JAN 25//

GOLD; UP $10.40 to $1851.95

SILVER: $23.87 UP 10 CENTS

ACCESS MARKET: GOLD: 1848.20..

SILVER: $23.83

Bitcoin: morning price: 36,410 up 1834

Bitcoin: afternoon price: 36,737 up 2161

Platinum price: closing up $6.45 to $1030.15

Palladium price; closing up $50.50 at $2201.90

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filed COMEX//NOTICES: 0/0

FILED zero

NUMBER OF NOTICES FILED TODAY FOR JAN. CONTRACT: 0 NOTICE(S) FOR nil OZ (0.00000 TONNES)

total notices so far: 5651 contracts for 565,100 oz (17.577 tonnes)

SILVER NOTICES:

17 NOTICE(S) FILED TODAY FOR 85,000 OZ/

total number of notices filed so far this month 2856 : for 14,280,000 oz

GLD

WITH GOLD UP $10.40

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS): NO CHANGES IN GOLD INVENTORY AT THE GLD

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

CLOSING INVENTORY: 1008.45 TONNES/

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 10 CENTS:/: ANOTHER HUGE CHANGE IN SILVER INVENTORY INTO THE SLV/ A DEPOSIT OF 2.311 MILLION OZ INTO THE SLV

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY SLV/ TONIGHT: 535.003 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUMONGOUS 3066 CONTRACTS TO 148,932 AND RESTS FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THIS HUGE LOSS IN OI WAS ACCOMPANIED WITH THE STRONG $0.48 DROP IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.48) AND WERE SUCCESSFUL IN KNOCKING OUT SOME SILVER LONGS AS WE HAD A HUGE LOSS OF 3066 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A ZERO ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 10.505 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUEUE. JUMP //NEW STANDING 14.485 MILLION OZ V) SMALL SIZED COMEX OI LOSS.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS 2896

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTACTS for 16 days, total contracts: : 14,833 contracts or 74.165 million oz OR 4.635 MILLION OZ PER DAY. (927 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 14,833 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 74.165 MILLION OZ

.

LAST 8 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3066 WITH OUR LARGE 48 CENT LOSS SILVER PRICING AT THE COMEX// MONDAY THE CME NOTIFIED US THAT WE HAD A ZERO SIZED EFP ISSUANCE OF 0 CONTRACTS( 0 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY:/ AS WELL AS TODAY /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN OF 10.505 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUEUE JUMP //NEW STANDING 14.485, MILLION OZ// .. WE HAD A HUGE SIZED LOSS OF 3066 OI CONTRACTS ON THE TWO EXCHANGES FOR 15.330 MILLION OZ//THIS IS THE FIRST TIME SINCE THE CROOKS STARTED TO USE EFP THAT WE DID HAVE ZERO EFP ISSUANCE.

WE HAD 17 NOTICES FILED TODAY FOR 85,000 OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 3730 TO 557,626 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -11,781 CONTRACTS

.

THE FAIR SIZED INCREASE IN COMEX OI CAME WITH OUR STRONG GAIN IN PRICE OF $10.15//COMEX GOLD TRADING/MONDAY/.AS IN SILVER WE MUST HAVE HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION AS THE TOTAL GAIN ON OUR TWO EXCHANGES TOTALED A GOOD SIZED 4945 CONTRACTS…

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JAN AT 3.5614 TONNES FOLLOWED BY TODAY’S 300 OZ QUEUE. JUMP//NEW STANDING: 17.629 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $10.15 WITH RESPECT TO MONDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 4945 OI CONTRACTS (15.38 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALLED A SMALL SIZED 1215 CONTRACTS:

FOR FEB 1215 ALL OTHER MONTHS ZERO//TOTAL: 1215

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 557,626.

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4945, WITH 3730 CONTRACTS INCREASED AT THE COMEX AND 1215 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4945 CONTRACTS OR 15.38TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1215) ACCOMPANYING THE HUGE SIZED GAIN IN COMEX OI (15511): TOTAL GAIN IN THE TWO EXCHANGES 16,726 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR JAN. AT 3.7262 TONNES//FOLLOWED BY TODAY’S 300 OZ QUEUE. JUMP.//NEW STANDING 17.629 TONNES 3)ZERO LONG LIQUIDATION,4) FAIR SIZED COMEX OI. GAIN 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB.WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2021 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN : 55,814 CONTRACTS OR 5,581,400 oz OR 173.60 TONNES 16 TRADING DAY(S) AND THUS AVERAGING: 3488 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES: 173.60 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 173.60/3550 x 100% TONNES 4.90% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO DATE

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//FINAL ISSUANCE//

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A HUGE SIZED 3730 CONTRACTS TO 148,932 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 0 CONTRACTS (FIRST TIME THAT THIS HAS HAPPENED SINCE INCEPTION)

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3066 CONTRACTS AND ADD TO THE 0 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF 3066 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 15.330 MILLION OZ,

OCCURRED WITH OUR $0.48 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED DOWN 91.04 PTS OR 2.58% //Hang Sang CLOSED DOWN 412.85 PTS OR 1.67% /The Nikkei closed DOWN 457.03 PTS OR 1.66% //Australia’s all ordinaires CLOSED DOWN 2.60% /Chinese yuan (ONSHORE) closed DOWN 6.3299 /Oil DOWN TO 83.79 dollars per barrel for WTI and UP TO 86.42 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3299. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3370: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING WEAKER AGAINST USA DOLLAR

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 3,730 CONTRACTS AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR GAIN OF $10.15 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A SMALL EFP (1215 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. LOOKS LIKE OUR BANKERS ARE FINALLY BAILING OUT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE NON ACTIVE DELIVERY MONTH OF JAN.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1215 EFP CONTRACTS WERE ISSUED: ;: , DEC : 0 & FEB. 1215 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1215 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED 4945 TOTAL CONTRACTS IN THAT 1215 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 3730 CONTRACTS..

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR JAN (17.629),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $10.15)

AND THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS THE TOTAL GAIN ON THE TWO EXCHANGES REGISTERED A GOOD 15.38 TONNES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JAN (17.629 TONNES)…

WE HAD A MONSTROUS – 11,781 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 4945 CONTRACTS OR 494,500 OZ OR 15.38 TONNES

Estimated gold volume today: 245,796 /// poor

Confirmed volume yesterday: 353,554 contracts fair

INITIAL STANDINGS FOR JAN ’22 COMEX GOLD //JAN 25

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 35,310.73 oz BRINKS HSBC |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 0 notice(s)00 OZ 0 TONNES |

| No of oz to be served (notices) | 17 contracts 1700 oz 0.05287 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5651 notices 565,100 OZ 17.576 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

No dealer deposit 0

No dealer withdrawal 0

0 customer deposit

total deposit: nil oz

2 customer withdrawals

i) Out of BRINKS: 34,915.980 0z

ii) Out of hsbc 394.75 oz

total withdrawals: 35,310.73 OZ oz

ADJUSTMENTS: 1

BRINKS/DEALER TO CUSTOMER: 96.45 (3 KILOBARS)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of JANUARY we have an oi of 17 stand for JANUARY GAINING 1 contract. We had 2 notices filed on MONDAY, so we GAINED 3 contracts or an additional 300 oz will stand for

gold in this very non active delivery month of January.

FEBRUARY LOST 31,134 CONTRACTS TO 112,154

March GAINED 285 contracts to stand at 3124..

We had 0 notice(s) filed today for 00 oz FOR THE JAN 2022 CONTRACT MONTH

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN /2021. contract month,

we take the total number of notices filed so far for the month (5651) x 100 oz , to which we add the difference between the open interest for the front month of (JAN: 17 CONTRACTS ) minus the number of notices served upon today 0 x 100 oz per contract equals 566,500 OZ OR 17.629 TONNES the number of TONNES standing in this NON active month of JAN. (numbers corrected from yesterday)

thus the INITIAL standings for gold for the JAN contract month:

No of notices filed so far (5651) x 100 oz+ (17) OI for the front month minus the number of notices served upon today (0} x 100 oz} which equals 565,900 oz standing OR 17.629 TONNES in this NON active delivery month of JAN.

We GAINED 3 contracts or an additional 300 oz of gold will stand for metal on this side of the pond.

TOTAL COMEX GOLD STANDING: 17.629 TONNES (HUGE FOR A JANUARY DELIVERY MONTH

IF THIS HOLDS TO THE END OF THE MONTH, THIS WILL BE THE HIGHEST EVER RECORDED GOLD STANDING FOR A JANUARY, GENERALLY A VERY POOR DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

206,468.649, oz NOW PLEDGED /HSBC 6.42 TONNES

174,041.913 PLEDGED MANFRA 5.413 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690

288,481,604, oz JPM No 2 8.97 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonne

Loomis: 18,615.429 oz

total pledged gold: 1,653,017.372 oz 51.415 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 33,581,836.107 OZ (1044,53 TONNES)

TOTAL ELIGIBLE GOLD: 16,001,295.648 OZ (497.70 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,580,540.519 OZ (546.82 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,976,154.0 OZ (REG GOLD- PLEDGED GOLD) 496.92 tonnes

END

JANUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//JAN 25

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1197,482.486 oz Brinks CNT Delaware |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 604,733.470 oz cnt Delaware |

| No of oz served today (contracts) | 17 CONTRACT(S) (85,000 OZ) |

| No of oz to be served (notices) | 41 contracts (205,000 oz) |

| Total monthly oz silver served (contracts) | 2856 contracts (14,280,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

| S |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 2 deposits

i) Into CNT: 593,717.57 oz

ii) Into Delaware: 11,015.900 oz

JPMorgan has a total silver weight: 185.232 million oz/355.125 million =52.15% of comex

ii) Comex withdrawals: 3

a) Out of CNT 819,672.797 oz

b) Out of Delaware; 3955.479 oz

c) Out of Brinks: 373,854.210 oz

total withdrawal 1197,482.486 oz

we had 1 adjustment:

Brinks/dealer to customer: 154,667.630 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 82.461 MILLION OZ

TOTAL REG + ELIG. 355.125 MILLION OZ

TOTAL NO OF CONTRACTS SERVED UPON THIS MONTH: 2838 CONTRACTS FOR 14,190,000 OZ

CALCULATION OF SILVER OZ STANDING FOR JANUARY

NUMBER OF NOTICES FILED TODAY: 1 NOTICES OR 5,000 OZ

silver open interest data:

FRONT MONTH OF JAN//2022 OI: 58 CONTRACTS LOSING 1 contract on the day

We had 2 notices filed for MONDAY so we GAINED 1 contracts or 5,000 additional oz will stand for delivery in this non active delivery month of January.

FOR FEB WE HAD A LOSS OF 22 CONTRACTS UP TO 577

FOR MARCH WE HAD A LOSS OF 2896 CONTRACTS UP TO 113,039 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 17 for 85,000 oz

Comex volumes: 54,476// est. volume today//fair

Comex volume: confirmed YESTERDAY: 76,050 contracts (good)

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 2856 x 5,000 oz =. 14,280,000 oz

to which we add the difference between the open interest for the front month of JAN (58) and the number of notices served upon today 17 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JAN./2021 contract month: 2856 (notices served so far) x 5000 oz + OI for front month of JAN (58) – number of notices served upon today (17) x 5000 oz of silver standing for the JAN contract month equates 14,485,000 oz. .

We GAINED 1 contracts or an additional 5,000 oz will stand for delivery on this side of the pond.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

GLD

JAN 25/WITH GOLD UP $10.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 24/WITH GOLD UP $10.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: AN UNBELIEVABLE DEPOSIT OF 27.59 TONNES INTO THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 21/WITH GOLD DOWN $10.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 980.86 TONNES

JAN 20/WITH GOLD UP $.20 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 980.86 TONNES

JAN 19/WITH GOLD UP $29.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 5.27 TONNES INTO THE GLD/INVENTORY RESTS AT 981.44 TONNES

JAN 18/WITH GOLD DOWN $3.25//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 14/ WITH GOLD DOWN $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 13/WITH GOLD DOWN $5.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 12/WITH GOLD UP $8.65//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 11/WITH GOLD UP $19.25/A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FROM THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 10/WITH GOLD UP $2.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.08 TONNES

JAN 7/WITH GOLD UP $8.15//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWLA OF 1.16 TONNES FROM THE GLD////INVENTORY RESTS AT 978.83 TONNES

JAN 6/WITH GOLD DOWN $35.30//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .32 TONNES/INVENTORY RESTS AT 979.99 TONNES

JAN 5/WITH GOLD UP $10.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 980.31 TONNES

Jan 4/WITH GOLD UP $14.00//A HUGE CHANGE OF 4.65 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 980.31 TONNES

JAN 3/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 31/WITH GOLD UP $14.05 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 30/WITH GOLD UP $7.75 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 29/WITH GOLD DOWN $5.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 975.66 TONNES

DEC 28/WITH GOLD UP $2.00 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 973.63 TONNES

DEC 27/WITH GOLD DOWN $2.05: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.63 TONNES.

DEC 23/WITH GOLD UP $9.85 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.94 TONNES FROM THE GLD/// INVENTORY RESTS AT 973.63 TONNES

DEC 22/WITH GOLD UP $12.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 21/WITH GOLD DOWN $7.05 TODAY, NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 20/WITH GOLD DOWN $9.65 TODAY; A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.37 TONNES INTO THE GLD///INVENTORY RESTS AT 977.20 TONNES

DEC 17/WITH GOLD UP $7.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.20 TONNES

CLOSING INVENTORY: 1008.45 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SLV

JAN 26/WITH SILVER UP 10 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.311 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 535.003 MILLION OZ/

.JAN 24/WITH SILVER DOWN 48 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.8 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 532.692 MILLION OZ//.

JAN 21/WITH SILVER DOWN 41 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 527.792 MILLION OZ

JAN 20/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.998 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 527.792 MILLION OZ

JAN 19/WITH SILVER UP 71 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.942 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 525.804 MILLION OZ

JAN 18/WITH SILVER UP 51 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS OF 1.11 MILLION OZ AND 1.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 527.246 MILLION OZ//

JAN 14/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 529.780 MILLION OZ//

JAN 13/WITH SILVER DOWN 2 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 832,000 OZ FROM THE SLV////INVENTORY RESTS AT 529.780 MILLION OZ

JAN 12/WITH SILVER UP 38 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//

JAN 11/WITH SILVER UP 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ/.

JAN 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 7/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 6/WITH SILVER DOWN 94 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL PF 226,000 OZ FROM THE SLV///INVENTORY RESTS AT 530.612 MILLION OZ?/

JAN 5/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 4/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 3/WITH SILVER DOWN 45 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.219 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 530.838 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC30/WITH SILVER UP 14 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.624 MILLILON OZ FROM THE SLV.//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 29/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ/

DEC 28/WITH SILVER UP 9 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.682 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 27/WITH SILVER UP 6 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681

DEC 23/WITH SILVER UP 19 CENTS TODAY:A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 22/WITH SILVER UP 29 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 538.883 MILLION OZ/

DEC 21/WITH SILVER UP 19 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.728 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 540.085 MILLION OZ

DEC 20/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 538.282 MILLION OZ

DEC 17/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 538.282 MILLION OZ//

CLOSING INVENTORY: 535.003 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,James RICKARDS

3.Chris Powell of GATA provides to us very important physical commentaries

Chris Powell is the correct one on this and not Ted Butler.

(Chris Powell/Ted Butler below)

Ted Butler: JPMorgan must have ‘tricked’ Bank of America into shorting so much gold and silver

Submitted by admin on Mon, 2022-01-24 11:51 Section: Daily Dispatches

11:54a ET Monday, January 24, 2022

Dear Friend of GATA and Gold:

Silver market analyst Ted Butler writes today that Bank of America has taken what seem huge short positions in gold and silver because the bank was “tricked in some way” by bullion bank JPMorganChase & Co.

Butler writes: “No one, no matter how dumb or misinformed, would do such a thing after careful and objective due diligence. There’s no way BofA senior management woke up one day and decided to put the organization in potential harm’s way by borrowing and selling short gold and silver in the quantities I claim. It had to be tricked in some way.

But what if the gold and silver positions attributed to the banks are not their own at all but the positions of an entity less concerned about risk — like an entity authorized to create and dispense money in infinite amounts?

What if the banks hold such astounding positions because they are only brokers for an entity or entities far larger? You know, like a government.

After all, the gold and silver futures markets in the United States, operated by CME Group, are actually designed for secret government intervention via what CME Group calls its Central Bank Incentive Program, under which governments and central banks and their agents receive volume discounts for trading all major futures contracts:

https://www.gata.org/node/18925

So it’s far less likely that Bank of America has been “tricked” here than that Butler himself has been. His analysis is headlined “Solving a Great Gold Mystery” and it’s posted at GoldSeek here:

https://goldseek.com/article/solving-great-gold-mystery

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Solving A Great Gold Mystery

January 24, 2022

Ted Butler

Butler Research

496Shares

If there is one mystery in the gold market that I believe has eluded analysts and commentators (certainly including yours truly), it is a compelling explanation for the unprecedented and massive inflow of physical metal, more than 30 million ounces, that came to be deposited in a matter of months, starting around April 2020, into mostly the COMEX-approved gold warehouses, but also into the big gold ETF, GLD. The physical gold inflows were so large that many wrote about it extensively at the time, but none of the explanations seemed to be on the mark – my own included.

Remembering that special time, now approaching the two-year mark, there were so many unprecedented developments around that massive physical gold inflow, including a blow out in COMEX spread differentials in both gold and silver futures, so as to defy simple economics. For a short time back then, the impossible occurred, namely, the contango (the near month discount to more deferred months) grew so extreme that a significant real return was guaranteed with no risk for the first time ever (to this old-time spread trader).

Now nearly two years later, it has dawned on me what occurred back then that explains the most unusual time period ever in both gold and silver. It has occurred to me that the simple explanation for all the strange occurrences in the gold market back then was that Bank of America borrowed and sold short as many as 30 million ounces of gold and not just the 800 million oz of silver I’ve been writing about. BofA borrowing and shorting gold fits like a glove with it doing the same in silver, as I hope to explain.

Upfront, while I discovered BofA borrowing and selling short 800 million oz of silver from the Office of the Comptroller of the Currency’s quarterly derivatives report and fitting that into what transpired in real world silver events, no such verification (or rejection) is possible in the OCC report for gold. As I’ve previously explained, the OCC moved gold into the FX derivatives category back in 2015, making it impossible to track gold OTC derivatives because the FX category is so large – measured in the trillions of dollars – so as to obscure gold developments in the same category. (At the same time gold’s removal from the precious metals category made it really simple to detect changes in silver derivatives).

The net result is that if Bank of America did borrow and sell short 30 million oz of gold, as I contend, the roughly $50 billion in cash proceeds and derivatives position that BofA ended up with as a result, wouldn’t show up in the OCC report, as BofA has held between $4 and $5 trillion in FX/gold derivatives positions since Dec 31, 2019 and $50 billion in gold derivatives simply wouldn’t stand out – as $50 billion would represent little more than 1% of BofA’s total FX/Gold category position. Therefore, my contention that Bank of America borrowed and sold short 30 million oz of physical gold in the April-June 2020 time period can be neither proven nor disproven by the OCC report alone. Then what am I basing my contention on?

First is a bit of common sense. When it comes to the idiocy and fraud of precious metals leasing/short selling, gold is always the preferred metal to borrow and sell short. This was true back in the last precious metals leasing/short sale fiasco of 20 years ago and likely remains true in today’s massive blunder by BofA. That’s because the gold price is so much higher than the price of silver, that it takes much less in ounce terms to borrow and sell short physical gold than silver. By borrowing 30 million ounces of gold, BofA ended up with around $50 billion in cash proceeds (30 million oz X $1700). BofA had to borrow and short sell 800 million oz of silver to end up with $18 billion in cash proceeds (800 million oz X $23).

Let’s face it, as dumb and dangerous as it is to borrow and sell short precious metals, there is somewhat of a perverse logic in borrowing and selling short gold rather than silver. That’s because there are billions of ounces of gold bullion in the world, 3 billion oz to be precise (plus another 3 billion oz in non-bullion equivalent form) and the 30 million oz I contend BofA is short is only 1% of all the gold bullion in the world. In silver, the 800 million oz I contend BofA is short is close to 40% of the two billion oz of world silver in 1000 oz bars – making it much more difficult to buy and deliver silver than gold.

Sure, a hundred dollar move up in gold will “cost” BofA $3 billion in adverse mark to market, but the gold market is deep enough to make it more feasible that Bank of America could limit the damage if it put its mind to it. But how the heck would it buy back 800 million oz of silver in a world where only two billion oz exist and pronounced shortage seems around the next corner?

To be fair, while the 30 million oz gold short position that I claim Bank of America holds in the OTC market is small relative to total world bullion inventories, it is still large enough that, by itself, it is much greater than the entire net commercial short position on the COMEX, the world’s leading precious metals derivatives exchange. BofA’s 30 million oz short position is equal to 300,000 COMEX gold contracts, substantially larger than the 221,000 contracts of the total commercial net short position – meaning one bank may be holding a larger short position than the combined net short position of all the commercials on the COMEX.

One of the more recent developments that points to Bank of America having borrowed and gone short 30 million oz of physical gold is that it has been, for more than a year, a big stopper of gold and silver deliveries on the COMEX in its house account (but was a big net issuer of both in December). In meaningful terms, Bank of America has, quite literally, burst upon the precious metals’ scene starting a year and a half ago, after never really participating in this market before – strongly suggestive its debut was due to a sudden and massive borrowing and short selling binge.

I continue to believe Bank of America was duped into its current predicament of being short 30 million oz of gold and 800 million oz of physical silver. No one, no matter how dumb or misinformed, would do such a thing after careful and objective due diligence. There’s no way BofA senior management woke up one day and decided to put the organization in potential harms’ way by borrowing and selling short gold and silver in the quantities I claim – it had to be tricked in some way.

As to who did the hoodwinking of BofA, you should know by now the only possible answer is JPMorgan, which also happens to be the only entity capable of such a feat. After all, I have chronicled how JPM accumulated 1.2 billion oz of physical silver and 30 million oz of physical gold on these pages over the past decade or so. And please understand that when I say JPMorgan has done this or done that, that anyone would be hard-pressed to find an ounce of silver or gold on JPM’s books – it’s all held in affiliate and nominee names. JPM knew when it embarked on its physical silver and gold accumulation plan that it must conceal and camouflage what it was doing and took great pains to hide its actual ownership from the get go.

As to why JPMorgan would go out of its way to entice and hoodwink Bank of America into borrowing and then short selling 30 million oz of gold and 800 million oz of silver, the answer is so obvious and straightforward as to be self-evident – to greatly benefit JPM primarily and, secondarily, to damage a competitor.

The benefit to JPMorgan is for it to be able to vastly increase its overall silver and gold long position in the only manner possible. By lending BofA the physical gold and silver it borrowed, JPM knew full-well that BofA would immediately short sell the borrowed metal (that’s how these nutty precious metals “loans” work) and knowing this, you can be sure that the same JPM interests which loaned the metal were in place to buy all the metal sold short by BofA. This is so criminally genius that only JPMorgan could have devised and implemented the scam. By the way, it is interesting to note that more than two-thirds of the 30 million oz inflow into the COMEX warehouses in 2020 came into just two warehouses, Brinks and, drumroll, ..…..the JPMorgan warehouse.

Of course, I’m not suggesting that JPM and its friends and family could actually increase the amount of physical metal they owned, as they are criminal geniuses not magicians of alchemy. But the net effect was that JPM owned the same amount (more or less) of physical metal after BofA sold it short (unknowingly) back to JPM as it did before the transactions – but with a giant kicker. JPMorgan as a result of its criminal cunning and duplicity, greatly increased its physical holdings by a derivatives bonus of up to 30 million gold oz and 800 million silver oz – courtesy of the dingbats at BofA. In other words, interests related to JPMorgan ended up owning the same amount of physical metal as they did all along, but augmented by a new massive derivatives long position – courtesy of BofA. In terms of criminal genius, no one comes close to JPMorgan.

As with all of the things that I’ve discovered over the decades, my imagination is nowhere near fertile enough to have dreamed up any of them on a whim. All, including this massive snookering of Bank of America by JPMorgan, are borne out in the continuing flow of public facts and data. Hard to believe, but that’s the way it is.

Perhaps the most important takeaway from the solving of a mysterious “cold case” in gold, namely, explaining how 30 million oz of gold suddenly got deposited in the Spring of 2020 into the COMEX warehouses, also explains another great mystery of the recent past. Many (most) have scratched their heads looking for an explanation for why gold and silver prices have performed so poorly over the past year or so in the face of record surges in the price of just about every asset class there is – from stocks and real estate to cryptocurrencies and collectibles of all types – including virtual reality collectibles called NFTs. Well, scratch your heads no more – the “dumping” of 30 million oz of physical gold and 800 million oz of physical silver should explain why gold and silver prices did nothing while everything else – including inflation – soared.

Of course, what I just described, the dumping and market adjustment to such massive amounts of physical gold and silver is now completed and reflected in past price performance. Now all that remains is the “other side” of leasing/short selling in which the borrower, Bank of America, must seek to “undo” its ill-conceived venture into precious metals. For gold and silver investors, that should represent the start of very good times.

As always, if Bank of America or the Office of the Comptroller of the Currency have a radically different explanation from mine, I would encourage both to offer that explanation.

Ted Butler

January 24, 2022

end

4.OTHER GOLD COMMENTARIES

END

5.OTHER COMMODITIES/

end

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.3299

OFFSHORE YUAN: 6.3371

HANG SANG CLOSED DOWN 412.85 PTS OR 1.67%

2. Nikkei closed DOWN 457.03 PTS OR 1.66%

3. Europe stocks ALL GREEN

USA dollar INDEX UP TO 96.22/Euro FALLS TO 1.1274-

3b Japan 10 YR bond yield: RISES TO. +.141/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 114.04/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 83.79 and Brent: 86.42-

3f Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE CLOSED DOWN// OFF- SHORE DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.0.082%/Italian 10 Yr bond yield FALLS to 1.27% /SPAIN 10 YR BOND YIELD RISES TO 0.64%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.35: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 1.63

3k Gold at $1841.30 silver at: 23.74 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble UP 12/100 in roubles/dollar AT 78.70

3m oil into the 83 dollar handle for WTI and 86 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 114.04 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9196– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0367 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 1.774 UP 1 BASIS PTS

USA 30 YR BOND YIELD: 2.121 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.53

“Volatility Is Back”: Futures Resume Sliding After Historic Rollercoaster Reversal

TUESDAY, JAN 25, 2022 – 08:01 AM

Following one of the greatest intraday market reversals in history, US index futures resumed their decline led by the Nasdaq, signaling more pain for richly valued technology shares as investors braced for the highly anticipated Fed meeting and a flurry of earnings as geopolitical tensions between Russia and Ukraine persisted. Companies including GE, J&J, Verizon and Microsoft report earnings on Tuesday, as the Fed starts a two-day meeting. As of 7:30am ET, emini S&P futures were down 60 points or 1.36% to 4,343, Nasdaq futures were down 1.88% or 272 points and Dow futures were down 236 points or 0.68%. The VIX was at 33, after swinging between 29 and 39 on Monday; 10Y Treasury yields were unchanged at 1.77% and the dollar gained.

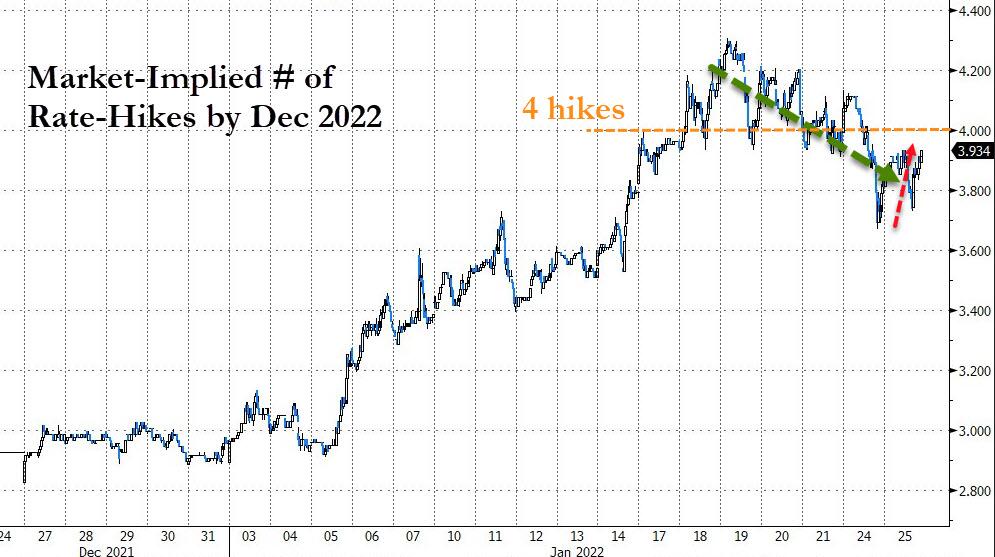

US equities swung in a rollercoaster of volatility on Monday as both underlying gauges had erased intraday losses to end the session slightly higher as dip-buyers came in. According to JPM’s trading desk, yesterday’s 5% reversal in the Nasdaq is an uncommon occurrence: “If you exclude March 2020, yesterday was the 7th 5%+ NDX reversal since GFC. The following day, markets were down 4 of the previous 6 times, with an average return of -1.6%. In 2000 – 2002 and in 2008, there are many more observations of 5% reversals, occurring 194 times during those time periods. Overall, intraday reversals of this magnitude seems to suggest more volatility rather than a directional change.” In other words, expect much more volatility. That said, the market has sent the Fed a message: an overly hawkish message tomorrow and stocks get it.

“The recent market turmoil will certainly soften the Fed’s tone, or at least prevent the Fed from sounding too hawkish,” said Ipek Ozkardeskaya, senior analyst at Swissquote. “The Fed can’t afford to trigger a financial crisis.”

She is right, but things are not looking too good for Powell right now as the VIX, rose for a sixth session on Tuesday, after briefly jumping intraday to the highest since October 2020 on Monday. Global equities at one point wiped almost $3 trillion on Monday, with the S&P 500 down more than 10% from a record high, before a dramatic reversal saw major U.S. benchmarks end in the green.

“Volatility is back,” Lori Calvasina, head of U.S. equity strategy at RBC Capital Markets, said on Bloomberg Television. “We’re having a sea-change in terms of Fed policy. Equity investors frankly have been behind the curve in anticipating what’s coming, so there’s a lot of catch-up to do.”

In premarket trading, General Electric dropped after missing sales expectations, while International Business Machines Corp. and American Express Co. gained after posting revenue that beat forecasts. Big tech and growth stocks declined amid a slide in Nasdaq 100 Index futures, as worries linger over the prospect of Fed rate hikes and rising bond yields. Apple (AAPL US) -1.4%, Microsoft (MSFT US) -0.7%, chipmaker Nvidia (NVDA US) -2.1%, Amazon.com (AMZN US) -1.8%. IBM shares gained 3.2% after the technology company reported revenue for the fourth quarter that beat the average analyst estimate. Other notable premarket movers:

- General Electric (GE) shares are down 5.9% in premarket trading on Tuesday, after the industrial conglomerate reported revenue for the fourth quarter that missed the average analyst estimate

- Retail-trader favorites GameStop (GME US) and AMC (AMC US) declined in U.S. premarket trading, suggesting losses for so-called meme stocks may continue in Tuesday’s session.

- Nvidia Corp. (NVDA US) shares are lower in premarket trading after Bloomberg News reported it is quietly preparing to abandon its purchase of Arm Ltd. from SoftBank Group Corp. after making little to no progress in winning approval for the $40 billion chip deal, according to people familiar with the matter.

- SmileDirectClub (SDC US) shares rise 8% in premarket trading after it announced plans to cut jobs and suspend operations in some countries.

- Robinhood (HOOD) shares slump 3.7% in premarket trading after Mizuho analyst Dan Dolev slashed his price target on the stock to $20 from $55 previously.

- Inter Parfums (IPAR US) gained in postmarket trading Monday after boosting its net sales guidance for 2022, which beat the average analyst estimate.

In Europe, equities recovered from yesterday’s selloff, grinding back to best levels after a choppy start; banks, telecoms and energy are the strongest Stoxx 600 sectors, gaining over 2%. The Stoxx Europe 600 Index up 0.6%, after being up more than 1% earlier; CAC is the marginal outperformer. Logitech jumped 11%, the most since October 2020, after the Swiss-based producer of computer accessories reported better-than-expected earnings and raised its 2022 profit outlook.

Earlier in the session, Asian stocks slumped to their lowest since November 2020 amid investor concerns over upcoming monetary-policy tightening by the Federal Reserve and rising tension between Russia and Ukraine. The MSCI AsiaPacific Index slid as much as 1.7%, driven by losses in the information-technology and financial sectors. Key benchmarks tumbled more than 2% in Japan, Australia and South Korea. China’s CSI 300 Index falls as much as 2.2%, the most since Aug. 20, driven by losses in energy and telecom shares. The gauge drops to its lowest intraday level in nearly six months. The biggest decliners include Jafron Biomedical, Lepu Medical Technology and Huaneng Power, all down more than 7%. Shanghai Composite -2.4%, Shenzhen Composite -3.2%, ChiNext -2.4%.

Ukraine-related market risk “has become a bit more real now, so investors are confused about what to do,” said Naoki Fujiwara, chief fund manager at Shinkin Asset Management. “It will be a shock if Russia does make a move, so some are feeling the need to run from stocks for now.” The Asian stock benchmark is down more than 15% from its peak last February. Japan’s Topix and New Zealand’s S&P/NZX 50 have touched correction levels, down 10% from recent highs, while key measures for in mainland China and South Korea inched closer to the 20% drop that indicates a bear market

India’s key equity gauges snapped their five-day decline to outperform Asian peers, helped by robust earnings performances of local companies ahead of the announcement of the federal budget next week. The S&P BSE Sensex rose 0.6% to 57,858.15 in Mumbai while the NSE Nifty 50 Index gained 0.8%, the biggest single-day surges of both since Jan. 12. The indexes erased losses of as much as 1.9% and 1.8%, respectively, earlier in the session. All but two of the 19 sector sub-indexes compiled by BSE Ltd. closed high, led by a gauge of telecom companies. The rally in Indian equities were in contrast to most cohorts in the region, with the MSCI Asia Pacific Index slumping to its lowest since November 2020 amid concerns over monetary-policy tightening and rising tension between Russia and Ukraine. “The earnings season has gathered pace with revenue largely in-line with estimates, however higher commodity prices taking toll on margin and profitability to some extent,” Mitul Shah, head of research at Reliance Securities, wrote in a note.

In rates, Treasury and gilt curves all bear steepen as Monday’s haven bid fades. Treasuries are steady with yields cheaper by at least 1bp across long-end, slightly steepening the curve. 10-year TSY yields hover around 1.77%, with gilts trading almost 4bp cheaper on the sector as dealers prepare for a new 50-year bond syndication next month; spreads slightly wider with long-end marginally underperforming. A $55b 5-year note auction at 1pm ET, second of three this week, follows strong 2-year sale that drew a yield 1.2bp lower than the WI at the bidding deadline; cycle concludes with $53b 7-year notes Thursday. WI 5-year yield at ~1.568% is above auction stops since December 2019 and ~30.5bp cheaper than last month’s result. IG dollar issuance slate remains moribund, though desks expected around $20b this week. Gilts underperforming at the back end after the DMO announces a new 50y syndication due in early February. Peripheral spreads tighten, with 10y Italy narrowing 3.5bps to core as day 2 of presidential voting resumes.

In FX, Bloomberg Dollar Spot drifts back up through Monday’s best levels extending yesterday’s gains as it climbed against most of its Group-of-10 peers. The Australian dollar outperformed and was bought against the kiwi after a strong 4Q inflation report boosted yields across the curve and reinforced RBA tightening bets. Australian three-year yield jumped as much as 9bps to highest since April 2019 and all but one of 17 analysts polled by Bloomberg expect the RBA will end quantitative easing at its Feb. 1 meeting. The euro extended an overnight loss to trade below $1.13; the currency was sold for the dollar and yen after NATO said it would boost its deployments in eastern Europe to deter a new Russian invasion in Ukraine. The euro’s volatility skew shifts lower compared to a week ago as the options space tracks the spot market, where the common currency is under pressure. The pound advanced versus the euro, rebounding after it reached the weakest level against the common currency this year on Monday. The yen eased from a five-week high and Japanese government bonds traded in narrow ranges after a solid auction. BOJ Governor Haruhiko Kuroda said the Bank of Japan must continue with monetary easing because its 2% inflation target remains distant. RUB outperforms in EMFX, fading part of Monday’s weakness.

In commodities, crude futures tick higher. WTI adds ~$1, regaining a $84-handle, Brent pushes back above $87. Spot gold drops to about $1,838/oz. Most base metals are in the red, with LME tin down over 2.5%.

Looking at the day ahead, data releases include the Ifo’s business climate indicator from Germany for January, along with the US Conference Board’s consumer confidence indicator for January. Earnings releases include Microsoft, Johnson & Johnson, Verizon Communications, NextEra Energy, Texas Instruments, American Express, General Electric and Moderna. And on top of that, the IMF will be releasing their World Economic Outlook Update.

Market Snapshot

- S&P 500 futures down 0.9% to 4,363.50

- STOXX Europe 600 up 1.0% to 460.80

- MXAP down 1.5% to 187.12

- MXAPJ down 1.4% to 612.92

- Nikkei down 1.7% to 27,131.34

- Topix down 1.7% to 1,896.62

- Hang Seng Index down 1.7% to 24,243.61

- Shanghai Composite down 2.6% to 3,433.06

- Sensex up 0.6% to 57,862.85

- Australia S&P/ASX 200 down 2.5% to 6,961.63

- Kospi down 2.6% to 2,720.39

- Brent Futures up 1.3% to $87.36/bbl

- German 10Y yield little changed at -0.07%

- Euro down 0.3% to $1.1297

- Gold spot down 0.3% to $1,838.19

- U.S. Dollar Index up 0.14% to 96.05

Top Overnight News from Bloomberg

- Global traders already on tenterhooks over this week’s key Federal Reserve meeting were jolted further Tuesday by Australian inflation data that smashed expectations, a surprise monetary tightening in Singapore and further swings in U.S. equity futures

- Western allies are pushing ahead with diplomatic efforts to avert war between Russia and Ukraine, after U.S. President Joe Biden held what he described as a “great” call with European leaders on Monday

- German Ifo Institute’s business expectations gauge rose to 95.2 in January, more than economists predicted. Manufacturers saw supply bottlenecks easing at the start of the year, and even services providers were optimistic about the future — despite current curbs on activity

- U.K. Prime Minister Boris Johnson’s office has confirmed that staff gathered to celebrate his birthday during the 2020 lockdown, adding to existing allegations of rule-breaking parties

- While positive turnarounds are often viewed as a good sign, that might not be the case this time. According to calculations by Bespoke Investment Group, Monday was the sixth time since 1988 that the Nasdaq erased a 4%-plus intraday decline to close higher on the day. On previous occasions the tech-heavy gauge saw a median decline of 5.5% one month later and a drop of 7.9% three months down the line

- Deutsche Bank AG turned the blame on its ex-client Palladium Group for crippling losses it suffered investing in risky foreign exchange derivatives the German lender sold

A more detailed breakdown of global markets courtesy of Newsquawk

In Asia, markets were heavily pressured after yesterday’s whirlwind session in the US. ASX 200 (-2.5%) slumped with losses exacerbated as firm CPI supports RBA tightening calls. Nikkei 225 (-1.7%) briefly fell beneath 27,000 for the first time since August last year. KOSPI (-2.6%) ignored strong GDP as South Korea reported record daily COVID-19 cases and North Korea fired cruise missiles.

Hang Seng (-1.7%) and Shanghai Comp. (-2.5%) conformed to the downbeat mood with Hong Kong dragged by notable losses in its tech sector and with Chinese property names also subdued amid ongoing Evergrande woes

Top Asian News

- Asian Stocks Slump to 14-Month Low on Concerns Over Fed, Ukraine

- Bear Markets, Corrections Loom for Many Asian Stock Gauges

- Shimao Dollar Bonds Jump on Asset Sale Report: Evergrande Update

- Korea Considering Fully Resuming Short-Selling in 1H: Yonhap

European bourses are firmer taking the lead from the resurgence in Wall St. trade that they failed to benefit from yesterday, Euro Stoxx 50 +0.7. Sectors are all in the green in Europe though defensives are the relative laggards. Stateside, US futures are pressured with the NQ (-1.4%) the current underperformer after yesterday’s turnaround and as yields climb Volkswagen (VOW3 GY) is to collaborate with Bosch on automated driving software, could be sold to other autos in the future. Level 2 ‘hands free’ technology to be deployed in the Volkswagen fleet in 2023. Nvidia (NVDA) is said to be preparing to ditch its takeover of Arm, according to reports; subsequently, a spokesperson states that they continue to hold views expressed in detail in the latest regulatory filing.

Top European News

- Deutsche Bank Blames Client in $565 Million FX Mis-Selling Suit

- Oil Buyers Snap Up Diesel-Rich Crude as Omicron Fears Abate

- Swedish Sex-Toy Retailer Purefun Seeks SEK250m Valuation in IPO

- Kuwait Refers Army Officers for Prosecution in Eurofighter Deal

In FX, the DXY nudges further over 96.000 as hawkish FOMC expectations overshadow less supportive risk dynamics, but the Franc loses safe haven appeal across the board in what appears to be an orchestrated effort to curb demand. Euro fails to benefit from a better than expected German Ifo survey on balance, as technical impulses and yield differentials weigh. Pound relatively resilient as policy probe PM Johnson and Tory party for potential lockdown breaching events. Loonie holds off lows awaiting BoC amidst forecasts for an early hike. Aussie also underpinned by further predictions for the RBA to bring forward tightening after stronger than anticipated Q4 inflation data. CBRT opens a gold swap auction via the traditional method for 20/T of gold, three-month maturity.

In commodities, WTI and Brent March contracts have continued to nurse yesterday’s losses, with the benchmarks picking up further with geopolitics around Ukraine, China and North Korea dominating newsflow. WTI March is back on a USD 84/bbl handle (vs USD 83.43 intraday low) while its Brent counterpart reclaims USD 87/bbl from a USD 86.50/bbl daily low. Spot gold and silver are subdued amid USD upside, and as such remain comfortable above a number of DMAs that have drawn recent focus; while LME Copper is modestly softer in familiar ranges

DB’s Jim Reid concludes the overnight wrap

At one point yesterday it felt like we were in a full blown crisis let alone a recession. At Europe closed their laptops down the S&P was as much as -3.98% lower, which would have been the worst daily return since June 2020. The NASDAQ was -4.90% lower, the worst potential close since September 2020. However at that point Manic Monday turned and remarkably the S&P 500 (+0.28%) and NASDAQ (+0.63%) closed higher. The volatility continues this morning though with S&P 500 futures down -1.1% and Nasdaq futures -1.4%. Note that earning season starts to get going with some momentum today. The highlights of those reporting are in the day ahead at the end but Microsoft is probably the biggest and most important.

This morning Asian markets are trying to come to terms with the sharp down, sharp up and then down move and are trading lower. The Kospi (-2.86%), Nikkei (-2.14%), Hang Seng (-1.59%), Shanghai Composite (-1.12%) and CSI (-0.80%) are all around the lows for the session as we type. It could be all change by the time you read this though.

Reviewing the US session in more detail now and cyclical sectors staged an impressive rebound, led by discretionary (+1.21%), energy (+0.55%), and industrials (+0.53%) stocks while defensives lagged, with the three worst performing sectors being utilities (-1.03%), health care (-0.37%), and consumer staples (-0.35%). Itwas interesting that the reversal was so broad-based. With a market this concentrated among mega-cap stocks, it’s usually safe to assume a few big names drove the changes in the headline index, but the FANG+ index was actually lower by -0.91%. Amazon was emblematic of the broader move, however, declining more than -5% intraday before finishing +1.33% in the green, but it looks like its fortunes were tied with the broader recovery in discretionary stocks than its status as a mega-cap. At the end of the day, 320 stock prices advanced. Much like the turns-for-the-worse last week, the reversal in fortunes came absent a clear catalyst, which is much more common when volatility is this high. Speaking of this the Vix index of volatility also took an intraday round trip, increasing +10.08pts before ending the day just +1.27pts higher at a still-elevated 30.12pts, right around levels seen during the initial Omicron outbreak.

This late rally left European bourses behind, with the STOXX 600’s decline (-3.81%) marking it the worst daily performance since June 2020, with indices slumping across the continent including the DAX (-3.80%), the CAC 40 (-3.97%) and the FTSE MIB (-4.02%). After the US rebound but the Asian falls Stoxx futures are only +0.7%.

The current high volatility in markets comes as the FOMC are set to begin their two-day policy deliberations today.

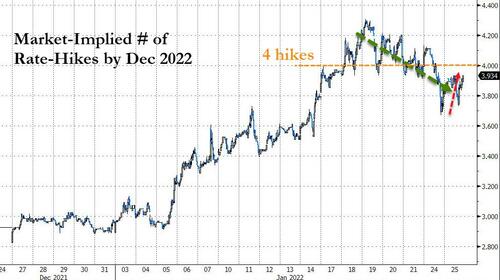

The year-to-date selloff in risk assets was sparked by the release of the December FOMC minutes in the first week of January, when investors took fright at the possibility of a more hawkish Fed over the coming months. So will Powell change the mood tomorrow night? With inflation at 7% that’s tough but we might get an idea of how much financial conditions tightening will frighten the Fed and how much they are actually comfortable with.

While markets are certainly concerned about the Fed and other central banks right now, the market also has to contend with the backdrop of an increasingly hostile geopolitical environment, with tensions ratcheting up continuously between Russia and the West. Reports note both sides are increasing their troop presence and putting current troops on higher alert within the region, while western leaders including Presidents Biden and Macron, Chancellor Scholz, and Prime Minister Johnson reportedly had a productive call on western cooperation on Ukraine issues. Separately, there was a meeting of EU foreign ministers that was joined by US Secretary of State Blinken, and the EU reiterated its warning that “any further military aggression by Russia against Ukraine will have massive consequences and severe costs”. The latest developments saw Russian assets lose further ground yesterday, with the Ruble down -1.68% against the US Dollar, whilst Russian equities underperformed globally, with the MOEX Russia index down -5.93% by the close but before the US bounce. Meanwhile European natural gas futures surged again given the higher perceived risk of conflict, with the benchmark future up by +17.75%. For those wanting further info, our colleagues in CEEMEA research put out a note on this last week (link here).

Back to yesterday, and there were few places in markets immune to yesterday’s volatility, with oil prices giving up a decent chunk of their recent gains from the European afternoon. By the close, Brent Crude was down -1.84% and WTI had shed -2.15%, marking the worst day of 2022 so far for both of them. Indeed, commodities more broadly lost ground, with copper down -2.14%, which is often taken to be a key industrial bellwether. Oil is back up around +0.5% this morning.

Amidst the woes for markets more broadly, sovereign bonds were fairly subdued, with the long-end of the Treasury curve selling off from intraday lows in line with the turn in risk. Yields on 10yr Treasuries increased +1.3bps to 1.77% (1.755% in Asian), with real yields declining -3.8bps but breakevens cancelled out the decline by rebounding alongside equities late in the afternoon, ending the day +4.9bps higher. Breakevens moved with risk assets on the day, so the price action seemed to reflect the broader growth outlook rather than incremental updates to the Fed’s inflation-fighting bona fides, having already declined -22.9bps from the start of the year’s hawkish pivot.

In line with the turn in risk, the 2s10s US yield curve bounced from intraday lows of 70.3 bps to increase +4.5bps to 79.5bps at the close. However it’s back down to 74.5bps in Asia but 2-3bps of this is a 2yr benchmark change. The rally in the front end of the curve left the market pricing 3.83 Fed hikes this year, the lowest level in more than a week. Faith in the Fed put is alive and well. The probability of March liftoff dipped as well, with the market pricing 98.5% chance of a rate hike. As I wrote in my latest chartbook, the 2s10s is one of the best recessionary indicators and a classic late-cycle signal, and it’s lost around half its steepness in less than a year, having peaked at 157.6bps at the end of Q1 2021. However don’t let’s get too ahead of ourselves. It hasn’t inverted yet so recession is likely someway off yet even if we’re moving in that direction. Over in Europe, sovereign bond yields wound up the day a little lower, having missed the late selloff, with those on 10yr bunds (-4.2bps to -0.11%), OATs (-2.8bps) and gilts (-4.5bps) seeing declines, thus coming off their recent highs last week that saw 10yr bund yields back in positive territory at one point in trading.

Staying on Europe, our economists updated their ECB call yesterday (link here), and are now expecting liftoff to begin in December 2022 with a 25bp hike. Given the latest upgrading of their inflation forecasts, this means that the ECB’s “triple lock” criteria for liftoff will be met earlier, potentially as soon as the end of this year, with the ECB set to act at the start of this window. And as well as bringing forward the timing of liftoff, they’ve also accelerated the pace of tightening, and now see 25bp hikes in the deposit rate each quarter until rates hit +0.5% in September 2023, followed by less frequent hikes.

Earlier this morning, South Korea’s Q4 GDP expanded +1.1% q/q, in line with market expectations, up from a +0.3% rise in the third quarter. For the full year, the economy grew +4.0%, recording the fastest pace of growth since 2010 buoyed by a jump in exports and corporate investments and rebounded from the previous year’s -0.9%.

Given the array of other events yesterday, the flash PMIs for January took a bit of a backseat relative to normal. They showed a fairly divergent picture across the global economy, with surprises to the upside and downside depending on the country. For the Euro Area as a whole, the composite PMI fell to an 11-month low of 52.4 (vs. 52.6 expected). However, that came as the manufacturing PMI rose unexpectedly to 59.0 (vs. 57.5 expected), whereas the services PMI fell to 51.2 (vs. 53.1 expected). In Germany, there was a significant upside surprise as the composite PMI rose to 54.3 (vs. 49.4 expected), but France’s fell back to 52.7 (vs. 54.7 expected), as did the UK’s to 53.4 (vs. 54.0 expected). Over in the US, there were downside surprises there too, with the services PMI down to an 18-month low of 50.9 (vs. 55.4 expected).

To the day ahead now, and data releases include the Ifo’s business climate indicator from Germany for January, along with the US Conference Board’s consumer confidence indicator for January. Earnings releases include Microsoft, Johnson & Johnson, Verizon Communications, NextEra Energy, Texas Instruments, American Express, General Electric and Moderna. And on top of that, the IMF will be releasing their World Economic Outlook Update.

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED DOWN 91.04 PTS OR 2.58% //Hang Sang CLOSED DOWN 412.85 PTS OR 1.67% /The Nikkei closed DOWN 457.03 PTS OR 1.66% //Australia’s all ordinaires CLOSED DOWN 2.60% /Chinese yuan (ONSHORE) closed DOWN 6.3299 /Oil DOWN TO 83.79 dollars per barrel for WTI and UP TO 86.42 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3299. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3370: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING WEAKER AGAINST USA DOLLAR

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

3B JAPAN

end

3c CHINA

CHINA/

China’s empty buildings

(Davidson/EpochTimes)

China Builds 27 Empty New York Cities

Commentary by James Dale Davidson via The Epoch Times (emphasis ours),

As of 2016, China’s empty apartment units could house New York City 27 times over.Skyline of Shenzhen in Guangdong Province, China, in this undated photo. (Peter Parks/AFP/Getty Images)

What does this mean to you? There are a lot of carry-on effects from wasting so many resources. As you delve into a thought exercise to get more acquainted with the ruinous consequences of credit bubbles, be grateful that you don’t really have to worry about malicious genies magically tagging you with mortgaged deeds.

That could be scary. Imagine that some cruel genie took a perverse dislike to you. What worse instance of malevolent magic could the genie perform than to present you with deeds to the astonishing inventory of 70 million empty apartments structures accumulating dust throughout China.

You might think it would make you a billionaire, a real estate magnate on par with Donald Trump. But think again.

This may be a good moment to retell an uncharacteristically charming story Trump told on himself, dating to the savings and loan crisis (S&L crisis) of the late 1980s and early 1990s. That was a time when 1,043 out of the 3,234 savings and loan associations in the United States failed as they tried to digest billions in over-mortgaged real estate properties.

At that time, Trump found himself walking the streets of the Upper East Side of Manhattan one evening with his girlfriend of the moment. As they walked, they came upon a bum in a tattered peacoat lying on a grate. Trump remarked to his companion, “That guy has $1 billion more than I do.” She responded, “But he doesn’t look like he has a penny.” Trump replied, “He doesn’t.”

When he said that, Trump’s fortune was hostage to the banks to which he owed about a billion dollars more than his properties would have realized in a fire sale. I describe this “as an uncharacteristically charming story” because Trump is hardly famous for making jokes at his own expense. Nonetheless, he confirmed to me in a conversation that the above account I share with you is valid. It shows Trump humorously acknowledging the implications of double-entry bookkeeping at his best.

With that in mind, how could you afford to pay the construction mortgages on 70 million apartment units with no residents deeded to you by the evil genie? A challenging question. You would have to do some fast talking with the Chinese banks of the sort Trump managed with New York banks decades ago during the S&L crisis.

Your only hope of avoiding being sucked into a black hole of debt defaults would be to hire some creative scoundrels disguised as accountants to help you persuade the banks to lend you additional billions (or more probably, trillions) to postpone the day of reckoning. Note that the extent to which you could succeed would only worsen the ultimate malinvestment problem. Your assets would not be enhanced in any way by being encumbered with additional debt. They would just become more costly.

Could you keep kiting the debt?

A $36.4 Trillion Question?

That is at least a $36.4 trillion question. Maybe a $45.9 trillion, or possibly even a $116.6 trillion question. The correct answer depends on China’s actual debt level. Unlike Trump’s challenge of three decades ago when the systemic debt issue was denominated in billions of dollars, the Chinese bad debt problem is 1,000 times worse.

Forbes reports the estimate of Professor Victor Shih of the University of California San Diego. Shih believes that Chinese official debt figures have proven woefully inadequate.

A $45.9 Trillion Question?

In 2017, Shih put total Chinese debt at 328 percent of GDP (reported at $14 trillion), therefore $45.9 trillion. According to Shih, “total interest payments from June 2016 to June 2017 exceeded the incremental increase in nominal GDP by roughly 8 trillion RMB.”

If so, that hints that the end is near. However, as rough as that sounds, the actual situation may be even worse.

Or a $116.6 Trillion Question?

If you are a connoisseur of forbidden truths, as I am, you don’t take official figures at face value. You keep digging for tells that reveal the real story. I am convinced that Chinese government statistics are as bogus as those in the United States. And more so.An aerial view shows the Evergrande Changqing community in Wuhan, Hubei Province, China, on Sept. 26, 2021. (Getty Images)

Professor Christopher Balding of HSBC Business School, Peking University, an authority with good sources in the People’s Bank of China’s (PBOC) Financial Stability Board, recently did some subversive arithmetic combining “on balance sheet assets” with “off-balance sheet assets.” Remember, while debts are liabilities to the borrowers, they are assets to the lenders.

He concludes that total debt in China is a breathtaking 833 percent of GDP. That means a debt of roughly $116.6 trillion.

Wow. Just wow!

The actual debt level could be three and a half times higher than suggested by official figures. The National Development and Reform Commission says Chinese debt amounts to 260 percent of GDP ($36.4 trillion). The International Monetary Fund (IMF) accepts a lower official estimate of 230 percent. But suppose Balding’s report of 833 percent is correct. In that case, this is a matter of capital importance to the world economy and your investments.

Annual Interest Payments of 29 Percent of GDP?

Remember, interest rates in China are not as minuscule as those in the United States or negative as those in Europe and Japan. Assume the average interest rate paid equals the short-term interbank deposit rate of 3.5 percent. Balding observes, “this would imply financial services costs to the economy of 29% nominal GDP.” A large nut to crack. Even Chinese growth rates would not come close to covering annual carrying costs of 29 percent.

Is it possible that Balding is right?

Yes. I see several hints that he is.

Are Official Financial Figures Wildly Wrong?

For one thing, almost every Chinese bankruptcy case brings evidence of undisclosed liabilities of individual companies. Balding observes, “it is common to find enormous amounts of undisclosed debts or (Enron-like) asset management products in Chinese bankruptcies or defaults.”

This underscores the suspicion that the actual level of debt has been low-balled. In Balding’s words, it also means that “official on balance sheet financial figures are wildly wrong with disastrous consequences.” He warns, “This implies that we need to rethink the entire story of Chinese development and finance since probably about 2000.”

Balding continues: “Excessive indebtedness is distributed in virtually every sector of the economy. Before, if there was a shock to the corporate sector, householders and the government could step in and help. However, virtually no sector of the Chinese economy does not have an enormous indebtedness. Distributing it throughout simply lowers the capacity to handle a shock.”