January 20, 2022 · by harveyorgan · in Uncategorized · Leave a comment ·Edit

GOLD; UP $0.20 to $1842.20

SILVER: $24.66 UP 52 CENTS

ACCESS MARKET: GOLD: 1839.65..

SILVER: $24.47

Bitcoin: morning price: 41,220 down 651

Bitcoin: afternoon price: 41,443 down 223

Platinum price: closing up $14.10 to $1044.45

Palladium price; closing up $64,15 at $2012.45

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filed COMEX//NOTICES FILED 12/1343

EXCHANGE: COMEX

CONTRACT: JANUARY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,843.100000000 USD

INTENT DATE: 01/19/2022 DELIVERY DATE: 01/21/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 H MACQUARIE FUT 300

624 H BOFA SECURITIES 297

661 C JP MORGAN 3

TOTAL: 300 300

MONTH TO DATE: 5,564

NUMBER OF NOTICES FILED TODAY FOR JAN. CONTRACT: 300 NOTICE(S) FOR 30000 OZ (0.9331 TONNES)

total notices so far: 5564 contracts for 556,400 oz (17.306 tonnes)

SILVER NOTICES:

301 NOTICE(S) FILED TODAY FOR 1,505,000 OZ/

total number of notices filed so far this month 2766 : for 12,830,000 oz

GLD

WITH GOLD UP $0.20

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES OF GOLD FROM THE GLD/

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

CLOSING INVENTORY: 980.86 TONNES/

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 52 CENTS:/: A BIG CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 1.988 MILLION OZ INTO THE SLV//

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY SLV/ TONIGHT: 527.792 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG 2055 CONTRACTS TO 150,792 AND RESTS CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THIS GAIN IN OI WAS ACCOMPANIED WITH THE $0.71 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.71) AND WERE UNSUCCESSFUL IN KNOCKING OUT SOME SILVER LONGS AS WE HAD AN ATMOSPHERIC GAIN OF 4,051 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 10.505 MILLION OZ FOLLOWED BY TODAY’S 10,000 OZ E.F.P.. JUMP TO LONDON//NEW STANDING 14.335 MILLION OZ V) STRONG SIZED COMEX OI GAIN.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS -96

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTACTS for 13 days, total contracts: : 10019 contracts or 50.095 million oz OR 3.853 MILLION OZ PER DAY. (770 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 10,019 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 50.095 MILLION OZ

.

LAST 8 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2,055 WITH OUR 71 CENT GAIN SILVER PRICING AT THE COMEX// WEDNESDAY THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 1990 CONTRACTS( 1990 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY:/ AS WELL AS TODAY /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN OF 10.505 MILLION OZ FOLLOWED BY TODAY’S 10,000 E.F.P. JUMP TO LONDON //NEW STANDING 14.335, MILLION OZ// .. WE HAD ATMOSPHERIC SIZED GAIN OF 4051 OI CONTRACTS ON THE TWO EXCHANGES FOR 20.255 MILLION OZ//

WE HAD 301 NOTICES FILED TODAY FOR 1,505,000 OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A VERY STRONG 13,402 TO 552,606 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -3454 CONTRACTS

.

THE VERY STRONG SIZED INCREASE IN COMEX OI CAME DESPITE OUR GAIN IN PRICE OF $29.40//COMEX GOLD TRADING/WEDNESDAY/.AS IN SILVER WE MUST HAVE HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION AS THE TOTAL GAIN ON OUR TWO EXCHANGES TOTALLED AN ATMOSPHERIC SIZED 22,322 CONTRACTS…

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JAN AT 3.5614 TONNES FOLLOWED BY TODAY’S 0 OZ QUEUE. JUMP//NEW STANDING: 17.601 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $29.40 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD AN ATMOSPHERIC SIZED GAIN OF 22,322 OI CONTRACTS (69.43 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALLED A GIGANTIC SIZED 8920 CONTRACTS:

FOR FEB 8920 ALL OTHER MONTHS ZERO//TOTAL: 8920

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 556,060.

IN ESSENCE WE HAVE A HUMONGOUS SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 22,322, WITH 13,402 CONTRACTS INCREASED AT THE COMEX AND 8920 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 22,322 CONTRACTS OR 69.43TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (8920) ACCOMPANYING THE GIGANTIC SIZED GAIN IN COMEX OI (13,402): TOTAL GAIN IN THE TWO EXCHANGES 22,322 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR JAN. AT 3.7262 TONNES//FOLLOWED BY TODAY’S ZERO OZ QUEUE. JUMP.//NEW STANDING 17.601 TONNES 3)ZERO LONG LIQUIDATION,4) VERY STRONG SIZED COMEX OI. GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB.WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2021 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN : 50,406 CONTRACTS OR 5,040,600 oz OR 156.78 TONNES (13 TRADING DAY(S) AND THUS AVERAGING: 3877 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAY(S) IN TONNES: 156.78 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 156.78/3550 x 100% TONNES 4.41% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO DATE

JANUARY: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//INITIAL ISSUANCE//

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 2055 CONTRACTS TO 150,792 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 1990 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 1900 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1900 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2055 CONTRACTS AND ADD TO THE 1990 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF 4045 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 20.225 MILLION OZ,

OCCURRED WITH OUR $0.71 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 3.12 PTS OR 0.09% //Hang Sang CLOSED UP 824.50 PTS OR 3.42% /The Nikkei closed UP 305.70 PTS OR 1.11% //Australia’s all ordinaires CLOSED UP 0.16% /Chinese yuan (ONSHORE) closed UP 6.3452 /Oil UP TO 86.61 dollars per barrel for WTI and UP TO 87.92 for Brent. Stocks in Europe OPENED ALL MIXED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3452. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3491: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING STRONGER AGAINST USA DOLLAR

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A VERY STRONG SIZED 13,402 CONTRACTS AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX INCREASE OCCURRED DESPITE OUR GAIN OF $29.40 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A POWERFUL EFP (8920 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. LOOKS LIKE OUR BANKERS ARE FINALLY BAILING OUT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE NON ACTIVE DELIVERY MONTH OF JAN.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 8920 EFP CONTRACTS WERE ISSUED: ;: , DEC : 0 & FEB. 8920 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 8920 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: AN ATMOSPHERIC SIZED 22,322 TOTAL CONTRACTS IN THAT 8920 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A VERY STRONG SIZED COMEX OI GAIN OF 13,402 CONTRACTS..

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR JAN (17.601),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $29.40)

AND THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS THE TOTAL GAIN ON THE TWO EXCHANGES REGISTERED A WHOPPING 80.174 TONNES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JAN (14.93 TONNES)…

WE HAD – XXX CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 25,776 CONTRACTS OR 2,577,600 OZ OR 80.174 TONNES

Estimated gold volume today: 295,922 /// fair

Confirmed volume yesterday: 416,378 contracts strong

INITIAL STANDINGS FOR JAN ’22 COMEX GOLD

JAN 20

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 13,655.303 ozManfra |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | 20,090.680 ozBRINKS |

| No of oz served (contracts) today | 300 notice(s)30000 OZ0.9331 TONNES |

| No of oz to be served (notices) | 95 contracts 9500 oz 0.2954 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5564 notices 556,400 OZ17.306 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

No dealer deposit 0

No dealer withdrawal 0

1 customer deposit

i) 20,090.680 OZ

total deposit: 20,090.680 oz

1 customer withdrawals

i) Out of Manfra: 13,655.303 0z

ADJUSTMENTS: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of JANUARY we have an oi of 395 stand for JANUARY LOSING 1343 contracts. We had 1343 notices filed on WEDNESDAY, so we GAINED 0 contracts or an additional NIL oz will stand for

gold in this very non active delivery month of January.

FEBRUARY LOST 1833 CONTRACTS TO 184,136

March GAINED 90 contracts to stand at 2407..

We had 300 notice(s) filed today for 30,000 oz FOR THE JAN 2022 CONTRACT MONTH

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 300 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 12 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN /2021. contract month,

we take the total number of notices filed so far for the month (5464) x 100 oz , to which we add the difference between the open interest for the front month of (JAN: 395 CONTRACTS ) minus the number of notices served upon today 300 x 100 oz per contract equals 565,900 OZ OR 17.601 TONNES the number of TONNES standing in this NON active month of JAN. (numbers corrected from yesterday)

thus the INITIAL standings for gold for the JAN contract month:

No of notices filed so far (5564) x 100 oz+ (395) OI for the front month minus the number of notices served upon today (300} x 100 oz} which equals 565,900 oz standing OR 17.601 TONNES in this NON active delivery month of JAN.

We GAINED 0 contracts or an additional NIL oz of gold will stand for metal on this side of the pond.

TOTAL COMEX GOLD STANDING: 17.601 TONNES (HUGE FOR A JANUARY DELIVERY MONTH

IF THIS HOLDS TO THE END OF THE MONTH, THIS WILL BE THE HIGHEST EVER RECORDED GOLD STANDING FOR A JANUARY, GENERALLY A VERY POOR DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

206,468.649, oz NOW PLEDGED /HSBC 6.42 TONNES

174,041.813 PLEDGED MANFRA 5.41 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690

288,481,604, oz JPM No 2 8.97 TONNES

698,821.330 oz pledged June 12/2020 Brinks/27,96 TONNES

12,244.444 oz International Delaware: 0..3808 tonne

Loomis: 18,615.429 oz

total pledged gold: 1,653,017.372oz 51.42 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 33,567,534,149 OZ (1044,09 TONNES)

TOTAL ELIGIBLE GOLD: 15,986,993,639 OZ (497.26 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,580,540.519 OZ (546.82 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,927,523.0 OZ (REG GOLD- PLEDGED GOLD) 495.41 tonnes

END

JANUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//JAN 20

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,403,724.989 oz BrinksDelawareJPMorganHSBC |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 3,186,697.125 oz BrinksDelawareJPMorganManfra |

| No of oz served today (contracts) | 301 CONTRACT(S)1,505,000 OZ) |

| No of oz to be served (notices) | 101 contracts (505,000 oz) |

| Total monthly oz silver served (contracts) | 2766 contracts 12,830,,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 4 withdrawals

ii) Into Delaware; 228,216.706 oz

iii) Into JPmorgan: 578,945.100 oz

iv) Into Manfra; 1,183,665.519 oz

JPMorgan has a total silver weight: 185.500 million oz/354.142 million =52.38% of comex

ii) Comex withdrawals: 3

a) Out of CNT 925,629.560 oz

b) Out of Delaware; 175,637.090 oz

c) Out of Brinks 101,248.170 oz

d) out of manfra 1183,665.519 oz

total withdrawal 3,186.697.125 oz

we had 1 adjustment

customer to dealer..manfra 1,463,243.149 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 82.626 MILLION OZ

TOTAL REG + ELIG. 355.927 MILLION OZ

TOTAL NO OF CONTRACTS SERVED UPON THIS MONTH: 2347 CONTRACTS FOR 11,735,000 OZ

CALCULATION OF SILVER OZ STANDING FOR JANUARY

NUMBER OF NOTICES FILED TODAY: 301 NOTICES OR 1,505,000 OZ

silver open interest data:

FRONT MONTH OF JAN//2022 OI: 402 CONTRACTS LOSING 120 contracts on the day

We had 118 notices filed for WEDNESDAY so we LOST 2 contracts or 10,000 additional oz will NOT stand for delivery in this non active delivery month of January.

FOR FEB WE HAD A LOSS OF 14 CONTRACTS DOWN TO 656

FOR MARCH WE HAD A GAIN OF 1503 CONTRACTS UP TO 116,711 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 301 for 1,505,000 oz

Comex volumes: 69,975// est. volume today//fair

Comex volume: confirmed YESTERDAY: 79,573 contracts (strong)

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 2766 x 5,000 oz =. 12,830,000 oz

to which we add the difference between the open interest for the front month of JAN (x402) and the number of notices served upon today 301 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JAN./2021 contract month: 2766 (notices served so far) x 5000 oz + OI for front month of JAN (402) – number of notices served upon today (301) x 5000 oz of silver standing for the JAN contract month equates 14,335,000 oz. .

We LOST 2 contracts or an additional 10,000

oz will NOT stand for delivery on this side of the pond.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

GLD

JAN 20/WITH GOLD UP $.20 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 980.86 TONNES

JAN 19/WITH GOLD UP $29.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 5.27 TONNES INTO THE GLD/INVENTORY RESTS AT 981.44 TONNES

JAN 18/WITH GOLD DOWN $3.25//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 14/ WITH GOLD DOWN $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 13/WITH GOLD DOWN $5.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 12/WITH GOLD UP $8.65//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 11/WITH GOLD UP $19.25/A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FROM THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 10/WITH GOLD UP $2.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.08 TONNES

JAN 7/WITH GOLD UP $8.15//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWLA OF 1.16 TONNES FROM THE GLD////INVENTORY RESTS AT 978.83 TONNES

JAN 6/WITH GOLD DOWN $35.30//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .32 TONNES/INVENTORY RESTS AT 979.99 TONNES

JAN 5/WITH GOLD UP $10.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 980.31 TONNES

Jan 4/WITH GOLD UP $14.00//A HUGE CHANGE OF 4.65 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 980.31 TONNES

JAN 3/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 31/WITH GOLD UP $14.05 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 30/WITH GOLD UP $7.75 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 29/WITH GOLD DOWN $5.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 975.66 TONNES

DEC 28/WITH GOLD UP $2.00 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 973.63 TONNES

DEC 27/WITH GOLD DOWN $2.05: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.63 TONNES.

DEC 23/WITH GOLD UP $9.85 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.94 TONNES FROM THE GLD/// INVENTORY RESTS AT 973.63 TONNES

DEC 22/WITH GOLD UP $12.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 21/WITH GOLD DOWN $7.05 TODAY, NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 20/WITH GOLD DOWN $9.65 TODAY; A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.37 TONNES INTO THE GLD///INVENTORY RESTS AT 977.20 TONNES

DEC 17/WITH GOLD UP $7.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.20 TONNES

DEC 16/WITH GOLD UP $33.05TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.4 TONNES FROM THE GLD////INVENTORY REST AT: 977.20 TONNES

DEC15/WITH GOLD DOWN $7.80 TODAY/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.04 TONNES FROM THE GLD////INVENTORY RESTS AT 980.60 TONNES.

DEC 14/WITH GOLD DOWN $18.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64 TONNES

DEC 13/WITH GOLD UP $3.20 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 982.64 TONNES

DEC 10.WITH GOLD UP $7.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64 TONNES

DEC 9/WITH GOLD DOWN $9.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64.

DEC 8/WITH GOLD UP $5.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 984.38 TONNES

DEC 7/WITH GOLD UP $5.15 TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 984.38 TONNES

DEC 6/WITH GOLD DOWN $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 986.17 TONNES//

CLOSING INVENTORY: 980.86 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SLV.

JAN 20/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.998 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 527.792 TONNES

JAN 19/WITH SILVER UP 71 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.942 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 525.804 MILLION OZ

JAN 18/WITH SILVER UP 51 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS OF 1.11 MILLION OZ AND 1.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 527.246 MILLION OZ//

JAN 14/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 529.780 MILLION OZ//

JAN 13/WITH SILVER DOWN 2 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 832,000 OZ FROM THE SLV////INVENTORY RESTS AT 529.780 MILLION OZ

JAN 12/WITH SILVER UP 38 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//

JAN 11/WITH SILVER UP 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ/.

JAN 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 7/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 6/WITH SILVER DOWN 94 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL PF 226,000 OZ FROM THE SLV///INVENTORY RESTS AT 530.612 MILLION OZ?/

JAN 5/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 4/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 3/WITH SILVER DOWN 45 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.219 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 530.838 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC30/WITH SILVER UP 14 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.624 MILLILON OZ FROM THE SLV.//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 29/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ/

DEC 28/WITH SILVER UP 9 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.682 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 27/WITH SILVER UP 6 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681

DEC 23/WITH SILVER UP 19 CENTS TODAY:A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 22/WITH SILVER UP 29 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 538.883 MILLION OZ/

DEC 21/WITH SILVER UP 19 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.728 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 540.085 MILLION OZ

DEC 20/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 538.282 MILLION OZ

DEC 17/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 538.282 MILLION OZ//

DEC 16/WITH SILVER UP 91 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.33 MILLION OZ FROM THE SLV//INVENTORY REST AT 538.282 MILLION OZ

DEC 15WITH SILVER DOWN 38 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 2.48 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 541.612 MILLION OZ

DEC 14/WITH SILVER DOWN 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.092 MILLION OZ

DEC 13/WITH SILVER UP 11 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 3.561 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 543.092 MILLION OZ//

DEC 10.WITH SILVER UP 19 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 546.653 MILLION OZ..

DEC 9/WITH SILVER DOWN 43 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 2.96 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 546.653 MILLION OZ/

DEC 8/WITH SILVER DOWN 7 CENTS TODAY; NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.693 MILLION OZ///

DEC 7/WITH SILVER UP 24 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.693 MILLION OZ..

DEC 6/WITH SILVER DOWN 25 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.110 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 543.693 MILLION OZ//

CLOSING INVENTORY: 527.792 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: The Fed Made This Bed And Now We Have To Lie In It

THURSDAY, JAN 20, 2022 – 06:30 AM

Inflation is running hot. Economic data is running cold. Stocks and bonds are under pressure. The Fed is scrambling. In his podcast, Peter Schiff talked about the trajectory of the economy. He said we’re on the cusp of the most obvious crisis that virtually nobody saw coming. The Federal Reserve made this bed. Now we have to lie in it.

Stocks and bonds are off to a rough start in 2022 with the expectation of rate hikes on the horizon. In fact, many analysts now think that the Fed could raise interest rates five times in 2022. And some also think the first hike in March could be 50 basis points.

Hedge fund manager Bill Ackman called a .5% rate hike “shock and awe.”

Peter called this “ridiculous.”

It’s not shock and awe. When you’re talking about 7% inflation, a move from zero to 50 basis points is still recklessly low interest rates. And for a Fed that’s actually serious about fighting inflation, raising interest rates to 50 basis points is not nearly enough for the task at hand.”

Even so, a .5% rate hike could have a profound impact and pop the bubble economy.

Given the incredible amount of leverage that’s in the system, a 50 basis point rate hike can still do a lot of damage. And I think Bill Ackman is underestimating the extent of the damage. But not just the damage from the initial hike, but from all the subsequent hike, which aren’t going to do any good about slowing down this inflation freight train.”

Peter noted the price of oil hit has continued its upward trajectory this week. The price of oil is at a seven-year high with plenty of room to keep running up. In 2021, a lot of producers ate their rising costs. But they may well begin passing on those costs in 2022, which would mean more big jumps in CPI.

There is going to be a lot more upward pressure on the CPI despite the Fed’s rate hikes, even if we get them, even if we get more than the market expects. It still won’t be enough to stop inflation from getting worse.”

Peter said it seems clear the bond market is slowly starting to grasp this reality. And when they really start to get it, the dollar is going to tank.

Interestingly, silver had a strong day on Tuesday, up almost 50 cents. Peter said this shows the underlying strength in the commodity complex due to all the inflation baked into the cake.

Gold faced headwinds with rising bond yields and was down about $5.

But at some point, investors are going to realize that surging nominal yields mean nothing to the gold market because real yields are not rising. The Fed is so far behind the curve. And even if real yields were rising, meaning that negative yields were becoming less negative, any negative yield is a positive for gold because you don’t want to lose money in bonds. Whether you’re losing 3% a year, or 5% a year, or 7% a year — all of that is bad. You want to avoid losses. And one way to avoid losses is by owning gold. And more people are going to recognize that gold is a much better alternative than negative yielding bonds.”

The Empire State Manufacturing Index came in at -0.7 versus an expectation of 25.7. This indicates contraction and is the kind of number you see during a recession. Peter said the Fed is starting its tightening campaign even as the economy is rolling over.

The economy is getting weaker and they haven’t even begun to raise rates yet.”

The economic numbers are getting weaker even as inflation continues to run hot.

It is stagflation. This is the perfect storm. The Fed has got itself in a box. There is no way out. And the fact that the Fed is in this no-win situation on inflation should not surprise anybody. This was the most obvious outcome that nobody wanted to acknowledge.”

The Fed says it can deal with inflation. But if the central bank uses the tools at its disposal to address the inflationary problem, it will bring down the bubble economy. Peter has been warning about this since the Fed first launched quantitative easing in the wake of the financial crisis.

The Fed has been operating looking in the rearview mirror for over a decade. What they do is they print all this money, keep interest rates artificially low, do QE, and then they look back at the CPI, or the core CPI, or the personal consumption expenditure index, whatever measure they like. And as long as that number is below 2%, they think the road ahead is clear, and they keep on printing money. They keep on stimulating, looking back over their should seeing where the inflation numbers are. And then, all of a sudden, they look forward, and they see 7% CPI in 2021. Of course, there was evidence that inflation was going to be bad early in 2021. But of course, they ignored all that. They kept saying, ‘Well, this can’t be. This is transitory.’”

Meanwhile, they just ignored all the money they were printing out of thin air.

Well, now, because they printed so much money because they were looking in the rearview mirror instead of looking ahead like I was doing from the beginning, now, all of a sudden, they’re in this situation. They’ve got 7% interest rates. They can’t slam on the brakes. So, now they’re trying to come up with some way to ease their foot off the gas. But that is impossible because that’s not going to slow down the inflation. So, the Fed made this bed and we all have to lie in it because they were too loose for too long, and they’ve let loose the mother of all inflation genies. And everything they’re talking about doing is inefficient to actually put a stop to it.”

* * *

Learn more about real interest rates and what they mean for the gold and silver market here.

END

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,James RICKARDS

LAWRIE WILLIAMS: Gold and silver surge. Reality or fantasy?

In the slightly altered words of pop group Queen: Is this the real thing? Is this just fantasy? Gold and silver at last seem to be making a strong positive move. It’s probably too early to tell – we‘ve been here before as recently as last November, but this time it just feels different. The rises could be shot down in the key North American markets and the real test may well be at what level gold and silver are allowed to close the week tomorrow. We suspect gold may be held back below $1,850 at the week’s close, but if not it could surge further in the weeks ahead

Gold equities too – which often lead – were also up sharply yesterday – an early year bonus for their investors. A further firming of precious metals prices, if sustained, should lead to a continuing rise in dividends from those which pay them, while a gold and silver price boost gives a strong fillip to the junior markets too.

The rises in precious metal prices – yes platinum and palladium were both up strongly too – were accompanied by more weakness globally in general equity markets which could also morph towards an investment move into perceived safe havens like gold in particular. Equities seem to be recovering today, but that could just be a temporary delayed contrary reaction to recent falls. Gold as a wealth protector has stood the tests of time as such.

Investors have been bombarded over the past months with opinions from respected economists and analysts, although countered by others, that stock market prices are at unjustifiably high levels and that a serious market crash is imminent. Those commentators who end up proving to be wrong will quietly forget publicly that they ever made such predictions, while those that are right will, no doubt, shout their perspicacity from the virtual rooftops. Such is what passes for financial predictions nowadays. I suppose it has always been thus, but social media now pushes such boasts, or reticence, to the forefront.

On this subject, we have not ourselves been silent in predicting gold price growth. We certainly have been proved wrong on occasion in calling a false dawn with precious metals seeing subsequent setbacks, although the overall trend in terms of year-on-year price averages has been positive. But again we could be wrong that it looks like this time around precious metals could be in for a period of ascendance. We thus persist with our theorising on the basis that as we see it, positive factors currently outweigh the negatives, at least for gold and silver.

However, it is important to recognise that the gold price in particular will likely be driven, up or down, by the myriad of data releases, and U.S. Federal Reserve Bank (Fed) statements that will be forthcoming over the weeks and months ahead. Even so, we stick to our guns in noting that whatever the Fed decides to do on interest rate rises, the ever-continuing scourge of high inflation will keep real interest rates in negative territory for the foreseeable future. And negative real rates always make gold a positive investment asset choice, particularly when general equities are showing signs of weakness as they have been of late.

Of course there are well respected naysayers who predict a completely different outcome. They have looked at gold’s past performance when the Fed has started to raise interest rates and are forecasting a sharp dip in prices once the Fed’s likely tightening programme begins to get under way, and will deteriorate further on each successive rate rise. But we think this time is different due to the aforementioned negative real interest rate situation.

On the most recent few occasions when gold has plunged on expectations of Fed interest rate rises, this was before worrying inflation levels kicked in. While real interest rates were extremely low they were not nearly as negative as they are likely to be even at current inflation levels. We think high negative real rates will predominate investment thinking and that gold price progress will be largely unaffected until real rates start trending back to zero, or move into positive territory. Until this happens, which may yet be some years ahead, gold will remain a more attractive asset – particularly if equities remain weak.

Of course the current seemingly out-of control Covid infection rates in the U.S. will also have an impact on Fed thinking and likely action. The latest strain of the virus is proving to be highly transmissible and infection worries and consequent restrictive state and national legislation may well slow down Fed moves on tightening. This would be gold positive if it happens. With daily infection rates in the U.S. approaching 1 million per day – a huge psychological level if this comes about – coupled with the fact that activity in the U.S. is the current principal gold price driver, we could well see another short term surge in gold and silver prices. The effects could be less positive, though, for pgms which are much more affected by rises and falls in industrial demand.

In summary, we do think that current precious metal prices will at least be maintained. Further, there would seem to be a good chance that they will continue upwards and perhaps, with the occasional stutter, gold will reach $1,900 by the mid-year point and perhaps touch $2,000 again before the year-end. Silver may well even exceed our $25.50 year- end target wit that price level achievable in the next couple of months if our overall expectations on the path of gold and silver end up being accurate.

20 Jan 2022

3.Chris Powell of GATA provides to us very important physical commentaries

A very important commentary today from Chris Powell:

(ChrisPowell)

Delightful speculation on the new gold price needed to back the U.S. dollar

Submitted by admin on Wed, 2022-01-19 15:29 Section: Daily Dispatches

3:35p ET Wednesday, January 19, 2022

Gold Newsletter editor Brien Lundin today calls attention to a new report by Myrmikan Capital’s Dan Oliver about the gold price that would be necessary for U.S. gold reserves to back the dollar at levels that once were traditional:

Lundin writes of Myrmikan Capital: “This group has published some amazing analyses in recent months and quickly become one of my favorite sources of macro insights, particularly in relation to the massive bubbles created by decades of the Fed’s ever-easing monetary policy.

“But a report they just issued yesterday — entitled ‘The Bubble Is Bursting and Gold Is Strong’ — exceeds anything I’ve seen from them before.”

You’ve probably come across speculations like this over the years. Our friend Jim Rickards has offered them authoritatively from time to time.

They usually assume a market price for gold, though GATA has shown that market prices for monetary metals long have been opposed by the most powerful governments:

https://www.gata.org/node/20925

Other analysts, including the three most often cited by GATA — the U.S. economists Paul Brodsky and Lee Quaintance and the Scottish economist Peter Millar — have speculated that the gold price would be driven up spectacularly not by ordinary markets but by central bank decrees aiming to devalue debts and currencies and to reliquefy central banks holding gold.

The Brodsky and Quaintance speculation is here:

https://www.gata.org/node/11373

The Millar speculation is here:

https://www.gata.org/node/4843

These speculations are delightful “visions of sugarplums” for investors in the monetary metals, and today’s sharp rise in their prices will boost hope that government’s derivatives-based scheme of monetary metals price suppression is failing at last.

But this speculation presumes that markets, governments, and central banks eventually will demand gold as backing for currencies, as they did many years ago, rather than choose other commodity (oil is looking pretty good lately) or maybe cryptocurrency. This speculation also presumes that when the derivatives scheme fails, governments will not seek to demolish the appeal of the monetary metals with outright confiscation, confiscatory taxes, or some other fascist mechanism.

How people and governments will react in changing situations is always a speculation in itself. The past may be a guide but nothing requires people and governments to act exactly as they did before.

The only certainty here may be that governments will always want not just to control the value of money but also to control what is considered money.

Oliver’s new analysis is posted in PDF format at the Myrmikan internet site here:

Your secretary/treasurer believes that it is hard enough these days to discern what government is doing and so it is impossible to know what government will do, beyond its general objective of cheating people. So his recommendation remains what it always has been: Accumulate all the monetary metal you can, find a safe planet to keep it on, and, when you do, please call.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

4.OTHER GOLD STORIES

END

5.OTHER COMMODITIES/

6.CRYPTOCURRENCIES

Bank Of Russia Calls For Ban On Crypto Mining And Trading

THURSDAY, JAN 20, 2022 – 09:21 AM

Like many governments, Russian financial regulators have had a complicated relationship with cryptocurrencies. Back in October, Russian leader Vladimir Putin praised cryptocurrencies as a possible tool to help dismantle the global dollar-based financial system.

That didn’t stop Russia from barring the use of cryptocurrencies for payment. And now the country’s financial regulators are pushing for a China-style ban on crypto mining, something that could disrupt the international network supporting popular cryptocurrencies like bitcoin and ethereum. In a report published Thursday, the Russian Central Bank called for a full ban on crypto. Its findings were presented during an online press conference led by Elizaveta Danilova, the director of the Bank of Russia’s Financial Stability Department.

The report claimed cryptocurrencies have become widely used in illegal activities like fraud (in the west, they have become closely associated with ransomware attacks like the one that shut down the Colonial Pipeline and JBS). Because of this, Russia needs new laws that would effectively ban any crypto-related activities in the country. This ban should apply to exchanges, over-the-counter trading and peer-to-peer trading, the report said.

The bank, therefore, suggest Russia needs new laws and regulations that effectively ban any crypto-related activities in the country. In particular, cryptocurrency issuance and organization of its circulation in Russia must be banned. The ban should apply to exchanges, over-the-counter trading desks and peer-to-peer platforms. Russian institutional investors should not be allowed to invest in crypto assets and no Russian financial organizations or infrastructure should be used fro cryptocurrency transactions. And the existing ban on crypto payments should be more aggressively enforced.Elizaveta Danilova

But the biggest issue highlighted in the report is mining, which has flourished across Russia in recent years. Presently, Russia is the third-largest player in bitcoin mining, behind only the US and former Soviet Republic Kazakhstan. But, as Reuters points out, miners in Kazakhstan have been looking for greener pastures ever since the start of the latest round of unrest. As of August 2021, Russian miners accounted for 11.2% of the bitcoin network’s hashrate.

The RCB report claimed the proliferation of mining operations across Russia had created problems for energy consumption. Because of this “the best solution is to introduce a ban on cryptocurrency mining in Russia.”

Not only did the report also characterize crypto as a sophisticated Ponzi scheme (where price growth is driven by attracting new investors in a pyramid-like fashion), it also claimed crypto is a threat to the “sovereignty” of Russia’s monetary policy, the report claimed.

Back in September, China intensified its crackdown on cryptocurrencies with a blanket ban on all crypto transactions and mining. The news briefly hit bitcoin and crypto prices.

Russia is also following in China’s footsteps in another important way: The Russian central bank is working on a “digital ruble”, a central bank-backed digital currency similar to the “e-RMB”.

Back in the US, some twitter users scoffed at Russia’s push to suppress crypto while using the core technology for its own purposes.

Others mocked the notion that such a crackdown could ever be successful (although the CCP has done a pretty good job over in China).

The report found that cryptocurrencies are volatile and used widely in illegal activities like fraud. Russia has already banned the use of cryptocurrency for payments

At one point, Russia’s parliament and central bank had half-heartedly embraced crypto.

Whether the government now follows through with this crackdown remains to be seen.

Interested parties can find the full report below (beware: it’s written in Russian):

Consultation Paper 20012022 by Joseph Adinolfi Jr. on Scribd

end

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.3452

OFFSHORE YUAN: 6.3491

HANG SANG CLOSED UP 824.50 PTS OR 3.42%

2. Nikkei closed UP 305.70 PTS OR 1.11%

3. Europe stocks ALL MIXED

USA dollar INDEX DOWN TO 95.63/Euro FALLS TO 1.1338-

3b Japan 10 YR bond yield: RISES TO. +.145/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 114.27/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 86.61 and Brent: 87.92-

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE CLOSED UP// OFF- SHORE UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.0.028%/Italian 10 Yr bond yield FALLS to 1.31% /SPAIN 10 YR BOND YIELD RISES TO 0.67%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.34: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 1.70

3k Gold at $1840.00 silver at: 24.16 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble; Russian rouble UP 50/100 in roubles/dollar AT 76.66

3m oil into the 86 dollar handle for WTI and 87 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 114.27 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9158– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0383 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 1.833 DOWN 4 BASIS PTS

USA 30 YR BOND YIELD: 2.152 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.37

Futures Recover From Wednesday Rout As Yields, VIX Stabilize

THURSDAY, JAN 20, 2022 – 07:51 AM

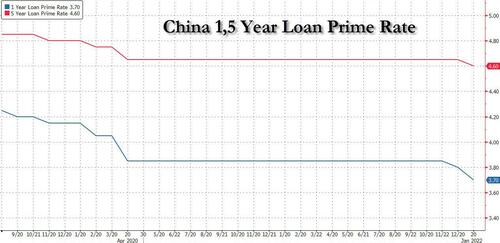

Whereas the stock plunge on Tuesday could be blamed on surging rates, the repeat tumble on Wednesday took place as Treasury yields dropped sharply, so with markets at a loss how to read rate signals, so far this morning S&P e-mini futures have rebounded by 23 points ot 0.5% from yesterday’s low just above 4,500 – a key support level according to JPMorgan – as volatility eased and global bond yields appear to have stabilize for now, and hours after China’s latest easing measure when Beijing lowered mortgage lending benchmark rates on Thursday as monetary authorities step up efforts to prop up the slowing economy. 10Y Treasuries rose from session lows, last trading at 1.84%, European stocks fluctuated as the dollar index was little changed and crude oil slipped after a three-day rally as gold held around a two-month high.

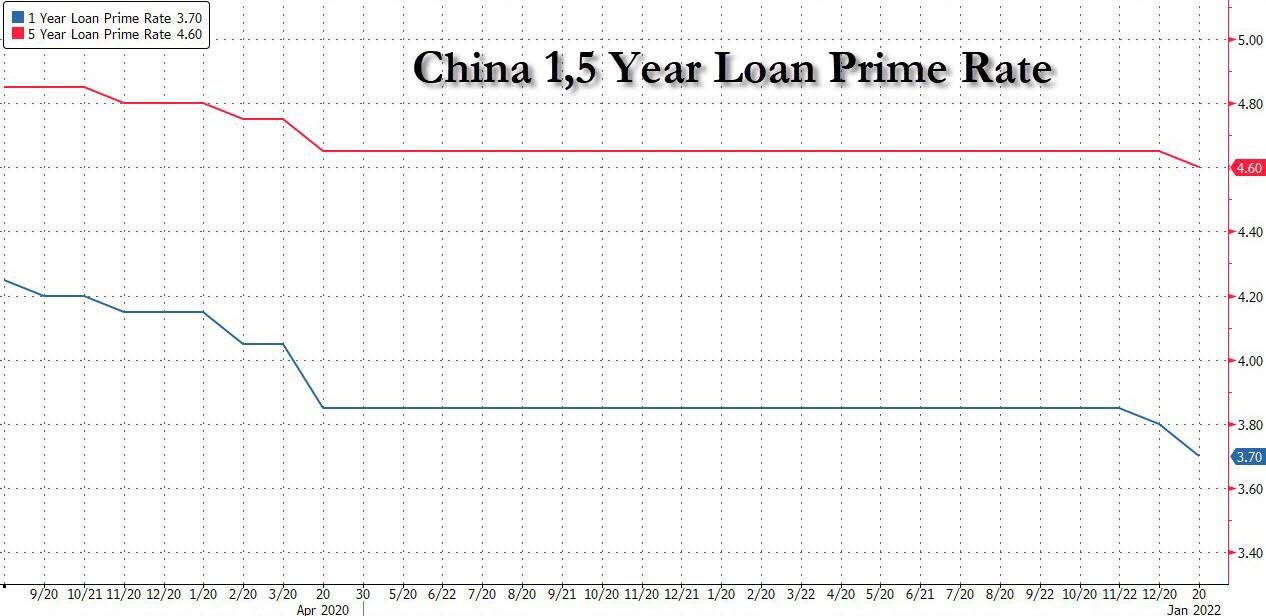

China’s cut to the one-year and five-year loan prime rates (LPR) which lowered the one-year LPR by 10 basis points to 3.70% from 3.80% – the second consecutive monthly cut – and the five-year LPR by 5 basis points to 4.60% from 4.65%, its first cut since April 2020….

… followed surprise cuts by China’s central bank on Monday to its short- and medium-term lending rates, and came days after the central bank’s vice governor flagged more moves ahead. China’s central bank “should hurry up, make our operations forward-looking, move ahead of the market curve, and respond to the general concerns of the market in a timely manner,” People’s Bank of China Vice Governor Liu Guoqiang said on Tuesday, heightening market expectations for more stimulus.

So as China goes all-in on easing the economy again, western markets are enjoying some of the benefits from the stabilization and seeking a bottom in the recent rout which has pushed the Nasdaq to the worst annual start since 2008.

“There is a certain will to buy a dip in U.S. indices, yet the aggressive hawkish Federal Reserve pricing doesn’t allow the appetite to get restored,” said Ipek Ozkardeskaya, senior analyst at Swissquote. “Strong earnings are the only hope for the equity bulls in the short-run.” Investors awaited data including unemployment claims and Netflix earnings.

The dominant theme for markets remains prospective Fed rate hikes and the possible reduction of its holdings in Treasuries starting later in 2022. The withdrawal of outsized stimulus threatens to inject more volatility across a range of assets.

“The focus of the rates market is still very much on the Fed and the anticipated dual-pronged attack of interest rate rises and balance sheet reduction, all of which we would expect to keep uncertainty levels elevated and volatility bubbling along over the coming weeks/months,” Simon Ballard, chief economist at First Abu Dhabi Bank, wrote in a note.

In premarket trading, automakers and energy companies held declines as crude oil slipped from a seven-year high. Alcoa rose 2.3% after the aluminum producer predicted rising demand and warned that any conflict between Russia and Ukraine could deepen the existing supply constraints for the metal. Other notable premarket movers:

- Ford (F US) drops 2.4% in premarket trading after Jefferies downgrades the automaker to hold from buy with limited scope seen for positive surprises.

- Advanced Micro Devices (AMD US) and NXP Semiconductors (NXPI US) both cut to neutral from overweight at Piper Sandler in note, with downside risks seen for both stocks. AMD slips 1.3% in premarket, NXPI unchanged.

- Casper Sleep (CSPR US) shares jump 12% in U.S. premarket trading, after the mattress retailer said that stockholders approved its merger with Durational.

- Silvergate Capital (SI US) gains 0.8% in premarket following Goldman Sachs analyst William Nance’s upgrade to buy from neutral.

- American Homes (AMH US) is down 4.9% in premarket after launching a stock sale via BofA, JPMorgan, Citi, Morgan Stanley.

- KemPharm (KMPH US) gained 4.6% postmarket after the biopharma company said it’s decided to make KP1077, a treatment for idiopathic hypersomnia, its next lead development candidate.

Investors now await U.S. data including unemployment claims and Netflix earnings after the close. The reporting season so far has been a little bit rocky, and investors need to monitor commentary from companies about price and wage pressures, Rebecca Felton, RiverFront Investment Group senior market strategist, said on Bloomberg Television.

“We do believe stocks can continue to go higher even as the Fed changes policy,” she said, adding corporate profits will still likely beat estimates.

In Europe, gains in the travel and media industries outweighed declines for carmakers and energy companies pushing pulling the Stoxx 600 Index up 0.15% after dropping as much as 0.5%. French semiconductor company Soitec sank 16%, the most in almost two years, after the executive committee at the French semiconductor company released a letter criticizing the board for an “incomprehensible” choice of new chief executive. Alstom SA fell after sales missed estimates. Citigroup has asked London staff to come into the office at least three days a week after the U.K. government ended a work-from-home requirement, with Goldman also telling staff to return.

European Central Bank President Christine Lagarde said the ECB has “every reason” not to respond as forcefully as the Fed to soaring consumer prices. The central bank has come under pressure to act, but officials say an interest-rate increase is highly unlikely this year since the current bout of inflation is driven by supply shocks and a spike in energy costs.

Stocks in Asia climbed, ending a five-day slump, as sentiment was boosted by a decline in Treasury yields from recent highs and a cut in China’s lending rates. The MSCI Asia Pacific Index rose as much as 1.1%, driven by consumer-discretionary and communication-services shares. Hong Kong’s Hang Seng Index had its best day since July 2020, leading regional benchmarks, and China stocks rose after banks cut borrowing costs, a move set to benefit struggling property developers. The 10-year U.S. Treasury yield fell to 1.84%, as traders appeared calmer about the Federal Reserve’s next policy move. Prospects of faster-than-expected tightening hammered Asian equities this week, driving the MSCI Asia Pacific Index into negative territory for the year. “Equity adjustments to higher inflation are driven by higher input costs, interest rates, and higher selling prices,” DBS Bank Strategist Joanne Goh wrote in a note. “Consumer staples goods, which have lower pricing power, would be most affected by rising material costs.” Tencent and Alibaba were among the biggest contributors to the regional measure’s gain Thursday, as China’s internet regulator denied reports of drafting deals-related rules.

Japanese equities closed higher, after a volatile morning session following Wednesday’s selloff, as the market remained wary over Covid-19 infections and U.S. interest-rate hikes. Electronics makers and service providers were the biggest boosts to the Topix, which rose 1%. The benchmark swung between a gain of as much as 1.4% and loss of 0.6% Thursday. Fast Retailing and Sony were the largest contributors to a 1.1% rise in the Nikkei 225, which similarly fluctuated. “Speculation over U.S. rate hikes, inflation concerns spurred by rising oil prices and worry over corporate earnings are things weighing on sentiment,” said Takashi Ito, an equity market strategist at Nomura Securities. Still, “the drop in U.S. equities has softened, and the current situation isn’t likely to develop into any prolonged global stock rout.” Stocks rose in Hong Kong and China after Chinese lenders lowered borrowing costs for a second straight month. U.S. shares fell overnight, with the Nasdaq Composite entering a correction, as investors assessed outlooks for earnings growth amid the potential for monetary policy tightening.

Australian stocks also edged higher, with the S&P/ASX 200 index rising 0.1% to close at 7,342.40, recovering from an earlier loss of as much as 0.5% as miners surged. Northern Star was the top performer after it maintained its full-year gold production forecast and issued a 2Q update. Kelsian Group was the worst performer, falling for a third day. Investors also assessed jobs data. Australia’s unemployment rate tumbled to a 13-year low in December, potentially setting the stage for the Reserve Bank to scrap its bond-buying program and bring forward interest-rate increases. In New Zealand, the S&P/NZX 50 index fell 0.9% to 12,497.10, notching its lowest close since June.

In rates, Treasuries trade near day’s highs as U.S. trading begins after erasing Asia-session losses, with futures near top of Wednesday’s range. The Treasury curve bull-flattened and the U.S. notes outperformed German and U.K. benchmarks with yields richer by 2bp to 3bp across the curve, spreads within 1bp of Wednesday’s closing levels; 10-year yield near 1.84% outperforms bunds and gilts by 2bp and 1bp. Peripheral spreads tighten at the margin. Bank issuance expected to continue following Wednesday’s jumbo Goldman Sachs deal, which saw swap spreads tighten, adding support for Treasuries. Treasury sells $16b 10-year TIPS new issue at 1pm ET.

In FX, the Bloomberg Dollar Spot Index was little changed as most Group-of-10 peers consolidated while AUD topped the G-10 after Australia’s unemployment rate tumbled to a 13-year low. The Australian dollar touched its strongest level this week after the December jobless rate fell to a 13-year low, beating expectations. Short-end yields climbed amid bets on an early end to RBA’s bond buying. The euro traded in a narrow range around $1.1350; euro-dollar one-week implied volatility, which now captures the next Federal Reserve meeting, rises by as much as 118 basis points to touch 6.16%, the highest since Jan. 7; the relative premium rises above parity for the first time since mid-December and stands around 72 basis points as of 7am London. The pound edged higher against the dollar as Wednesday’s comments from Bank of England Governor Andrew Bailey failed to derail market positioning for monetary tightening and sterling resilience. Money markets are close to fully pricing a 25bps hike next month. Norway’s krone was little changed even as the central bank said it’s on track to raise borrowing costs in March, citing a continued upswing in the oil-rich economy and signaling less worry over the resurgent virus. The yen steadied after Wednesday’s advance as traders sought clarity on the direction of the greenback. Benchmark 10-year JGB yields were little changed.

In commodities, crude futures are in the red; March WTI off 0.5% near $85.30, Brent back below $88. Spot gold holds a narrow range close to the top of Wednesday’s sharp rally near $1,840/oz. Base metals trade well, lead by LME nickel.

Looking at the day ahead, data releases from the US include the weekly initial jobless claims, December’s existing home sales, and the Philadelphia Fed’s business outlook for January. Meanwhile in Europe, there’s Germany’s PPI for December and the final Euro Area CPI reading for December. From central banks, the ECB will be publishing the minutes from their December meeting. Finally, earnings releases include Netflix, Union Pacific and American Airlines Group.

Market Snapshot

- S&P 500 futures up 0.4% to 4,540.75

- STOXX Europe 600 down 0.2% to 480.02

- MXAP up 1.1% to 193.34

- MXAPJ up 1.2% to 636.48

- Nikkei up 1.1% to 27,772.93

- Topix up 1.0% to 1,938.53

- Hang Seng Index up 3.4% to 24,952.35

- Shanghai Composite little changed at 3,555.06

- Sensex down 1.1% to 59,457.79

- Australia S&P/ASX 200 up 0.1% to 7,342.39

- Kospi up 0.7% to 2,862.68

- Brent Futures down 0.8% to $87.76/bbl

- Gold spot down 0.1% to $1,839.41

- U.S. Dollar Index little changed at 95.52

- German 10Y yield little changed at -0.02%

- Euro little changed at $1.1349

- Brent Futures down 0.7% to $87.80/bbl

Top Overnight News from Bloomberg

- The European Central Bank has “every reason” not to respond as forcefully as the Federal Reserve to soaring consumer prices, according to President Christine Lagarde

- Britain’s acute cost-of- living crunch will hit in April, instantly stretching household and company budgets and penalizing the poorest households, many of which have already been most impacted by Covid-19

- President Joe Biden said he thinks Vladimir Putin doesn’t want a full- blown war but will “move in” on Ukraine after amassing 100,000 troops on its border, part of an extraordinarily blunt assessment of Russian intentions and the West’s likely response

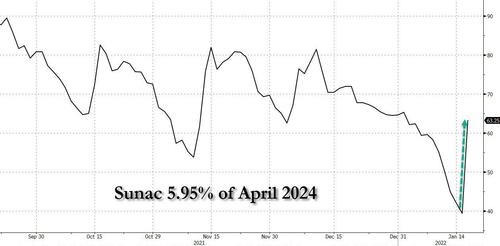

- A record-breaking rally in Chinese property bonds petered out on Thursday amid growing investor doubt over how much a reported plan to allow developers greater access to funds from presold homes will benefit distressed firms

- Near-record food costs risk climbing further as surging oil prices boost the appeal of turning more agricultural commodities into biofuels

- Turkey is set to pause its cycle of interest-rate cuts Thursday after a sliding currency and rising global energy prices pushed consumer inflation to its highest level since the beginning of President Recep Tayyip Erdogan’s rule

A more detailed look at global markets courtesy of Newsquawk

GEOPOLITICS

- US President Biden said he thinks Russian President Putin does not want a full-blown war but thinks Putin will test the West. Furthermore, Biden added that Putin has never seen sanctions like the ones he has promised, while he added that Ukraine joining NATO in the new term is not likely. (Newswires)

- US senior administration official said no option has been taken off the table in terms of sanctions on Russia and the US is prepared to look at sanctions on the largest financial institutions in Russia if there is a Ukraine invasion. Furthermore, the official stated that any move by Russian military to acquire land in Ukraine will merit a severe economic response and the White House also warned that if any Russian military move across the Ukrainian border, it will be met with a swift, severe and united response from US and its allies, while it added that any Russian aggression short of military action will be met with a decisive, reciprocal and united response. (Newswires)

- Russia’s Kremlin notes there have been some positive signals on NATO’s willingness to discuss some security issues with Russia but they are not fundamentally important to Russia; doesn’t rule out a conversation between President Putin and US President Biden at some stage. (Newswires)

- Chinese military said a US warship entered waters near the Paracel Islands without permission, while Chinese forces followed the US ship and warned it to leave. Furthermore, China’s military demanded that the US immediately stop such provocations or it will bear serious consequences of unforeseen events. (Newswires)

- Russia, Iran, and China will hold joint naval drills on Friday, according to ISNA. (Newswires)

- North Korea’s Politburo meeting on Wednesday which was presided over by leader Kim, called for reconsidering trust building measures due to US hostile policy and ordered to examine a restart of all temporarily suspended activities.

APAC TRADE

- Asian equity markets eventually traded mostly higher but with price action choppy after US bourses waned.

- ASX 200 (+0.1%) lacked firm direction.

- Nikkei 225 (+1.1%) was choppy on FX fluctuations and positive domestic trade data.

- Hang Seng (+3.4%) and Shanghai Comp. (U/C) benefited from PBoC LPR action in APAC hours.

Top Asian News

- Asia Stocks Snap Rout as China Cuts Lending Rates, Yields Slip

- Fintech Giant Kakao Pay’s Top Execs Quit After Investor Revolt

- BHP Holders Set to Back Single Listing as Miner Mulls M&A

- Bank Indonesia Sends First Hints of Policy Normalization

European Trade

- Major bourses in Europe are softer, Euro Stoxx 50 -0.2%, in an indecisive morning as initial post-PBoC upside fizzled out with catalysts/drivers minimal.

- US equity futures are firmer, ES +0.4%, picking back up from yesterday’s pressure with the NQ +0.7% outperforms amid a pull-back in yields

- European sectors are mixed with Travel & Leisure modestly outperforming while Oil & Gas and Banking benchmarks lagging given crude and yield action respectively.

Top European News

- Valneva Soars After Vaccine Update; Bryan Garnier Says Buy Stock

- Turkey May Spend $3.8 Billion to Boost State Banks’ Capital

- Unilever CEO Misses Out on Advil Just as He May Need It

- Asia Stocks Snap Rout as China Cuts Lending Rates, Yields Slip

FX

- Dollar drifts alongside Treasury yields after solid 20 year auction and ahead of jobless claims, Philly Fed and existing home sales.

- Aussie rules G10 roost as upbeat jobs data leads to more hawkish and aggressive RBA rate and QE expectations.

- Pound retains post UK inflation momentum but wary about further political upheaval, Norwegian Crown slips as Norges Bank sticks to tightening in March script and USD/TRY moves lower on an unchanged CBRT decision which emphasises the aim of prioritising the TRY.

- However, Yuan remains firm after PBoC sets near 4 year high CNY midpoint fix and trims Chinese LPRs.

Commodities

- WTI and Brent front month futures are choppy intraday; WTI & Brent pivot USD 85.50/bbl and USD 88/bbl respectively.

- Spot gold and silver trade horizontally, but retain the gains derived in yesterday’s session.

- LME copper remains supported and is nearing USD 10k/t to the upside once more.

- Kiruk-Ceyhan oil pipeline (150k BPD) has now returned to full capacity, according to Reuters citing a KRG source. (Newswires)

US Event Calendar

- 8:30am: Jan. Initial Jobless Claims, est. 225,000, prior 230,000; Continuing Claims, est. 1.56m, prior 1.56m

- 8:30am: Jan. Philadelphia Fed Business Outl, est. 19.0, prior 15.4

- 10am: Dec. Existing Home Sales MoM, est. -0.5%, prior 1.9%; Home Resales with Condos, est. 6.42m, prior 6.46m

DB’s Jim Reid concludes the overnight wrap

We’re having more operations in my family at the moment than a WWII army general. One of my twins is having two grommets inserted today and the other twin has to have the same procedure soon and I’m leaning towards fresh knee surgery in 10 days time. My wife is the only one holding us all together currently! Talking of which she has already left for the hospital (first time up earlier than me in 11 years of knowing her) and has just WhatsApp-ed to say that I need to put Maisie’s hair in a plait before I drop her and one of her brothers off at school given her absence. I didn’t have the guts to say that I’ve no idea how to do this, so I’ve just spent 5 minutes on YouTube looking into it. So apologies if the EMR is a bit later than it could have been but I had to find out how to plait at 5am.

Sentiment has weaved in and out of positive/negative territory like the most tangled of hairstyles over the last 24 hours but the US session was ultimately defined by the S&P 500 nose diving in the last 45 minutes of trading to end the day down -0.97%. The tech sector was amongst the biggest laggards again (-1.37%) and the bigger tech companies in the discretionary sector (-1.81%) encouraged bigger declines there. Financials (-1.65%) also declined on the back of a flattening yield curve, even if the narrative around financial earnings released yesterday painted a slightly more positive picture than earlier reporters. The S&P is now -5.50% below its peak reached to start the year, while the NASDAQ’s -1.15% decline brings it -10.69% below its all-time high and into correction territory. Tech stocks taking a hit from higher discount rates makes intuitive sense, and the last time the Nasdaq had a -10% correction was February 2021, when real 10yr rates had also sold off around 50bps. Next week we see a slew of tech earnings which have the ability to magnify or reverse the move. Netflix is up today.

Sovereign yields have proved much quieter over the last 24 hours. The treasury yield curve bull flattened, with 10yr yields down a modest -0.9bps to 1.86%, while 2yr yields increased +1.5bps. Policy expectations for this year were left unchanged, the market is still pricing in 4 Fed rate hikes this year, having priced in 1 full additional hike to start the year. Our US economists flag that the risk from here is for even tighter rate policy, see more here.

In Europe it was a very different story however, particularly in the UK where data showed yet another upside surprise on inflation. The latest numbers put CPI inflation at +5.4% in December (vs. +5.2% expected), which marked the fastest pace of inflation since 1992, having surpassed the more recent peaks in both 2008 and 2011. In response, investors moved to dial up the probability of further hikes from the Bank of England, and overnight index swaps are now fully pricing in a 25bp rate hike from the Bank of England at their meeting in 2 weeks’ time, which is in line with our UK economist’s call. As a result, gilt yields rose across the curve as well, with the 10yr yield up +3.9ps to 1.25%, the highest in almost 3 years.

This pattern of higher yields was echoed elsewhere in Europe, where there was a significant milestone reached as yields on 10yr bunds traded in positive territory during the European morning for the first time since May 2019. They did fall back throughout the day, but in closing +0.7bps higher at -0.02%, it still marked the nearest to positive territory that they’d closed since that time. Otherwise on the continent, yields on French OATs (+1.3bps) hit their highest level since April 2019, those on 10yr BTPs (+2.2bps) hit their highest level since June 2020, whilst equities outperformed the US as the STOXX 600 advanced +0.23%.

The main force driving the recent shift from central banks has been the continued persistence of inflation, and developments in commodity markets yesterday suggested there’d be little respite on that front anytime soon. Oil prices continued to advance higher, with Brent Crude up +1.06% to $88.44/bbl, and WTI up +1.79% to $86.96/bbl, which in both cases puts them at their highest levels since 2014, whilst WTI’s gains means that its YTD performance now stands just below +15% after less than 3 weeks of 2022 so far.

Asian markets are stronger overnight after a reduction in Chinese borrowing costs coupled with Japan’s double-digit export growth. The Shanghai Composite (+0.30%) and CSI (+1.11%) are both up after the PBOC cut its one-year loan prime rate (LPR) by 10bps to +3.7% to while the five-year LPR – which is a reference rate for mortgages, was cut by 5bps from +4.65% to +4.6%, the first time since April 2020, as part of the efforts to shore up the economy. Regulators also seem to be easing access to cash for property developers from pre-sold properties in a sign that the authorities want to limit the recent property sector woes.

Elsewhere, the Nikkei (+1.21%) is trading higher after exports in Japan increased for the 10th consecutive month, growing faster than expected (+17.5% y/y) in December (vs +15.9% market expectations) as supply bottlenecks continued to ease in the final quarter of 2021. Although it did follow a +20.5% rise in November. Separately, the Hang Seng (+2.33%) is edging higher, breaking a five-day losing run as China’s easing measures improved investor risk appetite. Meanwhile, the Kospi (+0.49%) is holding in better.

Following on from this, equity futures are indicating a positive start in the DM world with contracts on the S&P 500 (+0.43%) and DAX (+0.27%) pointing higher.

President Biden held his second press conference since taking office at around the US close last night. It came at a crucial juncture for his administration, as he tried to rally support for his social spending agenda, particularly among recalcitrant members of his own party. The presser covered a range of topics, domestic and foreign. The main takeaway was some capitulation on the build back better bill, which Biden admitted would likely need to be broken into smaller chunks to pass, and his hawkish tone on the recent tensions with Russia. He believes Russia will “move in” on Ukraine in some form or another.