GOLD:$1833.90 DOWN $2.30 The quote is London spot price

Silver:$23.97 UP 8 CENTS London spot price ( cash market)

ACCESS MARKET

i)Gold : $1836.50 LONDON SPOT 4:30 pm

ii)SILVER: $23.99//LONDON SPOT 4:30 pm

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

c

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 1.31 POINTS OR .04% //Hang Sang CLOSED DOWN 92.25 POINTS OR .35% /The Nikkei closed DOWN 61.70 POINTS OR 0.23%//Australia’s all ordinaires CLOSED DOWN 0.69%

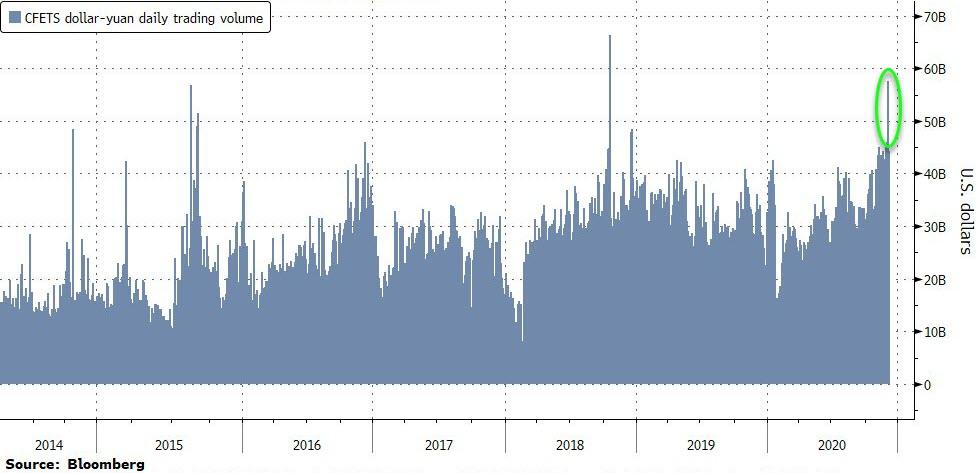

/Chinese yuan (ONSHORE) closed DOWN AT 6.5435 /Oil UP TO 46.10 dollars per barrel for WTI and 49.45 for Brent. Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.5435. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.5365 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

We had 1 kilobar transactions

ADJUSTMENTS: 0 //

The front month of DEC registered a total of 8,085 contracts for a loss of 1699. We had 1637 notices filed upon yesterday so we LOST A TINY 62 contacts or 6,200 additional oz will NOT stand in this very active delivery month of December as these small number of longs gave up on physical over here and thus they morphed into London based forwards and they received a fiat bonus for their efforts.

January lost 58 contracts to stand at 2196 contracts. FEBRUARY LOST a STRONG 4476 contracts DOWN TO 400,179.

THE BIG STORY AGAIN TODAY IS THE HIGH INITIAL OI STANDING FOR DECEMBER (93.206 tonnes). LONGS STANDING FOR GOLD REFUSE TO TRAVEL TO LONDON

We had 395 notice(s) filed today for 39,500 oz OR 1.2286 TONNES.

To calculate the INITIAL total number of gold ounces standing for the DEC /2020. contract month, we take the total number of notices filed so far for the month (22,266) x 100 oz , to which we add the difference between the open interest for the front month of (DEC 8095 CONTRACTS ) minus the number of notices served upon today (395 x 100 oz per contract) equals 2,996,600 OZ OR 93.206 TONNES) the number of ounces standing in this active month of DEC

thus the INITIAL standings for gold for the DEC/2020 contract month:

No of notices filed so far (22,266, x 100 oz +8095 OI) for the front month minus the number of notices served upon today (395) x 100 oz which equals 2,996,600 oz standing OR 93.206 TONNES in this active delivery month of December. This is a HUGE amount for gold standing for DEC delivery month (generally the strongest delivery month of the year). THE COMEX IS UNDER A HUGE FRONTAL ATTACK FROM EUROPEAN BANKS SEEKING PHYSICAL METAL! JUDGING FROM THE INITIAL NOTICES FILED VS THE NUMBER OF NOTICES STANDING, IT WILL BE EXTREMELY DIFFICULT FOR OUR BANKERS TO FIND THE NECESSARY GOLD TO SATISFY OUR EUROPEANS.

NEW PLEDGED GOLD: BRINKS

455,219.430, oz NOW PLEDGED SEPT 15.2020/HSBC

60,784.803 PLEDGED APRIL 3/2020: SCOTIA:

deleted Int. Delaware pledge July 7 (600 tonnes)

292,197.145 oz JPM 8.70 TONNES

819,082.972 oz pledged June 12/2020 Brinks/

88,796.123 oz Pledged August 21/regular account 1.588 tonnes JPMORGAN

178,807.987 oz Pledged Nov 27.2021 MANFRA

total pledged gold: 1,894,888.460. oz 58.93 tonnes

total registered, pledged and eligible (customer) gold 37,434,347.176 oz 1,164.36 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 1038.02 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of July 2018. and it continues to present day.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

And now for the wild silver comex results

And now for the wild silver comex results

INITIAL STANDINGS

DEC. SILVER COMEX CONTRACT MONTH//INITIAL STANDING

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

|

Withdrawals from Customer Inventory |

1916.450 oz

CNT

|

| Deposits to the Dealer Inventory |

nil oz

Manfra

|

| Deposits to the Customer Inventory |

1,047.860 oz

CNT

|

| No of oz served today (contracts) |

80

CONTRACT(S)

(400,000 OZ)

|

| No of oz to be served (notices) |

1015 contracts

5,075,000 oz)

|

| Total monthly oz silver served (contracts) | 8172 contracts

40,860,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

https://www.youtube.com/watch?v=qL_OSus7LQw

Comex catch 22. Stand for Physical Gold delivery at an Unallocated paper price and get paid NOT to take delivery!

This is unsustainable.

Best

Andrew

Attachments area

Preview YouTube video Andrew Maguire: Gold, Silver Smashes Sanctioned By BIS

Andrew Maguire: Gold, Silver Smashes Sanctioned By BIS

end

A biggy!!

huge demand for silver eagles coins, now surpassing 30 million. Investment demand is now surpassing industrial demand

Steve St Angelo/SRSReport

and special thanks to Doug C for bringing this to my attention

Silver Eagle Sales Blow Pass 30 Million & Prepare For Fireworks As Investment Demand Surpasses Industrial Demand

U.S. Silver Eagle sales this year are RED HOT pushing total silver investment demand to record highs. According to the U.S. Mint’s most recent update, Silver Eagle sales in 2020 have surpassed 30 million and may continue to increase over the next few weeks in December. Also, for the first time ever, total silver investment demand exceeded industrial demand by a wide margin.

So, for the analysts who continue to harp on “Industrial Demand” as an important factor for the silver market to focus on in the future, I say… RUBBISH. And, if you have been reading my analysis for several years, I’ve stated over and over again, that industrial demand will become less of a driver of the silver price in the future.

Thus, when I read the Zerohedge article today, Saxo Bank, 2021 Will Be A “Reality Check On Extend-And-Pretend” – Saxo Bank Unveils Its ‘Outrageous Predictions’ For The Year Ahead, quoting the following about silver in 2021.

Sun shines on silver, which sizzles on solar panel demand

2021 brings the usual suspects that power silver higher on its hard asset/precious metal side as the US dollar weakens, and as investors are faced with the harsh reality of no relief in sight from negative real interest rates. This is exacerbated as inflation suddenly jolts higher in 2021, and policymakers are slow to respond, wanting to offer maximum support for their still-recovering economies. With a Covid-19 vaccine in rapid rollout by the middle of the year, the excessive liquidity and over-easy policy drives a powerful bid into any hard asset.

Turbocharging the rise in the silver price in 2021, even relative to gold, is the rapidly rising demand for silver in industrial applications. In fact, a real silver supply crunch is on the cards in 2021, and it frustrates the full throttle political support for solar energy investments under a Biden presidency, the European Green Deal, and China’s 2060 carbon neutral goal, among other initiatives.

While Saxo Bank analysts get it right about a likely “Silver Supply Crunch” in 2021, their focus on Solar Power as a leading factor for the silver market in the future is typical of a financial industry that is stuck on STUPID. Gosh, I hate to be so BLUNT, but there it is.

If I hear one more analyst regurgitate about the “WONDERS” of future silver PV Solar demand, I will send them the following chart.

According to the new Silver Important Role In Solar Power Report by CRU Consulting for the Silver Instutite (June 2020), silver consumption in PV Solar Cells will continue to trend lower until 2026 and then remain flat until 2030. Also, the Metals Focus Consultancy stated in the Silver Institute’s 2021 Interim Report, that silver demand in PV Solar will fall 11% in 2020.

The falling silver consumption in the Solar Industry has to do with the PV cells becoming more efficient and a flattening of new solar installations.

Regardless, the notion that silver industrial demand will continue to be a key factor in the future becomes LESS IMPORTANT when we look at the following chart.

The 2021 Silver Interim Report published last month forecasts industrial and photography demand to decline to 495 million oz (Moz) in 2020 versus 544 Moz last year. However, total silver physical and ETF investment demand is estimated to reach 587 Moz, the highest ever and the first time that it has surpassed industrial demand.

You will notice that the 10-year average annual industrial silver demand is 529 Moz compared to 261 Moz of total silver investment. Thus, over the past decade, industrial demand (including photography) has been twice that of total investment demand. That all changed this year as total silver investment demand is nearly 100 Moz more than industrial demand.

What happens next year if we see the same amount of total silver investment demand?? We could see huge moves in the silver price as I believe it will be hard for the Silver ETFs and Dealers to access another 600 Moz easily.

SRSrocco Report Forecast 2021-2025

Watch as Silver Investment demand begins to overwhelm the market as the Fed and central banks continue to print trillions of worthless fiat-digital currency as the debt skyrockets. At some point, the central banks will have to deal with SOLVENCY ISSUES, and you don’t want to be in most STOCKS and BONDS at that time.

Silver Eagle Sales Blow Past 30 Million In 2020

The U.S. Mint updated its figures for December reported 751,000 Silver Eagles were sold during the first seven days and 22,500 oz of Gold Eagles. This puts the total Silver Eagles for 2020 at 30,089,500 and Gold Eagles at 817,000 oz. Silver Eagle sales in 2020 are now double what they were last year at 14,863,500.2020 Gold Eagle sales are 817,000 oz versus 152,000 oz during full-year 2019.

What’s amazing about the 2020 Silver Eagle sales? They are almost the same amount compared to full-year 2018 and 2019 combined.If the U.S. Mint continues to sell 2020 Silver Eagles to the Authorized Dealers, we could easily see 31-31.5 million for the year. However, at some point, the U.S. Mint will begin to produce the new 2021 Silver Eagles and will no longer offer the 2020 coin. We will see.

With the ERA of CHEAP GOLD & SILVER gone forever, investors need to realize there aren’t that many assets that protect wealth. As I have stated repeatedly, most STOCKS, BONDS, and REAL ESTATE are Energy IOUs, while GOLD & SILVER are stores of Energy Equivalent Value.

Most investors may not understand that the precious metals are stores of energy equivalent value, but as the world heads over the ENERGY CLIFF, they will begin to get reacquainted… and quickly.

DISCLAIMER: SRSrocco Report provides intelligent, well-researched information to those with interest in the economy and investing. Neither SRSrocco Report nor any of its owners, officers, directors, employees, subsidiaries, affiliates, licensors, service and content providers, producers or agents provide financial advisement services. Neither do we work miracles. We provide our content and opinions to readers only so that they may make informed investment decisions. Under no circumstances should you interpret opinions which SRSrocco Report or Steve St. Angelo offers on this or any other website as financial advice.

Check back for new articles and updates at the SRSrocco Report. You can also follow us on Twitter and Youtube below:

Please, consider becoming an SRSrocco Report Member!!

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Futures Fail To Rebound After Wednesday Rout On Growing Brexit, Covid Fears

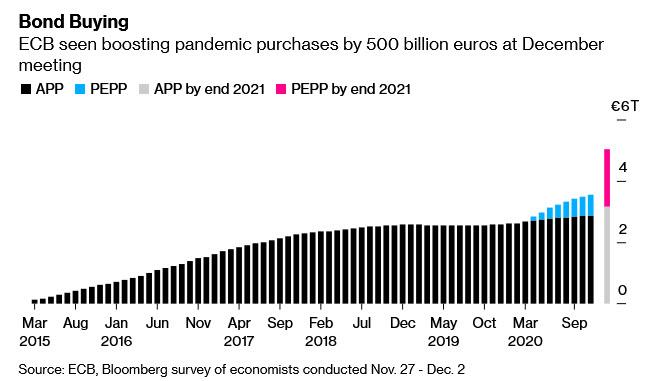

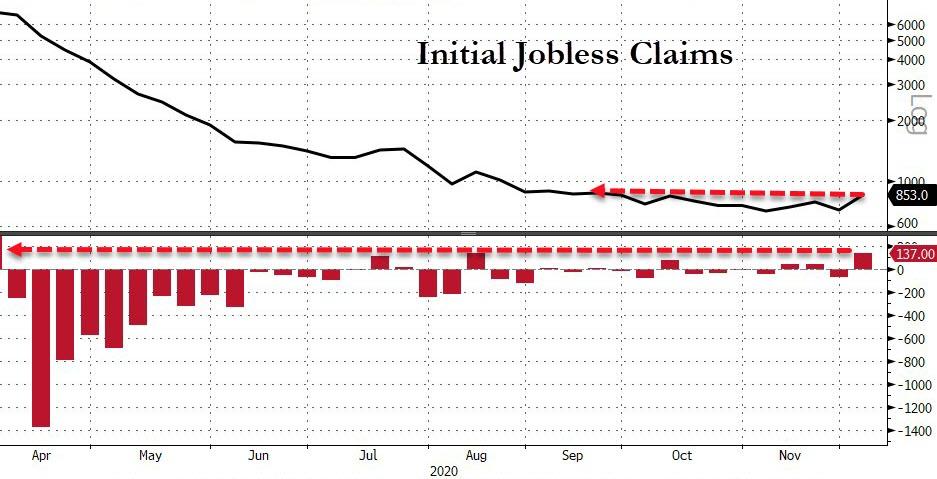

Futures tried and failed to rebound from Wednesday’s rout as fears that the Brexit process was coming unhinged and growing pessimism for a fiscal deal in Congress offset optimism for a swift roll out of a COVID-19 vaccines while concerns about a double dip were set to grow after a report that shows another increase in weekly jobless claims. Not even the ECB’s imminent reveal of another €500 billion in QE helped push stocks higher.

The furious November rally in global equities which pushed stocks to record highs as recently as Tuesday, slowed this week as the pandemic causes even more shutdowns and negotiations over a U.S. aid package seem bogged down. That has investors counting on continued easing and bond buying by central banks to support risk assets and possibly reflation into 2021, including the ECB decision today. Nasdaq 100 contracts turned lower, accelerating its biggest drop in a month on news that Facebook was being sued by U.S. antitrust officials. The social media giant slipped further in pre-market trading on Thursday. Airbnb Inc. priced its long-awaited initial public offering above a marketed range to value the company at about $47 billion.

“We’ve risen so far so fast that it’s making investors cautious,” said Michael McCarthy, chief strategist at stockbroker CMC Markets in Sydney. “The fall in tech stocks was a bit of a concern, given that they’ve risen in all market weather over the last six weeks, so to see them come off might signal that we’re looking at a short- term corrective move.”

Europe’s STOXX 600 index was flat, though London’s FTSE 100 did score its eighth straight gain as the Brexit uncertainty pushed the pound down 0.7% to $1.33 and 90.86 pence per euro. Gains in food and beverage shares were undercut by declines in technology stocks. STMicroelectronics NV dropped as much as 3.3%, extending Wednesday’s 12% plunge that followed the chipmaker’s disappointing medium-term outlook.

European Union and British leaders gave themselves until the end of the weekend to seal a new trade pact, with some $1 trillion in annual trade at risk of tariffs if they can’t reach a deal by Dec. 31, when transition arrangements end. “There’s still clearly some scope to keep talking, but there are significant points of difference that remain,” Foreign Secretary Dominic Raab told BBC TV. “(On) Sunday, they need to take stock and decide on the future of negotiations.”

News on the pandemic also added pessimism to markets. Germany’s latest measures have failed to contain the spread in Europe’s largest economy, while deaths in the U.S. surpassed 3,000 a day for the first time. The U.K.’s vaccination campaign hit a stumbling block after two people with allergies experienced reactions to the Pfizer shot.

The top highlight in Europe today is the ECB announcement, where as previewed, economists expect its 1.35 trillion-euro PEPP stimulus plan to be expanded by at least 500 billion euros and its duration extended by six months to the end of 2022, with

risks skewed towards even more. The bank will announce its policy decision at 1245 GMT, followed by ECB chief Christine Lagarde’s 1330 GMT news conference. Traders will be also listening to what she says about the euro’s near 14% rise since March.

“The critical element is that there has been an impact on (euro zone) growth recently,” said Shoqat Bunglawala, head of global portfolio solutions for EMEA & APAC at Goldman Sachs Asset Management, referring to the second wave of lockdowns. “So we would expect to see some further support.

“Central banks are likely to remain in ultra-accommodative mode,” UBS Chief Investment Officer Mark Haefele wrote in a note predicting the ECB would boost its bond-buying program. “As a result, the hunt for yield is unlikely to get easier anytime soon,” they said, recommending emerging-market sovereign bonds among other debt issues.

Earlier in the session, the MSCI Asia index eased 0.4%, with Japan’s Nikkei ending 0.2% lower. Both are up more than 60% from March lows. S&P Dow Jones Indices then said it would remove 10 Chinese companies from its equities indices and several others from its bond indices overnight. It followed a move by Donald Trump’s outgoing administration to ban U.S. investors from buying certain Chinese securities.

In rates, Treasuries were slightly higher across the curve, following bigger gains for gilts, which gathered pace after U.K. Prime Minister Johnson said a no-deal Brexit looks more likely. Treasury auction cycle concludes with 30-year bond reopening. Yields lower by ~2bp at long end of the curve, with spreads slightly flatter; 10-year at 0.918% is lower by 1.8bp vs 6.2bp drop for U.K. 10-year.Euro zone government bond yields also continued to fall. Italian 10-year yields fell to a record low at 0.53%. Spain and Portugal’s hit 0.013% and -0.022% respectively.

In FX, the pound sank further after a report that talks between the EU and the U.K. are on course to end without a trade deal, barring a dramatic last-minute intervention. The euro erased earlier gains just before the European Central Bank policy decision that’s expected to add 500 billion euros ($605 billion) to its emergency bond-buying program.

In commodities, faith in the recovery appeared to be holding up with Brent oil futures up 0.8% at $49.23 a barrel and U.S. crude was up 0.9% at $45.96 a barrel. Gold nursed losses at $1,839 an ounce. “We think the market has certainly got confidence in the sustainability of this recovery,” Goldman’s Bunglawala said. Iron ore futures jumped to more than $150 a ton, while crude oil rose.

Looking at the day ahead, and the aforementioned ECB meetings and the EU leaders’ summit will be the highlights. Otherwise, we also have the FDA meeting in the US where they’ll discuss an Emergency Use Authorization for the Pfizer/BioNTech vaccine. Data releases include UK GDP and French industrial production for October, while from the US there’s the CPI reading and the monthly budget statement for November, along with the weekly initial jobless claims.

Market Snapshot

- S&P 500 futures up 0.2% to 3,679.75

- STOXX Europe 600 up 0.03% to 395.01

- MXAP down 0.5% to 193.92

- MXAPJ down 0.4% to 642.29

- Nikkei down 0.2% to 26,756.24

- Topix down 0.2% to 1,776.21

- Hang Seng Index down 0.4% to 26,410.59

- Shanghai Composite up 0.04% to 3,373.28

- Sensex down 0.3% to 45,959.06

- Australia S&P/ASX 200 down 0.7% to 6,683.12

- Kospi down 0.3% to 2,746.46

- German 10Y yield fell 1.0 bps to -0.615%

- Euro up 0.2% to $1.2103

- Italian 10Y yield fell 0.8 bps to 0.471%

- Spanish 10Y yield fell 0.6 bps to 0.015%

- Brent futures up 0.9% to $49.29/bbl

- Gold spot down 0.5% to $1,830.75

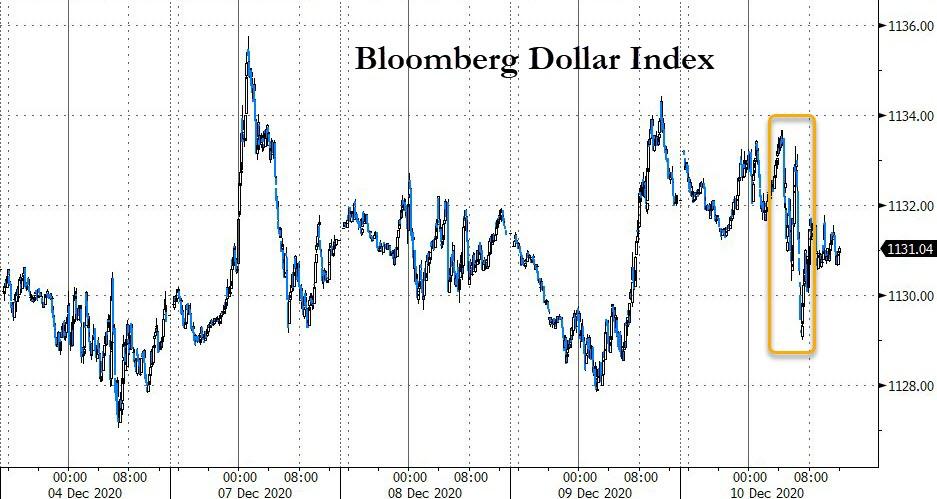

- U.S. Dollar Index down 0.1% to 90.99

Top Overnight News from BLoomberg

- Brexit negotiators have until Sunday to come up with a deal after talks over dinner between Prime Minister Boris Johnson and European Commission President Ursula von der Leyen ended without a breakthrough

- European Commission proposes contingency measures ensuring basic reciprocal air and road connectivity between the EU and the U.K., as well as allowing for the possibility of reciprocal fishing access by EU and U.K. vessels to each other’s waters after Dec. 31, according to statement

- China said it will sanction more U.S. officials and place new travel restrictions on American diplomats in retaliation for measures taken by the Trump administration over Hong Kong

- Switzerland’s foreign- exchange interventions to weaken the franc will be enough for the U.S. to qualify the country as a currency manipulator, though it has the option to hold back on the designation, according to people familiar with the matter

- In Europe, investors are starting to say their goodbyes to the bund market, worried that soon there may not be any place left for them as the the European Central Bank keps squeezing them out

- The investigation into Hunter Biden’s foreign business dealings has been underway since 2018, and involves not only the Justice Department but also the Internal Revenue Service, according to two people familiar with the matter who discussed the sensitive inquiry on condition of anonymity. The probe is focusing on Hunter Biden’s business dealings with China, as CNN reported earlier, and Joe Biden isn’t a target, according to a third person

- Steven Major, HSBC Holdings Plc’s global head of fixed-income research, has relocated to Hong Kong from London to boost the firm’s Asia business

- The U.K. economy grew just 0.4% in October, down from 1.1% in September, as new measures to control the pandemic kicked in, shuttering businesses in some areas and curbing household mixing in others

Asian equity markets were cautious amid headwinds from the soured mood on Wall St where the major indices pulled back from record levels amid frictions in US stimulus talks and lack of any breakthrough in Brexit negotiations across the pond, with the downturn led by hefty losses in the Nasdaq. ASX 200 (-0.7%) was pressured amid notable weakness in gold miners after recent losses in the precious metal and as tech stocks reflect the underperformance of their stateside peers, with the ongoing deterioration in Aussie-Sino ties also adding to the glum. This was after MOFCOM issued its ruling on anti-subsidies investigation on Australian wine imports and confirmed to collect anti-subsidy deposits from Friday, while Nikkei 225 (-0.2%) traded negative for most the session but with downside cushioned by favourable currency flows on Gotobi day and with SoftBank shares surging double digits which was attributed to paper profits from the DoorDash IPO. Hang Seng (-0.4%) and Shanghai Comp. (U/C) began subdued although the mainland bourse showed resilience and briefly recouped opening losses which also follows the recent jump in lending and financing data, while Hong Kong languished as its Chief Executive Lam faces a freeze-out from Japanese banks with US operations after Tokyo said it will abide by US sanctions. Finally, 10yr JGBs were higher on a rebound from support near 152.00 and following a similar mild recovery in T-notes with prices helped by the cautious tone in stocks, although gains were pared following mixed results and weaker demand at the 20yr JGB auction.

Top Asian News

- A $2.5 Billion Default Shows China Has no Mercy for Weak Firms

- SoftBank Soars on $11 Billion DoorDash Gain, Buyout Prospect

- Top Indian Hospital Chain Ready to Vaccinate 1 Million Daily

European equities (Eurostoxx 50 +0.3%) post mild gains ahead of today’s crunch ECB meeting with policymakers set to unveil another easing package, predominantly by expanding and extending its PEPP and adjusting its TLTRO offerings. Across the pond, US equity index futures have stabilised after yesterday’s tech-induced sell-off in the US which saw the Nasdaq close with losses of -1.9% (vs S&P -0.8%). That said, some of the hangover for IT names can be observed in Europe with the sector near the foot of the pile for the region, with Infineon and STMicroelectronics softer by 2% and 1% respectively. In the states, the US House has come together on passing the one-week stopgap funding measure to avoid a government shutdown and provide more time for discussions on government funding and pandemic relief, which the Senate plans to vote on today. Closer to home, last night’s meeting between UK PM Johnson and European Commission President von der Leyen has had little follow-through to equity markets. Sectoral performance in Europe is mixed with energy and consumer staples faring better than peers, whilst the aforementioned IT sector and beleaguered travel & leisure industry lag with the latter weighed on by Tui (-3.5%) after the Co. posted a EUR 3bln loss. As the session progresses and events in Frankfurt unfold, the banking sector may prove to be the one to watch. Corporate updates are once again on the light side with Ocado (-4.1%) one of the main standouts thus far to the downside despite raising its FY20 outlook with some desk highlighting moderating growth in Q3.

Top European News

- ECB Set to Pump More Cash Into Virus-Hit Economy: Decision Guide

- Russia to Conduct First Naval Drill with NATO Since 2012

- Hungary Exempts $2.3 Billion Bank Merger From Competition Probe

In FX, the Dollar sees another caged session in early European hours and in the run-up to the ECB policy decision (full preview available in the Newsquawk Research Suite), with the index constrained within a current intraday band at 90.973-91.136 ahead of yesterday’s 91.203 peak, Monday’s 91.241 high, the 21DMA (91.807) and the psychological 92.00 mark, whilst immediate downside levels consist yesterday and Monday’s lows at 90.688 and 90.612 respectively ahead of 90.500 and the YTD low at 90.471. Looking ahead to the session, several risk events are present for the Buck including ECB, COVID-relief talks at Capitol Hill, EUCO summit and the FDA EUA meeting (schedule available on the Newsquawk headline feed), whilst the data slate sees November CPI and the weekly IJCs.

GBP, EUR – Another subdued session for the Sterling in the aftermath of the meeting between UK PM Johnson and European Commission President Von der Leyen whereby the sides failed to narrow differences on outstanding issues but have given negotiators until Sunday to bridge the “very large gaps, with the two sides also intimating early morning that LPF remains the most contentious sticking point and the EU reportedly hardening its position on the matter according to Foreign Minister Raab. Cable has yielded its 1.3300 handle (vs. high 1.3412) after tripping reported stops just under its 21DMA (1.3318), to a current base matching Tuesday’s 1.3291 low ahead of Monday’s 1.3223 low. Elsewhere, EUR/USD trades on either side of 1.2100 in relatively contrained 1.2076-1.2108 range ahead of a risk-packed agenda with the ECB and EUCO meetings garnering full attention on both monetary and fiscal fronts. (full preview for both events can be found in the Newsquawk Research Suite). From a technical standpoint, support levels for the pair could include yesterday’s 1.2057 low ahead of 1.2050, the 1.2038 low set on 2nd Dec ahead of 1.2000 and below that the 21DMA at 1.1962. Upside levels consists of the psychological 1.2150, the YTD peak at 1.2177 ahead of 1.2200.

AUD, NZD, CAD – The non-US Dollars post gains to varying degrees, with the Aussie yet again propped as AUD/USD hover around YTD high and just under 0.7500, with NZD/USD also making headway above 0.7000 (0.7014-52 range), but with gains less pronounced vs. its Aussie counterpart as the AUD/NZD cross breached 1.0600 to the upside and resides towards the top of the current 1.0583-0631 range. The Loonie meanwhile meanders on either side of 1.2800 vs. the Buck (1.2791-2829 range) with the currency underpinned by firmer crude prices.

- JPY – Notwithstanding the cautious risk tone, the Yen trades on a softer footing as the pair briefly eclipsed 104.50 to the upside to a high of 104.57 (vs. low 104.21) with some player also citing Gotobi demand.

In commodities, WTI and Brent front-month futures eke modest gains in lockstep with price action seen across European equity future and with no fresh catalysts throughout the European morning ahead of a barrage of risk events including ECB, EUCO Summit, and state-side stimulus talks. Upside in WTI Jan picked up after breaching mild resistance at USD 46/bbl (vs. low 45.52/bbl) whilst Brent Feb makes headway above USD 49.50/bbl (vs. low USD 48.86/bbl). Elsewhere, spot gold and silver trade lacklustre with the former just above1830/oz (vs. high 1842/oz) and the latter south of USD 24/oz (vs. high 24.061/oz). In terms of base metals, Dalian iron ore futures continued to gain as the raw material continues to be propelled by Chinese demand coupled with Aussie-Sino woes, LME copper meanwhile tracks the modest gains seen in stocks.

US Event Calendar

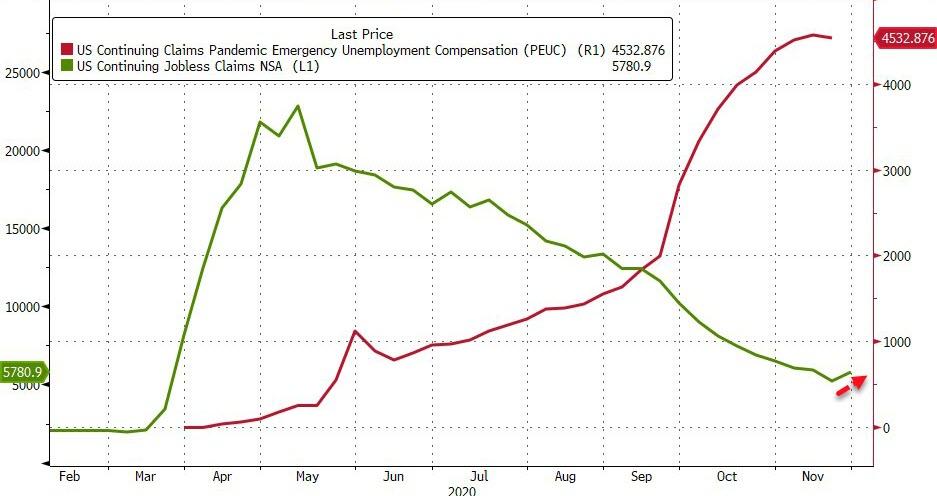

- 8:30am: Initial Jobless Claims, est. 725,000, prior 712,000; Continuing Claims, est. 5.21m, prior 5.52m

- 8:30am: US CPI MoM, est. 0.1%, prior 0.0%; US CPI Ex Food and Energy MoM, est. 0.1%, prior 0.0%

- 8:30am: US CPI YoY, est. 1.1%, prior 1.2%; US CPI Ex Food and Energy YoY, est. 1.51%, prior 1.6%

- 12pm: Household Change in Net Worth, prior $7.61t

- 2pm: Monthly Budget Statement, est. $199.0b deficit, prior $208.8b deficit

DB’s Jim Reid concludes the overnight wrap

Today marks the final ECB meeting of the year, where the Governing Council is widely expected to announce a recalibration of their monetary policy stance. In their preview (link here), our European economists say that they expect the core of this package to involve an extension of the PEPP net asset purchase period and the TLTRO3 discounted interest rate period beyond their current expiry in June 2021. Their baseline sees this being extended 6 months to the end of 2021, though they say that a longer 12-month extension to mid-2022 is a possibility. They also expect a €400bn increase in the PEPP envelope and other moves on TLTRO3, though not a deposit rate cut. The meeting comes against a difficult backdrop for the ECB, with the single currency area still in deflationary territory, and with the euro having appreciated further since their last gathering to move above $1.20.

With markets anticipating additional stimulus, there was a further narrowing in spreads between core and periphery yesterday, with yields on 10yr bunds (+0.2bps) and gilts (+0.4bps) rising, whereas both Italian (-0.8bps) and Spanish (-0.8bps) yields fell to all-time lows of 0.58% and 0.02% respectively. Will Spain soon follow Portugal into negative yield territory at the 10yr part of the curve?

However the performance of the tech sector in the US was the biggest story of the day. Following news that Facebook (-1.93%) has been sued by US antitrust officials and a coalition of states, and also headlines that Tesla (-6.99%) was dramatically “overvalued” from a research analyst, the NASDAQ fell -1.94% on the day. The Facebook suit seeks to break up the tech company by unwinding the acquisitions of Instagram and WhatsApp. This comes after the October anti-trust suit filed by the US Justice Department against Google, though this differs by explicitly pursuing breaking up of the company.

Risk assets actually started off with a strong performance yesterday but renewed concerns over the likelihood of a US stimulus package led to an initial reversal midway in the session, before the anti-trust news dominated the end of trading. Equity indices took a hit after Senate Majority leader McConnell’s comments that the Democrats were moving the goalposts, and had “poured cold water” on his proposal. By the end of trading, the S&P 500 had fallen from an all-time intraday high to shed -0.79%, while the Dow Jones (-0.35%) similarly moved lower. Earlier European equities continued their steady recent rise with the Stoxx 600 climbing +0.32%, led by autos (+1.27%) and Media (+1.14%), while technology stocks (-0.35%) were the index’s biggest laggard.

On the topic of corporate actions, our quant team has launched a survey taking the temperature on private equity intentions and investments for 2021. If you are an asset manager that looks into this market and can offer some insight please take a few minutes to help our colleagues out. Link here.

As noted above fiscal stimulus discussions took a step backward yesterday. There are just nine days, including today, left in the congressional session and there remains confusion as just which bill the sides are discussing – the bipartisan bill that originated in the Senate or Secretary Mnuchin’s bill that he debuted earlier this week. It appears now that any pandemic relief deal will end up attached to the government-spending bill. The current funding for federal agencies runs out this Friday night, and the House yesterday passed a new one week continuing resolution to avoid a government shutdown. US Treasuries were up +3.3bps midday even after the “cold water“ stimulus deal headlines, however the anti-trust news saw Treasuries rally when risk markets faltered and yields finished +1.8bps at 0.936%. 10yr breakevens closed at their highest (1.909%) since early May of 2019.

The other important discussion yesterday was on Brexit, where last night UK Prime Minister Johnson met with European Commission President von der Leyen. The two leaders have given negotiators until Sunday to reach an agreement. Following a face to face dinner, von der Leyen tweeted, “We understand each other’s positions…They remain far apart. The teams should immediately reconvene to try to resolve these issues.” The pound is down -0.23% to $1.3368 this morning.

The meeting with Johnson came ahead of today’s summit of EU leaders, and we heard yesterday from the Polish Deputy PM that a compromise had been agreed by Poland, Hungary and Germany on the ongoing budget standoff that saw Poland and Hungary veto the long-term budget and recovery fund over rules that would make the disbursement of funds conditional on adherence to rule-of-law requirements. The deal with Germany (who hold the rotating presidency) would need to be agreed with other EU leaders, but according to the Polish Deputy PM that could happen at the summit, which runs into tomorrow.

Asian markets are trading without a clear direction this morning with the Nikkei (+0.04%) and Kospi (+0.05%) flattish while the Hang Seng (-0.17%) and Asx (-0.67%) are down but the Shanghai Comp +0.24% is up. Futures on the S&P 500 are trading flattish while those on the Nasdaq are down -0.24%. Yields on 10y USTs are down -1.2bps to 0.925%. In commodities, DCE iron ore futures are up +4.62% this morning.

Looking ahead, today is an important one on the vaccine front, as the US FDA will be holding a meeting that will discuss the Emergency Use Authorization request for the Pfizer/BioNTech vaccine. They’ve already published a report indicating that it’s highly effective in preventing Covid-19, and a successful approval would follow similar moves in both the UK and Canada (yesterday). However, though the vaccine has begun to be distributed outside trials, rising caseloads throughout the world have led to further warnings that people needed to reduce their social contact over the coming weeks, not least with Christmas ahead. Indeed Chancellor Merkel said to the Bundestag that “we need to make one more effort” and encouraged people to limit their social contacts, while here in the UK, there were further reports that London could be placed under Tier 3 restrictions soon given the recent rise in cases, which would involve the closure of bars and restaurants except for takeaway. I’ve booked a night out with my wife next week on the day the new tiering comes out and my area is in danger of also moving into tier 3. Across the other side of Atlantic, the White House coronavirus task force has recommended to President Donald Trump that the US start allowing in travelers from Brazil, the UK and 27 other EU countries. Under recommendations, travel restrictions on travelers from China and Iran wouldn’t be relaxed. This comes as the US witnessed the deadliest day of the virus yet and reported 3,125 fatalities in the past 24 hours.

Finally, there wasn’t a great deal of data yesterday, but we did hear that the number of US job openings in October rose to a three-month high of 6.652m (vs. 6.3m expected). That said, this is ahead of the more recent spike in Covid cases that the US has seen. Elsewhere, the Bank of Canada announced they were keeping rates on hold, in line with expectations.

To the day ahead now, and the aforementioned ECB meetings and the EU leaders’ summit will be the highlights. Otherwise, we also have the FDA meeting in the US where they’ll discuss an Emergency Use Authorization for the Pfizer/BioNTech vaccine. Data releases include UK GDP and French industrial production for October, while from the US there’s the CPI reading and the monthly budget statement for November, along with the weekly initial jobless claims.

3A/ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 1.31 POINTS OR .04% //Hang Sang CLOSED DOWN 92.25 POINTS OR .35% /The Nikkei closed DOWN 61.70 POINTS OR 0.23%//Australia’s all ordinaires CLOSED DOWN 0.69%

/Chinese yuan (ONSHORE) closed DOWN AT 6.5435 /Oil UP TO 46.10 dollars per barrel for WTI and 49.45 for Brent. Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.5435. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.5365 TRADE TALKS STALL//YUAN LEVELS //TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS/PANDEMIC/TRUMP TESTS POSITIVE FOR COVID 19 : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

CHINA/USA

The “war” with China intensifies as they slap more sanctions on the uSA with travel restrictions on various USA officials. The feud over Hong Kong intensifies.

(zerohedge)

China Slaps Sanctions, Travel Restrictions On US Officials As Feud Over Hong Kong Intensifies

Considering all that has happened in the year since the first coronavirus cases were discovered, one might expect China and the CPC to be somewhat more contrite. But although President Xi has promised to dole out billions of doses of China-developed vaccines throughout the developed world, Beijing has rattled its rivals in the West by putting its foot down and pushing back against American efforts to curb China’s growing geopolitical rivals.

On Thursday, China warned that it would retaliate against the US by slapping new sanctions on American officials and place travel restrictions on diplomats, following the announcement of sanctions on 14 members of China’s NPC, the massive legislative body that functions as China’s “Congress” (it’s merely a rubber-stamp legislature, to be sure).

SCMP claimed these tit-for-tat restrictions are the result of President Trump trying to preserve his “tough on China”, and box VP Joe Biden into preserving the approach, something Biden has promised to do, at least, at first. Biden has even reportedly brought in Mayor Pete Buttigieg to handle the whole situation and maintain the tough stance.

However, last night, Hunter Biden revealed that he his facing a tax-fraud investigation tied to his business dealings in China, not exactly a vote of confidence in his father’s ability to remain objective.

China is aiming to sanction powerful Americans including lawmakers, NGO personnel and their families, Foreign Ministry spokeswoman Hua Chunying told a regular news briefing Thursday in Beijing.

The sanctions drama initially xploded in Beijing earlier this week when Chinese vice foreign minister Zheng Zeguang summoned a top US diplomat to the Forbidden City for a tongue-lashing over the Americans’ “barbaric actions” – a reference to sanctions imposed on more than a dozen top Chinese officials earlier in the week.

China added that the sanctions would only “strengthen its resolve” to crush Hong Kong’ democratic freedoms – Beijing’s primary goal in all of this.

While Trump’s rhetoric and actions certainly seem aggressive, Washington has been careful not to cross an important red line: Beijing has warned that it would never tolerate sanctions on members of China’s seven-member standing committee, otherwise known as the Politburo, which is the group of the 7 most powerful government officials in all of China

end

4/EUROPEAN AFFAIRS

As expected the ECB is boosting their QE b y 500 billion euros. The Euro rises on a lack of dovish surprises. This is good for gold as all nations are undergoing massive QE

(zerohedge)

ECB Boosts QE By €500BN, Euro Jumps On Lack Of Dovish Surprises

As previewed earlier, the ECB announced that in order to arrest Europe’s economic double dip, it will expand its PEPP (pandemic emergency purchase programme) QE by €500BN (as expected), will extend the duration of the PEPP through March 2022 (it was expected to end 2021); calibrates TLTRO further by adding three more operations in 2021 and extended it by 12 months.

Here are the highlights from what the ECB just did in its final meeting for 2020:

- Rates unchanged, expects rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2 per cent within its projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.

- Increases the envelope of the pandemic emergency purchase programme (PEPP) by €500 billion to a total of €1,850 billion.

- Extended the horizon for net purchases under the PEPP to at least the end of March 2022, and the Governing Council will conduct net purchases until it judges that the coronavirus crisis phase is over.

- Extends the reinvestment of principal payments from maturing securities purchased under the PEPP until at least the end of 2023.

- In any case, the future roll-off of the PEPP portfolio will be managed to avoid interference with the appropriate monetary policy stance.

- Further recalibrate the conditions of the third series of targeted longer-term refinancing operations (TLTRO III); extends the period over which considerably more favourable terms will apply by twelve months, to June 2022. Three additional operations will also be conducted between June and December 2021.

- Decided to raise the total amount that counterparties will be entitled to borrow in TLTRO III operations from 50 per cent to 55 per cent of their stock of eligible loans. In order to provide an incentive for banks to sustain the current level of bank lending, the recalibrated TLTRO III borrowing conditions will be made available only to banks that achieve a new lending performance target.

- To extend to June 2022 the duration of the set of collateral easing measures adopted by the Governing Council on 7 and 22 April 2020. The extension of these measures will continue to ensure that banks can make full use of the Eurosystem’s liquidity operations, most notably the recalibrated TLTROs.

- The Governing Council will reassess the collateral easing measures before June 2022, ensuring that Eurosystem counterparties’ participation in TLTRO III operations is not adversely affected.

- Decided to offer four additional pandemic emergency longer-term refinancing operations (PELTROs) in 2021, which will continue to provide an effective liquidity backstop.

In response to the announcement of yet another massive liquidity injection – which was in line with expectation- the EURUSD actually jumped, as most of what Lagarde unveiled was already priced in, on the lack of additional dovish surprises, and amid concerns that the ECB is running out of ammo to truly stimulate the economy.

The full statement is below:

In view of the economic fallout from the resurgence of the pandemic, today the Governing Council recalibrated its monetary policy instruments as follows:

First, the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00 per cent, 0.25 per cent and -0.50 per cent respectively. The Governing Council expects the key ECB interest rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2 per cent within its projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.

Second, the Governing Council decided to increase the envelope of the pandemic emergency purchase programme (PEPP) by €500 billion to a total of €1,850 billion. It also extended the horizon for net purchases under the PEPP to at least the end of March 2022. In any case, the Governing Council will conduct net purchases until it judges that the coronavirus crisis phase is over.

The Governing Council also decided to extend the reinvestment of principal payments from maturing securities purchased under the PEPP until at least the end of 2023. In any case, the future roll-off of the PEPP portfolio will be managed to avoid interference with the appropriate monetary policy stance.

Third, the Governing Council decided to further recalibrate the conditions of the third series of targeted longer-term refinancing operations (TLTRO III). Specifically, it decided to extend the period over which considerably more favourable terms will apply by twelve months, to June 2022. Three additional operations will also be conducted between June and December 2021. Moreover, the Governing Council decided to raise the total amount that counterparties will be entitled to borrow in TLTRO III operations from 50 per cent to 55 per cent of their stock of eligible loans. In order to provide an incentive for banks to sustain the current level of bank lending, the recalibrated TLTRO III borrowing conditions will be made available only to banks that achieve a new lending performance target.

Fourth, the Governing Council decided to extend to June 2022 the duration of the set of collateral easing measures adopted by the Governing Council on 7 and 22 April 2020. The extension of these measures will continue to ensure that banks can make full use of the Eurosystem’s liquidity operations, most notably the recalibrated TLTROs. The Governing Council will reassess the collateral easing measures before June 2022, ensuring that Eurosystem counterparties’ participation in TLTRO III operations is not adversely affected.

Fifth, the Governing Council also decided to offer four additional pandemic emergency longer-term refinancing operations (PELTROs) in 2021, which will continue to provide an effective liquidity backstop.

Sixth, net purchases under the asset purchase programme (APP) will continue at a monthly pace of €20 billion. The Governing Council continues to expect monthly net asset purchases under the APP to run for as long as necessary to reinforce the accommodative impact of its policy rates, and to end shortly before it starts raising the key ECB interest rates.

The Governing Council also intends to continue reinvesting, in full, the principal payments from maturing securities purchased under the APP for an extended period of time past the date when it starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

Seventh, the Eurosystem repo facility for central banks (EUREP) and all temporary swap and repo lines with non-euro area central banks will be extended until March 2022.

Finally, the Governing Council decided to continue conducting its regular lending operations as fixed rate tender procedures with full allotment at the prevailing conditions for as long as necessary.

Separate press releases with further details of the measures taken by the Governing Council will be published this afternoon at 15:30 CET.

The monetary policy measures taken today will contribute to preserving favourable financing conditions over the pandemic period, thereby supporting the flow of credit to all sectors of the economy, underpinning economic activity and safeguarding medium-term price stability. At the same time, uncertainty remains high, including with regard to the dynamics of the pandemic and the timing of vaccine roll-outs. We will also continue to monitor developments in the exchange rate with regard to their possible implications for the medium-term inflation outlook. The Governing Council therefore continues to stand ready to adjust all of its instruments, as appropriate, to ensure that inflation moves towards its aim in a sustained manner, in line with its commitment to symmetry.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today.

Lagarde’s final press conference for the year will be at 830am. Watch it live here.

end

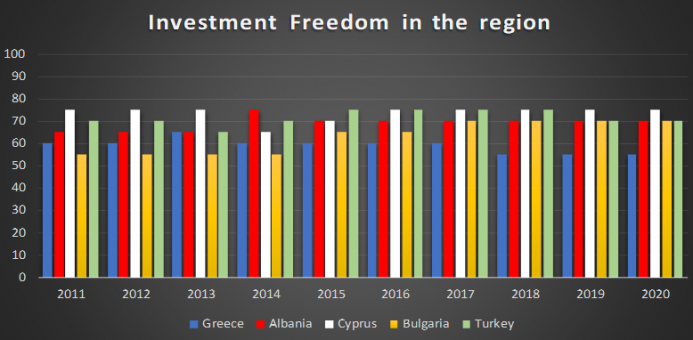

GREECE

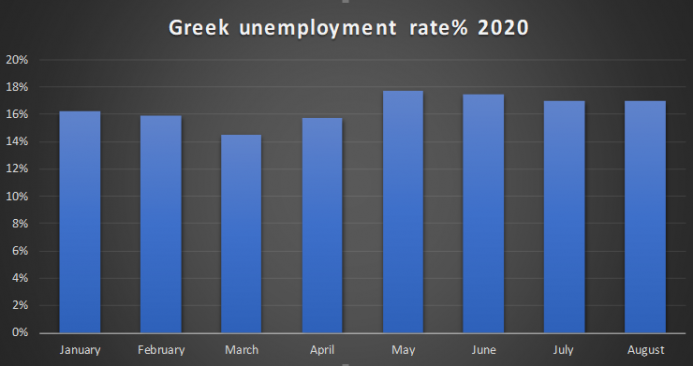

Big trouble for Greece as the shutdowns in the country caused its Debt to to GDP approach 200 %

The lockdowns are hurting the country as well as the lack of tourism. Generally tourism for Greece is 20% of their GDP. Trouble ahead..

(Gatestone)

Greece Is Setting Itself Up For Another Financial Crisis

Authored by Antonis Giannakopoulos via The Mises Institute,

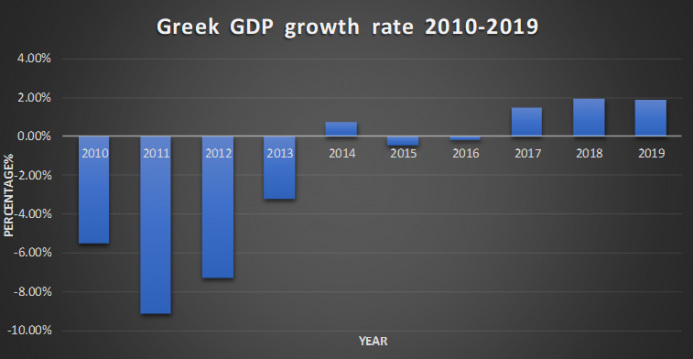

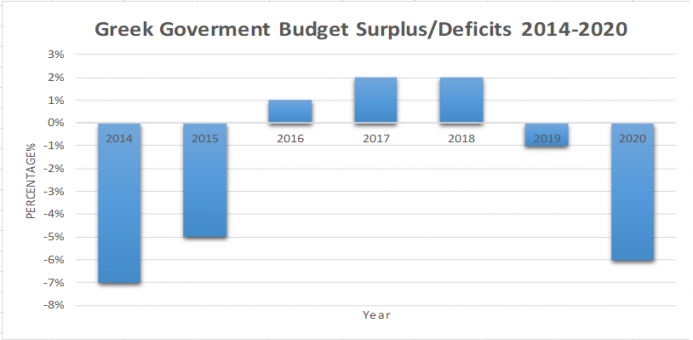

The Greek economy shrunk by a record 14 percent in the second quarter of 2020 while at the same time government efforts to ‘’cure’’ the economy have set the country on the road to cross the 200 percent debt-to-GDP ratioas the IMF forecasts. In the meantime, government budget deficits have reached new heights (around 7 percent).

The Government’s Response to the Recession

The Greek government tried to combat the economic downturn with a loose fiscal and monetary policy (through the European Central Bank). The initial aim was to support pretty much everyone from the public and private sector for the bad months of the covid-19 lockdown and hope for economic recovery when the summer arrived, with the tourist industry saving the day. It soon became evident, however, that this was wishful thinking. People from the tourist industry admitted that it could take years for the industry to recover its past numbers. The situation looked even worse once people realized how dependent the whole economy is on tourism: it accounts for 20 percent of GDP and provides 22 percent of all employment in Greece. Furthermore, the Greek government’s solutions, like those of most of the other governments in Europe, were primarily demand-side policies.

As I predicted in one of my past articles, these measures could only provide short-run relief, only postponing the pain until later. The unemployment rate saw a 1.2 percent increase from March to April, of 1.3 percent from April to May, and it saw a minor decrease during the summer tourist period. The Organisation for Economic Co-operation and Development (OECD) has estimated that the unemployment rate will reach roughly 20 percent by the end of the year.

Source: Trading Economics.

In the meantime, that the GDP saw a 14 percent contraction in the second quarter means that the Greek economy will need years to reach its precorona numbers, especially considering its anemic growth rate over the last decade.

Source: International Monetary Fund, World Economic Outlook: The Great Lockdown (Washington, DC: International Monetary Fund, April 2020).

What Went Wrong?

The ECB’s balance sheet had a massive increase from 39 percent of the GDP to 54 percent during the summer. In comparison the Fed’s balance sheet is around 32 percent of GDP. The injections of liquidity via the ECB have effectively zombified a considerable number of companies in the EU, with corporate debts reaching new highs. In the case of Greece, the government has exploited its new, EU-sanctioned fiscal leeway, which has allowed it to perpetuate structural problems in its economy along with large deficits. During the tourist season, the costs were so high that a considerable segment of the tourist industry decided to not even work this summer since they would lose less money this way.

Government intervention made things even worse by failing to address the biggest problem in the economy, which is its inflexible labor laws. Rather than partially liberalizing the laws, the state made them even more restrictive and inflexible. For this reason, businessmen have failed to adjust to the corona crisis shock. Making hiring more expensive and riskier is a recipe for disaster, especially in a fragile economy that lacks savings and investments like Greece. While the spending didn’t manage to stimulate the economy, we can’t say that it had an immediate negative effect short term at least, since it was mostly financed by the European Union. On the other hand, cheap credit and loans were made possible by the ECB and by putting political pressure on banks, thus prolonging another major structural problem of the overall economy: lack of savings and more debt. The budget deficits are also a matter that needs to be addressed, since it has reached new highs, making the 2010s a lost decade for the whole economy, since the whole point of ‘’European austerity’’ was to make the debt more sustainable.

Source: Trading Economics

As the Greek minister of finance admitted the tax cuts that were made during the last few months won’t be permanent, since the new target is for Greece to have the biggest fall in debt-to-GDP in the eurozone. The state secretary of finance also talked recently about a possible new austerity program similar to that of the previous decade. On the surface, budget surpluses are a good thing and much needed, but it is important to ask these surpluses will become a reality. The tax cuts won’t be permanent, so it seems that Greeks will soon be undertaking the same failed strategy that they tried for a decade and was promoted by European officials in Brussels—high tax rates to increase government revenues but very minimal cuts in public expenditures. But the problem wasn’t the tax cuts but government spending and deficits. Deficits have a greater crowding-out effect on the private sector than just spending. At the end of the day, these deficits will have to be paid by future generations. Potential tax increases in the future would be an even bigger disaster for the private sector. The cure is worse than the disease.

The center-right government that came into power in July of 2019 has failed to liberalize the economy and make market-oriented reforms, and the pandemic has made things even worse. It hasn’t made any major tax cuts that would be permanent and could have a big impact on alleviating some of the pressure on the private sector. Deregulation was also a major issue: the Greek economy was and still is in desperate need of foreign investment; however, investment freedom hasn’t seen a significant increase, and major investments and infrastructure programs are way behind schedule. Bureaucratic obstacles extend even to the judiciary branch, making it inefficient and slow, with corruption widespread.

Source: Heritage Foundation, Index of Economic Freedom, 2020.

The Heritage Foundation’s Index of Economic Freedom can give us some useful insight on state economic freedom in Greece.

The following graph compares investment freedom in Greece with countries that compete for investment in the same region.

Source: Heritage Foundation, Index of Economic Freedom, 2020.

Conclusion

People need to understand that when you have an economy with weak productivity that’s highly indebted,shutting down the economy two times in one year has repercussions that will be here to stay for years depending on the recovery policies. The economy needs major structural reforms. Labor laws need to be liberalized. Budget surpluses are indeed the correct goal, especially now, to avoid another debt crisis, but the surpluses need to come from cuts made in the public sector. Tax cuts need to become permanent and even bigger for the economy to grow and expand. Last but not least, making foreign and domestic investments easier, less expensive, and minimizing the potential risk is a matter of utmost urgency, since Greece is being outcompeted by neighboring countries.

Greece needs to take advantage of its potential. A business-friendly environment with a liberalized market is the way to go. It can minimize the negative effects of the corona crisis and solidify a slow but strong recovery that will make the country more productive and give it prospects of getting out economic trouble and becoming an economic powerhouse in the region.

end

Bill Blain on the failure of the UK to make a deal with Europe

(Bill Blain)

Blain: It’s Clear That UK And Europe Remain Miles Apart

Authored by Bill Blain via MorningPorridge.com,

After hearing the disappointing news from Brussels – a dinner where nothing really moved forward, except a splutter-saving agreement to stretch out the talking till Sunday – it looks like a no-deal Brexit exit is on the cards. The blocks to a deal were put in position the moment Boris took No 10 and grandly promised the UK the best deal ever with his faux-Trumpian bluster.

It’s clear the UK and Yoorp remain miles apart. (21 miles from Dover.)

You can paint it as Europe punishing the UK for the temerity of abandoning the project, Europe being defensive to demonstrate to waverers how leaving the EU is impossible, the UK’s foolishness for leaving, or for the UK being silly for not agreeing to give up its fish and leave its sovereignty with Brussels. Or, it might be the reasons the UK are leaving are most obvious in our likely rejection of Europe’s demands.

My immediate thought was to panic buy. I was thinking of running to the shops this morning to buy a big wheel of Brie, a couple of cases of Champagne, and all the other stuff we all love about Yoorp.. and then I thought about it. Who cares if there are suddenly shortages of Yoorpean stuff.

Nope. Don’t care

I’ve bought my Christmas sparkler – a couple of cases of the excellent Black Dog, crafted just off the South Downs on the slopes of Ditchling Beacon by my chum Jim Nolan. (Seriously it’s a cracking sparkling wine, knocks the expensive UK wines and top champagnes out..) Cheese this Christmas will all be British, including Isle of Wight Blue – it really is excellent. In fact, my big worry is can I get some Gallybagger? It will be sad to be without a toasted camembert, but Welsh Rarebit is some much better.

And from next year.. Well I guess we will all be become pescatarians… because the UK is going to have an awful lot of fish. I know some Scots and Devon fishermen and can guarantee they won’t be happy.. there will be so much fish they’ll be giving it away for nothing! (Yes, we will find an accommodation to let the Dutch, Spanish and Danes have access to our fish, but any French boat a milli-inch over on our side will be sunk with prejudice!)

Sure, we might have to build a couple of gunboats to protect our maritime borders – but that will create jobs!, Heaven help you if your French car breaks down – your fault for buying it in first place.

The bottom line is if the UK exits without a sane and logical trade deal than would have benefited everyone, it’s not the end of the world. Dashed awkward though. Messy, but just means we will have to try even harder to recover from the ravages of Covid and the stupidity of Boris.

Whenever you think it may overwhelm you, remember: Things are never as good as we hope, but never as bad as we fear.

I am pretty sure the UK and Yoorp have reached the end of what could have have been a constructive negotiation where the UK would have got back our impression of sovereignty and retained Europe as our closest trading partner. We would have been outside the EU, but within Europe. Everyone would have been nice and happy.The UK decided to leave Europe for (somewhat misguided and badly informed) reasons of sovereignty and pride. Yoorp wants to keep us tied to their rules – and I can understand exactly why when face with what they’ve seen in Westminster. We Brits are not perfect – and it’s now time we learn that the hard way. Neither side has room left to compromise. So let’s just get on with it.

And if we get to tar and feather Boris Johnson for not delivering another promise… what’s to worry about..?

end

UK/EU

Emergency plans are being placed in order to prevent economic chaos (most probably)should Brexit talks fail.

(zerohedge)

UK, EU Impose Emergency Plans To Prevent Economic Chaos Should Brexit Talks Fail

As we await the next round of last-minute talks involving Boris Johnson and European Commission head Ursula von der Leyen, markets are expressing an as-yet-unseen level of anxiety.

Looking at the GBPUSD futures curve, it looks like investors are finally pricing in near-term risk that the UK will crash out of the EU without a deal.

European Commission proposes contingency measures ensuring basic reciprocal air and road connectivity between the EU and the U.K., as well as allowing for the possibility of reciprocal fishing access by EU and U.K. vessels to each other’s waters after Dec. 31, according to statement.

Now, it looks like both Brussels and London are battening down the hatches, as the chances of a deal wane. The EU is threatening to revoke various safety certificates for products that could create serious disruptions in trade as the UK retaliates as well.

It all started weeks ago when Brussels said it might not allow reciprocity for UK financial services – trading, clearing etc. – a move that Europe hopes would help force London to return to the table.

As BoJo ventures back to the Continent for last minute negotiations, Brussels has published emergency plans to keep planes flying, trucks moving and prevent other chaos in the event that trade talks fail. HMG and Brussels have warned osignificant uncertainty” over the fate of the Brexit negotiations.

The Commission adopted the proposals on Thursday, ensuring that Britain falling over the Brexit cliff won’t disrupt air travel between their normal routes between the EU and UK and that hauliers could continue to cross the English Channel after Britain leaves the single market on January 1.

“While the commission will continue to do its utmost to reach a mutually beneficial agreement with the UK, there is now significant uncertainty whether a deal will be in place on 1 January 2021,” a EU executive said in a statement.

Many feared that publishing these contingency plans could weaken the EU’s negotiating position, but Brussels insisted that it was doing the bare minimum required to prevent a serious economic disruption that would weaken both the UK and the EU European citizens and businesses. The aim, it said, was to “provide a transitory solution, while negotiations on a future partnership continue, and not look to mitigate the negative impacts of Brexit in a sustained manner”.

The UK has also imposed its own “reciprocal” measures that the EU will need to accept t

These measures mostly deal with areas where there is no “international fallback solution” to prevent chaos should Britain crash out of the single-market/customs union without any kind of contingency plan in place to prevent the inevitable chaos that night ensue. For example, failure to put in place a stopgap system for road hauliers “would create unmanageable disruptions and pose a serious threat to EU interests.” This could be particularly problematic as the UK scrambles to compensate for its conspicuously high death toll by getting a jump on vaccinations.

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

A must read.. Iran vs Europe

Iran sends a warning to Europe!

(Gatestone/Kemp)

Terrorism: A Warning From Iran To Europe

Authored by Richard Kemp via The Gatestone Institute,

Last month the trial began in Belgium of Assadolah Assadi and three other Iranians accused of planning a bomb attack in Paris in 2018. Since 2015 Assadi had been the most senior officer of Iran’s Ministry of Intelligence and Security in Europe, at the time operating under diplomatic cover at the Iranian embassy in Vienna. He is the first Iranian government official to be tried by an EU country for terrorist offences, despite numerous attack attempts on EU soil ordered by Tehran.

State supported terrorism is not just an act in itself but also an instrument of national power and coercion. Together, these plots were a malevolent message and clear threat to Europe that unfortunately have been received and acted upon as intended in London, Berlin, Paris and Brussels.

Assadi’s failed plot was reportedly ordered by Iranian President Hassan Rouhani and approved by Supreme Leader Ali Khamenei. His target was a rally for the National Council of Resistance of Iran, with 80,000 supporters present and attended by former Canadian Prime Minister Stephen Harper, President Trump’s lawyer Rudy Giuliani and several British and European members of parliament. The explosives, allegedly brought into Europe from Iran by Assadi on a commercial flight, were TATP, the same type as was used to kill 22 and wound 800 in a jihadist attack at the Manchester Arena, UK, in 2017 and the London 7/7 bombings that killed 52 and wounded 700 in 2005. The message was clear. In March Assadi, who has refused to attend his own trial claiming diplomatic immunity, threatened retaliation if he is convicted. The Iranian government has also warned of a “proportionate response” against countries involved in the trial.

Assadi’s bombing was prevented by European security authorities using intelligence provided by Israel. Mossad previously passed intelligence to the British security agency MI5 that enabled them to disrupt another Iranian-directed bomb plot in 2015. Terrorists linked to the Iranian proxy Hizballah had stockpiled three metric tons of ammonium nitrate in North London — the same explosive material that caused such devastation in Beirut earlier this year. The quantity in London was greater than the ammonium nitrate that killed 168 people, injured 680 and damaged hundreds of buildings in the 1995 Oklahoma City bombings.

The same year as the London attempt, another Hizballah bomb plot was uncovered in Cyprus, also an EU member, this time involving 8.2 metric tons of ammonium nitrate, and again revealed to Cypriot authorities by Mossad. There had also been an attempt in Thailand in 2012 and, two years after the London plot was uncovered, indications of a similar plan in New York. The same year as the Thailand plot, Hizballah murdered five Israeli tourists and a driver when they bombed a bus at Burgas in Bulgaria, another EU member state.

Iranian-organized terrorist attack plans were uncovered in Germany in 2017 and Denmark in 2018, both EU members, and also in 2018 in Albania, a formal candidate for accession to the EU. Two Dutch citizens of Iranian origin were assassinated in the Netherlands, another EU state, on orders from Tehran in 2015 and 2017.