GOLD:$1910.20 UP $6.20

Silver:$24.48 UP $0.18 London spot price ( cash market)

your data…

Closing access prices: London spot

i)Gold : $1908.00 LONDON SPOT 4:30 pm

ii)SILVER: $24.36//LONDON SPOT 4:30 pm

DONATE

CLOSING FUTURES PRICES: KEY MONTHS

OCT GOLD: 1904.40 CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: $5.80- BACKWARD//

NOV GOLD 1908.20 CLOSE 1:30 PM SPREAD SPOT/FUTURE NOV:$2.00 BACKWARD

DEC. GOLD $1912.00 CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $1.80/ CONTANGO// $1.20 BELOW CONTANGO

CLOSING SILVER FUTURE MONTH

SILVER NOV COMEX CLOSE; $24.50…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : ( 2 CENTS CONTANGO/

SILVER DECEMBER CLOSE: $24.54 1:30 PM SPREAD SPOT/FUTURE DEC. : 6 CENTS PER OZ CONTANGO ( 3 CENTS ABOVE NORMAL) CONTANGO

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving:4/99

EXCHANGE: COMEX

CONTRACT: OCTOBER 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,902.700000000 USD

INTENT DATE: 10/26/2020 DELIVERY DATE: 10/28/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

118 H MACQUARIE FUT 2

323 C HSBC 84

332 H STANDARD CHARTE 7

657 C MORGAN STANLEY 14 1

657 H MORGAN STANLEY 64

661 H JP MORGAN 4

690 C ABN AMRO 4 1

800 C MAREX SPEC 1

905 C ADM 16

____________________________________________________________________________________________

TOTAL: 99 99

MONTH TO DATE: 34,425

issued 0

GOLDMAN SACHS STOPPED 0 CONTRACTS.

NUMBER OF NOTICES FILED TODAY FOR OCT. CONTRACT: 99 NOTICE(S) FOR 9900 OZ (.3079 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 34,425 NOTICES FOR 3,442,500 OZ ( 107.076 tonnes)

SILVER//OCTOBER CONTRACT

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 2269 for 11,345,000 oz

MARGIN REQUIREMENTS INCREASE FOR SILVER

BITCOIN MORNING QUOTE $13,404 UP 343

BITCOIN AFTERNOON QUOTE.: $13,664 UP 612 DOLLARS .

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

GLD AND SLV INVENTORIES:

WITH GOLD UP $6.20 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

INVENTORY RESTS:

GLD: 1,263.80 TONNES OF GOLD//

WITH SILVER UP 18 CENTS TODAY: AND WITH NO SILVER AROUND:

NO CHANGE IN SILVER INVENTORY AT THE SLV//

SLV: 561.194 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A GOOD SIZED 862 CONTRACTS FROM 159,221 UP TO 160,083 AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE GAIN IN OI OCCURRED DESPITE OUR CONSIDERABLE $0.18 LOSS IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS DUE TO CONSIDERABLE BANKER AND ALGO SHORT COVERING.. COUPLED AGAINST A STRONG EXCHANGE FOR PHYSICAL (1345 CONTRACTS). WE ALSO HAD ZERO LONG LIQUIDATION, AND A ZERO INCREASE IN SILVER OUNCES STANDING AT THE COMEX FOR OCT. WE HAD A GOOD NET GAIN IN OUR TWO EXCHANGES OF 2298 CONTRACTS (SEE CALCULATIONS BELOW).

WE WERE NOTIFIED THAT WE HAD 1345 COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: AS WE HAD THE FOLLOWING ISSUANCE: OCT 0; DEC: 1345, MARCH 0 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1345 CONTRACTS. THE BANKERS ARE NOW BEING BITTEN BY THOSE SERIAL FORWARDS (EFP’S CIRCULATING IN LONDON)AS THEY ARE NOW BEING EXERCISED AND COMING BACK TO NEW YORK FOR REDEMPTION OF METAL. THE COST TO SERVICE THESE SERIAL FORWARDS IS HIGH TO OUR BANKERS

HISTORY OF SILVER OZ STANDING AT THE COMEX FOR THE PAST 26 MONTHS.

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

86.470 MILLION OZ FINAL STANDING IN JULY.

6.475 MILLION OZ FINAL STANDING IN AUGUST

55.400 MILLION OZ FINAL STANDING IN SEPT

11.355 MILLION OZ INITIALLY STANDING IN OCT.

MONDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL $0.18) ).. AND, OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS AS WE HAD A STRONG GAIN IN OUR TWO EXCHANGES (2298) CONTRACTS). NO DOUBT THE GAIN IN OI WAS DUE TO i) HUGE BANKER/ALGO SHORT COVERING. WE ALSO HAD ii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A ZERO GAIN IN SILVER OZ STANDING FOR OCTOBER, iii) GOOD COMEX GAIN AND iv) ZERO LONG LIQUIDATION. YOU CAN BET THE FARM THAT OUR BANKERS ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER..

We have now switched to silver for our spreaders!!

FOR DETAILS ON THE SPREADING EXERCISE HERE IS A BRIEF OUTLINE:

SPREADING OPERATIONS/NOW SWITCHING TO SILVER (WE SWITCH OVER TO GOLD ON NOV 1)

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN SILVER AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF NOV.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT. HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF OCT. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

OCT

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF OCT:

9087 CONTRACTS (FOR 19 TRADING DAY(S) TOTAL 9087CONTRACTS) OR 45.43 MILLION OZ: (AVERAGE PER DAY: 478 CONTRACTS OR 2.390 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF OCT: 45.43 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 6.49% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)*

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,504.965 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EFP 71.15 MILLION OZ.

JULY EFP 133.95 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

AUGUST EFP 127.46 MILLION OZ (EXCHANGE FOR PHYSICALS STARTING TO DECREASE AGAIN)

SEPT EFP 78.360 MILLION OZ (EXCHANGE FOR PHYSICALS DRAMATICALLY FALLING OFF A CLIFF)

OCT EFP 45.43 MILLION OZ (LOOKS LIKE THEY ARE FALLING OFF A CLIFF IN NUMBERS)

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 953, DESPITE OUR $0.18 LOSS IN SILVER PRICING AT THE COMEX ///MONDAY.…THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1345 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. YOU WILL RECALL THAT DECEMBER SILVER WAS BACKWARD TO THE FRONT MONTH AND THAT ALLOWED THE CROOKS TO ISSUE EFP’S AS THE COST TO CARRY IS MUCH LESS. HOWEVER THEY ARE ALSO EXPOSED TO LONDONERS ATTACKING THE FRONT MONTH OF DECEMBER AND ASKING FOR DELIVERY.

TODAY WE GAINED A STRONG SIZED 2207 OI CONTRACTS ON THE TWO EXCHANGES(DESPITE OUR $0.18 FALL IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICAL

i.e 1345 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A GOOD SIZED INCREASE OF 862 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH OUR $0.18 LOSS IN PRICE OF SILVER/AND A CLOSING PRICE OF $24.40 // MONDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.797 BILLION OZ TO BE EXACT or 114% of annual global silver production (ex Russia & ex China).

FOR THE NEW OCT DELIVERY MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR nil OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 WAS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A TINY SIZED 398 CONTRACTS TO 557,154 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE TINY SIZED LOSS IN COMEX OI OCCURRED DESPITE OUR INCREASE IN PRICE OF $1.50 /// COMEX GOLD TRADING// MONDAY. WE PROBABLY HAD STRONG BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED ISSUANCE OF EXCHANGE FOR PHYSICALS. WE HAD ZERO LONG LIQUIDATION AND ANOTHER STRONG INCREASE IN GOLD OUNCES STANDING AT THE COMEX….THIS ALL HAPPENED WITH OUR GAIN IN PRICE OF $1.50. I FEEL THAT DOMINANT FORCE IN CONTRACTION OF OI WAS BANKER SHORT COVERING. THEY ARE TRYING TO “GET OF DODGE” QUICKLY AS THEY FEEL SOMETHING IS “UP”…(MAYBE A SUDDEN REVALUATION IN GOLD?)

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 74//

WE HAD A FAIR SIZED GAIN OF 2740 CONTRACTS (8.522 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED 3138 CONTRACTS:

CONTRACT .; OCT: 0 DEC: 3138; JUNE: 0 ALL OTHER MONTHS ZERO//TOTAL: 2740. The NEW COMEX OI for the gold complex rests at 557,154. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2740 CONTRACTS: 398 CONTRACTS DECREASED AT THE COMEX AND 3138 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 2740 CONTRACTS OR 8.522 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3138) ACCOMPANYING THE TINY SIZED LOSS IN COMEX OI (398 OI): TOTAL GAIN IN THE TWO EXCHANGES: 2740 CONTRACTS. WE NO DOUBT HAD 1) STRONG BANKER SHORT COVERING AND CONSIDERABLE ALGO SHORT COVERING ,2.)ANOTHER STRONG INCREASE STANDING AT THE GOLD COMEX FOR THE FRONT OCT. MONTH TO 108.32 TONNES) 3) ZERO LONG LIQUIDATION ;4) TINY COMEX OI LOSSAND 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL ...ALL OF THIS WAS COUPLED WITH OUR SMALL GAIN IN GOLD PRICE TRADING//MONDAY//$1.50.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

OCT.

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAY(S) IN TONNES: 129.51 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 129.51/3550 x 100% TONNES =3.70% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3,666.28 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES (EFP ISSUANCE EXTREMELY LOW)

JULY TOTAL EFP ISSUANCE; 313.09 TONNES ..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

AUGUST TOTAL EFP ISSUANCE; 150.78 TONNES FINAL (AGAIN: RETREATING IN NUMBERS)

SEPT TOTAL EFP ISSUANCE: 178.49 TONNES (EFP’s AGAIN RISING DUE TO BACKWARDATION/LOWER FUTURE PREMIUMS//THUS LESS COST TO CARRY)

OCT TOTAL EFP ISSUANCE. 129.51 TONNES (LOOKS LIKE THESE ARE DROPPING IN NUMBERS AGAIN)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GOOD SIZED 862 CONTRACTS FROM 159,221 UP TO 160,083 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE GOOD SIZED GAIN IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) CONSIDERABLE BANKER SHORT COVERING//ALGO SHORT COVERING , 2) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A ZERO INCREASE IN STANDING FOR SILVER AT THE COMEX FOR OCT., AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 1345 CONTRACTS..

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

OCT: 0 AND DEC. 1345 AND MARCH: 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1345 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 862 CONTRACTS TO THE 1345 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG SIZED GAIN OF 2207 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 11.035 MILLION OZ, OCCURRED DESPITE OUR $0.18 LOSS IN PRICE///

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 3.20 PTS OR .10% //Hang Sang CLOSED DOWN 131.59 PTS OR .53% /The Nikkei closed DOWN 155.22 POINTS OR 0.61%//Australia’s all ordinaires CLOSED DOWN 1.73%

/Chinese yuan (ONSHORE) closed /Oil DOWN TO 38.89 dollars per barrel for WTI and 40.70 for Brent. Stocks in Europe OPENED ALL RED// ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7065. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6948 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

We had 1 kilobar transactions +

ADJUSTMENTS: 1 //

OUT OF BRINKS: DEALER TO CUSTOMER:

i)Loomis 175,731.900 oz (5466 kilobars

The front month of OCT registered a total of 499 contracts for a LOSS of 65 contracts. We had 154 notices filed on Monday so we gained A STRONG 89 contracts or 8,900 additional oz will stand for delivery in this active delivery month of October. I wrote this at the beginning of the month:” In gold we have not seen queue jumping start so early in the month. Thus you can bet the farm that throughout October, the total number of gold oz standing will increase from this level.” Seems that I was right on this very important development. We started the month at 95 tonnes and now so far we have 108.3 tonnes standing!!!!

November LOST ONLY 133 contracts to stand at 1603.

NOVEMBER OI NUMBERS ARE NOT CONTRACTING MUCH. WE ARE GOING TO HAVE ANOTHER DANDY DELIVERY FOR GOLD FOR THIS UPCOMING DELIVERY MONTH.

The big December contract LOST 629 contracts DOWN to 439,099 contracts..

THE BIG STORY AGAIN TODAY IS THE HIGH OI STANDING FOR OCTOBER (108.320 tonnes). GENERALLY OCTOBER IS A POOR DELIVERY MONTH AS MOST INVESTORS PREFER TO SKIP THIS MONTH AND MOVE STRAIGHT TO DECEMBER. IT LOOKS LIKE SOME MAJOR ENTITY(GOLDMAN SACHS) JUST CANNOT WAIT FOR DECEMBER AS THEY ARE MAKING THEIR MOVE ON OCTOBER FOR PHYSICAL METAL. GOLDMAN SACHS ONE OF THE LEADERS OF THE NEW LONDON LME EXCHANGE NEEDS THE GOLD INVENTORY FOR LIQUIDITY AND INITIAL CONTRIBUTION WITH OTHER MAJOR PLAYERS. THE MAJOR DIFFERENCE BETWEEN THIS MONTH AND OTHER MONTHS IS THAT THIS GOLD STANDING IN OCTOBER WILL LEAVE THE COMEX AND HEAD FOR LONDON.

We had 99 notices filed today for 9900 oz OR .307 TONNES.

To calculate the INITIAL total number of gold ounces standing for the OCT /2020. contract month, we take the total number of notices filed so far for the month (34,425) x 100 oz , to which we add the difference between the open interest for the front month of OCT (499 CONTRACTS ) minus the number of notices served upon today (99 x 100 oz per contract) equals 3,482,500 OZ OR 108.320 TONNES) the number of ounces standing in this active month of Oct

thus the INITIAL standings for gold for the OCT/2020 contract month:

No of notices filed so far (34,425, x 100 oz +499 OI) for the front month minus the number of notices served upon today (99) x 100 oz which equals 3,482,500 oz standing OR 108.320 TONNES in this active delivery month. This is a HUGE amount for gold standing for a OCT delivery month (a poor active delivery month).

We gained 89 contracts or an additional 8900 oz will stand on this side of the pond searching for metal.

NEW PLEDGED GOLD: BRINKS

593,649.694 oz NOW PLEDGED SEPT 15.2020/HSBC 18.465 TONNES ( A HUGE INCREASE FROM 10.6)

60,784.803 PLEDGED APRIL 3/2020: SCOTIA/ OCT 23: 1.8906 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

277,934.09 oz (some deleted august 3) JPM 8.644 TONNES

610,238.285 oz pledged June 12/2020 Brinks/ July 2/July 21 19.017 tonnes

67,289.041 oz Pledged August 21/regular account 2.092 tonnes JPM

total pledged gold: 1,609,895.918 oz 50.074 tonnes

total registered, pledged and eligible (customer) gold 37,532,664.459 oz 1,167.42 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1041.08 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

And now for the wild silver comex results

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

1987.848 oz

Delaware

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

1,196,350.566 oz

JPMorgan

Delaware

Brinks

Loomis

|

| No of oz served today (contracts) |

0

CONTRACT(S)

(0 OZ)

|

| No of oz to be served (notices) |

2 contracts

10,000 oz)

|

| Total monthly oz silver served (contracts) | 2269 contracts

11,345,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

67 Million Ounces: World’s Biggest Gold Reserves Discovered Deep In Siberia

Last week the world’s largest stockpile of gold was revealed when Russia’s largest gold producer, Polyus PJSC, said its untapped Sukhoi Log deposit in Siberia holds the world’s biggest reserves.

A company audit showed Sukhoi Log has 40 million ounces of proven reserves as measured by international JORC standards, with an average gold content of 2.3 grams per ton, according to Chief Executive Officer Pavel Grachev. Additionally, the estimated Mineral Resources for Sukhoi Log stand at 1,110 million tonnes, with an average grade of 1.9 g/t Au and containing 67 million ounces of gold as at 31 May 2020. This means that the monetary value of the estimated gold holdings is just over $127 billion at today’s prices.

That means the field – accounting for more than a quarter of Russian gold reserves – is bigger than Seabridge Gold Inc.’s KSM Project in Canada and Donlin Gold in Alaska.

“The estimate of the reserves is an important milestone in development of the field,” Grachev said in interview in Moscow.

Sukhoi Log, located in the isolated Irkutsk region deep in the heart of Siberia, was discovered by Soviet geologists in 1961 and studied in the 1970s. The government had long considered offloading the deposit, and in 2017 sold the field in an auction to Polyus and a state partner, which the mining company later bought out.

Some more details on Sukhoi Log:

- The audit shows that as well as economically mineable reserves, the deposit has 67 million ounces of total resources, up from 63 million ounces previously estimated.

- That figure may rise after more drilling and studies.

- Main investment is due to start in 2023. Polyus has already started spending on infrastructure for the project, including co-investing with the government on the reconstruction of a local airport.

The world’s biggest gold deposits will likely remain untouched for the foreseeable future. According to Bloomberg, Polyus said earlier this year that it would focus on smaller projects and reducing its debt ratio in the coming years before developing the giant field. The company plans to announce details on expected production and investment at Sukhoi Log once a pre-feasibility study is ready by year-end. It previously said that costs could reach $2.5 billion, with annual output totaling about 1.6 million ounces, or just over $3 billion at current gold prices.

While developing giant deposits is typically a lengthy and costly process, the field may allow Polyus to boost annual output by at least 70%. Gold prices have rallied about 60% since the company purchased it, and reached a record in August as vast amounts of stimulus were pumped into economies to curb the damage from the coronavirus pandemic.

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Futures Rebound From Monday’s Plunge On Strong Earnings, Mega Merger

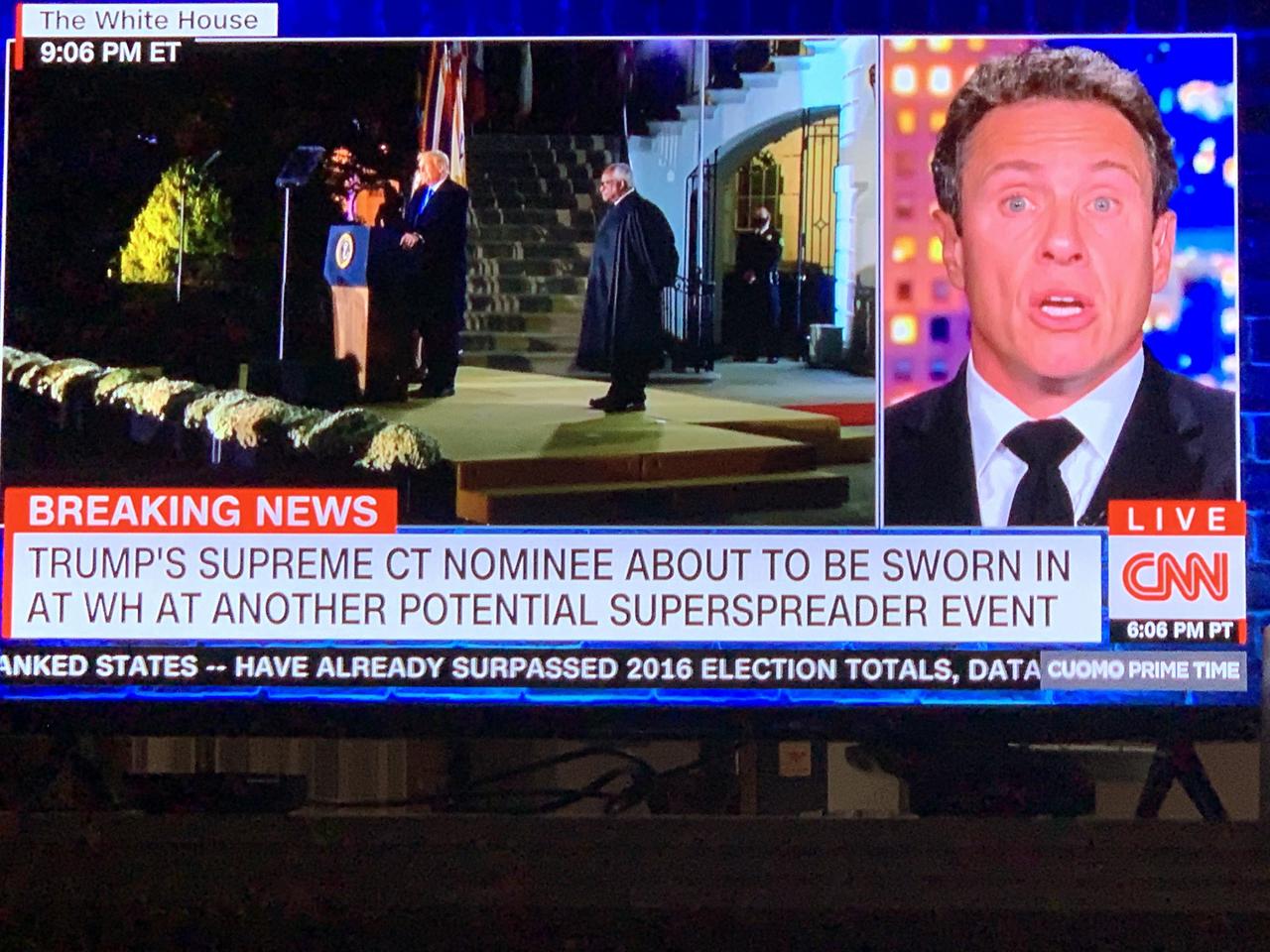

U.S. index futures and European stocks rebounded on Tuesday following the S&P 500’s worst day in a month as investors parsed through strong corporate earnings which offset Monday’s SAP shocker, while bracing for volatility ahead of Election Day, assessing rising coronavirus cases across the globe and conceding that a fiscal stimulus deal just won’t happen now that the Senate has closed for recess after rushing through the appointment of Amy Coney Barrett to the SCOTUS late on Monday night, which was also Hillary Clinton’s birthday. AMD’s $35 billion acqusition of Xilinx also helped boost trader optimism.

The S&P 500 and Nasdaq hit three week lows on Monday as record number of new coronavirus infections in the United States and some European countries and a lack of agreement in Washington over the next U.S. fiscal stimulus raised worries about the economic recovery. The chances are “very, very slim,” Appropriations Chairman Richard Shelby said talking about a stimulus, pointing out the patently obvious. Differences between the two sides “have narrowed,” but “the more it narrows, the more conditions come up on the other side,” White House economic adviser Larry Kudlow told reporters. Of course, Nancy Pelosi remains optimistic, her spokesman said, but she’s used similar language throughout three months of talks as she does not want to take the blame for the continued gridlock.

Also on Monday, the VIX spiked to its highest closing level in nearly two months on “concerns” about President Donald Trump’s unexpected victory or the uncertain election outcome we first reported on Sunday night. As we also reported, while Joe Biden leads the official polls, the race is much tighter in battleground states which determine the election outcome.

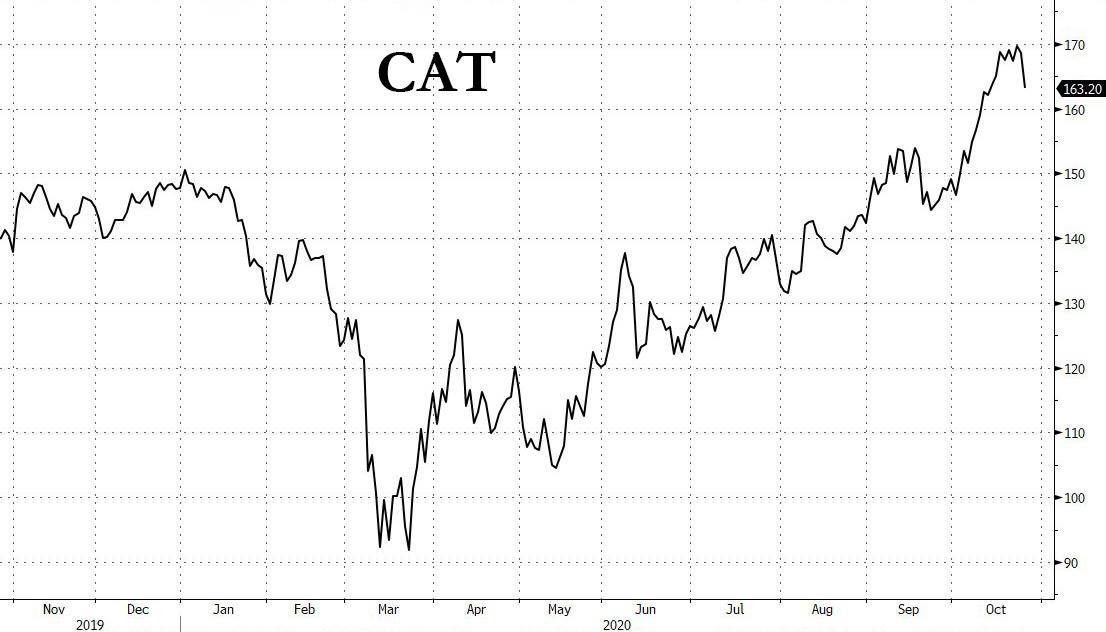

In premarket trading, Drugmaker Eli Lilly fell 4% after it reported a fall in quarterly profit. Industrial companies 3M Co and Caterpillar Inc were also slightly lower after results. Investors are looking forward to results from Apple, Amazon.com, Alphabet and Facebook Inc in an earnings-heavy week as the technology giants have managed to stand out during the coronavirus pandemic. Chipmaker Xilinx soared after AMD announced a $35BN takeover offer, while Merck climbed after the drugmaker boosted its guidance.

At 8am S&P 500 E-minis rose 0.47% to 3,409.5 points.

The Stoxx Europe 600 Index erased most of its decline after earlier heading toward its lowest close since June on coronavirus lockdown fears. France’s benchmark CAC 40 Index underperformed other major European stock indexes on Tuesday, amid concerns that tougher restrictions may be introduced in the country as soon as tomorrow to curb a spike in coronavirus cases. Declines in miners and energy firms offset positive earnings from banking powerhouses HSBC Holdings and Banco Santander, which both signaled a brighter outlook for dividends. Following two tumultuous quarter, HSBC said it would consider paying a 2020 dividend after the bank unveiled a better-than-expected third quarter profit on lower provisions for bad loans. The bank on Tuesday reported a 36 per cent year-on-year drop in pre-tax profits to $3.1bn for the third-quarter, which was above analysts’ forecasts. Noel Quinn, HSBC’s chief executive, labelled the results “promising.” Energy giant BP Plc warned of many challenges ahead as the pace of recovery in oil demand remained uncertain. Meanwhile, Europe took a step closer to the strict rules imposed during the initial wave of the pandemic, with leaders struggling to regain control of the spread while confronting growing opposition to restrictions.

Earlier in the session, Asian stocks fell, led by the energy and finance sectors, after falling in the last session. Most markets in the region were down, with Australia’s S&P/ASX 200 dropping 1.7% and South Korea’s Kospi falling 0.6%, while India’s S&P BSE Sensex Index increased 0.5%. The Topix was little changed, with Nintendo climbing and Nidec slipping.

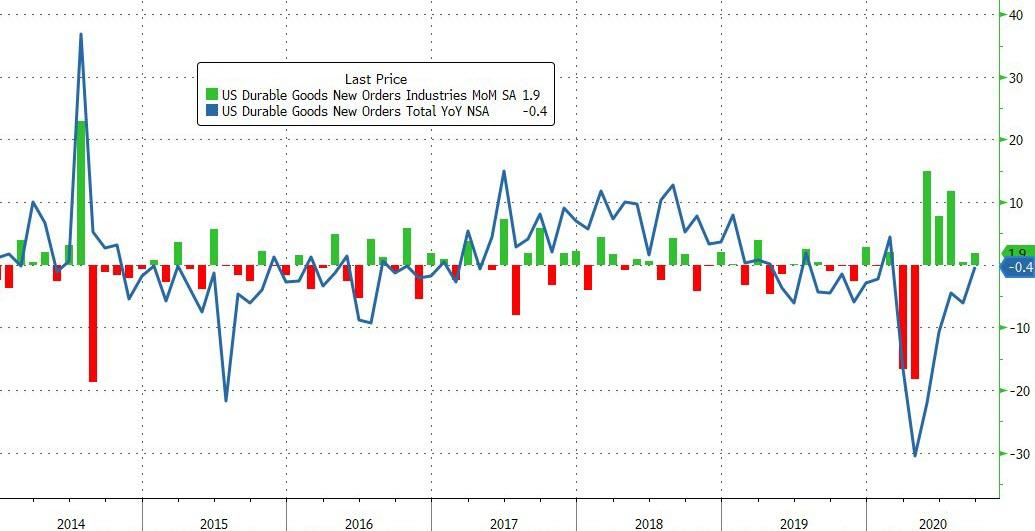

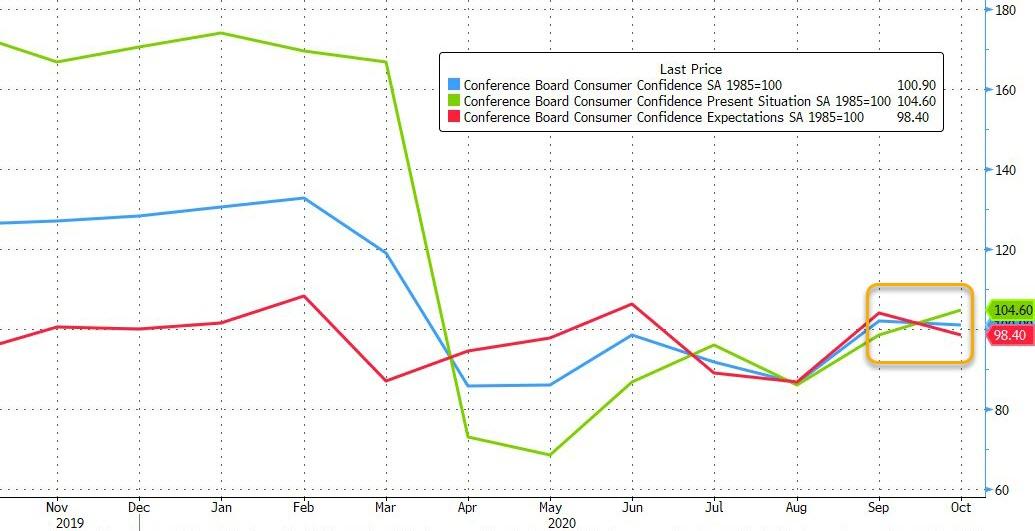

As Bloomberg notes, with time effectively over to finish an aid package before Americans vote, investors are looking for market catalysts later on Tuesday from data and earnings. Durable-goods orders and consumer confidence reports are due, as well as results from Microsoft Corp. and AMD after market.

In rates, Treasuries were steady overnight, holding Monday session gains despite gains in S&P 500 e-minis amid poor volumes, trading around 60% of recent average during Asia, early Europe. Preliminary open interest data shows some unwind of long-end short positions into Monday’s rally. Yields were mixed, although within a basis point of Monday’s close across the curve; 10-year steady at around 0.80%, trading inline with bunds and outperforming gilts by ~1bp. Treasury auctions kick-off with $54b 2-year note sale today, followed by 5- and 7- year sales Wednesday and Thursday, respectively.

On Monday, BlackRock strategists downgraded U.S. Treasuries and upgraded their inflation-linked peers ahead of the U.S. election on a growing likelihood of significant fiscal expansion. They said Covid infections in Europe threaten to derail a fragile recovery as they recommended investors hold a neutral position on bunds to hedge a downturn.

“As Covid infections have picked up, the focus on further policy response has shifted to more monetary easing including additional asset purchases,” said strategists Mike Pyle, Scott Thiel and Beata Harasim.

In Fx, a gauge of the dollar’s strength edged lower after Monday’s bounce, while the euro and the pound were little changed; cable slipped earlier with strategists predicting limited gains in the currency on a Brexit trade-deal breakthrough. The Norwegian krone and the Japanese yen led G-10 currency gains, while the Swiss franc and the Swedish krona weakened the most. China’s currency weakened after Reuters reported the country’s central bank asked lenders to suspend a key factor used to calculate the yuan’s daily reference rate.

Elsewhere, crude oil nudged higher while gold remains largely unchanged.

In terms of data today we will get the preliminary September durable goods orders and nondefence capital goods orders ex-air. There will also be August’s FHFA house price index, the Richmond Fed manufacturing index and the October Conference Board consumer confidence reading. The Fed’s Kaplan is the only major speaker on the docket. Lastly the second major week of earnings ramps up as Microsoft, Novartis, Pfizer, Merck & Co., Eli Lilly & Co, Caterpillar, HSBC and BP all report.

Market Snapshot

- S&P 500 futures up 0.2% to 3,3400.50

- STOXX Europe 600 down 0.4% to 354.57

- MXAP down 0.2% to 175.21

- MXAPJ down 0.3% to 581.84

- Nikkei down 0.04% to 23,485.80

- Topix down 0.09% to 1,617.53

- Hang Seng Index down 0.5% to 24,787.19

- Shanghai Composite up 0.1% to 3,254.32

- Sensex up 0.6% to 40,372.74

- Australia S&P/ASX 200 down 1.7% to 6,051.02

- Kospi down 0.6% to 2,330.84

- Brent futures up 0.7% to $40.75/bbl

- Gold spot down 0.1% to $1,900.30

- U.S. Dollar Index little changed at 93.07

- German 10Y yield unchanged at -0.581%

- Euro down 0.04% to $1.1805

- Italian 10Y yield fell 1.9 bps to 0.536%

- Spanish 10Y yield fell 0.2 bps to 0.184%

Top Overnight News from Bloomberg

- The world’s biggest money manager is shorting the dollar on expectations that unprecedented fiscal and monetary stimulus will prolong its losses — regardless of who wins the U.S. election

- Turkey’s banking regulator took another step to slow lending after a massive credit boom contributed to a currency rout

- U.S. President Donald Trump’s push for a second poll-defying victory is relying on a hallmark of his first — raucous campaign rallies that Trump sees as a crucial sign of voter enthusiasm but that pollsters say may only be cementing his defeat

- More than 50 of Boris Johnson’s own Conservative members of Parliament have demanded a clear route out of lockdown for parts of northern Britain that helped give his party a majority in last year’s election. In a letter to the prime minister, the MPs warned that his pandemic strategy of targeting local areas with restrictions is disproportionately damaging the economies of northern regions of the country

Asian equity markets resumed the weak performance seen across global peers amid the ongoing risk-averse themes including the worsening COVID-19 pandemic, tougher lockdown restrictions in Europe and the continued US stimulus stalemate which culminated in Wall St’s worst day in more than a month. ASX 200 (-1.7%) and Nikkei 225 (-0.1%) were lower with the Australian benchmark the underperformer amid losses across all sectors and the declines led by energy as the COVID-19 situation did no favours for the demand outlook, while sentiment in Tokyo was also lacklustre but with downside limited by a relatively stable currency and the KOSPI (-0.9%) briefly nursed opening losses after better than expected GDP data and stronger revenue from Kia Motors which drove shares in the automaker higher by nearly double-digits. Hang Seng (-0.9%) and Shanghai Comp. (Unch.) were both lacklustre after data showed Industrial Profit growth in September moderated to 10.1% from 19.1% and due to lingering US-China tensions after the US government approved potential USD 2.4bln in arms sale to Taiwan despite an earlier announcement by China’s Foreign Ministry to impose sanctions on US entities that partake in arms sales to Taiwan, although there were some bright spots with HSBC shares rallying around 5% on return from the lunch break following better than expected Q3 results and with Tencent also buoyed after US Appeals Court rejected an attempt by the Justice Department to impose an immediate ban on WeChat. Finally, 10yr JGBs traded higher as prices conformed to the mild upside seen in T-notes and with demand also spurred by the risk aversion, although gains were capped by the 2 year auction results which were marginally weaker than prior.

Top Asian News

- HSBC Flags Conservative Return to Dividends on Profit Beat

- Hong Kong Police Arrest Activist Seeking U.S. Asylum, SCMP Says

- Dubai in Talks on London Air-Travel Agreement to Boost Demand

Ahead of the cash open, index futures indicated a positive open in Europe with the DAX Dec’20 contract at one stage showing gains of 0.7% in what was initially a paring of yesterday’s heavy losses. However, as cash products opened, indices faced a bout of selling pressure with the DAX Dec’20 contract now lower by 0.5%; Eurostoxx 50 cash is down -0.6% – notably, both are off session lows. In terms of fundamental drivers, downbeat sentiment from yesterday has been carried over into today’s session as the spread of COVID across the region saps investor risk appetite. One of the more concerning updates this morning has comes from Germany with the economy minister warning that the number of new infections in the nation are rising exponentially and will likely have 20k daily new infections by the end of the week (on October 24th it posted 14.7k new infections). From a sectoral standpoint, banking names have bucked the downbeat trend this morning with HSBC (+6.6%) one of the Stoxx 600’s best performers following Q3 earnings. HSBC exceeded expectations for revenues, net income and adj. pretax profits, whilst noting that it will reduce 2022 costs by more than the initially targeted USD 31bln. Santander (+3.6%) are also firmer on the session and providing support to peripheral banks after the Co. reported a marked improvement in Q3 earnings, compared to Q2 and noted a 14% decline in quarterly provisions. Other large cap earnings include BP (+1.6%), who trade firmer on the session after reporting an unexpected Q3 profit of USD 86mln with results underpinned by a lack of significant write-offs and a recovery in the broader oil & gas environment. Despite opening higher, Novartis (-1.3%) have drifted lower throughout the session in the wake of Q3 earnings, which saw revenues miss analyst estimates

Top European News

- Merkel Wants to Shutter Restaurants in Battle Against Virus

- Italy Readies New Virus Relief Package Amid Mounting Protests

- Lockdowns Loom for European Governments Running Out of Options

- Novartis Lifts 2020 Forecast as Drugmaker Counters Covid Impact

In FX, although the Dollar is somewhat mixed vs major counterparts, the DXY looks firmly anchored around 93.000 and eclipsed Monday’s high amidst underlying safe-haven demand when EU stocks lost their initial/early recovery momentum due to ongoing COVID contagion, exacerbated by Germany’s Economy Minister warning of the pandemic’s exponential resurgence that may see the daily rate of new cases reach 20k by the end of this week. The index has stalled at 99.137 for now with some technical resistance in the form of a double top around 93.100 perhaps weighing, but the latest pull-back was relatively shallow, at 92.875 vs 92.784 yesterday and last week’s 92.469 base.

- CAD/NZD – Both bucking the overall trend, as the Loonie rebounds from sub-1.3200 alongside a partial/mild bounce in crude prices and the clock ticks down to Wednesday’s BoC policy meeting. Meanwhile, crosswinds continue to keep the Kiwi afloat close to 0.6700 and 1.0650 vs its US and Aussie rivals in wake of broadly in line NZ trade data.

- JPY/AUD/EUR/CHF/GBP – All rangebound against the Greenback and within familiar confines, with the Yen meandering between 104.90-67 and well inside decent option expiries at 104.25 (1 bn) and the 105.00 strike (1.8 bn). Back down under, the Aussie remains comfortably above 0.7100 ahead of Q3 CPI overnight and in wake of supportive comments from RBA Assistant Governor Debelle seeing signs of growth in Q3. Conversely, the Euro, Franc and Sterling seem more precarious near round numbers (1.1800, 0.9100 and 1.3000 respectively) as the coronavirus spreads and the former eyes 1.2 bn expiry interest in close proximity (1.2 bn from 1.1800 to 1.1805), while the Pound awaits Brexit developments.

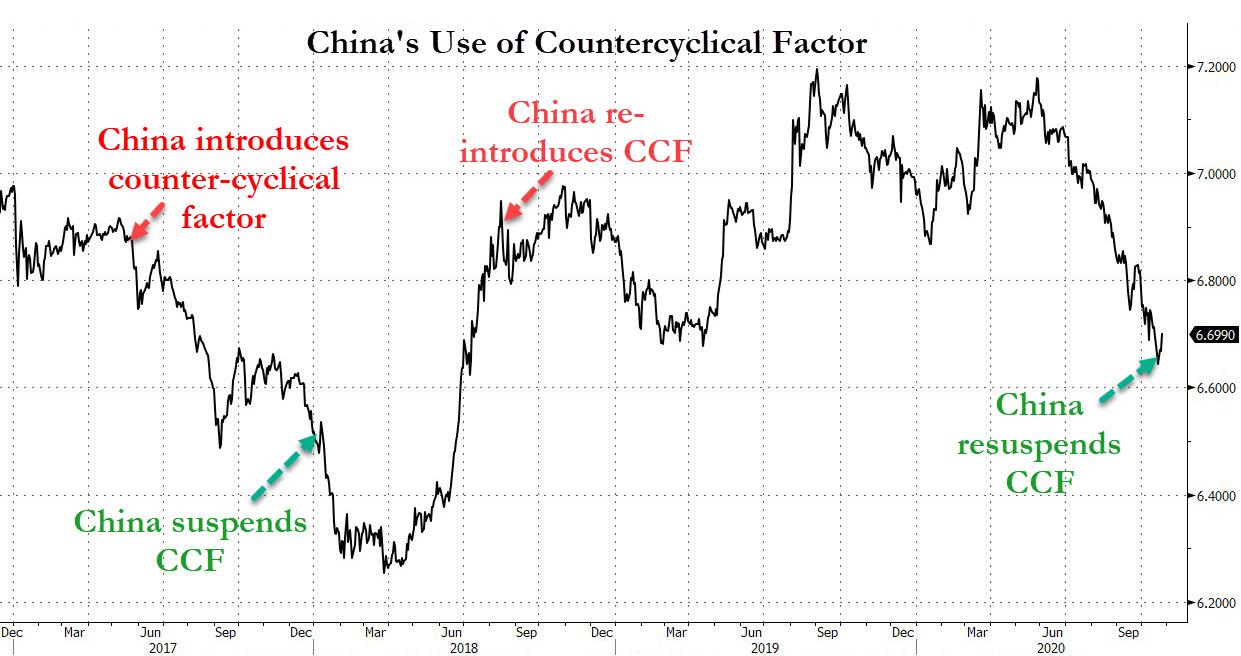

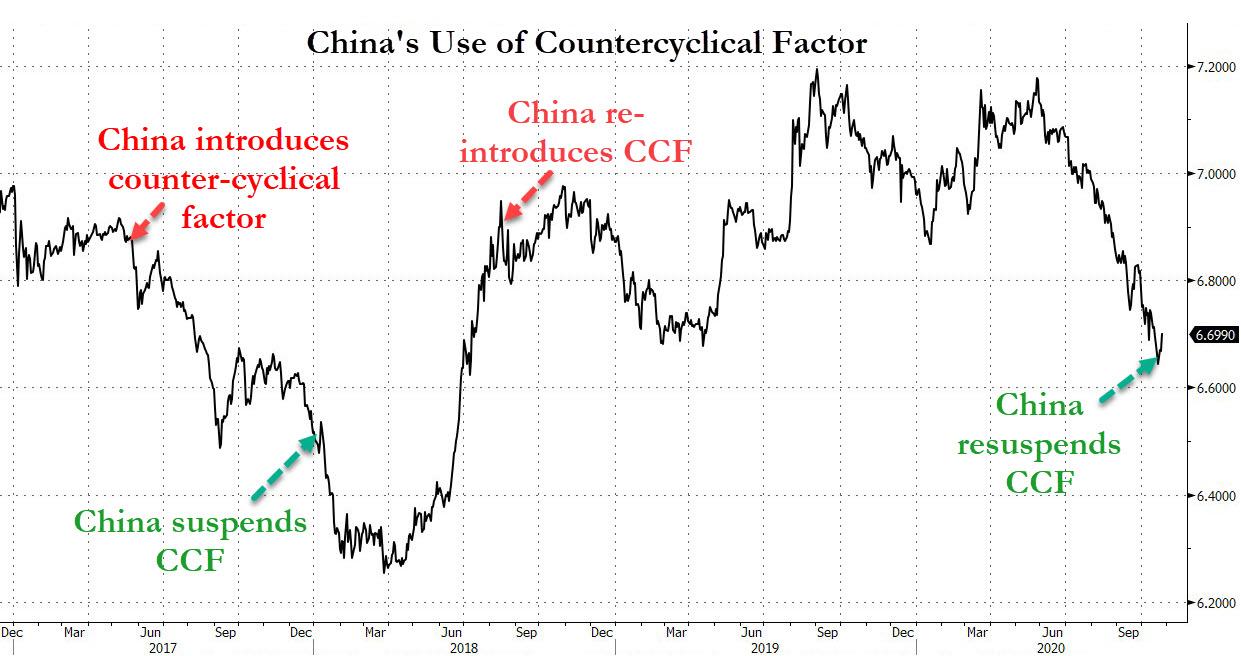

- SCANDI/EM – Not much sign of a positive reaction to Sweden turning a trade deficit around in September to show a wider surplus, as Eur/Sek pivots 10.3300, but the modestly firmer tone in oil is capping Eur/Nok around 10.9000 and well off recent 11.0000+ peaks. Elsewhere, the Yuan has found some support beneath 6.7100 vs the Dollar after a firmer than forecast PBoC midpoint fix and hardly responding to the request made for banks to neutralise the counter-cyclical factor in the formula, but the Lira’s travails rumble on as fresh all time lows are hit below 8.1600.

In commodities, WTI and Brent front month futures are holding in positive territory of around USD 0.30/bbl as the session stands in-spite of the deterioration in risk-sentiment post the European cash equity open. The current relative resilience is largely a factor of Hurricane Zeta which as of yesterday had shuttered around 16% of Gulf of Mexico oil production and 6% of gas output. The BSEE will provide another update later in the session at 18:00GMT/14:00ET which could well see further impact as the NHC believes the storm will re-strengthen as it progress to the Northern side of the Gulf prior to making landfall. Additionally, it’s worth highlighting that yesterday’s BSEE survey only focused on 7 companies in the Gulf compared to the survey’s sample contained in excess of 20 companies during Hurricane Delta earlier in the month. Elsewhere, post-earnings this morning BP noted that the Hurricane has shut down 20/30k BPD of its oil & gas production thus far. Storm updates aside, the sessions scheduled focus point explicitly for crude is the private inventory release which is expected to show a build of around 1.1mln barrels for the prior week as the effect of Delta diminishes but Zeta is yet to be included in the survey period. Moving to metals, spot gold has come under pressure this morning as while the metal isn’t currently suffering from USD strength as the DXY has dropped into negative territory it has failed to benefit from traditional safe-haven demand with silver & JPY seemingly receiving some of this allure.

US Event Calendar

- 8:30am: Durable Goods Orders, est. 0.5%, prior 0.5%; Durables Ex Transportation, est. 0.35%, prior 0.6%

- 8:30am: Cap Goods Orders Nondef Ex Air, est. 0.5%, prior 1.9%; Cap Goods Ship Nondef Ex Air, est. 0.4%, prior 1.5%

- 9am: FHFA House Price Index MoM, est. 0.7%, prior 1.0%

- 9am: S&P CoreLogic CS 20- City MoM SA, est. 0.5%, prior 0.55%; S&P CoreLogic CS 20-City YoY NSA, est. 4.2%, prior 3.95%

- 10am: Conf. Board Consumer Confidence, est. 102, prior 101.8; Present Situation, prior 98.5; Expectations, prior 104

- 10am: Richmond Fed Manufact. Index, est. 17.5, prior 21

DB’s Jim Reid concludes the overnight wrap

Nice to be back luxuriating in the home office again after a few days of high intensity childminding over part of half-term. The drive through safari park was the highlight with lions, tigers and cheetahs brushing up to the car and monkeys climbing on top of it. The last time I went on safari was during a school cricket tour to Kenya in 1991. We were told before the trip not to take expensive cameras as the risk was they would get stolen. I didn’t have an alternative option anyway as I only had a basic one I’d bought for 10 pounds with my paper round money. However some of the other kids ignored this and brought cameras with big telescopic lenses. As such with my photos you were unable to tell whether the orangish blobs were rocks or lions whereas with my friends you could tell whether the lions had recently flossed or not. 29 years later my trusty iPhone got me some very decent pictures even if it did cost more than 10 pounds.

Looking at the finance pages on my iPhone this morning, it’s quite clear that global equities have taken a large step back at the start of this week after a weekend that saw covid-19 cases hit new highs in the US and fresh restrictions seemingly building daily in Europe. The S&P 500 finished down -1.86% last night, its worst daily performance since 23 September as the US saw its highest weekly cases of the pandemic so far. Sentiment was not helped by the ever dropping probability of a fiscal stimulus agreement prior to the election. Nearly 92% of stocks in the S&P were lower by the end of the session, led by declines in the energy sector (-3.47%) as oil prices fell sharply. WTI and Brent crude fell -3.24% and -3.14% respectively, as the global demand outlook worsened. Tech hardware (-0.58%) and Biotech (-0.85%) were among the more resilient industries, however the NASDAQ was still down -1.64%. The VIX rose +4.9pts to 32.5pts in its biggest move since 3 September.

Overnight Asian markets have tracked Wall Street’s move though the declines are more modest. The Nikkei (-0.24%), Hang Seng (-0.97%), Shanghai Comp (-0.37%), Kospi (-0.50%) and Asx (-1.70%) are all down. Meanwhile, in a sign of abating risk off sentiment, the US dollar index is down -0.11% this morning and futures on the S&P 500 are up +0.18%. HSBC is trading up +1.86% after reporting better than expected earnings as the bank paired back its expected credit losses. They also said that they are considering paying a conservative dividend for 2020 contingent on economic conditions in early 2021, subject to regulatory consultation. In terms of overnight data, South Korea’s Q3 GDP print came in better than expectations at 1.9% qoq (vs. 1.3% qoq expected).

Earlier European equities, and the DAX (-3.71%) in particular, pulled back strongly on news that SAP was lowering its revenue forecast for the full year of 2020 and that the pandemic could weigh on demand into the first half of next year. The largest tech company in Europe was down -22.20% and is now -18.55% YTD. Contrast this to Apple – the largest US tech company – which is +56.7% YTD with the NYFANG index +76.9% against Europe’s tech index at -8.0% YTD.

Every sector in the Stoxx 600 (-1.81%) declined led by Technology (-7.37%) and Travel & Leisure (-3.29%). The latter was heavily influenced by the new restrictions across the continent, which outweighed the positive vaccine news from Astrazenca and Johnson and Johnson that we highlighted yesterday morning. After the positive vaccine news yesterday, our CoTD highlighted the work of our colleague Robin Winkler, looking at different R0 and efficacy scenarios to see what is required for herd immunity. We likely remain multiple quarters away from a mass rollout however the upcoming efficacy data should in theory have a major impact on life and markets going forward. As a benchmark the FDA has set its threshold as 50% – similar to the flu vaccine. See the CoTD here to see how much of the population would have to be vaccinated if the efficacy was only 50%, as well as the link to Robin’s note.

We are now just one week away from Election Day in the US. However, over 58.6 million ballots have already been cast across the country. This is more early votes (both in-person and mail-in) than in all of 2016, and there is still a week to go. Early indications point to a possible record turnout, if this pace continues, especially given the number of “new and infrequent” voters. The AP reported as many as 26.3% of Georgia’s early voters and just over 30% of Texas’s early voters are either a new or infrequent voter, which points to just how much important some feel this election is.

National polls have tightened slightly in the last 2 weeks. Former Vice President Biden led by as much +10.7% in fivethirtyeight.com’s polling average back on October 17 but that has come in to +9.4% as of today. This is still a substantial lead and Biden still holds the polling advantage in key battleground states such as Michigan (+8.3%), Wisconsin (+7.1%) and Pennsylvania (+5.1%). The fivethirtyeight.com model gives Biden an 87% chance of winning the Electoral College and therefore the election.

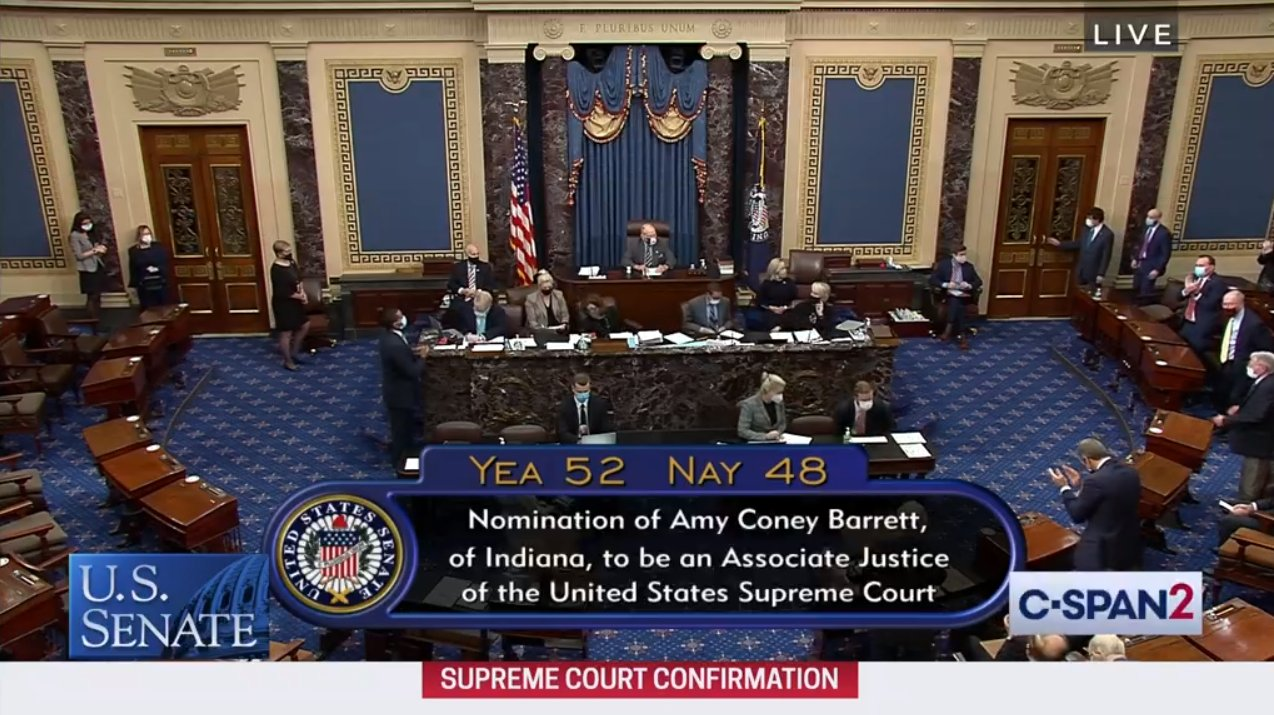

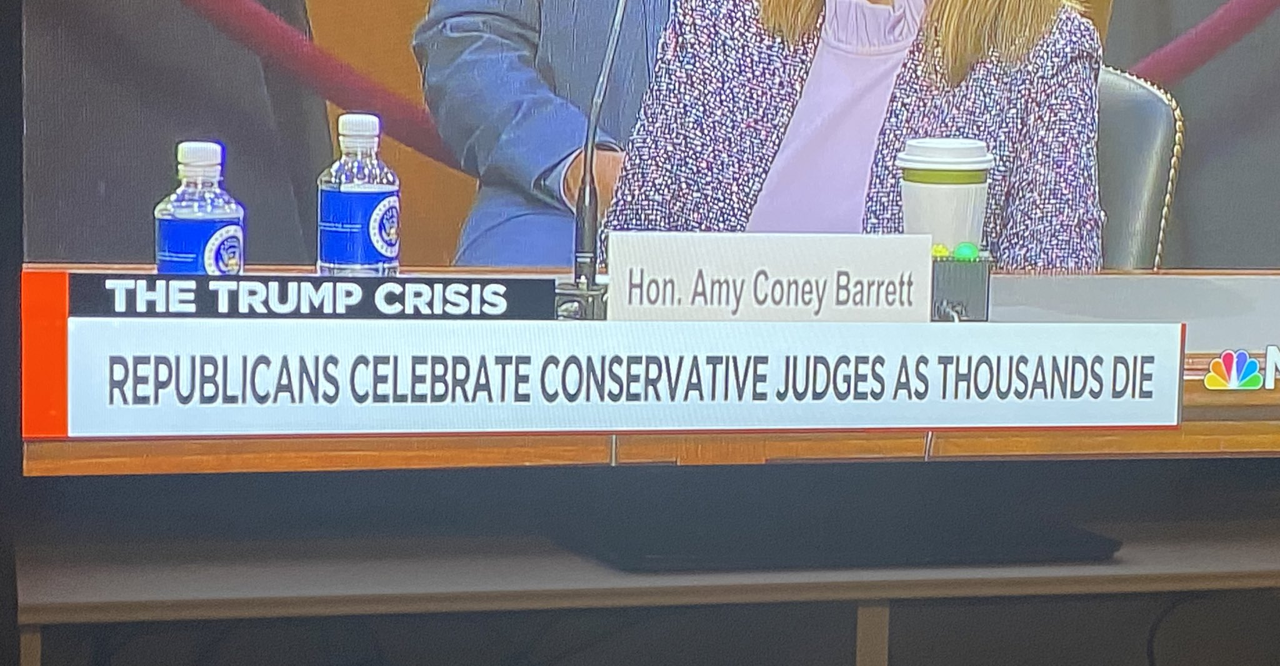

Lastly on US politics, late last night the Senate confirmed Amy Coney Barrett to the Supreme Court of the US, thereby giving the court a 6-3 conservative majority. The vote was 52-48 and mostly along party lines, with one Republican, Senator Susan Collins, joining Democrats in opposition.

Coronavirus cases remain in focus as more regions of Europe contemplate or enact further restrictions to quell the current wave. France reported over 250,000 new cases over the last week and nearly 70% of ICU beds in the Paris region are occupied, according to local authorities. President Macron is expected to convene a defense cabinet meeting later today to address the issue, which may lead to further restrictions. This comes as the head of the scientific council that advises the French government on the pandemic said the situation is moving towards that of early March, and that the second wave will probably be worse than the first one. The Netherlands passed 300,000 confirmed cases yesterday, after over 10.3k new cases yesterday. Dutch Prime Minister Rutte has said he wants to wait for the new data over the coming days before making a final call on further restrictions for the country.

Elsewhere, German Chancellor Angela Merkel convened her task force yesterday and it was reported she plans to present a “lockdown light” plan which would see bars, restaurants and public events shut in order to minimise a second wave. Furthermore, shops would remain open and schools would not have to close under the new plan. Meanwhile, Italy’s new rules went into effect yesterday after Prime Minister Conte approved the government’s plan to limit hours for bars and restaurants as well as shutting down gyms and entertainment venues. Italians have also been asked not to travel under the new restrictions, which are currently in place until November 24. Meanwhile on top of the national curfew that was set in Spain, the country’s parliament approved an extension of the state of emergency until May 9, in order for the Prime Minister to avoid continually seeking approval to implement further restrictions.

In the US, the rolling 7-day Covid-19 case count hit a new high with over 480,000 cases. This surpasses the high of 472,083 we saw back in late July. While testing capacity is higher, the number of newly confirmed weekly cases as a percent of weekly US tests is over 6% for the first time since August and has been rising sharply over the last 2-3 weeks. On therapeutics, Eli Lilly has confirmed overnight that its US clinical trial of experimental antibody therapy will end as data suggested that the treatment is unlikely to help hospitalised patients recover from advanced forms of the virus. The stock is down -1% in after-hours trading. In other worrying news, according to a large Imperial College London covid study, the proportion of people in England with antibodies dropped by more than a quarter in the space of three months. This will raise concerns about how long people can go without risking being reinfected.

European risk sentiment was not helped by the German October Ifo business climate indicator, which fell to 92.7 (93.0 expected). This is -0.5pts down from last month and was the first monthly decline since April. In the US, the September reading of the Chicago Fed national activity index missed expectations by quite a bit, down to 0.27 (0.73 expected) from an upwardly revised 1.11 last month. A reading above ‘0’ translates to above-trend growth, indicating that while growth is positive it has slowed significantly. Similarly, new home sales dropped to 959k from 994k the month prior, and well below the 1,025k homes expected. Lastly, the October Dallas Fed manufacturing index beat expectations at 19.8 (vs 13.5 expected) in its highest reading since October 2018.

In terms of data today we will get Euro Area M3 money supply for September as well as slew of US data. In hard data there is the preliminary September durable goods orders and nondefence capital goods orders ex-air. There will also be August’s FHFA house price index, the Richmond Fed manufacturing index and the October Conference Board consumer confidence reading. The Fed’s Kaplan is the only major speaker on the docket. Lastly the second major week of earnings ramps up as Microsoft, Novartis, Pfizer, Merck & Co., Eli Lilly & Co, Caterpillar, HSBC and BP all report.

3A/ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 3.20 PTS OR .10% //Hang Sang CLOSED DOWN 131.59 PTS OR .53% /The Nikkei closed DOWN 155.22 POINTS OR 0.61%//Australia’s all ordinaires CLOSED DOWN 1.73%

/Chinese yuan (ONSHORE) closed /Oil DOWN TO 38.89 dollars per barrel for WTI and 40.70 for Brent. Stocks in Europe OPENED ALL RED// ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7065. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6948 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

CHINA/

China is trying to stem the yuan’s recent rise: it has now unexpectedly suspends counter cyclical factors in the fixing of the yuan

(zerohedge)

Yuan Slides After China Unexpectedly Suspends “Counter-Cyclical Factor” In FX Fixing

China keeps telling the world to stop buying the yuan, and the world keeps refusing to listen.

Just over two weeks after Beijing made it easier to short the yuan after the PBOC cut the reserve requirement ratio for FX derivative sales from 20% to 0%, a move which was “an attempt to moderate the yuan’s increase”, and which Goldman said “likely signals the PBOC’s discomfort with the recent rapid appreciation of CNY”, yet which failed to lead to a sustainable drop in the yuan, On Tuesday China lobbed another shot across the bow of the increasingly strong yuan when a statement on website of China Foreign Exchange Trade System announced that some banks that contribute to the yuan’s daily reference rate have recently halted the use of the counter-cyclical factor (CCF).

The confirmation followed a Reuters reports that the PBoC has asked banks to neutralize the counter-cyclical factor which is typically used when the currency is weakening at a pace that is uncomfortable for the central bank i.e. effectively removing it in the midpoint fixing. Under the reported tweak, lenders would have more room to submit quotes for a weaker fixing and guide the currency lower in the spot market, which is precisely Beijing’s goal in light of the recent yuan appreciation. The move followed sellside analyst reports in recent months that as a result of the recent strength in the Yuan, the CCF had not been used.

As a reminder, the counter-cyclical factor was introduced by the PBOC on May 26, 2017 to reduce exchange-rate volatility while undermining efforts to increase the role of market forces. At the time, the move was seen as Beijing “moving the goalposts” in its bid to reduce yuan volatility, to punish currency manipulators (read Yuan shorts) and limit capital outflows (the currency had weakened for three straight years, triggering draconian capital controls and the surge of bitcoin). The CCF was then suspended in January 2018 when the yuan surged, only to be reinstalled later that year when the Yuan slumped again.

And now the CCF has been re-suspended again.

According to Citi FX trader Charmaine Cheok this is “yet another signal from the central bank that they are loosening the reins on the currency and allowing for more flexibility. I reckon the reason the market is moving higher on spot now is merely a reflection of positioning, this announcement doesn’t have any immediate impact on spot.”

Other trading desks agreed, noting that this is in line with the policy direction to allow the FX to be more market driven and ties into the goal to promote RMB internationalization. Or at least allowing it to be market driven when it is strong, hoping the recent deflationary appreciation in the yuan will end.

In any case, now that China has confirmed the move, strategists expect higher volatility of the CNH/CNY given the CCF typically dampens stronger USD impact on fixing more than the appreciation side, even if the actual impact could be relatively limited.

While the market impact was muted indeed, the offshore yuan fell after the Reuters report, dropping as much as 0.34% to 6.7234 a dollar afterward. The currency has rallied 6.9% from a low in May and last week reached a two-year high.

And now that the PBOC has both cut reserves and re-suspended the CCF in hopes of weakening the yuan, and seemingly failed…

4/EUROPEAN AFFAIRS

FRANCE

Wow! this is high! 79% of all French believe that Islam has declared war on France

(zerohedge)

79% Of French Believe Islamism Has “Declared War” On Their Country; New Poll Finds

Authored by Paul Joseph Watson via Summit News,

A new poll conducted after the beheading of a teacher in Paris has found that 79% of French people believe Islamism has “declared war” on their country.

The survey was carried out by polling firm Ifop following the jihadist murder of geography teacher Samuel Paty, who was targeted for showing pupils cartoons of the Prophet Muhammad during a lesson about freedom of expression.

The murder prompted numerous mass protest marches across the country in defense of free speech and against the Islamic takeover of France.

“87% of French people say they agree with the fact that secularism is now in danger in France, and 79% that Islamism has declared war on the nation and the Republic,” reports Ifop.

The poll also found that the political leader the French people have the most trust in when it comes to combating Islamism is Marine Le Pen.

A previous poll also found that the French are becoming increasingly hostile to allowing more immigrants to enter their country, with 64% believing migrants have a negative impact, while 60% believe welcoming them is no longer feasible due to cultural differences.

As we previously highlighted, disorder in France’s migrant dominated suburbs has become so chronic that some are calling for the military to be sent in.

France’s feared banlieues are suburbs on the edge of major cities controlled by large groups of Muslim gangs who attack police officers, fire crews and ambulance workers who venture into the area.

Earlier this year, French intellectual Eric Zemmour said the problem was so bad that the only option was to “reconquer by force.”

Over 250 French people have been killed as a result of Islamist attacks since 2015.

France Weighs Return To Lockdown As Russia Refuses Despite Spike In COVID-19 Cases, Deaths: Live Updates

Already Tuesday morning we are seeing some headlines out of Europe that portend more headlines that could spook markets later on in the session. For starters, a second Bavarian county has declared a partial lockdown. Rottal-Inn has recorded well over 200 new infections per 100,000 inhabitants over the past week, well above the threshold of 50 new infections per 100,000 people at which new measures are required.

On Tuesday, the Robert Koch Institute reported 11,409 new infections, bringing Germany’s total to 455,829. Another 42 people died on Tuesday, bringing the country’s overall virus death toll to 10,098. Hospitals and ICUs are filling up again and German Chancellor Angela Merkel has expressed grave concern, saying the current restrictions are not strong enough to slow down the spread of the virus, as the country widely expects her government to impose more nationwide rules shortly. These could include closing restaurants and stopping live events.

Merkel will meet with the state governors Wednesday. The German press has reported that new restrictions are expected, including taking school closures and restrictions on nonessential businesses nation-wide. It comes after Italy, Spain and a host of other European countries imposed new COVID-inspired restrictions over the weekend.

But looking ahead, all eyes are on France, where a government minister recently warned the pace of infections might be as high as 100k/day, 2x the official total. On Wednesday, President Emmanuel Macron, Prime Minister Jean Castex (Macron’s virus point man) and other top officials are meeting to discuss new nationwide restrictions, possibly including another brief lockdown, something that Macron has said would be ‘unavoidable’ if the condition deteriorates beyond a certain point.

The Local published a handy guide to the different types of measures reportedly under consideration, which, at this point, is either localized lockdowns (Paris, Lyon and Marseille and possibly other cities and metro areas) or a nationwide closure (text below courtesy of the Local).

1. Total lockdown

The first option is a total, nationwide lockdown such as the one France imposed in March. Back then, the whole country was confined to their homes and only allowed out for short periods to run essential errands such as grocery shopping, medical appointments and walking the dog.

French political commentators say this is the least likely scenario because of the high economic and psychological costs that would entail.

“I think that Macron is desperate to avoid another complete lockdown – for economic reasons but also for reasons of public order. A second “confinement” would be resisted much more widely than the first,” The Local’s political commentator John Lichfield said.

Delfraissy said the main goals of the government was to protect France’s elderly and vulnerable and maintain economic activity, while at the same time reducing the spread of the virus.

If the government were to impose a new lockdown, it would likely be adapted to the lessons drawn from this spring, avoiding to close down parts of society where the health gains were small compared to the economic and social costs – such as primary schools.

“It would probably allow for a certain level of educational activity and a certain number of economic activity,” Delfraissy said, adding that this kind of lockdown “could be set in place for a shorter period of time if it were to be introduced now.”

He also said this kind of lockdown would likely be followed by a period of curfew such as the one in place now.

2. Local lockdowns

Another option is to continue the government’s strategy to adapt measures to local conditions and introduce lockdowns in the country’s hardest hit areas.

This would target areas with high levels of spread and areas where hospital struggle to cope with the pressure of new Covid-19 patients, such as Paris, Marseille and Lyon.

“I’d rather have local lockdowns now than a nationwide lockdown at Christmas,” Damien Abad, parliament chief for the rightwing opposition Les Republicains, told France Info radio.

3. Weekend lockdowns

The third option would be a lighter and adapted version of lockdown, which could include measures such as a weekend confinement and an earlier curfew than the 9pm curfew currently in place in roughly half of the country.

“This would be much tougher than the curfew currently in place,” Delfraissy said about that option.

Such a strategy has received support from a group of doctors in Lyon, who called for a 7pm curfew and a weekend lockdown.

“The situation is serious and we cannot afford to take half-measures any longer,” they said in a press statement.

This strategy could also entail closing secondary schools, high schools and universities, such as suggested by Antoine Flahault, Director of the Institute for Global Health at the University of Geneva, which monitors the development of Covid-19 in the world.

We already have taken lockdown measures, they might be sufficient,” he told French media.

* * *

Meanwhile, France’s small businesses are understandably anxious. On Tuesday morning, the CPME confederation of small and medium-sized businesses warned that a partial or total lockdown could risk provoking an economic collapse. Companies are “much more fragile than in March” and many, especially the smallest, would be incapable of taking on additional debt, the CPME says in statement on Tuesday “We would risk seeing a collapse in the French economy, a sort of unprecedented third wave, this time an economic one,” CPME says

Russia is balking at reintroducing tough measures even as its outbreak explodes and deaths hit record highs. Masks will be compulsory in some public places starting on Wednesday, but the authorities are avoiding action that could hurt businesses. The consumer health watchdog recommended on Tuesday to close bars and restaurants from 11 p.m. to 6 a.m. amid reports that many hospitals are at capacity. Kremlin spokesman Dmitry Peskov said earlier the authorities are confident they can handle the latest wave without a lockdown (Source: Bloomberg).

Eli Lilly said last night that it would be ending clinical trials for patients in a hospital setting after NIH researchers found that BAMLANIVIMAB, one of the antibody therapeutics the company is working on, doesn’t help to improve hospitalized patients recovery from advanced stages of the virus, although Eli Lilly noted that all other studies related to its treatment are ongoing. It’s the latest setback to therapeutics. The FDA recently gave remdesivir, a drug developed by Gilead originally to treat ebola, the greenlight for widespread use, even as studies show it has little to no benefit (Newswires).

The French government is reportedly mulling a localized lockdowns for the Paris, Lyon and Marseille metro areas, which would include 7pm curfew, a public transport shutdown and closing non-essential shops, while reports noted that a three-week lockdown could start from Friday evening with the details to be announced on Wednesday (Source: Bild).

Germany Economy Minister says that the number of new infections in the nation are rising exponentially and will likely have 20k daily new infections by the end of the week (Newswires).

Imperial College London/Ipsos MORI study among 365k randomly selected adults which conducted tests at home, showed that 4.4% had antibodies in September vs. 6.0% in June which suggested the antibody immunity may not last over time in some of those that were infected. (Newswires) Russia is to impose new COVID-19 restrictions (Source: RIA Novosti).

END