march 23, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

MARCH23

GOLD; $1937.15 UP $15.75

SILVER: $25.06 UP $0.24

ACCESS MARKET: GOLD $1945.00

SILVER: $25.13

Bitcoin morning price: $42,053 DOWN 545

Bitcoin: afternoon price: $42,301 DOWN 307

Platinum price: closing DOWN $5.45 to $1021.00

Palladium price; closing UP $73.95 at $2521.50

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

March: JPMorgan stopped/total issued 5/10

EXCHANGE: COMEX

CONTRACT: MARCH 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,920.700000000 USD

INTENT DATE: 03/22/2022 DELIVERY DATE: 03/24/2022

FIRM ORG FIRM NAME ISSUED STOPPED

363 H WELLS FARGO SEC 1

435 H SCOTIA CAPITAL 3

661 C JP MORGAN 5

709 C BARCLAYS 1

880 C CITIGROUP 10

TOTAL: 10 10

MONTH TO DATE: 11,520

NUMBER OF NOTICES FILED TODAY FOR Mar. CONTRACT 10 NOTICE(S) FOR 1000 OZ (0.0311 TONNES)

total notices so far: 11,520 contracts for 1,152,000 oz (35.832 tonnes)

SILVER NOTICES:

19 NOTICE(S) FILED TODAY FOR 95,000 OZ/

total number of notices filed so far this month 10,487 : for 52,435,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD UP $15.75

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD//

INVENTORY RESTS AT 1083.60 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 24 CENTS

AT THE SLV// NO CHANGES IN SILVER INVENTORY AT THE LV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 550.288 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 2516 CONTRACTS TO 155,456 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED WITH OUR $0.29 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.29) BUT WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A TINY LOSS OF 170 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A VERY STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 42.860 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 105,000 OZ //NEW STANDING 52.690 MILLION OZ // V) STRONG SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -240

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTACTS for 17 days, total contracts: : 32,051 contracts or 160.225 million oz OR 9.42 MILLION OZ PER DAY. (1885 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 32,051 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 160.224 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 160. 224 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2516 WITH OUR $0.16 LOSS IN SILVER PRICING AT THE COMEX// TUESDAY THE CME NOTIFIED US THAT WE HAD A VERY STRONG SIZED EFP ISSUANCE OF 2106 CONTRACTS( 2106 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAR. OF 42.860 MILLION OZ FOLLOWED BY TODAY’S 105,000 OZ QUEUE JUMP//NEW STANDING 52.690 MILLION OZ// /// .. WE HAD A SMALL SIZED LOSS OF 410 OI CONTRACTS ON THE TWO EXCHANGES FOR 2.050 MILLION OZ WITH THE SMALL LOSS IN PRICE.

WE HAD 19 NOTICES FILED TODAY FOR 95,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 5698 CONTRACTS TO 605,191 AND FURTHER CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: —759 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE GOOD SIZED DECREASE IN COMEX OI CAME WITH OUR LOSS IN PRICE OF $7.75//COMEX GOLD TRADING/TUESDAY/.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MARCH AT 14.818 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 1600 OZ//NEW STANDING 36.298 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $7.75 WITH RESPECT TO FRIDAY’S TRADING

WE HAD AN SMALL SIZED GAIN OF 1204 OI CONTRACTS (3.744 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6902 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 605,191.

IN ESSENCE WE HAVE AN FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1204, WITH 5698 CONTRACTS DECREASED AT THE COMEX AND 6902 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1204 CONTRACTS OR 3.744 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (6902) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (5698,): TOTAL GAIN IN THE TWO EXCHANGES 1204 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR MARCH. AT 14.818 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 1600 OZ//NEW STANDING 36.298 TONNES /// 3) ZERO LONG LIQUIDATION ///. ,4) STRONG SIZED COMEX OI. LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MARCH

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

107,673 CONTRACTS OR 10,767,300 OR 334.90 TONNES 17 TRADING DAY(S) AND THUS AVERAGING: 6333 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES: 334.90TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 334.90/3550 x 100% TONNES 9.43% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 334.90 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE MONTH.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL.WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MARCH HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 2516 CONTRACTS TO 155,456 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 2106 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 2106 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2106 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2516 CONTRACTS AND ADD TO THE 2106 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED LOSS OF 410 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 2.050 MILLION OZ,

OCCURRED WITH OUR SMALLISH $0.29 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 11.17 PTS OR 0.34% //Hang Sang CLOSED UP 264.80 PTS OR 1.21 % /The Nikkei closed UP 816.05 PTS OR 2.00% //Australia’s all ordinaires CLOSED UP 0.58% /Chinese yuan (ONSHORE) closed DOWN 6.3727 /Oil UP TO 111.99 dollars per barrel for WTI and UP TO 118.95 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3737. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3879: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER//

A)NORTH KOREA/

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 5698 CONTRACTS TO 605,191 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED DESPITE OUR LOSS OF $7.75 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (1364 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE NON ACTIVE DELIVERY MONTH OF MAR.. THE CME REPORTS THAT THE BANKERS ISSUED A VERY STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 6902 EFP CONTRACTS WERE ISSUED: ;: , & FEB. 0 APRIL:6902 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6902 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 1204- CONTRACTS IN THAT 6902 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI LOSS OF 5698 CONTRACTS..AND THIS SMALL GAIN OCCURRED WITH THE LOSS IN PRICE OF $7.75.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAR (36.298),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.298 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $7.75) BUT THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A SMALL SIZED GAIN OF 6.1057 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAR (36.298 TONNES)…

WE HAD -759 CONTRACTS SUBTRACTED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1204 CONTRACTS OR 120400 OZ OR 63.744 TONNES

Estimated gold volume today: 179,166 ///poor

Confirmed volume yesterday: 207,806 contracts poor

INITIAL STANDINGS FOR MAR ’22 COMEX GOLD //MARCH 23

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 46,789.663 oz Manfra Brinks Int Delaware all kilobars Brinks 48 int Delaware 39 Manfra: 1362, oz |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 10 notice(s)1100 OZ 0.0311 TONNES |

| No of oz to be served (notices) | 150 contracts 15000 oz 0.4666 TONNES |

| Total monthly oz gold served (contracts) so far this month | 11,520 notices1,152,000 OZ 35.832 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit nil oz

No dealer withdrawal 0

0 customer deposits

total customer deposit: nil oz

total gold deposits in tonnage: nil tonnes

3 customer withdrawal

i) Out of Brinks 1543.25 oz (48 kilobars)

ii) out of Int. Delaware 964.53(30 kilobars)

iii) Out of Manfra: 43,789.663 oz (1362 kilobars

total withdrawals: 46,397.442 oz

ADJUSTMENTS: 1

manfra..// customer to dealer//385,812 oz (12 kilobars)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MARCH.

For the front month of MARCH we have an oi of 160 contracts having LOST 5

We had 21 notices filed yesterday so we gained 16 contracts or 1600 oz will stand at the comex as these guys refused to be EFP’d over to London.

Our banker friends have run out of gold metal everywhere.

April saw a loss of 25,921 contracts down to 172,707.

May saw a GAIN of 43 contracts to stand at 4392

June saw a GAIN of 19,636 contracts up to 356,933 contracts

We had 10 notice(s) filed today for 1000 oz FOR THE MAR 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 19 notices were issued from their client or customer account. The total of all issuance by all participants equates to 10 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 5 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR /2021. contract month,

we take the total number of notices filed so far for the month (11,520) x 100 oz , to which we add the difference between the open interest for the front month of (MAR: 160 CONTRACTS ) minus the number of notices served upon today 10 x 100 oz per contract equals 1,165,400 OZ OR 36.298 TONNES the number of TONNES standing in this active month of mar.

thus the INITIAL standings for gold for the MAR contract month:

No of notices filed so far (11,520) x 100 oz+ (160) OI for the front month minus the number of notices served upon today (10} x 100 oz} which equals 1,165,400 oz standing OR 36.298 TONNES in this NON active delivery month of MAR.

TOTAL COMEX GOLD STANDING: 36.298 TONNES (A WHOPPER FOR A MAR (NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

191,133,764.7, oz NOW PLEDGED /HSBC 5.94 TONNES

99,258.893 PLEDGED MANFRA 3.08 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690 tonnes

243,923.704, oz JPM No 2 7.58 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonnes

Loomis: 18,615.429 oz

total pledged gold: 1,506,092.234 oz 46.84 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 34,445,439.080 OZ (1071.39TONNES)

TOTAL ELIGIBLE GOLD: 16,752,298.506 OZ (521.06 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,693,140.574 OZ (550.34 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 16,187,048.0 OZ (REG GOLD- PLEDGED GOLD) 503.49 tonnes

END

MAR 2022 CONTRACT MONTH//SILVER//MARCH 23

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 802,000.690 oz Delaware CNT Manfra |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 338,737.240 oz Delaware |

| No of oz served today (contracts) | 19CONTRACT(S) 95,000 OZ) |

| No of oz to be served (notices) | 51 contracts (255,000 oz) |

| Total monthly oz silver served (contracts) | 10487 contracts 52,435,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

i) Into Delaware: 338,737.240 oz

total deposit: 338,737.240 oz

JPMorgan has a total silver weight: 180.228 million oz/340.961 million =52.86% of comex

ii) Comex withdrawals: 3

A) Out of CNT: 99,560.470 oz

ii) Out of Delaware: 2006.000 oz

iii) Out of HSBC: 600,341.700 o

total withdrawal 802,000.690 oz

one adjustment:

Manfra/dealer to customer 205,613.728 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 92.243 MILLION OZ

TOTAL REG + ELIG. 340.961 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR MARCH

silver open interest data:

FRONT MONTH OF MARCH OI: 70, HAVING GAINED 16 CONTRACTS FROM TUESDAY.

WE HAD 5 NOTICES SERVED UPON YESTERDAY, SO WE GAINED 21 CONTRACTS OR AN ADDITIONAL 105,000 OZ WILL STAND

FOR DELIVERY OVER HERE AS THESE GUYS REFUSED TO BE EFP’D TO LONDON.

APRIL HAD A 54 CONTRACT LOSS// CONTRACTS LOWERS TO 54

MAY HAD A LOSS OF 1951 CONTRACTS UP TO 117,117 contracts

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 19 for 95,000 oz

Comex volumes: 32,199// est. volume today//poor/

Comex volume: confirmed yesterday: 49,657 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in MAR. we take the total number of notices filed for the month so far at 10,487 x 5,000 oz = 52,435,000 oz

to which we add the difference between the open interest for the front month of MAR (70) and the number of notices served upon today 19 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2021 contract month: 10,487 (notices served so far) x 5000 oz + OI for front month of MAR (70) – number of notices served upon today (19) x 5000 oz of silver standing for the MAR contract month equates 52,690,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MARCH 23/WITH GOLD UP $15.75//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1083.60 TONNES

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

MARCH 21//WITH GOLD UP $.25 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.00 TONNES INTO THE GLD////INVENTORY RESTS AT 1082.44 TONES

MARCH 18/WITH GOLD DOWN $13.55 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1073.44 TONES

MARCH 17/WITH GOLD UP $33.50: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.61 TONNES INTO THE GLD//INVENTORY RESTS AT 1073.44 TONNES

MARCH 16/WITH GOLD DOWN $18.50//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.33 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.83 TONNES

MARCH 15/WITH GOLD DOWN $30.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1064.16 TONNES

MARCH 14//WITH GOLD DOWN $22.75, HUGE CHANGES IN GOLD INVENTORY AT THE GLD//STRANGE: A DEPOSIT OF 2.62 TONNES INTO THE GLD.//INVENTORY RESTS AT 1064.16 TONNES

MARCH 11/WITH GOLD DOWN $14.60: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1061.54 TONNES

MARCH 10//WITH GOLD UP $11.55: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FORM THE GLD///INVENTORY RESTS AT 1063.28 TONNES

MARCH 9/WITH GOLD DOWN $53.85//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.64 TONNES INTO THE GLD//INVENTORY RESTS AT 1067.34 TONNES

MARCH 8/WITH GOLD UP $46.10: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 8.42 TONNES INTO THE GLD///INVENTORY RESTS AT 1062.70 TONNES

MARCH 7/WITH GOLD UP $28.40 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1054.28 TONNES

MARCH 4/WITH GOLD UP $28.40//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1050.22 TONNES

MARCH 3/WITH GOLD UP $13.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 7.84 TONNES//INVENTORY RESTS AT 1050.22 TONNES

MARCH 2/WITH GOLD DOWN $20.80//A MONSTER CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 13.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1042.38 TONNES

MARCH 1/WITH GOLD UP $42.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: //INVENTORY RESTS AT 1029.32 TONNES

FEB 28/WITH GOLD UP $12.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 25/WITH GOLD DOWN $38.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 24/WITH GOLD UP $17.35//A HUGE CHANGE AT THE GLD: 5.23 TONNES INTO THE GLD// IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1029.32 TONNES

FEB 23/WITH GOLD UP $2.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1024.09 TONNES

FEB 22/WITH GOLD UP $6.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1024.09 TONNES

FEB 18/WITH GOLD DOWN $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 17/WITH GOLD UP $29.50: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 16/WITH GOLD UP 414.60 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 15/WITH GOLD DOWN $12.70 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 14/WITH GOLD UP $27.20 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 11/WITH GOLD UP $4.50 A HUGE CHANGE IN GOLD IVNETORY AT THE GLD// A DEPOSIT OF 3.48 TONNES INTO THE GLD//INVENTORY RESTS AT 1019.44 TONES

CLOSING INVENTORY FOR THE GLD//1083.44 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 23/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 21/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 18/WITH SILVER DOWN 37 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 17/ WITH SILVER UP 72 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.049 MILLION OZ INTO THE SLVV//INVENTORY RESTS AT 548.071 MILLION OZ

MARCH 16/WITH SILVER DOWN 56 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 462,000 OZ FROM THE SLV//INVENTORY RESTS AT 544.560 MLLION O

MARCH 15/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.022 MILLION OZ

MARCH 14/WITH SILVER DOWN 64 CENTS TODAY; STRANGE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.125 MILLION OZ/INVENTORY RESTS AT 545.022 MILLIONOZ

MARCH 11/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ

MARCH 10/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ/

MARCH 9/WITH SILVER DOWN 88 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.174 MILLION OZ OF FAKE SILVER.//INVENTORY RESTS AT 542.897 MILLION OZ//

MARCH 8/WITH SILVER UP 88 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV////INVENTORY RESTS A 548.071 MILLION OZ//

MARCH 7/WITH SILVER UP 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 4/WITH SILVER UP 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ/

MARCH 3/WITH SILVER UP 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.32 TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 198,000 OZ FROM THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 1/WITH SILVER UP $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 546.052 MILLION OZ//

FEB 28/WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 546.052 MILLION OZ//

FEB 25/WITH SILVER DOWN 64 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.510 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 546.052 MILLION OZ/

FEB 24/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ

FEB 23/WITH SILVER UP 22 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ//

FEB 22/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 350,000 OZ INTO THE SLV///INVENTORY RESTS AT 551.597 MILLION OZ//

FEB 18/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.017 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 551.227 MILLION OZ

FEB 17/WITH SILVER UP 31 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.402 MILLION OZ//INVENTORY RESTS AT 550.210 MILLION OZ/

FEB 16/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.808 MILLIONOZ

FEB 15/WITH SILVER DOWN 46 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.808 MILLION OZ//

FEB 14/WITH SILVER UP 49 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.235 MILLION OZ INTO THES LV////INVENTORY RESTS AT 547.808 MILLION OZ

FEB 11/WITH SILVER DOWN 18 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ///

SLV FINAL INVENTORY FOR TODAY: 550.288 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: Beware Of Gold Scams

WEDNESDAY, MAR 23, 2022 – 06:30 AM

Gold is an important part of your investment portfolio. But when you’re buying gold, you don’t want to overpay and you need to be on the lookout for scams.

In a recent podcast, Peter Schiff said he doesn’t view gold as an “investment.” He considers gold “savings.”

Instead of holding dollars, or holding euros, I’m holding real money. I’m holding gold.”

Of course, there is volatility in the price of gold, just like there’s volatility in the price of every currency.

If you decide to hold Swiss francs instead of US dollars, every day, those Swiss francs are going to change in price. There’s an exchange rate between the dollar and the Swiss franc. Well, there’s an exchange rate between the dollar and gold. There’s an exchange rate between every currency and gold. I think gold is the only real money and therefore, I would rather own it relative to its fiat alternatives that are inferior.”

The key is to buy physical gold from a reputable dealer and don’t overpay.

When you buy physical gold, there are two main components to the price you’ll pay.

- The first is the spot price. That represents the market price of the metal when you buy it. It’s the “price of gold” you see quoted in the financial media every day.

- The second component is the premium, an amount over the spot price. This is how sellers cover their overhead and make a profit. (There are also applicable taxes, and depending on the amount of gold you buy, you will also likely pay shipping.)

SchiffGold has some of the lowest premiums in the industry.

In his podcast, Peter shared an experience related to him by a SchiffGold customer. He initially tried to buy gold from a competitor and was hit with the “bait and switch” scam. In fact, a lot of companies do this.

The customer was shopping for American Gold Eagles. He got a price from SchiffGold and then found a lower price from another company. The customer wanted SchiffGold to match the competitor’s price, but it was so low we couldn’t match it. So, the customer decided to take advantage of the lower price and buy from the other company.

The first red flag was the company wanted him to wire all of the money to them first.

They wouldn’t even lock in the price. They said, ‘If you want to buy these coins, you need to send us all the money, and then once we get the money in our bank account, well, then you can buy the coins.’”

SchiffGold doesn’t do business that way. We’ll let you lock in the price in advance and send the money later.

We trust you to make good on your commitment to buy gold. And we give you an honest price right off the bat.”

So, the customer sent his money to this other company to take advantage of this great deal. But once he sent the money, the company told him the price was no longer available. Not only was the deal unavailable, but the new price wasn’t even close to what SchiffGold quoted.

Then came the switch.

The salesman tried to talk the customer into buying overpriced fractional coins. The price was about $700 above the spot price of gold. Peter called it a “complete, total ripoff.”

Yet, this is what the salesman at this gold company is trying to get him to buy once the money came in. That’s why it’s a ‘bait-and-switch.’ You catch the customer with the bait. You dangle the bait of these cheap US Gold Eagles, and then when someone takes the bait and they send you the money, then you switch over and try to sell them something completely different than what they sent you the money to buy.”

It’s important to remember that a lot of these salespeople are not fiduciaries. They don’t care about you.

They just want to make the most money possible. So, they’re going to push you to buy the most overpriced coins that they’re selling. They’re like used car salesmen.”

One of the reasons a lot of these gold sellers have to charge so much is the high overhead. They pay millions on celebrity endorsers and commercials on the big networks.

These celebrities get a lot of money and the only way you can afford to pay them a lot of money is if you get it back from your customers by ripping them off.”

If these salespeople sell you a legitimate coin like an American Gold Eagle or a Canadian Maple Leaf at a price as low as Schiffgold, they won’t make any money. They’ll make a lot more money selling you overpriced products.

Thus the bait-and-switch.

They will give you all kinds of reasons the coins they’re hawking are better. Most of it is just hot air. They’ll claim the government can’t confiscate them or that they aren’t reportable to the IRS.

And if they already have your money in hand, it’s a lot easier to pressure you.

But the bottom line is they are not selling the gold that’s best for you. They’re selling the gold that’s best for the salesperson.

This customer didn’t fall for it. He made them send his money back and bought his American Eagles from SchiffGold.

You can count on SchiffGold to offer great prices on quality gold and silver bullion products. It may not always be the lowest price out there, but it will be close.

What you’ll always get from SchiffGold is honesty and integrity. Nobody is going to bait-and-switch. Nobody is going to push you into these overpriced coins. No one is going to try to turn you into a coin collector as opposed to a gold or silver investor. I know that because I make sure of that.”

For more information on gold scams, download our free report at the link below.

END

Peter Schiff: This “Everything Is Great” Attitude Can’t Last Forever

WEDNESDAY, MAR 23, 2022 – 01:09 PM

Despite rising interest rates and more hawkish talk from Federal Reserve Chairman Jerome Powell, the stock markets keep pushing upward. Everybody seems to think the Fed has things under control and everything will be just fine. In his podcast, Peter explained why this “everything is great” attitude will have to come to an end.

The markets don’t seem to comprehend how much has changed since the Federal Reserve embarked on its last tightening cycle.

We’re no longer in this world where the Fed can simply pretend that there’s no inflation. Because inflation is so much higher now than it was at any prior point for the beginning of a tightening cycle. And the economy is also in a much more precarious situation than it typically is when the Fed is hiking rates.”

Despite Jerome Powell and others claiming that the economy is strong, this is really an environment where you would typically expect the Fed to cut rates and launch a new QE program to stop the economy from sliding into a recession.

But the Fed has an inflation problem that it can no longer ignore. It can’t pretend inflation is transitory and that it will go away on its own.

They now have to actively engage in doing something about it. And so, that’s one of the reasons that this cycle is going to be very different from the ones that preceded it. And it’s going to end very differently.”

But the markets aren’t bracing for this.

Bonds have gotten clobbered over the last few days. Yields have risen significantly, though they remain low in historical terms. The markets seem sanguine about the carnage in the bond market. Peter said perhaps investors think we are close to the top of the rise in rates because they’ve become so accustomed to a low rate environment. But the only thing that will stop interest rates from rising is a pivot by the Fed. And as long as the markets ignore the situation and continue to rise, there is no reason for the Fed to pivot.

Remember, the only reason Powell is confident that the Fed can raise rates and shrink its balance sheet is because Powell is convinced we have this super-strong economy. And one of the reasons for the economic strength is the stock market. So, as long as the stock market is going up, Powell has no reason to question that narrative that the economy is strong.”

Keep in mind, the Fed doesn’t even have to tighten. Interest rates will rise in anticipation when Powell talks about tightening. This is likely the reason he came out this week and floated the idea of 50 basis point hikes in the future. He wanted to see how the markets would react.

As long as Powell remains on this path, interest rates are going to keep going up — until the stock market rolls over.”

Rising interest rates will have a significant negative impact on the economy. After all, the US economy is built on borrowing and spending. When the cost of borrowing rises, the economy slows down. But it will take a while before the impact of rising rates on the economy becomes obvious. The stock market is really the canary in the coal mine.

If the market tanks, that’s obvious right away. … So, as long as the market ignores rising interest rates, interest rates will keep rising.”

But at some point, rates will rise high enough that the market can no longer ignore it. Peter said he doesn’t know what the level is, but we’re going to find out pretty soon.

The yield curve has inverted, signaling investors think the rate hikes will cause a recession. On Tuesday, the yield on the 5-year Treasury was 2 basis points higher than the yield on the 10-year. Peter said he agrees with the recession expectation. But the markets think the Fed will respond the way it always does. They expect the Fed to cut rates and yields to fall again. They expect more quantitative easing. And they expect everything will be fine. They think the recession will end inflation. But Peter said at some point, the easy money cycles have to come to an end.

There is no way it can go on forever. It’s just that the people who are buying these bonds, the people who are in the market, have no conception of this reality. They somehow believe that it can go on forever. And they expect that when the Fed goes back to QE and goes back to zero, it’s just going to be another cycle just like the ones we’ve had in the past.”

But again, there is a difference this time.

Inflation.

We already have a huge inflation problem that didn’t exist in the prior cycles.

And so, when the US economy tips over into recession, inflation is still going to be well north of the Fed’s 2% target. And so, there’s no justification for the Fed to go back to zero and back to QE when we still have an inflation problem that has not been solved.”

If Powell and Company are serious about price stability, if they really want to rein in inflation, they will have to ignore the coming recession and the bear market in stocks and bonds. And if they don’t rein in inflation, at some point they will kill the dollar.

The question is will they be willing to do it?

In this podcast, Peter also talks about stagflation, how the next round of QE will be different from the last four, the economy’s addiction to cheap money, and more on the inflation problem.

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

-END

–WALL STREET ON PARADE

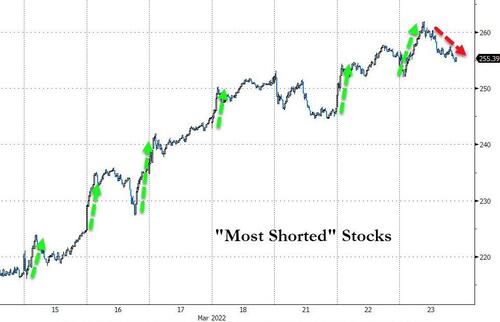

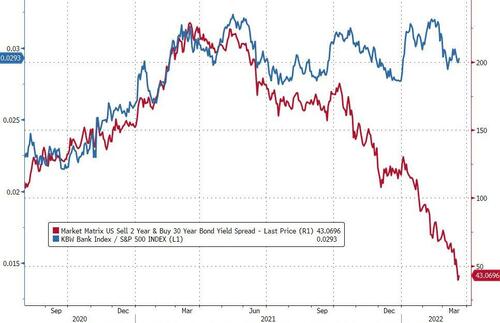

These 3 Charts Strongly Suggest the U.S. Stock Market Has an Invisible Hand Propping It UpBy Pam Martens: March 23, 2022As someone who has watched trading screens for the past 36 years, it’s pretty easy to spot a fake market. As the charts below indicate, there is an invisible hand (or hands) pushing this stock market up when it should be plunging. The likely suspects are U.S. Treasury Secretary Janet Yellen’s Plunge Protection Team, known as the Exchange Stabilization Fund; foreign central banks that are aligned with the U.S. position on Ukraine and want to help stabilize financial markets in the West; hedge funds and Wall Street’s Dark Pools owned by megabanks that are net long the market; or a combination of all of the above.One thing’s for sure, the stock market is not responding in a normal fashion to soaring inflation, a hawkish Fed, spiking interest rates, and military aggression by an out-of-control dictator with 6,000 nuclear warheads.Consider the chart below: since the Russian invasion of Ukraine on February 24, the yield on the 10-year U.S. Treasury note has skyrocketed by 20 percent, currently reaching 2.38 percent. That was a correct and normal reaction since inflation is already soaring in the U.S. and the military aggression is going to disrupt oil and gas supplies from Russia via sanctions, thus likely pushing commodity prices even higher. In a normally functioning stock market, an increase in yield of that magnitude on the 10-year Treasury note would have caused the stock market to plunge. Instead, per the chart below, the S&P 500 stock index has actually risen 5 percent since the Russian invasion of Ukraine.The stock market’s bizarre behavior is further evidenced by the chart below. It shows how the S&P 500 stock index has performed in relation to the S&P GSCI commodity index since the Russian invasion of Ukraine on February 24. Notice particularly how the dramatic spike in commodity prices between February 24 and March 8 was not met with a dramatic plunge in stock prices during that same period. It should have been. Then there is the equally important fact of a big yawn from the stock market as a nuclear power invades a sovereign nation of 44 million people, bombs its cities and towns to rubble, and persists in making threats against the U.S. and allies that are supporting Ukraine.And, finally, there is the disparate reaction of the stock market versus the correct share price reaction of the global banks that will be impacted by the Russian invasion. The chart below shows the radically different response from the stock market, as measured by the S&P 500 index, versus global banks since February 1, 2022. We selected the date of February 1 because that was the point at which Russia had amassed 100,000 troops near Ukraine’s borders, backed up with tanks and artillery. The global banks shown on the chart below are those with significant exposure to Russia. The worst performing of these, Austria’s Raiffeisenbank, has lost 50 percent of its value while the S&P 500 is down less than one percent from February 1 as of yesterday’s market close.The stock market is supposed to be an efficient pricing mechanism. When it stops efficiently pricing risk, it loses the public’s confidence. Those invisible hands should think long and hard about that reality.-END

-END-

LAWRIE WILLIAMS

3. Chris Powell of GATA provides to us very important physical commentaries

Amazing: some central banks are beginning to ask questions as to whether they should store dollars as reserves in light of the sanctions imposed by trigger happy USA

(CNBC/GATA)

Sanctions by ‘trigger-happy’ U.S. may push countries away from the dollar, security expert says

Submitted by admin on Tue, 2022-03-22 10:43Section: Daily Dispatches

By Abigail Ng

CNBC, New York

Monday, March 21, 2022

The U.S. has been “extremely trigger-happy” with stinging economic measures, and central banks may decide to diversify their portfolio of foreign reserves instead of relying heavily on the U.S. dollar, according to the co-director of the Institute for the Analysis of Global Security.

“Central banks are beginning to ask questions,” said Gal Luft of the Washington-based think tank, adding that they are wondering if reliance on the dollar and “putting all their eggs in one basket” is a smart idea.

“The United States has extended itself, has been extremely trigger-happy when it comes to the use of sanctions and other economic punishments,” he said.

The White House did not respond to a CNBC request for comment.

Luft said the U.S. took “unacceptable and unheard-of steps” in recent weeks, such as effectively freezing Russia’s central bank reserves and disconnecting Russia from the interbank messaging system, SWIFT.

He said one in 10 countries in the world is under some form of U.S. sanctions.

“That has a cumulative effect and as a result, we see the dollar playing less and less of a role and portfolios of central banks,” Luft said. …

… For the remainder of the report:

end

Half hearted sanctions against Russia have already failed

a good read…

(Ambrose Evans Pritchard…/(GATA)

Ambrose Evans-Pritchard: Half-hearted sanctions against Russia have already failed

Submitted by admin on Tue, 2022-03-22 11:35Section: Daily Dispatches

By Ambrose Evans-Pritchard

The Telegraph, London

Tuesday, March 22, 2022

Russia has not defaulted on its sovereign debt after all. Nor is it likely to do so under the current sanctions regime, and as long as Europe continues to finance Vladimir Putin’s military state with purchases of gas, oil, and coal.

The Kremlin is already sufficiently confident to reopen the Moscow stock exchange for bond transactions. The U..S Treasury’s sanctions office has made life easier by leaving a loophole for sovereign debt repayments, concerned that there might otherwise be a Lehmanesque shock to global finance.

The uninterrupted flow of fossil revenues – at windfall prices – is enough to cover interest service costs and redemptions. Goldman Sachs even thinks that the central bank will be able to relax capital controls gradually.

The rouble has not collapsed. It has stabilised after a 40pc devaluation, a manageable drop for a semi-autarkic closed economy. The fall is less than the currency slide in Turkey over recent months, which few even noticed outside specialist circles.

We are facing the failure of western sanctions policy. …

… For the remainder of the analysis:

https://www.telegraph.co.uk/business/2022/03/22/half-hearted-sanctions-against-russia-have-already-failed/Ambrose Evans-Pritchard: Half-hearted sanctions against Russia have already failed

By Ambrose Evans-Pritchard

The Telegraph, London

Tuesday, March 22, 2022

https://www.telegraph.co.uk/business/2022/03/22/half-hearted-sanctions-against-russia-have-already-failed/

Russia has not defaulted on its sovereign debt after all. Nor is it likely to do so under the current sanctions regime, and as long as Europe continues to finance Vladimir Putin’s military state with purchases of gas, oil, and coal.

The Kremlin is already sufficiently confident to reopen the Moscow stock exchange for bond transactions. The U..S Treasury’s sanctions office has made life easier by leaving a loophole for sovereign debt repayments, concerned that there might otherwise be a Lehmanesque shock to global finance.

The uninterrupted flow of fossil revenues – at windfall prices – is enough to cover interest service costs and redemptions. Goldman Sachs even thinks that the central bank will be able to relax capital controls gradually.

The rouble has not collapsed. It has stabilised after a 40pc devaluation, a manageable drop for a semi-autarkic closed economy. The fall is less than the currency slide in Turkey over recent months, which few even noticed outside specialist circles.

We are facing the failure of western sanctions policy.

Calibrated half-measures are not sufficient to change the Kremlin calculus or to dissuade Putin from a policy of attrition against civilian targets.

Yes, Russia is having to sell some crude oil at a steep discount but the gap is already narrowing as shippers learn to navigate the political reefs.

India and others are competing for bargain supplies, cutting the discount to $20 this week from $28 a barrel after the invasion of Ukraine. If Europe is still buying Russian oil, how can distant states in Asia be persuaded to desist?

The Kremlin is still earning almost $100 a barrel at today’s global prices ($118), twice the average of the last eight years. The Russian current account is in rude good health. Clemens Grafe from Goldman Sachs expects the surplus to top $200bn this year as imports of western consumer goods are slashed.

Russia has enough usable foreign currency to stay afloat for a long time. Western sanctions against the central bank are not proving to be the killer blow supposed at first, and nor is the ejection of some Russian banks from the SWIFT nexus of global payments. There are too many deliberate exemptions.

Goldman’s deep-dive into the effect of sanctions ought to end all wishful thinking. The US investment bank forecasts that the Russian economy will contract by 10pc this year, a bad recession but not an economic breakdown. Growth will then recover to 2.4pc next year and 3.4pc in 2024 as the country adjusts. Exports will be back to 98pc of prior levels by early next year. If so, Putin is not going to lose sleep over this.

Russia’s trade will mostly be diverted rather than destroyed. There may even be some short-term growth stimulus as Russia replaces western goods with home-made manufactures. Putin has been building a fortress economy ever since the annexation of Crimea. Net foreign funding is negligible. Total public debt is 18pc of GDP, one of the lowest ratios in the world.

Over four-fifths of GDP come from sectors that import just 15pc or less of their inputs, falling to 7pc in the mining industry. This is a radically different economic structure from western states such as Poland.

“If Russia were fully integrated into global supply chains, restrictions on imports and exports would be immediately destructive. However, Russia largely exports goods that are almost fully produced locally,” said Mr Grafe.

Iran endured tougher sanctions without buckling. Cornell professor Nick Mulder, author of The Economic Weapon, said the country settled into a new equilibrium within a couple of months. “If Iran’s experience is any guide, Russia will survive and return to lacklustre growth,” he said.

“Historically, sanctions have hardly ever been successful in stopping wars,” he said. A rare exception was the Balkan ‘war of the stray dog’ in 1925. Needless to say, Putin’s war on Ukraine is not a border skirmish. It is a long-planned attempt to overturn the post-Cold War settlement and alter the world’s balance of power.

European ministers once again grappled with a hydrocarbon embargo – the fifth package of sanctions – at an EU meeting on Monday. Once again the proposals ran into resistance from Germany, with Italy and others happy to tuck in behind.

There is a pervasive fear of a gilets jaunes uprising across Europe, a suspicion that a fickle public will not tolerate a cost-of-living shock once the horrors of Ukraine lose their novelty on TV screens – but that is to abdicate leadership.

The business-as-usual lobbies in Germany have dusted down a catastrophe scenario known as Lükex 18, a report by the German civil defence agency (BBK) painting a portrait fit for Hieronymous Bosch of what might happen if gas supplies were ever cut off.

It is to throw sand in our eyes. We are already in late March. The winter is over and Europe will have enough gas to last deep into the late autumn. It has sufficient spare import capacity for liquefied natural gas to rebuild some of its depleted storage with shipments of LNG from the US and Qatar over the summer months.

Professor Moritz Schularick from Bonn University said an immediate halt to all purchases of Russian gas, oil, and coal, would cut German GDP by 3pc this year and cost around €120bn but is perfectly feasible. “The world wouldn’t end,” he said.

The possible measures are by now well known. Every one degree cut in home heating saves 10 billion cubic metres (BCM) of gas. If Europe dialled down from an average of 22 to 19 degrees, which happened in some states in the 1973 crisis, it could already cover one fifth of total Russian supply. Targeted sections of heavy industry can be rationed with a small loss of GDP.

As for oil, the International Energy Agency has just cut its forecast for global demand this year by 1.3m barrels a day (b/d). It has issued a 10-point plan for rapid cuts that could shave a use by a further 2.7m b/d without causing an economic crisis, chiefly by a string of temporary measures such as lowering speed limits by 10 km/h, car-free Sundays, and less air travel. Together these savings add up to 4m b/d, equal to most of Russia’s oil exports to Europe.

The issue is no longer whether it can be done but whether Europe has the political courage to try. What is clear is that western sanctions policy is the worst of all worlds. We are suffering an energy shock that is further inflating Russia’s war-fighting revenues.

While it is hard to separate the effect of sanctions from war disruption and market psychology, the current situation is intolerable. We are allowing Putin to exploit Russia’s leverage as a full-spectrum commodity superpower.

The spot price for ammonia in Europe has risen sevenfold this year, deliberately pushed higher by a Kremlin ban on fertiliser exports that has no other purpose than causing maximum chaos and probably a global food shortage over the next year. Shortages of nickel, palladium, and other metals are becoming critical.

It is a strategic imperative to bring this crisis to a head immediately by raising the ante. A total energy embargo would buttress the military resistance of the Ukrainian armed forces and test whether it is even possible for Putin to continue prosecuting a bungled invasion.

As matters now stand, the sanctions have failed to achieve anything. It is Ukrainian resistance, and military kit mostly provided by the Anglo-Saxon powers of Nato and frontline EU states, that have so far held the line. Core Europe has done little more than bleat on the margins.

The spontaneous willingness of European nations to welcome millions of refugees is marvellous – and the UK should drop its tone-deaf visa requirement immediately – but what is most needed is to confront the cause of this vast human convulsion.

END

4.OTHER GOLD/SILVER COMMENTARIES

From Bill Murphy: from his brother

“Tim Murphy, Scottsdale Bullion & Coin tells us that all of a sudden the premiums on silver coins are taking off, confirming what some of our other sources have said for some time now. With the US government not minting silver coins for the rest of the year, supply has dried up. The premium to buy a one ounce Silver Eagle coin has taken off so much that a retail price of that coin is now at least $40. And yet, JP Morgan is so uptight, the spot internet price keeps going nowhere at around $25 an ounce. How long can JPM get away with this crap? How long before the silver price explodes?”

END

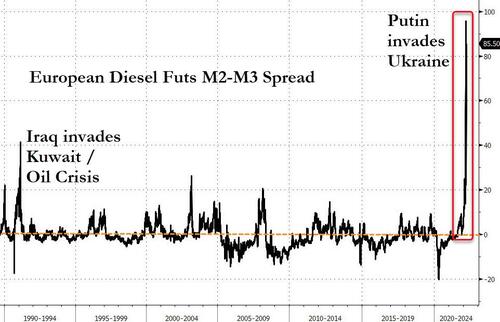

5.OTHER COMMODITIES/DIESEL FUEL

Diesel fuel is short supply as gas stations are running dry

(zerohedge)

“Gas Stations Will Run Dry”: Catastrophic Scenario For Diesel Emerging According To World’s Biggest Energy Traders

TUESDAY, MAR 22, 2022 – 06:05 PM

While the world has been obsessively focused on crude oil and gasoline in recent weeks, we instead alerted readers to a far more dire scenario playing out in diesel, a source of energy which is absolutely critical in keeping the “just in time” world running on time.

As a reminder, here are some of the articles we have published on the topic in recent weeks, many even before the Ukraine war:

- Diesel Is The U.S. Economy’s Inflation Canary – Feb 8

- U.S. Diesel Stocks Set To Fall Critically Low – Feb 18

- China Asks State-Owned Refiners To Halt Gasoline, Diesel Exports – Mar 10

- Global Diesel Shortage Raises Risk Of Even Greater Oil Price Spike – Mar 12

Fast-forward to today, when our warning was echoed by the heads of one of the largest commodity trading houses and the biggest independent oil trader who were speaking at the FT Commodities Global Summit in Lausanne, Switzerland on Tuesday.

The corporate leaders estimated that as much as 3 million barrels of oil and its products a day could be lost from Russia as a result of sanctions, in line with previous estimates, and warned that global markets face a squeeze on diesel with Europe most at risk of a “systemic” shortage that could lead to fuel rationing.

“The thing that everybody’s concerned about will be diesel supplies. Europe imports about half of its diesel from Russia and about half of its diesel from the Middle East,” said Russell Hardy, chief of Switzerland-based oil trader Vitol. “That systemic shortfall of diesel is there.”

Those imports mean that Russian supplies account for about 15% of Europe’s diesel consumption, according to the FT which carried their comments.

Hardy said the shift to more diesel consumption over gasoline in Europe had helped to create shortages of the fuel. He added that refineries could boost their diesel output in response to higher prices at the expense of other oil-derived products to shore up supply, but warned that rationing was a possibility.

Torbjorn Tornqvist, co-founder and chair of Geneva-headquartered Gunvor Group, added: “Diesel is not just a European problem; this is a global problem. It really is.”

Tornqvist also warned that European gas markets were no longer functioning properly as traders faced huge demands from banks for cash to cover hedging positions. “I think it’s broken. It really is,” he said. “I never thought that somebody could say ‘ah, gas has fallen below 100 per megawatt hours is really cheap’.”

Gas futures linked to TTF, Europe’s wholesale gas price have swung from about €70 a megawatt hour before Russia’s invasion of Ukraine to about €230 two weeks ago and then slid below €100 this week. Before May 2021, European gas prices were below €20 a megawatt hour.

As noted last week, Europe’s largest energy traders called on governments and central banks to provide emergency liquidity support to keep gas and power markets functioning as sharp price moves triggered by the Ukraine crisis have strained commodity markets. Hardy said that to move a cargo equivalent to 1 megawatt hour of liquefied natural gas priced at €97, traders must provide €80 in cash, straining their capital requirements.

Worse, confirming that Europe faces an even colder winter, Tornqvist said European utilities would struggle to fill gas storage for next winter given the “paralysed” state of the spot market for gas unless policymakers stepped in to provide guarantees to protect buyers against price swings.

But going back to diesel, Bloomberg’s Javier Blas tweeted a handful of the scariest quotes from the energy CEOs at today’s FT commodities summit:

- Trafigura CEO Jeremy Weir: “The diesel market is extremely tight. It’s going to get tighter and will probably lead into stock outs” referring to when fuel stations run dry.

- Gunvor CEO: “Europe is so short of diesel”

- Vitol CEO: “The thing that everybody’s concerned about will be diesel supplies”

Needless to say, without diesel, not only will traffic in Europe grind to a halt, but much if not all US truck based logistical support and supply chains will soon be paralyzed. The consequences for the global economy will be dire.

END

Inflation is intensifying and a lot of it is coming from resource nationalism

(Bloomberg)

Next Inflation Shock Comes From Resource Nationalism

TUESDAY, MAR 22, 2022 – 08:05 PM

By Valerie Cerasuolo, Bloomberg Markets Live commentator and reporter

First there was supply-chain disruption brought on by the coronavirus, then war in Ukraine further rocked commodity markets. The next bout of inflation via raw material prices will be brought on by resource nationalism.

While the cost pressures brought on by the difficulty in moving goods in a world in lockdown are fading, other factors are more enduring.

For instance, the post-Cold War spread of e-commerce allowed companies to treat the world as both factory floor and marketplace. Comparative advantage, strategic partnerships and the success of globalization led to growth and prosperity. Russia’s invasion of Ukraine jarred that dynamic and has set in motion a series of quasi-isolationist responses.

What started as economic sanctions on Russia has tipped the balance: we are no longer in a uni-polar world. We have entered into a multi-polar one where traditional economic superpowers can no longer call the shots. Service-driven economies are price takers and have far less leverage over those producing raw materials.

The geopolitical landscape has changed and economic incentives along with it. The growing emergency that sanctions on Russia have caused over energy supply security will be inflationary for years to come. Nowhere is this more evident than in Europe, given its direct exposure to Russia energy, with individual countries prioritizing domestic energy security as a first port of call.

The European Union entered an era of energy inflation given its commitment to address climate change and fossil fuel dependence by “greening” the economy. Such aims create price pressure, and has led to discussion at the European Central Bank on whether its inflation target should be adjusted.

Russia and Ukraine are two of the globe’s top grain producers. Conflict has triggered panic and price squeezes on everything from fertilizer to cooking oil, and has also led nations to rethink their approach to national stockpiling.

Energy security pulls into focus security of other commodities. The list of countries restricting agriculture exports is growing. It includes Indonesia, Hungary, Argentina, and Turkey. China’s begun stockpiling corn and soybeans while sources mention state refiners are considering pausing exports of gasoline and diesel in April.

Effectively, every resource a nation produces has the potential to become a bargaining chip. There is a price to meet security of resources. As more economies step away from globalization that cost will get steeper as isolationist tendencies produce greater trade frictions.

The process is unlikely to extend to a fear-driven mania. Consider it more of a purposeful step-change in both governments’ and corporations’ mental accounting and future planning, increasing both cost and scarcity to ensure resource security.

Nations cannot adopt a complete isolationist approach — it’s impossible to fully unwind decades of economic integration. However, lack of supply reliability results in additional inflation premia, regardless of the war’s outcome or duration.

END

Lithium…

Lithium prices have nearly doubled in 2022

(OilPrice.com)

Lithium Prices Have Nearly Doubled In 2022 Amid Insane Commodity Rally

WEDNESDAY, MAR 23, 2022 – 05:00 AM

By Alex Kimani of OilPrice.com,

Oil and commodity markets have been taking out fresh highs after the shuttering of Ukrainian ports, sanctions against Russia, and disruption in Libyan oil production sent energy, crop, and metal buyers scrambling for replacement supplies. Russia is one of the world’s biggest exporters of key raw materials, from crude oil and gas to wheat and aluminum, and the possible exclusion of supplies from the country due to sanctions has sent traders and importers into a frenzy.

Base metals prices have been coming off recent highs (and in the case of aluminum, copper, and tin, all-time highs) set earlier in the month that were spurred by fears over the potential for disruption to Russia’s metal exports following its invasion of Ukraine. Broad-based supply concerns remain, ranging from the potential for sanctions targeting exports, to actual output disruption and logistical dislocations (see ‘Implications of the Russia-Ukraine crisis for metals’ for details).

But the Ukraine crisis is only layering onto another more powerful trend: the global transition to low-carbon energy.

The energy transition is driving the next commodity supercycle, with immense prospects for technology manufacturers, energy traders, and investors. Clean energy technologies require more metals than their fossil fuel-based counterparts, with prices of green metals projected to reach historical peaks for an unprecedented, sustained period in a net-zero emissions scenario.

But few, if any, green metals have witnessed a price explosion as epic as that of lithium.

After more than quadrupling in value last year, lithium carbonate continues to soar in 2022, according to Benchmark Mineral Intelligence. The mid-March assessment by the battery supply chain research outfit shows that battery-grade lithium carbonate (EXW China, ≥99.5% Li2CO3) is averaging $76,700 a tonne, up 10% over just two weeks and 95% since the beginning of the year. A year ago, the commodity was trading at $13,400 a tonne.

The rally in lithium hydroxide, used in high-nickel content cathode manufacture, is accelerating, up 120% so far this year, narrowing the discount to lithium carbonate, which historically is priced below hydroxide.

Benchmark says that Chinese inventory levels for hydroxide, carbonate, and spodumene feedstock remain very low, sustaining the high price environment:

“Robust demand for material, and hence high prices, will be sustained in the near-term, with expectations that the seasonal recommencement of supply from domestic Qinghai brines in the coming months will provide little relief to the growing market deficit.“

Many investors who got burned by the last lithium price bust of 2018 have probably been watching on the sidelines, not sure what to make of the current mega-rally.

To be fair, China’s spot market, where small tonnages can have big price impacts, may be accentuating the scale of this mega-rally, but make no mistake about it: this is no false flag, with everything from mined spodumene to high-purity hydroxide, and every component of the lithium processing chain experiencing a wild price surge.

The price explosion tells you that lithium supply is simply nowhere near enough to feed this demand surge.

Demand Explosion

The last lithium boom five years ago was attributed to a failure by producers to anticipate the demand wave emanating from China’s subsidy-driven roll-out of EVs.

The subsequent supply response, particularly from hard-rock spodumene producers in Australia, proved to be overkill leading to the price bust of 2018-2020.

Consequently, new mines were mothballed, expansion projects were deferred, and many explorers folded operations and left to try their luck elsewhere.

Then suddenly, in a classic boom-bust-boom commodity cycle, it happened: lithium producers have been caught flat-footed again, ill-prepared to meet the current even stronger demand surge fueled by the global energy transition and EV revolution.

But the ongoing lithium boom has plenty of steam.

EV and new energy vehicle (NEV) sales in the pivotal Chinese market jumped 157.5% to 3.52 million units in 2021, marking robust growth in an otherwise lackluster domestic automotive market.

Many electric buses in China have switched to lithium iron phosphate (LFP) batteries. Two years ago, Tesla Inc. (NASDAQ:TSLA) introduced LFP batteries in its standard range Model 3s in China and dropped the starting price from 309,900 yuan ($48,080) to 249,900 yuan ($38,773). Last year, the EV kingpin Tesla announced that it’s switching battery chemistry for all standard-range Models 3 and Y from nickel cobalt aluminum (NCA) chemistry to an alternative, older technology that uses an LFP chemistry. CEO Elon Musk has revealed that the improving energy density of LFP batteries now makes it possible to use the cheaper, cobalt-free batteries in its lower-end vehicles so as to free up more battery supply of lithium-ion chemistry cells for Tesla’s other models.

But Chinese battery-makers are now discovering that you can play around with the metallic cathode mix as much as you want, but lithium still rules.

In a recent report, Benchmark Intelligence says that record-high Chinese lithium carbonate prices have pushed the costs of lithium iron phosphate – or LFP cells – higher than high-nickel cells on a dollar per kilowatt-hour basis, compared to a deep discount historically. Indeed, the analysts have warned that the chaos in nickel metal markets may spill over onto the metal’s use in the battery supply chain, potentially reversing the LFP trend.

END

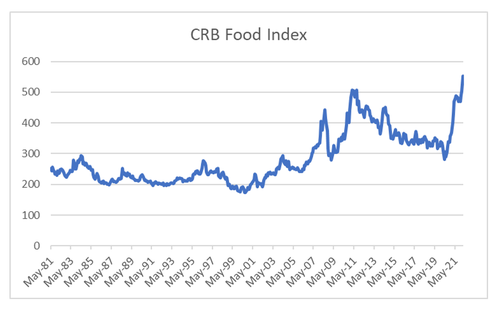

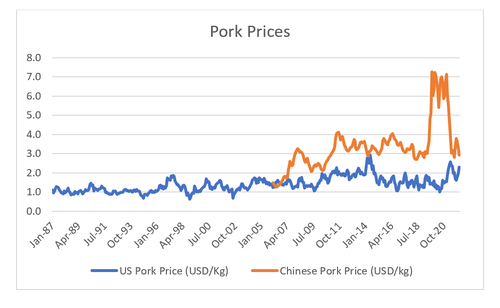

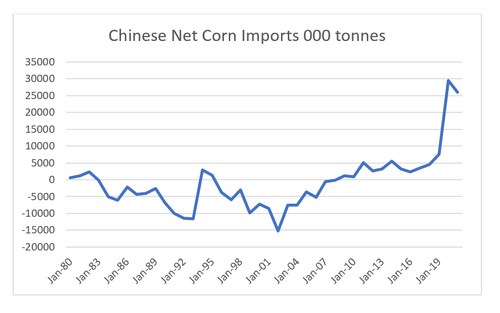

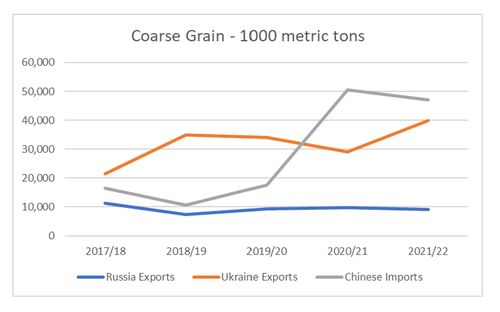

Huge food inflation coming

Russell Clark (formerly Horseman Capital)

Food Inflation: A Primer From Russell Clark

WEDNESDAY, MAR 23, 2022 – 12:31 PM

By Russell Clark, published on the Capital Flows and Asset Markets substack

Food prices have recently touched all time highs. The speed of the increase has also been very noteworthy.

The move higher in food prices so far, has been driven by two shocks. The first shock was African Swine Flu, which decimated Chinese pig herds in 2019, but have been rebuilt since then.

The collapse in the pig herd caused Chinese pork prices to rise dramatically. At its peak it was 6 times higher than US prices.

Pork farmers tend to look at pork/corn ratio as a guide to profitability. This spiked to all time high in China in 2020.

If you think of a pig, as a store of grain (4 kg of grain is needed for 1kg of pork), Chinese needed to rebuild inventory. The upshot was that China has moved to becoming a very large corn importer.

While this has been very bullish for grain, as the pork to corn ratio highlights above, pig farming in China is now loss making. So Chinese demand for grain cannot be taken for granted. But just as demand destruction was becoming a concern for grain prices, the Russian invasion of Ukraine has created a supply shock. As pointed out earlier for Chinese demand for coarse grain (corn, sorghum and barley) is more than the combined exports of Russia and Ukraine.

Historically speaking, at this level of food price inflation, demand destruction has normally taken hold, and short agricultural commodities has been the better trade. But I think we are transitioning to a new political environment, which suggests food inflation and rising agricultural prices are here to stay. This will be the subject of my next post.

END

trading houses will collapse as the margin call doom loop outlines by Poszar becomes realityl

Trading Houses Will Collapse As “Margin Call Doom Loop” Goes Global, Trafigura CFO Warns

Sometimes repo guru Zoltan Pozsar is so far ahead of his time, it takes the “experts” weeks just to read up on all the required source docs to even grasp what he is talking about.

Last week we reported that the Bloomberg news that one of the world’s largest independent energy merchants – the secretive Trafigura which trades hundreds of billion in commodities every year – was facing “margin calls in the billions of dollars” meant that the commodity “margin call doom loop” idea floated more than three weeks ago by Pozsar who warned that commodity traders and clearinghouses could be facing a liquidity crisis of historic proportions, was coming true and despite Barclays’ earnest attempts to minimize its impact, could threaten broader financial stability and was manifesting itself in broad liquidity squeezes which could be observed in the surge in such unsecured funding markets as the FRA-OIS.

That was just the start, because the very next day Zoltan was proven correct again, after the FT reported that Europe’s largest energy traders have taken the place of Europe’s insolvent banks in calling on governments and central banks to provide “emergency” assistance to avert a cash crunch as sharp price moves triggered by the Ukraine crisis strain commodity markets.

Yes, that’s what happens when a “margin call doom loop” goes global.

The FT wrote that in a letter it had seen, the European Federation of Energy Traders, a trade body that counts BP, Shell and commodity traders Vitol and the margin-call stricken Trafigura as members, said the industry needed “time-limited emergency liquidity support to ensure that wholesale gas and power markets continued to function”.

“Since the end of February 2022, an already challenging situation has worsened and more [European] energy participants are in [a] position where their ability to source additional liquidity is severely reduced or, in some cases, exhausted,” EFET said in its letter, dated March 8 and sent to market participants and regulators.

It was “not infeasible to foresee . . . generally sound and healthy energy companies . . . unable to access cash”, the letter warned, clearly ignoring that “generally sound” companies would have anticipated such a fat tailed scenario. The fact that they didn’t suggests that they were either not “generally sound”, or “healthy” and certainly did not plan accordingly. And yet somehow their stupidity and/or greed makes them eligible for Fed bailouts?

Days came and went, with nothing but silence from the central banks who perhaps ignored the severity of the coming liquidity crisis, and why not – after all most of the world’s biggest commodity traders have more than one billionaire in their org chart, let them spend money to bail out their companies. But while this particular bailout request may have sounded too grotesque to both central banks and the general public, to the commodity firms the sudden margin-call induced liquidity shortage was all too real.

Fast forward to today, when in a follow up to its report from last week, the FT writes that according to Christophe Salmon, Trafigura’s chief financial officer, the crisis in global energy markets will force some smaller commodity traders out of business and unleash a wave of consolidation in the sector.

Salmon warned that the spike in capital needed to keep commodities flowing around the world since Russia invaded Ukraine would squeeze smaller trading houses out of the market.

“When we go through these crises — and let’s not forget we’re getting out of two-and-a-half years of Covid situation — there will be another set of consolidation of the commodity trading sector,” Salmon told the FT Commodities Global Summit in Lausanne on Wednesday.

The global commodity trading sector is dominated by large groups such as Trafigura, Vitol and Gunvor but Salmon said many smaller traders were facing a multitude of problems from rising capital requirements to a lack of access to credit.

“The barriers to entry to our sector as supply chain managers are increasing,” he said.

Salmon’s dire comments come as every day we see confirmation of Pozsar’s worst case scenario, and amid the rising concerns about a liquidity crisis sweeping commodity financing, Europe’s largest traders continue to plea with banks and governments to offer “emergency” assistance to prevent a cash crunch as large swings in commodity prices push up the cost of trading. Of course, since these are independent trading houses which several years ago their paid-for lobbyists were trotted out to explain that they are not – in fact – systematically important, we fail to see how they could possibly make a case where taxpayer funds goes to bail out a handful of billionaires, when simple nationalization would do.

It is this worst case scenario that has prompted nothing short of panic among traders at the FT conference, who have voiced concerns that difficult conditions such as banks demanding hefty initial margins — cash for hedging future contracts — had contributed to a breakdown in the proper functioning of commodity markets, particularly gas and nickel.