April 5, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

April 6, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

april6, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1920.50 DOWN $4.10

SILVER: $24.34 DOWN $0.09

ACCESS MARKET: GOLD $1925.50

SILVER: $24.44

Bitcoin morning price: $44,912 DOWN $1024

Bitcoin: afternoon price: $43,671 DOWN 2265

Platinum price: closing DOWN $20.45 to $954.95

Palladium price; closing DOWN 43.10 at $2197.60

END

EXCHANGE: COMEXCONTRACT: APRIL 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,922.900000000 USD

INTENT DATE: 04/05/2022 DELIVERY DATE: 04/07/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 10104 C MIZUHO 5

118 C MACQUARIE FUT 1

132 C SG AMERICAS 1

363 H WELLS FARGO SEC 4

435 H SCOTIA CAPITAL 9

624 H BOFA SECURITIES 16

657 C MORGAN STANLEY 11

661 C JP MORGAN 165 51

709 C BARCLAYS 35

800 C MAREX SPEC 1

880 H CITIGROUP 33

TOTAL: 171 171

MONTH TO DATE: 21,795

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

March: JPMorgan stopped/total issued

NUMBER OF NOTICES FILED TODAY FOR APRIL. CONTRACT 171 NOTICE(S) FOR 17,100 OZ (0.5319 TONNES)

total notices so far: 21,795 contracts for 2,179,500 oz (67.791 tonnes)

SILVER NOTICES:

6 NOTICE(S) FILED TODAY FOR 30,000 OZ/

total number of notices filed so far this month 720 : for 3,600,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD DOWN $4.10

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.68 TONNES FROM THE GLD//

INVENTORY RESTS AT 1087.30 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 9 CENTS

AT THE SLV// A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ THE SLV//A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 566.392 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 981 CONTRACTS TO 148,526 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN OI WAS ACCOMPLISHED DESPITE OUR $0.16 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.16) BUT WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A STRONG GAIN OF 1836 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.305 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 115,000 OZ//NEW STANDING: 5.005 MILLION OZ// V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : —-455

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTACTS for 4 days, total 1662 contracts: 8.310 million oz OR 2.75MILLION OZ PER DAY. (415 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 1662 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 8.310 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 8.310 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 981 DESPITE OUR $0.16 LOSS IN SILVER PRICING AT THE COMEX// TUESDAY THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 400 CONTRACTS( 400 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAR. OF 4.305 MILLION OZ FOLLOWED BY TODAY’S 115,000 OZ QUEUE JUMP//NEW STANDING: 5/005 MILLION OZ/// .. WE HAD AN STRONG SIZED 1381 OI CONTRACTS ON THE TWO EXCHANGES FOR 8.174 MILLION OZ DESPITE THE LOSS IN PRICE.

WE HAD 6 NOTICES FILED TODAY FOR 30,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A TINY SIZED 61 CONTRACTS TO 560,066 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: + 177 CONTRACTS. (differentials are lowering in gold)

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE TINY SIZED DECREASE IN COMEX OI CAME DESPITE OUR GOOD SIZED LOSS IN PRICE OF $5.70//COMEX GOLD TRADING/TUESDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD SOME LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 80.139 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $5.70 WITH RESPECT TO TUESDAY’S TRADING

WE HAD AN GOOD SIZED GAIN OF 2567 OI CONTRACTS (8.174 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2567 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 560,066.

IN ESSENCE WE HAVE AN TINY SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2628, WITH 61 CONTRACTS INCREASED AT THE COMEX AND 2567 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2628 CONTRACTS OR 78.174 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2567) ACCOMPANYING THE TINY SIZED GAIN IN COMEX OI 61,): TOTAL GAIN IN THE TWO EXCHANGES 2828 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 78.33 TONNES FOLLOWED BY TODAY’S 24,400 OZ QUEUE JUMP//NEW STANDING 80.139 TONNES/// 3) SOME LONG LIQUIDATION ///. ,4) TINY SIZED COMEX OI. GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MARCH

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

12,383 CONTRACTS OR 1,238,300 OR 38.51 TONNES 4 TRADING DAY(S) AND THUS AVERAGING: 3095 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAY(S) IN TONNES: 38.51TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 38.51/3550 x 100% TONNES 0.860% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 38.51 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 981 CONTRACTS TO 148,526 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 400 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 400 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 280 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1436 CONTRACTS AND ADD TO THE 400 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 1381 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 6.905 MILLION OZ,

OCCURRED WITH OUR STRONG LOSS $0.16 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 0.71 PTS OR .02% //Hang Sang CLOSED DOWN 421.79 PTS OR 1.87% /The Nikkei closed DOWN 437.68 PTS OR 1.58% //Australia’s all ordinaires CLOSED DOWN 0.57% /Chinese yuan (ONSHORE) closed UP 6.3626 /Oil UP TO 103.14 dollars per barrel for WTI and UP TO 107.66 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3626 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3686: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

A)NORTH KOREA/

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 61 CONTRACTS TO 560,066 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS TINY COMEX DECREASE OCCURRED DESPITE OUR LOSS OF $5.70 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2567 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF APRIL.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2567 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :2567 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2567 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2628 CONTRACTS IN THAT 2567 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A TINY SIZED COMEX OI GAIN OF 61 CONTRACTS..AND THIS LOSS OCCURRED DESPITE OUR LOSS IN PRICE OF GOLD $5.70.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR APRIL (80.139),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 80.139

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $5.70) AND THEY WERE UBSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A FAIR SIZED GAIN OF 8.174 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR APRIL (80.139 TONNES)…

WE HAD +177 CONTRACTS ADDED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 2628 CONTRACTS OR 262,800 OZ OR 8.174 TONNES

Estimated gold volume today: 147,946 ///poor

Confirmed volume yesterday: 155,356 contracts poor

INITIAL STANDINGS FOR APRIL ’22 COMEX GOLD //APRIL 6

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 2,799.690 oz Brinks 84 kilobars |

| Deposit to the Dealer Inventory in oz | 38,388.294OZ Manfra |

| Deposits to the Customer Inventory, in oz | 106,839.704 oz HSBC |

| No of oz served (contracts) today | 171 notice(s)17,100 OZ. 5319 TONNES |

| No of oz to be served (notices) | 3970 contracts 397,000 oz 12.348 TONNES |

| Total monthly oz gold served (contracts) so far this month | 21,795 notices2,179,500 OZ 67.791 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 1

i)Into Manfra: 38,388.294.oz

total dealer deposit n38,388.294 oz//

No dealer withdrawal 0

1 customer deposits

i) Into HSBC 106,839.704 oz

total customer deposit: 106,839.704 oz //

1 customer withdrawal

ii) Out of Brinks: 2700,690 oz 84 kilobars

total withdrawals: 2700.6900 oz

ADJUSTMENTS: customer to dealer

ii) HSBC 16,011.198 oz

dealer to customer:

i) Brinks: 146,222.748 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 4141 contracts having LOST 16.

We had 260 notices filed yesterday so we gained 244 contracts or 24,400 oz will stand for delivery at the comex

May saw a LOST of 179 contracts to stand at 5000

June saw a GAINED of 2924 contracts down to 470,789 contracts

We had 260 notice(s) filed today for 26,000 oz FOR THE APRIL 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 165 notices were issued from their client or customer account. The total of all issuance by all participants equates to 171 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 51 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 16 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2021. contract month,

we take the total number of notices filed so far for the month (21,795) x 100 oz , to which we add the difference between the open interest for the front month of (APRIL 4141 CONTRACTS ) minus the number of notices served upon today 171 x 100 oz per contract equals 2,576,500 OZ OR 80.139 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month:

No of notices filed so far (21,795) x 100 oz+ (4141) OI for the front month minus the number of notices served upon today (171} x 100 oz} which equals 2,576,500 oz standing OR 80.139 TONNES in this active delivery month of APRIL.

We gained 24400 oz queue jump as our banker friends are desperate for gold.

TOTAL COMEX GOLD STANDING: 80.139 TONNES (A WHOPPER FOR A APRIL ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

191,133,764.7, oz NOW PLEDGED /HSBC 5.94 TONNES

99,258.893 PLEDGED MANFRA 3.08 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690 tonnes

243,923.704, oz JPM No 2 7.58 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

International Delaware:: 0

Loomis: 18,615.429 oz

total pledged gold: 1,487,476.805 oz 46.27 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 35,388.294 OZ (1100,73TONNES)

TOTAL ELIGIBLE GOLD: 18,254,596.165 OZ (567.80 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,655,266.657 OZ (549.15 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 16,167,790.0 OZ (REG GOLD- PLEDGED GOLD) 502,886 tonnes

END

APRIL 2022 CONTRACT MONTH//SILVER//APRIL 6

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 614,210.800 oz Delaware JPM |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 9752,722 oz |

| No of oz served today (contracts) | 6CONTRACT(S)30,000 OZ) |

| No of oz to be served (notices) | 281 contracts (1,405,000 oz) |

| Total monthly oz silver served (contracts) | 720 contracts 3,600,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 2 deposits into the customer account

i) Into Brinks 1767.57 oz

ii) Into Delaware: 7985.152

total deposit: 9752.7220oz

JPMorgan has a total silver weight: 177,110 million oz/336.920 million =52.56% of comex

i) Comex withdrawals: 2

i) Out of JPM 610,366.260 oz

ii) Out of Delaware: 3844,620 oz

total withdrawal 614,210.800 oz

1 adjustments: customer to dealer

jpmorgan; 480,110.960 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 86.249 MILLION OZ

TOTAL REG + ELIG. 336.920 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL OI: 287, HAVING GAINED 20 CONTRACTS FROM TUESDAY. We had 3 notices filed yesterday,

so we gained 23 contracts or an additional 115,000 oz will stand on this side of the pond

MAY HAD A LOSS OF 861 CONTRACTS DOWN TO 100,188 contracts

JUNE HAD A GAIN OF 183 TO STAND AT 484

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 29 for 145,000 oz

Comex volumes: 46,646// est. volume today// extremely poor/

Comex volume: confirmed yesterday: 56,150 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 720 x 5,000 oz = 3,600,000oz

to which we add the difference between the open interest for the front month of APRIL (287) and the number of notices served upon today 6 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL./2021 contract month: 720 (notices served so far) x 5000 oz + OI for front month of APRIL (287) – number of notices served upon today (6) x 5000 oz of silver standing for the APRIL contract month equates 5,005,000 oz. .

We gained 23 contracts or 115,000 oz will stand on this side of the pond.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

APRIL 4/WITH GOLD UP $.70//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1091.73 TONNES

APRIL 1///WITH GOLD DOWN $19.00 : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES INTO THE GLD///INVENTORY RESTS AT 1091.73 TONNES

MARCH 31/WITH GOLD UP $13.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD FROM MONDAY A WITHDRAWAL OF 1.71 TONNES FROM THE GLD:INVENTORY RESTS AT 1091.44

MARCH 28/WITH GOLD DOWN $14.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.18 TONNES

MARCH 25/WITH GOLD DOWN $7.60 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.52 TONNES INTO THE GLD///INVENTORY RESTS AT 1093.18 TONNES

MARCH 24/WITH GOLD UP $24.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1087.66 TONNES

MARCH 23/WITH GOLD UP $15.75//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1083.60 TONNES

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

MARCH 21//WITH GOLD UP $.25 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.00 TONNES INTO THE GLD////INVENTORY RESTS AT 1082.44 TONES

MARCH 18/WITH GOLD DOWN $13.55 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1073.44 TONES

MARCH 17/WITH GOLD UP $33.50: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.61 TONNES INTO THE GLD//INVENTORY RESTS AT 1073.44 TONNES

MARCH 16/WITH GOLD DOWN $18.50//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.33 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.83 TONNES

MARCH 15/WITH GOLD DOWN $30.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1064.16 TONNES

MARCH 14//WITH GOLD DOWN $22.75, HUGE CHANGES IN GOLD INVENTORY AT THE GLD//STRANGE: A DEPOSIT OF 2.62 TONNES INTO THE GLD.//INVENTORY RESTS AT 1064.16 TONNES

MARCH 11/WITH GOLD DOWN $14.60: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1061.54 TONNES

MARCH 10//WITH GOLD UP $11.55: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FORM THE GLD///INVENTORY RESTS AT 1063.28 TONNES

MARCH 9/WITH GOLD DOWN $53.85//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.64 TONNES INTO THE GLD//INVENTORY RESTS AT 1067.34 TONNES

MARCH 8/WITH GOLD UP $46.10: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 8.42 TONNES INTO THE GLD///INVENTORY RESTS AT 1062.70 TONNES

MARCH 7/WITH GOLD UP $28.40 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1054.28 TONNES

MARCH 4/WITH GOLD UP $28.40//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1050.22 TONNES

MARCH 3/WITH GOLD UP $13.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 7.84 TONNES//INVENTORY RESTS AT 1050.22 TONNES

MARCH 2/WITH GOLD DOWN $20.80//A MONSTER CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 13.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1042.38 TONNES

MARCH 1/WITH GOLD UP $42.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: //INVENTORY RESTS AT 1029.32 TONNES

FEB 28/WITH GOLD UP $12.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 25/WITH GOLD DOWN $38.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 24/WITH GOLD UP $17.35//A HUGE CHANGE AT THE GLD: 5.23 TONNES INTO THE GLD// IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1029.32 TONNES

FEB 23/WITH GOLD UP $2.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1024.09 TONNES

CLOSING INVENTORY FOR THE GLD//1087.30 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

APRIL 4/WITH SILVER DOWN 5 CENTS TO CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 6.326 MILLION OZ//INVENTORY REST AT 564.966 MILLION OZ//

APRIL 1/WITH SILVER DOWN 39 CENTS A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.302 MILLION OZ INTO THE SLV////INVENTORY REST AT 558.647 MILLION OZ//

MARCH 31/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.171 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 556.345 MILLION OZ

MARCH 28/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.847 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 554.167 MILLION OZ//

MARCH 25/WITH SILVER DOWN 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 24/WITH SILVER UP 54 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.092 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 23/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 21/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 18/WITH SILVER DOWN 37 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 17/ WITH SILVER UP 72 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.049 MILLION OZ INTO THE SLVV//INVENTORY RESTS AT 548.071 MILLION OZ

MARCH 16/WITH SILVER DOWN 56 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 462,000 OZ FROM THE SLV//INVENTORY RESTS AT 544.560 MLLION O

MARCH 15/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.022 MILLION OZ

MARCH 14/WITH SILVER DOWN 64 CENTS TODAY; STRANGE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.125 MILLION OZ/INVENTORY RESTS AT 545.022 MILLIONOZ

MARCH 11/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ

MARCH 10/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ/

MARCH 9/WITH SILVER DOWN 88 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.174 MILLION OZ OF FAKE SILVER.//INVENTORY RESTS AT 542.897 MILLION OZ//

MARCH 8/WITH SILVER UP 88 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV////INVENTORY RESTS A 548.071 MILLION OZ//

MARCH 7/WITH SILVER UP 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 4/WITH SILVER UP 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ/

MARCH 3/WITH SILVER UP 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.32 TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 198,000 OZ FROM THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 1/WITH SILVER UP $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 546.052 MILLION OZ//

FEB 28/WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 546.052 MILLION OZ//

FEB 25/WITH SILVER DOWN 64 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.510 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 546.052 MILLION OZ/

FEB 24/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ

FEB 23/WITH SILVER UP 22 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ//

SLV FINAL INVENTORY FOR TODAY: 566.352 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

I sure looks like we are heading for a wicked stagflation: hug inflation with no growth/recession

(Peter Schiff)

Peter Schiff: America Is Heading For Stagflation

WEDNESDAY, APR 06, 2022 – 08:15 AM

Most people seem to think that tighter monetary policy will bring on a recession, but they believe that it will solve the inflation problem. In his podcast, Peter Schiff explained why they’ve got it half right. We are heading toward a recession, but it’s not going to solve the inflation problem. In reality, we’re heading for stagflation.

Inflation is a problem globally, but the only major central bank talking about fighting inflation is the Fed. The European Central Bank and the Bank of Japan continue to hold interest rates down and run quantitative easing, despite rising prices in both economies. And as Peter said, all the Fed is doing is talking. It won’t actually fight inflation.

Their inconsequential, tiny rate hikes are going to do anything. In fact, the only reason they’re raising rates at all is to pretend they can keep on doing it. But at some point, they will reverse course because the bond market has that right. These higher rates are going to cause a recession, and it’s not going to take that many hikes to push the economy into recession given how addicted the economy is and how overleveraged the economy is. So, once the impact on the economy and on the financial markets is felt, then the Fed is going to give up all the tough talk and inflation is going to continue to get worse.”

As Peter mentioned, the bond market is already signaling recession warnings with inversions of the yield curve. Meanwhile, bonds had their worst quarter in 40 years. And the data is starting to reveal cracks in the economy.

Construction spending disappointed, coming in 0.4% below expectation. It was up 0.5%. The expectation was a 0.9% increase. This reflects an increase in the dollars spent on construction, not an increase in construction per see. Peter said he thinks construction is slowing down due to rapidly rising costs.

What’s happening is we’re constructing fewer structures, but we are paying a lot more to construct the ones we are building, and that’s why construction spending is going up — because builders are spending more money to build fewer homes. So, again, this is not good news. This is bad news for the economy.”

And it’s only going to get worse as mortgage rates increase. Mortgage applications have already dropped as rates charted the fastest run-up since 1994.

ISM manufacturing numbers also came in weaker than expected. Manufacturing grew in March, but it was down from February. The expectation was for the ISM to come in at 59, up slightly from 58.6 in February. The actual number was 57.1.

We also got the March jobs numbers last week. Most pundits spun them as good news with the addition of 431,000 jobs and significant upward revisions the January and February. But this was largely a function of huge adjustments made by the BLS. Nevertheless, the unemployment rate dropped down to 3.6%. Of course, government numbers understate unemployment. But this is still a low number.

Most mainstream economists, particularly those at the Fed, believe low unemployment is correlated to inflation. That being the case, Peter said interest rates should be much higher.

We have a huge inflation problem, and the Fed continues to drag their feet. Even though they acknowledge that it’s a big problem, they’re doing nothing about solving it. Raising interest rates from zero to 25 basis points in the face of this huge problem is not solving it. It’s continuing to make it worse. They are throwing gasoline on a fire even though they acknowledge that the fire is burning, which again proves it’s not about inflation. The Fed knows they can’t fight inflation. But they also know they can’t admit that. So, they’re trying to solve the problem by pretending they’re fighting inflation even though they continue to create it.”

There are all kinds of reasons bandied about for rising prices. But ultimately, it is the Federal Reserve and its expansion of the money supply.

To the extent that the economy gets weaker, they’re going to try to expand the money supply even more aggressively to try to stimulate it, which is why we’re going to have more inflation during the next recession.”

All of this adds up to stagflation.

In this podcast, Peter also talks about the stock market, the dollar, the bond market and commodities.

END

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

LAWRIE WILLIAMS:

-END

–

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

Interesting!! The USA has decided not to allow dollars to be paid on USA dollar denominated debt.

Thus Russia defaults@@!!

(Reuters/GATA)

U.S. stops Russian bond payments, raising risk of default

Submitted by admin on Tue, 2022-04-05 11:45Section: Daily Dispatches

By Megan Davies and Alexandra Alper

Reuters

Tuesday, April 5, 2022

The United States on Monday stopped the Russian government from paying holders of its sovereign debt more than $600 million from reserves held at U.S. banks, in a move meant to ratchet up pressure on Moscow and eat into its holdings of dollars.

Under sanctions put in place after Russia invaded Ukraine on Feb. 24, foreign currency reserves held by the Russian central bank at U.S. financial institutions were frozen.

But the Treasury Department had been allowing the Russian government to use those funds to make coupon payments on dollar-denominated sovereign debt on a case-by-case basis.

On Monday, as the largest of the payments came due, including a $552.4 million principal payment on a maturing bond, the U.S. government decided to cut off Moscow’s access to the frozen funds, according to a U.S. Treasury spokesperson. …

… For the remainder of the report:

end

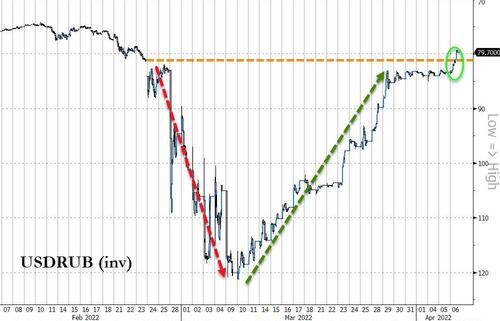

Russia sends in rubles for payment after the USA treasury blocked dollar use!

(zerohedge)

Russia Sends $650 Million Bond Payment In Rubles After US Treasury Blocks Dollars

WEDNESDAY, APR 06, 2022 – 10:50 AM

The Russian Finance Ministry may have avoided technical default on Tuesday by sending $649.2 million in rubles to satisfy bond payments, after the US Treasury on Monday banned them from making dollar debt payments from accounts at US financial institutions.

The ministry said foreign banks had rejected USD bond payments for both April maturities and coupons on notes which come due in April 2042, leaving Russia no choice but to send rubles to the National Settlement Depository. According to ministry officials, Russia “considers it fulfilled its obligations in full.”

That said, neither of the bonds allows Russia the option to pay in rubles, according to Bloomberg, raising concern among investors that a technical default could be declared after a 30-day grace period.

“The default issue is tricky,” said Abdul Kadir Hussain, the head of fixed-income asset management at Dubai-based Arqaam Capital. “Russia can claim we are willing to pay, we have the money to pay, but banks are not letting us pay. I’m not sure how the courts would handle that.”

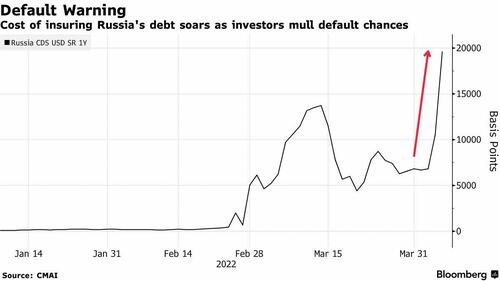

Earlier this year, rating firms S&P Global and Fitch said they would consider Russia to be in default if they satisfied payments on notes in a different currency than the one agreed upon, leading investors to load up on credit swaps and read the fine print on around $40 billion in contracts.

Russia’s Default Swaps Signal $40 Billion Payday Is Imminent

Credit-default swaps protecting $10 million of the government’s bonds for one year were quoted as high as $7 million upfront and $100,000 annually, according to market participants on Wednesday. That implies around 87% probability of default. -Bloomberg

The last time Russia defaulted on its ruble debt was 1998, two years before Vladimir Putin assumed power.

One US Treasury insider told Business that bondholders can still get paid if Russia can find a way to send dollars without using immobilized funds in US accounts – however the Russian Finance Ministry’s announcement suggested that they wouldn’t be exploring other avenues, and would continue to pay in rubles.

I do not share his opinion on this, but there it is

(Avery Goodman)

Avery Goodman: Buy gold but only for the right reasons

Submitted by admin on Tue, 2022-04-05 11:57Section: Daily Dispatches

By Avery Goodman

Seeking Alpha, New York

Monday, April 4, 2022

The alternate financial “news,” such as Zerohedge, has recently been flooded with an increasing number of ridiculous articles that claim Russia has “profoundly altered the international trade and monetary system by linking the Russian ruble to gold.”

According to this muddy thinking, Russia’s announcement that it will buy gold at 5000 rubles per gram puts “a floor under the price of gold and the ruble.”

Simply put, it is a ridiculous claim that is easily refuted.

Russia’s willingness buy gold at 5,000 rubles per gram is irrelevant. It does absolutely nothing to tie the ruble to either gold or the U.S. dollar.

If the ruble sinks back down to 150 rubles to the dollar, for example, Russia’s central bank offer will be to buy gold at half of gold’s dollar price. How many people will sell gold to Russia’s central bank under those circumstances?

Only people who have a gun pointed at their heads. …

… For the remainder of the analysis:

https://seekingalpha.com/article/4499736-buy-gold-but-only-for-the-right-reasons

end

Kinross sells its major Russian gold assets for a song: $680 million dollars to Highland Gold Mining company.

(Reuters/GATA)

Kinross Gold to sell Russian assets for $680 million

Submitted by admin on Tue, 2022-04-05 14:55Section: Daily Dispatches

From Reuters

Tuesday, April 5, 2022

Kinross Gold Corp is selling its Russian assets to the Highland Gold Mining group of companies for a total of $680 million in cash, the Canadian company said today, nearly a month after suspending its operations in the country.

Several companies with exposure to Russia are taking steps to comply with sweeping Western sanctions against Moscow over its invasion of Ukraine.

Kinross will receive $400 million for its Kupol mine and the surrounding exploration licenses and would receive a total of $280 million in cash for its Udinsk project.

Highland Gold is one of the largest gold mining companies in Russia and operates several mines in the country, including in Chukotka and Khabarovsk regions where the Kupol mine and Udinsk project are located. …

… For the remainder of the report:

https://www.reuters.com/business/kinross-gold-sell-russian-assets-680-mln-2022-04-05/

END

4.OTHER GOLD/SILVER COMMENTARIES

5.OTHER COMMODITIES/

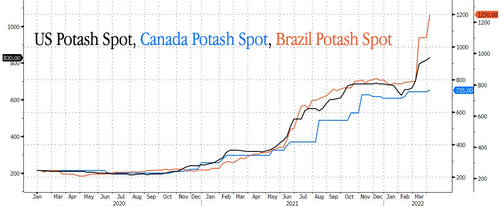

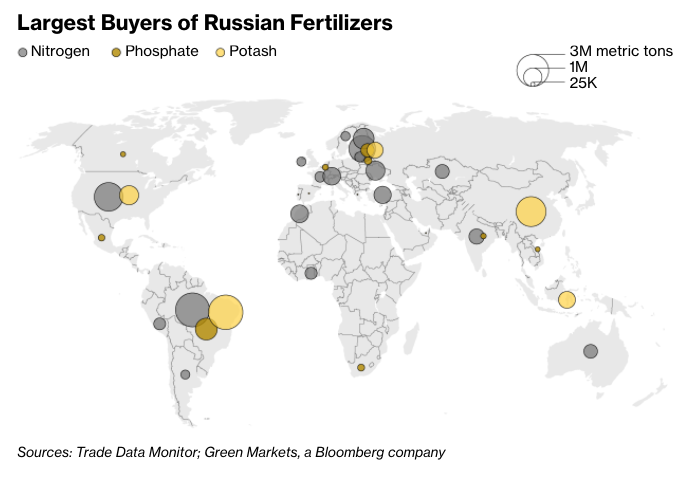

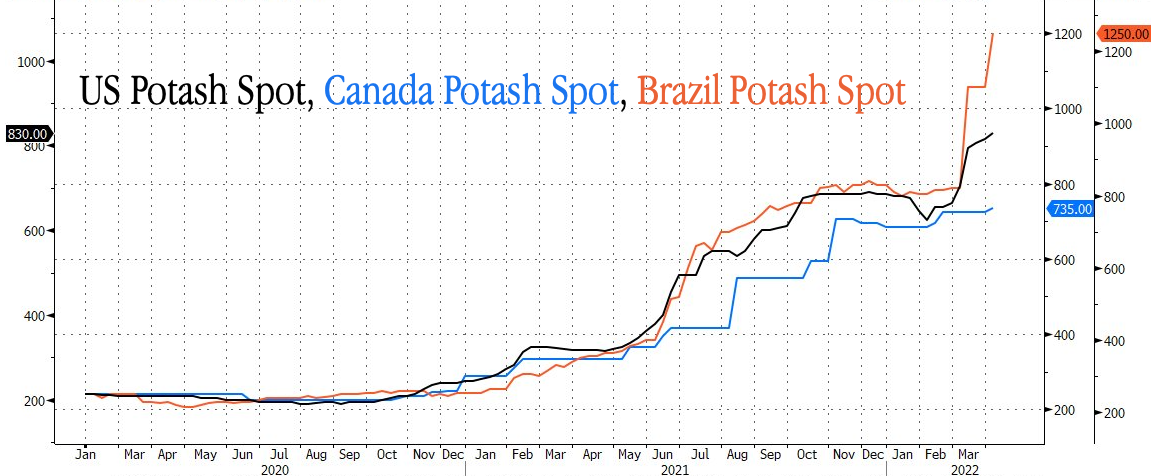

POTASH//EUROPE

Europe to deliver another shock to the agricultural sector as they plan to cap potash imports just as the planting season begins..Brilliant!

(ZEROHEDGE)

Europe To Cap Potash Imports As Planting Season Begins

WEDNESDAY, APR 06, 2022 – 05:45 AM

The EU is expected to deliver another shock to its agricultural sector by capping Russian imports of potash, a crucial ingredient for growing food, according to Bloomberg, citing a Dow Jones report.

The European Commission is expected to imminently unveil broad new sanctions on Russia. Much of the fertilizer is purchased from Belarus; the landlocked country in Eastern Europe could also be slapped with new sanctions for its involvement in Russia’s invasion of Ukraine.

Potash is a key ingredient for agricultural fertilizers. Europe produces only a negligible amount of the fertilizer, and to potentially cap imports from Russia and or Belarus (top producers) seems idiotic for Europe as the spring planting season is only beginning.

Even if Europe were to rework its supply chains to import potash elsewhere, only a few other countries would export it. The impact of capping imports will send prices even higher and create fertilizer shortages for crops. This can dramatically affect crop harvests at the end of the growing season.

A handful of North American fertilizer stocks jumped on the report, including CF Industries +3% and Intrepid Potash 2%.

About 90% of potash is used as fertilizer in Europe; the rest is used to produce table salt, help slow the aging of wine, preserve canned food, and give chocolate its aroma.

Global spot prices for potash show prices continue to accelerate to the upside. This may discourage farmers from purchasing or even spread less of it during the planting season.

Even before the invasion of Ukraine, all fertilizer production in the West was declining (read: here) due to high natural gas prices. The shortage of fertilizers, not just potash, but also nitrogen and phosphates, on global markets, is inevitable. What Europe is doing to potentially cap potash imports from Russia and Belarus is idiotic and can spark a food crisis.

end

6.CRYPTOCURRENCIES

7. GOLD/ TRADING TODAY

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.3626

OFFSHORE YUAN: 6.3686

HANG SANG CLOSED DOWN 421.79 PTS OR 1.87%

2. Nikkei closed DOWN 437.68PTS OR 1.58%

3. Europe stocks ALL RED

USA dollar INDEX DOWN TO 99.42/Euro RISES TO 1.0924

3b Japan 10 YR bond yield: RISES TO. +.245/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 123.86/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 103.14 and Brent: 107.66

3f Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: UP -SHORE CLOSED DOWN// OFF- SHORE UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.665%/Italian 10 Yr bond yield RISES to 2.35% /SPAIN 10 YR BOND YIELD RISES TO 1.64%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.68: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 2.75

3k Gold at $1925.90 silver at: 24.24 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble;// Russian rouble UP 0 1/3 in roubles/dollar; ROUBLE AT 82.69

3m oil into the 103 dollar handle for WTI and 108 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 122.91 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9325– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0187 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

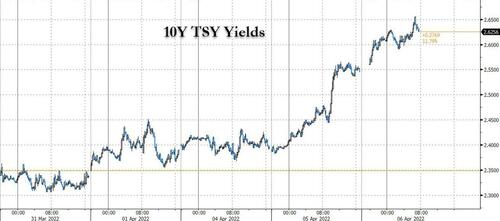

USA 10 YR BOND YIELD: 2.626 UP 7 BASIS PTS

USA 30 YR BOND YIELD: 2.664 UP 9 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.74

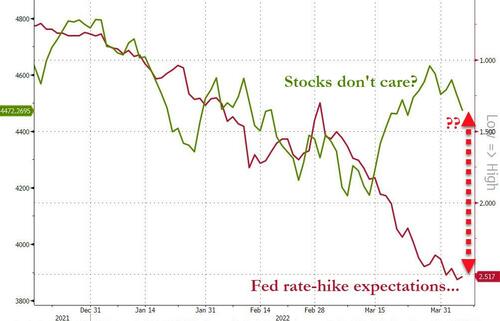

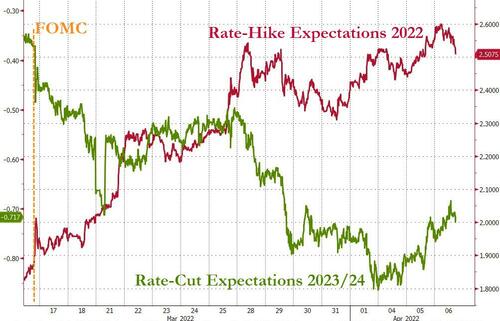

Futures, Treasuries Tumble On Fed Tightening Fears As FOMC Minutes Loom

WEDNESDAY, APR 06, 2022 – 08:03 AM

There is a scene in My Cousin Vinny where Joe Pesci’s puzzled wannabe-lawyer character asks the judge if he was really serious ’bout dat.

On Tuesday and overnight, incredulous algos and 15 year old hedge fund managers had a similar question to the Fed about its market-crushing, rate-hiking intentions, after yesterday the Fed’s in house permadove and Hillary Clinton donor, Lael Brainard, shocked markets when she not only made the case for accelerated rate hikes but also a faster balance sheet drawdown after she said that curbing inflation is “paramount” and the central bank may start trimming its balance sheet rapidly as soon as May.

As a result, investors once again feared out that a more restrictive U.S. central bank could end up tipping the world’s largest economy into a downturn, or even a recession, something which is now Deutsche Bank’s base case for 2024. The virus resurgence in Asia and the war in Ukraine are also clouding the outlook for prices and growth.

“Market participants finally acknowledged that central banks are serious and will raise interest rates significantly to bring inflation rates down,” Florian Spate, a senior bond strategist at Generali Investments, wrote in a note. “We expect the selloff to lose momentum but the general trend for yields is likely to point still upwards.”

It also meant a plunge in both US stocks and bonds, and a continuation of this selloff across global markets overnight, which then fed back into US future weakness again this morning and saw tech companies lead U.S. index futures lower on Wednesday as concerns mounted over the pace of the Federal Reserve’s monetary tightening and a worsening pandemic in China.

Futures on the Nasdaq 100 were down about 1.5% and contracts on the S&P 500 slid -1% with tech heavyweights among the worst performers in premarket trading. Global stocks and bonds also fell. The Stoxx Europe 600 index was down more than 1%, with travel, carmakers and tech leading declines. 10Y yields soared as high as 2.65% and a gauge of the dollar’s strength rose to a three-week peak.

Tesla, Nvidia, Applied Materials, Amazon, Alphabet, Qualcomm and Boeing were among the worst performers in premarket trading. Starbucks slipped after the company announced the ousting of its top lawyer. Here are some other notable movers:

- Shares of Spirit Airlines (SAVE US) fall 2.6% in U.S. premarket, erasing some of prior day’s steep gains after the budget carrier received a $3.6 billion takeover offer from JetBlue (JBLU US) that topped a competing bid by Frontier Group. JetBlue -4.3%.

- Twitter (TWTR US) slips 1.3% after two-day surge of about 30%. Elon Musk refiled the disclosure of his stake to classify himself as an active investor, making the change after taking a seat on the social media company’s board.

- Array Technologies’ (ARRY US) strong order book and better-than-expected FY22 guidance were welcomed by analysts, however they also highlight margin pressure and potential impacts from an antidumping and countervailing duties (AD/CVD) investigation. Array gains 11% premarket.

- Tech companies led U.S. index futures lower on Wednesday as concerns mounted over the pace of the Federal Reserve’s monetary tightening and a worsening pandemic in China. Apple (AAPL US) -0.8%.

- Gogo (GOGO US) gains 11% premarket on news that it will join the S&P Smallcap 600 Index before trading opens April 8, according to S&P Dow Jones Indices.

- US-listed Chinese stocks fall in premarket trading Wednesday, tracking Asian peers, as a selloff in bonds pressures tech shares. The decline in Chinese ADRs follows a 3.8% drop in Hang Seng Tech Index, the most in more than a week, with Alibaba and JD.com among the biggest decliners In premarket trading, Alibaba drops 2.2%, JD.com falls 2.5% and Pinduoduo declines 2.8%; Baidu -1.6%, while Bilibili -1.2%. Among electric carmakers, Nio -2.4%, Li Auto -2% and XPeng -2.4%.

Even more hawkish surprises from the Fed may be on deck: according to Swissquote analyst Ipek Ozkardeskaya, the Fed minutes expected on Wednesday afternoon may hint at a 50 basis-point hike at the next meeting. The latest comments from policy makers, surging inflation, strong jobs data and rising wages all support an accelerated tightening campaign, she said. “The market risks remain tilted to the downside,” said Ozkardeskaya. “If there is a good time for the Fed to hit the brakes on its ultra-lose policy, it is now.”

The selloff was broad based and also hammered rates, with the 10-year Treasury yield rising as high as 2.65%, taking it back into the ranges traded in 2018 and 2019. Money-market traders are betting on the steepest Fed tightening in almost three decades following Brainard’s comments. Sovereign debt across Europe retreated after bonds in Australia and New Zealand tumbled.

“The QE honeypot looks close to being empty now,” Jeffrey Halley, a senior market analyst at Oanda, wrote in a note. “I’m not sure we will get a soft landing, and nor am I sure the FOMO gnomes of the equity market will be able to continue ignoring reality, particularly if U.S. yields continue to rise.”

In Europe, automotive, travel, technology and consumer companies were the worst performers, leading declines in the Stoxx Europe 600 Index which dropped 1.5%. Delivery Hero sank 5% in Germany. Imperial Brands rose 3.1% after the U.K. cigarette producer forecast a slight increase in profit this year. Here are some of the biggest European movers today:

- Chr. Hansen shares rise as much as 5.5%, leading gains on the Stoxx 600 and the Health Care sub-index, after the nutritional ingredients manufacturer reported consensus-beating 2Q earnings.

- Imperial Brands shares climb as much as 3.5% after the company said its FY outlook is in line with the revised guidance issued last month. It’s been a solid start to the year, RBC says.

- IWG shares rise as much as 6% after the stock is raised to buy from hold at Peel Hunt, with the broker seeing multiple ways the flexible offices firm could create value.

- Avio shares rise as much as 15% the most intraday in a year after the stock was raised to buy from neutral at Banca Akros after Amazon’s “massive order” for Ariane 6 launches.

- Huber + Suhner shares climb to a record high after UBS upgrades to buy from neutral, citing “under-appreciated” prospects for the maker of radio- frequency and fiber-optic technology.

- Semiconductor stocks lead European tech stocks lower on Wednesday as a selloff in bonds steepens amid hawkish commentary from Federal Reserve Governor Lael Brainard.

- Among semiconductor stocks, ASML drops 3.4%, ASM International -5%, Infineon -3.7%, Nordic Semi -7.6%, BE Semi -4.8%

- Royal Mail shares fall as much as 4.6%, hitting the lowest since Dec. 21, as Barclays cut its PT on the postal group to 400p from 640p with FY23 likely to be a challenging year.

- Stroeer shares drop after HSBC cut the advertising firm’s rating to hold, saying the stock may find it difficult to withstand cyclical headwinds as the Ukraine war weighs on economic growth.

- Avon Protection shares drop as much as 25% with Jefferies saying the protective-equipment maker’s latest update is “disappointing.”

Earlier in the session, Asian stocks traded lower across the board following the losses on Wall Street as Mainland China returned from its long-weekend. ASX 200 conformed to the downbeat tone which isn’t helped by the RBA’s hawkish hold yesterday. Japan’s Nikkei 225 saw most of its construction and machinery-related names with losses. KOSPI was pressured by its large tech exposure. Hang Seng was also weighed on by its tech exposure as yields continued to rise overnight. The Shanghai Comp returned for the first time this week following its domestic holiday and saw less pronounced losses, with the Real Estate sector feeling relief from reports that over 60 Chinese cities ease policies on housing purchases to support the market.

In rates, the Treasuries selloff extended with the curve steepening sharply out to the 10-year sector after Tuesday’s aggressive selloff — spurred by hawkish Fed comments — was extended during the Asia session. Wednesday’s focal points include the March FOMC minutes release, expected to feature balance-sheet runoff details. Yields are higher by as much as 8bp after the 10-year rose as much as 11bp to nearly 2.66%, highest since March 2019; The 2s10s curve is steeper by ~4.5bp on the day near 7bp, while 2s10s30s fly cheapens around 5bp follows Tuesday’s 9bp jump wider; 10s30s curve spread is back around 2bp after briefly inverting for first time since 2006. Into the selloff, long-end swap spreads have widened, 10- and 30-year by 1bp-2bp.

In FX, Bloomberg dollar spot index fades a push higher to trade flat. GBP and NZD are the strongest performers in G-10 FX, CHF and JPY underperform.

In FX, a gauge of the dollar’s strength rose to a three-week peak.

In commodities, WTI crude rose above $103 a barrel, before stalling near $104 . Worries remain that Russia’s growing isolation over the war in Ukraine may further disrupt commodity flows. Fresh sanctions on Russia are expected, including a U.S. ban on investment in the country and a European Union proscription on coal imports. Most base metals trade in the red; LME lead falls 0.7%, underperforming peers. Spot gold rises roughly $6 to trade near $1,929/oz.

Crypto markets experienced sudden selling pressure overnight with Bitcoin losing USD 45k, a level it has

acquired a foothold on during the European session

Market Snapshot

- S&P 500 futures down 1% to 4,475.00

- STOXX Europe 600 down 0.9% to 458.77

- German 10Y yield little changed at 0.66%

- Euro little changed at $1.0912

- Brent Futures up 0.9% to $107.63/bbl

- MXAP down 1.4% to 179.00

- MXAPJ down 1.2% to 593.59

- Nikkei down 1.6% to 27,350.30

- Topix down 1.3% to 1,922.91

- Hang Seng Index down 1.9% to 22,080.52

- Shanghai Composite little changed at 3,283.43

- Sensex down 0.8% to 59,672.08

- Australia S&P/ASX 200 down 0.5% to 7,490.09

- Kospi down 0.9% to 2,735.03

- Brent Futures up 0.9% to $107.63/bbl

- Gold spot up 0.0% to $1,923.71

- U.S. Dollar Index little changed at 99.50

Top Overnight News from Bloomberg

- Money-market traders are betting the Federal Reserve will implement 225 basis points of interest-rate hikes by the end of the year. Factoring in the hike already delivered in March, that would mean an increase of 2.5 percentage points for the whole year. The Fed hasn’t done that much tightening in one year since 1994, a famously brutal year for bond investors that even included a 75 basis-point hike

- The Bloomberg Global Aggregate Index fell below a measure of so-called par value Tuesday, with its price falling to 99.9 — under the key 100 level at which bonds are often sold to investors. It’s the first time since 2008 that the gauge has traded at a discount to face value

- The Federal Reserve will unveil details of its likely plans to shrink its massive balance sheet with the release of minutes of the U.S. central bank’s March meeting, as policy makers confront the highest inflation in four decades

- Leaving the European Central Bank to fight the current bout of energy-driven inflation alone would only work at a steep cost to society, according to Executive Board member Fabio Panetta

- German factory orders fell in February, dropping for the first time in four months in the runup to Russia’s invasion of Ukraine and underscoring concerns over slower growth in Europe’s largest economy

- Turkey’s Recep Tayyip Erdogan approved on Wednesday a set of changes to the country’s electoral rules that would bolster his party’s prospects and consolidate the shift toward an all- powerful presidency set to be tested at the ballot box next year

- The U.S., European Union and Group of Seven are coordinating on a fresh round of sanctions on Russia, including a U.S. ban on investment in the country and an EU ban on coal imports, following the discovery of civilian murders and other atrocities in Ukrainian towns abandoned by retreating Russian forces

- The European Union’s foreign policy chief described a summit with Chinese President Xi Jinping as a “deaf dialog,” casting doubt on how much cooperation the Asian nation will offer to end the war in Ukraine

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac markets traded lower across the board following the losses on Wall Street; Mainland China returned from its long-weekend. ASX 200 conformed to the downbeat tone which isn’t helped by the RBA’s hawkish hold yesterday. Nikkei 225 saw most of its construction and machinery-related names with losses. KOSPI was pressured by its large tech exposure. Hang Seng was also weighed on by its tech exposure as yields continued to rise overnight. Shanghai Comp returned for the first time this week following its domestic holiday and saw less pronounced losses, with the Real Estate sector feeling relief from reports that over 60 Chinese cities ease policies on housing purchases to support the market.

Top Asian News

- Hong Kong Chief Secretary John Lee Resigns, Government Says

- China Backs Ex-Security Chief to Lead Hong Kong, SCMP Says

- Singaporeans Need $73,549 Just for Right to Buy a Car

- EU’s Top Envoy Calls Summit With China’s Xi a ‘Deaf Dialog’

European bourses deteriorated further from a tepid cash open, in-fitting with the Wall St./APAC handover, Euro Stoxx 50 -1.6% Such downside was exacerbated by weak Construction PMIs and as yields continue to make further advances ahead of ECB’s Lane & FOMC Minutes. As such, the NQ -1.0% is the morning’s laggard, though price action thus far has seen the ES give-up 4500 ahead of the 200-DMA at 4484.

Top European News

- U.K. Covid Cases at Highest Level as Immunity Wanes, Study Finds

- Erdogan Changes Turkey’s Electoral Laws to Bolster His Rule

- BNP Allows Staff in Europe to Work From Home Half the Time

- Infineon, STMicro Attractively Valued Despite Softer 2023: Citi

In FX, dollar fades fast following rapid rise to fresh 2022 high post-hawkish Fed Brainard and pre-FOMC minutes – DXY reaches 99.759 before retreat to sub 99.500. Swedish Krona outperforms after latest comments from Riksbank member Floden upping the ante for a near term repo rise, EUR/SEK capped below 10.3000. Franc lags as yield and policy divergence weigh and EUR/CHF cross rebounds in a fashion that suggests official intervention, USD/CHF tests 0.9350 and EUR/CHF close to 1.0200 vs sub-1.0150 at one stage. Euro and Pound take advantage of Buck pull back and some chart support to recoup losses, EUR/USD and Cable back on 1.0900 and 1.3100 handles after dip through 1.0895 Fib and 1.3050. Yen reverses more repatriation gains as BoJ maintains YCC, USD/JPY hovering beneath 124.05 peak.

In commodities, WTI and Brent are firmer, shrugging off the tepid tone and benefitting from geopolitical premia. amid ongoing sanction announcements/ discussions. However, the benchmarks are once again in relatively thin ranges of circa. USD 3.00/bbl at present. US Private Energy Inventory Data (bbls): Crude +1.08mln (exp. -2.1mln), Cushing +1.791mln, Gasoline -0.543mln (exp. +0.1mln), Distillate +0.593mln (exp. -0.8mln). Gas flows via Yamal-Europe pipeline resume eastward, according to Gascade data, according to Reuters; however, subsequently reported that such flows have stopped. Spot gold/silver are modestly firmer, benefitting from the general risk tone and as the USD takes a breather from recent advances.

Central Banks

- ECB’s Wunsch said the inflation target is essentially met and expects the deposit rate to be raised to zero by year end. He said the ECB’s rate could rise to 1.5-2% in the longer term, but caveat that even within the ECB there has been no discussion about raising interest rates, according to Reuters.

- ECB’s Panetta says they would not hesitate to tighten policy if supply shocks fed into domestic inflation, not seeking any de-anchoring of inflation expectations. Asking the ECB to bring down high inflation in the near-term would be extremely costly.

- RBA’s Deputy Governor Bullock notes Australian labour market is tight, was seeing some response in wages, with unemployment at 4.0%. Expects some revision upward in inflation forecasts; are now seeing more underlying inflation pressures.

- Riksbank’s Floden says inflation will be much higher in the coming year than predicted in February. We must raise the policy rate much earlier than previously planned. Evident we must reassess and substantial adj. monetary policy plans.

US Event Calendar

- 07:00: April MBA Mortgage Applications, prior -6.8%

- 14:00: March FOMC Meeting Minutes

Central Banks

- 09:30: Fed’s Harker Discusses the Economic Outlook

- 14:00: March FOMC Meeting Minutes

DB’s Henry Allen concludes the overnight wrap

DB Research have released a significant World Outlook document yesterday, in which we’ve updated our views on the global economy and financial markets given developments since the start of the year. In terms of the key takeaways, we’ve downgraded our growth forecasts, with an out-of-consensus view that a US recession is now the base case by the end of next year, since higher inflation will require a more aggressive tightening in monetary policy from central banks, and we now see the Fed moving much faster, with 50bp hikes at the next 3 meetings, and a terminal rate of 3.6% by mid-2023. The outlook has been further dampened by Russia’s invasion of Ukraine, which has pushed up energy prices and led to further disruption for key commodity markets and supply chains.

With the outlook moving in a more stagflationary direction, we expect growth to slow materially in the second half of 2023, tipping the US into recession by the end of that year. Indeed historically, there’s been just 2 occasions over the last 70 years when the Fed has raised rates by 300bps and left inflation on a downward trajectory without causing a recession. And as we’ve written many times in the EMR, the recent inversion of the 2s10s curve has on average preceded the start of a recession by around 18 months (see more in our recent chartbook here). Over in the Euro Area, we’re also forecasting a more aggressive tightening cycle, with the ECB raising rates by 250bps between this September and December 2023. But unlike in the US, we think Euro Area growth will be modestly above zero in the winter of 2023-24. Along with the updated call for US recession, Jim’s also expecting credit spreads to widen out by the end of next year. See the full credit update from him here.

Many of those themes we wrote about in the World Outlook were echoed in markets over the last 24 hours, with a massive bond selloff that was turbocharged by some hawkish rhetoric from Fed Governor Brainard (who’s also been nominated to become Vice Chair). Among the headlines, she said the FOMC would “continue tightening policy methodically” and would start reducing the balance sheet “at a rapid pace as soon as our May meeting.” Furthermore, she went on to say that she expected the balance sheet “to shrink considerably more rapidly than in the previous recovery, with significantly larger caps and a much shorter period to phase in the maximum caps compared with 2017-19.” Today’s FOMC minutes should give more detail about what QT may look like, which our US econ team and Tim from our team covered here. And there was also a comment that inflation was “subject to upside risks”. Brainard is typically perceived to be dovish, that the comments came from her left little doubt about the consensus of the entire committee voting bloc.

Those remarks saw market pricing shift to expect even more aggressive moves from the Fed over the rest of the year. In fact by yesterday’s close, futures were pricing in an 83% chance of a 50bps move at the next meeting in May, whilst the amount of tightening priced for 2022 as a whole hit its highest yet as well, with 220bps worth of further hikes on top of the 25bps from last month. If realised, that would be the largest amount of Fed tightening in a single calendar year since 1994, when they moved Fed funds up by 250bps, and remember that our economists’ latest forecasts now see the Fed matching that 250bps worth of hikes this year as well. Terminal rates are also repricing higher, with 1y1y OIS rates hitting their highest level this cycle at 3.17%, up from 1.11% at the start of the year.

These expectations of a more aggressive Fed led to a major selloff in Treasuries across maturities, with yields on 10yr Treasuries up by +15.2bps to 2.55% by the close, echoing the volatility in yields we saw at the start of last month as Russia’s invasion of Ukraine got underway, and marking the largest daily rise in the 10yr yield since the Covid-induced volatility in March 2020. That also marks the first time the 10yr yield has closed above 2.5% since May 2019, and the move went alongside a large rise in real yields (+9.7bps) as well, which at -0.31% put it at levels not seen since March 2020 as well. Another feature of yesterday was that the big rise in yields at the long end of the curve proved enough to un-invert the 2s10s curve, which ended the day in positive territory for the first time since last Wednesday, at 2.5bps. And this morning those moves have gained added momentum, with the 10yr Treasury up another +7.1bps to 2.62%, and the 10yr real yield up +5.8bps to -0.25%.

That selloff in Treasuries was echoed in Europe too yesterday, with yields on 10yr bunds (+10.8bps), OATs (+14.9bps), BTPs (+19.3bps) and gilts (+10.7bps) all seeing similarly big rises. From Europe, one interesting point to note is that the spread of French 10yr yields over bunds widened to 54bps yesterday, which is its widest level in almost 2 years. That came amidst a broader underperformance in French assets yesterday, with the CAC 40 index losing -1.28% as the tightening polls ahead of the first round this Sunday have led to increasing doubt as to whether President Macron will win another term in office. He’s still ahead in the polls for now, but the gap between himself and his main challenger Marine Le Pen has narrowed in Politico’s polling average from a peak of 30%-17% less than a month ago to just 27%-21% now. Furthermore, the second round average is at 54%-46%, which is also significantly tighter than Macron’s 66%-34% victory over Le Pen in 2017.

US equities were also affected by the more hawkish rhetoric from Governor Brainard, and the S&P 500 fell -1.26% as investors continued to price in higher interest rates. Cyclical sectors were among the worst performers, and technology stocks lost significant ground with the NASDAQ (-2.26%) and the FANG+ index (-3.28%) both undergoing serious declines. In Europe the situation was somewhat better, although the main indices there closed before the later decline in the US, meaning that the STOXX 600 still advanced +0.19%. As mentioned however, that masked serious regional divergences, with the FTSE 100 advancing +0.72%, whilst the Germany’s DAX (-0.65%) and France’s CAC 40 (-1.28%) both lost ground.

Staying on Europe, there were further developments on Russian sanctions yesterday, with the EU proposing a 5th package of measures that would include an import ban on Russian coal, among others. Commission President von der Leyen said that they were working on further sanctions “including on oil imports”, but there wasn’t yet a discussion about banning either oil or gas, with differing opinions among the member states on such a move.

That pattern of losses has been seen overnight in Asia as well, where equity markets are trading in negative territory amidst that continued rise in Treasury yields overnight. The Nikkei (-1.89%) is leading losses across the region with the Hang Seng (-1.69%) trading sharply lower as the index reopened after a holiday. Stocks in mainland China are also struggling with the Shanghai Composite (-0.29%) and CSI (-0.52%) both down after their own reopenings following holidays, which also comes as the Caixin services PMI dropped to 42.0, its lowest level since February 2020 and beneath the 49.7 reading expected by the consensus. Looking ahead, equity futures are pointing towards further losses today, with contracts on the S&P 500 (-0.04%) and the DAX (-0.41%) both falling.

Data releases took something of a back seat yesterday, but we did get the release of the final services and composite PMIs from around the world, with many European countries having upward revisions relative to the flash readings. For example, the Euro Area composite PMI came in at 54.9 (vs. flash 54.5), whilst the UK composite PMI came in at 60.9 vs. flash 59.7). The US was one of the few exceptions, where the composite PMI was revised down to 57.7 (vs. flash 58.5), and the ISM services index also came in modestly beneath expectations at 58.3 (vs. 58.5 expected), although that did mark a rebound following 3 consecutive months of declines.

To the day ahead now, and the release of the FOMC minutes from the March meeting will be one of the main highlights later. Otherwise, central bank speakers include ECB Vice President de Guindos, Chief Economist Lane, and Philadelphia Fed President Harker. Data releases include the UK and German construction PMIs for March, German factory orders for February, and Euro Area PPI for February.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 0.71 PTS OR .02% //Hang Sang CLOSED DOWN 421.79 PTS OR 1.87% /The Nikkei closed DOWN 437.68 PTS OR 1.58% //Australia’s all ordinaires CLOSED DOWN 0.57% /Chinese yuan (ONSHORE) closed UP 6.3626 /Oil UP TO 103.14 dollars per barrel for WTI and UP TO 107.66 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3626 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3686: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER//

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

END

3B JAPAN

end

3c CHINA

CHINA/

end

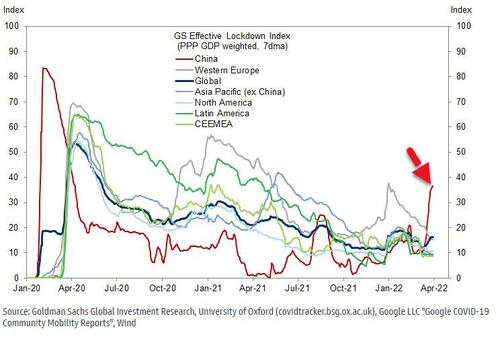

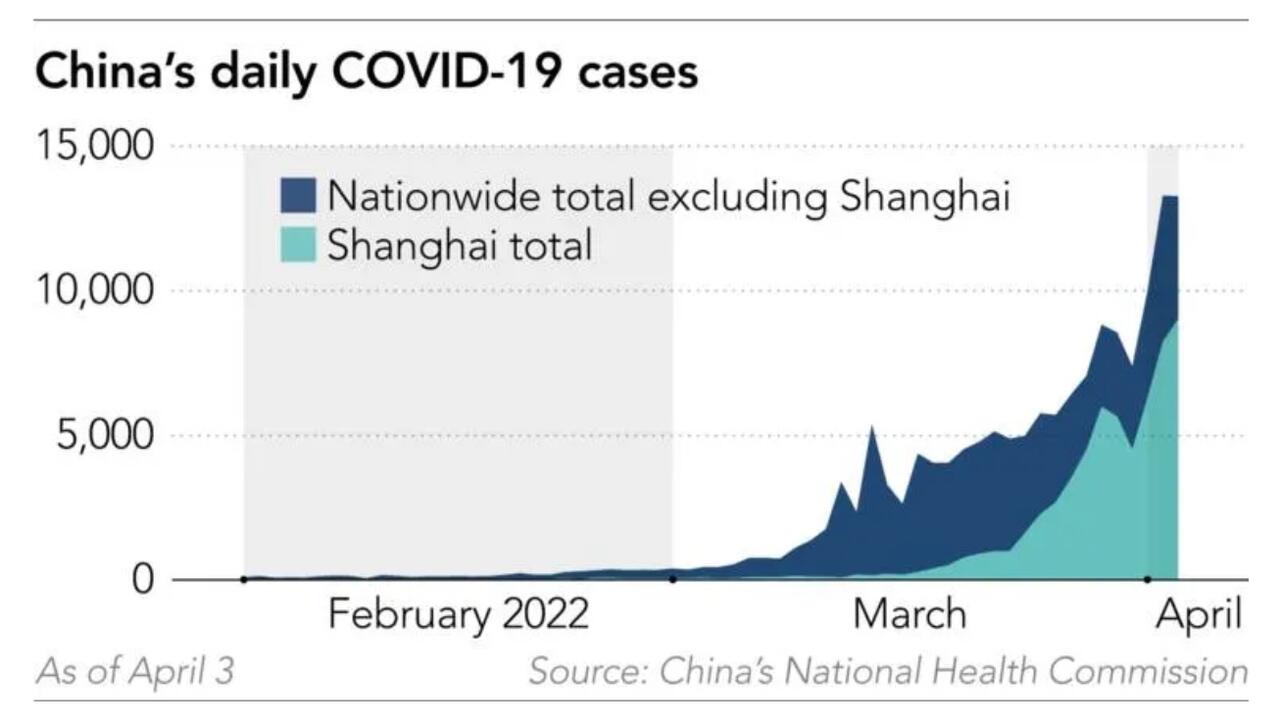

CHINA/SHANGHAI/COVID

Covid cases spiral northbound as this becomes very problematic for Shi. The Omicron seems to be morphing to the XE hybrid. Most of China is vaccinated but they used their own sinopak/ stupnik vaccines of which we know nothing.

It seems that the vaccines are altering the citizens immunity badly. What scares me the most: the virus is hitting little children which has no ACE 2 receptors. How is the new virus entering the cells?

(zerohedge)

President Xi Faces An Impossible Dilemma In Shanghai As COVID Outbreak Worsens Despite Lockdown

TUESDAY, APR 05, 2022 – 10:40 PM

In the span of just over a week, CCP authorities have gone from denying plans for a citywide lockdown of Shanghai to announcing what was supposed to be a two-part staggered lockdown – to simply locking down the entire city and sending in the military and a contingent of medical workers as locals accuse the government of violating its social compact to put the people’s interests first.

Now, as the entire city of roughly 26 million faces what’s already shaping up to be the most punishing lockdown in China since the original three-month Wuhan lockdown nightmare, Nikkei reports that Beijing has found itself in an incredibly difficult position.

On Sunday, Shanghai counted 9,006 mainly asymptomatic infections, more than two-thirds of the national tally.

The reason the situation in Shanghai presents such a difficult conundrum is that backing down from its lockdown in Shanghai would mean admitting that the “Zero COVID” approach has been an abject failure.

But continuing with the heavy-handed lockdown risks spurring even more unrest – something the CCP has bent over backwards to avoid. For the CCP, it’s an impossible dilemma.

Already, social media has been flooded with reports of locals dying from neglect as hospital resources have been stretched thin (and not from COVID; it’s other ailments that are killing people now).

While the entire city has been locked down for less than a week, many individual residential compounds have been locked down for much longer – some since mid-March.

“It is so uncharacteristic of Shanghai to have to go through this,” said Zhong Lei, a teacher in the city, whose residential compound was locked down even earlier, in mid-March.

On Tuesday, authorities reiterated that they must try to keep the city’s port and its factories running at full capacity. But accomplishing this – as we have already reported – will require even more draconian measures like forcing workers to essentially live inside the city’s factories.

Here’s a rundown of some of the obstacles that have led to the surge in cases and deaths, which local authorities have been accused of obscuring and underreporting.

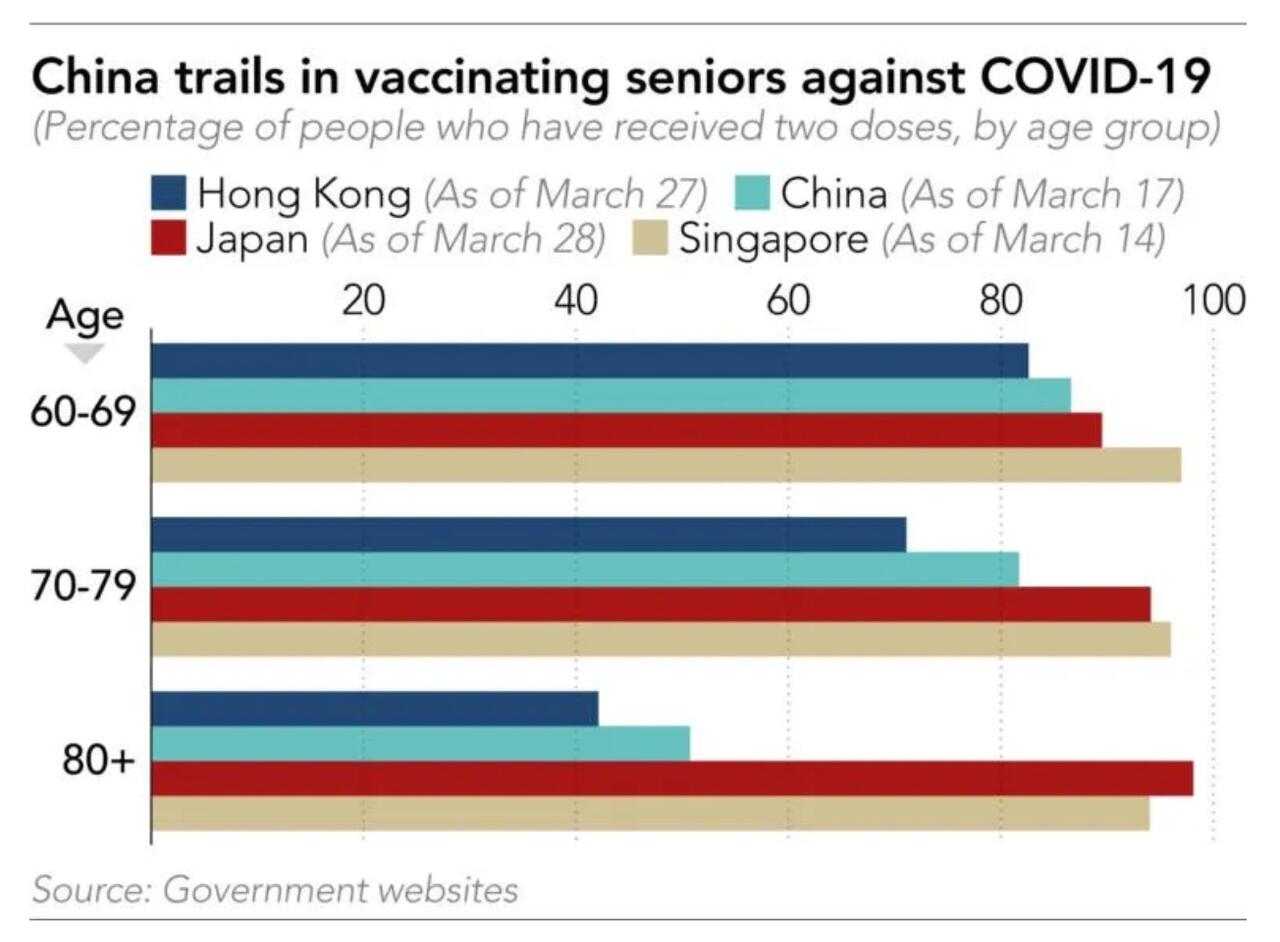

- Experts are divided over what those costs are. Some warn of heavy economic losses, while others suggest the strict measures ensure industrial stability, not to mention saving lives. Likewise, there is division over China’s vaccination program. Authorities say nearly 90% of the population of 1.4 billion has been inoculated, a staggering feat by any measure. Yet the rate among the most vulnerable seniors lags behind, and China continues to insist on using homegrown shots despite questions over efficacy.

- What seems evident is that there is no clear path for China to join the growing number of countries “living with COVID” anytime soon, which presents profound risks to China’s economy, as well as its status in global trade.

- “If we stop all containment measures now, it means all the previous efforts are for nothing,” Liang Wannian, a top official at the National Health Commission, said in late March in response to a reporter’s query on why China is not shifting toward treating COVID as endemic, like influenza.

- “The recent fine-tuning is an indication that the country is experimenting with a less costly – and thus more sustainable – zero-COVID approach,” Xu Tianchen, a China economist at The Economist Intelligence Unit, told Nikkei Asia.

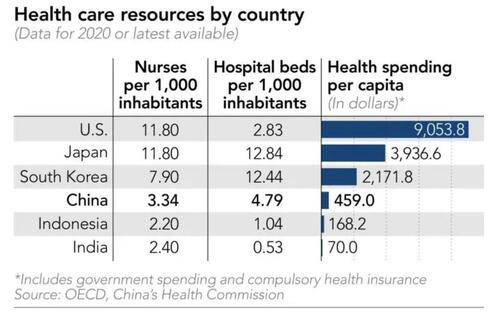

Nikkei added that despite China’s efforts to reform and build up its health care infrastructure over the past decade, the country still faces capacity limitations. The latest available data shows the country had 3.34 registered nurses per 1,000 people, compared to 11.8 in the US. China’s health spending per capita was $459 in 2018, while US spending came to $9,054 in 2019.