FEB 10

FEB10

· by harveyorgan · in Uncategorized · Leave a comment ·Edit

GOLD; UP $1.00 to $1836.20

SILVER: $23.52 UP 19 CENTS

ACCEDD MARKET: GOLD $1826.85

SILVER: $23.20

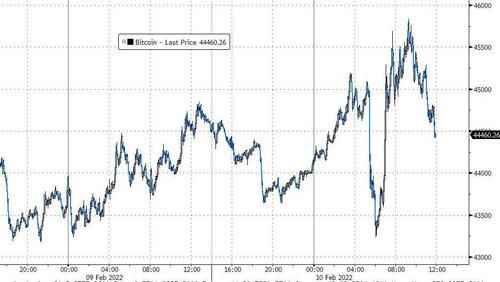

Bitcoin: morning price: 44,730 DOWN 55

Bitcoin: afternoon price: 43,527 DOWN 1258

Platinum price: closing UP $8.20 to $1041.00

Palladium price; closing DOWN $10.70 at $2288.40

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filedcomex notices//JPMorgan notices filed 255/614

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,835.200000000 USD

INTENT DATE: 02/09/2022 DELIVERY DATE: 02/11/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 100 29

332 H STANDARD CHARTE 28

363 H WELLS FARGO SEC 16

435 H SCOTIA CAPITAL 2

624 H BOFA SECURITIES 264

661 C JP MORGAN 141

661 H JP MORGAN 114

709 C BARCLAYS 506 5

732 C RBC CAP MARKETS 4

800 C MAREX SPEC 10

905 C ADM 8 1

TOTAL: 614 614

MONTH TO DATE: 17,433

COMEX//NOTICES:EXCHANGE: COMEX FILED:EXCHANGE: COMEX

NUMBER OF NOTICES FILED TODAY FOR FEB. CONTRACT: 614 NOTICE(S) FOR 61400 OZ (1.9097 TONNES)

total notices so far: 17,433 contracts for 1,743,300 oz (54.233 tonnes)

SILVER NOTICES:

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month 1249 : for 6,245,000 oz

GLD

WITH GOLD UP $1.00

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

NO CHANGES IN GOLD INVENTORY AT THE GLD/

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

CLOSING INVENTORY: 1015.96 TONNES/

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 19 CENTS:/:

NO CHANGE IN SILVER INVENTORY AT THE SLV/:

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY SLV/ TONIGHT: 544.573 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE 3144 CONTRACTS TO 150,523 AND RESTS CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND DESPITE THIS HUGE GAIN IN OI, IT WAS ACCOMPANIED WITH OUR SMALL $0.14 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.14) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A HUGE GAIN OF 3319 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A TINY ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.110 MILLION OZ FOLLOWED BY TODAY’S 190,000 OZ QUEUE JUMP//NEW STANDING 6.535 MILLION OZ. V) HUGE SIZED COMEX OI GAIN.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS -220

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB:

TOTAL CONTACTS for 8 days, total contracts: : 4045 contracts or 20.225 million oz OR 2.528 MILLION OZ PER DAY. (505 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 4045 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 20.225 MILLION OZ

.

LAST 10 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 20.225 MILLION OZ//

SPREADING OPERATIONS

(/NOW SWITCHING TO SILVER) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAR.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3144 DESPITE OUR SMALL $0.14 GAIN SILVER PRICING AT THE COMEX// WEDNESDAY THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 175 CONTRACTS( 175 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 4.1 MILLION OZ FOLLOWED BY TODAY’S 190,000 OZ QUEUE JUMP //NEW STANDING 6.535, MILLION OZ// .. WE HAD A VERY STRONG SIZED GAIN OF3319 OI CONTRACTS ON THE TWO EXCHANGES FOR 16.595 MILLION OZ//

WE HAD 0 NOTICES FILED TODAY FOR nil OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 7784 TO 520,699 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: — 73 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE STRONG SIZED INCREASE IN COMEX OI CAME WITH OUR STRONG GAIN IN PRICE OF $8.05//COMEX GOLD TRADING/WEDNESDAY/.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION AS THE TOTAL GAIN ON OUR TWO EXCHANGES TOTALED 12,314 CONTRACTS…

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR FEB AT 64.3 TONNES FOLLOWED BY TODAY’S 300 OZ QUEUE JUMP //NEW STANDING: 58.463 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $8.05 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 12,241 OI CONTRACTS (38.074 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4457 CONTRACTS:

FOR APRIL 4457 ALL OTHER MONTHS ZERO//TOTAL:4457

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 520,626.

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,241, WITH 7784 CONTRACTS INCREASED AT THE COMEX AND 4457 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 12,241 CONTRACTS OR 38.074TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4457) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (7784,): TOTAL GAIN IN THE TWO EXCHANGES 12,241 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 64.30 TONNES WHICH FOLLOWS TODAY’S QUEUE JUMP OF 300 OZ//NEW STANDING 58.463 TONNES// 3) ZERO LONG LIQUIDATION ,4) STRONG SIZED COMEX OI. GAIN 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

12919 CONTRACTS OR 1,291,900 oz OR 40.18 TONNES 8TRADING DAY(S) AND THUS AVERAGING: 1615 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES: 40.18 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 40.18/3550 x 100% TONNES 1.13% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 40.18 TONNES//INITIAL

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GIGANTIC SIZED 3144 CONTRACTS TO 150,523 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 175 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 175 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 175 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3364 CONTRACTS AND ADD TO THE 175 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 3319 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 16.595 MILLION OZ,

OCCURRED DESPITE OUR SMALL $0.14 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED UP 5.96 PTS OR 0.17% //Hang Sang CLOSED UP 94.36 PTS OR 0.38% /The Nikkei closed UP 116.21 PTS OR 0.42% //Australia’s all ordinaires CLOSED UP 0.30% /Chinese yuan (ONSHORE) closed UP 6.3676 /Oil UP TO 90.29 dollars per barrel for WTI and DOWN TO 92.10 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3676. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3608: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFF SHORE STRONGER/

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 7784 CONTRACTS AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR STRONG GAIN OF $8.05 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (4457 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF FEB.. THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4457 EFP CONTRACTS WERE ISSUED: ;: , & FEB. 0 APRIL: 4457 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4457 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED 12,241 TOTAL CONTRACTS IN THAT 4457 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI GAIN OF 7784 CONTRACTS..

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR FEB (58.463),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

FEB 2022: 58.463 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $8.05)AND THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A GAIN OF 38.301 TONNES OF TOTAL OI, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR FEB (58.463 TONNES)…

WE HAD –73 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 4327 CONTRACTS OR 432,700 OZ OR 13.455 TONNES

Estimated gold volume today: 225,470 /// fair

Confirmed volume yesterday: 147,663 contracts poor

INITIAL STANDINGS FOR FEB ’22 COMEX GOLD //FEB 10

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | NIL oz |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 614 notice(s) 61,400 OZ 1.9097 TONNES |

| No of oz to be served (notices) | 1363 contracts 136,300 oz 4.239 TONNES |

| Total monthly oz gold served (contracts) so far this month | 17,433 notices 1,743,300 OZ 54.233 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

No dealer deposit 0

No dealer withdrawal 0

0 customer deposit

total deposit: nil oz

0 customer withdrawal

total withdrawals: NIL oz

ADJUSTMENTS: 1//DEALER TO CUSTOMER/

OUT OF BRINKS 62,983.809 oz (1959 kilobars)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of FEBRUARY we have an oi of 1977 stand for LOSING 10 contracts.

We had 13 contracts served upon yesterday, so we GAINED 3 contracts or an additional 300 oz will stand on this side of the pond looking for gold metal.

The month of March saw a loss of 134 contracts and thus the OI standing is 4311.

April saw a GAIN of 7463 contracts up to 405,126.

We had 614 notice(s) filed today for 61,400 oz FOR THE FEB 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 614 contract(s) of which 127 notices were stopped (received) by j.P. Morgan dealer and 128 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB /2021. contract month,

we take the total number of notices filed so far for the month (17,433) x 100 oz , to which we add the difference between the open interest for the front month of (FEB: 1977 CONTRACTS ) minus the number of notices served upon today 614 x 100 oz per contract equals 1,879,600 OZ OR 58.463 TONNES the number of TONNES standing in this active month of FEB.

thus the INITIAL standings for gold for the FEB contract month:

No of notices filed so far (17,433) x 100 oz+ (1977) OI for the front month minus the number of notices served upon today (614} x 100 oz} which equals 1,878,300 oz standing OR 58.463 TONNES in this active delivery month of FEB.

We gained 3 contracts or an additional 300 oz will stand for gold over here

TOTAL COMEX GOLD STANDING: 58.463 TONNES (HUGE FOR A FEBRUARY DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

157,392.690, oz NOW PLEDGED /HSBC 4.89 TONNES

125,410.592 PLEDGED MANFRA 2.90 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690

288,481,604, oz JPM No 2 8.97 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonne

Loomis: 18,615.429 oz

total pledged gold: 1,553,863.297 oz 48.331 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 32,705,495.033 OZ (1017.27 TONNES)

TOTAL ELIGIBLE GOLD: 15,452,304.256 OZ (480.63 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,253,190.377 OZ (536.64 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,699,327.0 OZ (REG GOLD- PLEDGED GOLD) 488.31 tonnes

END

FEBRUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//FEB 10

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 402,353.088 oz HSBC CNT |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 0CONTRACT(S) NIL OZ) |

| No of oz to be served (notices) | 58 contracts (290,000 oz) |

| Total monthly oz silver served (contracts) | 1249 contracts 6,245,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 0 deposit into the customer account

total deposit: nil oz

JPMorgan has a total silver weight: 184.649 million oz/352.754 million =52.16% of comex

ii) Comex withdrawals: 2

a)Out of CNT 105,594.398 oz

b) Out of HSBC: 296,758.690 oz

total withdrawal 402,353.088 oz

we had 0 adjustments

the silver comex is in stress!

TOTAL REGISTERED SILVER: 84.153 MILLION OZ

TOTAL REG + ELIG. 32.754 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR FEBRUARY

silver open interest data:

FRONT MONTH OF FEB//2022 OI: 58 CONTRACTS gaining 38 contracts on the day. We had 0 contracts served upon yesterday.

So we gained 38 contracts or an additional 190,000 oz will stand for silver on this side of the pond.

FOR MARCH WE HAD A LOSS OF 7360 CONTRACTS DOWN TO 75,923 CONTRACTS.

APRIL HAD A SMALL GAIN OF 8 CONTRACTS UP TO 78

MAY HAD A GAIN OF 9630 CONTRACTS UP TO 56,631 contracts

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes: 94,730// est. volume today//strong

Comex volume: confirmed YESTERDAY: 75,956 contracts (good)

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 1249 x 5,000 oz =. 6,245,000 oz

to which we add the difference between the open interest for the front month of FEB (58) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2021 contract month: 1249 (notices served so far) x 5000 oz + OI for front month of FEB (58) – number of notices served upon today (0) x 5000 oz of silver standing for the FEB contract month equates 6,535,000 oz. .

We gained 38 CONTRACTS OR 190,000 ADDITIONAL oz of silver will stand at the comex.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

GLD

FEB 10/WITH GOLD UP $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1015.96 TONNES

FEB 9/WITH GOLD UP $8.05//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1015.96 TONNES

FEB 8/WITH GOLD UP $5.95 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1015.96 TONNES

FEB 7/WITH GOLD UP $14.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.24 TONNES FROM THE GLD/////INVENTORY RESTS AT 1011.60 TONNES//

FEB 4/WITH GOLD UP $3.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.84 TONNES

FEB 3/WITH GOLD DOWN $5.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 1016.59 TONNES

FEB 2/WITH GOLD UP $7.95//A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.78 TONES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1018.04 TONNES

FEB 1/WITH GOLD UP $5.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 31/WITH GOLD UP $10.10//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 28/WITH GOLD DOWN $8.30//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 27/WITH GOLD DOWN $36.15//ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES INTO THE GLD.//INVENTORY RESTS AT 1014.26 TONNES

JAN 26/WITH GOLD DOWN $21.60 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES INTO THE GLD///INVENTORY RESTS AT 1013.10 TONNES

JAN 25/WITH GOLD UP $10.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 24/WITH GOLD UP $10.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: AN UNBELIEVABLE DEPOSIT OF 27.59 TONNES INTO THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 21/WITH GOLD DOWN $10.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 980.86 TONNES

JAN 20/WITH GOLD UP $.20 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 980.86 TONNES

JAN 19/WITH GOLD UP $29.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 5.27 TONNES INTO THE GLD/INVENTORY RESTS AT 981.44 TONNES

JAN 18/WITH GOLD DOWN $3.25//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 14/ WITH GOLD DOWN $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 13/WITH GOLD DOWN $5.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 12/WITH GOLD UP $8.65//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 11/WITH GOLD UP $19.25/A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FROM THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 10/WITH GOLD UP $2.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.08 TONNES

JAN 7/WITH GOLD UP $8.15//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWLA OF 1.16 TONNES FROM THE GLD////INVENTORY RESTS AT 978.83 TONNES

JAN 6/WITH GOLD DOWN $35.30//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .32 TONNES/INVENTORY RESTS AT 979.99 TONNES

JAN 5/WITH GOLD UP $10.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 980.31 TONNES

CLOSING INVENTORY: 1015.96 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SLV/FEB 10/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 9/WITH SILVER UP 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 8/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.143 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 7/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.218 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 541.430 MILLION OZ/

FEB 4/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 539.212 MILION OZ

FEB 3/WITH SILVER DOWN 35 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT539.212 MILLION OZ//

FEB 2/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.411 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 539.212 MILLION OZ/

FEB 1/WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.801 MILLION OZ

JAN 31/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FORM THE SLV.//INVENTORY RESTS AT 533.801 MILLION OZ//

JAN 28/WITH SILVER DOWN 36 CENTS : NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 27/WITH SILVER DOWN $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 26/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 25/WITH SILVER UP 10 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.311 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 535.003 MILLION OZ/

.JAN 24/WITH SILVER DOWN 48 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.8 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 532.692 MILLION OZ//.

JAN 21/WITH SILVER DOWN 41 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 527.792 MILLION OZ

JAN 20/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.998 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 527.792 MILLION OZ

JAN 19/WITH SILVER UP 71 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.942 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 525.804 MILLION OZ

JAN 18/WITH SILVER UP 51 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS OF 1.11 MILLION OZ AND 1.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 527.246 MILLION OZ//

JAN 14/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 529.780 MILLION OZ//

JAN 13/WITH SILVER DOWN 2 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 832,000 OZ FROM THE SLV////INVENTORY RESTS AT 529.780 MILLION OZ

JAN 12/WITH SILVER UP 38 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//

JAN 11/WITH SILVER UP 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ/.

JAN 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 7/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 6/WITH SILVER DOWN 94 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL PF 226,000 OZ FROM THE SLV///INVENTORY RESTS AT 530.612 MILLION OZ?/

JAN 5/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 4/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 3/WITH SILVER DOWN 45 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.219 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 530.838 MILLION OZ//

CLOSING INVENTORY: 544.573 MILLION OZ

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: The Fed’s Important Admission

THURSDAY, FEB 10, 2022 – 02:01 PM

Atlanta Fed President Raphael Bostic made an important admission during a CNBC interview. He confessed the Fed wasn’t really going all-in on the inflation fight. That raises a question: how is it going to tame the inflation monster? Peter Schiff talked about this admission during his podcast, along with a head-scratching article about the trade deficit in the Wall Street Journal.

The US trade deficit shattered historical records in 2021. The Wall Street Journal claims this is a sign of a strong economy. Peter said that’s an absurd statement.

That’s like your kid brings home an F on his report card and you’re like, ‘Oh, that must stand for fabulous.’ It doesn’t. It is failure. A 27% explosion in a deficit is an abysmal failure of an economy.”

Imagine if the trade surplus was up 27%. Would the Wall Street Journal be reporting this as a sign of a weak economy? Of course not.

You can’t have it both ways. Either an increase in your trade surplus is good or an increase in your trade deficit is good. They can’t both be good. And clearly, a bigger surplus is a good thing.”

When you produce a surplus of goods and then sell them, you can take the earnings from those surpluses and invest them. That makes the country richer because you’ve earned assets in exchange for your exports.

That’s how creditor nations become richer because they invest their earnings from trade. On the other hand, when you are running a trade deficit, you are accumulating liabilities in order to pay for those deficits. So, debtor nations go deeper into debt as a result of running trade deficits. That’s why the US has gone from the world’s biggest creditor nation to the world’s biggest debtor because we used to run surpluses and now we run deficits.”

Peter called the WSJ article “all spin.”

They’re trying to take the facts and spin them around and make lemonade out of economic lemons.”

Speaking of trying to turn lemons into lemonade, Atlanta Fed President Raphael Bostic made an important admission during a recent interview. Journalist Steve Leisman noted that the Fed plans to raise interest rate about 1% this year. But he pointed out that the central bank would have done that anyway, even if there wasn’t inflation to fight. So, how is this rate hike going to work as “inflation-fighting,” and how has the Fed adjusted its policy in light of the fact that inflation is much higher than originally anticipated? The only thing the Fed is doing differently now that it’s admitted inflation isn’t transitory is speeding up the rate hike timeline. But the trajectory of liftoff is identical to what it might have been if inflation had remained under 2%.

Bostic actually admitted the Fed wasn’t really doing anything significant, but he said the hope was by communicating to the markets that the central bank intends to return to historically normal monetary policy would be enough to bring inflation down.

Well, why should it?

If we have this abnormally high inflation rate, how is a return to ‘normal’ monetary policy going to do anything about that inflation problem?”

The pretense for the Fed’s easy money stance in the Greenspan era has been the lack of inflation. The central bank has justified low rates by pointing to inflation below 2% and claiming that was too low.

When inflation is 7%, what is the justification for going back down to the same type of monetary policy that was supposedly appropriate when inflation was less than 2% and your goal was to make inflation higher?”

In the same interview, Bostic said the Fed would be moving to a “less accommodative stance.” Notice he did not say a “restrictive” stance. He said less accommodative, implying that the monetary policy will continue to be accommodative despite high inflation.

We’re not talking about tight money. We’re talking about less loose. And that’s exactly what Bostic confirmed. The Fed is going to go to a less accommodative policy than the accommodative policy it has right now. Well, how do you fight inflation with an accommodative policy?”

In this podcast, Peter also talked about the quiet rally in gold, bitcoin’s bear market rally, unemployment numbers and COVID and the labor market.

end

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARD

end

3. Chris Powell of GATA provides to us very important physical commentaries

Awful!

(Reuters/GATA)

Fed insists on concealing correspondence on members’ trading and ethics

Submitted by admin on Wed, 2022-02-09 10:41Section: Daily Dispatches

By Howard Schneider

Rueters

Wednesday, February 9, 2022

The U.S. Federal Reserve, responding to a Freedom of Information Act request by Reuters, said there are about 60 pages of correspondence between its ethics officials and policymakers regarding financial transactions conducted during the pandemic year 2020.

But it “denied in full” to release the documents, citing exemptions under the information act that it said applied in this case

The disclosure of trading by two regional reserve bank presidents during the pandemic led them to resign last fall, and prompted Fed chair Jerome Powell to overhaul Fed ethics rules and request the central bank’s inspector general to investigate. …

… For the remainder of the report:

Fed Refuses To Release 60 Pages Of Correspondence On Pandemic Trades Scandal

WEDNESDAY, FEB 09, 2022 – 10:30 PM

Having cost the jobs of three top Fed officials, including the Dallas and Boston Fed presidents as well as that of Vice Chair Clarida, one would think that matters relating to (potentially extremely lucrative) insider trading by members of the Federal Reserve should be fully in the public domain. One would be wrong.

In response to a Reuters Freedom of Information Act, the Fed said that there are about 60 pages of correspondence between its ethics officials and policymakers regarding financial transactions conducted during the pandemic year 2020 which have become an extremely sore spot for the Fed, with members of Congress demanding full transparency as to who knew and did what, when. The only problem: nobody is allowed to see them, as the Fed “denied in full” to release the documents, citing exemptions under the information act that it said applied in this case. Exemptions traditionally involve matters of national security, so how exactly alleged insider trading by a bunch of millionaires threatens “US Democracy” is something we would love to understand.

The disclosure of trading by two regional reserve bank presidents during the pandemic led them to resign last fall, and prompted Fed chair Jerome Powell to overhaul Fed ethics rules and request the central bank’s inspector general to investigate.

The FOIA responses to Reuters for the first time quantify how much back and forth may have occurred over policymakers’ personal trading in a year when markets first cratered, then rebounded on the basis of both massive federal fiscal stimulus and an aggressive rescue effort by the Fed.

Reuters reports that it had requested release under the information act of any 2020 communication “regarding the propriety of individual financial transactions” exchanged between the Fed’s general counsel or ethics staff and members of the Board of Governors, then Dallas Fed president Robert Kaplan, or then Boston Fed president Eric Rosengren.

Fed FOIA officer and deputy board secretary Margaret McCloskey Shanks responded to Reuters that staff had identified “approximately 47 pages of information” involving Fed board members and around 13 pages involving either Kaplan or Rosengren. However release of the documents was denied.

“The responsive documents contain predecisional and deliberative information, as well as information that is subject to attorney-client privilege,” she wrote. There was, she said, nothing in the documents that was “reasonably segregable” and not exempt from release under FOIA.

Gunita Singh, a staff attorney at the Reporters Committee for Freedom of the Press, said the FOIA exemption cited by the Fed is meant to “protect agency candor” so U.S. government staff and officials can discuss issues freely as decisions are being made.

The response from Shanks did not detail what current discussions or deliberations warranted withholding the information.

Demands for more disclosure from the Fed about the ethics scandal has been widespread, with public interest groups and elected officials including Elizabeth Warren calling on the central bank to release more details about policymakers’ stock trading and the guidance or opinions provided to them by ethics officials.

The inspectors general’s investigation of Fed trading during the pandemic is still underway. The Fed is also still finalizing the procedures and rules for the new ethics regulations adopted because of the controversy.

The Fed has released the substance of one email sent from its ethics office to policymakers at the height of the crisis. In late October, after a New York Times report, the Fed released a March 23, 2020, email from its ethics officer which noted that Fed rules were meant to avoid even the appearance that officials used their access to market moving information for personal profit.

Policymakers were advised to “consider observing a trading blackout and avoid making unnecessary securities transactions for at least the next several months,” or until Fed meetings and decisions moved back to normal from the emergency footing of that spring.

The advice was ignored by at least three Fed officials.

The ethics scandal blindsided the Fed last fall after reports in the Wall Street Journal and Bloomberg about Kaplan’s active trading in stocks during the pandemic and Rosengren’s investment in real estate securities.

That activity was noted in the annual financial disclosure reports that Fed policymakers are required to file. Both officials initially responded that their trades complied with Fed ethics rules, but said they planned to divest nevertheless. They eventually resigned.

END

Fat chance that this will happen!!

London’s Financial Times/GATA

Turkey to target ‘under the mattress’ gold in effort to bolster the lira

Submitted by admin on Wed, 2022-02-09 20:18Section: Daily Dispatches

By Laurel Pitel

Financial Times, London

Wednesday, February 9, 2022

Turkey will expand its drive to lure savers back to the lira next week with a scheme aimed at bringing billions of dollars worth of “under the mattress” gold into the banking system, the country’s finance minister told investors during a visit to London.

Nureddin Nebati, who this week made his first trip to the UK since being appointed at the end of last year, said that the government hoped that 10% of the estimated $250 billion worth of gold kept by Turks in their homes would be converted into lira under the initiative, according to two participants at the event.

Nebati said that 30,000 gold shops would play a central role in the scheme, which will build on a broader package of emergency measures unveiled in December in order to halt a freefall in the lira, which lost 44% of its value against the dollar in 2021.

The government had signed contracts with five gold refineries to convert jewellery handed over under the programme into gold bullion that would contribute to the country’s central bank reserves, he added.

The ministry of finance declined to comment on the plan but Turkey’s state-run Anadolu news agency cited Nebati as saying that new measures would soon be announced to put “under the mattress gold into the [financial] system.”

A traditional gift given for weddings and births, gold has long been a preferred way for Turks suspicious of the banking system — and their country’s history of inflation — to guard their wealth. But Turkish officials see it as part of a broader problem of “dollarisation,” or flocking to foreign currencies and precious metals, that has been a persistent source of pressure on the Turkish lira.

While the new deposit schemes have had some success, attracting about $23 billion in total, analysts are sceptical that they will provide a lasting solution to mistrust of the lira. Turkey has negative real interest rates of almost 35% once Turkey’s inflation rate of 48.7% in January is taken into account. …

end

Special thanks to Doug C for providing this for us:

The Royal Mint saw significant demand for gold and silver from international markets in Q4 of 2021, achieving record sales in America as investors flocked for Britannia bars and coins.

They British manufacturer, with a 1,100 year history of working with precious metals, observed a14.4% increase of sales from international markets (excluding the UK) compared to the same period the year before.

The Royal Mint has been growing its footprint internationally over the last two years, and the USA has seen the biggest growth in terms of gold – with sales of gold increasing by 96% in the final quarter of 2021 (versus Q4 2020). Silver has also seen a buying frenzy in markets such as mainland Europe where silver has increased 342% vs last year following Brexit and the continued pandemic uncertainty. In the UK it is the primary producer of gold and silver bars and coins, with gold sales experiencing an 84% increase YoY.

Nick Bowkett, Head of Bullion Sales at The Royal Mint, said: “We are famous in the UK for making coins and bars from precious metals, and over recent years we have focused on appealing to international markets too. The Royal Mint represents trust, security, and quality, which has seen investors in markets such as the US and Germany look to add our bullion products to their portfolio as a safe haven asset.

Globally precious metals continue to experience a buying frenzy with retail buying increasing to record levels in markets such as Europe and the US showing that the retail investor is concerned over the progress of the global economic recovery as the pandemic continues.

In the last quarter of 2021, we saw significant demand from international markets as investors looked to offset inflations risks by adding precious metals to their portfolio. Our increased global sales and marketing activity meant we were able to capitalise on this and saw sales increase by 92% between September and December year on year.”

As part of its commitment to sustainability, last year The Royal Mint signed an agreement with Canadian clean tech start up Excir to introduce a world first technology to the UK, to safely retrieve and recycle gold and other precious metals from electronic waste. Initial use of the technology at The Royal Mint has already produced gold with a purity of 999.9, and when fully scaled up, the process has potential to also recover palladium, silver and copper. The Royal Mint and Excir technology has the potential to ensure electronic waste is handled in a controlled and regulated manner – preserving natural resources for longer, helping to reduce the environmental impact of e-waste and fostering new skills and employment in the UK.

For more information visit: royalmint.com/invest

SPECIAL THANKS TO KEVIN W FOR PROVIDING THE FOLLOWING FOR US:

June 1978 and February 2022

Inbox

| Kevin Wallien | 9:34 PM (2 hours ago) | ||

| to me |

Who is afraid of higher nominal rates with high levels of inflation? The Fed is and not much they can do about it because the markets are wise to their errors and no longer afraid of their mass weapon of destruction. The $USD is a dud.

Very close to breaking out of range in similar scope and momentum to Q3 1978 in not just gold and silver but nominal interest rates. Higher nominal rates with high levels of inflation

Monthly Charts compare June 1978 with Feb. 2022 – using 36 period RSI (Purple Line) and 36 period SMA on RSI aka RSI momentum (Orange line); 9 period price SMA (blue line); 36 period price SMA (Red line)

Quarterly Charts compare Q2 (APRIL-JUNE) 1978 with Q1 2022 – using 36 period RSI; 9 period price SMA (blue line); 36 period price SMA

Real Interest Rates using 1 yr. Treasury Rate minus yearly percentage change in CPI (bear in mind 1978’s CPI was more accurate than today’s recalculated misnomer)

5.OTHER COMMODITIES/OIL TO GOLD

SPECIAL THANKS TO DOUG C FOR SENDING THIS TO US:

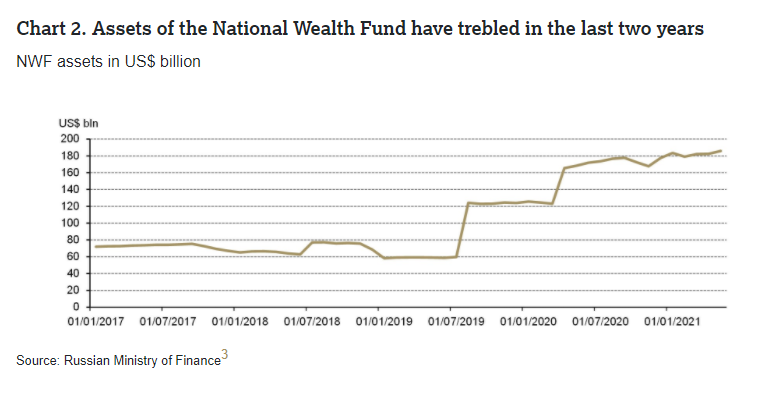

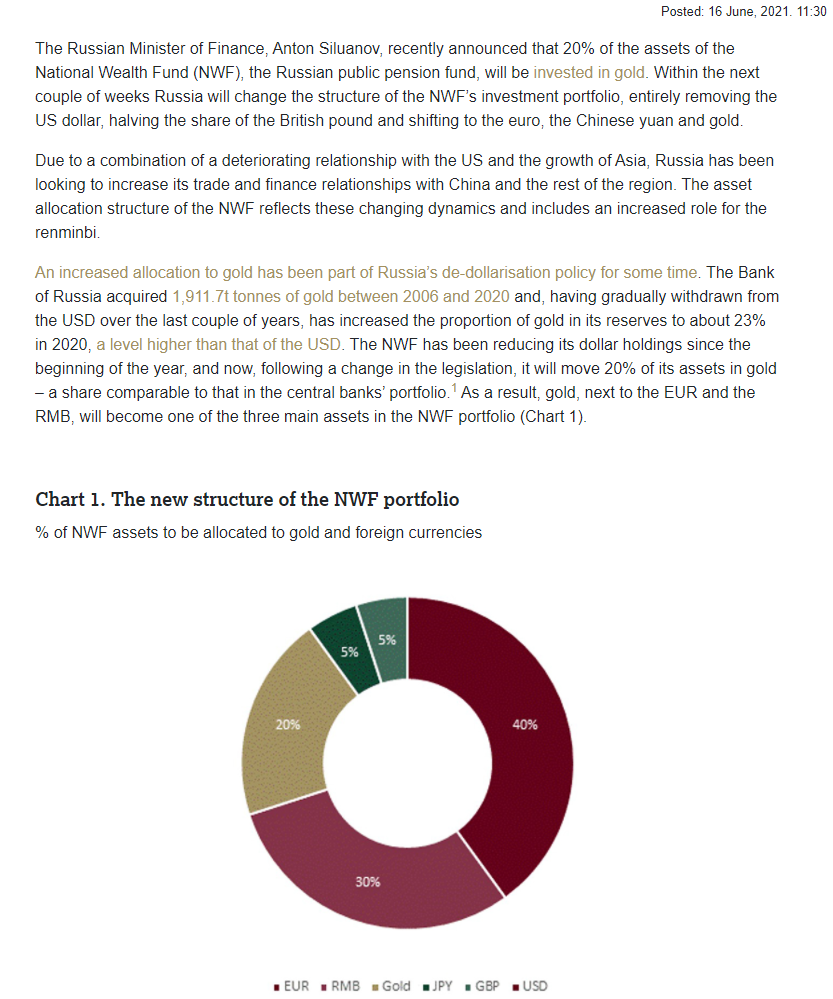

Russia Eyes $65-$73 Billion Plus Oil Windfall in 2022, 20% Allocated to Gold

February 10, 2022

Peter Spina

President, GoldSeek.com

- Russia’s “National Wellbeing Fund”

- Total assets: $197.8 Billion (Nov-2021) & GORWING!

- 2022: Russia projects $65 – $73Billion “Oil Windfall” ($90-$100 oil)

- By Law windfall goes into Fund: 20% Allocation to Gold

- $13-$14.6 Billion in Oil flows into Physical Gold!

More:

Bloomberg reports, “By law, the bulk of the windfall will go to the National Wellbeing Fund, most of which is held in gold and foreign currency by the central bank as part of its reserves.”

The Russian National Wealth Fund has seen its assets grow substantially over the prior couple of years. With the rising oil price, total assets should exceed $200 Billion by now.

The largest change to occur to the fund was the re-organization of its assets last June of 2021 when it was announced that the Russian National Wealth Fund would de-dollarize with a focus on the Euro, Yuan and Gold.

June 2021:

“The Russian Minister of Finance, Anton Siluanov, recently announced that 20% of the assets of the National Wealth Fund (NWF), the Russian public pension fund, will be invested in gold. Within the next couple of weeks Russia will change the structure of the NWF’s investment portfolio, entirely removing the US dollar, halving the share of the British pound and shifting to the euro, the Chinese yuan and gold.”

6.CRYPTOCURRENCIES

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.3676

OFFSHORE YUAN: 6.3608

HANG SANG CLOSED UP 94.38 PTS OR 0.38%

2. Nikkei closed UP 116.21 PTS OR 0.42%

3. Europe stocks ALL GREEN

USA dollar INDEX UP TO 95.53/Euro RISES TO 1.1435-

3b Japan 10 YR bond yield: RISES TO. +.230/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 115.78/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 90.29 and Brent: 92.10–

3f Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE CLOSED UP// OFF- SHORE UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.0.221%/Italian 10 Yr bond yield FALLS to 1.79% /SPAIN 10 YR BOND YIELD FALLS TO 1.09%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.57: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 2.50

3k Gold at $1831.60 silver at: 23.35 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble UP 25/100 in roubles/dollar AT 74.80

3m oil into the 90 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 115.78 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9242– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0569well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 1.933 UP 1 BASIS PTS

USA 30 YR BOND YIELD: 2.233 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.54

Futures Paralyzed Ahead Of Critical CPI Print

THURSDAY, FEB 10, 2022 – 07:52 AM

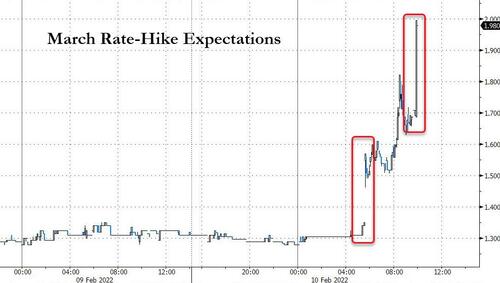

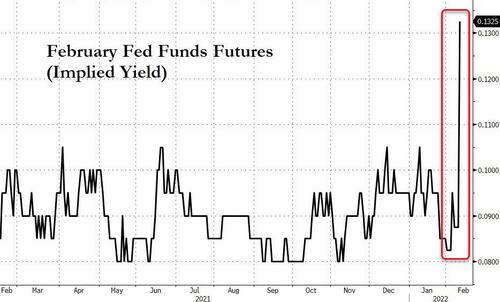

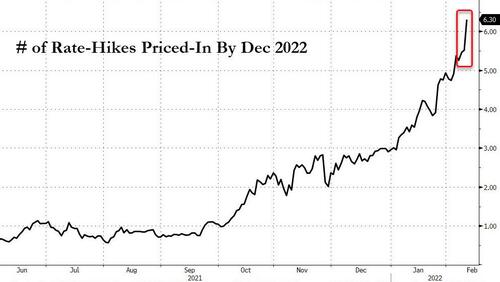

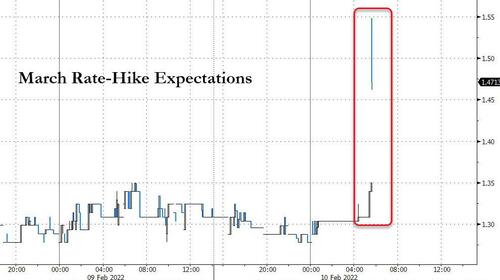

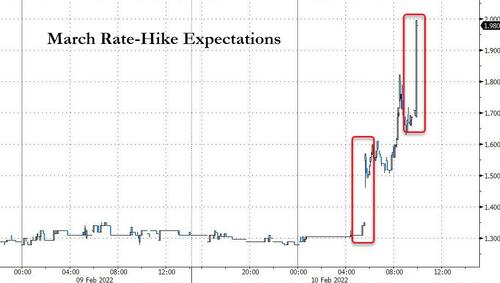

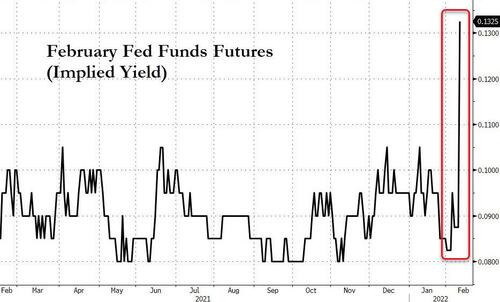

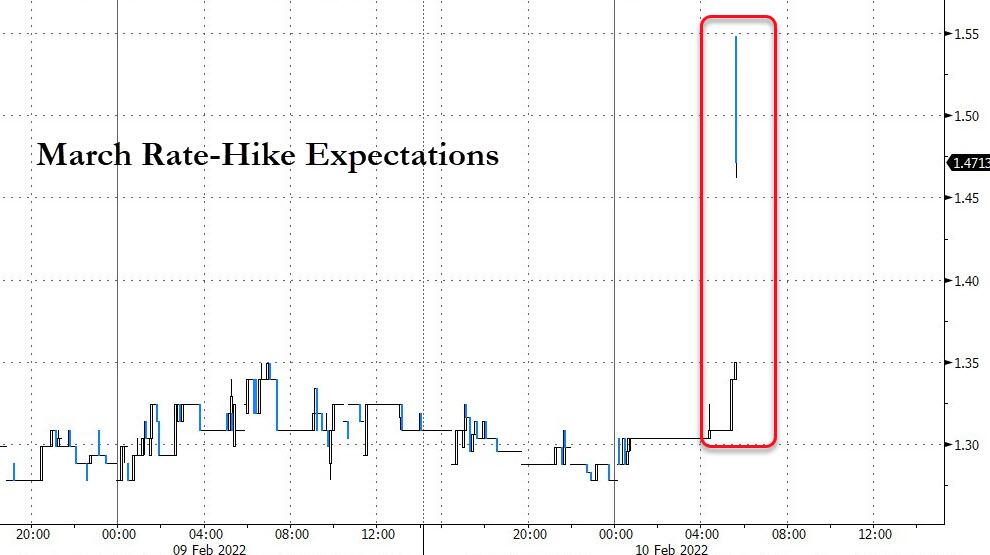

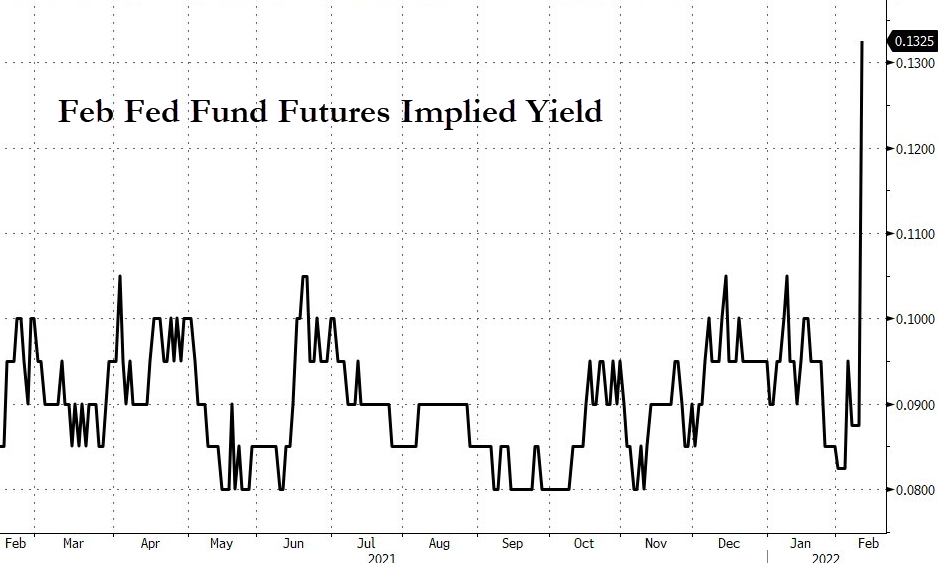

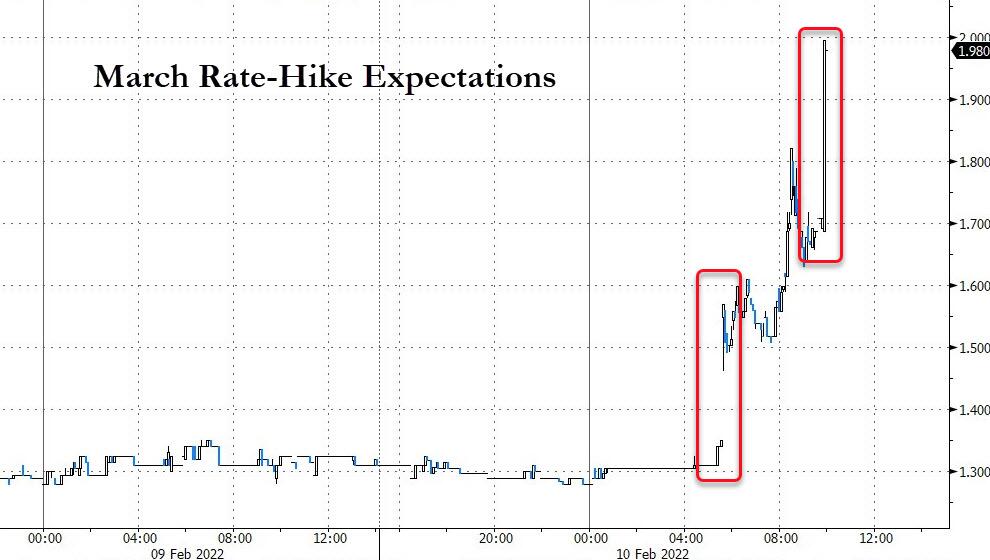

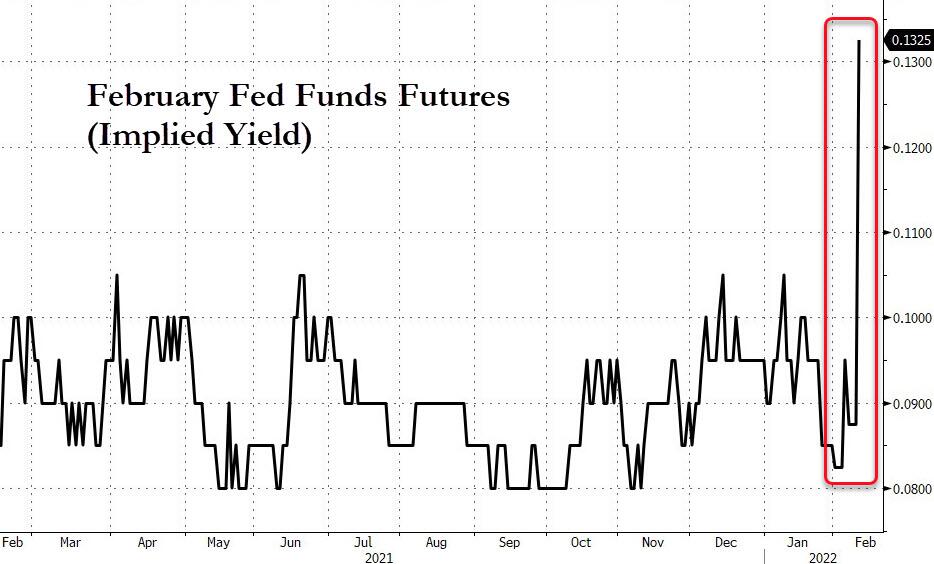

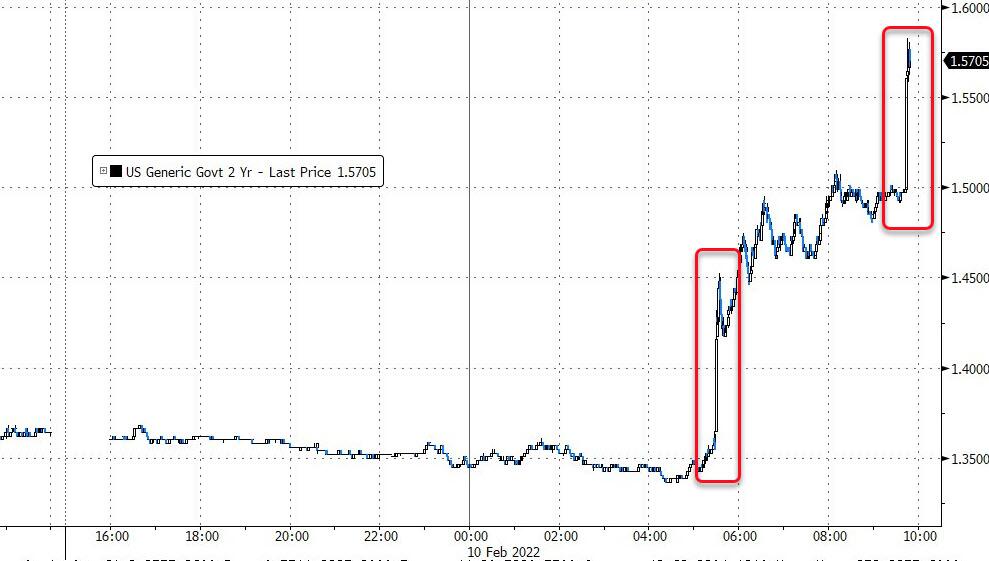

US index futures are unchanged from Wednesday’s close after some rangebound trades in another illiquid, overnight session, as traders were paralyzed and unwilling to commit capital ahead of today’s critical CPI print which consensus expects to come in at 7.2% YoY headline and 5.9% core, but which may well surprise to the downside (we explained why yesterday) after beating expectations on 8 of the past 10 occasions. A miss will likely send yields lower and risk sharply higher, especially when considering that the BLS will revise its CPI basket weightings and seasonal adjustments today. On the other hand, an upside surprise could spur additional pricing for a 50bp rate hike at the March meeting, currently priced in the swaps market at around 28%, and as such the 830am CPI print will shape views on how aggressively the Federal Reserve will tighten monetary policy in coming weeks.

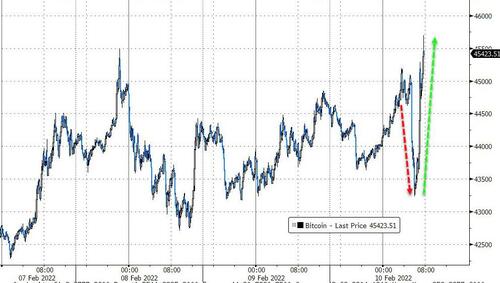

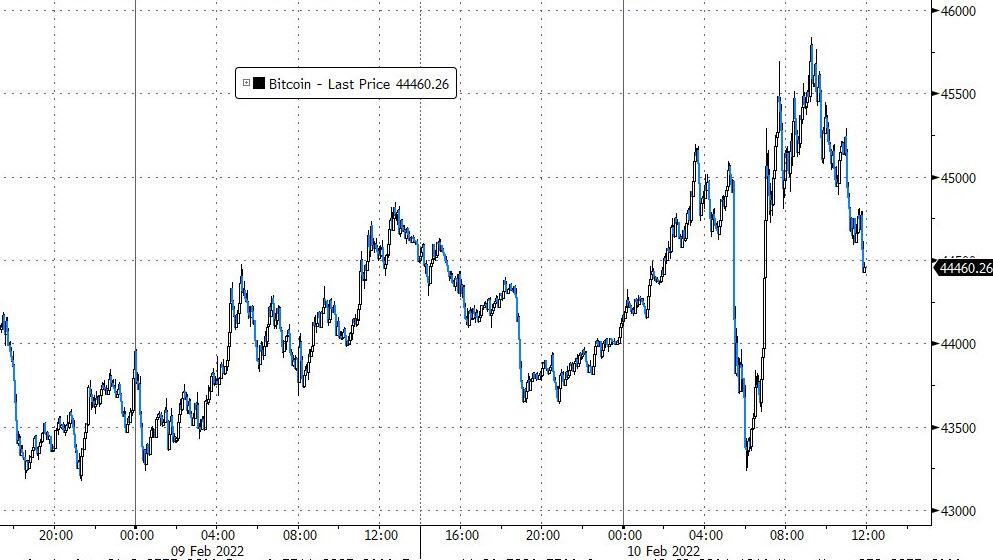

Contracts on the S&P 500 were flat, and the Nasdaq drifted lower after a broad Wall Street rally on Tuesday, US Treasury yields were lower as was the dollar while bond yields in most of Europe ticked higher, as did bitcoin which briefly rose above $45,000 .

“This inflation data will provide investors with more clues on how aggressive the Fed could be at its next policy meeting, sparking volatility in both bond and stock markets,” said Pierre Veyret, a technical analyst at ActivTrades.

Markets are pricing in more than five quarter-point Fed hikes in 2022. Some remain skeptical about such bets, such as Bokeh Capital Partners Chief Investment Officer Kim Forrest, who said on Bloomberg Television that she sees expects inflation to ease as government handout programs are removed.

Five to seven Fed hikes “is just so crazy — it’s a lot driven by bond people here who really just want to get that 10-year to the 3% rate and I don’t know that’s possible,” said Forrest, who expects maybe two Fed rate increases in 2022.

Walt Disney jumped in premarket trading after beating estimates, with positive surprises from streaming service subscriptions and theme parks. Twitter rose in premarket trading after announcing a $4 billion share buyback to offset earnings and projections that disappointed expectations. Coca-Cola and Pepsico also climbed on robust earnings. Here are some other notable premarket movers:

- Uber (UBER US) rises 5% in premarket trading after it reported fourth- quarter revenue that beat the average analyst estimate. Analysts say pandemic-linked headwinds may ease for the ride-hailing company.

- Mattel (MAT US) jumps 11% in premarket trading. The toy manufacturer reported an “impressive” beat in 4Q, according to Truist Securities.

- Twilio (TWLO US) shares jump 19% in U.S. premarket trading, after the infrastructure software company reported fourth-quarter results that beat expectations and forecast first-quarter revenue ahead of the analyst consensus. Analysts were particularly positive on the firm’s improved growth prospects.

- Shares of MGM Resorts (MGM US) rose 3% in post- market trading, after the entertainment company reported adjusted earnings per share for the fourth quarter above the average analyst estimate.

- Emcore (EMKR US) tumbles 16% in postmarket trading after the aerospace and communications supplier’s fiscal second-quarter revenue outlook missed the average analyst estimate.

- O’Reilly Automotive (ORLY US) shares rallied 9% in postmarket trading after the car-parts retailer’s 2022 profit forecast beat the average analyst estimate.

- Vimeo (VMEO US) slumped 21% in postmarket trading after the software company forecast full-year revenue growth below the average analyst estimate and said its chief financial officer is departing.

- Lumen Technologies (LUMN US) shares plunged over 11% in postmarket trading after the company’s 2022 adjusted Ebitda forecast missed the average analyst estimate.

- Impinj (PI US) forecast revenue for the first quarter that exceeded the average analyst estimate at the midpoint. The stock tumbled in postmarket trading after rallying more than 19% in the past four trading sessions.

While robust corporate earnings provided support for stocks this week, the U.S. inflation print is the center of attention on Thursday. Data are expected to show U.S. inflation exceeding 7%. A surprise reading either side could shift bets on the pace of Fed interest-rate hikes and inject more volatility into stocks and bonds.

“The market is being somewhat sanguine about what will happen in the second half of 2022,” Sonal Desai, chief investment officer at Franklin Templeton Fixed Income, wrote in a note. “There is an expectation that inflation will decline sharply. I think that might be optimistic because a lot of the factors driving inflation will still be with us. The Fed is already behind the curve.”

Fed Bank of Cleveland President Loretta Mester and her Atlanta counterpart Raphael Bostic said all options are on the table for the size of policy makers’ first interest-rate increase in March, but Mester doesn’t see a “compelling case” for a 50-basis-point hike. They indicated they prefer the Fed to start reducing its balance sheet soon.

In Europe, the Stoxx Europe 600 Index erased earlier gains to drop 0.1%, dragged by consumer goods and personal care sectors after a slew of earnings reports. Personal-care heavyweight Unilever Plc dropped after sounding the alarm on cost increases, and L’Oreal SA declined even after reporting record sales, with traders focusing on eroding margins; Delivery Hero slumped after providing a disappointing guidance. Travel, real estate and health care outperformed. Siemens and AstraZeneca were lifted by stronger-than-expected earnings. Here are some of the biggest European movers today:

- Siemens shares jump as much as 8% after the company reported first-quarter earnings that analysts said beat estimates “across the board.” The gain is the steepest since November 2020.

- Societe Generale shares climb as much as 4.2%, to the highest since Oct. 2018, after the lender reported 4Q results that Jefferies says are “very strong,” with net profit 40% above consensus.

- Huhtamaki shares rise the most since July 2020, after the Finnish maker of food packaging reported adjusted Ebit for the fourth quarter that beat the average analyst estimate.

- AstraZeneca rises on 4Q earnings which beat analyst expectations on core EPS and product sales. Handelsbanken calls the outlook a “relief although broadly in line.”

- H&M rises after Deutsche Bank upgraded the company to hold, saying the Swedish fashion retailer has an attractive valuation on about “5.5% dividend yield that is growing.”

- Delivery Hero shares lose a quarter of their value in a record one-day loss following a quarterly update, with analysts saying that the online food delivery firm’s Ebitda guidance for 2022 is disappointing.

- Credit Suisse shares fall as much as 5.1% after the lender rounded off a challenging 2021 with a fourth- quarter net loss of CHF2 billion, with analysts calling the quarter “messy.”

Earlier in the session, Asian equities rose for a second straight day ahead of key U.S. inflation data due later that may provide clues on the Federal Reserve’s tightening pace. The MSCI Asia Pacific Index advanced as much as 0.7%, helped by technology and material stocks. Shares in Japan, Hong Kong and Taiwan rose on Thursday while mainland China’s CSI 300 declined. Global stocks have had a broadly positive week as the 10-year U.S. Treasury yield’s slip from multi-year highs helped boost demand for growth stocks. Still, the prospect of hotter-than-expected U.S. inflation spurring a big Fed rate hike has kept investors on edge. “Inflationary pressure will probably stay for a while –the takeaways from the current earnings season mean it is not going away for the next quarter or so,” Christina Woon, investment manager at Abrdn Asian Equities, said in an interview on Bloomberg TV. “So investors need to watch out for margins.” The Reserve Bank of India stuck to its dovish tone to ensure an economic recovery in a surprise move, while Indonesia’s central bank kept borrowing costs unchanged to maximize support for the economy

Japanese equities rose, capping a third day of gains and a second-straight weekly advance amid an extended rebound from the rate-driven selloff. Electronics and chemical makers were the biggest boosts to the Topix, which rose 0.5%, rounding a weekly advance of 1.7%. Tokyo Electron and Advantest were the largest contributors to a 0.6% gain in the Nikkei 225. “People are waiting for U.S. CPI figures,” said Tetsuo Seshimo, a portfolio manager at Saison Asset Management Co. “But for Japan stocks, earnings will likely continue to provide support.”

Indian stocks rose as the Reserve Bank of India’s monetary policy panel kept the benchmark interest rate unchanged to extend its stance of focusing on growth despite mounting inflation. The S&P BSE Sensex gained 0.8% to 58,926.03 in Mumbai while the NSE Nifty 50 Index advanced by a similar measure. The key gauges extended their rally into a third day. All but one of the 19 sector sub-indexes compiled by BSE Ltd. climbed, led by a gauge of power companies. “It is quite reassuring for stocks that the RBI has continued with an accommodative stance and kept the inflation estimate at its current level,” said Abhay Agarwal, a fund manager at Piper Serica Advisors Pvt. He sees rate-sensitive shares to be the biggest beneficiaries of the central bank’s decision and commentary. RBI’s priority on growth is not unwarranted given that economic recovery is yet to gather momentum while private consumption lags pre-pandemic levels, according to Naveen Kulkarni, chief investment officer at Axis Securities. “We believe over the medium term, policy rates are likely to gradually harden, and markets will continue to gauge impact from global policy changes,” he said. Corporate earnings for the quarter through December have been mixed, with rising input costs eating into margins of manufacturing-linked companies. Automaker Mahindra and miner Hindalco Industries were the latest Nifty 50 companies to report profit that beat analysts estimates. Of the 43 Nifty 50 companies that have reported quarterly numbers thus far, 23 either met or exceeded analyst estimates, 18 missed and two can’t be compared. Hero MotoCorp will be reporting results later Thursday. HDFC Bank contributed the most to the Sensex’s gain, increasing 1.8%. Out of 30 shares in the Sensex index, 26 rose and 4 fell

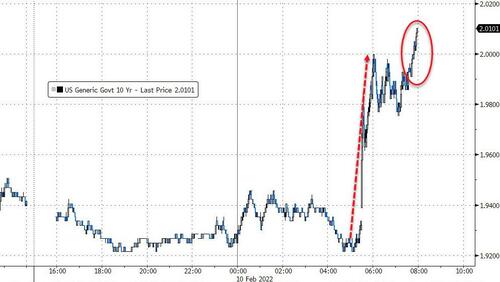

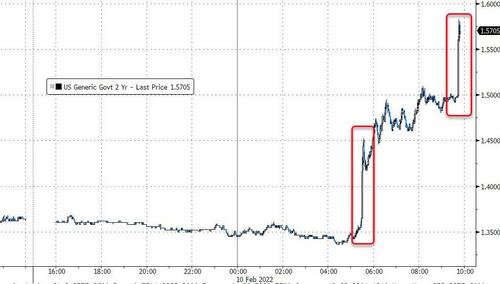

In rates, treasuries were richer across tenors led by front-end, with long-dated yields off session lows, steepening the curve ahead of January CPI report and 30-year bond auction. Yields were richer by more than 2bp across 2-year sector, steepening 2s10s by 1.7bp; the 10-year yield traded around 1.925%, outperforming bunds and gilts by 1.5bp and 0.5bp. Italian bonds lead euro-zone bonds lower as ECB rate hike wagers increase ahead of EU and U.S. inflation numbers. January CPI data is expected to show 7.2% y/y increase; an upside surprise could spur additional pricing for a 50bp rate hike at the March meeting, currently priced in the swaps market at around 28%. Treasury auction cycle concludes with $23b 30-year new issue at 1pm ET, week’s third and final sale; demand was strong for 3- and 10-year notes

Fixed income was broadly steady with the belly of the German curve underperforming U.K. and U.S. peers. Curve moves are modest, U.S. 2s10s ~1.5bps steeper ahead of today’s inflation print. Peripheral spreads have a small widening bias with 10y Italy ~2bps wider to Germany near 156bps. JGB futures snap higher, JPY goes small offered after a BOJ special purchase operation announcement.

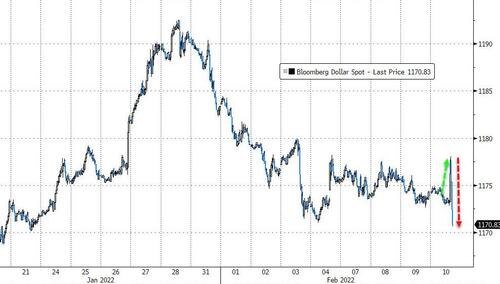

In FX, the Bloomberg Dollar Spot Index gave up a modest gain as the greenback slipped against risk-sensitive peers, led by the kiwi; short-end Treasury yields slipped. The euro edged up a second day to near $1.1450; yield curves bear-steepened in the region, and peripheral bonds underperformed the core. One-month implied volatility in the euro now captures the next ECB meeting and the relative premium suggests options are fairly priced. The pound led gains before a speech by BOE Governor Andrew Bailey. Sweden’s krona was the worst performer, dropping as much as 0.6%, after the Riksbank kept up its dovish monetary-policy stance as Governor Stefan Ingves blocked a push from officials for stimulus withdrawal; Swedish yields dropped by up to 7bps, led by the front end. The yen weakened while Japanese government bonds fell with the benchmark 10-year yield rising to a six-year high amid wariness over U.S. CPI data ahead of a Japanese holiday on Friday. The BOJ offered to buy an unlimited amount of bonds at a fixed rate, pushing back against traders that are testing its yield curve control policy.

In commodities, crude futures drift: WTI trades either side of $90, Brent near $91.50. Base metals trade well with most up over 1.5%, Spot gold trades a narrow range near $1,833/oz.

To the day ahead now, and the aforementioned US CPI release will be the main highlight. Other data releases include the US weekly initial jobless claims and the monthly budget statement for January. From central banks, we’ll hear from BoE Governor Bailey, ECB Vice President de Guindos, and the ECB’s Lane and Villeroy. Earnings releases include The Coca-Cola Company, PepsiCo, Philip Morris International and Twitter. Finally, the European Commission will be publishing their latest economic forecasts.

Market Snapshot

- S&P 500 futures down 0.2% to 4,569.50

- MXAP up 0.6% to 191.62

- MXAPJ up 0.7% to 630.21

- Nikkei up 0.4% to 27,696.08

- Topix up 0.5% to 1,962.61

- Hang Seng Index up 0.4% to 24,924.35

- Shanghai Composite up 0.2% to 3,485.91

- Sensex up 0.9% to 58,996.33

- Australia S&P/ASX 200 up 0.3% to 7,288.45

- Kospi up 0.1% to 2,771.93

- STOXX Europe 600 little changed at 473.35

- German 10Y yield little changed at 0.24%

- Euro up 0.1% to $1.1442

- Brent Futures up 0.6% to $92.07/bbl

- Gold spot down 0.1% to $1,831.24

- U.S. Dollar Index little changed at 95.48

Top Overnight News from Bloomberg

- The ECB will take a gradual approach to unwinding some of its ultra-expansionary monetary policy, Governing Council member Olli Rehn says in Helsinki seminar

- Euro-area inflation will ease below the ECB’s 2% target next year, according to new draft projections from the EU that will feed the growing debate about how quickly to raise interest rates

- Worries about Britain’s cost of living crisis and a shortage of workers pushed U.K. starting salaries up by their third-fastest pace on record in January, according to a survey that will add to growing concerns at the BOE about inflation and rampant wage gains

- The BOE’s quantitative easing program is on course to book a 3 billion-pound ($4.1 billion) loss in the coming weeks as the central bank’s massive bond holdings start their journey from government cash cow to a drain on the public finances

- EU and U.K. attempts to jump-start negotiations over the post-Brexit trading relationship in Northern Ireland have so far failed to make any progress, and diplomats see little chance for any substantial progress until they get past a key election scheduled for May

- Bank of Japan chief Haruhiko Kuroda says that it’s impossible for the central bank to make a hawkish turn before his term ends next year, Mainichi newspaper reported, citing an interview with the governor

- Some of this year’s worst-performing emerging markets will get another chance to lure back bond investors after their first round of aggressive rate hikes failed to contain inflation. At least seven countries including Russia, Mexico and India are set to follow Poland and Romania, which raised benchmark rates this week

A more detailed look at global markets courtesy of Newsquawk

Asian stocks traded mixed as participants digested another deluge of earnings and US-China frictions. ASX 200 (+0.3%) was supported by tech and with financials boosted after AMP and NAB reported higher H1 profits. Nikkei 225 (+0.5%) finished off highs with the index swayed by a choppy currency and numerous earnings. Hang Seng (-0.2%) and Shanghai Comp. (-0.3%) were subdued after Hong Kong reported its first COVID death in five months, while Biden administration is said to mull trade actions on China. Nifty 50 (+0.7%) was initially choppy heading into the RBI decision but was then lifted after the central bank kept the Repurchase Rate at 4.00% and unexpectedly maintained the Reverse Repo Rate at 3.35%.

Top Asian News

- BOJ Seeks to Rein in Yields With Unlimited Fixed-Rate Purchases

- BOJ to Conduct Unlimited Fixed-Rate JGB Purchases at 0.25%

- Credit Suisse Hires 80 Wealth Bankers for Asia Growth

- India’s Central Bank Chief Says Crypto Is ‘Not Even a Tulip’

European bourses are mixed/positive having pulled back modestly from a firmer cash open, individual movers heavily dictated by pre-market earnings. Sectors are mixed with Basic Resources outperforming while Consumer Products/Services are pressured on earnings dynamics.

Top European News

- Italy Is Set to Approve Start of Process to Sell Airline ITA

- U.K. Salaries Jump as Workers Grapple With Cost-of-Living Crisis

- Delivery Hero Slumps Most on Record as Outlook Disappoints

- Turkey Kicks Off Latest Round of Capital Injections in Banks

Central Banks:

- BoJ to purchase unlimited 10yr JGBs on Feb 14th at 0.25% (#363, #364 and #365); decided on fixed rate operation given recent yield moves. Will firmly keep policy to keep 10yr yields around 0%.

- Riksbank maintains its Repo Rate at 0.00% as expected. QE maintained for Q2 (SEK 37bln for Q1 2022); three hawkish dissenters on QE. Q1 2024 rate path lifted marginally; even if the risk of too low inflation has declined, it still remains. Governor Ingves says a rate hike is inching closer than we earlier believed.

- RBI kept the Repurchase Rate unchanged at 4.00% and maintained accommodative policy stance, as expected, but also surprisingly held the Reverse Repo Rate at 3.35% (exp. 20bps increase). RBI Governor Das said the MPC flagged potential downside risks to activity from Omicron and they are seeing some loss of momentum for economic activity, while the MPC was of the view that continued policy support is

- warranted for a durable and broad-based recovery.

- ECB’s Rehn says it is more preferable to progress one step at a time in normalising monetary policy in an uncertain environment; will use all tools to stabilise inflation around 2%.

In FX, DXY somewhat deflated into US CPI even though expectations are lofty, as Fed’s Mester sees no compelling case for 50bp March liftoff. Riksbank rattles SEK with only minor rate path tweak and no real tilt from transitory inflation view. BoJ undermines YEN by announcing unlimited JGB purchases to prevent 10 year yield spiking further from target. ZAR continues shine alongside Gold in the run up to SA State of Nation Address. Turkish Finance Minister is to announce “a new support package” on Feb 12th; will focus on measures to curb recent price rises whilst providing support to export firms, plans to bring “under-the-mattress gold” into the Turkish banking system.

In fixed income, core bonds back-off after a fade below midweek highs as US CPI looms before the long bond refunding leg. JGBs buck the bearish trend as the BoJ steps in to defend its YCT via unlimited purchases of 10 year maturities from February 14th.

In commodities, WTI and Brent remain choppy in fairly tight ranges in the context of recent performance, focus very much on geopols as Russian military drills commence. White House said President Biden and Saudi King spoke about commitment to ensure stability of global energy supplies, while Energy Intel noted that Saudi’s King Salman stressed importance of maintaining balance and stability in oil markets, highlighting importance of maintaining the OPEC+ agreement. OPEC MOMR to be released at 12:45GMT/07:45EST. Spot gold trades sideways and confirmed support at USD 1,830/oz, which acted as resistance on the way up. Base metals derived support in APAC hours while Coal pulled-back given recent commentary.

US Event Calendar

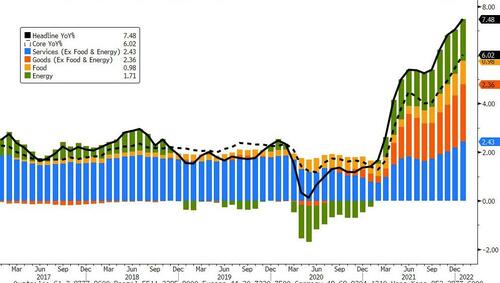

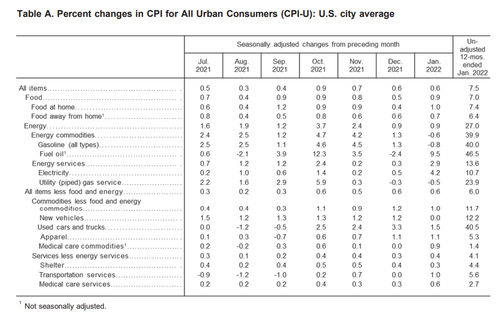

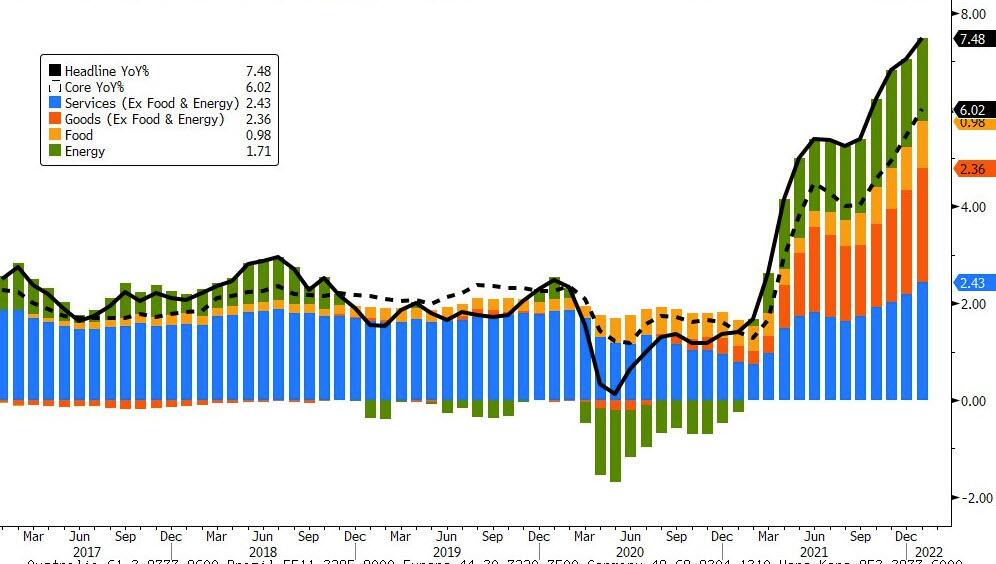

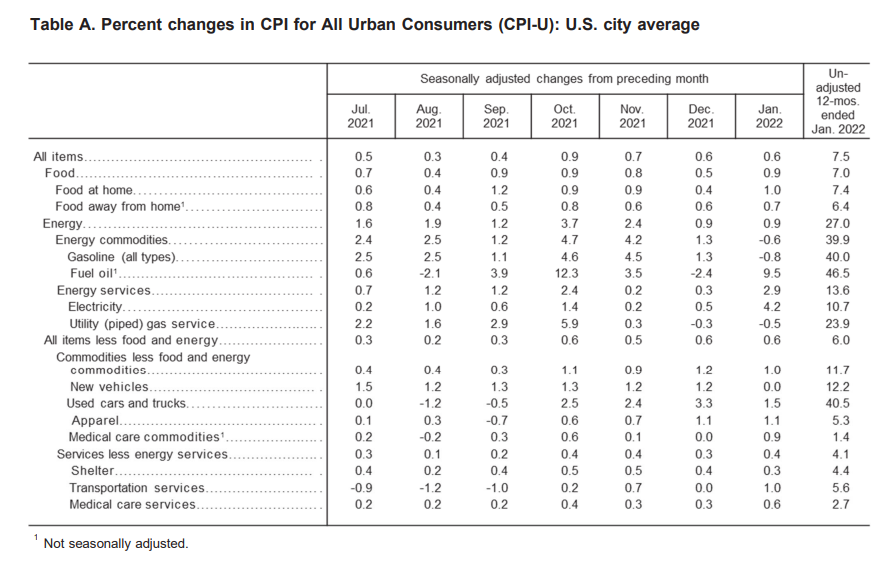

- 8:30am: Jan. CPI YoY, est. 7.2%, prior 7.0%; CPI MoM, est. 0.4%, prior 0.5%, revised 0.6%

- 8:30am: Jan. CPI Ex Food and Energy YoY, est. 5.9%, prior 5.5%, CPI Ex Food and Energy MoM, est. 0.5%, prior 0.6%

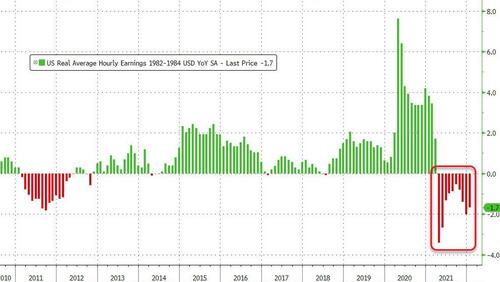

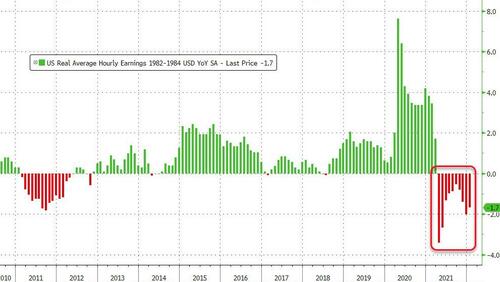

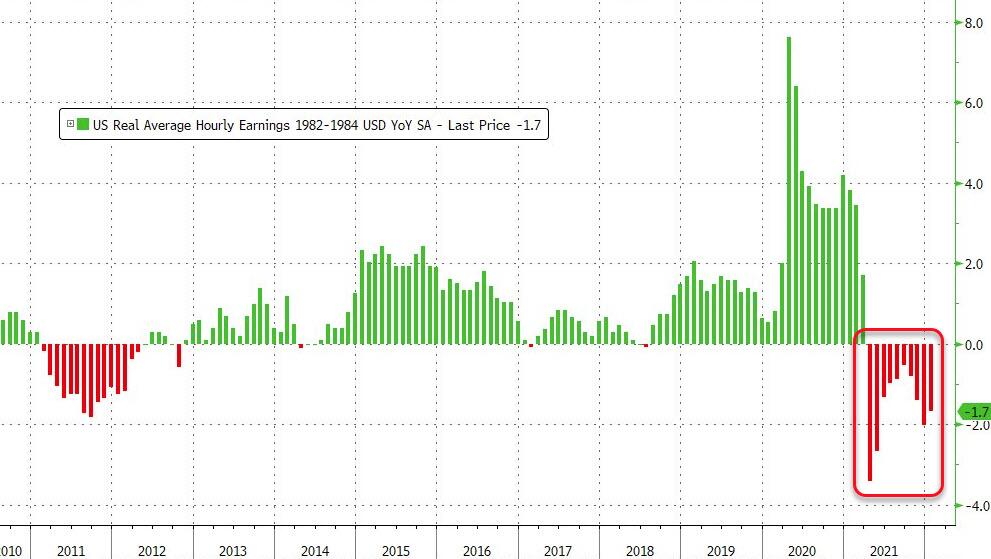

- 8:30am: Jan. Real Avg Hourly Earning YoY, prior -2.4%, revised -2.0%; Real Avg Weekly Earnings YoY, prior -2.3%, revised -2.0%

- 8:30am: Feb. Initial Jobless Claims, est. 230,000, prior 238,000; Continuing Claims, est. 1.62m, prior 1.63m

- 2pm: Jan. Monthly Budget Statement, est. $23b, prior -$162.8b

DB’s Jim Reid concludes the overnight wrap

I’ll be honest, life is so dull for me at the moment that work is my salvation. 9.5 days down on crutches now and 32.5 to go. Given I only went through the same thing on my other knee in September and October last year it is fair to say I’m ready for a decent stretch of no injuries. As is my wife who has to deal with me and also our 6-year old Maisie who is going to continue to be in wheelchair for the best part of this year. For those that have kindly asked the good news is that she’s swimming 4 times a week now and absolutely loves it. In fact she’s very good now and is a couple of years better than her age so that is one silver lining that has come out of her hip condition. The only benefit for me is that as I’m not going outside much, my usual blast of January onwards hay fever has not really made an appearance this year. Usually the silver birches (I think) at the golf course are my Kryptonite at this time of year. It is usually horrendous.

The Kryptonite for markets is undoubtedly inflation at the moment and it’s that time again with US CPI today the main event of the week. Last summer on a couple of occasions I suggested that the then upcoming day’s US CPI number could be the most important economic data release in perhaps a generation given the potential for regime change. However the summer inflation prints whilst consistently higher than expected were largely shrugged off by the market so my hyperbole was clearly misplaced. Without repeating my mistake, we are approaching a crucial point for US CPI. If we don’t start gliding lower in line with expectations soon, the market is going to be pricing some 50bps Fed hikes into the equation for 2022. Today’s number is a complicated one as Omicron could create distortion that unwind next month.

As readers will likely be familiar, recent months have seen repeated upside surprises, with the monthly headline CPI print above the consensus estimate on Bloomberg for 8 of the last 10 releases, sending the year-on-year number up to +7.0% for the first time since 1982. In terms of what to expect, our US economists are looking for a further increase in the year-on-year figure to +7.2% (in line with consensus), with core also rising to +5.8% (consensus 5.9%). That said, their view is that the month-on-month measure should subside to +0.38% from +0.58% in December, which would be a 5-month low and mark a third consecutive decline in the monthly reading. Core is expected to dip to +0.40% from +0.58% mom.

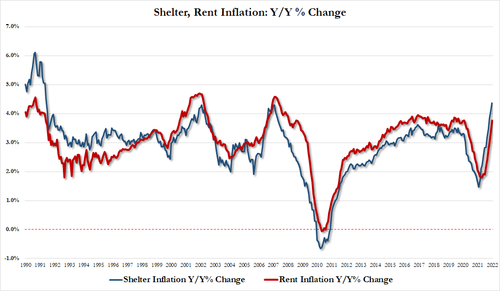

The wildcards might be lodging away and airfares due to Omicron. These fell -2.7% and -8.6% last August around the Delta variant. So the risks feel a touch skewed toward the downside this month even if that will likely be a temporary thing given the Omicron wave is well past the peak. Structurally we still see primary rents and OER as seeing enough upward pressure to keep the glidepath lower (when it comes) more shallow than the market thinks regardless of what happens today. As an aside, food prices continue to increase which won’t help, with Bloomberg’s Agriculture Spot index up +1.68% yesterday to its highest levels since 2011.

We’ll have to wait and see what happens, but it was only last Friday that a much stronger-than-expected jobs report turbocharged calls for a 50bp hike from the Fed. Immediately afterwards, futures moved to pricing in a more than 40% chance one could happen, although that number’s since fallen back to 30% this morning. Fed Chair Powell notably did not rule out moving by 50bps at the press conference after the last meeting, and a higher-than-expected inflation number today would only add fuel to the fire.

On the other hand, yesterday we did begin to see some signs of pushback on recent market pricing, with a number of central bank officials adopting a more cautious and measured tone relative to the market narrative of recent days. The comments on Monday evening from the ECB’s Villeroy after the European close that there “were perhaps reactions that were very high and too high in recent days” helped matters from the get-go. We then heard from the Fed’s Mester (a voter on the FOMC this year), who didn’t find a compelling case for raising rates by +50bps at liftoff. And earlier in the day, BoE Chief economist Pill also said that “I worry that taking unusually large policy steps may validate a market narrative that bank policy is either foot-to-the-floor on the accelerator or foot-to-the-floor with the brake”.

That pushback held more water in Europe, where there was a rally across all maturities and countries, with yields on 10yr bunds (-5.3bps), OATs (-5.5bps) and BTPs (-9.6bps) all moving lower on the day. Bunds saw their first yield fall in 12 days and ended the longest run of increases since reunification in 1990. Meanwhile in the US, the yield curve twist flattened, with 2yr Treasuries +2.3bps higher and 10yr Treasuries down -2.2bps, bringing the 2s10s yield curve to a fresh low of just +57bps yesterday, the lowest closing level since October 2020. Nevertheless, US rate moves were small in magnitude with most investors looking to CPI today as a key risk event.

Even with some pushback to the recent yield rises, the global tightening continued apace yesterday, with Romania’s central bank announcing a 50bps hike in their monetary policy rate, and Iceland’s central bank announced a 75bps hike in their 7-day term deposit rate as well, their biggest hike since 2008.

With the bond rout easing yesterday, equities continued their advance as both the S&P 500 (+1.45%) and Europe’s STOXX 600 (+1.72%) closed at their highest level in a week. It was a very broad-based advance for both indices; 428 companies in the S&P were in the green, the second-highest number of 2022 so far, while every sector advanced. Tech and mega cap stocks put in a strong performance in particular, with the NASDAQ (+2.08%) and the FANG+ index (+2.44%) both seeing a decent advance for the second day running.