GOLD:$1867.90 DOWN $11.80 The quote is London spot price

Silver:$23.35 DOWN 4 cents London spot price ( cash market)

“How dreadful knowledge of the truth can be when there’s no help in the truth.” … Sophocles, (495-405 BCE)

seems appropriate for what is going on in the uSA

your data…

Closing access prices: London spot

i)Gold : $1867.00 LONDON SPOT 4:30 pm

ii)SILVER: $23.25//LONDON SPOT 4:30 pm

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 3.49 PTS OR .11% //Hang Sang CLOSED DOWN 122.20 PTS OR .49% /The Nikkei closed DOWN 86.57 POINTS OR 0.37%//Australia’s all ordinaires CLOSED DOWN 1.50%

/Chinese yuan (ONSHORE) closed /Oil DOWN TO 35.94 dollars per barrel for WTI and 37.47 for Brent. Stocks in Europe OPENED ALL RED// ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7140. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7174 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total withdrawals; 38,132.279 oz

We had 2 kilobar transactions +

ADJUSTMENTS: 1 //

dealer to customer:

Brinks: 128,861.208 oz

The front month of OCT registered a total of 9 contracts for a LOSS of 457 contracts. We had 460 notices filed yesterday so we gained 3 contracts or 300 additional oz will stand for delivery in this active delivery month of October. In gold we have not seen queue jumping start so early in the month. Thus you can bet the farm that throughout October, the total number of gold oz standing will increase from this level.

November LOST ONLY 99 contracts to stand at 1432.

WE WILL HAVE A STRONG NUMBER OF OZ STANDING FOR NOVEMBER OF AROUND 4 TONNES OF GOLD..

The big December contract LOST 11,860 contracts DOWN to 428,909 contracts..

THE BIG STORY AGAIN TODAY IS THE HIGH OI STANDING FOR OCTOBER (108.53 tonnes). GENERALLY OCTOBER IS A POOR DELIVERY MONTH AS MOST INVESTORS PREFER TO SKIP THIS MONTH AND MOVE STRAIGHT TO DECEMBER. IT LOOKS LIKE SOME MAJOR ENTITY(GOLDMAN SACHS) JUST CANNOT WAIT FOR DECEMBER AS THEY ARE MAKING THEIR MOVE ON OCTOBER FOR PHYSICAL METAL. GOLDMAN SACHS ONE OF THE LEADERS OF THE NEW LONDON LME EXCHANGE NEEDS THE GOLD INVENTORY FOR LIQUIDITY AND INITIAL CONTRIBUTION WITH OTHER MAJOR PLAYERS. THE MAJOR DIFFERENCE BETWEEN THIS MONTH AND OTHER MONTHS IS THAT THIS GOLD STANDING IN OCTOBER WILL LEAVE THE COMEX AND HEAD FOR LONDON.

We had 9 notices filed today for 900 oz OR 0.0279 TONNES.

To calculate the INITIAL total number of gold ounces standing for the OCT /2020. contract month, we take the total number of notices filed so far for the month (34,894) x 100 oz , to which we add the difference between the open interest for the front month of OCT (9 CONTRACTS ) minus the number of notices served upon today (9 x 100 oz per contract) equals 3,489,400 OZ OR 108.53 TONNES) the number of ounces standing in this active month of Oct

thus the INITIAL standings for gold for the OCT/2020 contract month:

No of notices filed so far (34,894, x 100 oz +9 OI) for the front month minus the number of notices served upon today (9) x 100 oz which equals 3,489,400 oz standing OR 108.53 TONNES in this active delivery month. This is a HUGE amount for gold standing for a OCT delivery month (a poor active delivery month).

We gained 3 contracts or an additional 300 oz will stand on this side of the pond searching for metal.

NEW PLEDGED GOLD: BRINKS

596,952.410 oz NOW PLEDGED SEPT 15.2020/HSBC 18.433 TONNES ( A HUGE INCREASE FROM 10.6)

60,784.803 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

277,934.09 oz (some deleted august 3) JPM 8.644 TONNES

610,238.285 oz pledged June 12/2020 Brinks/ july 2/july 21 19.017 tonnes

67,289.041 oz Pledged August 21/regular account 1.588 tonnes jpm

total pledged gold: 1,613,198.634 oz 50.177 tonnes

total registered, pledged and eligible (customer) gold 37,518,127.513 oz 1,166.97 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1040.63 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

And now for the wild silver comex results

And now for the wild silver comex results

INITIAL STANDINGS

OCT. SILVER COMEX CONTRACT MONTH//INITIAL STANDING

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

1,818,995.360 oz

CNT

Brinks

Manfra

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

1,209,193.302 oz

CNT

Scotia

|

| No of oz served today (contracts) |

11

CONTRACT(S)

(55,000 OZ)

|

| No of oz to be served (notices) |

0 contracts

NIL oz)

|

| Total monthly oz silver served (contracts) | 2280 contracts

11,400,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

Former CFTC Chairman Admits Futures Can Be Used To Control Prices

October 29, 2020Financial Markets, Gold, Market Manipulation, Precious MetalsBitcoin, CFTC, cryptocurrencies, silver

Gold and silver futures have been used for decades to control the price of gold and silver. In fact, declassified letters )which can be found in the GATA archive) that bounced between Henry Kissinger and his advisors in the early 1970’s discuss the need for a market mechanism to help control the price of gold. Gold futures did not exist until 1974, three years after Nixon closed the gold window, shortly after which the Fed began to print money. The price of gold had more than quintupled between 1971 and 1974.

Fast forward to present times. A former CFTC Chairman, Christopher Giancarlo, was interviewed by CoinDesk a year ago. In that interview, he likely inadvertently admitted in reference to the creation of Bitcoin futures that futures contracts can be used to manipulate markets for the purpose of implementing and achieving official Government policies:

“One of the untold stories of the past few years is that the CFTC, the Treasury, the SEC and the [National Economic Council] director at the time, Gary Cohn, believed that the launch of bitcoin futures would have the impact of popping the bitcoin bubble. And it worked.” (CoinDesk)

Wittingly or unwittingly, that assertion by Mr. Christopher vindicates the contention – led by GATA starting in over 20 years ago and backed by reams of evidence – that gold and silver have been manipulated as part of official Government and Central Bank policy implementation to support fiat currencies and the dollar’s role as the reserve currency.

As an aside, I find it curious that Mr. Christopher states that the Government specifically identified Bitcoin as a bubble that needed to be deflated. Ever since the dot.com bubble of the late 1990’s, every Federal Reserve Chairman and FOMC member, starting with Alan Greenspan, as been adamant that investment bubbles are impossible to identify until AFTER they’ve popped. Yet, here is a former high level Government regulatory official explicitly stating that Bitcoin was not only identified as a bubble but that it needed to be deflated.

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

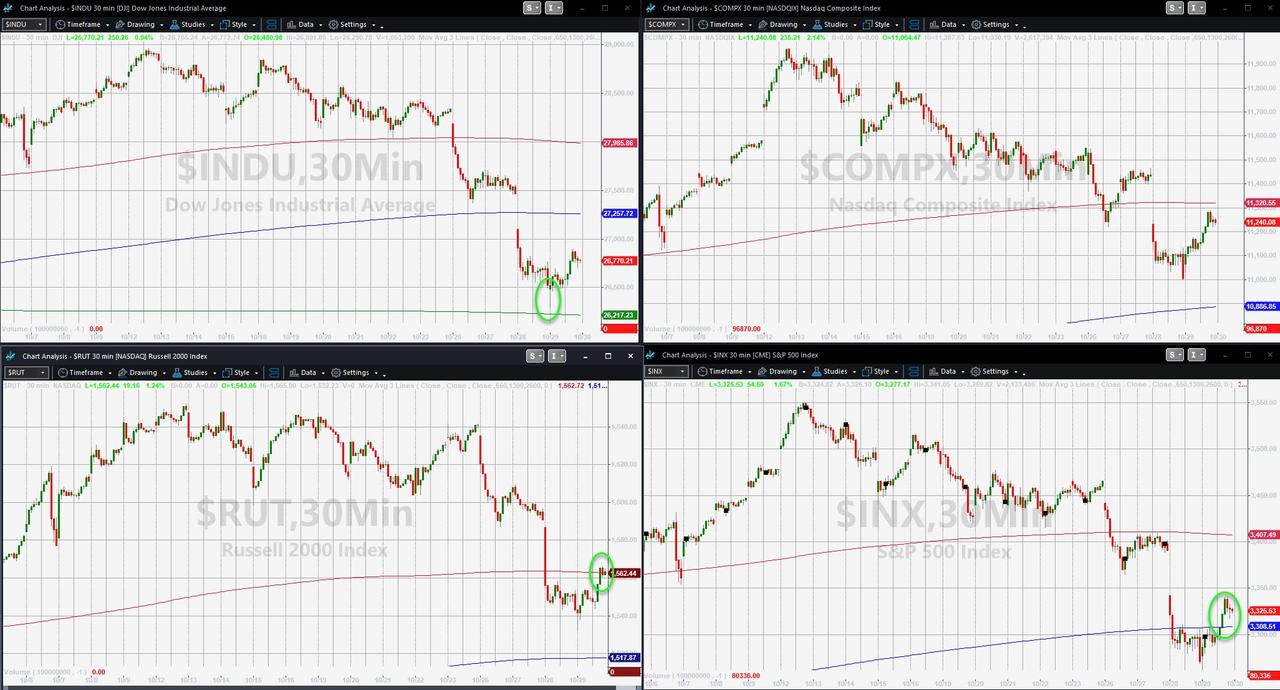

Stocks Struggle To Stabilize After Worst Rout Since June

US equity futures, European stocks and commodity markets rebounded after Wednesday’s rout which sent the S&P lower by 3.5%, the biggest one day drop since June 11, but they struggled to stabilize after a return to national lockdowns in Europe’s biggest economies.

“What I think has changed in the last few days is the significant spikes in the virus in Europe and the U.S, especially the U.S.” said Kempen Capital Management’s Chief Investment Officer Nikesh Patel. As a result, “the W-shaped scenario for the economy has now become consensus in the market” rather than one where economies broadly stabilize.

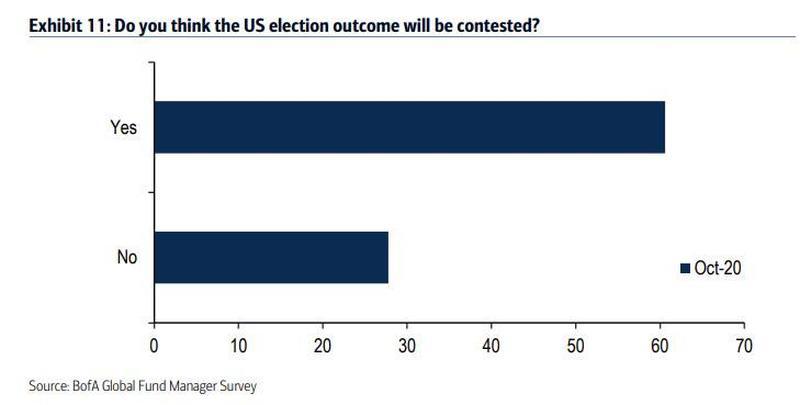

Global stock markets lost nearly $2 trillion yesterday, with volumes on the New York Stock Exchange up almost 40% to their highest level since September. In addition to 2nd and 3rd covid wave fears, investors are also increasingly wary of a contested U.S. election result that could unleash a wave of risk-asset selling. The VIX surged on Wednesday to its highest level since June and implied currency volatility indicates that a wild ride is expected. Marvell declines after it’s said to near a deal to acquire Inphi for about $10 billion.

“Market sentiment is turning, with investors buffeted by U.S. election uncertainty and now economic worries from rising Covid-19 cases across Europe,” said Kerry Craig, global market strategist at JPMorgan Asset Management. “These short-term forces are well beyond the control of individual investors, underscoring the need to maintain balance through the immediate uncertainty.”

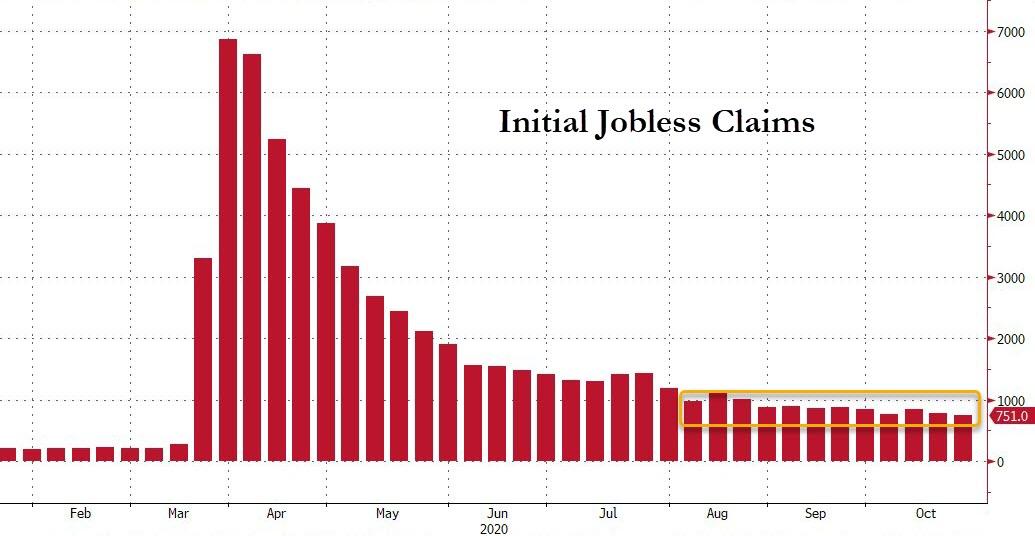

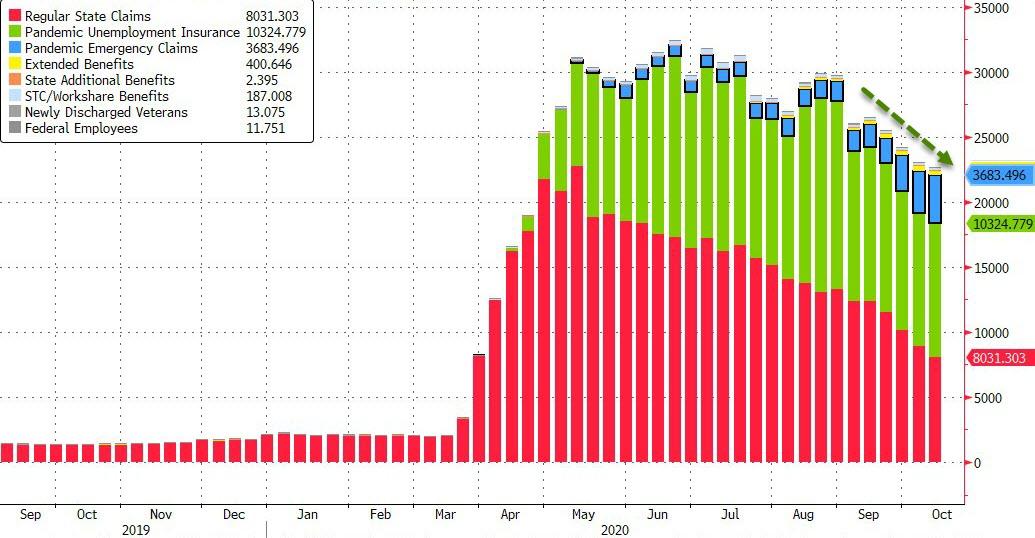

Economic data will be front and center today, with weekly initial jobless claims numbers expected to be slightly below last week’s 787000 as continuing claims drop below 8 million. The first reading of third-quarter GDP is also due at 830am and is forecast to be a record with annualized growth of more than 30% in the three months to the end of September as the U.S. economy reopened after the pandemic lockdown. Expect Trump to parade with the number as soon as it is out.

Ahead of today’s ECB meeting, European stocks got an earlier boost after earnings for telecoms firm BT Group, oil producer Royal Dutch Shell Plc and drinks giant Anheuser-Busch InBev all beat expectations, pushing their shares higher while Credit Suisse slipped after profit missed analyst estimates. Hopes that the ECB will signal it has more support to offer helped stemmed the rout that had wiped nearly 5% off European stocks on Wednesday, but the Stoxx 600 remained jittery and faded all early gains, trading unchanged at last check. Frankfurt’s DAX was up 0.5% in early trading, it was firmly on course for an 8% weekly drop which will be the steepest since the initial COVID panic of March.

Earlier in the session, Asian stocks were moderately lower, with the MSCI Asia Pacific Index down 0.3%. MSCI’s index of Asia-Pacific shares ex-Japan fell 0.6%, led by Australia, down 1.6%, and South Korea, down 1%. Japan’s Nikkei fell just 0.3%, while Chinese blue chips rose 0.5% and the yuan led a gentle bounce in Asian currencies against the greenback. Overnight, the Bank of Japan had made no changes to monetary policy settings as expected overnight, though it trimmed its growth forecasts to reflect sluggish services spending during summer.

“Asia is not really partaking in this second or third wave story because it’s got its COVID largely under control,” said Rob Carnell, chief economist in Asia at Dutch bank ING. “As a result, domestic economies look reasonable.”

As if to illustrate, Taiwan, which boasts Asia’s best-performing currency, marked its 200th straight day without local transmission on Thursday, while France and Germany prepared for lockdowns and as the virus sweeps across the U.S. Midwest.

In FX, the U.S. dollar edged up slightly and riskier currencies remained subdued. The Bloomberg Dollar Spot Index rebounded after droppping in the Asia session; the greenback traded mixed against its Group-of-10 peers as sentiment remained fragile, while the euro slipped for a fourth day. The pound strengthened versus the euro as European Union and U.K. negotiators made progress toward resolving some of the biggest disagreements, raising hopes that a Brexit deal could be reached by early November.

Elsewhere, the Aussie held up, despite paring an earlier gain, as local companies continued to buy the currency against the greenback to top up month-end hedging needs. The Norwegian krone swung from a gain to a loss as oil prices resumed their slump. The yen followed the dollar higher in early European trading. The Bank of Japan stood pat though Governor Haruhiko Kuroda said he stands ready to act if needed amid heightened uncertainty over a resurgence in the pandemic, though he still doesn’t see a pressing need to extend or change existing virus-response measures.

The euro hit a 10-day low on the dollar and a hundred-day low on the yen on Wednesday, before recovering slightly. It last traded at 1.1710 against the euro. Investors expect the ECB to similarly hold off on new measures, but to instead hint at action in December, which is likely to keep a lid on the euro.

“Given what is happening in France and Germany I think the ECB will talk about more stimulus even if they don’t deliver it today,” added Kempen’s Patel, referring to new COVID-19 restrictions announced this week.

In rates, benchmark U.S. 10-year yields had ticked up overnight to 0.7760, fading earlier losses as month-end extension flows may begin to support Treasuries. Treasury yields cheaper by up to 1bp across long-end of the curve, steepening 2s10s, 5s30s by 1.4bp and 0.3bp with front-end trading slightly rich. Treasury auctions conclude with $53b 7-year sale Thursday, after solid results from 2- and 5-year auctions so far this week. German government bonds were still in strong demand, with yields near seven-month lows.

In commodities, the rout continued, as WTI crude extended its decline to the lowest since the middle of June. Futures in New York slid as much as 3.4% to $36.11, the lowest intraday level since June 15. Brent also declined, falling as much as 3.3% to $37.82, also lowest since June. Gold was hammered as the dollar surged continued.

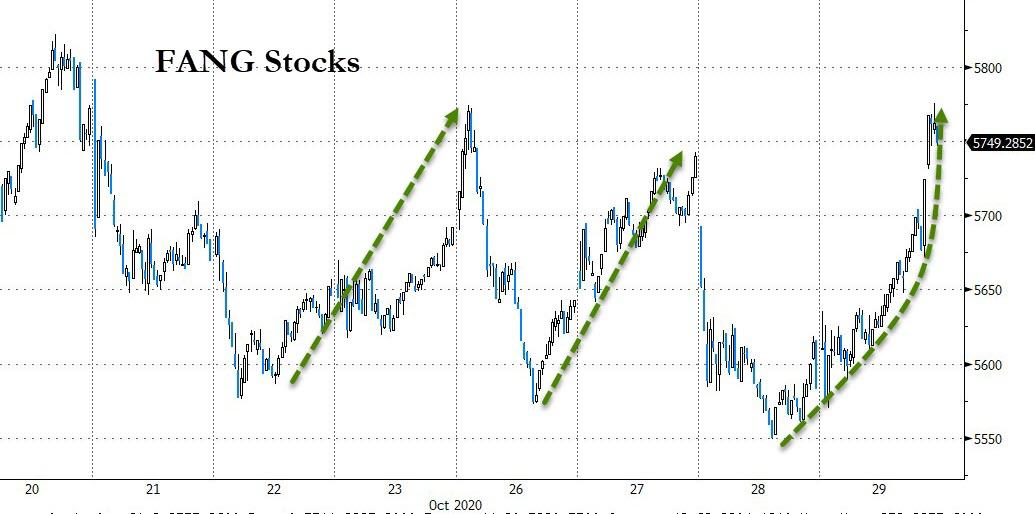

Economic data, including what is expected to be a blockbuster GDP report, and the ECB meeting are the main focus, with gathering uncertainty about Tuesday’s U.S. election also keeping investors on edge. Investors face a busy earnings day, with more than 70 S&P 500 members reporting, including Tech giants Apple, Amazon.com, Facebook and which are all scheduled to post results after the close.

Market Snapshot

- S&P 500 futures up 0.9% to 3,291.50

- STOXX Europe 600 up 0.3% to 343.01

- MXAP down 0.3% to 174.52

- MXAPJ down 0.5% to 577.78

- Nikkei down 0.4% to 23,331.94

- Topix down 0.1% to 1,610.93

- Hang Seng Index down 0.5% to 24,586.60

- Shanghai Composite up 0.1% to 3,272.73

- Sensex down 0.7% to 39,656.97

- Australia S&P/ASX 200 down 1.6% to 5,960.34

- Kospi down 0.8% to 2,326.67

- Brent Futures down 0.7% to $38.85/bbl

- Gold spot up 0.1% to $1,879.06

- U.S. Dollar Index up 0.1% to 93.50

- German 10Y yield rose 0.4 bps to -0.621%

- Euro down 0.1% to $1.1731

- Brent Futures down 0.7% to $38.85/bbl

- Italian 10Y yield rose 6.4 bps to 0.562%

- Spanish 10Y yield rose 2.3 bps to 0.201%

Top Overnight News from Bloomberg

- European Central Bank officials must decide on Thursday whether the renewed wave of coronavirus infections and lockdowns on the continent require an immediate dose of extra monetary support

- Germany and France will clamp down on movement for at least a month — coming close to last spring’s stringent lockdowns — with Germany’s daily caseload surpassing 20,000 for the first time amid a resurgence of Covid-19 across Europe

- Chancellor Angela Merkel defended her decision to once again severely limit movement in Germany, saying the country is in a “dramatic situation” as the rapid spread of the coronavirus stretches health-care services to their limit

- Coronavirus measures in England are failing to control the spread of the disease, scientists warned, adding pressure on U.K. Prime Minister Boris Johnson to introduce another national lockdown

- Italy sold benchmark bonds at the lowest average rate on record as support from the euro zone’s institutions and newfound political stability fueled demand for the securities

- Central banks became gold sellers for the first time since 2010 as some producing nations exploited near-record prices to soften the blow from the coronavirus pandemic

- For fragile oil markets, the outcome of next week’s U.S. election poses yet another risk: the prospect that major producer Iran may regain its role in international trade

A quick look across global markets courtesy of NewsSquawk

Asian equity markets traded mostly lower amid jitters following the bloodbath on Wall St where all major indices declined more than 3% and the DJIA fell over 900 points as risk appetite was decimated by concerns regarding lockdowns in France and Germany, whilst heavy losses were also observed in the tech sector. In addition, pre-election caution and comments from NIH’s Fauci that a vaccine won’t be available until January at the earliest added to the downbeat tone, although US stock index futures nursed some losses overnight after encouraging updates from both Regeneron and Eli Lilly regarding their COVID-19 treatment trials and with the US said to provide Huawei a lifeline by allowing more companies to supply the Chinese tech giant with components as long as it is unrelated to 5G. Nonetheless, Asian bourses weakened with tech and commodity-related sectors the underperformers in the ASX 200 (-1.6%) and financials were also pressured after ANZ Bank reported a 42% decline in full-year profit and Westpac reached an agreement to settle a BBSW class action in US. Nikkei 225 (-0.4%) was subdued following weak retail sales data and as participants awaited the BoJ policy announcement, which proved to be a damp squib as the central bank maintained policy settings as expected and continued to signal a lack of urgency for immediate support, although some of the losses have been pared amid mild currency outflows and as earnings supported the likes of Sony and Hitachi, while the KOSPI (-0.8%) suffered after Samsung Electronics failed to benefit from its final Q3 results which despite printing an increase from the prior year, it also flagged a decline in chip and mobile profitability for Q4. Hang Seng (-0.5%) and Shanghai Comp. (+0.1%) were cautious ahead of several blue-chip earnings including the first of the big 4 banks and with participants looking out for details of the 5-year plan when the 4-day plenum concludes today. Finally, 10yr JGBs failed to benefit from the broad risk-aversion and instead tracked the recent declines in T-notes with demand constrained amid the BoJ policy announcement in which the central bank provided a somewhat balanced tone that suggested it was likely to remain on the fence on future measures.

Top Asian News

- BOJ Stands Pat But Paints Gloomier Picture of Economy This FY

- India to Prioritize Covid Vaccine for Front Line Health Workers

- China’s Busiest Earnings Day to Shed Light on Economy

- Takeda to Supply Japan With 50m Doses of Moderna Vaccine

European equities (Eurostoxx 50 flat) have been relatively choppy thus far with regional indices unable to stage any meaningful recovery from yesterday’s heavy losses. Ahead of the cash open, futures at one stage suggested that European equities would look to claw back some of the declines seen yesterday, however, this has failed to materialise thus far as market participants fret over the economic impact of recent nationwide lockdown measures taken by France and Germany. It has been an exceptionally busy morning of earnings in Europe with divergences between different industries mostly a by-product of large-cap corporate updates. Tech has been one of the top performers thus far in the wake of yesterday’s tech-heavy losses on Wall St, with sentiment for the sector also aided by earnings from ASM International (+4.1%) who subsequently raised Q4 guidance amid strong demand. Capping gains for the tech sector is Nokia (-16.6%) after Q3 results fell short of analyst estimates and the Co. cut its FY profit outlook amid declining market shares in certain regions. Despite losses in the crude complex, oil & gas names have seen support throughout the session amid Q3 earnings from Shell (+2.1%) which saw the Co. exceed estimates for adjusted earnings and lift its dividend. Banking names are lower on the session amid losses in Credit Suisse (-6.0%) after Q3 profits missed analyst expectations, overshadowing the Co.’s decision to increase its dividend by 5% for 2020 and schedule CHF 1.5bln of share buybacks for next year. Lloyds (+3.7%) have provided some reprieve for the sector after the Co. beat on Q3 profits and noted a surge in the demand for mortgages. Volkswagen (+3.1%) are higher on the session after Q3 profits were bolstered by increasing auto demand from China, offsetting losses elsewhere. Of note for telecom names, (asides from Nokia who are also in the Stoxx 600 tech index), BT (+5.4%) and Orange (+4.6%) are firmer post-earnings, whilst Telefonica (-4.5%) are a laggard in the sector after Q3 results underwhelmed. Finally, AB Inbev (+2.9%) have acted as a source of support for the food & beverage sector after Q3 revenues beat estimates and the Co. stated that H2 performance will be better than H1.

Top European News

- Janus Henderson Sees Investor Withdrawals Slow in Third Quarter

- Germany, France Impose Month-Long Curbs to Rein in Virus

- BT Lifts Profit on Pandemic, Sheds Jobs to Cut Costs

- German Pig Backlog May Cram 1.2 Million Extra Hogs on Farms

In FX, far from all change in terms of the general market tone that remains suppressed and highly contingent on daily coronavirus developments, but a comparative air of calm has returned following Wednesday’s FTQ. As such, the so called cyclical, activity or high beta currencies are on a more even keel, albeit still precarious and prone to any headline bearing bad news on the COVID-19 front that could have adverse economic implications on top of the obvious social and human cost. Aud/Usd is modestly firmer and straddling 0.7050, Nzd/Usd is pivoting 0.6650 with some independent traction via improvements in NBNZ business confidence and especially the outlook for activity, while Usd/Cad has pared back from post-BoC highs to rotate around 1.3300 even though crude prices remain depressed. Next up for the Loonie, Canadian average weekly earnings and building permits, while the Aussie might be mindful of a decent 1 bn expiry option in the Aud/Jpy cross at 73.20.

- JPY/GBP/CHF/EUR – All narrowly mixed against the Dollar, as the Yen continues to fend off pressure below 104.50 that coincides with a key Fib level and has capped the pair for the last 2 trading sessions. However, 104.00 remains elusive and Usd/Jpy may remain supported into the round number given expiry interest at the strike in 1.8 bn. For the record, nothing new from the BoJ overnight, but top tier Japanese data looms in the form of CPI, jobs and IP. Elsewhere, Sterling continues to encircle 1.3000 on hopes of a key Brexit breakthrough and the Pound is outperforming vs the Euro just shy of 0.9000 compared to 0.9050 at the other extreme even though latest reports on UK-EU trade talks appear less positive than yesterday. Perhaps the proximity of 1.1 bn expiries between 0.9050-60 are impacting, or the fact that Eur/Usd is treading cautiously into the ECB within a 1.1758-26 range and flanked by expiry interest (1.3 bn from 1.1750-55 and 1.5 bn from 1.1725-15). Meanwhile, the Franc is largely tracking Buck moves on the 0.9100 axis as the DXY meanders from 93.560 to 93.237 in the run up to advance US Q3 GDP, weekly IJC tallies, pending home sales and more heavyweight corp earnings.

- SCANDI/EM – The aforementioned recoil in oil has hit the Nok back below 11.0000 vs the Eur and beyond recent lows, while in contrast the Cnh and Cny are both paring losses after another weaker PBoC midpoint fix and reports of Chinese bank selling of the onshore Yuan against the Greenback in spot and forward terms. However, the Try is struggling again just off sub-8.3200 record lows vs the Dollar and Brl looks set for catch-up declines after the BCB held rates last night, as expected, but acknowledged strong upside inflation pressure in the short term that requires close attention.

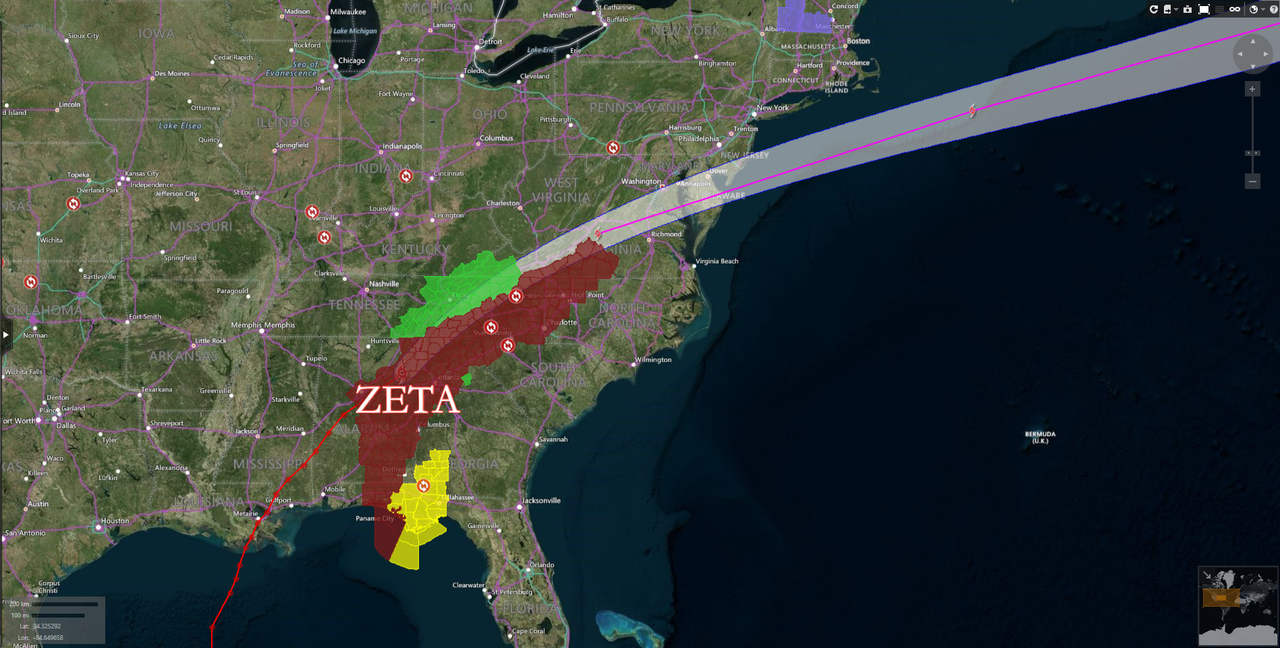

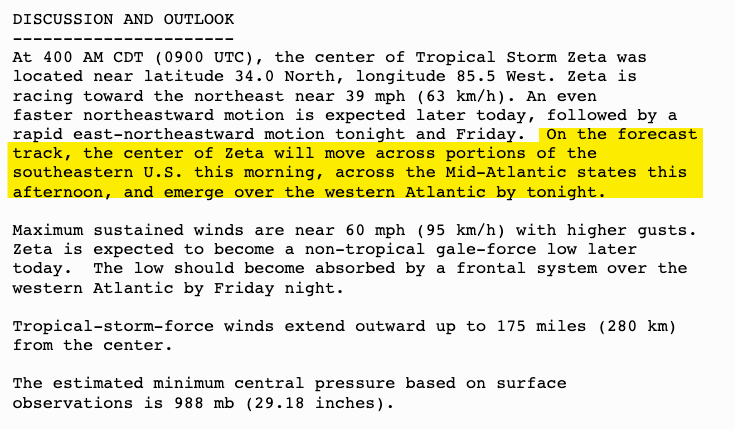

In commodities, WTI and Brent front month futures have come under pronounced pressure this morning as the complex was unable to partake in the European-earnings fuelled bounce in the equity futures around the cash equity open on the back of a number of well-received European earnings. As such, throughout the European morning the crude benchmarks have continued to deteriorate moving below the psychological USD 37/bbl & 36/bbl and USD 39/bbl for WTI and Brent respectively; and most recently in proximity to the USD 36/bbl & USD 38/bbl marks. Updates throughout the session explicitly for the crude complex have been sparse after the BSEE report showed further oil outage within the Gulf of Mexico but Storm Zeta is now forecast to continue weakening throughout the day and as such, assuming no damage occurred, platforms should begin returning to service in the near-term. Elsewhere, on the OPEC+ front Energy Intel reports indicate the cartel are considering extending oil output cuts at their current levels through to the end of March; reports which will likely garnering more focus as we approach the next JMMC and full OPEC+ gathering next month. Moving to metals, spot gold is essentially flat on the day perhaps as it struggles to garner clear direction from sentiment this morning which is choppy and diverging somewhat amongst asset classes thus far. Price-wise, the precious metal is little differed on the session around the USD 1875/oz mark.

Top Overnight News from Bloomberg

- 8:30am: Initial Jobless Claims, est. 770,000, prior 787,000; Continuing Claims, est. 7.78m, prior 8.37m

- 8:30am: GDP Annualized QoQ, est. 32.0%, prior -31.4%

- 8:30am: Personal Consumption, est. 38.9%, prior -33.2%

- 8:30am: GDP Price Index, est. 2.9%, prior -1.8%

- 8:30am: Core PCE QoQ, est. 4.0%, prior -0.8%

- 9:45am: Bloomberg Consumer Comfort, prior 46.6

- 10am: Pending Home Sales MoM, est. 3.0%, prior 8.8%; Pending Home Sales NSA YoY, est. 23.0%, prior 20.5%

DB’s Jim Reid concludes the overnight wrap

Its been a pretty sobering week so far for life as we knew it and for markets even if futures are a little more buoyant this morning. Risk assets buckled yesterday under the weight off fresh restrictions, especially those in the two largest European economies.

As we previewed 24 hours ago German Chancellor Merkel has reached a deal with leaders of the country’s 16 states over a one-month partial lockdown. Starting on Monday, and through to the end of November at least, restaurants, bars and nightclubs will be closed. Leisure facilities such as gyms, event venues, cinemas and amusement parks will also be closed. Residents will only be allowed out with those in their own household and one other, while gatherings will be limited to 10 people. Private travel and visits to relatives are discouraged. However unlike last Spring, schools and day cares shall remain open as well as hairdressers. As we also previewed yesterday French President Macron also announced tougher restrictions including the shuttering of bars and restaurants, banning domestic travel and public gatherings, closing non-essential retailers and encouraging work-from-home if possible. As in Germany, schools will remain in session. The measures are currently in place until at least 1 December which will gives some hope for the Xmas holiday season.

In Germany these restrictions are probably less severe than they could have been and probably sound more extreme than they are but the direction of travel is going to wrong way with perhaps 5 months of the peak flu/cold/virus season still ahead of us unlike the first wave when we only had a month or so of the normal peak period left when it struck. Our German economists expect that the lockdown measures should result in a Q4 GDP decline of at least -0.5% qoq. The hospitality industry and cultural institutions will suffer most again under the new restrictions. That contraction would still be consistent with a -5.6% FY20 GDP drop predicted by our economists, assuming that the upside risks to their Q3 call (+6%) materialises. See here for more of their thoughts and here for the immediate thoughts of our French economist.

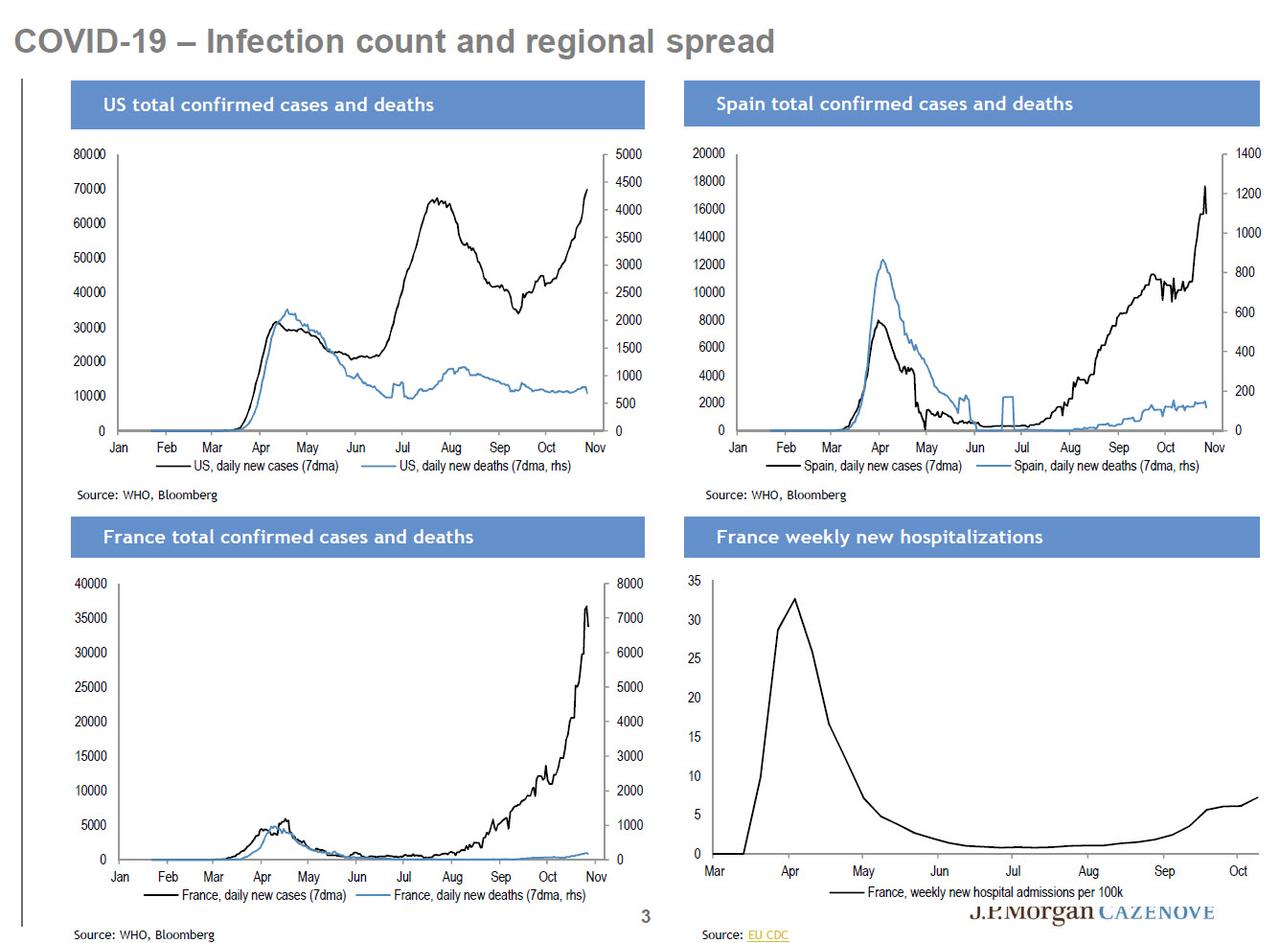

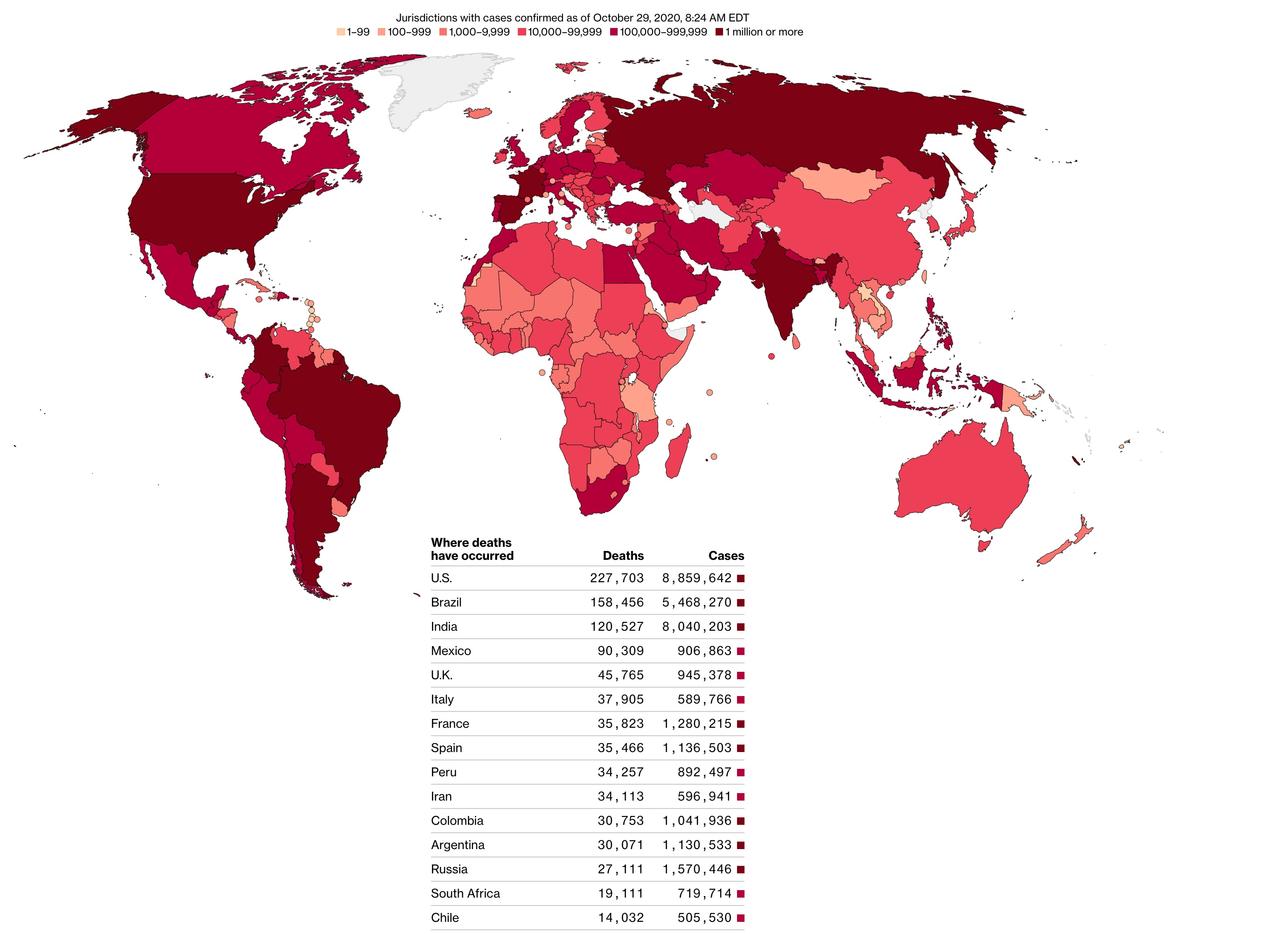

There’s an inevitability that other countries will go down the same path soon. A new study from Imperial College London and Ipsos Mori has indicated that the infections in England are doubling every nine days and an estimated 960,000 people are carrying the virus on any one day. In better news, the Guardian has reported overnight that the UK government has asked local health officials to deploy 30-minute saliva kits for coronavirus testing to accelerate the mass screening plan. The test plan is to cover as many of 10% of England’s population for coronavirus every week. Also overnight, Regeneron Pharmaceuticals said that data from a late stage trial indicated that its antibody cocktail therapy significantly reduces virus levels and the need for further medical care. Lastly, European Union leaders are planning to discuss adopting a singular approach to the practice of rapid antigen tests, which are faster than the PCR counterpart and could therefore allow for a more open economy. For more on how the virus is spreading see the table below.

Given the negative direction of restriction travel, US equities had their worst day since 11 June, with the S&P 500 down -3.53% and the VIX up +6.9pts to over 40 for the first time since the same day. That was when there was the original outbreak of covid-19 cases throughout the US Sunbelt. While the VIX is still considerably lower than we saw during the worst of the pandemic-induced selloff in March of this year, you have to go back to 2015 to see the equity volatility index at this level outside of the pandemic. The selloff was very broad with 97% of the S&P lower and the decline was led by Transportation (-4.86%) Software (-4.47%), Tech hardware (-4.45%) and Energy (-4.22%). The tech losses saw the NASDAQ fall -3.73%, the most since early September. It’s a big day for FANG earnings today with Facebook, Amazon, Apple and Alphabet all reporting.

Asian markets are seeing some respite this morning. The Nikkei (-0.33%), Hang Seng (-0.77%), Shanghai Comp (-0.12%) and Kospi (-1.05%) are mildly lower but with futures on the S&P 500 up +1.11% and those on the Stoxx 50 up +0.58%. Yields on 10y USTs are back up +1.2bps. Elsewhere, the BoJ kept it monetary policy unchanged at today’s meeting even as it further trimmed the growth forecast for the year ending in March to -5.5% yoy (from -4.7% yoy previously). In terms of overnight data, Japan’s September retail sales came in at -8.7% yoy (vs. -7.6% yoy expected).

In other overnight news, the FT has reported that the US is allowing a growing number of chip companies to supply Huawei with components as long as these are not used for its 5G business. If true, this will likely offer respite to Huawei’s smart phone arm. Separately, the FT has also reported that Tiffany’s board has approved the sale to LVMH at a lower price. Elsewhere, Standard Chartered beat earnings estimates overnight as loan losses eased. The bank also said that it has ample room to fund growth and pay dividends next year, pending approval from regulators. Boeing has said that it will eliminate an additional 7,000 jobs bringing the expected losses from layoffs, retirements and attrition to 30,000 people (19% of the pre-pandemic workforce) by the end of 2021.

Before all this, European equities fell to their lowest level in just over five months yesterday, with the STOXX 600 retreating -2.95% as 97% of the index also trading lower. Here it was led by cyclicals such as Autos (-4.81%), Chemicals (-3.71%) and Banks (-3.56%). The DAX (-4.17%) and CAC 40 (-3.37%) fell further on their shutdown lite news.

Sovereign yields in Europe declined for a third straight day after much of the focus last week was on their recent sharp rise. However the rally was relatively minimal given the large risk off. Gilts were down -1.9bps to 0.21% and 10yr bunds were down -1.0bps to -0.625%, steadily approaching 7 month lows. Whereas US Treasuries yields were actually up +0.3bps to 0.771% as there may have been some deleveraging of positions. Meanwhile the US dollar rallied +0.50%, the most in over a month. This partly led to gold (-1.61%) having its worst day in 2 weeks.

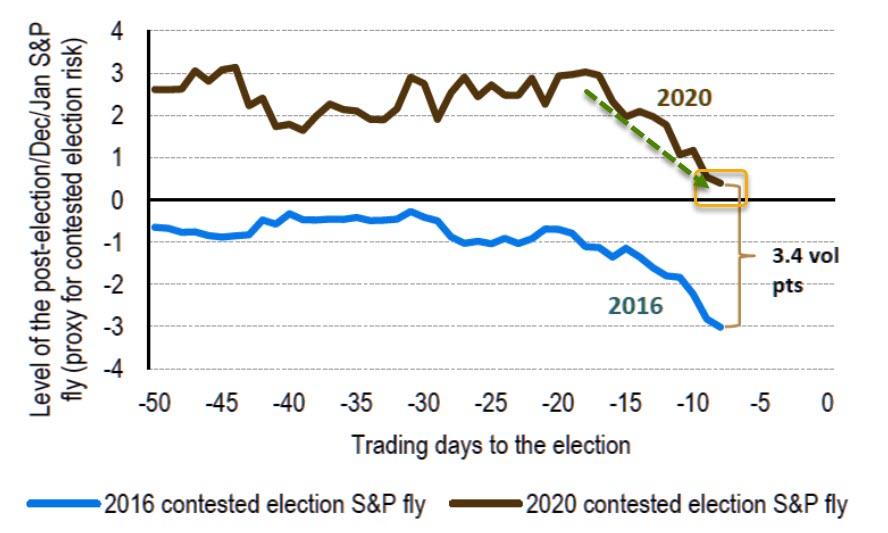

On the US Election, much of the focus remains on the Presidency, where former Vice President Biden remains an 88% to 11% favourite over President Trump in the fivethirtyeight model. The Democrats also remain favourite to gain control of the Senate (75% chance), though the number of seats is more uncertain. Republicans currently control the upper chamber 53-47 and considering that Democrats are very likely to lose a seat in Alabama, Democrats will need to win 4 seats and the Presidency to win control (the Vice President is the tie breaker). Using a mix of polls and past voting behaviour of the states Colorado (84% chance of Democrats winning according to fivethirtyeight) and Arizona (79%) are the Democrats best bets to turn blue. After that it is Maine (61%) and North Carolina (63%), which have tightened in recent days but in Maine the Democratic challenger has not lost a poll in weeks. In NC the challenger has only lost one in the last 3 weeks. After that the attention should be on Iowa (57%) and Georgia (33% and 64%), where the latter has a pair of Senate elections this year, in one of which the Democratic candidate is slightly favoured.

One interesting wrinkle this year is clearly the large number of early and mail-in votes. In states like Florida they have already seen 70% of the number of voters from 2016, Texas is at 91% (with little mail-in), North Carolina at 76.1% and Georgia at 76.8%. If current polling holds or the polling error happens to go in the Democrat’s favour – as happened in 2012 – it could be a quick night with North Carolina and Florida announcing fairly quickly, on the other hand a Trump win in those states and we could be waiting a week to hear the outcome out of the Midwest, namely Pennsylvania, Wisconsin and Michigan.

Given the historically divergent views on economic policy between the two candidates, our chief US economist Matt Luzzetti, considers the implications of the various election outcomes on the economic outlook in a new podcast which you can listen to here. He and his team have also refreshed their 2020 Election chartbook (found here) which contains sections on updated polling, projections, battleground states, and Congressional races.

Today we will hear from the ECB and our European economists (preview here ) expect the policy stance to be left unchanged, but that the ECB will also warn of growing downside risks amid an already weak outlook for inflation. This is likely to open the door to a further easing of policy in December. By then, there’ll be far more information on the status of the pandemic, the effect of the recent spate of shutdowns and the ECB staff will have updated their macroeconomic projections. These include the publication of the first estimates for growth and inflation for 2023.

Outside the ECB, today’s highlight’s include German October unemployment and CPI, along with Italian and Euro Area consumer confidence. In the US there is weekly initial jobless claims, Q3 GDP, personal consumption core PCE, and pending home sales. Lastly we will have Japan’s jobless rate and industrial production. In earnings we have the big ones with Apple, Amazon, Alphabet and Facebook along with Comcast, Sanofi, AB InBev, American Airlines.

3A/ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 3.49 PTS OR .11% //Hang Sang CLOSED DOWN 122.20 PTS OR .49% /The Nikkei closed DOWN 86.57 POINTS OR 0.37%//Australia’s all ordinaires CLOSED DOWN 1.50%

/Chinese yuan (ONSHORE) closed /Oil DOWN TO 35.94 dollars per barrel for WTI and 37.47 for Brent. Stocks in Europe OPENED ALL RED// ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7140. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7174 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

CHINA/USA

4/EUROPEAN AFFAIRS

FRANCE/TURKEY

Funny: Charlie Hebdo at it again and sparks Turkish fury as a cartoon of Erdogan looking up a skirt of a woman wearing a hijab.

(zerohedge)

France’s Charlie Hebdo Sparks Turkish Fury With Cartoon Of “Erdogan In Private”

A new satirical cartoon from the French weekly Charlie Hebdo has sparked fury in Turkey and is worsening the diplomatic spat between Turkey and France after Paris already recalled its ambassador when President Erdogan questioned Macron’s mental health while accusing the French president of attacking Islam over remarks made in the wake of the horrific beheading of a middle school teacher Samuel Paty on October 16.

The latest edition of the newspaper, first released online Tuesday night, features a front page cartoon mocking President Recep Tayyip Erdogan – he’s in his underpants, holding a can of beer and gazing up a skirt of a hijab wearing woman.

“Ooh, the prophet!” the character says in the French speech bubble, with the title reading: “Erdogan: in private, he’s very funny”.

It has set off outrage among the Turkish public especially after Erdogan shot back Wednesday saying the “worthless” cartoon had nothing to do with free speech but is in reality an attack on Islam. He accused European countries of wanting to “relaunch the Crusades“. There’s also been growing demonstrations in other parts of the Middle East over charges of France’s “anti-Islamic” stance.

Erdogan’s top press aide, Fahrettin Altun, additionally said in a tweet: “We condemn this most disgusting effort by this publication to spread its cultural racism and hatred.”

“French President Macron’s anti-Muslim agenda is bearing fruit! Charlie Hebdo just published a series of so-called cartoons full of despicable images purportedly of our President,” he added.

On Monday Erdogan called for aTurkish boycott of all French goods over what he called France’s ‘anti-Islamic’ stance towards Muslims and the Turkish people. Erdogan had said during a televised speech in Ankara: “As it has been said in France, ‘don’t buy Turkish-labelled goods’, I call on my people here. Never give credit to French-labelled goods, don’t buy them.”

Meanwhile Erdogan is threatening to sue every European leader that posts or defends the cartoons, as is happening with a Dutch politician:

Macron has emphasized a freedom of speech message, vowing that the French “not give up our cartoons” – in reference to both the latest row but also the events and controversy surrounding the January 7, 2015 Charlie Hebdo massacre, which left 12 people dead after the newspaper published a series of cartoons perceived as mocking the founder of Islam Muhammad.

According to Reuters, Turkey has launched an investigation into the French newspaper, saying it will take “all necessary legal, diplomatic steps against Charlie Hebdo caricature on President Recep Tayyip Erdogan.”

END

But…..

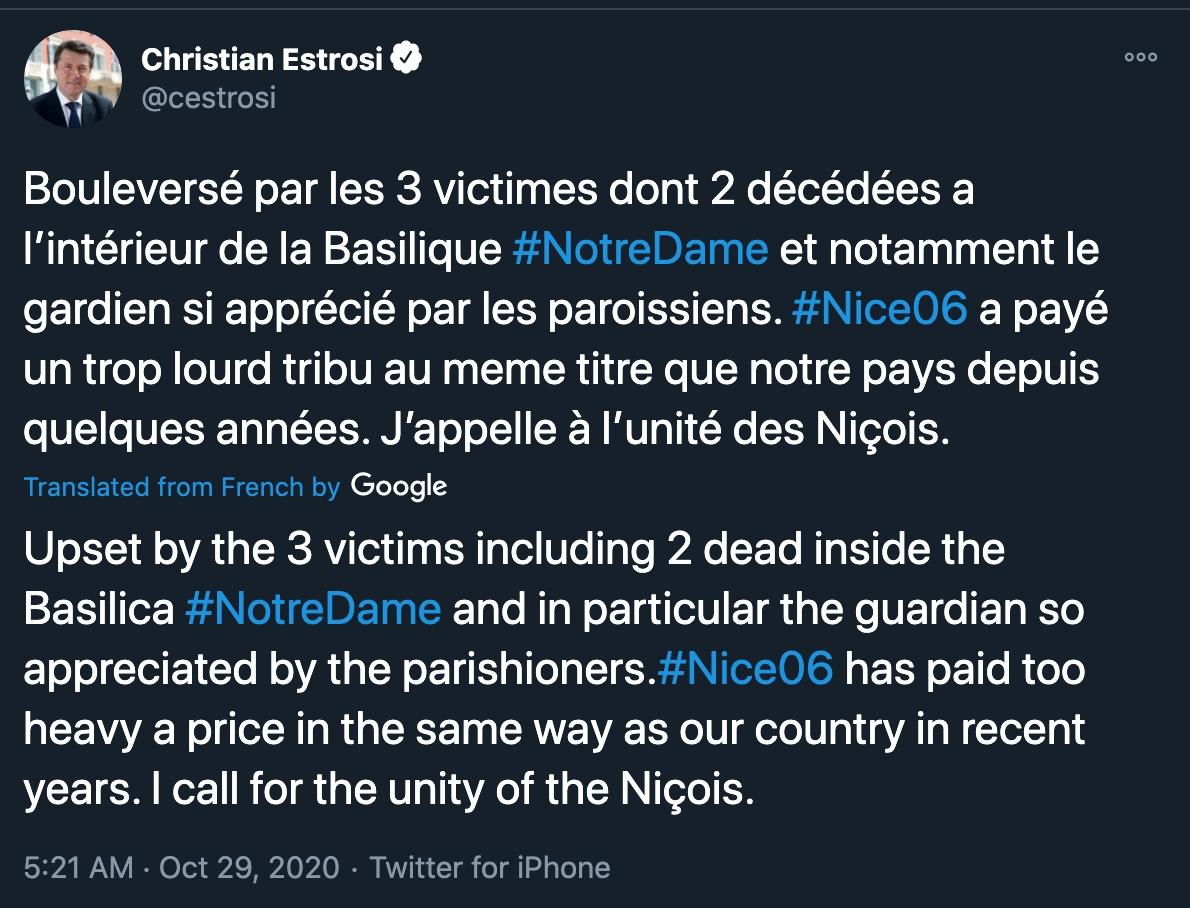

3 Killed, 1 Decapitated, In 2nd Gruesome Terror Attack To Rattle France In 2 Weeks

Update (0800ET): Just as a front-page Charlie Hebdo illustration was provoking a major diplomatic snafu after criticizing President Erdogan, Turkey has spoken up to “strongly condemn” Thursday’s attack in Nice, despite Turkish officials joining the chorus of critics suggesting Macron’s new terror crackdown was “Islamophobic”.

We imagine we’ll be hearing more apologies like this from the leaders of Pakistan

* * *

Update (0730ET): Reuters has confirmed that three have now been confirmed killed, with one woman having been decapitated, by the terrorist who carried out this morning’s attack. The attack was carried out during a morning gathering at Notre Dame church, the largest church in the city of Nice.

One of those killed was the Church warden.

As top French law enforcement officials meet with the minister of the Interior, French President Emmanuel Macron is on his way to Nice.

To recap:

In what appears to be the second major French terror attack in two weeks, at least two have been killed and one critically injured in a brutal knife attack that occurred during the morning service of a local Catholic church – Notre Dame basilica – in Nice.

In an echo of the brutal attack on a schoolteacher that recently galvanized the French government to launch a major anti-terror crackdown, reports claimed that at least one of the victims had been decapitated, like the teacher was.

The incident is believed to be terror-related according to the city’s mayor. The suspect is reportedly alive, and has been taken into custody by police. A security perimeter has been set up around the church the city said, and it’s almost completely empty except for armed guards.

Witnesses on social media reported hearing shots fired as armed police responded to the incident, one reported hearing at least seven shots. The national police in France have urged the public to avoid the area, while cautioning that there’s no need to panic.

He wrote on Twitter: “I am on site with the @PoliceNat06 and the @pmdenice who arrested the perpetrator of the attack. I confirm that everything suggests a terrorist attack in the Basilica of Notre-Dame de #Nice06.”

Estrosi told reporters that “Islamofacism” is at the heart of these attacks, and that the attacker reportedly shouted “Allah Akbar” – or “God is Great” in Arabic.

French Interior Minister Gérald Darmanin said he was convening a crisis meeting at the ministry in Paris.

Of course, these same leaders do nothing when China imprisons and tortures millions of Muslims.

This latest attack, we suspect, will only serve to further galvanize public support for an aggressive dismantling of terror networks, while also directing more support to Marine Le Pen and the French right.

‘Massive Traffic Jams’ Across Paris As People Flee Ahead Of Second COVID Lockdown

On Wednesday, French President Emmanuel Macron announced that France would enter a full lockdown from midnight on Thursday until the end of November due to the second wave of the coronavirus pandemic.

With hours to go before the month-long national lockdown takes effect, videos have surfaced on Twitter, showing massive traffic jams of people trying to escape the city as lockdowns go into effect.

“Traffic is barely moving in every direction as far as the eye can see. Lots of honking and frustrated drivers,” said one Twitter user.

Another Twitter user suggests “traffic jams around Paris tonight” could be due to “people leaving the capital before lockdown.”

Using real-time data to confirm, that, in fact, the videos posted by citizen journalists in Paris are accurate – TomTom traffic data shows much of the city is in serious gridlock.

TomTom real-time data shows a massive spike in Traffic Thursday night, the highest congestion so far this week, as lockdowns are only a few hours away.

While people flee Paris ahead of lockdowns, it wouldn’t be shocking if anti-lockdown protests flared up across the city this weekend.

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Satellite Images Show Iran Rebuilding Natanz Nuclear Centrifuge Site After Sabotage

Iran has launched a major construction project at its controversial Natanz nuclear facility according to satellite imagery featured Wednesday in the Associated Press. Allegedly an underground advanced centrifuge assembly plant is being reconstituted after it was previously destroyed by fire.

A mystery blast and fire on July 2nd had disabled operations at the facility, which later in the summer Iran’s Atomic Energy Organization declared was an act of sabotage and not due to an accident. It’s widely believed that Israeli intelligence was behind the sabotage to disable advanced centrifuge operations there.

Recall that before and after the fire which caused severe damage, setting back the development of advanced uranium enrichment centrifuges, there was a series of ‘mystery’ explosions and fires at various military and industrial sites across Iran, raising suspicions of a major Israeli or even US-backed covert campaign to destabilize the country’s defense and nuclear energy infrastructure.

While the White House exit from the 2015 nuclear deal (JCPOA) and recent ‘maximum pressure’ campaign was aimed at derailing what Washington claims are Iran’s nuclear ambitions, it appears to have done the opposite and strengthened Tehran’s resolve, also while under crippling sanctions.

As the AP underscores, the timing of the construction efforts couldn’t be worse for the Trump White House: “The construction comes as the U.S. nears Election Day in a campaign pitting President Donald Trump, whose maximum pressure campaign against Iran has led Tehran to abandon all limits on its atomic program, and Joe Biden, who has expressed a willingness to return to the accord.”

The report says further, “The outcome of the vote likely will decide which approach America takes. Heightened tensions between Iran and the U.S. nearly ignited a war at the start of the year.” Biden is seen as the candidate most likely to reenter the JCPOA agreement assuming Iran walks back its enrichment to come under caps stipulated by the Obama-era deal.

“Since August, Iran has built a new or regraded road to the south of Natanz toward what analysts believe is a former firing range for security forces at the enrichment facility, images from San Francisco-based Planet Labs show,” AP details.

“A satellite image Monday shows the site cleared away with what appears to be construction equipment there,” it says of the Planet Labs images.

The Armenian-Azerbaijani War After One Month

Submitted by SouthFront.org,

After a month of war, the Turkish-Azerbaijani bloc continues to keep the initiative in the conflict, exploiting its advantage in air power, artillery, military equipment and manpower. The coming days are likely to show whether Ankara and Baku are able to deliver a devastating blow to Armenian forces in Karabakh in the nearest future or not.

If Armenian forces repel the attack on Lachin, a vital supply route from Armenia to Nagorno-Karabakh, they will win the opportunity to survive till the moment when the ‘international community’ finally takes some real steps to pressure Turkey and Azerbaijan enough to force them to stop the ongoing advance. If this does not happen, the outcome of the war seems to be predetermined.

Meanwhile, Azerbaijani forces continue their advance in the region amid the failed US-sponsored ceasefire regime. Their main goal is Lachin. In fact, they have been already shelling the supply route with rocket launchers and artillery. The distance of 12-14km at which they were located a few days ago already allowed this. Now, reports appear that various Azerbaijani units are at a distance of about 5-8 km from the corridor. Armenian forces are trying to push Azerbaijani troops back, but with little success so far.

The advance is accompanied by numerous Azerbaijan claims that Armenian forces are regularly shelling civilian targets and that the ongoing advance is the way to deter them. Baku reported on the evening of October 27 that at least four civilians had been killed and 10 wounded in Armenian strikes on Goranboy, Tartar and Barda. On the morning of October 28, the Armenians allegedly shelled civilian targets in Tovuz, Gadabay, Dashkesan, and Gubadl.

On the morning of October 28, the Azerbaijani Defense Ministry claimed that in response to these Armenian violations its forces had eliminated a large number of enemy forces, an “OSA” air-defense system, 3 BM-21 «Grad» rocket launchers, 6 D-30, 5 D-20, and 1 D-44 howitzers, 2 2A36 «Giatsint-B» artillery guns, a 120 mm mortar, a “Konkurs” anti-tank missile and 6 auto vehicles.

On October 27, Azerbaijani sources also released a video allegedly showing the assassination of Lieutenant General Jalal Harutyunyan by a drone strike. Azerbaijani sources claim that he was killed. These reports were denied by the Armenian side, which insisted that the prominent commander was only injured. Nonetheless, the Karabakh leadership appointed Mikael Arzumanyan as the new defense minister of the self-proclaimed republic.

On the evening of October 27 , the Armenian Defense Ministry released a map showing their version of the situation in the contested region. Even according to this map, Armenian forces have lost almost the entire south of Nagorno-Karabakh and Azerbaijani forces are close to the Lachin corridor. An interesting fact is that the Armenians still claim that the town of Hadrut is in their hands. According to them, small ‘enemy units’ reach the town, take photos and then run away.

Al-Hadath TV also released a video showing Turkish-backed Syrian militants captured during the clashes. Now, there is not only visual evidence confirming the presence of members of Turkish-backed militant groups in the conflict zone, but also actual Syrian militants in the hands of Armenian forces.

Experts who monitor the internal political situation in Armenia say that in recent days the Soros-grown team of Pashinyan has changed its rhetoric towards a pro-Russian agenda. Many prominent members of the current Pashinyan government and the Prime Minister himself spent the last 10 years pushing a pro-Western agenda. After seizing power as a result of the coup in 2018, they then put much effort into damaging relations with Russia and turned Armenia into a de-facto anti-Russian state. This undermined Armenian regional security and created the conditions needed for an Azerbaijani-Turkish advance in Karabakh. Now, the Pashinyan government tries to rescue itself by employing some ‘pro-Russian rhetoric’. It even reportedly asked second President of Armenia Robert Kocharyan to participate in negotiations with Russia as a member of the Armenian delegation. It should be noted that the persecution of Kocharyan that led to his arrest in June 2019 was among the first steps taken by Pashinyan after he seized power. Kocharyan was only released from prison in late June 2020. Despite these moves in the face of a full military defeat in Karabakh, the core ideology of the Pashinyan government remains the same (anti-Russian, pro-Western and NATO-oriented). Therefore, even if Moscow rescues Armenia in Karabkah, the current Armenian leadership will continue supporting the same anti-Russian policy.

6.Global Issues

CORONAVIRUS UPDATE

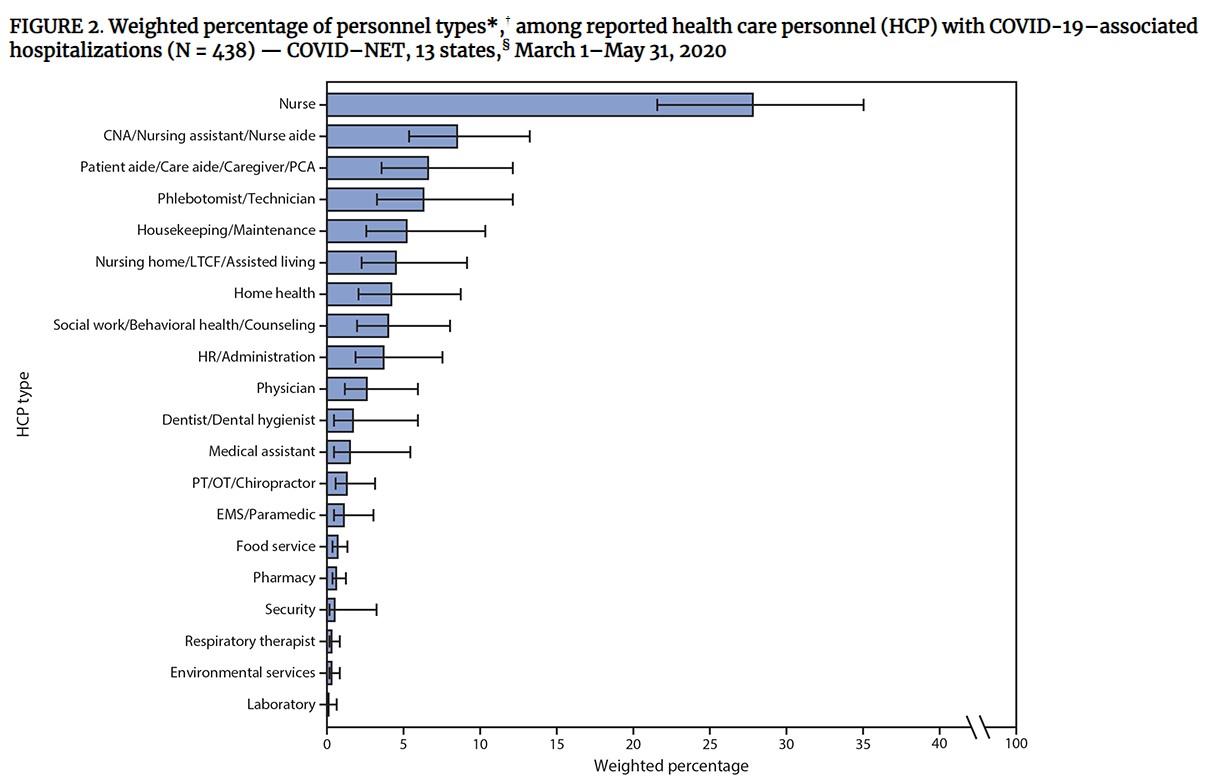

Approximately 6% of all hospitalizations with COVID 19 are healthcare workers and 36.3% of this were nurses.

(zerohedge)

Nurses Were 36.3% Of All COVID-19 Healthcare Worker Hospitalizations This Spring: CDC Study

Proof continues to emerge that nurses, who are usually the first line of help in any hospital setting, are bearing the worst brunt of the Covid epidemic amongst healthcare workers.

More than 33% of all healthcare workers that have been hospitalized with Covid-19 between March and May turned out to be in nursing-related positions, a new report from Becker’s Hospital Review notes, citing CDC analysis.

In general, healthcare workers have accounted for about 6% of total adults that have been hospitalized due to Covid. 36.3% of these hospitalizations have been nurses or Certified Nurses Assistants.

The CDC analysis looked at 6,760 hospitalizations across 13 states, including New York, Ohio and California. It also revealed that 90% of healthcare workers hospitalized due to Covid-19 had underlying conditions, such as obesity.

28% of those hospitalized were admitted to the ICE and 15.8% required invasive ventilation. 4.2% of those admitted died during hospitalization. The analysis didn’t differentiate whether or not the healthcare workers caught Covid-19 as part of their job duties, or within their respective communities.

The CDC stated: “Healthcare workers can have severe COVID-19-associated illness, highlighting the need for continued infection prevention and control in healthcare settings as well as community mitigation efforts to reduce transmission.”

And while the study doesn’t take into account pay associated with being a nurse, we’re willing to bet that they are hardly being compensated appropriately for the risks they have been taking across the nation.

Recall, months ago, this was an issue we pointed out with EMTs. We noted that many were leaving their jobs in “alarming numbers” because the Covid pandemic had made it overwhelming and not worth the menial salary they were making.

Robert Baer, an EMT in New York City who was formerly one of the first responders on September 11, told CBS several months ago: “I knew it would probably kill me if I went out there and had multiple exposures — and I’m not a chicken. I love the job, but my doctors were telling me I shouldn’t be going in the field, that it was very dangerous.”

He was supposed to be deployed to Elmhurst Hospital in Queens back in March, but decided his risks were too high and, instead, quit his job. As a result of the September 11 response, he suffers with asthma, chronic bronchitis and sleep apnea that put him at a higher risk for Covid.

Oren Barzilay, president of the FDNY-EMS Local 2507, representing New York City medics noted that about 60 EMTs had left the department over the last 4 months. Many of those retiring are over the age of 50.

“They see the risks associated with the job and the low pay, and it’s just not worth it,” Barzilay continued. EMTs start at just $30,000 per year in New York and pay tops out at about $50,000. Nationally, the job pays just $38,830 per year on average.

Top UK Scientists Warn “Many, Or All” COVID-19 Vaccine Projects Could Fail, First Gen “Likely To Be Imperfect”

MSM outlets seized on groundbreaking research produced by the Imperial College of London yesterday, claiming that the study’s findings that COVID-19 antibodies degrade during the months following infection to bash the Great Barrington Declaration, arguing that herd immunity would be virtually impossible to establish without the help of a vaccine that can provoke a stronger immune system response.

Well, on Wednesday morning, as the US government struck a deal to buy $375 million worth of an experimental Eli Lilly COVID-19 antibody drug following questionable trial results, a team of leading scientists in the UK warned that the quest for a vaccine could be complicated by an “imperfect” initial round of tests.

In fact, members of the UK’s Vaccine Taskforce warned in an article published in the Lancet that a fully effective vaccine might never be developed, and that early versions of approved vaccines might not work for all people.

The letter is clearly an effort to temper people’s expectations as a growing body of research shows that COVID-19 immunity is more complicated than many would suspect, while President Trump continues to insist that a vaccine will be available within weeks as he battles for reelection. Recently, Pfizer, the current US frontrunner, saw its CEO delay the release of trial data that was expected by the end of the week.

Importantly, the team warned that there might never be a working vaccine: “However, we do not know that we will ever have a vaccine at all. It is important to guard against complacency and over-optimism,” said Kate Bingham, the chair of the UK Vaccines Taskforce.

“The first generation of vaccines is likely to be imperfect, and we should be prepared that they might not prevent infection but rather reduce symptoms and, even then, might not work for everyone or for long.” The taskforce added that “many, and possibly all” of the vaccine projects currently in the works could fail.

Readers can find the letter below in its entirety (text courtesy of the Lancet).

* * *

No vaccine in the history of medicine has been as eagerly anticipated as that to protect against severe acute respiratory syndrome coronavirus 2 (SARS-CoV-2). Vaccination is widely regarded as the only true exit strategy from the pandemic that is currently spreading globally.

The UK is at the forefront of a huge international effort to develop clinically safe and effective vaccines. The Vaccine Taskforce was the brainchild of Sir Patrick Vallance, the UK Government’s chief scientific advisor, who saw the need for a dedicated, nimble private-sector team of experts embedded in the Government to drive forward the development of vaccines for the UK and internationally. The Vaccine Taskforce was set up under the Department for Business, Energy and Industrial Strategy in May, 2020, and I was asked to chair the taskforce, reporting directly to the prime minister, and working alongside Deputy Chair Clive Dix. The Vaccine Taskforce aims to ensure that the UK population has access to vaccines as soon as possible, while working with partners to support equitable access for populations worldwide, whether rich or poor.

However, we do not know that we will ever have a vaccine at all. It is important to guard against complacency and over-optimism. The first generation of vaccines is likely to be imperfect, and we should be prepared that they might not prevent infection but rather reduce symptoms, and, even then, might not work for everyone or for long.

Our strategy has been to build a diverse portfolio across different formats to give the UK the greatest chance of providing a safe and effective vaccine, recognising that many, and possibly all, of these vaccines could fail. We have focused on vaccines that are expected to elicit immune responses in the population older than 65 years: over three-quarters of deaths caused by SARS-CoV-2 infection are in this older population,1, 2 so it is essential that any vaccine is able to protect this group. Scalability of vaccine manufacture was also a key criterion, with the goal being to manufacture in the UK, if possible, to secure supply and create long-term resilience. We considered only vaccines that have the potential for approval by the Medicines and Healthcare products Regulatory Agency and European Medicines Agency and for vaccine delivery as early as the end of 2020 or, at the latest, in the second half of 2021.

The Vaccine Taskforce has now secured access to six vaccines (from more than 240 vaccines in development) across four different formats: adenoviral vectors, mRNA, adjuvanted proteins, and whole inactivated viral vaccines, which are promising in different ways. The most advanced vaccines, such as those developed by AstraZeneca and the University of Oxford, BioNTech and Pfizer, and Janssen, are based on novel formats for which we have little experience of their use as vaccines, although the initial immunogenicity and safety data are encouraging.3, 4, 5 Vaccines based on frequently used vaccine formats, such as adjuvanted protein vaccines developed by Novavax, and by GSK and Sanofi, and inactivated whole viruses developed by Valneva, will not be available until late in 2021.

We also have an agreement with AstraZeneca to supply a neutralising antibody cocktail as a prophylactic treatment once clinical trials are completed and it is approved by regulators. This treatment will be provided in the short term for people who cannot receive a vaccine, such as people who are heavily immunosuppressed and cannot mount an immune response, or people who need immediate protection, such as health-care workers.

The Vaccine Taskforce has options to purchase sufficient doses of each vaccine type to vaccinate the appropriate UK population. Following the interim advice by the UK’s Joint Committee of Vaccination and Immunisations,6 vaccination would be recommended for adults older than 50 years, health-care and social-care workers on the front line, and adults with underlying comorbidities. The precise dose required will be determined as part of the clinical trials and by the decisions made by the UK Government on the basis of the advice from the Joint Committee on Vaccination and Immunisation. We anticipate that most vaccines will require two doses, and we are also investigating whether annual or biannual revaccination booster shots might be required to maintain durable protection.

Developers of COVID-19 vaccines range from small biotechnology companies to big pharmaceutical companies, each with different commercial objectives and with different amounts of funding to support manufacturing scale-up and clinical trials. In some cases, the Vaccine Taskforce is investing at risk to support these activities before we know whether the vaccine is safe and effective, and, in other cases, we have negotiated an advanced purchase agreement. In both instances, government funding is usually linked to reaching clinical, regulatory, and other milestones. If a vaccine is not going to work, then we will stop funding.

Some of the developers, such as AstraZeneca, GSK and Sanofi, and Janssen, are pursuing the development of a vaccine on a non-profit basis, at least for the pandemic period; whereas others view the resources and risk that they are assuming as justification for seeking a profit.

The first phase 3 efficacy data from the leading vaccine candidates are due by the end of 2020, subject to accruing sufficient rates of infection within the clinical trial cohorts to show the vaccines’ efficacy. The primary endpoint is to show that the vaccine can protect against SARS-CoV-2 infection and reduce symptom burden. Two phase 3 efficacy clinical trials are now underway in the UK; the Oxford AstraZeneca adenovirus-vectored vaccine (NCT04400838) and the world’s first phase 3 study for Novavax’s protein-adjuvant vaccine (NCT04368988), both occurring at various sites across the UK. Numerous phase 3 studies are in preparation to start in the UK in 2020 and 2021 with US, European, Australian, and possibly Chinese vaccine developers, reflecting the UK’s strong reputation for running clinical trials and postauthorisation pharmacovigilance of high quality.

To help to accelerate the development of successful vaccines, we launched the National Health Service COVID-19 vaccine registry7 and have enrolled over 295 000 volunteers,8 with a focus on populations who are at high risk of severe infection and mortality from COVID-19. We plan to accelerate recruitment in disease hotspots with mobile research teams informed by robust PCR testing, and have provided funding for clinical trials of crucial importance, including Janssen’s two-dose Ad26 protocol (NCT04505722), Imperial College London’s self-amplifying RNA (ISRCTN17072692), and Valneva’s whole inactivated vaccine. We are also exploring the potential for future controlled human challenge studies, dependent on ethics and regulatory approvals. These studies have the potential to assess the efficacy of vaccines more quickly and with far fewer participants than a standard phase 3 trial. The Vaccine Taskforce is also supporting the development of heterologous boost clinical protocols, through the National Institute for Health Research, to explore whether different vaccine combinations can increase immunity or durability of protection.

To harmonise results from the various clinical trials, and to help to define immune correlates of protection, we have supported development of standardised, accredited assays, including quantitative high-throughput spike-protein ELISAs, live viral-neutralisation assays, and T-cell assays, which will be available to all vaccine developers.

A major challenge is that the global manufacturing capacity for vaccines is vastly inadequate for the billions of doses that are needed, and the UK manufacturing capability to date has been equally scarce. The Vaccine Taskforce has provided funding for flexible and surge production in several new UK sites for vaccine manufacture to provide the UK population with a new vaccine in less than 9 months from the identification of the pathogen. We also plan to bring new vaccine technologies and capabilities to the UK for future pandemic preparedness.

No-one has ever done mass vaccination of adults anywhere in the world before and the two-dose regimen, plus cold-chain restrictions for some vaccines, adds to the complexity of this deployment operation. National Health Service England has flexible deployment plans to start the vaccination of prioritised cohorts as soon as the vaccines are approved by the regulatory authorities, currently not to be coadministered with the influenza vaccination (although clinical trials are exploring coadministration of influenza and COVID-19 vaccines). Deployment plans have been developed for a range of settings from mass vaccination sites to large and small mobile (eg, pop-up) sites, general-practitioner surgeries and pharmacies, and even roving teams to visit people in care homes and people who are housebound or shielding.

The UK is committed to ensuring that everyone at risk of SARS-CoV-2 infection, anywhere in the world, has access to a safe and effective vaccine. The COVID-19 Vaccines Global Access Facility, to which the UK has committed £548 million, will deliver vaccines for the UK population and provide access to vaccines for lower income countries: initially 2 billion doses for 1 billion people worldwide. Working with Gavi, the Vaccine Alliance, Coalition for Epidemic Preparedness Innovations, WHO, and a broad alliance of 180 nations, this pooling of resources maximises the chances of securing access to a vaccine and making it available to all who need it. But we now need to make this global facility a permanent one: ready to respond to future pandemics quickly in the future and to control COVID-19.

The SARS-CoV-2 virus is likely to evolve, and other zoonotic pathogens are likely to pose future risks. China, Europe, the USA, and the UK need to work together. If we establish international collaboration right now, then we will be better prepared to control future pandemics without causing the largest global recession in history and the biggest threat to lives in living memory.

* * *