2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1836.30 DOWN $2.00

SILVER: $21.62 UP 9 CENTS

ACCESS MARKET: GOLD $1833/30

SILVER: $21.69

Bitcoin morning price: $21,252 UP 109

Bitcoin: afternoon price: $21,135 DOWN 8

Platinum price: closing UP $9.55 to $942.80

Palladium price; closing UP $56.-0 at $1881.45

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE:EXCHANGE: 0

COMEX 0

no. of contracts issued by JPMorgan: 0/0

_____________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 0 NOTICE(S) FOR 0 Oz//0 TONNES)

total notices so far: 23,741 contracts for 2,374,100 oz (73.947 tonnes)

SILVER NOTICES:

16 NOTICE(S) FILED 80,000 OZ/

total number of notices filed so far this month 1787 : for 8,935,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $2.00

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 1075.54 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 9 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV://BIG CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 3.506 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 547.166 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GOOD SIZED 515 CONTRACTS TO 143,588 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED DESPITE OUR $0.15 LOSS IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.15) BUT WERE SUCCESSFUL IN KNOCKING OFF SOME SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 16 CONTRACTS OR 80,000 OZ//NEW STANDING: 9,105,000 / // V) STRONG SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS :1005

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 14 days, total 11,002, contracts: 55.010 million oz OR 3.928 MILLION OZ PER DAY. (785 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 55.01 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 55.01 MILLION OZ

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 515 DESPITE OUR $0.15 LOSS IN SILVER PRICING AT THE COMEX// FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 450 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 80,000 QUEUE JUMP //NEW STANDING: 9,105,000 OZ // .. WE HAD A TINY SIZED LOSS OF 1 OI CONTRACTS ON THE TWO EXCHANGES FOR .005 MILLION OZ WITH THE GAIN IN PRICE.

WE HAD 16 NOTICES FILED TODAY FOR 80,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 2768 CONTRACTS TO 497,815AND FURTHER NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -2768 CONTRACTS.

.

THE FAIR GAIN IN COMEX OI CAME DESPITE OUR FALL IN PRICE OF $11.25//COMEX GOLD TRADING/FRIDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERING

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S 115 OZ QUEUE JUMP //NEW STANDING: 75.082TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $11.25 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 6070 OI CONTRACTS 18.88 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 745 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 497,815

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3302, WITH 2559 CONTRACTS INCREASED AT THE COMEX AND 743 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3302 CONTRACTS OR 10.270 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (743) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (2559,): TOTAL GAIN IN THE TWO EXCHANGES 3302 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING AND SOME ADDITION TO SPECULATOR SHORTS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 11,500 OZ//NEW STANDING: 75.082 TONNES / 3) ZERO LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING//SOME SPECULATOR SHORT ADDITIONS //.,4) FAIR SIZED COMEX OI GAIN 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

53,652 CONTRACTS OR 5,365,200 OZ OR 166.88 TONNES 14 TRADING DAY(S) AND THUS AVERAGING: 3832 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAY(S) IN TONNES: 166.88 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 166.88/3550 x 100% TONNES 4.70% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 166.88 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GOOD SIZED 451 CONTRACT OI TO 143,588 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 450 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 450 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 515 CONTRACTS AND ADD TO THE 450 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A TINY SIZED LOSS OF 1 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 0.005 MILLION OZ

OCCURRED WITH OUR FALL IN PRICE OF $0.15 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)TUESDAY MORNING// FRIDAY NIGHT

SHANGHAI CLOSED DOWN 8.71 PTS OR 0.26% //Hang Sang CLOSED UP 395.68 PTS OR 1.87% /The Nikkei closed UP 475.09 OR 1.40% //Australia’s all ordinaires CLOSED UP 1.38% /Chinese yuan (ONSHORE) closed UP 6.6994 /Oil DOWN TO 109.90 dollars per barrel for WTI and DOWN TO 115.05 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6994 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6991: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 2559 CONTRACTS TO 497,815 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR LOSS OF $11.25 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (743 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 743 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :743 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 743 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 6070 CONTRACTS IN THAT 743 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 5327 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR FALL IN PRICE OF GOLD $11.25.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JUNE (75.082),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 75.082 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $28.95) AND WERE UNSUCCESSFUL IN KNOCKING OFF SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A FAIR SIZED GAIN OF 3302 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (75.082 TONNES)…

WE HAD 2768 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3302 CONTRACTS OR 330,200 OZ OR 10.270 TONNES

Estimated gold volume 172,927/// poor/

final gold volumes/yesterday 147,432 /poor

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 21

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 163,455/679 oz Manfra JPMorgan 5069 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 0 notice(s)NIL OZ XXX |

| No of oz to be served (notices) | 398 contracts 39,800 oz1.2379 TONNES |

| Total monthly oz gold served (contracts) so far this month | 23,741 notices 2,374,100 OZ 73.947 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

0 customer deposits

total deposits: nil oz

2 customer withdrawals:

i) Out of Brinks 181,056.300 oz

ii) Out of Manfra 2218.419 oz (69 kilobars)

ii) Out of JPM: 160,755.000 oz (5000 kilobars)

total withdrawal: 163,455.679 oz

ADJUSTMENTS: 1/dealer to customer/Brinks:

160,787.151 oz Brinks

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 398 contracts having GAINED 63 contracts

We had 52 notices filed on FRIDAY so we GAINED 115 contracts or an additional 11,500 oz will stand for gold in this very active month of June

July has a LOSS OF 93 OI to stand at 1628

August has a GAIN of 1037 contracts UP to 412,817 contracts

We had 0 notice(s) filed today for NIL oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 52 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (23,741) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 398 CONTRACTS ) minus the number of notices served upon today 0 x 100 oz per contract equals 2,413,900 OZ OR 75.082 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (23,689) x 100 oz+ (398) OI for the front month minus the number of notices served upon today (0} x 100 oz} which equals 2,401,500 oz standing OR 75.082 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 75.082 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,419,784.828 oz 75.26 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 33,648,106.364 OZ

TOTAL ELIGIBLE GOLD: 16,300.766.440 OZ

TOTAL OF ALL REGISTERED GOLD: 17,347,339.924 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 14,921,555.0 OZ (REG GOLD- PLEDGED GOLD)

END

SILVWER/COMEX/JUNE 21

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 12,743.620 oz CNT Brinks |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 600.292.100 oz CNT |

| No of oz served today (contracts) | 16CONTRACT(S)80,000 OZ) |

| No of oz to be served (notices) | 18 contracts (90,000 oz) |

| Total monthly oz silver served (contracts) | 1803 contracts 9,015,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

| this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 0 deposit into the customer account

total deposit: 0 oz

JPMorgan has a total silver weight: 169,645 million oz/337.345 million =50.27% of comex

Comex withdrawals: 2

i)Brinks 7715.500 oz

ii)CNT 5028.12 oz

total withdrawal 12,743.620 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 71.388 MILLION OZ

TOTAL REG + ELIG. 337.375 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 34 HAVING LOST 11 CONTRACTS.

WE HAD 25 NOTICES FILED ON FRIDAY SO WE GAINED 16 CONTRACTS OR AN ADDITIONAL 80,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 2748 CONTRACTS DOWN TO 48,477 CONTRACTS.

AUGUST LOST 8 CONTRACTS TO STAND AT 982

SEPTEMBER HAD A GAIN OF 2325 CONTRACTS UP TO 74,980 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 16 for 80,000 oz

Comex volumes:83,386// est. volume today// good

Comex volume: confirmed yesterday: 58,701 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1803 x 5,000 oz = 9,015,000 oz

to which we add the difference between the open interest for the front month of JUNE(34) and the number of notices served upon today 16 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1803 (notices served so far) x 5000 oz + OI for front month of JUNE (34) – number of notices served upon today (16) x 5000 oz of silver standing for the JUNE contract month equates 9,105,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 21/WITH GOLD DOWN $2.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1075.54 TONES

JUNE 17/WITH GOLD DOWN $11.25: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.60 TONNES INTO THE GLD.///INVENTORY RESTS AT 1075.54 TONNES

JUNE 16/WITH GOLD UP $28.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.74 TONNES

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

JUNE 14/WITH GOLD DOWN $18.80/NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

GLD INVENTORY: 1075.54 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 21/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.506 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 547/166 MILLION OZ//

JUNE 17/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 739,000 OZ FROM THE SLV./:INVENTORY RESTS AT 543.660 MILLION OZ/

JUNE 16/WITH SILVER UP 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 14/WITH SILVER DOWN 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

CLOSING INVENTORY 547.166 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Is Fed Chair Powell’s “Soft Landing” Even Possible?

TUESDAY, JUN 21, 2022 – 01:45 PM

After last week’s FOMC meeting, Federal Reserve Chairman Jerome Powell claimed that a “soft landing” was still possible. In other words, he thinks the central bank will be able to slay red-hot inflation without tipping the economy into a recession.

Is this feasible? Or is it a fairytale?

Economist Daniel Lacalle leans toward fairytale. The word he uses is “impossible.”

After more than a decade of chained stimulus packages and extremely low rates, with trillions of dollars of monetary stimulus fueling elevated asset valuations and incentivizing an enormous leveraged bet on risk, the idea of a controlled explosion or a ‘soft landing” is impossible.”

Why?

Lacalle goes on to explain.

The following was originally published by the Mises Wire. The opinions expressed do not necessarily reflect those of Peter Schiff or SchiffGold.

In an interview with Marketplace, the Federal Reserve chairman admitted that “a soft landing is really just getting back to 2 percent inflation while keeping the labor market strong. And it’s quite challenging to accomplish that right now.” He went on to say that “nonetheless, we think there are pathways … for us to get there.”

The first problem of a soft landing is the evidence of weak economic data. While the headline unemployment rate appears robust, both the labor participation and employment rate show a different picture, as they have been stagnant for almost a year. Both the labor force participation rate, at 62.2 percent, and the employment-population ratio, at 60.0 percent remain each 1.2 percentage points below their February 2020 values, as the April Jobs Report shows. Real wages are down, as inflation completely eats away the nominal wage increase. According to the Bureau of Labor Statistics, real average hourly earnings decreased 2.6 percent, seasonally adjusted, from April 2021 to April 2022. The change in real average hourly earnings combined with a decrease of 0.9 percent in the average workweek resulted in a 3.4 percent decrease in real average weekly earnings over this period.

The University of Michigan consumer confidence in early May fell to an eleven-year low of 59.1, from 65.2, deep into recessionary territory. The current conditions index fell to 63.6, from 69.4, but the expectations index plummeted to 56.3, from 62.5.

The second problem of believing in a soft landing is underestimating the chain reaction impact of even allegedly small corrections in markets. With global debt at all-time highs and margin debt in the US alone at $773 billion, expectations of a controlled explosion where markets and the indebted sectors will absorb the rate hikes without significant damage to the economy are simply too optimistic. Margin debt remains more than $170 billion above the 2019 level, which was an all-time high at the time.

However, the biggest problem is that the Federal Reserve wants to curb inflation while at the same time the Federal government is unwilling to reduce spending. Ultimately, inflation is reduced by cutting the amount of broad money in the economy, and if government spending remains the same, the efforts to reduce inflation will only come from obliterating the private sector through higher cost of debt and a collapse in consumption. You know that the economy is in trouble when the fiscal deficit is only reduced to $360 billion in the first seven months of fiscal year 2022 despite record receipts and the tailwind of a strong recovery in GDP. Now, with GDP growth likely to be flat in the first six months but mandatory and discretionary spending still virtually intact, government consumption of monetary reserves is likely to keep core inflation elevated even if oil and gas prices moderate.

The Federal Reserve cannot expect a soft landing when the economy did not even take off, it was bloated with a chain of newly printed stimulus packages that have made the debt soar and created the perverse incentive to monetize all that the Federal government overspends.

The idea of a gradual cooling down of the economy is also negated by the reality of emerging markets and European banks. The relative strength of the US dollar is already creating enormous financial holes in the assets of a financial system that has built the largest carry trade against the dollar in decades. It is almost impossible to calculate the nominal and real losses in pension funds and the negative result of financial institutions in the most aggressively priced assets, from socially responsible investment and technology to infrastructure and private equity. We can see that markets have lost more than $7 trillion in capitalization in the year so far with a very modest move from the Federal Reserve. The impact of these losses is not evident yet in financial institutions, but the write-downs are likely to be significant into the second half of 2022, leading to a credit crunch exacerbated by rate hikes.

Central banks always underestimate how quickly the core capital of a financial institution can dissolve into inexistence. Even the financial system itself is unable to really understand the complexity of the cross-asset impact of a widespread slump in extremely generous valuations throughout all kinds of assets. That is why stress tests always fail. And financial institutions all over the world have abandoned the healthy process of provisioning expecting a lengthy and solid recovery.

The Federal Reserve tries to convince the world that rates will remain negative in real terms for a long time, but borrowing costs globally are surging while the US dollar is strengthening, creating an enormous vacuum effect that can create significant negative effects on the real economy before the Federal Reserve even realizes that the market is weaker than they anticipated, and liquidity is significantly lower than they calculated.

There is no easy solution.

There is no possible painless normalization path. After a massive monetary binge there is no soft hangover. The only thing that the Federal Reserve should have learnt is that the enormous stimulus plans of 2020 created the worst outcome: stubbornly high core inflation with weakening economic growth.

There are only two possibilities:

- To truly tackle inflation and risk a financial crisis led by the US dollar vacuum effect or

- to forget about inflation, make citizens poorer and maintain the so-called bubble of everything.

None is good but they wanted a decisive and unprecedented response to the pandemic lockdowns and created a decisive and unprecedented global financial risk. They thought money creation was not an issue and now the accumulated risk is so high it is hard to see how to tackle it.

One day someone may finally understand that supply shocks are addressed with supply-side policies, not with demand ones. Now it is too late. Powell will have to choose between the risk of a global financial meltdown or prolonged inflation.

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg

END

3. Chris Powell of GATA provides to us very important physical commentaries

Strange!! Russian gold is not taboo?? Switzerland imports 3 tons of gold from Russia

(Eddie Spence/Bloomberg/GATA)

Switzerland imports Russian gold for first time since Ukraine war

Submitted by admin on Tue, 2022-06-21 06:41 Section: Daily Dispatches

By Eddie Spence

Bloomberg News

Tuesday, June 21, 2022

Switzerland imported gold from Russia for the first time since the invasion of Ukraine, showing the industry’s stance toward the nation’s precious metals may be softening.

More than 3 tons of gold was shipped to Switzerland from Russia in May, according to data from the Swiss Federal Customs Administration. That’s the first shipment between the countries since February.

The shipments represent about 2% of gold imports into the key refining hub last month. It may also mark a change in perception of Russian bullion, which became taboo following the invasion.

Most refiners swore off accepting new gold from Russia after the London Bullion Market Association removed the country’s own fabricators from its accredited list. …

… For the remainder of the report:

end

Larry Summers’ new study finds inflation is as bad as in the 80’s

Robert Lambourne/GATA//Chris Powell

Robert Lambourne: Larry Summers’ new study finds inflation is as bad as in the ’80s

Submitted by admin on Sat, 2022-06-18 19:53Section: Daily Dispatches

But today’s U.S. debt burden is far worse, and so interest rate increases are far more dangerous.

* * *

By Robert Lambourne

Saturday, June 18, 2022

This month the National Bureau of Economic Research, based in Cambridge, Massachusetts, published a study titled “Comparing Past and Present Inflation”:

And:

One of the study’s three authors is former U.S. Treasury Secretary Lawrence Summers, a professor at Harvard University, who is well known to GATA followers as the joint author of the obscure economic study published in August 1985, “Gibson’s Paradox and the Gold Standard”:

A reasonably comprehensive summary of how the latter study fit into the government policy scheme to suppress gold prices is available in my report published by GATA six months ago:

https://www.gata.org/node/21603

Extracts from this summary are used here to highlight the principal modern reason for controlling the gold price. This reason was first examined outside official channels by GATA consultant Reginald Howe, who produced a report about it in 2005:

http://goldensextant.com/gibsonsparadox/

Gibson’s Paradox was the observation that the price level and nominal interest rates were positively correlated over long periods. In essence Summers’ study on Gibson’s Paradox claims to have found empirical evidence of an inverse relationship between the real price of gold and the real interest rate, a relationship that was examined by the authors over long periods that both included and excluded operation of a gold standard.

Essentially Summers’ study suggests that lower interest rates are correlated with higher gold prices. This implies that if gold prices are surreptitiously suppressed, with financial markets unaware of the suppression, the market comes to believe that interest rates are sufficiently high, making it much easier for monetary authorities to maintain lower real interest rates.

In Howe’s study is a chart suggesting that around 1995 the Gibson relationship between gold prices and interest rates broke down and this seems to have been the result of a policy decision by the U.S. monetary authorities.

Perhaps not coincidentally, Professor Summers was deputy Treasury secretary at the time.

GATA has collected more evidence that since the 1990s gold prices have been suppressed by way of gold leasing by central banks and the use of gold derivatives, plus the occasional dumping by central banks of physical gold. This period has coincided with a sharp fall in both nominal and real interest rates. In GATA’s view these low rates are the main objective of the gold price suppression policy followed since the 1990s.

The main interest in the new NBER study for monetary metals investors is the conclusion it draws about the present rate of inflation — that present inflation is far closer to the rate reported at the time of the monetary squeeze imposed in 1979 and the early 1980s by the Federal Reserve under Chairman Paul Volcker.

This NBER study’s conclusion is based on work done to recalculate, using present methods, the Consumer Price Index as it was reported in the 1980s.

That the current formula of calculating the CPI produces much lower rates of inflation than the formula used 40 years ago is well understood by many gold investors. For example, the internet site Shadowstats.com details many changes made to the calculation of official consumer price statistics to reduce the level of reported inflation from what earlier formulas would produce:

The recent NBER study suggests that the originally reported core CPI in June 1980, 13.6%, would have been only 9.1% using the current formula for calculating the CPI. This compares to a core CPI of 6.0% reported in May this year.

Consequently the study concludes “that to return to 2% core CPI today, we thus need disinflation of a similar magnitude as Chairman Volcker achieved.”

In commentary on the new NBER study published this month by The Guardian —

— the newspaper’s economics editor, Larry Elliot, wrote:

“The shock treatment administered by Volcker in the early 1980s resulted in official interest rates nudging 20% and the unemployment rate hitting a postwar high of 11%.”

Recent mainstream economic comment has suggested that a much lower level of nominal interest rates would be sufficient to bring the CPI down to 2%. But if the new NBER study is correct, this will not be nearly enough to cut inflation to 2% and interest rates will have to rise much higher.

Given that federal government debt is now in excess of $30 trillion, increasing short-term nominal rates to around 20% would have a disastrous impact on debt-funding costs. So it seems safe to conclude that policymakers would have to work out some way to devalue the debt, perhaps with some sort of debt jubilee or vast monetization of the debt by the Fed.

The new NBER study seems to be a reluctant recognition that the period of substantial government borrowing at low interest rates is over. As a result, much higher monetary metals prices may be expected with the dollar declining substantially in value. The years of gold price suppression seem likely to lead to the gold price in dollars rising to very high levels.

Regrettably, this suggests that outlawing the ownership of gold remains a distinct possibility.

—-

Robert Lambourne is a retired business executive in the United Kingdom and a GATA consultant.

CHRIS POWELL, Secretary/Treasurer

end

Pam and Russ Martens describes how the crypto and blockchains have been shams all along

(Pam and Russ Martens/WallStreet on Parade/GATA)

Pam and Russ Martens: Crypto and blockchain have been shams all along

Submitted by admin on Fri, 2022-06-17 11:34Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Friday, June 17, 2022

Crypto pushers hired themselves Trump’s outgoing SEC Chairman, Jay Clayton; a boatload of celebrities like Matt Damon, LeBron James, Spike Lee, Tom Brady, and Alec Baldwin, among numerous others; and high-priced lobbyists to sway Congress and state legislatures to back off any regulatory push. Crypto even slapped its name on sports stadiums and arenas — similar to Enron and Citigroup just before they blew up from specious business models.

Like any other pump-and-dump scheme, cryptomania worked for a while. Insiders grabbed their windfall profits early and left the unsophisticated with the losses.

Now crypto concerns are hiring themselves the likes of big law firm Akin Gump to explain why investors can’t get access to $11 billion in frozen accounts at Celsius Network.

The warnings have been out there for years now from experts in the legal and scientific communities, that when it comes to crypto, there is no “there” there. …

… For the remainder of the commentary:

end

A good read..

Alasdair Macleod/GATA)

Alasdair Macleod: A perfect storm in banking is brewing

Submitted by admin on Thu, 2022-06-16 11:00Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, June 16, 2022

Now that interest rates are rising with much further to go, the global banking system faces a crisis on a scale like no other in history. Central banks loaded with financial securities acquired through quantitative easing face growing losses, and their balance sheet liabilities are now significantly greater than their assets — a condition that in the private sector is termed bankruptcy. They will need to be recapitalised urgently to retain credibility.

Further, banking regulators have made a prodigious error in their oversight of the commercial banking system by focusing almost solely on bank balance sheet liquidity as the principal determinant of risk exposure. And on the few occasions in the past when they have demanded that banks increase their own capital, it has always been through the creation of preference shares and pseudo-equities to avoid diluting the true shareholders.

The consequence is that the level of leverage for common equity shareholders in the global systemically important banks has risen to stratospheric levels.

The regulators may be comfortable with their liquidity approach, but they have ignored the periodic certainty of a contraction in bank credit and the consequences for banks’ equity interests. Meanwhile, global systematically important banks have asset-to-common equity ratios often more than 50 times, with some in the eurozone over 70. It is hardly surprising that most G-SIBs are valued in the equity markets at substantial discounts to book value.

G-SIBs have accumulated excessive exposure to financial assets, both on-balance sheet and as loan collateral. With vicious bear markets now evident and further interest rate rises guaranteed by falling purchasing power for currencies, the one thing regulators have not allowed for is now happening. Like a deepening meteorological low, bank credit is contracting into a perfect storm.

Jamie Dimon’s recent warning that his bank (JPMorgan Chase) faces hurricane conditions confirms the timing. Central banks, bankrupt in all but name, will be tasked with rescuing entire commercial banking networks, bankrupted by a collapse in bank credit. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/a-perfect-storm-in-banking-is-brewing?gmrefcode=gata

end

4.OTHER GOLD/SILVER COMMENTARIES

Andrew Maguire says Blackrock defaulted on SLV during Silver Squeeze

While the world has gone on and many have forgotten that the Silver Squeeze of February 2021 ever occurred, some significant questions remain that affect the future path of the silver price.

And now adding to even further intrigue is that Andrew Maguire is reporting that

Blackrock actually defaulted on investors who requested metal during that volatile time in the silver market.

In one of his recent podcasts he made that shocking revelation, and also mentioned one calculation for how much leverage there is in the paper silver market relative to each ounce of physical silver.

So to find out more, as well as the rest of the latest news that will impact tomorrow’s silver price, click to watch this video now!

https://lemetropolecafe.com/pfv.cfm?pfvID=17778

end

5.OTHER COMMODITIES //LITHIUM

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.76994

OFFSHORE YUAN: 6.6981

HANG SANG CLOSED UP 395.68 PTS OR 1.87%

2. Nikkei closed UP 475.89% OR 1.84%

3. Europe stocks ALL CLOSED ALL GREEN

USA dollar INDEX DOWN TO 104.07/Euro RISES TO 1.0548

3b Japan 10 YR bond yield: FALLS TO. +.240/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 135.96/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen FOEN CHINESE YUAN: UP -// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.907%/Italian 10 Yr bond yield RISES to 4.03% /SPAIN 10 YR BOND YIELD RISES TO 3.03%…ALL BLOWING UP!!

3i Greek 10 year bond yield FALLS TO 3.88//

3j Gold at $1832.50 silver at: 21.65 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

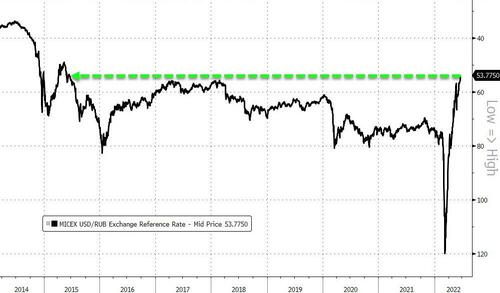

3k USA vs Russian rouble;// Russian rouble UP 1 & 1/10 roubles/dollar; ROUBLE AT 54.58

3m oil into the 109 dollar handle for WTI and 115 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 135.95DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9681– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0212well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.281 UP 4 BASIS PTS

USA 30 YR BOND YIELD: 3.325 UP 6 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.34

Futures, Cryptos Surge As Dip Buying Turns Into “Nasty Squeeze”

TUESDAY, JUN 21, 2022 – 08:02 AM

Following a relentless rout that erased nearly $2 trillion in market value from the S&P 500 last week, US equity futures have surged, extending their Monday holiday gains just as predicted on Sunday when we said that a “Nasty Squeeze” was on Deck following last week’s “Second Largest Ever” shorting by hedge funds. Nasdaq 100 futures rose as much as 2.2% before trading 1.7% higher as major US tech and internet stocks advanced, poised to extend Friday’s gains; shares of Tesla and Twitter also rose following billionaire Elon Musk’s comments at the Qatar Economic Forum; S&P 500 futures gained 1.8%; the cash market was closed on Monday for a holiday. Asian and European stocks also advanced as did bitcoin which jumped above $21K after sliding below $18K briefly on Saturday. Meanwhile Treasuries and the US Dollar retreated.

US stocks came under renewed pressure last week, with the S&P plunged into bear market territory amid surging inflation and fears that aggressive rate hikes by the Federal Reserve will push the economy into a recession. The S&P 500 is set for an 11% drop in June, poised for the worst month since March 2020, which marked the lows of the pandemic selloff. Sentiment was somewhat boosted by Biden’s Monday comments on the economy in which he said that a recession isn’t “inevitable” (what else will he say) but strategists have warned of more volatility ahead.

“Even if the mid-term investing landscape remains blurry to most market operators at the beginning of this summer season, some investors looking for opportunities to buy shares at a discounted price have been reassured,” said Pierre Veyret, a technical analyst at ActivTrades. “The fact central banks are moving quickly towards a super hawkish stance in order to tame inflation is also perceived as good news by some.”

In premarket trading, bank stocks also pushed higher amid a broader rebound in risk assets. In corporate news, HSBC has lost two senior investment bankers in Asia as global banks compete for financial technology talent and dealmaking slows. Meanwhile, the UK’s Payment Systems Regulator will focus a pair of market reviews on the rising card fees charged by Visa and Mastercard. Tech names were also solidly higher; notable movers included Apple +2.4%, Microsoft +2%, Amazon.com +2.6%, Alphabet +2.6%, Meta Platforms +2.1%, Nvidia +3.1% premarket; all six stocks closed higher on Friday, while US markets were closed for a holiday on Monday. Stocks related to cryptocurrencies were also indicating a rally as the price of Bitcoin continues to hold above $20,000 amid a tentative recovery and hopes that prices have bottomed. Meanwhile, Revlon surged as much as 27% in premarket trading, extending Friday’s rally after the cosmetics firm filed for Chapter 11 bankruptcy. Here are some other notable premarket movers:

Tesla (TSLA US) and Twitter (TWTR US) shares rose in premarket trading on Tuesday after billionaire Elon Musk said the CEO label at the social media firm was less important than driving the product and that Tesla will cut its salaried workforce by about 10% over the next three months. Tesla rose 3.1% and Twitter was up 1.2% in premarket trading

- Revlon shares surge as much as 27% in US premarket trading, extending Friday’s rally after the cosmetics firm filed for bankruptcy.

- Major US technology and internet stocks advanced in premarket trading on Tuesday, poised to extend Friday’s gains. Apple (AAPL US) +2.4%, Microsoft (MSFT US) +2%, Amazon.com (AMZN US) +2.6%, Alphabet (GOOGL US) +2.6%

- Spirit (SAVE US) shares jump 13% in US premarket trading, to $24, after JetBlue (JBLU US) raised its offer to $33.50 per share from $31.50 on June 6, the latest move in a multi-billion dollar takeover contest with rival Frontier (ULCC US). Arrival shares jump 8.6% in US premarket trading after the electric- vehicle maker announced that its zero-emission van has achieved EU certification and received European Whole Vehicle Type Approval.

- US-listed Chinese stocks are mostly higher in premarket trading, tracking a two-day 2.3% rise in the Hang Seng Tech Index.

- Alibaba (BABA US) +4.6%, Baidu (BIDU US) +3.5%, Pinduoduo (PDD US)+3.3%

- Stocks related to cryptocurrencies rise on Tuesday in US premarket trading as the price of Bitcoin continues to hold above $20,000 amid a tentative recovery and hopes that prices have bottomed. Riot Blockchain (RIOT US) +5.6%, Coinbase (COIN US) +4.7%, MicroStrategy (MSTR US) +5%

- Citi cuts ratings on International Paper Co. and WestRock to neutral from buy, citing increasing questions about demand as supply additions loom. International Paper falls 1.1% in premarket trading, WestRock -1.5%

- Keep an eye on Maxar shares as Wells Fargo said the stock is its top pick in the burgeoning space sector, initiating it at overweight, Rocket Lab at equal-weight and Virgin Galactic at underweight.

- Adobe (ADBE US) shares may be in focus today as the stock was downgraded to equal-weight and given Street-low $362 target from $591 by Morgan Stanley, on expectation of a slowing structural growth profile for the computer software company.

After unexpectedly accelerating to a fresh 40-year high in May, US consumer price growth is seen slowing, with a Bloomberg survey of economists predicting 6.5% by the fourth quarter and to 3.5% by the middle of next year. Yet fears are rampant that Federal Reserve policy makers intent on cooling price pressures will go too far and trigger an economic slowdown. Strategists at Morgan Stanley and Goldman Sachs Group Inc. warned equities may have further to fall to fully price in the risk of recession, reflecting wider skepticism about Tuesday’s rebound.

“We think equities will struggle to rebound sustainably until earnings expectations reset lower and/or central banks turn more dovish, which seems unlikely for now,” said Emmanuel Cau, head of European equity strategy at Barclays Plc.

European stocks also extended their recent recovery, with the region’s benchmark Stoxx 600 Index rising 1%, led by gains in basic resources and chemical companies’ shares. Consumer discretionary, chemicals and autos also trade well. CAC 40 outperforms.

- Leonardo jumps as much as 9.7% in Milan trading after its DRS unit agreed to buy Israeli radar-maker RADA Electronic in an all-stock transaction.

- Valneva rises as much as 23% after CEO Franck Grimaud said the company’s Lyme disease vaccine has the potential of becoming a “blockbuster” with sales of more than 1 billion euros.

- K+S and OCI shares gain after JPMorgan said valuations are “compelling” and fundamentals remain positive. European fertilizer shares had dropped recently because of rising gas prices. OCI rises as much as 4.6%; K+S +6.3%

- Air Liquide climbs as much as 3.9%, after the French industrial gas company signed a long-term power purchase agreement with Vattenfall.

- Mithra rises as much as 21% after the pharmaceutical company said it received subscription commitments for 3.87m new shares at an issue price of EU6.07 apiece, representing a 5% discount to last close.

- Richemont and Swatch advance after Swiss watch exports for the month of May showed strong demand versus the year-earlier period in the US and Japan as well as in European countries such as France and the UK. Luxury peers also trading higher in a wider rebound. Richemont gains as much as 2.8%, Swatch +2.8%, Hermes +3.3%, LVMH +3.7%

- European apparel retail shares drop after JPMorgan downgrades Asos, About You, Boohoo and Primark owner AB Foods to neutral from overweight, citing the cost of living crisis with cracks emerging in discretionary spending. Asos declines as much as 5.1%, Boohoo -4.8%, About You -4.3%, AB Foods -3.2%

- Proximus and Telenet slide after a statement by the Belgian telecom regulator showed that new entrant Citymesh partnered with Romanian carrier Digi Communications and acquired spectrum across various bands. Proximus shares fall as much as 7.8%, Telenet -3.9%

Earlier in the session, MSCI’s Asia-Pacific index snapped an eight-day slide to add more than 1% as Asian equities headed for their biggest gain this month. The MSCI Asia Pacific Index climbed as much as 1.8%, set to snap an eight-day losing streak, with financial and tech stocks among the biggest contributors to its advance. The US president spoke overnight after a conversation with former Treasury Secretary Lawrence Summers, as the White House and congressional Democrats are in talks on legislation that aims to fight inflation. Benchmarks in Taiwan, Japan and Hong Kong led gains in the region. Australia’s index advanced for the first time in days after central bank chief Philip Lowe signaled he will only raise interest rates by 25-to-50 basis points at the July meeting. Chinese shares edged lower after recent gains. “It’s a respite, not a rebound,” said Charu Chanana, a market strategist at Saxo Capital Markets. “We are still in a bear market that is facing a double whammy of Fed tightening and building recession fears, and the second-quarter earnings season is likely to be particularly painful for the markets” due to cost pressures, she added. Valuations for the MSCI Asia gauge have continued to slide toward pandemic lows, with the index down 18% this year. Still, it’s outperforming a measure of global shares, supported by a rally in Chinese equities this month as the country emerges from Covid-triggered lockdowns.

Japanese stocks advanced as investors weighed the impact of the yen’s weakness and the extent of the recent selloff. The Topix Index rose 2% to 1,856.20 as of market close Tokyo time, while the Nikkei advanced 1.8% to 26,246.31. Sony Group Corp. contributed the most to the Topix Index gain, increasing 4%. Out of 2,170 shares in the index, 2,023 rose and 108 fell, while 39 were unchanged. “Stocks that are expected to have an upward revision from the weak yen may be firm,” said Mitsushige Akino, a senior executive officer at Ichiyoshi Asset Management.

In Australia, the S&P/ASX 200 index rose 1.4% to close at 6,523.80, snapping a seven day losing steak. The benchmark was led by gains in banks and miners, with the financials sub-gauge rising the most since March 10. In early trade, Australia’s central bank Governor Philip Lowe said he didn’t see a recession on the horizon for the nation. In New Zealand, the S&P/NZX 50 index rose 1.1% to 10,701.59

India’s benchmark share index posted its biggest two-day advance since May 30, boosted by a recovery in information technology stocks and as investors looked for bargains after a sharp selloff last week. The S&P BSE Sensex rose 1.8% to close at 52,532.07 in Mumbai, taking its two-day advance to 2.3%. The NSE Nifty 50 Index advanced 1.9%. All of the 19 sectoral indexes compiled by BSE Ltd. gained, led by a measure of oil & gas companies. “Crude prices have corrected by almost 10% from its recent peak, providing some breather to the Indian market,” Motilal Oswal Financial analyst Siddhartha Khemka wrote in a note. Reliance Industries contributed the most to the Sensex’s gain, increasing 1.6%. All but one of 30 shares in the Sensex index rose. Of the top ten performers on the measure, half were information technology companies, led by Tata Consultancy Services Ltd. that clocked its biggest advance this month.

In rates, treasuries were cheaper across the curve as trading resumed after Monday’s US holiday; cash USTs bear steepened, but trim losses after cheapening ~5bps at the Asia reopen. Long-end leads losses with stock futures rising after last week’s rout. US yields are ere cheaper by as much as 6bp at long end, steepening 2s10s by nearly 3bp, 5s30s by nearly 4bp; 10-year, higher by ~5bp at 3.27% lags bund and gilts by 3bp and 4.5bp while Italian bonds outperform Treasuries by 12bp in the sector. Bunds and gilts outperform Treasuries, while Italian bonds extend recent gains after ECB’s Olli Rehn reiterated determination to combat unwarranted spikes in borrowing costs for some of the region’s most vulnerable economies. That said the ECB has yet to disclose said measures, a move which most agree will lead to selling the news. Gilts bull flatten, 10y yields drop 4bps after stalling near 2.6%. Bunds are comparatively quiet. Shorter-maturity Australian bonds rallied after central bank chief Philip Lowe said interest rates are likely to rise by 50 basis points at most in July. Money markets subsequently scrapped bets he would track the Federal Reserve with a 75 basis-point move. Japanese government bonds were mixed after a five-year note sale that drew the weakest demand in more than two years in the aftermath of wild price swings in futures that have made some traders uneasy about their exposure to cash bonds.

In FX, Bloomberg dollar spot index fell 0.3% as the greenback weakened against all of its Group-of-10 peers apart from the yen. JPY is the weakest in G-10, plunging to a fresh 24 year low of 136. NOK and SEK outperform. The euro advanced and European bonds rallied, led by the front end even as ECB Governing Council Member Peter Kazimir said negative rates must be history by September. Governing Council member Olli Rehn separetely said that “there has been good reason to expedite the normalization of monetary policy”. The pound extended gains amid broad dollar weakness while UK government bonds inched up. BOE Chief Economist Huw Pill said policy makers would sacrifice growth in order to bring down inflation, saying there’s a risk of prices developing a “self-sustaining momentum.

In commodities, WTI drifted 2.3% higher to trade near $112. Most base metals trade in the green; LME zinc rises 2.8%, outperforming peers. LME aluminum lags, dropping 0.3%. Spot gold is little changed at $1,838/oz.

Bitcoin is bid and above the USD 21k mark, after last week’s slip to a sub-USD 18k low. Elon Musk says he intends to personally support Dogecoin, via BBG TV. Coinbase (COIN) says connectivity issues across Coinbase and Coinbase Pro could cause failed trades and delayed transactions; issue was subsequently resolved.

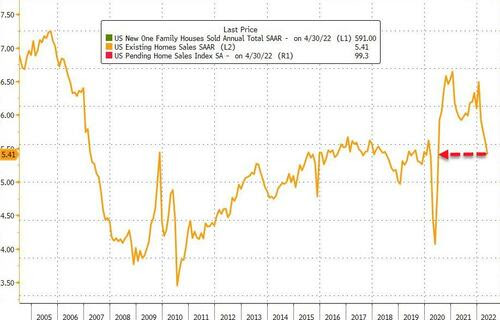

To the day ahead now, and data releases include US existing home sale for May, as well as the Chicago Fed’s national activity index for the same month. Otherwise, central bank speakers include the Fed’s Barkin and Mester, the ECB’s Rehn and the BoE’s Pill.

Market Snapshot

- S&P 500 futures up 1.9% to 3,744.50

- STOXX Europe 600 up 1.0% to 411.06

- MXAP up 1.5% to 158.77

- MXAPJ up 1.5% to 528.18

- Nikkei up 1.8% to 26,246.31

- Topix up 2.0% to 1,856.20

- Hang Seng Index up 1.9% to 21,559.59

- Shanghai Composite down 0.3% to 3,306.72

- Sensex up 2.2% to 52,741.19

- Australia S&P/ASX 200 up 1.4% to 6,523.81

- Kospi up 0.7% to 2,408.93

- German 10Y yield little changed at 1.76%

- Euro up 0.5% to $1.0567

- Brent Futures up 1.2% to $115.53/bbl

- Brent Futures up 1.2% to $115.52/bbl

- Gold spot down 0.2% to $1,835.31

- U.S. Dollar Index down 0.61% to 104.06

Top Overnight News from Bloomberg

- UK rail workers began Britain’s biggest rail strike in three decades after unions rejected a last-minute offer from train companies, bringing services nationwide to a near standstill. Britain’s local authorities say they can’t afford to pay a mandated increase in the legal minimum wage over the next year without a £400 million cash injection from the national government

- A majority of European businesses are worried about their ability to meet employee demands for higher wages amid the current spike in inflation, according to a regional survey by Intrum AB

- Companies in Germany, the UK, France, Spain and Italy are the most distressed since August 2020, according to the Weil European Distress Index. The study aggregates data from more than 3,750 listed European firms

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks gained across amid a broad constructive global risk tone despite a lack of fresh macro drivers and the recent holiday closure in the US, with Bitcoin and Chinese commodity prices also stabilising after the recent tumultuous price action. ASX 200 was led higher by the energy sector and after RBA’s Lowe effectively ruled out a 75bps hike next month. Nikkei 225 outperformed and reclaimed the 26,000 level amid a predominantly weaker currency. Hang Seng and Shanghai Comp. were positive with sentiment in Hong Kong underpinned by news the SAR is to propose a quarantine-free business travel corridor with mainland China, while mainland bourses lagged with the US ban on imports from Xinjiang taking effect from today. Japan’s PM Kishida says rapid JPY weakening is a source of concern, must closely watch FX moves and consider monetary policy and FX measures separately.

Top Asian News

- Chinese Developer Accepts Wheat, Garlic as Payment to Woo Buyers

- China Junk Bond Selloff in New Phase With Record Fosun Rout

- Gold Steady as Traders Weigh Central Bank Plans to Hike Rates

- Australian Tesla-Supplier Eyes First Lithium Exports

- Over- Optimism Among China Steel-Makers Behind Iron Ore’s Plunge

European bourses are firmer and building on Monday’s upside, Euro Stoxx 50 +1.1%; thus far, newsflow has largely focused on familiar themes. Additionally, participants are awaiting the return of the US after Monday’s market holiday. Currently, ES +1.7% with the region incrementally outperforming European peers. Elon Musk says there a still a few unresolved matters with Twitter (TWTR) including the number of spam users, via BBG TV; still awaiting a resolution, very significant. Adds, they are reducing the salaried workforce of Tesla (TSLA) by circa. 10% over the next three-months.

Top European News

- French President Macron will invite all parties able to form a group in the new parliament for talks on Tuesday and Wednesday, according to Reuters.

- BDI revises down 2022 German GDP forecasts: 1.5% (prev. 3.5%); return to pre-COVID level expected at end-2022 at the earliest

Central Banks

- ECB’s Lane said very high inflation means there is a risk inflation psychology could take hold and said the larger increment for rate increase in September does not represent a red alert assessment of inflation. Lane also commented that he doesn’t see a situation where they would need to revisit the plan for a July decision and there is no preview beyond September of what will be the appropriate pace of tightening, according to Reuters.

- ECB’s Villeroy said the new instrument should be available as much as necessary to make the no-limit commitment to protect the Euro very clear and the more credible such an instrument is, the less it may have to be used in practice. Villeroy added the new instrument will have rules but there will be elements of judgement also and said they would not necessarily need to hold purchases of government or private sector securities to maturity, according to Reuters.

- ECB’s Rehn says EZ inflation pressured are broader and stronger; very likely the September move is more than 25bp in magnitude.

- BoE’s Pill says if there is evidence of persistent price pressures, the MPC is certainly prepared to act, expects further tightening in the coming months, need to consider the exchange rate when assessing inflationary pressures. Worries that using monetary policy to stabilise the FX rate in the short-term would be a distraction from the BoE’s goals.

- HKMA purchases HKD 9.6bln from the market, as the HKD hits the weak-end of the trading range.

FX

- Euro firm as risk revival continues and ECB’s Rehn says 50bp hike in September is highly probable, EUR/USD eyeing 1.0600 after breaching 1.0550, but could be capped by 1bln option expiry interest between 1.0575-85.

- Sterling rebounds ahead of CBI industrial trends and after BoE chief economist Pill underlines willingness to act if price pressures prove persistent; Pound probes 1.2300 vs Dollar as DXY slips further from recent peaks through 104.000.

- Loonie and Nokkie boosted by firmer crude prices, as former awaits Canadian retail sales data; USD/CAD close to 1.2900 vs circa 1.3078 double top, EUR/NOK sub-10.4000 within 104.4200+/10.3400 range.

- Kiwi and Aussie underpinned by improvement in risk appetite, but hampered as NZ consumer sentiment slides to record low and RBA Governor Lowe pushes back on the amount of 2022 tightening priced in at present; NZD/USD hovers above 0.6350 and AUD/USD shy of 0.7000.

- Franc and Yen remain divergent with SNB and BoJ policy paths, latter largely ignoring latest verbal intervention; USD/CHF pivots 0.9650 and USD/JPY back above 135.00.

- Israel PM Bennett and Foreign Minister Lapid agreed on dissolving the Knesset and going for an early election, while the vote will take place next week and Lapid will become PM once the vote passes, according to Walla News.

Fixed Income

- Debt divergent and erratic awaiting the return of US cash markets from long holiday weekend.

- Bunds hold within 143.05-144.01 range and Gilts between 111.11-68 parameters.

- Treasury futures retreat and curve flits from marginal flattening to steepening ahead of US existing home sales and more Fed speak via Mester and Barkin

Commodities

- WTI and Brent are bid amid broader risk sentiment with newsflow focusing on familiar themes primarily around the reduction in Russia’s gas supply to Europe.

- Thus far, Brent has tested but failed to connivingly breach the USD 116.00/bbl mark ahead of touted USD 116.37/bbl resistance.

- US Treasury Secretary Yellen said she does not see resuming the Keystone XL oil pipeline as a short-term measure that can address high oil prices, while she added it would take years to have an impact. Yellen also commented that evidence is mixed on the level of pass-through from a gasoline tax holiday to lower prices and said that an exception or ban on insurance for certain Russian oil shipments would effectively provide a price cap on oil, according to Reuters.

- Brazilian Economy Minister Guedes said Brazil is part of the western energy security, particularly for Europe, while he added that privatising and moving Petrobras to Novo Mercado would increase its market cap from BRL 450bln to BRL 750bln. Guedes added that they will conduct new measures again if the war in Ukraine is escalating, according to Reuters.

- PetroEcuador may have to stop exports if protests continue and it declared a force majeure to avoid contract penalties, according to Reuters.

- Vitol CEO says markets are faced with underinvestment and falling production capacity for crude and there is a relatively tight refining situation, via Reuters; if China exports some more products, the tightness felt today won’t be felt.

- Denmark’s energy agency declared an ‘early warning’ stage of gas supply preparedness, according to Reuters.

- German regulator says they are not in a hurry to declare the highest gas emergency level yet, via Reuters citing BR; however, Sweden declares an “early warning” stage of gas supply preparedness for Western and Southern parts of the nation.

- Codelco’s union presidents ratified the start of a national strike beginning on Wednesday, according to Reuters; an update which, alongside broader risk, is supporting LME Copper.

US Event Calendar

- 08:30: May Chicago Fed Nat Activity Index, est. 0.47, prior 0.47

- 10:00: May Existing Home Sales MoM, est. -3.7%, prior -2.4%

- 10:00: May Home Resales with Condos, est. 5.4m, prior 5.61m

Central Banks

- 11:00: Fed’s Barkin Interviewed During NABE Event

- 12:00: Fed’s Mester Speaks at Women in Leadership Event

- 15:30: Fed’s Barkin Speaks in Richmond

DB’s Jim Reid concludes the overnight wrap

I’ll be publishing my latest monthly chartbook later today so keep an eye out for it. It will include the slides for last week’s webinar on the default study “The end of the ultra-low default world”. See here for the webinar replay and here for the original default study.

Welcome to the longest day of the year although most in markets will already say we’ve had numerous of those already so far this year. Actually if you’re outside of London, trying to get in it could be a very, very long day as the UK is today gripped by the first of three alternate day rail strikes. There is a tube strike today thrown in for good measure. It does seem industrial relations with the government are on a knife edge across the UK as at least 3 million workers across different professions are considering industrial action at the moment over pay and working conditions. So this could become a much bigger story if tensions are not eased. With inflation this high it’s not easy to see how they can be without big pay rises being offered.

However on this day of wall to wall sun (sorry to the Southern Hemisphere readers), there has been a little more light than dark in markets over the last 24 hours after what was the worst week for global equities since March 2020. The next major event(s) to look forward to are Fed Chair Powell’s congressional testimonies from tomorrow. To be honest though, its been a fairly quiet start to the week given the US holiday yesterday, with the biggest news instead being a fresh rise in European sovereign bond yields after President Lagarde reiterated the ECB’s intentions to start hiking next month, and also shone a bit more light on their plans to deal with any potential fragmentation.

We’ll start with those remarks from Lagarde, who appeared in a hearing at the European Parliament yesterday and spoke strongly against any potential fragmentation in the Euro Area. Indeed, she said that “we need to be absolutely certain” that monetary policy was being transmitted to the different Euro Area countries and went as far to say that it was “right at the core of the mandate”, whilst adding “anybody who doubts that determination will be making a big mistake”. So not quite “whatever it takes” but along the same lines.

Given the ECB has promised to deal with any fragmentation, that should make life easier for them when it comes to raising rates, and European sovereign bond yields responded accordingly yesterday. Looking at the specific moves, yields on 10yr bunds (+9.0bps), OATs (+11.8bps) and BTPs (+12.3bps) all moved noticeably higher, although by the standards of last week that seemed quite modest given that 10yr bund yields had seen absolute moves of 11bps in either direction on 3 out of 5 days last week.

When it came to bonds though, it was UK gilts who were one of the biggest underperformers yesterday after we heard from one of the more hawkish members of the Bank of England’s MPC. Catherine Mann (who was in the minority that favoured of a 50bps move last week) said in a speech that “the incoming data on inflation show increasingly domestic embeddedness, persistence, and momentum”. Furthermore, she also warned about the risk of embedded domestic inflation being “further boosted by inflation imported via a Sterling depreciation”. Against that backdrop, 10yr gilt yields rose by +10.6bps to close above 2.6% for the first time since 2014, whilst overnight index swaps are continuing to price in a more aggressive response from the BoE after the next meeting, with 50bp moves priced in for each of the next 3 meetings, which would be the fastest pace of hikes since they gained operational independence in 1997.

In spite of the sovereign bond selloff, equities put in a much better performance yesterday, with the STOXX 600 (+0.91%) seeing a broad-based advance that was supported by all the main sector groups. Other indices on the continent also moved higher, including the FTSE 100 (+1.50%), the DAX (+1.06%) and the FTSE MIB (+0.99%). The worst performer on a relative basis was France’s CAC 40 (+0.64%), which struggled following the news that President Macron had lost his parliamentary majority, which will make passing his agenda much more difficult in the coming years. See our economists’ piece on the topic here.