GOLD:$1890.40 UP $6.80 The quote is London spot price

Silver:$23.39 DOWN $0.96 London spot price ( cash market)

your data…

Closing access prices: London spot

i)Gold : $1897.50 LONDON SPOT 4:30 pm

ii)SILVER: $24.17//LONDON SPOT 4:30 pm

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 6.31 POINTS OR 0.20% //Hang Sang CLOSED UP 183.52 POINTS OR 0.79% /The Nikkei closed DOWN 359.98 POINTS OR 1.50%//Australia’s all ordinaires CLOSED DOWN 1.11%

/Chinese yuan (ONSHORE) closed DOWN at 6.8100 /Oil DOWN TO 3903 dollars per barrel for WTI and 41.10 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8100 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8151 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

i) Out of Brinks: 10,463.35 oz

ii) Out of Loomis: 16,075.500 oz 500 kilobars.

total withdrawals; 26,538.85 oz

We had 1 kilobar transactions +

ADJUSTMENTS: 1 // customer into the dealer

i) Scotia: 86,252.19 oz

The front month of OCT registered a total of 30524 contracts for a LOSS of 4043 contracts. Thus by definition we will have the following initially stand for metal in this generally weak delivery month of October:

30,524 x 100 oz = 3,052,400 oz or 94.94 tonnes

November gained 59 contracts to stand at 780.

The big December contract GAINED 3899 contracts UP to 441,181 contracts..

THE BIG STORY AGAIN TODAY IS THE HIGH OI STANDING FOR OCTOBER (94.95 tonnes). GENERALLY OCTOBER IS A POOR DELIVERY MONTH AS MOST INVESTORS PREFER TO SKIP THIS MONTH AND MOVE STRAIGHT TO DECEMBER. IT LOOKS LIKE SOME MAJOR ENTITY(GOLDMAN SACHS) JUST CANNOT WAIT FOR DECEMBER AS THEY ARE MAKING THEIR MOVE ON OCTOBER FOR PHYSICAL METAL. GOLDMAN SACHS ONE OF THE LEADERS OF THE NEW LONDON LME EXCHANGE NEEDS THE GOLD INVENTORY FOR LIQUIDITY AND INITIAL CONTRIBUTION WITH OTHER MAJOR PLAYERS. THE MAJOR DIFFERENCE BETWEEN THIS MONTH AND OTHER MONTHS IS THAT THIS GOLD STANDING IN OCTOBER WILL LEAVE THE COMEX AND HEAD FOR LONDON.

We had 6442 notices filed today for 644,200 oz OR 20.037 TONNES.

This is very low compared to what is initially standing. The comex does not have the deliverable gold so far that is necessary to satisfy the longs (Goldman Sachs) that is standing for metal.

To calculate the INITIAL total number of gold ounces standing for the OCT /2020. contract month, we take the total number of notices filed so far for the month (6442) x 100 oz , to which we add the difference between the open interest for the front month of OCT (30,524 CONTRACTS ) minus the number of notices served upon today (6442 x 100 oz per contract) equals 3,052,400 OZ OR 94.95 TONNES) the number of ounces standing in this active month of JUNE

thus the INITIAL standings for gold for the OCT/2020 contract month:

No of notices filed so far (6442, x 100 oz +30,524 OI) for the front month minus the number of notices served upon today (6442) x 100 oz which equals 3,052,400 oz standing OR 94.95 TONNES in this active delivery month. This is a HUGE amount for gold standing for a OCT delivery month (a poor active delivery month).

NEW PLEDGED GOLD: BRINKS

592,648.822 oz NOW PLEDGED SEPT 15.2020/HSBC 18.433 TONNES ( A HUGE INCREASE FROM 10.6)

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

277,934.09 oz (some deleted august 3) JPM 8.644 TONNES

610,238.285 oz pledged June 12/2020 Brinks/ july 2/july 21 19.017 tonnes

51,084.609 oz Pledged August 21/regular account 1.588 tonnes jpm

total pledged gold: 1,574,454.119 oz 48.97 tonnes

total registered, pledged and eligible (customer) gold 36,901,910.402 oz 1,147.80 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1021.50 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

END

And now for the wild silver comex results

And now for the wild silver comex results

INITIAL STANDINGS

OCT. SILVER COMEX CONTRACT MONTH//INITIAL STANDING

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

992.80 oz

DELAWARE

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

1,184,382.400 oz

JPMorgan

Scotia

|

| No of oz served today (contracts) |

1026

CONTRACT(S)

(5,130,000 OZ)

|

| No of oz to be served (notices) |

678 contracts

3,390,000 oz)

|

| Total monthly oz silver served (contracts) | 1026 contracts

5,130,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 2 deposits into the customer account (ELIGIBLE ACCOUNT)

i)into JPMorgan: 595,378.800 oz

ii) Into Scotia: 589,003.600 oz

JPMorgan now has 184.9 million oz of total silver inventory or 49.28% of all official comex silver. (184.9 million/375.2 million

total customer deposits today: 1,184,382.400 oz

we had 1 withdrawals:

total withdrawals; 992.800 oz

We had 2 adjustments/ customer to dealer

i) CNT 1,324,664.300 oz

ii) Manfra: 34,781.400 oz

Total dealer(registered) silver: 139.813 million oz

total registered and eligible silver: 375.203 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

October had an initial 1704 notices outstanding and so by definition the total no of silver oz initially standing is as follows:

1704 contracts x 5000 oz = 8,520,000 oz

November saw a gain of 63 notices up to 273 contracts.

December saw a gain of 2455 contracts up to 133,808 contracts.

The total number of notices filed today for the OCT 2020. contract month is represented by 1026 contract(s) FOR 5,130,000 oz

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 1026 x 5,000 oz = 5,130,000 oz to which we add the difference between the open interest for the front month of OCT( 1704) and the number of notices served upon today 1026x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the OCT/2019 contract month: 1,026 (notices served so far) x 5000 oz + OI for front month of SEPT (1704)- number of notices served upon today (1026) x 5000 oz of silver standing for the OCT contract month .equals 8,520,000 oz. ..VERY STRONG FOR A NON ACTIVE MONTH.

TODAY’S ESTIMATED SILVER VOLUME : 85,473 CONTRACTS // volume very good//

FOR YESTERDAY 83,860 ,CONFIRMED VOLUME// strong/

YESTERDAY’S CONFIRMED VOLUME OF 83,860 CONTRACTS EQUATES to 0.419 billion OZ 59.9% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO- 2.25% ((SEPT 30/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.60% to NAV: (SEPT 30/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/2.25%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 19.03 TRADING 18.34///NEGATIVE 3.62

END

And now the Gold inventory at the GLD/

SEPT 30//WITH GOLD DOWN $6.80 TODAY, NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1268.89 TONNES

SEPT 29/WITH GOLD UP $19.10//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1268.89 TONNES

/SEPT 28//WITH GOLD UP $14.30 DOLLARS: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.05 TONNES INTO THE GLD//INVENTORY RESTS AT 1268.89 TONNES

SEPT 25//WITH GOLD DOWN 410.80 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .3 TONNES FROM THE GLD////INVENTORY RESTS AT 1266.84 TONNES

SEPT 24/WITH GOLD UP $9.80 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1267.14TONNES.

SEPT 23//WITH GOLD DOWN $28.00 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 11.68 TONNES FROM THE GLD////INVENTORY RESTS AT 1267.14 TONNES

SEPT 22/WITH GOLD DOWN $4.50 TODAY, A MONSTROUS CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 18.98 TONNES OF PAPER GOLD ENTER THE GLD///// INVENTORY RESTS AT 1278.62TONNES

SEPT 21/WITH GOLD DOWN $47.20 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 12.94 TONNES INTO THE GLD///INVENTORY RESTS AT 1259.64TONNES

SEPT 18/WITH GOLD UP $10.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS THIS WEEKEND AT: 1246.99 TONNES

SEPT 17/WITH GOLD DOWN $18.05 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD//INVENTORY RESTS AT 1246.99 TONNES

SEPT 16.WITH GOLD UP $4.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1247.57 TONNES

SEPT 15//WITH GOLD UP $2.25 TODAY: A SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .43 TONNES FROM THE GLD//INVENTORY RESTS AT 1247.57 TONNES

SEPT 14/WITH GOLD DOWN 90 CENTS TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.96 TONNES FROM THE GLD////INVENTORY RESTS AT 1248.00 TONNES

SEPT 11/WITH GOLD DOWN $14.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1252.96 TONNES

SEPT 10/WITH GOLD UP $8.85 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.92 TONNES INTO THE GLD////INVENTORY RESTS AT 1252.96 TONNES

SEPT 9/WITH GOLD UP $19.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1250.04 TONNES

SEPT 8/WITH GOLD UP $8.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1250.04 TONNES

SEPT 4//WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1250.04 TONNES

SEPT 3/WITH GOLD DOWN $7.50 ON THIS 2ND DAY OF A 3 DAY RAID: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1250.04 TONNES

SEPT 2/WITH GOLD DOWN $34.00 TODAY, WE HAVE 2 SMALL CHANGES IN GOLD INVENTORY AT THE GLD: 2 WITHDRAWALS OF .87 TONNES AND.59 TONNES FROM THE GLD////INVENTORY RESTS AT 1250.04 TONNES

SEPT 1/WITH GOLD UP $7.10 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1251.50 TONNES

AUGUST 31//WITH GOLD UP $5.90 TODAY/WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD..//INVENTORY RESTS AT 1251.50 TONNES/

AUGUST 28/WITH GOLD UP $38.20 TODAY, WE SURPRISINGLY HAD A .59 TONNE WITHDRAWAL//INVENTORY RESTS AT 1251.50 TONNES

AUGUST 27/WITH GOLD DOWN 17.50 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 3.24 TONNES INTO THE GLD//INVENTORY REST AT 1252.09 TONNES

AUGUST 26/WITH GOLD UP $26.70 TODAY/ WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.53 TONNES FROM THE GLD//RESTS AT 1248.85 TONNES

AUGUST 25/WITH GOLD DOWN $14.60 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//RESTS AT 1252.38 TONNES

AUGUST 24//WITH GOLD DOWN $7.20 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1258.38 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

SEPT 30/ GLD INVENTORY 1268.89 tonnes*

LAST; 910 TRADING DAYS: +329.05 NET TONNES HAVE BEEN ADDED THE GLD

LAST 810 TRADING DAYS://+507.98 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 30//WITH SILVER DOWN 96 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 186,000 OZ FROM THE SLV.//INVENTORY RESTS AT 550.605 MILLION OZ..

SEPT 29/WITH SILVER UP 86 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.791 MILLILON OZ//

SEPT 28//WITH SILVER UP 48 CENTS TODAY: A HUGE DEPOSIT OF 3.769 MILLION OZ CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.791 MILLION OZ//

SEPT 25/WITH SILVER DOWN 14 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: 2 TRANSACTIONS: A PAPER WITHDRAWAL OF 8.28 MILION OZ FROM THE SLV AND A DEPOSIT OF 1.861 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 547.022 MILLION OZ//

SEPT 24//WITH SILVER UP 15 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 553.443 MILLION OZ//

SEPT 23//WITH SILVER DOWN $1.41: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.048 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 553.443 MILLION OZ///

SEPT 22/WITH SILVER DOWN ONE CENT TODAY: A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.141 MILLION OZ////INVENTORY RESTS AT 555.491 MILLION OZ..

SEPT 21/WITH SILVER DOWN $2.43 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV A PAPER WITHDRAWAL OF 1.862 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 553.350MILLION OZ//

SEPT 18. WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 555.212 MILLION OZ/

SEPT 17/WITH SILVER DOWN 31 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.537 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 555.212 MILLION OZ/

SEPT 16//WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.749 MILLION OZ//

SEPT 15/WITH SILVER UP 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.793 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 558.749 MILLION OZ..

SEPT 14/WITH SILVER UP 47 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS A) 1.675 MILLION OZ AND ANOTHER B) 0.931 MILLION OZ/ FROM THE SLV////INVENTORY RESTS AT 555.956 MILLION OZ//

SEPT 11/WITH SILVER DOWN 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.562 MILLION OZ//

SEPT 10/WITH SILVER UP 16 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.607 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 558.562 MILLION OZ.

SEPT 9/WITH SILVER UP 6 CENTS TODAY: STRANGE: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.63 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 561.169 MILLION OZ

SEPT 8/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 564.799 MILLION OZ

SEPT 4//WITH SILVER DOWN 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 3.631 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 564.799 MILLION OZ//

SEPT 3//WITH SILVER DOWN 50 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.258 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.430 MILLION OZ/./

SEPT 2.WITH SILVER DOWN $1.04 TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.365 MILLION OZ FROM THE SLV///INVENTORY REST AT 571.688 MILLION OZ.

SEPT 1//WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 31/WITH SILVER UP 80 CENTS TODAY: A HUGE CHANGE IN THE SLV//A DEPOSIT OF 2.982 MILLION OZ ENTERS THE SLV/INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 28/WITH SILVER UP 48 CENTS TODAY: A MASSIVE PAPER DEPOSIT OF 4.652 MILLION OZ ENTERS THE SLV//INVENTORY RESTS AT 571.071 MILLION OZ

AUGUST 27/WITH SILVER DOWN 28 CENTS TODAY// NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.419 MILLION OZ

AUGUST 26//WITH SILVER UP $1.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.65 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 566.419 MILLION OZ..

AUGUST 25/WITH SILVER DOWN 21 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.607 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 571.074 MILLION OZ//

AUGUST 24//WITH SILVER DOWN 18 CENTS TODAY: WE HAD A NO CHANGES//INVENTORY RESTS AT 573.843 MILLION OZ//

SEPT 30.2020:

SLV INVENTORY RESTS TONIGHT AT

550.791 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

Morgan admits rigging gold, silver, Treasury futures and will pay $920 million fine

Submitted by cpowell on Tue, 2020-09-29 19:32. Section: Documentation

JPMorgan Admits Spoofing by 15 Traders, Two Desks in Record Deal

By Matt Robinson and Tom Schoenberg

Bloomberg News

Tuesday, September 29, 2020

JPMorgan Chase & Co. today admitted wrongdoing and agreed to pay more than $920 million to resolve U.S. authorities’ claims of market manipulation involving two of the bank’s trading desks, the largest sanction ever tied to the illegal practice known as spoofing.

Over eight years 15 traders at the biggest U.S. bank caused losses of more than $300 million to other participants in precious metals and Treasury markets, according to court filings made today. JPMorgan admitted responsibility for the traders’ actions.

The Justice Department filed two counts of wire fraud against the bank’s parent company but agreed to defer prosecution related to the charges, under a three-year deal that requires the bank to report its remediation and compliance efforts to the government.

The New York-based lender will pay the biggest monetary penalty ever imposed by the Commodity Futures Trading Commission, including a $436.4 million fine, $311.7 million in restitution, and more than $172 million in disgorgement, according to a CFTC statement:

https://cftc.gov/PressRoom/PressReleases/8260-20

The CFTC said its order will recognize and offset restitution and disgorgement payments made to the Department of Justice and Securities and Exchange Commission.

Allegations of spoofing on the bank’s precious metals desk emerged more than a year ago in charges against several traders on the desk. But the settlement announced today also includes new allegations about spoofing by traders on the bank’s Treasuries desk.

The deal faults the bank for nearly eight years of manipulating prices of Treasury contracts, as well as trading in notes and bonds in the secondary market, that caused $106 million in losses. The government said five now-former JPMorgan traders executed thousands of deceptive trades. None of those traders has been charged publicly.

The accord also ends the criminal investigation of the bank that led to a half dozen employees being charged for allegedly rigging the price of gold and silver futures from 2008 to 2016. Two have entered guilty pleas, and three traders and a former JPMorgan salesman are awaiting trial. In all, according to the settlement deal, 10 JPMorgan traders caused losses of $206 million to other parties in the market. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2020-09-29/jpmorgan-pays-920-mil…

END

Hemke states that market rigging did not end with the criminal conviction: it continues and today with options expiry it is quite evident

(zerohedge)

Hemke: Metals market rigging didn’t end today; Grandich recalls two lying shills

Submitted by cpowell on Tue, 2020-09-29 20:05. Section: Daily Dispatches

4:06p ET Tuesday, September 29, 2020

Dear Friend of GATA and Gold:

Don’t think for a moment, the TF Metals Report’s Craig Hemke writes today at Sprott Money, that manipulation and corruption in the monetary metals markets will stop with JPMorganChase’s admission of rigging them and the bank’s paying a $920 million fine.

Market rigging, Hemke writes, remains too easy and profitable and the market regulators too corrupt or incompetent to stop it. Worse, Hemke adds, monetary metals mining companies accept rigging even when it’s done by their own banks. He hopes to motivate the miners to start playing for their own team.

…

Hemke’s analysis is headlined “Bullion Bank Criminal Corruption” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/Bullion-Bank-Criminal-Corruption-Craig-…

Meanwhile GATA’s old friend, market analyst Peter Grandich, recalls a couple of the “analysts” who were tools of the manipulation, denying it and mocking those who complained about it. Grandich’s comments are posted at Twitter here:

https://twitter.com/PeterGrandich/status/1311018646240743425

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

iii) Other physical stories:

Gold trading on options expiry:

Gold Pumped-n-Dumped As Stocks Melt-Up To Overnight Debate Highs

So… with futures down hard overnight, talking heads proudly proclaimed that this must mean Biden won the debate. So with stocks now surging to overnight highs, does that mean Trump won?

Some are claiming this panic-bid is driven by Pelosi’s “hopeful” comments on stimulus but she has said the same exact word every day for two weeks.

Meanwhile gold is chaotic with futures ripped back above $1900, only to be dumped again…

And bonds are being sold…

Month-/Quarter-end rebalancing?

Dave from Denver…

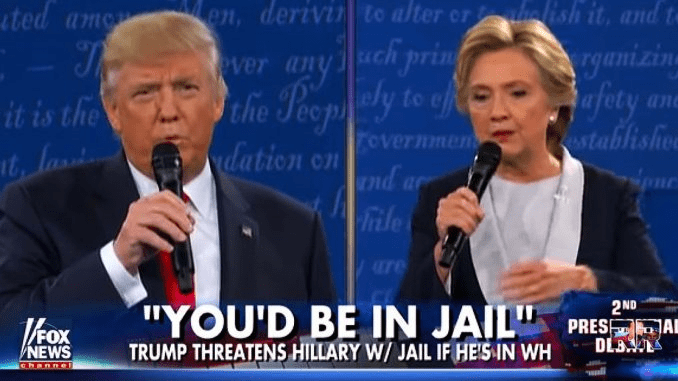

Gold, Silver And The “Shit-Show”

“I’m just gonna say it like it is – that was a shit- show.” Dana Bash, CNN in reference to the “Presidential” debate. “The debate was a national mortification – ‘shit-show’ was an understatement” – Chris Powell, GATA.

Last night’s debate was nothing short of a complete tragedy: the tragedy of a collapsing empire. I saw an ad on one of the financial propaganda cable channels that billed the debate as “The Main Event” as if it were to be promoted like a championship boxing match.

Politicians and the political environment are nothing more than a reflection of the surrounding system and populace at large. The entire U.S. system is a shit-show. The financial markets have become so disconnected from the underlying economic and fiscal reality that it takes several trillion dollars in monetary intervention from the Central Bank to keep them from collapsing.

The stock market’s complete dysfunctionality is represented by the dozens of tech-related “unicorn” type companies that collectively burn billions in cash every quarter and yet have market caps in the tens of billions of dollars. If anything, Tesla is emblematic of the degree to which the entire U.S. financial and political system is a complete fraud.

And then there’s gold and silver. The mainstream financial media dismissively reported the $950 million dollar fine to be paid by JP Morgan for manipulating the gold market. But it was just some rogue employees “spoofing” the market. Spoofing is not the issue. The gold market is, and has been for several decades, manipulated systematically to prevent the price of gold rising to a price level vs the dollar that reflects and embodies everything described above. “Spoofing” is nothing. It’s the creation of derivatives with a notional value in the trillions to be used in large quantities to push the price of gold lower. Here’s an example:

Part of the problem is that the mainstream financial media has become nothing more than hand-puppets for the Wall Street operators who pay their compensation by sponsoring their media abortion. They merely print the words fed to them. You’ll note that Investing.com is attributing the sell-off in gold this morning to a “weak dollar.” Yet yesterday Investing.com told us that the big move higher in gold was attributable to a “weak dollar.” See what I mean? Zombie hand-puppets.

That price plunge in the graphic above has nothing to do with the trading action in physical gold. Or to spoofing. It’s a product of the gold market manipulators like JP Morgan unloading a massive quantity of paper gold onto the Comex and triggering stop-loss orders set by hedge fund black box trading systems just as gold was about to launch through $1900 again. A $950 million fine is the cost of doing business for JP Morgan. The Fed has injected billions into JP Morgan since March. $950 million is not a deterrent – it’s an odd-lot.

The Central Banks, with the help of their bullion bank phalanges, are desperate to keep the gold price in check in order to maintain the credibility of the dollar-based fiat currency monetary system – a monetary system in which trillions worth of currency can be created with a computer keystroke and that is 100% fraudulent.

Who benefits the most? The primary target of the $3-plus trillion printed since mid-March are the big banks, which started to collapse last summer. The phony “repo” operation implemented in mid-September is the evidence of that fact. But the Government’s fiscal “shit-show,” a financial system held up by a currency printing press and an economy largely in a depression will lead to trillions more in Federal Reserve intervention.

The implication of the shit-show described above is that eventually the price of gold is going to move considerably higher in relation to all fiat currencies and, specifically, the U.S. dollar. You’ll never see Investing.com or financial TV report that the dollar has lost 98.2% of its value vs. gold since 1971. But do the math – it’s a fact. The loss of the remaining 1.8% vs gold is the what the western Central Banks are fighting to prevent. It’s their Maginot Line. And it’s the eventual loss of that 1.8% that will send the price of gold measured in fiat currencies into orbit.

The short term gold chart looks as bullish as it has looked YTD. Last week’s sell-off was a gift to those who understand what is happening, why it’s happening and what can be done to protect wealth. Think I’m blowing smoke? I put my money where my mouth is. Last week, all week long as the gold and silver were pushed lower in price vs the dollar, I bought gold and silver bullion coins for the first time since early 2017 when gold was near $1100 and silver was around $16. On a relative scale, in which the “scale” is the severity of the shit-show, gold and silver are cheaper now than in 2017. That’s why I converted more fiat currency into real money.

This chart is coup de grace:

The Central Banks are starting to lose their grip on that final 1.8%. The value of gold relative to the U.S. dollar is beginning to accelerate along with the amount of systemic corruption, fraud and general perversion.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

US Futures Slide After Debate Chaos

US equity futures and most global markets dropped after an acrimonious and chaotic US presidential debate, which CNN’s Dana Bash described as a “shitshow” on air, and which did little to change voters minds but underscored the risk of a contested vote in November. Safe assets, such as the yen and dollar also rose as a continued rise in COVID-19 spooked some traders although strong factory surveys boosted China’s markets.

S&P 500 futures were last 0.6% lower, with Dow Jones and Nasdaq 100 futures down by as much as 1%. Asian trading had been choppy rather than outright weak but Europe sank 0.5% early on amid worries too over the steep rises in coronavirus infections across the region again, although a wave of buying managed to bring European markets back to even. Google dipped after a report that China was preparing to launch an antitrust probe into Alphabet’s Google.

While futures initially rose, they kneejerked lower after the end of the debate as Trump cast doubt on whether he would accept the election’s outcome if he lost. Here

“What we’ve seen from the debate is the reinforcement that if Biden wins, Trump is not going to accept that,” said Chris Weston, head of research at Pepperstone Group Ltd. in Melbourne. “People positioned for an ugly contest afterwards have been validated….I don’t think we were expecting anything else from Trump. He continues to put that contested (result) risk premium back into the market.”

They have since rebounded however, as the first presidential debate offered little trading cues for bond and currency markets, according to Jun Kato, chief market analyst at Shinkin Asset Management, who noted that Trump’s performance was in line with his usual behavior and it was unclear if Biden emerged superior in the debate.

“The debate just added to the confusion about how the election will run,” said SEB investment management’s global head of asset allocation Hans Peterson. “But financially it doesn’t change anything.”

“The share market normally prefers the incumbent (president) to win,” said Shane Oliver, head of investment strategy at AMP Capital in Sydney. “U.S. futures initially rose, as perhaps Trump delivered some punches, but it wasn’t enough,” he said.

To be sure, the debate was an absolute mess with 69% of people in a CBS poll said they were annoyed with the event, “which featured expletives, name calling, insults and shouting that made it hard to hear what was actually being said.”

DB’s Jim Reid agrees, writing overnight that “there was very little substance in the debate and almost no new information proffered. The story of the debate will likely surround the President’s consistent interruption, though Mr Biden was not able to stay above the fray and traded insults at times with Mr Trump. Acrimony ruled.”

More to the point, and as we asked if the debate actually matters, Bloomberg’s John Authers writes that the debate “appears to have changed little” who shows trading over the last 24 hours on the Predictit contract for which party wins the election. Volume was heavy during the debate, and yet it translated into a just-perceptible improvement for the Democrats, nothing more.

Bookies reported much the same thing; betting markets had been slightly more optimistic for Donald Trump than the prediction markets, but now they are in exact alignment. Like Predictit, the Betfair exchange now puts Biden’s victory chance at 60%. Before the debate, Biden’s odds were 4/5 on (56%). They are now 4/6 (60%). Trump’s odds, if you fancy a bet, widened from 11/8 to 6/4. Biden is ahead but not by the kind of margin that anyone would want to risk a lot of money on.

The presidential debate yielded no clear winner and barely moved the needle in betting markets, which project a narrow Biden victory. Odds maker Smarkets slightly lowered Trump’s chance of re-election to 40% after the debate from 42% beforehand.

As we said last night, and as Authers repeats this morning, Biden succeeded by “surviving the debate” and giving the president one less opportunity to bring him down in future, and while both made statements that might be usable against them, it was hard to hear what either of them were saying for lengthy tracts of the debate. The conclusion: “It’s hard to see how any genuinely undecided voter would have changed their mind on the basis of this.”

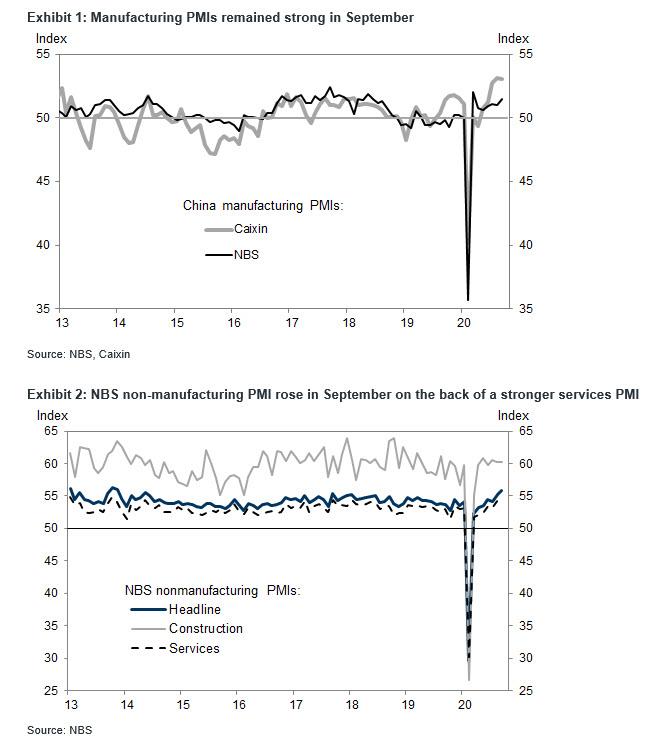

Perhaps more market moving was the latest Chinese official and Caixin PMI, both of which hit just before China goes on vacation for a week. The September Manufacturing PMIs from both the National Bureau of Statistics (NBS) and Caixin signaled continued solid expansion of manufacturing activity. The NBS non-manufacturing PMI rose in September as well with the services PMI climbing to the highest level since mid-2012. The China NBS purchasing managers’ indexes (PMIs) suggest manufacturing activity continued to expand at a solid pace in September:

- The NBS manufacturing PMI headline index was at 51.5 in September, vs 51.0 in August.

- The NBS non-manufacturing PMI (comprised of the service and construction sectors at roughly 80%/20% weightings, based on our estimates) rose 0.7pp to 55.9 in September on a stronger services PMI. The services PMI climbed to 55.2, the highest level since June 2012.

The Caixin manufacturing PMI released later in the morning came in at 53.0, only slightly lower than 53.1 in August which was the highest level since early 2011. Similar to the NBS manufacturing survey, the Caixin manufacturing survey suggest stronger new export orders, higher employment sub-index and higher input cost pressures. The new export order sub-index in the Caixin manufacturing survey surged to 54.4 in September, the strongest reading since September 2014.

As Goldman concludes, “manufacturing PMIs suggest overall activity continued to recover in September in the manufacturing sector, on the back of persistent strength in exports. Services sector activity recovery has been catching up, as suggested by the higher services PMI under the NBS PMI survey.”

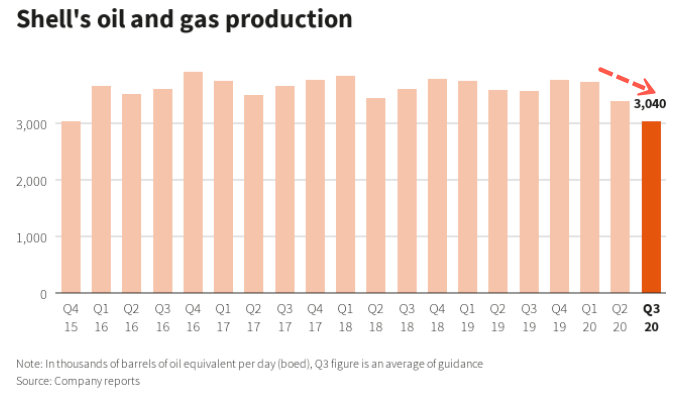

Alas, there were less good news on the US jobs front, following several blockbuster layoff announcements. Walt Disney made one of the deepest workforce reductions in not only the Covid-19 era but in history, when it announced it was firing 28,000 workers. Oil giant Royal Dutch Shell said it will cut as many as 9,000 jobs as it struggles with low demand and tries to restructure towards low-carbon energy. Dow also said it would cut 6% of its workforce, while Marathon Petroleum also started layoffs.

* * *

Back to market globally, most of which are headed for their first monthly retreats since March’s meltdown, either deepened losses or pulled back from highs scaled after data showed China’s economic recovery remains on track. MSCI’s broadest index of world shares dropped 0.2% for a 4% September loss. Oil is down just over 10% this month while gold’s 4.1% drop will make it its worst month since late 2016.

Asia had held its ground overnight, led by a 0.8% gain in Hong Kong, though Japan’s Nikkei fell 1.5% and Australia’s S&P/ASX 200 lost over 2%. Chinese property developers gained, led by a 15% jump in Evergrande shares after the heavily-indebted giant reached a deal to ease cash crunch concerns, as noted last night. China’s factory activity expansion accelerated in September, helped by rising export orders.

In Europe, declines in industrial-goods and tech shares outweighed gains in utilities.

In FX, options trade points to a volatile November. Two-month dollar/yen volatility, a gauge of expected moves in the yen, is elevated, and its premium over one-month volatility is near record levels. Major currencies eased against the dollar after the debate, The euro dipped from a one-week high to $1.1736 and the risk-sensitive Australian dollar fell 0.2% to $0.7118, heading for its worst month since March.

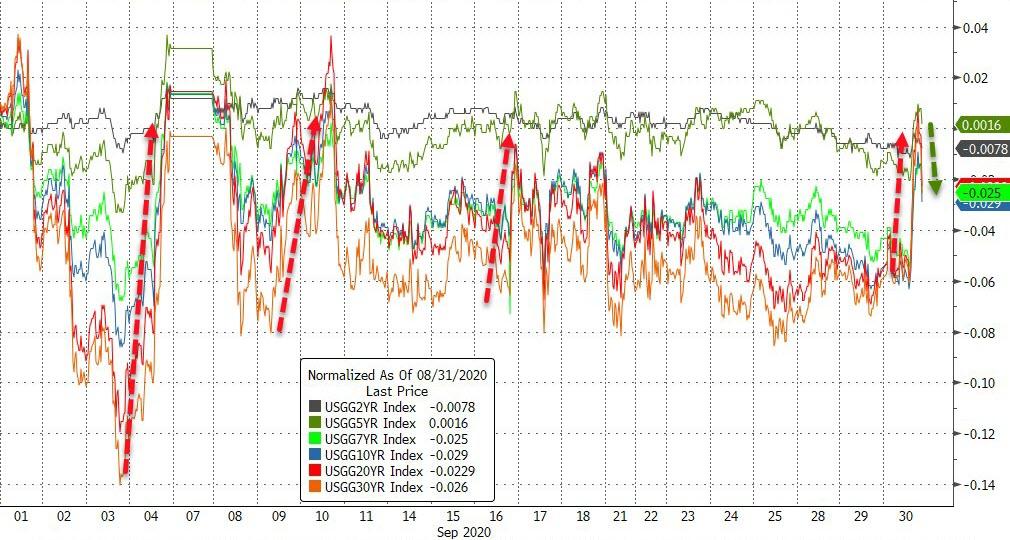

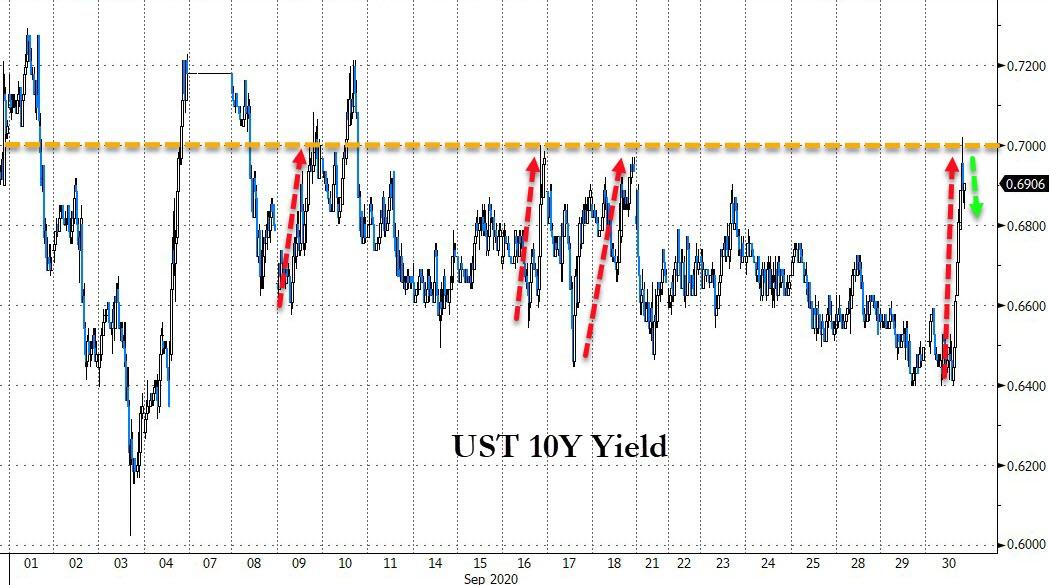

In rates, Treasuries barely budged, with yields remaining within a basis point of Tuesday’s closing levels ahead of U.S. data raft including September ADP employment change and 2Q GDP. Yields were higher by less than 1bp at long end, steepening 5s30s by ~1bp; 10-year yields steady around 0.65%, outperforming bunds and gilts by less than 1bp. Price action was choppy but not sustained during first U.S. presidential debate late Tuesday, leaving yields slightly cheaper at long end. The long end may draw support toward end of U.S. trading day from month-end index rebalancing.

In commodities, oil prices fell amid rising concerns about fuel demand as the coronavirus pandemic worsens. Brent crude futures were last down 0.9% at $40.66 a barrel and U.S. crude futures were down 0.7% at $39.00 a barrel. Gold slipped 0.4% to 1,890 an ounce.

Looking at the day ahead, Fed speakers include the Fed’s Bowman, Bullard, and Kashkari. In terms of data, we’ll get the third reading of Q2 GDP, August’s pending home sales, the MNI Chicago PMI for September and the ADP employment change for September.

Market Snapshot:

- S&P 500 futures down 0.9% to 3,305.50

- STOXX Europe 600 down 0.4% to 360.02

- MXAP down 0.6% to 169.28

- MXAPJ up 0.09% to 553.65

- Nikkei down 1.5% to 23,185.12

- Topix down 2% to 1,625.49

- Hang Seng Index up 0.8% to 23,459.05

- Shanghai Composite down 0.2% to 3,218.05

- Sensex up 0.5% to 38,156.23

- Australia S&P/ASX 200 down 2.3% to 5,815.94

- Kospi up 0.9% to 2,327.89

- German 10Y yield rose 0.4 bps to -0.541%

- Euro down 0.1% to $1.1728

- Italian 10Y yield fell 2.7 bps to 0.648%

- Spanish 10Y yield rose 0.4 bps to 0.229%

- Brent futures down 1.8% to $40.30/bbl

- Gold spot down 0.6% to $1,886.96

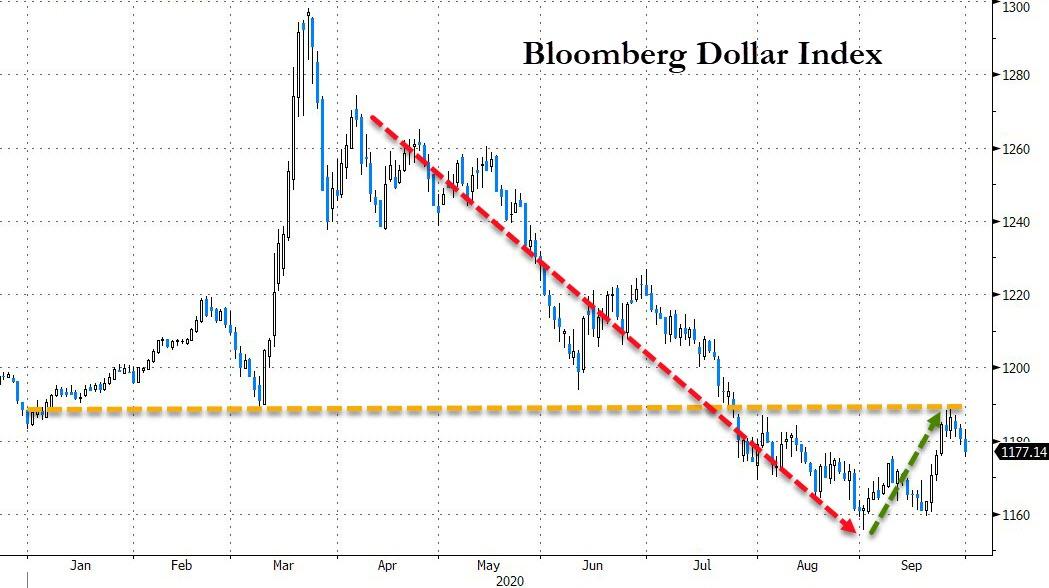

- U.S. Dollar Index up 0.3% to 94.16

Top Overnight News from Bloomberg:

- President Donald Trump and former Vice President Joe Biden hurled insults and repeatedly interrupted each other in their first debate, sparring over topics ranging from health care to the economy and their families as moderator Chris Wallace tried mostly in vain to control the conversation

- Trump Sees Wide Vote Fraud That Doesn’t Exist: Debate Fact Check

- Boris Johnson is braced for defeat in Parliament over his controversial plan to re-write the Brexit withdrawal agreement, a blow that could throw negotiations with the European Union into chaos at a critical time

- Japan’s industrial production increased for a third month in August as the economy continued to reopen, though the gains slowed from July’s record jump

- The European Union’s historic 1.8 trillion-euro ($2.1 trillion) budget and stimulus package is in danger of being delayed due to a disagreement among member states about how to enforce the adherence to democratic values, according to a spokesman for the German government

- Italy plans to bring its budget deficit back into line with European Union rules in 2023 after a dramatic increase in spending dictated by the coronavirus outbreak

- Oil held below $40 a barrel on rising concerns that it will be some time before there’s a meaningful recovery in demand

A quick look at global markets courtesy of NewsSquawk

Asian equity markets were mixed with participants indecisive as focus centred on the US Presidential Debate where US President Trump faced off with former VP Biden on a range of topics including COVID-19, the economy, taxes and foreign dealings of former VP Biden’s son. The debate featured plenty of bickering and highlighted no love lost between the candidates with President Trump criticizing Biden’s son and with Biden referring to Trump as a clown on several occasions, while marginal upside was seen in US equity futures early in the debate as the widely viewed front-runner Biden showed a more composed tone with President Trump seemingly disruptive and interrupting Biden and the moderator a few times, which favoured the notion of a Blue Sweep. However, all the gains were later pared at the end of the debate which descended into chaos with plenty of disruptions and President Trump also suggested the idea of a contested election which could last for months. As such, ASX 200 (-2.3%) and Nikkei 225 (-1.5%) were negative with Australia dragged lower by losses in the energy sector and with financials also underperforming, while Tokyo sentiment was lacklustre following Industrial Production data which despite beating expectations, still showed a double-digit percentage contraction Y/Y. Hang Seng (+0.7%) and Shanghai Comp. (-0.2%) were initially both positive on the eve of Golden Week as participants digested better than expected Chinese Official PMI data and although Caixin Manufacturing PMI slightly missed, the data showed new export orders rose by the most in 3 years and the employment gauge returned to growth; however, gains in Shanghai were pared back. Finally, 10yr JGBs traded lacklustre as prices reversed some of yesterday’s gains but with downside stemmed amid the BoJ’s presence in the market today and after the central bank also kept its purchase intentions for October unchanged.

Top Asian News

- CLSA Exodus Deepens as Beijing Tightens Grip, Reins In Pay

- Alibaba Expects First Profit From its Cloud Arm This Year

- Armenian-Azeri Fighting Continues, Ignoring Cease-Fire Appeals

- Japan’s Factory Output Rises for Third Month in August

A relatively choppy session thus far for European stocks, albeit with losses somewhat contained (Euro Stoxx 50 -0.6%), as sentiment was dampened overnight amid the fallout from the US Presidential debate, whilst fresh catalysts during European hours remain scarce. That being said, the EU released their report on rule of law deficiencies which singles out Hungary and Poland – a move which could threaten the swift implantation of the EU Recovery Fund as unanimity is needed to roll out the package. Meanwhile, China opened an antitrust probe into Google (-1.8% pre-market) over market dominance. European bourses see varying degrees of losses, with FTSE 100 (-0.1%) cushioned by a softer Sterling, and Spain’s IBEX (-0.1%) supported by gains in large-cap stocks including Telefonica (+0.6%) after reports said it is mulling the sale of an additional stake in its mobile telephone mast unit Telxius. Thus the telecom sector outperforms, with added tailwinds from gains in Orange (+0.7%), Bouygues (+0.9%) after the French Telecom Regulator said prices for the 5G spectrum are up by EUR 220mln following the first round of auctions, with the latter also buoyed by its disposal of Alstom (-2.2%) shares. IT meanwhile resides on the other side of the spectrum following earnings from Micron (-4.7% pre-mkt) despite beating on both top and bottom line is afflicted more-so on sub-par guidance. As such, Infineon (-1.2%), SAP (-1.2%) and STMicroelectronics (-1.2%) are subdued. Travel and Leisure also resides towards the bottom of the pile amid the ongoing woes for the sector with regards to rising COVID-19 infections. In terms of individual movers, Suez (+6.5%) is a top gainer in the Stoxx 600 after Veolia (+1.8%) upped its offer for the Co. to EUR 18/shr from EUR 15.50/shr. Shell (+0.5%) sees modest gains despite a rather gloomy Q3 update, but with upside potentially on further cost-cutting measures including global job losses of up to 9,000 employees by end-2022.

Top European News

- Damning Report Set to Worsen Spat Over EU’s Jumbo Recovery Fund

- ECB to Consider Allowing Inflation Overshoot, Lagarde Says

- SNB Spent 90 Billion Francs on Interventions as Virus Took Hold

- Merkel’s Old Foe May Finally Get His Chance to Undo Her Legacy

In FX, the Dollar and index by design seem to have found their footing after extending declines amidst all the bickering between incumbent US President Trump and rival Biden overnight. The DXY has revisited 94.000, albeit just within a 94.180-93.789 range and could be seeing late if not last minute rebalancing demand for the end of September and Q3 alongside a touch of safe-haven buying as broad risk sentiment wavers. Ahead, a busy US data schedule including ADP before Friday’s BLS report and more Fed speak via current FOMC voters Kashkari, Bowman and Kaplan.

- CHF/GBP – Lagging fellow G10 currencies, and perhaps surprisingly given the Swiss KOF indicator easily beating consensus and advancing further above the 100.0 mark, while revised UK GDP was not quite as abject as the initial estimates and a degree of Brexit positivity persists following reports that chief EU negotiator Barnier sees an improvement in the atmosphere, more engagement from the UK side and a fresh ’buzz’ in talks. However, the Franc is back under 0.9200 and Cable has tested support ahead of 1.2800, as Eur/Gbp consolidates above 0.9100. For the record, nothing new whatsoever from BoE’s Haldane – see headline feed at 9.30BST for bullets and a link to the full speech.

- NZD/AUD – In contrast to the above, recoveries in NZ business sentiment and the outlook for activity, not as weak as forecast Aussie building approvals and better than expected Chinese PMIs that are helping the YUAN claw back losses vs the Greenback towards 6.8100, are all keeping the Antipodes afloat. Nzd/Usd has been over 0.6600 and Aud/Usd up to 0.7150, albeit off peaks as their US counterpart continues to regain poise.

- JPY/CAD/EUR – The Yen remains rangebound vs the Buck and flanked by decent option expiry interest from 105.60-70 (1.1 bn) to 105.15-00 (1.3 bn) following moderately firmer than anticipated Japanese ip data, while the Loonie is still attempting to contain losses around 1.3400 ahead of Canadian monthly GDP and the Euro is striving to maintain 1.1700+ status in the face of stronger sell signals vs the US Dollar.

- SCANDI/EM – Little reaction to Sweden’s NIER upgrading its 2020 jobless rate projection or a reduction in Norges Bank daily FX purchases for October, as Eur/Sek straddles 10.5400 and Eur/Nok holds off 11.1100+ highs on the aforementioned single currency retracement. Elsewhere, EMs are correcting higher after recent heavy depreciation vs the Usd, and even the tormented Rub and Try as trouble across the Armenian-Azeri border rumbles on.

In commodities, crude futures remain softer in early European hours as the rising COVID-19 cases continue to weigh on demand prospects for the complex, with some added pressure for the lackluster sentiment across markets following the US debate. Price saw another leg lower on reports that Beijing is said to be preparing an antitrust investigation into Google, in a sign that US-Sino relations are getting no better. Elsewhere, Norway’s Industri Energi and Safe Labour unions said its workers will not go on strike after agreeing on a wage deal, but Lederne Labour union said its workers will go ahead with strikes and will potentially escalate the situations at today’s meeting. This could cut the country’s oil output by some 470k BPD, according to the Norwegian Oil and Gas Association. WTI Nov resides just sub-39/bbl whilst Brent Dec sees itself marginally above USD 41/bbl. Precious metals meanwhile succumb to the firmer Buck, with spot gold around the USD 1880/oz mark having had drifted from a high of USD 1899/oz; spot silver underperforms but remains north of USD 23.50/oz (vs. high USD 24.32/oz). LME copper prices edge lower in tandem with losses across the stock markets coupled with a firmer Dollar, whilst Dalian iron ore futures rose some 5% amid rekindled fears of supply disruptions.

US Event Calendar

- 8:15am: ADP Employment Change, est. 649,000, prior 428,000

- 8:30am: GDP Annualized QoQ, est. -31.7%, prior -31.7%

- 9:45am: MNI Chicago PMI, est. 52, prior 51.2

- 10am: Pending Home Sales MoM, est. 3.1%, prior 5.9%; Pending Home Sales NSA YoY, est. 17.6%, prior 15.4%

DB’s Jim Reid concludes the overnight wrap

I’m a proud father this morning. One of the twins came home from nursery yesterday with a big badge pinned on him, rewarded for an achievement. As I got closer to it to see what it was for I wondered which advanced skill was being recognised. Had he counted? Had he recognised a word? Had he sung in tune or perhaps been thoughtful towards another child? No, his badge simply said on it “well done for not shouting”. To be fair our twins are so loud that any moment they are not screaming is an achievement and the nursery obviously now feel the same way.

In a raucous debate that was indeed full of shouting, it is unclear that either President Trump or Vice President Biden changed the trajectory of the election last night. The President came into the night down -6.8% in the fivethirtyeight.com national polling average while trailing in many of the battleground states, and we will track how polls change in the next few days. There was very little substance in the debate and almost no new information proffered. The story of the debate will likely surround the President’s consistent interruption, though Mr Biden was not able to stay above the fray and traded insults at times with Mr Trump. Acrimony ruled.

Outside of the debate, we have seen China’s official September PMIs overnight with both the manufacturing (at 51.5 vs 51.3 expected) and non-manufacturing (at 55.9 vs. 54.7 expected) beating consensus expectations and reaffirming the message that the country’s recovery remains on track aided partly by strong exports. In details of the manufacturing PMI, new export orders climbed to 50.8 (vs. 49.1 last month), marking the first time it has printed above 50 this year while the new orders index also rose to 52.8 (vs. 52.0 ). Overall, the official composite PMI printed at 55.1 (vs. 54.5 last month). Alongside, the official PMIs we also saw China’s Caixin manufacturing PMI which came in a touch softer (0.1pt) than expectations at 53.0.

The Hang Seng (+1.18%) and Shanghai Comp (+0.45%) are trading up this morning following the PMI beat. Other markets in the region are mostly trading lower with the Nikkei (-0.84%) and Asx (-1.82%) both down while India’s Nifty (-0.05%) has opened weak. South Korea’s markets are closed for a holiday. Futures on the S&P 500 are also trading weak at -0.67% following the Presidential debate and European futures are pointing to a weak open (Stoxx 50 -0.44% and Dax -0.38%). Meanwhile, oil prices are trading down c. -1%. Elsewhere, Micron Technology said overnight that it has recently halted shipments to China’s Huawei. The company also announced a cut in its capital spending plans and warned about weaker demand from some corporate customers and forecast possible oversupply in a key market next year. Shares of the company fell -3.9% in afterhours trading due to this. In terms of other overnight data, Japan’s September retail sales printed at +4.6% mom (vs. +2.0% mom expected).

Ahead of the debate, risk assets fell back yesterday as markets were unable to maintain the strong momentum from Monday, with negative news on the coronavirus seemingly outweighing more positive consumer confidence numbers. By the close, equities had lost ground on both sides of the Atlantic, with the S&P 500 (-0.48%) and the STOXX 600 (-0.52%) both falling back. Energy stocks led the moves lower thanks to falling oil prices, as both Brent Crude (-3.30%) and WTI (-3.23%) underwent major falls, while banks also struggled to follow-through on their strong start to the week.

Starting with Covid, yesterday saw some negative news from the US, with the daily positivity rate in New York City rising above 3% yesterday for the first time in months, according to Mayor de Blasio. The threshold is a significant one, as de Blasio has said that the city’s schools will shut if the positivity rate is above 3% on a rolling 7-day average basis, though for now that still remains at 1.38%. The US overall has seen hosptilisations plateau at 30,000 after falling from nearly 60,000 in the middle of the summer. With cases again increasing marginally in the US over the last 2-3 weeks attention will shift to hospital capacity as the weather grows colder in the northern US. Meanwhile in Germany, Chancellor Merkel recommended that private parties were limited to 25 people, and in the UK a record 7,152 cases were reported yesterday, which also drove the 7-day average above 6,000. There was some weekend catch up to this data though. Best to look at the 7-day rolling number in the table below for the best state of play.

There was some good news overnight on the pharmaceutical front. A Regeneron Covid-19 antibody cocktail, still in early stage trials, saw positive data that it helped reduce viral levels and improved symptoms. At the same time, data from phase 2 testing showed that the Moderna vaccine triggered a “strong antibody” response in adults, with “severe” side effects in one volunteer. Meanwhile, in a sign of the pandemic’s lasting impact on the hospitality industry, Walt Disney said overnight that it is laying off 28,000 employees in its US resort business, marking one of the deepest workforce reductions of the pandemic. The cuts span the company’s theme parks, cruise ships and retail businesses and will include executives; however, 67% of those being terminated are part time employees.

In the world of central banks, Dallas Fed president Kaplan indicated that he did not expect the US economy to get back on track from the pandemic until late-2022 or even 2023. While not advocating for higher rates, Kaplan said that the Fed should remain accommodative but that may not mean keeping rates at zero. He warned that there were “real costs” to near-zero rates for elongated periods of time, specifically it can “adversely impact savers, encourage excessive risk taking and create distortions in financial markets.” We also heard from New York Fed president Williams who is not worried about inflation, though acknowledged they would deal with it if it came. Williams had a similar time frame for full recovery as Kaplan of 3 years and again seemed to call on fiscal stimulus help, saying that the recovery needed “all the official support it can get.”

And there was some more positive news on the prospects of US fiscal stimulus, with Speaker Pelosi’s deputy chief of staff tweeting that Pelosi and Treasury Secretary Mnuchin spoke yesterday morning on the phone for around 50 minutes, and agreed to speak again today. There will be a floor vote in the Senate on a relief package of some sort later this week according to reports, either the Democrat-written $2.2 trillion fiscal bill or a more bipartisan effort if one can come together. In spite of a lack of stimulus, data from the Conference Board showed US consumer confidence index experiencing the biggest monthly jump in 17 years, with a stronger-than-expected rise to 101.8 in September.

Staying with yesterday, there were some significant headlines from Europe, as a spokesperson for the German presidency of the Council of the European Union said on the recovery fund that “The timetable is in danger of slipping. A delay of the EU budget and the Recovery fund is becoming increasingly likely”. Remember that the package needs to be agreed unanimously, but there’ve been disputes over the possibility of rule-of-law conditions, and yesterday a letter was published from Hungarian PM Orban which called for the Commission Vice President for Values and Transparency to be sacked, after she called Hungary a “sick democracy”.

Over in the fixed income sphere, sovereign bonds rallied yesterday as investors moved out of risk assets. Perhaps the biggest headline came from Italy, where the country’s 30yr yield fell to a fresh all time record low of 1.74%. However there was a strong performance across the board, with yields on 10yr bunds (-1.7bps), OATs (-1.5bps) and BTPs (-2.7bps) all falling back. 10yr Treasury yields also fell -0.3bps, their 4th successive move lower. This came as the US dollar fell -0.41% Tuesday, to start the week with its worst 2-day performance since 31 Aug, however the currency is still set to record its first monthly gain since March.

On Brexit, the 9th round of negotiations began yesterday between the UK and the EU in Brussels, with Bloomberg reporting that the UK has submitted 5 confidential draft legal texts. Negotiations continue until Friday, and the question this week will be whether enough progress can be made for the two sides to be able to reach agreement by Prime Minister Johnson’s self-imposed deadline of October 15, when a summit of EU leaders takes place.

Wrapping up with some of Europe’s data from yesterday, German inflation fell to a 5-year low of -0.4% in September, which was below the -0.1% reading expected and will only add to concerns about weak price pressures in the Euro Area. That said, the European Commission’s economic sentiment indicator for the Euro Area rose for a 5th straight month in September, up to 91.1 (vs. 89.0 expected). Finally in the UK, consumer credit data showed that net borrowing was weaker-than-expected in August, coming in at £0.3bn (vs. £1.5bn expected).

To the day ahead now, and the highlights include an array of central bank speakers, including ECB President Lagarde, chief economist Lane, and the ECB’s Muller, Rehn and Kazimir. Otherwise, there’s also the Fed’s Bowman, Bullard, and Kashkari, along with the Bank of England’s chief economist Haldane. In terms of data, we’ll get the preliminary September CPI readings from France and Italy, the September change in unemployment from Germany, while from the US there’s the third reading of Q2 GDP, August’s pending home sales, the MNI Chicago PMI for September and the ADP employment change for September.

3A/ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 6.31 POINTS OR 0.20% //Hang Sang CLOSED UP 183.52 POINTS OR 0.79% /The Nikkei closed DOWN 359.98 POINTS OR 1.50%//Australia’s all ordinaires CLOSED DOWN 1.11%

/Chinese yuan (ONSHORE) closed DOWN at 6.8100 /Oil DOWN TO 3903 dollars per barrel for WTI and 41.10 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8100 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8151 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

CHINA VS USA//GOOGLE

China’s move after the Trump administration hit giant SMIC last wee, is to target Google’s android operating system in China in their anti trust crackdown

(zerohedge)

Beijing Targets Google’s Android Operating System In Looming Anti-Trust Crackdown

By imposing new sanctions on Chinese chipmaker giant SMIC last week, the Trump Administration signaled that it isn’t letting up on the economic war it’s waging against China. After essentially cutting China’s biggest chipmaker off from its largest customer, Huawei, with sanctions restricting the types of products that can be shipped to Huawei and its subsidiaries, the new sanctions on SMIC will rob it of what’s believed to be its second-most-valuable client, American chipmaker Qualcomm.

Even a ruling handed down on Sunday that spared TikTok from being barred from American app stores is only temporary, and the company must still contend with a later deadline, and further pressure to strike a deal.

Although Trump and his top trade officials have argued these measures are akin to giving China a taste of its own medicine, the expansive trade war being waged by the administration is infuriating to Beijing. Now, Beijing is lashing out at an American tech giant – Google parent Alphabet – by taking a page out of EU antitrust head Margrethe Vestager’s playbook. Reuters reports that China is preparing to launch an anti-trust probe into Alphabet’s Android operating system and attempts by Alphabet to stifle competition in the Chinese market. The case was reportedly first proposed by Huawei, has been submitted by the country’s top market regulator to the State Council’s antitrust committee for review.

Reuters reports that a formal investigation might come as soon as October, and will likely depend on “China’s relationship with the US”. In other words, Beijing is turning up the pressure on an American tech giant and creating a bargaining chip out of thin air.

China is preparing to launch an antitrust probe into Alphabet Inc’s Google, looking into allegations it has leveraged the dominance of its Android mobile operating system to stifle competition, two people familiar with the matter said.

The case was proposed by telecommunications equipment giant Huawei Technologies Co Ltd last year and has been submitted by the country’s top market regulator to the State Council’s antitrust committee for review, they added.

A decision on whether to proceed with a formal investigation may come as soon as October and could be affected by the state of China’s relationship with the United States, one of the people said.

China’s State Administration for Market Regulation, its top anti-trust regulator, is preparing new anti-trust measures that will create yet another barrier to foreign firms operating in the Chinese market. It’s also looking into whether companies like Google have caused “extreme damage” to Chinese companies like Huawei. We wouldn’t be surprised to see Google pay the price for some of the Trump Administration’s aggression.

It also comes as China embarks on a major revamp of its antitrust laws with proposed amendments including a dramatic increase in maximum fines and expanded criteria for judging a company’s control of a market.

A potential probe would also look at accusations that Google’s market position could cause “extreme damage” to Chinese companies like Huawei, as losing the U.S. tech giant’s support for Android-based operating systems would lead to loss of confidence and revenue, a second person said.

Unlike in Europe, most Chinese phones use an open-source version of Android that offers alternatives to Google services. So it’s unclear what, exactly, is being targeted by Beijing. The EU memorably fined Google several times in recent years, including a $5.1 billion hit in 2018 over “anticompetitive” practices like forcing phone makers to pre-install Google apps on Android devices, while adding barriers to non-Google products. Indian regulators, meanwhile, are looking into whether Google has abused its market position to unfairly promote its mobile payments app in India.

“China will also look at what other countries have done, including holding inquiries with Google executives,” said the person.

The second source added that one learning point would be how fines are levied based on a firm’s global revenues rather than local revenues.

Reuters points out that Huawei missed its 2019 revenue target by a whopping $12 billion, which the company blamed on American aggression. Now, just imagine how US stocks might react to Alphabet posting a massive miss on revenue because China effectively banned Android phones from the world’s biggest market.

4/EUROPEAN AFFAIRS

DENMARK/CORONAVIRUS UPDATE

After Sweden, we now have Denmark return to pre Covid normality: no masks no distancing in schools

(Henningsen/21st Century Wire)

Denmark Nears Pre-COVID Normality: No Masks Or Distancing In Schools, Just Common Sense

Authored by Patrick Henningsen via 21st Century Wire,

One of the more diabolical aspects of the protracted COVID ‘crisis’ in countries like the United Kingdom, the United States and Australia, is the intellectually dishonest claim that Coronavirus in their countries is somehow different from the Coronavirus in other western countries.

It’s like there are two parallel universes now. While the Anglosphere continues to ramp-up its emergency ‘pandemic’ measures and mandatory mask and quarantine policies, their Scandinavian counterparts like Sweden, Norway or Denmark have already returned to life as normal; no masks on public transport (although Norway just introduced a new rule today advising masks on crowded carriages), no obsessive social distancing rules, no snap lockdowns, and certainly no draconian laws and threats of £10,000 fines made by government leaders, or holding the country hostage until a wonder vaccine arrives in the spring. The contrast couldn’t be more extreme.

Why has normality not returned to the US and UK?

Perhaps the worst aspect of the new hypochondriac culture being aggressively promoted in the US and UK is how the state bureaucrats and schools are now targeting children and young adults with a relentless regime of restrictive and nonsensical health and safety policies. One of the main drivers of the school chaos in the UK has been the teachers/public service unions, who have seized on the crisis in order to leverage political power and carve out a platform in the national spotlight. Union officials repeated the fallacious claim that schools were no longer safe unless a whole new raft of new rules, regulations and government assurances were put into place. The list of issues and concerns keeps growing by the day and is now threatening to bring normal education to a grinding halt.

As a result of this over-the-top fear-based approach to risk mitigation, the lives of students and their families across the UK have been unnecessarily disrupted. In just the first few weeks of school, many thousands of students have already been removed from school and sent home and placed under under 14 day house arrest-quarantine order by school administrators – all because another student in school or a teacher had tested PCR positive for COVID.

Many schools are also ordering all primary, secondary and high school students to remain under house arrest at home over their half-term break, supposedly to “stop the spread of the virus.”

British authorities have even gone so as to demand that university students remain on campus over the Christmas break in order “stop the spread of COVID to their families back home.”

All of this is taking place at a time where hospitalisations and deaths due to COVID have dropped to near zero in the UK. In other words: the ‘pandemic’, if it ever was one, is now over.

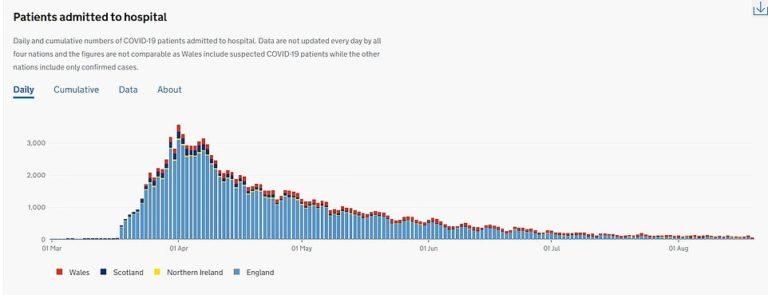

GRAPH: Since May, hospitalisations in the UK have plummeted, as have deaths attributed to COVID19.

Still, neither school or government health officials will readily admit the fact that young people at statistically at near zero risk of any complications due to COVID. Likewise, nearly all teachers fall well below the well-established elderly age-bracket risk zone. In addition to this, UK officials still refuse to acknowledge that the PCR test is not only unreliable as a diagnostic tool for COVID, it also cannot rightly identify whether a positive PCR test is indeed a ‘case’ or even an ‘infection.’ This means that the entire mass-testing effort championed by governments is fatally flawed at source. This is not up for debate, it is a scientific reality.

By contrast, from the very beginning of the crisis, Sweden never closed its schools and only required its university-aged students to temporarily migrate to remote teaching online. The results for Sweden have been impressive – minimal or no interruption for millions of students nationwide during such a crucial stage in their formative educational years.

Unfortunately, the opposite path has been pursued in the US and UK, and the results have been catastrophic.

IMAGE: ‘Normal life’ – a scene from Amagertorv Strøget in Copenhagen, Denmark (Source: Wikicommons)