by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1838.30 DOWN $11.25

SILVER: $21.62 DOWN $0.15

ACCESS MARKET: GOLD $1840.30

SILVER: $21.68

Bitcoin morning price: $21,143 DOWN 526

Bitcoin: afternoon price: $20,436 DOWN 181

Platinum price: closing DWN $10.85 to $933.25

Palladium price; closing DOWN $26.60 at $1825.45

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE:EXCHANGE:

COMEX

no. of contracts issued by JPMorgan: 26/52

DLV615-T CME CLEARING

BUSINESS DATE: 06/16/2022 DAILY DELIVERY NOTICES RUN DATE: 06/16/2022

PRODUCT GROUP: METALS RUN TIME: 20:34:48

EXCHANGE: COMEX

CONTRACT: JUNE 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,845.700000000 USD

INTENT DATE: 06/16/2022 DELIVERY DATE: 06/21/2022

FIRM ORG FIRM NAME ISSUED STOPPED

363 H WELLS FARGO SEC 20

657 C MORGAN STANLEY 3

661 C JP MORGAN 44 26

800 C MAREX SPEC 5

905 C ADM 4

972 C IRONBEAM INC 2

TOTAL: 52 52

MONTH TO DATE: 23,741

_____________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 52 NOTICE(S) FOR 5200 Oz//0.1617 TONNES)

total notices so far: 23,741 contracts for 2,374,100 oz (73.947 tonnes)

SILVER NOTICES:

25 NOTICE(S) FILED 125,000 OZ/

total number of notices filed so far this month 1787 : for 8,935,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $11.25

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.6 TONNES INTO THE GLD.

INVENTORY RESTS AT 1075.54 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 15 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV://BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 739,000 OZ FROM THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 543.660 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 1087 CONTRACTS TO 144,039 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED DESPITE OUR $0.46 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.46) BUT WERE SUCCESSFUL IN KNOCKING OFF SOME SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 27 CONTRACTS OR 135,000 OZ//NEW STANDING: 9,035,000 / // V) STRONG SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS :-799

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 12 days, total 10,552, contracts: 52.760 million oz OR 4.396 MILLION OZ PER DAY. (879 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 53.76 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 53.76 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1087 DESPITE OUR STRONG $0.46 GAIN IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 375 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 135,000 QUEUE JUMP //NEW STANDING: 9,035,000 OZ // .. WE HAD A STRONG SIZED LOSS OF 712 OI CONTRACTS ON THE TWO EXCHANGES FOR 3/560 MILLION OZ WITH THE GAIN IN PRICE.

WE HAD 25 NOTICES FILED TODAY FOR 125,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 3510 CONTRACTS TO 495.625 AND FURTHER NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -367 CONTRACTS.

.

THE FAIR GAIN IN COMEX OI CAME DESPITE OUR RISE IN PRICE OF $28.95//COMEX GOLD TRADING/THURSDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERING

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S 2900 OZ E.F.P. JUMP TO LONDON //NEW STANDING: 74.606 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $28.95 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 6345 OI CONTRACTS 19.73 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2465 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 492,113

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6345, WITH 3143 CONTRACTS INCREASED AT THE COMEX AND 3510 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 6712 CONTRACTS OR 20/87 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3202) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (3143,): TOTAL GAIN IN THE TWO EXCHANGES 6345 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING AND SOME ADDITION TO SPECULATOR SHORTS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S QUEUE. JUMP OF 3800 OZ//NEW STANDING: 74.696 TONNES / 3) ZERO LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING//SOME SPECULATOR SHORT ADDITIONS //.,4) STRONG SIZED COMEX OI LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

53,202 CONTRACTS OR 5,320,200 OZ OR 165.48 TONNES 13 TRADING DAY(S) AND THUS AVERAGING: 4092 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAY(S) IN TONNES: 165.48 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 165.42/3550 x 100% TONNES 4.66% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 155.52 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A HUGE SIZED 1886 CONTRACT OI TO 144,039 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 375 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 375 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1880 CONTRACTS AND ADD TO THE 375 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A LARGE SIZED LOSS OF 1511 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 7.55 MILLION OZ

OCCURRED WITH OUR GAIN IN PRICE OF $0.46 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED DOWN 20.02 PTS OR 0.61% //Hang Sang CLOSED DOWN 462.78 PTS OR 2.13% /The Nikkei closed UP 105.04 OR 0.40% //Australia’s all ordinaires CLOSED DOWN 0.03% /Chinese yuan (ONSHORE) closed DOWN 6.7149 /Oil DOWN TO 113.77 dollars per barrel for WTI and DOWN TO 116.23 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7149 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7204: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 3143 CONTRACTS TO 495,286 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED DESPITE OUR GAIN OF $28.95 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (3202 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3202 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :3202 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3202 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 6345 CONTRACTS IN THAT 3202 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 3143 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF GOLD $28.95.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JUNE (74.606),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.609 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $28.95) AND WERE UNSUCCESSFUL IN KNOCKING OFF SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A STRONG SIZED GAIN OF 6712 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (74.609 TONNES)…

WE HAD 367 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 6345 CONTRACTS OR 634,500 OZ OR 19.73 TONNES

Estimated gold volume 135,216/// poor/

final gold volumes/yesterday 188,634 /fair

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 17

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 343,579.605 oZ Brinks JPM int.Delaware 2015 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 52 notice(s) 55200 OZ 0.1667 TONNES |

| No of oz to be served (notices) | 283 contracts 28,300 oz 0.8802 TONNES |

| Total monthly oz gold served (contracts) so far this month | 23,741 notices 2,374,100 OZ 73.947 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

0 customer deposits

total deposits: nil oz

3 customer withdrawals:

i) Out of Brinks 181,056.300 oz

ii) Out of Int. Delaware 1768.385 oz (55 kilobars)

ii) Out of JPM: 160,755.000 oz (5000 kilobars)

total withdrawal: 343,579.605 oz

ADJUSTMENTS: 1/dealer to customer/Loomis:

4822.650 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 335 contracts having LOST 840 contracts

We had 878 notices filed on WEDNESDAY so we GAINED 38 contracts or an additional 3800 oz will stand for gold in this very active month of June

July has a LOSS OF 152 OI to stand at 1721

August has a GAIN of 3798 contracts UP to 411,780 contracts

We had 52 notice(s) filed today for 5200 oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 52 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 26 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (23,741) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 336 CONTRACTS ) minus the number of notices served upon today 52 x 100 oz per contract equals 2,398,600 OZ OR 74.609 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (23,689) x 100 oz+ (336) OI for the front month minus the number of notices served upon today (878} x 100 oz} which equals 2,401,500 oz standing OR 74.720 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 74,720 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,419,784.828 oz 75.26 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 33,811,562.083 OZ

TOTAL ELIGIBLE GOLD: 16,303,434.968 OZ

TOTAL OF ALL REGISTERED GOLD: 17,508,127.075 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,093154.0 OZ (REG GOLD- PLEDGED GOLD)

END

JUNE 2022 CONTRACT MONTH//SILVER//JUNE 17

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 464,323.742 oz Brinks CNT |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 25CONTRACT(S) 125,000 OZ) |

| No of oz to be served (notices) | 20 contracts (100,000 oz) |

| Total monthly oz silver served (contracts) | 1787 contracts 8,935,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 1 dealer deposit

Into Manfra: 228,361.000 oz

total dealer deposits: 228,361.000 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 0 deposit into the customer account

total deposit: 0 oz

JPMorgan has a total silver weight: 169,419 million oz/336.735 million =50.31% of comex

Comex withdrawals: 2

i)Brinks 374,724.110

ii)CNT 139,599.632 oz

total withdrawal 464,323.742 oz

adjustments: 1 jpm

dealer to customer: 191,084

the silver comex is in stress!

TOTAL REGISTERED SILVER: 71.898 MILLION OZ

TOTAL REG + ELIG. 336.780 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 45 HAVING LOST 44 CONTRACTS.

WE HAD 71 NOTICES FILED ON WEDNESDAY SO WE GAINED 27 CONTRACTS OR AN ADDITIONAL 135,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 5493 CONTRACTS DOWN TO 51,275 CONTRACTS.

AUGUST LOST 11 CONTRACTS TO STAND AT 990

SEPTEMBER HAD A GAIN OF 3644 CONTRACTS UP TO 74,655 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 25 for 125,000 oz

Comex volumes:54,075// est. volume today// fair

Comex volume: confirmed yesterday: 67,682 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1787 x 5,000 oz = 8,935,000 oz

to which we add the difference between the open interest for the front month of JUNE(45) and the number of notices served upon today 25 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1787 (notices served so far) x 5000 oz + OI for front month of JUNE (45) – number of notices served upon today (25) x 5000 oz of silver standing for the JUNE contract month equates 9,035,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 17/WITH GOLD DOWN $11.25: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPIST OF 11.60 TONNES INTO THE GLD.///INVENTORY RESTS AT 1075.54 TONNES

JUNE 16/WITH GOLD UP $28.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.74 TONNES

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

JUNE 14/WITH GOLD DOWN $18.80/NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

GLD INVENTORY: 1075.54 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 17/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 739,000 OZ FROM THE SLV./:INVENTORY RESTS AT 543.660 MILLION OZ/?

JUNE 16/WITH SILVER UP 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 14/WITH SILVER DOWN 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg

Hold On To Your Seat!

FRIDAY, JUN 17, 2022 – 06:30 AM

Authored by James Rickards via DailyReckoning.com,

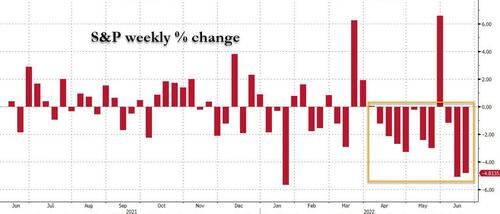

The S&P is in bear market territory, which is defined as a decline of 20% or more from recent highs.

And it may fall even further. Since World War II, there have been 14 bear markets. The median loss during these bear markets has been 30%, and they lasted about a year (hat tip to Bespoke Investment Group).

The Kind of Drop We Haven’t Seen in Decades

And with the Fed ready to raise interest rates again in July (after hiking by 75bps this week following last week’s red-hot inflation data – CPI and UMich expectations), we could be soon witnessing an even bigger drop in the market – the kind that we haven’t seen in decades.

That’s not fear-mongering or hyperbole. It’s just a sober assessment of the situation.

The Fed is deeply concerned about inflation, and it will continue to aggressively raise interest rates to try to tamp it down.

But neither the economy nor the stock market can take the kind of tightening required to really get a hold on inflation.

Since the end of World War II, the Fed has embarked on perhaps a dozen tightening cycles in which it raised interest rates.

All but one of these tightening cycles resulted in recession. That’s a nearly perfect record.

And there’s absolutely no reason to expect that this time will be any different, especially with the tremendous excesses within the financial system.

Which brings up the question, is the Federal Reserve broke?

How Can the Fed Be Broke?

When you bring up the topic of the Federal Reserve going broke, most individuals react by saying, “That’s impossible! The Fed can’t go broke. They can just print more money.”

That’s a typical reaction, but it displays a misunderstanding of what money is and how the Fed actually works. Yes, the Fed can print all the money it wants. But money is not an asset for the Fed; it’s a liability.

Take a $20 bill out of your purse or wallet and read it. On a banner across the top it says, “Federal Reserve Note.” A note is a form of debt; in other words, it’s a liability. That becomes clear when you look at the Fed’s balance sheet (it’s publicly available on the Fed’s website).

Assets consist mainly of securities: mostly U.S. Treasury bills and notes and mortgage-backed securities. Liabilities consist of cash, coins and reserves deposited by member banks at the Fed. The Fed’s net worth or capital is simply the net of the assets minus liabilities.

That equity account is a small sliver of capital relative to the total assets.

In other words, the Fed looks like a highly leveraged hedge fund. Printing money can be used to buy more securities, but all that does is leverage the balance sheet even more by piling more assets (securities) and liabilities (money and reserves) on top of the same sliver of capital.

But what if it’s worse than that? What if the assets are less than the liabilities so the Fed has a negative net worth?

Less Than Zero

A negative net worth is one definition of insolvency, which is a fancy name for broke. In the steady state, this would not happen. The Fed could just sit still; let assets mature at par value; and get paid the cash by the issuer, at which point the cash just disappears when the Fed receives it.

The Fed could gradually deleverage just by doing nothing. But what if the Fed balance sheet were marked to market like a real hedge fund? Or what if the Fed sold securities at a loss instead of just waiting for them to mature at par value?

The Fed’s accounting method does not mark to market, but any analyst can run the numbers anyway just by looking at asset maturities and using current market prices for those assets. If you do this, you find that higher interest rates have resulted in many securities in Fed’s portfolio being worth less than book value.

That’s bond math 101: higher rates = lower prices. Beyond that, the Fed does not want to wait to deleverage. It wants to reduce the balance sheet quickly. That means asset sales, especially the less liquid mortgage-backed securities.

That’s where real operating losses arise because an actual sale below par value results in a loss that must be charged against capital. So yes, the Fed is probably insolvent on a mark-to-market basis (a method it does not use).

A Fed Governor Admits the Fed Is Insolvent

If you evaluated the Fed on a mark-to-market basis the way you would with a hedge fund, its capital would be wiped out. It’s insolvent. I once had a conversation with a member of the Federal Open Market Committee who admitted this to me privately. I reached a conclusion on my own, but she confirmed it.

The conversation went like this: I said, “I think the Fed is insolvent.”

This governor first resisted and said, “No, we’re not.” But I pressed her a little bit harder and she said, “Well, maybe.”

And then I just looked at her and she said, “Well, we are, but it doesn’t matter.”

In other words, a governor of the Federal Reserve admitted to me, privately, that the Federal Reserve is insolvent but said it doesn’t matter because central banks don’t need capital.

Well, central banks do need capital.

She may be right in the short term that it doesn’t really matter. Most people don’t even know what the Federal Reserve is let alone the inside accounting issues I described here. But in the next panic, it just might matter.

Maybe Gold Is the Foundation of the Monetary System After All

The problem is each financial crisis is larger than the one that preceded it because the system itself is larger due to massive central bank interventions. It’s a matter of scale.

How can the Fed bail out big banks when the Fed itself is insolvent? The issue might not be a legal one so much as a matter of confidence.

Just in case, the Fed does have a hidden asset to offset all of those not-so-hidden losses. The Fed has a gold certificate on its books based on a quantity of gold valued at $42.22 per ounce.

If that gold were revalued to the current market price of $1,850 per ounce, another $500 billion would appear out of thin air. That could be added to Fed capital.

The Fed doesn’t like to talk about gold, but maybe the entire monetary system is based on gold after all.

One day we might just find out the hard way.

END

3. Chris Powell of GATA provides to us very important physical commentaries

end

CHRIS POWELL, Secretary/Treasurer

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //LITHIUM

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

Heavy losses from big crypto hedge fund 3AC

(zerohedge)

Three Arrows Founder Breaks Silence As Another Crypto Lender Starts Melting Down

FRIDAY, JUN 17, 2022 – 10:45 AM

Crypto hedge fund Three Arrows Capital (3AC) is exploring asset sales and other options after suffering heavy losses amid a broad selloff in cryptocurrencies and other digital assets, the firm’s founders said on Friday.

“We have always been believers in crypto and we still are,” co-founder Kyle Davies told the Wall Street Journal – the first communication from the company since Zhu Su, the firm’s other co-founder, fired off a cryptic tweet on Tuesday that simply said the company is “in the process of communicating with relevant parties and fully committed to working this out.”

The hedge fund had roughly $3 billion in assets under management in April, before ‘stablecoin’ TerraUSD, and its sister token, Luna, suddenly collapsed.

Three Arrows was among a group of large investors that took part in a $1 billion token sale earlier this year by Luna Foundation Guard, a nonprofit organization started by South Korean developer Do Kwon, the creator of TerraUSD. The funds went toward a bitcoin-denominated reserve for the stablecoin, and were meant to help maintain TerraUSD’s value at $1 per coin.

Mr. Davies said Three Arrows invested about $200 million in Luna as part of that deal, a sum that was effectively wiped out when TerraUSD and Luna both became worthless in a matter of days. -WSJ

According to Davies, the firm is hoping to reach an agreement with creditors that would allow it more time to work out a plan.

Before losing $60 billion in market cap, TerraUSD and Luna were among the top-10 largest digital coins – and were largely considered low-risk.

“The Terra-Luna situation caught us very much off guard,” said Davies, adding that the selloff was ‘unprecedented,’ and the fact that the Luna foundation began dumping bitcoin to help support TerraUSD also contributed to the selloff in bitcoin itself in May.

While Three Arrows was able to weather the Luna losses, a subsequent cascade of events led to a selling contagion that has destroyed the value of a number of coins and projects in the crypto space. For context, in November, Crypto’s total market cap was nearly $3 trillion. Now it stands at $910 million, according to CoinMarketCap.

As a result, some lenders have been demanding full, or at least partial repayment on loans they extended to crypto investors. Compounding the problem are rising interest rates, which has caused riskier assets to sell off.

“We were not the first to get hit…This has been all part of the same contagion that has affected many other firms,” said Davies, who added that 3AC is still trying to quantify its losses and place a value on their illiquid assets – such as VC investments in various crypto projects.

“We are the biggest investors in the fund, and our intent was always for everyone to do well in it,” said Zhu, who predicted last year that bitcoin would enter a ‘growth supercycle’ where prices continually rose and achieved mainstream adoption.

“Supercycle price thesis was regrettably wrong, but crypto will still thrive and change the world every day,” he tweeted in late May as the selloff in crypto rattled investors.

3AC raised eyebrows on Tuesday when it liquidated at least $40 million of “staked” Ether (stETH), making it the largest seller of the token in the past week, according to The Defiant.

Cracks began to form after stETH – which has historically traded with ETH – began to “de-peg” last week, causing the Celsius Network – a “centralized, one-stop-shop for crypto investors and traders” – to freeze customer assets so that it could “honor, over time, its withdrawal obligations.”

Who’s next?

With Bitcoin now hovering at just over $20,000, down from a peak of $64,000 a little more than six months ago, the crypto industry continues to reverberate from the selloff.

The latest firm on the chopping block appears to be Hong Kong-based asset manager Babel Finance, which on Friday officially announced that they were suspending redemptions and withdrawals, citing “unusual liquidity pressures,” according to Cointelegraph.

“Recently, the crypto market has seen major fluctuations, and some institutions in the industry have experienced conductive risk events,” reads the statement, which adds taht the firm is in close communication with “all related parties” and will do its best to protect customers.

The move echoes that of Celsius, a crypto staking and lending platform, which halted withdrawals on June 13.

Stay tuned…

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7149

OFFSHORE YUAN: 6.7204

HANG SANG CLOSED DOWN 462.78 PTS OR 2.13%

2. Nikkei closed UP 105.04% OR 0.40%

3. Europe stocks ALL CLOSED ALL RED

USA dollar INDEX DOWN TO 104.91/Euro FALLS TO 1.0399

3b Japan 10 YR bond yield: RISES TO. +.250/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 132.79/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN -// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.907%/Italian 10 Yr bond yield RISES to 4.03% /SPAIN 10 YR BOND YIELD RISES TO 3.03%…ALL BLOWING UP!!

3i Greek 10 year bond yield RISES TO 4.33//

3j Gold at $1822.40 silver at: 21.40 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 4/10 roubles/dollar; ROUBLE AT 56.66

3m oil into the 113 dollar handle for WTI and 116 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 134.49DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.98069– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0198well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.468 UP 7 BASIS PTS

USA 30 YR BOND YIELD: 3.474 UP 7 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.32

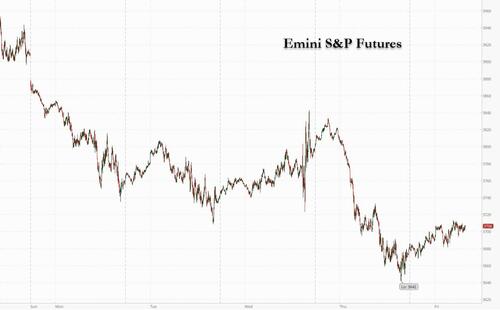

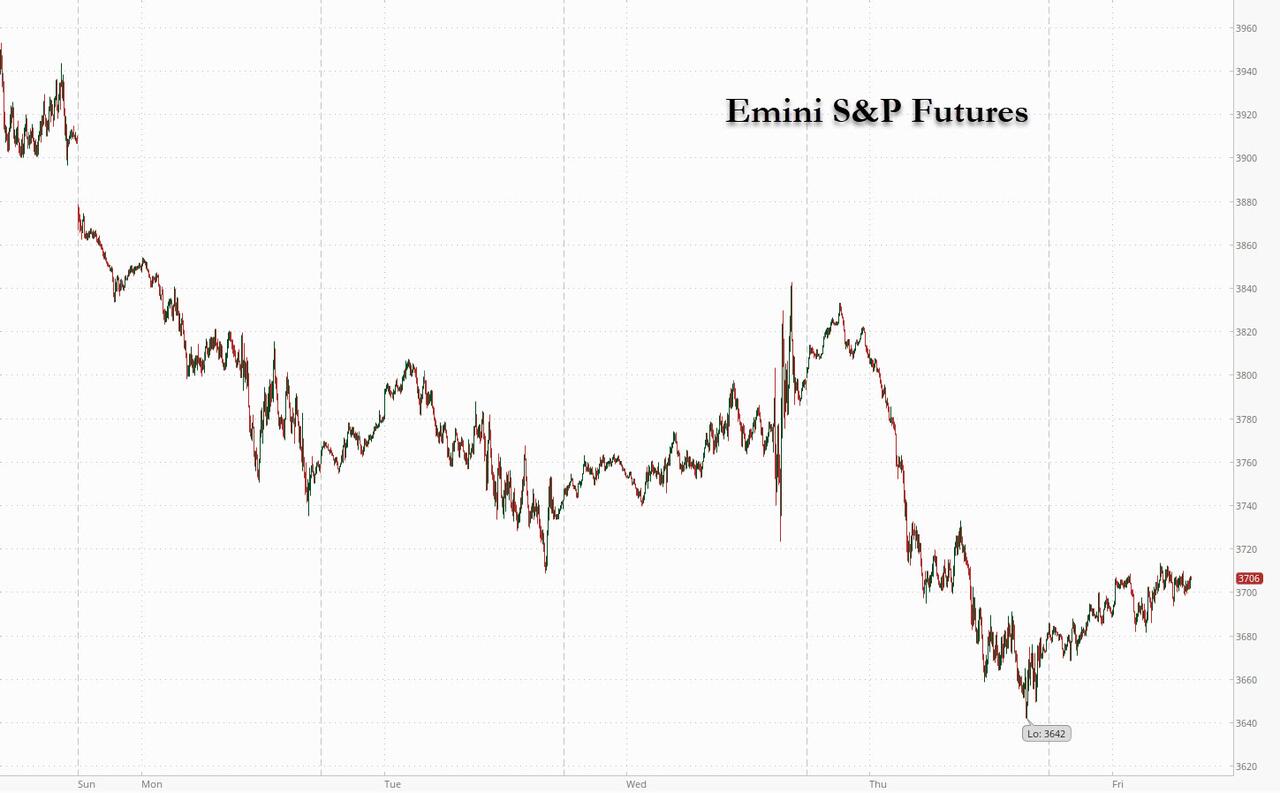

Futures Rebound, Yen Crashes To End Turbulent Week On $3.4 Trillion Quad-Witch Day

FRIDAY, JUN 17, 2022 – 08:12 AM

Ending a rollercoaster – but mostly lower – week for risk assets around the globe which saw the Fed hike the most since 1994, a shock Swiss National Bank hike and the latest boost in UK borrowing costs, as well as a bevy of central banks surprising hawkishly, stocks in Europe finally rebounded after hitting an 18 month low earlier this week, while US equity futures were bid Friday after a rout triggered by fears of recession pushed the S&P into a bear market on Monday. S&P futures rose 1% and Nasdaq futures rebounded 1.2% signaling steadier sentiment compared with Thursday’s plunge in US shares to the lowest since late 2020, after the BOJ refused to change its Yield Curve Control conditions, sending the Yen plunging, and helping the dollar snap two days of losses as Treasury yields were flat with the 10Y around 3.21%. The Stoxx Europe 600 index jumped about 1.2% after hitting its lowest level in more than a year.

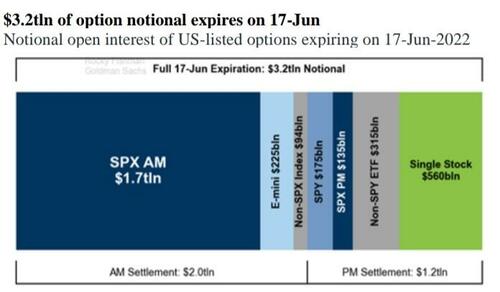

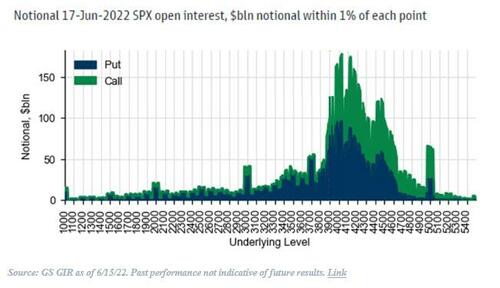

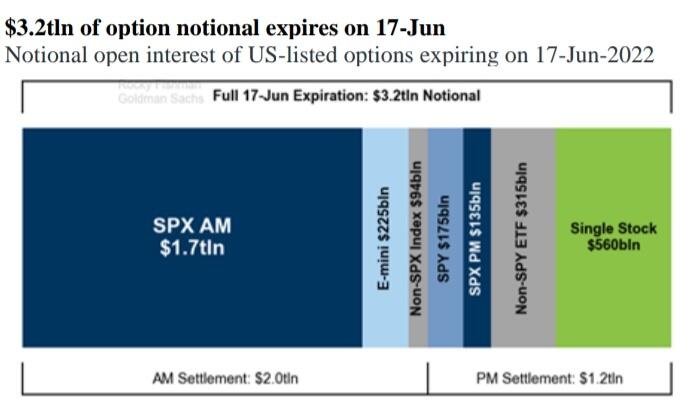

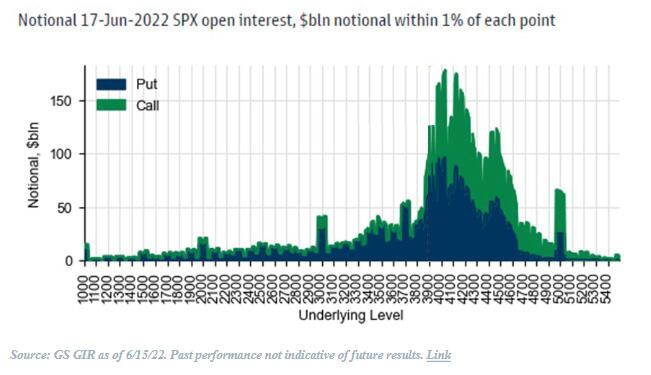

Friday also brings an absolutely massive triple-witching, and although Bloomberg believes that the roughly $3.2 trillion in options expiry may lead to short covering, which could bring temporary relief for the stock market…

… we disagree, as the bulk of open interest is around 4,100 or several hundred points above spot, meaning moves today will have little impact on “derivative tails wagging the dog.”

In any case, absent a massive 5% rally today which sends stocks into the green, the S&P is looking at being down 10 of the past 11 weeks, a feat that has been repeated just once in history: 1970. Let’s go Brandon!

In premarket trading, Revlon surged after a report that Reliance Industries Ltd. is considering buying the company. Major technology and internet stocks were higher, rebounding from Thursday’s rout. Apple Inc., Microsoft Corp. and Meta Platforms Inc. were among those advancing. US-listed Chinese stocks also soared in the premarket, a day after the Nasdaq Golden Dragon China Index’s 4.4% slide, with e-commerce giant JD.com (JD US) leading the pack ahead of the closely watched 618 online shopping event. Additionally, Chinese tech giants such as Alibaba surges on a Reuters report that China’s central bank has accepted Ant Group’s application to set up a financial holding company. Alibaba shares surge 11% following the report. Among other large- cap Chinese internet stocks, JD.com +9.3%, Pinduoduo +7.5%, Baidu +5.6%. Here are some of the biggest U.S. movers today:

- Adobe (ADBE US) shares fall 4% in premarket trading on Friday after the software company cut its revenue forecast for the full year as it expects currency fluctuations, seasonal shifts in demand and the decision to end sales in Russia and Belarus to weigh on its business.

- Roku (ROKU US) shares climb 3.9% in premarket trading after the company and Walmart said they entered a pact to enable streamers to purchase featured products fulfilled by Walmart directly on Roku.

- US Steel (X US) shares rise 5.2% in US premarket trading after the metal giant’s 2Q22 guidance came in well above consensus estimates, according to Morgan Stanley analysts led by Carlos De Alba.

- Rhythm (RYTM US) shares are 13% lower in US premarket trading after the company’s Imcivree injection failed to win approval for one of the two supplemental indications it sought and the company announced a financing agreement with HealthCare Royalty Partners.

- Revlon (REV US) shares surge 65% in premarket trading after Reliance Industries is considering buying Revlon in the US, ET Now reports, citing people familiar with the matter.

Markets are rounding off a turbulent week buffeted by interest-rate increases which are rapidly draining liquidity, sparking losses in a range of assets. Global stocks face one of their worst weeks since pandemic-induced turmoil of 2020. The question is how far assets have to sink before the tightening cycle is fully priced in. Bucking the global hawkish trend, Japan, retianed super-easy monetary policy and yield curve control, defying pressure to track the global trend toward tighter settings. As a result, the Japanese yen is on course for its biggest fall against the dollar since March 2020 while Japan’s 10-year bond yield retreated below the Bank of Japan’s cap of 0.25%, after earlier hitting 0.265%, the highest since 2016. The Swiss franc surged to its highest level against the yen since 1980.

“Investors have to ask themselves how long the rate-hiking cycle will go and how deep the economic slowdown will be,” said Michael Strobaek, global chief investment officer at Credit Suisse Group AG, which is overweight equities and recently closed its underweight position in bonds. “Peak hawkishness, i.e. the peak in expectations repricing, might be close. Once we are there, it is not only possible but likely that we will see a rebound in both equities and bonds. However, this rebound will be very difficult to time.”

Despite the ongoing slow-motion crash, US stocks attracted another $14.8 billion in the week to June 15, their sixth consecutive week of additions, according to EPFR Global data. In total, $16.6 billion flowed into equities globally in the period, while bonds had the largest redemptions since April 2020 and just over $50 billion exited cash, the data showed.

European equities climbed after a choppy start. Euro Stoxx 600 rallied 1.4%. FTSE MIB outperforms peers, adding 1.7%. European real estate companies are among the best performers, rebounding after several days of losses following concerns higher interest rates will weigh on the sector’s financing abilities. Sweden’s Samhallsbyggnadsbolaget i Norden (SBB) rises as much as 10%, Aroundtown +6.5%, Wallenstam +5.9%, Vonovia +4.9%. Here are some of the biggest European movers:

- Nokian Renkaat shares gain as much as 11% after the Finnish tire manufacturer raised its net sales guidance for 2022 while also keeping its profit guidance intact.

- Italy’s FTSE MIB index rises as much as 2%, leading gains among major European stock markets; Italy-Germany 10-year bond yield spread falls to one- month low. Best performers on the index include Campari +5.4%, Pirelli +5.3%, DiaSorin +5.1%, Recordati +4%

- Ferrari gains as much as 2.4% in the wake of upgrades from Intesa Sanpaolo and Banca Akros after the luxury carmaker unveiled its electrification strategy on Thursday.

- Glencore climbs as much as 3.9% in London after the commodities group said its first-half trading profit will be bigger than it typically reports for an entire year.

- Playtech rises as much as 6.4% after the gambling operator announced the deadline for TTB to make a firm offer has been extended to next month.

- Lisi advances as much as 9.6% after Kepler Cheuvreux upgraded the Boeing supplier to buy, saying its post-Covid recovery isn’t yet priced in.

- Volvo Cars falls as much as 5.4% to the lowest since April after DNB cut its recommendation on the shares to sell due to falling demand, also noting risks related to the Polestar SPAC listing.

- Rexel drops as much as 3.9% as Kepler Cheuvreux analyst William Mackie cuts his recommendation to hold from buy, citing the “rapidly rising probability of a recession.”

Italian bonds led a rally in European debt after European Central Bank President Christine Lagarde pledged that borrowing costs of more indebted nations in the euro-area won’t be allowed to spiral out of control. Italy’s 10-year yield fell 20 basis points and German equivalents dropped six basis points.

Asian stocks tumbled to a two-year low as traders fear the global rush to hike interest rates may result in a steep economic downturn. The MSCI Asia Pacific Index slumped as much as 1.5% Friday. The measure has fallen every session this week, and is on track to post its largest weekly drop since since the early days of the pandemic in March 2020. Asia stocks have fallen along with global peers as concerns over the potential for more jumbo rate hikes by the Federal Reserve, which raised its benchmark by 75 basis points on Wednesday, triggered a broad market rout. As the global campaign to rein in decades-high inflation continues, investors worry policy tightening may become overdone and throw major economies into recessions. Japanese shares led Friday’s slump in Asia, with the decision by the Bank of Japan to keep its ultra-loose monetary settings unchanged providing limited fillip as volatility in the yen grows. Stocks in China and Hong Kong bucked the regional selloff, as Beijing’s pro-growth policy lends support to views that Chinese equities can keep outperforming. Read: Yen Tumbles as BOJ Stands Pat, Makes Rare Reference to FX Market “In the immediate short term (next 2-3 months), we continue to expect Asian stocks to remain volatile,” Chetan Seth, Asia Pacific equity strategist at Nomura Holdings in Singapore, wrote in a note.“However, we do expect some stabilization into late 3Q as equity valuations reset and positive catalysts emerge.” The catalysts Nomura is looking for are the Fed turning less hawkish as US inflation shows signs of softening and China loosening its Covid-Zero stance. Equity benchmarks in Australia and Vietnam were the other big losers in Asia on Friday, with each dropping more than 1.5%.

Japanese stocks trimmed losses as the yen weakened after the Bank of Japan’s decision to maintain its easy-money policy. The Topix fell 1.7% to 1,835.90 as of market close, while the Nikkei declined 1.8% to 25,963.00. Both gauges had been down more than 2.6% earlier in the day. The yen was down 1.3% to around 134 per dollar. Toyota Motor Corp. contributed the most to the Topix Index decline, decreasing 3.6%. Out of 2,170 shares in the index, 423 rose and 1,689 fell, while 58 were unchanged. The Topix fell 5.5% this week, its worst since April 2020. BOJ Holds Firm to Deepen Outlier Status, Keep Pressure on Yen “If the yen further weakens, this will help the Nikkei 225 to remain firm to some extent,” said Makoto Furukawa, chief portfolio strategist at Mitsubishi UFJ Morgan Stanley. “The Japanese stock market is not so different from the global trend, and monetary policy that comes out from the US and Europe is much more important for Japanese equities.”

Key stock gauges in India completed their worst weekly declines in more than two years as spiraling inflation and rate hikes by central banks dampened the outlook for business recovery. The S&P BSE Sensex slipped 0.3% to 51,360.42 in Mumbai, bringing its weekly decline to 5.4%, the most since May 2020. The NSE Nifty 50 Index dropped 0.4% on Friday, taking its tumble to 5.6%. Tata Consultancy Services lost 1.7% and was the biggest drag on the Sensex, which had 22 of the 30 member stocks trade lower. Fifteen of 19 sectoral indexes compiled by BSE Ltd. declined, led by a gauge of oil and gas companies. Among central bank monetary-policy measures this week, the US Federal Reserve made its biggest increase in policy rates since 1994. India’s markets “are largely taking cues from the global markets, in absence of any major domestic event,” Ajit Mishra, vice-president research at Religare Broking Ltd. wrote in a note. Foreign institutional investors have withdrawn $25.7 billion from Indian stocks this year through June 15, and the sell-off is headed for its ninth consecutive month. “We reiterate our negative view on markets and suggest continuing with the ‘sell on rise’ approach,” according to the note.

In FX, Bloomberg dollar spot index rose by around 0.4% as the greenback advanced against all of its Group-of-10 peers apart from the Swiss franc. Treasury yields rose by up to 9 bps, led by the front end. The yen was the worst G-10 performer and slumped as much as 1.8% to 134.63 per dollar after the Bank of Japan kept policy on hold, defying speculation it would follow its global peers and move toward tightening. The BOJ made a rare reference to the currency market, saying it needed to watch its impact on the economy and markets. The euro fell below $1.05 before paring, after touching an almost one-week high yesterday. European bond yields fell and investors rushed back to Italian debt for a third day after ECB President Christine Lagarde pledged that borrowing costs of more indebted nations in the euro-area won’t be allowed to spiral out of control. Sterling eased against a broadly stronger dollar, giving up some of its sharp gains made the previous day, when the Bank of England’s pledge to take a more aggressive stance against inflation boosted the UK currency. Market awaits speeches by BOE policymakers Silvana Tenreyro and Huw Pill later in the day for possible clues into the outlook for inflation and monetary policy.

In rates, Treasuries are cheaper across the curve with losses led by front-end following flurry of block trade in 2-year note futures over the European session. US yields cheaper by up to 5bp across front-end of the curve, flattening 2s10s spread by 2.5bp on the day; 10-year yields around 3.22%, cheaper by 2.5bp and underperforming bunds by 7bp Italian bonds outperform after ECB President Christine Lagarde’s pledge to support borrowing costs of indebted nations in the euro-area. Bloomberg notes five block trades in 2-year note futures for combined 25k were posted between 3:25am ET and 4:36am ET appeared skewed toward sellers, helping front-end of the cash curve underperform. IG dollar issuance slate empty so far; at least six IG issuers are said to have stood down over the past couple of days, as investors wait for market calm before re-launching deals.

The German cash curve bull steepens, trading richer by ~12bps in 5s. Gilts bull flatten, with 10y yields down 8bps around this week’s lows near 2.4%. US 2s10s narrow 3bps. Peripheral spreads tighten to Germany with 10y BTP/Bund narrowing ~14bps to a one-month low near 188bps.

In commodities, crude futures advance. WTI drifts 1% higher to trade near $118.75. Base metals are mixed; LME tin falls 0.9% while LME nickel gains 1.1%. Spot gold falls roughly $7 to trade near $1,850/oz

Bitcoin is currently modestly firmer, but the overall sessions range is in proximity to USD 20k with the current trough at USD 20.19k.

Looking at the day ahead now, and data releases include US industrial production and capacity utilisation for May, along with the final Euro Area CPI reading for May. Central bankers include Fed Chair Powell, the ECB’s Simkus and the BoE’s Tenreyro and Pill. Of note, Jerome Powell gives welcome remarks before the Inaugural Conference on the International Roles of the U.S. Dollar at 845am ET. He is not expected to discuss monetary policy.

Market Snapshot

- S&P 500 futures up 1.0% to 3,703.75

- MXAP down 1.2% to 157.22

- MXAPJ down 0.4% to 521.87

- Nikkei down 1.8% to 25,963.00

- Topix down 1.7% to 1,835.90

- Hang Seng Index up 1.1% to 21,075.00

- Shanghai Composite up 1.0% to 3,316.79

- Sensex little changed at 51,457.72

- Australia S&P/ASX 200 down 1.8% to 6,474.80

- Kospi down 0.4% to 2,440.93

- STOXX Europe 600 up 1.2% to 407.54

- German 10Y yield little changed at 1.66%

- Euro down 0.4% to $1.0502

- Brent Futures up 0.5% to $120.35/bbl

- Brent Futures up 0.5% to $120.39/bbl

- Gold spot down 0.4% to $1,849.84

- U.S. Dollar Index up 0.75% to 104.41

Top Overnight News from Bloomberg

- A small tweak to the BOJ’s bond purchase plan this week blew up an arbitrage strategy popular with overseas investors known as the basis trade. It exacerbated a supply shortage of government bonds that has ramped up pressure on domestic financial institutions, leading them to turn to the BOJ for help to relieve the strain

- President Joe Biden said a US recession isn’t inevitable and acknowledged that aides warned him about the inflationary risk of his flagship relief bill, while insisting that he won’t soften his stance on Russia even if it costs him re-election

- The WTO clinched a historic package of accords including on vaccine production and fishery subsidies, ending the trade body’s seven-year negotiating drought

- China’s local governments are caught in an unexpectedly severe budget squeeze, creating a dilemma for officials over whether to boost debt or tolerate weaker economic growth

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks mostly suffered firm losses amid the global risk-aversion after the recent flurry of central bank rate increases and with weak data in the US stoking recession fears. ASX 200 was led lower by underperformance in tech and the commodity-related sectors, although gold miners have weathered the storm after the recent upside in the precious metal. Nikkei 225 was pressured and failed to benefit from the BoJ decision to keep policy settings unchanged. Hang Seng and Shanghai Comp. pared opening losses amid virus-related optimism after Beijing reported zero cases outside of quarantine and with US-China defence meetings showing signs of cooling tensions.

Top Asian News

- China in Talks With Qatar for Gas Field Stakes, Reuters Says

- Kuroda Deepens BOJ’s Outlier Status, Keeping Pressure on Yen

- ByteDance Disbands Shanghai Games Studio in Expansion Setback

- BOJ Offers to Buy Cheapest-to-Deliver JGBs for Extended Time

- Gold Heads for Weekly Drop as Traders Weigh Rate Hikes, Growth

European bourses are now firmer across the board, Euro Stoxx 50 +1.2%, as performance picks up following a mixed open amid comparably quiet newsflow. Stateside, US futures are performing similarly, ES +1.0%, though the complex is cognisant of commentary from Chair Powell later. Note, today is Quad Witching; recently, GS’ Rubner highlighted “literally massive” USD 3.2tln notional open interest of US listed options which expire on June 17th, writing that the passing of this may allow the market to move more freely.

Top European News

- UK is to set out new data rules which diverge from the EU on Friday as it seeks to ease pressure on businesses, while it believes the new rules will maintain free flow of data from Europe and does not expect the EU to object to its data reforms, according to Reuters.

- German Finance Minister Lindner told ECB President Lagarde that the ECB’s talk regarding fragmentation threatens to dent confidence, according to FT.

- Hungarian Chief of Staff Gulyas says the idea of a global minimum tax is not accepted by the Hungarian government.

Central Banks

- BoJ kept policy settings unchanged as expected with rates at -0.10% and QQE with yield curve control maintained to target 10yr JGB yields at around 0% with the decision on YCC made via an 8-1 vote as Kataoka dissented. BoJ repeated its April guidance that it will offer to buy 10yr JGBs at 0.25% every business day unless it is highly likely that no bids will be submitted and it also reiterated guidance on policy bias that it will take additional easing steps without hesitation as needed with an eye on the pandemic’s impact on the economy. Furthermore, the BoJ said the economy is picking up as a trend though some weakness has been seen and they must carefully watch the impact of FX moves on Japan’s economy and prices.

- BoJ’s Kuroda says upward pressure is being seen in bond yields, and it is important for FX to move stable reflecting fundamentals, no change to the concept that YCC strongly supports the economic recovery; does not see a limit in YCC. Recent rapid JPY weakness is a weakness for the economy.. Does not see a need for further policy easing now. Not thinking about raising the cap on the BoJ’s long-term yield target above 0.25%, as it could result in higher yields and weaken the effect of monetary easing.

- BoJ purchases JPY 70.1bln in ETFs.

- BoJ offers to purchase the cheapest-to-deliver issuance for an extended time as of June 20th.

- ECB’s Knot says that several 50bps rate increases are possible in the event that inflation worsens, via BNR; does not see hikes reaching 200bp before early-2023.

- BoE’s Pill says markets will have to make their own judgement on whether the BoE is considering a 50bp hike, via Bloomberg TV; stresses the conditionality around the inclusion of “forcefully” in the statement, in the context of “if necessary”. Trying to signal that we may need to act further, looking at the persistence of inflationary pressure. Price pressures becoming embedded would be a trigger for more aggressive BoE action.

FX

- Yen recoils after racking up big risk averse gains as BoJ sticks rigidly to ultra accommodative stance with additional measures to maintain YCC, USD/JPY hovers just under 135.00 vs 131.49 low on Thursday.

- Buck benefits after extending post-FOMC retreat in wake of weak US data and pronounced bounce in Treasuries, DXY extends recovery to 104.540 from 103.410 low.

- Franc maintains SNB hike momentum to rally further across the board, USD/CHF around 0.9650 compared to par-plus peaks earlier in the week.

- Euro underpinned by decent option expiry interest and hawkish ECB commentary, but Aussie undermined as Government gives authorities power to stop coal exports; EUR/USD on the 1.0500 handle and above 1+ bln rolling off between 1.0500-1.0495, AUD/USD capped just under 0.7000.

- Kiwi gleans some traction from a rise in NZ manufacturing PMI and RBNZ rate hike calls; NZD/USD straddles 0.6350, AUD/NZD cross sub-1.1050.

- Lira lags following latest CBRT survey showing higher inflation forecasts and USD/TRY rate, latter at 18.8874 by year end vs 17.5682 previously and circa 17.3200 at present.

Fixed Income

- Debt extends intraday ranges as volatility remains high on Friday.

- Bunds veer from 142.56 to 144.99, Gilts between 111.83 and 112.91 and the 10 year T-note within a 116-19/115.28+ range.

- Hawkish comments from ECB’s Knot largely discounted as EZ periphery bonds outperform on anti-fragmentation dynamic, but BoE’s Pill rattles Sonia strip.

Commodities

- WTI and Brent are currently set to end the week with gains in excess of USD 1.00/bbl overall, though the benchmarks reside towards the mid-point of the over USD 11.00/bbl range for the week.

- Newsflow has been comparably limited but primarily focused on familiar themes.

- US Energy Secretary called an emergency meeting with oil refiners next week to discuss steps companies can take to increase refining capacity and output, according to Reuters citing a DoE spokesperson.

- White House is reportedly considering fuel export limits as pump prices surge and options such as waiving anti-smog rules are also being discussed, according to Bloomberg.

- Qatar Energy set August Al-Shaheen crude term price at a premium of USD 9.24/bbl above Dubai quotes which is the highest in 3 months, according to traders cited by Reuters.

- Brazil’s Petrobras is to announce a fuel price increase today, according to Reuters citing local press.

- China’s national oil majors are reportedly in advanced discussions with Qatar around investment in North Field East LNG and for long-term contractual purchases of LNG, according to Reuters sources.

- Australia has invoked measures to give authorities the power to prevent coal exports if needed in an attempt to avert the risk of blackouts, according to the FT.

- Spot gold is rangebound in European hours having successfully surpassed the cluster of DMAs between USD 1843-1848/oz during Thursday’s blockbuster session.

US Event Calendar

- 09:15: May Capacity Utilization, est. 79.2%, prior 79.0%

- 09:15: May Manufacturing (SIC) Production, est. 0.3%, prior 0.8%

- 09:15: May Industrial Production MoM, est. 0.4%, prior 1.1%

- 10:00: May Leading Index, est. -0.4%, prior -0.3%

DB’s Jim Reid concludes the overnight wrap

The Bank of Japan (BOJ) continues to buck the global trend of monetary tightening, as this morning the central bank decided to maintain its purchases of government bonds and equities. The decision was widely anticipated but the BOJ indicated that it must “pay due attention” to foreign exchange markets, following the yen’s rapid weakening to its lowest level in 24 years earlier this week. The Yen has weakened around -1.3% to 134/USD as we type. Meanwhile, Japan’s benchmark 10yr bond yields hit a six-year high of 0.268% at one point, moving beyond the BOJ’s 0.25% cap ahead of the policy decision. However, yields retreated to the 0.25% after its daily unlimited fixed-rate purchasing operations.

This just continues what has been a very expensive week for the BoJ in terms of JGB QE after having had to buy $9.6tn yen worth. As one of our Asian FX strategists Tim Baker highlighted this morning, that’s US$72bn. Tim highlighted that this is almost what the Fed and ECB were doing in an entire month last year, for economies 5-3x larger than Japan’s. Japan’s QE this week has been running more than 20x the pace of the Fed’s QE in 2021, adjusted for the size of the economy. Can they continue to hold this line? You wouldn’t think they could but it depends on global yields and central banks, the Yen and Japanese inflation. See my CoTD (link here) on this earlier this week. Watch out for the BoJ press conference after this goes to print this morning for any hints as to how determined they are to continue their policy settings.

The BoJ caps an array of central bank meetings over recent days, and markets have experienced another rout over the last 24 hours as multiple headlines added to investors fears about an imminent recession. It marked a big shift from just a day earlier, when the initial focus after Chair Powell’s press conference had been on his comment (when referring to +75bps) that he didn’t “expect moves of this size to be common”. But futures swiftly turned negative as growing doubts were cast on how firm that commitment really was, not least since we’ve all seen just how swiftly the Fed have shifted posture over the last week in response to worse-than-expected data. On top of that, the latest decisions by the SNB and the BoE (more on which below) only added to the hawkish drumbeat that much higher rates are in the offing, whilst weak US housing data served to aggravate those fears about an imminent growth slowdown.

With all said and done, you were hard-pressed to find a major asset that didn’t lose ground yesterday. The major equity indices slumped heavily on both sides of the Atlantic, with the S&P 500 (-3.24%) losing more than -3% for the second time this week, as it also hit its lowest level since late 2020. Indeed, just 14 companies in the entire index moved higher on the day. Elsewhere, the NASDAQ saw an even larger decline, falling -4.08% to have now lost more than a third of its value since its all-time closing peak back in November. It’s lost -9.96% since Friday’s CPI and -6.12% this week. And it was a similar story in Europe too, as the STOXX 600 (-2.47%) fell to a one-year low of its own.

Whilst equities were selling off, sovereign bonds continued to trade with elevated volatility, a function of continued central bank surprises, murky forward guidance, and heightened uncertainty around the near-to-medium-term outlook as economic data gets worse. In short it was a wild, wild ride yesterday. The sell-off initially accelerated after the SNB became the latest central bank to surprise. They hiked rates for the first time in 15 years, executing a 50bps move, combined with a change in FX policy, that our strategist Robin Winkler argues marks a once-in-a-decade policy regime shift (link here). In turn, that led to a massive reaction in the Swiss Franc, which strengthened by +2.91% against the US Dollar on the day in its biggest daily appreciation since 2015.

Then we had the Bank of England, where they hiked rates by +25bps as widely expected, with 3 of the 9 committee members continuing to vote for a larger 50bp increment. Notably, their statement sent a stronger signal on inflation, saying that the Committee would be “particularly alert to indications of more persistent inflationary pressures, and will if necessary act forcefully in response.” In turn, that saw investors reappraise the path of future rate hikes in a more hawkish direction, and are now expecting more than +150bps worth of hikes over the next 3 meetings, so equivalent to at least a 50bp move at each one. Our UK economist writes in his reaction note (link here) that he expects the BoE to hike by 50bps in August and September now, which for reference would be the largest single hikes since they gained operational independence in 1997.

Against that backdrop, sovereign bond yields whipped around yet again. European yields were much higher on tighter policy and then Treasury yields moved higher in sympathy during European trading but gradually fell after another batch of underwhelming housing data lent new fears that growth was on unstable footing. Yields on 10yr Treasuries fell -8.9bps to 3.20%, but at their intraday peak they’d been up +20.7bps, so some sizeable moves in both directions. The move in nominal yields traced real yields, which were as high as +21.7bps intraday at the 10yr point, before finishing the day just +1.1bps higher. 10yr breakevens fell -10.4bps on the prospect of slower growth, which drove nominal yields lower on the day. In Asia, this morning, 10yr yields are witnessing a reversal with yields up +4.33bps to 3.24% while 2yr yields (+6bps) also moved higher to 3.15% as I type. Our US rates strategists have updated their views in the face of some large forces in both directions with the 10yr now expected to hit 3.85%. They also updated their year-end 2yr call to 3.85%, so a flat curve. See the full update here.

Meanwhile in Europe, 10yr bunds gained +7.2bps (+28.3bps at the peak) in a very choppy session. However, there was a considerable tightening in peripheral spreads for a second day running, with the gap between Italian and German 10yr yields down -13.7bps to 202bps, which followed comments from Italian central bank governor Visco that the spread should be under 150bps based on economic fundamentals. The heightened uncertainty and wild swings in yields also translated to heightened currency volatility, where the Euro traded in its widest intraday range since March 2020, which was as low as -0.60% and as strong as +1.50% against the dollar before ultimately appreciating +1.01%.

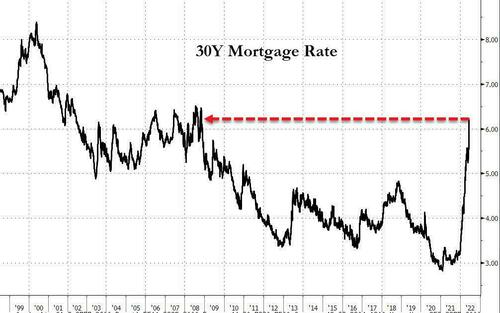

As mentioned, sentiment was further dampened by weak US housing data yesterday, with both housing starts and building permits in May falling by even more than expected. Housing starts were down to an annualised rate of 1.549m (vs. 1.693m expected), their lowest level in over a year, whilst building permits were down to an annualised rate of 1.695m (vs. 1.778m expected). We also got a sign of how tighter monetary policy was affecting the market, with Freddie Mac’s data showing that a 30-year fixed mortgage rate for the week ending yesterday rose to 5.78% (vs. 5.23% in the previous week). That’s the highest level since November 2008, as well as the largest weekly increase in the rate since 1987. And it just shows how the much more rapid pace of Fed hikes now expected by investors over the last week is already filtering its way through to the real economy.

Those moves lower in the US and European equities have been echoed in Asian markets this morning. The Nikkei (-1.59%) is the largest underperformer with the Kospi (-1.08%) also trading sharply lower. Elsewhere, the Hang Seng (+0.78%) is recovering from earlier losses while mainland Chinese stocks also turning around with the Shanghai Composite (+0.15%) and CSI (+0.26%) both trading up.

Outside of Asia, stock futures in the DMs are bouncing with contracts on the S&P 500 (+0.52%), NASDAQ 100 (+0.67%) and DAX (+0.31%) all heading higher.

Looking forward, Russian President Putin will be giving a speech today at the St Petersburg Economic Forum, which his press secretary Peskov has tried to build anticipation for, and could offer a flavour of how combative the Kremlin plans to be in its international approach. That came as German Chancellor Scholz, French President Macron and Italian PM Draghi endorsed Ukraine’s EU candidacy in a visit to the country yesterday. Otherwise, European natural gas futures pared back their significant increases in the morning to close -1.94% lower, marking a change in direction after their massive increases over the previous 2 sessions.

To the day ahead now, and data releases include US industrial production and capacity utilisation for May, along with the final Euro Area CPI reading for May. Central bankers include Fed Chair Powell, the ECB’s Simkus and the BoE’s Tenreyro and Pill.

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED DOWN 20.02 PTS OR 0.61% //Hang Sang CLOSED DOWN 462.78 PTS OR 2.13% /The Nikkei closed UP 105.04 OR 0.40% //Australia’s all ordinaires CLOSED DOWN 0.03% /Chinese yuan (ONSHORE) closed DOWN 6.7149 /Oil DOWN TO 113.77 dollars per barrel for WTI and DOWN TO 116.23 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7149 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7204: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

Yen Tumbles As BoJ Refuses To Change Ultra-Easy Monetary Policy

THURSDAY, JUN 16, 2022 – 11:00 PM

The yen weakened on Friday after the Bank of Japan maintained its ultra-easy monetary stance, increasing policy divergence with its global peers.

“While the decision was within expectations, those who want to challenge the BOJ will continue to do so, putting focus on Japan’s upper house election,” said Mari Iwashita, chief market economist at Daiwa Securities.

“I doubt if the challenge will pick up immediately after today’s decision, but the battle will resume in July.”

Governor Haruhiko Kuroda continued to signal a dovish stance, but the BOJ did make a rare reference to the currency market, saying it needed to watch its impact on the economy and markets.

“In this situation, it is necessary to pay due attention to developments in financial and foreign exchange markets and their impact on Japan’s economic activity and prices,” the central bank said in a statement, referring to risks from commodities, Covid-19, the war in Ukraine and overseas economic developments.

The 10Y JGB Yield is trading at around 27bps (2bps above the BoJ’s YCC upper bound), while JGB futures are signaling the break is imminent still…

That is the highest 10Y yield since January 2016.

As Mari Iwashita, chief market economist at Daiwa Securities, notes:

“If the BOJ were to be pushed into a corner, it would come from the yen weakness progressing further or the proportion of BOJ holdings of 10-year bonds approaching 100%. Neither is taking place as of now.”

The immediate reaction is obvious – dumping of the yen as The BoJ is left to provide unlimited support/defense for the JGB market in th eface of unrelenting pressure sending yields higher…

The simple reality is – The BoJ has no way out of this… tick, tock!

3c CHINA

CHINA/

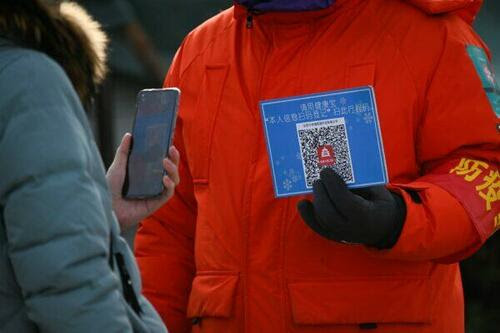

Chinese Banks Freeze Billions In Deposits: Officials Use Health QR Code To Bar Protestors

THURSDAY, JUN 16, 2022 – 10:20 PM

Chinese local banks are freezing deposits. Protestors cannot go near banks as their health app for COVID-19 turns red. Authorities provided no explanation…