March 15, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

MARCH15

GOLD; $1927.45 DOWN $30.80

SILVER: $25.16 DOWN $0.18

ACCESS MARKET: GOLD $1916.50

SILVER: $24.88

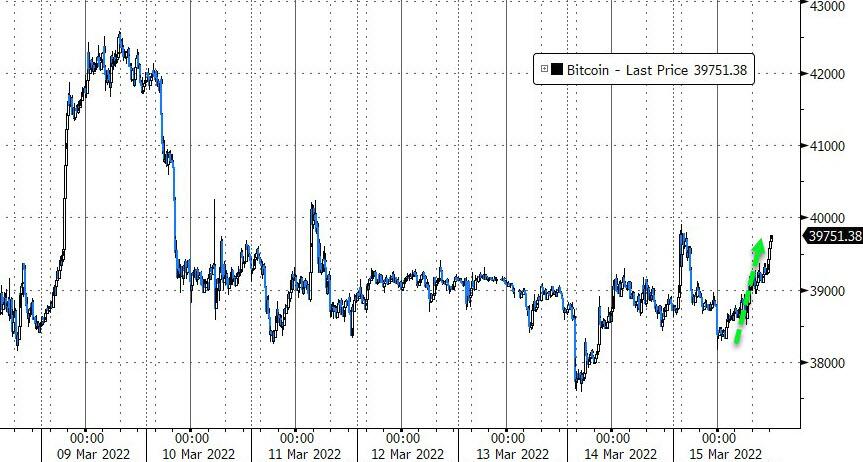

Bitcoin morning price: $38,734 UP 40

Bitcoin: afternoon price: $39,590 UP 896

Platinum price: closing DOWN $43.50 to $1043.75

Palladium price; closing UP $12.55 at $2436.75

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

March: JPMorgan stopped/total issued 39/75

EXCHANGE: COMEX

CONTRACT: MARCH 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,959.600000000 USD

INTENT DATE: 03/14/2022 DELIVERY DATE: 03/16/2022

FIRM ORG FIRM NAME ISSUED STOPPED

104 C MIZUHO 1

363 H WELLS FARGO SEC 3

435 H SCOTIA CAPITAL 8

624 H BOFA SECURITIES 7

657 C MORGAN STANLEY 6

657 H MORGAN STANLEY 7

661 C JP MORGAN 39

690 C ABN AMRO 15

709 C BARCLAYS 8

737 C ADVANTAGE 41 1

800 C MAREX SPEC 10

905 C ADM 3 1

TOTAL: 75 75

MONTH TO DATE: 10,317

NUMBER OF NOTICES FILED TODAY FOR Mar. CONTRACT:75 NOTICE(S) FOR 7500 OZ (0.2332 TONNES)

total notices so far: 10,317 contracts for 1,031,700 oz (32/090 tonnes)

SILVER NOTICES:

302 NOTICE(S) FILED TODAY FOR 1,510,000 OZ/

total number of notices filed so far this month 10,367 : for 51,835,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD DOWN $30.80

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD//

INVENTORY RESTS AT 1064.16 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $0.18

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

NO CHANGES IN SILVER INVENTORY AT THE SLV//

FROM THE SLV.

CLOSING INVENTORY: 545.022 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A VERY STRONG SIZED 3112 CONTRACTS TO 160,795 ON DAY 4 OF OUR CONTINUAL RAID, AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED WITH OUR HUGE $0.64 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.64) AND WERE UNSUCCESSFUL IN KNOCKING OUT SOME SILVER LONGS AS WE HAD A HUGE LOSS OF 2632 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 42.860 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 10,000 OZ //NEW STANDING 52.140 MILLION OZ // V) HUGE SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : —454

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTACTS for 11 days, total contracts: : 24,628 contracts or 123.140 million oz OR 11.190 MILLION OZ PER DAY. (2238 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 24,628 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 123.140 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 123.140 MILLION OZ//THIS IS GOING TO BE A HUGE EFP ISSUANCE MONTH AND MOST LIKELY WILL SET A RECORD FOR ANY MONTH

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3112 WITH OUR $0.64 LOSS SILVER PRICING AT THE COMEX// MONDAY THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 480 CONTRACTS( 480 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAR. OF 42.860 MILLION OZ FOLLOWED BY TODAY’S 10,000 OZ QUEUE JUMP /// .. WE HAD A HUGE SIZED LOSS OF 2632 OI CONTRACTS ON THE TWO EXCHANGES FOR 10.890 MILLION OZ

WE HAD 302 NOTICES FILED TODAY FOR 1,510,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 8950 CONTRACTS TO 624,775 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –724 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE STRONG SIZED DECREASE IN COMEX OI CAME WITH OUR STRONG LOSS IN PRICE OF $22.75//COMEX GOLD TRADING/MONDAY/.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MARCH AT 14.818 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 5500 OZ//NEW STANDING 36.040 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $22.75 WITH RESPECT TO MONDAY’S TRADING

WE HAD AN SMALL FALL OF 2054 OI CONTRACTS (6.388 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6896 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 624,775.

IN ESSENCE WE HAVE AN SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2054, WITH 8950 CONTRACTS DECREASED AT THE COMEX AND 6896 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 1330 CONTRACTS OR 4.136 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (6896) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (8,950,): TOTAL LOSS IN THE TWO EXCHANGES 2054 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR MARCH. AT 14.818 TONNES FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 5500 OZ//NEW STANDING 36.040 TONNES /// 3) SOME LONG LIQUIDATION ///. ,4) STRONG SIZED COMEX OI. LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

LADIES AND GENTLEMEN: THE GOLD COMEX IS ALSO BEING ATTACKED FOR GOLD METAL FROM LONDON ET AL.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MARCH

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

72,884 CONTRACTS OR 7,288,400 OR 226.69 TONNES 11 TRADING DAY(S) AND THUS AVERAGING: 663 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY(S) IN TONNES: 226.69TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 226.59/3550 x 100% TONNES 6.39% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 226.59 TONNES INITIAL( THIS WILL PROBABLY BE A RECORD EFP ISSUANCE MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL.WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MARCH HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A HUGE SIZED 3112 CONTRACTS TO 160,795 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 480 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 480 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 480 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3112 CONTRACTS AND ADD TO THE 480 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF 2632 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 13.16 MILLION OZ,

OCCURRED WITH OUR $0.64 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED DOWN 159.57 PTS OR 4.95% //Hang Sang CLOSED DOWN 1116,59 PTS OR 5.72 % /The Nikkei closed UP 38,63 PTS or 0.15% //Australia’s all ordinaires CLOSED DOWN 0.89% /Chinese yuan (ONSHORE) closed DOWN 6.3750 /Oil DOWN TO 103.25 dollars per barrel for WTI and DOWN TO 108.14 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3750. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.4090: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER//

A)NORTH KOREA/

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 8,950 CONTRACTS AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR STRONG LOSS OF $22.75 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (6896 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE NON ACTIVE DELIVERY MONTH OF MAR.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 6896 EFP CONTRACTS WERE ISSUED: ;: , & FEB. 0 APRIL:6896 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6896 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 2054 CONTRACTS IN THAT 6896 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 8,950 CONTRACTS..AND THIS OCCURRED WITH A STRONG LOSS IN PRICE OF $22.75.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAR (36.040),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.040 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $22.75) AND THEY WERE SUCCESSFUL IN FLEECING SOME LONGS AS WE HAVE REGISTERED A SMALL SIZED LOSS OF 6.388 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAR (36.040 TONNES)…

WE HAD –724 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 2054 CONTRACTS OR 205400 OZ OR 6.388 TONNES

Estimated gold volume today: 244,926 ///fair

Confirmed volume yesterday: 189,426contracts poor

INITIAL STANDINGS FOR MAR ’22 COMEX GOLD //MARCH 15

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 23,177.371 oz Manfra BRINKS 1 kilobars/Brinks |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | 5,397.868 oz Brinks |

| No of oz served (contracts) today | 75 notice(s 7500 OZ 0.2332 TONNES |

| No of oz to be served (notices) | 1270 contracts 127,000 oz 3.950 TONNES |

| Total monthly oz gold served (contracts) so far this month | 10,317 notices1,031,700 OZ 32.090 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

1)dealer deposit

total dealer deposit 0 oz

No dealer withdrawal 0

1 customer deposits

i) Into Brinks 5,397.868 oz

total deposit: 5,397.868 oz

2 customer withdrawal

i) Out of Manfra 23,145.220 oz

ii) Out of Brinks: 32.151 oz (1 kilobars)

total withdrawals: 23,177.371 oz

ADJUSTMENTS: 0/

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MARCH.

For the front month of MARCH we have an oi of 1345 contracts having LOST 733

We had 788 notices filed yesterday so strangely again on day 11 we gained another queue jump i.e. 55 contracts or an additional 5500 oz will stand for delivery and these guys refused again to be EFP’d over to London. They must

be after large amounts of gold on this side of the pond after Russia cannot//will not supply any precious metals to London. The 5500 oz is represented by 0.1710 tonnes,

April saw a loss of 15,976 contracts down to 303,567.

May saw a gain of 5 contracts to stand at 4148

June saw a GAIN of 7121 contracts up to 249,301 contracts

We had 788 notice(s) filed today for 78,800 oz FOR THE MAR 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 75 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 39 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 5 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR /2021. contract month,

we take the total number of notices filed so far for the month (10,317) x 100 oz , to which we add the difference between the open interest for the front month of (MAR: 1345 CONTRACTS ) minus the number of notices served upon today 75 x 100 oz per contract equals 1,158,700 OZ OR 36.040 TONNES the number of TONNES standing in this active month of mar.

thus the INITIAL standings for gold for the MAR contract month:

No of notices filed so far (10,317) x 100 oz+ (1345) OI for the front month minus the number of notices served upon today (75} x 100 oz} which equals 1,1587,00 oz standing OR 36.040 TONNES in this NON active delivery month of MAR.

TOTAL COMEX GOLD STANDING: 36.040 TONNES (A WHOPPER FOR A MAR (NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

191,133,764.7, oz NOW PLEDGED /HSBC 5.94 TONNES

123,963.792 PLEDGED MANFRA 3.86 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690 tonnes

243,923.704, oz JPM No 2 7.58 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonnes

Loomis: 18,615.429 oz

total pledged gold: 1,543,044.471 oz 47.99 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 33,144,155.164 OZ (1030.92TONNES)

TOTAL ELIGIBLE GOLD: 15,606,658.037 OZ (485.43 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,537,497.127 OZ (545.e48 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,994,453.0 OZ (REG GOLD- PLEDGED GOLD) 497.49 tonnes

END

MAR 2022 CONTRACT MONTH//SILVER//MARCH 15

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 902,317,820 oz Brinks CNT JPM |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 270,766.075 oz Delaware |

| No of oz served today (contracts) | 302CONTRACT(S) 1,510,000 OZ) |

| No of oz to be served (notices) | 63 contracts (315,000 oz) |

| Total monthly oz silver served (contracts) | 10,367 contracts 51,835,000 oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

i) Into Delaware: 270,766.075 oz

total deposit: 270,766.075 oz

JPMorgan has a total silver weight: 181.71 million oz/343.988 million =52.92% of comex

ii) Comex withdrawals: 3

a) Out of CNT: 72,487.149 oz

b) Out of Brinks 217,722.080 oz

c) Out of JPMorgan 612,108.600 oz

total withdrawal 902,317.820 oz

we had 1 adjustments// out of customer to dealer

JPMorgan 1,495,166.118

the silver comex is in stress!

TOTAL REGISTERED SILVER: 93.589 MILLION OZ

TOTAL REG + ELIG. 343.988 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR MARCH

silver open interest data:

FRONT MONTH OF MARCH OI: 365, HAVING LOST 133 CONTRACTS FROM MONDAY.

WE HAD 135 NOTICES SERVED UPON YESTERDAY, SO WE GAINED 2 CONTRACTS OR AN ADDITIONAL 10,000 OZ WILL STAND

FOR DELIVERY OVER HERE AS THESE GUYS REFUSED TO BE EFP’D TO LONDON.

APRIL HAD A 44 CONTRACT GAIN// CONTRACTS RISING TO 692

MAY HAD A LOSS OF 3343 CONTRACTS DOWN TO 122,811 contracts

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 302 for 1,510,000 oz

Comex volumes: 48,289// est. volume today//fair/

Comex volume: confirmed yesterday: 56,633 contracts (FAIR )

To calculate the number of silver ounces that will stand for delivery in MAR. we take the total number of notices filed for the month so far at 10,367 x 5,000 oz = 51,835,000 oz

to which we add the difference between the open interest for the front month of MAR (365) and the number of notices served upon today 302 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2021 contract month: 10,367 (notices served so far) x 5000 oz + OI for front month of MAR (365) – number of notices served upon today (302) x 5000 oz of silver standing for the MAR contract month equates 52,150,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MARCH 15/WITH GOLD DOWN $30.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1064.16 TONNES

MARCH 14//WITH GOLD DOWN $22.75, HUGE CHANGES IN GOLD INVENTORY AT THE GLD//STRANGE: A DEPOSIT OF 2.62 TONNES INTO THE GLD.//INVENTORY RESTS AT 1064.16 TONNES

MARCH 11/WITH GOLD DOWN $14.60: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1061.54 TONNES

MARCH 10//WITH GOLD UP $11.55: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FORM THE GLD///INVENTORY RESTS AT 1063.28 TONNES

MARCH 9/WITH GOLD DOWN $53.85//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.64 TONNES INTO THE GLD//INVENTORY RESTS AT 1067.34 TONNES

MARCH 8/WITH GOLD UP $46.10: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 8.42 TONNES INTO THE GLD///INVENTORY RESTS AT 1062.70 TONNES

MARCH 7/WITH GOLD UP $28.40 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1054.28 TONNES

MARCH 4/WITH GOLD UP $28.40//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1050.22 TONNES

MARCH 3/WITH GOLD UP $13.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 7.84 TONNES//INVENTORY RESTS AT 1050.22 TONNES

MARCH 2/WITH GOLD DOWN $20.80//A MONSTER CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 13.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1042.38 TONNES

MARCH 1/WITH GOLD UP $42.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: //INVENTORY RESTS AT 1029.32 TONNES

FEB 28/WITH GOLD UP $12.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 25/WITH GOLD DOWN $38.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 24/WITH GOLD UP $17.35//A HUGE CHANGE AT THE GLD: 5.23 TONNES INTO THE GLD// IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1029.32 TONNES

FEB 23/WITH GOLD UP $2.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1024.09 TONNES

FEB 22/WITH GOLD UP $6.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1024.09 TONNES

FEB 18/WITH GOLD DOWN $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 17/WITH GOLD UP $29.50: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 16/WITH GOLD UP 414.60 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 15/WITH GOLD DOWN $12.70 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 14/WITH GOLD UP $27.20 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 11/WITH GOLD UP $4.50 A HUGE CHANGE IN GOLD IVNETORY AT THE GLD// A DEPOSIT OF 3.48 TONNES INTO THE GLD//INVENTORY RESTS AT 1019.44 TONES

FEB 10/WITH GOLD UP $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1015.96 TONNES

FEB 9/WITH GOLD UP $8.05//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1015.96 TONNES

FEB 8/WITH GOLD UP $5.95 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1015.96 TONNES

FEB 7/WITH GOLD UP $14.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.24 TONNES FROM THE GLD/////INVENTORY RESTS AT 1011.60 TONNES//

FEB 4/WITH GOLD UP $3.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.84 TONNES

FEB 3/WITH GOLD DOWN $5.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 1016.59 TONNES

FEB 2/WITH GOLD UP $7.95//A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.78 TONES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1018.04 TONNES

FEB 1/WITH GOLD UP $5.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

CLOSING INVENTORY FOR THE GLD//1064.16 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 15/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.022 TONNES

MARCH 14/WITH SILVER DOWN 64 CENTS TODAY; STRANGE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.125 MILLION OZ/INVENTORY RESTS AT 545.022 TONNES

MARCH 11/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 TONNES

MARCH 10/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ/

MARCH 9/WITH SILVER DOWN 88 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.174 MILLION OZ OF FAKE SILVER.//INVENTORY RESTS AT 542.897 MILLION OZ//

MARCH 8/WITH SILVER UP 88 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV////INVENTORY RESTS A 548.071 MILLION OZ//

MARCH 7/WITH SILVER UP 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 4/WITH SILVER UP 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ/

MARCH 3/WITH SILVER UP 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.32 TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 198,000 OZ FROM THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 1/WITH SILVER UP $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 546.052 MILLION OZ//

FEB 28/WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 546.052 MILLION OZ//

FEB 25/WITH SILVER DOWN 64 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.510 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 546.052 MILLION OZ/

FEB 24/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ

FEB 23/WITH SILVER UP 22 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ//

FEB 22/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 350,000 OZ INTO THE SLV///INVENTORY RESTS AT 551.597 MILLION OZ//

FEB 18/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.017 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 551.227 MILLION OZ

FEB 17/WITH SILVER UP 31 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.402 MILLION OZ//INVENTORY RESTS AT 550.210 MILLION OZ/

FEB 16/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.808 MILLIONOZ

FEB 15/WITH SILVER DOWN 46 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.808 MILLION OZ//

FEB 14/WITH SILVER UP 49 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.235 MILLION OZ INTO THES LV////INVENTORY RESTS AT 547.808 MILLION OZ

FEB 11/WITH SILVER DOWN 18 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ///

SLV/FEB 10/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 9/WITH SILVER UP 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 8/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.143 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 7/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.218 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 541.430 MILLION OZ/

FEB 4/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 539.212 MILION OZ

FEB 3/WITH SILVER DOWN 35 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT539.212 MILLION OZ//

FEB 2/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.411 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 539.212 MILLION OZ/

FEB 1/WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.801 MILLION OZ

SLV FINAL INVENTORY FOR TODAY: 545.022 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff Warns Tucker Carlson: Inflation Only Has One Way To Go!

TUESDAY, MAR 15, 2022 – 08:11 AM

Last week, we got another big jump in consumer prices with the February CPI data. Peter Schiff appeared on Fox News with Tucker Carlson to talk about the rampant inflation. He said it’s only going to get worse. Inflation only has one way to go.

Up.

Tucker said Peter should feel vindicated. He’s been right on inflation all along. Peter emphasized that inflation didn’t just happen overnight.

Inflation has been a problem for a while. We just didn’t care about it when it made stocks go up or real estate go up. But now that it’s making food prices go up and energy prices go up and rents go up, it’s a bigger problem.”

Peter also emphasized that inflation isn’t created by COVID, or by Putin, or by “greedy corporations.”

There’s one source of inflation. The actual definition of inflation is an expansion of the money supply. And it’s the Federal Reserve that’s been expanding the money supply. They’ve called it quantitative easing, but they keep creating dollars. And it’s the US government that spends those dollars into circulation, and as it does that, the value of each dollar goes down. So, the price of everything that you buy with dollars goes up.”

Peter said the middle-class will feel the impact of the inflation tax the hardest.

Their wages are not going to go up nearly as much as the cost of living. There are other people who are retired, who are on fixed incomes, and those incomes aren’t going to go up at all.”

The CPI for February was 7.9%. That’s being called the worst inflation since 1982. But what they don’t tell you is they measured CPI differently then.

If we use the same CPI today that we used then, we would be over 15% inflation, which means 2021, or 2022, right now, this is the worst inflation in our lifetimes. We’re experiencing higher inflation now than anything in the 1970s. And this decade is just getting started. Inflation’s got only one way to go and that’s up.”

END

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

PAM AND RUSS MARTENS:

-END-

LAWRIE WILLIAMS:

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

4.OTHER GOLD/SILVER COMMENTARIES

a must view…

end

5.OTHER COMMODITIES/

end

NICKEL UPDATE

With Chinese Commodity Tycoon Bailed Out, LME Announces Nickel Market To Reopen

MONDAY, MAR 14, 2022 – 05:20 PM

With the Nickel market shuttered after a Chinese stainless steel tycoon was caught with a historic, potentially fatal $8 billion margin call hanging over its head, today the London Metal Exchange announced that it will reopen its nickel market on Wednesday, more than a week after it was closed last Monday, after the Chinese company at the center of the epic short squeeze was bailed out by a consortium of banks led by JPMorgan which is also the largest counterparty to the short (for a detailed breakdown read “The 18 Minutes of Trading Chaos That Broke the Nickel Market“) .

Trading in nickel will resume after Xiang Guangda, whose massive short position equivalent to approximately 150,000 tons of nickel, sent shockwaves across the commodity market last week, announced a standstill with his banks to avoid further margin calls as Bloomberg first reported earlier. Xiang’s Tsingshan Group had been in discussions with banks led by JPMorgan about a loan facility to backstop his short position and said Monday that talks on the funding would continue during the standstill period. As a reminder, Xiang is JPMorgan’s largest counterparty, and owes Jamie Dimon several billion, money which the largest US bank would not receive unless it bailed out the Chinese firm.

Here is the statement from the LME:

This Notice: (i) confirms that trading in LME Nickel Contracts will resume at 08:00 London time on Wednesday 16 March 2022 (“Resumption Date”) on all LME Execution Venues; (ii) sets out details of the application of daily upper and lower price limits to all outright Contracts in all Base Metals on all Execution Venues; (iii) sets out details of the deferral of delivery to Wednesday 23 March at level for all Nickel Contracts entered into prior to Wednesday 16 March and due for delivery between Wednesday 16 and Tuesday 22 March inclusive; (iv) details the Accountability Levels that shall apply to Nickel Contracts with effect from the Resumption Date and outlines information gathering measures that shall apply to Members in relation to aggregate on-exchange and OTC Nickel positions; and (v) provides additional guidance on the LME’s approach to the determination and publication of Official Prices and Closing Prices during any period

The discredited, Hong Kong-owned London Metals Exchange also announced that it would impose 15% limit on daily price moves across all metals – which will come in useful on Wednesday when nickel either explodes higher yet again in hopes of further squeezing Tsingshan, or crashes.

The exchange also said that it would require traders’ nickel positions to be reported going forward, something it should have thought of long ago.London Metals Exchange pit. Only Billy Ray and Lewis are missing.

Last week the LME attempted a bizarre process to try to close out short positions by matching market participants with long and short positions before the market reopened, but received little interest especially after Xiang told the banks and brokers last week that he would like to keep his short position, sparking fears that the short squeeze could continue as a GME scenario could emerge as specs sought to push the price even higher.

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING TODAY

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.3780

OFFSHORE YUAN: 6.4090

HANG SANG CLOSED DOWN 1116.58 PTS OR 5.72%

2. Nikkei closed UP 38.63 PTS 0.15%

3. Europe stocks ALL RED

USA dollar INDEX DOWN TO 98.81/Euro RISES TO 1.0983-

3b Japan 10 YR bond yield: RISES TO. +.211/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 118.05/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 94.86 and Brent: 97.78–

3f Gold DOWN /JAPANESE Yen UP CHINESE YUAN: ON -SHORE CLOSED DOWN// OFF- SHORE DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.352%/Italian 10 Yr bond yield RISES to 1.95% /SPAIN 10 YR BOND YIELD RISES TO 1.34%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.60: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.66

3k Gold at $1966.20 silver at: 25.30 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble UP 11.00/100 in roubles/dollar; ROUBLE AT 110.62

3m oil into the 94 dollar handle for WTI and 97 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 118.05 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9389– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0317 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

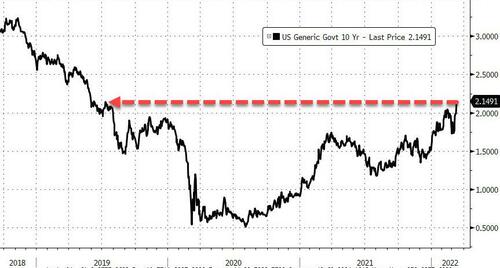

USA 10 YR BOND YIELD: 2.126 DOWN 2 BASIS PTS

USA 30 YR BOND YIELD: 2.471 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.79

US Futures Ignore China Implosion, Reverse Overnight Losses as Oil Tumbles

TUESDAY, MAR 15, 2022 – 07:53 AM

Welcome to another rollercoaster session where US equity futures first tumbled alongside the second consecutive day of stocks plunging in China, which also dragged Europe lower, only to hit a U-turn around 5am at which point sentiment reversed higher, ahead of tomorrow’s expected Federal Reserve rate hike and amid mounting risks from the war in Ukraine and a Chinese equity rout. Nasdaq 100 contracts trade 0.5% higher at 7:15 a.m. after earlier slumping as much as 0.8% following the first bear-market close for the first time since March 2020. S&P 500 futures also turned 0.3% green, as did Dow futures.

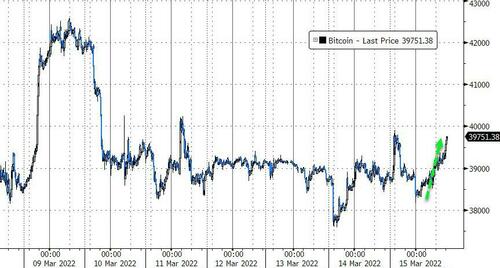

Much of the reversal in sentiment has been attributed to the latest drop in oil which tumbled over $8/bbl or 5.5%, sliding as low as $98 after hitting $139 one week ago. WTI crude oil also fell below $100 a barrel a barrel as traders reassessed the potential impact of disruptions in Russian oil supplies and a decline in demand from China. Iron ore futures fell for a sixth day, the longest streak since September. In other words, commodities are not sliding because of hopes for Russia peace, but because of fears about a global recession, but try explaining it all to algos. Treasuries gained, though the 10-year yield remains near the highest level since 2019. Yields across the euro region also declined. The dollar slipped, while the euro pushed higher and bitcoin dropped again.

Earlier in the session, a selloff across Chinese equities deepened as concerns about ties with Russia, a growing covid crisis, and persistent regulatory pressure sent a key index to its lowest level since 2008. The Hang Seng China Enterprises Index, which tracks Chinese shares listed in Hong Kong, sank 6.6%, following a plunge in the previous session that was the biggest since the global financial crisis.

The Hang Seng index tumbled Tech giants Alibaba Group Holding Ltd. and Tencent Holdings Ltd. led the decline. Hong Kong’s benchmark Hang Seng Index slumped 5.7%, its biggest fall since July 2015.

China’s equities are looking increasingly risky on concerns that Beijing’s ties with Russia could spark new U.S. sanctions. That’s adding to worries from regulatory developments including a possible delisting from the U.S. exchanges. While upbeat economic data was a rare bright spot in the market, growing lockdowns in major Chinese cities are dimming the outlook.

“The selloff is overdone, but so is everything else,” said Andy Maynard, head of equities at China Renaissance Securities. “The market is crazy — there’s no fundamentals anymore. This might be worse than the 2008 financial crisis.”

“Risk-off sentiment stemming from both the Russia-Ukraine war and the current wave of Covid-19 in China has driven equity markets sharply weaker this morning,” Siobhan Redford, an analyst at Rand Merchant Bank in Johannesburg, said in a client note. “This has been compounded by falling commodity prices as the intersection between limited supply — given sanctions on Russia and the war in Ukraine — and a weaker demand trajectory — given further waves of the pandemic — create a perfect storm of sorts.”

With zero liquidity, and trigger happy traders looking to sell any rally, swings in S&P 500 and Nasdaq 100 futures signaled another volatile day ahead for U.S. stocks. U.S.-listed Chinese stocks sank again on Tuesday, following a brutal rout in Asia, amid concerns that China’s ties with Russia may bring sanctions to Beijing, while persistent regulatory pressures also weighed. Alibaba (BABA US) fell 6.5% in premarket trading, while rival JD.com (JD US) declined 4.5%. Apple Inc. inched lower, heading toward a bear market — defined as a 20% drop from recent highs — on worries that lockdowns in China to contain a surge in Covid-19 cases could worsen supply-chain constraints. Other notable premarket movers:

- Shares in big U.S. energy companies slide in premarket trading as crude price fall, declining after last week’s rally as worries over growing coronavirus cases in top crude importer China weigh. Exxon Mobil (XOM US) -3.1% and Chevron (CVX US) -3.7%.

- Coupa Software (COUP US) slides 30% in postmarket trading after the company’s revenue forecast for the first quarter misses the average analyst estimate.

- Gitlab (GTLB US) shares rose 12% in extended trading on Monday, after the software company reported fourth-quarter revenue that beat expectations and gave a full-year forecast that is stronger than the analyst consensus.

U.S. technology stocks have been particularly hard hit in the past week with the Federal Reserve expected to begin a rate-hike cycle on Wednesday, another negative for growth stocks valued on future profits. Investors are also looking for cues from the central bank about how aggressively it plans to continue tightening monetary policy as Russia’s invasion of Ukraine sent commodity prices soaring when inflation was already running high. A reading on the producer price index is due on Tuesday.

“If we are entering a world of above-target inflation for several years to come, investors should ditch the easy answers,” said Sahil Mahtani, strategist at Ninety One. “Conventional 60-40 type portfolios are likely to struggle. Investors should reflect about what specifically is driving the inflationary process and invest in equities that have pricing power but are not at frothy valuations.”

The Stoxx Europe 600 index fell more than 1.5%, with basic resources, consumer and technology stocks leading a broad-based decline. All sectors are in the red. Euro Stoxx 50 slumps 2.4%. IBEX outperforms peers but still trades off ~1.5%. Here are some of the biggest European movers today:

- Ahold Delhaize shares gain as much as 3.2%, the best performer in the Stoxx 600’s personal care, drug and grocery stores subgroup, after being upgraded to buy from neutral at UBS, which says the stock is at an “attractive entry point.”

- S&T rallied in Frankfurt, climbing as much as 18%, after the Austrian company said a forensic audit by Deloitte found allegations by short seller Viceroy Research were almost completely inaccurate.

- Sensirion shares spike as much as 13%, the most since June 2020, after the Swiss sensor manufacturer reported full- year sales and gave a revenue forecast that blew past analysts’ estimates. Stifel says the company’s growth is driven by all end markets and the performance of new environmental sensors looks “impressive.”

- Wacker Chemie shares gain as much as 6.9%, as Baader sees dividend proposal 56% above and midpoint ‘22 Ebitda guidance 3% ahead of consensus.

- Tecan falls as much as 16% after reporting sales for the full year that missed the average analyst estimate, and as the outlook disappointed.

- Dr. Martens shares tumble as much as 11% to the lowest since listing in January 2021 after RBC cut its price target to a Street-low, citing the bootmaker’s growth outlook.

- Swedish Match drops as much as 8.4%, the most intraday since February 2021, after the company suspended the spinoff of its U.S. cigar business. The move highlights regulatory risk, according to JPMorgan.

Meanwhile, Russia has started the payment process of two bond coupons due this week. Investors are waiting to see if the nation defaults after the U.S. and its allies froze Russia’s foreign-currency reserves. The ruble gained in Moscow trading.

Asian stocks plunged, on track for a third-straight daily loss, as the selloff in Chinese technology stocks continued after Monday’s plunge, while traders tried to gauge the impact of an imminent interest-rate hike by the Federal Reserve. The MSCI Asia Pacific Index fell as much as 1.9%, heading for its lowest close since August 2020. Tencent and Alibaba Group were among the biggest drags on the regional index, along with TSMC. The sustained selling pressure came as investors mulled the potential consequences of China’s assistance for Russia’s war in Ukraine and delisting risk for Chinese stocks traded in the U.S. Hong Kong’s benchmark Hang Seng Index tumbled 5.7%, its biggest fall since July 2015, while the Hang Seng Tech Index lost 8.1% following a wild intraday swing. Read: Relentless Selling in China Stocks Evokes Memories of 2008 Crash China’s CSI 300 Index slumped 4.6% as the nation’s strong set of economic data failed to lift sentiment amid market jitters on the rising case numbers of Covid-19. Japanese stocks rose for a second day as a weaker yen boosted the outlook for the nation’s exporters. “There are plenty of storms blowing through China right now,” said Jeffrey Halley, senior market analyst at Oanda Asia Pacific. “Fears continue to dog stock markets, that lockdowns could spread, which would severely impact China’s growth.” The risk of tighter monetary policies globally remained on investors’ minds as the Fed this week is expected to announce its first interest rate hike in three years in a bid to curb rising inflation amid surging commodity prices. Markets are now pricing in as many as seven quarter-point hikes for the full year.

Lockdowns in major Chinese cities are dimming the outlook for economic growth and posing risks for energy and raw-materials demand, just as concerns about the country’s relationship with Russia stoke a relentless stock selloff. The virus is also making a comeback in Europe: Germany on Tuesday set a fresh record for infection rates for the four straight day. Austria has also reached new highs, while cases in the Netherlands have doubled since lifting curbs on Feb. 25.

Japanese equities rose, extending their rebound to a second day, supported by gains in exporters on a weaker yen. Auto and chemical makers were the biggest boosts to the Topix, which climbed 0.8%. KDDI and Recruit were the biggest contributors to a 0.2% rise in the Nikkei 225, while Fast Retailing fell. The Japanese currency extended its loss against the dollar to a seventh-straight session, weakening more than 3% in that span. Despite its “haven” status,” the yen has dropped as Russia’s war in Ukraine has driven up prices of oil and other raw materials which Japan imports. “The market has already factored in a lot of bad news” regarding Russia and Ukraine, said Hajime Sakai, chief fund manager at Mito Securities. “The weakening of the yen is positive for exporting, but looking further on we need to think of the negative effect from import costs.”

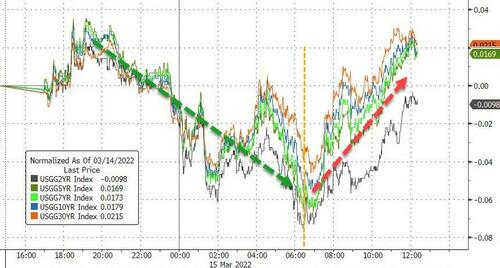

In rates, Treasuries unwound a portion of Monday’s sharp selloff with yields richer by up to 4.5bp across front-end of the curve into early U.S. session. U.S. 10-year yield near 2.12% is down ~2bp vs Monday’s close, outperforming bunds and gilts in the sector by ~1bp; 2-year yield drop back to ~1.83% after topping near 1.89% during Asia session. Gilts and bund curves bull-flatten while Treasuries bull-steepen; short-dated USTs outperform bunds and gilts by roughly 2bps.

In FX, the Bloomberg Dollar Spot Index fell 0.1% after rising to its highest level since July 2020 in early Asian trade. Treasury yields fell by up to 4bps led by the front-end after rising in early Asian session, when the 10-year yield climbed to 2.17%, the highest since June 2019. Antipodean currencies as well as the Canadian dollar and Norwegian krone were steady to lower as commodities extended losses. The euro extended an Asia session gain, to touch $1.1020 before paring. European benchmark bond yields also fell, yet underperforming Treasuries. Sweden’s krona advanced after inflation expectations rose considerably for the coming two years. Australia’s dollar pares reased an intraday loss, in part on short covering seen after Chinese economic data beat estimates. Reserve Bank said Russia’s invasion of Ukraine has the potential to prolong a period of elevated consumer-price growth and is clouding the economic outlook, minutes of its March 1 policy meeting showed. The yen whipsawed in the spot market as stocks and oil turned south, but options wagers suggest fresh lows versus the dollar may be in store. Whether the greenback can extend its recent rally and maintain its bullish momentum for long depends on options pricing changing course.

In commodities, crude futures decline. WTI drifts 5.3% lower to trade around $97.50. Brent falls 5.3% but holds above $101. Most base metals trade in the red; LME aluminum falls 2.3%, underperforming peers. LME tin outperforms, adding 0.4%. Spot gold falls roughly $17 to trade near $1,934/oz. Elsewhere, nickel trading will resume on the London Metal Exchange on Wednesday, over a week after being suspended amid a historic short squeeze.

Looking to the day ahead now, markets have PPI for February in the US. In Europe, Germany’s ZEW survey expectations, UK jobless claims change, ILO unemployment rate 3 months, Eurozone ZEW survey expectations and industrial production are all due. Elsewhere, housing starts and manufacturing sales in Canada will be released. Earnings include Volkswagen, RWE and Generali.

Market Snapshot

- S&P 500 futures down 0.4% to 4,154.75

- STOXX Europe 600 down 1.7% to 429.03

- MXAP down 1.7% to 165.53

- MXAPJ down 2.9% to 531.41

- Nikkei up 0.2% to 25,346.48

- Topix up 0.8% to 1,826.63

- Hang Seng Index down 5.7% to 18,415.08

- Shanghai Composite down 5.0% to 3,063.97

- Sensex down 1.4% to 55,702.16

- Australia S&P/ASX 200 down 0.7% to 7,097.45

- Kospi down 0.9% to 2,621.53

- Brent Futures down 5.7% to $100.79/bbl

- Gold spot down 0.9% to $1,934.19

- U.S. Dollar Index down 0.21% to 98.79

- German 10Y yield little changed at 0.33%

- Euro up 0.5% to $1.0995

Top Overnight News from Bloomberg

- Germany is preparing to boost the supply of a scarce bond entangled in Russian sanctions, a move that will likely ease pockets of tension in European repo markets. The nation is looking to sell on Tuesday an additional 5.5 billion euros ($6.1 billion) of the notes maturing 2024, which the German government believed became difficult to source after sanctions were imposed against some bondholders

- Chinese stocks suffered another deep selloff on Tuesday as concerns about the country’s ties with Russia and persistent regulatory pressure sent shares on a downward spiral. The Hang Seng China Enterprises Index, which tracks Chinese shares listed in Hong Kong, sank 6.6%, following a plunge in the previous session that was the biggest since the global financial crisis

- Fund managers are leery of buying Chinese stocks as the country’s close ties to Russia, extreme Covid-19 curbs and lack of clarity on the end of regulatory crackdowns overwhelm the dip buying opportunity presented by the 75% plunge from their peak

- China wants to avoid being impacted by U.S. sanctions over Russia’s war, Foreign Minister Wang Yi said, in one of Beijing’s most explicit statements yet on American penalties that are contributing to a historic market selloff

- The global economy is bracing for greater disruption as China scrambles to contain its worst outbreak of Covid-19 since the pandemic began

- Russia’s economy is fraying, its currency has collapsed, and its debt is junk. Next up is a potential default that could cost investors billions and shut the country out of most funding markets

- The dollar has powered ahead of every major currency over the past nine months due to the prospect of Federal Reserve interest-rate hikes but the end of its rally may be in sight, if history is any guide. The U.S. currency has weakened by an average of 4.1% during the Federal Open Market Committee’s four previous tightening cycles

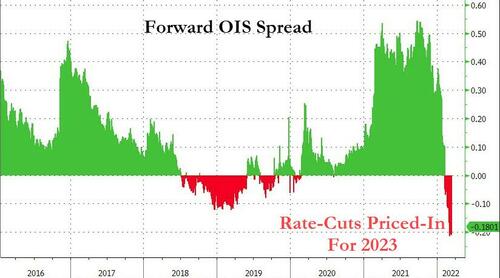

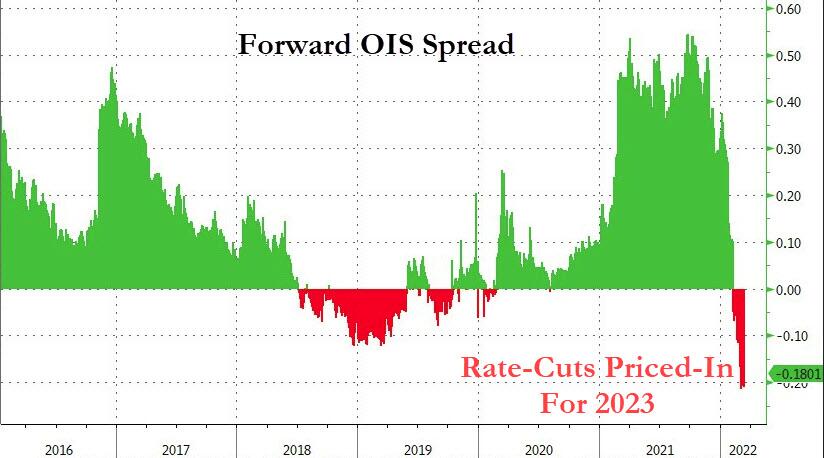

- Traders are ramping up their bets on the amount of Federal Reserve rate hikes in 2022 but are still toying with the possibility of a rate cut as soon as next year

- U.K. unemployment dropped below its pre- pandemic level for the first time as companies generated more jobs and granted higher wages than expected. The jobless rate fell to 3.9% in the three months through January, the lowest since the start of 2020

US Event Calendar

- 8:30am: Feb. PPI Final Demand YoY, est. 10.0%, prior 9.7%; MoM, est. 0.9%, prior 1.0%

- 8:30am: Feb. PPI Ex Food and Energy YoY, est. 8.7%, prior 8.3%; MoM, est. 0.6%, prior 0.8%

- 8:30am: March Empire Manufacturing, est. 6.1, prior 3.1

- 4pm: Jan. Total Net TIC Flows, prior -$52.4b

DB’s Jim Reid concludes the overnight wrap

Some hints of positive diplomatic developments in the Ukraine crisis that materialised on Sunday night helped contribute to another major sell-off in bonds and a mild risk on move in European equities yesterday. While in the States, the reality of the impending Fed tightening cycle pushed yields higher and drove equities lower.

Bonds are in a strange situation at the moment as we seem to have reached a point where higher energy prices are deemed to be signalling recessionary risks and encourage flight to quality flows that push nominal yields lower, outweighing the potentially savage inflationary impact. Conversely, the collapse in the likes of oil and gas since early last week has led to a huge rise in yields as it appears policy tightening is back on the central bank menu. Brent is around -25% from its intra-day highs last Tuesday and 10yr bunds are +46.6bps higher since hitting -0.10% last Monday morning. Meanwhile, 1-month futures on Dutch Gas have fallen from a high of 335 last Monday morning to 110.50 at the close last night. Remarkable moves.

On the conflict, Russia and Ukraine finished a fourth day of negotiations yesterday and decided to take a pause to assess outcomes. Still, it seems that negotiations are making some progress. Meanwhile, President Zelensky is set to address the US Congress tomorrow, while there were reports that President Biden was considering a trip to Europe to express the US’s steadfast support for NATO allies.

Overnight in Asia, most equity markets are down with Hong Kong and Chinese stocks leading regional losses. The Hang Seng (-3.56%) opened sharply lower, slipping more than 4% before recovering slightly as a resurgence of Covid-19 in Hong Kong and China and potential delisting of Chinese stocks from US exchanges weighed on sentiment. The Shanghai Composite (-2.18%) and CSI (-1.75%) are also down even if losses were pared following the release of stronger-than-anticipated economic data. A fresh lockdown in China’s Jilin province of 24 million people is offsetting this. Elsewhere, the Nikkei (+0.33%) is advancing while the Kospi (-0.56%) is lagging. Moving forward, equity futures on the S&P 500 (+0.17%) and Nasdaq (+0.47%) are higher while DAX contracts (-0.45%) are weak.

On that China data, industrial output rose a more-than-expected +7.5% y/y in January and February, (vs market estimates of +4.0%) and against a +9.6% gain in December while retail sales grew +6.7% y/y in the same period compared with analyst estimates of a +3.0% increase amid rising demand during the Lunar New Year holidays and the Winter Olympic Games. Meanwhile, fixed asset investment also beat, up by +12.2% y/y YTD in February and well above the forecast for a +5.0% increase. Separately, the People’s Bank of China (PBOC) unexpectedly kept the one-year medium-term lending facility rate (MLF) at 2.85%, resulting in a net injection of 100 billion yuan in fresh funds. The central banks’ action dashed hopes of a rate cut as the policymakers may want to avoid widening policy divergence with the US ahead of their expected hike tomorrow.

Oil prices have extended their recent declines this morning with Brent futures sliding -4.0% to trade at $102.64/bbl and with WTI futures -4.2%, breaking below $100/bbl. It saw a similar fall yesterday after opening the week above $109/bbl. Elsewhere, the yield on the 10-year US Treasury note is roughly flat at 2.138%.

As discussed at the top, the calm in yields overnight followed a rout yesterday. 10yr bunds eventually rose +11.9bps yesterday as risk premium eased, and to the highest level since November 2018. With a modest +2.2bps uptick in breakevens, most of the move was in real yields. Note that page 24 of the “Dislocations” chart book shows that 10yr real bund yields last week hit all-time low levels. Since those lows last week we’ve backed up +48.8bps. The move in other European sovereign yields was remarkably similar to bunds yesterday with BTPs (+11.3bps), Spanish (+11.0bps) and even Greek (+11.8bps) bonds seeing hardly any change in spreads.

US Treasury yields sold even more (10yr +14.1bps) and unlike in Europe, higher yields were met with falling breakevens (-2.3bps) with real yields +16.4bps putting in their biggest daily move since February 2021. No small feat given the considerable sell-off in real rates that marked the beginning of this year. The 2s10s (+2.8bps) curve steepened a little which might be welcomed by the Fed. Yields across the US curve notched fresh cycle highs, with those on 2y (+11.3bps) and 10y reaching the highest levels since summer 2019.

Notably, US futures moved to fully price in 7 Fed hikes in 2022 for the first time this cycle, in line with our US econ team’s view. While there were reports of incoming corporate issuance and hedging flows driving the Treasury rate sell-off, it appears markets are waking up to the magnitude of tightening the Fed is about to embark on, starting this week. If the war wasn’t enough to get the ECB to strike a dovish tone, the Fed will be all the more emboldened given fewer direct linkages to growth shocks from the conflict and the higher starting point for inflation. Indeed, in a new periodical we launched yesterday, Questions for the Chair, link here, DB Research personnel offer the questions they would ask Chair Powell at his FOMC press conference. A common question was wouldn’t policy rates need to be higher than current forecasts given the inflationary outlook. It seems markets are coming around to that view.

That line of thinking passed through to US equities, where the S&P 500 slid -0.74%. The tech-heavy NASDAQ, which is more exposed to rising rates, underperformed, falling -2.04%. Sector-wise, amid plummeting oil prices energy stocks (-2.93%) performed the worst after a sustained run of outperformance, while financials (+1.23%) were the top performers in the S&P 500 amid a steeper yield curve.

European stocks outperformed their American counterparts, with the positive geopolitical noise outweighing a tighter monetary policy path to push major indices into positive territory. The STOXX 600 rallied +1.20%, but gains in country-level benchmarks like the German DAX (+2.21%) and the French CAC 40 (+1.75%) were even more startling amid recent sharp underperformance relative to their US counterparts.

The same positive risk sentiment pushed commodity prices lower. We’ve already mentioned the slump in Oil but European gas prices also fell, with front month Dutch TTF contracts losing -17.29%. Oil prices fell despite no additional supply via Iran, US, Venezuela, or OPEC appearing likely. Instead, it seems as though Russian supply may make its way to buyers such as China and India with fewer frictions than were previously feared. As a secondary consideration, reports of Covid-19 lockdowns in China may have pushed prices lower due to potential lower demand needs.

Industrial metals lost steam as well, with aluminium and copper falling -4.69% and -2.24%, respectively, while gold lost -1.89% as markets revised geopolitical risks downwards.

One developing story with unclear implications so far is Russia’s request for Chinese support of its invasion. There have been conflicting reports about the veracity of the original claims. We do know that the US National Security Advisor met with his Chinese counterpart yesterday to try and dissuade China from offering any such support. One to keep a very close eye on.

To the day ahead now. In today’s data releases, markets have PPI for February in the US. In Europe, Germany’s ZEW survey expectations, UK jobless claims change, ILO unemployment rate 3 months, Eurozone ZEW survey expectations and industrial production are all due. Elsewhere, housing starts and manufacturing sales in Canada will be released. Earnings include Volkswagen, RWE and Generali.

END

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED DOWN 159.57 PTS OR 4.95% //Hang Sang CLOSED DOWN 1116,59 PTS OR 5.72 % /The Nikkei closed UP 38,63 PTS or 0.15% //Australia’s all ordinaires CLOSED DOWN 0.89% /Chinese yuan (ONSHORE) closed DOWN 6.3750 /Oil DOWN TO 103.25 dollars per barrel for WTI and DOWN TO 108.14 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3750. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.4090: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER//

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

3B JAPAN

3c CHINA

CHINA/COVID

Another 51 million citizens in China lockdown as numbers of COVID cases increase, with the entire north east province of Jilin hit along with Shenzhen.

China Orders 51 Million Into Lockdown As COVID Numbers Spike

MONDAY, MAR 14, 2022 – 08:40 PM

Beijing is learning the hard way that its “COVID Zero” approach toward combating the virus is having serious drawbacks. For example, while the US and Europe continue to roll back their tightening measures, a growing number of Chinese citizens are facing draconian lockdowns similar to the one imposed on Wuhan during the early days of the outbreak two years ago.

According to ABC News, the total number of Chinese citizens under lockdown rose to 51 million on Monday. Beijing has ordered a lockdown covering the entire northeastern province of Jilin, where 24 million people live. What’s more, the southern cities of Shenzhen and Dongguan, with 17.5 million and 10 million, respectively, have both been locked down in recent days.

China reported 1,437 cases across dozens of cities on Monday. That’s a four-fold increase within the span of a week.

Although the record number of new cases being reported is testing the feasibility of China’s zero-tolerance approach, there is still no sign that the country’s leadership is thinking about abandoning the policy altogether.

Authorities announced on Monday that 24 million people in Jilin Province would be forced into lockdown. That number includes the population of the previously locked down city of Changchun. Jilin’s lockdown marks the first province-wide lockdown since that of Wuhan and Hubei in January 2020.

The lockdown in Shenzhen threatens manufacturing and tech production in a city that’s home to Huawei and Tencent, along with one of the country’s main ports. As we noted earlier, the lockdown in Shenzhen has forced Apple supplier Foxconn to halt production of iPhones, which weighed on Apple shares earlier Monday.

While the lockdowns were initially given a short-term timeline of a week, authorities can always choose to extend them.

In keeping with the CCP’s propaganda, Professor Heiwai Tang at Hong Kong University told ABC News that he doesn’t expect these week-long lockdowns to have a significant impact on GDP growth.

“It seems the lockdowns will be shorter this time with more tracking, which means a short disruption of work and production,” Tang said. “If it ends up lasting for weeks it’s another issue, including inflation risks.”

Looking back, Professor Michael Song from Hong Kong’s Chinese University estimated that the two-month lockdown in Wuhan lopped 2 percentage points off China’s GDP growth.

Shanghai-based virologist Zhang Wenhong described the latest outbreak as “the most difficult moment in the past two years” of China’s efforts to stamp out the virus. Shanghai, China’s financial capital, has so far avoided a full-scale lockdown, but has faced some restrictions.

Many believe the most recent outbreak in mainland China likely traveled across the border from Hong Kong, which has seen case numbers soar over the past few weeks, prompting authorities to impose lockdowns and construct thousands of makeshift quarantine beds.

Mandatory quarantines and other strict anti-COVID measures have already taken their toll on the mental health of Chinese citizens: police reported 3 suicide attempts at one quarantine “camp” during the past day as of mid-morning on Monday in the Eastern US.

end

CHINA/

China’s stock market plummeted by 159.57 pts last night. The PBOC tried to give phony numbers hoping to convince people that their economy is good.

It did not work

(zerohedge)

Just As All Hope Seemed Lost, China Reports Miraculously Good Economic Data

MONDAY, MAR 14, 2022 – 10:40 PM

Going into Tuesday, all hope seemed lost in China.

First, China reported a whopping 5,154 new covid cases (3,507 new local confirmed Covid cases and 1,647 asymptomatic cases) for Monday, well more than double from the day before, and confirming that the country’s covid troubles – which over the past 48 hours led to the lockdown of Shenzhen and other cities – are only getting worse. So worse, in fact, that questions have emerged: how did China not report more than 100 cases on any one day for two years, and then now – with the Ukraine war raging – Beijing is suddenly locking down key US supply chain arteries.

Second, for the second day in a row, the PBOC fixed the yuan more than 100 pips weaker than expected, as the central bank telegraphs it will no longer tolerate a weak currency, relentless capital inflows be damned, as the country remembers that it is after all, an export-driven mercantilist which above all, needs a favorable exchange rate.

Third, one day after Chinese stocks traded in HK suffered their biggest drop since 2008, we are bracing for another major crash:

- ALIBABA SHARES INDICATED 9.8% LOWER IN HONG KONG

- MEITUAN SHARES INDICATED 11% LOWER IN HONG KONG

Elsewhere, China’s CSI 300 Index tuimbled 2.5%, while the Shanghai Composite declined 2.4% and the Hang Seng fell 3.7%, while the Hang Seng Tech Index lost as much as 7.2% soon after open Tuesday, and is now down almost 40% in under a month.

Why? Because contrary to expectations set by the PBOC itself (via its own media mouthpiece), the PBOC decided to keep the MLF rate unchanged despite an intensifying rout in nation’s equities, adding to investor concerns from lockdowns to geopolitical and regulatory risks.

And then, as even the firmest China believers were getting ready to throw in the towel, moments ago the National Bureau of Statistics reported a trio February economic numbers that were so ridiculously good they were, well… simply ridiculous. To wit:

- Jan.-Feb. Industrial Output +7.5%, y/y, smashing estimates of +4%, printing above the highest economist forecast (range +3.2% to +5.5%, 24 economists) and far higher than the Ded +4.3%.

- Jan.-Feb. Retail Sales +6.7% y/y; smashing est. +3%, printing above the highest economist forecast (range +1.5% to +5.5%, 23 economists), and far, far higher than the Dec. +1.7%

- Jan.-Feb. Fixed-Asset Investment excluding rural households +12.2% y/y; smashing est. +5% and also printing above the highest economist forecast (range +3% to +9%, 29 economists) as well as more than 2x higher than Jan.-Dec. +4.9%

While the above data was the most closely watched, not all the data was flawless:

- Jan.-Feb. property investment +3.7% y/y vs +4.4% in Jan.-Dec.

- Jan.-Feb. residential property sales -22.1% y/y vs +5.3% in Jan.-Dec.

- End- Feb. surveyed jobless rate 5.5% vs 5.1% end-Dec.

Then there were the tertiary data:

- China Jan.-Feb. Power Output Rose 4% Y/y to 1314.1b kwh

- China Feb. Power consumption rises 16.9% Y/Y, to 623.5 billion kilowatt-hours (kWh), the state TV reports, citing the National Energy Administration.

- Power output in Jan.-Feb. rose 4% y/y to 1314.1b kwh

- Crude processing in Jan.-Feb. fell 1.1% y/y to 113.01m tons

- Crude oil output in Jan.-Feb. rose 4.6% y/y to 33.47m tons

- Natural gas output in Jan.-Feb. rose 6.7% y/y to 37.2bcm

- Ethylene output in Jan.-Feb. rose 3.9% y/y to 4.87m tons

- Coal output in Jan.-Feb. rose 10.3% y/y to 686.6m tons

China’s apparent oil demand, which includes oil processing volume and net imports of refined oil products, remained stable in the first two months of the year, despite higher prices: China’s apparent oil demand rose 2.89% in January-February from a year earlier, to 13.710m b/d.

A closer read of the data hints that not all was as strong as indicated: the growth in retail sales was driven by a surge in petroleum and jewelry which saw the highest increase across all categories. That, as Bloomberg notes, could be the impact of price increase, instead of volume.

Still, the fact that the big 3 were so stellar should placate those who are seeing a collapse (even if nobody actually believes these numbers).

So why did Beijing report such ridiculous prints? Well, one possible reason is to justify the PBOC’s decision earlier in the session to hold the key, MLF interest rate unchanged instead of cutting it as analysts expected.

Either that, or to justify what would be a powerful Plunge Protection intervention immediately after the data, and sure enough:

- *HANG SENG TECH INDEX ERASES LOSS OF AS MUCH AS 7.2%

- *TENCENT PARES LOSS TO 0.5% FROM AS MUCH AS 8%

And as goes China, so go US equity futures…

end

China is uninvestable!

(zerohedge)

“The Market Is Crazy” – Despite ‘Miraculous’ Macro Data, Chinese Stocks Remain “Uninvestable”

TUESDAY, MAR 15, 2022 – 11:45 AM

Despite what some described as a “miraculousy timed” good economic data last night, the selling in Chinese stocks continues unabated as anxiety over a resurgent COVID, blowback concerns over Russia-ties, domestic regulatory fears, and recently weak credit data all piled up to drag the market to its lowest relative valuation versus the world on record…

Source: Bloomberg

“When faith is gone, people are ready to see a dark shadow in everything, some are even suspicious of the solid economic figures today,” said Yu Yingbo, an investment director at Shenzhen Qianhai United Fortune Fund Management Co Ltd.

“It’s just a planned, persistent and synchronized selling.”

The collapse, as we detailed earlier, has been heavily focused on the tech sector with the Hang Seng Tech Index crashing 8.1% (extending declines from a February 2021 peak to nearly 70%) amid what Bloomberg describes as its greatest intraday swing in history…

Source: Bloomberg

But what feels capitulative may just be getting going as Jeffrey Halley, senior market analyst at Oanda Asia Pacific, warns “there are plenty of storms blowing through China right now,” adding that “fears continue to dog stock markets, that lockdowns could spread, which would severely impact China’s growth.”

“The selloff is overdone, but so is everything else,” said Andy Maynard, head of equities at China Renaissance Securities.

“The market is crazy — there’s no fundamentals anymore. This might be worse than the 2008 financial crisis.”

JPMorgan analysts have even labeled some Chinese internet names as “uninvestable”.

“We are underweight Chinese equities due to several factors,” said Cesar Perez Ruiz, chief investment officer of Pictet Wealth Management, citing the nation’s zero-Covid policy that’s affecting growth as one of the reasons.

“The tech sector will continue to suffer from regulation challenges plus the risk of U.S. delisting and penalization of growth stocks as rates continue to normalize.”

And of course, for the world’s investors – now conditioned to expect every dip to be rescued by a Fed Put (and dissonant that The Fed is now selling calls) – hope is rapidly becoming a four-letter word as the market is now anticipating an inflation-fighting Fed will hike 7 times in 2022…

Source: Bloomberg

…and the crushing collapse in credibility of any Fed reversal from its hawkish positioning now would likely (after an initial breathless recovery) lead to far worse outcomes.

And the PBOC’s recent actions (holding rates rather than cutting as expected) disappointed a demanding investor base expecting to be bailed out.

end

CHINA//USA//RUSSIA/UKRAINE

China angry at the uSA over “smears” on Russian assistance. They are stating that they are not a party to this war.

(zerohedge)

China Warns Of Retaliation Amid US “Smears” Over Russian Assistance, Says “Not A Party” To This War

TUESDAY, MAR 15, 2022 – 07:25 AM

The Chinese Foreign Ministry warned on Tuesday that China would retaliate following a series of US statements which told Beijing not to assist Russia in either sanctions evasion or military equipment support for its Ukraine war.

“We call on the US not to harm China’s legitimate rights and interests when handling its relations with Russia,” ministry spokesperson Zhao Lijian stressed – however at this point it’s still at the level of US warnings and accusations, also after reports said that Moscow has even requested drones.

Zhao in a daily briefing was asked if China fears US sanctions amid charges that it’s quietly supporting Russia’s war effort in Ukraine: “The Chinese side has repeatedly expressed its position regarding sanctions. Beijing discourages the use of sanctions to settle problems and even more opposes unilateral sanctions that lack international legal grounds,” Zhao said.TASS/Getty Images

And separately Chinese Foreign Minister Wang Yi China in a phone call to his Spanish counterpart stressed that “China is not a party to the crisis, nor does it want sanctions to affect China.” Wang said in the Monday statements discussing the Ukraine crisis.. “China has the right to safeguard its legitimate rights and interests.”

Calling the Ukraine war part of “European security conflicts” which have built up over the years, the top diplomat said China stands for negotiations and dialogue and rejects sanctions. He said in what can be seen as a likely indirect defense of Moscow: