GOLD:$1902.80 DOWN $9.30 The quote is London spot price

Silver:$23.88 DOWN $0.17 London spot price ( cash market)

your data…

Closing access prices: London spot

i)Gold : $1900.90 LONDON SPOT 4:30 pm

ii)SILVER: $23.76//LONDON SPOT 4:30 pm

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED //Hang Sang CLOSED /The Nikkei closed DOWN 155.22 POINTS OR 0.61%//Australia’s all ordinaires CLOSED DOWN 1.42%

/Chinese yuan (ONSHORE) closed /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED ALL RED// ONSHORE YUAN CLOSED AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7530 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total withdrawals; nil oz

We had 0 kilobar transactions +

ADJUSTMENTS: 0 //

The front month of OCT registered a total of 18,263 contracts for a LOSS of 5871 contracts. We had 5949 notices filed yesterday so we gained 78 contracts or 7800 additional oz will stand for delivery in this active delivery month of October. In gold we have not seen queue jumping start so early in the month. Thus you can bet the farm that throughout October, the total number of gold oz standing will increase from this level.

November gained 148 contracts to stand at 932.

The big December contract GAINED 4298 contracts UP to 445,286 contracts..

THE BIG STORY AGAIN TODAY IS THE HIGH OI STANDING FOR OCTOBER (95.347 tonnes). GENERALLY OCTOBER IS A POOR DELIVERY MONTH AS MOST INVESTORS PREFER TO SKIP THIS MONTH AND MOVE STRAIGHT TO DECEMBER. IT LOOKS LIKE SOME MAJOR ENTITY(GOLDMAN SACHS) JUST CANNOT WAIT FOR DECEMBER AS THEY ARE MAKING THEIR MOVE ON OCTOBER FOR PHYSICAL METAL. GOLDMAN SACHS ONE OF THE LEADERS OF THE NEW LONDON LME EXCHANGE NEEDS THE GOLD INVENTORY FOR LIQUIDITY AND INITIAL CONTRIBUTION WITH OTHER MAJOR PLAYERS. THE MAJOR DIFFERENCE BETWEEN THIS MONTH AND OTHER MONTHS IS THAT THIS GOLD STANDING IN OCTOBER WILL LEAVE THE COMEX AND HEAD FOR LONDON.

We had 4015 notices filed today for 401500 oz OR 12.49 TONNES.

To calculate the INITIAL total number of gold ounces standing for the OCT /2020. contract month, we take the total number of notices filed so far for the month (16,406) x 100 oz , to which we add the difference between the open interest for the front month of OCT (18,263 CONTRACTS ) minus the number of notices served upon today (4015 x 100 oz per contract) equals 3,065,400 OZ OR 95.347 TONNES) the number of ounces standing in this active month of Oct

thus the INITIAL standings for gold for the OCT/2020 contract month:

No of notices filed so far (16,406, x 100 oz +18,263 OI) for the front month minus the number of notices served upon today (4015) x 100 oz which equals 3,065,400 oz standing OR 95.104 TONNES in this active delivery month. This is a HUGE amount for gold standing for a OCT delivery month (a poor active delivery month).

We gained 78 contracts or an additional 7800 oz will stand on this side of the pond searching for metal.

NEW PLEDGED GOLD: BRINKS

592,648.822 oz NOW PLEDGED SEPT 15.2020/HSBC 18.433 TONNES ( A HUGE INCREASE FROM 10.6)

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

277,934.09 oz (some deleted august 3) JPM 8.644 TONNES

610,238.285 oz pledged June 12/2020 Brinks/ july 2/july 21 19.017 tonnes

51,084.609 oz Pledged August 21/regular account 1.588 tonnes jpm

total pledged gold: 1,574,454.119 oz 48.97 tonnes

total registered, pledged and eligible (customer) gold 36,858,025.492 oz 1,146.43 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1020.09 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

END

And now for the wild silver comex results

And now for the wild silver comex results

INITIAL STANDINGS

OCT. SILVER COMEX CONTRACT MONTH//INITIAL STANDING

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

131,497.150 oz

CNT

Delaware

HSBC

|

| Deposits to the Dealer Inventory |

546,552.500 oz

Manfra

|

| Deposits to the Customer Inventory |

1,012,674.220 oz

JPMorgan

Delaware

Scotia

|

| No of oz served today (contracts) |

162

CONTRACT(S)

(810,000 OZ)

|

| No of oz to be served (notices) |

573 contracts

2,865,000 oz)

|

| Total monthly oz silver served (contracts) | 1207 contracts

6,035,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

total dealer deposits: 546,552.500 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 3 deposits into the customer account (ELIGIBLE ACCOUNT)

i)into JPMorgan: 575,718.600 oz

ii) Into Delaware; 992.800 oz

iii) Into Scotia: 546,552.500

JPMorgan now has 186.7 million oz of total silver inventory or 49.27% of all official comex silver. (186.7 million/378.941 million

total customer deposits today: 3,339,411.780 oz

we had 3 withdrawals:

total withdrawals; 131,497.150 oz

We had 2 adjustments/ dealer to customer

i) Brinks: 5023.400

ii) CNT: 5,134.300

Total dealer(registered) silver: 140.918 million oz

total registered and eligible silver: 378.941 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

October had 735 notices outstanding for a GAIN of 68 contracts. We had 19 notices served upon yesterday so we GAINED 87 contracts or 435,000 additional oz of silver will stand in this non active month of October.

November saw a gain of 91 notices up to 382 contracts.

December saw a GAIN of 173 contracts up to 131,941 contracts.

The total number of notices filed today for the OCT 2020. contract month is represented by 162 contract(s) FOR 810,000 oz

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 1207 x 5,000 oz = 6,035,000 oz to which we add the difference between the open interest for the front month of OCT( 735) and the number of notices served upon today 162x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the OCT/2019 contract month: 1,207 (notices served so far) x 5000 oz + OI for front month of OCT (735)- number of notices served upon today (162) x 5000 oz of silver standing for the OCT contract month .equals 8,900,000 oz. ..VERY STRONG FOR A NON ACTIVE MONTH.

We gained 87 contracts or 435,000 additional oz will stand for silver metal on this side of the pond as they refused to morph into a London based forwards.

TODAY’S ESTIMATED SILVER VOLUME : 66.411 CONTRACTS // volume rather slow//

FOR YESTERDAY 76,636 ,CONFIRMED VOLUME// slower than normal/

YESTERDAY’S CONFIRMED VOLUME OF 97,254 CONTRACTS EQUATES to 0.486 billion OZ 69.4% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 2.79% ((OCT 2/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.67% to NAV: (OCT 2/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/2.79%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 19.26 TRADING 18.60///NEGATIVE 3.42

END

And now the Gold inventory at the GLD/

OCT 2/WITH GOLD DOWN $7.30 TODAY, A HUGE CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 9.3 TONNES INTO THE GLD//INVENTORY RESTS AT 1278.19 TONNES

OCT 1/WITH GOLD UP $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1268.89 TONNES

SEPT 30//WITH GOLD DOWN $6.80 TODAY, NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1268.89 TONNES

SEPT 29/WITH GOLD UP $19.10//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1268.89 TONNES

/SEPT 28//WITH GOLD UP $14.30 DOLLARS: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.05 TONNES INTO THE GLD//INVENTORY RESTS AT 1268.89 TONNES

SEPT 25//WITH GOLD DOWN 410.80 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .3 TONNES FROM THE GLD////INVENTORY RESTS AT 1266.84 TONNES

SEPT 24/WITH GOLD UP $9.80 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1267.14TONNES.

SEPT 23//WITH GOLD DOWN $28.00 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 11.68 TONNES FROM THE GLD////INVENTORY RESTS AT 1267.14 TONNES

SEPT 22/WITH GOLD DOWN $4.50 TODAY, A MONSTROUS CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 18.98 TONNES OF PAPER GOLD ENTER THE GLD///// INVENTORY RESTS AT 1278.62TONNES

SEPT 21/WITH GOLD DOWN $47.20 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 12.94 TONNES INTO THE GLD///INVENTORY RESTS AT 1259.64TONNES

SEPT 18/WITH GOLD UP $10.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS THIS WEEKEND AT: 1246.99 TONNES

SEPT 17/WITH GOLD DOWN $18.05 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD//INVENTORY RESTS AT 1246.99 TONNES

SEPT 16.WITH GOLD UP $4.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1247.57 TONNES

SEPT 15//WITH GOLD UP $2.25 TODAY: A SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .43 TONNES FROM THE GLD//INVENTORY RESTS AT 1247.57 TONNES

SEPT 14/WITH GOLD DOWN 90 CENTS TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.96 TONNES FROM THE GLD////INVENTORY RESTS AT 1248.00 TONNES

SEPT 11/WITH GOLD DOWN $14.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1252.96 TONNES

SEPT 10/WITH GOLD UP $8.85 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.92 TONNES INTO THE GLD////INVENTORY RESTS AT 1252.96 TONNES

SEPT 9/WITH GOLD UP $19.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1250.04 TONNES

SEPT 8/WITH GOLD UP $8.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1250.04 TONNES

SEPT 4//WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1250.04 TONNES

SEPT 3/WITH GOLD DOWN $7.50 ON THIS 2ND DAY OF A 3 DAY RAID: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1250.04 TONNES

SEPT 2/WITH GOLD DOWN $34.00 TODAY, WE HAVE 2 SMALL CHANGES IN GOLD INVENTORY AT THE GLD: 2 WITHDRAWALS OF .87 TONNES AND.59 TONNES FROM THE GLD////INVENTORY RESTS AT 1250.04 TONNES

SEPT 1/WITH GOLD UP $7.10 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1251.50 TONNES

AUGUST 31//WITH GOLD UP $5.90 TODAY/WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD..//INVENTORY RESTS AT 1251.50 TONNES/

AUGUST 28/WITH GOLD UP $38.20 TODAY, WE SURPRISINGLY HAD A .59 TONNE WITHDRAWAL//INVENTORY RESTS AT 1251.50 TONNES

AUGUST 27/WITH GOLD DOWN 17.50 TODAY: WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 3.24 TONNES INTO THE GLD//INVENTORY REST AT 1252.09 TONNES

AUGUST 26/WITH GOLD UP $26.70 TODAY/ WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.53 TONNES FROM THE GLD//RESTS AT 1248.85 TONNES

AUGUST 25/WITH GOLD DOWN $14.60 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//RESTS AT 1252.38 TONNES

AUGUST 24//WITH GOLD DOWN $7.20 TODAY: WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1258.38 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

OCT 2/ GLD INVENTORY 1268.89 tonnes*

LAST; 913 TRADING DAYS: +338.35 NET TONNES HAVE BEEN ADDED THE GLD

LAST 813 TRADING DAYS://+517.28 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

OCT 2/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 549.116 MILLION OZ//

OCT 1/WITH SILVER UP 66 CENTS TODAY, A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.489 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 549.116 MILLION OZ//

SEPT 30//WITH SILVER DOWN 96 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 186,000 OZ FROM THE SLV.//INVENTORY RESTS AT 550.605 MILLION OZ..

SEPT 29/WITH SILVER UP 86 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.791 MILLILON OZ//

SEPT 28//WITH SILVER UP 48 CENTS TODAY: A HUGE DEPOSIT OF 3.769 MILLION OZ CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.791 MILLION OZ//

SEPT 25/WITH SILVER DOWN 14 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: 2 TRANSACTIONS: A PAPER WITHDRAWAL OF 8.28 MILION OZ FROM THE SLV AND A DEPOSIT OF 1.861 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 547.022 MILLION OZ//

SEPT 24//WITH SILVER UP 15 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 553.443 MILLION OZ//

SEPT 23//WITH SILVER DOWN $1.41: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.048 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 553.443 MILLION OZ///

SEPT 22/WITH SILVER DOWN ONE CENT TODAY: A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.141 MILLION OZ////INVENTORY RESTS AT 555.491 MILLION OZ..

SEPT 21/WITH SILVER DOWN $2.43 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV A PAPER WITHDRAWAL OF 1.862 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 553.350MILLION OZ//

SEPT 18. WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 555.212 MILLION OZ/

SEPT 17/WITH SILVER DOWN 31 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.537 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 555.212 MILLION OZ/

SEPT 16//WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.749 MILLION OZ//

SEPT 15/WITH SILVER UP 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.793 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 558.749 MILLION OZ..

SEPT 14/WITH SILVER UP 47 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS A) 1.675 MILLION OZ AND ANOTHER B) 0.931 MILLION OZ/ FROM THE SLV////INVENTORY RESTS AT 555.956 MILLION OZ//

SEPT 11/WITH SILVER DOWN 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.562 MILLION OZ//

SEPT 10/WITH SILVER UP 16 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.607 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 558.562 MILLION OZ.

SEPT 9/WITH SILVER UP 6 CENTS TODAY: STRANGE: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.63 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 561.169 MILLION OZ

SEPT 8/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 564.799 MILLION OZ

SEPT 4//WITH SILVER DOWN 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 3.631 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 564.799 MILLION OZ//

SEPT 3//WITH SILVER DOWN 50 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.258 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.430 MILLION OZ/./

SEPT 2.WITH SILVER DOWN $1.04 TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.365 MILLION OZ FROM THE SLV///INVENTORY REST AT 571.688 MILLION OZ.

SEPT 1//WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 31/WITH SILVER UP 80 CENTS TODAY: A HUGE CHANGE IN THE SLV//A DEPOSIT OF 2.982 MILLION OZ ENTERS THE SLV/INVENTORY RESTS AT 574.053 MILLION OZ//

AUGUST 28/WITH SILVER UP 48 CENTS TODAY: A MASSIVE PAPER DEPOSIT OF 4.652 MILLION OZ ENTERS THE SLV//INVENTORY RESTS AT 571.071 MILLION OZ

AUGUST 27/WITH SILVER DOWN 28 CENTS TODAY// NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.419 MILLION OZ

AUGUST 26//WITH SILVER UP $1.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.65 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 566.419 MILLION OZ..

AUGUST 25/WITH SILVER DOWN 21 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.607 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 571.074 MILLION OZ//

AUGUST 24//WITH SILVER DOWN 18 CENTS TODAY: WE HAD A NO CHANGES//INVENTORY RESTS AT 573.843 MILLION OZ//

OCT 2.2020:

SLV INVENTORY RESTS TONIGHT AT

549.116 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

Butler thinks that the raids on gold and silver will be over and that only the algos and their HFT brethren will be left to move the precious metals. He thinks gold and silver will now rise from this point on

Ted Butler

Ted Butler: Government’s settlement with JPMorgan is more than a slap on the wrist

8:50p ET Thursday, October 1, 2020

Dear Friend of GATA and Gold:

Silver market analyst Ted Butler today explains why he thinks the settlement by the Justice Department and Commodity Futures Trading Commission with JPMorganChase about the bank’s manipulation of gold and silver futures prices is more than the trivial “slap on the wrist” widely suspected.

Butler notes that the bank now is operating under a “deferred prosecution agreement” with the Justice Department and isn’t likely to mess with the gold and silver futures markets for a while

…

He thinks the bank’s termination of its “spoofing” will increase the price impact of “high-frequency trading.” He also thinks the resolution of the case will increase suspicions of market rigging in gold and silver and cause traders to be more watchful.

And the settlement, Butler argues, increases the likelihood that gold and silver prices will rise.

Butler’s analysis is headlined “The DOJ-CFTC-JPMorgan Settlement” and it’s posted at GoldSeek’s companion site, SilverSeek, here:

https://silverseek.com/article/dojcftcjpmorgan-settlement

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Actiom Committee Inc.

CPowell@GATA.org

The DOJ/CFTC/JPMorgan Settlement

As widely telegraphed over the past week, the US Justice Department and Commodity Futures Trading Commission (along with the SEC) have settled the precious metals spoofing/manipulation case which first came into view in November 2018 with the announcement of a guilty plea by a former JPMorgan trader. The total fine of $920 million was the largest in CFTC history and the settlement included a Deferred Criminal Prosecution Agreement, the third (by my count) such agreement involving precious metals manipulation (BankAmerica and Scotiabank had previously entered into DPA’s involving precious metals manipulation).

As expected, the settlement narrowly focuses on spoofing, the illegal short term trading device and not the much more serious long term suppression of silver (and gold) prices that I claim JPMorgan has been guilty of since 2008. As such, any claims by victims of JPMorgan’s illegal activities would have to show damage from very short term trading, a difficult and expensive undertaking. As I have explained previously, were the Justice Department and CFTC to have alleged a long term suppression of prices by JPMorgan that would have, effectively, put the bank out of business – period. Accordingly, no such finding was possible.

I’m not going to spend too much time on summarizing the case to this point, as it would be more instructive to look ahead and I believe there is plenty to anticipate as a result of the settlement. As long term subscribers might be aware, I began my focus on JPMorgan’s manipulation of silver and gold a year before I started this subscription service (in August 2009) when I discovered, via the August 2008 Bank Participation Report that JPM became the largest short seller in COMEX silver and gold as result of its takeover of Bear Stearns in March 2008. Subsequently, of the more than 1100 articles I have penned on these pages, almost all have featured and accused JPMorgan of manipulation. (I’ve sent all my articles to JPMorgan and the CFTC, as well as the CME Group).

As a result of a number of my articles around the time of the August 2008 Bank Participation Report and reader petitions, a formal 5 year investigation was initiated by the CFTC into silver manipulation, involving the DOJ and which was later reported to have focused on JPMorgan. Although that investigation was concluded with no charges, I continued to allege that JPMorgan was manipulating the silver and gold markets.

On April 30, 2018, I called and wrote to the Public Integrity Section of the FBI, complaining that the CFTC was guilty of malfeasance in allowing JPMorgan to amass a perfect trading record in COMEX silver and gold futures, in which it never suffered a trading loss when shorting excessive amounts of metals contracts and then used its ability to suppress prices to accumulate massive amounts of physical silver and gold on the cheap. Based upon the timeline of the case and recent reporting on Bloomberg, I’m convinced my complaint prompted the Justice Department to take a closer look at JPMorgan, the first step of a process that concluded yesterday.

So while the Justice Department took a pass on going after JPMorgan on the much more serious grounds of price suppression and the accumulation of physical silver and gold at the manipulated prices it created by excessive short selling, at least it dinged JPM pretty good and, most importantly, brushed the bank back from hugging the plate (a baseball term for intimidation). While the $920 million monetary penalty is the largest in CFTC history, it’s widely acknowledged that to JPMorgan, it is no more than nickels and dimes.

The same cannot be said of the Deferred Criminal Prosecution Agreement; particularly because this is not JPMorgan’s first DPA. The only thing worse is a straight criminal prosecution, which would, effectively, put a financial institution out of business (think Arthur Anderson). Although individual traders from JPMorgan still face criminal prosecution, that’s quite different than the bank itself being so charged. More than any amount of a monetary fine, a DPA carries serious ramifications and you can be sure that it has gotten JPM’s attention – just as it did BankAmerica/Merrill Lynch and Scotiabank, which also agreed to DPA’s for precious metals spoofing/manipulation. It’s getting to be easier to name those banks not (yet) agreeing to a DPA for spoofing.

Make no mistake, none of these banks would be so foolhardy as to knowingly violate the terms of their agreements with the Justice Department. And these agreements are not limited to spoofing; they include all manner of activities that can be considered illegal or manipulative. You can be sure that every attempt will be made at JPMorgan and the other banks, even those not charged, to remain on the up and up in precious metals for the foreseeable future. As such, this is not a big inducement to continue the decades-old COMEX manipulation. And that’s the first big takeaway.

I know the popular prevailing opinion is that JPMorgan got a wrist slap and it will soon be back to manipulating silver and gold. I would respectfully disagree. Criminal activity is not well-served when it is under close scrutiny by those capable of putting the criminals in prison or out of business. Suddenly, the landscape for continued price manipulation in silver (and gold) has gotten quite inhospitable. The old way of doing business would appear to have changed. Let me be clear in what I am saying. I think this settlement is far more significant than is widely believed.

I will acknowledge upfront that just because I have been on JPMorgan’s case like white on rice since the fall of 2008 and engaged in attempting to end the COMEX silver manipulation for more than 35 years, does it mean that my take is correct. If I turn out to be wrong, I will admit it, as and when the evidence dictates. But at this point, I believe the settlement is a seminal event in what has been a lifetime journey for me. Not just because of the settlement, but including other important factors as well, I believe the price path ahead for silver will be markedly different from the past.

In addition to confirming (at least to me) that my complaint of April 30, 2018 to the FBI was what tripped off the fresh look by the Justice Department into JPMorgan months later, I learned something important from the Bloomberg article written in advance of the just-announced settlement.

What I learned from the article was that spoofing – the entering of orders immediately canceled and intended to manipulate prices in the very short term – was a trading device developed by JPMorgan and other banks to offset the effects of High Frequency Trading (HFT) – computer to computer operations run by non-bank trading firms. I did know that the banks were the main practitioners of spoofing (due to repeated public charges), but never knew why that was so. Let’s face it, I and most of you aren’t engaged in high-speed computer to computer trading, as it has nothing to do with long term analysis and investment.

Yet, at the same time, as I described just a few days ago in the weekly review, this HFT and high-speed computer to computer trading has come to dominate not just silver and gold, but trading in all markets. I’m not excusing in any way the banks resorting to the illegal practice of spoofing to counterbalance the price-controlling influence of widespread and all-encompassing computer to computer trading, I’m just explaining that I learned something I feel is important from the Bloomberg article.

As a result, it seems to me, at a minimum, that the crackdown by the regulators on spoofing by the banks means that an important counterbalance to the all-pervasive influence of computer to computer trading has just been eliminated, or largely so, making HFT even more of a price influence than otherwise. I can’t imagine this was the Justice Department’s or CFTC’s intent, but the road to (price) perdition is paved with good intentions. It’s hard for me to see how the settlement doesn’t strengthen the influence of high-speed computer to computer trading. What does this mean for silver and gold?

Well for starters, as I discussed on Saturday, this should increase price volatility and the magnitude of both up and down price moves. There’s little question in my mind that the sharp, near $10 price rise in silver in mid-July, followed by the more recent sharp, near $7 price selloff, reflects the growing influence of high speed computer to computer trading, aided by the forced withdrawal from spoofing by the banks. I am not necessarily putting a value judgement on this development, just trying to analyze the facts as they appear. That said, I think the price discovery process is nuts, but it is what it is.

Therefore, it seems most reasonable to expect sharper up and down moves than we’ve seen until now and position ourselves as appropriately as possible – meaning first to be mentally prepared for big down, but especially big up moves in silver. In fact, I don’t have much difficulty seeing a fairly quick up move in silver, whenever it starts, of $20 or more due to the effect of now-unencumbered high-speed computer to computer trading, coupled with silver’s spectacular fundamentals and the inevitability of an industrial user/investor rush to the physical metal.

Overarching the retreat from spoofing by the banks and the strengthening of HFT, of course, is the likely behavior of the 8 big shorts in COMEX silver and gold. While the Justice Department and CFTC will remain silent on this issue, from fear of attracting attention to the main reason for silver’s long term price suppression, the CFTC’s own data reveal a remarkable change of pattern over the past year or so in gold and more recently in silver. It’s no secret that these big shorts have suffered mightily (despite very recent relief on the latest selloff) for the first time where they have always enjoyed previous consistent success. And the big shorts have certainly appeared to have lost their previous appetite for shorting in near-unlimited quantities on rallies of late.

I am not suggesting the risk of selloffs is a thing of the past. What I am suggesting is that a confluence of forces have aligned that promise to propel silver (and gold) prices far higher than is currently imagined. While it is in the eye of the beholder as to whether the just-announced settlement between the DOJ/CFTC and JPMorgan was a wrist slap or a seminal event, I would suggest it could be both. Lost in the settlement is the fact that JPMorgan still has managed to pull off the double cross of the ages against its former big short partners in crime. In fact, its agreement with the regulators puts it in perfect position to do the one thing that would make the bank the most money possible, namely, nothing.

If JPMorgan abides by the terms of the Deferred Criminal Prosecution Agreement it has just entered into with the Justice Department and ceases to spoof or otherwise engage in manipulative trading practices, it’s hard for me to see how silver (and gold) prices don’t soon soar. In effect, the DOJ and CFTC have given JPMorgan the go-ahead to make a bloody fortune (on top of the bloody fortune it has already amassed). By not adding to shorts or engaging in spoofing to offset HFT high-speed computer to computer trading, there’s no reason prices won’t soar at some point.

I still reckon that JPMorgan or its insiders hold at least 700 million ounces of physical silver and 25 million ounces of physical gold on which more than $20 billion in open profits have accrued (despite the recent selloff). And my estimates may be too low. For instance, I claim that JPMorgan has been accumulating physical metals for some 9 years. In the case of gold, JPM’s holdings would amount to less than one percent of all the gold bullion in the world (less than a half of one percent of all the gold in the world). But seeing how long JPM has been accumulating physical metal and has, effectively, unlimited buying power, is it inconceivable that it could have accumulated, instead of less than one percent of the world’s gold bullion, less than two percent? That would give it 50 million ounces of gold. Just sayin’.

If the settlement does result in JPMorgan sitting on its hands and allowing silver and gold prices to soar, then we are about to enter a new era – quite different than the past several decades. If, however, JPMorgan and the other big shorts quickly resort to past practice, as most widely believe, and add aggressively to short positions on the next rally, then what I just opined will be wrong and I will admit as much. But it has been quite some time – more than six months since either JPM or the other big COMEX shorts have aggressively added to silver and gold shorts on the COMEX and I believe it is no coincidence that the lack of new shorting contributed mightily to what were the greatest price rallies in gold and silver in history. And I see no reason that, if the lack of shorting continues, even greater rallies lie ahead.

Finally, the fact that the settlement has now been finalized and widely publicized means that more observers, not less, are now at least somewhat aware that JPMorgan and other banks have engaged in illegal trading activities in COMEX silver and gold. With that greater awareness comes a greater sensitivity to suspicions or allegations of additional illegal activities in the future. Certainly, if JPMorgan (or the big 8) adds aggressively to short positions on the next rally, in addition to admitting that my premise about the future was wrong, you can be sure that I will do everything in my power to convince the regulators to get after these sleazy crooks and SOBs. Count on it.

Ted Butler

October 2

END

Your weekend reading material: emerging evidence of hyperinflation

(Alasdair Macleod)

Alasdair Macleod: The emerging evidence of hyperinflation

By Alasdair Macleod

GoldMoney, St. Helier, Jersey, Channel Islands

Thursday, October 1, 2020

In last week’s article I showed why empirical evidence of fiat money collapses are relevant to monetary conditions today. In this article I explain why the purchasing power of the dollar is hostage to foreign sellers, and that if the Fed continues with current monetary policies the dollar will follow the same fate as John Law’s livre in 1720.

As always in these situations, there is little public understanding of money and the realisation that monetary policy is designed to tax people for the benefit of their government will come as an unpleasant shock.

…

The speed at which state money then collapses in its utility will be swift.

This article concentrates on the U.S. dollar, central to other fiat currencies, and where the monetary and financial imbalances are greatest. …

… For the remainder of the commentary:

https://www.goldmoney.com/research/goldmoney-insights/the-emerging-evide…

END:

Dalio and Kitco pretend central banks do not create imaginary of paper gold/silver.

a good read…

(Ray Dalio/Kitco/GATA)

Dalio’s Bridgewater Associates and Kitco News pretend central banks don’t create gold

10:08p ET Thursday, October 1, 2020

Dear Friend of GATA and Gold:

Who is more negligent here — Ray Dalio’s Bridgewater Associates for recommending investment in gold because “it’s wise to hold some of what central banks can’t create more of,” or Anna Golubova of Kitco News for failing to challenge that premise by noting that central banks long have created vast amounts of imaginary gold by leasing it and swapping it with other central banks and their agent bullion banks?

…

Have the Bridgewater people and Golubova really never taken a look at the secret March 1999 report of the staff of the International Monetary Fund, published by GATA eight years ago? The report dislcoses that IMF-member central banks couldn’t bear to publicize their gold swaps and leases because doing so would expose their interventions in the gold and currency markets and be “highly market-sensitive.”

That is, disclosure of swaps and leases might reveal just how much central banks already had rigged the gold and currency markets with imaginary metal and how much ammunition they had left for their rigging.

The secret IMF staff report is here:

http://www.gata.org/node/12016

And don’t the Bridgewater people and Golubova remember the March 2010 hearing of the U.S. Commodity Futures Trading Commission at which it was disclosed that bullion banks commonly trade as much as a hundred times more gold than they actually possess? With the help of metal consultancy CPM Group’s Jeffrey Christian, the late GATA board member Adrian Douglas explained it here:

And have the Bridgewater people and Golubova never heard of Federal Reserve Chairman Alan Greenspan’s testimony to Congress in July 1998? That’s when Greenspan explained that central banks were not leasing gold according to their cover story — to earn a little income on a supposedly dead asset — but rather to push the gold price down. “Central banks,” Greenspan said, “stand ready to lease gold in increasing quantities should the price rise”:

https://www.federalreserve.gov/boarddocs/testimony/1998/19980724.htm

That is, for all practical purposes central banks long have been “creating” gold — imaginary gold, unbacked certificate gold — precisely to prevent the old monetary metal from gaining too much value against their own currencies. That’s why the great disparagement of gold in the last two decades has been that even as it has risen in price, it has not kept up with inflation.

Bridgewater Associates, an investment company, is a fiduciary and so is obliged not to mislead its investors. As a news organization Kitco News is obliged not to mislead its readers and viewers, and obliged to question misinformation like Bridgewater’s before reporting it.

But nothing could be more misleading than to tell people that central banks can’t “create” gold when “creating” imaginary gold has been their desperate work for decades.

Golubova’s credulous report on Bridgewater’s pious nonsense can be found at Kitco News here:

https://www.kitco.com/news/2020-10-01/Ray-Dalio-s-Bridgewater-on-gold-It…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

iii) Other physical stories:

J Johnson’s Commodity report

https://www.jsmineset.com/2020/10/02/golds-3-4-billion-dollar-order-is-waiting-to-get-real/

Gold’s 3.4 Billion Dollar Order Is Waiting to Get Real

Posted October 2nd, 2020 at 9:17 AM (CST) by J. Johnson & filed under General Editorial.

Great and Wonderful Friday Morning Folks,

Gold is flat to lower in the early morning with the trade at $1,914, down $2.30 after dipping down to $1,895.20 with the high so far today up at $1,923.60. Silver is down 16.9 cents with the trade at $24.07 recovering from the low at $23.58 with the high up at $24.285. The US Dollar is up 13.3 points with the value pegged at 93.895, after passing the double zeros again, with the high at 94.09 and the low much closer at 93.76. Of course, all this happened before 5 am pst, the Comex open, the London close, and after Nancy and team decided to give themselves a higher relief package instead of learning how to spend within a budget. Please don’t get me wrong here, funds are definitely needed for those that got their jobs canceled by politics. I’m simply waiting to see the list of added-on benefactors. Will these additional funds go to a group of “woke” colleges and institutions, that are currently being defunded because they teach worst-case socialism instead of teaching our children exceptionalism, which is to stand on their own two feet, live within their abilities, adapt, and to thrive on their own earned incomes?

Could it be the Emerging Markets Currencies we watch, are leading today’s US$ futures prices? It’s something to consider, maybe, with Venezuela’s Bolivar now pricing Gold at 19,116.08, a gain of 118.87 Bolivar with Silver’s price now at 240.399 it too gaining 3.246 Bolivar. Argentina’s Peso price for Gold is now at 145,812.36, an increase of 973.08 Peso’s with Silver price gaining 26.41 with the last trade at 1,833.26 A-Peso’s. Gold under the Turkish Lira also gained 93.42 T-Lira’s with the last trade at 14,812.32, Silver under the same conditions is now priced at 186.343, gaining 0.314 of a T-Lira.

October Silver’s Delivery Demands now has a post of 735 fully paid for contracts with a Volume of 12 up on the board and a trading range between $24.05 and $23.58 with the last swap at the high, down 14.3 cents from yesterday’s fix. Thursday’s activity inside the deliveries happened in between $23.975 and $23.395 with the last buy at the high with the calculated Comex close figured at $24.19, up 76 cents, and where no trade was made, which included a Volume of 214 which also increased today’s demand count by 68 contracts. Silver’s Overall Open Interest also increased by 625 Contracts bringing today’s early morning total to 155,514 Overnighters to go against the physicals.

October Gold’s Delivery Demands now has a post of 18,263 fully paid for contracts up on the board with a trading range between $1,913 and $1,893.90 with the last buy at $1,907.20, down $1.20 with a total of 101 contracts swapping hands already. Yesterday’s activity inside the deliveries happened in between $1,909.60 and $1,882.50 with the last buy at $1,903.50 with the cCc at $1,908.40. This is still a 3.483 Billion Dollar order waiting to get real. As of this early morning, Gold’s Overall Open Interest is tallied at 557,424 proving a gain of 768 shorts to trade against the physicals. And just in time too, since we have the Unemployment numbers to deal with in under an hours’ time.

5 days from today we’ll have another biased debate between the President and all the socialists inside the challengers earpiece and with another clear and pure Joe supporter to ask the fair and balanced questions. I wonder if this debate committee will ever allow the president to pick a narrator, after all Trump did request another Joe to moderate, and it appears the main stream media, cannot let that happen because Joe Rogan is not one of them. Something else that is happening is the NYTimes admits WHO’s decision, not to close our borders at the start of the plandemic, was based on “Politics”, Not Science. We all remember the continued Xenophobic remarks being made with Nancy going to China town to say “Don’t Worry, Be Happy” and how the left was claiming they had science on their side. So, what’s the difference between real science and media promoted (or is it programmed) science? It’s right here being used to support a political side.

Something else came up last night, our Justice Department sent this …. Proposed Amendments To Address Interest Rate Benchmarks…. “ISDA’s process, including its cooperation with government regulators and its consultation-driven process for obtaining feedback from industry participants, has had the effect of clarifying the practical issues involved in planning for when LIBOR and other IBORs are no longer available and preparing for a smooth transition away from IBORs to other reference rates,” ….. “This is in part because investigations by U.S. and regulators from other jurisdictions uncovered explicit manipulation of the submissions from certain banks to administrators of LIBOR and other interest rate benchmarks. In addition, the United Kingdom’s Financial Conduct Authority, LIBOR’s regulator, has publicly stated that firms cannot rely on LIBOR being published after 2021.”

Is this Brexit or another exit?

Enjoy your weekend and keep the attitudes positive. If you are in possession of physical Silver and Gold, and it’s in your hand, you have more reasons to Don’t worry Be Happy. As Always …

Stay Strong!

Jeremiah Johnson

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

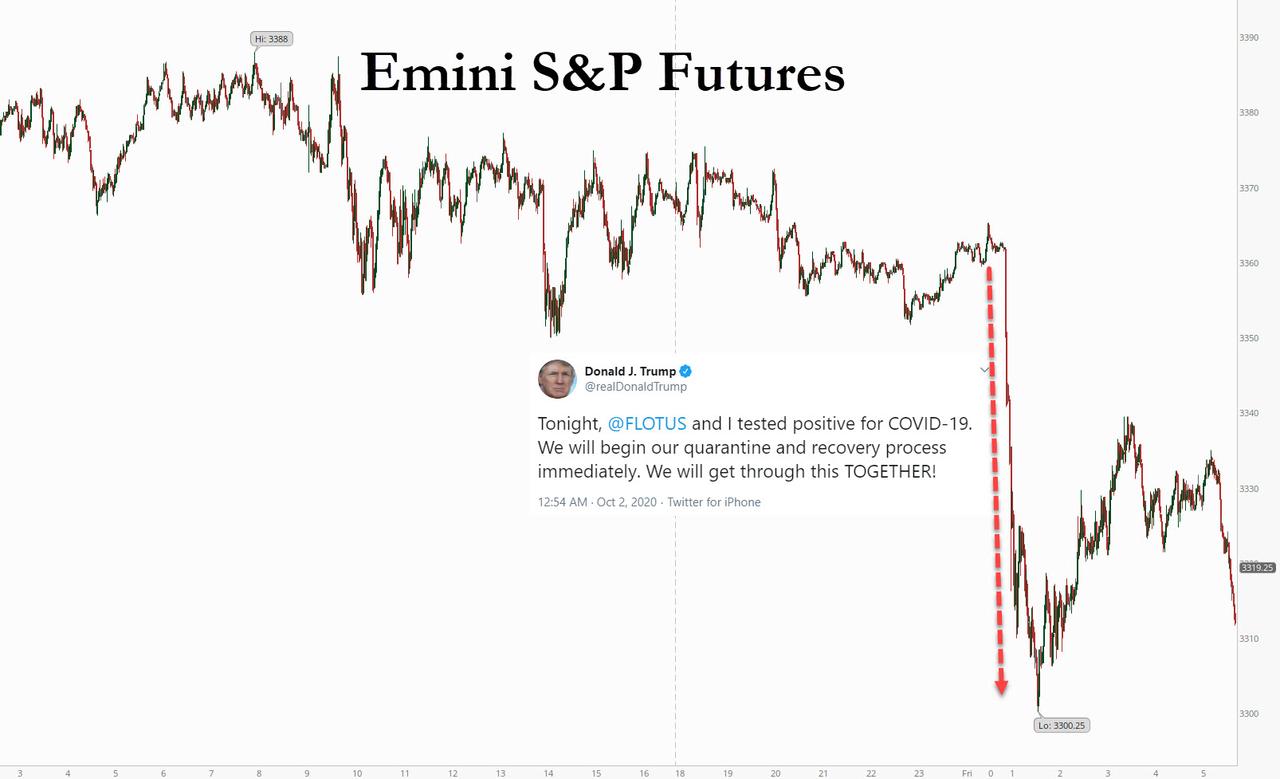

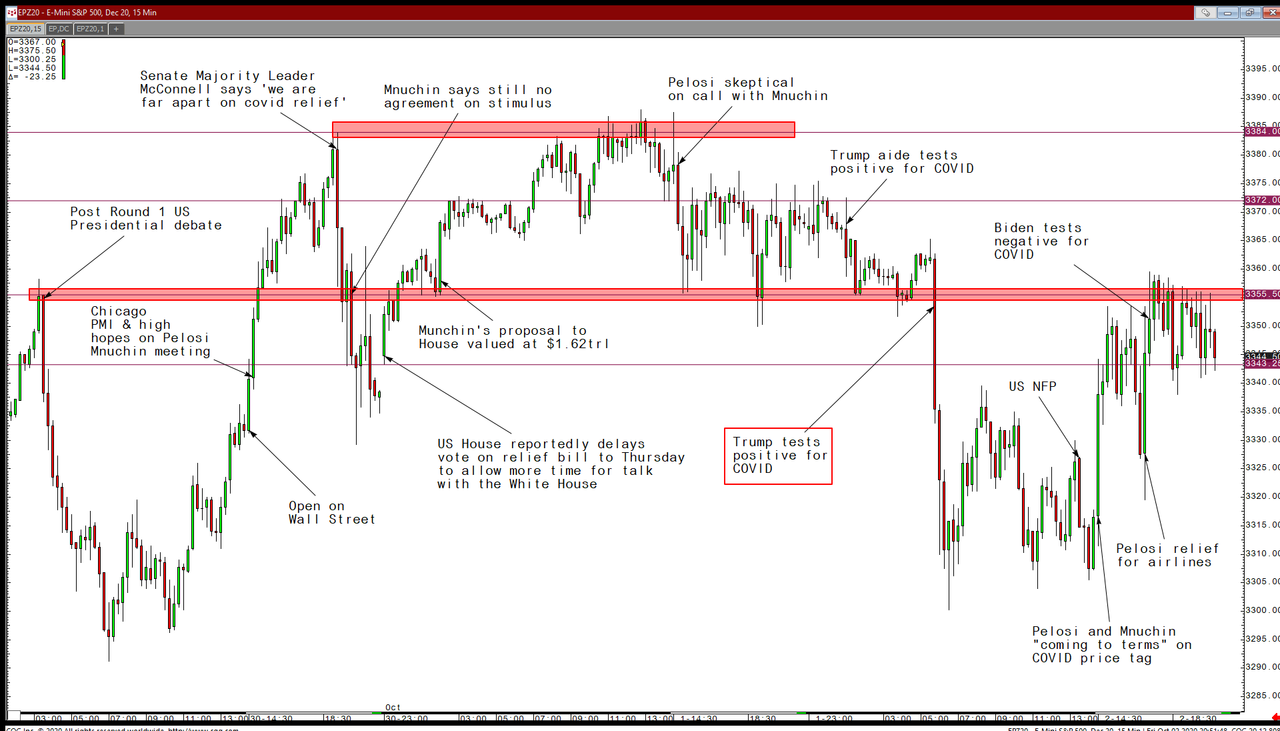

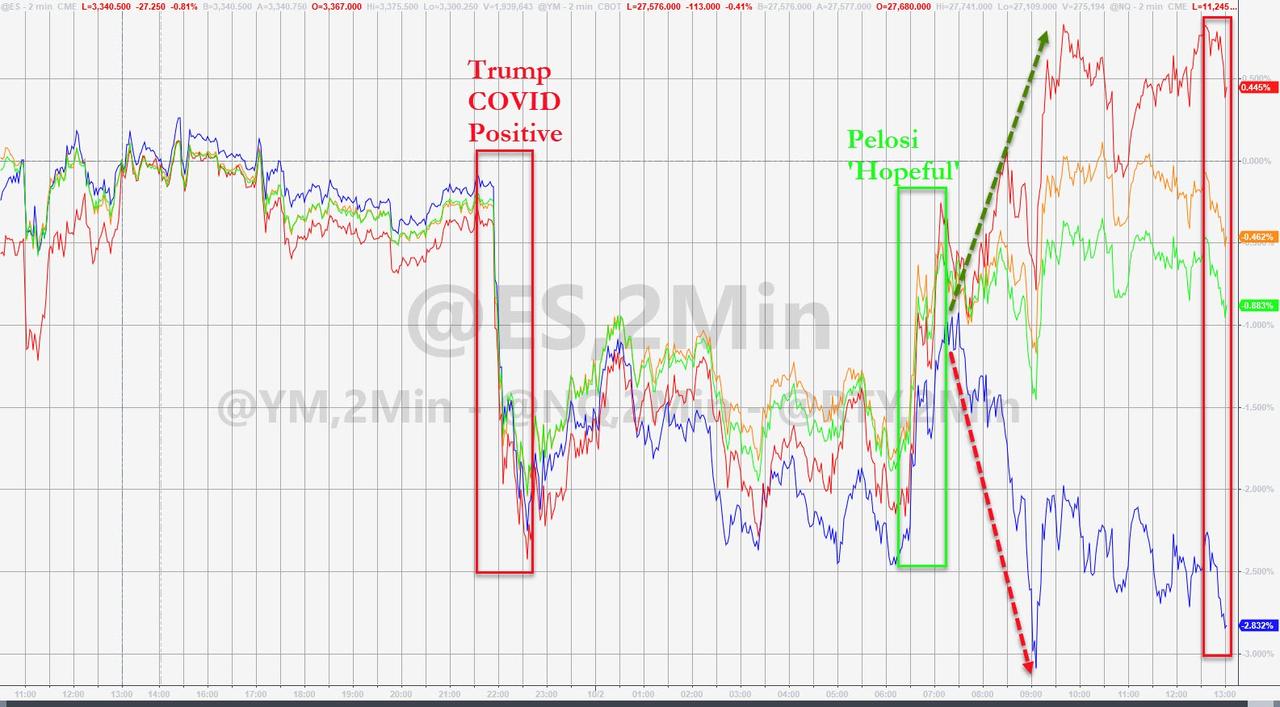

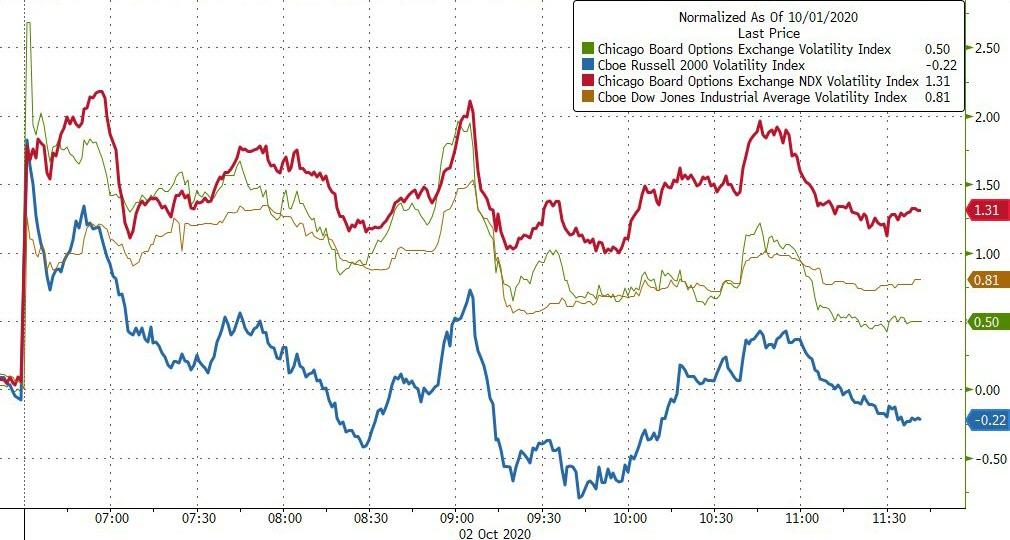

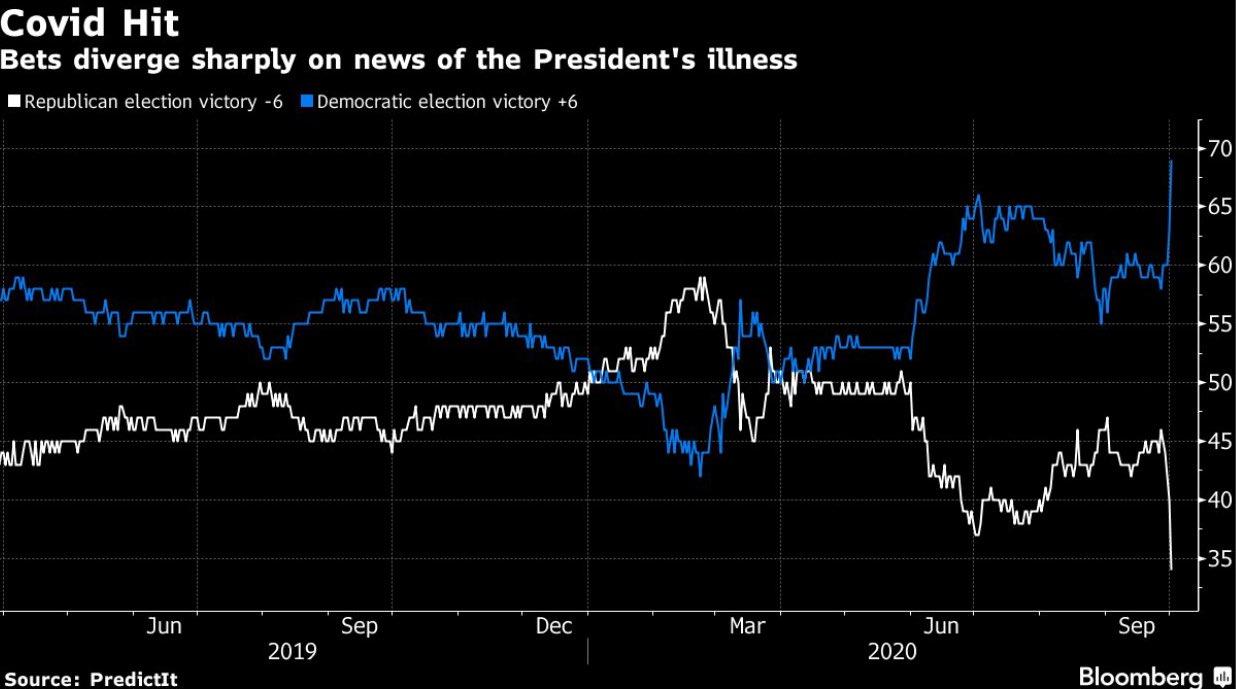

“October Shock”: Markets Tumble After Trump Tests Positive For Covid

After going to bed expecting today’s jobs report to be the highlight of the day, shocked traders woke up this morning to the real October shock: the news tweeted by Donald Trump himself at 12:54am ET, that he and the first lady had tested positive for covid after Hope Hicks, a senior advisor who recently traveled with the president, tested positive.

The result was an immediate flush in US equity futures and global markets which saw the Emini tumble to exactly 3,300 before rebounding modestly into the European open.

AS they sold risk assets, investors rush to safe assets such as gold, U.S. Treasuries and the Japanese yen. European shares also opened sharply lower, although they recovered some losses in early London trading after the initial overnight move. The STOXX 600 was down 0.6% as of 730am ET. The MSCI world equity index was down 0.2%.

“We’re just a month to the election so this news does throw the election campaign into a disarray for the Republican Party,” said Jingyi Pan, market strategist at IG Asia. “Even though Joe Biden is seen as the friendlier choice for Asia and a Trump absence could in some way or another keep that status quo of a Biden lead, generally, a contested election would generate uncertainties across the world and would not bode well for Asia equities as well.”

After Trump said he had coronavirus, online gambling site Betfair suspended betting on the outcome of the U.S. election. Betfair’s odds had previously shown Democratic challenger Joe Biden’s probability of winning at 60% on Wednesday after the first U.S. presidential debate.

Even before news of Trump’s infection, markets had been more bearish after Washington failed to reach an agreement on a fiscal stimulus package to help the U.S. economy recover from the impact of coronavirus. Late on Thursday, the House passed the Democratic stimulus plan which Republicans oppose, after Speaker Pelosi announce no bipartisan deal was achieved last night

The question now is what happens next as Trump’s exposure could cause a new wave of market volatility with investors braced for the presidential election in November. How long the risk-averse moves will last depends on the extent of the infection within the White House, said Francois Savary, chief investment officer at Swiss wealth manager Prime Partners.

“We may have to wait until the end of the weekend for more clarity on the situation,” he said. “The reaction has been a bit excessive with U.S. stock futures. It doesn’t mean the U.S. administration is not able to function. It will weigh on the market today and early next week but will not induce a long-lasting correction if the infection is contained to Trump,” he added.

Following the news, the U.S. dollar index rose and the safe-haven yen made its biggest jump in more than a month, reaching 104.95. Versus a basked of currencies, the dollar was up 0.1% on the day at 93.820. The Australian dollar, which serves as a liquid proxy for risk, was down 0.5%. The euro was down 0.3% against the dollar, at $1.1721.

In rates, Treasuries remained higher led by long end after fading from session lows. Yields are still inside Wednesday’s ranges ahead of September jobs report at 8:30am ET. Yields were lower by less than 2bp at long end of the curve, with 2s10s, 5s30s spreads flatter less than 1bp; 10-year is down 1.6bp at 0.661%, outperforming little-changed bunds and gilts, after shedding as much as 2.6bp. Yields rebounded from session lows as stock futures pared declines; S&P E-minis have trimmed a 2% drop on Trump health news to about 1.4%. Germany’s benchmark 10-year bond was down around 2 basis points at -0.545%.

In commodities, oil fell, with Brent down 3.3% at $39.57 a barrel to the lowest level since June, having fallen overnight and stabilized somewhat as European markets opened. Gold rose, up 0.1% at $1,906.26 per ounce. “Depending on how this situation evolves over the weekend, notably if more members of the U.S. government’s senior leadership are diagnosed positive, gold could be set for an extended rally,” said Jeffrey Halley, a senior market analyst at OANDA.

Elsewhere, in geopolitics, EU leaders reached an agreement regarding Belarus and Turkey in which they will impose sanctions on Belarus for violence and its election, although President Lukashenko was not included in the sanctions, while it warned that Turkey could face sanctions if it continues with its gas exploration in Cypriot waters. European Council President Michel said the next 2 weeks will be crucial with Turkey and the summit deal opened a path for dialogue but also showed firmness, while they will return to the Turkey question at the December summit. Furthermore, German Chancellor Merkel said EU leaders agreed they want constructive relations with Turkey and hope for negotiating dynamic with the country

Looking ahead, the last round of monthly U.S. unemployment data before the elections is due at 0830 (see preview here), although analysts say this has been relegated to secondary importance. We also get Factory Orders, Uni. of Michigan (F), Fed’s Harker, European Council Special Meeting. Trump’s illness prompted the White House to cancel political events on Friday, including a rally planned outside Orlando, Florida. Campaign and fundraising trips planned for the coming days — including visits to key battlegrounds including Wisconsin, Pennsylvania and Nevada — are expected to be scrapped.

Market Snapshot

- S&P 500 futures down 1.2% to 3,327.75

- STOXX Europe 600 down 0.4% to 360.49

- MXAP down 0.3% to 169.91

- MXAPJ down 0.2% to 558.19

- Nikkei down 0.7% to 23,029.90

- Topix down 1% to 1,609.22

- Hang Seng Index up 0.8% to 23,459.05

- Shanghai Composite down 0.2% to 3,218.05

- Sensex up 1.7% to 38,697.05

- Australia S&P/ASX 200 down 1.4% to 5,791.50

- Kospi up 0.9% to 2,327.89

- Brent Futures down 3% to $39.71/bbl

- Gold spot up 0.2% to $1,909.27

- U.S. Dollar Index up 0.06% to 93.77

- German 10Y yield fell 0.5 bps to -0.541%

- Euro down 0.2% to $1.1721

- Brent Futures down 3% to $39.71/bbl

- Italian 10Y yield fell 4.4 bps to 0.618%

- Spanish 10Y yield fell 0.2 bps to 0.23%

Top Overnight News

- Trump’s illness prompted the White House to cancel political events on Friday, including a rally planned outside Orlando, Florida. Campaign and fundraising trips planned for the coming days — including visits to key battlegrounds including Wisconsin, Pennsylvania and Nevada — are expected to be scrapped.

- Four months of European Commission consultations with insurance companies, academics and others ends Friday, aimed at agreeing by next year what really counts as “green” in projects funded by such debt

A quick look across global markets courtesy of NewsSquawk

Asian equity markets traded lower and the E-mini S&P is showing substantial losses after US President Trump tested positive for COVID-19. ASX 200 (-1.4%) reversed yesterday’s strength in which energy and mining-related sectors led the downside following weakness across the commodities complex and as a lacklustre financials sector also contributed to the losses for the index. Nikkei 225 (-0.7 %) was initially buoyed at the open as it played catch-up on return from yesterday’s surprise trading halt in Tokyo due to hardware issues, which Japan’s FSA is reportedly to consider a punishment for. This subsequently weighed on Japan Exchange Group shares and Fujitsu was also pressured given that the Co. is the hardware provider for the market operator, while most the gains in the benchmark index were gradually pared alongside a broad tentative tone and with a lack of participants due to closures in China, Hong Kong, Taiwan, South Korea and India. Finally, 10yr JGBs were rangebound amid the mixed risk tone and with price action stuck near the 152.00 focal point, while a tepid Rinban announcement by the BoJ which were present in the market for JPY 570bln, also ensured the lackadaisical price action for government bonds.

Top Asian News

- Malaysia Airlines in Urgent Restructuring as Pandemic Worsens

- Australia’s Central Bank Is ‘Dysfunctional,’ Ex- Researcher Says

European cash indices briefly trimmed earlier losses (Euro stoxx 50 -0.9%) which were triggered by US President Trump announcing his positive COVID-19 test, in turn sparking risk aversion across markets. Since then, cash and futures have been attempting to lift off lows, with some Brexit optimism potentially providing support as the news of a videoconference between the European Commission President and the UK PM was received well by participants, alongside the Pound, whilst the two sides will continue with negotiations in the run up to the EU Summit mid-month. That being said, EU diplomats are still downbeat over a Brexit breakthrough whilst a UK minister highlighted that very significant issues need to be resolved. Nonetheless, the attempted recovery was fleeting, Europe trades mostly lower with the exception of Spanish and Austrian stocks, with the former supported by ACS (+18%) after Vinci (+2.6%) submitted a bid to acquire the Co’s industrial division. Sectors meanwhile opened lower across the board, but thereafter gained some composure; albeit, Energy remains the laggard whilst Telecoms tops the charts with follow-through from yesterday’s French 5G auction – which raised EUR 2.8bln, as Iliad (+4.0%), Orange (+2%) and Bouygues (+1.3%) prop up the sector. The sectoral breakdown paints a similar picture with Travel & Leisure still under pressure amid the implications of the COVID-19 resurgence on the sector. In terms of individual movers, Lagardere (-0.2%) trades with modest losses despite Vivendi (+0.6%) upping its shareholding of the Co. to 26.7% from 21.2%. Ryanair (-2.2%) meanwhile sees losses amid source reports that the Co. is mulling purchasing Boeing 737Max aircrafts for ~EUR 16bln, whilst traffic September traffic numbers fell -64% YY and the Co. was operating at around 53% of normal September schedule.

Top European News

- ECB Takes Major Step Toward Introducing a Digital Euro

- ACS in Talks to Sell Industrial Unit to Vinci for $6.1 Billion

- German Regulator Limits Staff Trading After Wirecard Scandal

- BlackRock Sees Board Governance at VW Going in Reverse

In FX, the Yen is in demand on safe-haven grounds after an initial Greenback rally on news of US President Trump catching the coronavirus saw the DXY knee-jerk just over 94.000, with Usd/Jpy subsequently retreating from around 105.66 to test bids/support below 105.00 and the index hovering just above a 93.709 low. Conversely, the Aussie has borne the brunt of risk aversion, as Aud/Usd reverses from the high 0.7100 region through 0.7150, with little consolation from retail sales not dropping quite as much as expected in August. Ahead, NFP would ordinarily command headline status on the first Friday of a new month, but the data now looks somewhat inconsequential in light of the aforementioned events in Washington.

- GBP – More wild swings for Sterling, partly in line with broad sentiment, but again due to Brexit developments in the main and independently of other external or domestic factors. Cable is firmly back over 1.2900 and Eur/Gbp circa 0.9060 compared to 0.9100+ at one stage following reports that UK PM Johnson and European Commission President von der Leyen will hold a video call on Saturday to assess the situation on trade talks after this week’s formal round of discussions, and the former will push for the 2 sides to enter the tunnel stage of negotiations even though EU chief of Brexit matters, Barnier, is unsure the time is right.

- CAD/NZD/EUR/CHF – All still softer against their US counterpart, with the Loonie pivoting 1.3300, Kiwi midway between 0.6654-16 parameters, Euro holding above 1.1700 within a 1.1697-1.1750 range and Franc straddling 0.9200. Aside from keeping a White House vigil in the run up to monthly US jobs data, Eur/Usd looks well flanked by decent option expiries given 1.3 bn at 1.1700, 2 bn at 1.1750 and 1.7 bn at 1.1800, if recent peaks in the headline pair are breached. For the record, very little reaction to softer than forecast prelim Eurozone inflation as the individual national reports indicated a downside skew to consensus.

- SCANDI/EM – The Norwegian Crown may be deriving some traction from a lower than anticipated September jobless rate to compensate for weak oil prices and the impending strike action, but Eur/Nok is not down as much in percentage terms as Eur/Sek, albeit back under the psychological 11.0000 level in similar vein to the latter that has crossed 10.50000 to the downside. Elsewhere, EM currencies are broadly softer vs the Usd, but especially the Rub amidst ongoing diplomatic and geopolitical tensions, on top of Brent losing grip of the Usd 40/brl handle

In commodities, WTI and Brent futures remain pressured, albeit volatility has somewhat cooled down in recent trade, with the initial downside sparked by the risk aversion experienced following President Trump’s positive test. Newsflow which sent WTI Nov and Brent Dec to lows of USD 37.22/bbl (vs. high 38.65/bbl) and USD 39.40/bbl respectively (vs. high 40.77/bbl). Again, crude-specific news flow has been light and we are awaiting the NFP data for some impetus; alongside any further developments around Trump’s COVID-19 diagnosis. Looking ahead, next week seems fairly quiet in terms of crude-specific events, although the OPEC World Oil Outlook on the 8th could garner some attention with regards to its medium-term forecasts, but there is a possibly the release will get sideline if the report is consistent with the July release – as was the case last year. Spot gold meanwhile was bid early-doors on safe-haven inflow, which took the yellow metal to a high of USD 1917/oz, whilst spot silver briefly topped USD 24/oz before both precious metals waned off highs. In terms of base metals, LME copper fell to the lowest in seven weeks due to USD upside and sentiment effect from US President Trump. Meanwhile, aluminium prices fell amid talks of US aluminium exemptions for producers in UAE and Bahrain.

US Event Calendar

- 8:30am: Change in Nonfarm Payrolls, est. 875,000, prior 1.37m; Change in Private Payrolls, est. 875,000, prior 1.03m

- Unemployment Rate, est. 8.2%, prior 8.4%

- Average Hourly Earnings MoM, est. 0.2%, prior 0.4%; Average Hourly Earnings YoY, est. 4.8%, prior 4.7%

- Average Weekly Hours All Employees, est. 34.6, prior 34.6

- Labor Force Participation Rate, est. 61.9%, prior 61.7%; Underemployment Rate, prior 14.2%

- 10am: U. of Mich. Sentiment, est. 79, prior 78.9; Current Conditions, prior 87.5; Expectations, prior 73.3

- 10am: Factory Orders, est. 0.9%, prior 6.4%; Factory Orders Ex Trans, est. 1.1%, prior 2.1%

- 10am: Durable Goods Orders, est. 0.4%, prior 0.4%; Durables Ex Transportation, est. 0.4%, prior 0.4%

- 10am: Cap Goods Orders Nondef Ex Air, est. 1.7%, prior 1.8%; Cap Goods Ship Nondef Ex Air, prior 1.5%

DB’s Jim Reid concludes the overnight wrap

I’m not sure if it’s just me but I seem to have fought off more “Daddy longlegs” in the last few weeks than I can remember in my entire life. It could be local to me but they are everywhere. The twins are very amusing as they have only just discovered Daddy longlegs and think they are the funniest thing in the world. They also ask where Mummy shortlegs are? They then laugh at their own jokes. I’ve taught them well.

The US political spider’s web continued to dominate the narrative yesterday. Notwithstanding this, markets got off to a steady but solid start to Q4. By the close, the S&P 500 was up +0.53% and at a two-week high, though the index fell back somewhat from its opening gains following a report that Speaker Pelosi had told her deputies that she was sceptical a stimulus agreement would be reached. Markets seem to be caught between the crossfire of volatile stimulus news and a steady increase in the probability of a Biden victory in recent days according to respected modellers. Indeed FiveThirtyEight’s model ticked up to an 80% probability of a Biden win for the first time yesterday. Although Trump has traditionally been seen as good for stocks, the uncertainty of a close election, and a possible contested one at that, has been a dampener of late. If markets got more and more convinced of a Democrat clean sweep then this a) reduces uncertainty and b) potentially paves the way for a bigger fiscal stimulus after January. So Biden positive news can outweigh short-term negative news on stimulus.

Indeed, US fiscal stimulus discussions again dominated headlines yesterday. Pelosi said that the two parties are still a ways apart on the total size of stimulus and the means in which it is apportioned. It is likely that the latter is the larger sticking point as the White House has offered $1.6 trillion, well above $1 trillion figures many Senate Republicans were already uncomfortable with. The Democrats’ most recent offer of $2.2 trillion – down from their original $3.5 trillion bill – passed late last night although Senate Republicans are expected to reject it. Pelosi said that she would continue talks with Mnuchin while the passed bill will act as public account for what here caucus was pushing for. The S&P 500 dropped half a per cent yesterday when the intention to vote was announced as it signaled the talks had likely not closed the gap. Lawmakers in both chambers are expected to recess ahead of the elections next week but can be called back to take part in a vote if anything were to get done.

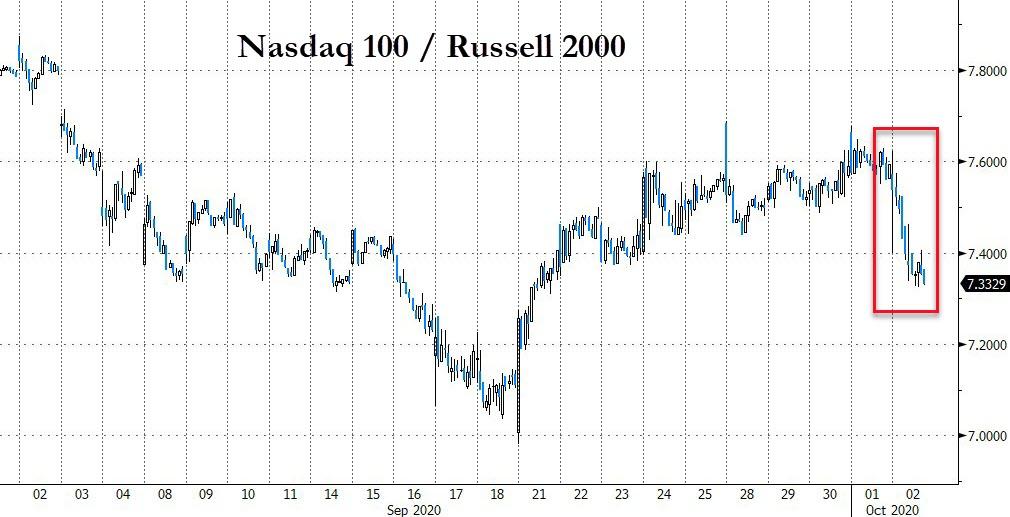

In advance of that, equity markets generally moved higher on both sides of the Atlantic yesterday amidst the stimulus discussions and increased probabilities of a more definitive election outcome, particularly large cap tech stocks once again as the NASDAQ gained +1.42%, while the S&P 500 was ‘only’ up +0.53% with the STOXX 600 up +0.20%. The biggest drivers of the S&P and the NASDAQ were those mega-cap tech stocks such as Netflix (+5.50%) and Amazon (+2.30%). On the gap between US and European equity markets, our CoTD yesterday showed that although the gap has been widening over the last decade, if you strip out just 10 mega-cap growth stocks from the S&P 500 then the Stoxx 600 has only been slightly behind the “S&P 490” since the end of 2014. See the evidence here.

Back to markets, andthe energy sector lagged behind yesterday as a result of the major declines in oil prices. Both Brent crude (-3.24%) and WTI (-3.73%) suffered significant losses thanks to concerns about oversupply. Copper, another industrial commodity, had its worst performance (-5.51%) since March as poor global demand weighed on the metal. Precious metals on the other hand rose with gold rising +1.07% and silver gaining +2.40%. Sovereign bonds rallied for the most part as well, with yields on 10yr treasuries (-0.6bps) and bunds (-1.4bps) both falling. Italian debt was the real outperformer though, with 10yr yields down -4.5bps and at a 1-year low, while the country’s 30-year yield fell a further -3.2bps to an all-time low. The dollar fell (-0.19%) for the fifth time in the last six sessions, though Wednesday’s was nearly unchanged.

In terms of the coronavirus, there was further negative news from Western Europe, as Italy reported another 2,548 cases, which was the country’s highest daily total since April 24 albeit with higher testing now. This has prompted Prime Minister Conte to seek an extension of his emergency powers until the end of January. Meanwhile in the UK, another 6,914 cases were reported, which sent the 7-day average up to 6,260. However we should note that the 7-day rolling average as seen in the table below is “only” slightly higher than it was a week ago. A similar story for most of the second wave candidates. Regardless officials noted that London may be at a “tipping point” while further restrictions were announced for parts of northern England, including Liverpool, where it will be illegal to meet with other households indoors. More restrictions may be coming to France as well where the Health Minister said they “may have no choice” but to close bars and restaurants again in Paris, saying the city is on “maximum alert”. And over in the US, New York reported the most new virus cases since May. New York City’s positivity rate on first time tests continued to climb, but remained below the 3% threshold that would close schools. Elsewhere in the US, two Wisconsin mayors have asked President Trump to cancel large rallies in the state which currently has one of the highest daily cases per capita in the US.

Today, attention will turn to the US jobs report, which also has added political significance as the last jobs report before Election Day on November 3rd. In terms of what to expect, our US economists think that nonfarm payrolls will grow by another +800k in September (consensus +875k), which should be enough to lower the unemployment rate to 8.2% from 8.4%. Remember however, that even if this were realised, nonfarm payrolls would still be over 10m beneath their peak back in February, so there’s still a long way to go before we get back to pre-Covid levels of employment.

Ahead of that later, the weekly initial jobless claims data for the week through September 26th showed a reduction to 837k, the lowest since the pandemic began. The continuing claims number for the week through September 19th also fell to a post-pandemic low of 11.767m, and the insured unemployment rate fell to 8.1%. The other main data highlight came from the manufacturing PMIs, though these were fairly unexciting, and saw little movement compared to the flash readings. The Euro Area PMI came in at 53.7, exactly in line with the flash reading, the German number was revised down slightly to 56.4 (vs. flash 56.6), and the French number was revised up slightly to 51.2 (vs. flash 50.9). Over in the US, the ISM manufacturing index came in at 55.4 (vs. 56.5 expected), which was a modest pull back from its 56.0 reading in August.

Elsewhere, it was a volatile day for the pound sterling as a raft of Brexit news came through that saw sentiment switch dramatically as the day went on. In the morning, the European Commission President Ursula von der Leyen announced the beginning of infringement proceedings against the UK on account of the parts of the UK’s internal market bill that violate the Withdrawal Agreement. The EU had previously given the UK until the end of September to remove the relevant provisions from the bill, but with that deadline passing they announced they would be sending a “letter of formal notice” to the UK, which the UK has until the end of October to respond to. Sterling fell to an intraday low of -0.77% in response, though in reality, this is arguably somewhat second order to the ongoing trade negotiations, particularly with the bill having not yet become law and facing serious obstacles in the UK House of Lords. Notably the end-month deadline for the UK to respond is also after Prime Minister Johnson’s self-imposed deadline of October 15 to reach a free-trade deal, so by that point we could be in a very different world depending on how things progress.