020 saw a monstrous 171.39 tonnes stand.

However, we will have one major difference: all of the October gold will leave for London. June and August gold stayed at the comex vaults.

November gained 42 contracts to stand at 542.

The big December contract GAINED 605 contracts UP to 432,240 contracts..

THE BIG STORY AGAIN TODAY IS THE HIGH OI STANDING FOR OCTOBER. GENERALLY OCTOBER IS A POOR DELIVERY MONTH AS MOST INVESTORS PREFER TO SKIP THIS MONTH AND MOVE STRAIGHT TO DECEMBER. IT LOOKS LIKE SOME MAJOR ENTITY(GOLDMAN SACHS) JUST CANNOT WAIT FOR DECEMBER AS THEY ARE MAKING THEIR MOVE ON OCTOBER FOR PHYSICAL METAL. GOLDMAN SACHS ONE OF THE LEADERS OF THE NEW LONDON LME EXCHANGE NEEDS THE GOLD INVENTORY FOR LIQUIDITY AND INITIAL CONTRIBUTION WITH OTHER MAJOR PLAYERS.

We had 33 notices filed today for 3,300 oz

To calculate the INITIAL total number of gold ounces standing for the SEPT /2020. contract month, we take the total number of notices filed so far for the month (4922) x 100 oz , to which we add the difference between the open interest for the front month of SEPT (48 CONTRACTS ) minus the number of notices served upon today (33 x 100 oz per contract) equals 493,700 OZ OR 15.356 TONNES) the number of ounces standing in this active month of JUNE

thus the INITIAL standings for gold for the SEPT/2020 contract month:

No of notices filed so far (4922, x 100 oz +48 OI) for the front month minus the number of notices served upon today (33) x 100 oz which equals 493,700 oz standing OR 15.356 TONNES in this active delivery month. This is a HUGE amount for gold standing for a SEPT delivery month (a NON active delivery month).

We gained 0 contracts or an additional oz will try their luck searching for metal on this side of the pond. Goldman Sachs is in urgent need of physical gold tonight as they are the major player standing for gold on the October 2020 contract .

NEW PLEDGED GOLD: BRINKS

592,648.822 oz NOW PLEDGED SEPT 15.2020/HSBC 18.433 TONNES ( A HUGE INCREASE FROM 10.6)

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

277,934.09 oz (some deleted august 3) JPM 8.644 TONNES

610,238.285 oz pledged June 12/2020 Brinks/ july 2/july 21 19.017 tonnes

51,084.609 oz Pledged August 21/regular account 1.588 tonnes jpm

total pledged gold: 1,574,454.119 oz 48.97 tonnes

total registered, pledged and eligible (customer) gold 36,833,435.618 oz 1,145.67 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1019.33 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

END

And now for the wild silver comex results

And now for the wild silver comex results

FINAL STANDINGS

SEPT. SILVER COMEX CONTRACT MONTH//INITIAL STANDING

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

655,412.325 oz

CNT

DELAWARE

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

1,758,362.99 oz

CNT

Scotia

|

| No of oz served today (contracts) |

12

CONTRACT(S)

(60,000 OZ)

|

| No of oz to be served (notices) |

0 contracts

nil oz)

|

| Total monthly oz silver served (contracts) | 11033 contracts

55,165,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 2 deposits into the customer account (ELIGIBLE ACCOUNT)

i)into JPMorgan: ZERO

ii) Into CNT: 568,705.600 oz

iii) Into Scotia: 1,189,657.390 oz

JPMorgan now has 183.738 million oz of total silver inventory or 48.96% of all official comex silver. (183.738 million/373.767 million

total customer deposits today: 1,758,362.99 oz

we had 2 withdrawals:

total withdrawals; 658,412.324 oz

We had 0 adjustments/

Total dealer(registered) silver: 142.345 million oz

total registered and eligible silver: 373,767 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

the front month of SEPTEMBER registered an open interest of 12 contracts thus losing 21 contracts. We had 13 notices filed on FRIDAY so we LOST 8 contracts or an additional 40,000 oz will NOT stand in this active delivery month of September as they morphed into London based forwards and thus they also accepted a fiat bonus for their effort. The boys no doubt are having trouble locating silver over here and thus they will try their luck over in London

Oct saw another loss of 29 contracts to stand at 1915. November GAINED 78 contracts to stand at 150,

The big December contract month saw its OI contract by 1693 contracts down to 130,375

The total number of notices filed today for the SEPT 2020. contract month is represented by 12 contract(s) FOR 60,000 oz

To calculate the number of silver ounces that will stand for delivery in SEPT we take the total number of notices filed for the month so far at 11,033 x 5,000 oz = 55,165,000 oz to which we add the difference between the open interest for the front month of SEPT( 12) and the number of notices served upon today 12 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the SEPT/2019 contract month: 11,033 (notices served so far) x 5000 oz + OI for front month of SEPT (12)- number of notices served upon today (12) x 5000 oz of silver standing for the SEPT contract month .equals 55,165,000 oz. ..VERY STRONG FOR AN ACTIVE MONTH.

We lost 8 contracts or AN ADDITIONAL 40,000 oz. WILL NOT STAND FOR DELIVERY IN THIS ACTIVE DELIVERY MONTH,

TODAY’S ESTIMATED SILVER VOLUME : 73,669 CONTRACTS // volume very good//

FOR YESTERDAY 95,228 ,CONFIRMED VOLUME// strong/

YESTERDAY’S CONFIRMED VOLUME OF 95,228 CONTRACTS EQUATES to 0.426 billion OZ 68.0% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 2.67% ((SEPT 28/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.70% to NAV: (SEPT 28/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/2.67%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 19.12 TRADING 18.42///NEGATIVE 3.66

END

And now the Gold inventory at the GLD/

SEPT 28//WITH GOLD UP $14.30 DOLLARS: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.05 TONNES INTO THE GLD//INVENTORY RESTS AT 1268.89 TONNES

SEPT 25//WITH GOLD DOWN 410.80 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .3 TONNES FROM THE GLD////INVENTORY RESTS AT 1266.84 TONNES

SEPT 24/WITH GOLD UP $9.80 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1267.14TONNES.

SEPT 23//WITH GOLD DOWN $28.00 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 11.68 TONNES FROM THE GLD////INVENTORY RESTS AT 1267.14 TONNES

SEPT 22/WITH GOLD DOWN $4.50 TODAY, A MONSTROUS CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 18.98 TONNES OF PAPER GOLD ENTER THE GLD///// INVENTORY RESTS AT 1278.62TONNES

SEPT 21/WITH GOLD DOWN $47.20 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 12.94 TONNES INTO THE GLD///INVENTORY RESTS AT 1259.64TONNES

SEPT 18/WITH GOLD UP $10.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS THIS WEEKEND AT: 1246.99 TONNES

SEPT 17/WITH GOLD DOWN $18.05 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD//INVENTORY RESTS AT 1246.99 TONNES

SEPT 16.WITH GOLD UP $4.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1247.57 TONNES

SEPT 15//WITH GOLD UP $2.25 TODAY: A SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .43 TONNES FROM THE GLD//INVENTORY RESTS AT 1247.57 TONNES

SEPT 14/WITH GOLD DOWN 90 CENTS TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.96 TONNES FROM THE GLD////INVENTORY RESTS AT 1248.00 TONNES

SEPT 11/WITH GOLD DOWN $14.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1252.96 TONNES

SEPT 10/WITH GOLD UP $8.85 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.92 TONNES INTO THE GLD////INVENTORY RESTS AT 1252.96 TONNES

SEPT 9/WITH GOLD UP $19.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1250.04 TONNES

SEPT 8/WITH GOLD UP $8.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1250.04 TONNES

SEPT 4//WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1250.04 TONNES

SEPT 3/WITH GOLD DOWN $7.50 ON THIS 2ND DAY OF A 3 DAY RAID: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1250.04 TONNES

SEPT 2/WITH GOLD DOWN $34.00 TODAY, WE HAVE 2 SMALL CHANGES IN GOLD INVENTORY AT THE GLD: 2 WITHDRAWALS OF .87 TONNES AND.59 TONNES FROM THE GLD////INVENTORY RESTS AT 1250.04 TONNES

SEPT 1/WITH GOLD UP $7.10 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1251.50 TONNES

AUGUST 31//WITH GOLD UP $5.90 TODAY/WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD..//INVENTORY RESTS AT 1251.50 TONNES/

AUGUST 28/WITH GOLD UP $38.20 TODAY, WE SURPRISINGLY HAD A .59 TONNE WITHDRAWAL//INVENTORY RESTS AT 1251.50 TONNES

AUGUST 27/WITH GOLD DOWN 17.50 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 3.24 TONNES INTO THE GLD//INVENTORY REST AT 1252.09 TONNES

AUGUST 26/WITH GOLD UP $26.70 TODAY/ WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.53 TONNES FROM THE GLD//RESTS AT 1248.85 TONNES

AUGUST 25/WITH GOLD DOWN $14.60 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//RESTS AT 1252.38 TONNES

AUGUST 24//WITH GOLD DOWN $7.20 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1258.38 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

SEPT 28/ GLD INVENTORY 1268.89 tonnes*

LAST; 908 TRADING DAYS: +329.48 NET TONNES HAVE BEEN ADDED THE GLD

LAST 808 TRADING DAYS://+508.01 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 28/WITH SILVER UP 48 CENTS TODAY: A HUGE DEPOSIT OF 3.769 MILLION OZ CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.791 MILLION OZ//

SEPT 25/WITH SILVER DOWN 14 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: 2 TRANSACTIONS: A PAPER WITHDRAWAL OF 8.28 MILION OZ FROM THE SLV AND A DEPOSIT OF 1.861 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 547.022 MILLION OZ//

SEPT 24//WITH SILVER UP 15 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 553.443 MILLION OZ//

SEPT 23//WITH SILVER DOWN $1.41: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.048 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 553.443 MILLION OZ///

SEPT 22/WITH SILVER DOWN ONE CENT TODAY: A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.141 MILLION OZ////INVENTORY RESTS AT 555.491 MILLION OZ..

SEPT 21/WITH SILVER DOWN $2.43 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV A PAPER WITHDRAWAL OF 1.862 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 553.350MILLION OZ//

SEPT 18. WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 555.212 MILLION OZ/

SEPT 17/WITH SILVER DOWN 31 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.537 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 555.212 MILLION OZ/

SEPT 16//WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.749 MILLION OZ//

SEPT 15/WITH SILVER UP 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.793 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 558.749 MILLION OZ..

SEPT 14/WITH SILVER UP 47 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS A) 1.675 MILLION OZ AND ANOTHER B) 0.931 MILLION OZ/ FROM THE SLV////INVENTORY RESTS AT 555.956 MILLION OZ//

SEPT 11/WITH SILVER DOWN 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.562 MILLION OZ//

SEPT 10/WITH SILVER UP 16 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.607 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 558.562 MILLION OZ.

SEPT 9/WITH SILVER UP 6 CENTS TODAY: STRANGE: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.63 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 561.169 MILLION OZ

SEPT 8/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 564.799 MILLION OZ

SEPT 4//WITH SILVER DOWN 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 3.631 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 564.799 MILLION OZ//

SEPT 3//WITH SILVER DOWN 50 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.258 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.430 MILLION OZ/./

SEPT 2.WITH SILVER DOWN $1.04 TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.365 MILLION OZ FROM THE SLV///INVENTORY REST AT 571.688 MILLION OZ.

SEPT 1//WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 31/WITH SILVER UP 80 CENTS TODAY: A HUGE CHANGE IN THE SLV//A DEPOSIT OF 2.982 MILLION OZ ENTERS THE SLV/INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 28/WITH SILVER UP 48 CENTS TODAY: A MASSIVE PAPER DEPOSIT OF 4.652 MILLION OZ ENTERS THE SLV//INVENTORY RESTS AT 571.071 MILLION OZ

AUGUST 27/WITH SILVER DOWN 28 CENTS TODAY// NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.419 MILLION OZ

AUGUST 26//WITH SILVER UP $1.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.65 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 566.419 MILLION OZ..

AUGUST 25/WITH SILVER DOWN 21 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.607 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 571.074 MILLION OZ//

AUGUST 24//WITH SILVER DOWN 18 CENTS TODAY: WE HAD A NO CHANGES//INVENTORY RESTS AT 573.843 MILLION OZ//

SEPT 28.2020:

SLV INVENTORY RESTS TONIGHT AT

550.791 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

Ron Paul doing fine recovering from a stroke like incident

(CNN.com/GATA)

Ron Paul recovering after stroke-like incident

Submitted by cpowell on Fri, 2020-09-25 23:58. Section: Daily Dispatches

From CNN.com, New York

Friday, September 25, 2020

Former Texas congressman Ron Paul was hospitalized today after an apparent medical episode but is now “doing fine,” according to a tweet posted to his Twitter account.

Paul — a well-known libertarian, three-time presidential candidate, and the father of Republican Kentucky Sen. Rand Paul — was seen slurring his words during a livestream on his YouTube channel today. The video has since been removed.

“Message from Ron Paul: ‘I am doing fine. Thank you for your concern,'” a tweet posted on the former congressman’s account stated, which also included an image of Paul, who is 85, sitting up and smiling from a hospital bed.

Rand Paul also tweeted out a brief statement, saying, “Thank God, Dad is doing well. Thank you for all your prayers today.” …

… For the remainder of the report:

https://www.cnn.com/2020/09/25/politics/ron-paul-hospitalized/index.html

end

Hugo…

a great history listen from Hugo Salinas Price and why the return to gold is the only way we can solve our problems

(Hugo Salinas Price/GATA)

Hugo Salinas Price: A tale of two revolutions

Submitted by cpowell on Sat, 2020-09-26 00:12. Section: Daily Dispatches

8:13p ET Friday, September 25, 2020

Dear Friend of GATA and Gold:

Removing the U.S. dollar’s direct convertibility to gold, the Mexican Civic Association for Silver’s Hugo Salinas Price writes today, led to the country’s deindustrialization and the demoralization of its working class. Salinas Price’s commentary is headlined “A Tale of Two Revolutions” and it’s posted at the association’s internet site, Plata.com, here:

http://plata.com.mx/enUS/More/395?idioma=2

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Vorley and Chanu convicted of spoofing. The authorities continue to go after spoofing which is minor to what these guys have done

(Bloomberg/GATA)

Former Deutsche Bank gold traders found guilty in spoofing trial

Submitted by cpowell on Sat, 2020-09-26 02:50. Section: Daily Dispatches

By Janan Hanna and Stephen Joyce

Bloomberg News

Friday, September 25, 2020

Prosecutors behind a sweeping U.S. crackdown on market “spoofing” scored a big win Friday when former Deutsche Bank AG traders Cedric Chanu and James Vorley were convicted of fraud for manipulating gold and silver prices.

A federal jury in Chicago, after three days of deliberations, concluded Chanu and Vorley made bogus trade orders between 2008 and 2013 to illegally influence precious-metals prices. The weeklong trial was the latest U.S. prosecution of a “spoofing” case since the global market “flash crash” in 2010

Chanu and Vorley engaged in a classic “bait and switch” by placing orders they never intended to execute and then canceling them, which “weaponized” the forces of supply and demand to mislead other traders, prosecutor Brian Young told jurors in closing arguments Tuesday.

Spoofing occurs when a trader enters buy or sell orders and then cancels them before they are executed, creating a false market indicator that can generate profit by taking the opposite position. While canceling orders isn’t prohibited, the 2010 Dodd-Frank Act made it illegal to place orders with no intention of executing them.

Transcripts of messages the two traders sent show they knew what they were doing was wrong, Young said. In one instance, Vorley wrote: “This spoofing is annoying me. It’s illegal for a start.” …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2020-09-25/ex-deutsche-bank-gold…

end

Ex-Deutsche Bank Gold Traders Found Guilty in Spoofing Trial

Prosecutors behind a sweeping U.S. crackdown on market “spoofing” scored a big win Friday when former Deutsche Bank AG traders Cedric Chanu and James Vorley were convicted of fraud for manipulating gold and silver prices.

A federal jury in Chicago, after three days of deliberations, concluded Chanu and Vorley made bogus trade orders between 2008 and 2013 to illegally influence precious-metals prices. The weeklong trial was the latest U.S. prosecution of a “spoofing” case since the global market “flash crash” in 2010.

Chanu and Vorley engaged in a classic “bait and switch” by placing orders they never intended to execute and then canceling them, which “weaponized” the forces of supply and demand to mislead other traders, prosecutor Brian Young told jurors in closing arguments Tuesday.

Spoofing occurs when a trader enters buy or sell orders and then cancels them before they are executed, creating a false market indicator that can generate profit by taking the opposite position. While canceling orders isn’t prohibited, the 2010 Dodd-Frank Act made it illegal to place orders with no intention of executing them.

Transcripts of messages the two traders sent show they knew what they were doing was wrong, Young said. In one instance, Vorley wrote: “This spoofing is annoying me. It’s illegal for a start.”

The star witness at the trial was their former Deutsche Bank coworker, David Liew, who told the jury he learned from Chanu and Vorley how to use spoof trades to manipulate prices. Liew faces his own criminal charges and agreed to cooperate with the government.

Read More: Spoofing Is a Silly Name for Serious Market Rigging

Chanu was convicted on seven fraud counts and Vorley on three counts, while they were found not guilty of other charges, including conspiracy. Each count carries a maximum penalty of 30 years in prison, though U.S. District Judge John Tharp said the government would seek about four or five years. Sentencing was set for Jan. 21, and both men remain free on bail.

Vorley’s attorney, Roger Burlingame, said he’ll appeal the conviction. He called the prosecution “misguided” because his client’s trading was “well within the law.”

“It was a compromise verdict by a jury that three times declared it was deadlocked, deliberating in the face of a Covid scare,” Burlingame said. The jury had been reduced to 11 after one juror complained of coronavirus-like symptoms and was dismissed. “The record is clear there was no fraud. The compromise conviction will not stand.”

Chanu’s attorney, Michael McGovern, said in an email that he was “gratified that the jury unanimously acquitted Cedric on the conspiracy and other charges, and we intend to continue the fight as to the remaining charges.”

The prosecutor declined to comment after the verdict.

Since anti-spoofing laws passed under the Dodd-Frank financial reforms a decade ago, the U.S. has prosecuted about a dozen criminal cases, including Navinder Sarao, the British day trader linked to the 2010 “flash crash” that erased $1 trillion in market value.

The Commodity Futures Trading Commission also has stepped up civil complaints and reached many settlements, including a $30 million deal with Deutsche Bank in 2018. JPMorgan Chase & Co. is poised to pay close to $1 billion to resolve market manipulation investigations by U.S. authorities into its trading of metals futures and Treasury securities, Bloomberg reported Wednesday.

Mixed Results

While prosecutors have secured several guilty pleas in spoofing cases — including Liew, Sarao and others — they’d had mixed results at trial.

In 2015, Michael Coscia was convicted in Chicago and sentenced to three years in prison. In 2018, Andre Flotron was acquitted after a federal judge in Connecticut threw out most of the charges on the grounds that the case should have been brought in Chicago, where the trading occurred. Last year, the case against Chicago programmer Jitesh Thakkar, the first non-trader prosecuted under anti-spoofing laws, ended in a mistrial and charges were dropped.

Defense lawyers for Chanu and Vorley didn’t present any witnesses at the trial. While questioning prosecution witnesses, they emphasized how difficult it is to determine criminal intent for “spoofing” in competitive global markets where traders keep strategies secret and try to outmaneuver rivals. The defense team cited several examples of legal trading practices that allow market players to hide their intentions from everyone else.

“If you fake a pass and run the ball, that’s competition, not fraud,” Burlingame told the jurors during closing arguments Tuesday. Every order placed by Vorley was “100% real,” Burlingame said.

The case is U.S. v. Vorley 18-cr-35, Northern District of Illinois (Chicago).

Doug Pollitt: MMT’s Stephanie Kelton meets the grifter of imperial France, John Law

Submitted by cpowell on Sun, 2020-09-27 01:02. Section: Daily Dispatches

9:21p ET Saturday, September 26, 2020

Dear Friend of GATA and Gold:

In his September letter for clients, Doug Pollitt of Pollitt & Co. in Toronto compares Modern Monetary Theory advocate Stephanie Kelton’s new book, “The Deficit Myth,” with a recent biography of a monetary theorist of three centuries ago, the infamous John Law, and concludes that the policies they pursued are essentially identical — infnite money.

Law’s policy brought down the government of imperial France in only four years in the 1700s. Kelton may not quite realize it, but the policy she advocates has been in force in the United States since long before she began writing about it. (Yes, the United States still issues debt instruments but debt that keeps growing rapidly, never can be repaid except in devalued currency, and is treated as money itself is no debt at all but the equivalent of new money, just as it was in Law’s time.)

Pollitt acknowledges that infinite money policy has had a much longer run in the United States — almost 50 years, figuring its duration from the termination of the dollar’s official convertibility to gold in 1971 — that it had in imperial France and that it might continue a lot longer even as the dollar devalues gradually instead of collapsing.

While only a high school graduate, your secretary/treasurer, by virtue of closely observing for 20 years the racket called the gold market, would add something else the MMT people don’t recognize and Pollitt doesn’t mention. That is, MMT, essentially infinite money, gains endurance from, and indeed requires, something the French regency of Law’s day lacked — an efficient mechanism of surreptitiously suppressing commodity prices and pushing infinite money creation into financial assets so the devaluation of the currency is more or less concealed from the masses.

Futures markets in which the government intervenes behind the cover of intermediary brokers have done the job nicely, though at the enormous cost of destroying the market economy, impoverishing the working class, enriching the ownership class, and exploding economic inequality.

Documenting and publicizing this is GATA’s tedious work, and since it is not respectable work, it would be a lot easier if respectable academics like Kelton suspended their theorizing long enough to join us in pressing the government with a few critical questions about its interventions. This wouldn’t require writing a book. The questions would fit on one sheet of paper, and even widely reporting the government’s refusal to answer them might shake the financial world far more than any theory.

Pollitt’s letter is fascinating reading and with his kind permission it is posted in PDF format at GATA’s internet site here:

http://gata.org/files/DougPollitt-KeltonMeetsLaw.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Eric Sprott talks about last week’s poor showing for gold and silver and concludes like Chris Powell that there are no markets, just interventions

(Craig Hemke/Sprott/GATA)

Lousy week for monetary metals prompts Sprott to quote GATA secretary

Submitted by cpowell on Sat, 2020-09-26 00:59. Section: Daily Dispatches

9p ET Friday, September 25, 2020

Dear Friend of GATA and Gold:

Beginning his review of a lousy week for the monetary monetary metals with Craig Hemke for Sprott Money, mining entrepreneur Eric Sprott quotes your secretary/treasurer’s observation at GATA’s Washington conference in 2008: “There are no markets anymore, just interventions.” (See: http://gata.org/node/6242.)

Sprott says he is “very suspicious of all that’s taking place in the markets” these days, prompting Hemke to note the reports this week that JPMorganChase is preparing to pay a billion-dollar fine for manipulating the monetary metals markets.

Sprott replies that Morgan has been doing far worse than the “spoofing” that its traders have confessed to.

On another matter, Sprott says that the coronavirus over which national economies are being curtailed is not as dangerous as it is being made out to me. He asks: What are the damages resulting from inducing an economic depression?

Nevertheless, Sprott says, he is expecting good earnings reports and dividend increases from monetary metals mining companies.

He concludes by discussing the prospects for several companies in which he has an interest.

The interview is 19 minutes long and can be heard at Sprott Money here:

https://www.sprottmoney.com/blog/Precious-Metals-Take-the-Escalator-Up-E…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

end

iii) Other physical stories:

J Johnson’s commodity report

https://www.jsmineset.com/2020/09/28/mr-resolute-steps-into-sept-silver-on-the-last-day/

Mr. Resolute Steps Into Sept Silver On The Last Day

Posted September 28th, 2020 at 9:20 AM (CST) by J. Johnson & filed under General Editorial.

Great and Wonderful Monday Morning Folks,

Gold is trading down $6.30 with the price at $1,860, right smack in the middle of the range between $1,869.10 and $1,851.10. Silver is flat to lower with the last trade at $23.02, down 7.3 cents after the dip down to $22.61 with the high to beat at $23.19. The US Dollar is not as flat as the metals with its value losing 42.2 points with the calculated value at 94.25, one point off the low with the high at 94.67. Of course, all this happened before 5 am pst, the Comex open, the London close, and after Project Veritas, a real news service, totally exposes the frauds that are called Ilhan Omar and her connection to a “car full” of already filled out – absentee ballots.

Gold in Venezuela now has an 18,576.75 Bolivar price attached to it showing a 12.98 pullback from Friday’s price with Silver now at 229.912 providing the holder a 1.797 Bolivar gain. In Argentina, Gold’s value is now at 140,933.73 A-Peso’s providing the holder a gain of 195.53 with Silver now at 1,744.24, already giving Friday’s buyer a 16.47 A-Peso profit. Turkey’s Lira popped in a gain of 306.76 for the Friday buyer with the price for Gold now at 14,496.99 T-Lira’s with Silver’s last trade at 179.504 T-Lira, a gain of 5.341.

September Silver’s last day of delivery now has a Demand Count of 12 fully paid for 5,000-ounce contracts waiting for delivery with a Volume of 41 already up on the board with a trading range between $22.74 and $22.695 with the last swap at the low, down 32.2 cents. That’s only an addition of 205,000 ounces of the real stuff, Hello Mr. Resolute! Friday’s delivery activity happened in between $22.98 and $22.73 with the last swap at the high, that also had a Volume of 21, which in turn, reduced the delivery demands by the same quantity (FIFO?), with that Calculated Close at $23.07, where no trade was made. Silver’s Overall Open Interest continues to wane with the count now at 153,396 short contracts, that go against the physicals, proving a reduction of 1,611 Overnighters since Friday mornings tally.

This morning’s September Delivery Demands in Gold, now has a total of 48 fully paid for 100-ounce contracts waiting for receipts, with a Volume of 19 already up on the board, yet with no trading range or price. Friday’s delivery activity happened with one price, at $1,856.30, and still a CCC had to be applied at $1,857.70, giving the noble metal a loss of $10.60 and only because of the papers, also reducing the delivery count by 180 contracts that might have gotten their receipts between here and London. Gold’s Overall Open Interest now has a total of 559,438 Overnighters, showing the continuing paper reduction with today’s early morning count taking away 2,479 short contracts that go against the physicals.

Friday evening, after all the markets closed, the DOJ reported that two former Deutsche Bank traders were convicted of engaging in deceptive and manipulative trading practices in our U.S. Commodities Markets. Towards the end of the article, it claims that “Individuals who believe that they may be a victim in this case should visit the Fraud Section’s Victim Witness website for more information”. If one is crazy enough to trade the markets, they may consider adding their names to the list. There may never be a return from these organized thefts from all the banks, but at the very least, it may provide a number of people and entities that were robbed daily by the central banks and friends, with their practices, helping to prove how bad the system really is, when the convicted NEVER have to give back money to those they stole from, and how the CFTC takes what it needs via their penalties, and allows the thieves, under their watch, to thrive.

The first 2020 presidential debate will be held tomorrow, at 5:00 pm pst with Trump asking for a Pre and Post Debate – drug test for himself and sleepy Joe. Now that we have several, factual, and “live”, evidence of ballot harvesting, I expect another category to be brought up during the debates. I really do believe the debates are absolutely necessary for both sides, and fun to watch, seriously. After all, it’s “Politics American Style”! I also think there should be an open forum, not just a list of topics. The best part will be those witty comebacks, that add so much to it all.

So smile, and hang on tight to the physicals, while we make it thru the last delivery day of September, the presidential debates, and the end of the 2020 fiscal year. What can go wrong, if one holds physical Silver and Gold? As always …

Stay Strong!

Jeremiah Johnson

More J.Johnson content is available with purchase of a JSMineset subscription.

end

We brought the Swiss data on exports/imports to you last week.

Of note: the huge fall in USA receiving Swiss gold (28 tonnes)

the 26 tonnes of gold exported by the USA is dore plus comex gold leaving the vaults.

LAWRIE WILLIAMS: Swiss gold imports suggest some profit-taking, but exports to India pick up

Switzerland remains an important conduit for the movement of refined gold around the world and the volume handled each year by the small Alpine nation’s gold refineries is equivalent to over half annual new mine global gold output. Given that China remains the world’s largest producer of gold annually (about 11% of global gold output), and exports none of this production, Switzerland’s dominance of overall movements of global refined gold becomes even more significant, so its announced monthly gold import and export figures are of particularly strong interest to gold followers.

This year we will almost certainly see an overall reduction in global new mined gold production, if only because of temporary closures and coronavirus mitigation measures imposed on some key gold mining operations. The industry was already hovering at, or close to, peak gold production so any such measures will have resulted in an overall fall anyway. So far this year Swiss gold imports have totalled 1,071 tonnes, equivalent to a 2020 first half output total of a little over 800 tonnes – which works out at almost exactly 50% of the World Gold Council’s latest estimate of global gold production in the first half of the year.

Swiss gold exports so far this year come to a rather lower 782 tonnes, but appear to be picking up. The shortfall is so far due to a drastic reduction in the export of Swiss gold to its traditional main markets in Asia and the Middle East. However the figure for gold exports in August show a big pick-up in the volume going to the world’s second largest consuming nation – India – which took 22 tonnes and what may be the beginnings of an important rise from the world’s largest consumer – mainland China – which took 9.6 tonnes. Perhaps significantly, Singapore which is making an attempt to rival Hong Kong as the region’s principal financial and trading centre, imported 6.6 tonnes. Interestingly no gold appears to have been exported to Hong Kong in August, further emphasising the decline of the Chinese autonomous territory in international gold trade, and as a proxy for Chinese gold imports.

The two charts below are from Nick Laird’s goldchartsrus.com website in Australia. Nick offers a statistical and graphical service covering many aspects of the international trade in gold.

The other principal recipients of the Swiss gold exports were the U.S. with 28.2 tonnes. The UK, which vaults a high proportion of ETF gold holdings, with 18.9 tonnes, Turkey, which is rapidly building its gold reserves, with 18.1 tonnes and France with 6.0 tonnes. Other European nations to figure were Germany with 2.9 tonnes and tiny Austria with 1.6 tonnes – both countries known for strong interest in investment gold.

The Swiss import statistics also throw up some interesting trends – albeit a continuation of other recent Swiss gold movement data. In addition to importing gold from many gold mining nations, probably as doré bullion, it also received considerable amounts from some traditional gold consumers – notably Hong Kong from which it received 25.5 tonnes, Thailand (27.4 tonnes), the United Arab Emirates (15.4 tonnes) and Italy (7.3 tonnes). These imports will have come from the running down of stocks due to reduced demand, and also due to profit taking as gold prices peaked in August. Imports from France were also interesting as they included a substantial amount of gold coins for remelting and re-refining – perhaps also an indicator of increasing scrap sales, again probably because of the attraction of high gold prices.

The other anomalous figure in the Swiss import statistics is the volume imported from the U.S. at 26.3 tonnes. The U.S. is a major gold producer in its own right but does not mine as much as 26 tonnes in a month. Last year, according to Metals Focus, it produced around 200 tonnes (16.66 tonnes a month on average) so the August total likely includes a substantial portion of gold scrap – as well as liquidated gold coins – which would again be a result of profit taking. However an almost identical amount came back as re-refined, probably higher-purity gold, leaving a net balance of near zero. There was undoubtedly demand for high purity refined gold, but perhaps in small sizes which could meet individual investor demand. It will be interesting to see what happens with the September figures given the sharp fall in the gold price.

Overall therefore, the Swiss import and export figures provide an extremely interesting insight into international gold flows with the small country punching way beyond its weight in terms of gold refining and distribution.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

“It’s Hard To Become Too Bearish”: Futures Surge Amid Optimism Selloff Has Gone Too Far

US stocks future indexes rose on Monday following Friday’s gains and tracking major gains in European and Asian markets amid optimism that the recent selloff in equity markets is overdone. The dollar weakened and Treasury yields rose. The pound strengthened on hopes that U.K. and European Union officials will be able to make progress as a key week of Brexit talks begins, while the Turkish lira crashed to a new all time low on fears the country would be dragged into the sudden breakout of war between Armenia and Azerbaijan.

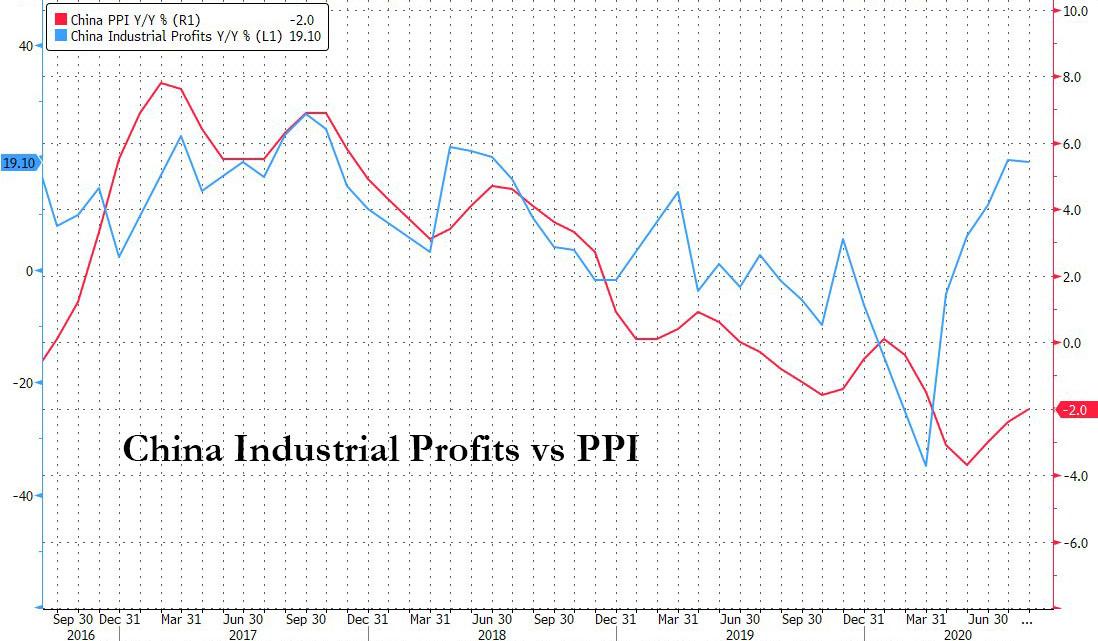

Hopes of a global economic recovery were supported by data showing continued growth in China’s industrial profits, despite fresh concerns that China’s data is once again being manipulated for political purposes with profits diverging massively from PPPI.

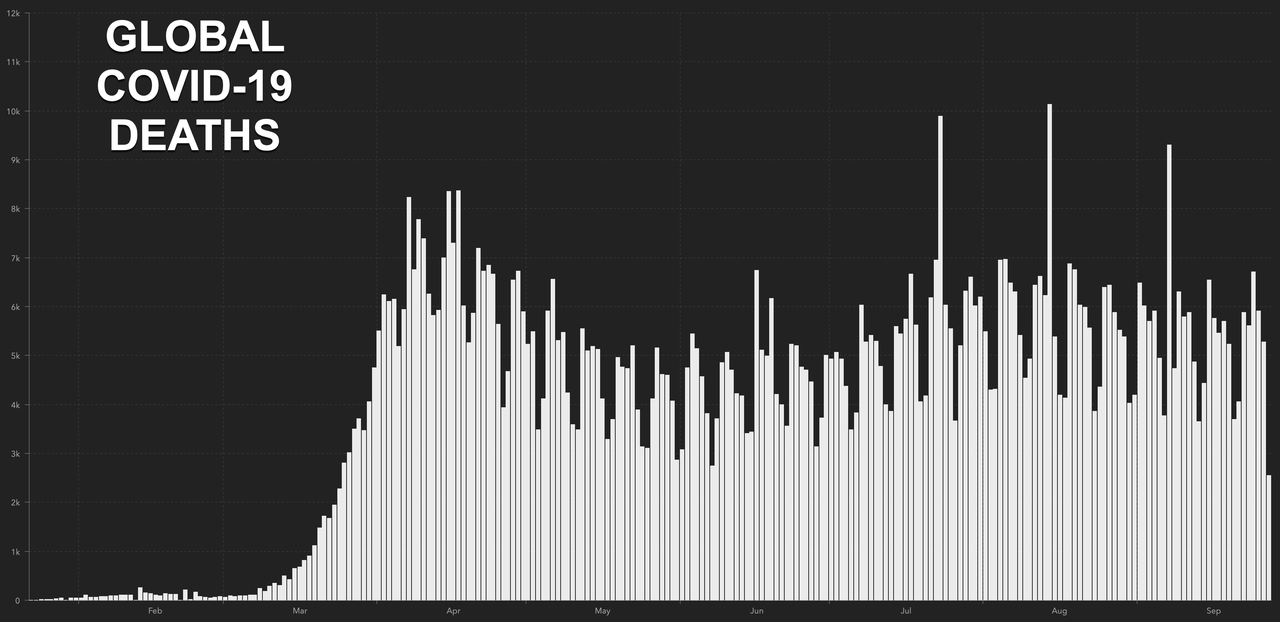

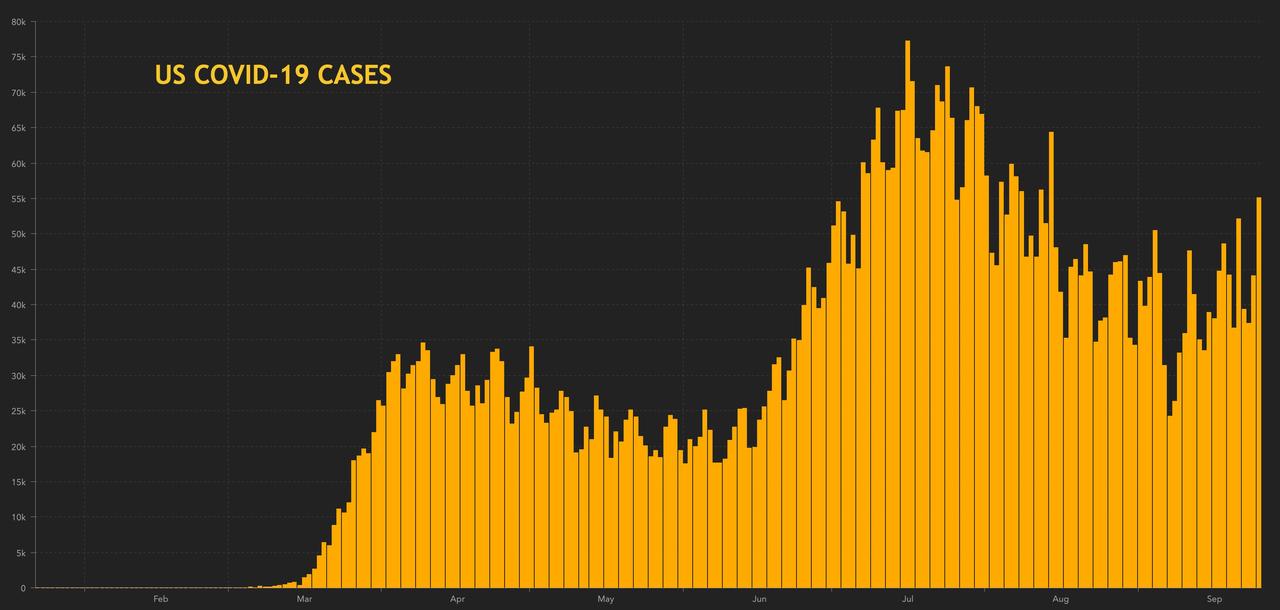

Shares of American Airlines, United Airlines, cruise operators Royal Caribbean Cruises Ltd and Carnival Corp rose between 2.5% and 5.6% in premarket trading as sentiment on covid-linked names reversed despite a continued rise in officially reported cases. The global death toll from Covid-19 will likely pass 1 million today, with cases already above 33 million. The milestone will be passed as governments continue to struggle to contain the disease, with authorities in many countries imposing or extending measures. The Times in London is reporting that the city may be forced into another lockdown. New York officials are concerned about localized spikes in infections, even as the city-wide rate remains low.

Late on Friday, American Airlines said it has secured a $5.5 billion Treasury loan and could tap up to $2 billion more in October depending on the allocation of extra funds under a $25 billion loan package for airlines. Uber surged in U.S. pre-market trading after a judge ruled that the ride-hailing app is “fit and proper” to operate in London. The FAAMG stocks rose between 1.1% and 2.2% as Nasdaq futures surged.

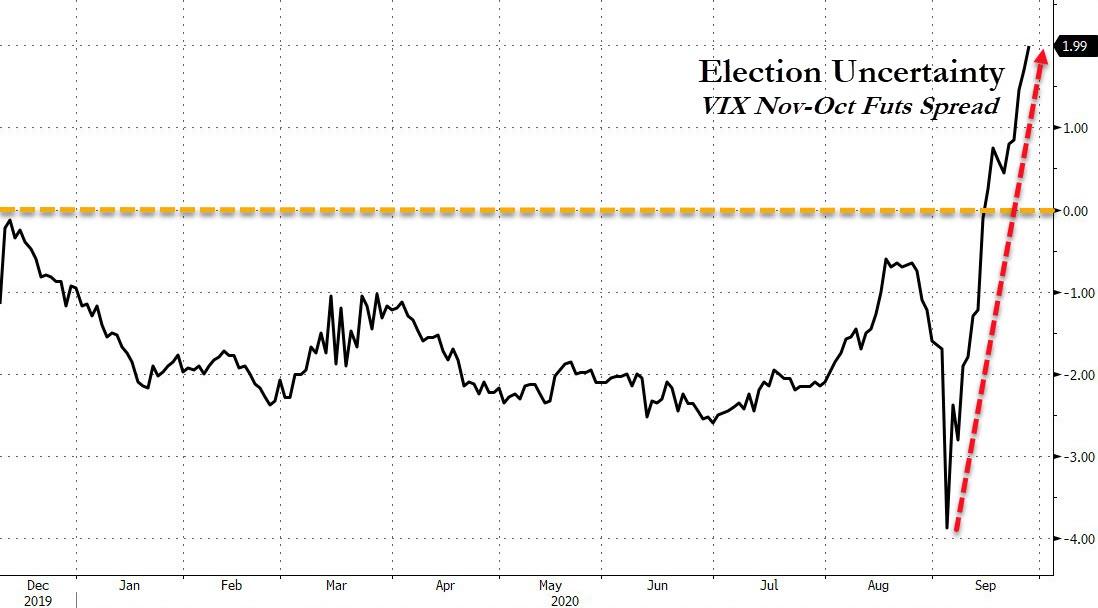

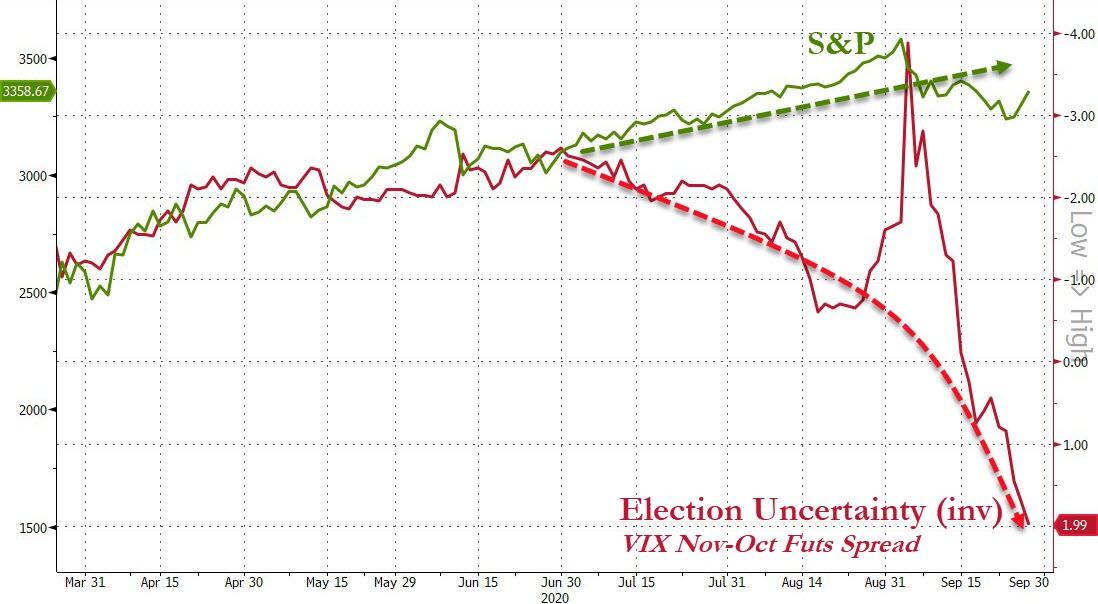

Global markets started the week solidly in the green, following Wall Street’s main indexes higher on Friday, helped by technology stocks, but the Dow Jones and the S&P 500 indexes posted their longest weekly losing streaks in a year on fears of a slowing pace of economic growth. Worries over rising coronavirus cases and waning hopes of more fiscal stimulus have led to a spike in market volatility in the past few weeks, and analysts expect trading to remain choppy in the run up to the Nov. 3 presidential election. The VIX spiked to its highest in nearly two weeks last Monday, with analysts warning of further upside to the index heading toward the end of the quarter, and Morgan Stanley warning of a “difficult trading environment” in the next 4-5 weeks.

Stocks also rose on lingering hopes a fiscal deal may still happen before the election. The rapidly diminishing chances of a new fiscal stimulus package ahead of the election got a modest kick after Speaker Nancy Pelosi said Democrats would unveil a new “proffer” shortly, adding that she would prefer the House majority to pass an actual deal than simply vote on a package that would be dead on arrival in the Senate. While there were some talks between Pelosi and Treasury Secretary Steven Mnuchin on Friday, the continuing deep divides on the size of any package and the very short timeline to the election means lawmakers remain skeptical a breakthrough is possible

The Europe Stoxx 600 Index rose more than 2% rebounding from the biggest weekly drop in more than three months as banks rallied the most in three weeks leading the advance among sectors. HSBC Holdings surged 9%, its biggest one-day gain since 2009 after Ping An Insurance Group, its biggest shareholder, raised its stake in the lender to 8%, in a bet the embattled lender will return to paying dividends and said it “remains confident” in HSBC’s long-term prospects.

European carmarkers rallied following comments from Nissan Motor that the company expects to return to profitability in 2021. Diageo rose after saying it expects business to improve as bars and restaurants reopen.

“It is hard to become too bearish,” said Mark Dowding, the chief investment officer at BlueBay Asset Management. “As we look into 2021, growth should be stronger, policy will stay supportive with further fiscal spending. A vaccine is also expected to be deployed and life to return closer to normal by the middle of next year.”

“Investors grapple with many variables that could bring increasing amounts of volatility in the week ahead,” said Hussein Sayed, chief markets strategist at FXTM.

Optimism spilled over from Asian trading hours after data over the weekend showed profits at China’s industrial firms grew for the fourth straight month in August.

Earlier in the session, Asian stocks gained, led by IT and industrials, after rising in the last session. Most markets in the region were up, with Taiwan’s Taiex Index gaining 1.9% and Japan’s Topix Index rising 1.7%, while Jakarta Composite dropped 0.8%. The Topix gained 1.7%, with Careerlink and Scala rising the most. The Shanghai Composite Index was little changed, with Shanghai Zijiang Enterprise Group advancing and Ribo Fashion declining the most.

At the same time, Bloomberg notes that tension between Beijing and Washington continues to simmer. President Donald Trump’s ban on TikTok was temporarily blocked by a federal judge, dealing a blow to the government in its showdown with the popular Chinese-owned app over national security concerns. China’s largest chipmaker, Semiconductor Manufacturing International Corp., sank to a four-month low in Hong Kong after the U.S. imposed export restrictions.

In rates, treasuries bear steepened, with long-end yields cheaper by ~2bp vs. Friday close as the the risk-on backdrop weighed on long-end. Treasury 10-year yields cheaper by 1.5bp at ~0.67%, trading broadly in line with bunds; gilts lag by ~1.2bp. Month-end flows may also support long-end with with Bloomberg Barclays U.S. Treasury index to extend by 0.09y, more than usual October extension. IG credit issuance slate includes AngloGold Ashanti Holdings 10Y; $25bn expected to price this week

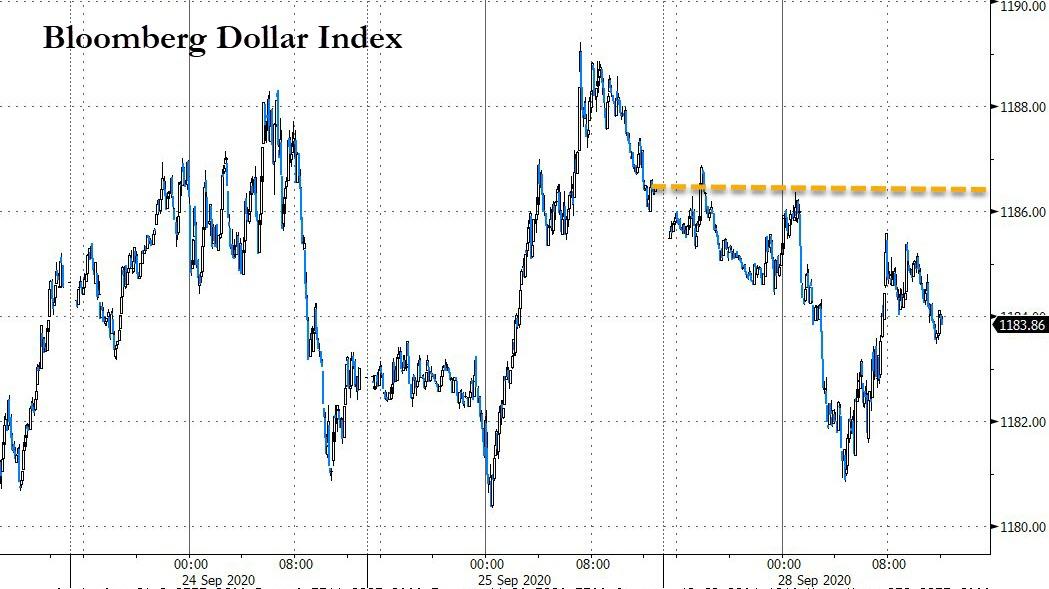

In FX, the Bloomberg Dollar Spot Index retreated from a two-month high reached on Friday, and the greenback fell versus most of its Group-of-10 peers. The pound was on track for its biggest gain this month, even with the EU stiffening its demands over how any trade deal will be enforced after losing trust in Boris Johnson because of his attempt to rewrite last year’s divorce agreement. The Canadian dollar was the weakest performer as oil prices struggled to build on recent gains. Australian dollar edged up as investors unwound short positions after Westpac pushed out its forecast for RBA easing to Nov. 3 from Oct. 6. Aussie bond futures drop briefly before recovering. Japan’s currency caught a bid after The Times of London reported the U.S. may relocate American assets away from an airbase in Turkey to Crete to boost its military presence in the eastern Mediterranean

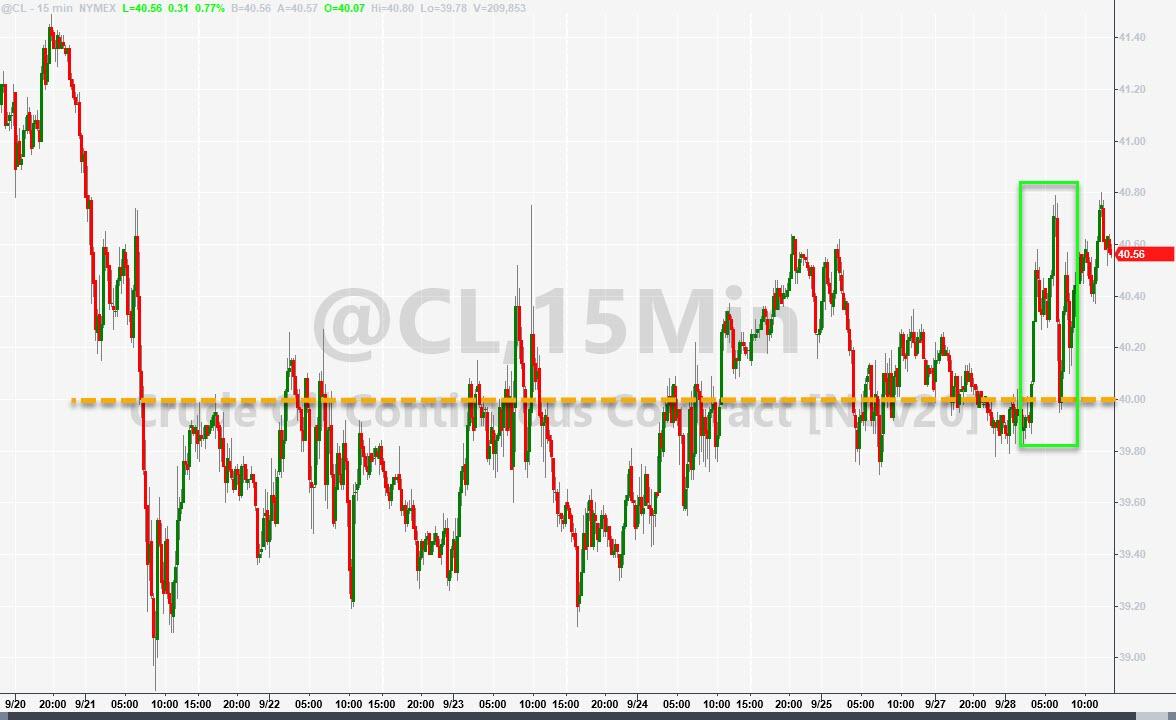

In commodities, oil and the dollar traded lower, while gold rebounded after hitting extremely oversold territory, aided by the drop in the dollar.

On today’s data calendar, we have the Dallas Fed Manufacturing Outlook, while Thor Industries and Cal-Maine Foods are set to report earnings.

Market Snapshot

- S&P 500 futures up 0.9% to 3,316.75

- STOXX Europe 600 up 1.7% to 361.53

- Brent Futures down 0.6% to $41.65/bbl

- Gold spot down 0.4% to $1,854.14

- U.S. Dollar Index down 0.2% to 94.45

- German 10Y yield rose 1.4 bps to -0.515%

- Euro up 0.04% to $1.1636

- Brent Futures down 0.6% to $41.65/bbl

- Italian 10Y yield fell 0.8 bps to 0.682%

- Spanish 10Y yield fell 0.3 bps to 0.245%

- MXAP up 1.1% to 170.21

- MXAPJ up 0.7% to 551.50

- Nikkei up 1.3% to 23,511.62

- Topix up 1.7% to 1,661.93

- Hang Seng Index up 1% to 23,476.05

- Shanghai Composite down 0.06% to 3,217.54

- Sensex up 1.6% to 37,968.28

- Australia S&P/ASX 200 down 0.2% to 5,952.32

- Kospi up 1.3% to 2,308.08

Top Overnight News from Bloomberg

- The Bank of England’s discussions on negative interest rates have been “encouraging,” according to policy maker Silvana Tenreyro, in a sign that the U.K. could yet follow peers such as the European Central Bank below zero

- London’s major clearinghouses for derivatives, energy and metal trades will be able to do business with banks in the European Union next year in a move that averts Brexit market disruption

- Bank of America Corp. and Lloyds Banking Group Plc have completed one of the first cross-currency swaps using Libor’s replacements, marking the latest step in the long exodus out of the scandal-tainted rate

- Safe-haven assets seen as traditional hedges aren’t panning out as they once did, according to JPMorgan Chase & Co. Easy- money policies may actually be keeping investors in cash and away from other traditional buffers, strategists led by John Normand wrote in a note Friday. That’s because such policies create a zero-yield environment where cyclical assets might be too difficult to hedge, they said

- A Conservative Party rebellion against Boris Johnson’s emergency coronavirus powers is gaining momentum after opposition parties signaled their support

- Battle lines are being drawn at the heart of the European Central Bank over whether to add monetary support soon to head off any economic slowdown, or wait for stronger evidence that it’s needed

A quick look at global markets courtesy of NewsSquawk:

Asian stocks began the week mostly higher, but ultimately finished mixed, as the region initially picked up the baton from last Friday’s tech-driven momentum on Wall Street. ASX 200 (-0.2%) and Nikkei 225 (+1.3%) were initially positive with Australia led by tech as the sector followed suit from US peers and with sentiment mildly underpinned by news Victoria state is to speed up its easing of COVID-19 restrictions. However, gains were capped and price action weighed on due to weakness in consumer staples and financials, while Tokyo stocks largely shrugged off a choppy currency. Hang Seng (+1.0%) and Shanghai Comp. (U/C) finished mixed mixed with underperformance in the mainland following a net liquidity drain by the PBoC and as participants digested the latest developments between the world’s 2 largest economies. This includes the US federal judge decision to grant a preliminary injunction against President Trump’s ban on TikTok downloads from US app stores which had been set to take effect from midnight, while SMIC shares slumped after the US Commerce Department announced tighter restrictions on China’s largest chipmaker on allegations that exports to the Co. posed an unacceptable risk of being diverted to military end-use. Nonetheless, the mood in Hong Kong was more constructive with HSBC registering its biggest intraday gain in over a decade after Ping An Insurance acquired 10.8mln H-shares to boost its stake to 8%. Finally, 10yr JGBs were rangebound with price action sideways as demand is sapped by the mildly positive risk tone but with downside stemmed amid the BoJ’s presence in the market for a total of JPY 900bln of JGBs.

Top Asian News

- Singapore Regulator, Banks in Talks to Extend Debt Relief Scheme

- Credit Suisse’s Pozsar Warns of Funding Flood: Liquidity Watch

- Betting on Yen Strength Is More Popular Than Ever Among Funds

Stocks in Europe kicked the week off higher across the board (Euro Stoxx 50 +2.1%) following a relatively mixed APAC session, with gains in Europe more pronounced than performance in State-side equity futures at present. Broad-based gains were seen across European bourses at the cash open, but since then Germany’s DAX (+2.6%) emerged as the front runner, whilst the UK’s FTSE 100 (+1.4%) waned on a currency dynamics and Switzerland’s SMI (-0.6%) remains the laggard due to a losses in large-cap stocks including Roche (-0.7%) and Nestle (-0.3%). Sectors are higher across the board with a cyclical/value tilt – with Banks outpacing on the back of HSBC (+8.8%) and Commerzbank (+5.1%) with the former bolstered by Ping An Insurance upping its stake in the Co. to 8% via a purchase of 10.8M, whilst the latter cheers the appointing of a new CEO effective Jan 2021. On the other side of the sector spectrum resides the defensive sectors such as healthcare, telecoms and consumer staples. In terms of individual movers, ArcelorMittal (+10%) extends on gains after M&A, with Cleveland-Cliffs (CLF) to acquire ArcelorMittal’s US operations for ~USD 1.4bln, meanwhile the Co. has also announced a share buyback programme. Diageo (+6.6%) is higher after highlighting that business is performing strongly and ahead of expectations. William Hill (-11.1%) unwinds some of Friday’s speculation-fuelled gains after Caesars offered to take over the group at GBP 2.72/shr (vs. Friday’s GBP 3.12/shr close). Rolls-Royce (-4.5%) also sees losses and resides towards the foot of the Stoxx 600 as the engine maker said there has been no final decision in regards any sovereign wealth fund taking a stake in the group. Despite the broader gains across the Travel & Leisure sector, Air France-KLM (-0.7%) bucks the trend as the Co. expects their November-December program to be at 50% of initial plan.

Top European News

- Siemens Energy Slumps on Debut Pushing Value Below Expectations

- Key London Clearinghouses Win Right to Operate in EU Post-Brexit

- Brexit Talks Enter Key Week With Time and Trust Running Out

- French Minister Says LVMH Letter Controversy Excessive

In FX, the Dollar has drifted down from Friday’s highs following a Wall Street recovery rally that has filtered through to APAC and EU equities to varying degrees. However, the DXY remains anchored around the 94.500 level and for once may derive some underlying support into month/quarter end given at least one bank model signalling a buy vs the Eur based on a relatively strong rotation into stocks from bonds to balance asset positions. Meanwhile, on an especially quiet Monday in terms of data, option expiries may have more influence on direction alongside another heavy slate of Central Bank speakers. The index is currently holding within a 94.344-640 range after reaching 97.745 at the tail end of last week, but the Buck is still maintaining strength vs EM currencies and extending gains against some.

- GBP – Sterling is firmer across the board, with Cable back on the 1.2800 handle again and Eur/Gbp down below 0.9100 amidst hope if not conviction of progress on a Brexit trade deal going into the latest formal negotiations between the UK and EU in Brussels this week. Moreover, the cross looks technically bearish (bullish from the Pound’s perspective) after breaching the 10 DMA and a key pivot point at 0.9153 and 0.9118 respectively, while Cable is nudging beyond 1.2850 having cleared its 10 DMA circa 1.2828 amidst latest NIRP nuances from the BoE (Tenreyro noting encouraging evidence from tests of sub-zero rates, but Ramsden more circumspect as he still sees the effective lower bound at 0.1%).

- AUD – Decent option expiry interest at the 0.7000 strike in Aud/Usd (1.3 bn) appears safe as the Aussie hovers near 0.7050 on a sudden change in RBA rate outlook from Westpac to -15 bp in November instead of the looming policy meeting next week, while COVID-19 restrictions are to be relaxed further in Victoria after the daily rate of infections in the state slowed to sub-20.

- JPY/CHF/EUR/NZD – All clawing back some losses vs the Buck, with the Yen rebounding above 105.50 where 1.8 bn expiries reside, but perhaps capped by another 1 bn sitting from 105.00 to 104.90, while the Franc has bounced just ahead of 0.9300 and is pivoting 1.0800 against the Euro following mixed weekly Swiss bank sight deposit balances. Elsewhere, Eur/Usd is just under 1.1650 and also eyeing option expiries as 1.1 bn roll off between the half round number and 1.1640, but ECB commentary could be more influential after a ramp up in verbal intervention from de Cos and Visco before 2 scheduled speeches by Schnabel and one from President Lagarde. Back down under, the Kiwi is straddling 0.6650 and 1.0750 against the Aussie awaiting official NZ election results that PM Adern’s Labour Party seems on course to win without requiring any assistance in the form of a coalition.

- SCANDI/EM – Contrasting starts to the new week as the Swedish and Norwegian Crowns recoup declines vs the Euro and unwind recent underperformance regardless of data that is weak on paper via retail sales and trade in the case of the former. Conversely, the Turkish Lira has lost all and more of its post-CBRT rate hike recovery momentum to trade at fresh record lows close to 7.7900 even though the country’s banking watchdog will lower the asset ratio for deposit banks to 90% from 95% effective this Thursday and President Erdogan reckons the resumption of talks with Greece will be constructive and views this week’s EU Summit as a chance to ‘reset’ relations.

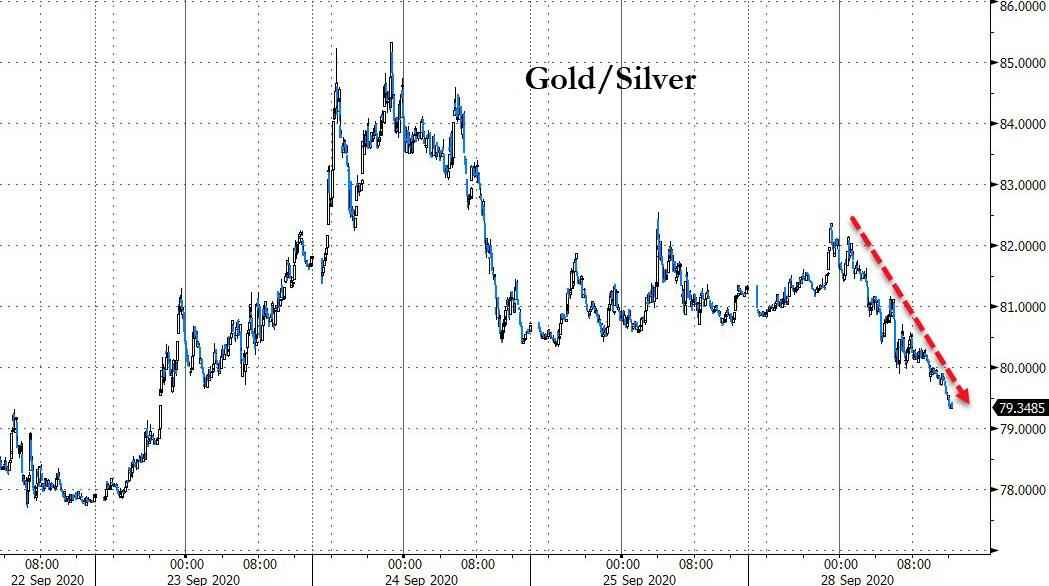

In commodities, WTI and Brent front month futures are modestly firmer and are beginning to derive benefit from the improving risk-sentiment more broadly. For the majority of the morning, the benchmarks have been drifting lower in-spite of the aforementioned gains seen across the equity complex, with attention remaining on the demand outlook for crude given the resurgence of COVID-19 triggering talks of tighter lockdowns in certain economies. Russian Energy Minister Novak emerged on the wires today and noted that global oil markets have been stable with restored balance; albeit, cited a second wave of COVID-19 as a downside risk. Subsequently, reports highlight that Russia’s Rosneft is intending to cut output by 10% in October from September levels potentially due to weaker refining margins and an expected drop in demand for oil products in Russia and Europe, the sources stated. Elsewhere, conflict has erupted between Armenia and OPEC member Azerbaijan, although reports thus far point to the military actions being contained within border regions and not close to any Azeri fields, refineries or ports. Something to keep on the radar – Norwegian offshore workers are planning strike action if annual pay negotiations fail, which could lead to the shuttering of around 22% of Norway’s oil and gas output, according to The Norwegian Oil and Gas Association. WTI Nov currently resides around the USD 40.40/bbl level and towards highs of 40.46/bbl, whilst Brent Nov sees itself just north of USD 42.00/bbl (vs. high 42.12/bbl). Elsewhere, precious metals are marginally softer with spot gold just above USD 1850/oz (vs. high 1865.96/oz) and spot silver above USD 22.50/oz (vs. high 23.08/oz) having tested the level in late APAC trade. In terms of base metals, LME copper remains firmer given the strength in stock markets, contained Dollar and expectations for firmer demand from China. Similarly, Dalian iron ore futures were buoyed overnight with participants also keeping an eye on lower volumes ahead of the Chinese October 1st – 8th National Day Holiday.

US Event Calendar

- 10:30am: Dallas Fed Manf. Activity, est. 9.5, prior 8

DB’s Jim Reid concludes the overnight wrap

Asian markets have started the week on front foot this morning with the Nikkei (+0.72%), Hang Seng (+0.74%), Kospi (+1.49%) and Asx (+0.11%) all up. Futures on the S&P 500 are also up +0.43%. Chinese bourses are trading flat to down however with the CSI (+0.07%) and the Shanghai Comp (-0.22%) lower. In Fx, the US dollar index is down -0.16%.

Looking forwards now, this week we move into Q4, on which we have an in-line with consensus view that it will start on Thursday. Politics will move increasingly into the spotlight for investors, with the coming week featuring the first presidential debate in the US tomorrow. This comes in what is likely to be a febrile atmosphere after the expected weekend announcement of President Trump’s pick for the Supreme Court. Staying with politics we’ll see the resumption of Brexit negotiations between the UK and the EU. In data terms the US jobs report on Friday and global manufacturing PMIs on Thursday will be the keys.

Going into more detail now and tomorrow we see the much-anticipated first debate between Mr Trump and Mr Biden. This will be the first time that the candidates have directly debated each other, and will last for 90 minutes, with the debate divided into six segments. We’ve already been informed that subject to new developments, the topics will be: the Trump and Biden records; the Supreme Court; Covid-19; the economy; race and violence in our cities; and the integrity of the election. The New York Times report over the weekend on the President’s tax returns, which he had avoided disclosing in the 2016 race, as well throughout his first term in office, is quite likely to make an appearance as well. This is the first of three debates between the two, with the others taking place on October 15 and 22, and a debate between the Vice Presidential candidates taking place as well on October 7.

Heading into this debate, Mr Trump picked Amy Coney Barrett to be his choice for the vacant US Supreme Court seat. Confirmation hearings are expected to start on October 12th with a full Senate vote possible by October 26th and just before the election. As has been well flagged this could turn the Supreme Court 6-3 in favour of the Republicans and could have legal ramifications for the US for a generation. And as has also been well flagged, this nomination is highly contentious this close to an election with the Democrats looking at all options to address the balance if they win the White House and Senate in November – assuming the nomination goes through before a new Senate is seated in January.

Elsewhere in the US we see the September jobs report on Friday, which will be the last report we get before Election Day. In August, the unemployment rate fell to a lower-than-expected 8.4%, and the consensus is looking for a further decline to 8.2 % in September. In terms of nonfarm payrolls, the consensus is looking for job growth of +865k, but it’s worth bearing in mind that having lost over -22m jobs in March and April, even this figure would mean that just over half of them have been recovered, still leaving nonfarm payrolls over 10m below their peak back in February.

The other important data release to watch out for next week will be the release of the manufacturing PMIs and the ISM manufacturing index on Thursday. The flash readings we’ve already had generally showed manufacturing holding up relative to expectations, whereas the services readings disappointed, possibly as hospitality/entertainment related industries start to see heightened restrictions again. For example in the Euro Area, the flash manufacturing PMI rose to 53.7, which was its highest reading since August 2018 but the services reading was down to 47.6 from 50.5 last month.

Elsewhere, a special European Council meeting of EU leaders will be taking place on Thursday and Friday. This was originally meant to have taken place the previous week, but was postponed after European Council President Michel had to self-isolate after coming into contact with a security officer who tested positive. In terms of the agenda, there are a number of items, including relations with Turkey and the situation in the Eastern Mediterranean, as well as relations with China. The full day by day calendar is at the end including key central bank speakers.

Back to last week and global equity markets continued to fall as a mix of rising coronavirus cases and further deteriorating data weighed on risk sentiment. The S&P 500 dropped -0.76% despite a strong Friday (+1.47%), declining for a fourth straight week. Banks (-6.18%) and Airlines (-8.01%) were among the largest laggards as the selling expanded from large cap tech. Tech stocks actually broke its recent slide, with Friday’s +2.26% gain helping the NASDAQ to finish up +1.11% on the week. It was the first weekly gain in the index since August. European equities continued their slide with the Stoxx 600 ending the week -3.60% lower (-0.10% Friday). The DAX (-4.93%), FTSE 100 (-2.74%), FTSE MIB (-4.23%), IBEX (-4.35%) and CAC (-4.99%) all posted deep weekly losses as the increasing Covid-19 cases have caused some restrictions to be reinstated in countries, most notably the UK, France and Spain.