January 26, 2022 · by harveyorgan · in Uncategorized · Leave a comment ·Edit

JAN 26//

TODAY IS OPTION EXPIRY FOR THE COMEX SO DO NOT GET TOO CONCERNED ON THE FALL IN GOLD/SILVER PRICE. THIS CRIMINAL ACTIVITY IS ROUTINE FOR THE CROOKSMONDAY IS OPTIONS EXPIRY FOR LONDON LBMA/OTC CONTRACTS.

GOLD; DOWN $21.60 to $1830.35

SILVER: $23.80 DOWN 7 CENTS

ACCESS MARKET: GOLD: 1819.00..

SILVER: $23.51

Bitcoin: morning price: 37,803 up 1066

Bitcoin: afternoon price: 36,737 up 2161

Platinum price: closing up $17.35 to $1047.80

Palladium price; closing up $155.20 at $2357.10

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filed COMEX//NOTICES: 0/0

FILED zero

NUMBER OF NOTICES FILED TODAY FOR JAN. CONTRACT: 0 NOTICE(S) FOR nil OZ (0.00000 TONNES)

total notices so far: 5651 contracts for 565,100 oz (17.577 tonnes)

SILVER NOTICES:

80 NOTICE(S) FILED TODAY FOR 400,000 OZ/

total number of notices filed so far this month 2936 : for 14,280,000 oz

GLD

WITH GOLD DOWN $21.60

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS): A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES INTO THE GLD//

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

CLOSING INVENTORY: 1013.10 TONNES/

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 7 CENTS:/:

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY SLV/ TONIGHT: 535.003 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE 2847 CONTRACTS TO 151,779 AND RESTS FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THIS HUGE GAIN IN OI WAS ACCOMPANIED WITH THE SMALL $0.10 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.10) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A HUGE GAIN OF 3007 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A ZERO ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 10.505 MILLION OZ FOLLOWED BY TODAY’S 425,000 OZ QUEUE. JUMP //NEW STANDING 14.910 MILLION OZ V) STRONG SIZED COMEX OI GAIN.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS 60

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTACTS for 17 days, total contracts: : 14,933 contracts or 74.665 million oz OR 4.392 MILLION OZ PER DAY. (878 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 14,933 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 74.665 MILLION OZ

.

LAST 8 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2847 WITH OUR SMALL 10 CENT GAIN SILVER PRICING AT THE COMEX// TUESDAY THE CME NOTIFIED US THAT WE HAD A TINY SIZED EFP ISSUANCE OF 100 CONTRACTS( 100 CONTRACTS ISSUED FOR MAR AND 100 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY:/ AS WELL AS TODAY /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN OF 10.505 MILLION OZ FOLLOWED BY TODAY’S 425,000 OZ QUEUE JUMP //NEW STANDING 14.910, MILLION OZ// .. WE HAD A HUGE SIZED GAIN OF 2947 OI CONTRACTS ON THE TWO EXCHANGES FOR 15.035 MILLION OZ//

WE HAD 80 NOTICES FILED TODAY FOR 400,000 OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GIGANTIC SIZED 14,452 TO 572,078 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -1104 CONTRACTS

.

THE GIGANTIC SIZED INCREASE IN COMEX OI CAME WITH OUR STRONG GAIN IN PRICE OF $10.40//COMEX GOLD TRADING/TUESDAY/.AS IN SILVER WE MUST HAVE HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION AS THE TOTAL GAIN ON OUR TWO EXCHANGES TOTALED A HUMONGOUS SIZED 21,244 CONTRACTS…

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JAN AT 3.5614 TONNES FOLLOWED BY TODAY’S 100 OZ E.F.P. JUMP TO LONDON//NEW STANDING: 17.626 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $10.40 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A HUMONGOUS SIZED GAIN OF 20,140 OI CONTRACTS (62.64 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALLED A GOOD SIZED 5688 CONTRACTS:

FOR FEB 5688 ALL OTHER MONTHS ZERO//TOTAL:5688

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 572,078.

IN ESSENCE WE HAVE A GIGANTIC SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 20,140, WITH 14,452 CONTRACTS INCREASED AT THE COMEX AND 5688 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 21,244 CONTRACTS OR 60.077TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5688) ACCOMPANYING THE HUGE SIZED GAIN IN COMEX OI (14,452): TOTAL GAIN IN THE TWO EXCHANGES 20,140 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR JAN. AT 3.7262 TONNES//FOLLOWED BY TODAY’S 100 OZ E.F.P. JUMP TO LONDON.//NEW STANDING 17.626 TONNES 3)ZERO LONG LIQUIDATION,4) HUGE SIZED COMEX OI. GAIN 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB.WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2021 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN : 61,502 CONTRACTS OR 6,150,200 oz OR 191.29 TONNES 17 TRADING DAY(S) AND THUS AVERAGING: 3618 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES: 191.29 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 191.29/3550 x 100% TONNES 5.38% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO DATE

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//FINAL ISSUANCE//

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A HUGE SIZED 2847 CONTRACTS TO 151,779 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 100 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 100 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 100 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2847 CONTRACTS AND ADD TO THE 100 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 2947 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 14.735 MILLION OZ,

OCCURRED WITH OUR $0.10 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 22.61 PTS OR 0.66% //Hang Sang CLOSED UP 46.29 PTS OR 0.19% /The Nikkei closed DOWN 120.01 PTS OR 0.44% //Australia’s all ordinaires CLOSED HOLIDAY /Chinese yuan (ONSHORE) closed UP 6.3225 /Oil UP TO 86.40 dollars per barrel for WTI and UP TO 89.19 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3225. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3262: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING STRONGER AGAINST USA DOLLAR

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GIGANTIC SIZED 14,452 CONTRACTS AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR GAIN OF $10.40 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (5688 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. LOOKS LIKE OUR BANKERS ARE FINALLY BAILING OUT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE NON ACTIVE DELIVERY MONTH OF JAN.. THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5688 EFP CONTRACTS WERE ISSUED: ;: , DEC : 0 & FEB. 5688 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5688 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUMONGOUS SIZED 21,244 TOTAL CONTRACTS IN THAT 5688 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GIGANTIC SIZED COMEX OI GAIN OF 15,556 CONTRACTS..

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR JAN (17.626),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $10.15)

AND THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS THE TOTAL GAIN ON THE TWO EXCHANGES REGISTERED A HUMONGOUS 62.64 TONNES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JAN (17.626 TONNES)…

WE HAD – 1104 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 21,244 CONTRACTS OR 212,4400 OZ OR 60.077 TONNES

Estimated gold volume today: 345,917 /// fair

Confirmed volume yesterday: 282,499 contracts poor

INITIAL STANDINGS FOR JAN ’22 COMEX GOLD //JAN 26

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 192.91 oz BRINKS 6kilobars |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 0 notice(s) 0 OZ 0 TONNES |

| No of oz to be served (notices) | 16 contracts 1600 oz 0.0437 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5651 notices 565,100 OZ 17.576 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

No dealer deposit 0

No dealer withdrawal 0

0 customer deposit

total deposit: nil oz

1 customer withdrawals

i) Out of BRINKS: 192.91 0z (6 KILOBARS)

total withdrawals: 192.91 oz

ADJUSTMENTS: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of JANUARY we have an oi of 16 stand for JANUARY LOSING 1 contract. We had 0 notices filed on TUESDAY, so we LOST ONE contract or an additional 100 oz will NOT stand for

gold in this very non active delivery month of January.

FEBRUARY LOST 13,751 CONTRACTS TO 98.403

March GAINED 175 contracts to stand at 3299..

We had 0 notice(s) filed today for 00 oz FOR THE JAN 2022 CONTRACT MONTH

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN /2021. contract month,

we take the total number of notices filed so far for the month (5651) x 100 oz , to which we add the difference between the open interest for the front month of (JAN: 16CONTRACTS ) minus the number of notices served upon today 0 x 100 oz per contract equals 566,700 OZ OR 17.626 TONNES the number of TONNES standing in this NON active month of JAN. (numbers corrected from yesterday)

thus the INITIAL standings for gold for the JAN contract month:

No of notices filed so far (5651) x 100 oz+ (16) OI for the front month minus the number of notices served upon today (0} x 100 oz} which equals 565,700 oz standing OR 17.626 TONNES in this NON active delivery month of JAN.

We LOST 1 contracts or an additional 100 oz of gold will NOT stand for metal on this side of the pond.

TOTAL COMEX GOLD STANDING: 17.626 TONNES (HUGE FOR A JANUARY DELIVERY MONTH

IF THIS HOLDS TO THE END OF THE MONTH, THIS WILL BE THE HIGHEST EVER RECORDED GOLD STANDING FOR A JANUARY, GENERALLY A VERY POOR DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

157,392.690, oz NOW PLEDGED /HSBC 4.89 TONNES

125,410.592 PLEDGED MANFRA 2.90 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690

288,481,604, oz JPM No 2 8.97 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonne

Loomis: 18,615.429 oz

total pledged gold: 1,555,310.092 oz 48.376 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 33,417,353.216 OZ (1039,42 TONNES)

TOTAL ELIGIBLE GOLD: 15,836,909.152 OZ (492.59 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,580,540.519 OZ (546.82 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 16,025230.0 OZ (REG GOLD- PLEDGED GOLD) 498.45 tonnes

END

JANUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//JAN 26

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 519,499.220 oz Brinks hsbc |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 80 CONTRACT(S) 400,000 OZ) |

| No of oz to be served (notices) | 46 contracts (230,000 oz) |

| Total monthly oz silver served (contracts) | 2936 contracts 14,680,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 0 deposits

JPMorgan has a total silver weight: 185.232 million oz/355.505 million =52.09% of comex

ii) Comex withdrawals: 2

a) BRINKS: 208,189.770 OZ

b) out of HSBC: 311,309.450 oz

total withdrawal 519,499.220 oz

we had 0 adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 82.421 MILLION OZ

TOTAL REG + ELIG. 354.505 MILLION OZ

TOTAL NO OF CONTRACTS SERVED UPON THIS MONTH: 2838 CONTRACTS FOR 14,190,000 OZ

CALCULATION OF SILVER OZ STANDING FOR JANUARY

NUMBER OF NOTICES FILED TODAY: 1 NOTICES OR 5,000 OZ

silver open interest data:

FRONT MONTH OF JAN//2022 OI: 126 CONTRACTS GAINING 68 contracts on the day

We had 17 notices filed for TUESDAY so we GAINED 85 contracts or 425,000 additional oz will stand for delivery in this non active delivery month of January.

FOR FEB WE HAD A LOSS OF 0 CONTRACTS REMAINING AT 577

FOR MARCH WE HAD A GAIN OF 1823 CONTRACTS UP TO 114,862 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 80 for 400,000 oz

Comex volumes: 46,732// est. volume today//POOR

Comex volume: confirmed YESTERDAY: 58,485 contracts (FAIR)

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 2936 x 5,000 oz =. 14,680,000 oz

to which we add the difference between the open interest for the front month of JAN (126) and the number of notices served upon today 80 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JAN./2021 contract month: 2936 (notices served so far) x 5000 oz + OI for front month of JAN (126) – number of notices served upon today (80) x 5000 oz of silver standing for the JAN contract month equates 14,910,000 oz. .

We GAINED 85 contracts or an additional 425,000 oz will stand for delivery on this side of the pond.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

GLD

JAN 26/WITH GOLD DOWN $21.60 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES INTO THE GLD///INVENTORY RESTS AT 1013.10 TONNES

JAN 25/WITH GOLD UP $10.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 24/WITH GOLD UP $10.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: AN UNBELIEVABLE DEPOSIT OF 27.59 TONNES INTO THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 21/WITH GOLD DOWN $10.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 980.86 TONNES

JAN 20/WITH GOLD UP $.20 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 980.86 TONNES

JAN 19/WITH GOLD UP $29.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 5.27 TONNES INTO THE GLD/INVENTORY RESTS AT 981.44 TONNES

JAN 18/WITH GOLD DOWN $3.25//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 14/ WITH GOLD DOWN $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 13/WITH GOLD DOWN $5.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 12/WITH GOLD UP $8.65//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 11/WITH GOLD UP $19.25/A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FROM THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 10/WITH GOLD UP $2.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.08 TONNES

JAN 7/WITH GOLD UP $8.15//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWLA OF 1.16 TONNES FROM THE GLD////INVENTORY RESTS AT 978.83 TONNES

JAN 6/WITH GOLD DOWN $35.30//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .32 TONNES/INVENTORY RESTS AT 979.99 TONNES

JAN 5/WITH GOLD UP $10.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 980.31 TONNES

Jan 4/WITH GOLD UP $14.00//A HUGE CHANGE OF 4.65 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 980.31 TONNES

JAN 3/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 31/WITH GOLD UP $14.05 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 30/WITH GOLD UP $7.75 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 29/WITH GOLD DOWN $5.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 975.66 TONNES

DEC 28/WITH GOLD UP $2.00 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 973.63 TONNES

DEC 27/WITH GOLD DOWN $2.05: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.63 TONNES.

DEC 23/WITH GOLD UP $9.85 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.94 TONNES FROM THE GLD/// INVENTORY RESTS AT 973.63 TONNES

DEC 22/WITH GOLD UP $12.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 21/WITH GOLD DOWN $7.05 TODAY, NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 20/WITH GOLD DOWN $9.65 TODAY; A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.37 TONNES INTO THE GLD///INVENTORY RESTS AT 977.20 TONNES

DEC 17/WITH GOLD UP $7.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.20 TONNES

CLOSING INVENTORY: 1013.10 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SLV

JAN 26/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 25/WITH SILVER UP 10 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.311 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 535.003 MILLION OZ/

.JAN 24/WITH SILVER DOWN 48 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.8 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 532.692 MILLION OZ//.

JAN 21/WITH SILVER DOWN 41 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 527.792 MILLION OZ

JAN 20/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.998 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 527.792 MILLION OZ

JAN 19/WITH SILVER UP 71 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.942 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 525.804 MILLION OZ

JAN 18/WITH SILVER UP 51 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS OF 1.11 MILLION OZ AND 1.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 527.246 MILLION OZ//

JAN 14/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 529.780 MILLION OZ//

JAN 13/WITH SILVER DOWN 2 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 832,000 OZ FROM THE SLV////INVENTORY RESTS AT 529.780 MILLION OZ

JAN 12/WITH SILVER UP 38 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//

JAN 11/WITH SILVER UP 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ/.

JAN 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 7/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 6/WITH SILVER DOWN 94 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL PF 226,000 OZ FROM THE SLV///INVENTORY RESTS AT 530.612 MILLION OZ?/

JAN 5/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 4/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 3/WITH SILVER DOWN 45 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.219 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 530.838 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC30/WITH SILVER UP 14 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.624 MILLILON OZ FROM THE SLV.//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 29/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ/

DEC 28/WITH SILVER UP 9 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.682 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 27/WITH SILVER UP 6 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681

DEC 23/WITH SILVER UP 19 CENTS TODAY:A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 22/WITH SILVER UP 29 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 538.883 MILLION OZ/

DEC 21/WITH SILVER UP 19 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.728 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 540.085 MILLION OZ

DEC 20/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 538.282 MILLION OZ

DEC 17/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 538.282 MILLION OZ//

CLOSING INVENTORY: 535.003 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Mainstream Suddenly Realizes Raising Interest Rates In A World Buried In Debt Might Be A Problem

WEDNESDAY, JAN 26, 2022 – 08:29 AM

Authored by Michael Maharrey via SchiffGold.com,

The Federal Reserve is talking about raising interest rates. But the US economy is buried under piles of debt. I’ve been asking how this is going to work for months. Apparently, the question has finally occurred to the mainstream.

A CNBC article declared, “Fed rate hikes will intensify a global debt crisis, research warns.”

Well, yeah. Duh.

According to the study came from a UK non-profit the Jubilee Debt Campaign, debt payments rose in developing countries by 120% between 2010 and 2021. They are currently at their highest levels since 2001.

The sharp increase in debt payments is hindering countries’ economic recovery from the pandemic, the report suggested, and rising US and global interest rates in 2022 could exacerbate the problem for many lower income countries.”

The study and the CNBC article are really a pitch for debt cancellation, but their narrative swerves into an unpleasant truth for US policymakers. Raising interest rates in a world awash in red ink is going to be a problem. And not just for “developing countries.”

The US government is closing in fast on $30 trillion in debt with no end to the borrowing and spending in sight. The federal government managed to run a deficit in December despite record receipts.

In December alone, the federal government spent $508 billion. The was the highest December spending level ever. Through the first three months of fiscal 2022, the federal government has already spent $1.43 trillion. That’s a record for the first quarter of any fiscal year.

Raising interest rates will drastically increase the cost of servicing all of that debt. And it will increase the cost of borrowing more money for the Biden spending coming down the pike.

In the fiscal year 2020, Uncle Sam spent $345 billion in net interest payments alone, despite near-zero interest rates. The nonpartisan Committee for a Responsible Federal Budget found that even a 2% increase in interest rates would cause net interest payments to rise to a whopping $750 billion. And this estimate was calculated before the passage of the American Rescue Plan and the Bipartisan Infrastructure Bill. That was followed up with a big surge in interest rates on US Treasuries. In other words, $750 billion underestimates the cost.

On top of that, American consumers are buried under debt. Consumer debt jumped 11% year-on-year in November. It was the biggest single-month jump in consumer debt in 20 years. Total consumer debt now stands at over $4.41 trillion. And that doesn’t include mortgages.

Revolving debt – primarily credit card balances – grew by a staggering 23.4% year-on-year in November. That was the biggest increase since 1998.

And that’s not all. Businesses and corporations are also leveraged to the hilt.

The year 2020 set a record for corporate debt issuance with $2.28 trillion of bonds and loans, comprising both new bonds and bonds issued to refinance existing debt.

All of this debt is a feature of the Fed’s loose monetary policy – not a bug.

The Federal Reserve and the US government have built a post-pandemic “economic recovery” on stimulus and debt. It is predicated on consumers spending stimulus money borrowed and handed out by the federal government or running up their own credit cards.

Now, the Fed is threatening to turn off that easy money spigot. How is that going to work? How will consumers buried under more than $1 trillion in credit card debt pay those balances down with interest rates rising? With rising rates, minimum payments will rise. It will cost more just to pay the interest on the outstanding balances.

Overleveraged companies have the same problem.

And so does the US government.

This does not bode well for an economy that depends on borrowing and spending to sustain itself.

The only reason Americans can borrow money is because the Fed is enabling them. It holds interest rates artificially low. That’s how the economy works. And that’s why I think the Fed will ultimately relent on any move it makes toward tighter monetary policy. As Peter Schiff put it, the Fed can’t do what it’s claiming it will do.

END

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,James RICKARDS

3.Chris Powell of GATA provides to us very important physical commentaries

Silver is on the launchpad, GATA’s Steer tells Wall Street Silver

Submitted by admin on Tue, 2022-01-25 11:59 Section: Daily Dispatches

11:58a ET Tuesday, January 25, 2022

Dear Friend of GATA and Gold:

GATA board member Ed Steer, editor of Ed Steer’s Gold & Silver Digest, was interviewed by the Wall Street Silver boys a few days ago and said that silver supplies are tight and that the metal is “on the launchpad.”

The interview is 17 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

A good read: Federal agency hides bank identities in a study of dangerous derivatives. They also highlight non bank entities engaging in dangerous derivatives

(Pam and Russ Martens/Wall Street on Parade)

Pam and Russ Martens: Federal agency hides bank identities in study of dangerous derivatives

Submitted by admin on Tue, 2022-01-25 12:06 Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Tuesday, January 25, 2022

The Office of Financial Research is the federal agency created under the Dodd-Frank financial reform legislation of 2010. Its role is to provide early warnings to U.S. bank regulators and the public of systemic risks that threaten U.S. financial stability, so that another 2008-style Wall Street crisis can never again devastate the U.S. economy.

The OFR was doing an outstanding job of sounding alarm bells until the Trump administration gutted the agency. The Biden administration has clearly not done enough to restore the integrity of the office.

Consider the research report that was released by the OFR on July 12 of last year, which we just discovered yesterday. The report is titled: “Counterparty Choice, Bank Interconnectedness, and Systemic Risk.” The researchers, Andrew Ellul and Dasol Kim, examined 18 different over-the-counter (OTC) derivative markets and noted the following:

“Bank interconnectedness through the OTC derivative markets was identified as an important factor that contributed to the severity of the Great Financial Crisis…and remains an area of fragility of systemically important banks on which we have very limited understanding. The trading of OTC derivatives is notoriously concentrated in the largest banks, which are also the ones for which we have data. One important feature is the substantial counterparty risk that banks face, in our context the most important counterparty risk is that faced by banks trading with non-bank entities.”

Exactly who are these “non-bank entities”?

According to the researchers, banks are increasingly using non-financial corporations on the other side of their derivative trades. …

… For the remainder of the report:

END

Interesting! the strange correlation on the price of Comex silver and GDX which is an exchange traded fund of gold miners.

(Craig Hemke)

Craig Hemke: The strange correlation of Comex silver and GDX

Submitted by admin on Tue, 2022-01-25 22:16 Section: Daily Dispatches

By Craig Hemke

Sprott Money, Toronto

Tuesday, January 25, 2022

As we all await the latest Federal Open Market Committee mutterings on Wednesday, I thought it might be fun to write this week about something you may not have noticed. And what’s that?

It’s the curious yet almost 100% long-term correlation between the price of Comex silver and the price of the popular gold mining share exchange-traded fund with the symbol GDX.

Now on the surface you wouldn’t expect these two to be so closely correlated. And why would you? Why would the price of Comex silver be in any way connected to the prices of shares in major, producing gold mining companies? …

… For the remainder of the analysis:

https://www.sprottmoney.com/blog/COMEX-Silver-and-the-GDX-Craig-Hemke-January-25-2022

end

4.OTHER GOLD COMMENTARIES

END

5.OTHER COMMODITIES/

end

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.3225

OFFSHORE YUAN: 6.3262

HANG SANG CLOSED UP 46.29 PTS OR 0.19%

2. Nikkei closed DOWN 120.01 PTS OR 0.44%

3. Europe stocks ALL GREEN

USA dollar INDEX UP TO 96.09/Euro FALLS TO 1.1278-

3b Japan 10 YR bond yield: FALLS TO. +.140/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 114.18/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 86.40 and Brent: 89.18-

3f Gold UP /JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE CLOSED UP// OFF- SHORE UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO -.0.072%/Italian 10 Yr bond yield RISES to 1.30% /SPAIN 10 YR BOND YIELD RISES TO 0.66%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.37: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 1.65

3k Gold at $1845.65 silver at: 23.86 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble DOWN 46/100 in roubles/dollar AT 79.17

3m oil into the 86 dollar handle for WTI and 89 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 114.18 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9205– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0382 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 1.787 UP 1 BASIS PTS

USA 30 YR BOND YIELD: 2.130 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.55

Futures Surge After Microsoft Reversal With All Eyes On Fed

WEDNESDAY, JAN 26, 2022 – 08:09 AM

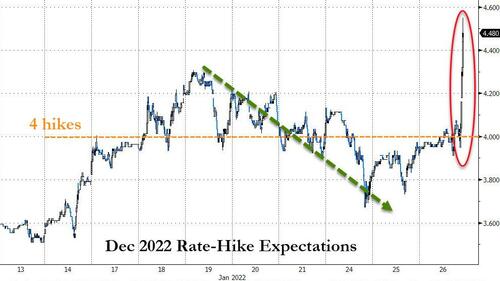

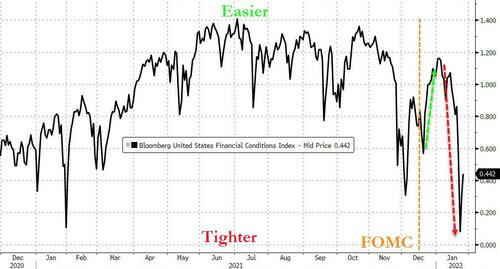

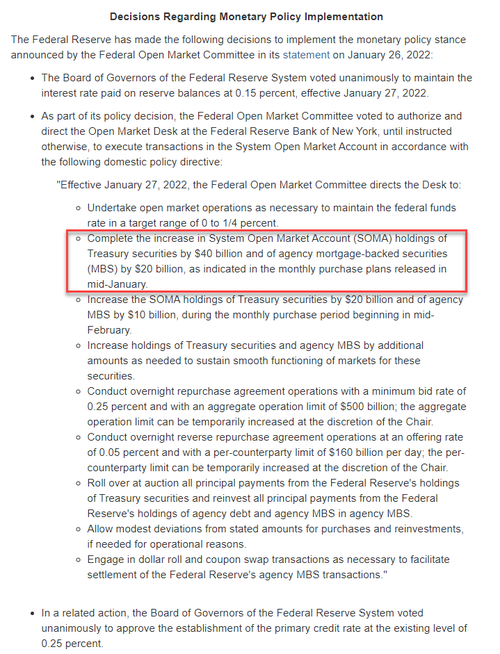

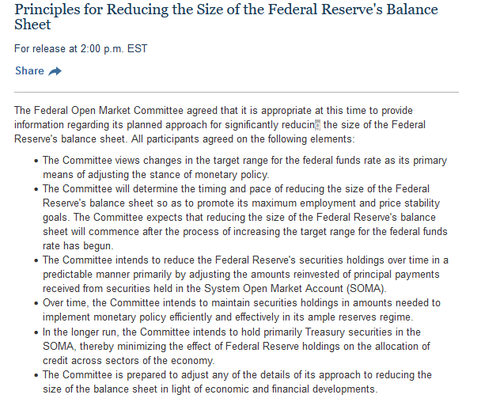

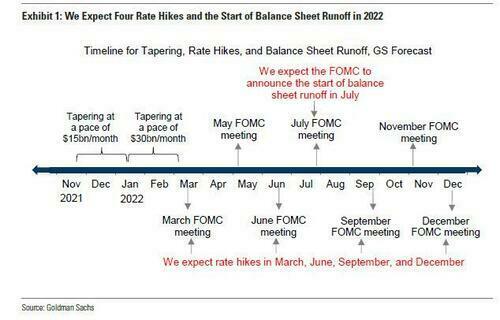

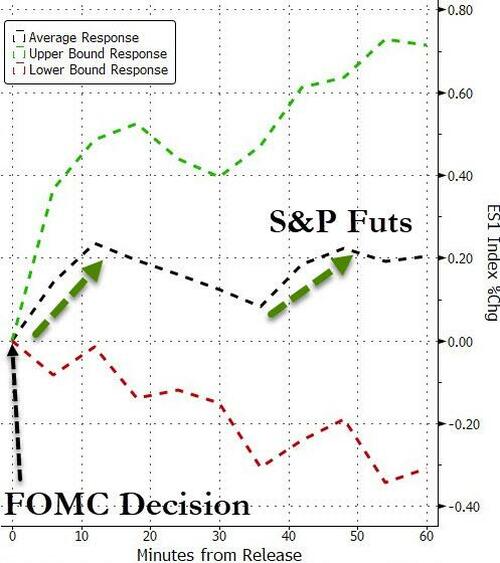

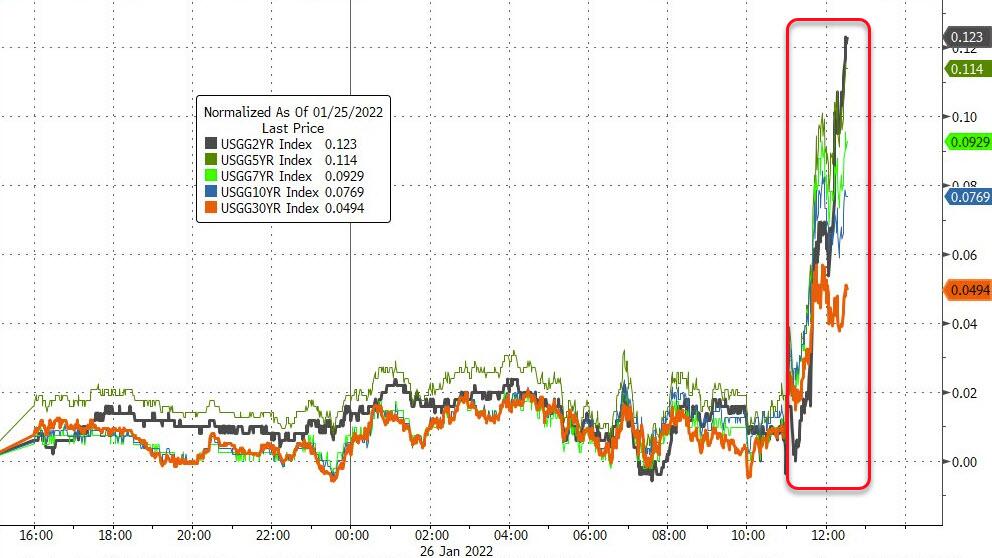

Yesterday, after Microsoft stock initially slumped despite beating across the board as the skeptical market latched on to even the smallest weakness to hammer the stock, dragging down both the Nasdaq and S&P futures close to session lows, we said that the reaction was premature and would reverse, as the earnings release did not include guidance and would promptly reverse once the company revealed its cloud guidance in its conference call a little over an hour later. Well, that’s precisely what happened and after first tumbling as much as 5% after hours, the 2nd largest US company (MSFT has $2.2 trillion in market cap) reversed all losses and is now trading solidly in the green, sparking broader tech momentum, lifting the Nasdaq as much as 2.1% this morning and (briefly) helping traders forget that today at 2pm the Fed is expected to unveil a March rate hike and balance sheet runoff a few months later.

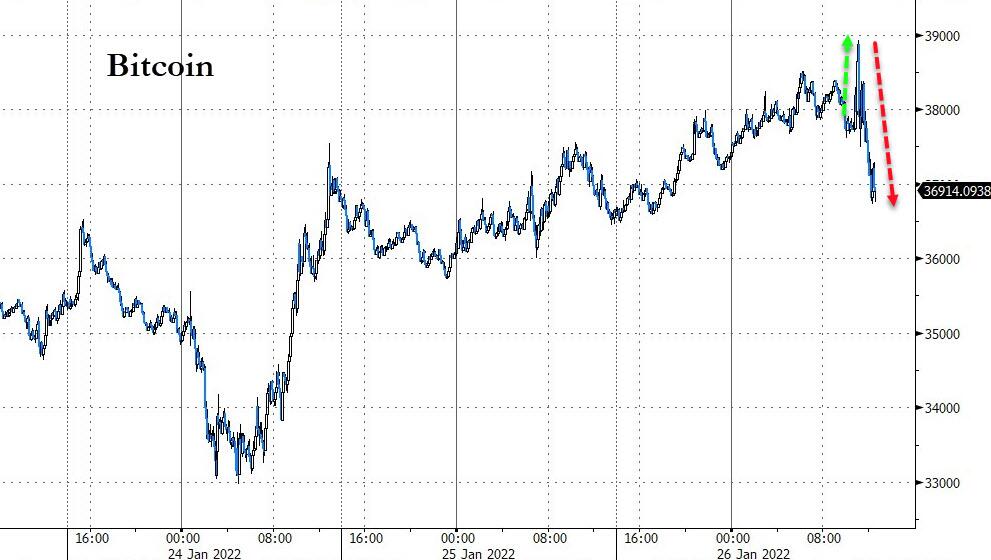

Indeed, contracts on the Nasdaq 100 led broad-based gains – which would have been gaping losses had MSFT failed to reverse late on Tuesday – as U.S. stock futures rallied, with investors bracing for the Federal Reserve’s decision and preparing for a slew of earnings from companies including Tesla, Intel and Boeing. Nasdaq 100 futures jumped as much as 2.1% while S&P 500 and Dow Jones futures also rallied. The VIX fell from a one-year high, snapping six days of gains. Elsewhere, the Stoxx Europe 600 rose 2% in the biggest jump in seven weeks. 10Y TSY yields rose to 1.79% with the Fed’s policy announcement in the limelight; the dollar was slightly higher, as was Bitcoin while Brent oil traded just shy of $90 on its way to triple digits.

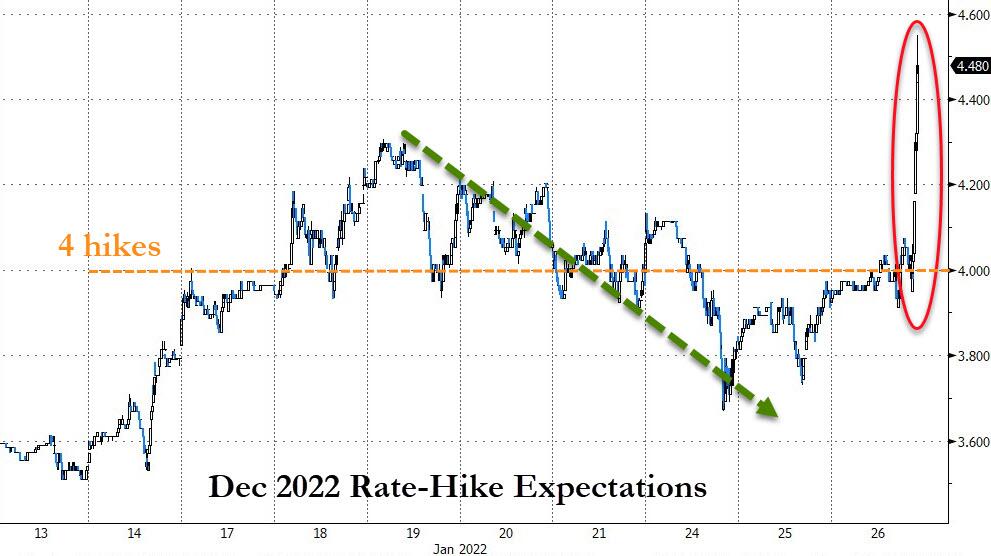

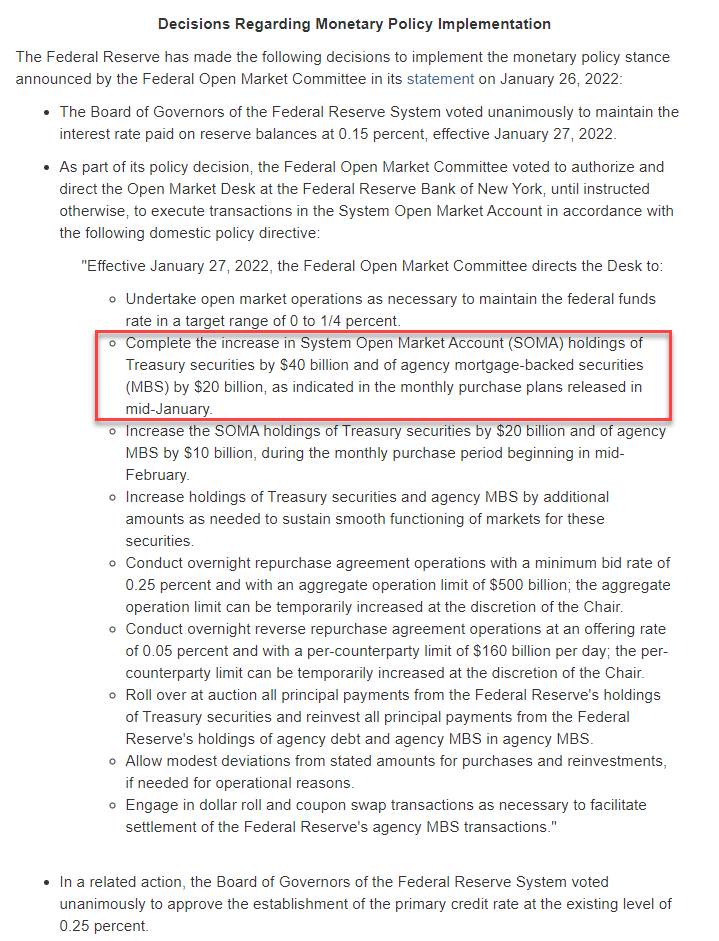

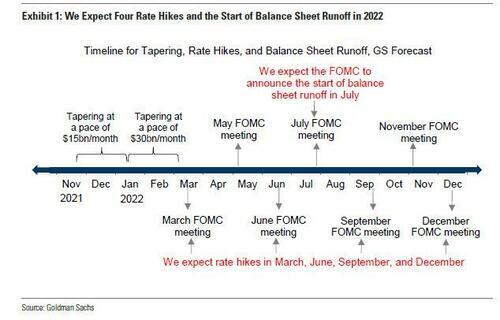

Of course, the big event today is the Fed policy statement at 2pm ET and press conference 2:30pm, which are expected to ratify expectations for rate increases beginning in March

- Short-term interest rate futures price in just 1bp of rate-hike premium for January meeting but fully price in 25bp for March

- Commentary on shrinking the central bank’s balance sheet is also anticipated

We will have a detailed post on what to expect from the Fed shortly.

“We expect inflation to remain high and interest rates to rise more than investors are expecting today,” said Norbert Frey, head of portfolio management at Fuerst Fugger Privatbank. “A rising interest rate environment is leading to a revaluation of all business models and we think 2022 can be a year of value stocks.”

While equities have had had a rocky start to 2022 as bond yields rose with investors anticipate tighter policy from the Fed, while Russia-U.S. tension added to investor concerns. Now, strategists from Goldman Sachs Group Inc. to Citigroup Inc. are saying it’s time to buy the dip.

“Any further significant weakness at the index level should be seen as a buying opportunity, in our view,” Goldman strategists including Peter Oppenheimer wrote in a note on Wednesday.

In U.S. premarket trading, Microsoft Corp rose, with analysts positive on the software maker’s outlook for growth for its Azure cloud-computing services. Shares gained 4.1% in U.S. premarket trading after initially tumbling before the market heard the company’s strong cloud guidance, with analysts positive on the software maker’s outlook for growth for its Azure cloud-computing services. Analysts also highlighted the company’s commercial bookings and a supportive IT spending backdrop. Texas Instruments shares also rose 4% after the chipmaker gave a first-quarter forecast that was stronger than expected, with analysts noting the company’s conservatism amid a still supportive demand backdrop. Texas Instruments also reported its fourth-quarter results. Other notable premarket movers:

- Cryptocurrency-exposed stocks in Europe and the U.S. are trading higher as Bitcoin kept regaining ground ahead of the Federal Reserve decision. Marathon Digital (MARA US) +6%, (RIOT US) Riot Blockchain +5%, (COIN US) Coinbase +3.4%.

- Electric vehicle stocks climb in U.S. premarket trading ahead of Tesla’s fourth-quarter results due Wednesday after the market close. Rivian (RIVN US) +3.5%; Tesla (TSLA US) +4.4%; Nikola (NKLA US) +3.6%.

- Moderna’s (MRNA US) stock valuation “makes a lot more sense” after more than halving since Deutsche Bank initiated in October, prompting the broker to upgrade the vaccine maker to hold from sell. Shares gain 4.6% premarket.

- Capital One (COF US) reported adjusted earnings per share for the fourth quarter that beat the average analyst estimate. Shares dropped postmarket, with higher expenses “the only wrinkle” in the bank’s quarter, according to Vital Knowledge.

- Stride (LRN US) shares gained 7% postmarket Tuesday after the technology-based education company boosted its revenue forecast for the full year. The guidance beat the average

Global stocks have shed about 7% in January, on track for the worst month since the pandemic roiled markets back in 2020. Some strategists are optimistic about the outlook following the declines.

“The growth-policy trade-off may be less favourable, yet we think a lot of bad news is now priced in,” Emmanuel Cau, head of European equity strategy at Barclays Plc, wrote in a note. “Starts of policy normalisation typically bring higher volatility but rarely terminate bull markets, although higher-than-usual P/E multiples mean equities are more rates-sensitive this time.”

In the latest developments involving Russia and Ukraine, president Joe Biden said he would consider personally sanctioning Vladimir Putin if he orders an invasion of Ukraine, escalating efforts to deter the Russian leader from war. In response, Russian Foreign Minister Sergei Lavrov signaled that Moscow will respond to any “aggressive” action by the U.S. and its European allies as Germany and France pursue efforts to broker a peaceful resolution to the tensions over Ukraine.

European equities rally, brushing off geopolitical tensions, with most indexes clawing back roughly 3/4 of Monday’s sharp sell off to rise over 2%. Europe’s Stoxx 600 adds as much as 2% with travel, energy, miners and autos leading what is broad sectoral support. Here are some of the biggest European movers today:

- Vestas Wind Systems shares rise as much as 6%, reversing an earlier decline, after guidance for 2022 was met with relief. Handelsbanken analysts said the guidance miss was unsurprising, and the market likely feared it would be worse.

- Other European renewables stocks — which have been hit hard in the recent selloff — gain after Vestas’ update, rebounding after declines triggered by Siemens Gamesa’s profit warning last week.

- Travel and leisure is the best-performing sector among Stoxx 600 groups on Wednesday. Airlines including Lufthansa and IAG lead gains, with the German carrier upgraded to buy at Stifel.

- AutoStore advances after being raised to buy at Citi. The upgrade follows a slump of more than 50% amid uncertainty regarding patent litigation and a broader sell-off in tech stocks.

- De Longhi rises as much as 8.9%, the most intraday since March 2021, after Equita upgrades to buy from hold, citing recent underperformance and more confidence in the company’s coffee business.

- Essity falls the most since Oct. 2020 after the Swedish hygiene products manufacturer reported weaker-than-expected earnings and announced further price hikes in 2022.

- Orpea shares continued their descent after its CEO was summoned to the French minister for elderly policy. The French nursing home operator also denied reports it had offered a journalist money to not publish a book critical of the company.

- Barry Callebaut shares fell, reversing earlier gains, after reporting 1Q sales. Citi noted “some more caution” on commodities amid waning supply of cocoa beans.

Earlier in the session, stocks in Asia were mixed after slumping across the board in the previous session, as investors awaited the Federal Reserve’s policy decision. The MSCI Asia Pacific Index was down 0.1%, on track to fall for a fourth day, with advances in communication services and financials offsetting losses in technology shares. Benchmarks in China, Hong Kong and Singapore were among the gainers, while Japan’s Topix Index fell deeper into correction territory. Asian equities have tumbled this month amid heightened volatility on the prospect of U.S. monetary-policy tightening, with the Fed expected to telegraph a March interest-rate hike on Wednesday. Worries over rising rates sent a gauge of the region’s tech hardware stocks to its lowest in months on Wednesday, with chipmakers TSMC and Samsung Electronics among the biggest drags. “There’s a lot of noise in the market right now, and I don’t think anyone’s confident that this is the bottom, because we aren’t sure about Fed policy yet,” said Kyle Rodda, analyst at IG Markets. Despite the broader drop in tech shares, Tencent advanced on dip-buying, helping to boost the Hang Seng Tech Index. The CSI 300 Index whipsawed to narrowly avoid entering a bear market

Fixed income takes a back seat. Curves adopt a modest bear steepening theme with gilts underperforming both bunds and USTs by 1-2bps. Eurodollars bear flatten a touch ahead of today’s FOMC meeting. Peripheral and semi-core spreads narrow with Italy, Belgium and France outperforming.

Treasuries are under pressure in early U.S. trade with U.S. stock index futures higher by 1%-2%, European benchmarks by 2%-3%, with travel, energy, miners and autos leading a broad advance. Front-end yields cheaper by more than 2bp with most curve spreads within 1bp of Tuesday’s close; 10-year yields around 1.785%, outperforming gilts by ~1bp. Focal point of U.S. day is Fed policy decision and Chair Powell news conference. Auction cycle pauses for Fed, concluding with 7-year notes Thursday. The stellar 2Y & 5Y auctions are underwater after stopping through (the 5Y produced record-low dealer award), There is no Fed POMO today. IG dollar issuance slate empty so far and expected to remain slim; Treasury auctions resume with $53b 7-year note sale on Thursday, following strong demand for 2- and 5-year notes earlier this week.

In FX, Bloomberg Dollar Spot is little changed but mixed price action across much of G-10. USD/JPY rises through 114, EUR/USD dips back onto a 1.12-handle. Commodity currencies trade well as crude futures drift back toward Monday’s highs.

Bitcoin extended its gains for the week, trading near $38,000.

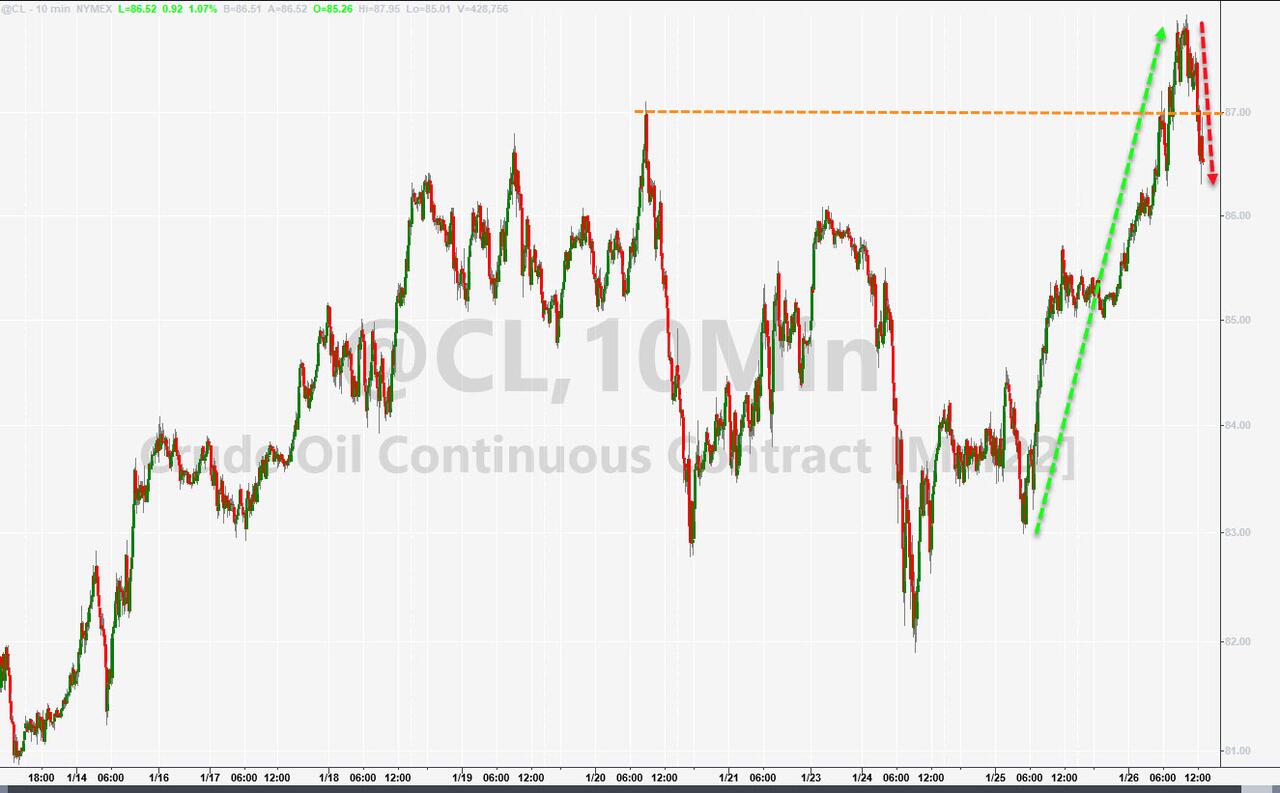

In commodities, WTI adds 0.6%, regaining a $86-handle after the latest APIR report showed a draw in U.S. stockpiles and investors tracked tensions over Ukraine for signs the conflict may disrupt supplies. Brent climbs to about $89. Spot gold trades a tight range near $1,846/oz. Most base metals are well bid, lead by LME copper and tin; aluminum underperforms.

Looking at the day ahead now, the main highlight will be the aforementioned Federal Reserve decision and Chair Powell’s subsequent press conference, whilst there’s also a policy decision from the Bank of Canada. On the data side, we’ve got US new home sales for December, along with the preliminary December reading of wholesale inventories. Meanwhile earnings releases include Tesla, Abbott Laboratories, Intel, AT&T and Boeing.

Market Snapshot

- S&P 500 futures up 1.2% to 4,399.50

- STOXX Europe 600 up 1.8% to 467.79

- MXAP down 0.1% to 186.79

- MXAPJ little changed at 612.28

- Nikkei down 0.4% to 27,011.33

- Topix down 0.3% to 1,891.85

- Hang Seng Index up 0.2% to 24,289.90

- Shanghai Composite up 0.7% to 3,455.67

- Sensex up 0.6% to 57,858.15

- Australia S&P/ASX 200 down 2.5% to 6,961.63

- Kospi down 0.4% to 2,709.24

- German 10Y yield little changed at -0.08%

- Euro down 0.2% to $1.1284

- Brent Futures up 0.8% to $88.92/bbl

- Gold spot down 0.1% to $1,846.69

- U.S. Dollar Index up 0.15% to 96.09

Top Overnight News from Bloomberg

- Federal Reserve policy makers are poised to signal plans for their first interest rate hike since 2018 and discuss shrinking their bloated balance sheet as they seek to restrain the hottest inflation in nearly 40 years

- The Treasury market appears more likely to respond in a logical way to Wednesday’s Federal Reserve communications because of indications that the past week’s U.S. stock-market bloodbath cleared out a crowded camp of bets on higher yields

- The employment cost index, which Federal Reserve Chair Jerome Powell cited in December as a key reason for the central bank’s pivot to a more aggressive stance on inflation, is seen registering a fourth-quarter gain nearly on par with the record increase in the prior three months

- Lithuanian Central Bank Governor Gediminas Simkus warned that Europe’s economy would suffer a significant blow if tensions escalate further between Russia and Ukraine, urging politicians to step up efforts to deter hostilities

- OPEC and its allies are expected by delegates to stick to their plan and ratify another modest production increase next week as they try to satisfy rebounding oil demand

A more detailed look at global markets courtesy of Newsquawk

In Asian trading, APAC markets were subdued ahead of the FOMC and holiday-quietened conditions. Nikkei 225 (-0.4%) oscillated around the 27k level after record daily COVID-19 cases. KOSPI (-0.4%) faded opening gains with attention on earnings. Hang Seng (+0.2%) and Shanghai Comp. (+0.7%) were mixed as PBoC liquidity efforts and government support signals were offset as Evergrande default woes resurfaced.

Top Asian News

- Foreigners Cash Out of Key Asian Emerging Markets Before Fed

- China to Start Three-Year Crackdown on Money Laundering

- China Criticizes U.S. Diplomats Seeking Exit Over Covid Rules

- China South City Bonds Rally as Consent Given to Extend 2022s

European bourses are firmer in an extension of yesterday’s upside, with the Stoxx 600 +2.0% on the session but still lower on the week. US futures are firmer across the board with the NQ, +2.0%, outpacing and benefitting from MSFT post earnings, +4.0% in pre-market. European sectors are all in the green with Travel & Leisure outperforming amid broker action while Oil & Gas is a relatively close second given crude action. EU antitrust decision against Intel (INTC) has been annulled in part by the EU General Court. Microsoft (MSFT) Q2 2022 (USD): EPS 2.48 (exp. 2.31), Revenue 51.73bln (exp. 50.88bln). Co. sees Q3 product revenue between USD 15.6bln-15.8bln and expects Azure revenue growth to increase significantly, while it guides Q3 rev. USD 48.5bln-49.3bln (implied) vs exp. USD 47.7bln. +4.0% in the pre-market.

Top European News

- Inflation Outlook No Reason for ECB to Change Track: Simkus

- Italy Asks Firms Not to Meet With Putin Amid Ukraine Crisis

- Finland ‘Wise’ to Sell Long-Maturity Debt Ahead of ECB Tapering

- Europe Travel Stocks Gain on Airlines Boost; Lufthansa Upgraded

In FX, Loonie loving risk recovery and WTI revival in run up to likely BoC hike. Aussie rebounds in absence of those away for a national holiday. Greenback stands firm awaiting something hawkish from the Fed. Kiwi hovering ahead of NZ CPI. -Pound pensive before Partygate findings are published. Rouble unable to benefit from Brent bounce as Russia begins big drills in Black Sea to keep geopolitical tensions elevated.

In commodities, WTI and Brent March futures have continued grinding higher despite quiet news flow as focus remains on geopolitics and the benchmarks also benefit from equity action. At best, WTI and Brent have surpassed USD 86.00/bbl and USD 89.00/bbl respectively thus far. Spot Gold remains contained amid relatively rangebound USD action while Silver is buoyed ahead of USD 24.00 /oz and touted resistance marks. US Private Energy Inventory Data (bbls): Crude -0.9mln (exp. -0.7mln), Gasoline +2.4mln (exp. +2.5mln),

Distillates -2.2mln (exp. -1.3mln), Cushing -1.0mln. Qatar’s Emir is to meet US President Biden on Monday to discuss Afghanistan and contingency plans to supply natural gas to Europe in the event of a Russian invasion of Ukraine. Qatar Emir and US President Biden are to discuss additional Qatari gas supplies to Europe in the case of a Russian-Ukraine conflict at next week’s discussions, via Reuters sources; Qatar has little spare gas for Europe as most gas is pre-sold.

Geopolitics

- US State Department said the US hasn’t seen the de-escalation that is necessary if diplomacy and dialogue with Russia is to prove successful, while US Department of Defense Spokesman Kirby said the US will not rule out adding further troops to the already 8,500 on alert.

- Ukraine Foreign Ministers says the proposals the US will send to Russia do not raise Ukraine’s objections; subsequently, Moscow says received some answers to security guarantee proposals, but not in written form – awaiting further details.

- Ukrainian President Zelensky said the situation in the east is under control and they are working to establish that the meeting of Presidents of Ukraine, Russia, Germany, and France takes place as soon as possible.

- Russian navy has commenced large-scale training in the Black Sea, according to Ifax.

- UK Foreign Minister Truss, when question if they would sanction Russia’s Putin, says they are not ruling anything out.

- Ukraine envoy to Japan said that they are fully committed to a diplomatic solution to the current tensions with Russia, while the envoy also stated that a full-scale war is very difficult to expect although they may see more localised conflict.

US Event Calendar

- 7am: Jan. MBA Mortgage Applications, prior 2.3%

- 8:30am: Dec. Advance Goods Trade Balance, est. -$96b, prior -$97.8b, revised -$98b

- 8:30am: Dec. Retail Inventories MoM, est. 1.5%, prior 2.0%; Wholesale Inventories MoM, est. 1.2%, prior 1.4%

- 10am: Dec. New Home Sales MoM, est. 2.1%, prior 12.4%; New Home Sales, est. 760,000, prior 744,000

- 2pm: FOMC Rate Decision

DB’s Jim Reid concludes the overnight wrap

With markets awaiting today’s policy decision from the Federal Reserve, yesterday marked another volatile session that saw the resumption of the equity selloff as investor jitters remained at the prospect of monetary policy tightening alongside burgeoning geopolitical tensions. Indeed, in many ways it was a repetition of Monday’s session with a further bout of wild intraday swings. At the start, the S&P 500 sold off heavily after the US open to hit an intraday low of -2.79%, with the index back in correction territory. Then it recovered to actually move back into the green for a few minutes, before selling off in the last hour to finish the day down -1.22%, closing -9.18% off its all-time highs reached at the start of the year. With Fed policy so acutely driving risk assets in recent weeks, it sets up an interesting day of communications ahead for the FOMC.

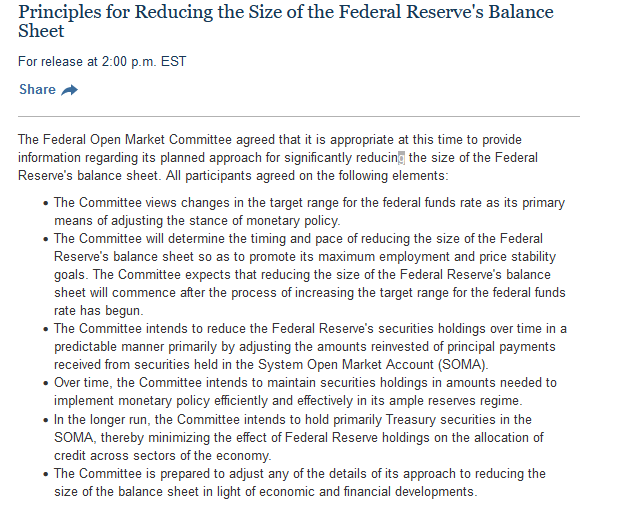

On that front, the Fed are expected to telegraph the start of their latest hiking cycle today, and our US economists write in their preview (link here) that the meeting statement and Chair Powell’s subsequent press conference should confirm that lift-off in the policy rate is likely at the following meeting in March. It comes as the unemployment has now fallen back beneath 4% for the first time since the pandemic began, while CPI in December hit +7.0% year-on-year for the first time since 1982. Our economists’ baseline is for that March hike to be the first of 4 this year, although as they’ve written recently (link here) there is the tail risk of a more aggressive pace still. The market agrees: pricing liftoff for March and 3.96 total hikes through the rest of the year. Balance sheet policy will be of particular focus. Our US econ team believes the Fed will begin QT in Q3. The year-to-date selloff of real rates and equity markets began with the Fed surprising markets by how much they were already considering an early and aggressive use of QT to augment their tightening of policy, so any incremental information will be devoured. While it’s likely too early for the Fed to deliver specific QT details today, our economists believe it’s possible Chair Powell begins to socialise a range of potential QT outcomes to start the give-and-take involved with guiding market expectations. Also of interest will be whether Powell is asked about the possibility of a larger +50bps increase in rates at some point, which had been the topic of some speculation before the latest selloff should the Fed need to tighten financial conditions quickly.

Back to the equity selloff, and there wasn’t a consistent sectoral revival story to tell yesterday, with the volatility sending the VIX higher for a 6th consecutive session to 31.16pts, the longest run of gains in over a year. Tech ended the day as the worst performer, down -2.34%, after rallying in the middle of the session, and the NASDAQ finished the day down -2.28%. Energy (+3.96%) was the key outperformer on the other hand, followed by financials (+0.47%) as the only other sector that managed to finish the day higher. Those moves came as oil rebounded from Monday’s losses, with Brent crude (+2.24%) and WTI (+2.75%) both advancing. After the close we also got earnings from Microsoft, which beat analyst sales and earnings expectations. The stock was slightly higher in after-hours trading on the growth prospects of the company’s cloud computing services. Later today we’ll get Tesla’s earnings and Apple’s tomorrow.

Amidst the equity volatility, sovereign bonds were comparatively subdued again yesterday, with yields on 10yr Treasuries down a paltry -0.2bps to 1.77%. The yield curve managed to flatten, with the 2s10s slope down -4.8bps yesterday to 74.8bps, its lowest closing level in almost a month. This is one of a number of classic late-cycle indicators Jim mentions in the chartbook, and it’s worth noting that on average the 2s10s curve has flattened by around 80bps following the first year of a hiking cycle, so if the Fed does hike in March and the curve follows that historic playbook, we could be looking at an inversion within the next 12-18 months.

Overnight in Asia, equities are putting in a more mixed performance, with the Nikkei (-0.21%), the Kospi (-0.33%) and the Hang Seng (-0.14%) seeing modest falls, whilst the Shanghai Comp is up +0.14%. Futures are pointing to a more positive session in the US and Europe today however, with those on the S&P 50 (+0.20%) and the DAX (+0.49%) both moving higher.

Back in Europe, markets followed a very different playbook yesterday. Having not been open at the time of the late US recovery on Monday, European equities advanced across the board following their rout at the start of the week, and the STOXX 600 rose +0.71%. Meanwhile, with the ECB’s Governing Council not meeting until next week, sovereign bonds also diverged from the US, with yields on 10yr bunds (+2.7bps), OATs (+2.7bps) and gilts (+3.8bps) all moving higher on the day.

With tensions remaining high between Russia and the West over Ukraine, President Biden said in response to a question that the US would consider personal sanctions against President Putin in the event of a Russia invasion. Sanctions against heads of state are an extremely rare step, but the US and others have already threatened severe sanctions if an invasion took place.

On the data side, the Conference Board’s consumer confidence index for January fell a bit less than expected to 113.8 (vs. 112.2 expected). It came as the present situation reading rose to 148.2, but the expectations measure fell to 90.8. Separately in Germany, the Ifo’s business climate indicator in January rose to 95.7 (vs. 94.5 expected), marking the first increase in the indicator after a run of 6 consecutive monthly declines.

Finally, the IMF released their World Economic Outlook update yesterday, in which they downgraded their global growth forecast for 2022 to +4.4% (vs. +4.9% in October). That included cuts to the projections for both the advanced and emerging market economies, with the US and China among those seeing the biggest downgrades. Indeed, the US forecast for this year was cut to +4.0% (vs. +5.2% in October), and China’s was cut to +4.8% (vs. +5.6% in October). One marginal respite was that 2023 did see a modest upgrade, with global growth now projected at +3.8% (vs. +3.6% in October).

To the day ahead now, and the main highlight will be the aforementioned Federal Reserve decision and Chair Powell’s subsequent press conference, whilst there’s also a policy decision from the Bank of Canada. On the data side, we’ve got US new home sales for December, along with the preliminary December reading of wholesale inventories. Meanwhile earnings releases include Tesla, Abbott Laboratories, Intel, AT&T and Boeing.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 22.61 PTS OR 0.66% //Hang Sang CLOSED UP 46.29 PTS OR 0.19% /The Nikkei closed DOWN 120.01 PTS OR 0.44% //Australia’s all ordinaires CLOSED HOLIDAY /Chinese yuan (ONSHORE) closed UP 6.3225 /Oil UP TO 86.40 dollars per barrel for WTI and UP TO 89.19 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3225. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3262: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING STRONGER AGAINST USA DOLLAR

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

3B JAPAN

end

3c CHINA

CHINA/

end

4/EUROPEAN AFFAIRS

//EUROPE/COVID/

WHO now states that once Omicron is finished Europe will have a quiet period. No doubt Europe will reach herd immunity then. However damage from the vaccine will still prevail

(Roberts/EpochTimes)

WHO Suggests Europe Will Experience “Quiet” COVID-19 Period After Current Cases Subside

WEDNESDAY, JAN 26, 2022 – 02:00 AM

Authored by Katabella Roberts via The Epoch Times,

The World Health Organization on Monday suggested that Europe will experience a “quiet” COVID-19 period before the virus returns toward the end of the year, albeit without a full pandemic.

WHO Regional Director of Europe, Hans Kluge, told Agence France-Presse that the highly infectious Omicron variant of the CCP (Chinese Communist Party) virus, which causes COVID-19, could infect 60 percent of Europeans by March before tapering off for some time thanks to global immunity and increased vaccinations, among other things.

Omicron cases are sweeping throughout several European countries, and the EU health agency, the European Center for Disease Prevention and Control (ECDC) says that the overall level of risk to public health is “very high.”

ECDC said earlier this month that it expects more cases to emerge in the coming weeks, driven by the Omicron variant, and warned of increased worker shortages among health care and other essential workers, and potential difficulties with testing and contact tracing capacities in many EU member states.

However, once the number of cases across Europe subsides, “there will be for quite some weeks and months a global immunity, either thanks to the vaccine or because people have immunity due to the infection, and also lowering seasonality,” Kluge said.

“So we anticipate that there will be a quiet period before COVID-19 may come back towards the end of the year, but not necessarily the pandemic coming back,” he said.

Kluge’s comments come after White House chief medical adviser Dr. Anthony Fauci on Sunday said that he’s “as confident as you can be” that most of the United States will reach a peak in Omicron infections in the middle of February.

“If you look at the patterns that we’ve seen in South Africa, in the UK, and in Israel and in the northeast and New England and upper Midwest states, they have peaked and [are] starting to come down rather sharply,” Fauci told ABC’s “This Week.”

While there are still some Southern and Western states that continue to see case numbers rise, if the pattern follows the downward trend seen in other places, such as the Northeast, the United States will start to see a similar “turnaround throughout the entire country,” Fauci said.

However, the director of the National Institute of Allergy and Infectious Diseases cautioned against being “overconfident” when it comes to the virus and its potential effects across the nation.

He also noted that those areas of the country that haven’t been fully vaccinated against COVID-19 or received booster shots may still see “a bit more pain and suffering with hospitalizations.”

Kluge on Monday also cautioned that it was too early to forecast the virus becoming less severe and endemic, noting that new variants could still emerge.

“There is a lot of talk about endemic but endemic means … that it is possible to predict what’s going to happen. This virus has surprised [us] more than once so we have to be very careful,” Kluge said.

The WHO’s comments come as a growing number of European countries have rolled back their COVID-19 restrictions citing declining hospitalizations and data suggesting Omicron cases have peaked.

Beginning Jan. 27, people in the United Kingdom no longer have to wear masks in public or show proof that they’ve been vaccinated to enter some venues, Prime Minister Boris Johnson announced.

Fully vaccinated people arriving into the UK will also no longer face testing requirements as of Feb. 11.

French Prime Minister Jean Castex said on Thursday the country will start to roll back restrictions within weeks, pointing to an improvement in the country’s COVID-19 case numbers and hospitalizations.

Spanish Prime Minister Pedro Sánchez also told reporters on Jan. 10 that he wants the European Union to consider approaching COVID-19 in the same way it approaches flu.

“The situation is not what we faced a year ago,” Sánchez said in a radio interview with Spain’s Cadena SER.

“I think we have to evaluate the evolution of COVID to an endemic illness, from the pandemic we have faced up until now.”

However, Austria is moving closer to implementing a COVID-19 vaccination mandate for most adults after Parliament’s lower house on Thursday voted in favor of the proposal.

end

UK/WALES/VACCINE MANDATE

Welsh businesses demand the end of vaccine passport mandates after the government fails to prove that they work

(Watson/SummitNews)

Welsh Businesses Demand Vaccine Passport Exemptions After Government Fails To Prove They Work

WEDNESDAY, JAN 26, 2022 – 03:30 AM

Authored by Paul Joseph Watson via Summit News,

Businesses in Wales are demanding vaccine passport exemptions after the government failed to provide any evidence that the scheme prevents the spread of COVID-19.

COVID passes were introduced in Wales in October and applied to nightclubs, as well as indoor non-seated events for more than 500 people and outdoor events of more than 4,000 people.

In response to the Omicron outbreak, in December pubs were also restricted to the “rule of six” and table service only, while all nightclubs were ordered to close.

Despite restrictions supposedly being lifted later this week, nightclubs, cinemas and theaters will still be forced to demand COVID passports.

A Freedom of Information Act request was sent to the Welsh government asking for “any and all data that Welsh Government have used to develop the restrictions announced on 16th and 17th December 2021.”

“This should include but not be limited to: a. Statistical information regarding numbers of Covid cases developed from nightclubs b. Statistical information surrounding rates of transmission from businesses to be impacted by the one way system rule. c. Minutes of the meeting and all this in attendance held on 16th December by Welsh Government regarding the restrictions,” stated the FOIA request.

The government responded to to first two questions by stating, “This information is not available. There is no guarantee about where someone caught Covid-19, therefore there is no data on cases caught in specific locations.”

In other words, despite imposing COVID passports on nightclubs and numerous other venues, the government has no information on whether they work at all.

Publican Jon Bassett told Wales Online the response to the FOIA request was “unbelievable” and clearly shows that the restrictions aren’t justified.

“My WhatsApp group with other licensees is going crazy since this has gone into the public domain,” said Mr Bassett.

“I would have thought there would have to be more evidence for them to do it. I just don’t get it,” he added.

“I think there is a lot of anger because it’s been a dreadful two months. The concern we’ve got now is if there’s another variant come December this year and it happens again. I just fear we’re in a loop.”

The UK government’s own report into vaccine passports also found that the scheme not only failed to prevent the spread of the virus, it could actually worsen the situation.

England went ahead anyway and introduced vaccine passports for nightclubs in December, although those rules are set to expire later this week.

As we previously highlighted, COVID passports were introduced in Wales after a dodgy vote that the government won because a Conservative MP who was set to vote against the measure couldn’t log in to a Zoom call.

Welsh First Minister Mark Drakeford also stupidly claimed that Omicron was just as severe as Delta, while also boasting about how stricter lockdown measures had put Wales in a better place than England, despite Wales recording higher case numbers.

END

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

UKRAINE/RUSSIA/USA/ EU/UK/NATO

Crisis de-escalating fast!!

Russia-Ukraine Crisis Deescalating As NATO Countries Break From Bellicose US-UK Stance

TUESDAY, JAN 25, 2022 – 05:15 PM

Deescalation appears to be accelerating over the Ukraine crisis given a number of rapid developments which have seen lead NATO countries break from the more bellicose and threatening tone of the United States and UK. After Germany’s neutrality toward the Russia-Ukraine crisis became apparent, Sweden is the latest to follow its lead of forbidding arms transfers to Kiev, while Croatia is out with a firm statement saying it will recall all of its troops from NATO in the event of war.

This followed on the heels of Ukrainian President Volodymyr Zelensky announcing that circumstances in the region are now “under control” and that there’s “no reason to panic” according to The Associated Press.

It appears the earlier hyped messages of an ‘imminent Russian invasion’ have backfired, as Ukraine officials have now turned to castigating the media for spreading a sense of overblown panic and doom among the population. Defense Minister Oleksii Reznikov went so far as to say the threat of a Russian invasion “doesn’t exist” despite there still being “risky scenarios”. Other Ukraine defense officials have echoed this as well…

“As of today, we don’t see any grounds for statements about a full-scale offensive on our country,” Danilov had stated confidently on Monday. Here’s more from the defense chief:

“As of today, the Russian army has not formed a strike group that would be able to carry out an invasion,” Reznikov was quoted saying in local media after a meeting with lawmakers in Kyiv. “There are no grounds to think that an invasion will happen tomorrow from a military point of view.”

“But that doesn’t mean,” he said, “that they won’t develop—there are threats.”

“The Kremlin is trying to destabilize Ukraine with hybrid means, particularly by sowing panic,” he wrote in an op-ed published by Ukrainskaya Pravda a day earlier. “We must not give them the opportunity.”

This perhaps more realist sentiment is spreading, and now with a European consensus emerging that direct conflict with Russia must be avoided at all cost, the message has reached the White House, which is singing a different tune from even a day ago…

“President Joe Biden told reporters Tuesday that he does not foresee U.S. troops moving into Ukraine,” Axios writes Tuesday afternoon. Biden stressed, “There is not going to be any American forces moving into Ukraine,” which seems a reversal of the “stand by orders” he gave the day before. Here’s further details on the administration’s backing off the prior confrontational tone, as it’s looking more and more like diplomacy is winning out…

- He added that the decision to put troops on high alert is “not provocative” but intended to reassure the U.S.’ allies.

- “We have no intention of putting American forces, or NATO forces, in Ukraine. But as I said, there will be serious economic consequences if he moves,” he added, referring to Russian President Vladimir Putin.

- Asked if he could see himself personally sanctioning Putin in the case of an invasion, Biden replied, “Yes…I would see that.”

State Department spokesman Ned Price still thought it necessary to go and act tough for the cameras – “no concessions” he warned… even as allies like France are vowing they’ll always be willing to site down dialogue and negotiate with Russia. “We will never give up dialogue with Moscow,” French President Macron said Tuesday.