GOLD:$1888.10 DOWN $16.00 The quote is London spot price

Silver:$23.81 DOWN 9 CENTS London spot price ( cash market)

your data…

Closing access prices: London spot

i)Gold : $1888.00 LONDON SPOT 4:30 pm

ii)SILVER: $23.78//LONDON SPOT 4:30 pm

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED //Hang Sang CLOSED UP 262.21 OR 1.09% /The Nikkei closed DOWN 10.91 POINTS OR 0.05%//Australia’s all ordinaires CLOSED UP 1.22%

/Chinese yuan (ONSHORE) closed /Oil UP TO 39.68 dollars per barrel for WTI and 41.81 for Brent. Stocks in Europe OPENED ALL RED// ONSHORE YUAN CLOSED AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7331 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total withdrawals; NIL; oz

We had 0 kilobar transactions +

ADJUSTMENTS: 1 //

The front month of OCT registered a total of 12,634 contracts for a GAIN of 230 contracts. We had 396 notices filed on Tuesday so we gained a humongous 626 contracts or 62,600 additional oz will stand for delivery in this active delivery month of October. In gold we have not seen queue jumping start so early in the month. I wrote the following yesterday: “thus you can bet the farm that throughout October, the total number of gold oz standing will increase from this level.” So far it seems that I am right. Gold must be secured for comex contracts standing for metal as well as exercised EFP’s.

November gained 235 contracts to stand at 1389.

The big December contract LOST 312 contracts DOWN to 448,572 contracts..

THE BIG STORY AGAIN TODAY IS THE HIGH OI STANDING FOR OCTOBER (100.818 tonnes). GENERALLY OCTOBER IS A POOR DELIVERY MONTH AS MOST INVESTORS PREFER TO SKIP THIS MONTH AND MOVE STRAIGHT TO DECEMBER. IT LOOKS LIKE SOME MAJOR ENTITY(GOLDMAN SACHS) JUST CANNOT WAIT FOR DECEMBER AS THEY ARE MAKING THEIR MOVE ON OCTOBER FOR PHYSICAL METAL. GOLDMAN SACHS ONE OF THE LEADERS OF THE NEW LONDON LME EXCHANGE NEEDS THE GOLD INVENTORY FOR LIQUIDITY AND INITIAL CONTRIBUTION WITH OTHER MAJOR PLAYERS. THE MAJOR DIFFERENCE BETWEEN THIS MONTH AND OTHER MONTHS IS THAT THIS GOLD STANDING IN OCTOBER WILL LEAVE THE COMEX AND HEAD FOR LONDON.

We had 2283 notices filed today for 228,300 oz OR 7.1010 TONNES.

To calculate the INITIAL total number of gold ounces standing for the OCT /2020. contract month, we take the total number of notices filed so far for the month (22,060) x 100 oz , to which we add the difference between the open interest for the front month of OCT (12,634 CONTRACTS ) minus the number of notices served upon today (2283 x 100 oz per contract) equals 3,241,100 OZ OR 100.818 TONNES) the number of ounces standing in this active month of Oct

thus the INITIAL standings for gold for the OCT/2020 contract month:

No of notices filed so far (22,060, x 100 oz +12,634 OI) for the front month minus the number of notices served upon today (2283) x 100 oz which equals 3,241,100 oz standing OR 100.818 TONNES in this active delivery month. This is a HUGE amount for gold standing for a OCT delivery month (a poor active delivery month).

We gained 626 contracts or an additional 62,600 oz will stand on this side of the pond searching for metal.

NEW PLEDGED GOLD: BRINKS

592,648.822 oz NOW PLEDGED SEPT 15.2020/HSBC 18.433 TONNES ( A HUGE INCREASE FROM 10.6)

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

277,934.09 oz (some deleted august 3) JPM 8.644 TONNES

610,238.285 oz pledged June 12/2020 Brinks/ July 2/July 21 19.017 tonnes

51,084.609 oz Pledged August 21/regular account 1.588 tonnes JPM

total pledged gold: 1,574,454.119 oz 48.97 tonnes

total registered, pledged and eligible (customer) gold 37,203,231.729 oz 1,157.17 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1030.83 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

END

And now for the wild silver comex results

And now for the wild silver comex results

INITIAL STANDINGS

OCT. SILVER COMEX CONTRACT MONTH//INITIAL STANDING

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

10,141.250 oz

CNT

Delaware

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

11,849.200 oz

CNT

|

| No of oz served today (contracts) |

7

CONTRACT(S)

(35,000 OZ)

|

| No of oz to be served (notices) |

206 contracts

1,030,000 oz)

|

| Total monthly oz silver served (contracts) | 1689 contracts

8,445,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

we had 1 deposits into the customer account (ELIGIBLE ACCOUNT)

i)into JPM: NIL oz

JPMorgan now has 187.1 million oz of total silver inventory or 49.20% of all official comex silver. (187.1 million/380.6 million

ii) Into CNT: 11,849.200 oz

total customer deposits today: 11,849.200 oz

we had 2 withdrawals:

total withdrawals; 10,141.250 oz

We had 1 adjustments/ dealer to customer

i) CNT 418,427.893 oz

Total dealer(registered) silver: 142.098 million oz

total registered and eligible silver: 380.597 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

October had 213 notices outstanding for a LOSS of 313 contracts. We had 314 notices served upon yesterday so we GAINED 1 contracts or 5,000 additional oz of silver will stand in this non active month of October.

November saw a gain of 15 notices up to 445 contracts.

December saw a LOSS of 1199 contracts DOWN to 131,445 contracts.

The total number of notices filed today for the OCT 2020. contract month is represented by 7 contract(s) FOR 35,000 oz

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 1689 x 5,000 oz = 8,445,000 oz to which we add the difference between the open interest for the front month of OCT( 213) and the number of notices served upon today 7x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the OCT/2019 contract month: 1,689 (notices served so far) x 5000 oz + OI for front month of OCT (213)- number of notices served upon today (7) x 5000 oz of silver standing for the OCT contract month .equals 9,475,000 oz. ..VERY STRONG FOR A NON ACTIVE MONTH.

We gained 1 contracts or 5,000 additional oz will stand for silver metal on this side of the pond as they refused to morph into a London based forwards.

TODAY’S ESTIMATED SILVER VOLUME : 61,910 CONTRACTS // volume rather slow//

FOR YESTERDAY 75,638 ,CONFIRMED VOLUME// much slower than normal/

YESTERDAY’S CONFIRMED VOLUME OF 75,638 CONTRACTS EQUATES to 0.378 billion OZ 54.0% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 3.11% ((OCT 7/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.60% to NAV: (OCT 6/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/3.11%

(courtesy Sprott/GATA

3. SPROTT CEF .A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 19.19 TRADING 18.58///NEGATIVE 3.19

END

And now the Gold inventory at the GLD/

OCT 7/WITH GOLD DOWN $16.00 DOLLARS TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.98 TONNES FROM THE GLD////INVENTORY RESTS AT 1271.62 TONNES

OCT 6/WITH GOLD DOWN $10.70 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1275.60 TONNES

OCT 5/WITH GOLD UP $12.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.59 TONNES//INVENTORY RESTS AT 1275.60 TONNES

OCT 2/WITH GOLD DOWN $7.30 TODAY, A HUGE CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 9.3 TONNES INTO THE GLD//INVENTORY RESTS AT 1278.19 TONNES

OCT 1/WITH GOLD UP $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1268.89 TONNES

SEPT 30//WITH GOLD DOWN $6.80 TODAY, NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1268.89 TONNES

SEPT 29/WITH GOLD UP $19.10//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1268.89 TONNES

/SEPT 28//WITH GOLD UP $14.30 DOLLARS: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.05 TONNES INTO THE GLD//INVENTORY RESTS AT 1268.89 TONNES

SEPT 25//WITH GOLD DOWN 410.80 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .3 TONNES FROM THE GLD////INVENTORY RESTS AT 1266.84 TONNES

SEPT 24/WITH GOLD UP $9.80 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1267.14TONNES.

SEPT 23//WITH GOLD DOWN $28.00 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 11.68 TONNES FROM THE GLD////INVENTORY RESTS AT 1267.14 TONNES

SEPT 22/WITH GOLD DOWN $4.50 TODAY, A MONSTROUS CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 18.98 TONNES OF PAPER GOLD ENTER THE GLD///// INVENTORY RESTS AT 1278.62TONNES

SEPT 21/WITH GOLD DOWN $47.20 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 12.94 TONNES INTO THE GLD///INVENTORY RESTS AT 1259.64TONNES

SEPT 18/WITH GOLD UP $10.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS THIS WEEKEND AT: 1246.99 TONNES

SEPT 17/WITH GOLD DOWN $18.05 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD//INVENTORY RESTS AT 1246.99 TONNES

SEPT 16.WITH GOLD UP $4.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1247.57 TONNES

SEPT 15//WITH GOLD UP $2.25 TODAY: A SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .43 TONNES FROM THE GLD//INVENTORY RESTS AT 1247.57 TONNES

SEPT 14/WITH GOLD DOWN 90 CENTS TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.96 TONNES FROM THE GLD////INVENTORY RESTS AT 1248.00 TONNES

SEPT 11/WITH GOLD DOWN $14.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1252.96 TONNES

SEPT 10/WITH GOLD UP $8.85 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.92 TONNES INTO THE GLD////INVENTORY RESTS AT 1252.96 TONNES

SEPT 9/WITH GOLD UP $19.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1250.04 TONNES

SEPT 8/WITH GOLD UP $8.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1250.04 TONNES

SEPT 4//WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1250.04 TONNES

SEPT 3/WITH GOLD DOWN $7.50 ON THIS 2ND DAY OF A 3 DAY RAID: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1250.04 TONNES

SEPT 2/WITH GOLD DOWN $34.00 TODAY, WE HAVE 2 SMALL CHANGES IN GOLD INVENTORY AT THE GLD: 2 WITHDRAWALS OF .87 TONNES AND.59 TONNES FROM THE GLD////INVENTORY RESTS AT 1250.04 TONNES

SEPT 1/WITH GOLD UP $7.10 TODAY, WE HAVE NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1251.50 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

OCT 7/ GLD INVENTORY 1271.62 tonnes*

LAST; 917 TRADING DAYS: +331.78 NET TONNES HAVE BEEN ADDED THE GLD

LAST 817 TRADING DAYS://+510.71 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

OCT 7/WITH SILVER DOWN 9 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 466,000 OZ INTO THE SLV////INVENTORY RESTS AT 561.566 MILLION OZ/

OCT 6/WITH SILVER DOWN 51 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 561.100 MILLION OZ//

OCT 5/WITH SILVER UP 53 CENTS TODAY: A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 11.984 MILLION OZ INTO THE SLV //INVENTORY RESTS AT 561.100 MILLION OZ//

OCT 2/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 549.116 MILLION OZ//

OCT 1/WITH SILVER UP 66 CENTS TODAY, A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.489 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 549.116 MILLION OZ//

SEPT 30//WITH SILVER DOWN 96 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 186,000 OZ FROM THE SLV.//INVENTORY RESTS AT 550.605 MILLION OZ..

SEPT 29/WITH SILVER UP 86 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.791 MILLILON OZ//

SEPT 28//WITH SILVER UP 48 CENTS TODAY: A HUGE DEPOSIT OF 3.769 MILLION OZ CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.791 MILLION OZ//

SEPT 25/WITH SILVER DOWN 14 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: 2 TRANSACTIONS: A PAPER WITHDRAWAL OF 8.28 MILION OZ FROM THE SLV AND A DEPOSIT OF 1.861 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 547.022 MILLION OZ//

SEPT 24//WITH SILVER UP 15 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 553.443 MILLION OZ//

SEPT 23//WITH SILVER DOWN $1.41: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.048 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 553.443 MILLION OZ///

SEPT 22/WITH SILVER DOWN ONE CENT TODAY: A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.141 MILLION OZ////INVENTORY RESTS AT 555.491 MILLION OZ..

SEPT 21/WITH SILVER DOWN $2.43 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV A PAPER WITHDRAWAL OF 1.862 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 553.350MILLION OZ//

SEPT 18. WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 555.212 MILLION OZ/

SEPT 17/WITH SILVER DOWN 31 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.537 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 555.212 MILLION OZ/

SEPT 16//WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.749 MILLION OZ//

SEPT 15/WITH SILVER UP 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.793 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 558.749 MILLION OZ..

SEPT 14/WITH SILVER UP 47 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS A) 1.675 MILLION OZ AND ANOTHER B) 0.931 MILLION OZ/ FROM THE SLV////INVENTORY RESTS AT 555.956 MILLION OZ//

SEPT 11/WITH SILVER DOWN 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.562 MILLION OZ//

SEPT 10/WITH SILVER UP 16 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.607 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 558.562 MILLION OZ.

SEPT 9/WITH SILVER UP 6 CENTS TODAY: STRANGE: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.63 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 561.169 MILLION OZ

SEPT 8/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 564.799 MILLION OZ

SEPT 4//WITH SILVER DOWN 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 3.631 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 564.799 MILLION OZ//

SEPT 3//WITH SILVER DOWN 50 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.258 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.430 MILLION OZ/./

SEPT 2.WITH SILVER DOWN $1.04 TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.365 MILLION OZ FROM THE SLV///INVENTORY REST AT 571.688 MILLION OZ.

SEPT 1//WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 574.053 MILLION OZ//

OCT 7.2020:

SLV INVENTORY RESTS TONIGHT AT

561.566 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Is Silver about to “Pop” or “Drop”? [Chart]

The chart of silver at the moment shows that it is poised for a breakout move.

It has failed on a number of occasions recently to close above resistance at $24.40. If we do see it closing above this level that could signal a quick move up to the next major resistance at $26.50.

However it is also also finding support from the major upward trend line that has held since the March lows and a break below this could signal a retest of the recent lows (approx. $22.65) and ultimately support further down at $19.50.

With the precious metals markets being heavily influenced at the moment by the vagaries of the stock market and the relative strength of the US dollar, any “News-bomb” will have a increased impact on the short-term price action for the white metal.

NEWS and COMMENTARY

Gold eases after Trump’s discharge, weaker dollar cushions decline

Gold Is Still an Excellent Diversifier: UBS (Bloomberg TV)

Dollar on defensive as U.S. stimulus hopes, Trump discharge boost risk sentiment

U.S. commercial bankruptcies up 33% year to date

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

05-Oct-20 1899.65 1909.60 1467.48 1472.49 1616.41 1620.49

02-Oct-20 1906.40 1903.05 1473.46 1471.82 1627.87 1624.44

01-Oct-20 1895.55 1902.00 1477.01 1476.33 1615.96 1619.74

30-Sep-20 1883.40 1886.90 1468.49 1467.63 1609.74 1613.30

29-Sep-20 1882.40 1883.95 1461.87 1465.71 1610.02 1606.44

28-Sep-20 1850.95 1864.30 1440.78 1448.37 1589.41 1597.52

25-Sep-20 1870.05 1859.70 1467.05 1462.65 1605.25 1598.78

24-Sep-20 1850.75 1861.75 1453.21 1460.92 1588.68 1598.50

23-Sep-20 1888.10 1873.40 1483.48 1470.06 1611.49 1603.63

22-Sep-20 1903.10 1906.00 1487.46 1493.16 1621.63 1625.25

21-Sep-20 1930.90 1909.35 1503.21 1489.48 1638.18 1624.47

18-Sep-20 1954.75 1950.85 1505.16 1508.01 1647.85 1648.66

17-Sep-20 1936.10 1936.25 1494.67 1499.82 1642.78 1640.20

16-Sep-20 1964.80 1961.80 1521.15 1512.55 1654.56 1656.74

15-Sep-20 1963.55 1949.35 1523.13 1513.09 1652.13 1644.67

Own gold coins and bars in the safest vaults in Zurich, Switzerland with GoldCore. Learn why Switzerland remains a safe haven jurisdiction for owning precious metals. Access Our Most Popular Guide, the Essential Guide to Storing Gold in Switzerland here

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here

ii) Important gold commentaries courtesy of GATA/Chris Powell

LIARS!

CFTC says new capacity to interpret trading data revived silver investigation

JPMorgan Probe Was Revived by Regulators’ Data Mining

By Dave Michaels

The Wall Street Journal

Monday, October 5, 2020

WASHINGTON — Investigators probing whether traders at JPMorgan Chase rigged silver prices seven years ago decided there was no case to bring. Last week the same agency hammered the megabank with a $920 million fine.

How a small agency that once walked away from an investigation of price manipulation, only to later impose its biggest fine ever for the conduct, shows the advances government has made in using data to uncover market manipulation, said James McDonald, enforcement director of the Commodity Futures Trading Commission.

…

“We could not have brought the JPMorgan case without the data analytics program we have now,” said Mr. McDonald, who will step down as director this week after more than three years in the post.

The data needed to uncover the eight-year market manipulation scheme came from Chicago-based CME Group Inc., the operator of exchanges including one that offers trading in gold and silver futures. The volume of data — including trades, orders, and other messages flooding into CME’s computers — is so massive the CFTC couldn’t store or use it when Mr. McDonald began seeking it in 2017, he said.

Five years of complete CME trading data amounts to 1.7 terabytes, or 127 million pages of information, according to testimony in a recent trial that resulted in the conviction of two former Deutsche Bank AG traders on fraud charges related to spoofing.

As the CFTC added the ability to store and access more trading data in the cloud, it also hired former Chicago traders and other quantitative-minded employees to write programs that filter CME’s data for patterns of manipulation.

“There is really no other avenue that we have that allows us to be as proactive [investigating] as data,” Mr. McDonald said. …

… For the remainder of the report:

https://www.wsj.com/articles/jpmorgan-probe-revived-by-regulators-data-m…?

END

Gold seems to breaking away for the inverse relationship with the dollar

(Dave Kranzler/IRD/GATA)

Dave Kranzler: The price of gold when the dollar index hits 70

1:47p ET Tuesday, October 6, 2020

Dear Friend of GATA and Gold:

While they are inversely correlated over the long term, gold and the U.S. dollar don’t always behave consistently toward each other, Dave Kranzler of Investment Research Dynamics in Denver writes today. Indeed, Kranzler writes, since March gold has risen almost 32 percent while the dollar index has been largely unchanged.

…

But with economic conditions in the United States sinking steadily, Kranzler writes, the dollar is bound to fall, boosting the monetary metals again.

His analysis is headlined “The Price Of Gold When the Dollar Index Hits 70” and it’s posted at IRD here:

https://investmentresearchdynamics.com/the-price-of-gold-when-the-dollar…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

iii) Other physical stories:

The buggers raised margins on both gold and silver last night

no wonder gold/silver fell:

James McShirley..

Fed’s Kashkari sees ‘much worse’ downturn without more fiscal aid

Yes, the very same news that drove the Dow giddy with delight- a Trump tweet promising more free stuff, aka stimulus- is somehow counterintuitively BAD for gold. Even the dollar reacted negatively.

Yesterday’s puny trading volume that was heading to another record low was rescued late in the day when the selloff accelerated. Today’s volume is still puny, albeit less puny than Tuesday. That aforementioned accelerated selloff was HIGHLY likely due to the CME’s margin hikes on gold and silver. Silver margin in particular was hiked another 13% to $16,500, bringing its leverage all the way down to 7.2-1. Ya think they are scared sh*tless of the Kryptonite? Gold margin is now $11,550, giving it a leverage of 16.2-1.

The punishing margins on silver is proof positive they intend to stop as many speculators as possible from driving the price to the moon. No wonder trading volumes are so low. The cartel got wrist slapped, yet still exert influence over CME margin decisions. This is the same crap they have pulled over and over for many years. With this margin hike we now know for certain the physical market is in trouble. If Comex silver goes full margin soon it will not surprise me. The days of counterintuitive price moves and margin requirement gimmickry are going to end.

James M

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

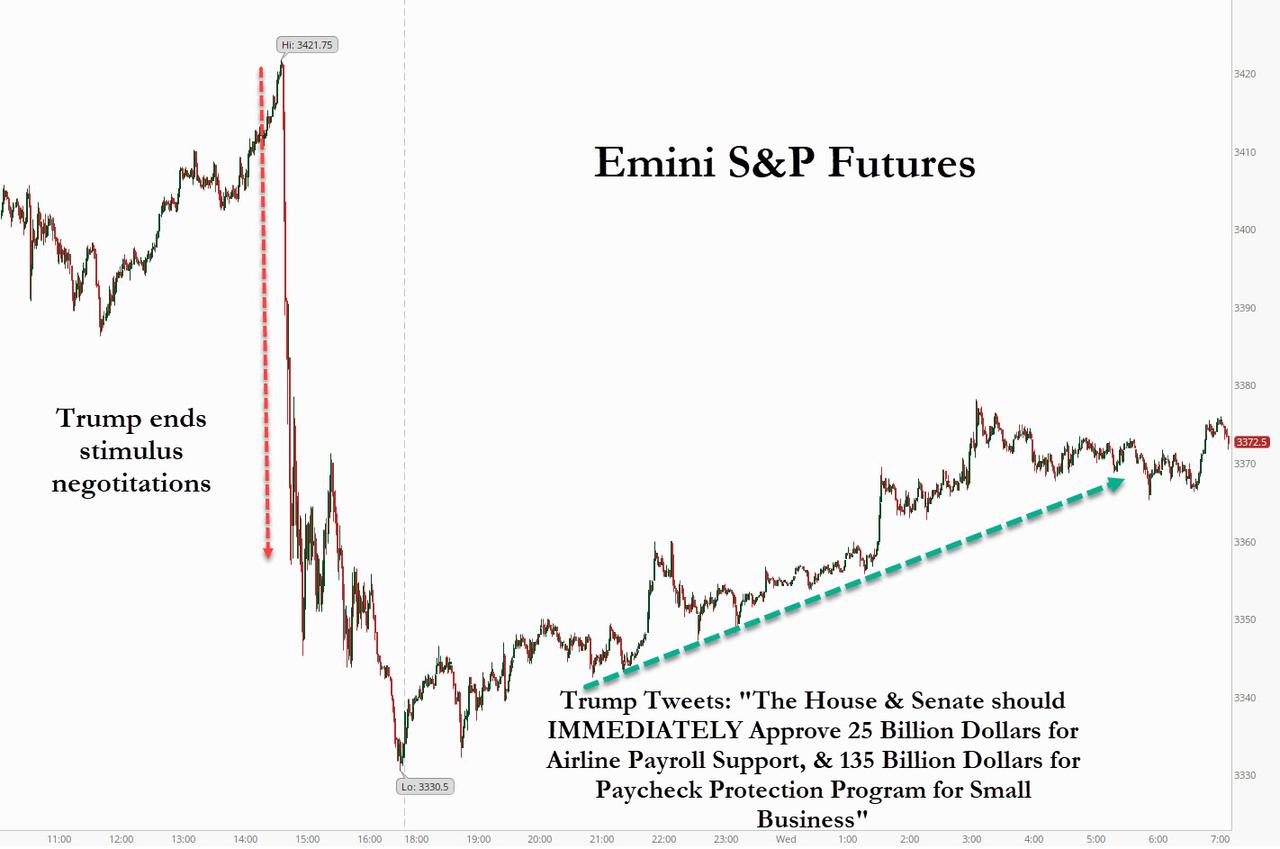

S&P Futures Rebound As Trump Tweetstorm Leaves Door Open For More Stimulus Talks

It’s been a rollercoaster 24 hours for markets, which initially surged on Tuesday on fresh fiscal stimulus hopes, only to see said hope crushed by Trump at exactly 2:47pm, when the president tweeted that had had “instructed my representatives to stop negotiating until after the election when, immediately after I win, we will pass a major Stimulus Bill that focuses on hardworking Americans and Small Business.” The tweet unleashed a furious selling spree, which saw S&P futures drop as low as 3,330 overnight after closing 1.4% lower, more than 90 point from their pre-Trump tweet highs.

The tweets sparked the worst session for the S&P 500 and the Dow in two weeks, while airlines sank 3% as the move appeared to scuttle $25 billion in new bailout for the industry. All this happened just hours after Fed Chair Jerome Powell called for more help for businesses and households to keep a nascent economic recovery from faltering.

Trump said the biggest sticking point in the negotiations was the Democratic demand for aid to cash-strapped state and local governments, without which they will have to push through aggressive budget cuts: “I am rejecting their request, and looking to the future of our Country. I have instructed my representatives to stop negotiating until after the election when, immediately after I win, we will pass a major Stimulus Bill that focuses on hardworking Americans and Small Business,” Trump tweeted.

However, about six hours later, in a furious tweet (and retweet) storm which touched on everything from the fake Russian collusion probe, to the FDA, the president appeared to backtrack from completely abandoning negotiations, when president made separate appeals for lawmakers to approve additional funding for airlines to prevent thousands of job cuts, more aid to small businesses and direct government payments worth up to $1,200 for most individuals.

In the aftermath of the Trump tweetstorm which took algos lots of milliseconds to parse through, futures resumed levitating and regained much of the Tuesday drop as markets in Asia recovered some ground following, with Japan’s Topix down 0.1% on Wednesday afternoon and Hong Kong’s Hang Seng index actually rising 0.6%.

“These tweets appear to have arrested the risk-off move,” Rabobank analyst Lyn Graham-Taylor wrote in an investor note “However, it seems a stretch to think that the Democrats would be fans of signing any standalone stimulus measures as, heading into the election, it would erode one of the differentiating factors between them and the Republicans.”

Trump’s apparent willingness to continue discussions helped push shares of Delta Air Lines, American Airlines Group, United Airlines and JetBlue higher between 2.4% and 6.9% in premarket trading. Amazon.com and Apple rose in premarket trading while Facebook was flat as investors seemed to take in stride a House panel’s proposal of stricter antitrust rules to curb the power of the four technology giants, including Google. Italian payments giant Nexi SpA slid after news of private-equity backers selling shares.

Still, odds of Democrats accepting a piecemeal deal instead of a bulk package are virtually nil. As the FT notes, “Trump’s subsequent statement that he was still interested in approving more federal aid on a piecemeal basis is unlikely to be greeted with enthusiasm among Democrats, who have long pushed for a comprehensive package. But it may leave a small sliver of hope that Mr Trump could yet compromise.”

Sure enough, according to Medley Global, Trump’s support for alternative stimulus measures are “removing the angst” from his earlier decision, allowing futures to push higher as investors digested the tweets; at the same time Treasuries resumed falling and the dollar was mixed, while oil reversed an earlier gain as the API report signaled U.S. crude stockpiles rose for the first time in four weeks. Gold gained.

Others, such as Axi Corp analyst Milan Cutkovic, quickly joined in attempting to spin the reversal of what until yesterday was the widely accepted narrative, as bullish: “(The halt in stimulus talks) is unlikely to be the catalyst for a significant sell-off as most market participants were not anticipating that a deal will be reached ahead of the election anyway.” He cautioned however that “should there be no stimulus package announced shortly after the election, investors could get increasingly nervous about the economic recovery losing momentum.”

European stocks erased initial gains to trade lower at mid-session on Wednesday, weighed down by declines among insurers and banking stocks. The Stoxx 600 Index was down 0.2% at 11:45 a.m. London time, with investors looking ahead to the release of the minutes from the U.S. Federal Reserve’s September meeting and continuing to digest President Donald Trump’s decision to halt stimulus talks. Gazprom PJSC’s shares fell after it was hit with a 29 billion zloty ($7.6 billion) fine from Poland’s antitrust watchdog, which said its proposed Nord Stream 2 gas pipeline impedes competition on European Union energy markets.

Earlier in the session, Asian stocks gained, led by energy and IT, after rising in the last session. The Topix was little changed, with Olympic rising and Tokai Soft Co Ltd falling the most.

Meanwhile, with Trump now out of the hospital, investors continue to monitor the virus’s impact on economic recoveries around the world. Signs are mounting the virus is returning to the New York area, with infections reaching three-month highs. The European Commission is due to announce a contract to procure as many as 500,000 treatment courses of remdesivir from Gilead Sciences Inc., an EU official said.

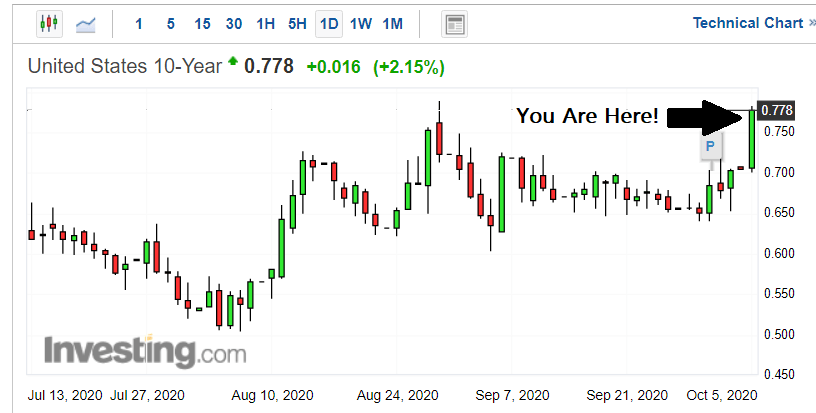

In rates, Treasuries bear-steepen as stocks advanced ahead of today’s 10Y auction, reversing all of yesterday’s gains, and were near session lows after U.S. President Trump reversed Tuesday’s position against negotiating economic stimulus measures. Yields were higher by 4bp-5bp at long end, steepening 5s30s by ~2bp, 2s10s by nearly 4bp; 10-year, higher by 4bp at 0.775%, lags bunds and gilts by 2bp-3bp. Supply was also a factor as dealers prepare to underwrite 10- and 30-year re-openings Wednesday and Thursday. Euro-area bonds mostly slipped before Lagarde speaks.

In FX, the Bloomberg Dollar Spot Index inched lower as it erased an Asia session gain and the Treasury curve steepened, following yesterday’s flattening. Risk-sensitive currencies, led by Norway’s krone and the Australian dollar, advanced versus the dollar; the yen was the worst performer as it extended losses in European hours.

In commodities, WTI and Brent remained under pressure at/near session lows as markets balance supply and demand side developments. On the demand side, woes of the implications of the resurging cases persist, in turn prompting the EIA to downgrade its 2020 world oil demand growth forecast by 300k BPD to a decline of 8.62mln BPD Y/Y and cut 2021 world oil demand growth forecast by 280k BPD to an increase of 6.25mln BPD Y/Y, with the OPEC and IEA releases due next week. From a supply standpoint, Private Inventory data printed a larger than expected build (+1.0mln bbls vs. Exp. +0.3mln bbls) and markets await confirmation from the EIA which showed similar expectations for the headline figure. (+0.294mln bbls).

And now hold on to your hats because the political rollercoaster is not done yet, and all eyes later in the day will be on the only debate between Vice President Mike Pence and Democratic challenger Kamala Harris, which comes less than a week after Trump said he had contracted COVID-19.

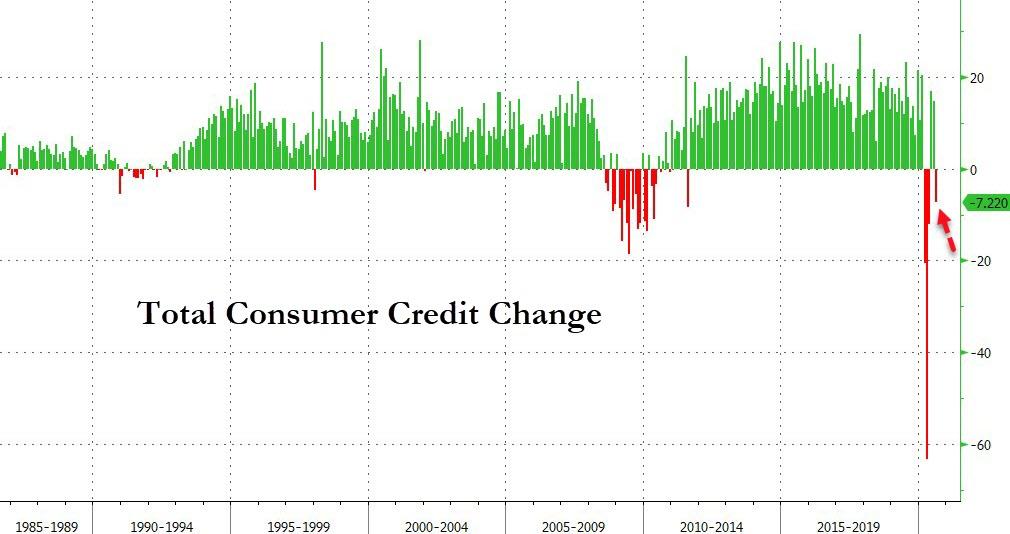

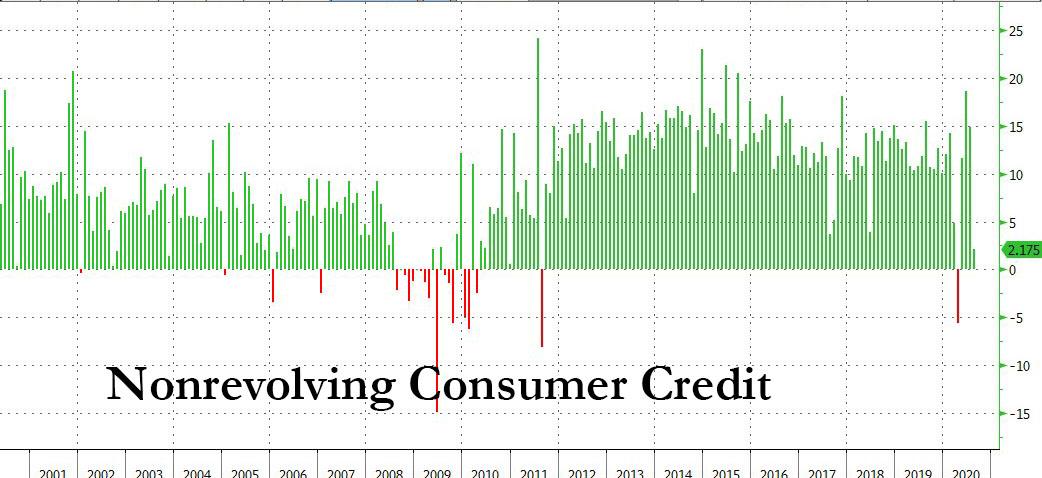

We also get the FOMC’s minutes from their September meeting, and hear from the ECB’s Lagarde, Villeroy, and the Fed’s Rosengren, Bostic, Kashkari, Williams and Evans. Finally, the data highlights include August data on German industrial production, Italian retail sales and US consumer credit.

Market Snapshot

- S&P 500 futures up 0.5% to 3,369.75

- STOXX Europe 600 down 0.1% to 365.53

- MXAP up 0.4% to 173.75

- MXAPJ up 0.7% to 572.81

- Nikkei down 0.05% to 23,422.82

- Topix up 0.04% to 1,646.47

- Hang Seng Index up 1.1% to 24,242.86

- Shanghai Composite down 0.2% to 3,218.05

- Sensex up 0.7% to 39,845.35

- Australia S&P/ASX 200 up 1.3% to 6,036.38

- Kospi up 0.9% to 2,386.94

- Brent futures down 1.4% to $42.07/bbl

- Gold spot up 0.7% to $1,891.79

- U.S. Dollar Index little changed at 93.73

- German 10Y yield fell 0.6 bps to -0.513%

- Euro up 0.2% to $1.1759

- Italian 10Y yield fell 3.1 bps to 0.573%

- Spanish 10Y yield fell 1.4 bps to 0.222%

Top Overnight News from Bloomberg

- The ECB is running down its stock of so-called commercial paper — short-term debt instruments issued by companies to meet immediate funding needs — while the Bank of England announced plans to discontinue purchases. It’s a dramatic turnaround from April when some of Europe’s biggest firms, including Iberdrola SA and Volkswagen AG, were urging the ECB to quicken short-term debt purchases to head-off crippling cash crunches

- The French president is standing firm on his demand to keep the same access to British waters his country’s fishing industry enjoys today, according to officials familiar with the talks. That’s angering the British and creating tensions even among his allies within the EU

- Spain’s growing list of risks is starting to make investors nervous. The nation’s debt is lagging a regional rally that has driven the rate on Italian bonds — long regarded as the pariah of Europe and among the highest yielding — close to a record low. That’s narrowed the gap between Spanish and Italian yields to the smallest in more than two years

- The European Union looks set to launch a $118 billion foray into social bonds, a market that has already swelled four-fold this year to fund projects to help societies recover from the coronavirus

- Norway’s government is on track to withdraw a record amount from its sovereign wealth fund this year, and to continue pumping historic amounts of stimulus in 2021, to fight the “severe setback” triggered by the Covid crisis

A quick look at global markets courtesy of NewsSquawk

Asian equities traded mixed as the region partially shrugged off the negative mood which initially rolled over from Wall St, where stock markets slumped in late trade after US President Trump announced that he is to walk away from COVID relief talks until after the election amid disparities regarding the value of the stimulus package. This resulted to losses of more than 1% for all major US indices and the large tech names were also pressured in extended trade after the House democrats antitrust committee report noted several tech giants enjoyed ‘monopoly power’ and recommended changes including structural separations and prohibiting dominant platforms from entering adjacent lines of business. Nonetheless, the tone in Asia gradually improved with ASX 200 (+1.3%) first to buck the trend as it reclaimed the 6000 level, led by strength in consumer stocks after the announcement of an expansionary budget which brought forward tax cuts and with sentiment also helped by increased calls for the RBA to loosen policy next month. Nikkei 225 (-0.1%) was weaker as exporters suffered from the ill effects of recent flows into the local currency but with the index off worst levels amid the slightly brightening picture, while the Hang Seng (+1.1%) reclaimed the 24000 level after shrugging off early indecision following tepid Hong Kong PMI data which showed an improvement although remained in contraction territory for a 31st consecutive month. Finally, 10yr JGBs eked minimal gains amid the lacklustre risk tone in Tokyo and following the tepid Rinban operation by the BoJ which were in the market for a reserved JPY 400bln of JGBs mostly concentrated in 3-5yr maturities.

Top Asian News

- Vedanta Sinks Most Since March Amid Delisting Price Uncertainty

- Yuan Looks Good for 2021 on China Recovery: FX Macro Ranking

- Greentown China Soars to 7-Year High on Big September Sales Gain

- Netflix Wins India Legal Battle Over Rogue Billionaires Series

European equities (Eurostoxx 50 -0.2%) trade with mild losses as US equity futures trimmed losses seen in the wake of President Trump’s decision to pull the plug on COVID stimulus talks until after the election. Note, after the initial announcement, Trump suggested he would be willing to back certain aspects of a broader stimulus package such as USD 25bln for airline payroll support and USD 135bln for the Paycheck Protection Program. This helped provide some reprieve for US futures, whilst markets also continue to assess the post-November election landscape with increased focus on the prospects of a Democratic “Blue Sweep” as recent polling data moves further in favour of former VP Biden. In recent months, the main inference from such an outcome has been centred around the likelihood of a less favourable tax environment for US corporates, however, given the inertia in Congress over the past few weeks, markets could take some solace in the likelihood of a more functional legislature that could pass a sizeable support package and help soothe the concerns raised by Fed Chair Powell yesterday. In Europe, the session hasn’t seen much in the way of out or underperformance across regional bourses as markets await the US entrance to market. From a sectoral standpoint, food & beverage names lead the way higher after Diageo (+1.4%) and Pernod Ricard (+2.6%) were both upgraded at Jefferies. To the downside, travel names such as Tui (-3.6%), easyJet (-4.8%) and IAG (-0.3%) have been hampered by reports in the Guardian noting that the UK decision on introducing COVID-19 testing for international arrivals – which is designed to reduce quarantine times – will not take place until November at the earliest. Individual movers include Tesco (+2.0%) after the Co.’s HY profits rose 28.7% relative to 2019, whilst Dialog Semiconductor (+0.6%) shares are firmer after raising Q3 revenue guidance and noting that improving trends are expected to continue into Q4.

Top European News

- Billionaire Arnault Buys Influence Through Media Deals in France

- It’s Spain, Not Italy, That European Investors Are Worried About

- Norway Reveals Record Withdrawals From $1.1 Trillion Fund

- Tesco’s New CEO Takes Over as Online Shopping Surges in U.K.

In FX, the broader Dollar and Index trade modestly softer in early European hours after US President Trump called off coronavirus stimulus talks until after the elections but is ready to sign a standalone bill for stimulus checks if he is sent one. Thus, DXY has waned off its best levels (93.900) as it drifts lower to test its 21 DMA (93.622) ahead of the 93.500 psychological mark, with the 55 DMA touted at 93.321. Looking ahead, FOMC Minutes could garner attention with regards to QE maturities after Fed’s Mester suggested that the Fed should have the scope to lengthen QE maturities, alongside any meat on the bones on AIT (full primer available on the newsquawk headline feed), albeit fiscal updates are likely to steal the limelight throughout the session. The calendar from a data-standpoint is light, but speakers on the docket include voters Williams (x2), Kashkari and 2021 voter Evans.

- AUD, NZD, CAD – The non-US Dollars are posting varying degrees of gains, with the Aussie outperforming as it retraces some of yesterday’s post-RBA/budget losses, but remains sub-0.7150 against the Dollar, currently at the top of today’s 0.7097-7146 range. The Kiwi meanwhile benefits from the broader Dollar weakness as it re-eyes 0.6600 to the upside (vs. 0.6576 at worst) with the 50 and 21 DMAs seen at 0.6632 and 0.6640 respectively. The Loonie’s gains are hampered by the overnight crude decline, but nonetheless ekes mild gains against the Buck as USD/CAD decline from a high of 1.3340 and dipped below 1.300 to open the door to its 21 DMA at 1.3271 ahead of the 1.3250 psychological mark.

- GBP, EUR, CHF – Modest gains seen across the European currencies as Sterling leads the gains with pertinent newsflow including reports that Chancellor Sunak is mulling new support for businesses impacted by COVID-19, whilst from a Brexit standpoint, EU member states are said to be taking an increasingly hard stance over concessions – with President Macron standing firm on the issue of fisheries. Cable has yielded the 1.2900 handle (vs. low 1.2864). EUR/USD retraces some of yesterday’s losses and resides north of 1.1750 at the time of writing (vs. low 1.1726) as it eyes its 55 DMA (1.1791) ahead of the 1.1800 figure. Levels to the downside include Monday’s low (1.1705) and Friday’s low (1.1694), with today’s OpEx comprising of EUR 750mln rolling off between 1.1740-50. CHF also stands as a beneficiary of the Dollar softness, with USD/CHF remaining below in a tight range 0.9200 (0.9161-84 range), with the 55 DMA seen around 0.9136.

- JPY – The Yen bucks the trend and fails to benefit from the softer Dollar, with some pointing to technical play and after touted stops were triggered around 105.80, with more reported at 106.00+. USD/JPY resides at the top if the current 105.61-106.00 band, and with a notable USD 2.1bln in options scattered between 105.45-106.10 to keep in mind for today’s NY cut.

- EM – EM FX see broad-based Dollar induced gains, with the exception of the Turkish Lira which succumbed to renewed pressure in early EU hours, potentially on heightened geopolitical risk after the Iranian President warned that the Azeri-Armenian conflict could lead to a regional war, whilst Turkey continues to support its ally Azerbaijan. USD/TRY notched a fresh record high ~7.8680 from a low of 7.7800.

In commodities, WTI and Brent front month futures remain under pressure with both benchmarks at/near session lows as markets balance supply and demand side developments. On the demand side, woes of the implications of the resurging cases persist, in turn prompting the EIA to downgrade its 2020 world oil demand growth forecast by 300k BPD to a decline of 8.62mln BPD Y/Y and cut 2021 world oil demand growth forecast by 280k BPD to an increase of 6.25mln BPD Y/Y, with the OPEC and IEA releases due next week. From a supply standpoint, Private Inventory data printed a larger than expected build (+1.0mln bbls vs. Exp. +0.3mln bbls) and markets await confirmation from the EIA which showed similar expectations for the headline figure. (+0.294mln bbls). Sticking with supply, Norway sees some 330k BPD of total production shuttered amid oil and gas strikes, with plans for an escalation on the 10th of October, albeit production at the 470k BPS Johan Sverdrup field is said to be unaffected despite some workers on strike. Over to the Gulf of Mexico, NHC noted that Hurricane Delta could become a Category 4 hurricane again by later Thursday, with weakening expected as it approaches the Gulf Coast. Note, the BSEE yesterday estimated that approximately 29.22% of the current oil production and approximately 8.59% of the natural gas production in the Gulf of Mexico has been shut-in, with the next update expected around 19:00BST/14:00ET. WTI resides sub-40/bbl with the current base at USD 39.63/bbl (vs. high 40.35/bbl), while its Brent counterpart yields the USD 42/bbl mark (vs. high 42.40/bbl), with the current low at USD 41.69/bbl. Elsewhere, spot gold remains below USD 1900/oz and has largely moved at the whim of the Buck in European trade, whilst spot silver outperforms but remains shy of the USD 24/oz mark. LME copper prices meanwhile have ease off best levels but remains in the green, whilst from a fundamental standpoint, some tout the increasing possibility of potential strikes at the Candelaria mine in Chile after the latest wage offer was rejected, whilst ING also cite the petering out of LME copper inventory builds.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -4.8%

- 2pm: FOMC Meeting Minutes

- 3pm: Consumer Credit, est. $14.0b, prior $12.3b

Central Bank Speakers

- 2pm: FOMC Meeting Minutes

- 2pm: Fed’s Williams Moderates Henry Kissinger Discussion

- 2:40pm: Fed’s Kashkari, Bostic, Rosengren to Speak on Racism

- 3pm: Fed’s Williams Speaks on Flexible Average Inflation Targeting

- 4:30pm: Fed’s Evans Discusses the U.S. Economy and Monetary Policy

DB’s Jim Reid concludes the overnight wrap

President Trump once again took control of the headlines yesterday when he tweeted late in the US session that he had instructed White House negotiators to stop further US stimulus discussions with Congressional Democrats until after the election. He argued that Speaker Pelosi was not arguing in “good faith” and that he wants Congress to focus on the Supreme Court nomination of Judge Barrett instead. This came as a surprise after relatively positive headlines from Pelosi and Treasury Secretary Mnuchin earlier in the week, and also represented a reversal in tone given comments late Monday from White House Chief of Staff Meadows, who said “There are a lot of people that continue to hurt, are waiting on stimulus, and the President’s committed to getting a deal done…He wants to make sure we move expeditiously, but also in a fiscally responsible manner.”

The tweet also came just a few hours after Fed Chair Powell’s speech at the NABE’s annual meeting. While not much new information was proffered, Powell made one of his plainest cases for fiscal stimulus yet, saying “the risks of policy intervention are still asymmetric”, and that “the risks of overdoing it seems, for now, to be smaller” compared with the risks of offering too little support. If the current polling at both the national and state level holds, and former Vice President Biden were to win the election in November, fiscal stimulus may indeed come but will have to wait until Q1 of next year when a new government is seated. Even though many observers had attributed a low probability to an agreement prior to the election given the short timeframe and the negotiating distance between the two groups, the President’s comments rippled through markets late in the US session.

The S&P 500 dropped over 2.05% in the last hour and a half of trading after the tweet. By the close the S&P 500 was down -1.40%, with the NASDAQ down slightly more at -1.57%. The VIX volatility index rose +1.5pts to 29.5, the highest level since early September. The news also caused the US Dollar to rise 0.33% intraday to finish the day up +0.19%, just the second gain in the last seven sessions. Yesterday we said that markets were starting to look through the likely lack of short-term stimulus and were instead focusing on the prospect of more stimulus after the increased likelihood of a Democratic clean sweep. The late price action last night suggests otherwise but I would still say that further evidence that this election will result in a definitive result will offset any short term stimulus disappointment.

Overnight President Trump is slightly softening his stance as he called for support for airlines and the Paycheck Protection Program in a Tweet. On individual checks, he tweeted that ‘If I am sent a Stand Alone Bill for Stimulus Checks ($1,200), they will go out to our great people IMMEDIATELY. I am ready to sign right now. Are you listening Nancy?’. He also tweeted that he supports $25bn aid for airlines to support payroll and $135bn for the Paycheck Protection Program aimed at small businesses. This likely indicates that the President is still up for a skinny deal with the Democrats before the election. These tweets have helped S&P 500 futures rally over half a percent from the session lows to trade broadly flat at +0.05%.

Sticking with the US, the House panel draft report on sweeping reforms of the technology sector that we had mentioned yesterday has been proposed overnight. The House antitrust subcommittee recommends the most dramatic proposal to overhaul US competition law in decades, and could lead to the breakup of tech companies if approved by Congress. The findings target four of the biggest US tech companies – Amazon, Google, Facebook, and Apple – describing them as gatekeepers of the digital economy that can use their control over markets to pick winners and losers while also abusing power to snuff out competitive threats. As things stand the report has been largely shunned by the Republicans but could be a marker for the future if we indeed get a Democrats sweep in the election, as polls are leaning towards.

Asian markets are trading mixed this morning with the Nikkei (-0.22%) down while the Hang Seng (+0.46%) is up and India’s Nifty (+0.01%) is broadly flat. In Fx, the US dollar is up a further +0.17% after yesterday’s +0.18% advance. Meanwhile, European futures point to a weaker open after these markets missed the late US dip last night, with the Stoxx 50 -0.50%, FTSE 100 -0.16% and Dax -0.43% all down. Before this the STOXX 600 managed a +0.07% gain yesterday, led by recent laggards Banks (+3.37%) and Travel & Leisure (+2.95%), while pandemic winners like Health Care (-0.96%) and Technology (-0.81%) were the among the biggest decliners.

Back to the US election and though there had been speculation that the second presidential debate on October 15 might not be held depending on the timing of the President’s quarantine, Trump tweeted yesterday that “I am looking forward to the debate on the evening of Thursday, October 15th in Miami. It will be great!”

Speaking of debates, tonight the Vice Presidential debate take place at 21:00 ET between incumbent VP Mike Pence and California Senator Kamala Harris. There’ll be a number of Covid-related changes however, including plexiglass barriers between the candidates and the moderator, while the candidates will now be seated 12 feet apart rather than 7. Like the last debate it’ll be 90 minutes long, though broken down into 9 smaller segments of 10 minutes each. President Trump remains over +8pts behind former Vice President Biden in national polling averages, though recent polls have started to show Biden possibly increasing that lead, notably CNN (+15pt) and WSJ/NBC (+14pts). Pennsylvania, the state where Biden was born and the state that fivethrityeight.com’s model currently calculates has the best chance of being the tipping point of the electoral college, has Biden up by +6.5pts on average.

If you want more insight into the polls, don’t miss the latest DB speaker series invite “Who is going to win the 2020 US Presidential election?” – with US polling experts Amy Walter, National Editor, The Cook Political Report; G. Elliott Morris, data journalist for The Economist and Matthew Luzzetti, Chief DB US Economist. This is on Tuesday, 13 October 2020 at 3pm BST/4pm CET/10am ET, and is a live video call. Register here

On the coronavirus, there were further concerning signs out of Western Europe yesterday as cases continued to rise. Here in the UK a further 14,557cases were reported as cases have remained stubbornly above the 10k mark in recent days. This increase is now evident in hospital admissions too, and in England the numbers in hospital rose to 2,783 yesterday, which is their highest number since late June (though for context still well below the peak above 17k back in April). France reported 10,489 new cases yesterday with the 7 day rolling average rising back above 12,000 for the first time in 8 days. Cases in the Netherlands have risen over 25,000 over the past week, the highest of the pandemic. Elsewhere, Italy reported a further 2,677 cases, and the country’s health minister said that there was consideration over making the use of masks outdoors compulsory. Of the most severely hit first wave countries, Italy has certainly done the best relative job in minimising a second wave. In the US, there continues to be action in New York City to contain the outbreaks. Governor Cuomo has closed businesses and schools in some regions of the city and outlaying suburbs for 14 days, with different levels of restrictions based on distance from the “hotspots”. See the table below for the latest global case numbers. Meanwhile, in a widening out break at the White House, Stephen Miller, a senior adviser to the US President, became the latest White House staffer overnight to test positive for the coronavirus.

On the vaccine front the US Food and Drug Administration notified coronavirus vaccine developers yesterday that it would want at least two months of safety data before the agency would authorize it for emergency use. This requirement would likely push any availability of a US vaccine well past the Nov. 3 elections. Overnight, President Trump has accused the FDA of carrying out a “political hit job” against him by setting new vaccine review guidelines.

Over in the fixed income sphere, there was a further narrowing in sovereign bond spreads between core and periphery in Europe, and by the session’s close, the spread of Italian 10yr yields over bunds had fallen a further -3.4bps to reach its tightest closing level in over 2 years, at 1.28%. Italian BTPs have performed strongly lately, and the country’s 5-year yields actually fell -2.9bps to an all-time low yesterday of 0.163%. Bunds were unchanged. US 10yr Treasury yields fell -4.6bps lower, mostly after Trump’s tweet but are back up +1.3bps this morning.

Sterling had another volatile session yesterday as a number of further headlines on Brexit came through. The initial selloff was sparked by a Bloomberg report which said that the EU was not planning to make any concessions before next week’s summit of EU leaders – which a month ago Prime Minister Johnson had previously set as the deadline for reaching an agreement. According to the report, the EU was prepared to let the talks continue into November or December and call Johnson’s bluff on whether to break off talks and leave without a deal or stay at the negotiating table beyond his self-imposed deadline. Sterling recovered later on however on some more positive Reuters headlines, which said that the talks last week on Brexit were “one of the most positive so far”, and that the two sides were close to an agreement on reciprocal social security rights.

In terms of yesterday’s data, the US trade balance for August showed the country’s trade deficit widened to its largest since 2006, with a $67.1bn deficit. Other data showed that the number of job openings fell in August to 6.493m, which is the first decline since April. Finally in Europe, German factory orders rose by a stronger-than-expected +4.5% in August (vs. +2.8% expected), and the country’s construction PMI fell deeper into contractionary territory with a 45.5 reading.

To the day ahead now, and the highlight will likely be the Vice-Presidential Debate in the US later on. Otherwise, we’ll get the FOMC’s minutes from their September meeting, and hear from the ECB’s Lagarde, Villeroy, and the Fed’s Rosengren, Bostic, Kashkari, Williams and Evans. Finally, the data highlights include August data on German industrial production, Italian retail sales and US consumer credit.

3A/ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED //Hang Sang CLOSED UP 262.21 OR 1.09% /The Nikkei closed DOWN 10.91 POINTS OR 0.05%//Australia’s all ordinaires CLOSED UP 1.22%

/Chinese yuan (ONSHORE) closed /Oil UP TO 39.68 dollars per barrel for WTI and 41.81 for Brent. Stocks in Europe OPENED ALL RED// ONSHORE YUAN CLOSED AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7331 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

CHINA/USA

White House Targets Ant Group, Tencent Payment Systems As Economic Assault On China Continues

As Beijing complains that the WTO that the Trump Administration’s attempt to ban TikTok violates international trade rules, the Trump Administration isn’t slowing down in its economic assault on the Chinese technology industry.

According to media reports, the administration is considering new restrictions on Ant Group and Tencent’s payment systems.

Stocks dumped on the headline, but the gap has filled fast.

By specifically going after the payment systems, the Trump Administration is taking a different approach on trying to curtail Chinese tech firms’ access to American markets and consumers. An American judge has already blocked the administration’s attempt to bar Tencent’s WeChat app from American app stores (while still allowing US companies like Apple to work with WeChat in foreign markets).

4/EUROPEAN AFFAIRS

UK/EU

Boris Johnson is now threatening to walk way from Brexit talks if no deal by the end of next week

(zerohedge)

UK Threatens To “Walk Away” From Brexit Talks If No Deal By End Of Next Week

Prime Minister Boris Johnson has pressed ahead with his Intermarket Bill, calling Brussels’ bluff about its threats to sue London over what many have described as a unilateral violation of an international treaty.

As Brussels presses ahead with a drawn-out and tedious legal action – which will ultimately come to nothing since a decision might not arrive until after the transition period ends Dec. 31 – allowed per the resolution mechanisms hashed out in the withdrawal agreement, Johnson is once again drawing a line in the sand, upping the pressure by declaring Oct. 15 – ie a week from Thursday – as the UK’s deadline for a deal. Otherwise, it will walk away.

“We do need to be in a position where we’re able to provide certainty to businesses as to what the terms of our future trading relationship with EU are going to be, and we do believe that we need to be able to give clarity on whether or not there’s going to be a deal by the 15th of October,” the spokesman said.

The EU insists that it won’t be pressured into concessions, and that they’re also preparing for ‘no deal’ and are prepared to call BoJo’s bluff. Bloomberg reported, citing an anonymous official from No. 10, that BoJo was “serious” about walking away…but anonymous comments like this should probably be taken with a grain of salt.

Meanwhile, Michael Gove, a top official in Johnson’s government, told Parliament that HMG is stepping up preparations for a no-deal scenario when its transition deal with the European Union expires. While the government would prefer a deal with Brussels, it refuses to be “held hostage”.

“No one would be happier than me if we could conclude an agreement, but we have an absolute obligation to ensure that the country is ready in the event that we don’t,” Gove told a parliamentary committee.

Gove added that no-deal planning was being undertaken to ensure “that this country is not held hostage in a negotiation process.”

Meanwhile, In the Republic of Ireland, the only EU member to share a land border with part of the UK, Foreign Minister Simon Coveney warned on Wednesday that it would be difficult to envision a compromise that would satisfy both Ireland and the EU’s other Atlantic member states, along with Britain.

“This is a big obstacle and I don’t think the British government should underestimate the strength of feeling on fishing of many of the Atlantic member states,” he said.

Though as we’ve learned in the past, the mood of Brexit talks can change on a time. Boris Johnson said last week that he was “pretty optimistic” that deal would be struck. However, the last round of formal talks ended without a deal last week. And while both sides insist that they’re committed to finding common grand, many fraught areas of disagreement remain, including the fisheries issue mentioned above. Aside from fisheries, the other main issue for the UK is rules on state subsidies. For more on this, Politico has published a comprehensive guide to what might happen if ‘no deal’ becomes a reality.

British trade minister Liz Truss offered an apt summary of the UK’s negotiating position during an interview Wednesday on BBC radio, where Tess insisted that a deal with the European Union is “do-able”, so long as the bloc remembers where the UK is coming from. “A deal is absolutely do-able. We know the type of deal we want, it’s the deal that Canada has with the EU,” Truss said.

The pound weakened against the dollar Wednesday suggesting that markets are taking Johnson’s threat seriously. To be sure, if we’ve learned anything from the last three years, it’s that both sides need to run out the clock, since both the EU27 and BoJo have a political interest in convincing their electorates that they managed to win hard-fought concessions from the other.

France confirms Turkish military involvement in the Nagorno Karabakh region.

(zerohedge)

France Confirms Turkish ‘Military Involvement’ In Karabakh After NATO Appeal Mocked

Just yesterday NATO Secretary General Jens Stoltenberg called on Turkey to use its “considerable influence to calm tensions” between Armenia and Azerbaijan as fierce fighting continues in the disputed Nagorno-Karabakh breakaway region.

The appeal was widely mocked by commentators in the West as well as in Armenian media, given it’s been well documented since the start of the conflict that Turkey has been a party to the conflict in backing its declared “brother country” Azerbaijan. And of course there’s the historic Armenian Genocide which caused many to laugh at the strange NATO appeal, as if Turkey is somehow ‘neutral’.

France has joined in the controversy over alleged Turkish intervention, as according to the AFP French government sources are now formally charging there’s evidence of Turkish ‘military involvement’ in Karabakh.

This comes nearly a week after French President Emmanuel Macron issued statements suggesting Turkish involvement in transferring Syrian mercenaries to the war theater.

“We now have information which indicates that Syrian fighters from jihadist groups have (transited) through Gaziantep (southeastern Turkey) to reach the Nagorno-Karabakh theatre of operations,” Macron told reporters on arrival at an EU summit last week. “It is a very serious new fact, which changes the situation.”

Macron’s office later said after talks with Russia’s Putin that “They [Russia] also shared their concern regarding the sending of Syrian mercenaries by Turkey to Nagorno-Karabakh,” according to a statement.

Following this, Armenia’s defense ministry had reported one of its fighter jets was downed over Armenian territory after it was fired upon by a Turkish F-16 jet which had taken off from Baku. The legitimacy of the allegation was never backed up by either the Europeans or other international observers. Turkey had adamantly denied claims that the Sept. 29 shootdown had anything to do with a Turkish jet.

Meanwhile the US, France, and Russia have jointly called for an immediate ceasefire and for both sides to come to the negotiating table.

Currently Armenia has reportedly mustered reserve forces and continues sending national troops to the frontlines, where Azerbaijan forces continue shelling cities in the breakaway region of Nagorno-Karabakh.

According to recent Armenian military figures, there are nearly 300 deaths among its armed forces, while casualties among civilians are likely in the hundreds on both sides.

But amid the fog of war the number of casualties has not been regularly reported, especially on the Azeri side.

Putin also expressed “hope” that the Karabakh “tragedy” will end soon. It should be noted that while Turkey has close ties with Muslim majority Azerbaijan, Russia has a military defense pact with Orthodox Christian Armenia, as well as a major military base within its borders.

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Strange!! without real evidence France and Germany are ready to push for more EU sanctions against Russia much to delight of Trump

(zerohedge)

6.Global Issues

CORONAVIRUS UPDATE/USA /GLOBE

Eli Lilly Seeks Emergency FDA Approval For Antiviral; Italy Mandates Masks Outdoors, NFL Outbreak Grows: Live Updates

Summary:

- Italy calls for masks worn outdoors

- Brussels closes bars

- Eli Lilly asks FDA for emergency approval for antiviral

- Patriots Stephen Gilmore tests positive, along with 2 more Titans

* * *

In the face of growing evidence that wearing masks outdoors isn’t an effective strategy for combating the spread of COVID-19 (the CDC, at the behest of the WHO, has acknowledge that aerosol transmission is only a major risk factor in ‘poorly ventilated’ areas), Italy is following through with plans to impose mandatory mask requirements across the country, part of a wave of rollbacks sweeping across Europe as the long-feared fall “second wave” appears to crest.

Italy’s top public health officials imposed the mandatory mask order, the latest in a series of rollbacks in Italy aimed to try and tamp down a resurgence of the virus. Italy’s council of ministers also voted to extend a state of emergency first imposed in March through the end of January, according to ANSA.

Effective immediately, the council also approved a new requirement for Italians to wear masks outdoors whenever they’re near people who do not live together, ANSA added.

The measures arise as Italy’s leaders extend and reshape the country’s emergency measures to account for the resurgence.

But Italy wasn’t alone in adopting new measures on Wednesday. As an outbreak roars in Brussels, the de facto capital of the EU, the Belgian capital decided to reinstate its lockdown conditions, closing all bars immediately for the second time.

Restaurants serving meals at a table can remain open, but bars and drinking in public will be banned until at least Nov. 8. Belgium, which has a surprisingly high mortality rate (the highest in Europe, and second only to Peru globally), has seen an alarming spike not just in new cases but in hospital admissions, which many fear could lead to another surge in deaths.

As infection rates surge in the UK, Prime Minister Boris Johnson’s “localized lockdown” strategy has come under attack from opposition Labour MPs, including Keir Starmer, the party’s new leader. Roughly 25% of Britons are currently living under restrictive virus-related restrictions.