GOLD; UP $8.65 to $1827.65

SILVER: $23.15 UP 38 CENTS

ACCESS MARKET: GOLD: 1827.05..

SILVER: $23.19

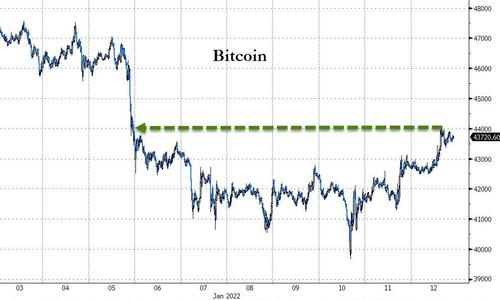

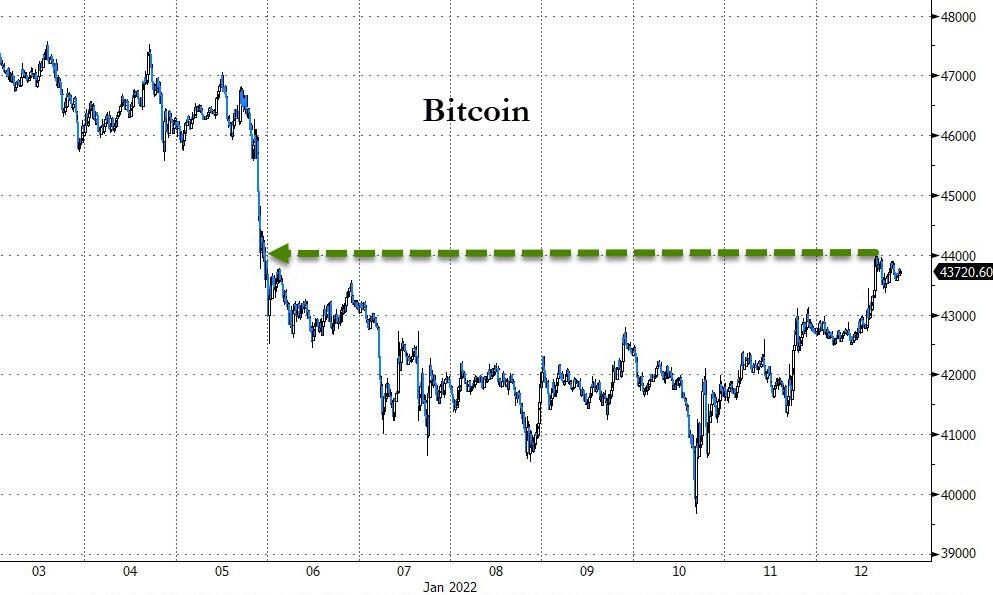

Bitcoin: morning price: 43,050 up 142

Bitcoin: afternoon price: 43,721 up $813

Platinum price: closing up $7.80 to $982.90

Palladium price; closing down $8.90 at $1915.55

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filed 122/863

DLV615-T CME CLEARING

BUSINESS DATE: 01/11/2022 DAILY DELIVERY NOTICES RUN DATE: 01/11/2022

PRODUCT GROUP: METALS RUN TIME: 20:26:54

CONTRACT: JANUARY 2022 PLATINUM FUTURES NYMEX

SETTLEMENT: 973.800000000 USD

INTENT DATE: 01/11/2022 DELIVERY DATE: 01/13/2022

FIRM ORG FIRM NAME ISSUED STOPPED

190 H BMO CAPITAL 18

332 H STANDARD CHARTE 18

357 C WEDBUSH 1

555 C BNP PARIBAS SEC 54

624 H BOFA SECURITIES 85

661 C JP MORGAN 500 223

686 C STONEX FINANCIA 39

730 C PTG DIVISION SG 46

732 H RBC CAP MARKETS 101

905 C ADM 8 3

TOTAL: 548 548

MONTH TO DATE: 2,731

NUMBER OF NOTICES FILED TODAY FOR JAN. CONTRACT: 863 NOTICE(S) FOR 86,300 OZ (2.6892 TONNES)

total notices so far: 2384 contracts for 238400 oz (7.4152 tonnes)

SILVER NOTICES:

185 NOTICE(S) FILED TODAY FOR 925,000 OZ/

total number of notices filed so far this month 2336 : for 11,680,000 oz

GLD

WITH GOLD UP $8.65

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

CLOSING INVENTORY: 976.21 TONNES/

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 38 CENTS:/:

NO CHANGES IN SILVER INVENTORY:

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY SLV/ TONIGHT: 530.612 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A VERY STRONG 1925 CONTRACTS TO 144,421 AND RESTS CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020…... WITH THE $0.33 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.33) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A HUGE GAIN OF 2384 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 10.505 MILLION OZ FOLLOWED BY TODAY’S 500,000 OZ QUEUE JUMP V) VERY STRONG SIZED COMEX OI GAIN.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS -29

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTACTS for 8 days, total contracts: : 4619 contracts or 23.095 million oz OR 5.75 MILLION OZ PER DAY. (577 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 4619 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 23.095 MILLION OZ

.

LAST 8 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

RESULT: WE HAD A VERY STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1925 WITH OUR 33 CENT GAIN SILVER PRICING AT THE COMEX// TUESDAY THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 430 CONTRACTS( 430 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY:/ AS WELL AS TODAY /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN OF 10.505 MILLION OZ FOLLOWED BY TODAY’S 500,000 QUEUE JUMP//NEW STANDING 13.620, MILLION OZ// .. WE HAD A HUGE SIZED GAIN OF 2356 OI CONTRACTS ON THE TWO EXCHANGES FOR 11.920 MILLION OZ//

WE HAD 185 NOTICES FILED TODAY FOR 925,000 OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A HUMONGOUS SIZED 20,294 TO 546,516, AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -3303 CONTRACTS

.

THE HUGE SIZED INCREASE IN COMEX OI CAME DESPITE OUR STRONG GAIN IN PRICE OF $19.25//COMEX GOLD TRADING/TUESDAY/.AS IN SILVER WE MUST HAVE HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION AS THE TOTAL GAIN ON OUR TWO EXCHANGES TOTALLED AN ATMOSPHERIC SIZED 21,925 CONTRACTS…

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JAN AT 3.5614 TONNES FOLLOWED BY TODAY’S 72,800 OZ QUEUE. JUMP//NEW STANDING: 7.608 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $19.25 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A GIGANTIC SIZED GAIN OF 21,925 OI CONTRACTS (68.195 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALLED A SMALL SIZED 1631 CONTRACTS:

FOR FEB 1631 ALL OTHER MONTHS ZERO//TOTAL: 1631

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 546,516.

IN ESSENCE WE HAVE A HUGE SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 21,925, WITH 20,294 CONTRACTS INCREASED AT THE COMEX AND 1631 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 25,228 CONTRACTS OR 78.469TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1631) ACCOMPANYING THE GIGANTIC SIZED GAIN IN COMEX OI (20,294): TOTAL GAIN IN THE TWO EXCHANGES 21,925 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR JAN. AT 3.7262 TONNES//FOLLOWED BY TODAY’S 72,800 OZ QUEUE. JUMP.//NEW STANDING 7.608 TONNES 3)ZERO LONG LIQUIDATION,4) GIGANTIC SIZED COMEX OI. GAIN 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB.WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2021 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN : 23,026 CONTRACTS OR 2,302,600 oz OR 71.62 TONNES (8 TRADING DAY(S) AND THUS AVERAGING: 2878 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES: 66/55 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 71.62/3550 x 100% TONNES 2.01% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO DATE

JANUARY: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//INITIAL ISSUANCE//

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A VERY STRONG SIZED 125 CONTRACTS TO 144,442 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 430 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 430 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 430 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 125 CONTRACTS AND ADD TO THE 430 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 2356 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 11.775 MILLION OZ,

OCCURRED WITH OUR $0.33 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING TUESDAY NIGHT

SHANGHAI CLOSED UP 29.99 PTS OR 0.84% //Hang Sang CLOSED UP 663.11 PTS OR 2.79% /The Nikkei closed UP 543,18 PTS OR 1 .92% //Australia’s all ordinaires CLOSED UP .67% /Chinese yuan (ONSHORE) closed UP 6.3656 /Oil UP TO 81.52 dollars per barrel for WTI and UP TO 83.85 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3656. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3717: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING STRONGER AGAINST USA DOLLAR

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY AN ATMOSPHERIC SIZED 20,294 CONTRACTS AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX INCREASE OCCURRED WITH OUR GAIN OF $19.25 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A SMALL EFP (1631 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. LOOKS LIKE OUR BANKERS ARE FINALLY BAILING OUT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE NON ACTIVE DELIVERY MONTH OF JAN.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1531 EFP CONTRACTS WERE ISSUED: ;: , DEC : 0 & FEB. 1531 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1531 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUMONGOUS SIZED 21,925 TOTAL CONTRACTS IN THAT 1631 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GIGANTIC SIZED COMEX OI GAIN OF 20,294 CONTRACTS..

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR JAN (7.605),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $19.25)

AND THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS THE TOTAL GAIN ON THE TWO EXCHANGES REGISTERED 78.469 TONNES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JAN (7.605 TONNES)…

WE HAD – XXX CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 25,228 CONTRACTS OR 2,522,800 OZ OR 78.469 TONNES

Estimated gold volume today: 235,270 poor///

Confirmed volume yesterday: 240,356 contracts poor

INITIAL STANDINGS FOR JAN ’22 COMEX GOLD

JAN 12

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | nil oz |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 863 notice(s)86300 OZ2.6892 TONNES |

| No of oz to be served (notices) | 61 contracts 6100 oz 0..1899 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2384 notices 238,400 OZ7.4152 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

No dealer deposit 0

No dealer withdrawal 0

0 customer deposit

0 customer withdrawal

i

ADJUSTMENTS: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of JANUARY we have an oi of 924 stand for JANUARY GAINING 381 contracts. We had 346 notices filed on TUESDAY, so we GAINED A WHOPPING 727 contracts or an additional 72,700 oz will stand for

gold in this very non active delivery month of January

FEBRUARY LOST 6661 CONTRACTS TO 298,626

March added 117 contracts to stand at 2358..

We had 863 notice(s) filed today for 86,300 oz FOR THE JAN 2022 CONTRACT MONTH

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 139 notices were issued from their client or customer account. The total of all issuance by all participants equates to 863 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 122 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN /2021. contract month,

we take the total number of notices filed so far for the month (2384) x 100 oz , to which we add the difference between the open interest for the front month of (JAN: 924 CONTRACTS ) minus the number of notices served upon today 863 x 100 oz per contract equals 244,500 OZ OR 7.608 TONNES the number of TONNES standing in this NON active month of JAN. (numbers corrected from yesterday)

thus the INITIAL standings for gold for the JAN contract month:

No of notices filed so far (2384) x 100 oz+ (924) OI for the front month minus the number of notices served upon today (863} x 100 oz} which equals 244,500 oz standing OR 7.605 TONNES in this NON active delivery month of JAN.

We GAINED 728 contracts or an additional 72,800 oz of gold will not stand for metal on this side of the pond.

TOTAL COMEX GOLD STANDING: 7.608 TONNES (VERY STRONG FOR A JANUARY DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

206,468.649, oz NOW PLEDGED /HSBC 6.42 TONNES

174,041.813 PLEDGED MANFRA 5.41 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690

288,481,604, oz JPM No 2 8.97 TONNES

698,821.330 oz pledged June 12/2020 Brinks/27,96 TONNES

12,244.444 oz International Delaware: 0..3808 tonne

Loomis: 18,615.429 oz

total pledged gold: 1,653,017.372oz 51.42 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 33,636,248.801 OZ (1046.22 TONNES)

TOTAL ELIGIBLE GOLD: 16,027,355.260 OZ (498.51 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,608,893.542 OZ (547.71 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,955,876.0 OZ (REG GOLD- PLEDGED GOLD) 496.29 tonnes

END

JANUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//JAN 12

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 660,123.239 oz DelawareCNTManfra |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 24,567.467 ozDelaware |

| No of oz served today (contracts) | 185 CONTRACT(S)925,000 OZ) |

| No of oz to be served (notices) | 388 contracts (1,940,000 oz) |

| Total monthly oz silver served (contracts) | 2336 contracts 11,680,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We had 1 deposit

i) into Delaware: 24,567.467 oz

JPMorgan has a total silver weight: 184.635 million oz/353.068 million =52.29% of comex

ii) Comex withdrawals: 3

a) out of Delaware: 1001.70 oz

b) out of Manfra: 613m592.339 oz

total withdrawal 660,123.239 oz

we had 0 adjustments

the silver comex is in stress!

TOTAL REGISTERED SILVER: 81.331 MILLION OZ

TOTAL REG + ELIG. 353.068 MILLION OZ

TOTAL NO OF CONTRACTS SERVED UPON THIS MONTH: 1980 CONTRACTS FOR 45,095,000 OZ

CALCULATION OF SILVER OZ STANDING FOR DECEMBER

NUMBER OF NOTICES FILED TODAY: 185 NOTICES OR 925,000 OZ

silver open interest data:

FRONT MONTH OF JAN//2022 OI: 573 CONTRACTS LOSING 71 contracts on the day

We had 171 notices filed for TUESDAY so we GAINED 100 contracts or 500,000 additional oz will stand for delivery in this non active delivery month of January.

FOR FEB WE HAD A GAIN OF 28 CONTRACTS UP TO 725

FOR MARCH WE HAD A GAIN OF 738 CONTRACTS UP TO 114,378 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 185 for 925,000 oz

Comex volumes: 57,685 poor// est. volume today

Comex volume: confirmed YESTERDAY: 53,934 contracts (poor)

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 2336 x 5,000 oz =. 11,680,000 oz

to which we add the difference between the open interest for the front month of JAN (573) and the number of notices served upon today 185 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JAN./2021 contract month: 2336 (notices served so far) x 5000 oz + OI for front month of JAN (573) – number of notices served upon today (185) x 5000 oz of silver standing for the JAN contract month equates 13,620,000 oz. .

We GAINED 100 contracts or an additional 500,000 oz will stand for delivery on this side of the pond.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

GLD

JAN 12/WITH GOLD UP $8.65//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 11/WITH GOLD UP $19.25/A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FROM THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 10/WITH GOLD UP $2.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.08 TONNES

JAN 7/WITH GOLD UP $8.15//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWLA OF 1.16 TONNES FROM THE GLD////INVENTORY RESTS AT 978.83 TONNES

JAN 6/WITH GOLD DOWN $35.30//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .32 TONNES/INVENTORY RESTS AT 979.99 TONNES

JAN 5/WITH GOLD UP $10.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 980.31 TONNES

Jan 4/WITH GOLD UP $14.00//A HUGE CHANGE OF 4.65 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 980.31 TONNES

JAN 3/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 31/WITH GOLD UP $14.05 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 30/WITH GOLD UP $7.75 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 29/WITH GOLD DOWN $5.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 975.66 TONNES

DEC 28/WITH GOLD UP $2.00 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 973.63 TONNES

DEC 27/WITH GOLD DOWN $2.05: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.63 TONNES.

DEC 23/WITH GOLD UP $9.85 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.94 TONNES FROM THE GLD/// INVENTORY RESTS AT 973.63 TONNES

DEC 22/WITH GOLD UP $12.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 21/WITH GOLD DOWN $7.05 TODAY, NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 20/WITH GOLD DOWN $9.65 TODAY; A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.37 TONNES INTO THE GLD///INVENTORY RESTS AT 977.20 TONNES

DEC 17/WITH GOLD UP $7.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.20 TONNES

DEC 16/WITH GOLD UP $33.05TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.4 TONNES FROM THE GLD////INVENTORY REST AT: 977.20 TONNES

DEC15/WITH GOLD DOWN $7.80 TODAY/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.04 TONNES FROM THE GLD////INVENTORY RESTS AT 980.60 TONNES.

DEC 14/WITH GOLD DOWN $18.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64 TONNES

DEC 13/WITH GOLD UP $3.20 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 982.64 TONNES

DEC 10.WITH GOLD UP $7.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64 TONNES

DEC 9/WITH GOLD DOWN $9.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64.

DEC 8/WITH GOLD UP $5.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 984.38 TONNES

DEC 7/WITH GOLD UP $5.15 TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 984.38 TONNES

DEC 6/WITH GOLD DOWN $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 986.17 TONNES//

CLOSING INVENTORY: 976.21 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SLV.

JAN 12/WITH SILVER UP 38 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//

JAN 11/WITH SILVER UP 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ/.

JAN 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 7/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 6/WITH SILVER DOWN 94 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL PF 226,000 OZ FROM THE SLV///INVENTORY RESTS AT 530.612 MILLION OZ?/

JAN 5/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 4/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 3/WITH SILVER DOWN 45 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.219 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 530.838 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC30/WITH SILVER UP 14 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.624 MILLILON OZ FROM THE SLV.//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 29/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ/

DEC 28/WITH SILVER UP 9 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.682 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 27/WITH SILVER UP 6 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681

DEC 23/WITH SILVER UP 19 CENTS TODAY:A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 22/WITH SILVER UP 29 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 538.883 MILLION OZ/

DEC 21/WITH SILVER UP 19 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.728 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 540.085 MILLION OZ

DEC 20/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 538.282 MILLION OZ

DEC 17/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 538.282 MILLION OZ//

DEC 16/WITH SILVER UP 91 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.33 MILLION OZ FROM THE SLV//INVENTORY REST AT 538.282 MILLION OZ

DEC 15WITH SILVER DOWN 38 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 2.48 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 541.612 MILLION OZ

DEC 14/WITH SILVER DOWN 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.092 MILLION OZ

DEC 13/WITH SILVER UP 11 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 3.561 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 543.092 MILLION OZ//

DEC 10.WITH SILVER UP 19 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 546.653 MILLION OZ..

DEC 9/WITH SILVER DOWN 43 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 2.96 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 546.653 MILLION OZ/

DEC 8/WITH SILVER DOWN 7 CENTS TODAY; NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.693 MILLION OZ///

DEC 7/WITH SILVER UP 24 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.693 MILLION OZ..

DEC 6/WITH SILVER DOWN 25 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.110 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 543.693 MILLION OZ//

CLOSING INVENTORY: 530.612 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

PETER SCHIFF

Peter Schiff: The Real Reason Gold Hasn’t Gone Up And Why It Ultimately Will

WEDNESDAY, JAN 12, 2022 – 12:06 PM

Authored by Peter Schiff via SchiffGold.com,

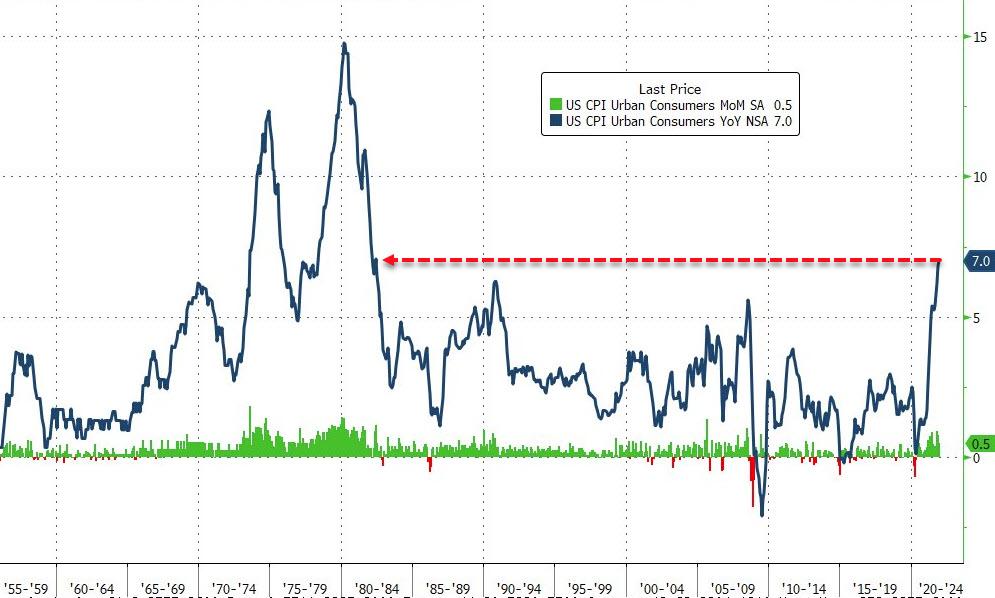

Inflation in the US is at historically high levels.

So, why hasn’t gold taken off?

We hear this question over and over again. In this video, Peter Schiff answers this question and explains why the markets will eventually wake up to their misperception.

That’s the key word – misperception.

Taper tantrums and fear of Fed rate hikes have distorted perception in the markets. People are selling gold when they should be buying gold on the dips.

And at the root of this misperception is the market’s focus on nominal interest rates instead of real interest rates.

The Federal Reserve now plans to raise interest rates three, possibly four, times in the next year. The conventional wisdom is that these rate hikes are bearish for the price of gold. This is why every time we got hotter than expected inflation news last year, the price of gold fell. Everybody assumed the central bank would speed up the pace of these rate hikes.

Gold has been rangebound around $1,800 for months. Peter pointed out that the fact gold hasn’t really gone down despite this universally held belief that monetary tightening is negative for gold is a positive sign.

But it’s key to understand that not only are these projected rate hikes not negative for gold – they are actually going to be a positive.

The Missing Puzzle Piece – Real Interest Rates

Why do investors assume rate hikes are bad for gold?

Generally speaking, rising interest rates increase the opportunity cost of holding gold.

Gold does not generate a yield. If interest rates rise and you’re holding gold, you’re forgoing the interest income you could earn on dollars if you put them in a bank account or invest them in bonds. That’s why rising interest rates tend to create headwinds for gold. And it’s why we’ve seen gold sell off on high inflation news. The markets expect the Fed to fight inflation with rate hikes, thus raising the opportunity cost of holding gold.

Rates have been at zero for a long time. That means there has been no opportunity cost to own gold. The Fed’s artificially low interest rates have been supportive of gold. The fear (and misperception) is if the Fed removes those supports by raising rates, gold will crash.

Peter says that’s not going to happen.

The key is understanding the difference between nominal interest rates and real interest rates.

When you’re talking about an opportunity cost, the interest rate has to be real. And by real, I mean above the rate of inflation.”

Even based on the government’s flawed CPI, inflation rose by about 7% in 2021.

Even if the Fed follows through with all of the rate hikes that it’s projecting, it’s talking about slowly raising interest rates in one-quarter point increments until, at the end of this year, they’re at 1%. And they’ll continue the process in 2023 until at the end of 2023, we’re at 2%. And supposedly, the 2% rate of interest represents a huge headwind for gold because it’s an opportunity cost, and a lot of people that are in gold are not going to want to be in gold when they can get a 2% yield on their cash.”

Peter said the whole idea is absurd.

If you accept a 7% inflation, even though the actual rate of inflation is probably 15% if the government measured it accurately, that means the dollar is losing 7% of its purchasing power every year. In exchange for that, you’re going to be able to earn 2% in interest to offset the 7% you’re losing to inflation. You are still -5%.

Negative 5% is not an opportunity cost. Nobody wants the opportunity to lose 5%. So, if you’re giving up a 5% loss, you’ve given up nothing.”

In order for there to be an opportunity cost, you have to have an interest rate above the rate of inflation. If the Fed raised rates to 10%, that might be a problem for gold. With an inflation rate of 7%, you would be giving up 3% in real interest that you could otherwise earn.

But if they’re just talking about raising rates to 2%, that’s nothing! I’m going to stay in gold to avoid a 5% loss. The opportunity cost is not owning gold. It’s owning US dollars and losing 5%. What the Fed is doing is too little too late to derail the gold bull market.”

In fact, Peter said he thinks the Fed will initiate the next leg up for gold when the markets wake up to this reality.

The Inflation Fight the Fed Can’t Win

Right now, everybody is fixated on the Fed’s fight against inflation. They assume that the central bank is going to win. So, why own gold?

At some point, the markets will realize that these incremental, tiny rate hikes are not nearly enough to stop inflation. The Fed is way behind the curve, and inflation is rising much faster than the Fed is talking about hiking. In fact, the Fed isn’t really talking about tight monetary policy at all. The Fed is talking about slightly less loose monetary policy. Less loose isn’t tight.

What the Fed is talking about doing is reducing the amount of gasoline that is pouring on the inflation fire. That still means the fire is going to get bigger. Even if it gets bigger more slowly, it’s still going to get bigger.”

But Peter said he thinks it may get bigger even faster.

When the markets realize these rate hikes aren’t doing any good, and that inflation is getting worse, that’s another reason to buy gold.”

And while the rate hikes won’t be big enough to tame inflation, they may well be big enough to prick the bubble economy.

When you develop an addiction to a certain amount of monetary heroin, even if you get monetary heroin, but you get a smaller dose, it’s not enough for your habit. And I think that’s going to happen in the markets.”

Ultimately, it will bleed into the economy and drive it into recession. That means we’ll not only have inflation but stagflation.

In the face of that, the Fed is ultimately going to do an about-face. It’s going to start cutting interest rates again and restarting the QE program even though the inflation problem has gotten worse.”

When that happens, gold is going to go ballistic.

But between now and then, take advantage of the misperception in the market that these rate hikes, if they actually come, are bearish for gold. That’s keeping a temporary lid on the price of gold. Eventually, reality is going to blow that lid off. But in the meantime, buy yourself some gold. In fact, maybe even better, buy some silver as well.”

This sale is not going to go on forever.

When you get a gift horse, don’t look it in the mouth. Just take advantage of it.”

end

LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,James RICKARDS

END

Important gold commentaries courtesy of GATA/Chris Powell

Craig Hemke discusses his forecast for gold/silver for 2022

(CraigHemke/GATA)

Craig Hemke’s gold and silver forecast for 2022

Submitted by admin on Tue, 2022-01-11 21:04 Section: Daily Dispatches

9p ET Tuesday, January 11, 2022

Dear Friend of GATA and Gold:

The TF Metals Report’s Craig Hemke, writing tonight at Sprott Money, gives his gold and silver forecast for the new year and details the reasons for it. Monetary metals investors won’t be too disappointed. The report is headlined “Reality Bites: A Forecast for Precious Metals in 2022” and it’s posted at Sprott Money here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Perfectly correct: the dollar’s once solid link to bond yields is breaking down. Also the dollar vs gold

(BloombergNews/GATA)

Dollar’s once-solid link to bond yields is breaking down

Submitted by admin on Tue, 2022-01-11 15:37 Section: Daily Dispatches

By Vassilis Karamanis and Payne Lubbers

Bloomberg News

Tuesday, January 11, 2022

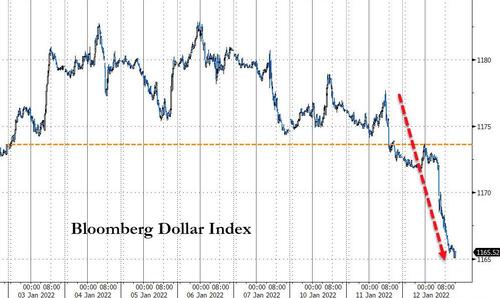

The dollar is starting to decouple from the Treasury yields that it tracked so closely last year, adding to signs that the bulk of the currency’s windfall from higher rates has already passed.

Two-year U.S. yields surpassed 0.94% on Tuesday, hitting levels last seen before the pandemic, as money markets moved toward pricing in four rate increases from the Federal Reserve this year. Yet the Bloomberg Dollar Spot Index has failed to budge much above a six-week low seen at the end of 2021.

The contrast affirms investor views that while the greenback has scope to climb this year, it has already benefited substantially from traders who started front-running a hawkish Fed in the last few months of 2021, taking the Bloomberg dollar index to an annual gain of close to 5%, its biggest since 2015. Once the U.S. central bank raises borrowing costs and rolls bonds off its balance sheet, the dollar’s gains are widely expected to moderate into the second half of 2022.

Part of the reason for the subdued move in the dollar is that traders are front-loading hikes for other central banks, which diminishes the dollar’s relative advantage on the rates side, according to Valentin Marinov, head of G-10 FX strategy at Credit Agricole. …

… For the remainder of the report:

END

OTHER GOLD STORIES

END

OTHER COMMODITIES/BEEF

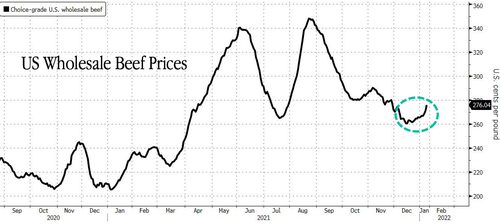

Beef Prices Jump As Omicron Spread Sickens Meat Plant Workers

TUESDAY, JAN 11, 2022 – 08:25 PM

The COVID-19 Omicron variant’s spread among U.S. meatpacker workers is threatening beef output and raising prices, according to Bloomberg.

New data from the U.S. Department of Agriculture shows beef output last week dropped 5.3% YoY, and wholesale prices jumped 1.3% on Monday, the most significant increase since August.

Rising meat prices have been the Biden administration’s core focus as food inflation is a big concern for working poor Americans. Biden’s polling data is near an all-time low as inflation wipes out wage gains.

The administration has blamed the meat industry for price-gouging. Still, it appears they have very little knowledge or are unable to or unwilling to admit problems actually driving inflation in the industry, which is related to labor issues.

“The beef market is finding some strength because you’re having trouble with absentee workers,” Don Roose, president of U.S. Commodities Inc. in West Des Moines, Iowa, told Bloomberg by phone.

Recently absenteeism at processing, packaging, and distribution of meat plants has recorded around 8%, up from 4-5%, said Mark Lauritsen, vice president of meatpacking at the United Food and Commercial Workers Union, representing thousands of plants employees.

“Meat plants don’t tend to be as bad as the general population,” Lauritsen said, adding that many meat workers are fully vaccinated and kept absenteeism relatively low.

However, the spread of the highly contagious omicron virus variant that can infect fully vaccinated people has begun to sicken workers from meatpacking plants to supermarkets. It is producing supply problems in the new year.

Cargill Inc., a top U.S. meatpacker, said it was experiencing a rise in infections at its plants, though all the plants are still operating.

Other food makers, such as Conagra Brands Inc. and Campbell Soup Co., are seeing upticks in absenteeism among workers due to COVID.

Meanwhile, Americans begin to panic as many have taken to social media to voice their concerns about food shortages at supermarkets.

This all means that food inflation will remain elevated through 2022 despite Biden’s attempt to squash it ahead of midterms.

END

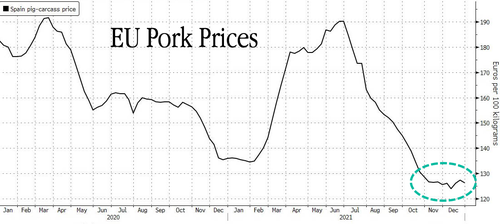

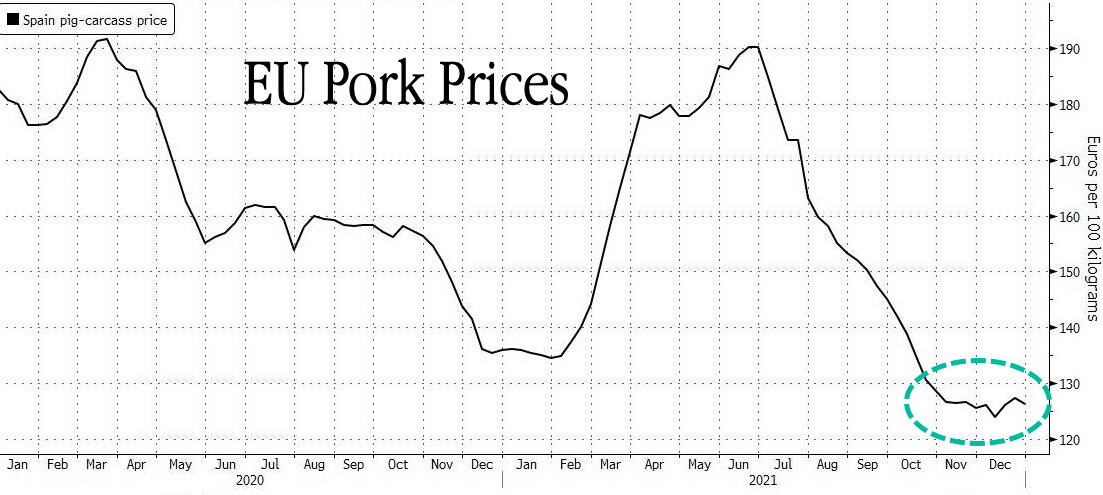

PORK

Is Europe heading for another pig ebola outbreak which will cause pork prices to skyrocket

(zerohedge)

Is A Pig Ebola Outbreak Imminent In Europe?

WEDNESDAY, JAN 12, 2022 – 04:15 AM

The highly transmissible and fatal disease for pigs, known as African swine fever (ASF), continues to spread throughout Europe. Leading some to believe the next major outbreak could be nearing and may result in soaring pork prices.

Bloomberg reports the latest case has been reported in a wild boar in Italy. It’s the first reported case in the country since the virus was first detected in Western Europe in 2018.

ASF doesn’t present a risk to humans but is devastating for pig herds. Italy is the seventh-largest pork producer in the European Union, with about 9 million pigs.

Italy’s national reference centre confirmed the ASF case was detected in the northern Italian region Piedmont. The department said crisis units were being set up to control the spread.

“We are acting with the utmost timeliness, the immediate and coordinated implementation of control measures in wild suids (pigs) is essential in an attempt to confine and eradicate the disease as much as possible,” said Piedmont’s health deputy, Luigi Icardi.

ASF appears to be spreading closer and closer to Spain and France, two of the European Union’s top pork suppliers. Germany has been battling ASF for more than a year as China has already placed an import ban from there.

A possible outbreak in Europe comes as the continent faces a supply glut of pork that has sent prices to a multi-year low.

“ASF is not only a German problem or a Polish problem or an Italian problem, it’s a European problem,” said Miguel Angel Higuera Pascual, director of Spanish pig-farmers association Anprogapor.

“The disease is moving. It’s a nightmare to think about how we can control the movement of wild animals,” Pascual said.

What’s also concerning is the ASF strain found in the wild bore in Italy matches the one that spread around Europe in 2007.

Justin Sherrard, a global animal protein strategist at Rabobank International, said the latest outbreak is a “further warning shot across the bow.” It could result in the culling of herds that would send pork prices soaring, adding to food inflation woes

end

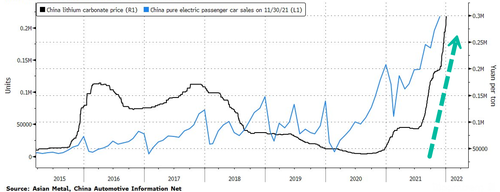

NICKEL

And now nickel is rising in price>>>

(zerohedge)

Green Revolution Sends Nickel Prices To Seven-Year High

WEDNESDAY, JAN 12, 2022 – 05:45 AM

Prices of rare earth metals used for battery making have soared in recent days as the parabolic growth in the electrification of vehicles forces automakers to lock in supplies.

Nickle, one of the key components in lithium-ion batteries, hit a seven-year high on Tuesday, rising as much as 3.4% to $21,500 a ton on the news that Tesla signed a nickel supply deal with Talon Metals Corp’s Tamarack mine project in Minnesota.

Notice how nickel trading on the London Metal Exchange marches higher as stockpiles continue to slump on increasing demand due to accelerated electric car production.

On Monday, lithium prices hit a new record high. Lithium carbonate trading in China was about 300,000 yuan (just over $47k per ton), an increase of about six times from January 2021. Soaring prices come as electric-car makers, such as Tesla, report exponential growth in the US, Europe, and China.

Lithium, nickel, and cobalt are the essential elements in battery technology powering electric vehicles that steadily replace combustion engines.

Michael Widmer, head of metals research at Bank of America, told Bloomberg, “we have so many stories all pointing in the same direction,” indicating that “people do realize that there is potentially a tightness in supply going on, and that is taking nickel prices ultimately higher.”

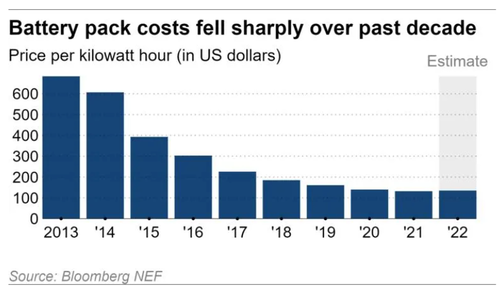

Even though prices for rare earth metals are increasing, the overall battery pack costs remain relatively inexpensive compared with a decade or so ago – however, 2022 will be the first year in years that battery pack prices will slightly increase.

A very different type of commodity supercycle could be playing out, driven by a green revolution, not China’s industrial economy.

.

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.3656

OFFSHORE YUAN: 6.3717

HANG SANG CLOSED UP 663.11 PTS OR 2.79%

2. Nikkei closed UP 543,18 PTS OR 1.92%

3. Europe stocks ALL GREEN

USA dollar INDEX DOWN TO 96/61/Euro RISES TO 1.1361-

3b Japan 10 YR bond yield: FALLS TO. +.129/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 115.43/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 81.52 and Brent: 83.85-

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE CLOSED UP// OFF- SHORE UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO -.0.043%/Italian 10 Yr bond yield FALLS to 1.29% /SPAIN 10 YR BOND YIELD FALLS TO 0.63%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.33: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 1.55

3k Gold at $1818.85 silver at: 22.82 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble; Russian rouble UP 6/100 in roubles/dollar AT 74.92

3m oil into the 81 dollar handle for WTI and 83 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 115.43 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9224– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0484 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 1.746 UP 1 BASIS PTS

USA 30 YR BOND YIELD: 2.076 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.81

Futures Slightly Green Ahead Of Today’s “Brutal” CPI Print

WEDNESDAY, JAN 12, 2022 – 08:00 AM

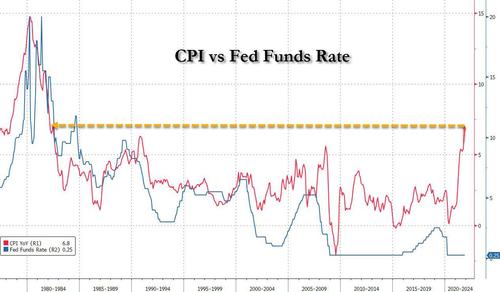

U.S. index futures were little changed, if slightly in the green on Wednesday as investors settled into a wait-and-see mode ahead of today’s “brutal” CPI report which is expected to show the highest CPI print in nearly 40 years, a time when the fed funds rate was 11% compared to 0% now…

… and gauge the pace of Federal Reserve tightening. Consensus expects December CPI to show inflation climbing to 7.0%, a result which could see front- end fully price in a March rate hike (currently priced at 85%). Helping the overnight mood in Asia, was a moderation in China’s inflation pressures, with CPI dipping to 10.3% y/y in December, giving the central bank scope to cut interest rates to cushion the economy’s downturn just as most major nations look to tighten policy. At 730am ET, S&P futures were up 0.2% of 7.50, and Nasdaq futures rose 22 points or 0.14%, recovering toward Asia’s best levels; Dow futures were up about 0.1%. The dollar was slightly lower, extending on its recent sharp drop, while Treasury yields were steady.

“All we know is that the Fed has waited too long before taking action,” said Ipek Ozkardeskaya, senior analyst at Swissquote. “If today’s inflation print is higher than expected, recent gains in equities will melt like snow in the sun,” she wrote, even though investors seemed to put aside fears that tighter policy will stifle the economic rebound and market rally after soothing words from Federal Reserve Chair Jerome Powell. His testimony Tuesday helped arrest a five-day slide in the S&P 500, just as we predicted it would.https://platform.twitter.com/embed/Tweet.html?dnt=false&embedId=twitter-widget-0&features=eyJ0ZndfZXhwZXJpbWVudHNfY29va2llX2V4cGlyYXRpb24iOnsiYnVja2V0IjoxMjA5NjAwLCJ2ZXJzaW9uIjpudWxsfSwidGZ3X2hvcml6b25fdHdlZXRfZW1iZWRfOTU1NSI6eyJidWNrZXQiOiJodGUiLCJ2ZXJzaW9uIjpudWxsfSwidGZ3X3NwYWNlX2NhcmQiOnsiYnVja2V0Ijoib2ZmIiwidmVyc2lvbiI6bnVsbH19&frame=false&hideCard=false&hideThread=false&id=1480907130441981954&lang=en&origin=https%3A%2F%2Fwww.zerohedge.com%2Fmarkets%2Ffutures-swing-ahead-todays-brutal-cpi-print&partner=tweetdeck&sessionId=6d1c6c4828f1eebe944382445d49f0eba7181602&siteScreenName=zerohedge&theme=light&widgetsVersion=86e9194f%3A1641882287124&width=550px

As Deutsche writes, the highlight of the last 24 hours was Chair Powell’s renomination hearing before the Senate Banking Committee. The overall communicated stance of policy wasn’t much changed with the hawkish pivot still on. Nevertheless, there were a few incremental takeaways. Powell did nothing to push back on liftoff being on the table in March, in line with our US econ team’s call and the increasing probability implied by the market, which is currently 85%. He made it clear that QE (yes it’s still happening) would finish in March, despite speculations it may come to an abrupt halt beforehand. In line with growing consensus, he painted a picture that made the start of QT likely in 2022. Finally, on the overall stance of policy, he emphasized the Fed needs to pull back from extreme levels of accommodation, but didn’t need to rush to get to a neutral stance of policy.

“It was a masterful performance really, leaving the bowls neither too full nor too shallow, but just right from the financial market’s perspective,” said Jeffrey Halley, senior market analyst at Oanda Asia Pacific, in an email. “The music can still play in equity markets in 2022, it’s just that we’ve likely seen the best of the technology gains.”

With three and possibly four Fed rate increases now priced in, strategists are turning more sanguine about inflation and focusing on positives such as the start of the earnings season. Markets have been buffeted by volatility at the start of the year on the prospect of faster interest-rate increases to subdue price pressures.

“Hawkish Fed repricing is likely largely done for now,” and “resilient earnings should help equities rebound,” Barclays Plc strategists led by Emmanuel Cau wrote in a note to clients on Wednesday.

Looking at the CPI print, DB’s Jim Reid notes that repeated upside surprises in the inflation data have sent the year-on-year numbers up to multi-decade highs, putting significant pressure on the Fed. Indeed if you look at the monthly headline CPI reading, 7 of the last 9 releases have come in above the consensus estimate on Bloomberg. In terms of what to expect this time around, economists think that year-on-year CPI will rise to +7.0%, which will be the highest annual CPI number since 1982. And if that figure is realized, it would also mean that the real Fed Funds rate in December was around -7%, which for reference is lower than at any point in the 1970s, when the lowest the fed funds rate got in real terms was around -5%.

In the premarket, Dish Network Corp. rose more than 7% on a New York Post report of merger talks with DirecTV. PayPal shares dropped 1.9% in premarket trading after Jefferies cut its recommendation for the digital payments provider to hold from buy. Here are some of the biggest U.S. movers today:

- U.S.-listed Chinese stocks rally in premarket trading, as Asian listings rebound amid bargain hunting and a reassuring tone from Fed Chair Jerome Powell. Alibaba (BABA US) +2.4%, JD.com (JD US) +1.5%, Pinduoduo (PDD US) +3.3%

- Biogen (BIIB US) drops 9.1% in premarket trading after the U.S. government limited Medicare coverage of the company’s Aduhelm Alzheimer’s disease treatment and similar drugs to patients enrolled in clinical trials. The highly unusual move will curb access to the controversial treatment approved last year

- Wells Fargo (WFC US) advanced in premarket trading as Piper Sandler upgraded its rating to overweight from neutral; cuts Premier Financial to neutral from overweight

- Bed Bath & Beyond (BBBY US) shares jump as much as 4.9% in U.S. premarket trading, boosted by disclosures of insider purchases of the retailer’s stock made on Jan. 7

- Rocket Lab USA (RKLB US) started at overweight, with $17 target by Morgan Stanley, which says the company offers high-quality exposure to the space race. Stock gains 4.1% in premarket trading

- Cogent Communications (CCOI US) faces a “challenging setup” on weak growth and a high multiple, Wells Fargo writes in note as downgrades to underweight from equal-weight

European equities climbed back toward opening highs after a choppy first hour of cash trading. The Euro Stoxx 50 added 0.7%, FTSE 100 outperforms at the margin. Miners, oil & gas and tech are the strongest performing sectors. In Europe, mining and technology companies led the Stoxx 600 Index up 0.5%. Philips slumped 14%, the most in two decades, after the Dutch producer of medical equipment reported lower preliminary revenue than expected. Here are some of the biggest European movers today:

- Rexel jumps to an eight-year high after the French maker of electrical products said 2021 organic growth will be higher than forecast with Citi noting positive demand comments from firm.

- VAT shares post their steepest gains in more than a month after the Swiss supplier of products for the semiconductor industry reported 4Q order intake that was well above expectations.

- DFS Furniture shares gain as much as 6.4%, among the top advancers in the FTSE All-Share Index, after the U.K. retailer kept its FY pretax profit forecast unchanged.

- Just Eat Takeaway stock rises after initially falling following an update. Citi analysts say the online food delivery firm’s 4Q results are broadly in line with an expected deceleration.

- TeamViewer shares rise as much as 15% in Frankfurt after the company reported 4Q and FY billings that beat market expectations with RBC calling the results “reassuring.”

- Sainsbury shares rise as much as 3.9% after the U.K. grocer boosted its outlook for the year. Profit delivery is strong, according to Jefferies.

- BHP Group and European mining peers are among the biggest gainers Wednesday with UBS saying in a sector note that shares are cheap — but valuations are not compelling.

- Sweco shares fall as much as 6.8% after Danske Bank downgrades to hold from buy, noting “stalling execution” despite solid market demand for the engineering consultancy’s services.

- Taylor Wimpey shares drop as much as 2.2% after a holder sold about 86m shares in the company at 163.75p apiece, representing a 3.7% discount to Tuesday’s close.

Earlier in the session, Asian stocks climbed to their highest level in almost seven weeks as Federal Reserve Chair Jerome Powell’s remarks spurred expectations that anticipated rate hikes won’t derail the global economic recovery. The MSCI Pacific Index added as much as 1.6% to its highest since Nov. 26, bolstered by gains in the consumer-discretionary and information-technology sectors. Alibaba Group and Tencent Holdings were among the biggest contributors to the measure’s rise. Benchmarks in Hong Kong and Japan led gains for the region. Powell pledged to do what’s necessary to contain an inflation surge and prolong the economic expansion at his confirmation hearing for a second term as U.S. central bank chief. Futures on the S&P 500 advanced in Asia trading after halting a five-day slide. A gauge of Chinese technology shares rallied after the Nasdaq 100 outperformed major benchmarks. “The market view is that containing inflation with early rate hikes will turn out to be good for the economy — that we’ll be able to push back on inflation while keeping the economy strong,” said Naoki Fujiwara, chief fund manager at Shinkin Asset Management in Tokyo. “Before, the market had been reacting simply to the words ‘monetary tightening’.” Asia’s equity benchmark is attempting a rebound following last year’s 3.4% slump, when the gauge was hit by concerns over U.S. tightening, Covid-19 and a selloff in Chinese tech shares. Solid gains during Wednesday’s session will likely help spread a sense of relief, according to Fujiwara. “We think there’s more attractiveness here in Asia and EMs overall. And valuations are much more compelling given overall EM/Asia markets have underperformed compared to U.S. and Europe,” Ken Wong, Asian equity fund specialist at Eastspring Investments, told Bloomberg Television. “In 2022, there will be opportunities to be selective.”

Japanese equities posted their first gain in four sessions, following a similar rebound in U.S. peers after soothing comments from Federal Reserve Chair Jerome Powell. Electronics makers and telecoms were the biggest boosts to the Topix, which closed 1.6% higher. Tokyo Electron and SoftBank Group were the largest contributors to a 1.9% rise in the Nikkei 225. Powell pledged to do what’s necessary to contain an inflation surge and prolong the expansion, while steering clear of fresh details on the path of U.S. monetary policy. The S&P 500 rose for the first time in six sessions. “The market view is that containing inflation with early rate hikes will turn out to be good for the economy – that we’ll be able to push back on inflation while keeping the economy strong,” said Naoki Fujiwara, chief fund manager at Shinkin Asset Management in Tokyo. “Before, the market had been reacting simply to the words ‘monetary tightening’.”

Indian stocks rose along with Asian peers after Federal Reserve Chair Jerome Powell reassured investors that the U.S. central bank will tackle inflation to extend the economic expansion. The S&P BSE Sensex climbed for a fourth day, up 0.9% to 61,150.04 in Mumbai. The benchmark is 1% away from surpassing its record high touched in October. The NSE Nifty 50 Index advanced by a similar magnitude. Reliance Industries Ltd. rose 2.7% and was among the biggest boosts to the key indexes. Of the 30 shares on the Sensex, 24 gained. All but two of the 19 sector indexes compiled by BSE Ltd. rose, led by a gauge of telecom companies. IT major Wipro Ltd. reported net income for the third quarter that missed the average analyst estimate. Tata Consultancy Services Ltd. and Infosys Ltd. are also scheduled to announce Oct.-Dec. earnings in the day

Australian stocks also rebounded as mining shares hit 5-month highs. The S&P/ASX 200 index rose 0.7% to 7,438.90, with miners and health-care contributing the most to the benchmark’s gain. The materials subgauge led the rebound, hitting the highest since Aug. 17. Afterpay surged after the company said that Block, formerly known as Square, has now received approval from the Bank of Spain in respect of the acquisition by Lanai AU 2 Pty Ltd. Domino’s Pizza Enterprises dropped to its lowest since May. Official data Wednesday showed job vacancies climbed to a record in Australia, up 18.5% to almost 400,000 in the three months through November. In New Zealand, the S&P/NZX 50 index fell 0.2% to 12,804.48

In rates,Treasuries were marginally cheaper across the curve, with the front-end underperforming ahead of December CPI release at 8:30am ET. Treasury 2-year yields higher by 1.8bp vs. Tuesday close while rest of the curve is less than 1bp cheaper on the day; 10-year yields around 1.74% with both bunds and gilts outperforming by over 2bp in the sector. Cash USTs bear flatten, cheapening roughly 2bps across the short end. Session highlight also includes 10-year note auction, a $36b reopening: US auctions resume with a $36BN 10-year reopening at 1pm, followed by $22b 30-year reopening Thursday. The WI 10-year at around 1.745%, above auction stops since January 2020 and ~23bp cheaper than December stop-out which tailed 0.4bp. Elsewhere, bunds and gilts drift higher, with the 10y point outperforming. Bund futures regain 170. Peripheral spreads tighten slightly.

In FX, most G-10 currencies were confined to narrow ranges after the dollar’s drop yesterday and the Bloomberg Dollar Spot Index hovered while the Treasury curve bear-flattened as yields rose by up to 2bps, while commodity currencies outperform but trade off best levels with G-10 FX generally trading narrow ranges.

Demand for long gamma exposure into the next Federal Reserve meeting remains subdued even as realized volatility stays relatively high. The Norwegian krone was the best G-10 performer, followed by the Canadian dollar, as oil steadied above $81 barrel after posting the biggest one-day surge this year as investors embraced risk assets, commodities climbed and industry estimates pointed to another drawdown in U.S. crude stockpiles. The euro moved in a tight $1.1355-1.1378 range and Bund yields inched lower, led by the belly of the curve. The pound treaded water as investors monitored London hospital admissions for any signs of an easing in pandemic pressures and questioned how much further the currency can rise when rate hikes are already priced in.Australian dollar edged up amid iron ore hitting a three-month high as heavy rains disrupted southeastern Brazil’s iron ore industry. Japanese government bonds rallied across maturities after a smooth five-year note auction, driving down benchmark 10-year yields from a 10-month high and the yen steadied. BOJ Governor Haruhiko Kuroda said he expects the country’s underlying inflation to pick up gradually over the long-term after moderate near-term gains led by energy prices.

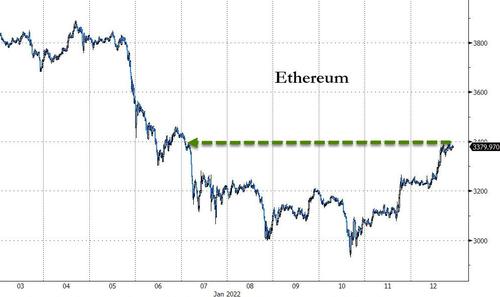

In commodities, crude futures fade a modest push higher. WTI stalls after a test of $82, Brent trades near $84. Spot gold drifts slightly lower near $1,817/oz. Base metals are in the green with LME nickel up 4%. Bitcoin jumped back over $43K while ether was above $3,300.

Looking at the day ahead now, and the aforementioned US CPI release for December will be the highlight. Other data releases include Euro Area industrial production for November and the US monthly budget statement for December. From central banks, the Fed will be releasing their Beige Book, and speakers include BoE Deputy Governor Cunliffe and the Fed’s Kashkari.

Market Snapshot

- S&P 500 futures up 0.1% to 4,710.50

- STOXX Europe 600 up 0.5% to 485.30

- MXAP up 1.6% to 196.29

- MXAPJ up 1.6% to 641.50

- Nikkei up 1.9% to 28,765.66

- Topix up 1.6% to 2,019.36

- Hang Seng Index up 2.8% to 24,402.17

- Shanghai Composite up 0.8% to 3,597.43

- Sensex up 1.0% to 61,200.72

- Australia S&P/ASX 200 up 0.7% to 7,438.90

- Kospi up 1.5% to 2,972.48

- German 10Y yield little changed at -0.04%

- Euro little changed at $1.1370

- Brent Futures up 0.5% to $84.17/bbl

- Gold spot down 0.3% to $1,815.68

- U.S. Dollar Index little changed at 95.59

Top Overnight News from Bloomberg

- Bank of France Governor Francois Villeroy de Galhau says the European Central Bank will do what is necessary to get inflation around 2% in the medium term

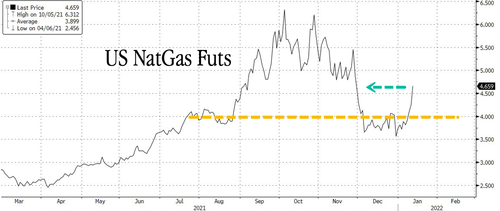

- Natural gas prices are likely to remain high for the next two years, with very few options to boost supplies quickly, according to the chief executive of Britain’s biggest energy supplier

- China’s inflation pressures moderated to 10.3% y/y in December, giving the central bank scope to cut interest rates to cushion the economy’s downturn just as most major nations look to tighten policy

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac bourses traded positively as stocks took their cue from the energy and tech-led gains in the US where sentiment was underpinned as yields eased and focus centred on Fed Chair Powell’s confirmation hearing where he noted that the Fed is prepared to act to control inflation if required but refrained from ramping up the hawkish rhetoric. ASX 200 (+0.7%) was led higher by strength in commodity-related sectors after gold made headway above the USD 1800/oz level and WTI crude notched its biggest gain in a month, while the tech sector was also inspired following the growth and duration bias stateside. Nikkei 225 (+1.9%) was underpinned amid the broad constructive mood and recent JPY weakening with Softbank among the top performers after it was reported to have repurchased around JPY 42.9bln of shares during December. Hang Seng (+2.8%) and Shanghai Comp. (+0.8%) also benefitted from the risk momentum with the former spearheaded by tech and energy shares including CNOOC which saw an initial double-digit percentage jump due to the rally in oil prices and after it raised its production guidance for 2022. However, the gains in the mainland were modest in comparison as Chinese property developers face key bond payments this week and with participants digesting softer than expected Chinese inflation data. Finally, 10yr JGBs clawed back yesterday’s losses following a rebound in USTs and despite the heightened risk appetite, while prices briefly stalled after the 5yr JGB auction showed weaker results across all metrics although this was only momentarily with further upside on a break above the 151.00 level.

Top Asian News

- Asia Stocks Jump to Near 7-Week High After Powell’s Fed Remarks

- Primavera, ABCI Are Said to Weigh Joining Hong Kong SPAC Race

- Just Two Listings Priced in Slow Hong Kong IPO Start: ECM Watch

- China’s Credit Stabilizes as PBOC Calls For More Home Loans

Overall a positive but choppy morning for European cash equities thus far (Euro Stoxx 50 +0.7%; Stoxx 600 +0.6%), with the regional mood underpinned by the upside seen on Wall Street and then across APAC markets. The gains were attributed to Powell refraining from sounding more hawkish, while noise has also been growing regarding the possibility for China to further ease monetary policy amid domestic growth concerns. US equity futures saw some mild selling shortly after the European cash open despite a lack of fundamental catalysts, and with action contained to the equity space – potentially as players take some chips off the table ahead of US CPI and following this week’s gains. Futures are back in modest positive territory at the time of writing, with the NQ (+0.2%) back to narrowly leading and the RTY (-0.1%) the slight laggard. Back to Europe, the region also saw some modest losses in lockstep with state-side futures but mostly remained in positive territory with relatively broad-based gains. The SMI (-0.2%) lags amid the pro-cyclical/anti-defensive nature of the European sector composition, with Healthcare and Food & Beverages at the bottom of the pile – thus exerting some pressure on heavyweights Roche (-1.5%) and Nestle (-0.6%). The sectors table sees Basic Resources, Oil & Gas and Tech towards the top – the former two amid price action in their respective complexes, and the latter tracking the sectoral gains on Wall Street and APAC. Taking a look at some individual movers, Just Eat Takeaway (+2%) and Sainsbury’s (+2%) gain on the LSE following trading updates, with the latter upping its guidance in the pre-market. The other end of the spectrum sees Philips (-14%) plumbing the depths after missing forecasts and reporting higher-than-expected costs. In terms of analyst commentary, Goldman Sachs has conformed to the view that European stocks will outperform this year as the US stocks’ outlook gets dimmer against the backdrop of a hawkish Fed; “The unusually high concentration of stocks within the S&P leaves it more vulnerable to pressures coming from antitrust regulation or higher bond yields”, the analysts said

Top European News

- Gas Prices to Stay High for Next Two Years, Centrica CEO Says

- Germany Tells Banks to Rebuild Capital Buffers as Lending Booms

- Goldman’s Stehn Sees ECB Remaining Patient on Rate Hikes

- WeTransfer to Kick Off Europe Listing Window With Amsterdam IPO

In FX, the Greenback is hovering off deeper post-NFP lows in advance of CPI data that is tipped to show another acceleration in headline terms, albeit due to base effects on a y/y basis, and could rekindle hawkish Fed policy vibes that were doused somewhat by chair Powell on Tuesday. To recap, at his renomination hearing in front of the Senate Banking Committee he was noncommittal on the timing for tightening and also pushed back on the notion that running down the balance sheet is likely to start soon after, if not immediately following lift-off and the end of tapering. Looking at the Dollar index as a proxy, a partial recovery in early European trade fell a fraction short of 95.700 and 95.500 is holding on the downside as Treasury yields meander between new cycle peaks and overnight retracement troughs awaiting the second leg of this week’s auction schedule in the form of Usd 36 bn 10 year notes alongside rhetoric from former Fed dove Kashkari.

- CAD – Ongoing strength in crude prices is helping to keep the Loonie aloft, and Usd/Cad is now testing support and underlying bids around 1.2550 as a result. However, the 55 DMA comes in just below the half round number and could stall the fall as WTI encounters some resistance circa Usd 82/brl.

- EUR/AUD/NZD/CHF/JPY/GBP – All narrowly mixed, marginally softer or off peaks against their US counterpart to be precise, with the Euro easing off after breaching 1.1350 and the 55 DMA on the way to peaking at 1.1378, the Aussie back under the 10 DMA having reached 0.7223 irrespective of softer than expected Chinese inflation metrics and the Kiwi fading from just a few pips shy of 0.6800 ahead of NZ building consents. Meanwhile, the Franc is maintaining 0.9250+ status, the Yen is staying afloat of the 115.50 mark after the BoJ upgraded its outlook for all 9 Japanese regions and Sterling retains a firm grip of the 1.3600 handle even though PM Johnson’s position is looking increasingly precarious as he heads for Question Time at the Commons. Note also, from a technical perspective there are several hurdles for Cable to overcome if its scales 1.3650, as Fibs sit at 1.3675 and 1.3706, while the 200 DMA resides at 1.3737.

- SCANDI/EM – The Nok has extended gains through 10.0000 vs the Eur in wake of firmer than forecast Norwegian mainland GDP and much less contraction in the overall economy compared to the previous quarter, while the Sek has pared some losses from recent lows with encouragement from news that Sweden plans to offer compensation to households facing higher energy bills to the tune of Sek 6 bn. Elsewhere, the Rub is lagging amidst ongoing angst between Russia and the West and the Try has not really taken on board latest protestations from Turkish PM Erdogan about inflation not matching fundamentals and his promise to lower prices soon. Conversely, the softer Usd in general is propping up the Cnh and Cny following the aforementioned downturn in Chinese PPI and CPI, while the Zar is continuing its bull run regardless of Gold waning beyond Usd 1820/oz, the Czk has more hawkish remarks from CNB’s Mora to lean on and the Brl could also benefit from BCB Governor Campos Neto repeating that further is appropriate.

In commodities, WTI and Brent front-month futures initially gained following a period of consolidation in APAC hours, although recently the benchmarks have drifted off best levels. Prices are underpinned by the softer Buck heading into the US CPI metrics, with the former finding resistance at USD 82/bbl (vs low 81.17/bbl) and the latter extending above USD 84/bbl (vs low 83.52/bbl). News flow for the complex on the lighter side in the European morning. Eyes remain on the US CPI metrics, whilst China’s zero-COVID policy remains as a headwind to global demand, with China halting more flights and China’s Tianjin locking down three districts due to the COVID outbreak, whilst the Dalian port also reported cases. From a data perspective, the contracts were little-swayed by the smaller-than-expected draw in Private Inventories, whilst the internals also saw a much larger-than-expected in gasoline stocks (+10.9mln vs exp. +2.4mln) but US NatGas futures remain firmer by some 4% at the time of writing. The EIA STEO yesterday meanwhile upped their 2022 oil prices forecast by almost USD 5/bbl vs last month but sees those levels falling throughout the year. In terms of geopolitics, France has poured some cold water on the recent optimism surrounding the Iranian nuclear deal, suggesting the sides are still some ways apart despite the reported progress. The Russian/Ukrainian front hasn’t seen any further developments thus far. Turning to metals, spot gold has been moving in lockstep with the Dollar and has waned off yesterday’s USD 1,822/oz best, with the downside seeing the 50 DMA (1,806), 21 DMA (1,803) and 200 DMA (1,801) ahead of the psychological USD 1,800/oz. Elsewhere, LME copper inches closer towards USD 10k/t from a USD 9,818/t intraday base, with the softer Dollar and upbeat mood in China spurring prices.

US Event Calendar

- 7am: Jan. MBA Mortgage Applications 1.4%, prior -5.6%

- 8:30am Dec. CPI data:

- 8:30am: Dec. CPI YoY, est. 7.0%, prior 6.8%; MoM, est. 0.4%, prior 0.8%

- 8:30am: Dec. CPI Ex Food and Energy YoY, est. 5.4%, prior 4.9%; MoM, est. 0.5%, prior 0.5%

- 8:30am: Dec. Real Avg Hourly Earning YoY, prior -1.9%, revised -1.7%

- 8:30am: Dec. Real Avg Weekly Earnings YoY, prior -1.9%

- 2pm: U.S. Federal Reserve Releases Beige Book

- 2pm: Dec. Monthly Budget Statement, est. -$5b, prior -$191.3b

DB’s Jim Reid concludes the overnight wrap

While we’re advertising we have a vacancy in our credit team to work with Craig and myself. We’re looking for a VP level European IG credit strategist. The candidate needs to work in IG credit and is most suitable for someone of 5-8 year experience. Because of HR/compliance procedures applicants have to apply at the following link here a little more on the role can be found. I won’t be able to respond directly to anybody on this. So if you or anyone you know is interested please use the link above.

The highlight of the last 24 hours was Chair Powell’s renomination hearing before the Senate Banking Committee. The overall communicated stance of policy wasn’t much changed with the hawkish pivot still on. Nevertheless, there were a few incremental takeaways. Powell did nothing to push back on liftoff being on the table in March, in line with our US econ team’s call and the increasing probability implied by the market, which is currently 85%. He made it clear that QE (yes it’s still happening) would finish in March, despite speculations it may come to an abrupt halt beforehand. In line with growing consensus, he painted a picture that made the start of QT likely in 2022. Finally, on the overall stance of policy, he emphasised the Fed needs to pull back from extreme levels of accommodation, but didn’t need to rush to get to a neutral stance of policy.

All told, yields did rally with Powell after earlier climbing. Yields on 2yr Treasuries decreased -1.2bps while the 10yr dipped -2.5bps, with the bulk of declines again coming later in New York trading hours. All this ahead of the all-important December US CPI print later today? The print comes out at 13:30 London time, and as you’ll be familiar with by now, repeated upside surprises in the inflation data have sent the year-on-year numbers up to multi-decade highs, putting significant pressure on the Fed. Indeed if you look at the monthly headline CPI reading, 7 of the last 9 releases have come in above the consensus estimate on Bloomberg. In terms of what to expect this time around, our US economists think that year-on-year CPI will rise to +7.0%, which will be the highest annual CPI number since 1982. And if that figure is realised, it would also mean that the real Fed Funds rate in December was around -7%, which for reference is lower than at any point in the 1970s, when the lowest the fed funds rate got in real terms was around -5%.

Over in equity markets, US indices were buoyed by rates rallying, paring back their initial losses as Powell spoke. The S&P 500 was on track for a 6th consecutive loss for the first time since February 2020, before recovering its poise and ending the day up +0.92%, it’s first day in the green since the first trading day of the year. Sector dispersion was wide, as energy (+3.41%) saw a noticeable outperformance as Brent Crude (+3.52%) closed above its pre-Omicron closing level for the first time, reaching $83.72/bbl, just as WTI (+3.82%) also posted a decent advance. Meanwhile tech stocks continue to be the beneficiary of the calm in rates following their slump last week, with the NASDAQ surging +1.41% and the FANG+ index gaining +1.53%.