GOLD:$1904.00 UP $1.50

Silver:$24.30 DOWN $0.18 London spot price ( cash market)

your data…

Closing access prices: London spot

i)Gold : $1902.30 LONDON SPOT 4:30 pm

ii)SILVER: $24.29//LONDON SPOT 4:30 pm

DONATE

CLOSING FUTURES PRICES: KEY MONTHS

OCT GOLD: 1902.00 CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: $1.80-0 BACKWARD//

DEC. GOLD $1903.70 CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $0.30/ BACKWARD

CLOSING SILVER FUTURE MONTH

SILVER NOV COMEX CLOSE; $24.27…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : ( 3 CENTS BACKWARD/

SILVER DECEMBER CLOSE: $24.34 1:30 PM SPREAD SPOT/FUTURE DEC. : 4 CENTS PER OZ CONTANGO ( 0 CENTS ABOVE NORMAL) CONTANGO

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving: 14/154

EXCHANGE: COMEX

CONTRACT: OCTOBER 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,902.000000000 USD

INTENT DATE: 10/23/2020 DELIVERY DATE: 10/27/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

099 H DB AG 1

118 H MACQUARIE FUT 7

135 H RAND 1

323 C HSBC 100

332 H STANDARD CHARTE 22

657 C MORGAN STANLEY 15 5

657 H MORGAN STANLEY 129

661 C JP MORGAN 3

661 H JP MORGAN 11

690 C ABN AMRO 5

905 C ADM 9

____________________________________________________________________________________________

TOTAL: 154 154

MONTH TO DATE: 34,326

issued 0

GOLDMAN SACHS STOPPED 0 CONTRACTS.

NUMBER OF NOTICES FILED TODAY FOR OCT. CONTRACT: 154 NOTICE(S) FOR 15400 OZ (.4790 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 34,326 NOTICES FOR 3,432,600 OZ ( 106.768 tonnes)

SILVER//OCTOBER CONTRACT

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 2269 for 11,345,000 oz

MARGIN REQUIREMENTS INCREASE FOR SILVER

BITCOIN MORNING QUOTE $13,163 UP 134

BITCOIN AFTERNOON QUOTE.: $12,984 DOWN 48 DOLLARS .

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

GLD AND SLV INVENTORIES:

WITH GOLD UP $1.50 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

WE HAD A HUGE CHANGE AT THE GLD; 1.77 TONNES WITHDRAWAL

FROM THE GLD

INVENTORY RESTS:

GLD: 1,263.77 TONNES OF GOLD//

WITH SILVER DOWN 18 CENTS TODAY: AND WITH NO SILVER AROUND:

NO CHANGE IN SILVER INVENTORY AT THE SLV//

SLV: 561.194 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A FAIR SIZED 472 CONTRACTS FROM 158,749 UP TO 159,221 AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE GAIN IN OI OCCURRED DESPITE OUR SMALL $0.09 LOSS IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS DUE TO CONSIDERABLE BANKER AND ALGO SHORT COVERING.. COUPLED AGAINST A TINY EXCHANGE FOR PHYSICAL (350 CONTRACTS). WE ALSO HAD ZERO LONG LIQUIDATION, AND A ZERO INCREASE IN SILVER OUNCES STANDING AT THE COMEX FOR OCT. WE HAD A GOOD NET GAIN IN OUR TWO EXCHANGES OF 1105 CONTRACTS (SEE CALCULATIONS BELOW).

WE WERE NOTIFIED THAT WE HAD 415 COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: AS WE HAD THE FOLLOWING ISSUANCE: OCT 0; DEC: 415, MARCH 0 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 415 CONTRACTS. THE BANKERS ARE NOW BEING BITTEN BY THOSE SERIAL FORWARDS (EFP’S CIRCULATING IN LONDON)AS THEY ARE NOW BEING EXERCISED AND COMING BACK TO NEW YORK FOR REDEMPTION OF METAL. THE COST TO SERVICE THESE SERIAL FORWARDS IS HIGH TO OUR BANKERS

HISTORY OF SILVER OZ STANDING AT THE COMEX FOR THE PAST 26 MONTHS.

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

86.470 MILLION OZ FINAL STANDING IN JULY.

6.475 MILLION OZ FINAL STANDING IN AUGUST

55.400 MILLION OZ FINAL STANDING IN SEPT

11.355 MILLION OZ INITIALLY STANDING IN OCT.

FRIDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL $0.09) ).. AND, OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS AS WE HAD A GOOD GAIN IN OUR TWO EXCHANGES (1105) CONTRACTS). NO DOUBT THE GAIN IN OI WAS DUE TO i) HUGE BANKER/ALGO SHORT COVERING. WE ALSO HAD ii) A TINY ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A ZERO GAIN IN SILVER OZ STANDING FOR OCTOBER, iii) FAIR COMEX GAIN AND iv) ZERO LONG LIQUIDATION. YOU CAN BET THE FARM THAT OUR BANKERS ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER..

We have now switched to silver for our spreaders!!

FOR DETAILS ON THE SPREADING EXERCISE HERE IS A BRIEF OUTLINE:

SPREADING OPERATIONS/NOW SWITCHING TO SILVER (WE SWITCH OVER TO GOLD ON NOV 1)

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN SILVER AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF NOV.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT. HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF OCT. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

OCT

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF OCT:

7742 CONTRACTS (FOR 18 TRADING DAY(S) TOTAL 7742CONTRACTS) OR 38.71 MILLION OZ: (AVERAGE PER DAY: 430 CONTRACTS OR 2.150 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF OCT: 38.71 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 5.53% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)*

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,498.24 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EFP 71.15 MILLION OZ.

JULY EFP 133.95 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

AUGUST EFP 127.46 MILLION OZ (EXCHANGE FOR PHYSICALS STARTING TO DECREASE AGAIN)

SEPT EFP 78.360 MILLION OZ (EXCHANGE FOR PHYSICALS DRAMATICALLY FALLING OFF A CLIFF)

OCT EFP 38.71 MILLION OZ (LOOKS LIKE THEY ARE FALLING OFF A CLIFF IN NUMBERS)

RESULT: WE HAD A FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 690, DESPITE OUR $0.09 LOSS IN SILVER PRICING AT THE COMEX ///FRIDAY.…THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 415 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

TODAY WE GAINED A GOOD SIZED 1105 OI CONTRACTS ON THE TWO EXCHANGES(DESPITE OUR $0.09 FALL IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICAL

i.e 415 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A FAIR SIZED INCREASE OF 472 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH OUR $0.09 LOSS IN PRICE OF SILVER/AND A CLOSING PRICE OF $24.58 // FRIDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.797 BILLION OZ TO BE EXACT or 114% of annual global silver production (ex Russia & ex China).

FOR THE NEW OCT DELIVERY MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR nil OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 WAS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 3,497 CONTRACTS TO 557,552 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE FAIR SIZED LOSS IN COMEX OI OCCURRED DESPITE OUR TINY DECREASE IN PRICE OF $0.80 /// COMEX GOLD TRADING// FRIDAY. WE PROBABLY HAD STRONG BANKER/ALGO SHORT COVERING ACCOMPANYING OUR SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS. WE HAD SOME LONG LIQUIDATION AND ANOTHER STRONG INCREASE IN GOLD OUNCES STANDING AT THE COMEX….THIS ALL HAPPENED WITH OUR LOSS IN PRICE OF $0.80. I FEEL THAT DOMINANT FORCE IN CONTRACTION OF OI WAS BANKER SHORT COVERING. THEY ARE TRYING TO “GET OF DODGE” QUICKLY AS THEY FEEL SOMETHING IS “UP”…(MAYBE A SUDDEN REVALUATION IN GOLD?)

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 74//

WE HAD A TINY LOSS OF 597 CONTRACTS (1.856 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED 2900 CONTRACTS:

CONTRACT .; OCT: 0 DEC: 2900; JUNE: 0 ALL OTHER MONTHS ZERO//TOTAL: 2900. The NEW COMEX OI for the gold complex rests at 557,552. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 597 CONTRACTS: 3,497 CONTRACTS INCREASED AT THE COMEX AND 2900 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 596 CONTRACTS OR 1.8656 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2900) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (3497 OI): TOTAL LOSS IN THE TWO EXCHANGES: 597 CONTRACTS. WE NO DOUBT HAD 1) STRONG BANKER SHORT COVERING AND CONSIDERABLE ALGO SHORT COVERING ,2.)ANOTHER STRONG INCREASE STANDING AT THE GOLD COMEX FOR THE FRONT OCT. MONTH TO 108.04 TONNES) 3) TINY LONG LIQUIDATION ;4) FAIR COMEX OI LOSSAND 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL ...ALL OF THIS WAS COUPLED WITH OUR TINY LOSS IN GOLD PRICE TRADING//FRIDAY//$0.80.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

OCT.

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAY(S) IN TONNES: 119.75 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 119.75/3550 x 100% TONNES =3.37% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3,656.52 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES (EFP ISSUANCE EXTREMELY LOW)

JULY TOTAL EFP ISSUANCE; 313.09 TONNES ..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

AUGUST TOTAL EFP ISSUANCE; 150.78 TONNES FINAL (AGAIN: RETREATING IN NUMBERS)

SEPT TOTAL EFP ISSUANCE: 178.49 TONNES (EFP’s AGAIN RISING DUE TO BACKWARDATION/LOWER FUTURE PREMIUMS//THUS LESS COST TO CARRY)

OCT TOTAL EFP ISSUANCE. 119.75 TONNES (LOOKS LIKE THESE ARE DROPPING IN NUMBERS AGAIN)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A SMALL SIZED 472 CONTRACTS FROM 158,749 UP TO 159,221 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE SMALL SIZED GAIN IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) CONSIDERABLE BANKER SHORT COVERING//ALGO SHORT COVERING , 2) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A ZERO INCREASE IN STANDING FOR SILVER AT THE COMEX FOR OCT., AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 415 CONTRACTS..

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

OCT: 0 AND DEC. 415 AND MARCH: 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 415 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 472 CONTRACTS TO THE 415 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD SIZED GAIN OF 887 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 4.435 MILLION OZ, OCCURRED WITH OUR $0.09 LOSS IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED DOWN 26.88 PTS OR 0.82% //Hang Sang CLOSED UP 132.65 PTS OR .54% /The Nikkei closed DOWN 22.25 POINTS OR 0.09%//Australia’s all ordinaires CLOSED DOWN 0.26%

/Chinese yuan (ONSHORE) closed /Oil DOWN TO 39.04 dollars per barrel for WTI and 40.92 for Brent. Stocks in Europe OPENED ALL RED// ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7010. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6975 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

We had 3 kilobar transactions +

ADJUSTMENTS: 3 //

OUT OF BRINKS: DEALER TO CUSTOMER:

i) Brinks: 60,668.937

ii_HSBC: 2501.388

iii) out of Malca: 260,243.100 ox (8100 kilobars)

The front month of OCT registered a total of 564 contracts for a LOSS of 402 contracts. We had 531 notices filed on Friday so we gained A STRONG 129 contracts or 12,900 additional oz will stand for delivery in this active delivery month of October. I wrote this at the beginning of the month:” In gold we have not seen queue jumping start so early in the month. Thus you can bet the farm that throughout October, the total number of gold oz standing will increase from this level.” Seems that I was right on this very important development. We started the month at 95 tonnes and now so far we have 108 tonnes standing!!!!

November LOST 109 contracts to stand at 1735.

NOVEMBER OI NUMBERS ARE NOT CONTRACTING MUCH. WE ARE GOING TO HAVE ANOTHER DANDY DELIVERY FOR GOLD FOR THIS UPCOMING DELIVERY MONTH.

The big December contract LOST 4682 contracts DOWN to 440,264 contracts..

THE BIG STORY AGAIN TODAY IS THE HIGH OI STANDING FOR OCTOBER (108.04 tonnes). GENERALLY OCTOBER IS A POOR DELIVERY MONTH AS MOST INVESTORS PREFER TO SKIP THIS MONTH AND MOVE STRAIGHT TO DECEMBER. IT LOOKS LIKE SOME MAJOR ENTITY(GOLDMAN SACHS) JUST CANNOT WAIT FOR DECEMBER AS THEY ARE MAKING THEIR MOVE ON OCTOBER FOR PHYSICAL METAL. GOLDMAN SACHS ONE OF THE LEADERS OF THE NEW LONDON LME EXCHANGE NEEDS THE GOLD INVENTORY FOR LIQUIDITY AND INITIAL CONTRIBUTION WITH OTHER MAJOR PLAYERS. THE MAJOR DIFFERENCE BETWEEN THIS MONTH AND OTHER MONTHS IS THAT THIS GOLD STANDING IN OCTOBER WILL LEAVE THE COMEX AND HEAD FOR LONDON.

We had 154 notices filed today for 15,400 oz OR .4790 TONNES.

To calculate the INITIAL total number of gold ounces standing for the OCT /2020. contract month, we take the total number of notices filed so far for the month (34,326) x 100 oz , to which we add the difference between the open interest for the front month of OCT (564 CONTRACTS ) minus the number of notices served upon today (154 x 100 oz per contract) equals 3,473,600 OZ OR 108.04 TONNES) the number of ounces standing in this active month of Oct

thus the INITIAL standings for gold for the OCT/2020 contract month:

No of notices filed so far (34,326, x 100 oz +564 OI) for the front month minus the number of notices served upon today (154) x 100 oz which equals 3,473,600 oz standing OR 108.04 TONNES in this active delivery month. This is a HUGE amount for gold standing for a OCT delivery month (a poor active delivery month).

We gained 129 contracts or an additional 12,900 oz will stand on this side of the pond searching for metal.

NEW PLEDGED GOLD: BRINKS

593,649.694 oz NOW PLEDGED SEPT 15.2020/HSBC 18.465 TONNES ( A HUGE INCREASE FROM 10.6)

60,784.803 PLEDGED APRIL 3/2020: SCOTIA/ OCT 23: 1.8906 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

277,934.09 oz (some deleted august 3) JPM 8.644 TONNES

610,238.285 oz pledged June 12/2020 Brinks/ July 2/July 21 19.017 tonnes

67,289.041 oz Pledged August 21/regular account 2.092 tonnes JPM

total pledged gold: 1,609,895.918 oz 50.074 tonnes

total registered, pledged and eligible (customer) gold 37,532,664.459 oz 1,167.42 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1041.08 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

And now for the wild silver comex results

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

221,913.460 oz

Brinks

CNT

|

| Deposits to the Dealer Inventory |

546,552.500 oz

Manfra

|

| Deposits to the Customer Inventory |

2035.000 oz

Delaware

|

| No of oz served today (contracts) |

0

CONTRACT(S)

nil OZ)

|

| No of oz to be served (notices) |

2 contracts

10,000 oz)

|

| Total monthly oz silver served (contracts) | 2269 contracts

11,345,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

https://www.jsmineset.com/2020/10/26/silvers-value-remains-under-lock-and-key/

Silver’s Value Remains Under Lock and Key

Posted October 26th, 2020 at 9:31 AM (CST) by J. Johnson & filed under General Editorial.

Great and Wonderful Monday Morning Folks,

Gold is struggling to go green under Britain’s trading period with the December contract at $1,905.40, up 20 cents and close to the high at $1,907.50 and a low not that far away at $1,892.50. Silver must be super valuable because it’s kept under complete lock and key with its trade at $24.385, down 29 cents after being dipped to $24.145 with the high up at $24.765. The US Dollar is up 17.5 points at 92.94 after it made it up to 93.065 with the low at 92.73. Of course, all this happened before the Comex open, the London close, and after a massive Freudian slip, or a real f-up, by Joe Biden when he said he was assembling the “most extensive voter fraud organization in history”. Come-on-Man, where is your correction, if there is one? Just think what would happen if he made a gaffe like this as a president with a nuclear enemy?

In Venezuela, Gold is now valued at 19,030.18 Bolivar, shaving off 8.19 since Friday morning with Silver’s value now pegged at 243.545, proving a bigger price purge as the metal loses 5.094 in Bolivar value. Argentina’s Peso price for Gold is now at 148,800.05 showing a 429.97 A-Peso reduction with Silver being dragged down to 1,904.00 A-Peso’s reducing its value by 37.48. Turkey’s currency is the only one allowing a price rise with Gold gaining 104.46 T-Lira with the last trade at 15,356.45, yet Silver still “isn’t allowed” a price rise with its last trade at 196.488, down 1.942 T-Lira from Friday’s close.

October Silver’s Delivery Demands have had no additional purchases since last Wednesday with the count now at 2 and once again with no Volume up on the board so far today. This would be an ideal time for Mr. Resolute to pop in a quarter million-ounce order since the delivery boys have nothing else to do but wait, after they delivered 2 contracts leaving 2 orders on hold for at least another day. It must be really hard to pick which set of 1,000-ounce bars, brought in from all those new Comex smelters, to give to those last standing orders. Even though no physical purchases have shown up for Comex Silver, the papers are, as another 649 short contracts got added bringing the Overall Open Interest to 159,440 shorts against the physicals.

October Gold’s Delivery Demands now has 564 fully paid for contracts waiting for receipts and with a Volume of 84 up on the board with a trading range between $1,897.80 and $1,893.50 with the last buy at $1,897.60, down $4.40. Friday’s full day of activity happened in between $1,913.30 and $1,896.20 with the last swap at $1,902, a gain of 90 cents that had a total of 287 swaps, helping to reduce the demand count by 402 that may have gotten receipts somewhere. Gold’s Overall Open Interest lost 3,445 paper contracts, bringing the count to 557,787 Overnighters. How can the OI drop in Gold when the demands continue, with no new orders in Silver, yet it’s paper count rises?

Today Judge Amy Coney Barrett should be elected as the next SCOTUS, after Sunday’s successful procedural vote. We are now seeing the last set of data blockers that need to be removed to get the information out to the people so they can see what has been going on inside and away from prying eyes. These appointed and not elected people, have been intentionally sitting on data that would prove either the hoax was Russian or Democratic but will not release anything. Just like that former NYSD Geoffrey Berman ‘because he refused to drop Prince Andrew from the Epstein Investigation. Now President Trump promises he will ‘immediately’ fire FBI Director Christopher Wray and CIA Director Gina Haspel, along with Defense Secretary Mark Esper for doing nothing but sitting on data that should have been released over a year ago. If Trump was truly guilty, this data would have been used instead of Christopher Steele’s Fake Dossiers four years ago, so what is it they are intentionally sitting on? Could it be another Weiner or Biden laptop full of evidence?

Still we sit with physical precious metals, while all this crap gets played out. Even though margins have been raised 2 times within a month, it will not stop the physical buyers from buying, it will only keep small speculators away from the arena where the biggest profits are to be made because of leverage and control. If you trade stocks or commodities, God Bless You and Your Strength! If you hold physicals, give a prayer to those that trade against the proven central manipulators, keep that smile on your face and enjoy the ride. As always …

Stay Strong!

Jeremiah Johnson

More J.Johnson content is available with purchase of a JSMineset subscription.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

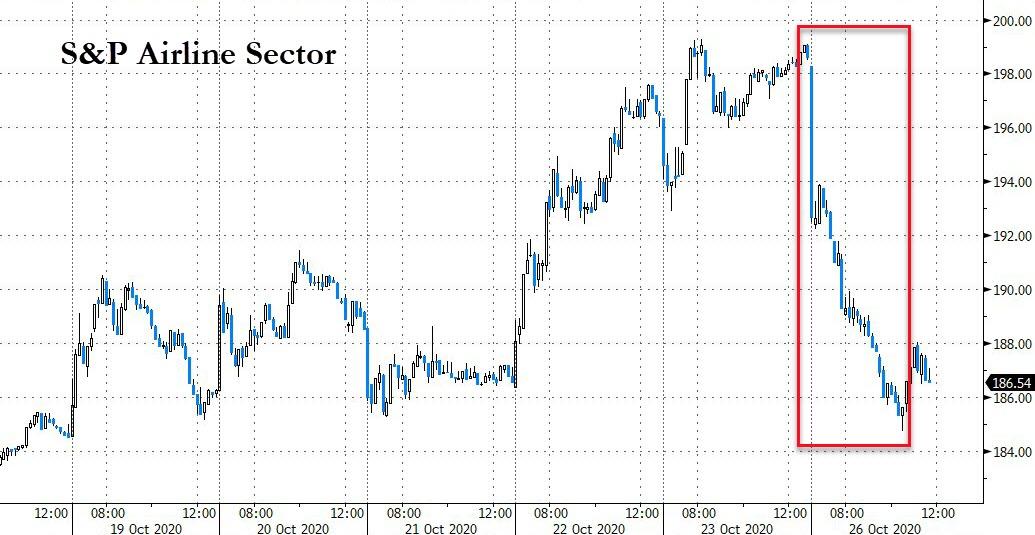

Futures Tumble, European Tech Stocks Plunge Amid Surging Virus Cases, Reflation Trade Fears

US equity futures, European tech stocks and global shares were hit hard on Monday as surging coronavirus cases in Europe (over the weekend, Spain announced a national curfew) and the United States clouded the global economic outlook, while sliding odds of a “Blue Wave” according to online bettor PredictIt sparked fresh doubt in the reflation trade; meanwhile China’s leaders meet to ponder the future of the world’s 2nd largest economy. Emini futures dropped as much as 1.1% in early Monday trading.

Boeing slid 1.3% in pre-market trading after China announced it will impose unspecified sanctions on the defense unit of Boeing, Lockheed Martin and Raytheon after the U.S. approved $1.8 billion in arms sales to Taiwan last week.

Even though by now it’s abundantly clear no deal is coming before the election, some traders remained focused on the prospect of a U.S. economic aid package, even as time runs out to finish a deal by the November election after months of wrangling. House Speaker Nancy Pelosi said the burden is on President Donald Trump to push forward on stimulus talks, while Treasury Secretary Steven Mnuchin said there’s been significant progress, but blamed Pelosi for holding up an agreement.

“The current mood in the market is bracing and non committal,” said Peter Rosenstreich, head of market strategy at Swissquote Bank SA. “The concern around the Covid-19 pandemic and U.S. fiscal stimulus is dominating the market. Everyone is talking up the Blue Wave, but behind the scenes ‘what if 2016 repeats?’ is keeping investors cautious.”

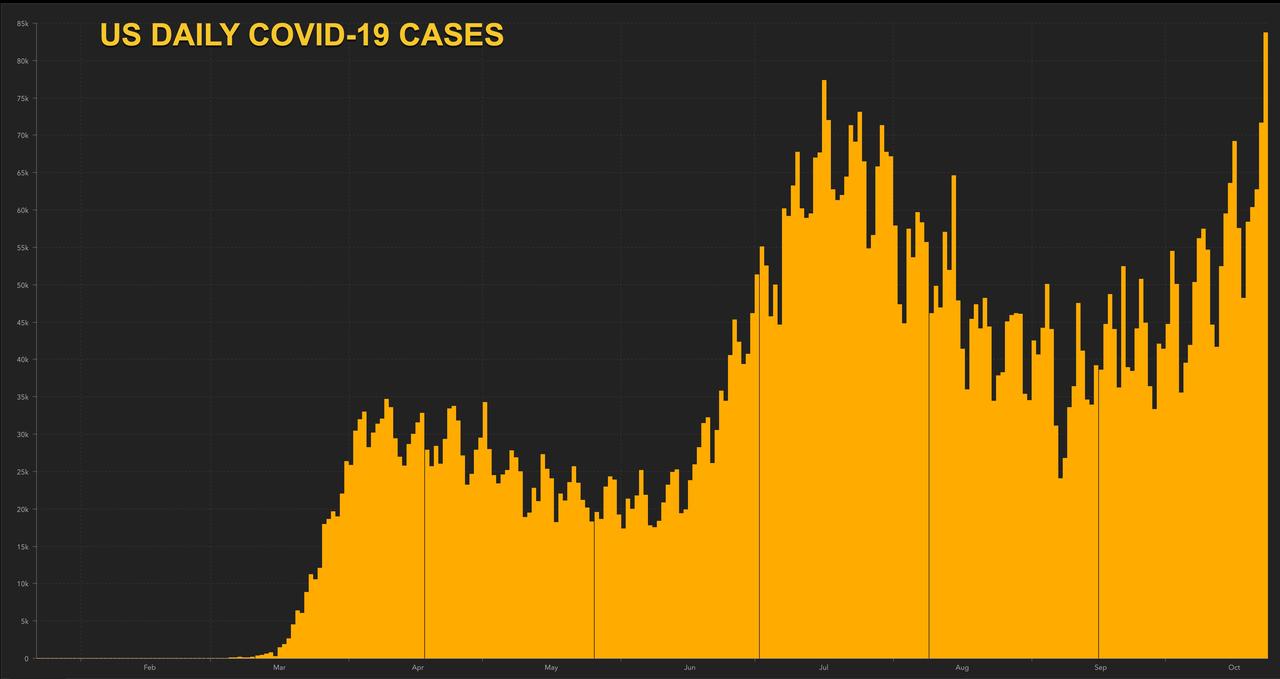

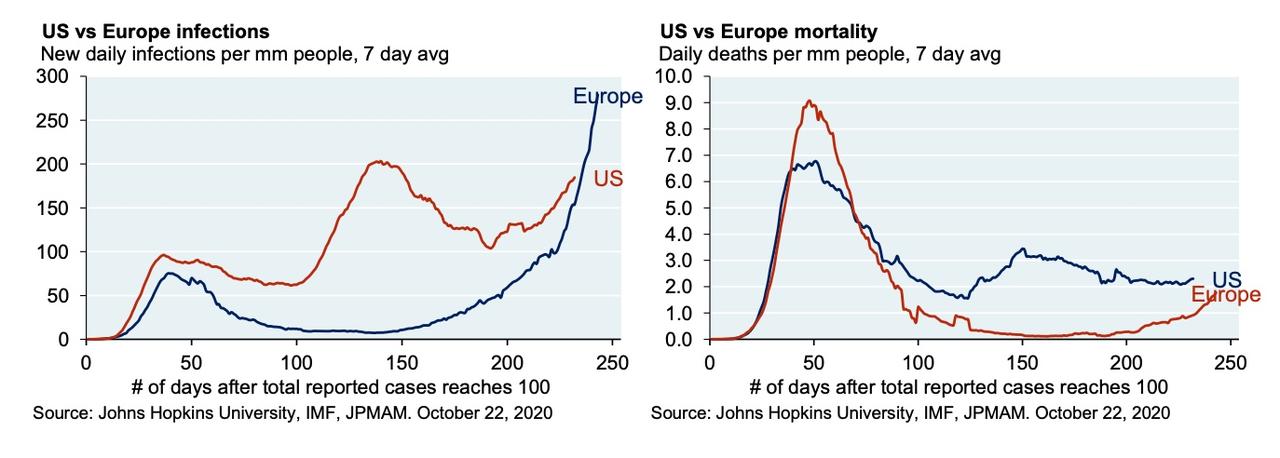

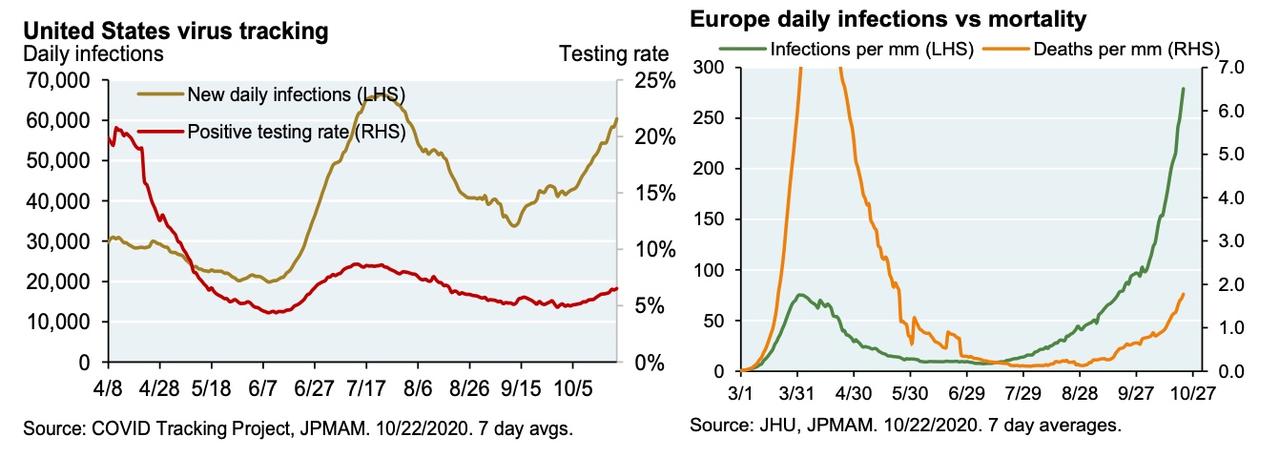

On the covid front, the United States saw its highest ever number of new COVID-19 cases in the past two days, while France also set case records and Spain announced a state of emergency. The World Health Organization’s director general said some countries in the northern hemisphere are facing a “dangerous moment” after U.S. infections hit a record for the second day. European countries are also tightening restrictions on business. Spain has announced a nationwide curfew and Italy introduced the strongest measures since May. That combined with no clear progress on a U.S. stimulus package and caution ahead of the election to drag the MSCI world equity index down 0.2%.

“The decreasing likelihood of U.S. fiscal stimulus pre-election, possibly even pre year-end, as well as worsening virus numbers and increasing lockdown measures all seem to be taking the shine of what was a rather complacent market view of the outlook,” said James Athey, investment director at Aberdeen Standard Investments.

In Europe, the Euro STOXX 600 shed 0.8%, let by Europe’s Stoxx Tech Index which fell as much as 6.3%, its biggest one-day loss since March, as SAP’s outlook cut weighs on software peers and IT services stocks.

Shares of SAP – which accounts for more than 20% of the index – plunged as much as 21%, its worst day since January 1999 after the software company cut its 2020 outlook saying that pandemic will hurt business through mid-2021. Analysts saw this as a sign that a recovery from pandemic-induced weakness had likely been pushed out, and were particularly disappointed that SAP pushed the timeline for its mid-term goals out to 2025 from 2023, with the targets lower than expectations.

The plunge in SAP shares dragged the German DAX index as much as 2.7% lower to a three-month low. Milan’s blue-chip index sank 1.2% as new curbs on public venues overshadowed Friday’s positive news that ratings agency S&P Global upgraded the nation’s sovereign outlook to stable from negative. Bayer AG climbed 2.8% after agreeing to buy U.S. biotech company Asklepios BioPharmaceutical Inc. for as much as $4 billion, bolstering its pharma division with experimental gene therapies before patents expire on some key drugs.

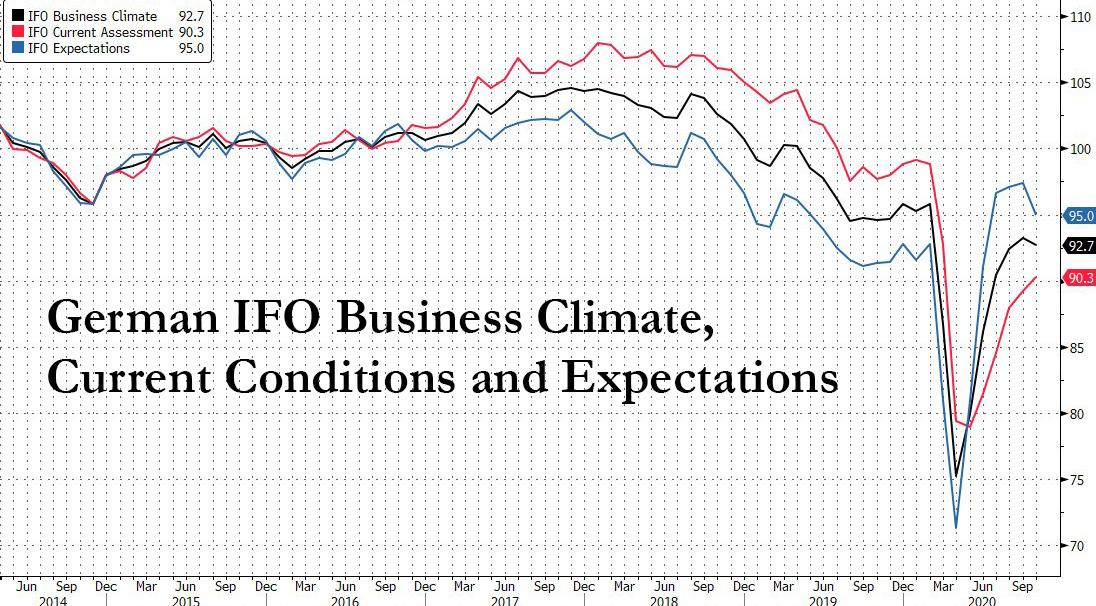

Not helping the dour European mood was the latest German IFO data whose expectations component came at 95.0, below the 96.0 expected and down from 97.7 last month, prompting fears of a double dip for Europe’s largest economy.

Earlier in the session, Asian shares dropped with MSCI’s index of Asia-Pacific shares outside Japan shedding 0.2%. Japan’s Nikkei finished 1% lower, and South Korea’s main index lost 0.7%. Chinese blue chips shed 0.6% as the country’s leaders met to chart the nation’s economic course for 2021-2025, balancing growth with reforms amid an uncertain global outlook and deepening

tensions with the United States.

In rates, as markets increasingly price in the likelihood of a Democratic president and Congress and resulting rise in government spending and borrowing, U.S. 10-year Treasury yields hit their highest since early June last week at 0.8720%. However, the risk off mood pushed 10Y yields down to 0.81% on Monday. Treasuries outperformed in the early European session, outperforming bunds and gilts as U.S. stock futures eased from Friday’s levels. Yields lower by 0.5bp to 3bp across the curve in a bull-flattening move, tightening 2s10s, 5s30s by 2.1bp and 1bp; 10- year yields around 0.813% outperforming bunds by ~4bp and gilts by 2.5bp. Italian bonds outperform in Europe session after S&P’s outlook revision to stable on Friday: the benchmark 10-year yield dropped 9 basis points to 0.68% and the spread over German bonds tightened to 126 bps.

“We have raised the probability of a Democratic sweep, already our base case, from 40% to just over 50% and have increased our expectation of Biden to win from 65% to 75%,” NatWest Markets analysts said in a note. “We see steeper U.S. yield curves and a weaker USD as likely to prevail in our base case.”

In FX, the standout was the Turkey lira which for the first time ever weakened through 8 per dollar for the first time. The country’s central bank rattled investors last week by unexpectedly keeping rates on hold, and geopolitical risks have sapped interest in Turkish assets.

Elsewhere, surging coronavirus cases sent investors to the safety of the dollar after it fell broadly last week; as a result the dollar rose against most G-10 peers as waning prospects for a near-term U.S. stimulus deal and rising coronavirus infections fueled haven bids. The euro extended its Asia session decline in early European trading, closing in on $1.18; bunds rise on haven demand as coronavirus case surge sends stocks lower. The Canadian dollar and Norway’s krone led the decline among Group-of-10 currencies as oil prices fell. The pound swung between losses and gains on the back of a broadly stronger dollar mixed with positive signals emerging from Brexit negotiations, with the U.K. government indicating optimism about signing a deal. Trade talks between Britain and the European Union will continue in London until the middle of this week.

In commodities, gold was flat just above $1,900. Oil prices extended last week’s losses as the prospect of increased supply and resurgent coronavirus infections worried investors. Brent crude was down 3% at $40.52 a barrel. U.S. West Texas Intermediate (WTI) dropped 3.2% to $38.57.

Looking ahead, we find a packed week for monetary policy decisions, Canada’s and Japan’s central banks are expected to hold fire for now, while the market assumes the European Central Bank will sound cautious on inflation and growth even if it skips a further easing. Data due out Thursday is forecast to show a record, consumer-led 31.9% rebound in U.S. economic output in the third quarter, after the second’s quarter’s historic collapse. Analysts at Westpac noted such a bounce would still leave 2020 GDP around 4% below last year’s, with business investment still lagging badly.

Market Snapshot

- S&P 500 futures down 1.1% to 3,415.50

- STOXX Europe 600 down 1.1% to 358.60

- MXAP down 0.3% to 175.62

- MXAPJ down 0.2% to 583.81

- Nikkei down 0.09% to 23,494.34

- Topix down 0.4% to 1,618.98

- Hang Seng Index up 0.5% to 24,918.78

- Shanghai Composite down 0.8% to 3,251.12

- Sensex down 1.7% to 39,991.53

- Australia S&P/ASX 200 down 0.2% to 6,155.63

- Kospi down 0.7% to 2,343.91

- German 10Y yield fell 1.0 bps to -0.584%

- Euro down 0.3% to $1.1823

- Italian 10Y yield fell 4.5 bps to 0.555%

- Spanish 10Y yield fell 3.1 bps to 0.164%

- Brent futures down 2.9% to $40.58/bbl

- Gold spot down 0.3% to $1,897.06

- U.S. Dollar Index up 0.2% to 92.99

Top Overnight News from Bloomberg

- Rates traders are starting to question the big short position that’s built up in long-maturity Treasuries on the expectation of a Democratic sweep in next month’s U.S. elections. In the market for options on Treasury futures, trades emerged in the past week that wager against a leap in volatility or a major breakout in yields heading into year-end

- German Ifo Institute’s business climate index dropped for the first time in six months, just as coronavirus infections in the country reached new records. The reading of 92.7 in October was lower than the median forecast of economists in a Bloomberg survey, and compares to 93.2 the previous month. A gauge of expectations also deteriorated

- China will impose unspecified sanctions on the defense unit of Boeing Co., Lockheed Martin Corp., and Raytheon Technologies Corp. after the U.S. approved $1.8 billion in arms sales to Taiwan last week. The sanctions will be imposed “in order to uphold national interests,” Chinese Foreign Ministry spokesman Zhao Lijian told reporters Monday in Beijing.

- House Speaker Nancy Pelosi said she’s waiting for the another counteroffer Monday from Treasury Secretary Steven Mnuchin, as she and White House Chief of Staff Mark Meadows accused each other of “moving the goalposts” in negotiations

- Amy Coney Barrett is on the cusp of confirmation, with the Senate ready to vote Monday night to elevate her to the Supreme Court a week before the presidential election and create a 6-3 conservative majority on the court

- Investors wondering how China plans to evolve its financial markets in the coming years need look no further than the commentary from the weekend’s Bund Summit in Shanghai for guidance. PBOC Governor Yi Gang said that promoting broader use of the yuan will continue alongside the opening of financial markets

- Europe took a step closer to the stringent restrictions imposed during the initial wave of the coronavirus pandemic as leaders struggle regain control of the spread

- Libya is set to restart the last of its major oil fields following a ceasefire in its civil war, a milestone for the OPEC member that’s been largely offline since January

A quick look at global markets courtesy of NewsSquawk

Asian equity markets began the week lacklustre and US equity futures were pressured with risk appetite subdued by the deteriorating COVID-19 situation in Europe after France and Italy reported record surges in daily infections, which prompted Italy to announce tougher restrictions and Spain also declared a state of emergency, as well as a nationwide curfew. ASX 200 (-0.2%) was initially buoyed by M&A news including an approach by Coca-Cola European Partners to acquire Coca-Cola Amatil which saw shares in the latter surge by more than 15% and Link Administration received a revised takeover proposal, although gains in the index were eventually offset by weakness in the commodity-related sectors and with financials on edge after Westpac flagged a AUD 1.2bln hit to H2 earnings. Nikkei 225 (-0.1%) was indecisive with price action choppy around the 23,500 level amid a mixed currency and the KOSPI (-0.7%) failed to hold onto opening gains in the absence of any significant follow-through to the early nostalgic lift in Samsung Group shares after the death of its Chairman Lee Kun-hee. Shanghai Comp. (-0.8%) was the worst performer amid commodity-related weakness, with demand also subdued by the absence of Hong Kong participants due to a holiday closure and tentativeness as China begins its 4-day plenum where policymakers will hammer out details of the next 5-year plan. Finally, 10yr JGBs traded higher as they made their back towards the 152.00 focal point with support provided by the cautious mood and with the BoJ in the market for a total of JPY 920bln of JGBs.

Top Asian News

- Amazon Set For Face-Off With Ambani For India Retail Dominance

- Lira Weakens Past 8 per Dollar as Currency Rout Deepens

- Hyundai Motor Posts Loss on Engine-Problem Costs; Sales Rise

- Australia Joins Global IPO Mania With Best Month in 2020

European equities (Eurostoxx 50 -1.5%) have kicked the week off with heavy losses as the region contends with the deteriorating COVID-19 situation in Europe after France and Italy reported record surges in daily infections, which prompted Italy to announce tougher restrictions whilst Spain declared a state of emergency and a nationwide curfew. The German DAX (-2%) is the laggard in Europe amid losses in SAP (-18.3%) who carry a 10.2% weighting in the index. Losses for the German tech heavyweight followed Q3 earnings in which the Co. reported declines in revenues and operating profits, cut guidance for 2020 and removed its forecast that profitability would expand over the medium-term. As such, the Stoxx 600 tech sector (in which it carries a 24% weighting) is the clear laggard in Europe. Elsewhere from a sectoral standpoint, health care names are bucking the trend and are modestly firmer on the session with AstraZeneca (+1.0%) shares supported by news that its COVID-19 vaccine is said to have triggered protective antibodies and T-cells in the elderly according to early results which offers hope to the most vulnerable. The upside in AstraZeneca, allied with gains in UK banks (Natwest +1.1%, HSBC +0.5%, Lloyds +0.4%, Barclays +0.5%) has helped stem the losses in the FTSE 100 (-0.2%) with support seen for the domestic banking sector in the wake of reports noting that UK regulators are reportedly mulling plans to permit banks to begin paying out dividends again next year. In contrast, in the Eurozone, regulators that were previously in favour of lifting the current ban on dividends are reportedly now more concerned and are looking at dividend caps as a compromise. In terms of M&A activity, Bayer (+0.9%) are to acquire Asklepios Biopharmaceutical for USD 2bln in up-front payments with a potential further USD 2bln in milestone payments. Finally, Rolls Royce (-2.5%) are lower on the session amid source reports in The Times suggesting that major investors in the Co. will only put their support behind its emergency fundraising bid if a massive overhaul of the “sprawling” business is undertaken.

Top European News

- Italy’s Bonds Surge After S&P Holds Off From Downgrading NationEuropean Stocks Fall as SAP Leads DAX Down After Cutting Outlook

In FX, the Dollar is back on a firmer footing and in demand as a safe-haven even though the US is far from immune to the 2nd pandemic waves sweeping through many countries and the upcoming election poses uncertainty alongside the ongoing stimulus stalemate. However, aversion is taking a toll on the more cyclical, activity and commodity currencies, with the DXY revisiting 93.000+ territory within 93.069-92.784 parameters as a result ahead of the national activity index, new home sales data and the Dallas Fed manufacturing business survey.

- CAD/NOK/EUR/CHF – Another retreat in crude prices and the more severe coronavirus resurgence in Spain, Italy, France and Germany to name just a few Eurozone member states, is weighing on the Loonie, Norwegian Krona and Euro in particular. As such, Usd/Cad has rebounded further from recent lows towards 1.3200 in the run up to Canada’s by-elections, Eur/Nok has retested 11.0000+ resistance and Eur/Usd has retreated from 1.1850+ through decent option expiry interest between 1.1840-35 (1 bn). Note also, Ifo metrics were softer than expected to keep the single currency pressured, while the Franc will have noted a rise in Swiss bank sight deposits as it straddles 0.9050 again.

- JPY/GBP/AUD – Also weaker vs the Greenback as the Yen trades at the lower end of a 104.97-66 band, Sterling recoils from 1.3060+ to probe support around 1.3000 in the form of the 50 DMA (1.3012) and 10 DMA (1.2996), and Aussie wanes from just shy of 0.7150 despite Australia looking to lift more of its anti-COVID measures intime for Xmas.

- NZD – The relative G10 outperformer, albeit largely due to cross flows than anything NZ specific, as the Kiwi pivots 1.0650 against its Antipodean counterpart and hovers just below 0.6700 vs its rival awaiting trade data for some independent direction.

- EM – Broad losses due to the downturn in risk appetite impacting oil and other commodities, but with Lira losses exacerbated by heightened diplomatic tensions as Usd/Try finally clears the 8.0000 level that was being defended. Ahead, CBRT minutes and the latest inflation report may explain why the Bank opted to shock markets and stand pat last Thursday, while an improvement in manufacturing confidence has hardly helped the worsening mood with the pair elevated between 8.0658-7.9628 extremes.

In commodities, WTI and Brent futures are subdued this morning following the substantial losses seen in the equity space alongside poor earnings from European heavyweight SAP (see equity section). At present, WTI and Brent are lower by just shy of USD 1.0/bbl but similarly to the equity space have lifted off lows most recently with a number of factors in play for the crude complex this morning. On the demand side, the rising COVID-19 cases and new restrictions implemented in areas such as Italy and France have served to bring existing concerns back to the forefront; while updates from Lufthansa that additional craft are to be grounded for the Winter period will be an area of concern. Moving to the supply side where factors are both supporting and hindering the crude complex; firstly, Tropical Storm Zeta is expected to become a Hurricane later on today and has already prompted BP to commence shut-in procedures within the Gulf of Mexico. However, updates out of Libya indicate that the force majeures on all ports and fields have now been lifted after El Feel field reopened this morning following such action for the Ran Lanuf and Es Sider ports on the weekend. As such, the NOC believes production will surpass the 1mln BPD mark in around 4-weeks’ time. Moving to metals, spot gold is essentially flat on the day but has been attempting to move higher throughout the morning given the general risk-tone. However, any potential shine for the metal has been halted by the USD’s upside which has seen the DXY eclipse 93.00. Elsewhere, steel output for the year from China is forecast to eclipse 1bln/T which would be a 3-5% YY increase according to the CISA industry association. An increase which is explained by increased consumption globally as well as support domestic gov’t policies for China’s steel industry.

US Event Calendar

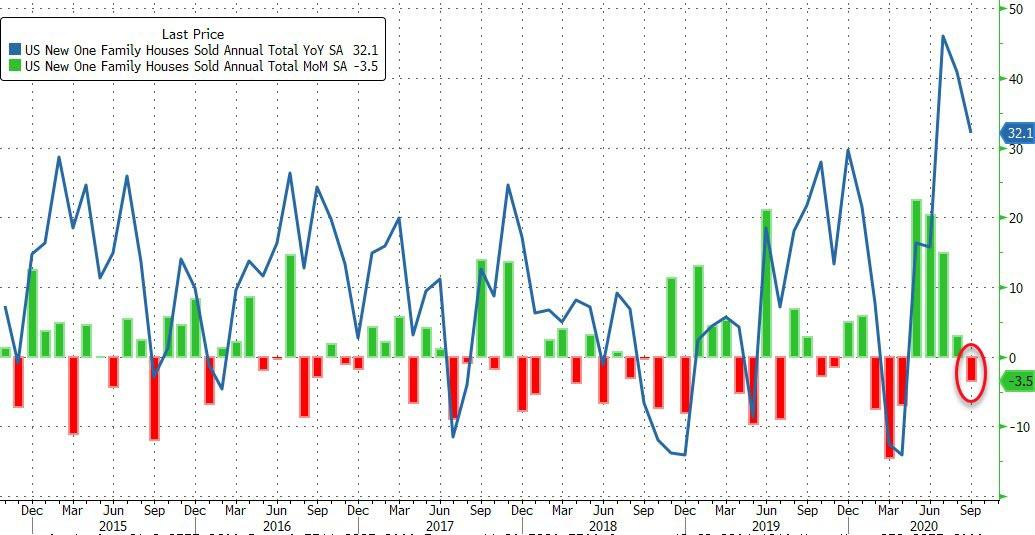

- 8:30am: Chicago Fed Nat Activity Index, est. 0.6, prior 0.8

- 10am: New Home Sales, est. 1.02m, prior 1.01m; New Home Sales MoM, est. 1.34%, prior 4.8%

- 10:30am: Dallas Fed Manf. Activity, est. 13.3, prior 13.6

DB’s Jim Reid concludes the overnight wrap

We’re into the business end of the US Election now with tomorrow marking the one week countdown to Election Day. Over the weekend there hasn’t been much of a shift in the polling averages with the main polling sites still showing a fairly consistent lead for Biden with the FiveThirtyEight average at 9.2pts and the RealClearPolitics average at 8.0pts. The same goes for the Senate race where FiveThirtyEight give the Democrats a 73% chance of winning control. Expect the market to remain fixated on these polls as the days tick down from here however.

It’ll be hard to knock the spotlight too far from Congress this week too with the daily stimulus deal headlines unlikely to show any sign of tiring just yet. The weekend has seen both sides trade barbs – Pelosi and Meadows accusing each other of “moving the goalposts” in interviews yesterday – with time as good as up for a pre-election deal. Pelosi did hint at a pandemic relief plan this week however our US economists think the odds of a much larger deal with the White House before year end are fairly slim with the start of next year a more realistic timeframe. On that, at the back end of last week the team published a detailed report looking at what fiscal prospects mean for the US economic outlook next, with unsurprisingly a Democratic clean sweep providing the most upside. See the full report here.

In other news, the latest on the virus includes the US reaching a record number of daily cases at just over 85k over the weekend, including Marc Short, US Vice President Pence’s chief of staff. While that raises the risk of the virus spreading to the Vice President’s inner circle, Pence has been confirmed negative and will continue to campaign this week. In Europe we’ve seen Italy introduce the strongest virus restrictions since the end of a national lockdown in May as the country reported a daily record of cases while Spain approved a new national curfew. France also reported a record number of infections at over 52k yesterday with the positive test rate increasing to 17% from 16%. On the vaccine front there was good news as the FT reported that AstraZeneca’s vaccine candidate produced a robust immune response in elderly people while J&J said that first batches of its vaccine could be available for emergency use as soon as January. J&J is set to resume its US trials after they had been paused earlier due to safety concerns.

In terms of markets this morning, the latest virus news and stimulus headlines has seen S&P 500 futures trade down -0.59%. Asian bourses have also started the week on the back foot with the Nikkei (-0.12%), Shanghai Comp (-0.72%), Kopsi (-0.42%) and ASX (-0.13%) all down. Hong Kong markets are closed for a holiday. In keeping with the risk off, the US dollar index is up +0.16% overnight while yields on 10y USTs are down -2.7bps. Elsewhere, oil is down just under -2%.

In other weekend news, the latest on Brexit is that EU Chief Negotiator Michel Barnier will remain in London for discussions through October 28 according to Bloomberg after the UK government indicated optimism about signing a deal. Elsewhere, China is rethinking its yuan internationalization strategy and a senior central bank official called for more proactive approach with policies to support markets, including improving bilateral currency swap agreements.

Looking ahead to the rest of this week, the other highlights include the ECB and BoJ meetings on Thursday. With regards to the former, while our European economists expect the policy stance to be left unchanged, they do expect the ECB to warn of growing downside risks amid an already weak outlook for inflation, which will open the door to an easing of policy in December. By then, there’ll be more information on the status of the pandemic, and the ECB staff will have updated their macroeconomic projections, including the publication of the first estimates for growth and inflation for 2023. See our economists’ full preview here. For the BoJ, our economists also expect no policy stance change in light of the slow-but steady economic recovery and stable exchange rate.

Elsewhere, datawise next week we’ll get a first look at Q3 GDP in the US and Europe and given the record contractions seen in Q2, it’s quite possible that the Q3 numbers will be among the best ever quarterly performances since records began. Our US economists forecast an eye watering +33.8% as an example which, if realised, would be by far the strongest quarterly growth number since comparative data starts back in the 1940s. Clearly a lot of this is a mechanical bounceback from the shutdowns and it’s worth reminding that economic activity is still expected to remain well below its pre-Covid peak for some time. Finally, if that wasn’t enough, it’s another big week for earnings too with 184 S&P 500 companies and 94 STOXX 600 companies reporting. The former includes tech heavyweights like Microsoft, Apple, Facebook, Amazon and Alphabet.

Quickly recapping last week now, and politics on either side of the Atlantic remained in focus, particularly the US election. Expectations of fiscal stimulus in the US and moderately improving economic data helped 10-year yields rise globally. US equities pulled back slightly even as the rise in rates helped cyclical industries, especially banks (+3.17%). The S&P 500 fell back -0.53% (+0.34% Friday) as technology stocks lagged and the NASDAQ declined a greater -1.06% (+0.37% Friday). It was the S&P 500’s first weekly decline since September. Equities in Europe generally underperformed as countries are seeing rising coronavirus caseloads and restrictions are being enacted across the continent. The Stoxx 600 ended the week -1.36% lower (+0.62% Friday), with the DAX (-2.04%) falling back further.

Again the story was the sharp rise in sovereign bond yields as growth prospects improved. US 10yr Treasury yields rose +9.7bps (-1.3bps Friday) to finish at 0.843%. It was the largest one week rise in US rates since mid-August and they now sit just below the local highs of June. The US 2-year-10-year yield curve steepened +8.5bps to its steepest weekly level since February of 2018. 10yr Gilt yields rose by +9.8bps (-0.4bps Friday) to 0.28%, while 10yr Bund yields were up +4.8bps (-0.8bps Friday) to -0.57%. Peripheral sovereign debt yields rose as well with Italian (+10.7bps), Spanish (+7.1bps), Portuguese (+6.0bps) and Greek (+13.7bps) 10yr bond yields all significantly.

In terms of data released on Friday, the highlight was the flash PMIs from around the globe. The euro zone flash October PMIs were stronger than expected. Euro Area manufacturing PMIs came in at 54.4 (vs. 53.0 expected) while services, at 46.2, missed (vs. 47.0 expected). Germany manufacturing was 58.0, 3.0 points above expectations on a recovering export business. France saw a sharper decline as the flash services reading of 46.5, down one point from September and the lowest reading in five months. In the US, the Markit PMIs came in largely in line with expectations – with manufacturing at 53.3 (vs. 53.5 expected) and services a touch stronger at 56.0 (vs. 54.6 expected).

3A/ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED DOWN 26.88 PTS OR 0.82% //Hang Sang CLOSED UP 132.65 PTS OR .54% /The Nikkei closed DOWN 22.25 POINTS OR 0.09%//Australia’s all ordinaires CLOSED DOWN 0.26%

/Chinese yuan (ONSHORE) closed /Oil DOWN TO 39.04 dollars per barrel for WTI and 40.92 for Brent. Stocks in Europe OPENED ALL RED// ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7010. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6975 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

CHINA/COVID 19

China not out of the woods yet as they scramble to suppress its biggest COVID 19 outbreak in months

(zerohedge)

Chinese Authorities Scramble To Suppress Biggest COVID-19 Outbreak In Months

Chinese authorities are scrambling to suppress yet another outbreak in far-flung Xinjiang after a 17-year-old garment factory worker tested positive.

Health authorities reported 137 new cases on Sunday, all of which were confirmed in Xinjiang Province, making this by far the largest new outbreak since the Spring. In keeping with Beijing’s prescribed “wartime posture” approach, authorities last night launched a mass-testing campaign to try and test all 4.75 million residents in and around the city of Kashgar. A couple of weeks ago, authorities pulled off a similarly massive testing drive in Qingdao, a city in the eastern Shangdong Province.

Thanks to sweeping smartphone-based mass surveillance/case-tracking, scapegoating and outright suppression of case numbers and deaths, China has managed to drive COVID-19 case numbers to almost zero. In Wuhan, locals travel to bars and concerts, sometimes, taking rapid COVID-19 tests, with their infection status logged on their smartphones in a way that can be examined by bouncers at the door.

To further confuse the international community, along with the Chinese public, China’s national health authorities have divided case classifications into imported vs. domestic and asymptomatic vs symptomatic.

Here’s how the ‘official’ tally of cases has evolved in recent weeks.

The new cases, all classified as asymptomatic, were linked to a factory in Shufu county where the 17-year-old girl and her parents worked, according to the Xinjiang health commission, which held a press briefing on Sunday following an exhaustive investigation of the source of the outbreak by Beijing’s NHC.

As of Sunday afternoon more than 2.8 million samples had been collected in the area and the rest would be completed within two days, the city government said in a statement.

Kashgar, near the country’s borders with Pakistan, Afghanistan, Tajikistan and Kyrgyzstan, is the cultural home of China’s Turkic Muslim ethnic Uighurs, a group that the CCP has relentlessly pressed into reeducation camps and concentration camps to force them to accept the country’s governing Communist ideology.The crackdown as provoked international outbreak, and a barrage of sanctions imposed by the US on officials and companies involved with the mass-detention program.

end

CHINA/USA

Beijing slaps sanctions on Raytheon and Lockheed in retaliation for Taiwan arms sales last month

(zerohedge)

Beijing Slaps Sanctions On Raytheon, Lockheed & Boeing In Retaliation For Taiwan Arms Sales

As President Trump and VP Mike Pence (recent COVID-19 infections be damned) fan out across the country for a last-minute pre-Election Day push to get out the vote, Beijing is adding to its long-promised retaliation for TikTok, Hong Kong, the Xinjiang sanctions, all President Trump’s COVID-19-related China bashing and – most importantly – Taiwan.

After Beijing sanctioned Lockheed Martin over its involvement in “Torpedoes for Taiwan”, the CCP is following up with more economic attacks on American defense contractors, guaranteeing that the Chinese response, and its attendant economic impact, will be elevated to an important talking point and – more importantly – another risk factor for already-uneasy markets, struggling to digest the political uncertainty combined with new record numbers of COVID-19 cases in the US and Europe.

According to Reuters, Beijing has decided to impose sanctions on Boeing’s defense unit, Raytheon and (again) Lockheed. The news was announced by Ministry of Foreign Affairs spokesman Zhao Lijian. He didn’t elaborate on what the sanctions will entail.

The sanctions come as the State Department approves the sale of three weapons systems to Taiwan, including sensors, missiles and artillery worth some $1.8 billion as the Trump Administration throws caution to the wind and goes all-in on beefing up Taiwan’s defense capabilities, even as Beijing adopts increasingly belligerent rhetoric about the “red line” that is Taiwan.

“To safeguard our national interests, China decided to take necessary measures and levy sanctions on U.S. companies such as Lockheed Martin, Boeing Defence, and Raytheon, and those individuals and companies who behaved badly in the process of the arms sales,” he said.”

Though it’s not the “just war” China has promised, it’s possible that US equities could take a hit if we hear more concrete details from the Chinese. Markets wobbled after China announced its last round of sanctions against Lockheed, though whatever Beijing did, it doesn’t look like it had much immediate impact on Lockheed’s bottom line, according to its latest earnings report, released roughly a week ago.

CHINA/USA

The war between China and the uSA escalates as Beijing demands information on finances and on staff members

(zerohedge)

Beijing Demands Info On Finances, Staff From 6 American Media Outlets Operating In China

Beijing is following up its announcement of impending sanctions to be levied against a trio of American defense contractors by ordering six American media companies to deliver detailed information about their finances, staff and other details.

The urgent demand – which gives the media companies a week to comply – follows another tit-for-tat attempt by Washington to crack down on Chinese media by labeling six entities as “foreign missions”, which could create problems for their employees working from the US.

This isn’t the first attack on American journalists. Back in March, the CCP kicked out all the most critical western journos from the NYT, WSJ and Washington Post, plus others.

However, some of the media orgs being targeted by Beijing have never been targeted before. Overall, the list includes mostly liberal-leaning outlets. ABC, LATimes, Minnesota Public Radio, Bureau of National Affairs, Newsweek and Feature Story News.

Ironically, all of these outlets typically promote a media narrative at odds – sometimes even directly hostile to – President Trump’s agenda.

Readers can find the full statement below.

Beijing’s Foreign Ministry claimed the decision was “entirely necessary” in retaliation for the Trump Administration’s latest effort.

The Foreign Ministry immediately called on Washington to “immediately change course, undo the damage, and stop its political oppression and arbitrary restrictions on Chinese media organizations” or face additional countermeasures.

end

4/EUROPEAN AFFAIRS

CORONAVIRUS UPDATE/ITALY/THE GLOBE/SATURDAY

Italy Plans Return To Partial Lockdown As Cases Hit Fresh Record: Live Updates

Summary:

- Italy release draft plan for return to semi-lockdown

- US tops 80k cases for first time

- Global daily cases top 500k

- New record reported in Portugal

- Austria sees record new cases for 4th day

- Brussels imposes new restrictions for 14 days

- Spain, Italy weighing stricter measures to fight outbreak

* * *

Update (1530ET): Italy’s PM has apparently leaked a draft of the new partial lockdown that’s expected to be implemented on Sunday, while Italy reported record new daily coronavirus cases of 19,644, roughly equal to yesterday.

According to the draft decree, the Italian government will impose closures and strict curfews, with most restaurants and nonessential businesses set to close at 1800 local time.

According to JHU, the five worst-hit countries in the world right now are all in Europe: the Czech Republic, Belgium, the Netherlands, Switzerland and France. All five have seen the number of new cases surge since the beginning of October.

* * *

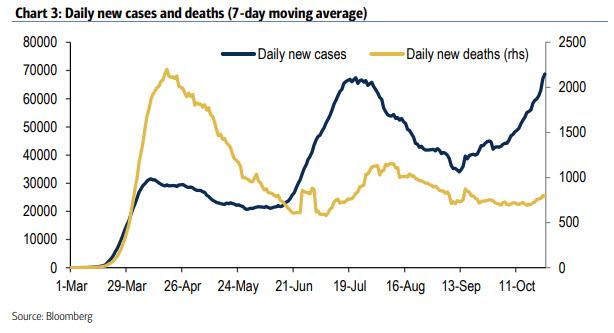

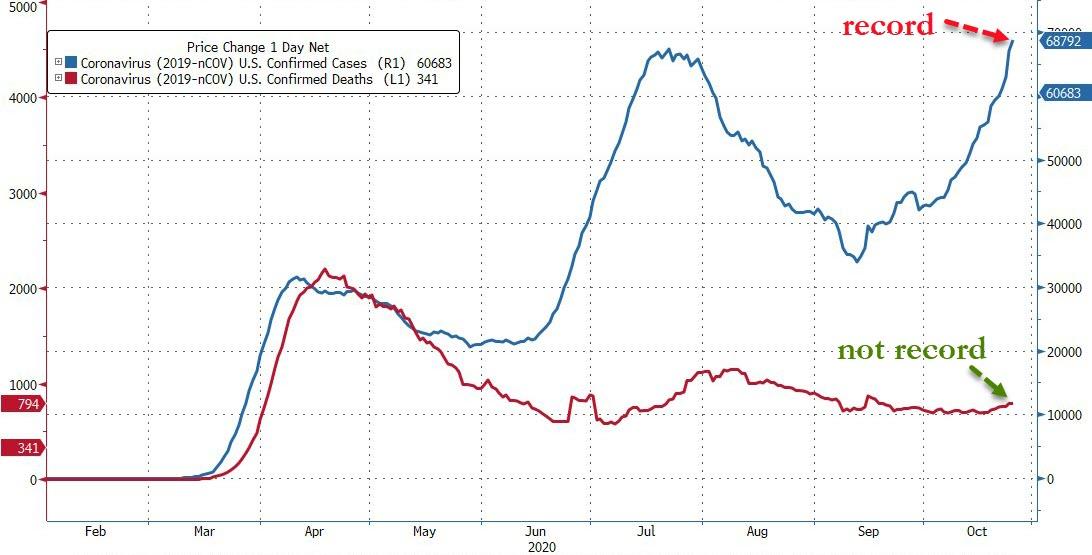

The US smashed its previous daily record on Friday when it reported 83,304 new cases, exceeding its prior July 29 peak with just 2 weeks to go before election day.

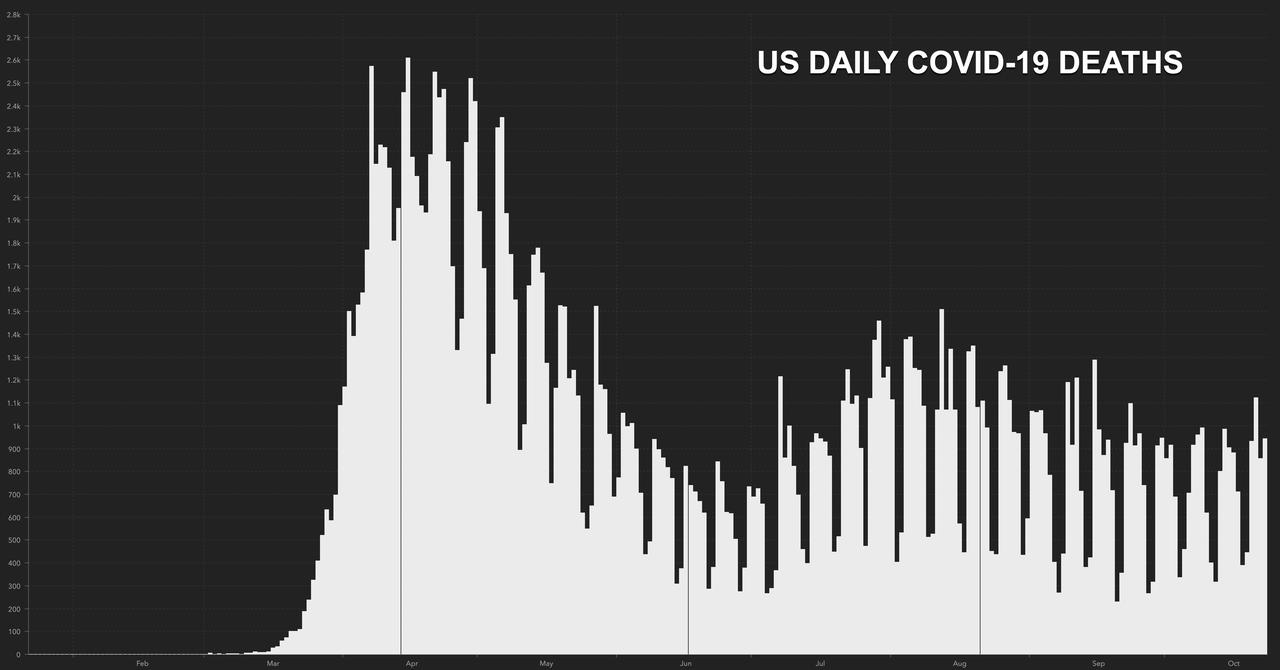

The new cases brought the US tally to 8,499,132 since the start of the pandemic, while another 945 new deaths reported on Friday once again swung the 7-day average for fatalities in the US to its highest level in at least a month. It brought the US death toll to 224,058, as hospitalizations across the US reach their highest levels in months, as we noted last night.

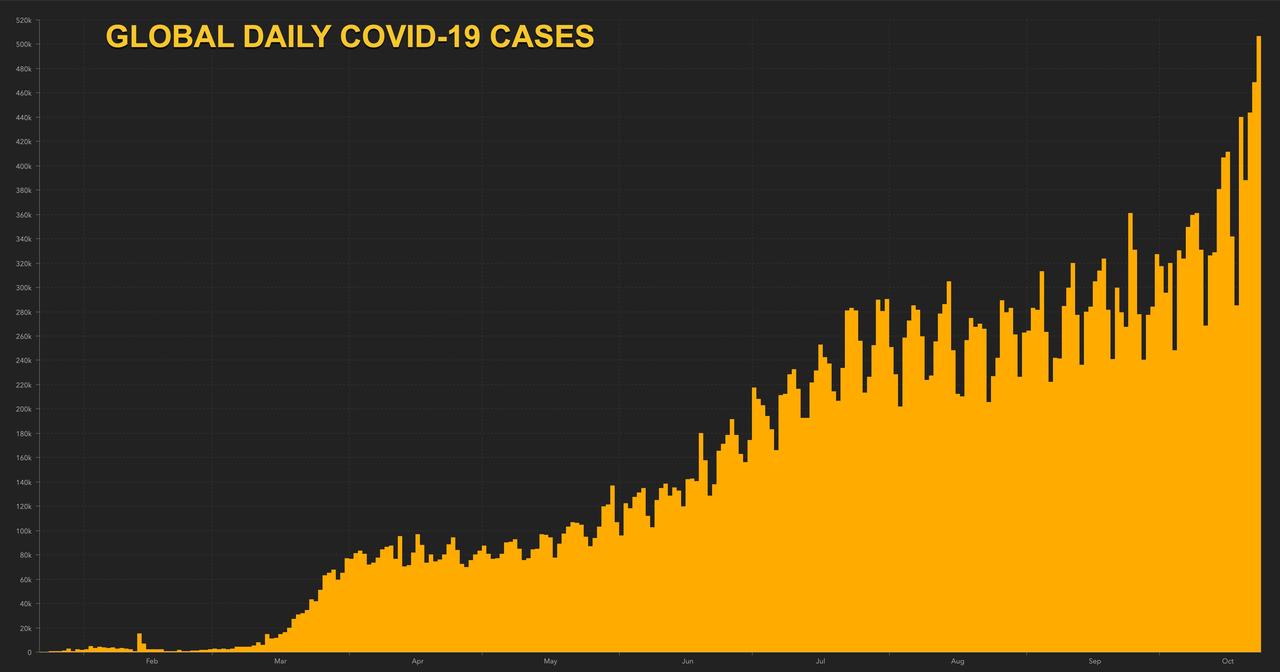

Globally, cases exceeded 42.3 million and deaths exceeded 1.1. million, as the number of new cases reported globally topped 500,000 for the first time yesterday, driven by rising case numbers in the US, Europe and Russia.

While an outbreak across the Midwest and Mountain West has seen states like Wisconsin, Ohio, Michigan and Montana report multiple record numbers within the span of a week as their total new confirmed cases climbed to record highs, states across Europe have suffered rising hospitalizations, cases, positivity rates and deaths.

As cases have risen, positivity rates have continued to climb across the US.

In Central Europe, Austria reported record new case numbers on Saturday for the fourth day in a row. Slovenia reported a record 1,963 new cases with an all-time high positivity rate of 27.9%. Another 19 deaths, a record for the tiny Alpine state with a population of 2.1 million, were reported, bringing the total death toll to 235. Poland also suffered its deadliest day yet, with 179 deaths, and 13,628 new cases.

In Germany, Chancellor Angela Merkel said the pandemic has worsened as a growing number of regional health authorities are struggling to track infections, Merkel said. “We’re not powerless against the virus,” she said. “Our behavior decides how strong and how fast it spreads.”

Of course, a growing body of evidence suggests that the worse an outbreak gets, the harder it is to trace contacts.

In Spain, Prime Minister Pedro Sanchez is reportedly holding an extraordinary cabinet meeting on Sunday to declare a national “state of alarm”. The Italian government is also expected to approve new COVID-19 restrictions on Sunday as new cases topped 19k on Friday, the highest number yet.

Source: Bloomberg

Brussels and the five Walloon provinces have 14-day incidence rates that are 2x those of the Flemish provinces in the north of Belgium, ranging from 1,262 per 100,000 in Luxembourg to 2,100 per 100,000 in Liege.

Portugal on Saturday reported yet another record, with 3,669 new cases in a day, more than the prior record of 3,270 reported on Thursday. The new cases took Portugal’s total to 116,109. The number of patients in the ICU rose by 23 to 221, still below the peak of 271 ICU patients from April.

END

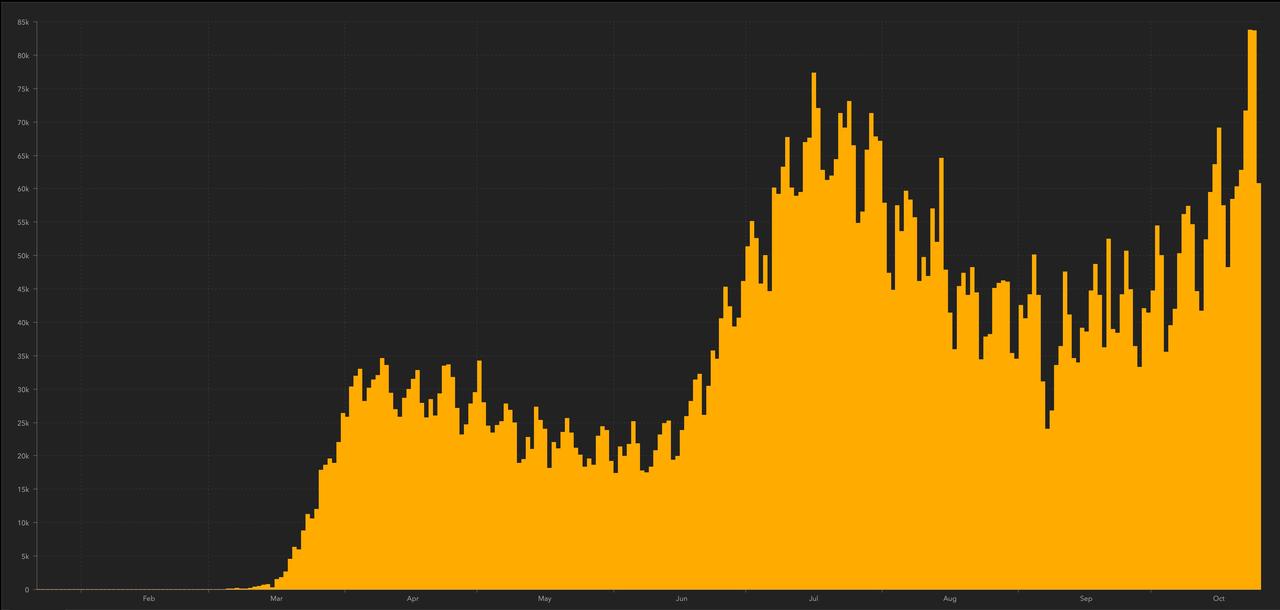

CORONAVIRUS UPDATE/MONDAY

Average New US COVID-19 Cases Hits New Record As Hospitals Run Out Of Space: Live Updates

Summary:

- US sees 7-day average for cases hit new record

- Hospitals across US near capacity

- Utah hospitals ask Gov to approve new triage plan

- French official warns France seeing 100k new cases per day

- Malaysia extends lockdown

- Hong Kong focuses COVID efforts on public transit

- UK approves new rapid test

- AstraZeneca trial data shows vaccine effective on elderly

* * *