FEB 25

· by harveyorgan · in Uncategorized · Leave a comment ·Edit

GOLD; $1886.30 DOWN $38.95

SILVER: $24.00 DOWN 64 CENTS

ACCESS MARKET: GOLD $1887.50

SILVER: $24.20

raid today in gold/silver due to options expiry at LBMA. The London OTC LBMA options expire Monday, Feb 28/2021

Bitcoin: morning price: $39371 UP 1015

Bitcoin: afternoon price: $38,790 UP 434

Platinum price: closing UP $3.00 to $1055.10

Palladium price; closing UP $26.20 at $2377.30

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filed//comex notices//JPMorgan notices filed 8/50

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,925.100000000 USD

INTENT DATE: 02/24/2022 DELIVERY DATE: 02/28/2022

FIRM ORG FIRM NAME ISSUED STOPPED

523 H INTERACTIVE BRO 7

657 C MORGAN STANLEY 15

661 C JP MORGAN 28

661 H JP MORGAN 23

686 C STONEX FINANCIA 8

905 C ADM 5 14

TOTAL: 50 50

MONTH TO DATE: 18,966

NUMBER OF NOTICES FILED TODAY FOR FEB. CONTRACT:50 NOTICE(S) FOR 5,000 OZ (0.1552 TONNES)

total notices so far: 18,966 contracts for 1,896,600 oz (58.99 tonnes)

SILVER NOTICES:

2 NOTICE(S) FILED TODAY FOR 10,000 OZ/

total number of notices filed so far this month 2024 : for 10,120,000 oz

GLD

WITH GOLD DOWN $38.95

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES AT THE GLD:

CLOSING INVENTORY :1029.32 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 64 CENTS:/:

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 5.510 MILLION OX FROM THE SLV

CLOSING INVENTORY: 546.052 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUMONGOUS 7819 CONTRACTS TO 155,661 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND WITH THIS HUGE LOSS IN OI, IT WAS ACCOMPANIED WITH OUR STRONG $0.15 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.15) BUT WERE SUCCESSFUL IN KNOCKING OUT SOME SILVER LONGS AS WE HAD A HUMONGOUS LOSS OF 4254 CONTRACTS ON OUR TWO EXCHANGES WITH ALL OF THE LOSS COMING FROM THE INITIATION OF SPREADER /TAS LIQUIDATION

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.110 MILLION OZ FOLLOWED BY TODAY’S NIL OZ QUEUE JUMP//NEW STANDING 10.120 MILLION OZ. V) HUGE SIZED COMEX OI LOSS//INITIATION OF SPREADER LIQUIDATION.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS -8103

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB:

TOTAL CONTACTS for 18 days, total contracts: : 14,478 contracts or 72.390 million oz OR 4.021 MILLION OZ PER DAY. (8043CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 14,478 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 72.39 MILLION OZ

.

LAST 10 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

SPREADING OPERATIONS

(/NOW SWITCHING TO SILVER) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAR.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 7819 WITH OUR STRONG $0.15 GAIN SILVER PRICING AT THE COMEX// THURSDAY THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 3565 CONTRACTS( 3565 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 4.1 MILLION OZ FOLLOWED BY TODAY’S NIL OZ QUEUE JUMP //NEW STANDING 10.120, MILLION OZ// .. WE HAD A HUGE SIZED LOSS OF 4254 OI CONTRACTS ON THE TWO EXCHANGES FOR 21.290 MILLION OZ//

WE HAD 2 NOTICES FILED TODAY FOR 10,000 OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG 6203 TO 611,953 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -7584 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE STRONG SIZED DECREASE IN COMEX OI CAME DESPITE OUR GAIN IN PRICE OF $17.35//COMEX GOLD TRADING/THURSDAY/.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION AS THE TOTAL GAIN ON OUR TWO EXCHANGES TOTALED 7776 CONTRACTS…

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR FEB AT 64.3 TONNES FOLLOWED BY TODAY’S 800 OZ QUEUE. JUMP //NEW STANDING: 58.995 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $17.35 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A STRONG SIZED LOSS OF 192 OI CONTRACTS (0.597 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6395 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 611,953.

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 192, WITH 6203 CONTRACTS DECREASED AT THE COMEX AND 6395 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 192 CONTRACTS OR 0.597TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (6395) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (6203,): TOTAL LOSS IN THE TWO EXCHANGES 192 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 64.30 TONNES WHICH FOLLOWS TODAY’S 800 OZ QUEUE JUMP //NEW STANDING 59.023 TONNES// 3) ZERO LONG LIQUIDATION ,4) STRONG SIZED COMEX OI. GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL//SOME SPREADER LIQUIDATION

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

59,689 CONTRACTS OR 5,968,900 OR 185.65 TONNES 18 TRADING DAY(S) AND THUS AVERAGING: 3316 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAY(S) IN TONNES: 185.65 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 185.85/3550 x 100% TONNES 5,21% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 185.65 TONNES//INITIAL

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GIGANTIC SIZED 7819 CONTRACTS TO 155,661 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 3565 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 3565 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3565 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 7819 CONTRACTS AND ADD TO THE 3565 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUMONGOUS SIZED LOSS OF 4254 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES. ALL OF THE LOSS DUE TO SPREADER LIQUIDATION/TAS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 21.290 MILLION OZ,

OCCURRED WITH OUR $0.15 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 21.48 PTS OR 0.63% //Hang Sang CLOSED DOWN 134.38 PTS OR 0.59% /The Nikkei closed UP 505.68 PTS or 1.95% //Australia’s all ordinaires CLOSED UP 0.28% /Chinese yuan (ONSHORE) closed UP 6.3148 /Oil DOWN TO 93.00 dollars per barrel for WTI and DOWN TO 98.36 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3148. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3132: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFF SHORE STRONGER/

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 6203 CONTRACTS AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS GOOD COMEX INCREASE OCCURRED DESPITE OUR STRONG GAIN OF $17.35 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (6395 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF FEB.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 6395 EFP CONTRACTS WERE ISSUED: ;: , & FEB. 0 APRIL:6395 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6395 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL TOTAL OF 192 CONTRACTS IN THAT 6395 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG COMEX OI LOSS OF 6203 CONTRACTS..

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR FEB (59.023),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

FEB 2022: 59.023 TONNES

THE BANKERS WERE UN SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $17.35) AND THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A SMALL LOSS OF .597 TONNES OF TOTAL OI, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR FEB (59.023 TONNES)…

WE HAD –7584 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NO DOUBT THE LOSS ON THE GOLD COMEX WAS DUE TO SOME SPREADER LIQUIDATION

NET LOSS ON THE TWO EXCHANGES 192 CONTRACTS OR 19200 OZ OR 0.597 TONNES

Estimated gold volume today: 224,306 ///FAIR

Confirmed volume yesterday: 455,034 contracts VERY STRONG

INITIAL STANDINGS FOR FEB ’22 COMEX GOLD //FEB 25

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | nil oz |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 50 notice(s)5000 OZ0.1552 TONNES |

| No of oz to be served (notices) | 10 contracts 1000 oz0.3110 TONNES |

| Total monthly oz gold served (contracts) so far this month | 18,966 notices1,896,600 OZ58.99 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

0 dealer deposit

No dealer withdrawal 0

0 customer deposit

total deposit: NIL oz

0 customer withdrawals

total withdrawals: nil oz

ADJUSTMENTS: 1// dealer to customer

a) 16,299.450 oz//JPMorgan

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEBRUARY.

For the front month of FEBRUARY we have an oi of 60, LOSING 687 contracts.

We had 695 contracts served upon yesterday, so we GAINED 8 contracts or an additional 800 oz will stand on this side of the pond looking for gold metal.

The month of March saw a GAIN OF 686 contracts and thus the OI standing is 4991.

April saw a LOSS of 12,589 contracts DOWN to 461,270.

June saw a gaIN of 5855 contracts up to 89,332 contracts

We had 50 notice(s) filed today for 5000 oz FOR THE FEB 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 23 notices were issued from their client or customer account. The total of all issuance by all participants equates to 50 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 8 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB /2021. contract month,

we take the total number of notices filed so far for the month (18,966) x 100 oz , to which we add the difference between the open interest for the front month of (FEB: 60 CONTRACTS ) minus the number of notices served upon today 50 x 100 oz per contract equals 1,897,600 OZ OR 59.023 TONNES the number of TONNES standing in this active month of FEB.

thus the INITIAL standings for gold for the FEB contract month:

No of notices filed so far (18,966) x 100 oz+ (60) OI for the front month minus the number of notices served upon today (50} x 100 oz} which equals 1,897,600 oz standing OR 59.023 TONNES in this active delivery month of FEB.

We GAINED 8 contracts or an additional 800 oz will stand for gold over here

TOTAL COMEX GOLD STANDING: 59.023 TONNES (HUGE FOR A FEBRUARY DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

157,392.690, oz NOW PLEDGED /HSBC 4.89 TONNES

123,963.792 PLEDGED MANFRA 3.86 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690 tonnes

262,049.904, oz JPM No 2 8.15 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonnes

Loomis: 18,615.429 oz

total pledged gold: 1,527,431.597 oz 47.50 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 32,528,644.909 OZ (1011.77 TONNES)

TOTAL ELIGIBLE GOLD: 15,202,228.847 OZ (472.85 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,326,416.062 OZ (538.92 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,798,985.0 OZ (REG GOLD- PLEDGED GOLD) 491.41 tonnes

END

FEBRUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//FEB 25

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 504,818.750 ozCNT |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 2CONTRACT(S)10,000 OZ) |

| No of oz to be served (notices) | 0 contracts (NIL oz) |

| Total monthly oz silver served (contracts) | 2024 contracts 10,120,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 0 deposits into the customer account

JPMorgan has a total silver weight: 182.9 million oz/348.321 million =52.51% of comex

ii) Comex withdrawals: 1

a)Out of CNT 504,868.750 oz

total withdrawal 504,818.750 oz

we had 2 adjustments//

dealer to customer account

CNT: 1,195,726.327 oz

customer to dealer

Brinks 647,659.720 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 80.564 MILLION OZ

TOTAL REG + ELIG. 348.321 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR FEBRUARY

silver open interest data:

FRONT MONTH OF FEB//2022 OI: 2 CONTRACTS LOSING 37 contracts on the day. We had 37 contracts served upon yesterday.

So we gained 0 contracts or an additional NIL oz will stand for silver on this side of the pond.

FOR MARCH WE HAD A LOSS OF 15,288 CONTRACTS DOWN TO 15,996 CONTRACTS.

WE HAVE ONE MORE READING DAY BEFORE FIRST DAY NOTICE.

APRIL HAD A 87 GAIN// CONTRACTS RISING TO 497

MAY HAD A GAIN OF 6910 CONTRACTS UP TO 116,198 contracts

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 2 for 10,000 oz

Comex volumes: 80,011// est. volume today//good/

Comex volume: confirmed THURSDAY: 204,046 contracts (OUT OF THIS WORLD)

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 2024 x 5,000 oz =. 10,120,000 oz

to which we add the difference between the open interest for the front month of FEB (2) and the number of notices served upon today 37 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2021 contract month: 2024 (notices served so far) x 5000 oz + OI for front month of FEB (2) – number of notices served upon today (2) x 5000 oz of silver standing for the FEB contract month equates 10,120,000 oz. .

We gained 0 CONTRACTS OR NIL ADDITIONAL oz of silver will stand at the comex. This should finalize the month of Feb for silver.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

FEB 25/WITH GOLD DOWN $38.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 24/WITH GOLD UP $17.35//A HUGE CHANGE AT THE GLD: 5.23 TONNES INTO THE GLD// IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1029.32 TONNES

FEB 23/WITH GOLD UP $2.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1024.09 TONNES

FEB 22/WITH GOLD UP $6.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1024.09 TONNES

FEB 18/WITH GOLD DOWN $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 17/WITH GOLD UP $29.50: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 16/WITH GOLD UP 414.60 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 15/WITH GOLD DOWN $12.70 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 14/WITH GOLD UP $27.20 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 11/WITH GOLD UP $4.50 A HUGE CHANGE IN GOLD IVNETORY AT THE GLD// A DEPOSIT OF 3.48 TONNES INTO THE GLD//INVENTORY RESTS AT 1019.44 TONES

FEB 10/WITH GOLD UP $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1015.96 TONNES

FEB 9/WITH GOLD UP $8.05//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1015.96 TONNES

FEB 8/WITH GOLD UP $5.95 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1015.96 TONNES

FEB 7/WITH GOLD UP $14.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.24 TONNES FROM THE GLD/////INVENTORY RESTS AT 1011.60 TONNES//

FEB 4/WITH GOLD UP $3.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.84 TONNES

FEB 3/WITH GOLD DOWN $5.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 1016.59 TONNES

FEB 2/WITH GOLD UP $7.95//A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.78 TONES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1018.04 TONNES

FEB 1/WITH GOLD UP $5.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 31/WITH GOLD UP $10.10//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 28/WITH GOLD DOWN $8.30//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

JAN 27/WITH GOLD DOWN $36.15//ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES INTO THE GLD.//INVENTORY RESTS AT 1014.26 TONNES

JAN 26/WITH GOLD DOWN $21.60 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES INTO THE GLD///INVENTORY RESTS AT 1013.10 TONNES

JAN 25/WITH GOLD UP $10.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1008.45 TONNES

JAN 24/WITH GOLD UP $10.10 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: AN UNBELIEVABLE DEPOSIT OF 27.59 TONNES INTO THE GLD//INVENTORY RESTS AT 1008.45 TONNES

CLOSING INVENTORY FOR THE GLD//1029.32 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 25/WITH SILVER DOWN 64 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.510 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 546.052 MILLION OZ/

FEB 24/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ

FEB 23/WITH SILVER UP 22 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ//

FEB 22/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 350,000 OZ INTO THE SLV///INVENTORY RESTS AT 551.597 MILLION OZ//

FEB 18/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.017 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 551.227 MILLION OZ

FEB 17/WITH SILVER UP 31 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.402 MILLION OZ//INVENTORY RESTS AT 550.210 MILLION OZ/

FEB 16/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.808 MILLIONOZ

FEB 15/WITH SILVER DOWN 46 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.808 MILLION OZ//

FEB 14/WITH SILVER UP 49 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.235 MILLION OZ INTO THES LV////INVENTORY RESTS AT 547.808 MILLION OZ

FEB 11/WITH SILVER DOWN 18 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ///

SLV/FEB 10/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 9/WITH SILVER UP 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 8/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.143 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 7/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.218 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 541.430 MILLION OZ/

FEB 4/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 539.212 MILION OZ

FEB 3/WITH SILVER DOWN 35 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT539.212 MILLION OZ//

FEB 2/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.411 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 539.212 MILLION OZ/

FEB 1/WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.801 MILLION OZ

JAN 31/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FORM THE SLV.//INVENTORY RESTS AT 533.801 MILLION OZ//

JAN 28/WITH SILVER DOWN 36 CENTS : NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 27/WITH SILVER DOWN $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 26/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 535.003 MILLION OZ//

JAN 25/WITH SILVER UP 10 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.311 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 535.003 MILLION OZ/

.JAN 24/WITH SILVER DOWN 48 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.8 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 532.692 MILLION OZ//.

SLV FINAL INVENTORY FOR TODAY: 546.052 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

end

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS

The War On Cash Entering Bold New Phase

THURSDAY, FEB 24, 2022 – 10:20 PM

Authored by James Rickards via DailyReckoning.com,

With so much news about Ukraine, inflation, massive government spending and exploding deficits, it’s easy to overlook the ongoing war on cash. That’s a mistake because it has serious implications not only for your money, but for your privacy and personal freedom, as you’ll see today.

The war on cash is a global effort being waged on many fronts. My view is that the war on cash is dangerous in terms of lost privacy and the risk of government confiscation of wealth.

Governments always use money laundering, drug dealing and terrorism as excuses to keep tabs on honest citizens and deprive them of the ability to use money alternatives such as physical cash, gold and, these days, cryptocurrencies.

The real burden of the war on cash falls on honest citizens who are made vulnerable to wealth confiscation through negative interest rates, loss of privacy, account freezes and limits on cash withdrawals or transfers.

The enemies of cash promote the ease and convenience of digital payments. Of course, there’s no denying that digital payments are certainly convenient. I use them myself in the forms of credit and debit cards, wire transfers, automatic deposits and bill payments. I’m sure you do too.

But the surest way to lull someone into complacency is to offer a “convenience” that quickly becomes habit and impossible to do without. The convenience factor is becoming more prevalent, and consumers are moving from cash to digital payments just as they moved from gold and silver coins to paper money a hundred years ago.

One survey revealed that more than a third of Americans and Europeans would have no problem at all giving up cash and going completely digital. Specifically, the study showed 34% of Europeans and 38% of Americans surveyed would prefer going cashless.

But in reality, the so-called “cashless society” is just a Trojan horse for a system in which all financial wealth is electronic and represented digitally in the records of a small number of megabanks and asset managers.

Once that is achieved, it will be easy for state power to seize and freeze the wealth, or subject it to constant surveillance, taxation and other forms of digital confiscation like negative interest rates.

They can’t do that as long as you can go to your bank and withdraw your cash. That’s the key. In other words, it’s much easier for them to control your money if they first herd you into a digital cattle pen. That’s their true objective and all the other reasons are just a smoke screen.

That’s what they won’t tell you.

Elites know that they can’t ram their unpopular agendas through in normal times. The global elites and deep state actors always have a laundry list of programs and regulations they can’t wait to put into practice. They know that most of these are deeply unpopular and they could never get away with putting them into practice during ordinary times.

Yet when a crisis hits, citizens are desperate for fast action and quick solutions. The elites bring forward their rescue packages but then use these as Trojan horses to sneak their wish lists inside. That’s what we’re seeing.

The USA Patriot Act passed after 9/11 is a good example. Some counterterrorist measures were needed, of course. But the Treasury had a long-standing wish list involving reporting cash transactions and limiting citizens’ ability to get cash.

They plugged that wish list into the Patriot Act and we’ve been living with the results ever since, even though 9/11 is long in the past.

Cash prevents central banks from imposing negative interest rates because if they did, people would withdraw their cash from the banking system.

If they stuff their cash in a mattress, they don’t earn anything on it; that’s true. But at least they’re not losing anything on it. Once all money is digital, you won’t have the option of withdrawing your cash and avoiding negative rates. You will be trapped in a digital pen with no way out.

What about moving your money into cryptocurrencies like Bitcoin?

Let’s first understand that governments enjoy a monopoly on money creation, and they’re not about to surrender that monopoly to digital currencies like Bitcoin. Libertarian supporters of cryptos celebrate their decentralized nature and lack of government control. Yet their belief in the sustainability of powerful systems outside government control is naïve.

Blockchain does not exist in the ether (despite the name of one cryptocurrency), and it does not reside on Mars. Blockchain depends on critical infrastructure including servers, telecommunications networks, the banking system and the power grid, all of which are subject to government control.

You need to understand that reality.

The good news is that cash is still a dominant form of payment in many countries including the U.S. The problem is that as digital payments grow and the use of cash diminishes, a “tipping point” is reached where suddenly it makes no sense to continue using cash because of the expense and logistics involved.

Once cash usage shrinks to a certain point, economies of scale are lost and usage can go to zero almost overnight. Remember how music CDs disappeared suddenly once MP3 and streaming formats became popular?

That’s how fast cash can disappear.

Once the war on cash gains that kind of momentum, it will be practically impossible to stop.

Besides the loss of privacy, other dangers from the cashless society arise from the fact that digital money, transferred by credit or debit cards or other electronic payments systems, is completely dependent on the power grid. If the power grid goes out due to storms, accidents, sabotage or cyberattacks, our digital economy will grind to a complete halt.

The time to protect yourself is now. The best way is to keep a portion of your wealth outside of the banking system.

That’s why it’s a good idea to keep some of your liquidity in paper cash (while you can) and gold or silver coins. The gold and silver coins in particular will be money good in every state of the world.

That’s why I’m always saying that savers and those with a long-term view should get physical gold now while prices are still attractive and while they still can.

I strongly recommend that you own physical gold (and silver). I recommend you allocate 10% of your investable assets to gold. If you really want to be aggressive, maybe 20%. But no more.

Just make sure you don’t store it in a bank, because it would be subject to confiscation. That defeats the whole purpose of having this sort of protection in the first place.

I hold a significant portion of my wealth in nondigital form, including real estate, fine art and precious metals in safe, nonbank storage. That’s not because I’m paranoid or a fanatic prepper. I just think it’s prudent in these times.

I strongly suggest you do the same. The cashless society could be here quicker than you think.

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

Chris Powell on gold rigging!

(Chris Powell)

Can gold market rigging get more obvious? Yes, and probably will tomorrow

Submitted by admin on Thu, 2022-02-24 12:03Section: Daily Dispatches

12:10p ET Thursday, February 24, 2022

Dear Friend of GATA and Gold:

Today’s “market” action in gold and silver evokes for your secretary/treasurer, and maybe a few others, a GATA dispatch from 10 years ago. An excerpt from that dispatch is below.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

May 30, 2012

https://www.gata.org/node/11426

If the Northern Hemisphere was destroyed in a nuclear war, the Federal Reserve, JPMorganChase, and HSBC would get some brokers to Sydney, Rio de Janeiro, and Johannesburg to sell gold futures massively and drive the price down by at least 5%.

Kitco market analyst Jon Nadler would crawl out from the rubble and opine to the cockroaches that the gold price had fallen because so many gold buyers had been killed, as he always had predicted would happen.

CPM Group’s Jeff Christian would telephone New Zealand not to worry because he was flying down with reams of gold-colored paper that would work just as well in Wellington as it did in New York as long as nobody asked what was behind it.

And the World Gold Council would console itself with whatever high-fashion models could be found wearing nose rings in French Polynesia.

But with London and New York razed, at least we’d be spared more contrived rationalizations about the strange market action from the Financial Times and Wall Street Journal.

Monetary metals investors should understand that, as geopolitical analyst Jim Rickards somehow was allowed to say on CNBC three years ago, “When you own gold you’re fighting every central bank in the world.”

It’s them or humanity, slavery or freedom. Get used to it. Besides, we’re winning.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

Your weekend reading material

Alasdair Macleod…

Alasdair Macleod: How Ukraine fits into the global jigsaw

Submitted by admin on Thu, 2022-02-24 20:45Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, February 24, 2022

Ukraine is part of a far bigger geopolitical picture.

Russia and China want U.S. hegemonic influence in the Eurasian continent marginalized. Following defeats for U.S. foreign policy in Syria and Afghanistan and following Brexit, Russian President Vladimir Putin is driving a wedge between America and the non-Anglo-Saxon European Union.

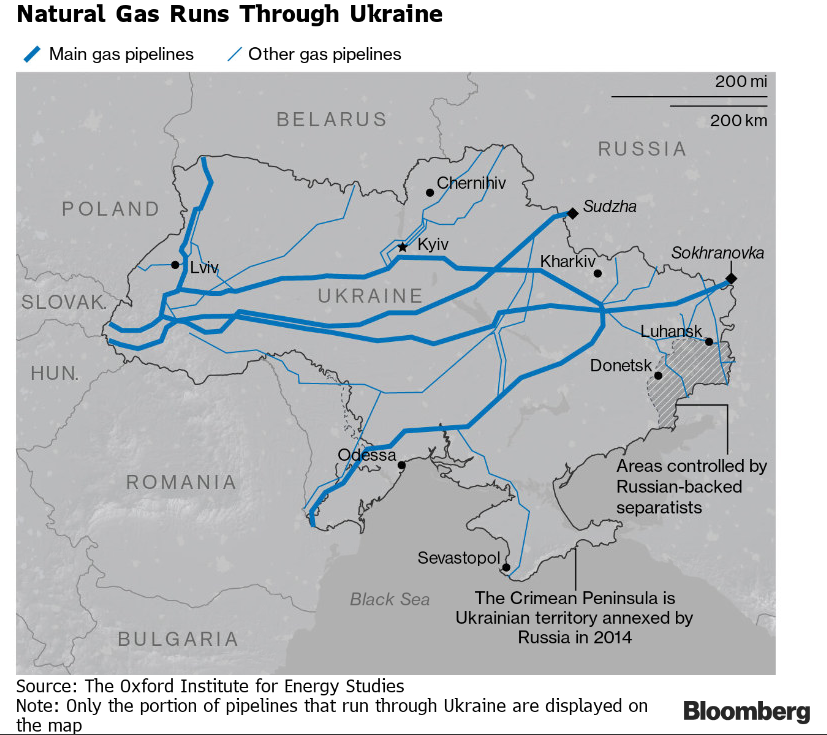

Due to global monetary expansion, rising energy prices are benefiting Russia, which can afford to squeeze Germany and other EU states dependent on Russian natural gas. The squeeze will stop only when America backs off.

Being keenly aware that its dominant role in NATO is under threat, America has been trying to escalate the Ukraine crisis to suck Russia into an untenable occupation. Putin won’t fall for it.

The danger for us all is not a boots-on-the-ground war — that’s likely to involve only the pre-emptive attacks on military installations Putin initiated last night — but a financial war for which Russia is fully prepared.

Both sides probably do not know how fragile the eurozone banking system is, with both the European Central Bank and its national central bank shareholders already having liabilities greater than their assets. In other words, rising interest rates have broken the euro system, and an economic and financial catastrophe on its eastern flank will probably trigger its collapse.

The developing tension over Ukraine is part of a bigger picture — a struggle between America and the two Eurasian hegemons, Russia and China. The prize is ultimate control over Mackinder’s World Island.

Halford Mackinder is acknowledged as the founder of geopolitics: the study of factors such as geography, geology, economics, demography, politics, and foreign policy and their interaction. His original paper was entitled “The Geographical Pivot of History,” presented at the Royal Geographical Society in 1905, in which he first formulated his Heartland Theory, which extended geopolitical analysis to encompass the entire globe.

In this and a subsequent paper (“Democratic Ideals and Reality: A Study in the Politics of Reconstruction,” 1919) he built on his Heartland Theory, from which his famous quote has been passed down to us: “Who rules East Europe commands the World Island” — Eurasia. “Who rules the World Island rules the world.”

Josef Stalin was said to have been interested in this theory, and while it is not generally admitted, the leaders and administrations of Russia, China, and America are almost certainly aware of Mackinder’s theory and its implications. …

… For the remainder of the analysis:

end

Jim Rickards: The dollar is becoming a victim of its own success

Submitted by admin on Thu, 2022-02-24 21:25Section: Daily Dispatches

By James G. Rickards

The Daily Reckoning, Baltimore

Tuesday, February 22, 2022

America’s most powerful weapon of war does not shoot, fly, or explode. It’s not a submarine, plane, tank, or laser.

America’s most powerful strategic weapon today is the dollar.

The United States uses the dollar strategically to reward friends and punish enemies. The use of the dollar as a weapon is not limited to trade wars and currency wars, although the dollar is used tactically in those disputes.

The dollar can be used for regime change by creating hyperinflation, bank runs, and domestic dissent in countries targeted by the U.S. The U.S. can depose the governments of its adversaries, or at least blunt their policies without firing a shot. …

… For the remainder of the analysis:

https://dailyreckoning.com/the-dollar-a-victim-of-its-own-success/

end

4.OTHER GOLD/SILVER COMMENTARIES

Special thanks to Doug C for providing this for us:

| douglas cundey |  10:32 AM (6 minutes ago) 10:32 AM (6 minutes ago) | ||

I now see the atheists that control the banking system also control the silver institute

END

5.OTHER COMMODITIES/EDIBLE OILS/HUGE PRICE INCREASES//

6.CRYPTOCURRENCIES

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.3148

OFFSHORE YUAN: 6.3132

HANG SANG CLOSED DOWN 134.38 PTS OR 0.59%

2. Nikkei closed UP 505.68 PTS O 1.95%

3. Europe stocks ALL GREEN

USA dollar INDEX DOWNP TO 96.91/Euro RISES TO 1.1216-

3b Japan 10 YR bond yield: RISES TO. +.208/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 115.58/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 93.00 and Brent: 98.36–

3f Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE CLOSED UP// OFF- SHORE UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.230%/Italian 10 Yr bond yield FALLS to 1.832% /SPAIN 10 YR BOND YIELD FALLS TO 1.20%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.60: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.55

3k Gold at $1890.00 silver at: 24.06 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble UP 168/100 in roubles/dollar;ROUBLE AT 82.73

3m oil into the 93 dollar handle for WTI and 98 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 115.58 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9273– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0339 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.005 UP 4 BASIS PTS

USA 30 YR BOND YIELD: 2.314 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.79

Futures Recover Overnight Losses After Torrid Thursday Rally As Uneasy Calm Returns

FRIDAY, FEB 25, 2022 – 07:57 AM

After yesterday’s furious gamma-squeeze rally, U.S. stock futures were slightly lower on the day, although near the overnight session highs as the ongoing Ukraine conflict and impact of Western sanctions continue to drive risk; sentiment was boosted after the Kremlin said that Ukraine’s neutrality offer is a move “toward positive” and following reports that China’s president Xi held a phone call with Putin who said Russia is willing to conduct high-level negotiations with Ukraine. S&P futures were down 10 points to 0.25% at 7:30am, after paring earlier declines of more than 1%, with Nasdaq futures down -0.15% and Dow futures down 0.4%. Europe’s Stoxx Europe 600 was in the green, and oil was steady after Bloomberg reported that oil importers in China are briefly pausing new seaborne purchases as they assess the potential implications of handling the shipments following the Ukraine invasion. Gold was steady, while Brent crude reached $100 a barrel and Treasuries rose.

In the latest developments, Ukraine’s president Zelensky said Moscow-led forces were continuing attacks on military and civilian targets on the second day of their invasion. Leaders from the North Atlantic Treaty Organization will hold virtual talks on the alliance’s next steps starting at 3 p.m. in Brussels. Meanwhile, President Joe Biden imposed stiffer sanctions on Russia, promising to inflict a “severe cost on the Russian economy” that will hamper its ability to do business in foreign currencies after Moscow-led forces attacked military targets in Ukraine, triggering the worst security crisis in Europe since World War II. China urged Russia and Ukraine to negotiate to address problems, according to Chinese state TV. Here is a full recap of the latest Ukraine developments:

- There were reports of heavy explosions rocking the Ukrainian capital of Kyiv and US Senator Rubio tweeted it appeared that at least three dozen missiles were fired at the Kyiv are in 40 minutes, while Ukrainian Foreign Minister Kuleba confirmed Russian rockets fired at Kyiv and President Zelensky also noted Russia resumed missile strikes at 04:00 local time/02:00GMT. Russia has not undertaken missile strikes on Kyiv, according to Russian press citing a source in the Defence Ministry.

- There is currently gunfire in Kyiv with Russians in the City, according to a reporter (08:45GMT/03:45EST)

- Gunfire has been heard near the government quarter of Kyiv, Ukraine, via LBC News (09:09GMT/04:09EST)

- Ukrainian military vehicles seized by Russian troops wearing Ukrainian uniforms, heading for Kyiv, defense official says – UNIAN, cited by BNO News.

- Russian paratroopers take control of Chernobyl nuclear power plant, according to the Ministry of Defence cited by Sputnik. Additionally, Ukraine nuclear agency says it is seeing higher radiation levels in Chernobyl; note, Sky News reports that the increase is insignificant and is due to military vehicles moving around the reactor.

- Ukraine President adviser says that Ukraine wants peace, if negotiations are still possible, they should be undertaken. Subsequently, Russian Foreign Minister Lavrov says that Ukraine President Zelenskiy is “lying” when he says he is prepared to discuss the neutral status of Ukraine; however, the Kremlin says it has taken note of Kyiv’s willingness to discuss neutral status; will need to analyze this.

- Ukraine President Zelensky says the Russian assault is like a repeat of WW2, accuses Europe of an insufficient reaction, Europe can still stop the Russian aggression if they act quickly.

- Ukrainian President Zelensky has proposed Russian President Putin joins him at the negotiating table, according to Ria.

In premarket trading, Block jumped after fourth-quarter sales beat consensus, while Coinbase dropped after warning that trading volume will decline in the first quarter. Zscaler slumped 13% after the security software company’s second-quarter results failed to live up to the most optimistic expectations, even though they beat estimates. Analysts slashed their price targets, including a new Street-low at Barclays. Here are some of the other notable U.S. premarket movers today:

- Block Inc. (SQ US) shares climb 15% in U.S. premarket trading after the firm posted fourth-quarter sales that beat Street consensus. Analysts say the results are a relief, supported by “impressive” Cash App figures.

- Coinbase Global Inc. (COIN US) shares were 1.6% lower in premarket trading after the biggest U.S. cryptocurrency exchange cautioned that trading volume will decline in the first quarter.

- Etsy (ETSY US) shares are up about 18% in premarket trading, after the e- commerce company reported fourth-quarter results that featured better-than-expected revenue and gross merchandise sales. It also gave a forecast.

- Beyond Meat (BYND US) shares dropped 10% in premarket as analyst questioned its profitability outlook and pricing strategy after the maker of plant-based foods forecast sales that missed market expectations.

- KAR Auction Services (CVNA US) climbs 50% in U.S. premarket after agreeing to sell its Adesa U.S. physical auction business to Carvana for $2.2 billion in cash. Truist Securities sees positive implications for both stocks.

- Farfetch (FTCH US) shares rally 27% in premarket trading after co. posted a smaller-than-expected 4Q loss.

A prolonged conflict could deliver a major blow to global markets and slow the normalization of central bank policy that’s expected this year. Wall Street strategists cut their forecasts on European equities on concern that the war in Ukraine will hurt economic growth, with Goldman Sachs Group Inc. expecting virtually no full-year returns.

A the same time, disruptions of raw materials and food could stoke already-high prices and heap pressure on central banks to act faster to curb inflation. Russia remains a commodity powerhouse and Ukraine is a major grain exporter. Markets still see around six quarter-point increases by the Federal Reserve, but bets on other central bank’s hiking cycles have been pared in recent days.

“This conflict implies a further deterioration of the already tricky growth-inflation trade-offs central banks have been facing, making the upcoming decisions particularly hard,” Silvia Dall’Angelo, senior economist at the international business of Federated Hermes, wrote in a note to clients. “Downside growth risks from the geopolitical backdrop mean that they are likely to proceed gradually and cautiously.”

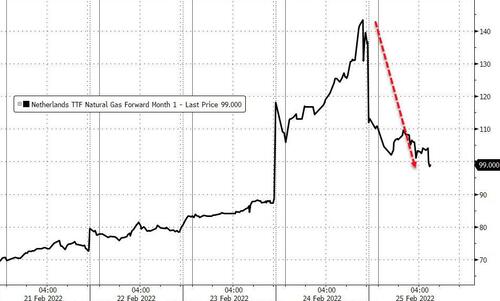

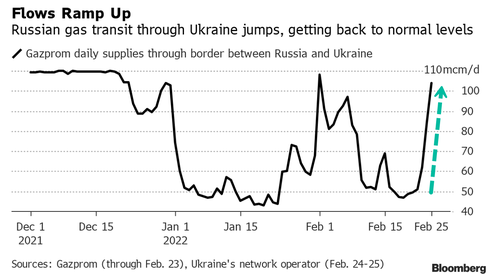

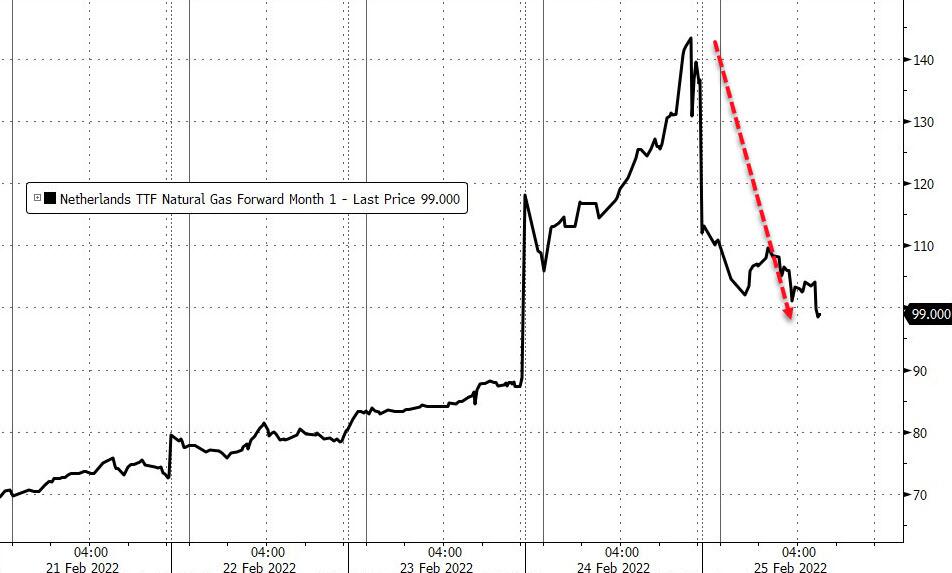

Penalties by the U.S. and its allies spared Russia’s oil exports and avoided blocking access to the Swift global payment network. With flows of natural gas returning to Europe, prices reversed a record-breaking rally with the benchmark contract down as much as 28%.

European stocks climbed as investors bought the dip after a volatile week led by developments on the Ukrainian front. Stocks trade at session highs after the Kremlin says that Ukraine’s neutrality offer is a move “toward positive” while oil slips to session low. U.S. futures decline. Euro Stoxx 50 rallies 1.2%. FTSE 100 outperforms, adding 1.8%, IBEX lags, adding 0.9%. CAC 40 up 1.3%. Utilities, real estate and food & beverages are the strongest sectors. Russia’s MOEX index rebounds, rising ~15%. Here are some of the biggest European movers today:

- European shares in sectors that were beaten down by Russia risk on Thursday rebound, with travel and basic resource stocks among the top gainers, as well as banks with exposure to eastern Europe.

- Bank Polska Kasa Opieki +14%, Dino Polska +7.3%, Polymetal International +7.5%, Wizz Air +5.8%

- The European utility sector leads gains among subindexes on the Stoxx 600, gaining about 5%, after European natural gas prices halted their rally rally, as Russian flows to the continent ramped up.

- Rightmove shares rise as much as 7.4% after the online property listings firm reported FY revenue growth of 48% from a year earlier. The results show encouraging momentum into 2022, Numis says.

- Pearson has its biggest gain in almost a year, rising 11% after results. Goldman Sachs notes the education publisher’s adjusted operating profit for FY22 was in line with market expectations.

- Freenet rises as much as 6.7% after results, the most since May, as analysts see positive profitability updates despite revenue weakness.

- Vallourec climbs as much as 20% after the French steel-pipe maker gave guidance that Oddo BHF calls “reassuring” in spite of incidents at a Brazil mine.

- Valeo falls as much as 12% in Paris after the French company set out targets for this year and 2025, with analysts noting 2022 guidance came in below expectations.

- BASF drops as much as 4.9% in Frankfurt after adjusted Ebit missed consensus and results show a squeeze on margins, Berenberg said.

- Swiss Re plunges as much as 8.4% after reporting results that missed analyst estimates. The insurer also proposed new targets that “don’t seem supportive enough,” Citi writes.

- Casino slumps as much as 17% to its lowest level in more than three decades after the French grocer reported FY results that Jefferies says showed “no progress” on deleveraging.

An uneasy calm returned to Asia’s stock markets on Friday, as investors assessed the fallout of Russia’s invasion of Ukraine and the outlook for China’s tech sector. The MSCI Asia Pacific Index climbed as much as 1.2%, rallying from its worst drop in a year on Thursday. Weaker-than-expected U.S. sanctions on Russia supported market sentiment, helping lift tech and industrial shares. China’s tech stocks advanced even after Alibaba announced the slowest revenue growth since it went public. Benchmarks in Japan and India were among the top performers. India’s Sensex turned from the biggest loser in Asia to the biggest winner on Friday. Hong Kong’s Hang Seng Index dropped as the city deals with record Covid-19 cases. Asian equities “showed signs of excessive drops, so today’s rise appears to be a technical rebound,” Seo Jung-hun, a strategist at Samsung Securities, said by phone. “Markets will continue to face volatility as Russia-sparked risks, the Fed’s policy tightening and inflation issues still persist.” Federal Reserve Governor Christopher Waller said a half percentage-point increase in U.S. interest rates next month could be justified, although the Ukraine conflict has added to uncertainty. The Asian stock benchmark is set for its worst week this month, down almost 4%, and remains close to entering a bear market. Geopolitical risks, regulatory concerns for Chinese private enterprises and a relatively slower pace of earnings growth compared with the rest of the world are all weighing on sentiment

Japanese equities climbed, sealing their first gain in six sessions, as blue chips led the charge following a late U.S. rally from the recent selloff in anticipation of Russia’s invasion of Ukraine. Electronics makers and telecoms were the biggest boosts to the Topix, which rose 1%. Tokyo Electron and SoftBank Group were the largest contributors to a 2% rise in the Nikkei 225. The yen retraced some of its 0.5% loss against the dollar overnight. “Expectations are spreading that the pace of rate hikes will be slowed down in the U.S. and Europe, considering the impact the Ukraine situation will have on the economy,” said Nobuhiko Kuramochi, a market strategist at Mizuho Securities

In rates, treasuries were slightly cheaper across the curve, with yields higher by 1bp to 1.5bp from Thursday’s session close. U.S. 10-year yield around 1.975%, cheaper by 1bp on the day with bunds lagging a further 1bp following data including France CPI beat, while Estoxx rally 1.5%; gilts outperform by around 2bp vs. Treasuries.

Treasuries pared an advance after Federal Reserve Governor Christopher Waller said a half percentage-point rate increase may be justified if economic data remain hot. European benchmark bonds traded steady to slightly lower. Gilts gained, led by the belly of the curve; Bank of England’s Huw Pill speaks later, with the pace of tightening in focus. IG dollar issuance slate empty so far; borrowers stepped away from debt sales Thursday leaving weekly total around $18b vs. $25b expected. German bunds bear-flatten on the back of a stronger-than-expected French CPI print, while money markets price as much as 42bps of ECB tightening in December, an increase of 5bps compared to Thursday.

In FX, the Bloomberg Dollar Spot Index was little changed as the greenback traded mixed versus its Group-of-10 peers, though most currencies were confined to narrow ranges relative to yesterday’s moves. The Australian and New Zealand dollars led G-10 gains on short covering after Thursday’s plunge; The yen was also higher while the euro fell a third consecutive day to trade below $1.12 and the pound erased an early advance. Hedging costs in the major currencies turned south early Friday, but investors aren’t ready to shift bias into risk-on exposure. French consumer prices rose 4.1% in February from a year earlier versus 3.3% in January. That’s the strongest reading since the data series started in 1997. Economists had forecast a 3.7% advance. Currencies from the European Union’s east weakened against the euro and the dollar, but were far from levels reached Thursday. A gauge of one-week implied volatility in the dollar against the Taiwan dollar jumped to a six-month high on Friday while the Taiwan dollar slid to the weakest since October in the spot market. The conflict in Ukraine may raise the risk premium for China and Taiwan over the medium term, according to Morgan Stanley.

In commodities, Brent trades around $99, while WTI slips below $93. Spot gold rises roughly $6 to trade near $1,910/oz. European natural gas prices halt a record-breaking rally. Benchmark futures fell as much as 28%, after four consecutive days of gains. Most base metals trade in the red; LME aluminum falls 2.5%, underperforming peers. LME lead outperforms

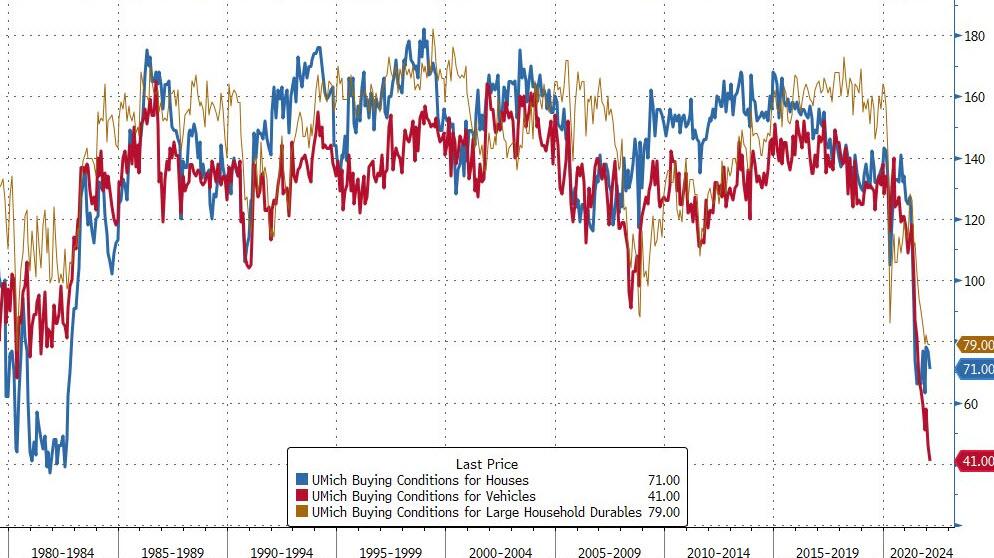

Looking at the day ahead, data highlights from the US include the personal income and personal spending data for January, preliminary durable goods orders and core capital goods orders for January, pending home sales for January, and the final University of Michigan consumer sentiment index for February. In Europe, we’ll also get the preliminary French CPI reading for February, and the Euro Area’s economic sentiment indicator for February.

Market Snapshot

- S&P 500 futures down 1.1% to 4,237.75

- MXAP up 1.0% to 181.44

- MXAPJ up 0.8% to 593.50

- Nikkei up 1.9% to 26,476.50

- Topix up 1.0% to 1,876.24

- Hang Seng Index down 0.6% to 22,767.18

- Shanghai Composite up 0.6% to 3,451.41

- Sensex up 2.5% to 55,878.05

- Australia S&P/ASX 200 up 0.1% to 6,997.81

- Kospi up 1.1% to 2,676.76

- STOXX Europe 600 up 0.8% to 442.68

- German 10Y yield little changed at 0.16%

- Euro down 0.2% to $1.1172

- Brent Futures up 0.9% to $99.98/bbl

- Gold spot up 0.3% to $1,909.09

- U.S. Dollar Index little changed at 97.18

Top Overnight News from Bloomberg

- Federal Reserve officials stuck to their resolve to raise interest rates next month despite uncertainty posed by Russia’s invasion of Ukraine, with at least one policy maker considering a half-point move

- Out of 18 potential red flags in Citi’s global Bear Market checklist, only seven are currently waving, far fewer than before bear markets of 2000 and 2007, strategists led by Beata Manthey wrote in a note. In Europe, the number of danger signs is only five, they said

- China’s Politburo vowed to strengthen macroeconomic policies to stabilize the economy this year, suggesting more support could be on the cards to boost growth ahead of a key leadership meeting later this year

- Russia still has about $300 billion of foreign currency held offshore – – enough to disrupt money markets if it’s frozen by sanctions or moved suddenly to avoid them

- China’s central bank ramped up its short-term liquidity injection in the banking system, providing support just as global markets are roiled by geopolitical tension

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks mostly gained after the firm rebound on Wall St. ASX 200 was capped amid a slew of earnings and with outperformance in tech offset by weakness in miners and financials. Nikkei 225 outperformed and reclaimed the 26k status with exporters underpinned by a more favourable currency. KOSPI gained with index heavyweight Samsung Electronics underpinned as it launched global sales of its flagship smartphone and latest tablet which have attracted record pre-orders. Hang Seng and Shanghai Comp. were mixed with the mainland underpinned after the PBoC boosted its daily liquidity operation which resulted in the biggest weekly cash injection in more than two years. although Hong Kong was constrained by losses in the energy majors and with financials subdued amid pressure in HSBC shares and after China Communist Party inspections on financial institutions.

Top Asian News

- China Pledges Stronger Economic Policies to Stabilize Growth

- China Leaves Russia’s War Off Front Pages as Xi Stays Silent

- Currency Traders Remain Vigilant Even as Hedging Costs Retreat

- Asian Stocks Gain as China Tech, India Rebound; Hong Kong Drops

European bourses are firmer and back in proximity to initial best levels after losing traction shortly after the cash open, Euro Stoxx 50 +1.3%; FTSE 100 +1.9% outperforms amid Basic Resources strength. US futures are lower across the board, ES -0.9%, after yesterday’s significant intra-day reversal to close positive; albeit, action has been rangebound within the European morning. US SEC’s EDGAR feed is reportedly down; fillings cannot be made. In Europe, sectors are all in the green featuring noted outperformance in Utilities and Basic Resources, Energy remains firmer in-spite of the crude benchmarks pullback

Top European News

- Wall Street Cuts European Stock Targets as War Prompts Outflows

- U.K. Takes Aim at Russia’s Opaque Embrace of London Property

- UBS Triggers Margin Calls as Russia Bond Values Cut to Zero

- What to Watch in Commodities: Ukraine Impact Roiling Markets

In FX, Aussie regroups alongside broad risk sentiment and rebound in Aud/Nzd cross amidst mixed NZ consumption and trade data – Aud/Usd near 0.7200 vs sub-0.7100 low yesterday. Buck bases after abrupt reversal from new 2022 highs in DXY terms and residual rebalancing may underpin alongside underlying safe haven bid – index above 97.000 again vs 96.770 low and 97.740 y-t-d best. Rouble supported by ongoing CBR intervention via higher repo auction cap – Usd/Rub around 84.000 compared to almost 90.000 record peak.

Yen and Gold off best levels, but both retain elements of safety premium – Usd/Jpy circa 115.35 and Xau/ Usd

hovering above Usd 1900/oz

In commodities, WTI and Brent have continued to pull back after overnight consolidation, Brent April notably below USD 99.00/bbl

vs USD 101.99/bbl highs. Focus remains firmly on geopolitics (see section above) while participants are also attentive to next week’s OPEC+ meeting. Japan’s Industry Minister said they will appropriately deal with an oil release from national reserves in cooperation with relevant countries and the IEA. Spot gold is rangebound after an initial move higher failed to gather steam and hit resistance at USD 1922/oz. Goldman Sachs recently commented that the rally for gold has a lot further to go on the situation in Ukraine and prices and that prices could reach as high at USD 2,350/oz if there is a build in demand for ETF.

Geopolitical updates

- US Senior US administration official said the US still has room to further tighten sanctions if Russian aggression accelerates further and is keeping the option open to impose import-export controls on less advanced mainline chips such as those used in the Russian auto industry.

- European Commission President von der Leyen said steps agreed by EU leaders include financial sanctions and they are targeting 70% of the Russian banking market, as well as key state owned companies including defence. Furthermore, the export ban will impact Russia’s oil sector by making it impossible to upgrade refineries and EU is limiting Russia’s access to key technologies such as semiconductors.

- EU Council President Michel says they are urgently preparing additional sanctions against Russia, via AFP; subsequently, a German gov’t spokesperson says a discussion of third sanctions package against Russia is in its early stages.

- French President Macron said EU sanctions will be followed by French national sanctions on certain people which are to be announced later, while they will offer EUR 300mln of aid to Ukraine and military equipment, as well as target Belarus for penalties.

- Russian Central Bank said it will provide any support needed for sanctions-hit banks and that banks have been well prepared in advance, while Ukraine’s Central Bank banned operations with RUB and BYR, as well as banned banks from making payments to entities in Russia and Belarus.

- Russia may retaliate for UK ban on Aeroflot flights to Britain, according to Tass citing the aviation authority; subsequently, Russia banned London registered craft from its airspace.

- Russian Parliamentary Upper Chamber speaker says that Russia has prepared sanctions to hit the weak points of the West, according to Interfax.

- Australian PM Morrison announced the nation is to impose further sanctions on Russian individuals and said it is unacceptable that China is easing trade restrictions with Russia at this time. Taiwan will join democratic countries to put sanctions on Russia for invasion of Ukraine and Japanese PM Kishida said they will immediately impose sanctions in Russia in three areas including the financial sector and military equipment exports, while Russia’s envoy to Japan later said there will be a serious Russian response to Japanese sanctions.

- UK Defence Minister Wallace says we would like to cut Russia off from SWIFT; French Finance Minister Le Maire says the option of cutting Russia off from SWIFT remains an option, but it a last resort.

- India is reportedly exploring setting up INR trade accounts with Russia to soften the blow on India from Russian sanctions, according to Reuters sources.

Central Banks

- Fed’s Waller (voter) said it is too soon to judge how Ukraine conflict will impact the world or US economy and concerted action to rein in inflation is needed. Waller said rates should be raised by 100bps by mid-year and there is a strong case for a 50bps hike in March if incoming data indicates economy is still exceedingly hot, but added it is possible a more modest tightening is appropriate in wake of Ukraine attack , while he also stated the Fed should start trimming the balance sheet no later than the July meeting, according to Reuters.

- ECB’s Lane said there would be a significant increase to 2022 inflation forecast amid the Ukraine crisis but hinted at inflation below target at end of horizon according to Reuters sources; Lane presented several scenarios: Mild scenario: no impact to EZ GDP; seen as unlikely; Middle scenario: 0.3-0.4ppts shaved off EZ GDP; Severe scenario: EZ hit by almost 1ppt. Note, sources cited by Reuters suggested these were rough calculations.

- BoE’s Mann says all of the MPC agree that UK inflation is way above the BoE’s goal; Mann added that domestic demand is strong and UK labour market is tight. BoE agents survey has been fundamental in guiding Mann’s view on policy.

US Event Calendar

- 8:30am: Jan. Personal Income, est. -0.3%, prior 0.3%

- 8:30am: Jan. Personal Spending, est. 1.6%, prior -0.6%

- 8:30am: Jan. Real Personal Spending, est. 1.2%, prior -1.0%

- 8:30am: Jan. Cap Goods Orders Nondef Ex Air, est. 0.3%, prior 0.3%

- 8:30am: Jan. Cap Goods Ship Nondef Ex Air, est. 0.5%, prior 1.3%

- 8:30am: Jan. -Less Transportation, est. 0.4%, prior 0.6%

- 8:30am: Jan. PCE Deflator MoM, est. 0.6%, prior 0.4%; PCE Deflator YoY, est. 6.0%, prior 5.8%

- 8:30am: Jan. PCE Core Deflator MoM, est. 0.5%, prior 0.5%; PCE Core Deflator YoY, est. 5.2%, prior 4.9%;

- 8:30am: Jan. Durable Goods Orders, est. 1.0%, prior -0.7%

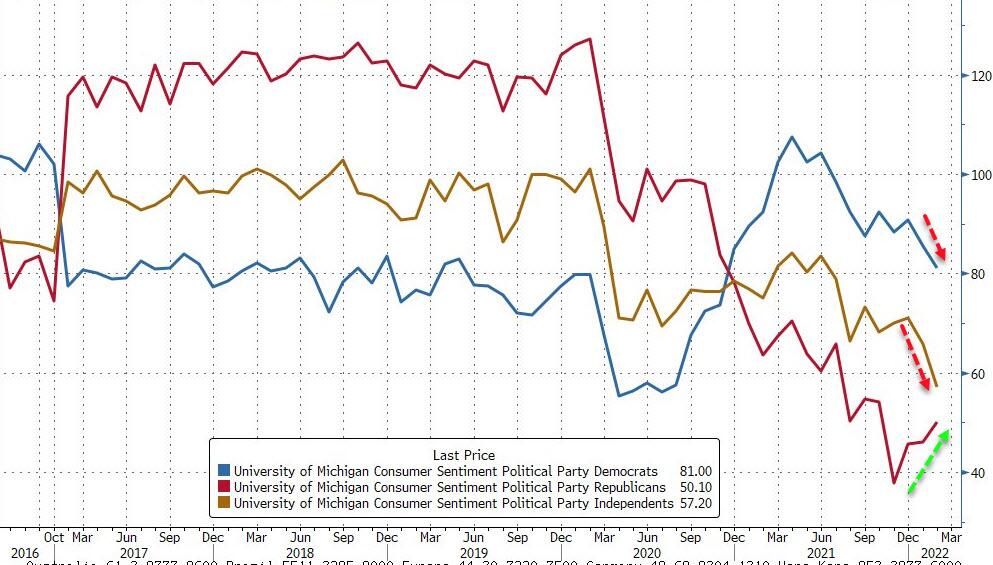

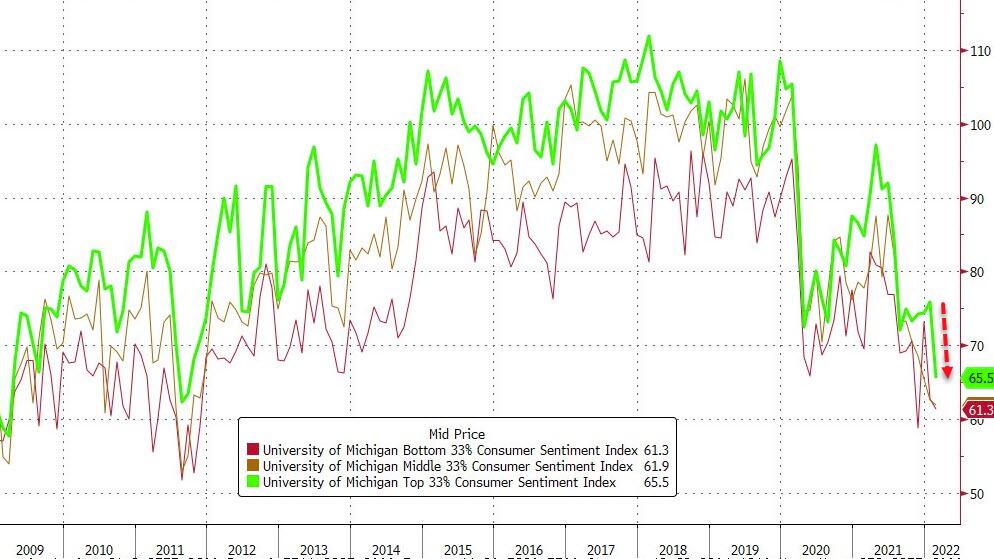

- 10am: Feb. U. of Mich. Sentiment, est. 61.7, prior 61.7; Current Conditions, est. 68.5, prior 68.5; Expectations, est. 57.3, prior 57.4

- 10am: Feb. U. of Mich. 1 Yr Inflation, prior 5.0%

- 10am: Feb. U. of Mich. 5-10 Yr Inflation, prior 3.1%

- 10am: Jan. Pending Home Sales (MoM), est. 0.2%, prior -3.8%; YoY, est. -1.8%, prior -6.6%

DB’s Jim Reid concludes the overnight wrap

It’s been a pretty seismic 36 hours and at some points yesterday the outlook for markets and economies felt very bleak. However remarkably after an 8 dollar round trip that first sent Brent crude over $105/bbl, oil (+2.31% on the day) eventually closed last night at $99.08 (still the highest since 2014), and only around the levels seen just before Russia launched the invasion just over 24 hours ago. It’s edged up again in the Asian session to $100.75 as I type but the fact that oil stopped going parabolically higher helped turn the whole market around yesterday.

Indeed markets hit peak pessimism around lunchtime in Europe but Biden not yet putting sanctions on Energy or restricting Russian access to SWIFT seemed to cap off a more positive tone thereafter. Indeed the S&P and Nasdaq rose +4.23% and +7.04% respectively from the opening lows to close up +1.50% and +3.34% on the day. A remarkable turnaround. S&P 500 (-0.53%) and Nasdaq (-0.76%) futures are down again this morning but this is still clearly well off the lows.

If this event is going to have a lasting macro and market impact it has to hit energy prices and for much of yesterday it looked like it was on course to aggressively do so, and to be fair still might. European natural gas will be one to watch today as it soared +63.89% at its peak yesterday, only to fade towards the close to be ‘only’ up +33.31%. On a bigger picture basis the events of this week have to be forcing governments to think of their energy security in much more detail than they have in the past. Will it also impact the green transition? Surely it makes it more urgent in the medium-term but tougher to stick with in the short-term. Much will depend on what happens next for energy prices. Clearly the West may still put sanctions on this Russian supply which will undoubtedly risk a renewed spike in energy.

Diving into yesterday. The intraday turnaround in asset prices followed clarity on what the west’s next round of sanctions would look like. The sanctions were expanded to more connected individuals and entities, were designed to cut off high-tech exports crucial to Russian defense and tech industries, impinge Russia’s ability to raise capital on foreign markets by restricting access and freezing assets of some of their largest banks, and restrict Russia’s ability to deal in dollars, yen, and euros. The sanctions not applied, however, drove an intraday turn in risk assets and reversed measures of inflation compensation. Namely, President Biden noted the sanctions package was specifically designed to allow energy payments to continue, and that the US would release strategic oil reserves as needed to help ameliorate price pressures. Further, they did not cut off Russia’s access to the international payments system, SWIFT, though maintained the option of doing so.

Before the rally back there was a complete rout in numerous markets yesterday, and when it came to Russian assets there was frankly a capitulation, with the MOEX equity index (-32.28%) shedding more than a third of its value in a single day (-45.06% at the session lows). Bloomberg wrote a piece saying that the worst single day equity loss in their database for any country’s index was Argentina’s -53.1% fall in January 1990. In total, there have been seven worst days in stock market history than -33.3%. For what it’s worth, those equity declines are the sort that would trigger circuit breakers if they happened elsewhere. For example we couldn’t see that for the S&P 500 in a single day, since trading rules stipulate that there’s a complete halt for the day once you get to a -20% loss.

On top of that, the Russian Ruble -5.15% hit a record low against the US dollar, after suffering its worst daily performance since the height of the Covid crisis back in March 2020. And yields on 10yr Russian sovereign debt were up by +435.0bps to 15.23%.

The STOXX 600 fell -3.28% as it reached its lowest level since last May, with major losses for the other European indices including the FTSE 100 (-3.88%), the CAC 40 (-3.83%) and the DAX (-3.96%).

With investors pricing in a less aggressive reaction function from central banks, sovereign bonds saw a decent rally yesterday, having also been supported by the dash for haven assets. However the moves didn’t match the severity of the flight to quality shock, even at the worse point of the day, as the real return consequence of buying government bonds at a yields of 0-2% was all too apparent with inflation rife.

There was some big ranges though. 10yr US real yields were -27.7bps lower and breakevens +14.4bps wider as news of the invasion, and commensurate stagflation fears hit. However, the intraday turn around led to much more modest closing levels, with 10yr real yields -4.2bps lower and breakevens +1.5bps higher. 10yr nominal Treasury yields settled -2.8bps lower on the day at 1.96%. At shorter tenors, 5yr breakevens also displayed a remarkable intraday roundtrip, finishing +1.4bps higher after having hit an intraday peak +24.8bps wider at +3.39%, which would have been the highest reading on record. In Europe the breakeven widening was more sustained, and the 10yr German breakeven actually managed to close above 2% for the first time in over a decade yesterday, having climbed +12.9bps to +2.10%. Meanwhile nominal yields on 10yr bunds (-5.8bps), OATs (-7.0bps) and gilts (-3.2bps) all moved lower.

Energy prices are going to continue to keep central bankers awake at night, since they can’t do anything about the supply issues directly. More shocks will lead to both lower growth (absent fiscal suppprt) and higher inflation, with the risk being that you start to see second-round effects if higher inflation becomes entrenched. Notably, one of the ECB’s biggest hawks, Robert Holzmann of Austria, said in a Bloomberg interview that the conflict meant “It’s possible however that the speed may now be somewhat delayed.” That was music to the ears of peripheral sovereign debt in particular, which rallied strongly on the news, with the Italian spread over 10yr bunds moving from an intraday high of 178bps to close at 164.5bps.

In Asia the Nikkei (+1.63%), Kospi (+1.15%), Shanghai Composite (+0.54%), and the CSI (+0.78%) all are higher in line with the second half rally yesterday. Meanwhile, the Hang Seng (-0.16%) is lower.

In economic data, overall inflation for Tokyo rose +1.0% y/y in February, its fastest pace of growth since December 2019, on higher energy prices and after an upwardly revised +0.6% increase in January. Bloomberg estimates were for a +0.7% rise. Excluding fresh food, consumer prices in Japan advanced +0.5% in February y/y, accelerating from a +0.2% increase in January and outpacing a +0.4% gain expected by analysts.

In central banks news, the People’s Bank of China (PBOC) beefed up liquidity by injecting 300 billion yuan ($47.4 bn) into the financial system via 7-day reverse repos, amid concerns over the Russia-Ukraine conflict. For the week, the PBOC injected a net 760 billion yuan – the biggest weekly cash offering since January 2020.

Data releases understandably took a back seat yesterday, but we did get the weekly initial jobless claims from the US for the week through February 19, which fell to 232k (vs. 235k expected). We also saw the continuing claims for the week through February 12 fall to a half-century low of 1.476m, a level unseen since 1970. Otherwise, new home sales in January fell to an annualised rate of 801k (vs. 803k expected), and the second estimate of Q4’s GDP was revised up by a tenth from the initial estimate to an annualised +7.0%.