JAN 31

January 31, 2022 · by harveyorgan · in Uncategorized · Leave a comment ·Edit

GOLD; UP $10.10 to $1796.00

SILVER: $22.38 UP 7 CENTS

ACCESS MARKET: GOLD: 1797.00..

SILVER: $22.46

Bitcoin: morning price: 37,200 down 143

Bitcoin: afternoon price: 38,348 UP 1005

Platinum price: closing up $15.15 to $1023.60

Palladium price; closing down $24.30 at $2357.50

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filed COMEX//NOTICES: 1/13

EXCHANGE: COMEX

CONTRACT: JANUARY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,793.300000000 USD

INTENT DATE: 01/27/2022 DELIVERY DATE: 01/31/2022

FIRM ORG FIRM NAME ISSUED STOPPED

NUMBER OF NOTICES FILED TODAY FOR FEB. CONTRACT: 3783 NOTICE(S) FOR 378300 OZ (11.766 TONNES)

total notices so far: 3783 contracts for 378,300 oz (11.766 tonnes)

SILVER NOTICES:

558 NOTICE(S) FILED TODAY FOR 2,790,000 OZ/

total number of notices filed so far this month 588 : for 2.790,000 oz

GLD

WITH GOLD UP $10.10

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

NO CHANGES IN GOLD INVENTORY AT THE GLD//

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

CLOSING INVENTORY: 1014.26 TONNES/

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 7 CENTS:/: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF: 1.202 MILLION OZ FROM THE SLV//

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY SLV/ TONIGHT: 533.801 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG 1300 CONTRACTS TO 148,381 AND RESTS FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THIS STRONG LOSS IN OI WAS ACCOMPANIED WITH OUR STRONG $0.36 LOSS IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.36) AND WERE SUCCESSFUL IN KNOCKING OUT A FEW SILVER LONGS AS WE HAD A SMALL LOSS OF 175 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.110 MILLION OZ V) STRONG SIZED COMEX OI LOSS.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS +100

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTACTS for 21 days, total contracts: : 18,092 contracts or 90.460 million oz OR 4.307 MILLION OZ PER DAY. (861 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 18,092 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 90.460 MILLION OZ

.

LAST 8 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1300 WITH OUR $0.36 LOSS SILVER PRICING AT THE COMEX// FRIDAY THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1125 CONTRACTS( 1125 CONTRACTS ISSUED FOR MAR AND 1125 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN OF 10.505 MILLION OZ FOLLOWED BY TODAY’S 145,000 OZ QUEUE JUMP //NEW STANDING 15.275, MILLION OZ// .. WE HAD A SMALL SIZED LOSS OF 298 OI CONTRACTS ON THE TWO EXCHANGES FOR 1.490 MILLION OZ//

WE HAD 588 NOTICES FILED TODAY FOR 2,790,000 OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 14,106 TO 527,614 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: +3 CONTRACTS

.

THE STRONG SIZED DECREASE IN COMEX OI CAME WITH OUR STRONG LOSS IN PRICE OF $8.30//COMEX GOLD TRADING/FRIDAY/.AS IN SILVER WE MUST HAD SOME COMEX SPREADER LIQUIDATION FOLLOWED BY HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION AS THE TOTAL LOSS ON OUR TWO EXCHANGES TOTALED A FAIR SIZED 3317 CONTRACTS…WITH THE ENTIRE TOTAL LOSS COMING FROM SPREADER LIQUIDATION.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JAN AT 3.5614 TONNES FOLLOWED BY TODAY’S 0 OZ QUEUE. JUMP //NEW STANDING: 17.7912 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $36.15 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A FAIR SIZED LOSS OF 10,367 OI CONTRACTS (32.24 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALLED A FAIR SIZED 3739 CONTRACTS:

FOR FEB 3739 ALL OTHER MONTHS ZERO//TOTAL:3739

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 527,614.

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,367, WITH 14,106 CONTRACTS DECREASED AT THE COMEX AND 3739 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 10,367 CONTRACTS OR 32.24TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3739) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (14,106,): TOTAL LOSS IN THE TWO EXCHANGES 10,367 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 64.30 TONNES// 3)SOME LONG LIQUIDATION AS SOME OF THE TOTAL LOSS WAS DUE TO SPREADER LIQUIDATION,4) STRONG SIZED COMEX OI. LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB.WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2021 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN :

79,459 CONTRACTS OR 7,945,900 oz OR 247.25 TONNES 21 TRADING DAY(S) AND THUS AVERAGING: 3783 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAY(S) IN TONNES: 247.25 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 247.25/3550 x 100% TONNES 6.96% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO DATE

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 1300 CONTRACTS TO 148,381 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 1125 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 1125 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1884 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2182 CONTRACTS AND ADD TO THE 1125 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED LOSS OF 175 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 0.875 MILLION OZ,

OCCURRED WITH OUR $0.36 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED //Hang Sang CLOSED UP 252.78 PTS OR 1.07% /The Nikkei closed UP 284.64 PTS OR 1.07% //Australia’s all ordinaires CLOSED UP 0.03% /Chinese yuan (ONSHORE) closed HOLIDAY /Oil DOWN TO 87362 dollars per barrel for WTI and DOWN TO 88.98 for Brent. Stocks in Europe OPENED ALL MIXED // ONSHORE YUAN CLOSED XX AGAINST THE DOLLAR AT XXX. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3813: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING WEAKER AGAINST USA DOLLAR

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 14,106 CONTRACTS AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR STRONG LOSS OF $8.30 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (3739 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. LOOKS LIKE OUR BANKERS ARE FINALLY BAILING OUT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF FEB.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3739 EFP CONTRACTS WERE ISSUED: ;: , DEC : 0 & FEB. 3739 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3739 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED 10,367 TOTAL CONTRACTS IN THAT 3739 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 14,106 CONTRACTS..MOST OF THE TOTAL LOSS WAS DUE TO THE CONTINUING SPREADER LIQUIDATION

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR JAN (17.7912),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $8.30) BUT THEY WERE UNSUCCESSFUL IN FLEECING SOME LONGS AS, EVEN THOUGH THE TOTAL LOSS ON THE TWO EXCHANGES REGISTERED A STRONG 32.24 TONNES ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JAN (17.7916 TONNES)…MOST OF THE LOSS WAS DUE TO THE CONTINUING OF SPREADER LIQUIDATION

WE HAD +19 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 10,367 CONTRACTS OR 1,036,700 OZ OR 32.24 TONNES

Estimated gold volume today: 137,217 /// poor

Confirmed volume yesterday: 258,435 contracts poor

INITIAL STANDINGS FOR FEB ’22 COMEX GOLD //JAN 31

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 8037.75 ozINT.DELAWARE 250 KILOBARSINT.DELAWARE |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 3783 notice(s)378300 OZ11.766 TONNES |

| No of oz to be served (notices) | 16,892 contracts 1,689,200 oz 52.54 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3783 notices 378300 OZ11.766 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

No dealer deposit 0

No dealer withdrawal 0

0 customer deposit

total deposit: nil oz

1 customer withdrawals

i)Out of Int. Delaware 8037.75 oz (250 kilobars)

total withdrawals: 8037.75oz

ADJUSTMENTS: 2//dealer to customer

i) Manfra: 385.812 oz (12 kilobars)

ii) Out of Brinks 96.453 (3 kilobarsw)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of FEBRUARY we have an oi of 20,675 stand for LOSING 11,296 contracts.

Thus by definition, the initial amount of gold standing in this active delivery month of February is as follows:

20,765 notices x 100 oz per notice = 2,076500 oz or 64.30 tonnes

March GAINED 264 contracts to stand at 4123..

APRIL LOST 3183 CONTRACTS DOWN TO 399,852

We had 3783 notice(s) filed today for 378300 oz FOR THE FEB 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 1229 notices were issued from their client or customer account. The total of all issuance by all participants equates to 3783 contract(s) of which 479 notices were stopped (received) by j.P. Morgan dealer and 642 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB /2021. contract month,

we take the total number of notices filed so far for the month (3783) x 100 oz , to which we add the difference between the open interest for the front month of (FEB: 20,675 CONTRACTS ) minus the number of notices served upon today 3783 x 100 oz per contract equals 2,067,500 OZ OR 64.30 TONNES the number of TONNES standing in this active month of FEB.

thus the INITIAL standings for gold for the JAN contract month:

No of notices filed so far (3783) x 100 oz+ (20,675) OI for the front month minus the number of notices served upon today (3783} x 100 oz} which equals 2,067,500 oz standing OR 64.30 TONNES in this active delivery month of FEB.

TOTAL COMEX GOLD STANDING: 64.30 TONNES (HUGE FOR A FEBRUARY DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

157,392.690, oz NOW PLEDGED /HSBC 4.89 TONNES

125,410.592 PLEDGED MANFRA 2.90 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690

288,481,604, oz JPM No 2 8.97 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonne

Loomis: 18,615.429 oz

total pledged gold: 1,555,310.092 oz 48.376 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 33,396,684.729 OZ (1038,77 TONNES)

TOTAL ELIGIBLE GOLD: 15,825,885.963 OZ (492.25 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,570,798.766 OZ (546.52 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 16,015,971.0 OZ (REG GOLD- PLEDGED GOLD) 498.16 tonnes

END

FEBRUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//JAN 31

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 301,998.840 oz DelawareCNT |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 14,914.500 ozBrinks |

| No of oz served today (contracts) | 588 CONTRACT(S)2,790,000 OZ) |

| No of oz to be served (notices) | 234 contracts (1170,000 oz) |

| Total monthly oz silver served (contracts) | 588 contracts 2,790,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits

i) Into Brinks: 14,914.500 oz

JPMorgan has a total silver weight: 185.232 million oz/354.098 million =52.30% of comex

ii) Comex withdrawals: 2

a) out of Delaware: 1931.800 oz

b) out of CNT: 300,067.040 oz

total withdrawal 301,998.840 oz

we had 4 adjustments:

a) dealer to customer

i) Manfra 59,450.921 oz

ii) Brinks 179,964.500 oz

iii) JPMorgan 90,385.730 oz

iv) 4,898.400 oz CNT

the silver comex is in stress!

TOTAL REGISTERED SILVER: 81.955 MILLION OZ

TOTAL REG + ELIG. 354.098 MILLION OZ

TOTAL NO OF CONTRACTS SERVED UPON THIS MONTH: 2838 CONTRACTS FOR 14,190,000 OZ

CALCULATION OF SILVER OZ STANDING FOR JANUARY

NUMBER OF NOTICES FILED TODAY: 10 NOTICES OR 50,000 OZ

silver open interest data:

FRONT MONTH OF FEB//2022 OI: 822 CONTRACTS LOSING 33 contracts on the day

FOR MARCH WE HAD A LOSS OF 2789 CONTRACTS DOWN TO 107,092 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 588 for 2,790,000 oz

Comex volumes: 39,529// est. volume today//weak

Comex volume: confirmed YESTERDAY: 69,132 contracts (fair)

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 588 x 5,000 oz =. 2,790,000 oz

to which we add the difference between the open interest for the front month of FEB (822) and the number of notices served upon today5880 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2021 contract month: 558 (notices served so far) x 5000 oz + OI for front month of FEB (822) – number of notices served upon today (558) x 5000 oz of silver standing for the FEB contract month equates 4,110,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

GLD

JAN 31/WITH GOLD UP $10.10//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 28/WITH GOLD DOWN $8.30//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 27/WITH GOLD DOWN $36.15//ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES INTO THE GLD.//INVENTORY RESTS AT 1014.26 TONNES

JAN 26/WITH GOLD DOWN $21.60 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES INTO THE GLD///INVENTORY RESTS AT 1013.10 TONNES

JAN 25/WITH GOLD UP $10.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 24/WITH GOLD UP $10.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: AN UNBELIEVABLE DEPOSIT OF 27.59 TONNES INTO THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 21/WITH GOLD DOWN $10.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 980.86 TONNES

JAN 20/WITH GOLD UP $.20 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 980.86 TONNES

JAN 19/WITH GOLD UP $29.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 5.27 TONNES INTO THE GLD/INVENTORY RESTS AT 981.44 TONNES

JAN 18/WITH GOLD DOWN $3.25//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 14/ WITH GOLD DOWN $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 13/WITH GOLD DOWN $5.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 12/WITH GOLD UP $8.65//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 11/WITH GOLD UP $19.25/A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FROM THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 10/WITH GOLD UP $2.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.08 TONNES

JAN 7/WITH GOLD UP $8.15//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWLA OF 1.16 TONNES FROM THE GLD////INVENTORY RESTS AT 978.83 TONNES

JAN 6/WITH GOLD DOWN $35.30//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .32 TONNES/INVENTORY RESTS AT 979.99 TONNES

JAN 5/WITH GOLD UP $10.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 980.31 TONNES

Jan 4/WITH GOLD UP $14.00//A HUGE CHANGE OF 4.65 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 980.31 TONNES

JAN 3/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 31/WITH GOLD UP $14.05 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 30/WITH GOLD UP $7.75 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 29/WITH GOLD DOWN $5.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 975.66 TONNES

DEC 28/WITH GOLD UP $2.00 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 973.63 TONNES

DEC 27/WITH GOLD DOWN $2.05: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.63 TONNES.

DEC 23/WITH GOLD UP $9.85 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.94 TONNES FROM THE GLD/// INVENTORY RESTS AT 973.63 TONNES

DEC 22/WITH GOLD UP $12.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 21/WITH GOLD DOWN $7.05 TODAY, NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 20/WITH GOLD DOWN $9.65 TODAY; A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.37 TONNES INTO THE GLD///INVENTORY RESTS AT 977.20 TONNES

DEC 17/WITH GOLD UP $7.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.20 TONNES

CLOSING INVENTORY: 1014.26 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SLV

JAN 31/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FORM THE SLV.//INVENTORY RESTS AT 533.801 MILLION OZ//

JAN 28/WITH SILVER DOWN 36 CENTS : NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 27/WITH SILVER DOWN $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 26/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 25/WITH SILVER UP 10 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.311 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 535.003 MILLION OZ/

.JAN 24/WITH SILVER DOWN 48 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.8 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 532.692 MILLION OZ//.

JAN 21/WITH SILVER DOWN 41 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 527.792 MILLION OZ

JAN 20/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.998 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 527.792 MILLION OZ

JAN 19/WITH SILVER UP 71 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.942 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 525.804 MILLION OZ

JAN 18/WITH SILVER UP 51 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS OF 1.11 MILLION OZ AND 1.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 527.246 MILLION OZ//

JAN 14/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 529.780 MILLION OZ//

JAN 13/WITH SILVER DOWN 2 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 832,000 OZ FROM THE SLV////INVENTORY RESTS AT 529.780 MILLION OZ

JAN 12/WITH SILVER UP 38 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//

JAN 11/WITH SILVER UP 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ/.

JAN 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 7/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 6/WITH SILVER DOWN 94 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL PF 226,000 OZ FROM THE SLV///INVENTORY RESTS AT 530.612 MILLION OZ?/

JAN 5/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 4/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 3/WITH SILVER DOWN 45 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.219 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 530.838 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC30/WITH SILVER UP 14 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.624 MILLILON OZ FROM THE SLV.//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 29/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ/

DEC 28/WITH SILVER UP 9 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.682 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 27/WITH SILVER UP 6 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681

DEC 23/WITH SILVER UP 19 CENTS TODAY:A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 22/WITH SILVER UP 29 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 538.883 MILLION OZ/

DEC 21/WITH SILVER UP 19 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.728 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 540.085 MILLION OZ

DEC 20/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 538.282 MILLION OZ

DEC 17/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 538.282 MILLION OZ//

CLOSING INVENTORY: 533.801 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: Consumers Are Concerned, Investors Are Clueless

MONDAY, JAN 31, 2022 – 08:15 AM

Is bitcoin an inflation hedge?

Peter Schiff recently appeared on RT Boom Bust with Natalie Brunell of Coin Stories to discuss inflation and whether bitcoin is a hedge. Peter said bitcoin is not an inflation hedge. He called it a “speculative token” with its price driven by supply and demand.

But what about gold? It didn’t perform like an inflation hedge in 2021 despite the inflation freight train. Peter said the reason gold has had some problems is because the market wrongly believes the Fed.

They believe Powell when he says he’s going to do whatever it takes to bring inflation back down to 2%. He’s going to raise interest rates. He’s going to start shrinking the balance sheet. And the markets are believing Powell. But I think he’s just bluffing. And even if he follows through with the rate hikes he’s promised, that’s too little too late. It’s not going to be nearly enough to slow down inflation. And so, it’s not going to restrain gold.”

The type of rate hikes and balance sheet reduction necessary to get ahead of the inflation curve would be too much for the bubble economy to bear.

If Powell actually tried to fight inflation, he would destroy the bubble economy. The stock market would crash. We’d be in a massive recession. Lots of unemployment. A huge financial crisis. And we would force the government into insolvency. Once the markets come to terms with reality, they’re going to be buying gold.”

Natalie agreed that the Fed can’t fight inflation and will be forced to pivot back to providing liquidity to the market. She said that will send both stocks and bitcoin higher.

So where will consumers look to hedge? Will they turn to gold? Bitcoin? Or possibly other cryptocurrencies that are out there?

Peter said right now most investors aren’t even really worried about inflation.

They believe the Fed. So, they think that the inflation problem is going to be solved.”

But at some point, people will realize that it’s actually going to get worse. The Fed is ultimately forced to do an about-face because Powell actually thinks he can raise rates without hurting the economy.

He thinks we have this strong economy. We don’t. We have a gigantic bubble. And even the smallest of pins is going to prick it. In fact, just talking about raising rates, and this has already pricked the bubble. We’re already pretty much in a bear market now. And so, I think that sometime this year, whether it happens before the first rate hike or after, Powell’s going to cave and he’s going to go back to bigger QE and rates go back to zero. And that’s when the markets are finally going to understand the predicament that we’re in.”

Peter said the markets should realize it already. “But for some reason, they need a safe to drop on their head.”

And when that happens, then they’re going to be looking for inflation hedges. They’re not going to care about bitcoin. That’s for gamblers. They’re going to look for a real store of value and they’re going to be buying gold. They may be buying silver as well. And I think they’re going to be buying all sorts of real assets to get dollars.”

Peter emphasized that consumers are concerned about inflation. Consumer sentiment data bears this out. But Peter said investors are clueless.

Consumers are very concerned. And they should be. And unfortunately, it’s going to get much worse for consumers.”

END

END

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS

Markets Have Seen This Movie Before (Spoiler Alert: The Ending Is Horrible)

MONDAY, JAN 31, 2022 – 06:30 AM

Authored by James Rickards via The Daily Reckoning,

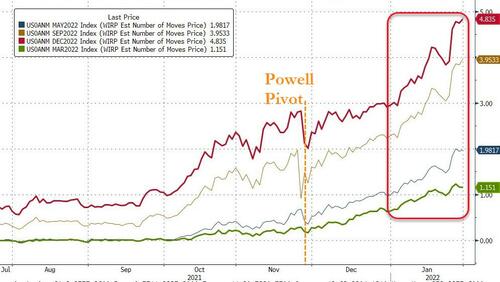

As I expected, the Fed didn’t raise rates this week at its January FOMC meeting.

If you were thinking the Fed would have to begin raising rates to counteract inflation, you’re probably going to have to wait until March, when the Fed’s Open Market Committee meets again.

The Fed says it “will soon be appropriate” to raise rates. It also says it will end asset purchases in March, so all signs point to a March rate hike.

How did the stock market react to this week’s messaging from the Fed?

[ZH: The initial reaction was a puke across all major US equity markets… followed by the ubiquitous overnight ramp to erase the loss. Thursday saw more selling at the open which extended into the US cash open on Friday.]

{ZH: At which point, a buying panic ensued, lifting The Dow and S&P back into the green post-FOMC, Nasdaq down modestly, but Small Caps crushed.]

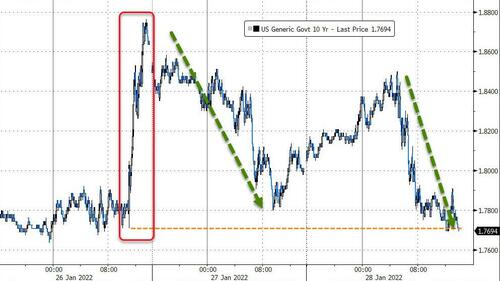

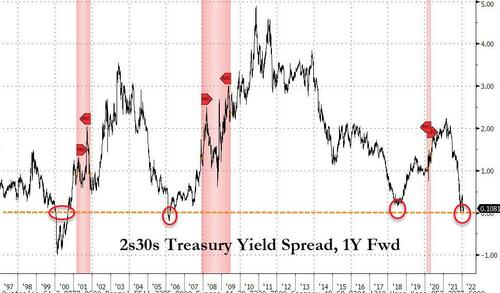

The All-Important 10-Year Treasury

Yields on the all-important 10-year Treasury note spiked to 1.876% on Wednesday – a 10bps surge. That’s an earthquake in bond land. [ZH: But, by the end of the week, amid fears of policy errors, the 10=year yield had tumbled back to unchanged post-FOMC.]

Ten-year yields opened the year under 1.6%, and the increase has spooked the stock market.

The 10-year note yield is a good proxy for long-term investment in mortgages, construction and infrastructure projects and therefore reflects expectations about the real economy.

Until recently, the interim high yield on the 10-year note had been 1.745% on March 31, 2021. Rates fell through the summer of 2021 and then began rising again, but the rate spikes fell short of that 1.745% level and then fell back.

That pattern prevailed until Jan. 14, 2022, when rates broke through and hit 1.794%. That was the highest level since Jan. 13, 2020, almost exactly two years ago, and before the pandemic became widespread in the U.S.

At that time, rates had declined from their pre-pandemic interim high of 2.761% on Jan. 23, 2019, almost exactly three years ago. Again, today’s yield is 1.848%.

What Are Bonds Saying About Inflation?

But if rates are not fundamentally higher than they were two years ago and are significantly lower than they were three years ago, what does that say?

If a wave of inflation is about to smash into us, why aren’t rates at 3.0% or higher? A yield of 1.876% is pretty puny if the inflation narrative is correct.

People throw the word “stimulus” around, even those who should know better, and say, “The Fed’s cut rates to zero. That’s stimulus. The Fed’s printing money. That’s stimulus.”

They then say, “If you’re going to print that much money, you’re going to get inflation.”

The Reality

But none of that is true. It’s far too simplistic. Reality is much more complicated than the simple money printing equals inflation narrative. Yes, the money printing is true. But it’s not inflationary unless the money gets put to use in the economy.

If the money gets put to use in the form of widespread lending and spending, that’s a setup where you have to think hard about inflation. But that’s not what we’re seeing.

What happens then to the money the Fed creates?

The big banks have accounts at the Fed. They take the money and they leave it at the Fed in the form of excess reserves, meaning basically more reserves than the law requires them to have.

So the money doesn’t go anywhere. It’s not being invested. It’s not being loaned out. It’s not being borrowed. It’s not being spent. So it doesn’t matter how much there is if the money doesn’t go anywhere, and that’s exactly the situation we’re facing.

It’s the Velocity, Stupid

I often refer to the velocity of money. Quite simply, velocity is the turnover of money, the rate at which money changes hands.

The Fed can create money just by buying bonds with money it creates out of thin air. But velocity is a psychological phenomenon.

It all depends how consumers feel. If they feel prosperous, if they feel that their job is secure, if they feel that their businesses are doing well, they might be more willing to borrow money to expand the business or spend money on personal consumption.

But we’re not seeing that. We’re seeing velocity drop. Some people are getting money, whether it’s in the form of government handouts or slightly higher wages, but they’re saving it. They’re not spending it. That doesn’t add up to rampant inflation.

I realize I may be in the minority, but the bond market is telling us that inflation will be much tamer than expected (I expect inflation to return with a vengeance eventually, but not yet).

In other words, the U.S. may be seeing peak inflation and peak interest rates for this cycle.

The One Thing the Fed Excels At

I expect the U.S. economy will slow from here (for many reasons including the pandemic, supply chain disruptions and excess debt), rates will level off and then decline and the dollar will weaken.

Of course, the Fed is preparing to tighten monetary policy at a time when the economy shows weakening. It’s tightening into weakness. But that’s no surprise.

Looking at the entire history of the Fed since 1913, it’s proven that it’s really good at wrecking the economy by doing the wrong thing at the wrong time. And it’s in the process of doing that again.

I feel like we’re watching the same movie that we’ve already seen. We’re seeing this movie again because the Fed did this before. From 2008–2013, the Fed did what they did the last couple of years.

“Normalizing”

They bought bonds, created money supply, blew up the balance sheet and cut rates to zero. The zero interest rate policy, the money printing, they did that from 2008–2013. They took the Fed’s balance sheet from about $800 billion to about $4 trillion (today it’s dramatically higher because of its response to the pandemic).

Then they tried to “normalize.” They began raising rates aggressively. They got the fed funds rate up to 2.25%, with nine 25-basis-point increases between December 2015 and December 2018.

They trimmed the balance sheet down. Not greatly, but they brought it down from about $4.5 trillion to about $3.7 trillion. That’s not an insignificant reduction.

Markets Have Seen This Movie Before

In other words, the Fed was trying to raise rates and reduce the balance sheet, and they were succeeding. But it all culminated on Dec. 24, 2018, in what I call the Christmas Eve Massacre.

The Fed sank the stock market. It fell 20% in 2½ months.

And that was after a long bull market from 2009–2018, when stocks tripled over that time period.

The lesson is that when the Fed tries to normalize, they can’t do it. They’re caught in a trap of their own creation, with no way out, or at least no easy way out without causing a lot of pain.

They’re about to make things worse with tightening into weakness, with tapering and with rate increases. The market already sees this coming because they’ve seen the movie before. They know how it ends.

And it ends poorly

end

LAWRIE WILLIAMS: Gold demand more than recovers in 2021

The World Gold Council has just released its much awaited Gold Demand Trends report for Q4 2021 and for the year as a whole, and what it has to say is probably more than encouraging for the gold investor. It showed that the world has perhaps more than fully recovered from the Covid- inflicted downturn of 2020, with demand levels increasing as the year progressed. Indeed the Q4 gold demand figure was the highest for around three years and the trend is upwards. The WGC’s own classified highlights are set out below:Q4 2021 demand reached a 10-quarter high of 1,147t.A jump in jewellery demand, together with a marked slowdown in ETF outflows, drove much of the Q4 recovery.Gold ETFs saw net annual outflows of 173t (US$9bn). Outflows were heavily concentrated in Q1, slowing to trivial levels by Q4.Annual jewellery consumer demand rebounded to pre- pandemic levels. In value terms, this equated to US$123bn, virtually matching the previous record of US$124bn from 2013.Bar and coin investment jumped 31% to an eight-year high of 1,180t.Retail investors sought a safe haven against rising inflation and ongoing uncertainty caused by the pandemic.Central banks bought 463t of gold in 2021.Global gold reserves are now just under 35,600t, their highest for almost 30 years.Total annual gold supply fell marginally to 4,666t. A 2% increase in mine production was counteracted by a sharp 11% drop in recycling.On the face of things, gold still remains in a small surplus, but demand has been rising and this could rapidly turn around. The latest price downturn after last week’s FOMC meeting looks to have been overdone, as is usually the case with significant price movements up or down, and looked to be recovering toward the $1,800 level again towards the end of the week. We’d expect it to break back up through this psychological level this week and perhaps regain $1,820 or higher.After all one thing which came out of the Jerome Powell post-FOMC meeting press conference was that inflation was running higher, and looked like being in place for longer, than had previously been admitted. The negative impact on gold was because this was interpreted by commentators and analysts as suggesting the Fed might be more aggressive in raising interest rates than had been previously anticipated. But whatever the Fed decides interest rates are unlikely to be increased sufficiently to bring real rates out of negative territory, and negative real rates are positive for gold – particularly if general equities are negatively affected at the same time.Positive U.S. equity price movement on Friday will have given the Fed some encouragement that a move to higher interest rates may not impact markets too adversely. But this should be set against equity price falls on the prior three days, and we would anticipate a further downwards correction this week. After all, businesses will have become used to Fed money being pumped into the markets indirectly via the central bank’s bond and security buying programmes and accompanied by ultra- low interest rates. TThe prospect of all this falling away is almost certainly bound to adversely affect markets. If U.S. equities fall further in the weeks ahead, then it is certainly possible that the Fed will temper some of its tightening moves, as it has done in similar situations in the past and, if so, this would likely give a sharp fillip to the gold price.Whatever the Fed decides to do don’t count out gold, therefore, as the ultimate wealth protection investment. Ongoing inflation is continuing to eat away at dollar purchasing power and that of other currencies, and gold has always in the past helped protect against such value degradation. It may suffer ups and downs, but overall it tends to hold its own when other protective options may suffer. Keep the faith.

30 Jan 2022.

end

3.Chris Powell of GATA provides to us very important physical commentaries

For your interest…

The gold rush returns to California

Submitted by admin on Sun, 2022-01-30 10:34 Section: Daily Dispatches

By Becki Robins

Undark Magazine, Cambridge, Massachusetts

Monday, January 24, 2022

On the outskirts of the northern California town of Grass Valley, a massive concrete silo looms over the weeds and crumbling pavement. Nearby, unseen, a mine shaft drops 3,400 feet into the earth.

These are the remains of Grass Valley’s Idaho-Maryland Mine, a relic from the town’s gold mining past. Numerous mines like this one once fueled Grass Valley’s economy, and today, Gold Rush artifacts are part of the town’s character: A stamp mill, once used to break up gold-bearing rock, now guards an intersection on Main Street, and old ore carts and other rusty remnants can be spotted in parking lots and storefronts around town.

Gold still exists in the veins of the abandoned mine, and Rise Gold, the mining corporation that purchased the mine in 2017, has reason to believe that reopening it makes financial sense.

When the mine shut down in 1956, it wasn’t because the gold was drying up; it was because of economic policy. The 1944 Bretton Woods Agreement had established a new international monetary system to create stability in exchange rates. As part of the effort, the price of gold was fixed at $35 per ounce. Gold mining became unprofitable in the U.S. …

… For the remainder of the report:

end

end

4.OTHER GOLD/SILVER COMMENTARIES

| Live from the Vault: Episode 59. |

| Hi Harvey, In this week’s Live from the Vault, Andrew Maguire reveals the two main reasons behind the current bullish shift in gold and silver and elaborates further on the fragile ETF flywheel, with gold set to rally. The precious metals expert continues to monitor the influence of Basel III on the markets and explains the mechanisms behind futures market backwardation in response to ever-tightening physical supply.Watch the video via the button below, or listen on Apple podcasts or Spotify.WATCH NOW |

Support Contact us Live chat |

|

END

Andy Schectman:

Silver premiums spike as COMEX paper silver crashes & burns

As the pressure on the COVID Deep State banking system mounts, physical silver premiums have spiked, while COMEX paper silver is crashing and burning.

And to offer you a view from the frontlines of the physical silver market, Andy Schectman of Miles Franklin joined me on the show to share what’s happening at this very minute.

So if you want to know what’s really going on with the silver price, click to watch this timely video now!

https://lemetropolecafe.com/pfv.cfm?pfvID=17440

5.OTHER COMMODITIES/

6.CRYPTOCURRENCIES

Steve Brown..

Crypto Apes Take a Hit

“Veritably these are young people born in an era of the vaporware US dollar, and fully programmed and committed to further its vaporware use.“

The Fed has created trillions upon trillions in debt, what some call money. After the government pays its bills with those trillions, it’s important to keep the result out of the pockets of the people. And if the bitcoin/crypto black hole for $ did not already exist, it would have to be invented.

A tech whitepaper produced by the mysterious “Satoshi Nakamoto” founded bitcoin, just subsequent to the financial collapse of the United States in 2008-2009. Whether Satoshi was some covert entity behind the monetary scene hoping to provide a place for inflationary fiat $ to go… or some brilliant individual who (by coincidence) wanted to do the same, is still a matter for conjecture and debate.

Regardless, the importance of bitcoin was to address a macro monetary issue by providing an inflationary asset store. The idea that bitcoin is a stable and reliable asset store is as fake and imaginary as the virtual apes who revel in their own virtual $ existence in the virtual DeFi world, and is the outcome when the world monetary system itself is built on fiat fakery. Link: https://chaindebrief.com/what-is-wonderland-time-avalanche/Justin Sun Founder Binance crypto apeDanielle Sestagalli, Wonderland ape

Before 2009, whenever a monetary scam was discovered by the state, the state usually prosecuted and/or shutdown the scam. But what happens when the scam benefits the monetary system? And by extension the state, for example the quasi-governmental Federal Reserve*?

In the Novus Confidential series Why the Fed Loves Bitcoin parts 1, 2 and 3 the Fed’s connection to bitcoin is documented. A covert governmental connection is shown by the CIA’S Bitcoin Heist.** And soon after bitcoin’s inception, Wall Street and the world’s largest ‘investors’ (but actually black holes of finance) namely: Vanguard Group; StateStreet; BlackRock etc*** gamed hundreds of billions via such dubious share issues as Microstrategy, Global Bitcoin Trust, Riot Blockchain, MARA, Cathie Wood’s ARK Innovation and many more Wall Street share issues.

Oh yes, there is plenty of governmental whining about bitcoin, but such histrionics seldom lead to any action. So far KYC and AML regulations have been it. Vanguard lackey CNBC admits that the government does things with its “secret massive stockpile of bitcoin” but fails to detail the extent of governmental seizure, and that the Fed-Treasury need to sterilize inflationary $ by hundreds of billions, via crypto. For defacto proof that the federal government uses bitcoin to its advantage, simply consider that the OCC could prevent any accredited US bank from transacting with any bitcoin exchange… but does not.

Point is that one good scam deserves another — whatever its origin — and a large criminal element has piggy-backed off the Fed’s own crypto criminality to its own advantage. Such lawsuits as vs XDB digitalbits and tether seldom make the mainstream media, which is pumped with pro-crypto nonsense by Vanguard Group’s major media outlets, from CNBC to Verizon (Yahoo) and a myriad of other bitcoin bullshit media operations. But occasionally bitcoin apes/ criminals do make the major media news for their criminal notoriety.

Two years ago Novus Confidential covered crypto exchange failures in Why Bitcoin? Why Now? which touched on the strange case of bitcoin/ETH ape Gerald Cotten. Cotten, at the age of thirty, supposedly left this world due to Crohn’s disease and by mysterious circumstances that are still not fully documented or understood. Link: https://www.vanityfair.com/news/2019/11/the-strange-tale-of-quadriga-gerald-cotten While Novus Confidential originally believed that Cotten faked his own death, after years of research, the conclusion is that Cotten is in fact deceased.

But his partner in crime, Michael Patryn AKA Omar Dhanani, is not. Dhanani-Patryn was sought for years in the Quadriga fraud case, and was only just voted out of his position as “treasurer” of the Wonderland token . Link: https://beincrypto.com/wonderland-cfo-outed-as-ex-convict-and-quadrigacx-co-founder-michael-patryn-steps-down/ Ape Sestagalli said she felt a criminal’s past should not affect their future, “All frogs for me are equal,” said Sestagalli. So perhaps Sestagalli would do even better as New York State’s attorney general. Truly the depth of criminality in crypto cannot be estimated, calculated, or even remotely imagined. And yet crypto’s criminality is only outdone by the criminality of the US-led monetary system itself. But now the question is what Canada’s law enforcement will do about bad actor Dhanani aka Mike Patryn?Ape Omar Dhanani alias Patryn, crypto crook

end

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED XX

OFFSHORE YUAN: 6.3813

HANG SANG CLOSED UP 252.18 PTS OR 1.07%

2. Nikkei closed UP 284.64 PTS OR 1.07%

3. Europe stocks ALL MIXED

USA dollar INDEX UP TO 97.17/Euro RISES TO 1.1160-

3b Japan 10 YR bond yield: RISES TO. +.176/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 115.45/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 87.36 and Brent: 88.98-

3f Gold UP /JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE CLOSED XX// OFF- SHORE DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.062%/Italian 10 Yr bond yield FALLS to 1.31% /SPAIN 10 YR BOND YIELD RISES TO 0.75%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.37: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 1.88

3k Gold at $1791.15 silver at: 22.58 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble UP 57/100 in roubles/dollar AT 77.61

3m oil into the 87 dollar handle for WTI and 88 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 115.45 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9329– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0411 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 1.801 UP 3 BASIS PTS

USA 30 YR BOND YIELD: 2.103 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.38

US Futures Start The Week With More Wild Swings In Another Volatile, Illiquid Session

MONDAY, JAN 31, 2022 – 08:03 AM

After a rollercoaster week that ended just barely higher following a late meltup on Friday, overnight volatile US stock futures swung to start the week, with Nasdaq 100 futures leading gains after rallying on Friday, before turning red and threatening to fizzle a global equity rally amid persistent worries over the Federal Reserve’s plan to hike interest rates this year. Emini S&P futures were down 0.5% or 21 points to 4401, after rising as high as 4437 and dropping as low as 4395 in another extremely illiquid session where China being offline for the week due to Lunar New Year did not help; Nasdaq futures were down 0.1% while Dow futures were lower 0.7%. Technology stocks led gains on the Stoxx Europe 600. Meanwhile, the dollar fell and oil rallied.

As investors reconcile to a hawkish U.S. central bank coupled with strong earnings, the expensive parts of the U.S. stock market are undergoing a valuation re-rating along with the bond markets. However, traders do see opportunities in less expensive segments of the global markets, such as European and emerging-market stocks (especially China), as well as higher-yielding currencies where rate hikes have already happened. The only thing money managers are certain about for the year is greater volatility.

The equity selloff “marks a long overdue correction rather than the start of a bear market,” BCA Research Inc. analysts including Peter Berezin and Melanie Kermadjian wrote in a note. “Stocks often suffer a period of indigestion when bond yields rise suddenly, but usually bounce back as long as yields do not move into economically restrictive territory.”

“The sharp fall in many high-quality tech firms is already creating opportunities for longer-term investors to add exposure,” Mark Haefele, the ever bullish chief investment officer at UBS Global Wealth Management, wrote in a note. “Rather than giving up on tech in the face of near-term headwinds, we recommend a more selective approach.”

In premarket trading, major technology and internet names such as Netflix Inc. and Tesla Inc. rose, with the electric carmaker getting an upgrade to outperform at Credit Suisse. Citi raised its recommendation on Netflix (NFLX US) and Spotify (SPOT US) to buy from neutral after pressure on subscription-based stocks. Netflix rises 2.7% in premarket, Spotify +1.8%. Citrix fell 3.7% in early New York trading. Elliott Investment Management and Vista Equity Partners are said to be nearing an agreement to acquire software-maker for about $13 billion, marginally less than the company’s current market cap. Other notable pre-market movers:

- Tesla (TSLA US) gains 2.4% in premarket trading after Credit Suisse upgrades the electric- vehicle maker to outperform following a sharp pullback and on “highly favorable” fundamentals.

- Beyond Meat (BYND US) growth prospects in the U.S. foodservice channel and international segments aren’t properly reflected in the shares, according to Barclays, which upgrades to overweight from underweight. Shares +4.4% in premarket.

- Alibaba (BABA US) and other Chinese tech firms were in focus as traders interpreted comments by China’s cyberspace regulator as positive toward the sector. Alibaba up 1.5% in premarket.

- Pullback in Intuitive Surgical (ISRG US) shares creates a good entry point into a premier medtech name which has executed strongly during the pandemic, Piper Sandler writes in note as upgrades to overweight. Shares up 0.6% in premarket.

Meanwhile, the stellar run of profitability in US companies continues this quarter. Of the 169 S&P 500 companies that have posted results so far, 81% have met or exceeded expectations. Profits have come about 5% more than the levels predicted. Companies from Alphabet to Exxon report financial results this week in the U.S., while the European earnings calendar is also full, with the likes of UBS Group AG and Roche Holding AG publishing their figures (more in our weekly preview post).

As Bloomberg notes, healthy earnings may cushion the impact of a technology-led selloff in the U.S. as investors adjust to a higher interest-rate regime. That may also help to alleviate some of the concerns sparked by geopolitical tensions between the U.S. and Russia over Ukraine.

European equities were well bid, with the Stoxx 600 gauge advancing for a fourth time in five days and an index of global equities pared its biggest monthly drop since March 2020. Euro Stoxx 50 rises as much as 1.6%, close to recouping last week’s losses, before drifting off best levels. Germany and Italy lead gains. Tech is the best performing Stoxx 600 sector, miners and travel underperform. Here are some of the biggest European movers today:

- Electrolux shares rise as much as 6%, the most since July 2020 and the biggest gainer on the Stockholm large-cap OMXS30 index, after several brokers upgraded the shares or their target prices. Handelsbanken upgrades to buy, citing “pricing power hiding in plain sight.”

- Vodafone shares rise as much as 4.5% after a Bloomberg report that activist investor Cevian Capital has built a stake in the firm. It highlights material “hidden value” in the U.K. telecoms operator, according to Andrew Lee, analyst at Goldman Sachs (buy).

- Adva Optical Networking shares rise as much as 16%, the most intraday since August, after the approval threshold for Adtran Inc.’s voluntary offer was crossed at the end of the initial acceptance period on Jan. 26.

- Aumann shares rise as much as 9% after the company reported margin guidance which Citi sees as positive indicator for ’22 profitability.

- KPN shares rise as much as 2.7% to their highest level since March 2021 after results. Analysts are positive on the company’s buyback plans, while KBC said KPN’s results are “comforting.” KPN forecast adjusted Ebitda after leases for 2022 of about EU2.40 billion.

- Saipem shares fall as much as 29% in Milan, the most intraday since 2013, after the Italian oil drilling specialist issued a warning on 2021 earnings and said it would hold discussions with creditors and shareholders for a financing package.

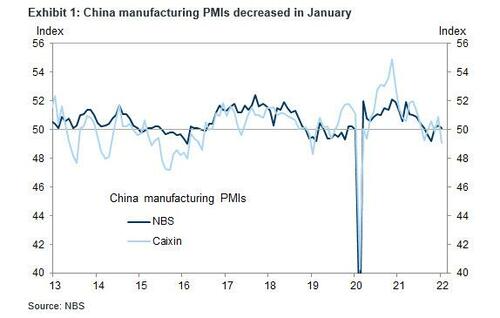

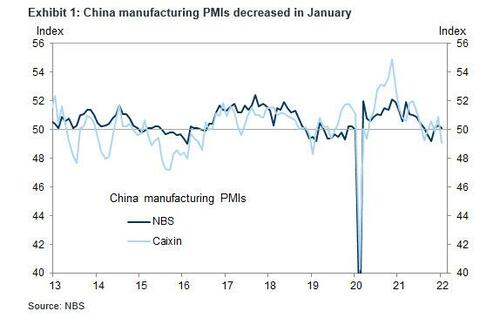

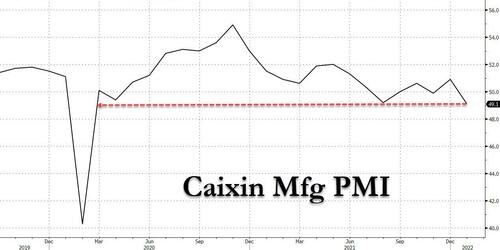

Monetary-policy decisions from the European Central Bank and Bank of England will help shape the market mood in the days ahead, while investors continue to watch for evidence of economic recovery from the pandemic effects. China’s economy continued to slow at the start of the year as manufacturing and services moderated.

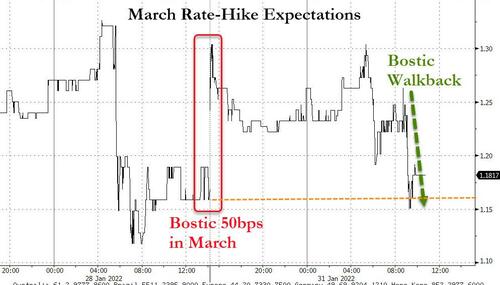

Earlier in the session, equities in Asia Pacific climbed in a quiet trading day, paring a portion of their worst monthly decline since July amid continued investor concerns about the pace of tightening by the U.S. Federal Reserve. The MSCI Asia Pacific Index gained as much as 0.8%, reversing an early loss of 0.4%, as consumer discretionary and communication services shares climbed. Alibaba and Tencent were among the biggest contributors to gains as the Hang Seng Tech Index closed up 2.4%. Asian tech stocks followed their U.S. peers higher after bellwethers including Apple and Microsoft announced strong quarterly results and outlooks. Benchmarks in Japan, India and Hong Kong rose, with the latter in a shortened trading session at the start of Lunar New Year holidays. Markets in China, South Korea and Taiwan were closed. The Asian benchmark is on track for a decline of about 4.7% in January, as more traders price in five interest-rate hikes this year and after Raphael Bostic, president of the Fed’s Atlanta branch, told the Financial Times that a 50 basis-point rate increase is on the table. This comes while China’s economy continued to slow at the start of the year. “Powell’s current inflation-fighting mode makes it more likely that a new policy error will occur,” Citi Private Bank strategists led by David Bailin wrote in a note. Citi has increased its overweight on China on preparations for “greater macro easing and growth support,” they wrote

Japanese equities climbed, erasing an early loss, as the market continued to rebound from losses on concerns over Federal Reserve monetary tightening. Electronics makers were the biggest boost to the Topix, which rose 1%, erasing a drop of as much as 0.8%. Tokyo Electron and SoftBank Group were the largest contributors to a 1.1% gain in the Nikkei 225. The Topix rose 1.9% Friday, paring its weekly decline to 2.6%. The gauge is still down 4.8% this year.

India’s benchmark equity index bounced back after losing 6.6% in the last two weeks, boosted by gains in Infosys Ltd., which climbed the most since mid-October. The S&P BSE Sensex rose 1.4% to 58,014.17 in Mumbai, joining peers across Asia as investors took a breather from volatility induced by possible U.S. Fed rate action. Infosys Ltd. rose 3% and offered the biggest boost to the index. Still, the gauge is down 0.4% in January, its biggest monthly decline since November. The NSE Nifty 50 Index advanced 1.4% on Monday. Fed’s near-term rate hike possibility and selling by foreign investors weighed on the key indexes this month, Prashanth Tapse, vice president at Mehta Equities Ltd. wrote in a note. “All eyes will now be on the GDP numbers and the union budget to be announced on February 1,” he said. All but one of 19 sectoral sub-indexes compiled by BSE Ltd. gained, led by a measure of realty companies. On the earnings front, out of the 25 Nifty 50 companies that have announced results so far, 13 either met or exceeded expectations, 10 missed, while two can’t be compared.

In rates, Treasury yields advanced while the curve flattened as bond markets braced for successive rate hikes by Fed starting March. Yields were cheaper by more than 3bp across front-end of the curve, flattening 2s10s spread by ~2bp on the day; 10-year yields around 1.79%, cheaper by more than 2bps vs Friday’s close with bunds lagging by additional 3bp.Treasuries remain cheaper across the curve after an opening gap higher in yields led by front-end, focused on expected path of Fed rate hikes this year. Long-end may draw support from month-end flows. US outperformed bunds, gilts and most euro-zone bond markets. S&P 500 futures are under slight pressure, near Friday’s high. Bund and gilt curves bear flatten with short-end Germany underperforming. Peripheral spreads tighten on the better risk on mood. Italy snaps tighter on the open as political uncertainties ease following Sergio Mattarella’s re-election as president over the weekend.

In FX, the Bloomberg Dollar Spot Index fell as the greenback weakened against all of its Group-of-10 peers apart from the Swiss franc and the yen. The Australian dollar led G-10 gains and rebounded from an 18-month low against the greenback as traders and local exporters hedged for a hawkish tilt from the nation’s central bank on Tuesday. Month-end flows were also supporting the currency. The euro crept higher, nearing $1.12, and Bunds sold off, led by the belly and underperforming Treasuries, while the yield premium to hold Italian government bonds over German securities narrowed. The pound rallied amid a broad risk-on tone in global currency trading, with U.K. focus on this week’s BOE meeting. Asset managers added to short bets against the currency for the first time in six weeks, according to Commodity Futures Trading Commission data for the week ended Jan. 25. Figures also showed leveraged funds added long contracts to become the most bullish since early November. Norway’s krone rallied amid supportive oil prices while it shrugged off the news that Norges Bank won’t conduct any foreign exchange transactions on behalf of the government in February. The central bank sold foreign exchange equivalent to NOK250m a day in January. Japan’s 10-year benchmark yield rose to a six-year high following the recent surge in Treasury equivalents. TRY leads gains in EMFX, strengthening just shy of 2% against the dollar before fading near 13.40/USD.

Crypto markets are subdued with Bitcoin slipping back beneath the 37,000 level overnight. BoE’s executive director for financial stability said cryptocurrency does not yet pose a risk to UK’s financial stability, according to The Times.

In commodities, crude futures are in the green but drift off Asia’s highs. WTI slips after a brief retest of $88 in late Asia; Brent tops $91. Oil markets headed for the biggest January gain in at least 30 years. Spot gold is range bound near $1,789/oz. Most base metals trade well with much of the complex up 0.6-0.8%. LME aluminum lags.

Looking at today’s calendar, it’s a relatively quiet day, with Euro Area Q4 GDP, Italy Q4 GDP, Germany preliminary January CPI, US January MNI Chicago PMI, Dallas Fed manufacturing index, and Japan’s December jobless rate. The Fed’s Daly speaks. Looking at the week ahead, earnings are due from Alphabet, Amazon, Exxon Mobil, Ford Motor, Meta Platforms, Qualcomm, Sony, Spotify, UBS Group. Tomorrow we get the Reserve Bank of Australia rate decision, Manufacturing PMIs, including euro zone; OPEC+ meeting on output is on Wednesday as is the latest Euro zone CPI. On Thursday, the Bank of England, European Central Bank rate decisions; also we get the Fed Board of Governors confirmation hearing and the U.S. factory orders, initial jobless claims, durable goods. Finally, on Friday, we get the payrolls report for January, while in China, winter Olympics kick off with Russia’s President Vladimir Putin due to attend opening ceremony.

Market Snapshot

- S&P 500 futures up 0.2% to 4,431.50

- STOXX Europe 600 up 1.0% to 470.31

- German 10Y yield little changed at -0.03%

- Euro up 0.2% to $1.1170

- Brent Futures up 0.7% to $90.62/bbl

- MXAP up 0.7% to 184.12

- MXAPJ up 0.7% to 602.30

- Nikkei up 1.1% to 27,001.98

- Topix up 1.0% to 1,895.93

- Hang Seng Index up 1.1% to 23,802.26

- Shanghai Composite down 1.0% to 3,361.44

- Sensex up 1.4% to 58,004.69

- Australia S&P/ASX 200 down 0.2% to 6,971.63

- Kospi up 1.9% to 2,663.34

- Brent Futures up 0.7% to $90.62/bbl

- Gold spot down 0.1% to $1,790.58

- U.S. Dollar Index down 0.22% to 97.05

Top Overnight News from Bloomberg

- U.S. senators are close to agreeing on a Russia sanctions bill that could include penalties even if President Vladimir Putin doesn’t send troops into Ukraine, Foreign Relations Committee Chair Bob Menendez said

- Moscow further boosted troop levels around the Ukrainian border at the weekend, adding to President Vladimir Putin’s options should he decide on a military incursion, the Pentagon said.

- The Federal Reserve could opt to raise its benchmark rate by 50 basis points if a more aggressive approach to taming inflation is needed, Raphael Bostic, president of the Fed’s Atlanta branch, told the Financial Times in an interview

- The Federal Reserve’s shift toward a major reduction of its footprint in the U.S. bond market this year has upended expectations for sustained cutbacks to the Treasury’s quarterly sales of longer-term debt — forcing dealers to gird for bigger auction sizes down the road

- The Reserve Bank of Australia is expected to announce the end of its bond purchases at its policy decision, setting the stage for an interest-rate hike in the third quarter

- BOE policy makers led by Governor Andrew Bailey are expected to hike interest rates to 0.5% on Thursday, according to a survey of economists by Bloomberg. That would complete the first back-to-back increase since 2004 and open the question of whether more increases will follow

- The ECB’s go-slow approach to monetary policy tightening is putting a wall around local bond markets against the global turmoil sparked by its U.S. counterpart

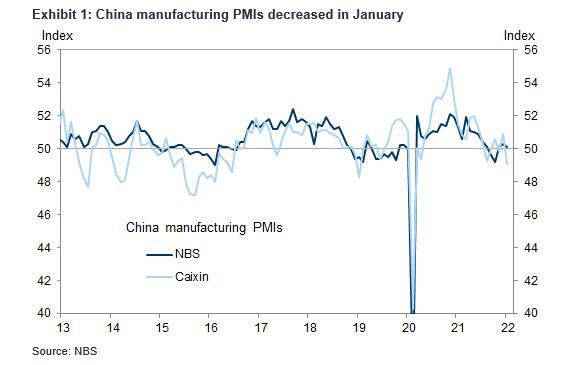

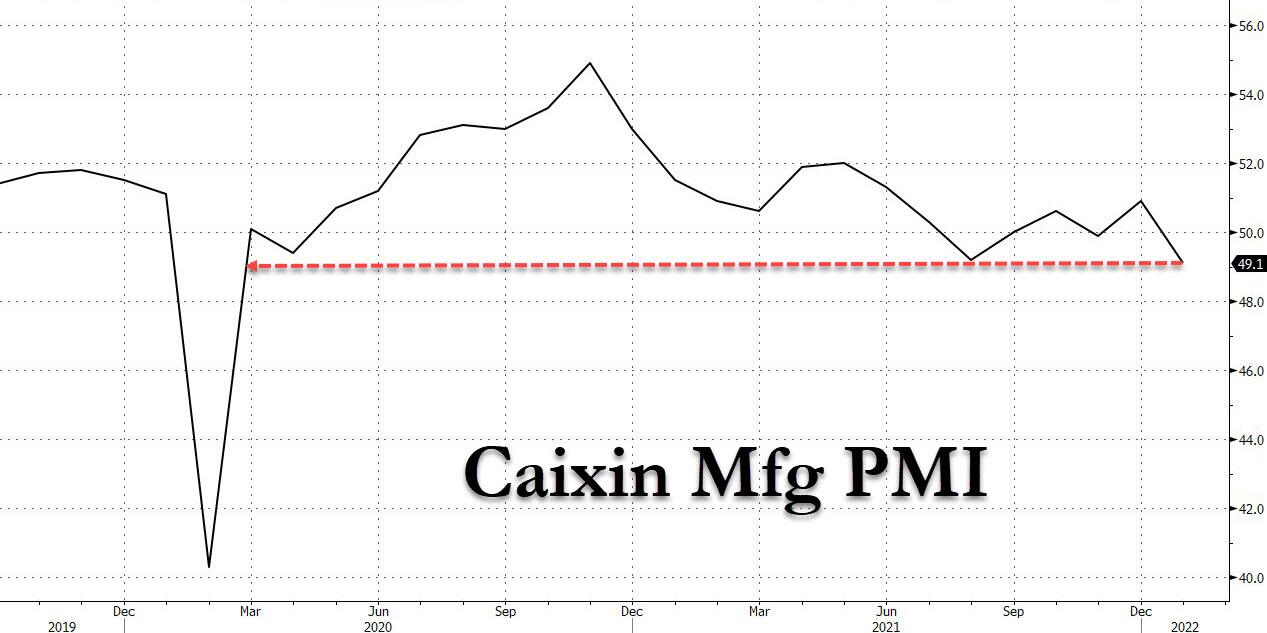

- China’s official manufacturing PMI declined to 50.1, the National Bureau of Statistics said Sunday, just above the median estimate of 50. The non-manufacturing gauge, which measures activity in the construction and services sectors, fell to 51.1, also marginally above the consensus forecast. The 50-mark separates expansion from contraction

- Investors are plowing money into hedge funds that don’t rely on the next macro genius or star stockpicker, but instead offer an army of traders who invest in an array of strategies. These behemoths secured pretty much all of the new money in the hedge fund industry last year, cementing a tectonic shift that’s accelerated since the pandemic

- Sales of bonds with sustainable targets have jumped sevenfold in Europe this month, competing with green debt to become the dominant force in the ethical market.

A more detailed look at global markets courtesy of Newsquawk

Asian stocks were mostly positive but with conditions thinned due to closures on Chinese New Year’s Eve. ASX 200 (-0.2%) was subdued with mining names pressured by lower metal prices and weaker output updates. Nikkei 225 (+1.1%) reclaimed the 27,000 level with the index underpinned by a weaker currency. Hang Seng (+1.1%) finished the shortened trading day higher with the index unfazed by mixed Chinese PMI data, while there was also an absence of Stock Connect flows with participants in the mainland away for the Lunar New Year.

Top Asian News

- Asian Stocks Climb With Tech Sector to Trim January Tumble

- Sri Lanka’s Inflation Accelerates to Asia’s Fastest on FX Crunch

- Sri Lanka Jan. Consumer Prices Rise 14.2% Y/y, Est. +13.2%

- JPMorgan Strategists See Better Risk-Reward for China and EM

European bourse kicked off the week with gains across the board before momentum waned (Euro Stoxx 50 +0.4%; Stoxx 600 +0.6%). European sectors have reconfigured to a more defensive bias since the European cash open; Tech outperforms and Basic Resource lag. US equity futures have eased off best levels to conform to a mostly downward bias; NQ (+0.5%) remains the outperformer.

Top European News

- U.K. Homebuilders ‘Deeply Undervalued,’ Have Spare Cash: HSBC

- Virgin Media O2 Said to Open Fiber Joint Venture Funding Talks

- Deliveroo Rises; Arete Cites Takeover Potential for Upgrade

- Orban Says Top EU Court Will Likely Reject Rule-of-Law Challenge

In FX, the dollar drifts along with other safe haven currencies as risk appetite improves into month end, but rebalancing flows should help the Buck find a base. Aussie regains composure in time for RBA policy meeting and manufacturing PMIs, while Kiwi tags along in slipstream amidst calls for the RBNZ to lift OCR to 2.5% by November. Pound holds firm pending Gray report and Partygate statement from PM Johnson. Euro regroups as Italian President Matarella agrees to serve second term and Portuguese PM Costa wins snap election unexpectedly. Turkish President Erdogan said they will lower interest rates and that inflation will fall too, while he also commented that problems which stem from a volatile FX rate and inflation are temporary, according to Reuters.

In commodities, WTI Mar’ and Brent Apr’ have been somewhat choppy with eyes on Russia and the upcoming OPEC+ meeting; NatGas holds onto overnight gains. Spot gold trades sideways below USD 1,800/oz ahead of a risk-packed week. LME copper meanwhile has seen a mild rebound from the USD 9,500/t with the red metal lacklustre overnight amid the absence of Chinese participants ahead of the Lunar New Year. German Nord Stream 2 approval is not expected during H1 this year, according to FAZ. IEA said Chinese gas demand growth forecast is to slow to 8% this year from 12% growth in 2021, while European gas demand forecast is to fall by 4.5% this year on higher coal consumption in the power sector, according to Reuters.

US Event Calendar

- 9:45am: Jan. MNI Chicago PMI, est. 61.8, prior 63.1, revised 64.3

- 10:30am: Jan. Dallas Fed Manf. Activity, est. 8.5, prior 8.1

- 11:30am: Fed’s Daly Speaks at Reuters Live Event

DB’s Jim Reid concludes the overnight wrap

It’s deja-vu all over again. I’m having yet more knee surgery today and will spend another 6 weeks on crutches with no weight bearing. Ironically I tore a hole in the cartilage while rehabbing the other knee. The fact that I can’t do squats and lunges without tearing my cartilage probably tells you the direction of travel for my knees. My surgeon wants to delay knee replacements as long as possible but I’ll be there eventually. Safe to say I’m unlikely to play tennis, squash, cricket and football etc, ever again. My opponents might suggest I didn’t really play them in the first place. So I exist to get my body back on the golf course asap.

Talking of football, if last week was a match it would have been one of the most exciting 0-0 draws in history. On the face of it, future historians might conclude that it must have been one of the dullest weeks in the NASDAQ’s history given that we closed the week +0.01% higher than the previous Friday, the fifth smallest % weekly move in the history of the index once we get down to the decimals. However beneath the surface there was extraordinary volatility as every day saw swings between 2.75% and 6%. Friday was seeing a recovery anyway but in the last 90 minutes the S&P 500 climbed c.2% and the NASDAQ over 2.5%. The S&P also ended the week higher (+0.77%), and saw the first positive week of the year. Until the market and the Fed stop leapfrogging each other in terms of interest rate expectations, the market will stay volatile. With such an extreme month, today’s month-end might see some position squaring so maybe there’ll be another late swing/surge/slump in the last 90 minutes.

Outside of stocktaking after a hectic month, what will this week hold in store for us? Well at least the Fed is out the way for now but central banks will continue to dominate the agenda as we move into February, with both the ECB and the Bank of England set to make their latest policy decisions on Thursday. Otherwise, there’ll be plenty of data to digest, including the all-important US jobs report on Friday, the final global PMIs tomorrow (manufacturing) and Thursday (services) and in the Euro Area there’s also the flash CPI reading for January (Wednesday) and the first look at GDP growth in Q4 (today). Earnings season will continue in full flow, with an additional 111 companies in the S&P 500 reporting, including Amazon (Thursday), Alphabet and Meta (both Wednesday). 56 report in the Stoxx 600.

China’s manufacturing PMI dipped to 50.1 on release yesterday, just above the 50 expected. The non-manufacturing slipped to 51.1, also marginally above consensus. Asian stock markets are trading higher this morning amid thin trading with markets in China and South Korea closed for the Lunar New Year holiday. The Nikkei (+1.39%) is up, erasing its opening losses while the Hang Seng (+1.07%) is also in positive territory.