SORRY THAT I WOULD NOT PROVIDE MORE DETAIL AS I WAS OUT MOST OF THE AFTERNOON

FEB 8

FEB8

· by harveyorgan · in Uncategorized · Leave a comment ·Edit

GOLD; UP $5.95 to $1827.15

SILVER: $23.19 UP 15 CENTS

ACCESS MARKET: GOLD: 1826.15..

SILVER: $23.19

Bitcoin: morning price: 43,068 DOWN 1368

Bitcoin: afternoon price: 44,031 DOWN 405

Platinum price: closing UP $10.85 to $1032.80

Palladium price; closing down $20.65 at $2249.35

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filed COMEX//NOTICES:EXCHANGE: COMEX FILED:EXCHANGE: COMEX 118/278CONTRACT: FEBRUARY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,820.600000000 USD

INTENT DATE: 02/07/2022 DELIVERY DATE: 02/09/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 19 14

332 H STANDARD CHARTE 8

363 H WELLS FARGO SEC 4

435 H SCOTIA CAPITAL 1

624 H BOFA SECURITIES 122

657 C MORGAN STANLEY 1

661 C JP MORGAN 250 65

661 H JP MORGAN 53

709 C BARCLAYS 8

732 C RBC CAP MARKETS 2

800 C MAREX SPEC 1 1

905 C ADM 7

TOTAL: 278 278

MONTH TO DATE: 16,806

NUMBER OF NOTICES FILED TODAY FOR FEB. CONTRACT: 278 NOTICE(S) FOR 27,800 OZ (0.8846 TONNES)

total notices so far: 16,806 contracts for 1,680,600 oz (52.273 tonnes)

SILVER NOTICES:

11 NOTICE(S) FILED TODAY FOR 55,000 OZ/

total number of notices filed so far this month 1249 : for 6,245,000 oz

GLD

WITH GOLD UP $5.95

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 4.36 TONNES OF GOLD INTO THE GLD//

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

CLOSING INVENTORY: 1015.96 TONNES/

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 15 CENTS:/:

A HUGECHANGE IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 3.143 MILLION OZ INTO THE SLV..

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY SLV/ TONIGHT: 544.573 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A TINY 375 CONTRACTS TO 148,206 AND RESTS FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND DESPITE THIS TINY LOSS IN OI, IT WAS ACCOMPANIED WITH OUR STRONG $0.52 GAIN ADVANCE IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.52) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A SMALL GAIN OF 435 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.110 MILLION OZ FOLLOWED BY TODAY’S 15,000 OZ QUEUE JUMP//NEW STANDING 6.330 MILLION OZ. V) TINY SIZED COMEX OI GAIN.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS -252

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB:

TOTAL CONTACTS for 6 days, total contracts: : 3511 contracts or 17.555 million oz OR 2.925 MILLION OZ PER DAY. (585 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 3511 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 17.555 MILLION OZ

.

LAST 10 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 17.555 MILLION OZ//

SPREADING OPERATIONS

(/NOW SWITCHING TO SILVER) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAR.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 375 DESPITE OUR STRONG $0.52 GAIN SILVER PRICING AT THE COMEX// MONDAY THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 558 CONTRACTS( 558 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 4.1 MILLION OZ FOLLOWED BY TODAY’S 15,000 OZ QUEUE JUMP //NEW STANDING 6.330, MILLION OZ// .. WE HAD A SMALL SIZED GAIN OF 183 OI CONTRACTS ON THE TWO EXCHANGES FOR 0.915 MILLION OZ//

WE HAD 11 NOTICES FILED TODAY FOR 55,000 OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 979 TO 509,402 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: — 145 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE SMALL SIZED INCREASE IN COMEX OI CAME DESPITE OUR STRONG GAIN IN PRICE OF $14.00//COMEX GOLD TRADING/MONDAY/.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION AS THE TOTAL GAIN ON OUR TWO EXCHANGES TOTALED 1774 CONTRACTS…

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR FEB AT 64.3 TONNES FOLLOWED BY TODAY’S 8400 OZ E.F.P. JUMP TO LONDON //NEW STANDING: 58.503 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $14.00 WITH RESPECT TO MONDAY’S TRADING

WE HAD A SMALL SIZED GAIN OF 1629 OI CONTRACTS (5.066 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALLED A SMALL SIZED 650 CONTRACTS:

FOR APRIL 650 ALL OTHER MONTHS ZERO//TOTAL:650

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 509,402.

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1629, WITH 979 CONTRACTS INCREASED AT THE COMEX AND 650 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1629 CONTRACTS OR 5.066TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (650) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (979,): TOTAL GAIN IN THE TWO EXCHANGES 1629 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 64.30 TONNES WHICH FOLLOWS TODAY’S EFP JUMP TO LONDON OF 8400 OZ//NEW STANDING 58.503 TONNES// 3)SOME LONG LIQUIDATION ,4) SMALL SIZED COMEX OI. GAIN 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

7575 CONTRACTS OR 757,500 oz OR 23.56 TONNES 6 TRADING DAY(S) AND THUS AVERAGING: 1263 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAY(S) IN TONNES: 23.56 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 23.56/3550 x 100% TONNES 0.6663% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 23.56 TONNES//INITIAL

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A TINY SIZED 375 CONTRACTS TO 148,206 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 558 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 558 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 558 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 375 CONTRACTS AND ADD TO THE 558 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED GAIN OF 183 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 0.915 MILLION OZ,

OCCURRED DESPITE OUR $0.52 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 23.05 PTS OR 0.67% //Hang Sang CLOSED DOWN 250.06 PTS OR 1.02% /The Nikkei closed UP 35.65 PTS OR 0.12% //Australia’s all ordinaires CLOSED UP 1.01% /Chinese yuan (ONSHORE) closed DOWN 6.3666 /Oil DOWN TO 89.73 dollars per barrel for WTI and DOWN TO 90.77 for Brent. Stocks in Europe OPENED ALL GREEN EXCEPT LONDON // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3666. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3674: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING WEAKER AGAINST USA DOLLAR

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 979 CONTRACTS AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS SMALL COMEX INCREASE OCCURRED DESPITE OUR STRONG GAIN OF $14.00 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (650 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF FEB.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 650 EFP CONTRACTS WERE ISSUED: ;: , & FEB. 0 APRIL: 650 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 650 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED 1629 TOTAL CONTRACTS IN THAT 650 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 915 CONTRACTS..

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR FEB (58.503),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

FEB 2022: 58.503 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $14.00)AND THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A GAIN OF 5.517 TONNES OF TOTAL OI, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR FEB (58.503 TONNES)…

WE HAD –145 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1774 CONTRACTS OR 177400 OZ OR 5.517 TONNES

Estimated gold volume today: 146,613 /// awful

Confirmed volume yesterday: 176,894 contracts poor

INITIAL STANDINGS FOR FEB ’22 COMEX GOLD //FEB 8

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 15,594.026 oz Manfra |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 278 notice(s) 27,800 OZ 0.8646 TONNES |

| No of oz to be served (notices) | 2003 contracts 200,300 oz 6.2302 TONNES |

| Total monthly oz gold served (contracts) so far this month | 16,806 notices 1,680,600 OZ 52.273 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

No dealer deposit 0

No dealer withdrawal 0

0 customer deposit

total deposit: nil oz

1 customer withdrawal

i) out of Manfra: 15,594.026 oz

total withdrawals: 15,594.026 oz

ADJUSTMENTS: 0.

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of FEBRUARY we have an oi of 2281 stand for LOSING 369 contracts.

We had 285 contracts served upon yesterday, so we lost 84 contracts or an additional 8,400 oz will not stand on this side of the pond and

these guys were E.F.P.’d to London where they received a handsome bonus for their effort. Looks like no gold to be found over here.

The month of March saw a loss of 285 contracts and thus the OI standing is 4749.

April saw a GAIN of 1745 contracts up to 393,440.

We had 285 notice(s) filed today for 28,500 oz FOR THE FEB 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 250 notices were issued from their client or customer account. The total of all issuance by all participants equates to 278 contract(s) of which 53 notices were stopped (received) by j.P. Morgan dealer and 65 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB /2021. contract month,

we take the total number of notices filed so far for the month (16,806) x 100 oz , to which we add the difference between the open interest for the front month of (FEB: 2281 CONTRACTS ) minus the number of notices served upon today 278 x 100 oz per contract equals 1,880,900 OZ OR 58.503 TONNES the number of TONNES standing in this active month of FEB.

thus the INITIAL standings for gold for the FEB contract month:

No of notices filed so far (16,806) x 100 oz+ (2281) OI for the front month minus the number of notices served upon today (278} x 100 oz} which equals 1,880,900 oz standing OR 58.503 TONNES in this active delivery month of FEB.

We lost 84 contracts or an additional 8400 oz will not stand over here and were EFP’d. to London

TOTAL COMEX GOLD STANDING: 58.503 TONNES (HUGE FOR A FEBRUARY DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

157,392.690, oz NOW PLEDGED /HSBC 4.89 TONNES

125,410.592 PLEDGED MANFRA 2.90 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690

288,481,604, oz JPM No 2 8.97 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonne

Loomis: 18,615.429 oz

total pledged gold: 1,553,863.297 oz 48.331 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 32,736,080.891 OZ (1018.22 TONNES)

TOTAL ELIGIBLE GOLD: 15,419,906.305 OZ (479.62 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,316,174.586 OZ (538.60 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,762,311.0 OZ (REG GOLD- PLEDGED GOLD) 490.27 tonnes

END

FEBRUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//FEB 8

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 198,322.08oz Brinks Manfra |

| Deposits to the Dealer Inventory | 572,166.170OZ Brinks |

| Deposits to the Customer Inventory | 600,812.220 oz CNT |

| No of oz served today (contracts) | 11CONTRACT(S) 55,000 OZ) |

| No of oz to be served (notices) | 17 contracts (85,000 oz) |

| Total monthly oz silver served (contracts) | 1249 contracts (6,245,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

| month |

And now for the wild silver comex results

we had 1 deposits into the dealer

i) Into Brinks: 572,166.170 oz

total dealer deposits: 572,166.170 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposit into the customer account

i) Into CNT: 600,812.220 oz

total deposit: 600,812.220 oz

JPMorgan has a total silver weight: 184.649 million oz/353.197 million =52.42% of comex

ii) Comex withdrawals: 2

Out of Brinks: 21,427.530 oz

ii) Out of Manfra: 176,894.550

total withdrawal 198,322.08 oz

we had 1 adjustments dealer to customer

a)Brinks 282,843.100 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 81.443 MILLION OZ

TOTAL REG + ELIG. 353,197 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR FEBRUARY

silver open interest data:

FRONT MONTH OF FEB//2022 OI: 28 CONTRACTS LOSING 27 contracts on the day. We had 30 contracts served upon yesterday.

So we gained 3 contracts or an additional 15,000 oz will stand for silver on this side of the pond.

FOR MARCH WE HAD A LOSS OF 7221 CONTRACTS DOWN TO 93,231 CONTRACTS.

APRIL HAD A SMALL GAIN OF 2 CONTRACTS UP TO 65

MAY HAD A GAIN OF 6857 CONTRACTS UP TO 37,876 contracts

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 11 for 55,000 oz

Comex volumes: 65,977// est. volume today//fair to good

Comex volume: confirmed YESTERDAY: 77,272 contracts (good)

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 1249 x 5,000 oz =. 6,1245,000 oz

to which we add the difference between the open interest for the front month of FEB (28) and the number of notices served upon today 11 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2021 contract month: 1249 (notices served so far) x 5000 oz + OI for front month of FEB (28) – number of notices served upon today (11) x 5000 oz of silver standing for the FEB contract month equates 6,330,000 oz. .

We gained 3 CONTRACTS OR 15,000 ADDITIONAL oz of silver will stand at the comex.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

GLD

FEB 8/WITH GOLD UP $5.95 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1015.96 TONNES

FEB 7/WITH GOLD UP $14.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.24 TONNES FROM THE GLD/////INVENTORY RESTS AT 1011.60 TONNES//

FEB 4/WITH GOLD UP $3.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.84 TONNES

FEB 3/WITH GOLD DOWN $5.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 1016.59 TONNES

FEB 2/WITH GOLD UP $7.95//A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.78 TONES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1018.04 TONNES

FEB 1/WITH GOLD UP $5.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 31/WITH GOLD UP $10.10//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 28/WITH GOLD DOWN $8.30//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 27/WITH GOLD DOWN $36.15//ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES INTO THE GLD.//INVENTORY RESTS AT 1014.26 TONNES

JAN 26/WITH GOLD DOWN $21.60 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES INTO THE GLD///INVENTORY RESTS AT 1013.10 TONNES

JAN 25/WITH GOLD UP $10.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 24/WITH GOLD UP $10.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: AN UNBELIEVABLE DEPOSIT OF 27.59 TONNES INTO THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 21/WITH GOLD DOWN $10.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 980.86 TONNES

JAN 20/WITH GOLD UP $.20 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 980.86 TONNES

JAN 19/WITH GOLD UP $29.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 5.27 TONNES INTO THE GLD/INVENTORY RESTS AT 981.44 TONNES

JAN 18/WITH GOLD DOWN $3.25//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 14/ WITH GOLD DOWN $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 13/WITH GOLD DOWN $5.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 12/WITH GOLD UP $8.65//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 11/WITH GOLD UP $19.25/A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FROM THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 10/WITH GOLD UP $2.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.08 TONNES

JAN 7/WITH GOLD UP $8.15//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWLA OF 1.16 TONNES FROM THE GLD////INVENTORY RESTS AT 978.83 TONNES

JAN 6/WITH GOLD DOWN $35.30//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .32 TONNES/INVENTORY RESTS AT 979.99 TONNES

JAN 5/WITH GOLD UP $10.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 980.31 TONNES

CLOSING INVENTORY: 1015.96 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SLV

FEB 8/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.143 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 7/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.218 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 541.430 MILLION OZ/

FEB 4/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 539.212 MILION OZ

FEB 3/WITH SILVER DOWN 35 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT539.212 MILLION OZ//

FEB 2/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.411 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 539.212 MILLION OZ/

FEB 1/WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.801 MILLION OZ

JAN 31/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FORM THE SLV.//INVENTORY RESTS AT 533.801 MILLION OZ//

JAN 28/WITH SILVER DOWN 36 CENTS : NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 27/WITH SILVER DOWN $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 26/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 25/WITH SILVER UP 10 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.311 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 535.003 MILLION OZ/

.JAN 24/WITH SILVER DOWN 48 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.8 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 532.692 MILLION OZ//.

JAN 21/WITH SILVER DOWN 41 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 527.792 MILLION OZ

JAN 20/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.998 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 527.792 MILLION OZ

JAN 19/WITH SILVER UP 71 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.942 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 525.804 MILLION OZ

JAN 18/WITH SILVER UP 51 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS OF 1.11 MILLION OZ AND 1.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 527.246 MILLION OZ//

JAN 14/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 529.780 MILLION OZ//

JAN 13/WITH SILVER DOWN 2 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 832,000 OZ FROM THE SLV////INVENTORY RESTS AT 529.780 MILLION OZ

JAN 12/WITH SILVER UP 38 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//

JAN 11/WITH SILVER UP 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ/.

JAN 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 7/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 6/WITH SILVER DOWN 94 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL PF 226,000 OZ FROM THE SLV///INVENTORY RESTS AT 530.612 MILLION OZ?/

JAN 5/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 4/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 3/WITH SILVER DOWN 45 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.219 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 530.838 MILLION OZ//

CLOSING INVENTORY: 544.573 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS

LAWRIE WILLIAMS: Latest prediction – gold at $2,100 by year end.

I had gone on record in my writings that the gold price would recover from its sharp post-FOMC meeting falls to back above $1,800 by last week, while silver might be a little slower to regain the $23 level, but would probably do so by this week. Equity prices would likely trend a little lower as the likely effects of the U.S. Federal Reserve (the Fed)’s more aggressive easing proposals generate more detailed analysis. So it has come to pass and, as I write, gold is at over $1,820, silver is at around $23.20 and global equities have been mostly falling.

That is the logical outcome of the Fed’s proposed remedies to counter the current high inflation levels now that it claims to have brought unemployment levels down to where they perhaps should be. In our view, however, these moves in precious metals prices and equities have not yet gone far enough. The gold:silver ratio has also reacted positively for silver in that it has come down below 79 after peaking at close to 81 only a week ago.

True the Fed will have found some justification for its proposals in the latest official nonfarm payroll data which has shown strong job creation levels as we are beginning to exit the adverse effects of pandemic-controls, but perhaps these recoveries and downturns have not yet gone far enough. Equities have fallen, but not yet dived sufficiently so to cause alarm and force the Fed to reverse some of its proposals.

We are thus looking for continued upwards movement in precious metals prices and further equity falls. These would likely occur once the Fed tightening programme actually starts to get under way, and particularly if rises in interest rates look as being as aggressive as many market analysts and commentators are predicting. The Fed’s moves, once they start to take effect, could be far more damaging to equity markets and the U.S. economy than most market influencers are prepared to admit.

Let us consider again what the likely effects of Fed policy changes will be. The ending of the asset purchasing programme, which has indirectly been filtering excess money into the equity markets, will alone be a massive blow to seemingly ever-continuing stock price rises. Higher interest rates will begin to reverse the excessively low borrowing costs which have enabled businesses to expand at a very low cost. Inflation seems to be continuing to increase to the kinds of levels which will lead to a downturn in retail sales as consumers need to tighten their belts accordingly.

We should interject here that the real inflation rate being experienced by the general public may well be around double that suggested by official government figures. John Williams (no relation) who runs the thought-provoking shadowstats service, calculates official government data in the way it used to be assessed before being massaged to present a less-damning picture – almost all governments tend to do these kinds of goalpost moving data restructuring exercises. This service assesses current U.S. cost inflation at near 15% as compared with the official Consumer Price Index (CPI) figure of 7%. The shadowstats calculation probably represents the real price rises being experienced by the average householder far better than the official CPI data would suggest.

As for precious metals, these do not generate interest per se. They do tend to hold their value against domestic currencies, though, and whatever the Fed does it will not be able to raise interest rates fast enough to make real interest rates positive (i.e. higher than the inflation rate) for some time to come. A zero interest rate generator is thus a far better asset to hold in times of negative real rates, which is the primary reason gold and silver in particular dominate as safe haven assets, particularly if other popular investment options, like equities, are seen as vulnerable.

Interestingly the latest gold price outlook from Wells Fargo Bank seems to take all the above factors into account and is thus somewhat ahead of the herd. We would anticipate other bank analysts to come up with similar conclusions as the Fed’s tightening programme gets under way. Wells Fargo analyst Austin Pickle comments as follows: “Risk asset returns may be choppier with higher volatility this year, which could prompt a rotation back into the perceived safe- haven — gold. The bull commodity supercycle should lend its support as well, as it is the tide that lifts all commodity boats.” Pickle thus feels that gold could end the year at around the $2,100 level – slightly higher therefore than our own estimate of a flat $2,000. However it’s nice to have confirmation that we are not the only ones predicting a strong gold price increase over the remainder of the year.

08 Feb 2022

end

3. Chris Powell of GATA provides to us very important physical commentaries

END

4.OTHER GOLD/SILVER COMMENTARIES

END

5.OTHER COMMODITIES/

6.CRYPTOCURRENCIES

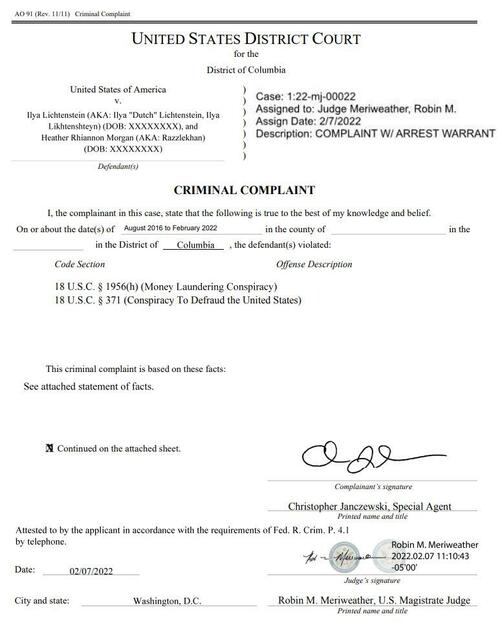

‘The Largest Financial Seizure Ever’ – DoJ Recovers Billions In Bitcoin From 2016 Bitfinex Hack, Couple Arrested

TUESDAY, FEB 08, 2022 – 11:56 AM

In what the Department of Justice is calling ‘the largest financial seizure ever’, the U.S. seized about $3.6 billion in Bitcoin stolen during a 2016 hack of the Bitfinex currency exchange.

On August 2, 2016, the exchange Bitfinex was hacked for approximately 119,756 BTC.

Notably, the stolen cryptocurrency was valued at $71 million at the time of the theft, is now valued at $4.5 billion, officials said.

Ilya Lichtenstein and his wife, Heather Morgan, were arrested in Manhattan on Tuesday morning and face federal charges of conspiracy to commit money laundering and conspiracy to defraud the United States.

“Today’s arrests, and the Department’s largest financial seizure ever, show that cryptocurrency is not a safe haven for criminals,” Deputy Attorney General Lisa Monaco said in a statement.

“In a futile effort to maintain digital anonymity, the defendants laundered stolen funds through a labyrinth of cryptocurrency transactions.”

According to court documents, Lichtenstein and Morgan allegedly conspired to launder the proceeds of 119,754 bitcoin that were stolen from Bitfinex’s platform after a hacker breached Bitfinex’s systems and initiated more than 2,000 unauthorized transactions.

Those unauthorized transactions sent the stolen bitcoin to a digital wallet under Lichtenstein’s control.

Over the last five years, approximately 25,000 of those stolen bitcoin were transferred out of Lichtenstein’s wallet via a complicated money laundering process that ended with some of the stolen funds being deposited into financial accounts controlled by Lichtenstein and Morgan.

According to DOJ, the couple used sophisticated techniques, including “using fictitious identities to set up online accounts; utilizing computer programs to automate transactions, a laundering technique that allows for many transactions to take place in a short period of time; depositing the stolen funds into accounts at a variety of virtual currency exchanges and darknet markets and then withdrawing the funds.”

The remainder of the stolen funds, comprising more than 94,000 bitcoin, remained in the wallet used to receive and store the illegal proceeds from the hack. After the execution of court-authorized search warrants of online accounts controlled by Lichtenstein and Morgan, special agents obtained access to files within an online account controlled by Lichtenstein.

Those files contained the private keys required to access the digital wallet that directly received the funds stolen from Bitfinex, and allowed special agents to la^vfully seize and recover more than 94,000 bitcoin that had been stolen from Bitfinex.

The recovered bitcoin was valued at over S3.6 billion at the time of seizure.

Lichtenstein and Morgan face up to 20 years in prison for the money laundering charges they face. In addition, they face an additional sentence of up to five years for conspiracy to defraud the U.S., according to the Justice Department statement.

Michael Saylor could not resist…

Steve Brown..

end

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.3666

OFFSHORE YUAN: 6.3674

HANG SANG CLOSED DOWN 250.06 PTS OR 1.02%

2. Nikkei closed UP 35.65 PTS OR 0.13%

3. Europe stocks ALL GREEN EXCEPT LONDON

USA dollar INDEX UP TO 95.61/Euro FALLS TO 1.1417-

3b Japan 10 YR bond yield: RISES TO. +.208/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 115.56/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 89.73 and Brent: 92.47–

3f Gold UP /JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE CLOSED DOWN// OFF- SHORE DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.267%/Italian 10 Yr bond yield FALLS to 1.85% /SPAIN 10 YR BOND YIELD RISES TO 1.17%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.58: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 2.67

3k Gold at $1827.05 silver at: 23.19 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble UP 33/100 in roubles/dollar AT 75.07

3m oil into the 89 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 115.57 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9248– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0558 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

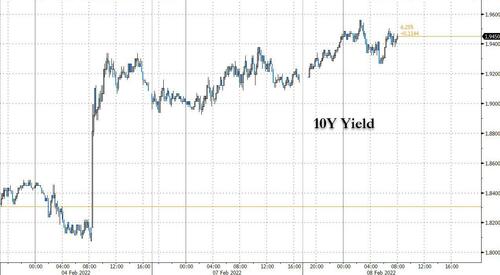

USA 10 YR BOND YIELD: 1.959 UP 4 BASIS PTS

USA 30 YR BOND YIELD: 2.258 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.77

Futures Swing As Treasury Yields Near 2%, China Plunge-Protectors Activated

TUESDAY, FEB 08, 2022 – 08:08 AM

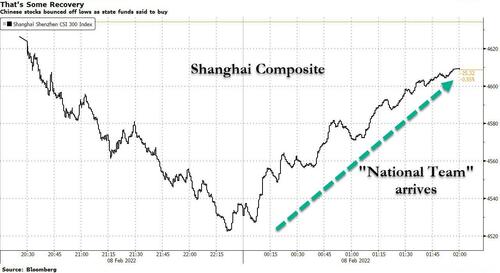

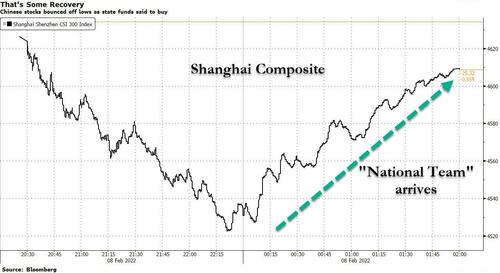

US equity futures have again swung sharply in illiquid overnight trade, and after yesterday’s wild dump in the last hour of trading, emini futures initially made some gains only to lose it all as US traders came to their desks as investors monitored the latest jump in Treasuries yields and as expectations for aggressive rate hikes mount. The yield on the U.S. 10-year Treasury traded as high as 1.9559% – a level last seen in December 2019 – closing in on 2% while Nasdaq 100, S&P 500 and Dow Jones futures all traded modestly in the red. Oil slid on potential de-escalation in Russia-Ukraine tensions and the resumption of Iran nuclear talks, while stocks in Europe made gains. Chinese stocks also tumbled, suffering their biggest intraday drop since August 2021, before the Beijing PPT in the face of Chinese state-backed funds intervened in the stock market on Tuesday, helping the benchmark index stage a strong recovery. Bitcoin declined for the first time in six days, falling below $44,000.

“We consequently see the announced combination of tapering, hiking and balance-sheet reduction in the same year as too risky for financial markets,” said Unigestion’s head of macro and dynamic allocation, Guilhem Savry. “The risks for U.S. growth are greater than highlighted by the Fed, and we see little room for a strong upside in risky assets.”

In premarket trading, shares in U.S.-listed Chinese stocks, including Alibaba Group Holding rose after Bloomberg reported that state-backed funds were said to have intervened in the Chinese stock market on Tuesday amid a worsening rout. China’s CSI 300 Index ended down just 0.6% at the close, paring an earlier slump of 2.4%, as state-related funds entered the market to buy local shares in the afternoon session, Bloomberg reported citing two sources.

Pfizer declined in premarket trading after its 2022 revenue forecast missed estimates (unclear if the company will now push to vaccinate embryos, pets and dead people next). Velodyne Lidar soared after Amazon.com Inc. acquired warrants that could result in a potential stake in the auto-sensor maker Here are some other notable premarket movers:

- Peloton (PTON US) drops 14% in premarket after the Wall Street Journal reports that Chief Executive Officer John Foley will step down and become executive chair. The maker of exercise bikes will also shed about 2,800 jobs, WSJ said.

- Nvidia (NVDA US) is abandoning its purchase of Arm from SoftBank, according to people familiar with the situation. Falls 1.3% in premarket.

- General Motors (GM US) shares slide 3.1% in premarket trading after Morgan Stanley analyst Adam Jonas cuts stock to equal-weight from overweight, citing lower than expected 2022 outlook.

- Selectquote (SLQT US) slumps as much as 48% in premarket trading after the insurance agency’s revenue forecast missed the average analyst estimate.

- Velodyne Lidar (VLDR US) jumps 42% in premarket trading after Amazon.com acquired warrants that could result in a potential stake in the auto-sensor maker.

- Second Sight Medical (EYES US) climbed 15% in premarket trading after announcing Monday evening it agreed to buy Nano Precision Medical for ~134m shares.

- U.S.-listed Chinese stocks, including Alibaba, rise in premarket trading, following a report that Chinese state-backed funds were said to have intervened in the Chinese stock market on Tuesday amid a worsening rout. Alibaba (BABA US) +0.8%, DiDi (DIDI US) +1.1%.

- Chegg (CHGG US) gains 8% in premarket trading after the online education company’s first- quarter and full-year revenue forecast beat the average analyst estimate.

- Graham (GHM US) tumbled 27% in extended trading after the industrials company cut its revenue outlook for fiscal 2022. It also suspended its dividend.

- Editas Medicine (EDIT US) falls 13% in premarket after saying the employment of Chief Medical Officer Lisa Michaels with the genome-editing company “was terminated.” She worked in the post for about 15 months.

- Bowlero (BOWL US) gained 5.4% in postmarket trading after the operator of bowling centers said its board has approved a $200 million share and warrant buyback program through Feb. 3, 2024.

Investors are awaiting data Thursday expected to show stubbornly high U.S. inflation. That could inject further volatility into financial markets bracing for a Federal Reserve cycle of rate hikes and eventual balance-sheet reduction. But the rise in yields could also support some equities, like banks and value stocks, according to Goldman Sachs Group Inc., amid generally solid earnings.

“Markets will get used to the tightening regime at some point,” Chris Iggo, chief investment officer, core investments at AXA Investment Managers, wrote in a note. “The growth and earnings forecast revisions in the next few months will be key.”

Investors are assessing the likely broader impact of Fed policy, “particularly within credit markets,” Kristen Bitterly, head of North America investments at Citi Global Wealth, said on Bloomberg Television. “That is what most investors are looking at right now in terms of what can actually inject volatility into the broader market.”

In Europe, the Stoxx Europe 600 index erased an earlier advance, with a drop in the technology sector weighing on the benchmark. Basic-resources stocks jumped more than 2% as iron ore roared past $150 a ton and aluminum headed toward a four-month high. BP Plc gained after reporting strong earnings and announcing a share buyback. Miners, insurance and banks were the strongest performing sectors; tech lags. Here are some of the biggest European movers today:

- Orpea rise as much as 11% alongside peer Korian, rallying after investors dumped shares in retirement-home operators due to allegations of mistreatment of elderly people at Orpea.

- BP advances as much as 2.3% after boosting its share buyback as its profit soared. Analysts noted strong cashflow and guidance.

- Continental rises after Handelsblatt reported it plans to make its Autonomous Mobility unit independent and may consider an IPO in the future, citing unidentified people familiar with the matter.

- AMS-Osram stock rises as much as 7.4%. Results beat estimates, helped by strong demand and high capacity utilization in auto sector, according to ZKB analyst Andreas Mueller.

- Befesa rises after Kepler upgrades the stock to buy, saying the latest market wobbles have created an attractive entry point for Befesa’s high-quality stock.

- Ocado shares plunge as much as 13%, the biggest decliner in the Stoxx 600 Index, after the British online grocer reported FY21 results that missed market expectations.

- Yara shares tumble as much as 7% after 4Q earnings missed estimates. Analysts claimed the miss was due to a time lag and isn’t reflective of the largest nitrogen producer’s fundamentals.

Asian equities fluctuated, as a broad selloff in Chinese stocks countered gains in financials along with rising bond yields. The MSCI Asia Pacific Index rose as much as 0.6% before erasing that gain and dipping 0.1%. Indexes dropped in China and Hong Kong while Australia and Singapore shares rose. Wuxi Biologics was the biggest drag on Hong Kong’s benchmark gauge, plunging by a record before trading was halted as the U.S. added the firm and other entities to its “unverified” list. The latest tensions between Beijing and Washington further cloud the outlook for China stocks after the CSI 300 Index entered a bear market just before the Lunar New Year holidays.

As noted above, China’s national team stepped into prevent a market rout, helping the CSI 300 index to close down just 0.6% after tumbling 2.0% earlier. The move by state funds was intended to slow the pace of declines, a Bloomberg source said, noting that financial shares including brokerages were among those to have been purchased. Sub-gauges of cyclical sectors such as energy, utilities and financials posted gains in Tuesday’s session even as the benchmark ended lower. There was no information on the amount purchased or the frequency of such buying.

Historically, Beijing has supported markets when needed around significant events or dates. The funds stepped in to stem a market rout during the National People’s Congress in March last year. Stocks on the mainland have had a weak start to 2022 as the monetary policy divergence between Beijing and Washington — touted as one key reason for global brokerages to recently turn bullish on Chinese shares — has yet to lead to any meaningful gains. Even last month’s cut to a key interest rate failed to excite local traders, with the CSI 300 down 6.7% so far this year.

Asian equities overall have been relatively less scathed than U.S. peers by the prospect of tighter monetary policy from the Federal Reserve. The Asian stock benchmark is down less than 3% so far this year, helped by a recent rebound, compared with a decline of nearly 6% in the S&P 500 Index. Sentiment remains fragile, however, as investors brace for central bank policy decisions this week from India, Thailand and Indonesia, as well as U.S. inflation data. “The bearish sentiment that has engulfed markets this past month has all to do with changing fundamentals and their potential impact on corporate earnings, and hence on valuations,” said Olivier d’Assier, head of APAC applied research at Qontigo, adding that investors should re-evaluate firms given a hawkish monetary policy

In rates, Treasuries remained under pressure, with yields higher by 2bp-3bp across the curve, after 10-year rose as much as 4bp to YTD high 1.956%. Treasury 10-year yield is just below 1.95%, where convexity hedging is expected to pick up; curve spreads are within 1bp of Monday’s closing levels. Refunding auction cycle begins with 3-year note sale at 1pm ET; 10- and 30-year new issues follow over next two days. Today’s auction includes $50b 3-year note, followed by the sale of a $37b 10-year note Wednesday and $23b 30-year bond Thursday. WI 3-year yields at ~1.588% is above auction stops since December 2019 and ~35bp cheaper than last month’s, which stopped 0.4bp through.

German Bunds bull-steepened, richening 4bps across the short end. Gilts bear-steepen with long end yields ~3bps higher. USTs bear-flatten, trading broadly in line with gilts at the short end. Most peripheral spreads fade an initial widening move, short-end Spain outperforms. 10y Bund/BTP spread remains slightly wider on the session.

In FX, Bloomberg dollar spot index rose as the greenback traded steady to higher versus most of its Group-of-10 peers, while NZD and GBP are the strongest performers in G-10 FX, NOK, CAD and EUR underperform. The euro temporarily dropped below $1.14 before steadying and European bonds reversed an early decline. The euro’s advance versus its Group-of-10 peers since the latest ECB policy decision is less pronounced versus the Swedish krona in the spot market and options bets are extensively in favor of the currency. The pound advanced versus the euro for the second day as traders weighed comments from ECB President Christine Lagarde on Monday, in which she stressed a “gradual” approach to adjusting monetary policy. Australian and New Zealand sovereign bond yields hit multi-year highs after their U.S. counterpart rose on bets for more aggressive Federal Reserve rate hikes; the RBA is seen raising rates to 1.25% this year by swaps traders. Japan’s benchmark 10-year government bond yield rose to a fresh six-year high, as markets tested the Bank of Japan’s tolerance for such moves; the yen fell

In commodities, crude futures slumped after French President Macron told reporters he got assurances from Russia’s Putin of no more escalation. WTI snapped 2% lower before finding support near $89, Brent drops below $91. Most base metals trade in the red; LME nickel falls 1.2%, underperforming peers. LME aluminum outperforms. Spot gold is little changed at $1,820/oz

Bitcoin declined for the first time in six days, falling below $44,000.

Looking at today’s calendar, it’s a fairly quiet day ahead – data releases include the US trade balance and Italian retail sales for December, and from central banks we’ll hear from the ECB’s Villeroy. Pfizer, KKR and Peloton are among the companies reporting results today.

Market Snapshot

- S&P 500 futures down 0.1% to 4,466.5

- STOXX Europe 600 up 0.8% to 469.03

- MXAP little changed at 187.59

- MXAPJ down 0.1% to 613.73

- Nikkei up 0.1% to 27,284.52

- Topix up 0.4% to 1,934.06

- Hang Seng Index down 1.0% to 24,329.49

- Shanghai Composite up 0.7% to 3,452.63

- Sensex up 0.4% to 57,866.39

- Australia S&P/ASX 200 up 1.1% to 7,186.69

- Kospi little changed at 2,746.47

- German 10Y yield little changed at 0.22%

- Euro down 0.3% to $1.1403

- Brent Futures down 0.6% to $92.13/bbl

- Gold spot down 0.1% to $1,818.69

- U.S. Dollar Index up 0.24% to 95.63

Top Overnight News from Bloomberg

- ECB Governing Council member Pablo Hernandez de Cos says he expects inflation to moderate, though there are currently upside risks to prices, especially in the short term

- While conventional logic suggests rising yields should buoy the greenback, traders are now betting the Fed’s policy tightening will crimp economic growth down the road. Demand for dollar call-options has plummeted to the lowest in nine months with the currency erasing its year-to-date gains. That’s the putting dollar bulls at Morgan Stanley, Bank of America Corp. and Citigroup Inc. on the defensive

- European natural gas prices rose after U.S. President Joe Biden said the controversial Nord Stream 2 pipeline won’t move forward if Russia invades Ukraine. Russian flows through a key route also declined

A more detailed look at global markets courtesy of Newsquawk

Asian stocks were mixed after the choppy mood in the US with global newsflow dominated by geopolitical headlines despite a lack of developments. ASX 200 (+1.1%) was led by miners and with the top-weighted financials sector lifted after earnings updates from Macquarie and Suncorp. Nikkei 225 (+0.1%) was supported by favourable currency flows and after US agreed to roll back Trump-era steel tariffs on a quota of Japanese steel products, but with upside limited after disappointing data including the miss on Household Spending and Labour Cash Earnings. Hang Seng (-1.0%) and Shanghai Comp. (+0.7%) initially pressured with Hong Kong announcing tighter COVID19 restrictions and amid US-China related frictions in which WuXi Biologics slumped more than 30% and its shares were halted after the inclusion of two units in the US ‘unverified’ list, while tech was also subdued with the ChiNext board now eyeing a bear market.

Top Asian News

- Asian Stocks Steady as China Slides, Financials Rise With Yields

- China Eases Loan Curbs on Public Rental Homes: Evergrande Update

- Abu Dhabi Ports’ Stock Surges After $1.1 Billion Share Sale

- Nissan Raises Profit Outlook on High Car Prices, Weaker Yen

European bourses are also mixed and in proximity to the unchanged mark following an indecisive open. Performance briefly picked up amid reports regarding China State funds, but this was shortlived and followed by a pullback. Sectors are mixed as Basic Resources & Banks outperform on base metals/yields while Tech lags on the latter and as the NQ probes negative territory. US futures are similarly mixed/unchanged, action directionally following European peers but has been more contained thus far.

Top European News

- European Gas Rises After Biden Issues Warning on Nord Stream 2

- Continental Weighs Options for Automated Driving Unit: HB

- Goldman Strategists See End of Europe’s Stock Woes in ECB Pivot

- Danske Picks Blessing as Chair as Bank Recoups From Scandal

In FX, the DXY was firmer around 95.50 pivot point as UST curve flips and flattens. Euro hands back more ECB inspired gains as President Lagarde warns against hasty hawkish conclusions. Loonie and NOK recoil in tandem with WTI and Brent. Yen yields to Buck bounce and technical headwinds after failing to breach resistance. Sterling boosted by EUR/GBP reversal, but Cable faces upside option expiry interest. Former RBA board member Edwards sees the RBA to start moving rates in August and thinks there could be four rate hikes this year, according to WSJ. Also, ANZ Bank sees every meeting by the RBA in June to be live.

In commodities, WTI and Brent have been extending to the downside throughout the European morning, with focus firmly on geopolitics; sending the benchmarks to lows of USD 89.01/bbl & USD 90.18/bbl. Numerous updates regarding Russia after yesterday’s talks with Macron who voiced progress; albeit, the Kremlin as expected highlighted a failure to achieve a deal. Iranian Vienna talks resume today and initial commentary has Iran sounding somewhat less optimistic. Spot gold/silver are softer but contained and in familiar levels around numerous DMAs.

US Event Calendar

- 6am: Jan. SMALL BUSINESS OPTIMISM, 97.1, est. 97.5, prior 98.9

- 8:30am: Dec. Trade Balance, est. -$83b, prior -$80.2b

DB’s Jim Reid concludes the overnight wrap

Last week’s global bond selloff has carried over into this one, with longer-end yields hitting new highs as markets adjust to the recent newsflow, even if the front end rallied a bit yesterday after an initial morning sell-off. This ultimately left curves steeper. A late European session speech from ECB President Lagarde helped calm peripheral spreads after a mini rout in the morning.

We’ll get to exactly what she said shortly but let’s look at the move and vol in bond markets, especially in Europe. At the wides for the day, 10yr BTPs and Greek bonds were +10.5bps and +25.5bps wider respectively. 10yr BTPs yields peaked before lunchtime and only closed +1.5bps wider. 2yr BTPs saw a bigger range, hitting 0.47% at the highs (+14.5bps) before closing at 0.30%, -2.1bps lower for the day. In Greece, 10yr yields only came back -6.1bps from the highs and closed +22.0bps at 2.45%. Note that at the lows in mid-2021, Greek 10yr yields got close to 0.5%. One to watch as the ECB accelerates pull back.

In the core of Europe, 10yr bunds (+2.0bps), which closed at 0.22%, and OATs (+1.8bps) both hit their highest level since January 2019. In both cases it was rising real yields that led the upward moves, with inflation breakevens actually declining as investors remain relatively calm for the time being that central banks can keep a grip on longer-term inflation. After opening a few bps higher, 2yr notes in both regions ended the day lower, declining -3.9bps in Germany and -2.0bps in France.

Credit started to crack in the morning and started to show signs of stress. EU iTraxx Main was over +5bps at one point before closing +2.75bps wider. The last +5bps daily move was on September 20th, when the market was briefly concerned about the potential of an Evergrande default. Crossover was +25bp in the morning but closed +12bps wider. IG is under-performing HY which makes sense if you believe we’re in a rates/central bank tantrum and not yet at a stage where there’s a real economic threat. Europe is also under-performing US in recent days which again makes sense given Europe has been the latest rates market to have been shaken. The peripheral widening of recent days has not helped European credit either. We are getting closer to what we thought were fairly aggressive widening targets for H1 from our 2022 outlook published in November. Back then we felt that after the rates tantrum we would eventually recognise the economy would survive it and we would recover. We will have to review that call one way or another soon. For now, no reason to suggest the thesis will change.

So what did ECB President Lagarde say in her address to lawmakers in the European Parliament yesterday? Overall her remarks struck a similar tone to the ECB communications last week, noting that inflation risks have moved to the upside, and did not explicitly push back on the market repricing of tighter ECB policy. She did highlight that the ECB would take a gradual approach to tightening policy, drawing a distinction from other advanced economies that may need to tighten quicker, and that the ECB would remain flexible and data dependent. Crucial for the intraday turnaround in peripheral spreads, President Lagarde voiced resolute support for the periphery across multiple questions, noting the ECB will use any instrument to ensure policy is transmitted to all member states.

Even if we’re a long way from crisis territory, the coming months will be fascinating in terms of just how far central banks are able to go when it comes to tackling inflation, and investors are getting more confident that we’re set to see plenty of hikes from global central banks over the coming months. Indeed, even if the Fed hikes in line with what futures are pricing (5 hikes in 2022) and doesn’t move to go faster, 125bps worth of hikes in a calendar year would still be the most we’ve seen since 2005, so a completely different playbook to the last cycle. And speaking of the US, there was a smaller rise in longer-dated sovereign bonds there yesterday, with 10yr Treasury yields up +0.7bps to 1.92%, just shy of their closing peak in December 2019. In Asia we are above that level though at 1.943% as I type.

Equities had a relatively quieter day, although the impact of widening spreads was evident as Italy’s FTSE MIB (-1.03%) and Spain’s IBEX 35 (-0.36%) lagged behind what was generally a decent performance across the rest of the continent, including a +0.68% advance for the STOXX 600 following five consecutive weekly declines. The US indices also put in a weak performance with the S&P 500 down -0.37%. The index was trading in a narrow range for most of the day before hitting both its intraday peak and trough within the last 45 minutes of trading, declining -1.11%. That time frame overlapped with President Biden and Chancellor Scholz’s joint press conference, (more below), but it doesn’t seem like there was any smoking gun that should have triggered that big of a selloff. Instead, it appears the S&P was keeping with the recent trend of heightened late day price action. Communication services (-2.24%) led the declines, with the mega-cap names within the sector performing the worst. Indeed, the FANG+ Index underperformed the S&P, declining -1.94%.

Overnight, Chinese stocks are slipping, with the Shanghai Composite (-0.90%) and CSI (-2.14%) both trading in the red. Additionally, the Hang Seng (-1.54%) is trading down, as Chinese tech stocks fall. Meanwhile, the Nikkei (+0.28%), Kospi (+0.45%) are both slightly higher. Looking forward, equity futures in the US are fairly flat as I type.

In terms of data, household spending in Japan fell -0.2% y/y, declining for the fifth straight month in December as consumer demand remained sluggish. It followed a -1.3% drop in the prior month. Separately, real cash earnings fell -2.2% y/y in December, posting its biggest decline since a -2.3% fall in May 2020 and against -0.8% analyst expectations. At the same line, nominal wages slipped -0.2% y/y in December marking their first fall in 10 months, after an upwardly revised +0.8% in November.

The attempts to find a diplomatic solution to the recent tensions along the Ukrainian-Russian border were elevated to the heads of state level yesterday. President Putin welcomed President Macron in Moscow for discussions, while Chancellor Scholz made his first White House visit as Chancellor to host a joint press conference with President Biden, where the situation in eastern Europe featured. There were the usual remarks that it was in the collective interest of all parties to find a diplomatic solution, and that all sides remained open to discussions, yet there was little the way in tangible progress. Chancellor Scholz did note that Germany would absolutely be united with the US on Russia sanctions, including offering support to President Biden’s assertion that the Nord Stream 2 pipeline project would be stopped were Russia to invade (European natural gas futures didn’t appear affected, declining -3.70% on the day). Meanwhile, President Putin noted he was preparing a response to the US and NATO on security guarantees.

In US Congressional news, the House Appropriations Committee Chair put forth a short-term bill that would keep the government funded through early March in attempt to prevent the government shutting down when the current continuing resolution expires at the end of next week. This would be the third such stopgap designed to give lawmakers time to negotiate program funding levels for this fiscal year.

In a bit of advertising for my team’s work, Galina and Luke have just published a presentation on the targets and penalties in sustainability-linked bonds. These bonds tie interest payments to hitting ESG goals and have been one of the fastest growing segments of the market. See the report here for more.

There wasn’t much data of note yesterday, though German industrial production unexpectedly fell -0.3% in December (vs. +0.5% expected), driven by a -7.3% decline in construction. That said, November’s reading was revised up to show a +0.3% expansion (vs. -0.2% contraction previously).

It’s a fairly quiet day ahead on the calendar now. Data releases include the US trade balance and Italian retail sales for December, and from central banks we’ll hear from the ECB’s Villeroy. Otherwise, Pfizer will be releasing earnings today.

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 23.05 PTS OR 0.67% //Hang Sang CLOSED DOWN 250.06 PTS OR 1.02% /The Nikkei closed UP 35.65 PTS OR 0.12% //Australia’s all ordinaires CLOSED UP 1.01% /Chinese yuan (ONSHORE) closed DOWN 6.3666 /Oil DOWN TO 89.73 dollars per barrel for WTI and DOWN TO 90.77 for Brent. Stocks in Europe OPENED ALL GREEN EXCEPT LONDON // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3666. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3674: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING WEAKER AGAINST USA DOLLAR

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

3B JAPAN

3c CHINA

CHINA//OLYMPICS

Covid breaks out in China’s southern border city of Baise, bordering VietNam. China has blocked the border

(zerohedge)

China Locks Down Border City Of 3.6 Million As COVID Flares Amid Winter Games

MONDAY, FEB 07, 2022 – 07:00 PM

As Beijing scrambles to wall off its 3,000-mile-long southern border with a new “Great Wall” of fencing, barbed wire and cameras/motion sensor tech – all iin the name of combating COVID – local authorities in one southern province have locked down a city situated along China’s border with Vietnam after discovering an outbreak there.

The latest lockdown in Baise, a city of nearly 4 million people, was ordered by authorities on Monday, Reuters reports. The decision comes as authorities have allowed COVID positive athletes to continue competing in the ongoing Winter Games (which have attracted abysmal viewership in the US).

Authorities in China’s southwestern city of Baise ordered residents to stay at home from Monday and avoid unnecessary travel as they enforced curbs that are among the toughest in the nation’s tool-box to fight rising local infections of COVID-19.

The outbreak in Baise, which has a population of about 3.6 million and borders Vietnam, is tiny by global standards, but the curbs, including a ban on non-essential trips in and out, follow a national guideline to quickly contain any flare-ups.

It’s worth noting that the size of the outbreak in Guangxi was surprisingly large, as typically authorities are only willing to admit to small numbers of locally spread cases. Authorities reported 99 domestically transmitted cases with confirmed symptoms between Saturday and noon on Monday, according to Pang Jun, deputy director of the regional health commission, who offered confirmation during a news briefing.

In that group of 99 cases, only 2 were said to be infected with omicron, according to the Chinese authorities.

Lockdown restrictions mirrored those of other earlier lockdowns: residents should stay indoors except for trips to buy essentials or test for COVID, and they should opt for delivery rather than in-store purchases whenever possible, state television said, citing a statement from the highest municipal authorities in Baise. Essential workers will be required to show special passes allowing them to travel between their homes and work.

The CCP authorities had locked down several Chinese cities – most notably Xi’an, the provincial capital of Shaanxi with a population of 13M – to try and prevent a potentially embarrassing outbreak ahead of the Winter Olympics.

While the total number of omicron cases reported in China isn’t clear, Reuters says cases of the variant have been confirmed in 10 of China’s provinces.

One local guide to tourists in Guangxi said he was worried that his income would suffer as authorities ordered him to cease taking new groups of travelers during the flare-up.

“My income is basically zero at this moment,” the guide, surnamed Luo, told Reuters, adding that he had already been affected in previous outbreaks in Guangxi and elsewhere.

In Baise, a hotel front desk agent who gave only his surname, Li, said, “Because of the outbreak, our hotel’s projected occupancy rate (this year) may not be as high as expected.”

The southern province of Guangdong and the municipalities of Beijing and Tianjin also reported small localized outbreaks on Sunday. In total, Chinese authorities reported 45 locally transmitted cases during the prior 24 hours, up from 13 cases reported during the prior day, according to data from China’s NHC

end

HONG KONG/COVID

Huge outbreak of Covid in Hong Kong. It is probably the Omicron but due to heavy vaccination, citizens immune systems have been compromised

(zerohedge)

MONDAY, FEB 07, 2022 – 10:40 PM

COVID outbreaks may be waning in the US, UK and a number of other countries – including far-flung Australia, where Prime Minister Scott Morrison just unveiled plans to reopen the country to tourists on Monday as that country’s omicron wave has diminished – but in Hong Kong, mainland China, and a handful of other countries in the Asia-Pacific region, case numbers are rising at an alarming rate, much to the consternation of local health officials.

On Monday, Hong Kong reported 614 new COVID cases, the largest daily tally since the start of the pandemic two years ago. The figure was double the number of cases reported the day prior, prompting local health officials to declare that the “fifth wave” of the pandemic has already begun, and that the city would soon be dealing with 1,000 new cases per day, according to Health minister Sophia Chan Siu-chee. 219 of the new cases were deemed asymptomatic or untraceable, and seven imported.

The prospect of exponential growth of the virus has prompted Hong Kong to impose even tougher quarantine restrictions, including sending both close contacts of the infected, and those who tested positive but exhibit mild symptoms, to a quarantine camp similar to the barbed-wire-enclosed camps opened in Australia where some infected people have been forced to sit out their illness (and a trio of persons made headlines around the world when they escaped late last year). The camp is already housing patients who are deemed symptomatic and at high risk of spreading the virus. Authorities will also consider adopting even tougher social distancing restrictions.

This facility is located at the Penny’s Bay facility on Lantau Island.

Officials have laid out plans to start sending more patients who meet the new criteria there on Tuesday, according to the SCMP. Although some infected patients will be allowed to quarantine at home if their digs are deemed “suitable” by the HK government (which, remember, is now under the untrammeled control of Beijing):

Warning that the Omicron-fueled fifth wave of the pandemic was spiraling out of control, officials laid out plans to begin sending infected people to Penny’s Bay from Tuesday and allow home quarantine for close contacts whose flats were approved as suitable for isolation.

The city’s leader will also meet her top advisers on Tuesday to discuss further tightening social-distancing measures to address the infection surge, partly blamed on Lunar New Year celebratory gatherings. Tougher steps could entail expanding the use of the vaccine pass to cover shopping malls and public transport.

Authorities blamed family gatherings during the Chinese Lunar New Year for fueling the surge in infections. There have been a few notable clusters of cases in the city so far, illustrated below:

As of Monday, COVID patients were occupying 1,146 of the 3,416 units available in the facility on Penny’s Bay. Meanwhile, more contacts of the infected will be required to quarantine at home for 14 days if their homes are deemed “suitable.”

With fewer spaces available, close contacts of patients and the family members of those secondary contacts can isolate at home starting from Tuesday, for 14 days and four days, respectively, provided their living arrangements proved suitable.

“Our colleagues will assess whether the household is suitable for home isolation, such as whether they need to share rooms or facilities with their family members,” said Centre for Health Protection controller Edwin Tsui Lok-kin.

Authorities in Hong Kong have imposed more draconian restrictions as of late, including locking down an entire housing complex after roughly 50 cases were found there. The city has also imposed a requirement for all Hong Kongers to be inoculated. If they aren’t fully vaccinated before Feb. 24, they will not be allowed to enter crowded public places, which will now require proof of inoculation to enter.

END

China/Canada

Trudeau administration turns a blind eye to a Canadian takeover of a lithium miner by huge Zijin Mining Group

(zerohedge)

“No National Security Risks”: Trudeau Admin Turns Blind Eye To Chinese Takeover Of Canadian Lithium Miner

MONDAY, FEB 07, 2022 – 11:00 PM

According to Justin Trudeau’s liberal administration, the Chinese takeover of a lithium mine located headquartered in Toronto “poses no national security risks whatsoever,” according to a report by True North.

The report comes after Neo Lithium Corp. was purchased by Zijin Mining Group Co. without a national security review. Neo Lithium spokesperson Carlos Vicens said last month that the government had only conducted a brief security screening of the potential purchase, stating: “The law states they have 45 days after announcement to start a review if they believe there is a specific concern. The timeline passed in early December and no review was done.”

Industry minister François-Philippe Champagne told True North: “This transaction was absolutely reviewed to make sure there was no security risk.”

Zijjin Mining acquired the company for $960 million. Neo Lithium “has developed one of the world’s largest overseas lithium brine projects in Argentina,” the report says.

In late January, some experts had warned against takeovers by the Chinese Communist Party, pointing out that they could have impacts on the country’s intellectual property and economic security.

Royal Roads University Professor Dr. Jeffrey B. Kucharski told MPs: “I think, as part of a bigger story, what I’m saying is that there are intellectual property issues, there is management knowledge and there is this company as part of a supply chain, potentially, that we now don’t have any longer to help build our own supply chain here in Canada.”

Senior Fellow of the Centre for International Governance Innovation Dr. Wesley Clark added: “I believe the government addressed the Neo Lithium acquisition using too narrow a framework; misjudged its significance to Canadian national and economic security, now and in the future; failed to translate policy promises into action; and was caught up in a protracted period of political transition while the transaction was being reviewed—all of which, I believe, led to a wrong decision.”

end

4/EUROPEAN AFFAIRS

EU/VACCINE/VACCINE MANDATE

END

GERMANY

GERMANY/USA

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

RUSSIA/USA/UKRAINE/BELARUS/ETC

| Russia’s Mediterranean port in Syria – Al-Monitor: The Pulse of the Middle East |

| Robert Hryniak <hryniak@me.com> | Mon, Feb 7, 2022 at 6:37 PM |