FEB 9

FEB9

· by harveyorgan · in Uncategorized · Leave a comment ·Edit

GOLD; UP $8.05 to $1835.20

SILVER: $23.33 UP 14 CENTS

ACCESS MARKET: GOLD: 1833.50..

SILVER: $23.30

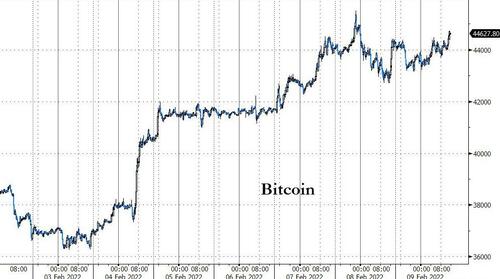

Bitcoin: morning price: 43,785 DOWN 468

Bitcoin: afternoon price: 44,785 UP 286

Platinum price: closing UP $7.55 to $1032.80

Palladium price; closing UP $39.05 at $2288.40

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filed COMEX//NOTICES:EXCHANGE: COMEX FILED:EXCHANGE: COMEX 7/13

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,826.600000000 USD

INTENT DATE: 02/08/2022 DELIVERY DATE: 02/10/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 3

624 H BOFA SECURITIES 6

661 C JP MORGAN 4

661 H JP MORGAN 3

685 C RJ OBRIEN 3

800 C MAREX SPEC 1

905 C ADM 6

TOTAL: 13 13

MONTH TO DATE: 16,819

NUMBER OF NOTICES FILED TODAY FOR FEB. CONTRACT: 13 NOTICE(S) FOR 1300 OZ (0.0404 TONNES)

total notices so far: 16,819 contracts for 1,681,900 oz (52.314 tonnes)

SILVER NOTICES:

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month 1249 : for 6,245,000 oz

GLD

WITH GOLD UP $8.05

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

NO CHANGES IN GOLD INVENTORY AT THE GLD/

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

CLOSING INVENTORY: 1015.96 TONNES/

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 14 CENTS:/:

NOCHANGE IN SILVER INVENTORY AT THE SLV/:

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY SLV/ TONIGHT: 544.573 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG 827 CONTRACTS TO 147,379 AND RESTS FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND DESPITE THIS STRONG LOSS IN OI, IT WAS ACCOMPANIED WITH OUR STRONG $0.15 GAIN ADVANCE IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.15) BUT WERE SUCCESSFUL IN KNOCKING OUT SOME SILVER LONGS AS WE HAD A SMALL LOSS OF 351 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.110 MILLION OZ FOLLOWED BY TODAY’S 15,000 OZ QUEUE JUMP//NEW STANDING 6.345 MILLION OZ. V) STRONG SIZED COMEX OI LOSS.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS -117

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB:

TOTAL CONTACTS for 7 days, total contracts: : 3870 contracts or 19.350 million oz OR 2.764 MILLION OZ PER DAY. (552 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 3870 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 19.350 MILLION OZ

.

LAST 10 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 17.555 MILLION OZ//

SPREADING OPERATIONS

(/NOW SWITCHING TO SILVER) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAR.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 827 DESPITE OUR STRONG $0.15 GAIN SILVER PRICING AT THE COMEX// TUESDAY THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 359 CONTRACTS( 359 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 4.1 MILLION OZ FOLLOWED BY TODAY’S 15,000 OZ QUEUE JUMP //NEW STANDING 6.345, MILLION OZ// .. WE HAD A FAIR SIZED LOSS OF351 OI CONTRACTS ON THE TWO EXCHANGES FOR 0.915 MILLION OZ//

WE HAD 0 NOTICES FILED TODAY FOR nil OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 3440 TO 512,842 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: — 231 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE FAIR SIZED INCREASE IN COMEX OI CAME DESPITE OUR STRONG GAIN IN PRICE OF $5.95//COMEX GOLD TRADING/TUESDAY/.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION AS THE TOTAL GAIN ON OUR TWO EXCHANGES TOTALED 4558 CONTRACTS…

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR FEB AT 64.3 TONNES FOLLOWED BY TODAY’S 1600 OZ E.F.P. JUMP TO LONDON //NEW STANDING: 58.454 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $5.95 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 4327 OI CONTRACTS (14.177 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 887 CONTRACTS:

FOR APRIL 887 ALL OTHER MONTHS ZERO//TOTAL:887

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 512,842.

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4327, WITH 3671 CONTRACTS INCREASED AT THE COMEX AND 887 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4558 CONTRACTS OR 14.177TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (887) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (3440,): TOTAL GAIN IN THE TWO EXCHANGES 4327 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 64.30 TONNES WHICH FOLLOWS TODAY’S EFP JUMP TO LONDON OF 1600 OZ//NEW STANDING 58.454 TONNES// 3) ZERO LONG LIQUIDATION ,4) FAIR SIZED COMEX OI. GAIN 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

8462 CONTRACTS OR 846,200 oz OR 26.32 TONNES 7TRADING DAY(S) AND THUS AVERAGING: 1208 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY(S) IN TONNES: 26.32 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 26.32/3550 x 100% TONNES 0.732% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 26.32 TONNES//INITIAL

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 827 CONTRACTS TO 147,379 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 359 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 359 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 359 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 827 CONTRACTS AND ADD TO THE 359 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED LOSS OF 468 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 2.340 MILLION OZ,

OCCURRED DESPITE OUR $0.15 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 27.32 PTS OR 0.70% //Hang Sang CLOSED UP 500.50 PTS OR 2.06% /The Nikkei closed UP 295.35 PTS OR 1.08% //Australia’s all ordinaires CLOSED UP 1.12% /Chinese yuan (ONSHORE) closed UP 6.3636 /Oil DOWN TO 89.04 dollars per barrel for WTI and DOWN TO 90.60 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3636. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3680: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFF SHORE WEAKER/

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 3440 CONTRACTS AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR GAIN OF $5.95 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (887 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF FEB.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 887 EFP CONTRACTS WERE ISSUED: ;: , & FEB. 0 APRIL: 887 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 887 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED 4327 TOTAL CONTRACTS IN THAT 887 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 3440 CONTRACTS..

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR FEB (58.454),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

FEB 2022: 58.454 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $5.95)AND THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A GAIN OF 14.177 TONNES OF TOTAL OI, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR FEB (58.454 TONNES)…

WE HAD –231 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 4327 CONTRACTS OR 432,700 OZ OR 13.455 TONNES

Estimated gold volume today: 63,940 /// atrocious

Confirmed volume yesterday: 159,155 contracts poor

INITIAL STANDINGS FOR FEB ’22 COMEX GOLD //FEB 9

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 30,585.858 oz Brinks |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 13 notice(s)1300 OZ 0.0404 TONNES |

| No of oz to be served (notices) | 1974 contracts 197,400 oz 6.1399 TONNES |

| Total monthly oz gold served (contracts) so far this month | 16,819 notices 1,681,900 OZ 52.314 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

No dealer deposit 0

No dealer withdrawal 0

0 customer deposit

total deposit: nil oz

1 customer withdrawal

i) out of Brinks: 30,585.858 oz

total withdrawals: 30,585.858 oz

ADJUSTMENTS: 0.

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of FEBRUARY we have an oi of 1987 stand for LOSING 294 contracts.

We had 278 contracts served upon yesterday, so we lost 16 contracts or an additional 1600 oz will not stand on this side of the pond and

these guys were E.F.P.’d to London where they received a handsome bonus for their effort. Looks like no gold to be found over here.

The month of March saw a loss of 304 contracts and thus the OI standing is 4445.

April saw a GAIN of 4223 contracts up to 397,663.

We had 13 notice(s) filed today for 1300 oz FOR THE FEB 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 13 contract(s) of which 4 notices were stopped (received) by j.P. Morgan dealer and 3 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB /2021. contract month,

we take the total number of notices filed so far for the month (16,819) x 100 oz , to which we add the difference between the open interest for the front month of (FEB: 1987 CONTRACTS ) minus the number of notices served upon today 13 x 100 oz per contract equals 1,878,300 OZ OR 58.454 TONNES the number of TONNES standing in this active month of FEB.

thus the INITIAL standings for gold for the FEB contract month:

No of notices filed so far (16,819) x 100 oz+ (1987) OI for the front month minus the number of notices served upon today (XX} x 100 oz} which equals 1,878,300 oz standing OR 58.454 TONNES in this active delivery month of FEB.

We lost 16 contracts or an additional 1600 oz will not stand over here and were EFP’d. to London

TOTAL COMEX GOLD STANDING: 58.454 TONNES (HUGE FOR A FEBRUARY DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

157,392.690, oz NOW PLEDGED /HSBC 4.89 TONNES

125,410.592 PLEDGED MANFRA 2.90 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690

288,481,604, oz JPM No 2 8.97 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonne

Loomis: 18,615.429 oz

total pledged gold: 1,553,863.297 oz 48.331 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 32,705,495.033 OZ (1017.27 TONNES)

TOTAL ELIGIBLE GOLD: 15,389,320.447 OZ (478.67 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,316,174.586 OZ (538.60 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,762,311.0 OZ (REG GOLD- PLEDGED GOLD) 490.27 tonnes

END

FEBRUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//FEB 9

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 235,041.120 oz CNT Int. Delaware |

| Deposits to the Dealer Inventory | 194,551.954 OZ Loomis |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 0-CONTRACT(S)nil OZ) |

| No of oz to be served (notices) | 20 contracts (100,000 oz) |

| Total monthly oz silver served (contracts) | 1249 contracts 6,245,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 1 deposits into the dealer

i) Into Loomis: 194,551.954 oz

total dealer deposits: 194,551.954 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 0 deposit into the customer account

total deposit: nil oz

JPMorgan has a total silver weight: 184.649 million oz/353.157 million =52.27% of comex

ii) Comex withdrawals: 2

a)Out of CNT 192,520.290 oz

b) Out of Int. Delaware: 42,520.830 oz

total withdrawal 235,041.120 oz

we had 2 adjustments customer to dealer

a)Brinks 1,563,065.352 oz

b) Malca 951,875.096 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 84.153 MILLION OZ

TOTAL REG + ELIG. 353,157 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR FEBRUARY

silver open interest data:

FRONT MONTH OF FEB//2022 OI: 20 CONTRACTS LOSING 8 contracts on the day. We had 11 contracts served upon yesterday.

So we gained 3 contracts or an additional 15,000 oz will stand for silver on this side of the pond.

FOR MARCH WE HAD A LOSS OF 9948 CONTRACTS DOWN TO 83,283 CONTRACTS.

APRIL HAD A SMALL GAIN OF 5 CONTRACTS UP TO 70

MAY HAD A GAIN OF 9125 CONTRACTS UP TO 47,001 contracts

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes: 26,226// est. volume today//awful plus!

Comex volume: confirmed YESTERDAY: 70,172 contracts (good)

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 1249 x 5,000 oz =. 6,245,000 oz

to which we add the difference between the open interest for the front month of FEB (20) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2021 contract month: 1249 (notices served so far) x 5000 oz + OI for front month of FEB (20) – number of notices served upon today (0) x 5000 oz of silver standing for the FEB contract month equates 6,345,000 oz. .

We gained 3 CONTRACTS OR 15,000 ADDITIONAL oz of silver will stand at the comex.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

GLD

FEB 9/WITH GOLD UP $8.05//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1015.96 TONNES

FEB 8/WITH GOLD UP $5.95 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1015.96 TONNES

FEB 7/WITH GOLD UP $14.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.24 TONNES FROM THE GLD/////INVENTORY RESTS AT 1011.60 TONNES//

FEB 4/WITH GOLD UP $3.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.84 TONNES

FEB 3/WITH GOLD DOWN $5.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 1016.59 TONNES

FEB 2/WITH GOLD UP $7.95//A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.78 TONES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1018.04 TONNES

FEB 1/WITH GOLD UP $5.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 31/WITH GOLD UP $10.10//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 28/WITH GOLD DOWN $8.30//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 27/WITH GOLD DOWN $36.15//ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES INTO THE GLD.//INVENTORY RESTS AT 1014.26 TONNES

JAN 26/WITH GOLD DOWN $21.60 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES INTO THE GLD///INVENTORY RESTS AT 1013.10 TONNES

JAN 25/WITH GOLD UP $10.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 24/WITH GOLD UP $10.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: AN UNBELIEVABLE DEPOSIT OF 27.59 TONNES INTO THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 21/WITH GOLD DOWN $10.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 980.86 TONNES

JAN 20/WITH GOLD UP $.20 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 980.86 TONNES

JAN 19/WITH GOLD UP $29.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 5.27 TONNES INTO THE GLD/INVENTORY RESTS AT 981.44 TONNES

JAN 18/WITH GOLD DOWN $3.25//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 14/ WITH GOLD DOWN $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 13/WITH GOLD DOWN $5.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 12/WITH GOLD UP $8.65//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 11/WITH GOLD UP $19.25/A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FROM THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 10/WITH GOLD UP $2.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.08 TONNES

JAN 7/WITH GOLD UP $8.15//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWLA OF 1.16 TONNES FROM THE GLD////INVENTORY RESTS AT 978.83 TONNES

JAN 6/WITH GOLD DOWN $35.30//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .32 TONNES/INVENTORY RESTS AT 979.99 TONNES

JAN 5/WITH GOLD UP $10.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 980.31 TONNES

CLOSING INVENTORY: 1015.96 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SLV

FEB 9/WITH SILVER UP 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 8/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.143 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 7/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.218 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 541.430 MILLION OZ/

FEB 4/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 539.212 MILION OZ

FEB 3/WITH SILVER DOWN 35 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT539.212 MILLION OZ//

FEB 2/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.411 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 539.212 MILLION OZ/

FEB 1/WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.801 MILLION OZ

JAN 31/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FORM THE SLV.//INVENTORY RESTS AT 533.801 MILLION OZ//

JAN 28/WITH SILVER DOWN 36 CENTS : NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 27/WITH SILVER DOWN $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 26/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 25/WITH SILVER UP 10 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.311 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 535.003 MILLION OZ/

.JAN 24/WITH SILVER DOWN 48 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.8 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 532.692 MILLION OZ//.

JAN 21/WITH SILVER DOWN 41 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 527.792 MILLION OZ

JAN 20/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.998 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 527.792 MILLION OZ

JAN 19/WITH SILVER UP 71 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.942 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 525.804 MILLION OZ

JAN 18/WITH SILVER UP 51 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS OF 1.11 MILLION OZ AND 1.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 527.246 MILLION OZ//

JAN 14/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 529.780 MILLION OZ//

JAN 13/WITH SILVER DOWN 2 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 832,000 OZ FROM THE SLV////INVENTORY RESTS AT 529.780 MILLION OZ

JAN 12/WITH SILVER UP 38 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//

JAN 11/WITH SILVER UP 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ/.

JAN 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 7/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 6/WITH SILVER DOWN 94 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL PF 226,000 OZ FROM THE SLV///INVENTORY RESTS AT 530.612 MILLION OZ?/

JAN 5/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 4/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 3/WITH SILVER DOWN 45 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.219 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 530.838 MILLION OZ//

CLOSING INVENTORY: 544.573 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARD

end

3. Chris Powell of GATA provides to us very important physical commentaries

Craig Hemke discusses gold prices and the rise of the USA interest rates. We must not be scared of rising interest rates with respect to gold prices

(Craig Hemke/GATA)

Craig Hemke at Sprott Money: On rates and gold

Submitted by admin on Tue, 2022-02-08 21:52Section: Daily Dispatches

9:54p ET Tuesday, February 8, 2022

Dear Friend of GATA and Gold:

Gold prices are not necessarily knocked down by rising interest rates, the TF Metals Report’s Craig Hemke writes today at Sprott Money. To the contrary, Hemke writes, gold has risen strongly along with Federal Reserve attempts to raise rates.

Hemke’s analysis is headlined “On Rates and Gold” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/On-Rates-and-Gold-Craig-Hemke-February-08-2022

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@ATA.org

END

For your interest…

Ed Steer: Deja vu all over again

Submitted by admin on Tue, 2022-02-08 23:16Section: Daily Dispatches

11:12p ET Tuesday, February 8, 2022

Dear Friend of GATA and Gold:

GATA board member Ed Steer’s weekend commentary in Ed Steer’s Gold and Silver Digest letter, headlined “Deja Vu All Over Again,” has been posted in the clear at GoldSeek’s compansion site, SilverSeek, here:

https://silverseek.com/article/deja-vu-all-over-again

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@ATA.org

END

4.OTHER GOLD/SILVER COMMENTARIES

This is big! Poland’s central bank buying 100 tonnes. Do not know where they are going to get it!

Poland bank buying 100Tonnes

Inbox

| Steve Organ | 12:07 PM (2 minutes ago) | ||

| to me |

END

Special thanks to Doug C for sending this to us:

Global Silver Demand Forecast To Reach A Record 1.112 Billion Ounces In 2022

- Posted on 02 09, 2022

Gains Will Be Broad-based, With Growth Expected From Most Key Demand Components

(Washington D.C. – February 9, 2022) The outlook for silver demand is exceptionally promising for 2022, with global silver demand forecast to rise to a record high of 1.112 billion ounces (Boz) in 2022. The increase will be driven by record silver industrial fabrication, which is forecast to improve by 5 percent, as silver’s use expands in both traditional and critical green technologies. Physical silver investment demand (consisting of silver bar and bullion coin purchases) is projected to jump 13 percent in 2022, achieving a 7-year high. Silver’s use in jewelry and silverware is also expected to strengthen in 2022 by 11 percent and 21 percent, respectively.

Macroeconomic and geopolitical conditions will generally support precious metals prices in the first half of this year. However, once the pace of U.S. policy rate hikes becomes more evident, the price outlook becomes more challenging.

The Silver Institute is pleased to provide the following insights on the major components of the 2022 silver market.

Silver Demand

In 2022 the silver market will build on the strong foundation set last year, when silver demand gained in all key sectors. Continuing the trend from 2021, this year’s upside will be broad-based, with gains expected from most key demand components. The global total for 2022 is forecast to achieve a new record high, increasing by 8 percent to 1.112 Boz.

Silver industrial offtake (accounting for more than half of total silver demand) is projected to strengthen further, establishing a new record high in 2022. Ongoing improvements in the global economy will give silver industrial applications an additional boost, mitigating near-term headwinds from supply chain bottlenecks and the challenges in certain regions from the ongoing COVID pandemic.

The outlook for silver’s use in the photovoltaic (PV) industry remains bright. Government commitments to carbon neutrality have resulted in a rapid expansion of green energy projects. As a result, even with ongoing efforts to reduce silver loadings, record PV installations are expected to lift silver demand in this segment to an all-time high in 2022.

Despite the prolonged worldwide chip shortage, the outlook for silver demand in automotive and 5G related applications remains robust this year. The former has been underpinned by increasing vehicle electrification, which leads to higher silver loadings per vehicle. Meanwhile, the latter has been assisted by the acceleration of building infrastructure to support 5G networks and strong demand from mobile devices. Moreover, as chip manufacturing bottlenecks are forecast to ease gradually in 2022, the rise in silver demand for these and other electrical and electronic applications is expected to expand.

Jewelry demand is forecast to strengthen by 11 percent this year. India remains the driving force, assisted by improving consumer sentiment. Even though the Omicron wave affected Indian demand in early 2022, an expected easing of COVID-19 restrictions and efforts by jewelry retailers to increasingly push silver to urban consumers will favor jewelry sales across India. In the U.S., following a significant rebound in 2021, jewelry sales expansion is expected to continue, albeit at a slower pace. Silverware fabrication is forecast to expand by 21 percent this year; again, India will account for the bulk of the increase for silverware in line with jewelry.

Silver Supply & Market Deficit

Total global silver supply is projected to rise by 7 percent to 1.092 Boz in 2022. The main contributor is silver mine production, which is forecast to grow 7 percent to a six-year high this year. This will be driven by higher output from primary silver mines, particularly from several large existing operations and supported by large new projects coming online.

The increase in silver recycling should be more modest in 2022, with volumes likely to advance by 3 percent, with the rise entirely due to higher industrial recycling. All other areas are expected to record lower volumes, as reduced distress selling weighs on jewelry and silverware scrap.

After shifting to a market deficit (total supply less total demand) in 2021 for the first time in six years, the silver market is expected to record a supply shortfall of 20 million ounces this year. However, the projected deficit is relatively modest in absolute terms.

Silver Physical Investment, Exchange-Traded Products & Price

Silver physical investment should enjoy double-digit gains in 2022 to hit a seven-year high. As the year advances, ongoing macroeconomic uncertainties, and elevated inflationary pressure, should encourage retail investors to seek physical silver for wealth preservation. Accordingly, profit-taking is likely to remain muted. Physical silver investment in India is also expected to strengthen on the back of improving economic conditions and positive price expectations.

Silver exchange-traded products (ETPs) saw a 6 percent rise to 1.132 Boz last year. So far this year, silver ETP holdings are little changed on year-end 2021 and remain close to record highs, a position which should be maintained for much of this year.

Early 2022 has seen GDP growth downgraded for several major economies, along with rising financial market volatility. This points to an increasing risk that the speed of the U.S. interest rate hiking cycle could turn out to be slower than current market expectations have allowed. As a result, silver prices should initially benefit from fresh investor interest in precious metals. Silver’s high beta should also see it outperform gold, with the gold:silver ratio projected to retreat below 70 by year’s end.

Overall, the 2022 annual average silver price (basis the LBMA silver price) is forecast to be $24.80, 1 percent lower than 2021’s average price of $25.14. Even so, it will still represent a historically high annual average.

# # #

The Silver Institute is the silver industry’s primary voice in expanding public awareness of silver’s essential role in today’s world. Its mandates are to provide the global market with reliable statistics and information on silver and create and execute programs that help drive silver demand. For more information on silver, including its use in the green economy, please visit www.silverinstitute.org.

Metals Focus, the respected global precious metals research consultancy based in London, contributed to this analysis. The firm will research and produce the Silver Institute’s annual report on the international silver market, World Silver Survey 2022, which will be released on April 20.

Disclaimer

-END-

5.OTHER COMMODITIES/

special thanks to G for sending this to us:

agricultural commodities breaking out

Inbox

| Gijs@regency-silver.com | 4:13 PM (14 minutes ago) | ||

| to Gijsbert, Michael, me, Tcosta@crescat.net, Bruce |

6.CRYPTOCURRENCIES

Steve Brown….

ttps://novusconfidential.wordpress.com/2022/02/09/wall-street-cartel-pumps-billions-into-crytpo/

Wall Street Cartel Pumps Billions into Crytpo

As we’ve examined before there are limited venues where liquidated $ US cash can go. See: Wall Street Cannot Crash Link: https://novusconfidential.wordpress.com/2021/12/09/wall-street-cannot-crash/ In just six days, the Money Trust cartel — as led by Fed lackeys Vanguard Group – BlackRock – StateStreet etc — have pumped billions into crypto.

Since the Wall Street taper tantrum in January See: Rulers of the Planet Pump the Bitcoin Ponzi Link: https://novusconfidential.wordpress.com/2022/01/23/a-taper-tantrum-will-it-last/ a fake system, inflated with fake “money” and run by criminals who should be languishing in prison instead of commanding the global monetary system, See: JP Morgan Five Felony Counts Link: https://gsiexchange.com/jpmorgan-chase-has-racked-up-5-criminal-felony-counts/ liquidated roughly $300Bn US from bitcoin alone, proving that the entire run-up in bitcoin from from $30K US per “coin” to about $70K was driven largely by what Max Keiser and RT claim to hate, namely Wall Street. Market propagandist Mike Saylor, the Microstrategy (MSTR) shill for Wall Street’s crypto con game, serves as the perfect example of such Wall Street rookery.

As written, Wall Street has never seen a scam it didn’t like. And the single fundamental to bitcoin is the nature of the scammery itself — especially since the financial crash of one dozen years ago. Crypto appeared after 2009 to fit that Wall Street need-to-thieve perfectly, because bitcoin is a true derivative of a phony fiat dollar US, where, ironically, the trust in the fiat $ constitutes the “trust” Wall Street has in this crypto game. Proof? The $124Bn run-up in bitcoin “market cap”* in just six days.

The approximately $124Bn increase in bitcoin cap in just six days is not due to apes, moms and pops, or even Raoul Pal, Saylor, and hat backwards Bukele whales pumping fiat billions into bitcoin. The Wall Street system is designed to house trillions and even quadrillions in fiat dollars and its derivatives, so that is where US debt dollars must stay, and the monetary cartel that Max Keiser claims to despise is pumping bitcoin.

Bitcoin is a necessary example of Fed-enforced sterilization of capital through its lackeys. We’ve seen the result when ginned-up dollars do get into the pockets of the Great Unwashed, and release pent-up demand; where Fed expansion of the “money” supply causes property prices and all prices to rocket higher. Bitcoin to an extent dampens demand for products and services, and locks up inflationary dollars, where hodlers and apes thus afflicted, religiously obey the mantra of crypto-messiahs like Max Keiser and Mike Saylor.

Interestingly, just now Wall Street and its bitcoin cohorts appear to have shrugged off inflation as a non-issue, and something commoners can live with. It’s an interesting proposition, and would be the first time ever in world history, where the major monetary powers believe that high inflation is long-term sustainable. Perhaps the scions of MMT Modern Monetary Theory link: https://www.investopedia.com/modern-monetary-theory-mmt-4588060 not only run government, Wall Street and the Fed… perhaps they now command the entire global monetary dollar cartel? That includes bitcoin and crypto. It appears that the monetary powers-that-be have chosen sterilization of dollars into bitcoin to be one key indicator.

In the end, Wall Street’s crypto movement is about control, See: Crypto is about Control link: https://www.bitchute.com/video/KliMNIAmAgHR/ as the monetary system has always been. Convincing the people this particular crypto form of control on offer is the right form, is of course the key.** When crypto is proven (btw there is evidence that a DARPA proxy assisted in the origination of bitcoin) the digital ID is next. As all apes and zombie lieutenants say, the future is now…

Seldom discussed is how the job market has been impacted by young people chasing a virtual future based on the crypto scam. In the past, young people might enlist in the military; perhaps choose college and a career; or work in industry. Since Wall Street has largely destroyed US manufacturing, and the get-rich-quick illusion is pushed by the monetary cartel now more than ever, NFT tokens and virtual reality have supplanted reality. Labor is thus tough to find, especially in North America. Where is the leading? If past performance is any indication of future, the crooks who infest Wall Street and the monetary cartel could care less.

NB: notes on crypto from experience:

Very slow to transact; crypto buy/sell fees are high; due to fee arbitrage amounts for transactions, buy/sell transaction amounts are inexact; if something goes wrong with an exchange or transaction you are hosed; major exchanges block donation addresses, example SouthFront; does not perform as a true or efficient currency.

*Surprisingly, the SEC does not consider bitcoin to be a security, perhaps due to its entirely speculative base.

** Another example here, digital ID:

end

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.3636

OFFSHORE YUAN: 6.3680

HANG SANG CLOSED UP 500,50 PTS OR 2.06%

2. Nikkei closed UP 295.35 PTS OR 1.08%

3. Europe stocks ALL GREEN

USA dollar INDEX UP TO 95.44/Euro RISES TO 1.1433-

3b Japan 10 YR bond yield: RISES TO. +.208/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 115.46/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 89.04 and Brent: 90.60–

3f Gold UP /JAPANESE Yen UP CHINESE YUAN: ON -SHORE CLOSED UP// OFF- SHORE DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.0.227%/Italian 10 Yr bond yield FALLS to 1.82% /SPAIN 10 YR BOND YIELD FALLS TO 1.10%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.59: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.44

3k Gold at $1828.05 silver at: 23.27 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble UP 25/100 in roubles/dollar AT 74.80

3m oil into the 89 dollar handle for WTI and 90 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 115.46 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9234– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0557 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 1.932 DOWN 3 BASIS PTS

USA 30 YR BOND YIELD: 2.228 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.60

Futures, Global Markets Jump As Bond Rout Eases

WEDNESDAY, FEB 09, 2022 – 08:01 AM

U.S. index futures jumped along with Asian and European markets, while the VIX declined for a fourth consecutive day, setting up Wall Street for a strong open as bond markets stabilized bringing some respite for markets whipsawed in recent weeks by concerns about tightening monetary policy. As of 730am ET, S&P emini futures rose 38 points or 0.84%, while Nasdaq futures were up 1.3% or 187 points, while Dow futures were up 0.60% or 215 points. The 10-year U.S. Treasury yield retreated from levels last seen in 2019, dropping from 1.97% at their high yesterday to 1.92%, and yields across Europe also fell after France’s central banker said markets may be getting ahead of themselves in pricing rate hikes for this year. A dollar gauge slipped and cryptos jumped.

Much of today’s rally is the result of Bank of France Governor Villeroy pushing back against market pricing yesterday, which suggests that there are indeed limits to just how far central banks are willing to be pushed by traders’ expectations. Still, despite today’s stabilization, the risk of market swings remains elevated ahead of U.S. inflation data on Thursday, with investors facing a likely “irreversible hawkish shift” by major central banks, according to Ipek Ozkardeskaya, an analyst at Swissquote. “The choppy trading is here to stay,” she said.

Investors are weighing up still-robust corporate earnings against worries about a rapid withdrawal of pandemic-era stimulus. Data this week is expected to show U.S. inflation continues to overheat, potentially stoking bets on a more aggressive Fed liftoff in March. About 76% of S&P 500 firms that have reported results beat earnings estimates, with profits coming in more than 6% above projected levels.

“We’re still in an environment where a lot is going quite well for the economy,” Lauren Goodwin, a multi-asset portfolio strategist at New York Life Investments, said on Bloomberg Television. “It’s still an all-cyclicals story from our perspective.”

Peloton shares rose 4.5% in premarket trading, extending this week’s bounce amid renewed speculation that the fitness company could become a takeover target, and following news that CEO John Foley will step down. Lyft dropped 4.4% as the number of reported active riders missed analyst expectations. Some other notable premarket movers:

- Alibaba (BABA US) could be active in U.S. trading after shares in Hong Kong jumped as SoftBank Group Corp. said it wasn’t involved in the Chinese tech giant’s filing of additional American depositary shares, allaying investor fears that the firm’s largest shareholder might be looking to cash out.

- Lyft (LYFT US) fell 4.7% after reporting mixed results on Tuesday, underlining Covid pressures on ridership and growth. Still, it reported revenue for the fourth quarter that beat the average estimate. Analysts focused on positive trends for 2022, and see light at the end of the omicron tunnel.

- Enphase Energy (ENPH US) gains as much as 19% in premarket trading after the solar company’s first-quarter revenue forecast beat the average analyst estimate.

- Chipotle Mexican Grill (CMG US) jumped in postmarket trading after it reported sales that topped estimates as smoked brisket, strong delivery orders and higher prices helped results in the fourth quarter.

- GlobalFoundries (GFS US) gained 4% postmarket after the semiconductor manufacturer’s first-quarter revenue and Ebitda forecast beat the average analyst estimate.

- New Relic (NEWR US) shares slumped 23% in extended trading on Tuesday, after the application software company reported its third-quarter results and gave an outlook where it widened its view for an adjusted full-year loss per share.

- Mandiant (MNDT US) rises 3.9% in premarket trading following an 18% surge on Tuesday after Bloomberg reported Microsoft is in talks to acquire the cybersecurity company. Mandiant also reported quarterly earnings after the close.

- Gevo (GEVO US) is within months of hitting a potential inflection point in its cash flow profile, Citi writes in note initiating on stock with a buy rating and $5 target. Stock climbs 7.6% premarket.

- Sundial Growers (SNDL US) shares climb 9.5% in extended trading after the Canadian cannabis producer said it has received a 180-day extension to regain compliance with Nasdaq’s minimum bid price requirement.

- NCR (NCR US) shares jumped 11% in postmarket trading on Tuesday, after the company said it has launched a board-led strategic review process to evaluate a full range of strategic alternatives available.

- Paycom Software (PAYC US) shares climbed 8% in extended trading on Tuesday, after the company reported fourth-quarter results that beat expectations and gave a full-year forecast that was ahead of the analyst consensus.

- XPO Logistics (XPO US) gained 3.4% in extended trading after the transportation services company forecast adjusted earnings per share for 2022 that beat the average analyst estimate.

- Adtalem Global Education (ATGE US) shares tumbled in extended trading after the company lowered its full-year forecasts for adjusted revenue and earnings per share.

In Europe, the Stoxx Europe 600 Index rose 1.5% as technology shares bounced back and carmakers surged. A raft of mostly positive earnings reports lifted sentiment. Adyen NV jumped more than 11% after the Dutch online-payments company reported second-half revenue growth that met analysts’ estimates. Amundi SA, Europe’s largest asset manager, climbed the most in a year after raking in more client cash than analysts’ expectations. Banks underperformed after disappointing results from ABN Amro Bank NV and Svenska Handelsbanken AB. Here are some of the biggest European movers today:

- Adyen shares jump as much as 12% after the payments firm reported second-half net revenue in line with estimates and volumes that beat expectations. While analysts said the results were mixed, they are “enough,” given a negative buy-side view into earnings, Jefferies says.

- Banco BPM gains as much as 6.7% after results from the Italian lender which Citi says highlight a “profound transformation.”

- Pandora shares rise as much as 8.2% after the Danish jewelry maker reported results and provided guidance for the year. The forecast seems realistic, according to Citi.

- Menzies shares gain as much as 42% to 475p after it rejected a preliminary and unsolicited 510p/share proposal from a unit of Agility Public Warehousing.

- Vontobel shares jump as much as 8% after FY earnings exceed estimates and as the Swiss bank raised its dividend. The driving force behind the beat was the digital investing division, ZKB says.

- GlaxoSmithKline shares fell as much as 1.4% after 4Q earnings. Jefferies says the company’s 2022 outlook was “as expected.” Citi says results and guidance “will do little to change investor sentiment.”

- Transport giant DSV A/S said operating profit doubled in the fourth quarter, helped by rising freight rates and its most recent acquisition.

- Equinor ASA, Europe’s second-largest supplier of natural gas, boosted its share buyback and increased the dividend after profiting from a surge in prices for the fuel.

Asian equities jumped the most since Jan. 12 to snap a two-day slide, boosted by Chinese tech shares including Alibaba Group Holding Ltd. The MSCI Asia Pacific Index advanced as much as 1.5% to a two-week high, helped by Japan and a rally in a Hong Kong technology index with consumer-discretionary shares also gaining. Alibaba was the biggest contributor to the Hang Seng Index, which jumped 2.1% to lead Asian benchmarks, after SoftBank Group Corp. said it wasn’t involved in the Chinese e-commerce firm’s filing of additional American depositary shares. China’s broader market also rose after state-backed funds’ intervention helped stage a strong recovery late in Tuesday’s session.

“Now it comes to the point where people will start to focus on economics and corporate earnings growth,” said Eva Lee, the head of Greater China equities at UBS Global Wealth Management Chief Investment Office. “Upward revisions of earnings will be a crucial signpost that we’ll be looking for.” Investors will focus on key U.S. inflation data on Thursday that could impact the outlook for future U.S. rates. Market participants will also keep an eye on central bank policy decisions this week, including those in India and Indonesia

Japanese equities rose, driven by gains in electronics and auto makers after the yen weakened. Service providers also boosted the Topix, which gained 0.9%. SoftBank was the largest contributor to a 0.9% rise in the Nikkei 225 after reporting results and confirming plans for an Arm IPO. The yen gained slightly after dropping 0.4% against the dollar overnight. “U.S. rate hike expectations have been priced in somewhat by now,” said Masahiro Ichikawa, chief market strategist at Sumitomo Mitsui DS Asset Management. “So there are going to be fewer situations where we see big selloffs triggered by rate-hike worries.”

Indian stocks gained for second straight session as automobile and banking companies rose on expectations that the monetary policy panel will keep benchmark interest rates unchanged to focus on growth. The S&P BSE Sensex climbed 1.1% to 58,465.97 in Mumbai, while the NSE Nifty 50 Index advanced by a similar measure. Eighteen of the 19 sector sub-indexes compiled by BSE Ltd. climbed, led by a gauge of automobile companies. The Reserve Bank of India’s monetary policy panel will conclude its three-day meeting on Thursday. All but one of the 39 economists surveyed by Bloomberg News expect the main repurchase rate to be held steady at 4%. Consumer prices in India rose for a third straight month in December. But the headline number is still within with the central bank’s 2%-6% target band, which allows policy makers the room to look away as some global peers lift rates to fight inflation. HDFC Bank contributed the most to the Sensex, increasing 2.5%. Carmaker Maruti Suzuki was the top gainer at 4.1%, its biggest surge since Jan. 25. Out of 30 shares in the Sensex index, 27 rose and 3 fell.

In rates, Treasury futures advanced paced by European bond rally after ECB policy makers pushed back on rate-hike expectations. Yields are richer by 2bp to 4bp across the curve led by intermediates, 10-year is down 3bps to 1.92%, flattening 2s10s by more than 1bp. Treasuries advance erodes outright concession for 10-year new-issue auction at 1pm ET. Fed speakers include Bowman and Mester. Auction cycle continues with $37b 10-year note, following strong demand for Tuesday’s 3-year sale, in which primary dealers were awarded record low share; cycle concludes Thursday with $23b 30-year new issue.

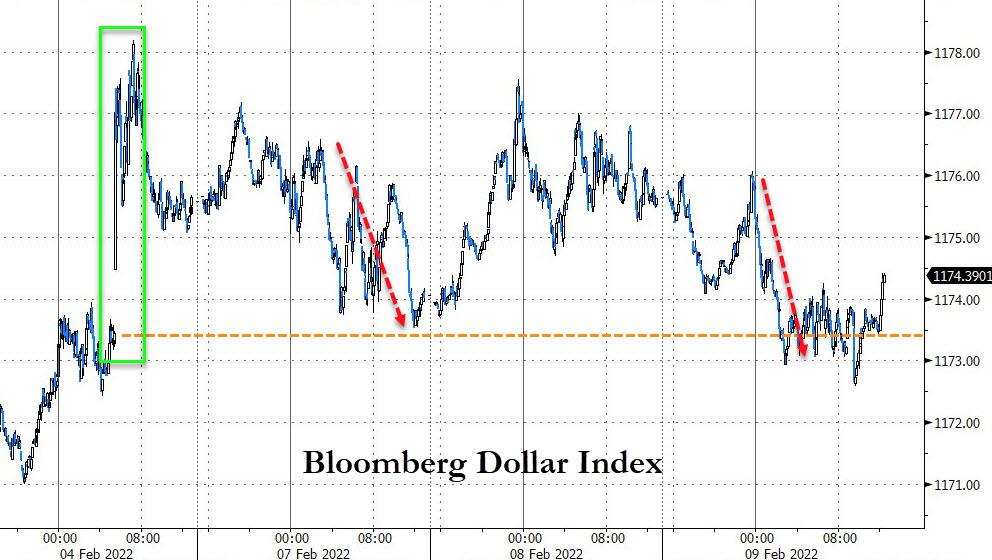

In FX, the Bloomberg Dollar Spot Index slipped as the greenback traded weaker against all of its Group-of-10 peers, with risk-sensitive currencies performing best. Benchmark Treasury yields fell up to 4bps, led by the long end as they halted a four-day rise. The euro bounced after a day low of $1.1403; yields across Europe fell after France’s central banker yesterday said markets may be getting ahead of themselves in pricing rate hikes for this year. Gilts rallied as traders pared their bets on Bank of England rate hikes, while the pound gained against a weaker dollar. Focus today will be on a speech from the BOE’s chief economist Huw Pill, with the market on the lookout for clues on the pace of tightening. Japan’s super-long bonds outperformed the benchmark 10-year note as the Bank of Japan refrained from stepping up bond purchases. The yen edged higher.

In commodities, oil held a drop as traders weighed tensions in Eastern Europe and the resumption of Iran nuclear talks. Aluminum traded near the highest level in more than 13 years. Bitcoin slipped below $44,000.

Looking at the day ahead data releases include the German trade balance and Italian industrial production for December. From central banks, we’ll hear from Bank of Canada Governor Macklem, BoE chief economist Pill, the ECB’s Schnabel and the Fed’s Bowman and Mester. Finally, today’s earnings releases include Disney, L’Oréal and Uber.

Market Snapshot

- S&P 500 futures up 0.7% to 4,543.50

- STOXX Europe 600 up 1.5% to 472.19

- MXAP up 1.4% to 190.27

- MXAPJ up 1.6% to 624.22

- Nikkei up 1.1% to 27,579.87

- Topix up 0.9% to 1,952.22

- Hang Seng Index up 2.1% to 24,829.99

- Shanghai Composite up 0.8% to 3,479.95

- Sensex up 1.1% to 58,445.55

- Australia S&P/ASX 200 up 1.1% to 7,268.33

- Kospi up 0.8% to 2,768.85

- German 10Y yield little changed at 0.21%

- Euro little changed at $1.1420

- Brent Futures down 0.5% to $90.37/bbl

- Gold spot up 0.1% to $1,827.06

- U.S. Dollar Index little changed at 95.56

Top Overnight News from Bloomberg

- After the inexorable surge of Treasury yields this year, investors are weighing how much of the damage from anticipating Federal Reserve rate hikes has already been done

- A relief rally spread across the world’s biggest government bond markets on Wednesday after yet another policy maker from the European Central Bank pushed back against traders betting on a rapid pace of interest-rate hikes this year

- One of the biggest players in global trade signaled disrupted supply chains rattling economies from Vietnam to Germany may be just months from returning to normal, easing concerns of a more protracted period of shipping chaos that has fanned consumer inflation, wreaked havoc on retail inventories and slowed factory production

- Bank of Japan Governor Haruhiko Kuroda faces a growing challenge to convince investors that a policy pivot isn’t on the horizon following a wave of hawkish turns by global central bankers

- China has renewed its campaign to keep commodities markets in check, as the government tries to prevent raw materials prices from overheating while it takes steps to stimulate a faltering economy

- Iceland’s central bank delivered its biggest interest- rate hike since the 2008 crisis, trying to quell inflation spurred by a rampant housing market. The Monetary Policy Committee in Reykjavik lifted the seven-day term deposit rate by 75 basis points to 2.75%, the highest level in almost two years

A more detailed look at global markets courtesy of Newsquawk

Asian stocks traded higher with earnings releases in focus and following the positive handover from Wall St where the major indices finished near the best levels of the day despite participants remaining in limbo ahead of US CPI. ASX 200 (+1.1%) was lifted by notable outperformance in the tech and financials sectors with the latter boosted by firm gains in Australia’s largest lender CBA which reported a 22% jump in H1 cash profit. Nikkei 225 (+1.1%) rose above 27,500 with biggest gaining stocks driven by earnings releases including IHI, AGC and Nissan, while Toyota reported a record 9-month profit and SoftBank was boosted after it began to pitch the ARM IPO. Hang Seng (+2.1%) and Shanghai Comp. (+0.8%) conformed to the constructive mood after reports yesterday that Chinese state funds stepped in to slow the market decline and with Hong Kong firmly boosted by a rebound in tech.

Top Asian News

- Hong Kong Virus Cases Top 1,000 as Outbreak Overwhelms Hospitals

- Top UAE Lender First Abu Dhabi Bank Offers to Buy EFG Hermes

- Philippines in No Rush to Tighten Monetary Policy: Diokno

- Hong Kong Reports 1,161 Covid Cases; Hospitals ‘Overwhelmed’

European bourses are firmer in a continuation of positive APAC/US trade, catalysts light thus far going into Thursday’s US CPI. Sectors are all in the green with Banking and Tech names lagging and outperforming respectively given the yield environment. US futures post broad-based gains in a continuation of yesterday’s action awaiting Central Bank speak.

Top European News

- Adyen Rises Most Since IPO as Volume Growth Beats Estimates

- Inflation-Stoking Supply Crunch Is Set to Ease in Second Half

- Glaxo Expects Profit to Rise as Drugmaker Prepares for Split

- Japan Ready to Divert Gas to Europe If Russian Supply Disrupted

In geopolitics:

- French Presidency said leaders of Germany, France and Poland expressed joint support for Ukrainian sovereignty and implementation of Minsk ceasefire agreement, according to Reuters.

- European and US regulators told banks to prepare for the threat of a Russian cyberattack, according to Reuters.

- Russian Deputy Foreign Minister calls reports of possible US THAAD missile systems being supplied to Ukraine as a provocation, via Reuters citing Ria.

- UK Foreign Minister Truss is set to fly to Moscow today to meet with Russian Foreign Minister Lavrov; PM Johnson will meet the Polish PM/President and NATO Secretary General on Thursday.

- Satellite images showed unusual activity at a North Korean shipyard, according to Yonhap citing a US think tank.

- Syrian air defences downed a number of missiles from Israeli aggression, while the Israeli military said a Syrian anti-aircraft missile fired towards Israel exploded in mid-air, according to Reuters.

- Iran has unveiled a missile with a range of 1450km, via Tasnim.

In Fixed Income, bonds regroup after Tuesday’s meltdown, but fade ahead of 10 year T-note supply and two Fed speakers. Spanish Bonos underpinned by strong demand and tight pricing for new 30 year benchmark. Bunds marginally outpace Gilts post-ECB’s Villeroy questioning the hawkish reaction to revised guidance and pre-BoE’s Pill.

In FX, the greenback ground down, but off recent lows ahead of Fed speakers on the eve of US CPI. High beta and cyclical currencies outperform on risk and relative rate or policy outlook dynamics. Yen underpinned by softer UST yields and protected by Fib resistance below decent option expiry interest. Euro retains grasp of 1.1400 handle irrespective of ECB’s Villeroy expressing the view that markets have reacted too hawkishly to policy pivot. Rouble remains optimistic about reaching a resolution to feud with Ukraine and the West Russian government and CBR have agreed on crypto regulation and Russia will recognise crypto assets as currencies, according to Kommersant

In commodities, WTI and Brent are choppy and relatively rangebound awaiting fresh developments amid incremental geopolitical updates.

White House Economic Adviser Bernstein told CNN that releasing more oil reserves from the SPR is an option. Japan, at the request of the US government, has decided to secure necessary LNG stocks and accommodate some of this for Europe, via NHK citing sources; subsequently confirmed. Russian Permanent Representative to the EU Chizhov says that Russian can raise nat gas supplies to Europe once a request is made to do so, according to Sputnik News Spot gold/silver are steady and continue to reside around familiar levels and technical marks. Turkey will announce a scheme this weekend to encourage households to convert gold into Lira according to Reuters. Copper initially benefitted from the upbeat risk sentiment but then faltered in late trade and with China eyeing iron ore price stability measures. China’s market regulator says will take further measures to ensure iron ore price stability, while it will strengthen market supervision and crackdown on price irregularities and hoarding.

US Event Calendar

- 7am: Feb. MBA Mortgage Applications -8.1%, prior 12.0%

- 10am: Dec. Wholesale Trade Sales MoM, est. 1.5%, prior 1.3%; Wholesale Inventories MoM, est. 2.1%, prior 2.1%

DB’s Jim Reid concludes the overnight wrap

Our latest monthly EMR survey aimed at market participants is now live. Given the major rates selloff so far this year there’s a heavy bias towards questions on that and its implications, such as where you think the Fed and ECB will take policy this year. We also ask whether you think the Russia/Ukraine situation will be worse, similar or fading from view in a couple of months? Given the recent vol this will hopefully be a good gauge of current sentiment, so all help filling it in is much appreciated. The link is here and it’ll close on Friday.

That global bond rout showed no sign of abating in yesterday’s session, with yields climbing to fresh highs as markets digested sovereign issuance on both sides of the Atlantic and investors continued to brace for tighter global monetary policy. For a sense of quite how unprecedented this current run is, yesterday marked the 11th consecutive session in which 10yr bund yields moved higher, which overtakes a run of 10 successive increases we saw around New Year 2000 and is something we haven’t seen in the data going all the way back to German reunification in 1990. That 11th straight gain saw them rise a further +3.9bps to a post-2019 high of 0.26%, just as 10yr French OATs (+5.7bps) also hit a post-2019 high of their own yesterday. As on Monday however, higher yields across the continent coincided with a further widening in peripheral spreads, with the gap between 10yr BTPs and bunds up another +2.7bps to 158bps, whilst the Spanish 10yr yield spread over bunds also widened +0.8bps to 86bps. In both cases that leaves them at their widest since July 2020, although Greek spreads were a notable exception after the massive +22.0bps widening on Monday, and actually came down -4.9bps yesterday to 218bps.

After the European close, we did begin to see some initial pushback against the market’s very hawkish interpretation to the ECB’s decision last week, with Bank of France Governor Villeroy saying that “I think there were perhaps reactions that were very high and too high in recent days.” That saw the Euro slip back slightly immediately after the remarks, though it swiftly recovered to only end the session down -0.24% against the US Dollar. This afternoon we’ll hear from Isabel Schnabel on the Executive Board who’s taking part in a Twitter Q&A, so it’ll be interesting to see if she echoes those comments.

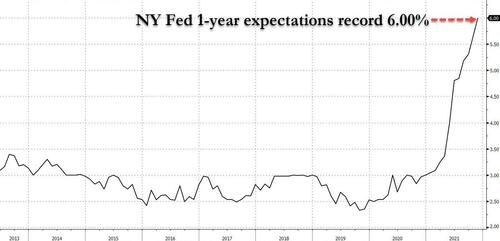

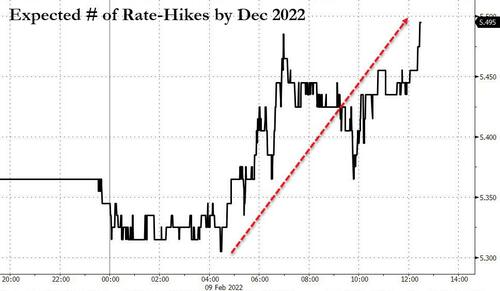

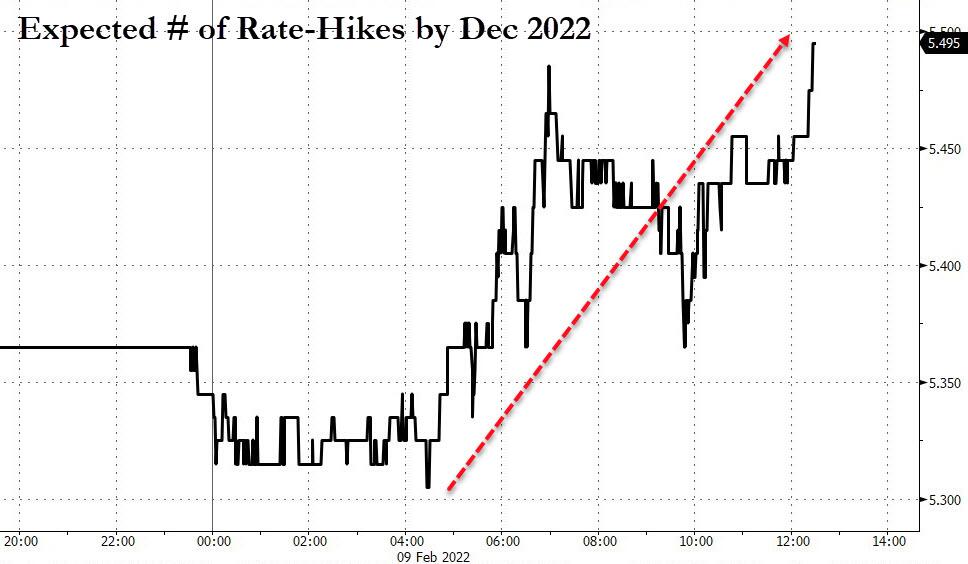

In the US, treasury yields followed the selloff in Europe, as the 10yr yield continues to get closer to breaching 2% for the first time since August 2019, coming within 3bps at its intraday peak of 1.97%, before ultimately closing up +4.7bps yesterday to 1.96%. Treasury yields have lagged the selloff in European sovereign yields since the hawkish showings from the ECB and BoE last week, though Treasuries made up ground following the strong employment and average hourly earnings data Friday morning, which has raised the stakes for tomorrow’s CPI as a potential catalyst for US rates. Fed funds futures are currently pricing approximately a 35% chance of a 50bp rate hike in March, and 5.45 rate hikes (assuming 25bp increments) for 2022 as a whole. For reference, our US economists see the year-on-year CPI increasing to +7.2%, which would be the highest going back to 1982.

The latest spike in yields didn’t prove as damaging to equities as some might have expected, with the S&P 500 (+0.84%) paring back early losses to move higher on the day, as part of a broad-based advance that left 381 companies in the green, and only three sectors lower on the day. The NASDAQ (+1.28%), FANG+ Index (+1.97%) of mega-cap stocks, and the small-cap Russell 2000 (+1.63%) all outperformed the S&P, with the Russell 2000 posting its third consecutive advance. For Europe there was a more muted performance and the STOXX 600 (+0.01%) eked out a marginal gain, but the prospect of ECB rate hikes has continued to be incredibly supportive for banks, and the STOXX Banks index (+2.24%) hit a post-2018 high, with its YTD performance now standing at +13.60%, the best performing STOXX 600 sector YTD.

One factor helping sentiment yesterday were more positive noises on the geopolitical front, with the latest meetings between various leaders raising hopes among investors that there could be some sort of de-escalation between Russia and the West over Ukraine. Obviously this can and has fluctuated day-to-day, but comments yesterday from President Macron that he “obtained that there will be no worsening and escalation” from his meeting with President Putin helped take some of the geopolitical risk premium out of various assets. Indeed by the close, Brent crude oil prices were down -2.06% to $90.78/bbl, which is their largest daily decline of 2022 so far, the MOEX Russia equity index surged +2.33%, and European natural gas futures were down -2.88% to a one week low.

Overnight in Asia, equity markets got off to a strong start following the positive performance on Wall Street. The Hang Seng Index (+1.98%) is leading the gains, with Alibaba shares up +7.28% in Hong Kong after SoftBank said they weren’t involved in the filing of further American depositary shares. Additionally, the Shanghai Composite (+0.40%), the CSI (+0.25%), the Nikkei (+1.09%), and the Kospi (+0.93%) are all trading in the green this morning. Going forward, equity futures are indicating a positive start in the US and Europe as well, with contracts on the S&P 500 (+0.44%), and DAX the (+0.66%) both advancing.

Otherwise, yields continued to rise in Japan with the 10-year JGB yield moving up to +0.215%, closer to the BOJ’s +0.25% ceiling, although those on 10yr US Treasuries are down -2.3bps this morning. Meanwhile, Iron ore futures in Singapore slumped from a 5-month high of $153 to $144 per ton after Chinese regulators cautioned information providers against fabricating prices to drive them up.

On the data front, the US monthly trade deficit came in at $80.7bn in December (vs. $83.0bn expected), which leaves the annual deficit at $859.1bn. That’s a second consecutive annual increase in the US trade deficit, having been at $676.7bn in 2020 and $576.3bn in 2019. Otherwise, the NFIB’s small business optimism index in January fell to an 11-month low of 97.1 (vs. 97.5 expected), but Italian retail sales unexpectedly rose +0.9% in December (vs. -0.3% expected).

To the day ahead now, and data releases include the German trade balance and Italian industrial production for December. From central banks, we’ll hear from Bank of Canada Governor Macklem, BoE chief economist Pill, the ECB’s Schnabel and the Fed’s Bowman and Mester. Finally, today’s earnings releases include Disney, L’Oréal and Uber.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 27.32 PTS OR 0.70% //Hang Sang CLOSED UP 500.50 PTS OR 2.06% /The Nikkei closed UP 295.35 PTS OR 1.08% //Australia’s all ordinaires CLOSED UP 1.12% /Chinese yuan (ONSHORE) closed UP 6.3636 /Oil DOWN TO 89.04 dollars per barrel for WTI and DOWN TO 90.60 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3636. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3680: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFF SHORE WEAKER//

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

3B JAPAN

3c CHINA

end

4/EUROPEAN AFFAIRS

EU/VACCINE/VACCINE MANDATE

AUSTRIA

Tyranny plus!!! This is how the Austrians are going to enforce their compulsory vaccine shots

(Watson/SummitNews)

Austrians Being Stopped Randomly By Authorities And Forced To Prove They Are Vaccinated

WEDNESDAY, FEB 09, 2022 – 05:00 AM

Authored by Steve Watson via Summit News,

After Austria became the first European country to mandate COVID vaccines for the ENTIRETY of its population, details have emerged on how the government plans to enforce the measure.

Reports note that citizens will be stopped randomly in the street and pulled over in their vehicles and forced to comply with vaccine status checks by the ‘authorities.’

If, heaven forbid, a person is found to be unvaccinated they will be fined on the spot, with the penalty increasing for each violation.

A first ‘offense’ will mean a €600 ($687) fine, with subsequent violations reaching up to €3,400 ($3,890).

The Austrian government will check citizens’ vaccination status against their vaccine registry. Anyone found to not have two vaccines plus a booster will be punished accordingly.

The development confirms previous reports that the Austrian government will hire people to “hunt down vaccine refusers.”

Indeed, this is merely an official confirmation of what has already been happening in the country. After the government placed the unvaccinated under an unprecedented lockdown, footage emerged showing police patrolling shops and highways checking people’s vaccination status.

Days after imposing the lockdown on the unvaccinated, Austria hit a new COVID case record.

In addition, the Austrian government has shortened the period in which vaccinations remain valid, meaning citizens are required to receive their next dose 90 days earlier than previously.

SchengenVisaInfo News reports that “‘From February 1, 2022, two-dose vaccinations are only valid for 180 days in Austria (exception: 210 days for under 18-year-olds). However, for ENTERING, the 270 days remain in place. The booster vaccination is valid for 270 days in both scenarios,’” the Austrian authorities explained.”

The government has put a sunset on the law, for January… of 2024, meaning Austrians face at least another two years of COVID tyranny.

As we have previously reported, an amendment to the law could also see those who refuse to pay the fines for being unvaccinated imprisoned.

The amendment also orders people who are jailed to pay for their own imprisonment.

“If detention is carried out by the courts, the associated costs shall be recovered by the courts from the obligated party in accordance with the provisions existing for the recovery of the costs of enforcing judicial penalties,” it states.

No one will be “forcibly brought” to a vaccination center to get jabbed against their will, although rest assured, they will be “forcibly” placed behind bars if they continue to refuse.

It remains to be seen whether other European countries will follow suit. Several countries have begin to scrap restrictions, including vaccine passports. However, the EU wants to keep the passes in place for another entire year.

END

EUROPE/

European electricity prices soar after France cuts its nuclear outpout

(zerohedge)

European Electricity Prices Soar After France Cuts Nuclear Output Forecast

WEDNESDAY, FEB 09, 2022 – 02:45 AM

When we first heard yesterday that Europe’s largest energy producer, French EDF (Electricite de France) had paradoxcially again cut its nuclear output target for a second time in a month – despite already ridiculously high energy costs in France and across the continent – we had a very quick reaction: this would make Putin very happy as Europe would become even more reliant on Russian gas.

EDF said nuclear output is expected to fall to 295 and 315 terawatt-hours in 2022, down from an earlier forecast of 300 and 330 terawatt-hours. The last time the company’s nuclear production fell below 300 terawatt-hours was more than three decades ago. Further cuts to next year’s output could come when EDF reports results later this month, Morgan Stanley said in a report.

“When the target is close to or under 300 terawatt-hours, it starts to raise concerns for next winter in terms of supply and demand,” said Emeric de Vigan, chief executive officer at French energy analysis firm COR-e.