GOLD:$1878.90 UP $11.00 The quote is London spot price

Silver:$23.58 UP 23 cents London spot price ( cash market)

your data…

Closing access prices: London spot

i)Gold : $1878.60 LONDON SPOT 4:30 pm

ii)SILVER: $23.65//LONDON SPOT 4:30 pm

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 48.19 PTS OR 1.47% //Hang Sang CLOSED DOWN 479.18 PTS OR 1.95% /The Nikkei closed DOWN 354.81 PTS OR 1.52%//Australia’s all ordinaires CLOSED DOWN 0.56%

/Chinese yuan (ONSHORE) closed /Oil DOWN TO 36.23 dollars per barrel for WTI and 38.13 for Brent. Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6844. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6861 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

We had 2 kilobar transactions +

ADJUSTMENTS: 4 //

dealer to customer: 3 OF THEM

I)Brinks: 161,105,054 oz

ii) Int. Delaware: 2797.065 oz (87 kilobars)_

iii) JPM: 100.099 oz

iv Customer to dealer

Manfra: 9163.04 oz (285 kilobars)

The front month of NOV registered a total of 1540 contracts for a GAIN of 108 contracts.

Thus by definition the initial amount of gold standing at the comex is as follows:

1540 notices x 100 oz per notice =154,000 OR 4.7900 TONNES

I PROMISED YOU AROUND 4 TONNES OF GOLD WOULD STAND SO I AM A LITTLE OFF

The big December contract LOST 5609 contracts DOWN to 423,300 contracts..

THE BIG STORY AGAIN TODAY IS THE HIGH INITIAL OI STANDING FOR NOVEMBER (4.7900 tonnes). GENERALLY OCTOBER AND NOVEMBER ARE POOR DELIVERY MONTH AS MOST INVESTORS PREFER TO SKIP THESE MONTHS AND MOVE STRAIGHT TO DECEMBER. IT LOOKS LIKE SOME MAJOR ENTITY(GOLDMAN SACHS) JUST CANNOT WAIT FOR DECEMBER AS THEY ARE MAKING THEIR MOVE FOR PHYSICAL METAL. GOLDMAN SACHS ONE OF THE LEADERS OF THE NEW LONDON LME EXCHANGE NEEDS THE GOLD INVENTORY FOR LIQUIDITY AND INITIAL CONTRIBUTION WITH OTHER MAJOR PLAYERS.

We had 1258 notices filed today for 125,800 oz OR 3.912 TONNES.

To calculate the INITIAL total number of gold ounces standing for the NOV /2020. contract month, we take the total number of notices filed so far for the month (1258) x 100 oz , to which we add the difference between the open interest for the front month of NOV (1540 CONTRACTS ) minus the number of notices served upon today (1258 x 100 oz per contract) equals 154,000 OZ OR 4.7900 TONNES) the number of ounces standing in this active month of NOV

thus the INITIAL standings for gold for the NOV/2020 contract month:

No of notices filed so far (1258, x 100 oz +1540 OI) for the front month minus the number of notices served upon today (1258) x 100 oz which equals 154,000 oz standing OR 108.53 TONNES in this active delivery month. This is a HUGE amount for gold standing for a NOV delivery month (a very poor non active delivery month).

NEW PLEDGED GOLD: BRINKS

596,952.410 oz NOW PLEDGED SEPT 15.2020/HSBC 18.433 TONNES ( A HUGE INCREASE FROM 10.6)

60,784.803 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

deleted Int. Delaware pledge July 7 (600 tonnes)

277,934.09 oz (some deleted august 3) JPM 8.644 TONNES

610,238.285 oz pledged June 12/2020 Brinks/ july 2/july 21 19.017 tonnes

67,289.041 oz Pledged August 21/regular account 1.588 tonnes jpm

total pledged gold: 1,613,198.634 oz 50.177 tonnes

total registered, pledged and eligible (customer) gold 37,518,127.513 oz 1,166.97 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1040.63 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

And now for the wild silver comex results

And now for the wild silver comex results

INITIAL STANDINGS

NOV. SILVER COMEX CONTRACT MONTH//INITIAL STANDING

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

131,497.150 oz

CNT

Delaware

HSBC

|

| Deposits to the Dealer Inventory |

546,552.500 oz

Manfra

|

| Deposits to the Customer Inventory |

1,012,674.220 oz

JPMorgan

Delaware

Scotia

|

| No of oz served today (contracts) |

255

CONTRACT(S)

(1,275,000 OZ)

|

| No of oz to be served (notices) |

189 contracts

9455,000 oz)

|

| Total monthly oz silver served (contracts) | 255 contracts

1,275,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

Von Greyerz: “Get Ready For The Biggest Collapse In Human History”

Authored by Egon von Greyerz via GoldSwitzerland.com,

Liftoff & Collapse

Get ready for the biggest collapse in the history of mankind. It will be devastating and reach all parts of society, economic, financial, political & social.

But wait, it won’t happen just yet. Because before that the world will experience a LIFTOFF in markets of gigantic proportions. This will be the grand finale of this financial era. It will involve inflationary liquidity injections of proportions never seen before in history and lead to a massive explosion in many asset markets.

Most investment assets will benefit as the disconnect between markets and reality grows to distortionary proportions.

TRUMP – YOU WIN! BIDEN – YOU WIN!

So there we have it. For investors the outcome of this election is totally irrelevant. In four years time, the difference for the economy and markets between a Trump or Biden victory will be insignificant.

Either one of them only has one choice. They are both facing a bankrupt country which has been running budget deficits since 1930 with four years of exception in the 1940s-50s. The Clinton surpluses were fake. Also, the US has had trade deficits for almost 50 years. The consequence has been an exponentially surging debt which was under $1 trillion when Reagan became President in 1981 and is now $27t. In the next four years, a $40t debt is guaranteed as I forecast four years ago but as the financial system implodes, the debt could easily run into $100s of trillions or $ quadrillions when the derivative bubble bursts.

The global financial system should have collapsed already in 2006-9 but the central banks managed to delay the inevitable demise for over a decade.

SUPER CYCLE BULL MARKETS END IN EUPHORIA

What we must understand is that the end of an economic supercycle doesn’t happen quietly. No, the conditions need to be uber-euphoric with maximum bullishness for the economy and stocks. This means that before this era is over, markets must surge in the final months, even double over a 9-18 months period.

Multiple factors are now in place for this to happen. Firstly both presidential candidates will need not just fistfuls of dollars but quantum computers that can print the required trillions and quadrillions of dollars.

The convenient excuse they have is of course Covid. Individuals not working need money, companies need money, municipalities, states and the Federal government need money.

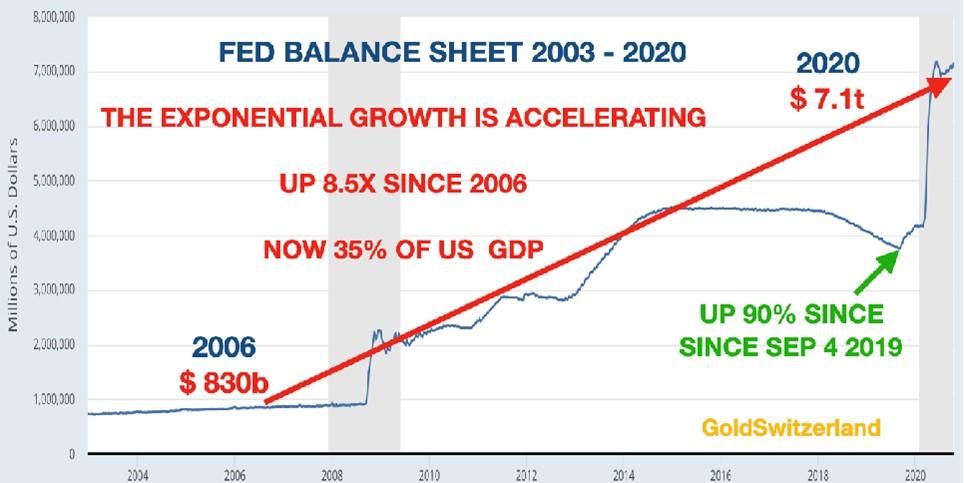

But we mustn’t forget how the end of the final phase of this economic era started. This was back in Aug-Sep 2019 when the Fed and the ECB shouted out from the roof tops that were going to do what it takes to save the system. They didn’t tell us what the problems were, but it was clear to some of us who understood the fragility of the financial system that it was in dire straits. When the last crisis started in 2006, the Fed’s balance sheet was $830b. At the end of the Great Financial Crisis in 2009, the balance sheet had grown to $2t.

But no one must believe that the problem had been solved by 2009. All it was, was a temporary stay of execution. Why otherwise would the Fed’s balance sheet have grown by another $5t since 2009. Just looking at the predicted budget deficits in the next 4 years, plus accelerating problems in the financial system the Fed’s balance sheet is likely to explode in coming years.

LIQUIDITY INJECTIONS WILL GIVE SHORT TERM BENEFIT TO THE ECONOMY

So the conditions are in place for the biggest liquidity injection in financial history. For many years we have experienced a total disconnect between economic reality and markets. The coming acceleration in money printing and liquidity injections in to the financial system will be so overwhelming that it will not just fuel markets but also give a short term, albeit artificial, boost to the economy.

This is a typical course of events at the beginning of an inflationary phase which leads to hyperinflation as the currency collapses.

The paralysation of the world economy due to Covid will probably peak with the current second wave and therefore add to the optimism in markets. But no one must believe that the pandemic is the cause of the problems in the world economy. No, it has just been a very vicious catalyst which hit an already fragile financial system.

When Covid gradually slows down, the initial optimism combined with the flooding of the system with printed money might last for a year or so. But as the world realises that you cannot solve a debt problem with more debt, the real difficulties in the economy and the financial system will reemerge with a vengeance.

FROM BOOM TO BUST

So let us look at a possible scenario of events following the election:

New president will flood the economy with money & boost stocks

Initial market volatility will settle down quickly and investors will respond optimistically to the new president’s promises of support to every corner of the economy.

Stock markets will surge and could double over a 9-18 month period. No cash will be left on the sidelines. Both institutions and retail investors will throw all the cash they have at the stock market. There will be a frenzy which will surpass the tech stock boom in the 1990s. There will be fanfares and blazing guns as the market seems unstoppable.

But after the likely short-term boom, there will be tears as markets fall by over 90% in real terms. And sadly most investors will ride the stock market all the way down. The big difference this time is that central banks will not and cannot save them.

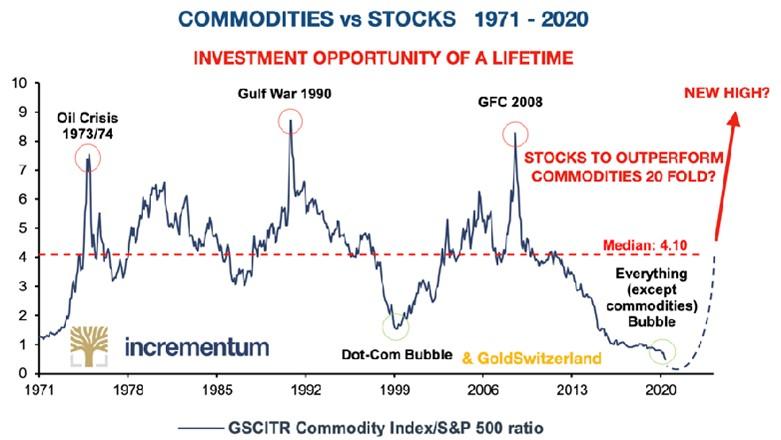

COMMODITIES WILL BOOM

The biggest beneficiary of this coming boom will be commodity markets which are at a 50 year low versus stocks. Looking at the chart below, the minimum target would be commodities outperforming stocks by 4 to 1. Eventually a new high in commodities against stocks is likely. This would mean commodities outperforming stocks by 20x. The first part of this outperformance will come as stock markets rise. But the final phase will be when general stock markets collapse and commodities continue to strengthen. Goldman Sachs expect commodities to rise 28% in 2021. They expect inflation plus a commodities deficit will drive prices higher. And this is of course what the chart below tells us.

PRECIOUS METALS WILL SHINE

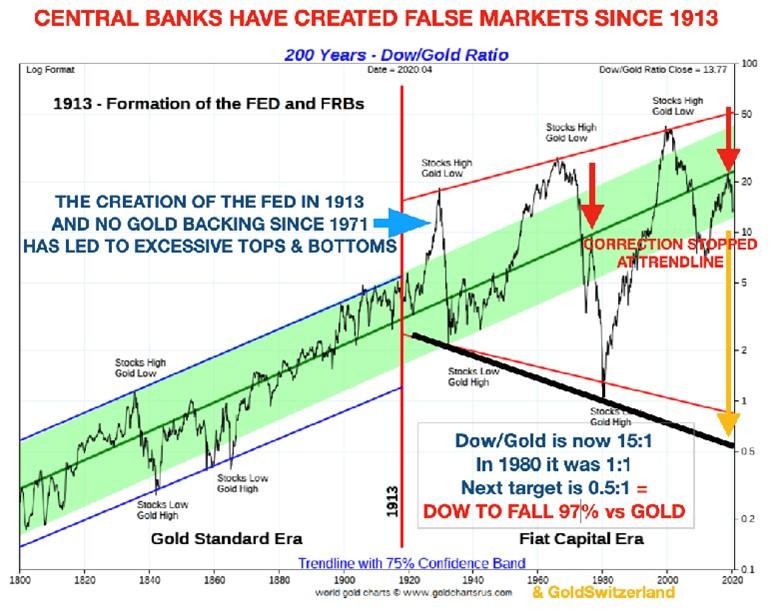

Gold, silver and platinum will vastly outperform stocks. The Dow – Gold ratio will initially reach 1 to 1 where it was in 1980 when gold was $850 and the Dow index 850. Eventually the ratio will reach at least 0.5 to 1 which means that the Dow will lose 97% against gold in the next five years.

Goldman Sachs expects gold to reach $2,300 in 2021 but I believe that target is too conservative. Before gold breaks out above the August high at $2,074, a correction down to $1,800-20 is possible and would not change gold’s unstoppable rise. In this latest phase, gold is in a bull market or more correctly, the currencies are in a bear market since 1999. The continued debasement of the currencies is guaranteed by the central banks since they only have one option – TO PRINT AND PRINT AND PRINT until money dies.

We must remember that gold is the king of the metals and therefore the safest precious metal to hold. But initially at least, silver and platinum will strongly outperform gold but with massive volatility.

Vital to hold physical metals stored in safe vaults in the investor’s name, outside the banking system. It is important not to forget that the risks in the financial system will be at a maximum for the next few years and a failure can happen at any time.

PRECIOUS METALS MINING STOCKS

For the smart investor, this is where more money will be made than in any area of stocks or other investments. Especially the juniors will really shine. But this is a market for specialists. So either best to follow some of the smartest investors in this area or to buy an index of these stocks. There will be many 10-20 baggers and even some 100 baggers but obviously also some losers. So important to have a spread.

The biggest risk with mining stocks is that they are normally held within the financial system. So even though they are a terrific investment opportunity, they are not the best form of wealth preservation. Therefore it is safer to have a much bigger allocation to the physical metals which, even though they will underperform the mining stocks, will see massive capital appreciation.

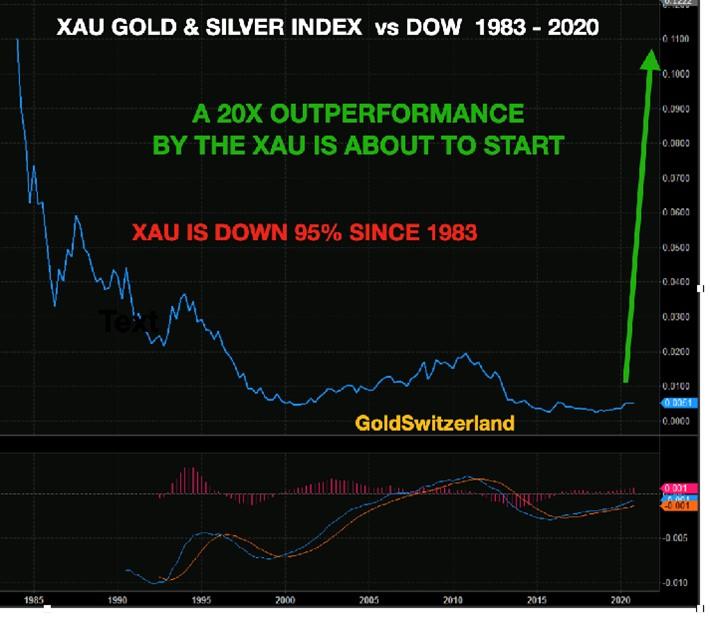

The chart below shows XAU gold – silver index against the Dow since 1983 when the XAU was introduced. Since then the XAU has lost 95% against the Dow. This fall is likely to be reversed in the next few years with the XAU going up 20x against the Dow . For Dow investors this means losing 95% against mining stocks.

And sadly, this is what will happen to 99% of investors as they stick to their ordinary stocks and miss the most incredible opportunity.

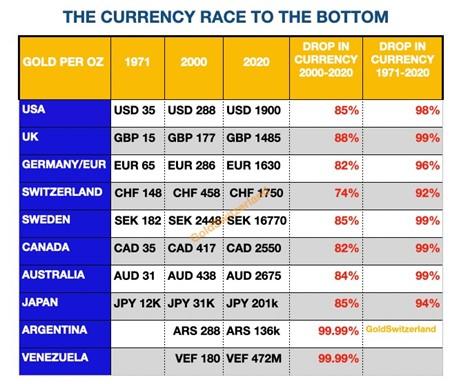

DOLLAR

Printing unlimited amounts of money always has consequences. Since 1971 the dollar has lost 98% in real terms which means against gold since gold is the only money that has survived in history.

The dollar is now starting its final journey to ZERO and as the table shows, even a weak and artificial currency like the euro will outperform the doomed dollar.

A falling dollar will accelerate US inflation until it leads to hyperinflation.

INTEREST RATES

Interest market is probably the most contrarian of all trades today. The whole investment world, including the Fed and the ECB believe that rates will stay at zero or below for years to come. Normally when consensus is that strong, the opposite is more likely to happen.

Precious metals normally benefit from negative real rates which means that inflation is higher than interest rates. Gold can still rise strongly with high nominal rates as long as inflation is higher. We saw this happen in the 1970s to the early 1980s when rates reached 20% and gold went from $35 to $850. During that time, inflation remained higher than rates.

I remember this period well as I experienced it in the UK with my first mortgage reaching 21%.

FROM BOOM TO BUST

So there is now an opportunity for all investors to double their money in the stock market in the next 9-18 months as ever more liquidity will fuel stock markets.

But a Caveat Emptor (Buyer Beware) warning is in place here. Asset markets are already in a major bubble and the financial system is so fragile that it could break at any time.

So rather than chasing the last leg of this bull market which most investors will do, it will be much better to look at safer alternatives.

I have outlined them above. Physical precious metals and precious metals stocks will outperform all other markets. And these all present the best risk. Both the metals and the metal stocks will boom in the final phase of the stock market boom. And as stock markets top and then crash, the precious metals sector will continue to perform extremely well as currencies are debased.

As I stated above, the general stock market is likely to lose at least 95% against the precious metals sector in the next five years.

There has probably never before been such a clear choice in investment markets but sadly most investors will miss it. They will instead stick to their conventional portfolio which will include a lot of the already overvalued tech stocks.

Holding gold and silver stocks will be the investment opportunity of a life time. But since they are held within a vulnerable financial system, we believe that a these holdings should represent a much smaller percentage than physical metals.

To hold physical gold, silver and platinum outside the fragile banking system is the ultimate form of wealth preservation and insurance against a debt infested and unsafe financial system.

With a portfolio of some precious metals stocks and physical metals, investors will be able to ride out the coming storm and volatility in markets and also benefit financially. Of course there will be volatility also in the metals market but the trend in the next 5+ years is virtually guaranteed.

So better to avoid the coming boom and bust in the general stock markets and stick to metals.

END

J Johnson’s commodity report

https://www.jsmineset.com/2020/10/30/the-great-reset-is-underway/

“The Great Reset is Underway”

Posted October 30th, 2020 at 9:34 AM (CST) by J. Johnson & filed under General Editorial.

Great and Wonderful Friday Morning Folks,

Rebound is the word of the day along with the titled phrase with Gold up $11 with the trade at $1,879, close to the high at $1,881.30 with the low at $1,863.30. Silver is trading at $23.525, up 16.5 cents after the dip down to $23.23 with the high to beat at $23.645. The US Dollar is flat to lower with its value pegged at 93.89, down 8.7 points inside a 21-point trading range with the high at 94.01 and the low at 93.80. Of course, all this couldn’t happen without London doing its thing, before 5 am pst, the Comex open, and after UPS finds the “lost” Biden evidence, and returning these said docs back to Tucker. How’s that for a fast-track?

Venezuela’s currency now has Gold’s value priced at 18,766.51 Bolivar showing a slight gain in price as the metal added 30.96 overnight with Silver gaining 2.996 Bolivar with the last quote at 234.956. Gold in Argentina is now priced at 146,986.88, another shallow gain of 224.83 A-Peso’s with Silver increasing its value by 21.91 A-Peso’s with its last trade at 1,840.22. Turkey’s Lira is showing a golden gain with the noble metal adding 88.19 T-Lira with the last quote at 15,696.30 with Silver gaining 3.012 with its last price at 196.141 T-Lira.

November Silver’s First Notice Day is here with the starting count at 444 fully paid for contracts waiting for receipts and with zero Volume up on the board. Yesterday’s activity before the FND had 27 contracts swapping hands between $23.28 and $22.96 with the last trade at 23.19 with the Comex Calculated Close at $23.339 a gain of 6/10ths of a cent that reduced the Demand count by 2 contracts. As of this morning, Silver’s Overall Open Interest is now at 155,974 Overnighters, showing another 1,287 contracts leaving the field of play.

November Gold’s Delivery Demands now stand at 1,540 fully paid for 100-ounce contracts waiting for receipts and with a Volume of 20 up on the board with a trading range between $1,870.10 and $1,862.80 with the last buy at the high, up $4.50 while the papers play the trade even higher. Yesterday’s full Comex/ICE activity happened in between $1,878.80 and $1,858.80 with the last swap at $1,865, with the CCC settled at $1,885.60, a loss of $11.50 that had 240 contracts swapping hands that provided a gain of 108 contracts standing in line for the real. The shorts against the physicals are continuing to exit Gold’s paper play as another 3,980 contracts left the arena, leaving 546,317 in Open Interest as we get closer and closer to another election.

Next Wednesday, we expect the usual political excuse to come from the loser about the “popular” vote that has never mattered EVER! What difference does a TV stations fake poll make if they only count one sides opinion? Is it the same pollsters this time as in 2016, that couldn’t equate the visual evidence of stadiums full of Trump supporters in their tallies?

Ironically or not, the returned copies to Tucker helped prove many things with yesterday’s Sean Hannity show asking Senate Homeland Security Committee Chairman Sen. Ron Johnson if the laptop and Tony Bobulinski story are real, to which the Senator responded, “All I can say is that all the verification, all the validation we’re doing, we haven’t turned up any discrepancies (yet). Everything appears to be authentic that we’ve looked at so far.” To think a TV show, would have the “real authentic files” instead of Homeland Security, is another one of those “look over here and not there” misdirection’s made by media, that failed. Btw, where’s Hunter?

I had expected Q would be silent going into the election, and I was wrong! Last night Q posted an open letter from Carlo Maria Vegani which in the fourth paragraph states “A global plan called the Great Reset is underway” (no dates), also bringing forth in his write-up more of the things we (Team Sinclair and Team GATA) have been discussing over the decade. It all seems to be coming to a head and is planned. Will the global arrangement against all mankind succeed or will it fail?

With precious metals in hand, and our understanding that Silver and Gold have survived all resets of the past, we gain more strength in our beliefs! So have a great weekend, keep your metals close, stock up on foods and what not’s before inflation hits hard, or the 2-week bankers shut down is applied. Keep the faith, have a prayer for all, and as always …

Stay Strong!

Jeremiah Johnson

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

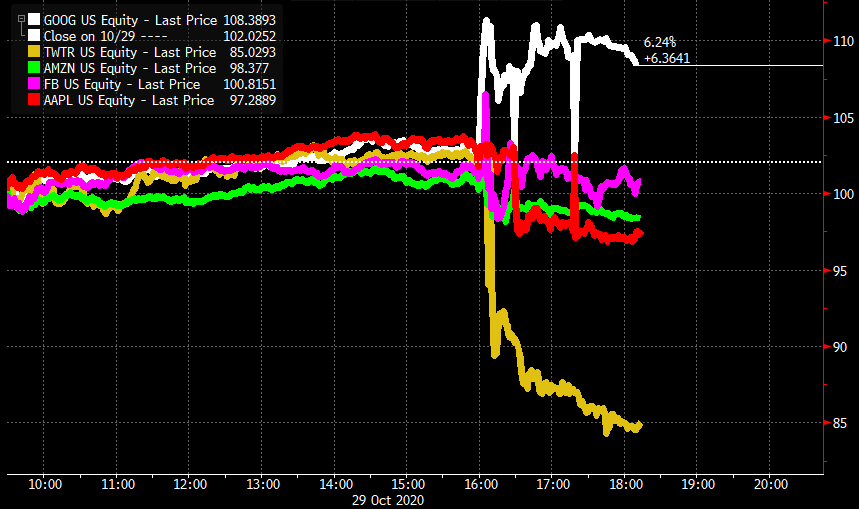

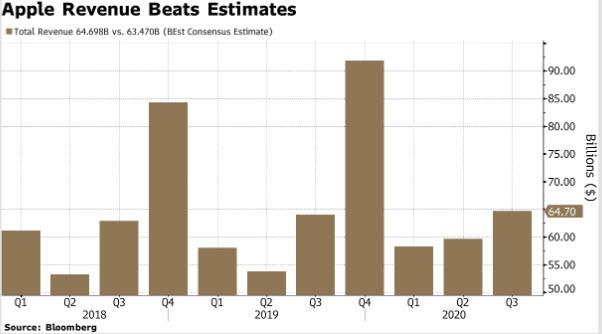

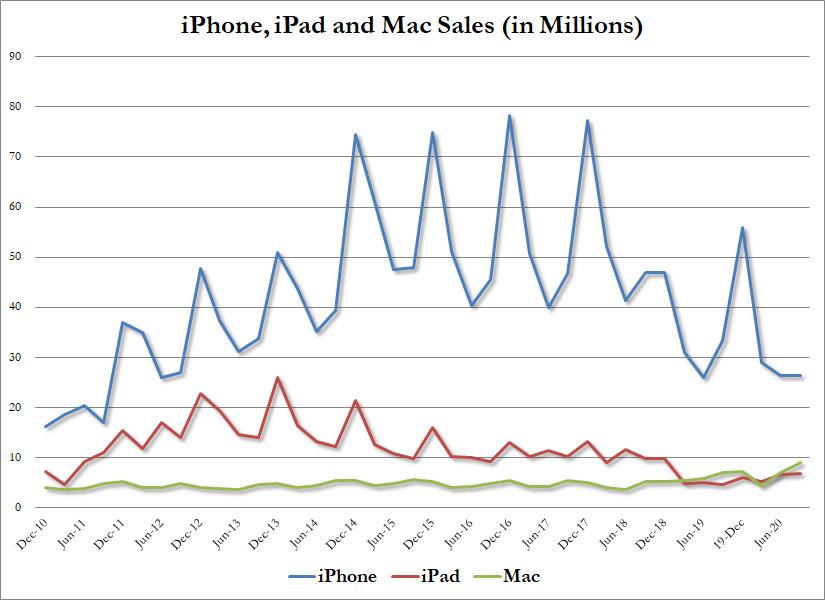

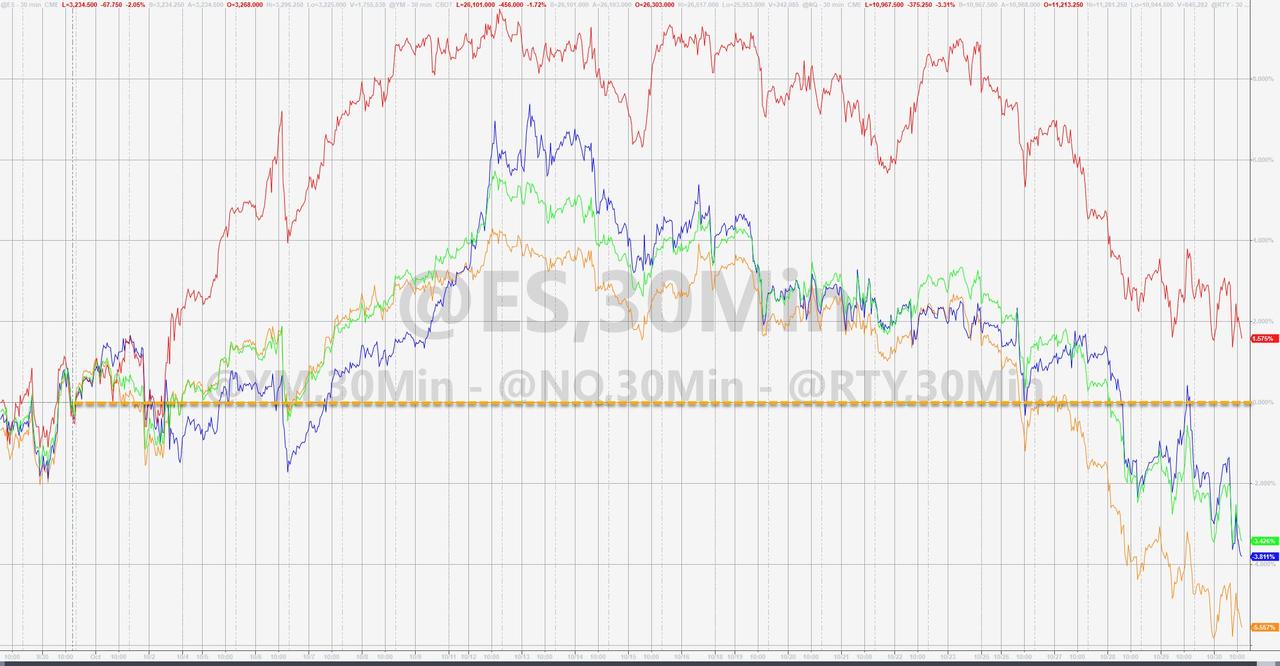

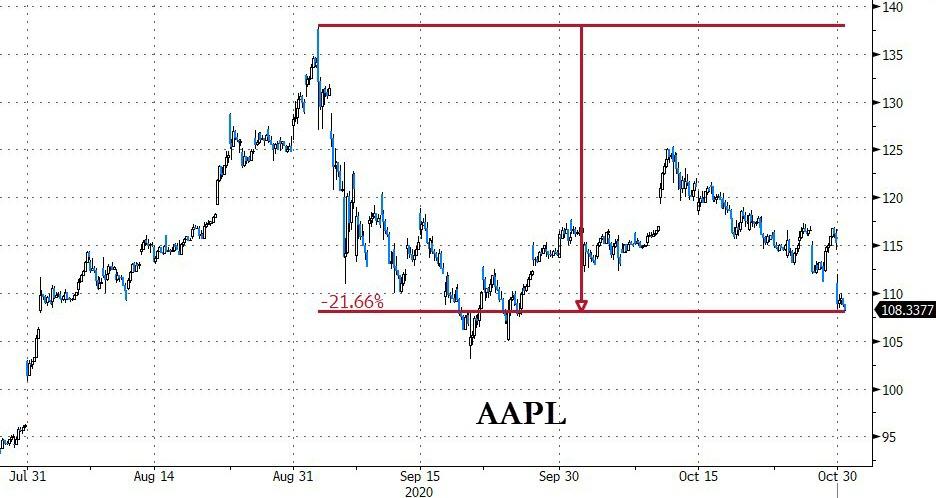

Futures Rebound From Overnight Tech Wreck

On Monday we presented readers with the latest observations from BofA quants who pointed out that Q3 earnings “smacked of the tech bubble” because despite impressive beats, in many cases stocks dropped (or outright tumbled) in kneejerk response as virtually everything has now been priced to (and beyond) perfection with little chance of upside surprise. Nowhere was this more evident than on Thursday afternoon when the world’s 4 biggest tech companies all reported blockbuster earnings and yet all sank subsequently with the exception of Alphabet which popped after hours (while Twitter cratered as countless conservatives bailed on the ultra-liberal and openly pro-Biden social network).

Nasdaq futures fell about 1%, erasing more than half of what was a 2.7% slide earlier after Apple’s iPhone sales and Twitter’s user growth both missed estimates. The two stocks sank in pre-market trading. Amazon.com fell 1.4% after it forecast a jump in costs related to COVID-19, while Facebook shed 2% as it warned of a tougher 2021. Google parent Alphabet was the only bright star among the FAAMGs with its shares jumping 7% after it beat estimates for quarterly sales as businesses resumed advertising.

Ahead of the overnight tech rout, global stock were already on course for the worst weekly decline since March as lockdown measures and the collapse of stimulus talks (which “nobody” could have predicted) crippled trader optimism. Treasuries, the dollar, oil and gold were little changed.

Third-quarter earnings season is past its halfway mark and about 84.8% of S&P 500 companies have beaten estimates for earnings, according to Refinitiv data. Overall, profit is expected to tumble 13.4% from a year ago.

The broad-based weakness in the market-leading giga-tech stocks added to trader concerns about a surge in coronavirus cases, and hammered stock futures on Friday, although futures are now off their worst levels of the day.

S&P e-minis fell 25.00 points or 0.9% and Nasdaq 100 E-minis were down 121 points, or 1.1%. A longer-term chart shows the precarious positioning for the S&P, with any further declines set to take out the Sept 24 lows and open up a trapdoor to much lower levels.

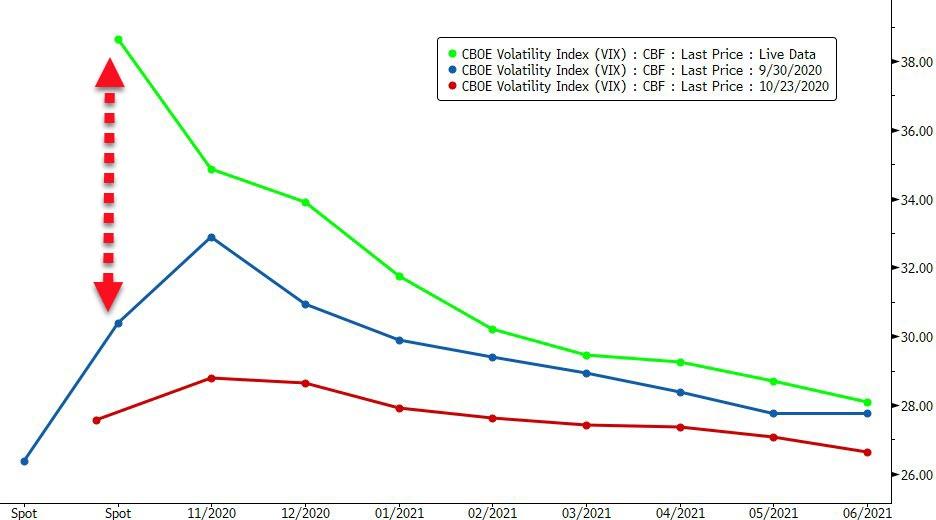

Shares of tech heavyweights had jumped ahead of tech results on Thursday, helping the S&P 500 close higher. Still, the benchmark index is set to wrap up its worst week since mid-June, while Wall Street’s fear gauge held at a 20-week high, also on fears of a contested election next week. Ahead of the final weekend before Election Day on Tuesday, President Donald Trump and Democratic challenger Joe Biden will barnstorm across battleground states in the Midwest where the coronavirus pandemic has exploded anew.

“Our short-term risk-appetite indicator is firmly in negative territory,” said Credit Agricole CIB head of global markets research Jean-Francois Paren. “The adjustment of risky asset prices to the weaker epidemic and economic outlook could continue, which is not encouraging for risk asset prices in the coming days, especially given the uncertainty regarding the U.S. elections.”

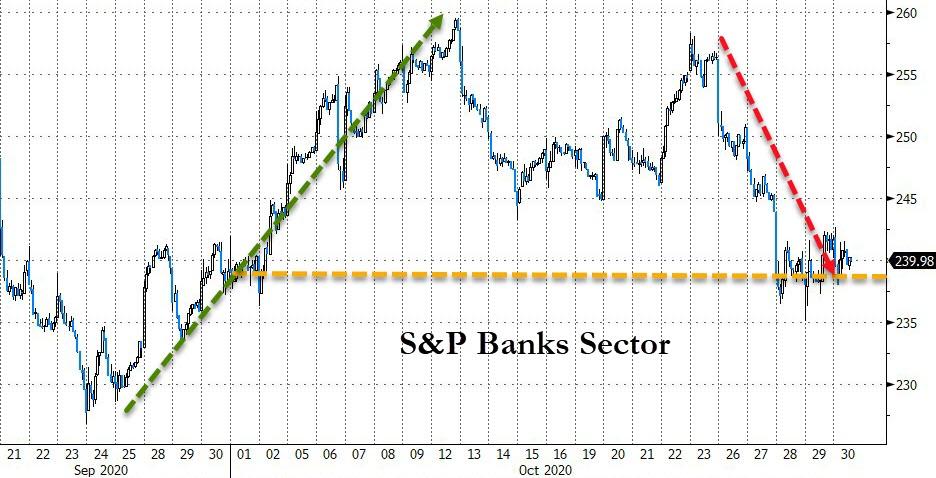

European shares fluctuated amid a string of mixed earnings reports. Europe’s Stoxx 600 Index erased declines of as much as 0.9%, climbing 0.3%, led by energy and banks, with E&P giants Total and Shell among biggest gainers; Total posted 3Q profit that exceeded the highest analyst estimate; Barclays raised Shell to equalweight, saying newly presented financial framework addresses main concerns. Tech stocks faltered as did Danish drug giant Novo Nordisk A/S, whose earnings underwhelmed analysts. Bank stocks advanced after Spain’s BBVA SA and the U.K.’s NatWest Group Plc reported improved pictures for soured loans.

Earlier in the session, Asian stocks fell, led by the health care and IT sectors. Trading volume for MSCI Asia Pacific Index members was 28% above the monthly average for this time of the day. The Topix lost 2%, with Takeda and Hoya contributing the most to the move. The Shanghai Composite Index retreated 1.5%, driven by China Life and Yili Industrial.

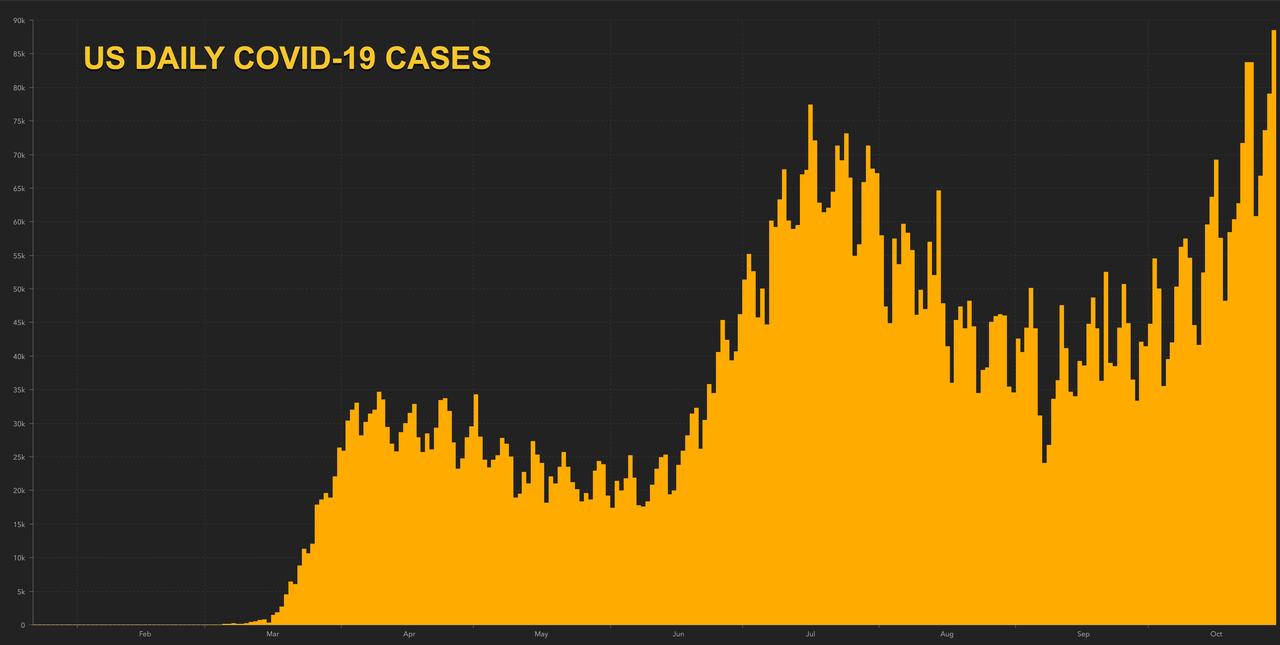

As Bloomberg notes, weakness in technology shares has added to volatility that’s likely to remain elevated heading into next week’s U.S. election. Global equities are on course for the worst weekly decline since March as lockdown measures in some countries and the lack of an agreement on U.S. stimulus dent sentiment. New U.S. coronavirus cases topped 89,000, setting a daily record.

In FX, the Bloomberg Dollar Spot Index steadied after swinging between gains and losses; the euro steadied but was set for its biggest weekly drop against the dollar since September. Sweden’s krona led gains among Group-of-10 peers, though the Japanese yen remained supported on haven demand. The Australian dollar advanced on month-end flows, with a stronger yuan also spurring appetite for the commodity-linked currency.

In rates, Treasuries were unchanged with long-end supported ahead of month-end. Yields are off richest levels of the day as e-minis recouped some early losses. Treasury yields are within a basis point of Thursday’s close, slightly lower across the curve; 10-year yields around 0.82%, remain toward cheaper end of 0.74% to 0.84% weekly range and outperforming bunds, gilts by almost a basis point each. Treasuries rallied in early Asia session as Apple stock fell over 4% in after-market trading on Thursday; into early U.S. session Nasdaq e-minis remain lower by 1.2%, S&P e-minis are off 0.9%.

In commodities, oil was flat after suffering a recent rout, while spot gold headed for its third consecutive monthly decline. Crude oil was little changed in New York.

On today’s calendar AbbVie, Exxon and Charter Communications are among Friday’s scheduled earnings. Personal spending, U. of Michigan sentiment are due.

Market Snapshot

- S&P 500 futures down 1.4% to 3,257.75

- STOXX Europe 600 up 0.1% to 342.16

- MXAP down 1.3% to 172.21

- MXAPJ down 1.2% to 572.11

- Nikkei down 1.5% to 22,977.13

- Topix down 2% to 1,579.33

- Hang Seng Index down 2% to 24,107.42

- Shanghai Composite down 1.5% to 3,224.53

- Sensex down 0.6% to 39,523.90

- Australia S&P/ASX 200 down 0.6% to 5,927.58

- Kospi down 2.6% to 2,267.15

- Brent Futures down 0.03% to $37.64/bbl

- Gold spot up 0.2% to $1,871.30

- U.S. Dollar Index down 0.04% to 93.92

- German 10Y yield rose 1.4 bps to -0.622%

- Euro down 0.05% to $1.1668

- Brent Futures down 0.03% to $37.64/bbl

- Italian 10Y yield fell 7.3 bps to 0.489%

- Spanish 10Y yield rose 1.7 bps to 0.15%

Top Overnight News from Bloomberg

- Germany and the rest of the euro area’s biggest economies surged in the third quarter, in a rebound that’s now being derailed by an intensifying pandemic and new government restrictions on businesses

- European Central Bank policy maker Robert Holzmann said it is right to assume that President Christine Lagarde signaled more monetary stimulus is coming, though not until December

- U.K. house prices posted their biggest annual gain since 2015 this month as a revival in the housing market defied a wider economic malaise

- Jeremy Corbyn’s suspension from the U.K. Labour Party he led until April threatened to re-open divisions in the party after six months of relative calm under new leader Keir Starmer

- Treasury Secretary Steven Mnuchin accused House Speaker Nancy Pelosi of pulling a “political stunt” and holding up a new stimulus bill by refusing to offer compromises, in an escalation of acrimonious finger-pointing over stalled virus-relief negotiations

- U.S. new virus cases topped 89,000, setting a new daily record, as the outbreak intensifies ahead of next week’s presidential election. The U.S. is seeing a jump in cases in New York and New Jersey again, and a record outbreak across the Midwest states

- France is aiming to limit the drop in economic activity to 15% during the country’s second coronavirus lockdown starting on Friday, Finance Minister Bruno Le Maire said in a government briefing on Thursday

- German Chancellor Angela Merkel delivered a wake-up call to fellow leaders in the 27-nation European Union, saying they all failed to step in quickly enough to control the pandemic as the cost of a second lockdown begins to come into focus

- Oil is poised for the biggest monthly decline since March as a resurgent coronavirus across the U.S. and Europe raised concerns the fragile demand recovery will be derailed.

Here’s a quick look at global markets courtesy of NewsSquawk

Asian equity markets weakened heading into month-end and after US stock index futures faded the recovery seen on Wall Street amid disappointment from the big tech earnings despite Apple, Alphabet, Amazon, Facebook and Twitter all beating on top and bottom lines. Apple shares declined over 4% in extended trade with investors discouraged by the miss on iPhone sales and lack of guidance, as well as a 29% Y/Y drop in its Chinese revenue which pressured its supply Chain in Asia and Twitter slumped nearly 18% after hours on slower user growth. ASX 200 (-0.6%) and Nikkei 225 (-1.5%) were weaker with industrials and tech frontrunning the declines in Australia although losses in the index were briefly pared by financials as AMP shares surged over 20% following a takeover approach by Ares Management, while the mood in Tokyo was clouded by currency effects and soft inflation data but with Panasonic shares a notable gainer on reports it is working with Tesla to build a new battery cell production line at the Gigafactory. Elsewhere, the Hang Seng (-2.0%) and Shanghai Comp. (-1.5%) remained cautious amid a plethora of large-cap earnings and with participants mulling over the initial details of the 5-year plan which seeks to build the nation into a technological powerhouse and emphasized quality growth over speed but refrained from specifying a targeted pace of growth. Finally, 10yr JGBs were lower and fell below support near 152.00 on spillover selling from T-notes as Wall Street initially nursed losses and following an uninspiring 7yr auction stateside, although the downside for JGBs was cushioned with the BoJ in the market for nearly JPY 1.3tln of JGBs with up to 10yr maturities.

Top Asian News

- Hong Kong Economy Shows Early Signs of Revival as Exports Jump

- Singapore Overtakes Thailand to Become Asia’s Worst Stock Market

- BOJ Widens Buying Ranges While Cutting Frequency for Short Bonds

European equities (Eurostoxx 50 -0.1%) have trimmed opening losses throughout the session despite underpeformance of Stateside peers. After a mixed close yesterday, equities in the region initially succumbed to some of the heavy selling pressure seen after the Wall St. close in the wake of earnings from US tech mega-caps. Despite the likes of Apple, Alphabet, Amazon, Facebook and Twitter recording beats on top and bottom lines, earnings (ex-Alphabet; up 5.6% pre-market) were received poorly with Apple shares currently lower by 4.5% in pre-market trade following a miss on iPhone sales and lack of guidance, as well as a 29% Y/Y drop in its Chinese revenue. Social media names Facebook (-2.4%) and Twitter (-17.5%) are seen lower ahead of the cash open, whilst e-commerce giant Amazon (-2.1%) are also lagging with some citing soft operating income guidance for December. In Europe, given the gravitational pull of the aforementioned large-caps, stocks across the continent commenced the session on the backfoot before staging a mild recovery with little in the way of clear fundamentals behind the move; as context the Eurostoxx 50 is lower by 6.4% on the week. Sectoral performance is somewhat mixed with oil & gas names the clear outperformer in the wake of earnings from Total (+2.3%) who reported a heavy beat on Q3 net income and maintained its dividend despite the likes of BP, Shell and Eni trimming theirs in 2020. Elsewhere, banking names are also performing well this morning following Q3 results from Natwest Group (+5.6%) which saw the Co. beat expectations for quarterly pre-tax profits and suggest that FY impairments are seen at the lower end of the range. IAG (+2.6%) have lent some support to the travel & leisure sector despite reporting a wider than expected loss for Q3 operating income with the CEO noting that his top priority will be reducing the Co.’s cost base. To the downside, underperformance has been observed in personal & household goods and food & beverage names. Health care names are also softer on the session following earnings from Novo Nordisk (-1.5%) with the insulin producer missing on expectations for EBIT and net profits.

Top European News

- Spanish Banks Join EU Peers in Painting Rosier Bad Loans Picture

- Continental CEO Degenhart to Resign, Citing Health Reasons

- Italy in Talks With Paschi on $1.75 Billion Capital Increase

- U.K. House Prices Jump Most in Five Years as Boom Gathers Pace

In FX, the Dollar remains relatively firm and resilient given a loss of safe-haven status or less demand amidst a fragile recovery in risk sentiment, month end portfolio rebalancing and positioning ahead of next week’s US Presidential Election. However, the index is back below 94.000 and Thursday’s 94.105 high within a 93.983-762 range as several major counterparts claw back some lost ground before another raft of data, the Chicago PMI and final Michigan sentiment.

- JPY/AUD – Leading the aforementioned G10 recovery in spite of somewhat mixed Japanese CPI, unemployment and ip updates, the Yen is back above 104.50 and a key Fib at the half round number alongside hefty option expiry interest (2.2 bn). On the flip-side, 1.4 bn expiries at the 104.00 strike will act as a barrier and support for Usd/Jpy after the pair got to within 2-3 pips of the level yesterday, and conversely the Aussie appears to be drawing comfort from the fact that it survived an equally close shave with 0.7000 to probe 0.7050 with assistance from ANZ’s CEO arguing against an RBA ease next week on the grounds it would flood the financial system with more liquidity, impair bank profitability and only boost the economy and jobs marginally.

- GBP – Also firmer vs the Buck after losing 1.2900+ status on Wednesday and maintaining momentum against the Euro close to 0.9000 in wake of the ECB, though wary of ongoing Brexit uncertainty and end of month Eur/Gbp cross flows that can deviate from RHS to LHS quite sporadically.

- NZD/EUR/CAD/CHF – All narrowly mixed vs the Greenback, as the Kiwi regains hold of the 0.6600 handle in wake of another upbeat sentiment survey (ANZ consumer confidence up to 108.7 in October from 100.0 previously), and the Euro pares some post-ECB losses after basing at 1.1650. Note, this coincided with the 100 DMA, which is now 5 pips firmer and the 2 chart points also align with 1.5 bn option expiries for today’s NY cut. Perhaps predictably, market contacts tout stops on a break of 1.1650 that would expose a virtual double bottom from late September (1.1615-12). Elsewhere, the Loonie is deriving a degree of comfort from stability in oil prices and the generally less risk averse tone to retest 1.3300 from 1.3390 or so, but the Franc is still lagging below 0.9150 and hovering near 1.0700 against the Euro.

In commodities, WTI and brent are modestly firmer this morning in a pull-back from some of the overnight losses after sentiment took a hit on the earnings-spurred downside in US equities last night. Following this, the crude complex has continued to lift off lows throughout the session alongside sentiment in general; WTI and Brent are currently firmer by around USD 0.30/bbl. Turning to OPEC where the Iraq oil minister pushed back on reports that the country and others are considering a rollover of existing OPEC+ output cuts into 2021 given developments on both the demand & supply side. While the remark is interesting there is still over a month until the next OPEC+ gathering and as such a pushback on such commentary at this stage is perhaps not too surprising. Elsewhere, the BSEE report of 43-companies had just shy of 85% of oil shut-in for the Gulf given Storm Zeta; its worth noting the storm is continuing to dissipate and as such production should be restored to the Gulf over the next few days – assuming no damage occurred. Moving to metals, spot gold is modestly firmer this morning as the USD has dipped as sentiment sees a moderate pick up from a European perspective. Separately, mining updates saw Glencore confirm their FY production guidance with the exception of coal given strike action at the Cerrjeon site; additionally, their YTD copper production is -8% vs. the prior period.

US Event Calendar

- 8:30am: Personal Income, est. 0.4%, prior -2.7%

- 8:30am: Personal Spending, est. 1.0%, prior 1.0%

- 8:30am: Employment Cost Index, est. 0.5%, prior 0.5%

- 8:30am: PCE Core Deflator YoY, est. 1.7%, prior 1.6%

- 9:45am: MNI Chicago PMI, est. 58, prior 62.4

- 10am: U. of Mich. Sentiment, est. 81.2, prior 81.2; Current Conditions, est. 84.9, prior 84.9; Expectations, est. 78.8, prior 78.8

DB’s Jim Reid concludes the overnight wrap

For the first 40-odd years of my life Halloween was a minor curiosity. My Dad’s dislike of trick or treaters didn’t help cement it in my social calendar as a kid. However since we’ve had kids my wife has slowly ensured it’s become a bigger and bigger event. Last night I learnt that she has gone into overdrive and bought what I thought were pretty expensive costumes ahead of us going to a pumpkin picking Halloween themed afternoon tomorrow at a local farm. Apparently I have an extravagant ghost costume and the twins have matching baby ghost costumes. My wife and Maisie have mother and daughter witch costumes and broomsticks. I’m not sure what the Halloween version of bah humbug is (maybe boooo humbug), but I’m slowly having it drummed out of me.

Over the last 24 hours we’ve gone from treat to trick as the prospect of big tech earnings first lured investors back in and then disappointed when they arrived after the bell. The S&P 500 was up over +2% late in the actual session last night prior to a sharp 70bp pullback in the last half hour of trading. It still closed +1.19%, with the NASDAQ rising a greater +1.64%.

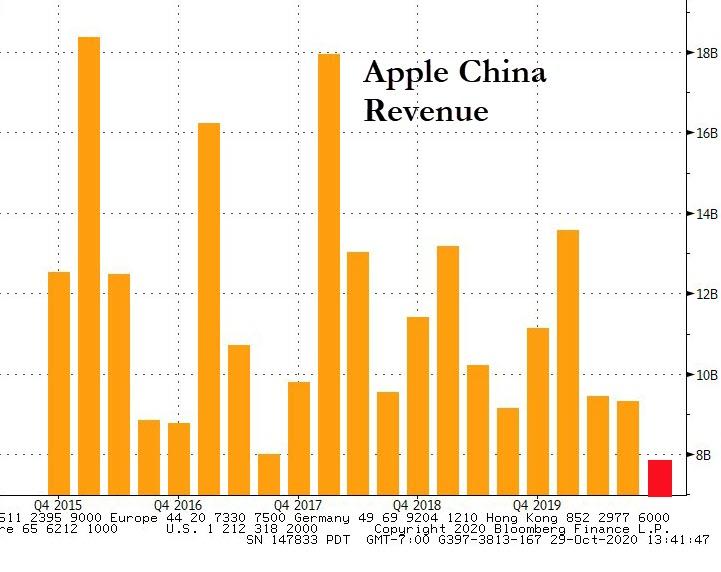

After the close, Apple (+4.53% daily gain) fell over -4% even as its quarterly results beat estimates with record sales of Macs and services. However the largest US company also revealed that iPhone revenues fell -21% with revenue in Greater China, one of the company’s most important regions, falling by -29% to the lowest level since 2014. Amazon (+2.33% earlier) was down nearly -2% after giving up an immediate postmarket gain as revenue and earnings both solidly beat analyst estimates. The dip came after the CFO indicated that covid-related expenses will go up to $4 billion. Facebook’s (+5.75% earlier) shares were down over -2.5% in the after-market, even as revenues and user growth both beat estimates. On a more positive note, Google’s (+4.16% earlier) parent company, Alphabet, gained over +6% in after-market trading with news that the company’s digital advertising profits bounced back strongly from the previous quarter.

Overnight, we also got a look into some details of China’s new five-year economic plan, which had tech in focus. The new plan elevated China’s self-reliance in technology into a national strategic pillar. Senior party officials of the Communist Party said that the nation would accelerate development of the kind of technology needed to spur the next stage of economic development with focus on bold measures to cut reliance on foreign know-how.

Back to yesterday and European stocks tried to turn positive after three straight days of declines to start the week as ECB President Lagarde outlined steps the central bank could take in December to recalibrate monetary policy in light of the worsening pandemic (more below). Her comments saw the STOXX 600 rise +1.76% off the lows of the day, however part of those gains were given back in the last half hour of trading with the index ending down -0.12% on the day. While the DAX (+0.32%) gained, other bourses such as the CAC (-0.03%) and FTSE (-0.02%) were not able to stay above water. European futures are down around -1.2% this morning.

As our economists point out (see their note here) this was a unique ECB meeting as for the first time we saw a unanimous post-dated decision to act at the next meeting (December in this case). The composition of that action remains to be determined however, and will be a function of events, both pandemic and economic, over the next six weeks. Our economists suggest that the emphasis on “all instruments” being under consideration is a message to think beyond just PEPP. The sensitivity to weak private credit implies changes to the TLTRO framework. For the time being, they hold onto their view of a composite easing strategy in December: a package of measures, including tweaks to the TLTRO framework, to complement more PEPP in one form or another to address the pandemic risk and more APP to address the persistent low inflation problem.

As they also point out, six weeks can be a long time in a non-linear pandemic. However, post-dated action is not to be confused for ECB inactivity for the next six weeks. ECB President Lagarde emphasised the flexibility of existing programmes like PEPP to respond to any downside surprises. There is still more than half the PEPP available and it is flexible enough to be deployed on an “anytime, anyplace, anywhere” basis. The pace of purchases can re-accelerate if necessary.

The euro fell -0.61% by the end of the day to one month lows but that was as much due to dollar strength as half the move occurred before the ECB meeting. 10yr bund yields fell -1.1bps to -0.64%. With the signal of added ECB support peripheral bond yields fell, with Italian (-6.2bps), Spanish (-3.4bps), Greek (-10.7bps) and Portuguese (-3.5bps) 10yr bonds all tightening to 10yr bunds. US Treasuries fell with the risk on sentiment, as yields rose +5.2bps to 0.823%, the largest one day rise in over three weeks.

In terms of data, the US economy expanded at a record 33.1% (annualised) pace off the lows of the pandemic, with business reopening and consumer spending powered by stimulus injections. The rise in GDP, which on a quarterly basis is 7.4%, slightly beat market expectations of 32.0%, and comes after Q2’s also record decline of -31.4%. Overall, GDP is now -3.5% below pre-virus (Q4 2019) levels. In terms of components, consumer services spending was -7.7% below pre-virus levels, but consumer goods spending +6.7% above. There was also initial jobless claims out of the US, where claims in regular state programs totaled 751k in the week ended Oct. 24, down 40k from the prior week. Continuing claims decreased 709k to 7.76mn in the week ended Oct. 1, having now fallen for five straight weeks. Overall these were positive data points, but the virus’s progression may impact the winter readings going forward.

With less than five full days before polls close in the US elections, former Vice President Joe Biden is currently in a strong position with the fivethirtyeight.com model giving him an 89% chance of winning, the highest so far, and a national polling average lead of +8.8. Biden holds strong polling leads in the key Midwest swing states of Pennsylvania (+5.2pts), Wisconsin (+8.4pts), and Michigan (+8.1pts), and is also leading to a smaller degree in the Sunbelt swing states of Florida (+2.1pts), North Carolina (+2.2pts) and Arizona (+2.7pts). Biden can win by just carrying the Midwest but, as has been highlighted before, we are likely to know results from the latter group of states earlier because they process mail-in ballots ahead of the election and both Florida and North Carolina will also be allowed to count votes ahead of time. A quick win there for Biden and the “Blue Wave” could materialise rapidly, but a Trump win in that part of the map and we could be waiting until the end of the week at least. The Secretary of State in Pennsylvania has said that the “overwhelming majority” of votes should be counted by next Friday, but that is still at least 3 days of uncertainty and that is before we get to any implications of Supreme Court rulings.

Staying on politics EU Commission President Ursula von der Leyen stated that Brexit talks are ‘making good progress’ and are now ‘boiling down to the two topics that are the most important – Level Playing Field and fisheries’. These two issues as well as a mechanism in the final treaty for resolving future disputes are among the most important outstanding points. European Council President Michel, expressed the expectation that the state of the negotiations would probably be assessed next week with his hope being to start the ratification process in mid-November.

On the coronavirus, hospitalisation rates in some countries are approaching peak levels seen during the first wave. Belgium reported 5,924 patients currently hospitalised, surpassing its previous peak from back in April. While in Portugal, the number of ICU patients is now 269, just short of its previous peak of 271. Similarly in Italy, there are now 17,615 patients in hospitals, though capacity still remains there compared to the nearly 29,000 back in April. This is why countries throughout Europe have been enacting new restrictions to try to flatten the curve again. Yesterday Sweden, whose actions have been among the most scrutinised, announced that residents in Stockholm are to avoid shops, gyms and any other indoor venues that don’t provide essential services. This comes as the country has seen around 3,000 new cases, a record daily rise. In the US, weekly cases have hit record highs as the virus continues to spread through the Southern and Midwestern regions. However yesterday there was troubling news out of the northeast, which had been resistant to a second wave, as New Jersey’s and New York’s positivity rates of covid-19 tests hit their highest levels since May. Lastly Dr Fauci predicted yesterday that normality may not return until late 2021 even with an effective vaccine broadly distributed.

Looking ahead to today there will be readings of France, German, Italian and Euro Area Q3 GDP. As well as CPI data for France and Italy and unemployment data for Italy and the Euro Area. In the US, we will get personal spending and income data along with PCE core deflator. There is also the MNI Chicago PMI and final University of Michigan sentiment reading for October. In terms of Central Banks, the ECB’s Weidmann is expected to speak. About halfway through earnings, we will see results today from Novo Nordisk, AbbVie, ExxonMobil, Charter Communications, Chevron, Total and NatWest Group.

3A/ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 48.19 PTS OR 1.47% //Hang Sang CLOSED DOWN 479.18 PTS OR 1.95% /The Nikkei closed DOWN 354.81 PTS OR 1.52%//Australia’s all ordinaires CLOSED DOWN 0.56%

/Chinese yuan (ONSHORE) closed /Oil DOWN TO 36.23 dollars per barrel for WTI and 38.13 for Brent. Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6844. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6861 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

CHINA/

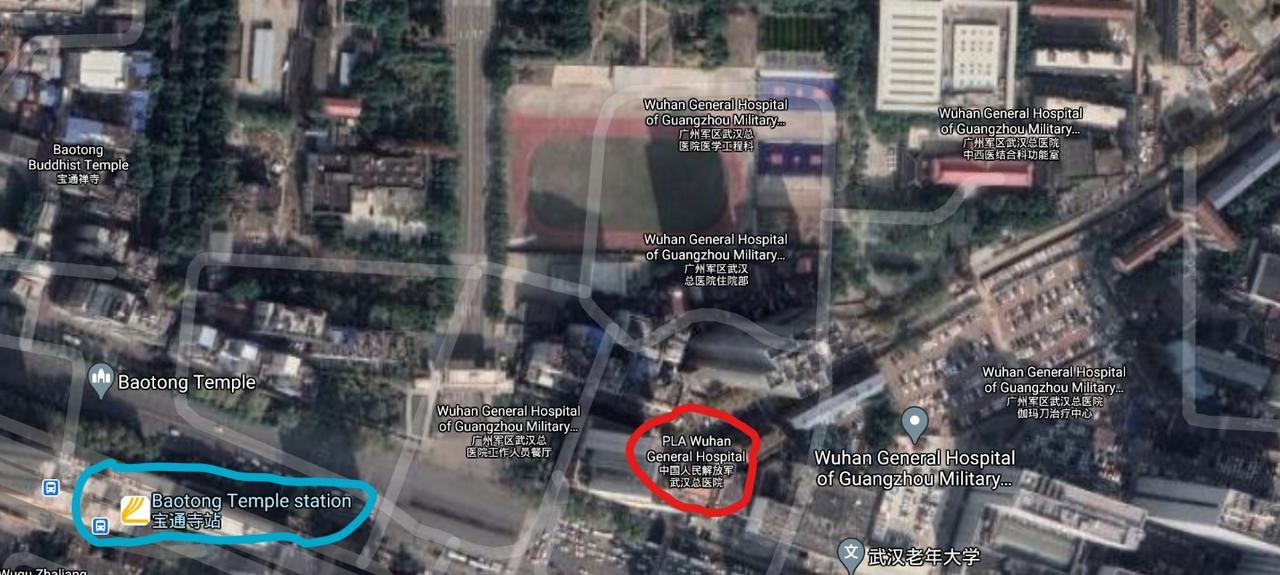

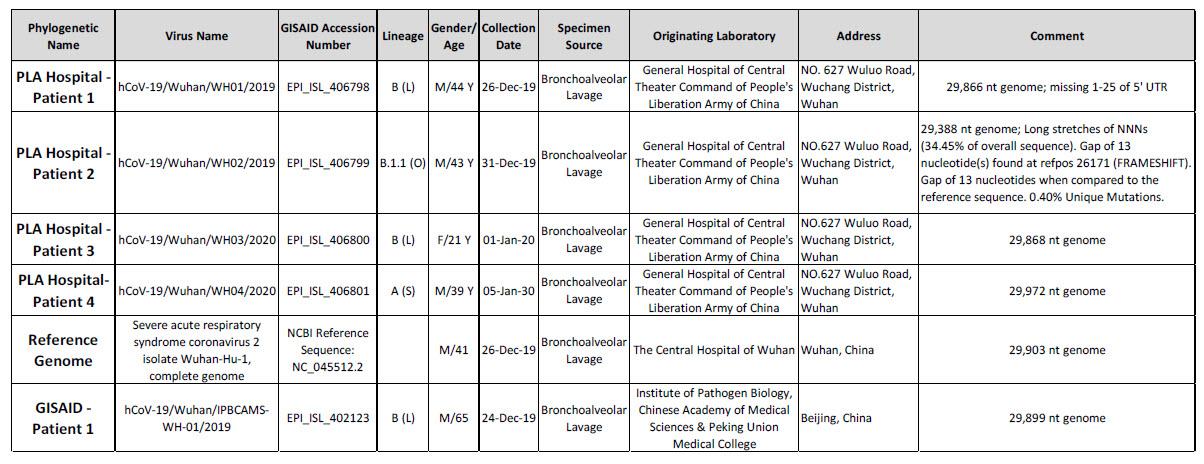

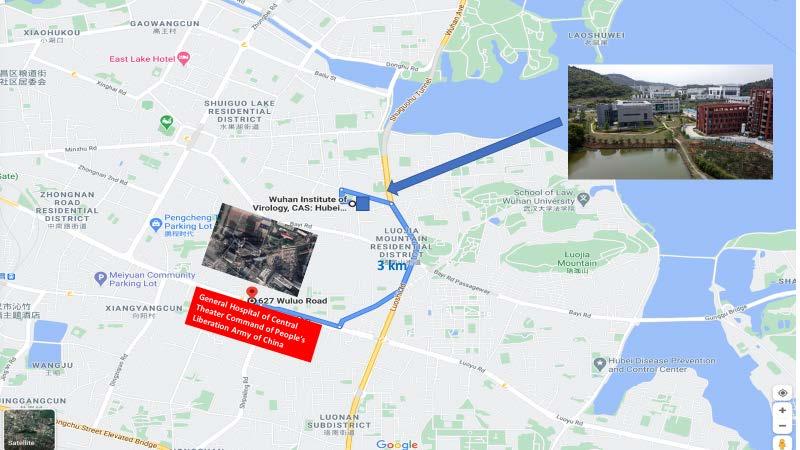

New Research Points To The People’s Liberation Army Hospital In Wuhan As Origin For Global Coronavirus Pandemic

A paper published on Zenodo (DOI 10.5281/zenodo.4119263) by Dr. Steven Quay, M.D., PhD., head of two COVID-19 therapeutic programs at Atossa Therapeutics, illuminates new scientific observations and conclusions documenting that the SARS-CoV-2 pandemic began at the General Hospital of Central Theater Command of People’s Liberation Army (PLA Hospital) in Wuhan, China, located at 627 Wulon Road, Wuchang District, Wuhan.

According to the paper, international biospecimen data repositories indicate as early as December 10, 2019 COVID patient records were being created by PLA personnel, weeks before the Chinese government informed the WHO of the pandemic.

The paper documents four patients from the PLA Hospital that have the earliest genetic signature of direct human-to-human coronavirus transmission. It also includes the patient whose coronavirus is genetically closest to a bat virus from the Wuhan Institute of Virology (WIV) that WIV scientists call “the closest relative of 2019-nCoV.”

The PLA Hospital is three kilometers from WIV and both are located on Line 2 of the Wuhan Metro System. The paper documents an analysis of the hospitals where the earliest COVID patients were seen, between December 1, 2019 to early January, and shows that all these hospitals were also located on the Metro Line 2.

This is the first paper in the world to observe that Line 2 is uniquely positioned to have been the worldwide human-to-human COVID pandemic conduit as it carries five percent of the population of Wuhan every day, allowing rapid spread throughout Wuhan and the entire Hubei Province; it includes the high-speed rail station, allowing rapid spread throughout China; and it terminates at the international airport station, allowing rapid spread throughout the world.

Line 2 also services the Hunan Seafood Market, previously suggested to be associated with the origin of the pandemic.

The full paper can be read below (pdf link)

A very big story: China’s digital yuan is aiming to halt dollarization. China is now ready to combat the USA and no doubt gold and the new gold-yuan will play a pivotal role

China’s Central Bank Poised To Legalize Digital Yuan As Part Of Sovereign Fiat Currency

China is poised to give legal backing to the launch of its own sovereign digital currency, cementing its trailblazer status in virtual currencies far ahead of other countries, after already recently experimenting with large-scale trials of actual payments by consumers, which was met with mixed results.

The South China Morning Post reported Tuesday that “The People’s Bank of China (PBOC) published a draft law on Friday that would give legal status to the Digital Currency Electronic Payment (DCEP) system, and for the first time the digital yuan has been included and defined as part of the country’s sovereign fiat currency.”

Up until very recently, the whole project has been kept very secretive even during the latest closed, limited tests among select parts of the population. Previous reports described it acting akin to well-known stablecoins in the cryptocurrency world.

The design framework for the digital yuan was released one year ago on the heels of Facebook’s ambitious but disastrous Libra token rollout after founding corporate partners split for lack of confidence in the project and on fears US federal regulators would seek to block it just as they did encrypted-messaging company Telegram’s Gram cryptocurrency.

“The draft law would also forbid any party from making or issuing yuan-backed digital tokens to replace the renminbi in the market,” SCMP continues.

Amid reports early this week that Beijing is fast moving on the digital yuan’s legal status, Bitcoin’s price hit a new 2020 high at $13,670 on Tuesday.

Within the past months the government conducted multiple trials in the cities Suzhou, Chengdu, Xiongan and Shenzhen – in the latter city conducting the largest test so far by issuing a total ten million yuan (US$1.5 million) in digital currency to 50,000 randomly selected people to use. “It was as quick as when I use Alipay,” one Shenzhen resident said in reference to one of China’s two largest mobile payment apps.

But regional media have also featured consistent negative reactions. China’s government has sought to downplay that the DCEP is a competitor to Alipay and WeChat, which was a consistent issue during the latest major trials among shoppers, as Asia Times relates:

“Alipay and WeChat Pay have been out for a long time,” said a shopper who gave only her surname, Zhong. “The new digital currency is similar to those so it’s quite late to just start the trial,” said Zhong, an accountant.

One bombshell section of the SCMP report lays out eyebrow raising ambitious goals as follows:

The central government has made it clear that the goals of the DCEP include replacing cash, maintaining government control over the currency and creating as many small retail application scenarios as possible. China is also looking to internationalize the yuan by enhancing its use in international settlements.

For the above goals to be realized the DCEP would have to prove itself just as efficient as using paper yuan, which obviously raises the issue of personal electronic devices going offline. The payment system is said to incorporate dual offline technology to compensate for this potential major issue in cases of weak signals. All of this would be crucial in getting the average consumer to adopt the technology, especially when it comes to small retail exchanges – which remains common to the majority of the Chinese population.

4/EUROPEAN AFFAIRS

UK

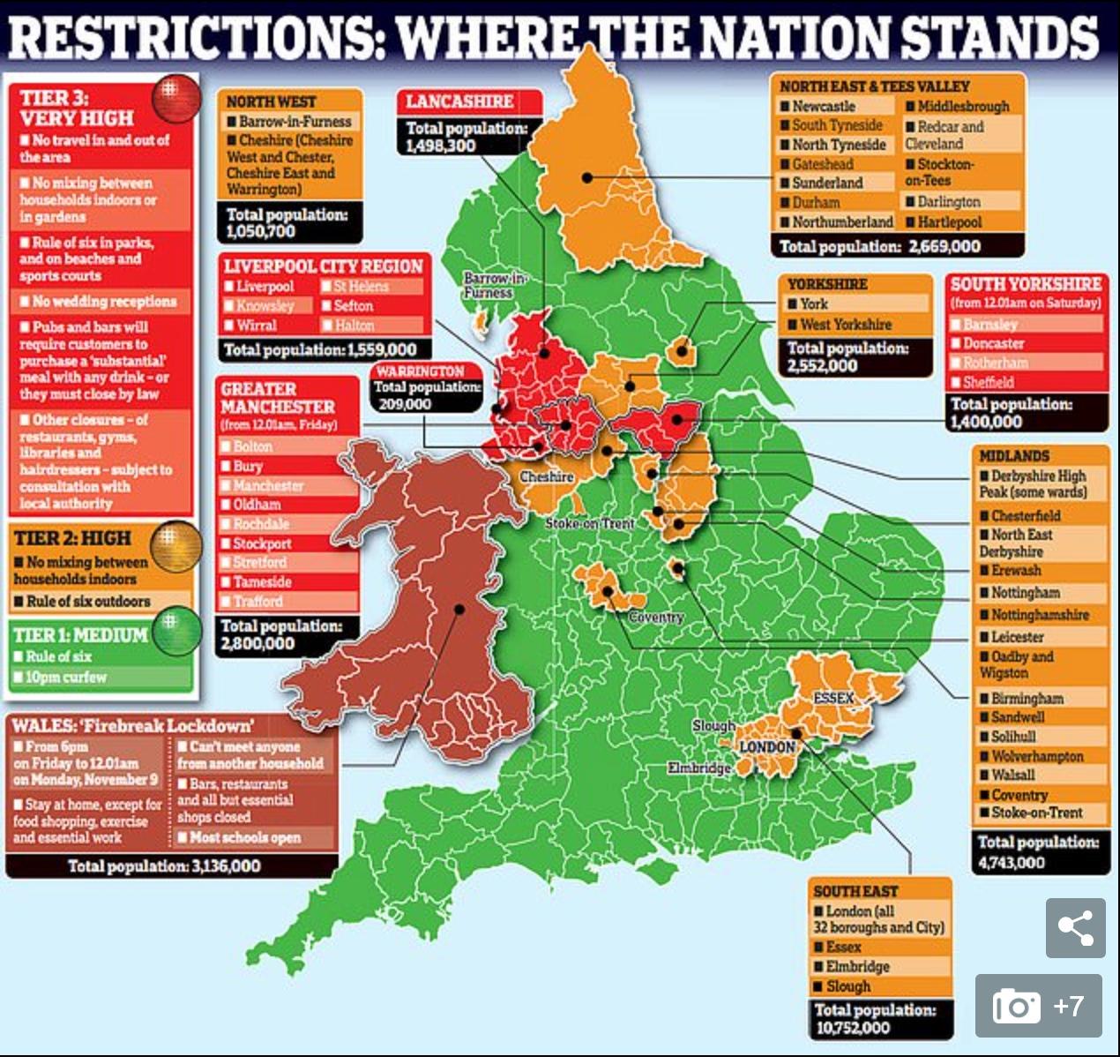

UK cops will raid lockdown rule defying citizens (Christmas celebrations) there is fear the move could very well spark civil unrest.

(zerohedge)

UK Cops Will Raid Lockdown-Rule-Defying Christmas Celebrations; Fear Move Could Spark Civil Unrest

As local mayors battle with the UK’s central government over the terms of anti-coronavirus lockdown measures, local police chiefs are warning that Britons may be in store for a holiday season distinctly reminiscent of the “Red Terror”.

Several police chiefs warned that family Christmas celebrations could be broken up by intruding officers if households are found to have violated the lockdown rules.

David Jamieson, commissioner of the West Midlands police, said officers will be compelled to investigate reports of rule-breaking over the festive period, since the West Midlands is currently under Tier 2 restrictions, meaning people can’t mix with anyone outside their own household or bubble.

Speaking to the Telegraph, Jamieson said “if we think there’s large groups of people gathering where they shouldn’t be, then police will have to intervene. If, again, there’s flagrant breaking of the rules, then the police would have to enforce.”

“It’s not the police’s job to stop people enjoying their Christmas. However, we are there to enforce the rules that the Government makes, and if the Government makes those rules then the Government has to explain that to the public.”

But seeing that the UK is, after all, a multicultural society, it’s not just Christmas that will be affected by the latest COVID-19 restrictions: Hanukkah and Diwali celebrations will face strict enforcement as well.

As we reported earlier this month, Johnson’s new system could be in place for as long as six months. It divides England into three tiers (the other constituent nations are handling their own restrictions. Wales recently imposed a 2-week “firebreak” lockdown).

Here’s a quick breakdown of restrictions across England courtesy of the Daily Mail.

Jane Kennedy, the top cop in Merseyside, another Tier 3 region, said she would investigate reports of illegal gatherings over Christmas, affirming the trend across the Tier 3 areas. Jamieson, meanwhile, said he fears unrest as the new restrictions arrive just as the furlough scheme for workers is ending, leaving many broke, desperate and depressed as we head into the holiday season.

“We’re sitting on a time bomb here,” he said.

“We’re getting very near the stage where you could see a considerable explosion of frustration and energy.”

Just like we’ve seen in the US, any rioting caused by the restrictions could be exacerbated by criminals taking advantage of the chaos.

War Spillover: Turkish & Azeri Mobs Hit Streets “Looking For Armenians” In France

The latest terrorist killings to rock France as tensions grow centered on the country’s firm free speech traditions as a secular republic vs. Muslim immigrant outrage over negative depictions of Muhammad in French media have grabbed international headlines, but other disturbing trends which have received much less attention suggest the violence looks to grow.

This week there have been reports of clashes between Turkish-Azeri demonstrators and Armenians on the streets of France. On Wednesday multiple videos circulated widely on social media which appear to show Muslim Turks and Azeris “hunting down” Armenian Christians as the war in Nagorno-Karabakh spills over onto the streets of Europe.

Some other European cities have also witnessed rising tensions between Turkish and Armenian neighborhoods related to conflict in the Caucasus.

Turkey is of course a close ally of Azerbaijan in the current fighting against Armenia in the breakaway Karabakh border region. Armenians as an ethnic group have also long been targets of Turkish hatred going all the way back to the Armenian Genocide of the early 20th century.

Here’s how The Independent describes the below video from Lyon, France:

In one video shared by an independent Armenian outlet, people can be seen marching in Lyon with Turkish flags and chanting the phrase “allahu akbar”, meaning “God is the greatest”.

In the same piece of footage, a man can be heard saying in French: “Where are you Armenians? Where are you? We are here… sons of b*****s”.

The Independent said the videos appear to confirm the angry demonstrators were “looking for Armenians”.

The mob reportedly formed after a pro-Armenia demonstration blocked a motorway connecting Lyon and Marseille on Wednesday morning.

The Armenian demonstration broke out into violence after Turkish nationalists reportedly tried to disrupt the rally. Clashes resulted in at least four injured, which French police are said to be investigating.

Turkish flags could be seen and nationalist chants heard, as well as anti-Armenian slogans amid the mayhem, which appeared to have eventually been broken up by police.

end

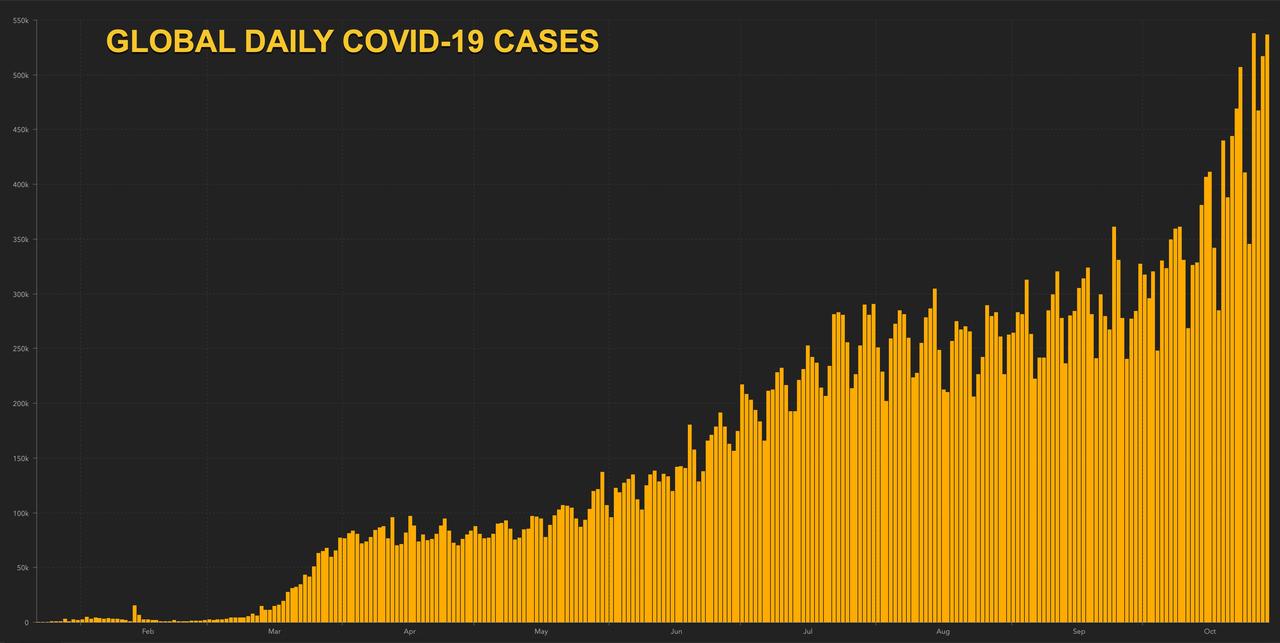

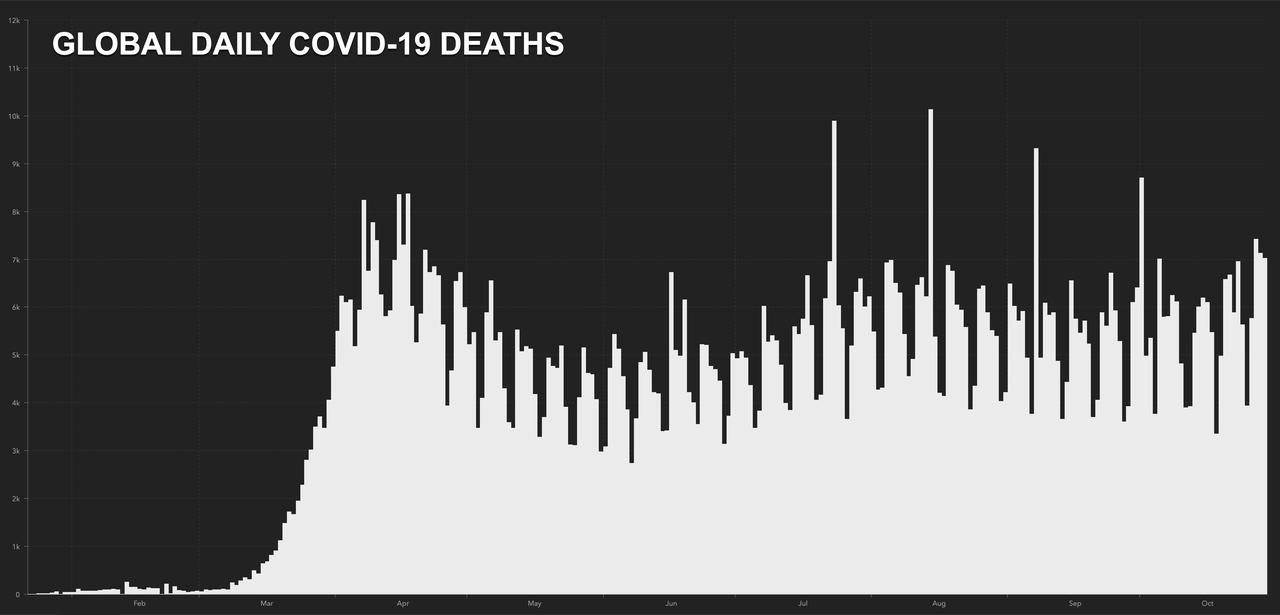

CORONAVIRUS UPDATE/GLOBE

UK Accelerates Vaccine Trials, US Reports Nearly 90k New COVID-19 Cases In Latest Record Jump: Live Updates

Summary:

- Global cases top 45 million

- Taiwan celebrates record COVID-19-free streak, best growth in developed world

- US reports 89k new cases

- UK accelerates vaccine approval

- Germany reports record jump

- Japan tops 100k

- HK customs agents seize counterfeit masks

- Indonesia reports most cases in 2 months

* * *

Global COVID-19 cases topped 45 million on Thursday as France outlined its plan for trying to mitigate the impact of the new quasi-lockdown (which began Friday) after European economies reported their Q3 GDP figures, with most coming in hotter than expected, even as deflation across the eurozone endured.

As Europe saw better-than-expected economic growth in the quarter, Taiwan, which has become – much to Beijing’s dismay – an exemplar of COVID-19-fighting efficiency, saw the fastest growth rate among any developed economy in Q3. Its economy actually expanded 3.3% year over year, its fastest rate of grwoth in more than 2 years, and a reversal from a 0.6% drop from Q2.

Health authorities from around the world reported another near-record on Thursday, with new cases again coming in above 530k for the second time ever (the first time was Monday):

Daily deaths topped 7k again yesterday, driving the 7-day average even higher as higher infection & hospitalization rates have finally started to cause mortality to creep higher.

The US, meanwhile, reported another record jump in new COVID-19 cases on Thursday, with 88k+ new cases, bringing the US total to 8,947,862, within striking distance of the 9 million mark.

Deaths in the US came in just below 1,000.

Perhaps the biggest vaccine-related news last night comes out of Europe, where the UK’s drug regulator is said to have ordered accelerated reviews of vaccines under development from Pfizer and AstraZeneca as UK PM Boris Johnson faces growing pressure to order a lockdown for before and after the Christmas holiday, to allow families to gather during the holiday.

German cases exceeded 500,000 after officials reported a new daily record of 18,681 new cases on Friday, as authorities added almost all of Austria and Italy to the list of high-risk areas, warning German travelers not to go there.

In Asia, Japan finally crossed the 100,000-case mark 9 months after reporting its first infection.

Here’s some more COVID-19 news from Friday and overnight:

Confirmed coronavirus infections in Slovakia have hit a new record high as the country gets ready for a nationwide testing. The Health Ministry says the day-to-day increase in the country of 5.4 million reached 3,363 on Thursday, over 300 more than the previous record set on Saturday (Source: AP).

Customs agents in the southern Chinese city of Hong Kong have seized 100,000 counterfeit face masks and arrested one person in what the government called the largest operation of its kind on record. The masks were set to be shipped overseas and had a market value of almost $400,000, the government’s Information Services Department reported Friday (Source: AP).

Indonesia reported 2,897 confirmed cases in the 24 hours through midday Friday, the least in almost two months. The country remains the site of Southeast Asia’s largest outbreak, and the government has been wary a long weekend doesn’t lead to a spike in infections (Sources: Bloomberg).

Sweden’s government has underestimated the cost of testing and tracing Covid-19 patients and the money that’s been earmarked for the purpose is now running out, TV4 reports (Source: Bloomberg).

Poland’s health-care system is “stretched to its limits,” Michal Dworczyk, chief of staff in Prime Minister Mateusz Morawiecki’s office, says in interview with public radio 1 (Source: Bloomberg).

END

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

TURKEY/FRIDAY MORNING

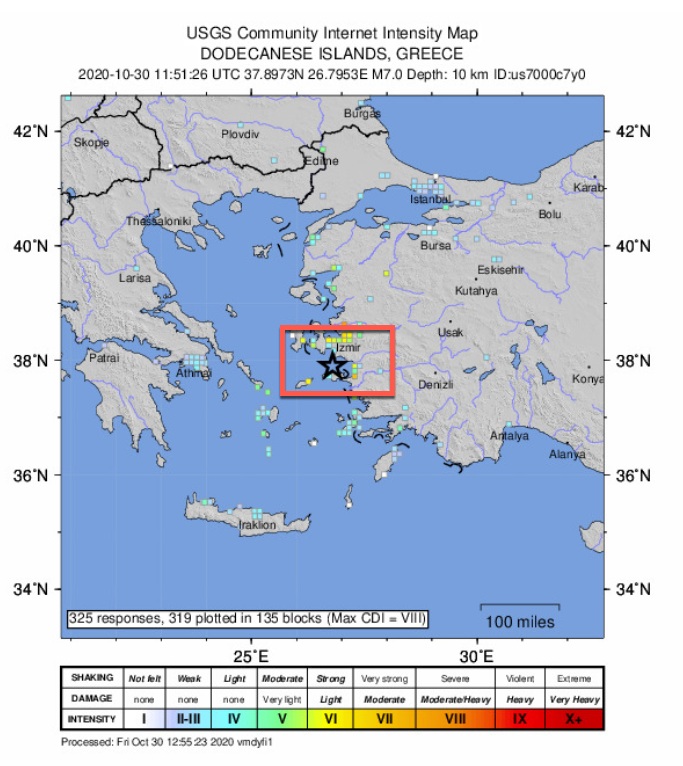

I guess when it rains, it pouts: Turkey hit with a powerful 7.0 earthquake just north of Izmir

(zerohedge)

Powerful Earthquake Rocks Turkey, Greece; Tsunami Reported

Update (0955 ET): Turkey’s Disaster and Emergency Management Presidency reports 120 injured in today’s earthquake. Judging by what we’ve seen so far, that number is expected to rise.

* * *

A powerful earthquake in the Aegean Sea rocked Turkey and Greece on Friday. The quake’s epicenter is off Turkey’s Aegean coast, north of the Greek island of Samos.

Turkey’s Disaster and Emergency Management Presidency said the quake was in the Aegean Sea at a depth of 10.3 miles. Seismometers in the area measured the quake at 6.6 magnitude. The U.S. Geological Survey said the earthquake measured at 7.0.

There are no official reports on casualties and or the destruction the quake left behind, but local media and citizen journalists report collapsed structures throughout Izmir, Turkey.

Social media users are also reporting a tsunami has struck the area.

Insane video of what appears to be a residential building in Izmir collapsing after the quake.

Numerous building structures across Izmir appear to have collapsed.

Turkish live streamer interrupted during the earthquake.

Canlı yayında #deprem #izmir #Seferihisar pic.twitter.com/tLYdkqKaYl

— Selâmi Haktan (@slmhktn) October 30, 2020

END

Report Alleges Trump Quashed Criminal Probe Into Turkish Bank That Funneled Billions To Iran

Prior bombshell claims in former national security advisor John Bolton’s book released last summer alleging that President Trump had agreed to quash a federal probe into a Turkish state-owned bank as a personal favor to Recep Tayyip Erdoğan just got a major boost.

Bolton wrote of scandal-hit Halkbank that in a 2018 phone call after Erdoğan insisted the bank was innocent of sanctions-busting by funneling billions of dollars in cash and gold to neighboring Iran: “Trump then told Erdoğan he would take care of things, explaining that the [New York] southern district prosecutors were not his people but were Obama people, a problem that would be fixed when they were replaced by his people,” according to the book.