FEB 16

FEB16

· by harveyorgan · in Uncategorized · Leave a comment ·Edit

GOLD; UP $14.60 to $1869.80

SILVER: $23.59 UP 21 CENTS

ACCESS MARKET: GOLD $1869.70

SILVER: $23.58

Bitcoin: morning price: $44,005 DOWN 135

Bitcoin: afternoon price: $44,269 UP $129

Platinum price: closing UP $38.90 to $1065.50

Palladium price; closing UP $30.30 at $222.70

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filed//comex notices//JPMorgan notices filed 0/0

COMEX//NOTICES:EXCHANGE: COMEX FILED:EXCHANGE: COMEX

NUMBER OF NOTICES FILED TODAY FOR FEB. CONTRACT: 0 NOTICE(S) FOR nil OZ (0.000 TONNES)

total notices so far: 17,478 contracts for 1,747,800 oz (54.363 tonnes)

SILVER NOTICES:

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month 1278 : for 6,390,000 oz

GLD

WITH GOLD UP $14.60

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES AT THE GLD:

CLOSING INVENTORY :1019.44 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 21 CENTS:/:

NO CHANGES IN SILVER INVENTORY AT THE SLV/:

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY SLV/ TONIGHT: 547.808 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG 2730 CONTRACTS TO 156,968 AND RESTS FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND DESPITE THIS TINY LOSS IN OI, IT WAS ACCOMPANIED WITH OUR CONSIDERABLE $0.46 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.46) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A GOOD GAIN OF 521 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.110 MILLION OZ FOLLOWED BY TODAY’S 100,000 OZ QUEUE JUMP//NEW STANDING 7.790 MILLION OZ. V) STRONG SIZED COMEX OI LOSS.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS -131

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB:

TOTAL CONTACTS for 12 days, total contracts: : 6818 contracts or 34.090 million oz OR 2.840 MILLION OZ PER DAY. (568 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 6818 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 34.090 MILLION OZ

.

LAST 10 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 34.090 MILLION OZ//

SPREADING OPERATIONS

(/NOW SWITCHING TO SILVER) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAR.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2599 ITH OUR CONSIDERABLE $0.49 GAIN SILVER PRICING AT THE COMEX// TUESDAY THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 750 CONTRACTS( 750 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 4.1 MILLION OZ FOLLOWED BY TODAY’S 100,000 OZ QUEUE JUMP //NEW STANDING 7.790, MILLION OZ// .. WE HAD A STRONG SIZED LOSS OF 1849 OI CONTRACTS ON THE TWO EXCHANGES FOR 9.245 MILLION OZ//

WE HAD 0 NOTICES FILED TODAY FOR nil OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1537 TO 558,645 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: —417 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE SMALL SIZED DECREASE IN COMEX OI CAME WITH OUR LOSS IN PRICE OF $12.70//COMEX GOLD TRADING/TUESDAY/.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR GOOD SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION AS THE TOTAL GAIN ON OUR TWO EXCHANGES TOTALED 2304 CONTRACTS…

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR FEB AT 64.3 TONNES FOLLOWED BY TODAY’S 1500 OZ E.F.P. JUMP TO LONDON //NEW STANDING: 58.373 TONNES

YET ALL OF..THIS HAPPENED WITH OUR STRONG GAIN IN PRICE OF $12.70 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A SMALL SIZED GAIN OF 2304 OI CONTRACTS (7.166 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3841 CONTRACTS:

FOR APRIL 3841 ALL OTHER MONTHS ZERO//TOTAL:3841

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 558,645.

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2304, WITH 1537 CONTRACTS DECREASED AT THE COMEX AND 3841 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2304 CONTRACTS OR 7.166TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3841) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (1537,): TOTAL GAIN IN THE TWO EXCHANGES 2304 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 64.30 TONNES WHICH FOLLOWS TODAY’S E.F.P. JUMP TO LONDON OF 1500 OZ//NEW STANDING 58.373 TONNES// 3) ZERO LONG LIQUIDATION ,4) SMALL SIZED COMEX OI. LOSS 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

30,268 CONTRACTS OR 3,026,800 oz OR 94.15 TONNES 12 TRADING DAY(S) AND THUS AVERAGING: 2522 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES: 94.15 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 94.15/3550 x 100% TONNES 2.64% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 94.15 TONNES//INITIAL

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 2730 CONTRACTS TO 156,968 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 750 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 750 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 750 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2599 CONTRACTS AND ADD TO THE 750 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 1980 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 9.90 MILLION OZ,

OCCURRED WITH OUR $0.46 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 19.74 PTS OR 0.57% //Hang Sang CLOSED UP 363.19 PTS OR 1.49% /The Nikkei closed UP 595.21 or 2/22% //Australia’s all ordinaires CLOSED UP 1.10% /Chinese yuan (ONSHORE) closed UP 6.3408 /Oil UP TO 93.47 dollars per barrel for WTI and UP TO 943.94 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3408. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3394: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFF SHORE STRONGER//

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 1537 CONTRACTS AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR LOSS OF $12.70 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (6903 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF FEB.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3841 EFP CONTRACTS WERE ISSUED: ;: , & FEB. 0 APRIL: 3841 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3841 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED 2304 TOTAL CONTRACTS IN THAT 3841 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI LOSS OF 1537 CONTRACTS..

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR FEB (58.370),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

FEB 2022: 58.370 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $12.70)BUT THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A GAIN OF 8.463 TONNES OF TOTAL OI, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR FEB (58.370 TONNES)…

WE HAD –417 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 2304 CONTRACTS OR 230400 OZ OR 7.166 TONNES

Estimated gold volume today: 123,450 /// POOR

Confirmed volume yesterday: 224,600 contracts fair

INITIAL STANDINGS FOR FEB ’22 COMEX GOLD //FEB 16

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | NIL oz |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 0 notice(s)0 OZ 1.660 TONNES |

| No of oz to be served (notices) | 1288 contracts 128,800 oz 4.000 TONNES |

| Total monthly oz gold served (contracts) so far this month | 17,478 notices1,747,800 OZ 103.25 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

No dealer deposit 0

No dealer withdrawal 0

0 customer deposit

total deposit: nil oz

0 customer withdrawal

total withdrawals: nil oz

ADJUSTMENTS: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEBRUARY.

For the front month of FEBRUARY we have an oi of 1288 stand for LOSING 16 contracts.

We had 0 contracts served upon yesterday, so we LOST 16 contracts or an additional 1600 oz will NOT stand on this side of the pond looking for gold metal.

The month of March saw a GAIN of 71 contracts and thus the OI standing is 4263.

April saw a LOSS of 3127 contracts down to 433,624.

June saw a gain of 806 contracts up to 70,397 contracts

We had 0 notice(s) filed today for 1000 oz FOR THE FEB 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB /2021. contract month,

we take the total number of notices filed so far for the month (17,478) x 100 oz , to which we add the difference between the open interest for the front month of (FEB: 1288 CONTRACTS ) minus the number of notices served upon today 0 x 100 oz per contract equals 1,876,600 OZ OR 58.370 TONNES the number of TONNES standing in this active month of FEB.

thus the INITIAL standings for gold for the FEB contract month:

No of notices filed so far (17,478) x 100 oz+ (1288) OI for the front month minus the number of notices served upon today (0} x 100 oz} which equals 1,876,700 oz standing OR 58.370 TONNES in this active delivery month of FEB.

We LOST 16 contracts or an additional 100 oz will NOT stand for gold over here

TOTAL COMEX GOLD STANDING: 58.370 TONNES (HUGE FOR A FEBRUARY DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

157,392.690, oz NOW PLEDGED /HSBC 4.89 TONNES

125,410.592 PLEDGED MANFRA 2.90 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690

288,481,604, oz JPM No 2 8.97 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonne

Loomis: 18,615.429 oz

total pledged gold: 1,553,863.297 oz 48.331 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 32,665,081 OZ (1016.02 TONNES)

TOTAL ELIGIBLE GOLD: 15,428,326.030 OZ (479.89 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,236,735.572 OZ (536.13 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,682,872.0 OZ (REG GOLD- PLEDGED GOLD) 487.95 tonnes

END

FEBRUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//FEB 16

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 993,579.860 oz Brinks CNT Manfra |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 31,167.150 oz Delaware |

| No of oz served today (contracts) | 0CONTRACT(S) (NIL OZ) |

| No of oz to be served (notices) | 280 contracts (1,400,000 oz) |

| Total monthly oz silver served (contracts) | 1278 contracts 6,390,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

i) Into Delaware: 31,167.150 oz

total deposit: 31,167.150 oz

JPMorgan has a total silver weight: 184.161 million oz/350.537 million =52.49% of comex

ii) Comex withdrawals: 3

a)Out of CNT 373,402.310 oz

b) Our of Brinks: 27,221.710 oz

c) out of Manfra: 592,954.990 oz

total withdrawal 993,579.860 oz

we had 0 adjustments

the silver comex is in stress!

TOTAL REGISTERED SILVER: 83.896 MILLION OZ

TOTAL REG + ELIG. 350.537 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR FEBRUARY

silver open interest data:

FRONT MONTH OF FEB//2022 OI: 280 CONTRACTS GAINING 20 contracts on the day. We had 0 contracts served upon yesterday.

So we gained 20 contracts or an additional 100,000 oz will stand for silver on this side of the pond.

FOR MARCH WE HAD A LOSS OF 57876 CONTRACTS DOWN TO 59,119 CONTRACTS.

APRIL HAD A 10 GAIN// CONTRACTS RISING TO 240

MAY HAD A GAIN OF 2497 CONTRACTS UP TO 77,449 contracts

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes: 58,028// est. volume today//poor

Comex volume: confirmed YESTERDAY: 78,274 contracts (FAIR- to GOOD)

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 1278 x 5,000 oz =. 6,390,000 oz

to which we add the difference between the open interest for the front month of FEB (280) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2021 contract month: 1278 (notices served so far) x 5000 oz + OI for front month of FEB (280) – number of notices served upon today (0) x 5000 oz of silver standing for the FEB contract month equates 7,790,000 oz. .

We gained 20 CONTRACTS OR 105,000 ADDITIONAL oz of silver will stand at the comex.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

GLD

FEB 16/WITH GOLD UP 414.60 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 15/WITH GOLD DOWN $12.70 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 14/WITH GOLD UP $27.20 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 11/WITH GOLD UP $4.50 A HUGE CHANGE IN GOLD IVNETORY AT THE GLD// A DEPOSIT OF 3.48 TONNES INTO THE GLD//INVENTORY RESTS AT 1019.44 TONES

FEB 10/WITH GOLD UP $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1015.96 TONNES

FEB 9/WITH GOLD UP $8.05//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1015.96 TONNES

FEB 8/WITH GOLD UP $5.95 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1015.96 TONNES

FEB 7/WITH GOLD UP $14.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.24 TONNES FROM THE GLD/////INVENTORY RESTS AT 1011.60 TONNES//

FEB 4/WITH GOLD UP $3.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.84 TONNES

FEB 3/WITH GOLD DOWN $5.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 1016.59 TONNES

FEB 2/WITH GOLD UP $7.95//A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.78 TONES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1018.04 TONNES

FEB 1/WITH GOLD UP $5.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 31/WITH GOLD UP $10.10//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 28/WITH GOLD DOWN $8.30//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 27/WITH GOLD DOWN $36.15//ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES INTO THE GLD.//INVENTORY RESTS AT 1014.26 TONNES

JAN 26/WITH GOLD DOWN $21.60 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES INTO THE GLD///INVENTORY RESTS AT 1013.10 TONNES

JAN 25/WITH GOLD UP $10.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 24/WITH GOLD UP $10.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: AN UNBELIEVABLE DEPOSIT OF 27.59 TONNES INTO THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 21/WITH GOLD DOWN $10.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 980.86 TONNES

JAN 20/WITH GOLD UP $.20 TODAY: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .58 TONNES FROM THE GLD///INVENTORY RESTS AT 980.86 TONNES

JAN 19/WITH GOLD UP $29.65 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 5.27 TONNES INTO THE GLD/INVENTORY RESTS AT 981.44 TONNES

JAN 18/WITH GOLD DOWN $3.25//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 14/ WITH GOLD DOWN $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 13/WITH GOLD DOWN $5.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 12/WITH GOLD UP $8.65//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 11/WITH GOLD UP $19.25/A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FROM THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 10/WITH GOLD UP $2.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.08 TONNES

CLOSING INVENTORY FOR THE GLD//1019.44 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 16/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.808 MILLIONOZ

FEB 15/WITH SILVER DOWN 46 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.808 MILLION OZ//

FEB 14/WITH SILVER UP 49 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.235 MILLION OZ INTO THES LV////INVENTORY RESTS AT 547.808 MILLION OZ

FEB 11/WITH SILVER DOWN 18 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ///

SLV/FEB 10/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 9/WITH SILVER UP 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 8/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.143 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 7/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.218 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 541.430 MILLION OZ/

FEB 4/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 539.212 MILION OZ

FEB 3/WITH SILVER DOWN 35 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT539.212 MILLION OZ//

FEB 2/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.411 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 539.212 MILLION OZ/

FEB 1/WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.801 MILLION OZ

JAN 31/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FORM THE SLV.//INVENTORY RESTS AT 533.801 MILLION OZ//

JAN 28/WITH SILVER DOWN 36 CENTS : NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 27/WITH SILVER DOWN $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 26/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 25/WITH SILVER UP 10 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.311 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 535.003 MILLION OZ/

.JAN 24/WITH SILVER DOWN 48 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.8 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 532.692 MILLION OZ//.

JAN 21/WITH SILVER DOWN 41 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 527.792 MILLION OZ

JAN 20/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.998 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 527.792 MILLION OZ

JAN 19/WITH SILVER UP 71 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.942 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 525.804 MILLION OZ

JAN 18/WITH SILVER UP 51 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: 2 WITHDRAWALS OF 1.11 MILLION OZ AND 1.424 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 527.246 MILLION OZ//

JAN 14/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 529.780 MILLION OZ//

JAN 13/WITH SILVER DOWN 2 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 832,000 OZ FROM THE SLV////INVENTORY RESTS AT 529.780 MILLION OZ

JAN 12/WITH SILVER UP 38 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//

JAN 11/WITH SILVER UP 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ/.

JAN 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY

RESTS AT 530.612 MILLION OZ//.

SLV FINAL INVENTORY FOR TODAY: 547.808 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Bullard Lets The Cat Out Of The Bag: The Fed Doesn’t Have The Stomach For An Inflation Fight

WEDNESDAY, FEB 16, 2022 – 01:20 PM

Authored by Michael Maharrey via SchiffGold.com,

St. Louis Federal Reserve President James Bullard unwittingly let the cat out of the bag and revealed the central bank doesn’t have the stomach to do what’s necessary to take on surging, persistent inflation.

After January’s CPI data came in even hotter than expected, Bullard shocked markets by calling for a full 1% rate hike by July. As CNBC reported, his comments sent stocks “on a wild ride” as futures markets began to price in as many as seven quarter-point rate hikes in 2022. That would push interest rates to 1.75% by the end of the year.

But just a day later, Bullard appeared on CNBC’s Squawk Box and did damage control. He didn’t back off his call for a 1% hike by this summer, but he did walk back his hawkishness, describing it as “front-loading” the Fed’s planned tightening.

I do think we need to front-load more of our planned removal of accommodation than we would have previously. We’ve been surprised to the upside on inflation. This is a lot of inflation.”

Bullard described his comments as “shading up” his position, and he emphasized he’s just one person on the committee.

Most significantly, Bullard insisted the Fed will continue to provide “accommodative” monetary policy.

We’re only removing accommodation, so it’s still an accommodative policy as we go through these initial rate hikes. They’re rather cheap actually.”

In other words, despite “a lot of inflation,” the Fed’s plan is to continue creating inflation with an accommodative monetary policy. Or to put it another way, the central bank will continue to pour gas on the inflationary fire.

Bullard’s damage control underscores the painful reality the Fed finds itself in. As economist André Marques put it, the Fed is trapped. It doesn’t really have room to raise rates or taper.

The Fed is trapped in its own web. It does not have much room to raise rates without major complications in the financial market and in the economy. Even if it finally delivers on tapering and starts raising rates, it won’t get any further than it did back in the last rate hike (2015–18) and balance sheet shrinking (2017–19) cycles.”

This is why Bullard emphasized the central bank can raise rates to address inflation, but “we can do it in a way that’s organized and not disruptive to markets.”

The freakout in the markets after Bullard’s initial statement on rate hikes is exactly why the St. Louis Fed president went on CNBC to do damage control and walk back his comments. Because deep down everybody knows any significant rate hikes will pop this bubble economy built on artificially low interest rates and monetary stimulus.

The reality is hiking interest rates 1 or 2 percent over the next year or two is not a tight monetary policy and it will do little nothing to get ahead of the inflation curve. Peter Schiff made this point in a recent interview on Fox Business. Keep in mind, Paul Volker had to raise rates to 20% in the early 1980s to tame the inflation of the 1970s. Inflation is every bit as high today if measured honestly.

If we still measured inflation the way we did 40 years ago, it would be 15%, not 7.5%. And the rate hikes they’ve proposed are completely inadequate. In fact, the Fed is intending to pursue an accommodative monetary policy. Even if they raise interest rates to 1 or 2%, that is highly accommodative. That’s the same type of interest rates they had when inflation was below 2%. You’ve got inflation at 7.5%, even the way they measure it – and rising. The only way to put out this fire is to have positive real interest rates. The Fed needs to get above the inflation rate. We’re not even going to get close. So, they’re going to continue to pour gasoline on the fire. And so, the entire time the Fed is inching up rates, inflation is actually going to be moving higher. Inflation is going to be worse in 2022 than it was in 2021, and real interest rates are going to continue to fall even as the Fed raises nominal rates.”

Bullard unwittingly let the cat out of the bag. To the extent that it enters the ring to fight, it’s going to lose because it doesn’t have the will to really fight. Peter made this point in a recent podcast.

It doesn’t matter if the Fed raises rates. Because it’s not going to raise them enough. Inflation is going to get worse no matter what the Fed does because the Fed doesn’t have the political will to actually raise rates high enough to fight inflation.”

The Fed will raise rates a little. As Peter put it, the central bank has to pretend it’s going to fight inflation, especially with inflation now widely considered a problem.

So, the markets are bracing for the fight. What they’re not bracing for is that the Fed is going to lose the fight — that inflation is going to win.”

end

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARD

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

This is your spreader operation@!! but a little more refined.

Craig Hemke at Sprott Money: ‘Trade at settlement’ rigging mechanism is at work in silver futures market

Submitted by admin on Tue, 2022-02-15 22:49Section: Daily Dispatches

10:42p ET Tuesday, February 15, 2022

Dear Friend of GATA and Gold:

The TF Metals Report’s Craig Hemke, writing at Sprott Money, reports tonight that the “trade at settlement” mechanism, seemingly used recently to knock the gold futures price down, is starting to be used in the silver futures market.

Hemke writes: “If the price of Comex silver pulls a full round trip next week, we may be able to say with confidence that we have uncovered the latest bank price manipulation technique.”

Hemke’s analysis is headlined “Comex Silver Trade at Settlement” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/COMEX-Silver-Trade-at-Settlement-Craig-Hemke-February-15-2022

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

END

end

!

4.OTHER GOLD/SILVER COMMENTARIES

$10,000 Silver: The Market Rigging Game Of The Last 170 Years Is About To End – Silver Doctors

Inbox

| douglas cundey | 7:09 AM (46 minutes ago) | ||

| to Chris, William, Bill, rkirby, me |

i believe this not the crypto part

$10,000 Silver: The Market Rigging Game Of The Last 170 Years Is About To End

Sponsored By: Mini Cboe VIX Futures

6226

Watch the bankers cringe at the sight of $10,000 silver…

by Bix Weir of Road to Roota

The “Silver Rigging Story” is now know by MILLIONS of people all around the world. The players and their tools are becoming common knowledge. Silver price suppression has left the Western Financial System extremely vulnerable…and the largest players in world finance know it. This game will not go on much longer. Get your PHYSICAL SILVER NOW!

END

5.OTHER COMMODITIES/GUACAMOLE (AVOCADO)

Chipotle On Brink Of Guacamole Shortage After US Bans Mexican Avocados

TUESDAY, FEB 15, 2022 – 09:45 PM

Four days have passed since the United States suspended all imports of Mexican avocados following a federal inspector threatened at an avocado farm in the state of Michoacan, Mexico (the central hub of Mexican avocado production). Now one of the largest US Mexican fast-food chains could be on the brink of a guacamole shortage.

NYPost reports Chipotle Mexican Grill sounded the alarm on possible future supply disruptions of avocados in the coming weeks.

“Our sourcing partners currently have several weeks of inventory available, so we’ll continue to closely monitor the situation and adjust our plans accordingly,” Chipotle’s CFO Jack Hartung said in a statement. He said the company is “working closely with our suppliers to navigate through this challenge.”

Hartung didn’t explain what supply distributions of avocados would mean for the company with nearly 3,000 US locations. The fast-food retailer was already dealing with some of the highest avocados prices, up 31% this year alone.

The price for a 20-pound box of avocados from the state of Michoacan was around $27.

Two decades of avocado prices show current prices are some of the highest ever for this time of year. And could be set to move higher, between the $30-$35 range if the import ban isn’t immediately lifted.

Chipotle has already raised prices to combat soaring food inflation. However, if the import ban remains in place, a shortage of guacamole could be seen as early March. There was no word if other fast food Mexican retailers such as Taco Bell, Qdoba Mexican Eats, Moe’s Southwest Grill, and Baja Fresh would experience similar issues.

end

6.CRYPTOCURRENCIES

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.3408

OFFSHORE YUAN: 6.3394

HANG SANG CLOSED UP 363.19 PTS OR 1.49%

2. Nikkei closed UP 595.21 PTS OR 2.22%

3. Europe stocks ALL RED

USA dollar INDEX DOWN TO 95.89/Euro RISES TO 1.1366-

3b Japan 10 YR bond yield: FALLS TO. +.221/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 115.68/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 93.47 and Brent: 94.67–

3f Gold UP /JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE CLOSED UP// OFF- SHORE UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.301%/Italian 10 Yr bond yield FALLS to 1.95% /SPAIN 10 YR BOND YIELD FALLS TO 1.22%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.68: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.68

3k Gold at $1853.00 silver at: 23.40 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble UP 10/100 in roubles/dollar AT 75.03

3m oil into the 93 dollar handle for WTI and 94 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 115.68 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9255– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0520 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

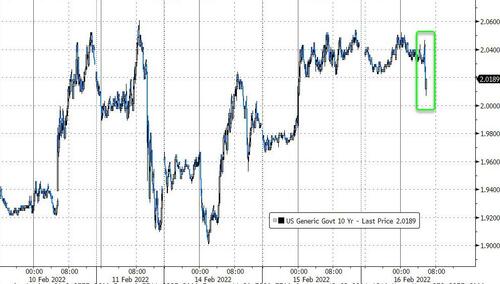

USA 10 YR BOND YIELD: 2.042 DOWN 1 BASIS PTS

USA 30 YR BOND YIELD: 2.348 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.60

Futures Tread Water Ahead Of FOMC Mintues As Russia Forgets To Invade Ukraine

WEDNESDAY, FEB 16, 2022 – 07:50 AM

The global rally stalled on Wednesday, and U.S. index futures were flat, treading water after a quiet overnight session, ahead of today’s FOMC minutes which some hope will unveil more detail on the Fed’s upcoming rate hike and QT, while also weighing the risks from the Ukraine tensions against inflation and tighter monetary policy. S&P 500 futures were flat and Nasdaq futures were little changed by 7:15 a.m. in New York, trimming earlier gains after NATO Sec. Stoltenberg pushed back on claims of Russian troop withdrawals, adding he is yet to see signs of a de-escalation. Treasury yields, bitcoin, gold and the dollar were also all flat. Oil recovered after the biggest one-day loss this year as worries about potential disruptions to commodity supplies eased.

Making a mockery of the Deep State/CIA/CNN which predicted that a Russian invasion would take place today, the Russian defense ministry announced more troops were returning to their bases after maneuvers ended in Crimea, while western officials remained cautious. Fed tightening bets were trimmed as traders speculated the size of the Fed’s interest-rate hike in March and tightening plans. And while the world is mocking US intelligence agencies, traders are awaiting the latest Federal Reserve minutes later Wednesday that may shape views on how fast the Fed will raise interest rates and shrink its bond holdings in coming months.

Airbnb advanced in premarket trading as analysts hiked price targets after its revenue for the fourth quarter beat estimates, while Roblox sumpled 16% after reporting bookings for the fourth quarter that missed estimates. Daily active users came in slightly below expectations too, and analysts were disappointed by the video game maker’s monetization metrics. Here are some other notable movers:

- Upstart (UPST US) shares are up 26% in U.S. premarket, after the cloud-based artificial intelligence lending platform reported “impressive” 4Q results and FY22 outlook, according to analysts.

- Toast (TOST US) shares slump 16% in premarket trading after the restaurant software company’s projection for 2022 adjusted Ebitda loss was wider than the average analyst estimate.

- Pinduoduo (PDD US) shares are attractively valued following decline since 3Q21 results and on global tech selloff, Citi writes in note upgrading to buy from neutral. Stock up 2.4% in premarket trading.

- Old National Bancorp shares dropped 1.7% postmarket despite an announcement from S&P Dow Jones Indices it will move to replace Urban Edge Properties in the S&P MidCap 400.

- Navitas Semiconductor (NVTS US) shares fall 6.1% in extended trading after the company gave a full-year revenue forecast that trailed analysts’ projections.

- Mirati Therapeutics (MRTX US) slipped 8.7% in postmarket trading after its application for approval of its lung cancer drug targeting a mutation known as KRAS was assigned a Dec. 14 date by U.S. regulators.

- Pacific Biosciences of California (PACB US) shares slumped 12% in postmarket trading after the company reported a net loss that was more than analysts estimated.

- Akamai Technologies (AKAM US) shares dropped 5% postmarket after the tech company reported adjusted earnings per share for the fourth quarter that beat the average analyst estimate.

The standoff between Russia and the West over Ukraine is continuing to vex markets as investors struggle to assess Moscow’s claim that some forces are being withdrawn. They’re also considering escalating costs and the likelihood of tightening monetary policy in places like the U.S. and the U.K., where inflation posted a surprise jump. While Russian stocks rose to the highest level in a week, volatility gauges for the S&P 500 and the Treasury market are sitting significantly above 12-month averages, a sign that traders remain on edge.

“Geopolitical tensions should not mask the fact that rates are in an uptrend,” ING Bank NV analysts led by Padhraic Garvey wrote in a note to investors. “This is a global trend if there ever was one.”

In Europe, the Stoxx 600 Index fluctuated after earlier extending Tuesday’s gains. The Euro Stoxx 600 was fractionally higher with the FTSE 100 lags dropping 0.2%. Sectors in Europe are a mixed bag with Basic Resources and Energy top of the leaderboard amid strength in underlying commodity prices, while personal care, telecoms and banks are the worst performing sectors. Here are some of the biggest European movers today:

- Air Liquide gains as much as 4% in Paris trading, the most intraday since Dec. 7, after the French company reported what Morgan Stanley describes as a strong set of results, with pricing and underlying margins both ahead of expectations.

- La Francaise des Jeux rises as much as 7.7%, the biggest one-day gain in a year, after the French lottery firm reported FY21 results that beat expectations and FY22 guidance that was also ahead of expectations, according to Citi (neutral).

- Umicore climbs as much as 8.6%, the most intraday since April, after net debt fell by more than analysts estimated.

- Swedish Match rises as much as 7%, the stock’s best day since December, after results. Handelsbanken notes strong volume for co.’s Zyn brand in the U.S. driving Ebit in the Smokefree product segment.

- Ericsson falls as much as 12% after the company’s CEO told Dagens Industri that the firm may have made payments to the ISIS terror organization in order to gain access to certain transport routes in Iraq.

- Vitrolife falls as much as 14% after the Swedish fertility company’s 4Q Ebitda missed estimates. ABG Sundal Collier notes organic growth also came in below expectations, but says acquisitions lessened the impact.

- Delivery Hero slides as much as 8.5% after Deutsche Bank analyst Silvia Cuneo downgraded the stock to hold from buy.

U.K. inflation unexpectedly accelerated for a fourth straight month in January, a surprise that highlights a brutal cost-of-living crisis that’s only set to worsen this year. Separately, the European Union won the right to use tough new powers to deny Poland and Hungary billions of euros of EU funding for allegedly failing to abide by the bloc’s democratic standards.

Earlier in the session, Asian stocks rallied, set to snap a three-day decline, as investors bet that geopolitical tensions over Ukraine may be easing. The MSCI Asia Pacific Index jumped as much as 1.6%, after falling more than 2% over the past three sessions. Information-technology firms provided the most support after Russia announced a partial pullback of some troops near Ukraine, easing concerns over the supply of key chip materials such as palladium. Chip supply chain companies outperformed after the Philadelphia Stock Exchange Semiconductor Index surged 5.5%, the most since March 2021. Benchmark gauges in Japan, South Korea and Taiwan were among the region’s best performers, with the latter two benefiting from tech gains. “The market is going up one day and falling the next depending on how things are unfolding with regards to Ukraine,” said Masahiro Ichikawa, chief market strategist at Sumitomo Mitsui DS Asset Management in Tokyo. “The overall trend is for stocks to recover, but market anxiety will continue to linger.” Biden Says Threat to Ukraine Remains, Awaits Russia Pullback Worries over potential U.S. rate hikes and the situation in Ukraine have kept Asian stocks from achieving a sustainable rally. The regional benchmark is down by about 1.5% so far this year after dropping 3.4% in 2021.

Japanese equities rose for the first time in three sessions, joining a global rally amid speculation over easing Russia-Ukraine tensions. Electronics and chemical makers were the biggest boosts to the Topix, which rose 1.7%. Tokyo Electron and Fast Retailing were the largest contributors to a 2.2% rise in the Nikkei 225, its biggest gain since Nov. 1. Travel-related stocks rose after reports that Japan will waive quarantine for some travellers.

“The Nikkei 225 is basically in a recovery trend,” said Masahiro Ichikawa, chief market strategist at Sumitomo Mitsui DS Asset Management. The easing of border controls “is a plus for reopening plays. But the local market now is dominated by overseas factors than domestic ones, like the Ukraine situation, the pace of U.S. rate hikes and their monetary-policy direction.”

Australian stocks also advanced, with the S&P/ASX 200 index rising 1.1% to close at 7,284.90 as most sectors gained. CSL contributed the most to the gauge’s climb after the biotechnology company effectively raised its guidance and posted first-half results that beat expectations. Liontown was the top performer after entering a lithium supply pact with Tesla. Netwealth was the biggest laggard after its 1H profit fell. In New Zealand, the S&P/NZX 50 index rose 1.5% to 12,121.89.

India’s benchmark equities index fell, after swinging between gains and losses several times through the day, as traders took a pause to evaluate the prospect of diminishing tension over Ukraine and easing crude oil prices. The S&P BSE Sensex slipped 0.3% to 57,996.68 in Mumbai, after moving between gains of as much as 0.7% and a loses of 0.6% in the session. The NSE Nifty 50 Index fell 0.2%. ICICI Bank Ltd. contributed the most to the Sensex decline, falling 1.6%. Out of the 30 shares in the Sensex index, 20 fell. The key indexes had climbed the most in over an year on Tuesday, erasing a similar magnitude of loss a day before. Prices of Brent crude, a major import for India, rose 0.9%, after plunging 3.3% in the previous session. Western officials remained cautious saying they have yet to verify Moscow’s claims that it started to pull back tens of thousands of soldiers massed along Ukraine’s borders. “Markets are currently dancing to the global tunes and we don’t see this changing anytime soon,” said Ajit Mishra, vice president research at Religare Broking Ltd. “The US Fed meeting minutes and lingering tension over the Russia-Ukraine crisis will remain on the radar.”

In rates, Treasuries were slightly richer across the curve into early U.S. session, with futures having erased declines. Short-dated gilts outperformed following the latest red-hot U.K. January CPI data. Yields richer by 1bp-2bp in parallel shift across the curve, 10- year 2.03%; U.K. 2- and 5-year yields are richer by 6.5bp and 5bp on the day, outperforming core euro-zone. Focal points of U.S. session include 20-year new-issue bond auction and release of minutes of FOMC’s Jan. 26 meeting, which conveyed the potential for a faster pace of rate hikes if needed to curb inflation. Gilts curve bull steepen with 2s10s widening 4.5bps. Bunds little changed. Peripheral spreads are mixed to Germany; Italy widens, Spain tightens and Portugal tightens.

In Fx,the dollar traded below 96 low as markets continue to weigh up conciliation from Russia against caution from the West and scepticism from NATO. Loonie bounces pre-Canadian CPI and Sterling bid post-firmer than forecast UK inflation data with Cable hovering above the 50% Fib of its 2022 range so far at 1.3554, while EUR/GBP respects resistance circa 0.8400. Aussie and Euro inch closer to round numbers at 0.7200 and 1.1400 respective after breaching upside chart levels, but Eur/Usd faces decent 1.5 bn or so option expiry interest between 1.1395-1.1405. Safe haven Yen and Franc lag, but latter yet to close below a key technical pivot at 115.67.

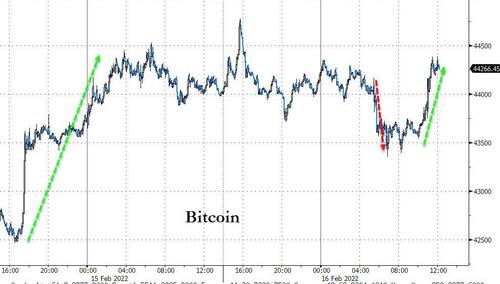

In commodities, oil recovered after the biggest one-day loss this year as worries about potential disruptions to commodity supplies eased. WTI trades within Tuesday’s range, adding 1% to trade near $93. Most base metals trade in the green; LME zinc rises 1%, outperforming peers. Spot gold is little changed at $1,855/oz. Bitcoin is modestly softer on the session and continues to consolidate around Tuesday’s parameters.

Looking at the day ahead, data releases include the UK and Canada’s CPI for January, whilst from the US there’s January’s retail sales, industrial production, capacity utilisation, and February’s NAHB housing market index. From central banks, we’ll get the minutes of the FOMC’s January meeting, and Minneapolis Fed President Kashkari is speaking. Finally, earnings releases include Nvidia, Cisco Systems, Applied Materials and AIG.

Market Snapshot

- S&P 500 futures dropped to 4,452.00

- MXAP up 1.5% to 190.11

- MXAPJ up 1.3% to 625.51

- Nikkei up 2.2% to 27,460.40

- Topix up 1.7% to 1,946.63

- Hang Seng Index up 1.5% to 24,718.90

- Shanghai Composite up 0.6% to 3,465.83

- Sensex little changed at 58,094.82

- Australia S&P/ASX 200 up 1.1% to 7,284.93

- Kospi up 2.0% to 2,729.68

- STOXX Europe 600 up 0.3% to 469.11

- German 10Y yield little changed at 0.32%

- Euro up 0.2% to $1.1384

- Brent Futures up 1.0% to $94.17/bbl

- Brent Futures up 1.0% to $94.17/bbl

- Gold spot up 0.2% to $1,856.88

- U.S. Dollar Index down 0.20% to 95.80

Top Overnight News from Bloomberg

- Stocks climbed, while bonds fell with the dollar as speculation that geopolitical tensions could be easing overshadowed data showing inflation is still running hot.

- U.K. inflation unexpectedly accelerated for a fourth straight month in January, a surprise that highlights a cost-of-living crisis that’s only set to worsen this year.

- The Russian defense ministry on Wednesday announced more troops were returning to their bases after maneuvers ended in Crimea, which Russia annexed in 2014. But western officials said they remain cautious.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded higher following the optimism seen in European and US peers yesterday. ASX 200 was kept afloat by its Healthcare sector, although gains were capped by losses in Energy and Metal names. Nikkei 225 and KOSPI both benefitted from a strong tech sector, whilst the former also benefits from favourable Yen dynamics. Hang Seng and Shanghai Comp. conformed to the regional gains, although the latter lacks momentum after a daily PBoC drain and following yesterday’s maintained MLF rate – which likely means the February LPRs will also be held.

Top Asian News

- Kuroda: BOJ Will Use Fixed-Rate Bond Operation Again If Needed

- China’s Xi Orders Hong Kong to Tackle Covid Surge by All Means

- PBOC Governor Vows More Support for ‘Weak Links’ in Economy

- Shimao Seeks Repayment Extension on $947 Million Trust Products

European bourses (Eurostoxx 50 unch.) trimmed early gains as NATO Sec. Gen. Stoltenberg pushed back on claims of Russian troop withdrawals, adding he is yet to see signs of a de-escalation. US futures (ES -0.1%) sit in minor negative territory amid the pullback in risk sentiment; traders await US retail sales and FOMC minutes. Sectors in Europe are a mixed bag with Basic Resources and Energy top of the leaderboard amid strength in underlying commodity prices

Top European News

- Europe Pushes Easing; Xi’s Order for Hong Kong: Virus Update

- U.K. Inflation Overshoot Adds to Brutal Cost of Living Squeeze

- Europe Heads Back to Normal as Germany Joins End of Covid Curbs

- Deutsche Bahn Said to Prepare $23 Billion Schenker Sale

In FX, DXY down to new sub-96.00 WTD low as markets continue to weigh up conciliation from Russia against caution from the West and scepticism from NATO. Loonie bounces pre-Canadian CPI and Sterling bid post-firmer than forecast UK inflation data with Cable hovering above the 50% Fib of its 2022 range so far at 1.3554, while EUR/GBP respects resistance circa 0.8400. Aussie and Euro inch closer to round numbers at 0.7200 and 1.1400 respective after breaching upside chart levels, but Eur/Usd faces decent 1.5 bn or so option expiry interest between 1.1395-1.1405. Safe haven Yen and Franc lag, but latter yet to close below a key technical pivot at 115.67

In commodities, WTI and Brent remain firmer on the session but reside within overnight ranges, in European hours the benchmarks have been moving on geopolitical updates from Russia & NATO. Currently, Brent is holding above the USD 94.00/bbl mark but remains shy of the USD 94.60/bbl session high. US Private Inventory Data (bbls): Crude -1.1mln (exp. -1.6mln), Cushing -2.4mln, Gasoline -0.9mln (exp. +0. 6mln), Distillates -0.5mln (exp. -1.5mln). Iraqi Kurdistan Regional Government PM says it has discussed possible gas and renewable energy investment with the Qatar Energy Minister, via Reuters. Spot gold/silver are little changed overall as the yellow metal holds onto the USD 1850/oz mark, awaiting fresh drivers and looking to US data/Fed speak & minutes.

In fixed income, solid demand for 10 year German issuance helps Bunds consolidate recovery gains off new cycle low. Gilts also off worst levels as NATO raises more doubt about Russia recalling troops from the border with Ukraine. US Treasuries lag ahead of busy agenda including primary data, 20 year note supply and January’s FOMC minutes

Central banks:

- PBOC Governor Yi Gang expects China’s economic growth to return to potential this year; China will keep accommodative monetary policy flexible, according to Reuters.

- Chinese press suggests the PBoC LPR will be maintained in February.

- BoJ Governor Kuroda says fixed-rate bond purchase offer was made amid the “unusual” market situation, via Reuters; if situation become unusual again could use such tools.

In geopolitics:

- Russia is preparing to withdraw additional military columns from Crimea following military drills, via Reuters citing Ifx

- NATO Secretary General Stoltenberg says they are yet to see any Russian de-escalation, Russia is continuing with its military buildup. Continue to convey message that we are prepared to talk. Messages on diplomacy from Moscow, Russia are proving some grounds for cautious optimism. Russia has always moved forces back and forth, movement is not confirmation of a withdrawal.

- Russia does not plan to move its embassy in Ukraine from Kiev, a source told Sputnik.

- Russia’s EU representative says he can confirm that there will be no invasion today, no escalation, neither next week nor next month.

- Russia will not partake in the special-OSCE meeting regarding Belarus military exercises, via Reuters citing Tass.

- NATO frigates tried to conduct electronic reconnaissance of Russian ships in the Mediterranean, according to Sputnik

- Ukraine Defence Ministry says the unprecedented DDoS attack is still ongoing, attackers succeeded in locating code vulnerabilities

DB’s Jim Reid concludes the overnight wrap

Geopolitics remained the dominant theme in markets yesterday, with risk assets recovering thanks to signs of easing tensions between Russia and the West over Ukraine. In fact the first market reaction of the day came not long after we went to press, when the news came through that Russia would be returning thousands of troops to bases following drills, raising hopes that a diplomatic solution could be found and boosting investor sentiment relative to the more downbeat tone on Monday.

The more positive newsflow helped numerous assets, and the decline in energy prices demonstrated how markets were taking the news positively. Brent crude oil prices (-3.32%) had their biggest daily decline of 2022 so far, whilst European natural gas futures were down -12.20% to €70.92/MWh, marking their lowest closing level since New Year’s Eve. Gold (-0.94%) also took a sharp turn lower as the news dampened demand for safer haven assets, and equities got the day off to a strong start from the get-go.

Even with that partial bounceback however, the situation remains volatile. In response to the news of a Russian withdrawal, NATO Secretary General Stoltenberg commented that this was “reason for cautious optimism”, but said “So far, we haven’t seen any sign of de-escalation on the ground”. President Biden struck a similar tone in public comments just before the US close yesterday, where he noted an attack was very much still a possibility and urged US citizens to leave the country, and also said that the US had not verified Russia’s claims about troop withdrawals. He reaffirmed sanctions would be severe in response to any invasion. Furthermore, Russian President Putin is calling for security guarantees that are still being rejected, including a commitment that Ukraine will not join NATO, which has been a non-starter for NATO, so many of the causes behind recent tensions are still in place. Nevertheless, sentiment incrementally improved, and the caveats from western leaders to the earlier news of Russian withdrawals weren’t enough to dampen risk appetite.

The relief in risk assets was evident across the board, with the S&P 500 (+1.58%) bouncing back alongside Europe’s STOXX 600 (+1.43%). Both saw a broad-based advance, with energy stocks one of the few underperformers in both jurisdictions due to the sharp decline in energy prices as mentioned at the top. Otherwise there was a very strong performance, and the small-cap Russell 2000 (+2.76%) posted even larger gains, as did the FANG+ index (+3.23%) of megacap tech stocks.

For those after further detail on what recent tensions mean for different economies, the European economics team published a note last night (link here) assessing the risks to the European economy from an escalation. They look at two shock scenarios: one that sees a 50% increase in gas prices and a 20% increase in oil prices, and a more severe one that has a 100% increase in gas prices and a 50% increase in oil prices. Both would see a notable rise in inflation relative to the non-conflict baseline, alongside a reduction in growth. In turn, this could see the ECB put its step-by-step exit on hold initially and maintain APP net asset purchases at €40bn per month, as well as a rise in deficits as the economy deteriorates and governments seek to shield their economies from the growing cost-of living crisis. There’s plenty of detail on those, as well as the ways in which a conflict would affect the European economy through numerous channels.

Whilst geopolitical events were the main driver in markets yesterday, there was another familiar theme too as we got a further upside surprise from US inflation, this time with the PPI reading for January. The monthly reading came in at +1.0% (vs. +0.5% expected), which was above every economist’s estimate on Bloomberg and the fastest monthly pace in 8 months. In turn that left the year-on-year figure at +9.7% (vs. +9.1% expected), only seeing a slight decline from the +9.8% figure in December. Elsewhere, the Empire State manufacturing survey’s prices received index reached a record high of 54.1 in February, and prices paid also held roughly steady at 76.6 (vs. 76.7 in January).

Yields on US Treasuries moved higher against that backdrop, with the 10yr yield up +5.6bps to 2.04%, which is their highest closing level since July 2019. That move was entirely driven by higher real yields, with the 10yr real yield up +8.2bps to -0.44%, and on top of that the 2s10s curve actually steepened yesterday after a run of 5 consecutive moves flatter, shifting up +5.5bps to 46.2bps. Continental Europe saw a similar move higher in yields, with those on 10yr bunds up +2.5bps to 0.30%, which is their own highest level since November 2018.

Overnight in Asia, equity markets across the region are witnessing a broad rally in line with that seen in the US and Europe. The Nikkei (+2.25%) is one of the strongest performers this morning, with the Kospi (+1.94%) and the Hang Seng (+1.18%) also moving higher, whilst the Shanghai Composite (+0.53%) and the CSI (+0.50%) have posted somewhat weaker gains. Overnight we’ve also had the latest inflation data from China which came in beneath expectations. That saw CPI fall to +0.9% in January on a year-on-year basis (vs. +1.0% expected), whilst PPI fell to +9.1% (vs. +9.5% expected). In turn, with the below-expected inflation numbers giving the PBOC more room to ease, Iron ore futures in Singapore rose +1.1% to $137.35/ton, reversing its earlier losses after declining around -11.0% in last three trading sessions. Outside of Asia, 10yr USTs are down -1.4bps to 2.029%, and equity futures are pointing to a slightly negative start in the US, with those on the S&P 500 down -0.17%.

Looking forward, we’ve a couple of adverts for you now. The first is Deutsche Banks’ annual Global ESG Conference on Feb 28th to March 2nd. The virtual event features presentations from 60+ companies and focused panels on a range of topics, and Michael Bloomberg, the UN Secretary-General’s Special Envoy for Climate Ambition and Solutions will be delivering the keynote address. The link for clients to register is here. Second, DB’s Maximilian Uleer will be hosting an expert call on power prices with Dr. John Feddersen, the CEO of Aurora Energy Research. Topics will include Europe’s dependence on Russian gas imports, and the call is taking place later today. For more details and the registration link click here.

In other news yesterday, President Biden’s nominees for various Federal Reserve positions will have to wait to have their candidacies put to the full Senate for a confirmation vote. It came as some Republicans on the Senate Banking Committee disapproved of certain nominees. Committee Chair Senator Brown, a Democrat, said he would reschedule the votes, which also include those on Fed Chair Powell’s nomination for a second term, Governor Brainard’s nomination as vice chair, and three additional nominees for Governor.

On the data front, the latest numbers continued to point to very tight labour markets in the UK, with vacancies hitting a record high of 1.298m in the 3 months ending January. The number of payrolled employees in January was also up by +108k, and unemployment came in at 4.1% in the three months ending December, in line with expectations. That’ll be followed by the CPI release this morning as well. Over in Germany, the ZEW survey for February came in a bit below expectations, but saw an improvement on January’s numbers. The expectations component rose to a 7-month high of 54.3 (vs. 55.0 expected), and the current situation ended a run of 4 consecutive declines to rise to -8.1 (vs. -6.5 expected).

To the day ahead now, and data releases include the UK and Canada’s CPI for January, whilst from the US there’s January’s retail sales, industrial production, capacity utilisation, and February’s NAHB housing market index. From central banks, we’ll get the minutes of the FOMC’s January meeting, and Minneapolis Fed President Kashkari is speaking. Finally, earnings releases include Nvidia, Cisco Systems, Applied Materials and AIG.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 19.74 PTS OR 0.57% //Hang Sang CLOSED UP 363.19 PTS OR 1.49% /The Nikkei closed UP 595.21 or 2/22% //Australia’s all ordinaires CLOSED UP 1.10% /Chinese yuan (ONSHORE) closed UP 6.3408 /Oil UP TO 93.47 dollars per barrel for WTI and UP TO 943.94 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3408. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3394: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFF SHORE STRONGER//

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

Ridiculous!! North Korean authorities arrest a dance tutor and her students for practicing capitalist dance moves

(Fredly/EpochTimes)

North Korean Authorities Arrest Dance Tutor, Students For Practicing “Capitalist” Dance Moves: Report

TUESDAY, FEB 15, 2022 – 10:45 PM

Authored by Aldgra Fredly via The Epoch Times,

North Korean authorities have reportedly arrested a dance tutor and several of her students for using foreign media to practice a “capitalist” dance routine, news outlet Radio Free Asia (RFA) reported on Friday, citing sources in the teacher’s neighborhood.

A resident of the northwestern city of Pyongsong said on Jan. 31 that a dance instructor, who appears to be in her 30s, was caught teaching “foreign-style disco dances” to teenage students in Yangji-dong of Pyongsong City.

In North Korea, anyone caught with large amounts of media from South Korea or the United States could face a life sentence or even a death penalty under the Elimination of Reactionary Thought and Culture Act enacted in December 2020.

While enforcement of the law is often lenient around Seollal, which refers to the Korean Lunar New Year, the Anti-Socialism Inspection Group has been particularly active in operating clampdowns this year, according to a source.

“The Anti-Socialism Inspection Group, a joint operation of the State Security Department and the police, has been intensively cracking down on people for watching South Korean movies and distributing foreign media,” the resident told RFA.

The source, who was speaking on the condition of anonymity, claimed that officers from the Anti-Socialism Inspection Group monitored the dance tutor’s residence in plain clothes for two days before conducting a raid.

“At the scene of the crackdown on the dance instructor that day, a USB flash drive containing foreign songs and dance videos had been plugged in, next to the flatscreen TV,” the source said, adding that the flash drive was also seized during the raid.

In this May 11, 2016, file photo, members of the Moranbong Band, North Korea’s most popular all-female pop group formed by leader Kim Jong Un, perform during a concert where high level officials, diplomats and foreign journalists were invited to watch, as part of celebrations on the conclusion of the ruling party congress in Pyongyang, North Korea.

The dance instructor is believed to have been working at Okchon high school in Pyongsong with a monthly salary of 3,000 won ($2.50), before deciding to open a private dance academy in her house for middle and high school students.

According to another source, the dance tutor charges around $10 per hour for a twice-weekly dance class. Most of her students come from wealthy families, which are often spared harsh punishment for minor transgressions.

“However, since the Central Committee has ordered that those who violate the Elimination of Reactionary Thought and Culture Act be severely punished regardless of their rank or class, the foreign dance instructor and students caught this time will not be spared from hard labor,” the source said.

“Their parents are also likely to be punished by being forced to leave the party.”

Meanwhile, a South Korean-based human rights group reported last year that at least seven people had been put to death for watching or distributing K-pop videos, or Korean popular music, since leader Kim Jong-un took power in 2011.

end

3B JAPAN

3c CHINA

CHINA

end

4/EUROPEAN AFFAIRS

EUROPE vs UK SPLIT

A very important read from Tom Luongo…

(Tom Luongo)

Will Lagarde & The ECB Survive This Inflection Point In Geopolitics?

WEDNESDAY, FEB 16, 2022 – 05:00 AM

Authored by Tom Luongo via Gold, Goats, ‘n Guns blog,

Recently, ECB President Christine Lagarde shocked markets with surprisingly hawkish talk at her monetary policy press conference.

Lagarde didn’t make any sudden moves in policy or anything. The ECB has yet to end any of its bond-buying and internal debt-transfer alphabet soup projects, and won’t until Q3 at the earliest.

Markets were not prepared by her previously that she would set such a hawkish tone. Say what you want about FOMC communications policy, at least under Jerome Powell, they tell you what they are going to do and then do it.

But Lagarde needed to do something dramatic because capital markets were moving quickly against her.

Traders stopped trying to disbelieve the illusion of Fed hawkishness and finally accepted what Powell was saying. For better or worse (and that debate was lively in this podcast I did with Peter Boockvar last week) the Fed will raise rates in March.

This isn’t an article about whether the Fed is making a policy error or not. This article isn’t even really about Christine Lagarde and the ECB. The actions of these two figures are downstream of the rapid changes occurring in the geopolitical landscape.

Those changes forced Lagarde to jawbone the euro higher and stave off a collapse in credit spreads.

So bear with me as I link the new gas deal between Russia and China to the the splits within the Anglo/Euro political hierarchy. Because once I’m done I hope you’ll see the inflection point we now find ourselves in the geopolitical Great Powers game.

So, back to Lagarde.

Central to Eurasia

I’ve talked in recent weeks about what I think the real story is behind the US/UK push for war over the breakaway Ukrainian republics known as the Donbass.

In short, it is a manufactured crisis to engineer the independence of the European Union from the US/UK traditional forces which have pushed the world to its current state. Biden will get to look tough staring down the Russians with sanctions threats and the Germans will finally get their shiny, new natural gas pipeline which will solidify their political control over the EU.

Despite ham-fisted propaganda and diplo-speak to the contrary, NATO is an aggressive alliance designed to further Anglo/European hegemony over Eurasia. The policy is informed by the writings of Halford Mackinder more than 100 years ago.

He who controls the world island of Eurasia controls the world. If you can’t control it, stop anyone else from doing so. That simple maxim drives so many people within Western foreign policy and military circles.

It’s an idea dying a little more with each generation but since Davos refuses to let the next generations take control in the U.S. and Europe, the policy persists with whatever energy a bunch of octogenarians can muster.

However, while Mackinder still dominates Western thinking about Russia and China, over the past couple of decades there has been a subtle but very real shift in the internal power balance of between Europe and the US, to the US’s disadvantage.

Europe wants to control Western foreign policy, supplanting the US/UK axis which has dominated since WWI or earlier.

This is at the heart of my theory of Davos — Old European money wants to take back control of Western economic and foreign policy from the Yanks and the Colonies after two centuries of subordination.

And what has become clear to me is that, post-Trump/post-Brexit, there are sincere faults within the cozy relationship between these two culturally very different tribes — the Anglosphere of the US/UK and the traditional European colonial powers.

As the USSR fell, when Russia was weak, it was easy for them to be united in common cause: Destroy the USSR, strip the resultant Russian Federation of its assets, take over the country from within, centralize control over Europe in Brussels, elevate the post-WWII Institutions to enforce a New World Order.

This is the essence of the Bill Browder story and all of the subsequent NATO expansion eastward.

Out with Brzezinski, in with Putin

This dynamic shifted when Putin came to power, but was really felt for real when Russia intervened in Syria in 2013, stopping Obama’s invasion plans, after the Tories refused David Cameron to follow Obama. Putin used diplomacy to pull things back from the brink.

Russia’s reward for this was the Maidan uprising in late 2013/14 and the ouster of Ukrainian President Viktor Yanukovich, which led to the current situation: The Donbass in limbo, Crimea now a part of Russia and the West fuming mad over having been stymied as Putin successfully played for time.

He planted a flag of defiance then and began making a stand. He’d make that stand stick in October 2015 when Russian armed forces began supporting Syrian Arab Army forces retaking territory from US-backed ISIS and Al-Qaeda forces.

At the same time, Russia built an edifice of relationships (with China, with India, with Turkey, etc.) which chipped away at the relationship between the US/UK and Europe. It exposed the fault lines between them using Europe’s growing dependence on energy imports and its ideological desire to raise itself above the US/UK and replace them; feeling their new Empire, the EUSSR, was inevitable.

Putin and Xi have exploited this European hubris and British/American ‘contrariness’ to deepen the divides between them, quite successfully over the years.

But now let’s look seriously at Ukraine. Europe wants out of the conflict. The Anglos are desperate for it. France’s Macron and Germany’s Scholz have tried to defuse the situation. Biden and the Brits have done nothing but enflame it with insanely hysterical propaganda.

They’ve even gone so far as to telegraph a false flag event to get the war they want while Russia steadfastly denies it has expansionist designs on Ukraine. Russia doesn’t want Ukraine. It’s now an albatross, economically, politically and socially.