JAN 19//

January 19, 2022 · by harveyorgan · in Uncategorized · Leave a comment ·Edit

GOLD; UP $29.40 to $1842.00

SILVER: $24.14 UP 71 CENTS

ACCESS MARKET: GOLD: 1840.55..

SILVER: $24.15

Bitcoin: morning price: 42,021 up 243

Bitcoin: afternoon price: 41,871 down 93

Platinum price: closing up $43.65 to $1030.35

Palladium price; closing up $109.55 at $2012.45

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filed COMEX//NOTICES FILED 12/1343

EXCHANGE: COMEX

CONTRACT: JANUARY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,812.300000000 USD

INTENT DATE: 01/18/2022 DELIVERY DATE: 01/20/2022

FIRM ORG FIRM NAME ISSUED STOPPED

323 H HSBC 837

624 H BOFA SECURITIES 1331

661 C JP MORGAN 500 12

905 C ADM 6

TOTAL: 1,343 1,343

MONTH TO DATE: 5,264

/

NUMBER OF NOTICES FILED TODAY FOR JAN. CONTRACT: 1343 NOTICE(S) FOR 134300 OZ (4.17 TONNES)

total notices so far: 5264 contracts for 526,400 oz (16.373 tonnes)

SILVER NOTICES:

118 NOTICE(S) FILED TODAY FOR 590,000 OZ/

total number of notices filed so far this month 2465 : for 590,000 oz

GLD

WITH GOLD UP $29.40

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS): A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A HUGE DEPOSIT OF 5.23 TONNES INTO THE GLD.

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

CLOSING INVENTORY: 981.44 TONNES/

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 71 CENTS:/: A BIG CHANGE IN SILVER INVENTORY AT THE SLV// STRANGE!!! A WITHDRAWAL OF 1.942 MILLION OZ FROM THE SLV//

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY SLV/ TONIGHT: 525.804 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC 3010 CONTRACTS TO 148,911 AND RESTS CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND SURPRISINGLY THIS GAIN IN OI WAS ACCOMPANIED WITH THE $0.51 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.51) AND WERE UNSUCCESSFUL IN KNOCKING OUT SOME SILVER LONGS AS WE HAD AN ATMOSPHERIC GAIN OF 4,895 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 10.505 MILLION OZ FOLLOWED BY TODAY’S 675,000 OZ QUEUE. JUMP//NEW STANDING 14.345 MILLION OZ V) GIGANTIC SIZED COMEX OI GAIN.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS -174

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTACTS for 12 days, total contracts: : 8119 contracts or 40.595 million oz OR 3.3382 MILLION OZ PER DAY. (676 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 8119 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 40.595 MILLION OZ

.

LAST 8 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3010 WITH OUR 51 CENT GAIN SILVER PRICING AT THE COMEX// TUESDAY THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 1885 CONTRACTS( 1885 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY:/ AS WELL AS TODAY /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN OF 10.505 MILLION OZ FOLLOWED BY TODAY’S 675,000 QUEUE JUMP //NEW STANDING 14.345, MILLION OZ// .. WE HAD ATMOSPHERIC SIZED GAIN OF 4895 OI CONTRACTS ON THE TWO EXCHANGES FOR 24.475 MILLION OZ//

WE HAD 118 NOTICES FILED TODAY FOR 590,000 OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR 3,153 TO 539,204 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -6283 CONTRACTS

.

THE FAIR SIZED INCREASE IN COMEX OI CAME DESPITE OUR LOSS IN PRICE OF $3.25//COMEX GOLD TRADING/TUESDAY/.AS IN SILVER WE MUST HAVE HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR HUMONGOUS SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION AS THE TOTAL GAIN ON OUR TWO EXCHANGES TOTALLED AN ATMOSPHERIC SIZED 17,731 CONTRACTS…

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JAN AT 3.5614 TONNES FOLLOWED BY TODAY’S STRONG 85,900 OZ QUEUE. JUMP//NEW STANDING: 17.601 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $3.25 WITH RESPECT TO TUESDAY’S TRADING

WE HAD AN ATMOSPHERIC SIZED GAIN OF 24,014 OI CONTRACTS (74.69 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALLED A GIGANTIC SIZED 14,578 CONTRACTS:

FOR FEB 14,578 ALL OTHER MONTHS ZERO//TOTAL: 14,578

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 545,487.

IN ESSENCE WE HAVE A HUMONGOUS SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 17M731, WITH 3,153 CONTRACTS INCREASED AT THE COMEX AND 14,578 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 24,014 CONTRACTS OR 74.69TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (14,578) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (3,153): TOTAL GAIN IN THE TWO EXCHANGES 17M731 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR JAN. AT 3.7262 TONNES//FOLLOWED BY TODAY’S 85,900 OZ QUEUE. JUMP.//NEW STANDING 17.601 TONNES 3)ZERO LONG LIQUIDATION,4) STRONG SIZED COMEX OI. GAIN 5) HUMONGOUS ISSUANCE OF EXCHANGE FOR PHYSICAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB.WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2021 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN : 41,486 CONTRACTS OR 4,148,600 oz OR 129.03 TONNES (12 TRADING DAY(S) AND THUS AVERAGING: 3457 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES: 129.03 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 129.03/3550 x 100% TONNES 3.63% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO DATE

JANUARY: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//INITIAL ISSUANCE//

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GIGANTIC SIZED 3010 CONTRACTS TO 148,737 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 1885 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 1885 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1885 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3010 CONTRACTS AND ADD TO THE 1885 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF 4895 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 24.475 MILLION OZ,

OCCURRED WITH OUR $0.51 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 11.73 PTS OR 0.33% //Hang Sang CLOSED UP 15.03 PTS OR 0.06% /The Nikkei closed DOWN 790.02 PTS OR 2.80-% //Australia’s all ordinaires CLOSED DOWN 1.02% /Chinese yuan (ONSHORE) closed UP 6.3468 /Oil UP TO 86.08 dollars per barrel for WTI and UP TO 87.86 for Brent. Stocks in Europe OPENED ALL GREEN EXCEPT ITALY // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3468. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3504: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING STRONGER AGAINST USA DOLLAR

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 3153 CONTRACTS AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX INCREASE OCCURRED DESPITE OUR LOSS OF $3.25 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A POWERFUL EFP (14,578 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. LOOKS LIKE OUR BANKERS ARE FINALLY BAILING OUT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE NON ACTIVE DELIVERY MONTH OF JAN.. THE CME REPORTS THAT THE BANKERS ISSUED A GIGANTIC SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 14,578 EFP CONTRACTS WERE ISSUED: ;: , DEC : 0 & FEB. 14,578 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 14,578 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: AN ATMOSPHERIC SIZED 17,731 TOTAL CONTRACTS IN THAT 14,573 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 3153 CONTRACTS..

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR JAN (14.93),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $3.25)

BUT THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS THE TOTAL GAIN ON THE TWO EXCHANGES REGISTERED A WHOPPING 55.15 TONNES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JAN (14.93 TONNES)…

WE HAD – 6283 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 17,731 CONTRACTS OR 1,773,100 OZ OR 55.15 TONNES

Estimated gold volume today: 185,216 /// poor

Confirmed volume yesterday: 485,006 contracts strong

INITIAL STANDINGS FOR JAN ’22 COMEX GOLD

JAN 19

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 20,737.395 ozMalca 645 kilobars |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 1343 notice(s)134,300 OZ4.1773 TONNES |

| No of oz to be served (notices) | 395 contracts 39,500 oz 1.2286 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5264 notices 526400 OZ16.373 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

No dealer deposit 0

No dealer withdrawal 0

0 customer deposit

1 customer withdrawals

i) Out of Malca: 20,737,395 0z

(645 kilobars)

ADJUSTMENTS: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of JANUARY we have an oi of 1738 stand for JANUARY GAINING 859 contracts. We had 0 notices filed on TUESDAY, so we GAINED 859 contracts or an additional 85,900 oz will stand for

gold in this very non active delivery month of January. The resulting queue jump equates to 2.672 tonnes,

FEBRUARY LOST 47,114 CONTRACTS TO 185,969

March LOST 17 contracts to stand at 2317..

We had 1343 notice(s) filed today for 134,300 oz FOR THE JAN 2022 CONTRACT MONTH

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 1343 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 12 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN /2021. contract month,

we take the total number of notices filed so far for the month (5264) x 100 oz , to which we add the difference between the open interest for the front month of (JAN: 1738 CONTRACTS ) minus the number of notices served upon today 1343 x 100 oz per contract equals 565,900 OZ OR 17.601 TONNES the number of TONNES standing in this NON active month of JAN. (numbers corrected from yesterday)

thus the INITIAL standings for gold for the JAN contract month:

No of notices filed so far (5264) x 100 oz+ (1738) OI for the front month minus the number of notices served upon today (1343} x 100 oz} which equals 565,900 oz standing OR 17.601 TONNES in this NON active delivery month of JAN.

We GAINED A HUGE 859 contracts or an additional 85,900 oz of gold will stand for metal on this side of the pond.

TOTAL COMEX GOLD STANDING: 17.601 TONNES (HUGE FOR A JANUARY DELIVERY MONTH

IF THIS HOLDS TO THE END OF THE MONTH, THIS WILL BE THE HIGHEST EVER RECORDED GOLD STANDING FOR A JANUARY, GENERALLY A VERY POOR DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

206,468.649, oz NOW PLEDGED /HSBC 6.42 TONNES

174,041.813 PLEDGED MANFRA 5.41 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690

288,481,604, oz JPM No 2 8.97 TONNES

698,821.330 oz pledged June 12/2020 Brinks/27,96 TONNES

12,244.444 oz International Delaware: 0..3808 tonne

Loomis: 18,615.429 oz

total pledged gold: 1,653,017.372oz 51.42 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 33,561,098.772 OZ (1043.89 TONNES)

TOTAL ELIGIBLE GOLD: 15,980,558.253 OZ (497.06 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,580,540.519 OZ (546.82 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,927,523.0 OZ (REG GOLD- PLEDGED GOLD) 495.41 tonnes

END

JANUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//JAN 19

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,202,510.800 oz BrinksCNTDelaware |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 2,213,232.567 ozBrinksDelawareJPMorganMalca |

| No of oz served today (contracts) | 118 CONTRACT(S)590,000 OZ) |

| No of oz to be served (notices) | 404 contracts (2,020,000 oz) |

| Total monthly oz silver served (contracts) | 2465 contracts 12,325,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We had 4 deposits

i)Into Brinks: 1,182,987.027 oz

ii) Into Delaware; 172,670.410 oz

iii) Into JPmorgan: 577,997.500 oz

iv) Into Malca; 279,577.630 oz

JPMorgan has a total silver weight: 185.500 million oz/354.142 million =52.38% of comex

ii) Comex withdrawals: 3

a) Out of CNT 925,629.560 oz

b) Out of Delaware; 175,637.090 oz

c) Out of Brinks 101,248.170 oz

total withdrawal 1,202,510,800 oz

we had 0 adjustment

the silver comex is in stress!

TOTAL REGISTERED SILVER: 81.163 MILLION OZ

TOTAL REG + ELIG. 354.142 MILLION OZ

TOTAL NO OF CONTRACTS SERVED UPON THIS MONTH: 2347 CONTRACTS FOR 11,735,000 OZ

CALCULATION OF SILVER OZ STANDING FOR JANUARY

NUMBER OF NOTICES FILED TODAY: 118 NOTICES OR 590,000 OZ

silver open interest data:

FRONT MONTH OF JAN//2022 OI: 522 CONTRACTS GAINING 131 contracts on the day

We had 11 notices filed for TUESDAY so we GAINED 135 contracts or 675,000 additional oz will stand for delivery in this non active delivery month of January.

FOR FEB WE HAD A LOSS OF 22 CONTRACTS DOWN TO 670

FOR MARCH WE HAD A GAIN OF 2695 CONTRACTS UP TO 115,268 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 11 for 55,000 oz

Comex volumes: 30,762// est. volume today//poor

Comex volume: confirmed YESTERDAY: 108,632 contracts (strong)

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 2465 x 5,000 oz =. 12,325,000 oz

to which we add the difference between the open interest for the front month of JAN (522) and the number of notices served upon today 118 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JAN./2021 contract month: 2465 (notices served so far) x 5000 oz + OI for front month of JAN (522) – number of notices served upon today (118) x 5000 oz of silver standing for the JAN contract month equates 14,345,000 oz. .

We GAINED 135 contracts or an additional 675,000

oz will stand for delivery on this side of the pond.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

GLD

JAN 18/WITH GOLD DOWN $3.25//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 14/ WITH GOLD DOWN $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 13/WITH GOLD DOWN $5.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 12/WITH GOLD UP $8.65//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 11/WITH GOLD UP $19.25/A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FROM THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 10/WITH GOLD UP $2.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.08 TONNES

JAN 7/WITH GOLD UP $8.15//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWLA OF 1.16 TONNES FROM THE GLD////INVENTORY RESTS AT 978.83 TONNES

JAN 6/WITH GOLD DOWN $35.30//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .32 TONNES/INVENTORY RESTS AT 979.99 TONNES

JAN 5/WITH GOLD UP $10.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 980.31 TONNES

Jan 4/WITH GOLD UP $14.00//A HUGE CHANGE OF 4.65 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 980.31 TONNES

JAN 3/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 31/WITH GOLD UP $14.05 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 30/WITH GOLD UP $7.75 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 29/WITH GOLD DOWN $5.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 975.66 TONNES

DEC 28/WITH GOLD UP $2.00 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 973.63 TONNES

DEC 27/WITH GOLD DOWN $2.05: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.63 TONNES.

DEC 23/WITH GOLD UP $9.85 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.94 TONNES FROM THE GLD/// INVENTORY RESTS AT 973.63 TONNES

DEC 22/WITH GOLD UP $12.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 21/WITH GOLD DOWN $7.05 TODAY, NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 20/WITH GOLD DOWN $9.65 TODAY; A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.37 TONNES INTO THE GLD///INVENTORY RESTS AT 977.20 TONNES

DEC 17/WITH GOLD UP $7.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.20 TONNES

DEC 16/WITH GOLD UP $33.05TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.4 TONNES FROM THE GLD////INVENTORY REST AT: 977.20 TONNES

DEC15/WITH GOLD DOWN $7.80 TODAY/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.04 TONNES FROM THE GLD////INVENTORY RESTS AT 980.60 TONNES.

DEC 14/WITH GOLD DOWN $18.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64 TONNES

DEC 13/WITH GOLD UP $3.20 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 982.64 TONNES

DEC 10.WITH GOLD UP $7.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64 TONNES

DEC 9/WITH GOLD DOWN $9.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64.

DEC 8/WITH GOLD UP $5.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 984.38 TONNES

DEC 7/WITH GOLD UP $5.15 TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 984.38 TONNES

DEC 6/WITH GOLD DOWN $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 986.17 TONNES//

CLOSING INVENTORY: 976.21 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SLV.

JAN 19/WITH SILVER UP 71 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 527.246 MILLION OZ

JAN 18/WITH SILVER UP 51 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS OF 1.11 MILLION OZ AND 1.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 527.246 MILLION OZ//

JAN 14/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 529.780 MILLION OZ//

JAN 13/WITH SILVER DOWN 2 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 832,000 OZ FROM THE SLV////INVENTORY RESTS AT 529.780 MILLION OZ

JAN 12/WITH SILVER UP 38 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//

JAN 11/WITH SILVER UP 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ/.

JAN 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 7/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 6/WITH SILVER DOWN 94 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL PF 226,000 OZ FROM THE SLV///INVENTORY RESTS AT 530.612 MILLION OZ?/

JAN 5/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 4/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 3/WITH SILVER DOWN 45 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.219 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 530.838 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC30/WITH SILVER UP 14 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.624 MILLILON OZ FROM THE SLV.//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 29/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ/

DEC 28/WITH SILVER UP 9 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.682 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 27/WITH SILVER UP 6 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681

DEC 23/WITH SILVER UP 19 CENTS TODAY:A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 22/WITH SILVER UP 29 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 538.883 MILLION OZ/

DEC 21/WITH SILVER UP 19 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.728 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 540.085 MILLION OZ

DEC 20/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 538.282 MILLION OZ

DEC 17/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 538.282 MILLION OZ//

DEC 16/WITH SILVER UP 91 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.33 MILLION OZ FROM THE SLV//INVENTORY REST AT 538.282 MILLION OZ

DEC 15WITH SILVER DOWN 38 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 2.48 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 541.612 MILLION OZ

DEC 14/WITH SILVER DOWN 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.092 MILLION OZ

DEC 13/WITH SILVER UP 11 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 3.561 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 543.092 MILLION OZ//

DEC 10.WITH SILVER UP 19 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 546.653 MILLION OZ..

DEC 9/WITH SILVER DOWN 43 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 2.96 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 546.653 MILLION OZ/

DEC 8/WITH SILVER DOWN 7 CENTS TODAY; NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.693 MILLION OZ///

DEC 7/WITH SILVER UP 24 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.693 MILLION OZ..

DEC 6/WITH SILVER DOWN 25 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.110 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 543.693 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: This Bubble Economy Is Going To Burst

WEDNESDAY, JAN 19, 2022 – 06:30 AM

Peter Schiff recently appeared on the Rob Schmidt Show on Newsmax to talk about the trajectory of the US economy. Peter explains how the Federal Reserve and the US government created a massive bubble, why it is going to ultimately pop, and how to protect your savings and investments when it does.

The First question Rob asked was how is the Federal Reserve going to fix the inflation problem?

Simply put, it’s not. The Fed will make it worse.

Peter said in the first place, the Fed is lying about the extent of the problem. The CPI doesn’t measure the rise in prices accurately.

If we just use the same CPI that we used during the 70s and 80s, and applied the numbers today, we would get about 15 percent inflation for 2021. So, last year was worse than any year of the 1970s, and it was worse than 1980 when CPI was up 13.5 percent. So, this is the worst inflation we’ve ever seen.”

Peter said, unfortunately, it’s going to get even worse.

We have just seen the tip of an inflationary iceberg.”

How did we get into this mess to begin with?

The Fed created the problem.

They’ve been printing all this money. They sent the printing presses into overdrive during the pandemic. But we had an even bigger problem. The government forced people to stop working during the pandemic. So, people weren’t on the job. They weren’t producing goods. They weren’t supplying services. They should have spent less money because they weren’t earning money. The government made the mistake of sending everybody stimulus money so they could go out and spend money to buy products that didn’t even exist because they weren’t created. That’s why we have a supply shortage — because everybody is spending money that the Fed printed, not money that they earned producing goods and providing services. So, it’s a double-whammy. Prices are going ballistic. And this year is going to be worse than last.”

The Fed has said it plans to raise rates, possibly to 2 percent by 2022. Rob said that doesn’t seem substantial. Peter likened it to spitting in the ocean.

Inflation is already 7 percent, even if you accept the government’s numbers, which are a lie. How do you fight 7 percent inflation with 2 percent interest rates? Remember, the Fed had interest rates at 2.5 percent in 2018 when they had no inflation to fight. CPI was only up 1.9 percent in 2018. Yet, the Fed is not going to raise interest rates now to a level they were back then. So, the whole thing is a lie. The truth is if the Fed actually raised interest rates high enough to fight inflation, it would crush the economy. We’d have a worse financial crisis than 2008. The stock market would crash –bond market, real estate market. Government would have to slash spending because interest rates would skyrocket. And so to prevent that from happening, the Fed is going to not fight inflation and that’s why it’s going to get so much worse.”

But the economy seems healthy. That is until you look beneath the surface. We have record trade deficits. The government is running massive budget deficits.

We’re living in a gigantic bubble, and now we’re beginning to see that because prices are really starting to rise and there’s no way to stop them from going up. And this is when everything comes collapsing down. Because eventually, this stagflationary environment that we’re in, which will be much worse than the 1970s – more inflation and a weaker economy – is going to prick that bubble. So, even if the Fed won’t prick it, the markets are going to prick it for them.”

With inflation so pervasive, Peter said anybody who is retired or who wants to retire needs to get out of dollars.

Inflation is going to wipe you out. It is a gigantic tax and it’s going to impoverish an entire generation unless they act quickly to get into real assets. … You have to own real things that can’t be printed because if you just own paper, you’re going to get wiped out.”

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,James RICKARDS

3.Chris Powell of GATA provides to us very important physical commentaries

Craig Hemke writes about the spreaders that which I have been detailing for over 2 years.

(CraigHemke)

Craig Hemke at Sprott Money: Another mechanism for rigging Comex gold futures prices?

Submitted by admin on Tue, 2022-01-18 12:01 Section: Daily Dispatches

11:57a ET Tuesday, January 18, 2022

Dear Friend of GATA and Gold:

Writing at Sprott Money today, the TF Metals Report’s Craig Hemke suggests that increases in “trade at settlement” trades in Comex gold futures signify another mechanism by which bullion banks conceal their trading the better to manipulate prices.

Hemke’s analysis is headlined “Comex Gold Trade at Settlement” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/COMEX-Gold-Trade-at-Settlement-Craig-Hemke-January-18-2021

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Will all 50 states and for that matter, the rest of the world remove all taxes on gold and silver…..the true money.

Will this be the year of sound money in the U.S.?

Submitted by admin on Tue, 2022-01-18 21:32 Section: Daily Dispatches

By JP Cortez

Money Metals News Service, Eagle, Idaho

Tuesday, January 18, 2022

Last year was a good year for state-level sound-money legislation across the United States, and 2022 could be even better.

To date, 42 states have removed some or all taxes from the purchase of gold and silver. And there are new bills pending in five of the eight remaining states — Tennessee, Mississippi, Kentucky, Hawaii, and New Jersey.

Taxing the exchange of Federal Reserve notes for the monetary metals is an atrocious policy, for several reasons. …

… For the remainder of the analysis:

https://www.moneymetals.com/news/2022/01/18/the-year-of-sound-money-002454

Building on the success enjoyed by sound-money advocates in Arkansas and Ohio last year, more than a half dozen states are now considering legislation that rolls back discriminatory taxes and regulations on the sale, use, and purchase of gold and silver.

END

4.OTHER GOLD STORIES

END

5.OTHER COMMODITIES/

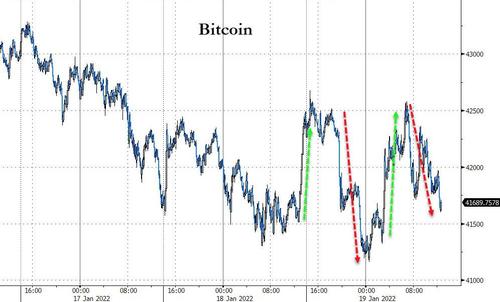

6.CRYPTOCURRENCIES

Latest on BTC

Inbox

S | 11:00 PM (1 minute ago) | ||

| to Chris, me |

Mostly a continuation of the previous article:

https://novusconfidential.wordpress.com/2022/01/19/iceland-kazakh-crypto-the-greater-malaise-for-bitcoin/

Corrections, constructive criticism, feedback, always appreciated.

The eight Fed use cases listed were inspired by the late great Andy Gause,his writing, his radio show discussions, as well as my own research.To some extent the Fed $ use case list leaves out the eurodollar, which has always bugged me.

The loss of Mr Gause was of course a major blow to Monetary Realism, and to all of us.

I’ve tried to (very imperfectly) write about much of what Mr Gause taught us, regarding the monetary system.

Back to the article, I hoped to highlight that the reverse repo situation is only one *indicator*of what’s happening with tapering, not a hard link to the recent decline in crypto.

Regards, Steve

end

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.3468

OFFSHORE YUAN: 6.3504

HANG SANG CLOSED UP 15.07 PTS OR 0.06%

2. Nikkei closed DOWN 790.02 PTS OR 2.80%

3. Europe stocks ALL GREEN EXCEPT ITALY

USA dollar INDEX DOWN TO 95.61/Euro RISES TO 1.1339-

3b Japan 10 YR bond yield: FALLS TO. +.137/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 114.47/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 86.08 and Brent: 87.86-

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE CLOSED UP// OFF- SHORE UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO -+.0.002%/Italian 10 Yr bond yield RISES to 1.34% /SPAIN 10 YR BOND YIELD RISES TO 0.68%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.34: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 1.65

3k Gold at $1819.80 silver at: 23.76 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble; Russian rouble UP 27/100 in roubles/dollar AT 76.06

3m oil into the 86 dollar handle for WTI and 87 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 114.47 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9160– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0387 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

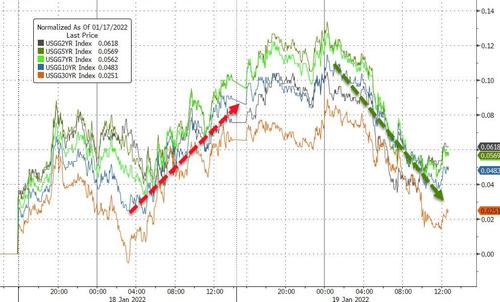

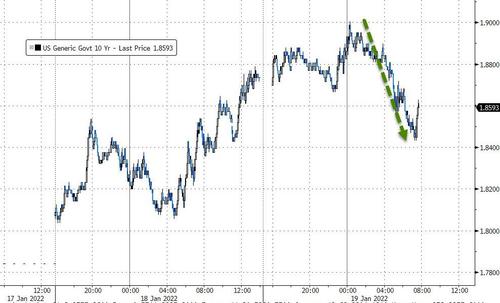

USA 10 YR BOND YIELD: 1.881 UP 1 BASIS PTS

USA 30 YR BOND YIELD: 2.189 UP 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.59

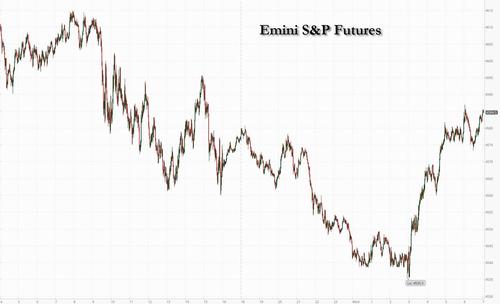

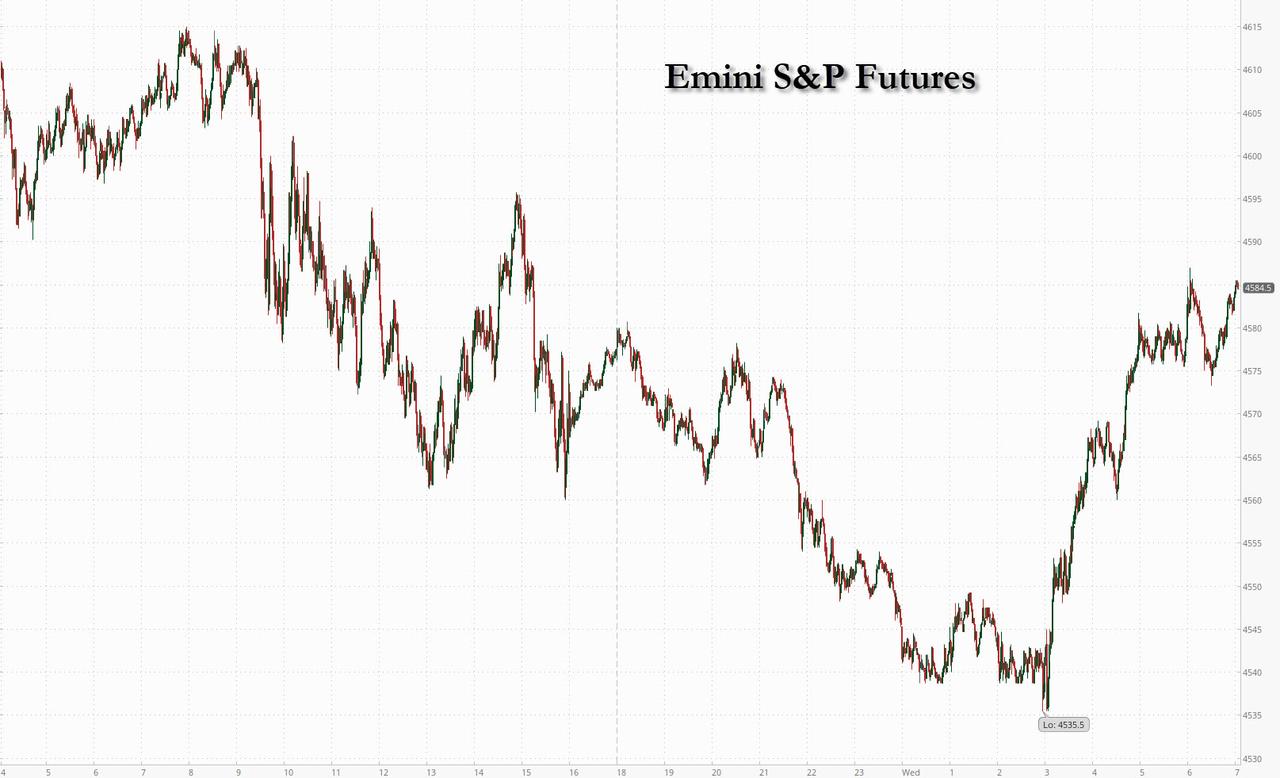

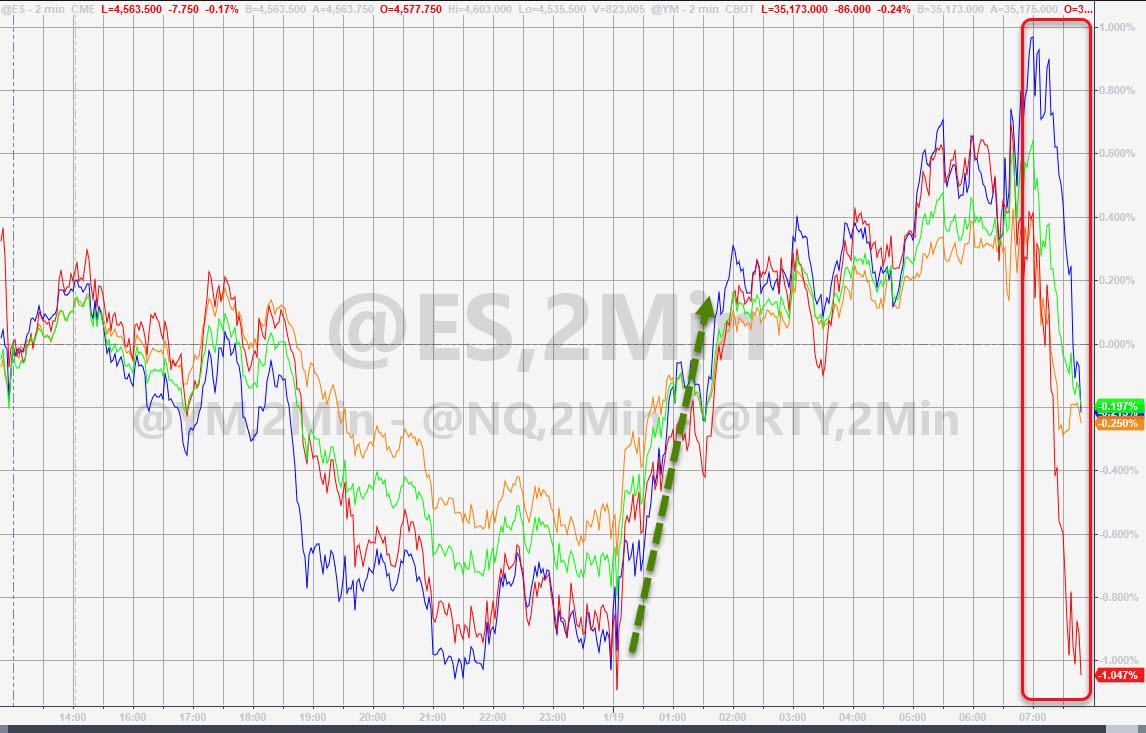

Futures Rebound Strongly From Overnight Rout As Yields Stabilize

WEDNESDAY, JAN 19, 2022 – 07:34 AM

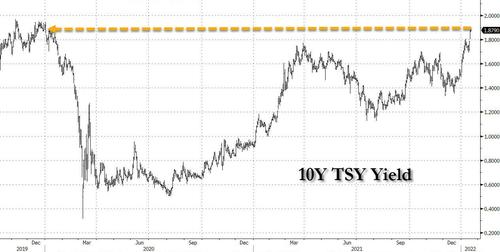

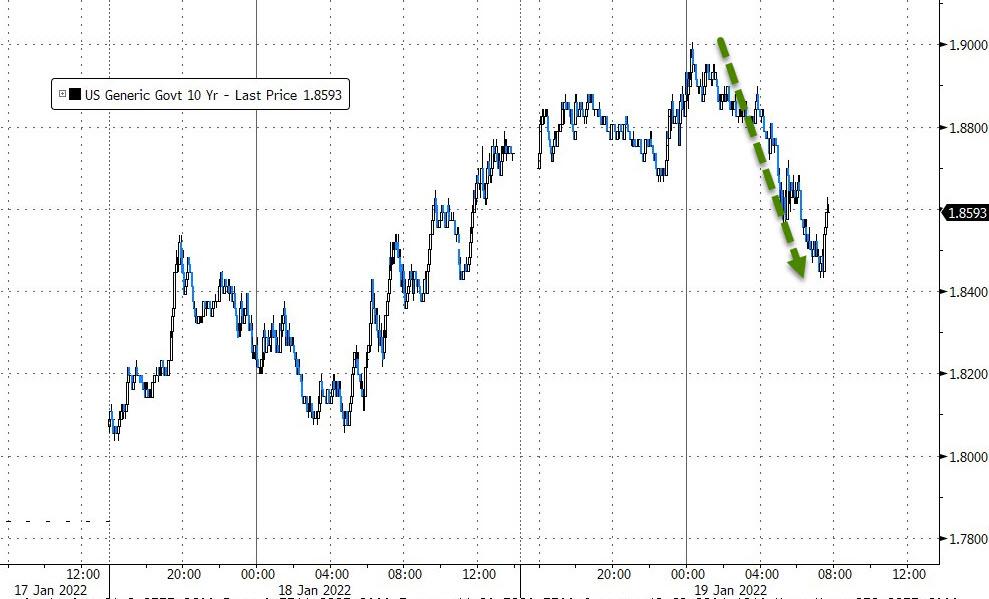

After what earlier looked like another assured overnight rout, especially after 10Y yields hit 1.90% and Brent rose as high as $89/bbl, US equity futures reversed earlier losses to trade higher as earnings optimism outweighed concerns over soaring bond yields and a 50bps March rate hike. As of 7:00am ET, emini S&P futures were up 14 points ot 0.3% to 4,585, Nasdaq futures were up 65 points or 0.44% and Dow futures were also in the green by 89 points or 0.25%. The dollar slumped after several days of sharp gains, the 10Y yield traded at 1.8826%, down from the session’s highest levels, and Brent was at $88.23.

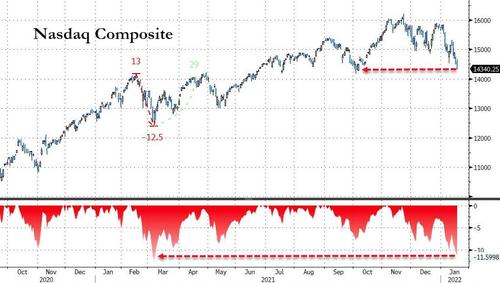

The prospect of accelerated policy tightening as well as concerns over the omicron variant and inflation hurting companies’ profits have whipsawed equities this year. The surge in Treasury yields has fueled a rotation out of expensive technology and growth shares and into cheaper parts of the market. Meanwhile, the 10Y yield has continued its aggressive push higher overnight, and hit a fresh 2 year high, rising just above 1.90% for the first time since Jan 2020, before retracing some of the move. Britain’s inflation rate surged unexpectedly to the highest since 1992 and Germany’s 10-year yield turned positive for the first time since 2019.

The surge in yields has routed high duration tech names – the Nasdaq 100 plunged 2.6% yesterday to the lowest level since mid-October. “The 2-year Treasury has moved too aggressively in pricing in Fed tightening, in our view, and we expect the yield curve to steepen,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “This steepening should further improve the positive backdrop for financial services companies,” he said.

SoFi Technologies, the financial firm led by former Twitter executive Anthony Noto, extended its gains in U.S. premarket session after the Office of the Comptroller of the Currency granted it a U.S. banking charter.

“We are in late stage of the cycle, where equities will post lower returns due to weaker growth and higher rates, but we expect the ongoing correction to be short,” Luca Paolini, chief strategist at Pictet Asset Management, said by email. He’s forecasting the S&P 500 index and U.S. 10-year yields at 2% by the end of the year.

Most European equities are in the green, recovering after a soggy start. Euro Stoxx 50 is up 0.5%, rallying ~1% from opening levels. Consumer products and services and retail names are the best performers after Richemont and Burberry Group Plc beat expectations; utilities and insurance names are the weakest. Shares in Switzerland’s Richemont are leading the STOXX 600 and up a whopping 7% after the world’s second-largest luxury group reported string demand for jewellery and watches.That had a positive effect across the sector and France’s heavyweights, LVMH, Kering and Hermes are up and lifting the Paris CAC 40 benchmark above the floatation mark.The UK’s Burberry is another strong performer, rising close to 5% as the luxury brand said annual profit would beat market expectations. The retail sector was also on a roll, rising over 2% with Spain’s Inditex leading the pack after Goldman Sachs upgraded the stock due to resilient earnings and cashflow. Marks & Spencer, Zalando and Kingfisher were all rising over 2%.

Earlier in the session, risk aversion deepened in stock markets across Asia on Wednesday as bond yields remained elevated, with investors trying to gauge the timing and scope of the Federal Reserve’s anticipated interest-rate hikes. The MSCI Asia Pacific Index slid as much as 1.5%, heading for a five-day slump, as tech and consumer-discretionary stocks furthered recent declines. Sony Group and Toyota Motor were among the biggest drags on the gauge. Energy shares climbed, even as the oil rally eased in Asia. Quantitative tightening may exert capital-outflows pressure on Asia, “which may theoretically lead to compression in asset valuations,” Nomura strategists including Chetan Seth wrote in a note. Given that valuations are currently modest, Asian stocks will not face as significant a de-rating as they did when the Fed tightened in 2017-2018, they added. Higher yields have damped investor appetite for global equities, particularly hitting richly valued tech shares. Asian firms are also weighed down by concerns over China’s economy. Still, the yield spike isn’t all bad for stocks, as “the sum total of expected rate hikes remains low,” BlackRock Investment Institute strategists wrote in a note. Japan’s stock benchmarks were the worst performers in Asia on Wednesday, with the Topix a whisker away from technical correction as Tokyo and other parts of the nation prepare to come under a state of quasi-emergency for three weeks starting Friday. Hong Kong-listed tech stocks capitulated ahead of a Reuters report in the late afternoon about China slapping new curbs on investment deals for the industry’s largest firms. Equity losses were relatively limited in mainland China, where the central bank pledged to use more monetary-policy tools.

Japanese equities fell and the yen strengthened amid extended global risk-off trading on concerns over expected Federal Reserve monetary tightening. Electronics and auto makers were the biggest drags on the Topix, which was down 3% as of 2:37 p.m. in Tokyo, with all 33 industry groups in the red. Tokyo Electron Ltd was the largest contributor to a 3% loss in the Nikkei 225 Stock Average. Sony Group Corp. dropped more than 12% after rival Microsoft Corp. announced it will acquire Activision Blizzard Inc. The Japanese currency gained 0.3% against the dollar. After initial enthusiasm following the Bank of Japan’s decision to maintain policy, Japanese stocks swung to a loss Tuesday amid regional concerns after U.S. Treasury yields spiked. U.S. stocks dropped overnight as speculation grew that central banks will have to boost interest rates sooner than earlier anticipated. “There’s market jitters over the possibility of a U.S. rate hike taking place earlier than March,” said Mitsushige Akino, a senior executive officer at Ichiyoshi Asset Management Co. “The level of market uncertainty is high and share price swings are likely to continue into March, until there’s clarity on the Fed’s monetary policy steps.” Meanwhile, the greater Tokyo region and other parts of Japan are set to come under a state of quasi-emergency for three weeks starting Friday as the government tries to rein in a surge in Covid-19. Tokyo will seek to have bars and restaurants close early, national broadcaster NHK said.

In Australia, the S&P/ASX 200 index fell 1% to 7,332.50, closing at its lowest level since Dec. 20. Global stocks dropped as Treasury yields soared on bets that central banks will have to boost interest rates earlier than expected. Yields in Australia and New Zealand also climbed. READ: Kiwi Dollar, Yields Jump on ANZ Rate View: Inside Australia/NZ Megaport was the worst performer on Australia’s benchmark after it reported 2Q sales results. Harvey Norman was among the top performers after it was upgraded at Credit Suisse. In New Zealand, the S&P/NZX 50 index fell 1.6% to 12,612.31, marking its worst session in almost a year

In rates, Treasury yields remained cheaper on the day despite futures rebounding sharply from session lows. Yields higher by 1bp-2bp across the curve and most spreads within a basis point of Tuesday’s close; 10-year 1.885% after topping 1.90% for first time since January 2020, while in Europe, bund yields climbed above zero for the first time since before the pandemic. Treasury coupon sales resume with $20b 20-year bond reopening. $20b 20-year bond reopening at 1pm ET follows small tails for last week’s 10- and 30-year auctions; a $16b 10-year TIPS new issue is slated for Thursday. German 2s10s steepen ~2bps with 10y bund yields turning slightly positive. Gilts bear-flatten, cheapening as much as 8bps across the curve after a hot inflation print; OIS rates price ~24bps of tightening for the Feb. BOE meeting. Cash USTs bear-flatten slightly.

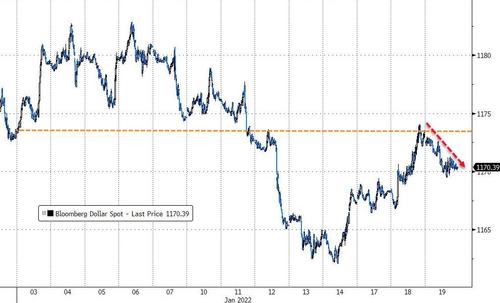

In FX, Bloomberg dollar spot drops 0.25%, slightly extending Asia’s weakness, and the dollar was steady-to-weaker against all of its Group-of-10 peers. The Norwegian krone and Canadian dollar rallied as oil prices continued to rise while New Zealand’s dollar gained and the nation’s short-end yields climbed after ANZ economists said they now expect the RBNZ’s official cash rate to peak at 3% by April 2023, up from a prior projection of 2% in 2H 2022. The pound inched up amid broad dollar weakening while the yield on 10-year Gilts soared through 1.30% following a report showing that Britain’s inflation rate surged unexpectedly to the highest since 1992. The euro inched up following yesterday’s deep loss versus the dollar; the rate on 10-year Bunds rose four basis points to 0.02%, crossing above zero for the first time since May 2019. The yen pared an advance as European stocks rebounded from opening losses. Commodity currencies lead broad gains against the dollar in G-10. ZAR leads in EMFX after Dec. inflation data nears the top of SARB’s target range.

In commodities, crude futures drift back up toward session highs after an early dip. WTI is up over 1% after finding support near $86, Brent regains $88. Spot gold pushes slightly higher, adding $3 near $1,817/oz. LME copper outperforms in a broadly positive base metals complex; tin lags.

Looking at the day ahead, data releases include the UK and Canada’s CPI reading for December, along with US housing start and building permits for December. Central bank speakers include BoE Governor Bailey, Deputy Governor Cunliffe and the ECB’s Holzmann. Finally, earnings releases include UnitedHealth Group, Bank of America, Procter & Gamble, Morgan Stanley, Charles Schwab, US Bancorp and United Airlines.

Market Snapshot

- S&P 500 futures down 0.1% to 4,565.50

- STOXX Europe 600 little changed at 479.76

- MXAP down 1.3% to 191.05

- MXAPJ down 0.5% to 628.97

- Nikkei down 2.8% to 27,467.23

- Topix down 3.0% to 1,919.72

- Hang Seng Index little changed at 24,127.85

- Shanghai Composite down 0.3% to 3,558.18

- Sensex down 1.0% to 60,142.26

- Australia S&P/ASX 200 down 1.0% to 7,332.50

- Kospi down 0.8% to 2,842.28

- Brent Futures up 1.1% to $88.45/bbl

- Gold spot up 0.2% to $1,817.04

- U.S. Dollar Index down 0.13% to 95.61

- German 10Y yield little changed at 0.01%

- Euro up 0.2% to $1.1343

- Brent Futures up 1.1% to $88.44/bbl

Top Overnight News from Bloomberg

- China’s central bank pledged to use more monetary policy tools to spur the economy and drive credit expansion, sending its clearest signal yet of an easing bias to boost market confidence

- The European Central Bank’s inflation forecasts aren’t a “blind certitude” and the institution will take action if the price surge proves more persistent, Bank of France Governor Francois Villeroy de Galhau said

- A group of rookie Tory MPs gathered on Tuesday to discuss whether there was any appetite to move together against the prime minister, several lawmakers said

- Oil held gains above the highest close since 2014 as the International Energy Agency said the market looked tighter than previously thought, with demand proving resilient to omicron. Some in the market now think it’s now a question of when — not if — oil hits triple digits

- The Cyberspace Administration of China is drafting new guidelines that will require any company with more than 100 million users or over 10 billion yuan ($1.6 billion) in revenue to seek the watchdog’s approval before such deals, Reuters reported. Any internet firm in sectors named on a “negative list” issued last year will also require approval, the news agency said

A more detailed look at global markets courtesy of Newqsuawk

Asian stocks followed suit to the losses on Wall St where all major indices declined led by tech and growth as US yields climbed to two-year highs and with financials also hit following earning releases in which Goldman Sachs and Charles Schwab both missed on their bottom lines. ASX 200 (-1.0%) traded lower in which tech mirrored the underperformance of the sector stateside as Nasdaq 100 futures dipped into correction territory after shedding 10% from its November peak and with BHP failing to benefit from an increase in its quarterly iron ore and petroleum output as the mining giant also reported a decline in coal production and warned of short-term disruptions from next month’s proposed easing of Western Australia border restrictions. However, the energy sector was buoyed by continued advances in oil prices due to the geopolitical risk premium and after an explosion in Turkey forced the shutdown of the Iraq-Turkey crude oil pipeline which is Iraq’s largest crude oil export line. Nikkei 225 (-2.8%) was heavily pressured by recent currency strength and with Japan set for tighter COVID-19 restrictions in key areas including Tokyo, while Toyota and Sony were the notable laggards after the automaker flagged a miss to its output targets due to chip shortages and with Sony impacted by news that rival Microsoft is to acquire video game publisher Activision. Hang Seng (U/C) and Shanghai Comp. (-0.4%) were choppy and initially fared better than their regional peers after the PBoC continued with its liquidity efforts and recently hinted of more easing, but with upside restricted amid reports of further scrutiny by the US on Chinese businesses including an examination into Alibaba’s cloud unit to determine if it poses a risk to US national security. Finally, 10yr JGBs were kept afloat amid the broad risk aversion in Tokyo although gains in JGBs were gradual as T-note futures remained pressured by a further rise in yields and following slightly weaker demand at the enhanced liquidity auction for 2yr-20yr JGBs.

Top Asian News

- Sunac China Dollar Bonds’ Record Surge Approaches 20 Cents

- Hamsters, Wings, Shrimp Ensnared by China’s Covid Zero Zeal

- China’s Sinopec Floods LNG Spot Market with Cargoes for 2022

- Tokyo to Press Bars to Close Early as Covid Cases Hit Record

Major bourses in Europe are now mostly in positive territory (Euro Stoxx 50 +0.5%; Stoxx 600 +0.3%) as the region recovered from the losses seen at the cash open – which saw the Euro Stoxx 50 and DAX 40 open lower by 0.5% and 0.8% respectively. US equity futures have also nursed earlier losses and now reside in positive territory, with the NQ recuperating from losses of over 1.0% at one stage as the US 10yr cash yield eclipsed 1.90% and the German 10yr yield turned positive for the first time in over three years. Back to cash equities, the CAC (+0.6%) and IBEX (+0.6%) outperform amid their large retail exposure, with the sector bolstered after stellar updates from Richemont (+9.1%) and Burberry (+6.0%) coupled with a broker upgrade for Inditex (+3.5%) at Goldman Sachs; in turn lifting the likes of LVMH (+3.0%) and Kering (+3.3%). Delving deeper into the sectors, the earlier defensive bias has evolved into a more cyclical one, with Basic Resources, Travel & Leisure and Retail at the top of the bunch, whilst Healthcare and Food & Beverages make their way down the ranks. Tech has recovered from its earlier yield-induced underperformance with the aid of a post-earnings ASML (+1.1%) which missed on net sales expectations, but the group announced a 100% Y/Y increase in its dividend, whilst the CEO suggests their production capacity cannot accommodate higher demand. For reference, ASML accounts for around 7.5% of the Euro Stoxx 50. In terms of other individual movers, Leoni (-14.0%) slumped as Co. sites were searched by the German Federal Cartel Office as part of an investigation into various cable manufacturers and other industry-related companies.

Top European News

- Richemont, Burberry Signal That Luxury Market Is Thriving

- Airbus Gears Up for Growth With Plans to Add 6,000 New Staff

- 5G Rollout Disrupts Flights Into U.S. From Across the World

- Hamsters, Wings, Shrimp Ensnared by China’s Covid Zero Zeal

In FX, sterling remains somewhat caught between stalls after stronger than forecast UK CPI readings that add more weight to expectations and pricing for further BoE policy normalisation, but cautious about carrying too much rate hike premium given the growing prospect of change at the highest level in Government and the rising rebellion against Tory Party leader Boris Johnson. Hence, the post-data pop above 1.3600 in Cable was relatively limited and short-lived, while Eur/Gbp only dipped marginally within a tight 0.8342-23 range before stabilising. However, the Pound is holding off Tuesday’s lows vs the Dollar by virtue of the fact that the Greenback has faded generally and topped a key Fib retracement level at 1.3610 as the index slips back a bit further towards 95.500 having reached 95.832 at best yesterday and consolidating between 95.792-549 ahead of US housing data and the 20 year auction.

- NZD/AUD – In contrast to Sterling, the Kiwi has no political inhibitions on the domestic front inhibitions and is outperforming amidst hawkish RBNZ calls from ANZ Bank, as Nzd/Usd bounces from overnight lows towards the psychological 0.6800 mark and the Aud/Nzd cross retreats through 1.0600 again. To recap, ANZ expects a 25 bp hike at every meeting from February to April 2023 that would push the OCR up to 3% from the current 75 bp. Meanwhile, the Aussie is lagging in wake of a fall in Westpac consumer sentiment and in advance of more pivotal jobs data tomorrow, albeit with Aud/Usd also off worst levels within a 0.7177-0.7214 band following a strong rise in iron ore prices.

- CAD/CHF/EUR/JPY – All recouping some lost ground against the Buck, and the Loonie still getting a lift from crude as WTI extends its heady rise to probe Usd 87/brl, while the Franc is approaching 0.9150 from sub-0.9175 and remains above 1.0400 vs the Euro even though Eur/Usd has regained enough poise to retest offers/resistance into 1.1350, including the 21 DMA that comes in at 1.1347 today (and incidentally matches Tuesday’s 55 DMA). Elsewhere, the Yen is rather betwixt and between on respective UST/JGB yield and broad risk grounds, as Usd/Jpy pivots 114.50 before Japanese inflation on Thursday. Back to Usd/Cad, Canadian CPI looms and could either compound BoC tightening perceptions or undermine, while the near term technical backdrop is basically flanked by resistance around 1.2550 and support circa 1.2450 beyond the current 1.2525-1.2472 bounds.

In commodities, WTI and Brent front month futures remain elevated following an initial blip lower in early European hours – which at the time emanated from reports that the Iraq-Turkey pipeline will resume oil flows after an explosion yesterday – said to have been an accident as opposed to an attack, which had been feared. The explosion was the cited driver behind yesterday’s rise in crude, with WTI Feb reaching a USD 86.41/bbl high and Brent March a peak of USD 89.05/bbl before waning off best levels. Nonetheless, prices see tailwinds in European trade as equities recovered off lows and following the IEA Monthly Oil Market report which raised its global demand growth forecast and suggested Omicron has had less of an impact than initially expected. Furthermore, the report suggested that OPEC+ effective spare capacity will be just 2.6mln BPD in H2-2022, “held primarily by Saudi Arabia and the UAE.” Saudi Arabia has usually kept more than 1.5-2mln BPD of spare capacity on hand for market management, according to the EIA. Elsewhere, spot gold has been driving higher as the Dollar remains near lows, with the yellow metal finding some support around USD 1,810/oz. LME copper meanwhile is on the front-foot and prices have extended on their APAC gains as stocks trim earlier losses, whilst mining giant Antofagasta sees the demand picture for the red metal continuing. Elsewhere, Indonesia has not issued any export permits for tin for 2022, according to a commodity exchange official.

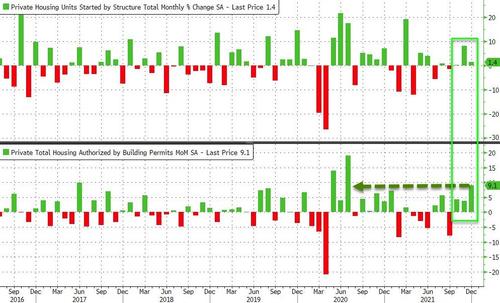

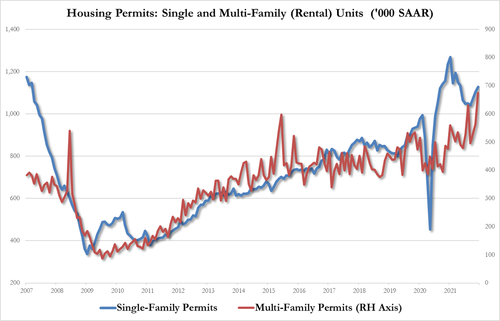

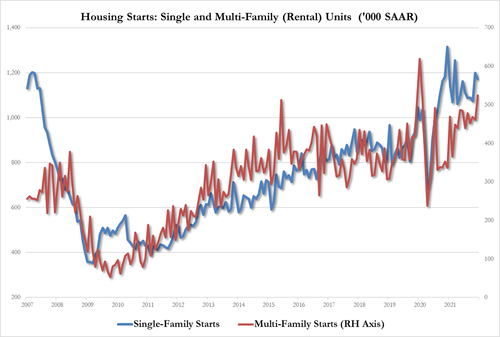

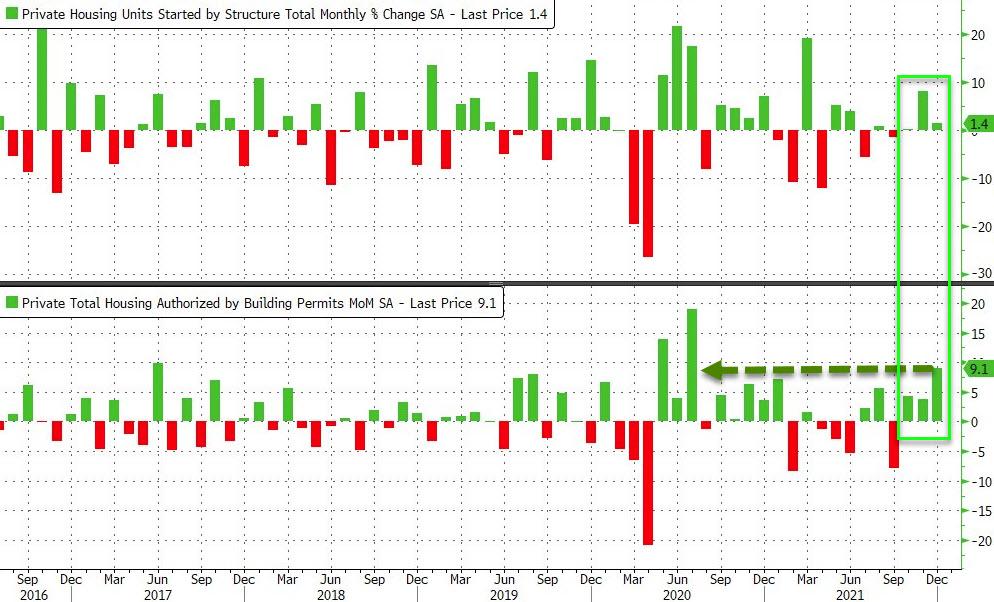

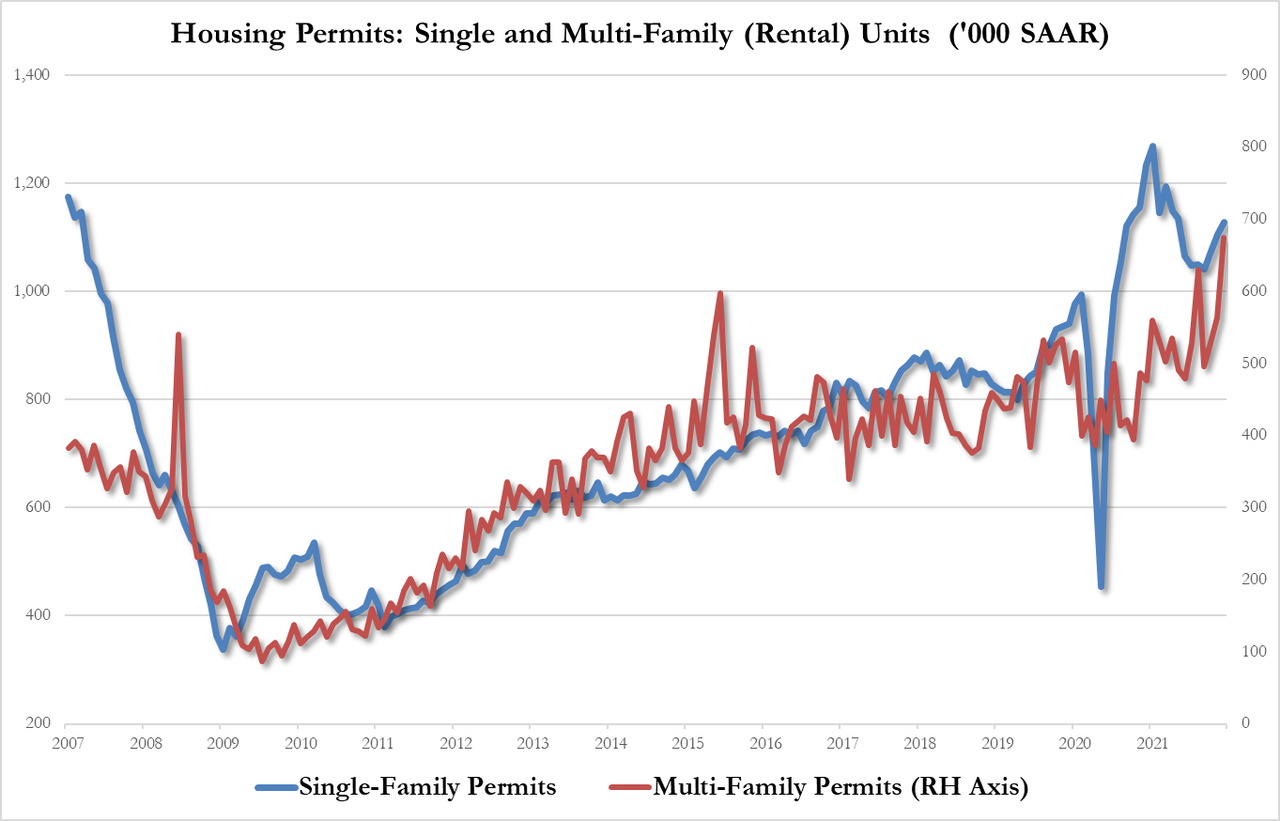

US Event Calendar

- 7am: Jan. MBA Mortgage Applications, prior 1.4%

- 8:30am: Dec. Building Permits MoM, est. -0.8%, prior 3.6%, revised 3.9%

- 8:30am: Dec. Housing Starts MoM, est. -1.7%, prior 11.8%

- 8:30am: Dec. Building Permits, est. 1.7m, prior 1.71m, revised 1.72m

- 8:30am: Dec. Housing Starts, est. 1.65m, prior 1.68m

DB’s Jim Reid concludes the overnight wrap

Yesterday we published our latest global monthly survey. It was a more bearish survey than last month, with the majority of respondents reacting more negatively on bonds and equities than they did in December. Higher-than-expected inflation remains the biggest risk, with Fed policy alongside this. Covid-related risks again dropped out of the top three after re-entering last month with Omicron. Respondents thought the policy risk was towards the Fed being too hawkish, while the risk from the ECB was towards the top dovish direction. An overwhelming majority think the next 25bp move in 10yr Treasuries is higher, with the average respondent edging up their year-end yield target for both Treasuries and Bunds. The average expected S&P 500 return also dropped more than a percent point to around 3% for 2022. The bearish tilt to this month’s survey ended with the latest US recession forecasts. 73% of respondents thinking the next US recession will hit by 2024, up from 63% last month. See the full report here

I appreciate the average reader doesn’t want to hear about my latest injuries but part of the payback for being subscribed is you have to partly act as my therapist. Yesterday I got the results of my latest knee scan. A chunk has come off my knee cartilage leaving a pothole. I ironically did this whilst doing gentle squats and lunges whilst rehabbing my other knee after surgery in December. My surgeon has suggested more microfracture which will be another 6 weeks on crutches and no weight bearing. It was giving way around once a day over Xmas but has calmed down a bit and is just stiff now, indicating that the broken piece has been absorbed leaving just the hole. My dilemma is whether to just get it done asap and move on or wait until towards the end of the year. The risk being that the “pothole” will likely get bigger. All advice from those having gone through this gratefully received. Meanwhile I think I have sciatica in my back as I’m experiencing searing nerve pain in my hip that is starting to go down my leg. The latest scan results when they come in might help identify the problem that my consultant can’t exactly pinpoint. I’m not sure what’s more likely, Tiger Woods playing at the Masters in April or me in the monthly medal at my club this weekend.

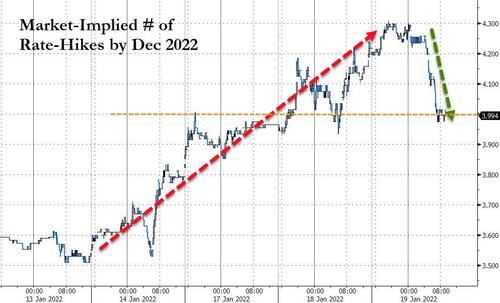

Sovereign bonds and equities landed deep in the rough yesterday, as the hawkish drumbeat in markets grew louder, with investors increasingly pricing in tighter monetary policy over the coming months. In fact, a number of fresh milestones were reached over the last 24 hours alone, and a notable one was that Fed funds futures are now pricing in at least 4 full hikes in 2022 for the first time. For reference, it’s been little more than a month since the FOMC released their dot plot in December, and back then just 2 of the 18 members signalled they were in favour of 4 hikes this year, with all the others expecting 3 or less.

While the Fed is naturally gaining the most attention, this hawkish pivot is being echoed right across the advanced economies, with imminent hikes expected in multiple countries. Looking at overnight index swaps, they’re currently pricing a +92% chance of a hike at the BoE’s next meeting in early February, an 82% chance of one at the Bank of Canada’s meeting next week, and are fully pricing in one at the Reserve Bank of New Zealand’s next meeting as well. The UK CPI just after we go to press will be the next central bank hiking pricing hurdle.

As markets moved to price in more and more tightening, US Treasuries sold off as they caught up following the previous day’s holiday, and the 10yr yield followed up 4 consecutive weekly gains by rising another +8.9bps to a 2-year high of 1.87%. Front-end yields also moved higher, with the 2yr yield up +7.6bps to close above 1% for the first time since the pandemic began. As has generally been the case this year, that move was driven by higher real rates, with the rise in the 10yr real yield leaving it at its highest level since last April, at -0.62%, while the 30yr real yield is now just 6bps from crossing into positive territory for the first time since last spring.

Over in Europe, there were similar moves higher in sovereign bond yields, with those on 10yr bunds (+0.7bps) closing at -0.02%, also nudging closer to positive territory than at any point since May 2019. That said, the growing divergence in policy expectations between the Fed and the ECB meant there was a further widening in the spread between 2yr yields on US and German debt, and yesterday saw the spread widen to a post-pandemic high of 162bps. Elsewhere in Europe, yields on 10yr gilts (+3.1bps) hit their highest since May 2019 as well, whilst those on 10yr OATs (+1.3bps) hit a post-pandemic high.

The prospect of a more rapid pace of hikes sent US equities to their lowest levels so far this year, with the S&P 500 (-1.83%) experiencing a broad-based decline that left just 58 companies in the index in the green for the day. Over the last year, there’s only been 9 days with fewer stocks advancing. Tech stocks underperformed yet again, with the NASDAQ down a further -2.60%, which in turn brings its decline since its all-time high in November to over -9%, so not far off a -10% correction. And against this backdrop, the VIX index of volatility rose +3.7pts to 22.9pts, its highest level so far this year, albeit still some way beneath its peak above 30 that it reached shortly after the news of the Omicron variant arrived. European equities struggled too, with the STOXX 600 down -0.97%.

To the extent one believes the recent equity market performance is driven by tighter central bank policy, which will be reversed should enough pain be endured (the proverbial Fed put, as it were), the problem in this cycle is that inflation will make that more troublesome. So the last 40 years of the central bank put could be severely tested before this cycle is out.

The one sector in the S&P 500 that actually ended the day in positive territory yesterday was energy (+0.40%), having been bolstered by a fresh rise in oil prices that took them to their highest levels since 2014. By the close, Brent Crude (+1.19%) had surpassed $87/bbl, whilst WTI (+1.92%) was above $85/bbl, which won’t be welcome news for policymakers who’d been hoping for some respite on the inflation front. The latest surge has had a number of drivers, one of which is that the Omicron variant proved much less severe than initially feared and helped prices recover their losses from late November when they fell into the mid-$60s. Separately, a drone attack in the UAE on oil facilities has alerted investors to supply-side risks, which comes amidst production outages elsewhere. Oil has again found support in the Asian session after a key pipeline that brings crude from Iraq to Turkey was knocked down by an explosion adding to supply concerns.

While financials have benefitted from the recent run higher in yields, their fourth quarter earnings have been a bit underwhelming so far. Six financials reported yesterday and only one beat on both earnings and sales estimates. A common finding among financials reporting thus far is that trading revenues were lower in the fourth quarter while expenses were higher. So the sector has stalled after the good start to the year on the higher rates/yields story.

Overnight in Asia, major bourses across the region are trading lower again led by the Nikkei (-2.27%) after Toyota Motor’s (-4.7%) sharp decline as the company warned that it would be very difficult to meet its production target for this fiscal year due to supply-chain constraints. Sony Corporation fell as much as -10.0% in Tokyo, recording its biggest intraday drop in almost two years following Microsoft’s Activision Blizzard deal worth $69 billion. Elsewhere the Kospi (-0.47%), CSI (-0.58%) and Shanghai Composite (-0.30%) are moving lower. However the Hang Seng Index (+0.02%) is holding in better.

Looking forward, stock futures in the DM world are indicating that the declines will continue with the S&P 500 (-0.67%), Nasdaq (-0.89%) and DAX (-0.67%) all trading in the red.

Back to yesterday and on the data front, UK unemployment fell to a post-pandemic low of 4.1% in the three months ending in November (vs. 4.2% expected). Meanwhile in Germany, the January ZEW survey saw the expectations component rise to a 6-month high of 51.7 (vs. 32.0 expected), although the current situation fell back to an 8-month low of -10.2 (vs. -8.8 expected). Finally in the US, the Empire State manufacturing survey for January fell to -0.7 (vs. 25.0 expected), and the NAHB’s housing market index fell to 83 (vs. 84 expected).

To the day ahead now, and data releases include the UK and Canada’s CPI reading for December, along with US housing start and building permits for December. Central bank speakers include BoE Governor Bailey, Deputy Governor Cunliffe and the ECB’s Holzmann. Finally, earnings releases include UnitedHealth Group, Bank of America, Procter & Gamble, Morgan Stanley, Charles Schwab, US Bancorp and United Airlines.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 11.73 PTS OR 0.33% //Hang Sang CLOSED UP 15.03 PTS OR 0.06% /The Nikkei closed DOWN 790.02 PTS OR 2.80-% //Australia’s all ordinaires CLOSED DOWN 1.02% /Chinese yuan (ONSHORE) closed UP 6.3468 /Oil UP TO 86.08 dollars per barrel for WTI and UP TO 87.86 for Brent. Stocks in Europe OPENED ALL GREEN EXCEPT ITALY // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3468. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3504: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING STRONGER AGAINST USA DOLLAR

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

3B JAPAN

end

3c CHINA

CHINA/COVID

4/EUROPEAN AFFAIRS

//GERMANY//NORDSTREAM II

Germany threatens Russia that if they enter the Ukraine, the will halt all Nordstream 2 passage

(zerohedge)

Germany Threatens To Halt Nord Stream 2 If Russia Attacks Ukraine

WEDNESDAY, JAN 19, 2022 – 05:45 AM

On Tuesday German Chancellor Olaf Scholz was asked directly in a press Q&A whether a Russian military offensive in Ukraine might lead to NATO military intervention on behalf of Kiev.

Scholz responded by underlining “serious” political and economic consequences, but appeared to rule out any assistance from Germany on the military front, saying there won’t be arms deliveries either. But importantly, he said that Berlin would mull halting the flow of natural gas from Russia.

“Germany may consider halting the Nord Stream 2 pipeline if Russia attacks Ukraine, Chancellor Olaf Scholz signaled on Tuesday, as pressure grew on his government to take a more hawkish stance on the Kremlin,” Reuters reports of the statements made after he met with NATO Secretary-General Jens Stoltenberg.

The ‘options on the table’ would include sanctioning the pipeline as well. Though amid already soaring energy prices in a frigid European winter, this ‘option’ would at the same time involve Germany shooting itself in the foot, if urgent supply needs can’t be met elsewhere.

“It is clear that there will be a high price to pay and that everything will have to be discussed should there be a military intervention in Ukraine,” Scholz said.

But the chancellor added: “We are not interested in long-term tensions, quite the contrary. But it is also important that everyone adheres to the principles that we have agreed on, and this means that Russia must adhere to the principles of the OSCE [the Organization for Security Co-Operation in Europe].”

He called for Russia to reduce its troop presence near Ukraine, while highlight that both Russia nad Germany desire to maintain “constructive and stable relations.”

Germany has long been engaged in a tightrope balance of sorts on Russia – on the one hand pushing through the €10 billion, over 1,200km long gas transit pipeline which bypasses Ukraine and Poland – while on the other seeking to satisfy its impatient powerful Western ally, the US.

Commenting on this, Reuters notes that “Some observers say he is sending mixed signals by calling the pipeline, which has already been built but not yet approved for operation, a private commercial project that should not be singled out for sanctions.”

In remains, meanwhile, that Russia holds on the leverage on the energy front when it comes to any potential Europe attempts to strike out with punitive measures…

end

Bund Yields Turn Positive For First Time In 3 Years, USTs Bounce Off Critical Support

WEDNESDAY, JAN 19, 2022 – 08:31 AM

German 10Y yields climbed above zero for the first time since May 2019 just as money markets brought forward bets on a 10-basis-point European Central Bank rate hike to September from October previously. Traders expect that by the end of next year, the policy rate will no longer be negative.

But, as Bloomberg’s Ven Ram notes, the key things to watch out for will be how sustainable the move is, how much of a tightening in financial conditions the ECB will tolerate (it may yet take a sanguine approach if Treasury yields continue to trek higher) and where the near-term top for yields is (my expectation is around 0.15%-0.20% — though this isn’t a year-end target). It would be a surprise if the ECB were to allow bund yields to climb all the way to where they need to be. Notice also that the 10-year swap rate is around 0.41%, closer to the implied level on bunds.

However, the two-year yield is still trailing the benchmark deposit rate. That nonchalance at the front end of the curve may yet continue given that the ECB is unlikely to raise rates this year, setting us up nicely for further curve steepening.

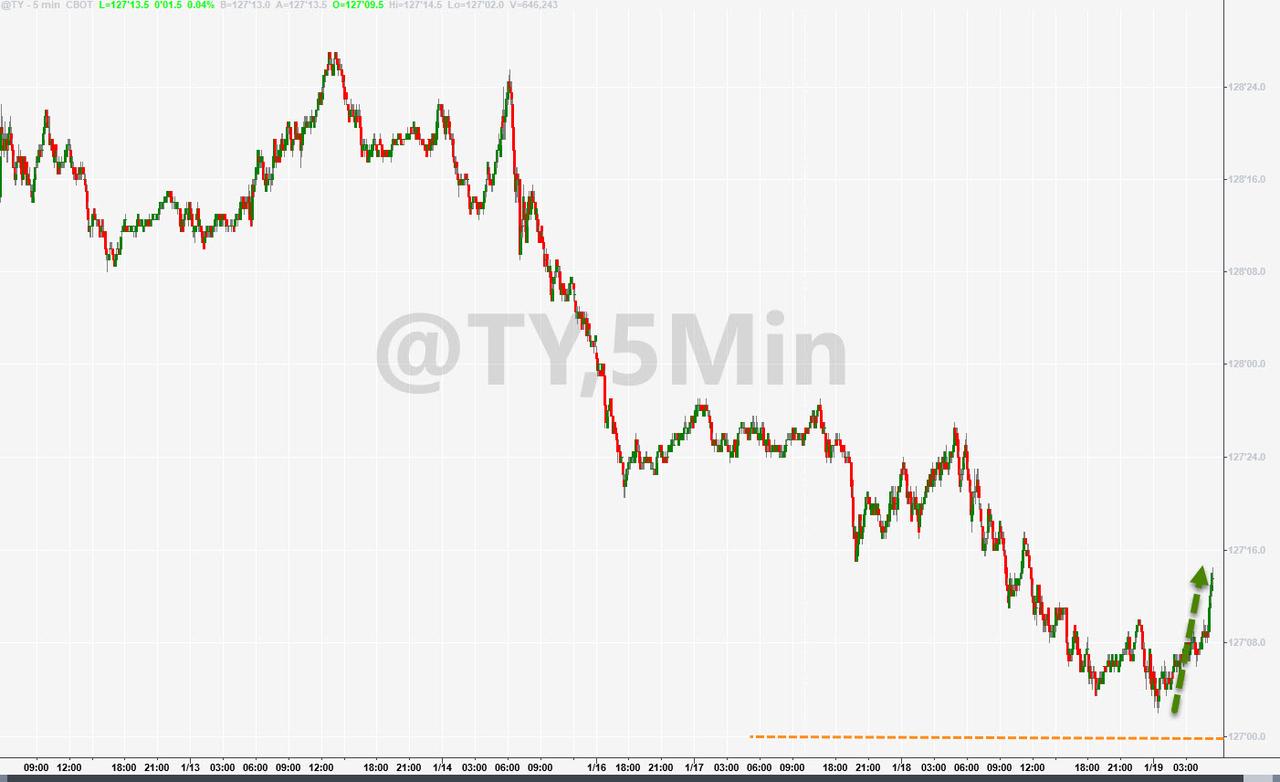

Meanwhile, US Treasuries are suddenly bid – after some weakness overnight – as the 10Y Future tagged the $127 level we warned about yesterday as critical and reversed rapidly.

As Nomura’s Charlie McElligott noted: the most critical security “level” in global markets right now is 127 in UST 10Y Treasury Futs (TYH2), because the Street is short just a massive amount of downside struck there in TYH2 Puts, with 321,729 of OI (while we continue blowing-through downside strikes of all levels, most notably the TYH2P 127.5 level and its 140,579 of OI and the 128 strike’s 105,818 of OI); if that 127 level goes, the potential for a “short gamma / negative convexity” event grows substantially on Dealer hedging “accelerant” flows.

And that reversal (from 1.90% – which is equiv to $127 in Futs) is accelerating…

Is this a pause that refreshes in the rates surge?

“It’s a done deal that 10-year Treasuries hit 2%, but the selloff is likely to slow for a bit then,” said Damien McColough, head of fixed-income research at Westpac Banking Corp. in Sydney.

“Yields will definitely go higher still once the Fed delivers its first hike.”

However, an extended spike in yields could spur the Fed to move to reassure markets, according to Resona Asset Management.

“I don’t expect 10-year U.S. Treasury yields to keep rising on and on beyond 2%,” said Mamoru Shimode, chief strategist at Resona.

“That’s unlikely to be something that the Fed will tolerate.”

Everyone and their pet rabbit is short bonds here, so perhaps the pain trade in the short-term is indeed lower in yield.

end

UK/COVID/VACCINE MANDATE

England Ends All COVID Passports, Mask Mandates, Work Restrictions

WEDNESDAY, JAN 19, 2022 – 12:45 PM

By Lily Zhou of the Epoch Times

Restrictions including COVID-19 passes, mask mandates, and work-from-home requirements will be removed in England, UK Prime Minister Boris Johnson announced on Wednesday. Johnson also suggested that self-isolation rules may also be thrown out at the end of March as the CCP (Chinese Communist Party) virus pandemic becomes endemic.

Effective immediately, the UK government is no longer asking people to work from home. The COVID pass mandate for nightclubs and large events won’t be renewed when it expires on Jan. 26. And from Thursday, indoor mask-wearing will no longer be compulsory anywhere in England.

The requirement for secondary school pupils to wear masks during class and in communal areas will also be removed from the Department for Education’s national guidance.

Roaring cheers from lawmakers could be heard in the House of Commons following Johnson’s announcements on masks.

People who test positive for COVID-19 and their unvaccinated contacts are still required to self-isolate, but Johnson said he “very much expect[s] not to renew” the rule when the relevant regulations expire on March 24.