GOLD:$1914.80 UP $12.00 The quote is London spot price

Silver:$24.41 UP 53 CENTS London spot price ( cash market)

your data…

Closing access prices: London spot

i)Gold : $1913.40 LONDON SPOT 4:30 pm

ii)SILVER: $24.36//LONDON SPOT 4:30 pm

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED //Hang Sang CLOSED UP 308.73 OR 1.32% /The Nikkei closed UP 282.24 POINTS OR 1.23%//Australia’s all ordinaires CLOSED UP 2.54%

/Chinese yuan (ONSHORE) closed /Oil UP TO 38.65 dollars per barrel for WTI and 40.71 for Brent. Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN CLOSED AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7300 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total withdrawals; 1606.600 oz

We had 0 kilobar transactions +

ADJUSTMENTS: 1 //

The front month of OCT registered a total of 14,306 contracts for a LOSS of 3957 contracts. We had 4015 notices filed on Friday so we gained 58 contracts or 5800 additional oz will stand for delivery in this active delivery month of October. In gold we have not seen queue jumping start so early in the month. Thus you can bet the farm that throughout October, the total number of gold oz standing will increase from this level.

November gained 90 contracts to stand at 1072.

The big December contract GAINED 366 contracts UP to 445,652 contracts..

THE BIG STORY AGAIN TODAY IS THE HIGH OI STANDING FOR OCTOBER (95.527 tonnes). GENERALLY OCTOBER IS A POOR DELIVERY MONTH AS MOST INVESTORS PREFER TO SKIP THIS MONTH AND MOVE STRAIGHT TO DECEMBER. IT LOOKS LIKE SOME MAJOR ENTITY(GOLDMAN SACHS) JUST CANNOT WAIT FOR DECEMBER AS THEY ARE MAKING THEIR MOVE ON OCTOBER FOR PHYSICAL METAL. GOLDMAN SACHS ONE OF THE LEADERS OF THE NEW LONDON LME EXCHANGE NEEDS THE GOLD INVENTORY FOR LIQUIDITY AND INITIAL CONTRIBUTION WITH OTHER MAJOR PLAYERS. THE MAJOR DIFFERENCE BETWEEN THIS MONTH AND OTHER MONTHS IS THAT THIS GOLD STANDING IN OCTOBER WILL LEAVE THE COMEX AND HEAD FOR LONDON.

We had 2975 notices filed today for 297,500 oz OR 9.2534 TONNES.

To calculate the INITIAL total number of gold ounces standing for the OCT /2020. contract month, we take the total number of notices filed so far for the month (19,381) x 100 oz , to which we add the difference between the open interest for the front month of OCT (814,306 CONTRACTS ) minus the number of notices served upon today (2975 x 100 oz per contract) equals 3,071,200 OZ OR 95.527 TONNES) the number of ounces standing in this active month of Oct

thus the INITIAL standings for gold for the OCT/2020 contract month:

No of notices filed so far (19381, x 100 oz +14,306 OI) for the front month minus the number of notices served upon today (2975) x 100 oz which equals 3,071,200 oz standing OR 95.527 TONNES in this active delivery month. This is a HUGE amount for gold standing for a OCT delivery month (a poor active delivery month).

We gained 58 contracts or an additional 5800 oz will stand on this side of the pond searching for metal.

NEW PLEDGED GOLD: BRINKS

592,648.822 oz NOW PLEDGED SEPT 15.2020/HSBC 18.433 TONNES ( A HUGE INCREASE FROM 10.6)

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

277,934.09 oz (some deleted august 3) JPM 8.644 TONNES

610,238.285 oz pledged June 12/2020 Brinks/ july 2/july 21 19.017 tonnes

51,084.609 oz Pledged August 21/regular account 1.588 tonnes jpm

total pledged gold: 1,574,454.119 oz 48.97 tonnes

total registered, pledged and eligible (customer) gold 36,930,173.286 oz 1,148.68 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1022.034 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

END

And now for the wild silver comex results

And now for the wild silver comex results

INITIAL STANDINGS

OCT. SILVER COMEX CONTRACT MONTH//INITIAL STANDING

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

175,518.900 oz

Loomis

|

| Deposits to the Dealer Inventory |

635,881.200 oz

CNT

|

| Deposits to the Customer Inventory |

599,330.470oz

CNT

|

| No of oz served today (contracts) |

161

CONTRACT(S)

(805,000 OZ)

|

| No of oz to be served (notices) |

487 contracts

2,435,000 oz)

|

| Total monthly oz silver served (contracts) | 1368 contracts

6,840,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

|

4:18 PM (0 minutes ago)

|

|

||

|

||||

https://www.mintpressnews.com/uk-court-venezuela-gold-juan-guaido/271752/

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Markets Rally On Optimism Trump May Be Discharged As Soon

As Today

In addition to optimism over a covid vaccine, optimism about the economic recovery, and optimism about a fiscal stimulus, we can now add another category of “optimism” cited by traders to justify overnight futures ramps (at least for the next few days): optimism Trump will be discharged from Howard Reed hospital any day now, perhaps as soon as today, and then stage a full recovery. Sure enough, on Monday US index future bounced after doctors said Trump could be discharged from Howard Reed imminently, while sentiment was also lifted amid tentative signs of progress on a new fiscal stimulus.

Late on Sunday Trump released a series of videos in an effort to reassure the public that he is recovering (following by a frenzied tweetstorm on Monday morning), although his condition remains unclear and outside experts warn that his case may be severe. Trump also surprised supporters outside Walter Reed with an impromptu drive through, even as it earned him a fresh round of anger by liberal commentators.

Feeding the improved market tone were comments from House Speaker Nancy Pelosi, who said on Sunday that progress was being made in talks with Treasury Secretary Steven Mnuchin on a new bipartisan package of coronavirus relief measures, although she has said exactly the same thing for weeks now, yet neither party is willing to budge and make the much needed final compromise. Doubts about the scale of further fiscal aid and a slowing economic recovery have weighed on the S&P 500 recently, with the benchmark index in September logging its worst month since the coronavirus-driven crash earlier this year.

At 730am, Dow e-minis were up 206 points, S&P 500 e-minis were up 23.75 points, or 0.72%, and Nasdaq 100 e-minis were up 100.75 points, or just under 1%. This follows a furious short covering spree in NQs last week, as discussed previously.

In premarket trading, Regeneron rallied after Trump was given an experimental antibody treatment made by the drugmaker. Tech gigacaps Apple, Nvidia, Netflix, Amazon.com, Microsoft and Tesla all rose after weighing heavily on the Nasdaq on Friday.

Overhanging the relief rally, however, were concerns that Trump’s case could be more severe than public disclosures suggest, and that more restrictive measures by governments to slow coronavirus infections could harm the economic recovery. Some traders were concerned by doctors’ admission that Trump had been given supplementary oxygen and steroids.

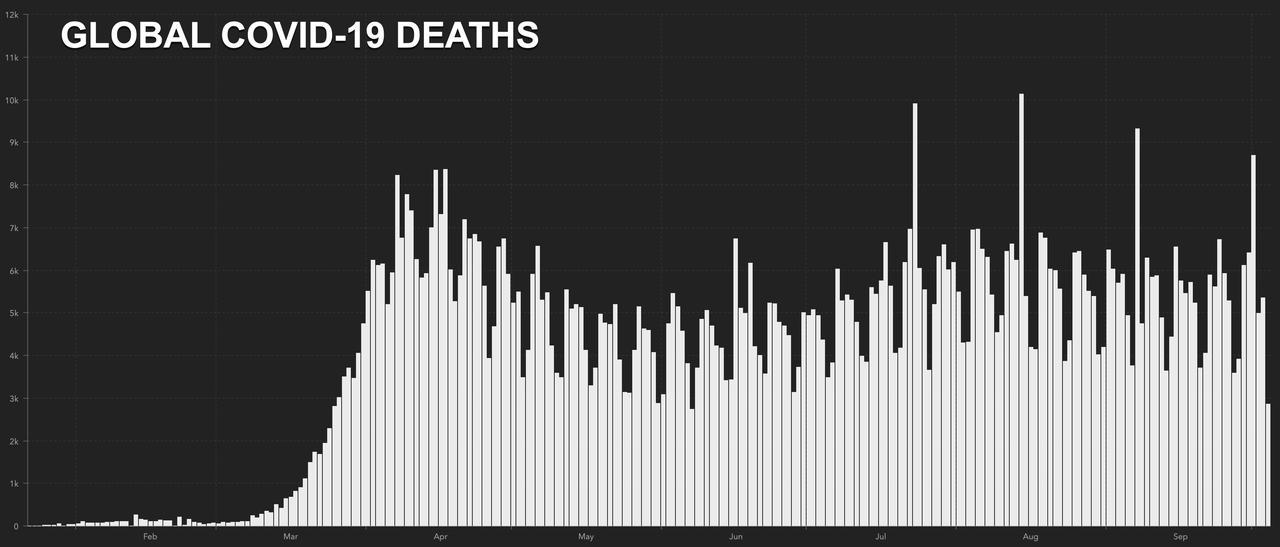

“Many questions remain including the use of the steroid drug … which is usually reserved for those with severe illness,” said Raymond James strategist Chris Bailey in London. “Global cases now top 35 million and various new restrictions in Paris, New York, etc”.

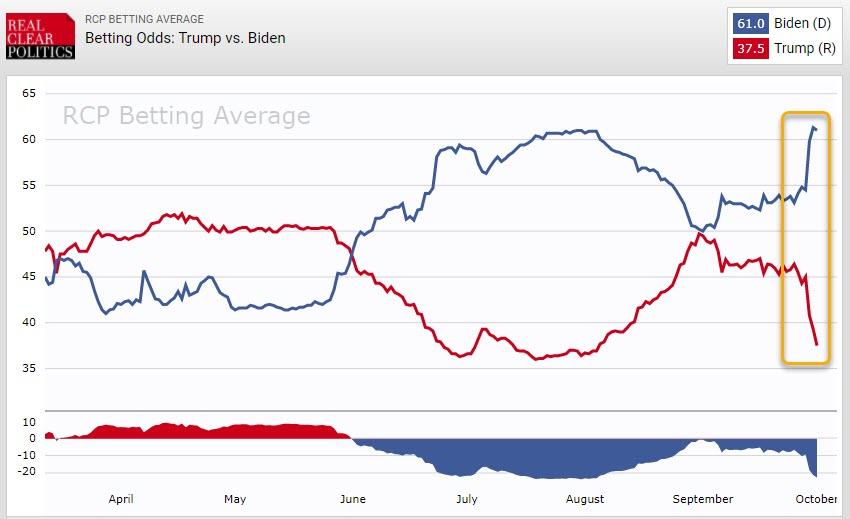

Trump’s infection also comes less than one month before the presidential election on Nov. 3, potentially fuelling more market volatility and making the outcome of the vote even more difficult to predict. “In terms of the impact on the election, we haven’t seen enough polling to assess whether this increases or decreases his chances of winning,” said Deutsche Bank strategists. According to a Reuters/Ipsos poll released on Sunday, Democrat contender Joe Biden opened his widest lead in a month in the U.S. presidential race. However, the same poll inexplicably polled far more Democrats than Republicans, and we all know what happened in 2016 when “polls” did the same.

The MSCI world equity index was up 0.4%, supported by overnight gains across Asia and a positive start in Europe. The pan-European STOXX 600 rose 0.7%. In Europe, consumer companies and banks led a broad advance. A survey on Monday showed the euro zone’s economic recovery faltered last month as new restrictions sent its dominant service sector into reverse. IHS Markit’s final composite Purchasing Managers’ Index fell to 50.4, just above the 50 mark separating growth from contraction, and down from 51.9 last month.

Equities in Asia notched gains, led by materials and finance, after falling in the last session. Japan’s Topix – which actually managed to stay open without crashing for the entire day – gained 1.7%, with Shimachu and Danto rising the most.

In rates, yields on benchmark 10-year Treasuries rose to 0.7138%, with yields higher by 2bp-3bp at long end, steepening 5s30s toward YTD highs above 123bp; 10-year yields around 0.712%, higher by more than 1bp vs Friday’s close. The long end of Treasury curve was cheaper as U.S. trading got under way. Aussie and Japanese bonds fell in Asia session, adding to long-end pressure. Treasury supply this week includes 10- and 30-year auctions Wednesday and Thursday. Euro zone bond yields edged lower on concerns about possible new restrictions to fight the coronavirus. The French government announced new restrictions, closing bars for two weeks. Other countries across Europe are also weighing up more measures.

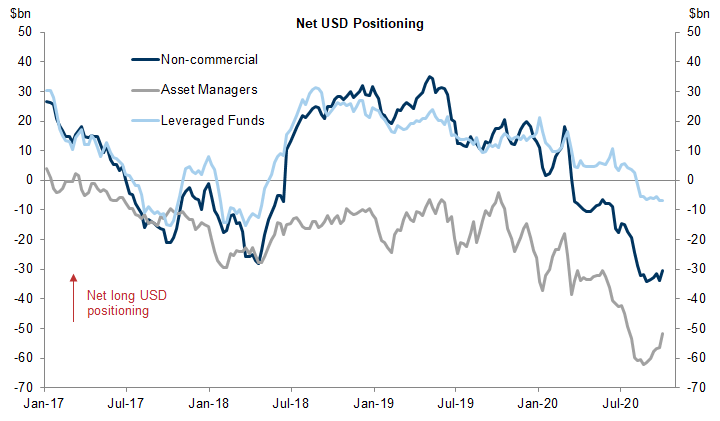

In FX, the dollar slumped, reversing some of Friday’s gains, as investors awaited positive news about U.S. Trump’s health and developments in fiscal aid talks in Washington; one possible upward catalyst for the dollar is that near record dollar shorts have started to reversed.

The yen retreated and Treasuries were steady. The euro advanced, while options capturing the immediate aftermath of the U.S. presidential election remain in demand amid uncertainty over Donald Trump’s condition. The Swiss franc gained amid speculative buying on the back of NEC Corp.’s purchase of Swiss banking software outfit Avaloq Group AG for $2.23 billion. The pound was steady; leveraged funds cut net longs on the pound to the lowest since August, according to data from the Commodity Futures Trading Commission for the week through Sept. 29. The funds increased net longs in the euro to the highest since August.

In commodities, speculation Trump could leave hospital sent oil prices up more than 2%, rebounding from a 3 week low. An escalating workers’ strike in Norway that has shut four of Equinor’s oil and gas fields also helped drive the gains. Brent prices were up 2% at $40.1 a barrel and U.S. West Texas Intermediate added 2.2% to $37.9 a barrel. Gold rebounded back over $1,900, driven by the weakness in the dollar.

Looking at the day ahead, we will get the final U.S. services and composite PMIs read for September at 9:45 a.m. with ISM services for the month at 10:00 a.m. Chicago Fed President Charles Evans and Atlanta Fed President Raphael Bostic are today’s Fed speakers, while EU chief negotiator, Michel Barnier will discuss the neverending Brexit drama with Angela Merkel ahead of resumption of negotiations in London later this week. Joe Biden will be on the campaign trail in Miami.

Market Snapshot

- S&P 500 futures up 0.5% to 3,355.75

- STOXX Europe 600 up 0.6% to 364.88

- MXAP up 1.2% to 171.63

- MXAPJ up 1.1% to 563.49

- Nikkei up 1.2% to 23,312.14

- Topix up 1.7% to 1,637.25

- Hang Seng Index up 1.3% to 23,767.78

- Shanghai Composite down 0.2% to 3,218.05

- Sensex up 0.9% to 39,047.63

- Australia S&P/ASX 200 up 2.6% to 5,941.58

- Kospi up 1.3% to 2,358.00

- Brent futures up 2.3% to $40.17/bbl

- Gold spot little changed at $1,899.73

- U.S. Dollar Index down 0.1% to 93.71

- German 10Y yield rose 0.3 bps to -0.533%

- Euro up 0.2% to $1.1738

- Italian 10Y yield fell 3.7 bps to 0.581%

- Spanish 10Y yield rose 1.5 bps to 0.236%

Top Overnight News from Bloomberg

- President Donald Trump briefly left his hospital in a car to greet supporters gathered outside, after posting a video on Twitter saying he was about to make a surprise visit

- Volatility eased in U.S. equity futures as optimism over President Donald Trump’s medical prognosis and hopes for fresh economic stimulus put a brake on selling that whipped up Friday

- Economists and investors see mixed messages from the ECB’s top policy makers. Most important is a perceived disconnect between President Christine Lagarde’s press conferences after policy decisions, and blog posts by Chief Economist Philip Lane the following day

- The stage is set for a showdown on Brexit at a European Union summit next week. French President Emmanuel Macron’s reluctance to make concessions on fish is stirring concern among officials he could sink efforts to reach a wider trade accord as negotiators begin on Monday a two-week period of intense talks

- European Commission President Ursula von der Leyen said she is going into isolation after contact with a person who tested positive for coronavirus

A quick look at global markets courtesy of NewsSquawk

Asian equity markets and US equity futures began the week with a constructive tone as the regional bourses reopened from recent holiday closures and participants also digested the positive updates regarding President Trump’s condition, which was said to have continued to improve and he could be discharged from hospital as early as today. In addition, some also attributed the positive tone to the latest polls which showed a widening lead for former VP Biden following last week’s presidential debate. ASX 200 (+2.6%) outperformed with the broad gains led by a surge in energy and financials on the eve of the budget announcement, where Australia’s national debt ceiling is expected to be raised to above AUD 1.1tln and income tax cuts valued at billions are set to be backdated in an effort to provide immediate economic stimulus. Nikkei 225 (+1.2%) traded positively as exporters reaped the benefits of a weaker currency that was spurred by the risk tone and alongside some murmuring of Gotobi demand. Hang Seng (+1.3%) was also upbeat as participants returned following the holidays although mainland China is to remain shut for most this week and won’t reopen until Friday, while there were some weak spots including SMIC shares which have dropped over 6% after the US informed its suppliers they will be subject to additional export restrictions. Finally, 10yr JGBs were weaker amid the gains in riskier assets but with downside stemmed by support near the 152.00 level and with the BoJ present in the market for a total JPY 840bln of JGBs with 1-3yr and 5-10yr maturities.

Top Asian News

- How Evergrande’s Billionaire Founder Skirted Latest Crisis

- Top India Court Asks Government to Outline Interest Waiver Plans

- Credit Suisse Hires HSBC Veteran Oey for Asia Wealth Push

- Singapore to Pay Would-Be Parents for Babies as Virus Drags On

European equities (Eurostoxx 50 +0.6%) kicked the week off on the front-foot, before staging a mild pullback, as markets continue to assess updates on US President Trump’s health, the Presidential election and stimulus discussions. In terms of President Trump, it appears that he could be discharged from hospital as soon as today with reports suggesting an improvement in his condition, albeit some in the medical community have raised doubts over the upbeat narrative presented by the administration. Polling is yet to encapsulate the news of Trump’s COVID-19 diagnosis, however, polls detailing the fallout of last week’s debate have moved in favour of former VP Biden who now holds a 14-point lead in the NBC/WSJ poll (prev. 8 point lead); desks have subsequently continued to talk up the possibility of a Democratic “blue sweep”. On the stimulus front, House Speaker Pelosi said that they are making progress on coronavirus relief legislation, whilst Senate Majority Leader McConnell said “we are getting closer” on stimulus negotiations. However, other reports noted that Republicans still give low odds on another pandemic stimulus bill. In terms of performance of European indices, the IBEX (+1.0%) is the main outlier to the upside with gains in the domestic banking sector spurred by reports that the Sabadell (+3.6%) CEO contacted his counterparts from BBVA (+3.2%) and Kutxabank in recent weeks with regards to a merger, according to sources. From a sector standpoint, aside from the banking sector, travel & leisure names lead the way higher this morning despite ongoing concerns about the pick-up in COVID-19 cases (particularly in the UK), whilst strength can also be seen in some of the other pro-cyclical sectors such as oil & gas and auto names. Support has also been seen for UK homebuilders this morning after UK PM Johnson promised to create a “Generation Buy” scheme to help young people enter the property market. The PM has reportedly asked minister to mull a scheme for long-term fixed-rate mortgages with 5% deposits. For individual movers, Cineworld (-31%) are the clear underperformer this morning after confirming it will close all of its cinemas in the UK, Ireland and US this week because of the impact of coronavirus (UK and US closures are to be temporary). K&S (+17.6%) are the best performer in the Stoxx 600 reports noted the Co. is in advanced discussions to sell their Morton Salt unit to Kissner Group for ~USD 3bln. Weir Group (+17.0%) shares have seen notable support after announcing a USD 405mln divestment of its oil & gas unit to Caterpillar for USD 405mln.

Top European News

- Europe Tightens Curbs as Leaders Gird for Long Virus Fight

- Two- Speed Europe Sees Germany Thriving as Rest of Region Suffers

- EU Commission President Von der Leyen Says She’s Self-Isolating

- ECB Has a Messaging Problem as Lagarde-Lane Dynamic Muddies View

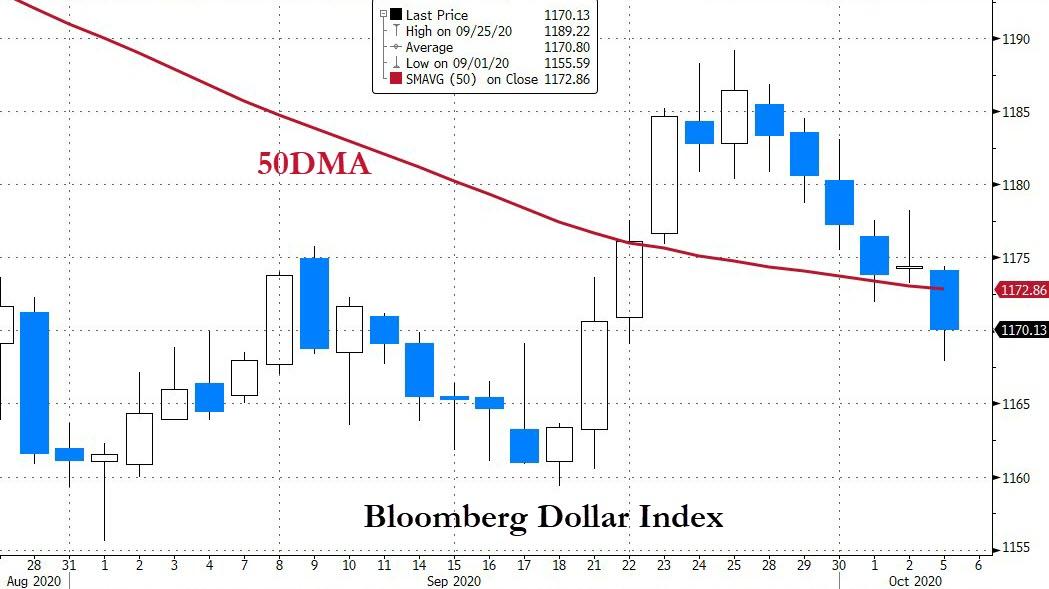

In FX, a softer start to the week for the broader Dollar and Index, with the latter currently contained within a tight 93.578-832 parameter following the fallout of US President Trump’s COVID-19 diagnosis which could see the President back at the White House as soon as today. Meanwhile, State-side stimulus talks remain with Senate Republican sources giving low odds for another bill, inferring that discussions could extend to after the 2020 Election. DXY tested its 21 DMA (93.646) to the downside, with the 50 DMA seen around 93.270, whilst upside levels see Friday’s high at 94.035 followed by last week’s peak at 94.298. Looking ahead, the docket sees Markit Services/Composite finals, ISM services PMI and potential comments from Fed 2021-voter Evans.

- CHF/JPY – The traditional safe-haven FX have seen an early divergence with participants attributing Swiss outperformance to some M&A flows amid reports Japan’s NEC was planning to acquire Swiss software maker Avaloq for USD 2.2bln, whilst some strength may still be garnered from speculation the US currency manipulation report may be postponed until after the US elections, with Switzerland now ticking all three boxes to be labelled as a currency manipulator. That being said, the US Treasury will then offer a period of negotiations, with more drastic measures imposed should discussions fail. USD/CHF briefly dipped below its 21 DMA (0.9163) but matched intraday lows set on Wednesday and Thursday last week (0.9160), with the pair’s 50 DMA residing around 0.9130. USD/JPY resides on the other side of the G10 spectrum with early losses coinciding with gains across APAC stock markets. USD/JPY tests Friday’s 105.66 high with eyes on the 50 DMA (105.74), with the pair failing to close above the MA for the past three consecutive sessions. USD/JPY Opex today includes USD 1.25bln rolling off at strike 105.00.

- EUR/GBP – Both on a firmer footing with the aid of a receding Buck, with the currencies on watch for Brexit developments in the aftermath of the videocall between PM Johnson and EC President, which noted that progress had been made but significant gaps remain, albeit the two sides have agreed to 11 days of “intensified” talks ahead of the UK de-facto deadline. Cable saw early sellers which prompted the pair to test 1.2900 to the downside, but thereafter nursed losses to print fresh session highs of 1.2964, with Sterling somewhat supported by surprise revisions higher to Services and Composite PMIs. EUR/USD meanwhile saw little action to revisions higher to final PMIs. EUR/USD retains a 1.1700+ status as it took out several potential resistance levels at 1.1750 (Fri high), 1.1755 (Wed high) ahead of 1.1763 (21 DMA), whilst the NY cut sees EUR 761mln at strike 1.1730 and around EUR 870mln at 1.1700.

- CAD, AUD, NZD – All firmer to varying degrees, with the Loonie outperforming the non-US Dollars as it coat-tails on the firmer crude prices, whilst the Aussie eyes the RBA and Aussie budget and the Kiwi eking mild gains but with gains capped on AUD/NZD dynamics. USD/CAD trickles lower below 1.3300 having had tested the level overnight, with a current base at 1.3264, with its 21 DMA at 1.3258 and 50 DMA at 1.3241. AUD/USD meanwhile inches closer towards the 0.7200 mark (vs. current low 0.7157), with its 21 and 50 DMAs residing at 0.7201 and 0.7207 respectively. Finally, NZD/USD remains contained in a narrow 0.6631-54 band as AUD/NZD reclaims 1.0800.

In commodities, WTI and Brent futures open the week on a firmer footing, with early strength coinciding with gains across stock markets overnight after Friday’s pessimism unwound amid weekend reports that US President Trump could be at the white house as early as today. Meanwhile, the conflict between Armenia and Azerbaijan over the disputed region of Nagorno-Karabakh reportedly escalated dramatically. It was also reported that the Nagorno-Karabakh region stated that 18 civilians were killed and over 90 were wounded in a week of fighting – with traders keeping eyes on any potential targeting of oil fields/refineries/ports of the OPEC+ member. Elsewhere, Libyan oil production ticked higher to 290k BPD from last week’s 270k BPD, according to sources. In terms of where we currently stand WTI Nov (USD 37/bbl) trades on either side of USD 38/bbl whilst Brent Dec reclaimed the USD 40/bbl handle (vs. low USD 39.14/bbl). Elsewhere, spot gold and silver are choppy, with earlier weakness in the yellow metal offset by a softer Dollar, with prices now back around the USD 1900/oz mark (vs. low 1887/oz), whilst spot silver attempted a breach of USD 24/oz to the upside – with the latest CFTC data suggesting hedge funds and money managers reduced positions in COMEX gold and increased them in silver contracts in the week to Sept 29th. Finally, LME copper prices are relatively flat having had drifted off highs in tandem with price action seen in stocks.

US Event Calendar

- 9:45am: Markit US Services PMI, est. 54.6, prior 54.6

- 9:45am: Markit US Composite PMI, prior 54.4

- 10am: ISM Services Index, est. 56.2, prior 56.9

DB’s Jim Reid concludes the overnight wrap

I can almost certainly guarantee that wherever you’re reading this from you had better weather than me this weekend. Or at least no worse. It rained from start to finish. Any weekend with the golf course closed is a bad one for me and watching Frozen 2 the twentieth time in two months to fill the time didn’t improve the mood. Then the coup de grace was seeing Liverpool concede 7 (seven – as they always used to type out and put in brackets for unusual scores) for the first time since 1963 last night! Quite astonishing.

The business world continues to be quite extraordinary at the moment too and Mr Trump again dominated the weekend headlines. I’m sure you’ve seen the conflicting and confusing reports concerning his health over the weekend so we won’t go into that here. The latest from yesterday was that his doctors suggested he could be released back to the White House as soon as today. He also appeared on a video last night looking in good spirits. According to the wires this has helped S&P 500 futures to trade up +0.61% this morning but to be honest it could also be because a poll showed that Biden was 14pp up over the weekend (more below). We actually published the EMR almost an hour earlier than usual on Friday and four minutes after it hit inboxes the headlines came through that the President had tested positive. So we will try not to be that efficient again and end up as virtual fish and chip paper as we were on Friday.

In terms of the impact on the election, we haven’t seen enough polling to assess whether this increases or decreases his chances of winning. There was an NBC-WSJ poll released over the weekend showing Biden ahead by 14 points – the biggest lead of the campaign. However this polling was carried out between the first debate last Tuesday and the positive Covid test early on Friday morning. For comparison the last poll from this combination saw at 8pp lead last month. An Ipsos and a YouGov poll have just been released before we go to print and they seem to show around a 10pp and 7pp lead for Biden respectively. These were conducted on Friday and Saturday.

This confirms what was suspected last week, namely that polls were edging further towards Biden even before Friday with the first evidence now coming through that this may have continued. Indeed the recent price action suggests that the market wants certainty more than anything else. Given the realistic options (assuming the polls are not completely out), perhaps the market would currently most like a Democratic clean sweep as this would increase the likelihood of near term certainty. This outcome was edging up in likelihood amongst respected political pundits ahead of Mr Trump’s positive test so Friday’s news brought back all sorts of uncertainties with tail risks increasing in all sorts of direction. The fact that Biden tested negative later in the day seemed to help markets which partly supports the theory above. So this week the market will await more news from the Trump camp and signs of movement in the polls. If Biden pulls away then markets will probably be pretty relaxed. So the batch of polls post Trump’s illness are going to be important.

As we’ll see below the VP debate takes place on Wednesday which is the next major planned event. We’ll also see what the latest on the stimulus package is. It feels like both sides are trying to show that they are doing the best they can to bridge the gap but the reality is that both sides seem to be quite far apart still and it will be an enormous feat to bridge the gap pre-election. Nonetheless, the FT reported yesterday that the US President Donald Trump has issued a call for negotiators to “work together” and complete a deal.

Overnight, Asian markets have started the week on front foot with the Nikkei (+1.20%), Hang Seng (+1.46%), Kospi (+1.18%) and Asx (+2.47%) all seeing strong advances and recovering from Friday’s morning’s shock. China’s markets are closed for holidays. In Fx, the US dollar is trading down -0.11%. In terms of overnight data, Japan September services PMI was confirmed at 46.9 (vs. 45.6 in flash).

Back to politics and onto Brexit. U.K. PM Johnson had the planned VC talk with EC President von der Leyen on Saturday and in a joint statement they instructed their chief negotiators to work intensively in order to try to bridge the obvious gaps that there are and emphasised “the importance of finding an agreement, if at all possible”. On Sunday Johnson reaffirmed that he’d like a deal but said the U.K. could prosper without one. The FT also had an article last night suggesting Barnier is going to hold talks with the impacted EU countries on fisheries which shows some progress and the possibility of negotiation movement. For me it seems like the probabilities of a deal have edged up over the last couple of weeks. In terms of news flow and headlines it’s seems to have been 7 steps forward and only 5 back. We will see. Sterling is broadly flat this morning at 1.2938 ahead of another week of talks.

Onto the virus and the UK reported an extremely high 35,850 new cases over the weekend but these were heavily impacted by around 16,000 previous unreported cases between September 25 to October 2 due to technical issues. Even after taking this into account the new weekend cases stood at 19,850, a higher run rate compared to previous weekends. Meanwhile, the delay in entering those 16,000 cases also means that their recent contacts were not immediately followed up. This will put more pressure on the government.

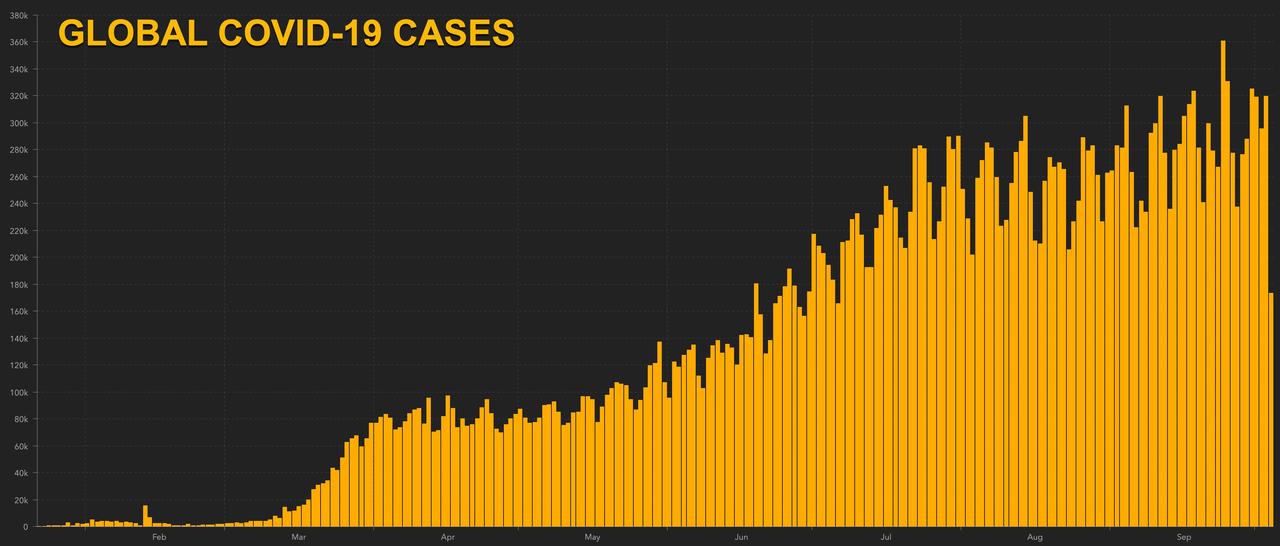

Bloomberg is also reporting that France may shut down bars in the Paris region and impose other new restrictions in the area. The country reported 29,537 new cases this weekend versus an average of c.25,000 cases over the previous two. In the US, New York City Mayor Bill de Blasio said he plans to close schools and non-essential businesses in nine neighbourhoods in Brooklyn and Queens where there’s been a surge in coronavirus infections. Indoor and outdoor dining will also be closed in these areas. For more details on how the virus is spreading in major regions of the world see the table below. There are a lot of footnotes so please see those in conjunction with the raw data. On the vaccine front, the FT reported the UK government’s head of the vaccine taskforce Kate Bingham as saying that less than half of the UK population could be vaccinated. She said, “There is going to be no vaccination of people under 18. It’s an adult-only vaccine for people over 50, focusing on health workers, care home workers and the vulnerable.”

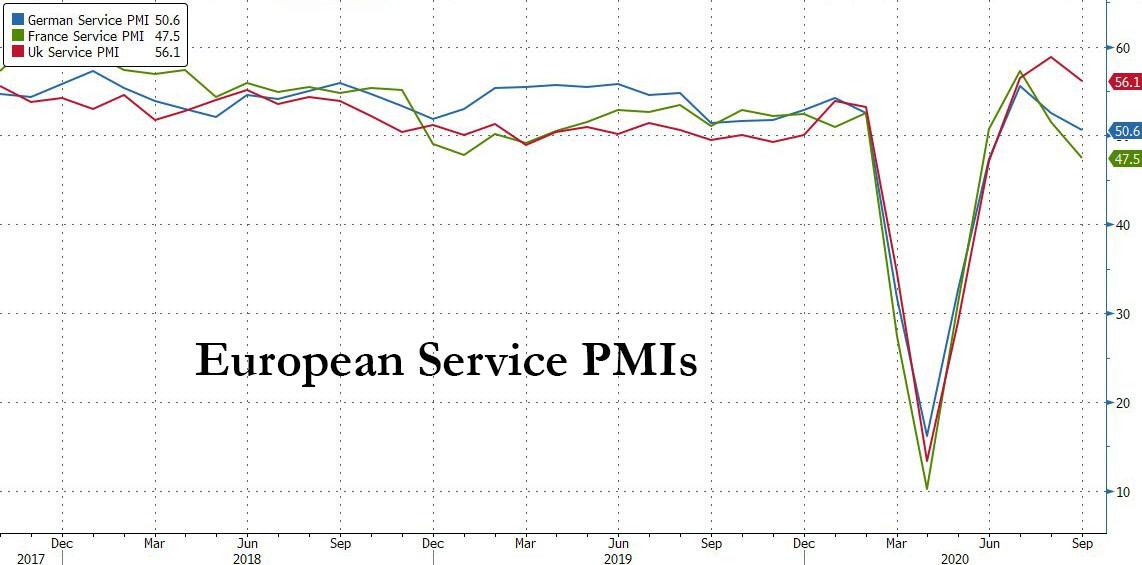

In terms of this week, outside of the VP debate on Wednesday we’ll get the latest minutes from recent Fed (Weds) and ECB (Thurs) meetings, and also hear from both Fed Chair Powell (tomorrow) and ECB President Lagarde (tomorrow and Weds). The only G20 decision next week is from the Reserve Bank of Australia tomorrow. Our Australia economists expects no change in policy, but we will be watching for clues about whether a rate cut might yet be delivered by the end of the year. The main data highlight will likely be the release of the services and composite PMIs from around the world. Most are today but the U.K. comes tomorrow and China’s on Thursday after holidays. The flash readings showed clear signs of the services sector in Europe being affected by the second wave of Covid-19, with the flash Euro Area services PMI falling to 47.6, which is below the 50-mark that separates expansion from contraction, with both Germany (49.1) and France (48.5) also in contractionary territory. We will see if this trend is confirmed and whether there was any late month deterioration from the initial flash reading. The day by day week ahead calendar is at the end.

Recapping last week now, as we moved into Q4, US equities saw their first positive week since August even with a weaker end of Friday. In a particularly hectic week that started with one of the most raucous US Presidential debates in memory and ended with the sitting US President testing positive for Covid-19 equity volatility jumped. The VIX volatility index rose +1.25pts to 27.63 even as equity prices rose – it was the second largest weekly rise in vol since June. Even with this uncertainty, the S&P 500 rose +1.52% (-0.96% Friday) on the week, breaking a streak of four losing weeks – the longest since August 2019. The NASDAQ rose +1.48% (-2.22% Friday) for the second weekly gain. European equities rose as well with the Stoxx 600 ending the week +2.02% (+0.25% Friday), the third weekly gain out of the last four. The IBEX (+1.90%), FTSE 100 (+1.02%), and CAC (+2.01%) all posted strong weekly equity performances even as their home countries reinstated some restrictions in the face of increasing Covid-19 caseloads.

The dollar dropped (-0.84%) as risk assets generally gained, for just its second weekly loss since the end of August. The drop in the dollar saw gold gain +2.06%, as the precious metal finished the week just under the $1900/oz level. Even though equities gained on the week, oil did not follow suit as worries on global demand saw WTI (-7.95%) and Brent crude (-6.32%) fall sharply and is now down four out of the last five weeks and is at its lowest weekly close since June. Core sovereign bonds were mixed on the week as US 10yr Treasury yields rose +4.6bps (+2.3bps Friday) to finish at 0.701% and 10yr Gilt yields rose +5.7bps (+1.2bps Friday) to 0.25%, while 10yr Bund yields were down -0.7bps (unchanged Friday) to -0.54%. Italian 10yr yields fell -10.2bps to 0.784% – their lowest levels since an all-time low last September.

On the data front, US Nonfarm payrolls rose by 661k (vs. 859k expected) on Friday while August’s numbers were revised up to 1.49 million from 1.37m. The unemployment rate fell 0.5 percentage points to 7.9% (vs. 8.2 expected), though the labour-force participation rate declined by 0.3 points to 61.4%. Meanwhile in Europe, the Euro-area CPI reading showed inflation slowed to -0.3% in August (vs. -0.2% expected) while the core rate set a six-year low at 0.2% (0.4% expected).

Markets Rally On Optimism Trump May Be Discharged As Soon As Today

In addition to optimism over a covid vaccine, optimism about the economic recovery, and optimism about a fiscal stimulus, we can now add another category of “optimism” cited by traders to justify overnight futures ramps (at least for the next few days): optimism Trump will be discharged from Howard Reed hospital any day now, perhaps as soon as today, and then stage a full recovery. Sure enough, on Monday US index future bounced after doctors said Trump could be discharged from Howard Reed imminently, while sentiment was also lifted amid tentative signs of progress on a new fiscal stimulus.

Late on Sunday Trump released a series of videos in an effort to reassure the public that he is recovering (following by a frenzied tweetstorm on Monday morning), although his condition remains unclear and outside experts warn that his case may be severe. Trump also surprised supporters outside Walter Reed with an impromptu drive through, even as it earned him a fresh round of anger by liberal commentators.

Feeding the improved market tone were comments from House Speaker Nancy Pelosi, who said on Sunday that progress was being made in talks with Treasury Secretary Steven Mnuchin on a new bipartisan package of coronavirus relief measures, although she has said exactly the same thing for weeks now, yet neither party is willing to budge and make the much needed final compromise. Doubts about the scale of further fiscal aid and a slowing economic recovery have weighed on the S&P 500 recently, with the benchmark index in September logging its worst month since the coronavirus-driven crash earlier this year.

At 730am, Dow e-minis were up 206 points, S&P 500 e-minis were up 23.75 points, or 0.72%, and Nasdaq 100 e-minis were up 100.75 points, or just under 1%. This follows a furious short covering spree in NQs last week, as discussed previously.

In premarket trading, Regeneron rallied after Trump was given an experimental antibody treatment made by the drugmaker. Tech gigacaps Apple, Nvidia, Netflix, Amazon.com, Microsoft and Tesla all rose after weighing heavily on the Nasdaq on Friday.

Overhanging the relief rally, however, were concerns that Trump’s case could be more severe than public disclosures suggest, and that more restrictive measures by governments to slow coronavirus infections could harm the economic recovery. Some traders were concerned by doctors’ admission that Trump had been given supplementary oxygen and steroids.

“Many questions remain including the use of the steroid drug … which is usually reserved for those with severe illness,” said Raymond James strategist Chris Bailey in London. “Global cases now top 35 million and various new restrictions in Paris, New York, etc”.

Trump’s infection also comes less than one month before the presidential election on Nov. 3, potentially fuelling more market volatility and making the outcome of the vote even more difficult to predict. “In terms of the impact on the election, we haven’t seen enough polling to assess whether this increases or decreases his chances of winning,” said Deutsche Bank strategists. According to a Reuters/Ipsos poll released on Sunday, Democrat contender Joe Biden opened his widest lead in a month in the U.S. presidential race. However, the same poll inexplicably polled far more Democrats than Republicans, and we all know what happened in 2016 when “polls” did the same.

The MSCI world equity index was up 0.4%, supported by overnight gains across Asia and a positive start in Europe. The pan-European STOXX 600 rose 0.7%. In Europe, consumer companies and banks led a broad advance. A survey on Monday showed the euro zone’s economic recovery faltered last month as new restrictions sent its dominant service sector into reverse. IHS Markit’s final composite Purchasing Managers’ Index fell to 50.4, just above the 50 mark separating growth from contraction, and down from 51.9 last month.

Equities in Asia notched gains, led by materials and finance, after falling in the last session. Japan’s Topix – which actually managed to stay open without crashing for the entire day – gained 1.7%, with Shimachu and Danto rising the most.

In rates, yields on benchmark 10-year Treasuries rose to 0.7138%, with yields higher by 2bp-3bp at long end, steepening 5s30s toward YTD highs above 123bp; 10-year yields around 0.712%, higher by more than 1bp vs Friday’s close. The long end of Treasury curve was cheaper as U.S. trading got under way. Aussie and Japanese bonds fell in Asia session, adding to long-end pressure. Treasury supply this week includes 10- and 30-year auctions Wednesday and Thursday. Euro zone bond yields edged lower on concerns about possible new restrictions to fight the coronavirus. The French government announced new restrictions, closing bars for two weeks. Other countries across Europe are also weighing up more measures.

In FX, the dollar slumped, reversing some of Friday’s gains, as investors awaited positive news about U.S. Trump’s health and developments in fiscal aid talks in Washington; one possible upward catalyst for the dollar is that near record dollar shorts have started to reversed.

The yen retreated and Treasuries were steady. The euro advanced, while options capturing the immediate aftermath of the U.S. presidential election remain in demand amid uncertainty over Donald Trump’s condition. The Swiss franc gained amid speculative buying on the back of NEC Corp.’s purchase of Swiss banking software outfit Avaloq Group AG for $2.23 billion. The pound was steady; leveraged funds cut net longs on the pound to the lowest since August, according to data from the Commodity Futures Trading Commission for the week through Sept. 29. The funds increased net longs in the euro to the highest since August.

In commodities, speculation Trump could leave hospital sent oil prices up more than 2%, rebounding from a 3 week low. An escalating workers’ strike in Norway that has shut four of Equinor’s oil and gas fields also helped drive the gains. Brent prices were up 2% at $40.1 a barrel and U.S. West Texas Intermediate added 2.2% to $37.9 a barrel. Gold rebounded back over $1,900, driven by the weakness in the dollar.

Looking at the day ahead, we will get the final U.S. services and composite PMIs read for September at 9:45 a.m. with ISM services for the month at 10:00 a.m. Chicago Fed President Charles Evans and Atlanta Fed President Raphael Bostic are today’s Fed speakers, while EU chief negotiator, Michel Barnier will discuss the neverending Brexit drama with Angela Merkel ahead of resumption of negotiations in London later this week. Joe Biden will be on the campaign trail in Miami.

Market Snapshot

- S&P 500 futures up 0.5% to 3,355.75

- STOXX Europe 600 up 0.6% to 364.88

- MXAP up 1.2% to 171.63

- MXAPJ up 1.1% to 563.49

- Nikkei up 1.2% to 23,312.14

- Topix up 1.7% to 1,637.25

- Hang Seng Index up 1.3% to 23,767.78

- Shanghai Composite down 0.2% to 3,218.05

- Sensex up 0.9% to 39,047.63

- Australia S&P/ASX 200 up 2.6% to 5,941.58

- Kospi up 1.3% to 2,358.00

- Brent futures up 2.3% to $40.17/bbl

- Gold spot little changed at $1,899.73

- U.S. Dollar Index down 0.1% to 93.71

- German 10Y yield rose 0.3 bps to -0.533%

- Euro up 0.2% to $1.1738

- Italian 10Y yield fell 3.7 bps to 0.581%

- Spanish 10Y yield rose 1.5 bps to 0.236%

Top Overnight News from Bloomberg

- President Donald Trump briefly left his hospital in a car to greet supporters gathered outside, after posting a video on Twitter saying he was about to make a surprise visit

- Volatility eased in U.S. equity futures as optimism over President Donald Trump’s medical prognosis and hopes for fresh economic stimulus put a brake on selling that whipped up Friday

- Economists and investors see mixed messages from the ECB’s top policy makers. Most important is a perceived disconnect between President Christine Lagarde’s press conferences after policy decisions, and blog posts by Chief Economist Philip Lane the following day

- The stage is set for a showdown on Brexit at a European Union summit next week. French President Emmanuel Macron’s reluctance to make concessions on fish is stirring concern among officials he could sink efforts to reach a wider trade accord as negotiators begin on Monday a two-week period of intense talks

- European Commission President Ursula von der Leyen said she is going into isolation after contact with a person who tested positive for coronavirus

A quick look at global markets courtesy of NewsSquawk

Asian equity markets and US equity futures began the week with a constructive tone as the regional bourses reopened from recent holiday closures and participants also digested the positive updates regarding President Trump’s condition, which was said to have continued to improve and he could be discharged from hospital as early as today. In addition, some also attributed the positive tone to the latest polls which showed a widening lead for former VP Biden following last week’s presidential debate. ASX 200 (+2.6%) outperformed with the broad gains led by a surge in energy and financials on the eve of the budget announcement, where Australia’s national debt ceiling is expected to be raised to above AUD 1.1tln and income tax cuts valued at billions are set to be backdated in an effort to provide immediate economic stimulus. Nikkei 225 (+1.2%) traded positively as exporters reaped the benefits of a weaker currency that was spurred by the risk tone and alongside some murmuring of Gotobi demand. Hang Seng (+1.3%) was also upbeat as participants returned following the holidays although mainland China is to remain shut for most this week and won’t reopen until Friday, while there were some weak spots including SMIC shares which have dropped over 6% after the US informed its suppliers they will be subject to additional export restrictions. Finally, 10yr JGBs were weaker amid the gains in riskier assets but with downside stemmed by support near the 152.00 level and with the BoJ present in the market for a total JPY 840bln of JGBs with 1-3yr and 5-10yr maturities.

Top Asian News

- How Evergrande’s Billionaire Founder Skirted Latest Crisis

- Top India Court Asks Government to Outline Interest Waiver Plans

- Credit Suisse Hires HSBC Veteran Oey for Asia Wealth Push

- Singapore to Pay Would-Be Parents for Babies as Virus Drags On

European equities (Eurostoxx 50 +0.6%) kicked the week off on the front-foot, before staging a mild pullback, as markets continue to assess updates on US President Trump’s health, the Presidential election and stimulus discussions. In terms of President Trump, it appears that he could be discharged from hospital as soon as today with reports suggesting an improvement in his condition, albeit some in the medical community have raised doubts over the upbeat narrative presented by the administration. Polling is yet to encapsulate the news of Trump’s COVID-19 diagnosis, however, polls detailing the fallout of last week’s debate have moved in favour of former VP Biden who now holds a 14-point lead in the NBC/WSJ poll (prev. 8 point lead); desks have subsequently continued to talk up the possibility of a Democratic “blue sweep”. On the stimulus front, House Speaker Pelosi said that they are making progress on coronavirus relief legislation, whilst Senate Majority Leader McConnell said “we are getting closer” on stimulus negotiations. However, other reports noted that Republicans still give low odds on another pandemic stimulus bill. In terms of performance of European indices, the IBEX (+1.0%) is the main outlier to the upside with gains in the domestic banking sector spurred by reports that the Sabadell (+3.6%) CEO contacted his counterparts from BBVA (+3.2%) and Kutxabank in recent weeks with regards to a merger, according to sources. From a sector standpoint, aside from the banking sector, travel & leisure names lead the way higher this morning despite ongoing concerns about the pick-up in COVID-19 cases (particularly in the UK), whilst strength can also be seen in some of the other pro-cyclical sectors such as oil & gas and auto names. Support has also been seen for UK homebuilders this morning after UK PM Johnson promised to create a “Generation Buy” scheme to help young people enter the property market. The PM has reportedly asked minister to mull a scheme for long-term fixed-rate mortgages with 5% deposits. For individual movers, Cineworld (-31%) are the clear underperformer this morning after confirming it will close all of its cinemas in the UK, Ireland and US this week because of the impact of coronavirus (UK and US closures are to be temporary). K&S (+17.6%) are the best performer in the Stoxx 600 reports noted the Co. is in advanced discussions to sell their Morton Salt unit to Kissner Group for ~USD 3bln. Weir Group (+17.0%) shares have seen notable support after announcing a USD 405mln divestment of its oil & gas unit to Caterpillar for USD 405mln.

Top European News

- Europe Tightens Curbs as Leaders Gird for Long Virus Fight

- Two- Speed Europe Sees Germany Thriving as Rest of Region Suffers

- EU Commission President Von der Leyen Says She’s Self-Isolating

- ECB Has a Messaging Problem as Lagarde-Lane Dynamic Muddies View

In FX, a softer start to the week for the broader Dollar and Index, with the latter currently contained within a tight 93.578-832 parameter following the fallout of US President Trump’s COVID-19 diagnosis which could see the President back at the White House as soon as today. Meanwhile, State-side stimulus talks remain with Senate Republican sources giving low odds for another bill, inferring that discussions could extend to after the 2020 Election. DXY tested its 21 DMA (93.646) to the downside, with the 50 DMA seen around 93.270, whilst upside levels see Friday’s high at 94.035 followed by last week’s peak at 94.298. Looking ahead, the docket sees Markit Services/Composite finals, ISM services PMI and potential comments from Fed 2021-voter Evans.

- CHF/JPY – The traditional safe-haven FX have seen an early divergence with participants attributing Swiss outperformance to some M&A flows amid reports Japan’s NEC was planning to acquire Swiss software maker Avaloq for USD 2.2bln, whilst some strength may still be garnered from speculation the US currency manipulation report may be postponed until after the US elections, with Switzerland now ticking all three boxes to be labelled as a currency manipulator. That being said, the US Treasury will then offer a period of negotiations, with more drastic measures imposed should discussions fail. USD/CHF briefly dipped below its 21 DMA (0.9163) but matched intraday lows set on Wednesday and Thursday last week (0.9160), with the pair’s 50 DMA residing around 0.9130. USD/JPY resides on the other side of the G10 spectrum with early losses coinciding with gains across APAC stock markets. USD/JPY tests Friday’s 105.66 high with eyes on the 50 DMA (105.74), with the pair failing to close above the MA for the past three consecutive sessions. USD/JPY Opex today includes USD 1.25bln rolling off at strike 105.00.

- EUR/GBP – Both on a firmer footing with the aid of a receding Buck, with the currencies on watch for Brexit developments in the aftermath of the videocall between PM Johnson and EC President, which noted that progress had been made but significant gaps remain, albeit the two sides have agreed to 11 days of “intensified” talks ahead of the UK de-facto deadline. Cable saw early sellers which prompted the pair to test 1.2900 to the downside, but thereafter nursed losses to print fresh session highs of 1.2964, with Sterling somewhat supported by surprise revisions higher to Services and Composite PMIs. EUR/USD meanwhile saw little action to revisions higher to final PMIs. EUR/USD retains a 1.1700+ status as it took out several potential resistance levels at 1.1750 (Fri high), 1.1755 (Wed high) ahead of 1.1763 (21 DMA), whilst the NY cut sees EUR 761mln at strike 1.1730 and around EUR 870mln at 1.1700.

- CAD, AUD, NZD – All firmer to varying degrees, with the Loonie outperforming the non-US Dollars as it coat-tails on the firmer crude prices, whilst the Aussie eyes the RBA and Aussie budget and the Kiwi eking mild gains but with gains capped on AUD/NZD dynamics. USD/CAD trickles lower below 1.3300 having had tested the level overnight, with a current base at 1.3264, with its 21 DMA at 1.3258 and 50 DMA at 1.3241. AUD/USD meanwhile inches closer towards the 0.7200 mark (vs. current low 0.7157), with its 21 and 50 DMAs residing at 0.7201 and 0.7207 respectively. Finally, NZD/USD remains contained in a narrow 0.6631-54 band as AUD/NZD reclaims 1.0800.

In commodities, WTI and Brent futures open the week on a firmer footing, with early strength coinciding with gains across stock markets overnight after Friday’s pessimism unwound amid weekend reports that US President Trump could be at the white house as early as today. Meanwhile, the conflict between Armenia and Azerbaijan over the disputed region of Nagorno-Karabakh reportedly escalated dramatically. It was also reported that the Nagorno-Karabakh region stated that 18 civilians were killed and over 90 were wounded in a week of fighting – with traders keeping eyes on any potential targeting of oil fields/refineries/ports of the OPEC+ member. Elsewhere, Libyan oil production ticked higher to 290k BPD from last week’s 270k BPD, according to sources. In terms of where we currently stand WTI Nov (USD 37/bbl) trades on either side of USD 38/bbl whilst Brent Dec reclaimed the USD 40/bbl handle (vs. low USD 39.14/bbl). Elsewhere, spot gold and silver are choppy, with earlier weakness in the yellow metal offset by a softer Dollar, with prices now back around the USD 1900/oz mark (vs. low 1887/oz), whilst spot silver attempted a breach of USD 24/oz to the upside – with the latest CFTC data suggesting hedge funds and money managers reduced positions in COMEX gold and increased them in silver contracts in the week to Sept 29th. Finally, LME copper prices are relatively flat having had drifted off highs in tandem with price action seen in stocks.

US Event Calendar

- 9:45am: Markit US Services PMI, est. 54.6, prior 54.6

- 9:45am: Markit US Composite PMI, prior 54.4

- 10am: ISM Services Index, est. 56.2, prior 56.9

DB’s Jim Reid concludes the overnight wrap

I can almost certainly guarantee that wherever you’re reading this from you had better weather than me this weekend. Or at least no worse. It rained from start to finish. Any weekend with the golf course closed is a bad one for me and watching Frozen 2 the twentieth time in two months to fill the time didn’t improve the mood. Then the coup de grace was seeing Liverpool concede 7 (seven – as they always used to type out and put in brackets for unusual scores) for the first time since 1963 last night! Quite astonishing.

The business world continues to be quite extraordinary at the moment too and Mr Trump again dominated the weekend headlines. I’m sure you’ve seen the conflicting and confusing reports concerning his health over the weekend so we won’t go into that here. The latest from yesterday was that his doctors suggested he could be released back to the White House as soon as today. He also appeared on a video last night looking in good spirits. According to the wires this has helped S&P 500 futures to trade up +0.61% this morning but to be honest it could also be because a poll showed that Biden was 14pp up over the weekend (more below). We actually published the EMR almost an hour earlier than usual on Friday and four minutes after it hit inboxes the headlines came through that the President had tested positive. So we will try not to be that efficient again and end up as virtual fish and chip paper as we were on Friday.

In terms of the impact on the election, we haven’t seen enough polling to assess whether this increases or decreases his chances of winning. There was an NBC-WSJ poll released over the weekend showing Biden ahead by 14 points – the biggest lead of the campaign. However this polling was carried out between the first debate last Tuesday and the positive Covid test early on Friday morning. For comparison the last poll from this combination saw at 8pp lead last month. An Ipsos and a YouGov poll have just been released before we go to print and they seem to show around a 10pp and 7pp lead for Biden respectively. These were conducted on Friday and Saturday.

This confirms what was suspected last week, namely that polls were edging further towards Biden even before Friday with the first evidence now coming through that this may have continued. Indeed the recent price action suggests that the market wants certainty more than anything else. Given the realistic options (assuming the polls are not completely out), perhaps the market would currently most like a Democratic clean sweep as this would increase the likelihood of near term certainty. This outcome was edging up in likelihood amongst respected political pundits ahead of Mr Trump’s positive test so Friday’s news brought back all sorts of uncertainties with tail risks increasing in all sorts of direction. The fact that Biden tested negative later in the day seemed to help markets which partly supports the theory above. So this week the market will await more news from the Trump camp and signs of movement in the polls. If Biden pulls away then markets will probably be pretty relaxed. So the batch of polls post Trump’s illness are going to be important.

As we’ll see below the VP debate takes place on Wednesday which is the next major planned event. We’ll also see what the latest on the stimulus package is. It feels like both sides are trying to show that they are doing the best they can to bridge the gap but the reality is that both sides seem to be quite far apart still and it will be an enormous feat to bridge the gap pre-election. Nonetheless, the FT reported yesterday that the US President Donald Trump has issued a call for negotiators to “work together” and complete a deal.

Overnight, Asian markets have started the week on front foot with the Nikkei (+1.20%), Hang Seng (+1.46%), Kospi (+1.18%) and Asx (+2.47%) all seeing strong advances and recovering from Friday’s morning’s shock. China’s markets are closed for holidays. In Fx, the US dollar is trading down -0.11%. In terms of overnight data, Japan September services PMI was confirmed at 46.9 (vs. 45.6 in flash).

Back to politics and onto Brexit. U.K. PM Johnson had the planned VC talk with EC President von der Leyen on Saturday and in a joint statement they instructed their chief negotiators to work intensively in order to try to bridge the obvious gaps that there are and emphasised “the importance of finding an agreement, if at all possible”. On Sunday Johnson reaffirmed that he’d like a deal but said the U.K. could prosper without one. The FT also had an article last night suggesting Barnier is going to hold talks with the impacted EU countries on fisheries which shows some progress and the possibility of negotiation movement. For me it seems like the probabilities of a deal have edged up over the last couple of weeks. In terms of news flow and headlines it’s seems to have been 7 steps forward and only 5 back. We will see. Sterling is broadly flat this morning at 1.2938 ahead of another week of talks.

Onto the virus and the UK reported an extremely high 35,850 new cases over the weekend but these were heavily impacted by around 16,000 previous unreported cases between September 25 to October 2 due to technical issues. Even after taking this into account the new weekend cases stood at 19,850, a higher run rate compared to previous weekends. Meanwhile, the delay in entering those 16,000 cases also means that their recent contacts were not immediately followed up. This will put more pressure on the government.

Bloomberg is also reporting that France may shut down bars in the Paris region and impose other new restrictions in the area. The country reported 29,537 new cases this weekend versus an average of c.25,000 cases over the previous two. In the US, New York City Mayor Bill de Blasio said he plans to close schools and non-essential businesses in nine neighbourhoods in Brooklyn and Queens where there’s been a surge in coronavirus infections. Indoor and outdoor dining will also be closed in these areas. For more details on how the virus is spreading in major regions of the world see the table below. There are a lot of footnotes so please see those in conjunction with the raw data. On the vaccine front, the FT reported the UK government’s head of the vaccine taskforce Kate Bingham as saying that less than half of the UK population could be vaccinated. She said, “There is going to be no vaccination of people under 18. It’s an adult-only vaccine for people over 50, focusing on health workers, care home workers and the vulnerable.”

In terms of this week, outside of the VP debate on Wednesday we’ll get the latest minutes from recent Fed (Weds) and ECB (Thurs) meetings, and also hear from both Fed Chair Powell (tomorrow) and ECB President Lagarde (tomorrow and Weds). The only G20 decision next week is from the Reserve Bank of Australia tomorrow. Our Australia economists expects no change in policy, but we will be watching for clues about whether a rate cut might yet be delivered by the end of the year. The main data highlight will likely be the release of the services and composite PMIs from around the world. Most are today but the U.K. comes tomorrow and China’s on Thursday after holidays. The flash readings showed clear signs of the services sector in Europe being affected by the second wave of Covid-19, with the flash Euro Area services PMI falling to 47.6, which is below the 50-mark that separates expansion from contraction, with both Germany (49.1) and France (48.5) also in contractionary territory. We will see if this trend is confirmed and whether there was any late month deterioration from the initial flash reading. The day by day week ahead calendar is at the end.

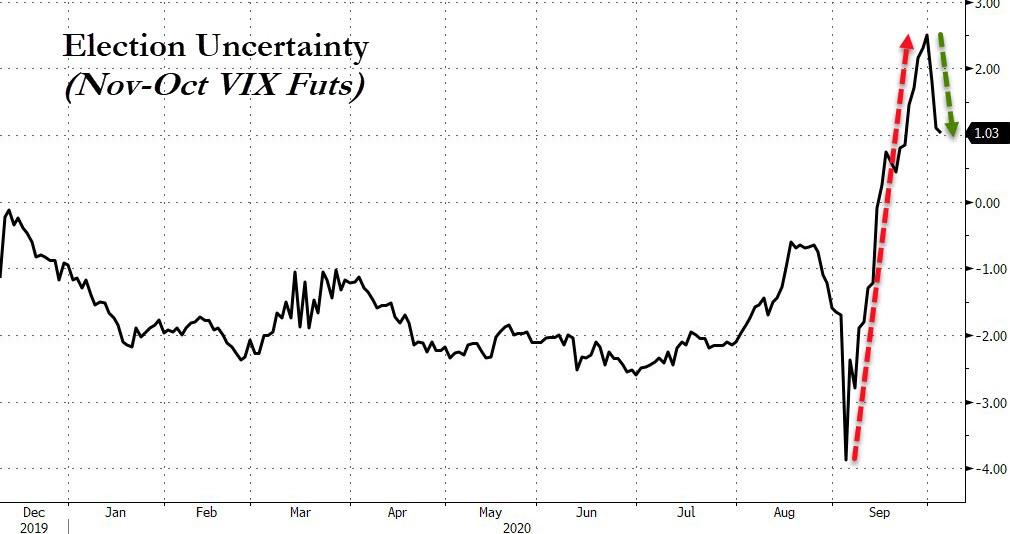

Recapping last week now, as we moved into Q4, US equities saw their first positive week since August even with a weaker end of Friday. In a particularly hectic week that started with one of the most raucous US Presidential debates in memory and ended with the sitting US President testing positive for Covid-19 equity volatility jumped. The VIX volatility index rose +1.25pts to 27.63 even as equity prices rose – it was the second largest weekly rise in vol since June. Even with this uncertainty, the S&P 500 rose +1.52% (-0.96% Friday) on the week, breaking a streak of four losing weeks – the longest since August 2019. The NASDAQ rose +1.48% (-2.22% Friday) for the second weekly gain. European equities rose as well with the Stoxx 600 ending the week +2.02% (+0.25% Friday), the third weekly gain out of the last four. The IBEX (+1.90%), FTSE 100 (+1.02%), and CAC (+2.01%) all posted strong weekly equity performances even as their home countries reinstated some restrictions in the face of increasing Covid-19 caseloads.

The dollar dropped (-0.84%) as risk assets generally gained, for just its second weekly loss since the end of August. The drop in the dollar saw gold gain +2.06%, as the precious metal finished the week just under the $1900/oz level. Even though equities gained on the week, oil did not follow suit as worries on global demand saw WTI (-7.95%) and Brent crude (-6.32%) fall sharply and is now down four out of the last five weeks and is at its lowest weekly close since June. Core sovereign bonds were mixed on the week as US 10yr Treasury yields rose +4.6bps (+2.3bps Friday) to finish at 0.701% and 10yr Gilt yields rose +5.7bps (+1.2bps Friday) to 0.25%, while 10yr Bund yields were down -0.7bps (unchanged Friday) to -0.54%. Italian 10yr yields fell -10.2bps to 0.784% – their lowest levels since an all-time low last September.

On the data front, US Nonfarm payrolls rose by 661k (vs. 859k expected) on Friday while August’s numbers were revised up to 1.49 million from 1.37m. The unemployment rate fell 0.5 percentage points to 7.9% (vs. 8.2 expected), though the labour-force participation rate declined by 0.3 points to 61.4%. Meanwhile in Europe, the Euro-area CPI reading showed inflation slowed to -0.3% in August (vs. -0.2% expected) while the core rate set a six-year low at 0.2% (0.4% expected).

3A/ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED //Hang Sang CLOSED UP 308.73 OR 1.32% /The Nikkei closed UP 282.24 POINTS OR 1.23%//Australia’s all ordinaires CLOSED UP 2.54%

/Chinese yuan (ONSHORE) closed /Oil UP TO 38.65 dollars per barrel for WTI and 40.71 for Brent. Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN CLOSED AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7300 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

CHINA/USA

Giuliani: correctly states that he holds China response for what happened to Trump

(Ivan Pentchoukov/EpochTimes)

Giuliani: I Hold China Responsible For What Happened To Trump

Authored by Ivan Pentchoukov via The Epoch Times,

Former New York City Mayor Rudy Giuliani on Sunday said he holds China responsible for President Donald Trump becoming infected with the Chinese Communist Party (CCP) virus, commonly known as the novel coronavirus.

Giuliani, the president’s personal attorney, made the comment in an interview with Fox News on Oct. 4.

“Don’t be paralyzed, please, our economy has to come back for the good of our children,” Giuliani said in reference to how Americans should deal with the risk of the virus.

“And we assert ourselves as the most powerful nation on earth because otherwise you know who will? The country that attacked us, China. And they attacked us with this, believe me,” Giuliani said.

“I hold them responsible for what happened to my president the day before yesterday and everybody else.”

The CCP virus outbreak began in Wuhan, China, in late 2019. The CCP’s attempts to cover up the contagion and the regime’s overall negligence contributed to the global outbreak of the virus. Trump regularly refers to the virus and the “China virus.”

The president has said that the United States will make China pay a “very substantial” price for its role in the outbreak, but official actions have so far been limited to a travel ban meant to stop the spread of the disease and the freezing of the trade talks.

“There are a lot of ways you can hold them accountable,” Trump said on April 27. “We are not happy with China, we are not happy with that whole situation. Because we believe it could have been stopped at the source, it could have been stopped quickly and it wouldn’t have spread all over the world.”

Giuliani said he spoke to the president on Saturday for 35-40 minutes about his health and politics. Trump passed Giuliani messages to his reelection campaign.

“I had to kind of get him off the phone so he went back and rested. He did say that he’d love to get out as quickly as possible,” Giuliani said.

“He feels like he could go out now. He said he felt pretty bad the first day, but now he feels, for the last 24 hours—and that was 3 o’clock yesterday—he felt perfectly fine. No fever. A little tired but not very tired. For him to feel a little tired is nothing.”

Prior to the president testing positive, Giuliani spent hours in a room with Trump and two others who had also tested positive—White House advisor Kellyanne Conway and former New Jersey Gov. Chris Christie. Giuliani said he tested negative for the virus on Friday and that he plans to get tested again on Monday.

The former New York City mayor told Fox News that he advised Trump to listen to the doctors and take a break from campaigning while supporters and allies fill for him on the campaign trail.

“Those of us who love him and care about him, makes you want to cry to think of what they’ve done to him. Every single day he’s been in the White House, they tried to get him out. From the day he started until now. I mean, last week Nancy Pelosi wanted to impeach him because he nominated judge [Amy Coney] Barrett,” Giuliani said, mentioning the House Speaker.