May 12, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1825.75 DOWN $26.50

SILVER: $20.68 DOWN $.88

ACCESS MARKET: GOLD $1822.00

SILVER: $20.70

Bitcoin morning price: $28,800 DOWN 876

Bitcoin: afternoon price: $28,681 DOWN 1077

Platinum price: closing DOWN $52.00 to $947.70

Palladium price; closing DOWN $119.45 at $1910.45

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

comex notices percentage of JPMorgan notices filed: 1094/1197

EXCHANGE: COMEX

CONTRACT: MAY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,852.600000000 USD

INTENT DATE: 05/11/2022 DELIVERY DATE: 05/13/2022

FIRM ORG FIRM NAME ISSUED STOPPED

323 H HSBC 317

657 C MORGAN STANLEY 17

657 H MORGAN STANLEY 93

661 C JP MORGAN 4 1094

709 C BARCLAYS 4

880 H CITIGROUP 829

905 C ADM 24

TOTAL: 1,191 1,191

MONTH TO DATE: 5,276

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT 1191 NOTICE(S) FOR 119,100 OZ (3.705 TONNES)

total notices so far: 5276 contracts for 527,600. oz (16.4105 tonnes)

SILVER NOTICES:

86 NOTICE(S) FILED 430,000 OZ/

total number of notices filed so far this month 4823 : for 24,115,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $26.50

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD

INVENTORY RESTS AT 1066.62 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 88 CENTS

AT THE SLV// A BIG CHANGE IN SILVER INVENTORY AT THE SLV://A WITHDRAWAL OF 5.487 MILLION OZ INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 570.439 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 1006 CONTRACTS TO 141,746 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED DESPITE OUR $0.08 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.08) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A STRONG GAIN OF 760 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 30.170 MILLION OZ FOLLOWED BY TODAY’S 50,000 OZ QUEUE JUMP //NEW STANDING 27.920 MILLION OZ/ // V) STRONG SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : 141

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTACTS for 8 days, total 12,329, contracts: 61.645 million oz OR 7.705 MILLION OZ PER DAY. (1541CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 61.645 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 61.645 MILLION OZ//INCREASING AGAIN

RESULT: WE HAD A VERY STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1006 DESPITE OUR $0.08 GAIN IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1625 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAY. OF 30.170 MILLION OZ FOLLOWED BY TODAY;S 50,000 OZ QUEUE JUMP //NEW STANDING 27.920 MILLION OZ// .. WE HAD A STRONG SIZED GAIN OF 619 OI CONTRACTS ON THE TWO EXCHANGES FOR 3095 MILLION OZ DESPITE THE GAIN IN PRICE.

WE HAD 86 NOTICE FILED TODAY FOR 430,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 3216 CONTRACTS TO 574,663 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –1429 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE GOOD SIZED INCREASE IN COMEX OI CAME DESPITE OUR GAIN IN PRICE OF $9.85//COMEX GOLD TRADING/WEDNESDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 5.353 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY”S QUEUE JUMP OF 85,800 OZ//NEW STANDING 16.569 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $9.80 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A VERY STRONG SIZED GAIN OF 11,598 OI CONTRACTS (36.07 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 8382 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 576,092.

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 13,027, WITH 3216 CONTRACTS INCREASED AT THE COMEX AND 8970 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 11,598 CONTRACTS OR 36.07 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (8382) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI (3216,): TOTAL GAIN IN THE TWO EXCHANGES 11,598 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY. AT 5.353 TONNES FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 85,800 OZ//NEW STANDING 16.569 /// 3) ZERO LONG LIQUIDATION //.,4) GOOD SIZED COMEX OI. GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

38,287 CONTRACTS OR 3,828,700 OR 119.08 TONNES 8 TRADING DAY(S) AND THUS AVERAGING: 4785 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES: 119.08 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 119.08/3550 x 100% TONNES 3.33% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 119.08 TONNES INITIAL// INCREASING AGAIN

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 1006 CONTRACT OI TO 141,746 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1625 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1936 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI loss OF 1006 CONTRACTS AND ADD TO THE 1936 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GOOD SIZED GAIN OF 619 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 3.095 MILLION OZ

OCCURRED DESPITE OUR GAIN IN PRICE OF $0.08 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED down 3.71 PTS OR 0.12% //Hang Sang CLOSED down 444.23 PTS OR 2.24% /The Nikkei closed DOWN 464.92 OR 0.18% //Australia’s all ordinaires CLOSED DOWN 1.89% /Chinese yuan (ONSHORE) closed DOWN 6,7914 /Oil UP TO 104.54 dollars per barrel for WTI and down TO 106.17 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7914 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8189: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 3216 CONTRACTS TO 574,663 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR GAIN OF $9.85 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (8382 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF MAY.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 8382 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :8382 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 8382 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 11,598 CONTRACTS IN THAT 8382 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD AN GOOD SIZED COMEX OI GAIN OF 3216 CONTRACTS..AND YET THIS GAIN OCCURRED WITH OUR GAIN IN PRICE OF GOLD $9.85.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (15.569),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 16.569 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $9.85) AND WERE UNSUCCESSFUL IN FLEECING ANY LONGS// AS WE HAVE REGISTERED A VERY STRONG SIZED GAIN OF 36.07 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAY (16.569 TONNES)…

WE HAD 1429 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1159,800 CONTRACTS OR 1302,700 OZ OR 36.07

TONNES

Estimated gold volume today: 306,808/// good

Confirmed volume yesterday:309,189 contracts good

INITIAL STANDINGS FOR MAY ’22 COMEX GOLD //MAY 12

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 32,279,608 oz BRINKS BRINKS ENHANCED |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 1191 notice(s)119,100 OZ 3.705 TONNES |

| No of oz to be served (notices) | 51 contracts 5100 oz 0.1586 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5276 notices 527,600 OZ 16.4105 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit nil oz//

No dealer withdrawals

0 customer deposits

2 customer withdrawals:

i) Out of Brinks: 32,279.604 oz

ii) Out of Brinks enhanced 4067.500 oz

total withdrawal: 36,343.104– oz

ADJUSTMENTS: 1 HSBC//dealer to customer 5497.821 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 1242 contracts having LOST 1315 contracts

We had 2173 notices filed on Tuesday, so we gained 858 contracts or AN ADDITIONAL 85,800 oz will stand for delivery in this non active delivery month of May.

June saw a loss of 19,938 contracts down to 303,252 contracts

July has a gain of 24 OI to stand at 178

August has a gain of 23,837 contracts up to 213,007 contracts

We had 1191 notice(s) filed today for 119100 oz FOR THE MAY 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1191 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1094 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2021. contract month,

we take the total number of notices filed so far for the month (5276) x 100 oz , to which we add the difference between the open interest for the front month of (MAY 1242 CONTRACTS ) minus the number of notices served upon today 1191 x 100 oz per contract equals 532,700 OZ OR 16.569 TONNES the number of TONNES standing in this non active month of MAY.

thus the INITIAL standings for gold for the MAY contract month:

No of notices filed so far (5276) x 100 oz+ (1242) OI for the front month minus the number of notices served upon today (1191} x 100 oz} which equals 532,700 oz standing OR 16.569 TONNES in this NON active delivery month of MAY.

TOTAL COMEX GOLD STANDING: 16.569 TONNES (A STRONG STANDING FOR A MAY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,026,795.134 oz

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 35,989.411.684 OZ

TOTAL ELIGIBLE GOLD: 18,189,609.255 OZ

TOTAL OF ALL REGISTERED GOLD: 17,799.802.429 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,77300.0 OZ (REG GOLD- PLEDGED GOLD)

END

MAY 2022 CONTRACT MONTH//SILVER//MAY 12

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 176,760.860 oz HSBC JPMorgan |

| Deposits to the Dealer Inventory | |

| Deposits to the Customer Inventory | 1,266.774.426 OZ CNT Delaware HSBC oz |

| No of oz served today (contracts) | 86CONTRACT(S (430,000 OZ) |

| No of oz to be served (notices) | 761 contracts (3,805,000 oz) |

| Total monthly oz silver served (contracts) | 4823 contracts 24,115,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposit into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 3 deposits into the customer account

i) Into CNT: 593,084.606 oz

ii) Into Delaware; 90,432.110

total deposit: 1,266,774.422 oz

JPMorgan has a total silver weight: 177.025 million oz/338.066 million =52.36% of comex

Comex withdrawals: 2

i) Out of JPMorgan 175,760.900 oz

ii) Out of HSBC 999.92 oz

total withdrawal 176m760.800 oz

0 adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 80.759 MILLION OZ

TOTAL REG + ELIG. 338.006 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY OI: 847 HAVING LOST 865 CONTRACTS. WE HAD 875 NOTICES FILED ON TUESDAY

SO WE GAINED 10 CONTRACTS OR AN QUEUE JUMP OF 50,000

JUNE HAD A GAIN OF 35 TO STAND AT 1531

JULY HAD A LOSS OF 1610 CONTRACTS UP TO 113,943 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 86 for 430,000 oz

Comex volumes: 81.880// est. volume today// good

Comex volume: confirmed yesterday: 88,622 contracts ( good )

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 4823 x 5,000 oz = 24,115,000 oz

to which we add the difference between the open interest for the front month of MAY(847) and the number of notices served upon today 86 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY./2021 contract month: 4823 (notices served so far) x 5000 oz + OI for front month of MAY (847) – number of notices served upon today (86) x 5000 oz of silver standing for the MAY contract month equates 27,920,000 oz. .

We GAINED 10 contracts or AN ADDITIONAL 50,000 will stand for delivery at the comex

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

GLD INVENTORY: 1066.62 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

INVENTORY TONIGHT RESTS AT 570.439 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

Trump-backed Mooney wins Republican House primary in West Virginia

Submitted by admin on Tue, 2022-05-10 22:17Section: Daily Dispatches

U.S. Rep. Alex Mooney, R-West Virginia, repeatedly has pressed the Federal Reserve, Treasury Department, and Commodity Futures Trading Commission with inconvenient questions about gold market manipulation.

* * *

By Paul Steinhauser

Fox News, New York

Tuesday May 10, 2022

Rep. Alex Mooney is projected by the Associated Press as the winner in the Republican congressional primary in West Virginia’s 2nd District in a battle with fellow Republican Rep. David McKinley.

And while former President Donald Trump wasn’t on the ballot, his prestige within the party was very much on the line in a bitter contest between two incumbent lawmakers, as Trump had endorsed Mooney.

“I Love West Virginia. Congratulations to Alex Mooney on his big win!,” Trump wrote on his social media platform, Truth Social.

West Virginia lost a congressional seat during the once-in-a-decade congressional reapportionment, and Mooney and McKinley were drawn into the state’s newly refigured 2nd District.

West Virginia lost a congressional seat during the once-in-a-decade congressional reapportionment.

The race partially turned into a test of the former president’s status as the most popular and influential politician in the Republican Party, nearly 16 months removed from the White House.

At his victory celebration, Mooney told supporters “the voters of West Virginia spoke loud and clear tonight.”

And the congressman thanked Trump for “his endorsement and support of my campaign,” adding, “When Donald Trump puts his mind to something, you better watch out.”

Mooney touted on the campaign trail and in ads that he’s the “only candidate Trump trusts to defend our values” and criticized McKinley as a “RINO” and a “sellout.” …

… For the remainder of the report:

https://www.foxnews.com/politics/west-virginia-trump-mooney-primary-mckinley

end

Craig Hemke at Sprott Money: Upward reversals for gold and silver coming soon

Submitted by admin on Tue, 2022-05-10 21:50Section: Daily Dispatches

9:45p ET Tuesday, May 10, 2022

Dear Friend of GATA and Gold:

The TF Metals Report’s Craig Hemke, writing today at Sprott Money, shrugs off the recent plunges in gold and silver futures and contends that upward reversals will happen soon as the Federal Reserve eases off its increases in interest rates to halt a stock market crash.

Hemke’s analysis is headlined “Reality Bites: An Update” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/Reality-Bites-An-Update-Craig-Hemke-May-10-2022

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //DIESEL

COMMODITIES IN GENERAL//DIESEL/OIL/INVENTORIES

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7914

OFFSHORE YUAN: 6.8189

HANG SANG CLOSED DOWN 444,23 PTS OR 2.24%

2. Nikkei closed DOWN 464.92 OR .1.97%

3. Europe stocks ALL CLOSED ALL RED

USA dollar INDEX UP TO 104.56/Euro FALLS TO 1.0416

3b Japan 10 YR bond yield:FALLS TO. +.24/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 129.95/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN -SHORE CLOSED UP// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +0.859%/Italian 10 Yr bond yield FALLS to 2.75% /SPAIN 10 YR BOND YIELD FALLS TO 1.90%…

3i Greek 10 year bond yield FALLS TO 3.35

3j Gold at $1842.70 silver at: 20.91 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1.9 roubles/dollar; ROUBLE AT 65.29

3m oil into the 103 dollar handle for WTI and 106 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 128.53 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9969– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0454well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.939 DOWN 7 BASIS PTS

USA 30 YR BOND YIELD: 2.990 DOWN 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 15.39

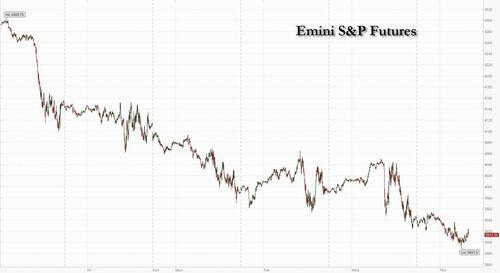

Slow-Motion Crash Drags Futures Below 3,900; Yields, Cryptos Tumble

THURSDAY, MAY 12, 2022 – 07:57 AM

The relentless slow-motion crash sparked by the Biden Fed (which is hoping that a market collapse will halt inflation) that has sent stocks lower for the past 6 weeks continued overnight, and Wall Street’s main equity indexes were set for more declines after losing $6.3 trillion in value since their late-March high as stubborn inflation in the world’s biggest economy bolstered the case for more aggressive monetary tightening by the Federal Reserve.

Nasdaq 100 futures were down 0.7% at 730am in New York, a day after the underlying gauge sank to its lowest since November 2020 on concerns that higher-than-expected inflation in April would lead to an even more aggressive pace of policy tightening by the Fed. S&P 500 were last down -1% and dropping below 3,900, the level. And with eminis trading around 3,900 means that stocks are now at bearish Morgan Stanley’s year-end base case price target of 3900, and 100 points away from Michael Hartnett’s Fed put of 3,800.

The dollar continues its relentless ascent, sending the euro to a five-year low while the yen also perked up, as investors took a cue from a rally in bonds and ploughed into “safe-haven” currencies on concerns about inflation risks to global economic growth. Meanwhile, bonds around the globe are surging as fears mount over an economic slowdown and traders start pricing in the next recession, sending the yield on 10-year German bunds and US Treasuries down more than 10 basis points to about 2.82%.

Among notable premarket moves, Disney shares dropped after the media giant said growth in the second half of the year may not be as fast as previously expected, while Beyond Meat slumped 24% as Barclays downgraded the stock and analysts slashed their price targets following underwhelming results. Bank stocks slump in premarket trading Thursday, set for a sixth straight day of losses. In corporate news, Carlyle Group is set to buy Chinese packaging firm HCP for about $1 billion. Meanwhile, Brookfield Asset Management said it plans to list 25% of its asset-management business in a transaction that would value the new entity at $80 billion. Economic data due late today include initial jobless claims. Here are all the notable premarket movers:

- Disney (DIS US) shares drop 4.8% in premarket trading after the media giant said growth in the second half of the year may not be as fast as previously expected.

- Apple (AAPL US) shares fall as much as 1.4% in premarket trading Thursday, putting them on course to open more than 20% below their January peak.

- Beyond Meat (BYND US) shares slump 24% in US premarket trading as analysts slashed their targets on the plant-based food company following underwhelming results.

- Riot Blockchain (RIOT US) -6.1% in premarket trading, Marathon Digital (MARA US) -5.8%, MicroStrategy (MSTR US)-10% and Coinbase (COIN US) -7.3%

- Zoom (ZM US) shares decline as much as 4.5% in US premarket as Piper Sandler analyst James Fish cut the recommendation on the stock to neutral as he sees limited upside to paid video service.

- Dutch Bros (BROS US) slumps 42% in premarket trading after the drive-thru coffee chain’s guidance lagged analyst estimates, though some analysts see the dip in shares as a buying opportunity.

- Lordstown Motors (RIDE US) shares jump as much as 27% in U.S. premarket trading after the electric truck maker completed the sale of its factory to Foxconn.

- Rivian (RIVN US) gains 2.9% in premarket trading after the electric vehicle startup reaffirmed its annual production guidance, even as it navigates through supply chain snarls.

- Coupang (CPNG US) shares jump as much as 18% in US premarket trading after the Korean e- commerce firm reported a first-quarter loss per share that was narrower than analysts’ expectations.

- Bumble (BMBL US) shares rise 8.3% in premarket after the company reported first-quarter results that beat expectations, despite currency risks and those related to the war in Ukraine.

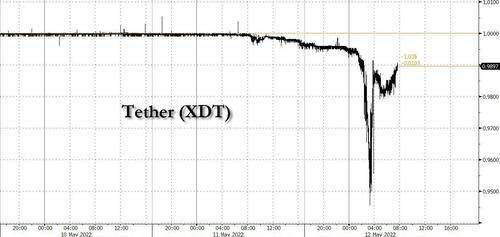

Cryptocurrency-exposed stocks also fell as digital tokens resumed declines after the collapse of the TerraUSD stablecoin, overnight the largest stablecoin, Tether, broke the buck spooking markets further that the contagion is spreading.

The hotter-than-expected inflation reading for April raised concern the Fed’s hikes aren’t bringing down prices fast enough and policy makers may have to resort to a 75bps move, rather than the half-point pace markets have come to grips with. Worries such a shift would crimp economic growth, combined with Russia’s war in Ukraine and China’s struggles with Covid, are battering risk assets.

The data halted a minor rebound in US equities, which are set for their longest weekly streak of losses since 2011, as investors worried that hawkish moves by central banks at a time of surging commodity prices and slowing earnings growth would spark a recession. While some strategists have said the rout has now made stock valuations attractive, others including Michael Wilson at Morgan Stanley warned of a bigger selloff.

“What these wild market moves are telling us is that investors have very little idea of whether we’re near a short-term base, or whether we’ve got further to fall,” said Michael Hewson, chief market analyst at CMC Markets UK.

“The higher-than-expected CPI figure may further fuel fears that the Fed will take policy higher than expected for longer than expected, draining precious liquidity from markets, which have until late been awash with it,” said Russ Mould, investment director at AJ Bell. “Until we get a meaningful move lower in inflation, not only one print, but a consistent two, three, four prints moving in the right direction, this market may remain range bound,” Mona Mahajan, senior investment strategist at Edward Jones & Co., said on Bloomberg Television.

Citigroup Inc. strategists said growth stocks, including the battered tech sector, will likely remain under pressure as central banks tighten monetary policy, driving yields higher. “Now that central banks are unwinding monetary support, growth stocks’ valuations have further to fall,” strategists including Robert Buckland wrote in a note. They are especially wary of growth stocks in the US, where the Nasdaq 100 is down 27% this year.

In Europe, the Stoxx 600 was down 2.2% with mining and consumer-products stocks leading declines. The Euro Stoxx 50 drops as much as 2.8%, Haven currencies perform well. The Stoxx 600 Basic Resources sub-index erased all YTD gains as a slide in metal prices and concerns about inflation fueled a selloff in the sector. Miners are the biggest laggard in the broader European equity benchmark on Thursday as major miners and steelmakers slip along with copper and iron ore prices. The basic resources sector (the sector is still second-best performing in Europe this year so far) fell as much as 5.6%, briefly erasing all YTD losses, and down to the lowest since January 3. Morgan Stanley strategists had downgraded miners to neutral on Wednesday, saying it’s time to take profits in the sector amid concerns inflation will lead to demand destruction. Here are the biggest movers:

- Telefonica shares rise as much as 4.5% after the Spanish carrier reported what analysts said was a solid set of quarterly earnings.

- STMicroelectronics gains as much as 4.1% as the chipmaker projects annual revenue of more than $20 billion for 2025-2027 period.

- Compass Group climbs as much as 2.5%, adding to Wednesday’s 7.4% advance, with Morgan Stanley lifting its price target to a Street-high.

- JD Sports rises as much as 3% after the UK sportswear chain said like-for-like sales for the 14-week period to May 7 were more than 5% higher than a year earlier.

- AS Roma advances as much as 15% after US billionaire Dan Friedkin made a tender offer for the roughly 13% of the Italian football team he doesn’t already own.

- The Stoxx 600 Basic Resources sub- index erases all YTD gains as a slide in metal prices and concerns about inflation fuel a selloff.

- Rio Tinto declines as much as 6%, Glencore -7.3%, Anglo American -6.9%, ArcelorMittal -4.8%, Antofagasta -7.9%

- Luxury stocks resume their declines after high US inflation bolstered the case for aggressive monetary tightening, deepening fears of an economic slowdown.

- Kering slides as much as 5.6%, Hermes -5.5% and Swatch -3.7%

- SalMar falls as much as 8.2% after the Norwegian salmon farmer published its latest quarterly earnings, which included a miss on operating Ebit.

Earlier in the session, Asian stocks resumed their slide after Wednesday’s modest gains, as US inflation topped estimates and new Covid-19 community cases in Shanghai damped prospects for a reopening. The MSCI Asia Pacific Index fell as much as 2%, with tech giants Alibaba and TSMC weighing the most on the gauge. Chinese shares snapped a two-day advance after Shanghai found two infections outside of isolation centers, pushing back the timeline for a relaxation of growth-sapping lockdowns. US inflation remained above 8% in April, keeping the Federal Reserve on the path of aggressive tightening. That prospect weighed on shares in Asia, as investors also factored in growth implications from continued lockdowns in the world’s second-largest economy. Markets appeared to be unimpressed by China’s Premier Li Keqiang’s comments urging officials to use fiscal and monetary policies to stabilize employment and the economy. Valuations for the MSCI Asia Pacific Index are hurtling toward pandemic lows as the index records a 29% decline from its 2021 peak, posting declines in all but one of the trading sessions so far this month.

“We’ve seen nearly the same amount of foreign investor selling in Asia as we saw during the global financial crisis, even though operating conditions aren’t as bad,” Timothy Moe, chief Asia-Pacific equity strategist at Goldman Sachs, told Bloomberg Television. “On our expected conditions over the next year, somewhere around 13 times should be a fair and appropriate valuation for Asian markets,” he added. Benchmarks in Indonesia and Taiwan were among the biggest decliners in the region, with the Jakarta Composite Index on the cusp of erasing gains for the year. Hong Kong shares also fell as the city intervened to defend its currency for the first time since 2019

In FX, the Bloomberg Dollar Spot Index rose to a fresh two-year high as the greenback climbed versus all of its Group-of-10 peers apart from the yen. The demand for havens sent the yield on 10-year German bunds and US Treasuries down more than 10 basis points. Stops were triggered in the euro below $1.0490 and 1.0450, weighed by EUR/CHF selling and yen buying across the board, according to traders. The yen rose by as much as 1.2% against the greenback as selling in stocks hurt risk sentiment. The BOJ indicated its lack of appetite for changing policy to help address a slide in the yen to a two-decade low during discussions at a meeting last month, according to a summary of opinions from the gathering. The Australian and New Zealand dollars fell on concern that lockdowns in China’s financial capital will extend, dragging economic growth in the world’s biggest buyer of commodities.

In rates, Treasuries extended Wednesday’s rally with yields richer by 6bp to 9bp across the curve, supported by risk-aversion as stocks extend losses. US 10-year yields around 2.82%, down 10bps on the session, and trailing gilts and bunds by 2.2bp and 3bp in the sector; intermediates lead the US curve, richening the 2s5s30s fly by 4bp on the day to tightest levels since March 23. Eurodollars are bid as well with the strip flattening out to early 2024 as rate-hike premium continues to erode. European fixed income extends gains. German and US curves bull-steepen; bunds outperform, richening ~12bps across the belly. Gilts bull-flatten, focusing on soft March GDP data over hawkish comments from BOE’s Ramsden. STIRs are similarly well bid with red pack euribor, eurodollar and sonia futures all up over 10 ticks. The US auction cycle concludes with $22b 30-year bond sale at 1pm ET; Wednesday’s 10-year is trading more than 10bp lower in yield after 1.4bp auction tail. WI 30-year around 2.965% is above auction stops since March 2019 and ~15bp cheaper than April stop-out. Super-long sectors led gains in Japanese bonds even as the 30-year sale was seen sluggish.

In commodities, base metals were under pressure; LME tin slumps over 8%, zinc down over 3.5%. European natural gas surged as much as 13% on supply concerns. Crude futures drop, fading roughly half of Wednesday’s rally. WTI is down over 2% near $103.50. Spot gold trades a narrow range near $1,850/oz. European natural gas prices jumped as disruptions to a key transit route through Ukraine and a move by Moscow to retaliate against sanctions ramped up the risk of supply cuts. Shanghai found two Covid cases outside government-run isolation centers on Wednesday, according to state-run CCTV, dampening prospects for potential easing of lockdowns. Prices of iron ore, the biggest commodity export from Australia, also fell on the news.

Looking at the day, data releases include the US PPI reading for April, the weekly initial jobless claims, and UK GDP for Q1. Central bank speakers include the ECB’s De Cos and Makhlouf. And in the political sphere, US President Biden will be hosting ASEAN leaders at the White House, whilst G7 foreign ministers are meeting in Germany.

Market Snapshot

- S&P 500 futures down 0.6% to 3,907.50

- STOXX Europe 600 down 1.9% to 419.41

- MXAP down 1.7% to 157.21

- MXAPJ down 2.5% to 512.05

- Nikkei down 1.8% to 25,748.72

- Topix down 1.2% to 1,829.18

- Hang Seng Index down 2.2% to 19,380.34

- Shanghai Composite down 0.1% to 3,054.99

- Sensex down 2.1% to 52,935.64

- Australia S&P/ASX 200 down 1.8% to 6,941.03

- Kospi down 1.6% to 2,550.08

- Gold spot down 0.1% to $1,849.85

- U.S. Dollar Index up 0.48% to 104.34

- German 10Y yield little changed at 0.89%

- Euro down 0.6% to $1.0449

- Brent Futures down 2.0% to $105.32/bbl

Top Overnight News from Bloomberg

- The EU is looking at creating bond futures and repurchase agreements to bolster its pandemic-era debt program

- The BOE will have to raise interest rates further to control surging prices, and there’s a risk that the UK’s worst inflation crisis in decades will take longer to ease fully, according to Deputy Governor Dave Ramsden

- The UK economy unexpectedly contracted in March. Gross domestic product fell 0.1% from February, when growth was flat. It meant the economy expanded just 0.8% in the first quarter, less than the 1% forecast by economists

- UK Prime Minister Boris Johnson will spend the next few days considering whether the UK will introduce legislation to override its post- Brexit settlement with the EU, a move that risks sparking a trade war

- A massive sell-off in cryptocurrencies wiped over $200 billion of wealth from the market in just 24 hours, according to estimates from price-tracking website CoinMarketCap

- Finland’s highest-ranking policy makers President Sauli Niinisto and Prime Minister Sanna Marin threw their weight behind an application and Sweden’s government is likely to do so in the coming days

- Sweden’s Riksbank’s target measure, CPIF, accelerated to 6.4% on an annual basis in April, the highest level since 1991, according to data released on Thursday. Economists surveyed by Bloomberg expected prices to rise by 6.2%

A more detailed look at global markets courtesy of Newsquawk

Asia-Pc stocks were pressured after the losses on Wall St where the major indices whipsawed in the aftermath of the firmer than expected CPI data and the DJIA posted a fifth consecutive losing streak. ASX 200 was lower amid heavy losses in tech and with financials subdued after flat earnings from Australia’s largest lender CBA. Nikkei 225 weakened with attention on earnings updates and with SoftBank amongst the worst performers ahead of its results later with the Co. anticipated to have suffered a record quarterly loss. Hang Seng and Shanghai Comp were subdued with early pressure from default concerns after developer Sunac China missed its grace period deadline and warned there was no assurance that the group will be able to meet financial obligations, although the mainland bourse recovered its earlier losses after further policy support pledges by Chinese authorities. SoftBank (9984 JT) – FY revenue JPY 6.2trln (prev. 5.6trln Y/Y). FY net profits -1.7trln (prev. +4.99trln). Foxconn (2317 TT) Q1 net profit TWD 29.45bln (exp. 29.76bln); sees Q2 revenue flat Y/Y, sees smart consumer electronics slightly declining Y/Y.

Top Asian News

- Rupee Tumbles to a Record Low, Stocks Slump on Inflation Woes

- SoftBank Vision Fund Posts a Record Loss as Son’s Bets Fail

- Yen Rebound Tipped as Recession Fears Push Down Treasury Yields

- More Defaults Seen Following Sunac’s Failure: Evergrande Update

European bourses are pressured as overnight risk sentiment reverberated into the region, in a continuation of the post-CPI Wall St. move; Euro Stoxx 50 -2.5%. US futures are lower across the board though the magnitude is less extreme, ES -0.6%; NQ fails to benefit from the yield pullback as participants focus on the normalisation’s impact on tech. Walt Disney Co (DIS) – Q2 2022 (USD): Adj. EPS 1.08 (exp. 1.19), Revenue 19.25bln (exp. 20.03bln). Disney+ subscribers 137.7mln (exp. 134.4mln). ESPN+ subscribers 22.3mln (exp. 22.5mln) -5.0% in the pre-market.

Top European News

- UK Retailers Sue Truckmakers Over Alleged Price Fixing

- Rokos Raising $1 Billion as He Joins Macro Hedge Fund Surge

- Siemens Abandons Russian Market After 170-Year Relationship

- Hargreaves Tumbles as Peel Notes Macro, Geopolitical Impacts

FX

- DXY tops 104.500 to set new 2022 peak as risk aversion intensifies.

- Yen regains safe haven premium to buck broadly weak trend vs Dollar, USD/JPY sub-128.50 vs top just over 130.00.

- Aussie and Kiwi flounder as commodities tumble on demand dynamics’; AUD/USD under 0.6900 and NZD/USD below 0.6250.

- Euro and Sterling give up big figure levels with the Pound also undermined by worse than forecast UK data; EUR/USD down through 1.0500 then 1.0450, Cable beneath 1.2200 and eyeing 1.2150 next.

- Swedish Crown holds up in wake of stronger than expected CPI and CPIF metrics; EUR/SEK straddles 10.6000.

- Yuan crushed as PBoC and Chinese Government reaffirm commitment to provide economic support; USD/CNY 6.7900+, USD/CNH just shy of 6.8300.

- Forint falls as NBH Deputy Governor contends that aggressive tightening period is over and future hikes likely more incremental.

- HKMA picks up pace of intervention to defend HKD peg, CNB steps in to support CZK.

Fixed Income

- Debt revival gathers pace amidst risk-off positioning elsewhere.

- Bunds probe 155.00, Gilts reach 120.71 and 10 year T-note nudges 120-00.

- BTP supply encounters few demand issues, unlike second US Quarterly Refunding leg ahead of USD 22bln long bond auction.

Commodities

- WTI and Brent are pressured in what has been a grinding move lower during European hours; however, benchmarks were lifted amid Kremlin/N. Korea updates.

- Currently, the benchmarks are lower by around USD 1.50/bbl.

- IEA OMR: Revises down oil demand growth projections for 2022 by 70k BPD, amid China lockdowns and elevated prices. Overall decline of Russian supply by 1.6mln BPD in May and 2mln BPD in June; could expand to circa. 3mln BPD from July onwards. Click here for more detail.

- OPEC MOMR to be released at 13:00BST/08:00EDT.

- Indian refineries purchased 25-30mln barrels of Russian oil at a discount for delivery in May-June, according to Interfax.

- Spot gold/silver are pressured amid the USD’s revival, but, the yellow metal remains in relatively contained parameters around USD 1850/oz.

US Event Calendar

- 08:30: May Initial Jobless Claims, est. 192,000, prior 200,000

- 08:30: April Continuing Claims, est. 1.37m, prior 1.38m

- 08:30: April PPI Final Demand MoM, est. 0.5%, prior 1.4%; YoY, est. 10.7%, prior 11.2%

- 08:30: April PPI Ex Food and Energy MoM, est. 0.6%, prior 1.0%; YoY, est. 8.9%, prior 9.2%

DB’s Jim Reid concludes the overnight wrap

It was all about the higher than expected US CPI report yesterday which added to Fed rate expectations, as well as hard landing expectations as revealed through the curve flattening that took place through the rest of the day. Longer dated Treasury yields fell (after initially spiking much higher) and equities fell sharply (S&P 500 -1.65%) after actually being higher for the first half of the US session. So a topsy-turvy day that kept the Vix above 30 for a fifth straight session.

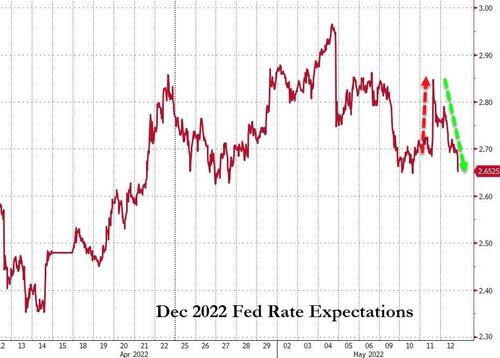

In terms of the details of that report, headline monthly CPI surprised to the upside with a +0.3% gain (vs. +0.2% expected), whilst monthly core CPI also surprised to the upside at +0.6% (vs. +0.4% expected). Thanks to base effects from last year, the year-on-year numbers managed to decline in spite of the upside monthly surprises, but they were also higher than expected with headline CPI at +8.3% (vs. +8.1% expected), and core CPI at +6.2% (vs. +6.0% expected).

Looking at the components, what will concern the Fed is that there are plenty of signs that inflation pressures remain broad and can’t be pinned on transitory shocks like the spike in energy prices of late. For instance, owners’ equivalent rent (which makes up nearly a quarter of the inflation basket) was up +0.45%, which is its fastest monthly pace since June 2006. Rents also remained strong with a +0.56% increase, which is just shy of its February increase and still the second-highest since December 1987. Food prices (+0.9%) also continued to move higher in April, bringing their year-on-year gain to a 41-year high of +9.4%. One consolation might be that the Cleveland Fed’s trimmed mean (which removes the outliers in either direction) saw its smallest monthly increase since last August at +0.45%, even if it’s still increasing well above rates seen throughout the 2010s.

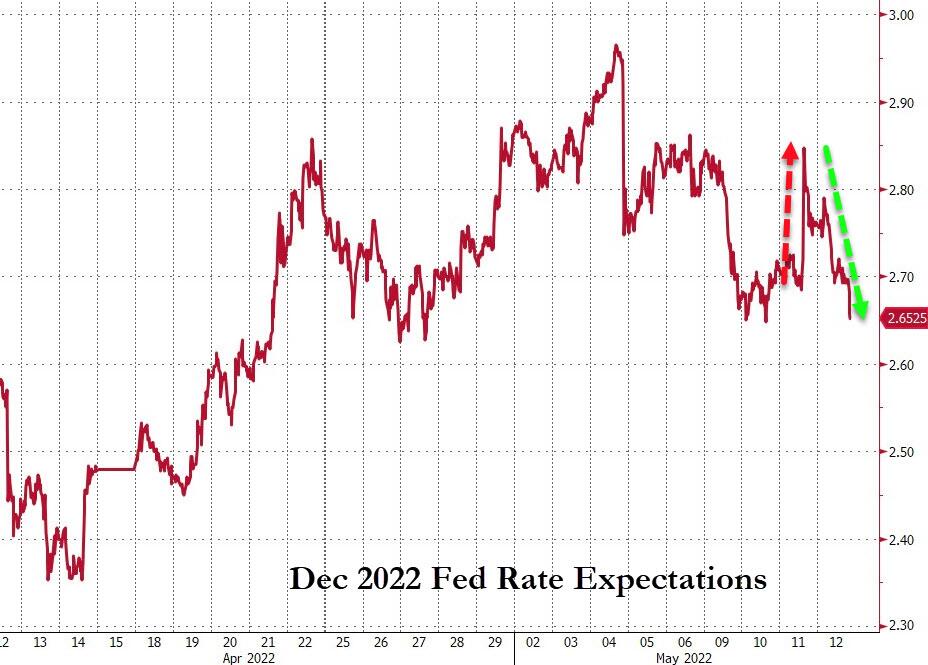

The fact the release surprised on the upside saw an immediate reaction across asset classes, with 10yr Treasury yields bouncing by more than +14bps intraday during the half hour following the report to 3.07%, before reversing all of this to end the day down -7.0bps to 2.92%. Ultimately the decline in real rates (-14.7bps) offset expectations of higher inflation (+8.1bps), but it was a different story at the front-end of the curve, where 2yr yields rose +2.5bps since the report was seen to raise the likelihood of larger hikes at the coming meetings, with the futures-implied rate for the December meeting rising +4.5bps on the day. In Asia, US 10 year yields are another -3.3bps lower with 2yrs flats. This has left the 2s10s curve at 24.3bps after trading as high as 48.5bps on Monday.

In terms of the reaction from Fed officials themselves, Atlanta Fed President Bostic said he would support +50bp hikes until policy reaches neutral, which suggests more +50bp hikes than just the next two meetings, which has been the common line from Fed speakers of late. Markets are placing a 58% chance on a +50bp hike at September, up from 49% the day before. Markets also increased the chance they place on the Fed being forced into a +75bp hike even at the June meeting, pricing a 14% chance versus 10% yesterday. We will also get the May CPI release ahead of the next FOMC meeting in June, but by that point they’ll be in their blackout period, so this is the last print they’ll be able to comment on ahead of their next decision, and will frame the chatter around whether 75bps might be back on the table at some point given inflation looks to be proving stickier than many had expected.

For equities, the CPI print drove indices lower at the open, but they bounced around all day as volatility remained elevated, ultimately closing near the lows. The S&P 500 fell -1.65%, led by tech and mega cap shares, while the Vix ended above 30 for the fifth straight session for the first time since the post-invasion bout of volatility gripped equity markets. As mentioned, tech stocks were the main underperformer, with the NASDAQ down by -3.18% as investors priced in faster hikes from the Fed this year. Separately in Europe, equities outperformed their US counterparts for a 3rd consecutive day, with the STOXX 600 posting a +1.74% advance but closing well before the US slump.

Whilst the main focus yesterday was on the US CPI report, there was significant central bank news in Europe as well after ECB President Lagarde put out a strong signal that July would be when the ECB starts hiking rates for the first time in over a decade. In her remarks, she said that the first hike “will take place some time after the end of net asset purchases”, and that “this could mean a period of only a few weeks”. A July hike would be in line with the call from our own European economists here at DB (link here), who see four consecutive quarter point hikes from July, taking the deposit rate up to +0.50% by year-end. That was then echoed by a separate Bloomberg report later in the session, which said that ECB officials were “increasingly embracing a scenario” where interest rates moved into positive territory by year-end. ECB policy pricing by the end of the year actually fell -1.3bps to 26.5bps, as a broader sovereign bond rally overpowered this.

With other ECB speakers having already been signalling their openness to a July hike, European sovereign bonds reacted more to the US CPI report than Lagarde’s remarks. So we ended up with a similar pattern to Treasuries, whereby yields surged following the US release before falling back to end the day lower on growth fears. Ultimately, that meant yields on 10yr bunds were down -1.5bps at 0.98%, and there was a significant narrowing in peripheral spreads too, with the gap between 10yr Italian yields and bunds down -9.9bps.

Asian equity markets are weaker overnight. The Hang Seng (-0.94%) is the largest underperformer across the region this morning after the Hong Kong Monetary Authority (HKMA) intervened into the currency markets for the first time since 2019 to defend the local dollar from capital outflows. The authority bought about HK$1.589 billion from the market to bolster the exchange rate in order to bring it back within the trading band i.e., between 7.75 and 7.85 versus the US dollar. Elsewhere, the Nikkei (-0.84%), Kospi (-0.56%) are also trading lower. Mainland Chinese stocks are showing a more mixed performance with the Shanghai Composite (+0.17%) higher while the CSI 300 (-0.07%) is a tad lower. Outside of Asia, US stock futures are flat but Euro Stoxx futures are catching down with the late US move last night and are around -2%.

According to the BOJ’s summary of opinions from the April 27-28 meeting, the board brushed aside the idea of countering sharp yen falls with interest rate hikes with several board members arguing in favour of maintaining the central bank’s massive stimulus programme.

Oil prices are lower in early Asian trade, taking a pause after Brent crude futures closed +4.93% higher last night. This morning, the contract is -1.15% down at $106.27/bbl as I type.

Elsewhere in markets, a significant story over the last 24 hours has been the significant price declines in a number of major cryptocurrencies. Bitcoin is at $27,617 as I type, a level not seen since December 2020. Coinbase’s share price was down a further -26.40% yesterday, bringing its losses over the last week alone to almost -60%.

A few other headlines worth highlighting. The Dallas Fed announced that Lorie Logan, the current manager of the Fed’s portfolio, would assume the role of President, which makes her a voter on the FOMC next year. Given her remit has been to manage the balance sheet, little is known about her views about monetary policy as of yet.

Finally on the Brexit front, there was a further ratcheting up in the comments between the UK and the EU over the Northern Ireland Protocol yesterday. UK PM Johnson said that “we need to sort it out”, and Levelling Up Secretary Gove said that “no option is off the table”. From the EU side however, Irish Foreign Minister Coveney said that the EU would need to react if the UK breached international law, and Bloomberg reported that the EU would likely suspend their trade deal with the UK if the UK were to revoke its commitments.

To the day ahead now, and data releases include the US PPI reading for April, the weekly initial jobless claims, and UK GDP for Q1. Central bank speakers include the ECB’s De Cos and Makhlouf. And in the political sphere, US President Biden will be hosting ASEAN leaders at the White House, whilst G7 foreign ministers are meeting in Germany.

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED down 3.71 PTS OR 0.12% //Hang Sang CLOSED down 444.23 PTS OR 2.24% /The Nikkei closed DOWN 464.92 OR 0.18% //Australia’s all ordinaires CLOSED DOWN 1.89% /Chinese yuan (ONSHORE) closed DOWN 6,7914 /Oil UP TO 104.54 dollars per barrel for WTI and down TO 106.17 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7914 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8189: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER//

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

END

3B JAPAN

3c CHINA

COVID//LOCKDOWNS//WHEAT CRISIS

What is going on in China?

Is A Wheat Crisis Developing In China As Farmers Cut Crops Early?

WEDNESDAY, MAY 11, 2022 – 06:40 PM

As global food prices remain at record highs and war wages in Europe between two of the world’s largest grain suppliers, troubling videos from China show farmers slashing winter wheat production ahead of harvest times, adding even more uncertainty about food security.

Bloomberg reports China’s agriculture ministry is very concerned about the matter. The ministry is investigating if there’s illegal destruction of wheat crops.

The ministry said this comes three weeks before harvests, adding the crop was subjected to devastating floods late last year. There’s also concern that soggy field conditions in southern China due to abnormal rainfall could affect farmers’ ability to harvest.

An analyst at Melbourne-based Thomas Elder Markets, Andrew Whitelaw, said it’s not surprising that farmers are cutting their wheat early for hay as this may be a better return on their money because of poor crop conditions.

“If China has a poor crop this season, then they will likely have to continue with a strong import program … there are “already question marks around China’s food security ambitions,” Whitelaw said, adding that the country has ramped up wheat imports this year.

Here are some videos of Chinese trucks loaded up with unripened wheat that will be used as animal feed instead flour for human consumption.

The situation in China adds to wheat production concerns in Ukraine, Russia’s unlikeness to ship the crop to “unfriendly” countries, India’s threats of wheat export bans due to severe weather, and planting issues in the US Northern Plains and Canada because of wet conditions. As a result of all of these issues that may tighten global food markets even further, US wheat futures hit a 14-year high on Monday.

END

CHINA/LOCKDOWNS

A very important read…it is also the real estate breakup that is causing much of the slowdown in China

(Daniel Lacalle/Mises Institute)

The Chinese Slowdown: Much More Than COVID

WEDNESDAY, MAY 11, 2022 – 05:40 PM

Authored by Daniel Lacalle via The Mises Institute,

The most recent macroeconomic figures show that the Chinese slowdown is much more severe than expected and not only attributable to the covid-19 lockdowns.

The lockdowns have an enormous impact. Twenty-six of 31 China mainland provinces have rising covid cases and the fear of a Shanghai-style lockdown is enormous. The information coming from Shanghai proves that these drastic lockdowns create an enormous damage to the population. Millions of citizens without food or medicine and rising suicides have shown that the infamous “zero covid” policy often disguises mass population control and repression.

It is easy to use the covid-19 lockdowns as the reason for the weakening of the Chinese economy but that would be a gross simplification. The problem is deeper.

China is going through a severe slowdown caused by the burst of the enormous real estate bubble and the crackdown on the private sector, which has led to a cut in investment growth.

According to Nomura Research, China faces the worst slowdown since the covid outbreak in 2020 and the world should be worried about a further slide, as the challenges persist. Official gross domestic product (GDP) figures may be massaged to deliver the government’s target, but all other macro figures point to a much weaker growth.

We must remember that there are two ways in which the Chinese government “boosts” real GDP: By publishing a low inflation and GDP deflator figure and by massively increasing credit and infrastructure spending. However, those two cannot disguise the importance of the weakening of the Chinese economy, because it is now structural.

The collapse of the real estate bubble is the biggest problem. A research paper by Kenneth Rogoff and Yuanchen Yang estimated that the real estate sector accounts for around 29 percent of China’s GDP. It is impossible for the Chinese government to offset the impact of such a massive part of the economy with other high-growth sectors. Furthermore, real estate’s impact on the job market is hard to substitute. Economist George Magnus warned that the impact of the real estate collapse would last for years.

To add to a difficult real estate problem, the government crackdown on the private sector makes it even more difficult to boost growth in other industries and businesses. The fear of constant political intervention is leading to a massive slowdown in foreign direct investment growth as well as fear of deploying capital and taking risks in the Chinese economy only to suffer grave penalties from the authorities when profits arrive.

The extent of the deterioration of the Chinese economy is evident in the recent leading indicators. The Caixin China General Manufacturing Purchasing Managers’ Index (PMI) slumped to a twenty-five-month low of 48.1 in March 2022, signaling contraction. The Caixin Services PMI plummeted to 42.0 in March from 50.2 in February, dropping below the level that separates growth from contraction. This reading indicates the sharpest activity decline since February 2020.

The political intervention in the technology sector, which is one of the leading job creators in China, has sparked fears of frozen headcounts and layoffs, according to various media reports. Additionally, the decision of the central bank to cut reserve requirements for banks has not avoided a significant decline in credit growth, as reported by JP Morgan.

To all this we must add a currency, the yuan, which is used in less than 3 percent of global transactions, according to Reuters, due to the extreme capital controls and the exchange rate fixing imposed by the central bank. Confidence in the local currency is low due to the extreme intervention on the currency market, which is preventing China from having a truly international means of payment.

China’s high debt is also a problem. Total debt stands above 300 percent of GDP, according to the Institute of International Finance. The European Central Bank (ECB) points out that China’s debt-to-GDP ratio for the entire private sector now stands at over 250 percent and the corporate component of this debt is the highest in the world. The ECB points also to the risk created because a “significant proportion of funding is supplied to the corporate sector by non-bank financial institutions” leading to higher risk taking and a shadow banking system that leads to large inefficiencies and solvency challenges.

The aggressive and misguided lockdowns are affecting supply chains and activity, but the structural problems of rising intervention in the currency and industries, as well as a heavily indebted economy, are likely to drag on real growth and jobs for a long t

END

HONG KONG

OH OH cracks are starting to appear for the first time in Hong Kong where they have to defend the Hong Kong dollar:

First Cracks: Hong Kong Intervenes To Prop Up Local Currency For First Time Since 2019

WEDNESDAY, MAY 11, 2022 – 10:00 PM

Things are starting to crack.

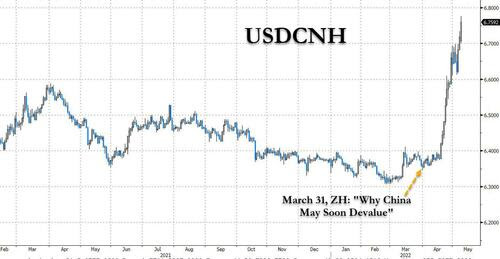

Two days after we reported that the Chinese yuan had cratered (just days after we warned that China will soon devalue) in what appears to be a concurrent devaluation alongside the plunging yen…

… a move that was of extreme importance for markets, yet which few financial commentators were discussing, on Wednesday the surging US dollar forced Hong Kong to intervene and defend its currency for the first time since 2019, putting further upward pressure on interest rates in an economy already reeling from strict pandemic border controls and a shaky property market.

Capital outflows fueled by rising interest rates in the US and continued modest easing in China, sent the Hong Kong dollar to the weak end of its 7.75-to-7.85 per greenback trading range late Wednesday.

And with the barrier in danger of breach, the Hong Kong Monetary Authority – the local central bank – bought about HK$1.59 billion to prop up the currency, which was still trading at the weak end on Thursday morning local time.

The testing of the band’s limit on Wednesday came around the same time as faster-than-expected US inflation data sent the greenback briefly up and Treasury yields surging. While gauges of the US dollar and longer-maturity Treasury yields subsequently retreated, Hong Kong’s currency continues to hover right near the band’s edge.

While the HKMA may have prevented the breach of the peg for now, further intervention will drain liquidity from Hong Kong’s financial system, slamming local assets and driving up borrowing costs at a time when the local economy is contracting under the weight of some of the world’s strictest Covid-containment controls. Rising interest rates also pose a threat to Hong Kong’s property market, with Goldman Sachs Group Inc. saying earlier this year that home prices in the world’s least affordable market may slump 20% by 2025.

While some commentators have called on Hong Kong to abandon its dollar peg, there’s little sign that authorities plan to change a system that has survived multiple speculative attacks since 1983 and helped turn the city into one of the world’s most important financial centers.

This time may be different, however, as selling of the local dollar has only intensified in recent months as the increasingly hawkish Fed boosted the US dollar, while pandemic restrictions in both China and the former British colony have damped local growth outlook, and forced authorities to keep rates and and consider how to ease further.

The Hong Kong dollar has weakened about 0.7% this year, far less thatn the Chinese yuan, with some of the declines coming as Fed rate hikes widened the funding rate gap between the US and the special administrative region, prompting traders to borrow the currency in the interbank market and sell it versus the higher-yielding greenback, Bloomberg reported. Making yield differential defense increasingly difficult, the premium of the three-month US interbank rate, known as Libor, over Hong Kong’s equivalent, Hibor, expanded to the widest since 2019 in April.

The Hong Kong dollar will remain under pressure as US yields climb on rate-hike bets, said Samuel Tse, an economist at DBS Bank Ltd. in Hong Kong.

end

4/EUROPEAN AFFAIRS//UK AFFAIRS/EU

.

FINLAND/NATO MEMBERSHIP

Finland Will Seek NATO Membership “Without Delay” As Russia Warns Of ‘Threat’ To National Security

THURSDAY, MAY 12, 2022 – 11:05 AM

In a final significant step just after the nation’s defense committee on Tuesday gave its formal recommendation in the affirmative, Finland’s president and prime minister have also now come out urging application for NATO membership “without delay”.

Sauli Niinisto and Sanna Marin said Thursday that a decision is likely during the next few days. “Finland must apply for NATO membership without delay,” they said in a joint statement. “We hope that the national steps still needed to make this decision will be taken rapidly within the next few days.”

A Thursday Pentagon spokesman statement was quick to welcome the imminent move, saying it would “not be difficult to integrate Finland into the NATO alliance” from a defense point of view, as cited by MSNBC.

At the same time NATO Secretary General Jens Stoltenberg vowed that the membership process would be “smooth and swift” for Finland. “This is a sovereign decision by Finland, which NATO fully respects,” Stoltenberg said, emphasizing that the Scandinavian country which shares an 810-mile long border with Russia would be “warmly welcomed into NATO”.