by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1820.35 DOWN $3.05

SILVER: $20.87 DOWN 26 CENTS

ACCESS MARKET: GOLD $1818.20

SILVER: $20.74

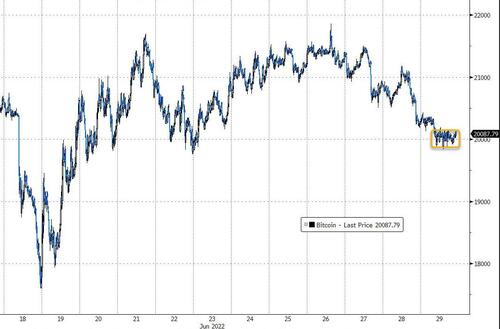

Bitcoin morning price: $20,004 DOWN 314

Bitcoin: afternoon price: $20,317 DOWN 417

Platinum price: closing UP $4.15 to $913.45

Palladium price; closing UP $4.00 at $1883.45

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE:EXCHANGE:

EXCHANGE: COMEX

CONTRACT: JUNE 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,817.500000000 USD

INTENT DATE: 06/28/2022 DELIVERY DATE: 06/30/2022

FIRM ORG FIRM NAME ISSUED STOPPED

435 H SCOTIA CAPITAL 1

657 C MORGAN STANLEY 4

661 C JP MORGAN 41 100

690 C ABN AMRO 78 32

737 C ADVANTAGE 10

905 C ADM 2

991 H CME 4

TOTAL: 136 136

MONTH TO DATE: 24,091

no. of contracts issued by JPMorgan: 100/136

_____________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 136 NOTICE(S) FOR 13,600 Oz//0.4230 TONNES)

total notices so far: 24,091 contracts for 2,409,100 oz (74.923 tonnes)

SILVER NOTICES:

30 NOTICE(S) FILED 150,000 OZ/

total number of notices filed so far this month 1881 : for 9,405,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $3.05

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.27 TONNES FROM THE GLD//

INVENTORY RESTS AT 1054.37 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 26 CENTS

AT THE SLV// ://NO CHANGES IN SILVER INVENTORY AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 542.000 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1896 CONTRACTS TO 135,775 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN OI WAS ACCOMPLISHED WITH OUR $0.26 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.26) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SOME SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS. ALL OF THE COMEX LOSSES DUE TO CONTINUATION OF SPREADER LIQUIDATION

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 6 CONTRACTS OR 30,000 OZ//NEW STANDING: 9,405,000 / // V) STRONG SIZED COMEX OI LOSS/SPREADER LIQUIDATION

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : –198

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 20 days, total 16,469, contracts: 82.345 million oz OR 4.1175MILLION OZ PER DAY. (823 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 82.345 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 82.345 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1896 WITH OUR $0.26 LOSS IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 695 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 30,000 QUEUE JUMP //NEW STANDING: 9,405,000 OZ // .. WE HAD A VERY STRONG SIZED LOSS OF 1201 OI CONTRACTS ON THE TWO EXCHANGES FOR 6.005 MILLION OZ WITH THE LOSS IN PRICE. ALL OF THE COMEX LOSS WAS DUE TO SPREADER LIQUIDATION.

WE HAD 30 NOTICES FILED TODAY FOR 150,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1026 CONTRACTS TO 497,005 AND FURTHER FROM RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: — CONTRACTS.

.

THE SMALL DECREASE IN COMEX OI CAME WITH OUR FALL IN PRICE OF $3.05//COMEX GOLD TRADING/TUESDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERING

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S 4400 OZ QUEUE JUMP //NEW STANDING: 74.933TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $3.05 WITH RESPECT TO MONDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 3270 OI CONTRACTS 10.171 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4296 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 497,005

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4958, WITH 1073 CONTRACTS INCREASED AT THE COMEX AND 3885 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2812 CONTRACTS OR 8.746TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4296) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (1026,): TOTAL GAIN IN THE TWO EXCHANGES 3270 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING AND SOME ADDITION TO SPECULATOR SHORTS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S E.F.P JUMP OF 2500 OZ//NEW STANDING: 74.715 TONNES / 3) ZERO LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING//SOME SPECULATOR SHORT ADDITIONS //.,4) SMALL SIZED COMEX OI LOSS 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

72,823 CONTRACTS OR 7,282,300 OZ OR 226.51 TONNES 20 TRADING DAY(S) AND THUS AVERAGING: 3641 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAY(S) IN TONNES: 226.51 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 226.51/3550 x 100% TONNES 6.00% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 226.51 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JULY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A HUGE SIZED 1896 CONTRACT OI TO 137,671 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 695 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 695 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1896 CONTRACTS AND ADD TO THE 695 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 1201 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 6.005 MILLION OZ

OCCURRED WITH OUR FALL IN PRICE OF $0.26 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 47.69 PTS OR 1.40% //Hang Sang CLOSED DOWN 422.08 PTS OR 1.88% /The Nikkei closed DOWN 244.87 OR 0.91% //Australia’s all ordinaires CLOSED DOWN 1.09 /Chinese yuan (ONSHORE) closed DOWN 6.6952 /Oil UP TO 112.93 dollars per barrel for WTI and UP TO 119.20 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6952 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6990: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 1026 CONTRACTS TO 497,005 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR LOSS OF $3.05 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (4052 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING PAST THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4296 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :4296 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4296 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3270 CONTRACTS IN THAT 4296 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI LOSS OF 1026 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $3.05.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JUNE (74.933),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $3.05) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A FAIR SIZED GAIN OF 10.171 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (74.933 TONNES)…

WE HAD -35 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3270 CONTRACTS OR 327,000 OZ OR 10.171 TONNES

Estimated gold volume 157,277/// poor/

final gold volumes/yesterday 122,214 /poor

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 29

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | NOT AVAILABLE oz |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 136 notice(s)13,600 OZ0.4230 TONNES |

| No of oz to be served (notices) | 0 contracts0.000 TONNES |

| Total monthly oz gold served (contracts) so far this month | 24,091 notices2,409,100 OZ74.933 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

INVENTORY MOVEMENTS NOT AVAILABLE TODAY

total dealer deposit 0

No dealer withdrawals

XX customer deposit

total deposits: XX oz

XX customer withdrawals:

total withdrawal: XXX oz

ADJUSTMENTS:

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 136 contracts having GAINED 74 contracts

We had 30 notices filed on TUESDAY so we GAINED 104 contracts or an additional 10,400 oz will stand for gold in this very active month of June

July has a LOSS OF 256 OI to stand at 1011

August has a LOSS of 2558 contracts DOWN to 402,916 contracts

We had 136 notice(s) filed today for 13,600 oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 41 notices were issued from their client or customer account. The total of all issuance by all participants equate to 136 contract(s) of which 100 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (24,091) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 136 CONTRACTS ) minus the number of notices served upon today 136 x 100 oz per contract equals 2,409,100 OZ OR 74.933 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (24,091) x 100 oz+ (136) OI for the front month minus the number of notices served upon today (136} x 100 oz} which equals 2,398,700 oz standing OR 74.933 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 74.933 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,419,784.828 oz 75.26 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 33,183,194,729 OZ

TOTAL ELIGIBLE GOLD: 16,003,775.914 OZ

TOTAL OF ALL REGISTERED GOLD: 17,179,418.815 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 14,792,235.0 OZ (REG GOLD- PLEDGED GOLD)

END

SILVER/COMEX/JUNE 29

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | NOT AVAILABLE oz |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 30CONTRACT(S)150,000 OZ) |

| No of oz to be served (notices) | 0 contracts |

| Total monthly oz silver served (contracts) | 24091 contracts 9,405,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

INVENTORY MOVEMENTS NOT AVAILABLE TODAY

i) 0 dealer deposit

total dealer deposits: XX oz

i) We had XX dealer withdrawal

total dealer withdrawals: XX oz

We have X deposit into the customer account

total deposit: XX oz

JPMorgan has a total silver weight: 169.097 million oz/333.529 million =50.67% of comex

Comex withdrawals: X

total withdrawal XXX oz

adjustments: XX

the silver comex is in stress!

TOTAL REGISTERED SILVER: 69.749 MILLION OZ

TOTAL REG + ELIG. 333.529 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 30 HAVING LOST 15 CONTRACTS.

WE HAD 21 NOTICES FILED ON TUESDAY SO WE GAINED 16 CONTRACTS OR AN ADDITIONAL 30,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 7887 CONTRACTS DOWN TO 6323 CONTRACTS.

AUGUST GAINED 90 CONTRACTS TO STAND AT 1376

SEPTEMBER HAD A GAIN OF 5716 CONTRACTS UP TO 109,396 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 30 for 150,000 oz

Comex volumes:55,731// est. volume today// FAIR

Comex volume: confirmed yesterday: 85,158 contracts ( strong )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1881 x 5,000 oz = 9,455,000 oz

to which we add the difference between the open interest for the front month of JUNE(30) and the number of notices served upon today 30 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1881 (notices served so far) x 5000 oz + OI for front month of JUNE (30) – number of notices served upon today (30) x 5000 oz of silver standing for the JUNE contract month equates 9,405,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 28/WITH GOLD DOWN $3.05//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.64 TONNES FROM THE GLD///INVENTORY RESTS AT 1056.40 TONNES

JUNE 27/WITH GOLD DOWN $4.90 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.04 TONNES

JUNE 24/WITH GOLD UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

JUNE 21/WITH GOLD DOWN $2.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1075.54 TONES

JUNE 17/WITH GOLD DOWN $11.25: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.60 TONNES INTO THE GLD.///INVENTORY RESTS AT 1075.54 TONNES

JUNE 16/WITH GOLD UP $28.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.74 TONNES

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

JUNE 14/WITH GOLD DOWN $18.80/NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

GLD INVENTORY: 1056.40 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 28/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.00 MILLION OZ..

JUNE 27/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

JUNE 21/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.506 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 547.166 MILLION OZ//

JUNE 17/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 739,000 OZ FROM THE SLV./:INVENTORY RESTS AT 543.660 MILLION OZ/

JUNE 16/WITH SILVER UP 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 14/WITH SILVER DOWN 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

CLOSING INVENTORY 542.000 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg

END

3. Chris Powell of GATA provides to us very important physical commentaries

END

4. OTHER GOLD STORIES

5.OTHER COMMODITIES

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.6952

OFFSHORE YUAN: 6.6990

HANG SANG CLOSED DOWN 422.08 PTS OR 1.88%

2. Nikkei closed DOWN 244.87% OR 0.91%

3. Europe stocks ALL CLOSED ALL RED

USA dollar INDEX UP TO 104.32/Euro FALLS TO 1.0516

3b Japan 10 YR bond yield: RISES TO. +.232/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 136.48/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN -// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.587%/Italian 10 Yr bond yield FALLS to 3.58% /SPAIN 10 YR BOND YIELD FALLS TO 2.66%…

3i Greek 10 year bond yield RISES TO 3.63//

3j Gold at $1826.90 silver at: 21.03 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 6/100 roubles/dollar; ROUBLE AT 51.88

3m oil into the 112 dollar handle for WTI and 119 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 136.48DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9502– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.99914well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.163 DOWN 5 BASIS PTS

USA 30 YR BOND YIELD: 3.286 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 16.64

Futures Slide Amid Renewed Recession Fears After China Doubles Down On “Covid Zero”

WEDNESDAY, JUN 29, 2022 – 08:00 AM

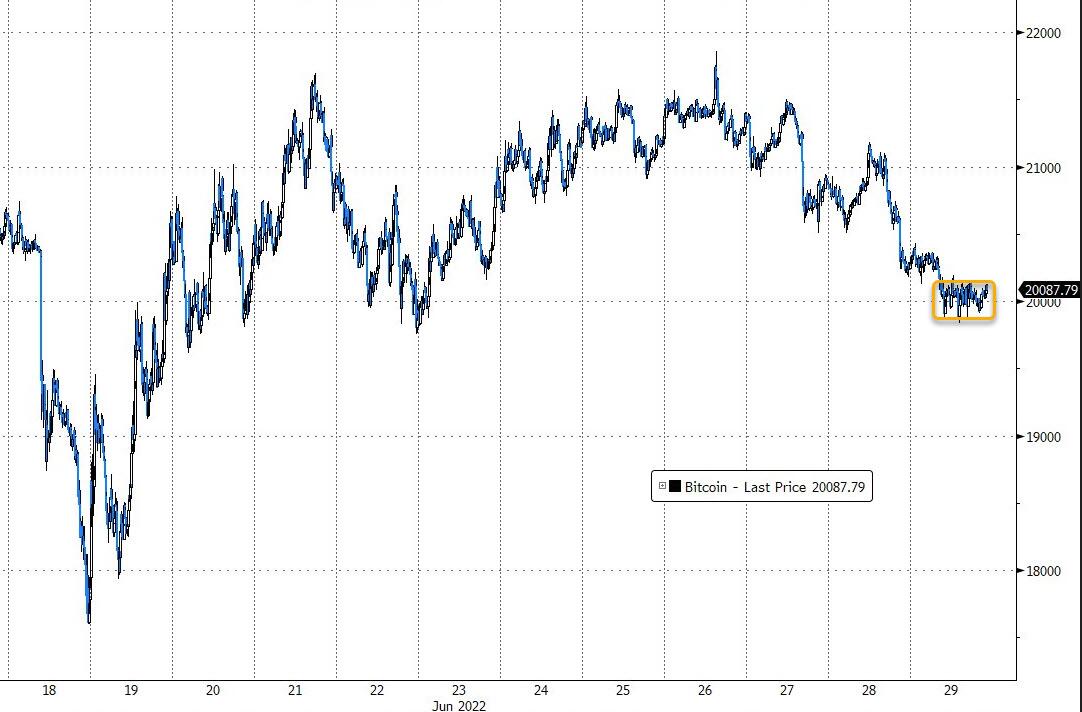

One day after futures ramped overnight (if only to crater during the regular session) on hopes China was easing its highly politicized Zero Covid policy after it cut the time of quarantine lockdowns, this morning futures slumped early on after China’s President Xi Jinping made clear that Covid Zero isn’t going anywhere and remains the most “economic and effective” policy for China during a symbolic visit to the virus ground zero in Wuhan, in which he cast the strategy as proof of the superiority of the country’s political system. That coupled with renewed recession worries (market is again pricing in a rate cut in Q1 2023) even as monetary policy tightens in much of the world to fight supply-side inflation, sent US futures and global markets lower. S&P futures dropped 0.2% and Nasdaq 100 futures were down 0.4% after the underlying index slumped on 3.1% on Tuesday. The dollar was steady after rising the most in over a week while WTI crude climbed above $112 a barrel, set for a fourth session of gains. In cryptocurrencies, Bitcoin dipped below the closely watched $20,000 level on news crypto hedge fund 3 Arrows Capital was ordered to liquidate.

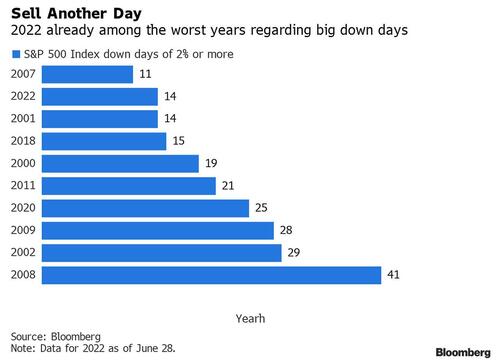

The Nasdaq’s Tuesday’s slump added to what was already one of the worst years in terms of big daily selloffs in US stocks. The S&P 500 Index has fallen 2% or more on 14 occasions, putting 2022 in the top 10 list, according to Bloomberg data.

Not helping the tech sector, on Wednesday morning JPMorgan cut its earnings estimates across the sector, especially for companies exposed to online advertising, citing macroeconomic pressures, forex and company-specific dynamics.

One of the chief drivers for overnight weakness, China’s Xi said during a trip Tuesday to Wuhan where the virus first emerged in late 2019 that relaxing Covid controls would risk too many lives in the world’s most populous country. China would rather endure some temporary impact on economic development than let the virus hurt people’s safety and health, he said, in remarks reported Wednesday by state media. As a result, China’s CSI 300 Index extended loss to 1.4% after the headline, while the yuan drops as much as 0.2% to trade 6.7132 against the dollar in the offshore market.

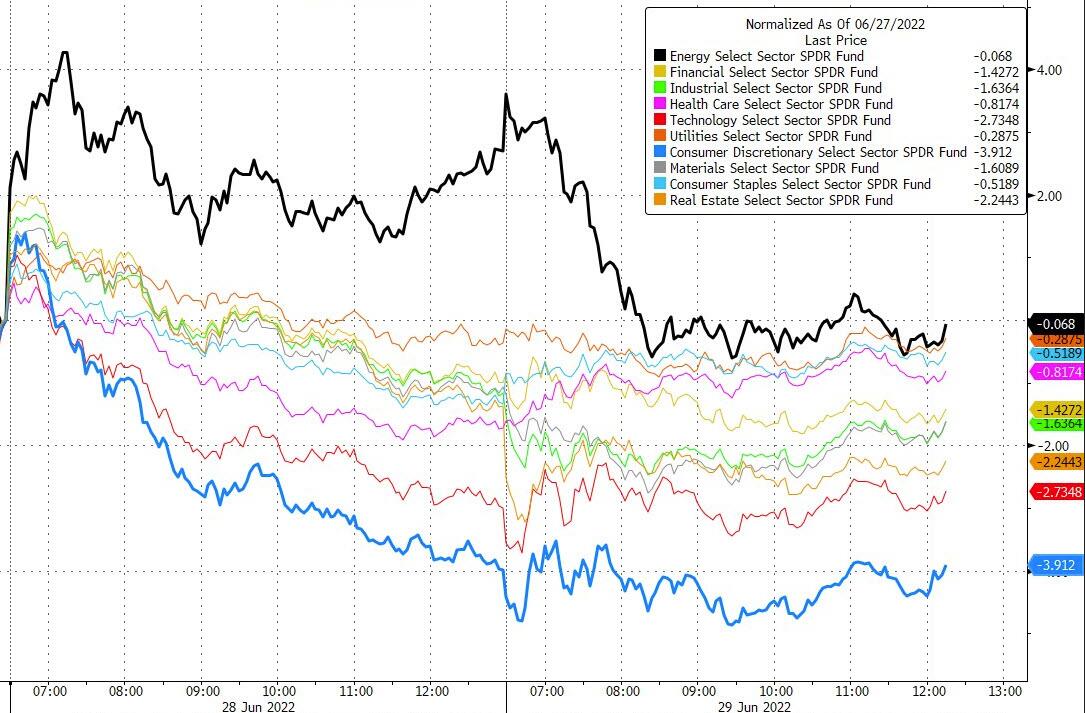

Among key premarket movers, Tesla slipped in US premarket trading. The electric-vehicle maker laid off hundreds of workers on its Autopilot team as it shuttered a California facility, according to people familiar with the matter. Carnival slumped as Morgan Stanley analysts warned that the London and New York-listed cruise vacation company’s shares could lose all their value in the event of another demand shock. Pinterest gained 3.7% as the company’s co- founder and CEO Ben Silbermann quit and handed the reins to Google and PayPal veteran Bill Ready in a sign the social-media company will focus more on e-commerce. Also, despite the pervasive weakness, the Energy Select Sector SPDR Fund ETF (XLE) rebounded off key support (50% Fibonacci) relative to the SPDR S&P 500 ETF (SPY). That said, energy was alone and most other notable movers were down in the premarket:

- Carnival (CCL US) shares fall 8% premarket as Morgan Stanley analysts warned that the cruise vacation firm’s shares could lose all their value in the event of another demand shock.

- Nio (NIO US) shares drop 8.2% after short-seller Grizzly Research published a report on Tuesday alleging that the electric carmaker used battery sales to a related party to inflate revenue and boost net income margins. The company rejected the claims.

- Upstart Holdings (UPST US) shares slump about 9% after Morgan Stanley downgraded the consumer finance company to underweight from equal-weight amid rising cyclical headwinds.

- Ormat Technologies (ORA US) rallies as much as 5% after the renewable energy company is set to be included in the S&P Midcap 400 Index.

- 2U (TWOU US) shares rise 16% premarket. Indian online-education provider Byju’s has offered to buy the company in a cash deal that values the US-listed edtech firm at more than $1 billion, a person familiar with the matter said.

- Watch Amazon (AMZN US) shares as Redburn initiated coverage of the stock with a buy recommendation and set a Street-high price target, saying “there is a clear path toward a $3 trillion value for AWS alone.”

- Shares in data center REITs could be active later in the trading session after short-seller Jim Chanos said in an FT interview that he’s betting against “legacy” data centers. Watch Digital Realty (DLR US) and Equinix (EQIX US), as well as data center operators Cyxtera Technologies (CYXT US) and Iron Mountain (IRM US)

Investors are growing increasingly skeptical that the Fed can avoid a bruising economic downturn amid sharp interest-rate hikes. Evaporating consumer confidence is feeding into concerns that the US might tip into a recession. Naturally, Fed officials sought to play down recession risk. New York Fed President John Williams and San Francisco’s Mary Daly both acknowledged they had to cool inflation, but insisted that a soft landing was still possible.

“It seems the market is in this tug of war between on the one hand the hope that we are close to the peak in inflation and rates, and on the other hand the challenge of a slowing economy and potential recession,” Emmanuel Cau, head of European equity strategy at Barclays Bank Plc, said in an interview with Bloomberg TV. “Central banks are walking a very tight line and to a certain extent dictate the mood in the markets.”

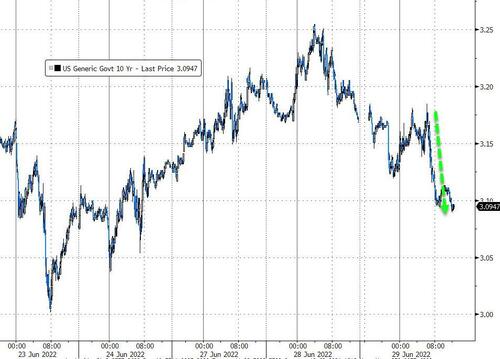

European equities snapped three days of gains, trading poorly but off worst levels with sentiment also hurt by China remaining committed to its zero-Covid approach. Spanish inflation unexpectedly surged to a record, dashing hopes that inflation in the euro zone’s fourth-biggest economy had peaked, and emboldening European Central Bank policy makers pushing for big increases in interest rates. The ECB should consider raising interest rates by twice the planned amount next month if the inflation outlook deteriorates, according to Governing Council member Gediminas Simkus, as calls not to exclude an outsized initial move grow. German benchmark bonds rose, while 10-year Treasury yields slipped to 3.16%. DAX lags, dropping as much as 1.8%. Real estate, autos and miners are the worst performing sectors.

In notable moves in European stocks, Hennes & Mauritz (H&M) gained after the Swedish low-cost retailer’s earnings beat analyst estimates. Just Eat Takeaway.com NV tumbled to a record low after Berenberg analysts rated the stock sell, saying the food delivery firm’s UK business will remain under pressure. Here are some of the biggest European movers today:

- Just Eat Takeaway shares plunge as much as 21% after Berenberg initiated coverage with a sell rating, saying the firm’s UK business will remain under pressure and a sale of its Grubhub unit is unlikely to satisfy the bulls.

- Carnival stocks slumped over 12% in London as Morgan Stanley analysts warned that the cruise vacation firm’s shares could lose all their value in the event of another demand shock.

- Pearson drops as much as 6.1% after the education company was cut to sell at UBS, which reduced forecasts to reflect a weak outlook for 2022 college enrollments.

- Grifols shares plunge as much as 13% on a media report the Spanish plasma firm is weighing a capital raise of as much as EU2b to cut its debt.

- Diageo shares fall after downgrades for the spirits group from Deutsche Bank and Kepler Cheuvreux, while Pernod Ricard also dips on a rating cut from the latter.

- Diageo declines as much as 4.2%, Pernod Ricard -3.7%

- Fluidra shares fall as much as 8.4% after Santander cut its rating on the Spanish swimming pools company. The bank’s analyst Alejandro Conde cut the recommendation to neutral from outperform.

- H&M shares rise as much as 6.8% after the Swedish apparel retailer reported 2Q earnings that beat estimates. Jefferies said the margin beat in particular was reassuring, while Morgan Stanley said it was a “positive surprise” overall.

- Ipsen shares rise as much as 3.1% after UBS analyst Michael Leuchten said that accepting palovarotene refiling priority review should be a net present value and confidence boost.

Asian stocks fell, halting a four-day gain, as renewed angst over the outlook for global economic growth and inflation help drive a selloff across most of the region’s equity markets. The MSCI Asia Pacific Index dropped as much as 1.5%, led by consumer discretionary and information sectors. Chinese equities in particular took a hit, as the CSI 300 Index fell 1.5% Wednesday after Xi Jinping reiterated his firm stance on Covid zero. Tech-heavy indexes in markets such as South Korea and Taiwan took the brunt of Wednesday’s drop amid lingering concerns that monetary tightening in much of the world to fight inflation will cause an economic slowdown. While Federal Reserve members have played down the risk of a US recession, gloomy data such as US consumer confidence have damped investor sentiment.

“Volatility is going to be the enduring feature of the market, I suspect, for the next couple of quarters at least until we get a firm sense that peak inflation has passed,” John Woods, Credit Suisse Group AG’s Asia-Pacific chief investment officer, said in an interview with Bloomberg TV. “Markets, I think, have aggressively priced in quite a serious or steep recession.” China’s four-day winning streak came to a halt, putting its advance toward a bull market on hold. “We will continue to see a risk of targeted lockdowns, and that spoils the initial euphoria seen in the markets from the announcement on relaxation of quarantine requirements,” said Charu Chanana, market strategist at Saxo Capital Markets. “Still, economic growth will likely be prioritized as this is a politically important year for China.”

Japanese equities decline as investors digested data that showed a drop in US consumer confidence over inflation worries and increased concerns of an economic downturn. The Topix Index fell 0.7% to 1,893.57 in Tokyo on Wednesday, while the Nikkei declined 0.9% to 26,804.60. Toyota Motor Corp. contributed the most to the Topix’s decline, decreasing 1.8%. Out of 2,170 shares in the index, 1,114 fell, 984 rose and 72 were unchanged. “There are concerns about stagflation,” said Hideyuki Suzuki a general manager at SBI Securities. “The consumer sentiment from the University of Michigan, which provides one of the fastest data points, has already shown poor figures.”

Stocks in India tracked their Asian peers lower as brent rose to the highest level in two weeks, while high inflation and slowing global growth continued to dampen risk-appetite for global equities. The S&P BSE Sensex fell 0.3% to 53,026.97 in Mumbai, while the NSE Nifty 50 Index declined by an equal measure. Both gauges have lost more than 4% in June and are set for their third consecutive month of declines. The main indexes have dropped for all but one month this year. Twelve of the 19 sub-sector gauges compiled by BSE Ltd. eased, led by banking companies while power producers were the top performers. Investors will also be watching the expiry of monthly derivative contracts on Thursday, which may lead to some volatility in the markets. Hindustan Unilever was the biggest contributor to the Sensex’s decline, decreasing 3.5%. Out of 30 shares in the Sensex, 10 rose and 20 fell.

The Bloomberg Dollar Spot Index inched up modestly as the greenback traded mixed against its Group-of-10 peers; the Swiss franc led gains while Antipodean currencies were the worst performers and the euro traded in a narrow range around $1.05. The relative cost to own optionality in the euro heading into the July meetings of the ECB and the Federal Reserve was too low for investors to ignore and has become less and less underpriced. The yen strengthened and US and Japanese bond yields fell.

In rates, fixed income has a choppy start. Bund futures initially surged just shy of 200 ticks on a soft regional German CPI print before fading the entire move over the course of the morning as Spanish data hit the tape, delivering a surprise record 10% reading for June and more hawkish ECB comments crossed the wires. Treasuries and gilts followed with curves eventually fading a bull-steepening move. Long-end gilts underperform, cheapening ~4bps near 2.75%. Peripheral spreads are tighter to core.

Treasuries are slightly higher as US trading day begins, off the session lows reached as bund futures jumped after the first monthly drop since November in a German regional CPI gauge. Yields are lower across the curve, by 1bp-2bp for tenors out to the 10-year with long-end yields little changed; 10-year declined as much as 5.3bp vs as much as 8.2bp for German 10- year, which remains lower by ~3bp. Focal points for the US session include a final revision of 1Q GDP, comments by Fed Chair Powell, and anticipation of quarter-end flows favoring bonds. Quarter-end is anticipated to cause rebalancing flows into bonds; Wells Fargo estimated that $5b will be added to bonds, with most of the flows occurring Wednesday and Thursday.

In commodities, crude futures advance. WTI drifts 0.3% higher to trade near $112.13. Base metals are mixed; LME tin falls 5.6% while LME zinc gains 0.4%. Spot gold falls roughly $5 to trade near $1,815/oz

Looking ahead, the highlight will be the panel at the ECB Forum that includes Fed Chair Powell, ECB President Lagarde and BoE Governor Bailey. We’ll also be hearing from ECB Vice President de Guindos, the ECB’s Schnabel, the Fed’s Mester and Bullard, and the BoE’s Dhingra. On the data side, releases include German CPI for June, Euro Area money supply for May, and the final Euro Area consumer confidence reading for June. From the US, we’ll also get the third reading of Q1 GDP.

Market Snapshot

- S&P 500 futures little changed at 3,829.00

- STOXX Europe 600 down 0.8% to 412.69

- MXAP down 1.3% to 159.96

- MXAPJ down 1.6% to 531.04

- Nikkei down 0.9% to 26,804.60

- Topix down 0.7% to 1,893.57

- Hang Seng Index down 1.9% to 21,996.89

- Shanghai Composite down 1.4% to 3,361.52

- Sensex little changed at 53,204.17

- Australia S&P/ASX 200 down 0.9% to 6,700.23

- Kospi down 1.8% to 2,377.99

- German 10Y yield little changed at 1.59%

- Euro little changed at $1.0510

- Brent Futures down 0.4% to $117.46/bbl

- Gold spot down 0.2% to $1,816.09

- U.S. Dollar Index little changed at 104.55

Top Overnight News from Bloomberg

- The Fed’s Loretta Mester said she wants to see the benchmark lending rate reach 3% to 3.5% this year and “a little bit above 4% next year” to rein in price pressures even if that tips the economy into a recession

- The ECB should consider raising interest rates by twice the planned amount next month if the inflation outlook deteriorates, according to Governing Council member Gediminas Simkus, as calls not to exclude an outsized initial move grow

- ECB has “ample room” to hike in 25bps-50bps steps to “whatever rate we think, we consider reasonable,” Governing Council member Robert Holzmann said in interview with CNBC

- Swedish consumers are gloomier than they have been since the mid-1990s, as prices surge on everything from fuel to food and furniture

- China’s President Xi Jinping declared Covid Zero the most “economic and effective” policy for the nation, during a symbolic visit to Wuhan in which he cast the strategy as proof of the superiority of the country’s political system

- NATO moved one step closer to bolstering its eastern front with Russia after Turkey dropped its opposition to Swedish and Finnish bids to join the military alliance

A more detailed look at markets courtesy of Newsquawk

Asia-Pac stocks were pressured amid headwinds from the US where disappointing Consumer Confidence data added to the growth concerns. ASX 200 failed to benefit from better than expected Retail Sales and was dragged lower by weakness in miners and tech. Nikkei 225 fell beneath the 27,000 level as industries remained pressured by the ongoing power crunch. Hang Seng and Shanghai Comp. conformed to the negative picture in the region although losses in the mainland were initially stemmed after China cut its quarantine requirements which the National Health Commission caveated was not a relaxation but an optimization to make it more scientific and precise.

Top Asian News

- Chinese President Xi said China’s COVID prevention control and strategy is correct and effective and must stick with it, via state media. Shanghai will gradually reopen museums and scenic sports from July 1st, state media reports.

- US Deputy Commerce Secretary Graves said the US will take a balanced approach on Chinese tariffs and that a clear response on China tariffs is coming soon, according to Bloomberg.

- China State Council’s Taiwan Affairs Office said it firmly opposes the US signing any agreement that has sovereign connotations with Taiwan, according to Global Times.

- BoJ Governor Kuroda said Japanese Core CPI reached 2.1% in April and May which is almost fully due to international energy prices and Japan’s economy has not been affected much by the global inflationary trend so monetary policy will stay accommodative, according to Reuters.

- Japanese govt to issue power supply shortage warning for a fourth consecutive day on Thursday, according to a statement.

European bourses are on the backfoot as the region plays catch-up to the losses on Wall Street yesterday. Sectors are mostly lower (ex-Energy) with a defensive tilt as Healthcare, Consumer Products, Food & Beverages, and Utilities are more cushioned than their cyclical peers. Stateside, US equity futures trade on either side of the unchanged mark with no stand-out performers thus far, with the contracts awaiting the next catalyst.

Top European News

- UK expects defence spending to reach 2.3% of GDP and said PM Johnson will announce new military commitments to NATO, according to Reuters.

- UK Weighs Capping Maximum Stake in Online Casinos at £5

- Europe Is the Only Region Where Earnings Estimates Are Rising

- European Gas Prices Rise as Supply Risks Add to Storage Concerns

- Gold Steady as Traders Weigh Fed Comments on US Recession Risks

- Choppy Start for Euro-Area Bonds on Mixed Inflation

FX

- Dollar mostly bid otherwise as rebalancing demand underpins – DXY pivots 104.500 within 104.700-350 confines.

- Franc outperforms on rate and risk considerations – Usd/Chf breaches 0.9550 and Eur/Chf approaches parity.

- Euro erratic in line with conflicting inflation data – Eur/Usd rotates around 1.0500.

- Aussie and Kiwi undermined by downturn in sentiment – Aud/Usd loses 0.6900+ status, Nzd/Usd wanes from just over 0.6250.

- Yen rangy following firmer than forecast Japanese retail sales and BoJ Governor Kuroda reaffirming intent to remain accommodative – Usd/Jpy straddles 136.00.

- Nokkie welcomes oil worker wage agreement with unions to avert strike action, but Sekkie hampered by softer Swedish macro releases pre-Riksbank policy call tomorrow – Eur/Nok probes 10.3000, Eur/Sek hovers around 10.6800.

- Rand rattled by decline in Gold and ongoing SA power supply problems, but Rouble rallies irrespective of CBR and Russian Economy Ministry divergence over deflation.

Central Banks

- ECB’s Lane said there are two-way inflation risks: “on the one side, there could be forces that keep inflation higher than expected for longer. On the other side, we do have the risk of a slowdown in the economy, which would reduce inflationary pressure”, via ECB.

- ECB’s Holzmann said “We will have to make an assessment where the economic development is going and where inflation stands and afterwards there’s ample room to hike in 0.25 and 0.5 levels to whatever rate we think, we consider reasonable” via CNBC.

- ECB’s Simkus said if data worsens, then he wants a 50bps July hike as an option, 50bps hike is very likely in September; ECB’s fragmentation tool should serve as a deterrent, via Bloomberg.

- ECB’s Herodotou said EZ inflation will peak this year, via CNBC.

- ECB’s Wunsch said government aid may spell more rate hikes, via Bloomberg; 150bps of hikes by March 2023 is reasonable

- ECB is said to be weighting whether or not they should announce the size and duration of their upcoming bond-buying scheme, according to Reuters sources.

- Fed’s Mester (2022, 2024 voter) said on a path towards restrictive interest rates; July debate between 50bps and 75bps hike, via CNBC. Mester said if inflation expectations become unanchored, monetary policy would have to act more forcefully; current inflation situation is a very challenging one, via Reuters.

- SARB Governor said a 50bps hike is “not off the table”, Via Bloomberg

- CBR Governor said she does not see risks of deflation; sees room to cut rates; sticking to policy of floating RUB exchange rate.

- PBoC will step up implementation of prudent monetary policy, will keep liquidity reasonably ample.

Fixed Income

- Bunds unwind all and a bit more of their hefty post-NRW CPI gains as other German states show smaller inflation slowdowns and Spanish HICP soars.

- Gilts suffer more pronounced fall from grace in relative terms and US Treasuries slip from overnight peaks in sympathy.

- UK debt and STIRs also await testimony from MPC member elect to see if newbie leans dovish, hawkish or middle of the road

- 10 year benchmarks settle off worst levels within 147.37-145.14, 112.66-11.85 and 117-12+/116-27 respective ranges awaiting comments from ECB, Fed and BoE heads at Sintra Forum.

Commodities

- WTI and Brent front-month futures traded with no firm direction in early European hours before picking up modestly in recent trade.

- US Private Inventory (bbls): Crude -3.8mln (exp. -0.6mln), Cushing -0.7mln, Distillate +2.6mln (exp. -0.2mln) and Gasoline +2.9mln (exp. -0.1mln).

- Norway’s Industri Energi and SAFE labour unions agreed a wage deal for oil drilling workers and will not go on strike, according to Reuters.

- OPEC to start today at 12:00BST/07:00EDT; JMMC on Thursday at 12:00BST/07:00EDT followed by OPEC+ at 12:30BST/07:30EDT, via EnergyIntel.

- Libya’s NOC suspends oil exports from Es Sider port.

- Spot gold is under some mild pressure as the Buck and Bond yields picked up, with the yellow metal back to near-two-week lows

- Base metals are mixed but off best levels after President Xi reaffirmed China’s COVID stance – LME copper fell back under USD 8,500/t

US Event Calendar

- 07:00: June MBA Mortgage Applications, prior 4.2%

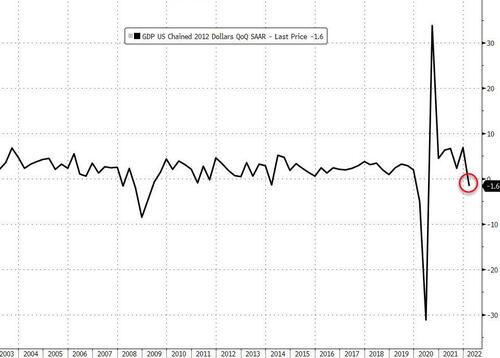

- 08:30: 1Q PCE Core QoQ, est. 5.1%, prior 5.1%

- 08:30: 1Q GDP Price Index, est. 8.1%, prior 8.1%

- 08:30: 1Q Personal Consumption, est. 3.1%, prior 3.1%

- 08:30: 1Q GDP Annualized QoQ, est. -1.5%, prior -1.5%

Central Banks

- 09:00: Powell Takes Part in Panel Discussion at ECB Forum in Sintra

- 09:00: Lagarde, Powell, Bailey, Carstens Speak in Sintra

- 11:30: Fed’s Mester Speaks on Panel at ECB Forum in Sintra

- 13:05: Fed’s Bullard Makes Introductory Remarks

DB’s Jim Reid concludes the overnight wrap

I’m finishing this off in a taxi on the way to the Eurostar this morning and I made the mistake of telling the driver I was slightly pressed for time. He seems to be taking the racing line everywhere and my motion sickness is kicking in.

A little like this car journey, it’s been another volatile 24 hours in markets, with a succession of weak data releases raising further questions about how close the US and Europe might be to a recession. That saw equities give up their initial gains to post a decent decline on the day, whilst there was little respite from central bankers either, with sovereign bonds selling off further as multiple speakers doubled down on their hawkish rhetoric. That comes ahead of another eventful day ahead on the calendar, with investors primarily focused on a panel featuring Fed Chair Powell, ECB President Lagarde and BoE Governor Bailey, as well as the flash German CPI print for June, who are the first G7 economy to release their inflation print for the month, which will provide some further clues on how fast central banks will need to move on rate hikes. Just as we go to print the NRW region of Germany has seen CPI print at 7.5% YoY, way below last month’s 8.1%. This region is around a quarter of GDP so it could imply the national numbers will be notably softer when we get them later. The energy tax cuts were always going to come through in June so some respite was always possible but at first glance this seems materially below what might have been expected.

This comes after a significant sovereign bond selloff in Europe once again yesterday as President Lagarde reiterated the central bank’s determination to bring down inflation, and described inflation pressures that were “broadening and intensifying”. And although Lagarde stuck to the existing script about the ECB raising rates by 25bps at the next meeting, we also heard from Latvia’s Kazaks who said that “front-loading the increase would be a reasonable choice” in the event that the situation with inflation or inflation expectations deteriorates. Lagarde did nod to this in part, saying that if the ECB was “to see higher inflation threatening to de-anchor inflation expectations, or signs of a more permanent loss of economic potential that limits resources availability, we would need to withdraw accommodation more promptly to stamp out the risk of a self-fulfilling spiral.” Separately on fragmentation, Lagarde said that they could “use flexibility in reinvesting redemptions” from PEPP starting July 1 in order to deal with the issue.

For now, overnight index swaps are only pricing in a +31.3bps move in July from the ECB, so still closer to 25 than 50 for the time being. Meanwhile the rate priced in by year-end rose also by +7.9bps as investors interpreted the comments in a hawkish light. That supported a further rise in yields, with those on 10yr bunds up another +8.1bps yesterday, following on from their +10.7bps move in the previous session. That’s now almost reversed the -21.9ps move over the previous week, which itself was the third-largest weekly decline in bund yields for a decade, and brought the 10yr yield back up to 1.63%, so not far off its multi-year high of 1.77% seen last week. A similar pattern was seen elsewhere, with 10yr yields on 10yr OATs (+9.6bps), BTPs (+4.2bps) and gilts (+7.2bps) all moving higher too.

Things turned near the European close with some poor US data releases piling on to some lacklustre confidence figures in Europe. Earlier in the day the GfK consumer confidence reading from Germany fell to -27.4 (vs. -27.3 expected), taking it to another record low. Separately in France, consumer confidence fell to 82 on the INSEE’s measure (vs. 84 expected), which we haven’t seen since 2013. Then in the US, the Conference Board’s measure fell to 98.7 (vs. 100.0 expected), which is the lowest since February 2021. The Conference Board’s one-year ahead inflation expectations hit a record high of 8.0%, surpassing the June 2008 record of 7.7%, adding to the pessimism. Along with waning confidence, the Richmond Fed’s Manufacturing Index registered a -19, its lowest since the peak onset of the pandemic, versus expectations of -7 and a prior of -9, showing that production data has weakened as well. This put a serious damper on risk sentiment which drove Treasury yields and equities lower intraday during the New York session.

10yr Treasury yields ended down -2.8bps after trading as much as +5.5bps higher during the European session. They are down another -4bps this morning. Concerningly as well, there was a fresh flattening in the Fed’s preferred yield curve indicator (which is 18m3m – 3m), which came down another -9.1bps to 165bps, which is the flattest its been since early March.

With that succession of bad news helping to dampen risk appetite, US equities gave up their opening gains to leave the S&P 500 down -2.01% on the day. Tech stocks saw the worst losses, with the NASDAQ (-2.98%) and the FANG+ (-3.74%) seeing even larger declines. And whilst there was a stronger performance in Europe, the STOXX 600 ended the day up just +0.27%, having been as high as +0.95% in the couple of hours before the close.

We didn’t hear so much from the Fed ahead of Chair Powell’s appearance today, although New York Fed President Williams said that at the upcoming July meeting “I think 50 to 75 is clearly going to be the debate”. Markets are continuing to price something in between the two, although since the last Fed meeting futures have been consistently closer to 75 than 50, with 69.0 bps right now.

Those sharp losses in US equities are echoing across Asia this morning. The Hang Seng (-1.86%) is leading the losses followed by the Kospi (-1.82%), the Nikkei (-1.07%) and the ASX 200 (-1.06%). Over in mainland China, the Shanghai Composite (-0.77%) and the CSI (-0.80%) are slightly out-performing after yesterday’s surprise move by China to slash the quarantine period for inbound travellers (more on this below). Looking ahead, US stock index futures point to a positive opening with contracts on the S&P 500 (+0.18%) and NASDAQ 100 (+0.19%) mildly higher.

Earlier today, data released showed that Japan’s retail sales advanced for the third consecutive month in May (+3.6% y/y) but lower than the consensus of +4.0%, but with the previous month’s data revised up to +3.1% (vs +2.9% preliminary). Meanwhile, South Korea’s consumer sentiment index (CSI) fell sharply to 96.4 in June (vs 102.6 in May), sliding below the long-term average of 100 for the first time since Feb 2021. Separately, Australia’s retail sales put in another strong performance as it climbed +0.9% m/m in May, surpassing analyst estimates of a +0.4% increase.

Oil has fallen back slightly overnight after three sessions of gains with Brent futures down -0.84% at $116.99 and WTI futures (-0.64%) at $111.04/bbl as I type.

Just after we went to press yesterday, it was also announced that China would be shortening the required quarantine period for inbound travellers to one week from two. So although China is still very-much committed to a Covid-zero strategy for the time being, this step towards loosening rather than tightening restrictions is an interesting development that helped support Chinese equities in yesterday’s session towards the close which filtered through into early northern hemisphere risk performance.

In terms of other data yesterday, there were signs that US house price growth might finally be slowing somewhat, with the S&P CoreLogic Case-Shiller index up by +20.4% in April, which is down slightly from the +20.6% gain in March. So still a long way from an absolute decline, but that marks a reversal in the trend after the previous 4 months of rises in the year-on-year measure.

To the day ahead now, and the highlight will likely be the panel at the ECB Forum that includes Fed Chair Powell, ECB President Lagarde and BoE Governor Bailey. We’ll also be hearing from ECB Vice President de Guindos, the ECB’s Schnabel, the Fed’s Mester and Bullard, and the BoE’s Dhingra. On the data side, releases include German CPI for June, Euro Area money supply for May, and the final Euro Area consumer confidence reading for June. From the US, we’ll also get the third reading of Q1 GDP.

WEDNESDAY /TUESDAY NIGHT

SHANGHAI CLOSED DOWN 47.69 PTS OR 1.40% //Hang Sang CLOSED DOWN 422.08 PTS OR 1.88% /The Nikkei closed DOWN 244.87 OR 0.91% //Australia’s all ordinaires CLOSED DOWN 1.09 /Chinese yuan (ONSHORE) closed DOWN 6.6952 /Oil UP TO 112.93 dollars per barrel for WTI and UP TO 119.20 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6952 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6990: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

end

3c CHINA

CHINA/VACCINE MANDATES.

China is nuts!!. Zero covid policy will not work, only herd immunity //natural immunity will work

(Watson/SummitNews)

China Suggests It Could Maintain ‘Zero COVID’ Policy For 5 Years

TUESDAY, JUN 28, 2022 – 06:05 PM

Authored by Paul Joseph Watson via Summit News,

China has suggested it will maintain its controversial ‘zero COVID’ policy for at least 5 years, eschewing natural immunity and guaranteeing repeated rounds of new lockdowns.

“In the next five years, Beijing will unremittingly grasp the normalization of epidemic prevention and control,” said a story published by Beijing Daily.

The article quoted Cai Qi, the Communist Party of China’s secretary in Beijing and a former mayor of the city, who said that ‘zero COVID’ approach would remain in place for 5 years.

After the story prompted alarm, reference to “five years” was removed from the piece and the hashtag related to it was censored by social media giant Weibo.

“Monday’s announcement and the subsequent amendment sparked anger and confusion among Beijing residents online,” reports the Guardian.

“Most commenters appeared unsurprised at the prospect of the system continuing for another half-decade, but few were supportive of the idea.”

Although western experts severely doubt official numbers coming out of China, Beijing claimed success in limiting COVID deaths by enforcing the policy throughout 2021.

However, this meant that China never achieved anything like herd immunity, and at one stage the Omicron variant caused more more coronavirus cases in Shanghai in four weeks than in the previous two years of the entire pandemic.

Back in May, World Health Organization Director General Tedros Adhanom Ghebreyesus suggested that China would be better off if it abandoned the policy, but Beijing refused to budge.

As we previously highlighted, the only way of enforcing a ‘zero COVID’ policy is via brutal authoritarianism.

In Shanghai, children were separated from their parents in quarantine facilities and others were left without urgent treatment like kidney dialysis.

Panic buying of food also became a common occurrence as the anger threatened to spill over into widespread civil unrest.

Former UK government COVID-19 advisor Neil Ferguson previously admitted that he thought “we couldn’t get away with” imposing Communist Chinese-style lockdowns in Europe because they were too draconian, and yet it happened anyway.

“It’s a communist one party state, we said. We couldn’t get away with it in Europe, we thought,” said Ferguson.

“And then Italy did it. And we realised we could,” he added.

* * *

Brand new merch now available! Get it at https://www.pjwshop.com/

In the age of mass Silicon Valley censorship It is crucial that we stay in touch. I need you to sign up for my free newsletter here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown. Get early access, exclusive content and behinds the scenes stuff by following me on Locals.

4/EUROPEAN AFFAIRS//UK AFFAIRS/

NATO//SWEDEN/FINLAND

NATO Issues Formal Invitation For Finland, Sweden To Join Alliance As Biden “Thanks” Erdogan

WEDNESDAY, JUN 29, 2022 – 12:25 PM

The huge development out of the Madrid NATO summit yesterday was Turkish President Recep Tayyip Erdogan dropping his veto over Finland and Sweden’s application for membership, unveiled in a joint communique issued by the three countries. Still, this major development hasn’t been much of a high priority for mainstream media coverage.

On Wednesday, NATO has issued the formal invitation for Finland and Sweden to join the alliance. An official summit declaration began as follows: “Today, we have decided to invite Finland and Sweden to become members of NATO, and agreed to sign the Accession Protocols.”

It continued: “In any accession to the Alliance, it is of vital importance that the legitimate security concerns of all Allies are properly addressed. We welcome the conclusion of the trilateral memorandum between Turkiye, Finland, and Sweden to that effect.”

At the same time, the declaration stressed that it said that it “warmly” welcomes Ukrainian President Volodymyr Zelensky’s participation in the summit “in full solidarity” with Ukraine.

While not mentioning Russia’s ‘red line’ issue of future potential Ukraine membership in the Western military alliance, the statement still spelled out that NATO “fully supports” Ukraine’s “inherent right to self-defense and to choose its own security arrangements.”

But within the document, there are “partner” countries named which is sure to be seen as immensely provocative in Moscow, particularly the invocation of the names Georgia and Moldova:

“In light of the changed security environment in Europe, we have decided on new measures to step up tailored political and practical support to partners, including Bosnia and Herzegovina, Georgia, and the Republic of Moldova. We will work with them to build their integrity and resilience, develop capabilities, and uphold their political independence,” the NATO statement said.

Also on Wednesday NATO labeled Russia the most “direct threat” facing the alliance today, and vowed to take further steps at modernizing Ukraine’s military. The alliance statement said Russia is the “most significant and direct threat to the allies’ security and stability.”

President Biden at the summit also announced a beefed up and permanent US military presence in Eastern Europe, namely in Poland. Additionally, “New US warships will go to Spain, fighter jet squadrons to Britain, ground troops to Romania, air defense units to Germany and Italy and a wide range of assets to the Baltics,” according to Biden’s announcement featured in Reuters.

“We mean it when we say an attack against one is an attack against all,” he told reporters upon meeting with NATO Secretary General Jens Stoltenberg. He said NATO will “defend every inch” of its territory.

Biden on Wednesday met with Turkish President Recep Erdogan, wherein he thanked the Turkish leader for backing Finland and Sweden’s NATO bids, after serious concessions were made regarding the Scandinavian countries willing to brand the Kurdish PKK a “terrorists organization”.

END

.

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS/

War is hell

Inbox

| Robert Hryniak | 9:50 AM (5 minutes ago) | ||

| to |

The sooner this tragic affair is over the sooner this country can get back to rebuilding… one does wonder what still remains in store for Ukrainians as their banks are systematically being looted by corruption ensuring that Russia will have to consider bailing out the financial system to prevent societal collapse when the fighting is over. One be sure that all the enablers and photo fans will become distant and silent. And Ukrainians will once again learn they are expendable, badly betrayed by Zelensky and his minions.

A very tragic affair that has been played many a time, whether it was Iraq, Afghanistan etc. and each time memory is short. This western disease in long overdue to be vaccinated as it simply does not work. The result is angst not love. It is a time for change where we become a brother’s brother and not a keeper.

6/29/22

By WarNews 24/7

translated from Greek

We have a significant development in Lisichansk as the Russian special forces became involved with mercenary forces. According to Russian military sources, there are 14 mercenaries dead and 12 prisoners.

The mercenaries come from different countries. The Russians report that there will be developments in the coming hours as “their countries of origin are quite interesting” meaning that they are Americans, British, French, etc.

Let’s not forget what exactly the New York Times revealed about the involvement of NATO commandos in Ukraine.

Military engagement of NATO commandos with Russians in Ukraine: Russian bases hit with HIMARS – NATO puts 300,000 troops on alert

Chaotic scenes are recorded in the Lisichansk region . Units of the Ukrainian Army are desperately trying to break the suffocating siege of Russian forces and escape from the city to Seversk.

Ukrainians count more than 1,000 dead in battles inside and outside the city of Lisichansk. The “Right Sector” has heavy losses while many are also prisoners.

Features are the videos you will see. Ukrainian forces try to escape from Lisichansk and shoot videos. Then they fall into an ambush and a battle with Russian paratroopers ensues.

In the fourth and the remaining videos, Russian drones locate Ukrainian military phalanxes trying to leave Lisichansk. An artillery barrage follows.

Watch videos from the moment of the escape

Chaotic scenes – 5-7,000 Ukrainians trying to escape

Lugansk Ambassador to Russia Rodion Miroshnik said Ukrainian soldiers were desperately trying to escape from Lisichansk.

“Groups of soldiers leave Lisichansk and try to cross to Seversk, where they are observed gathering.

Residents of the area say they are seeing the beginning of the withdrawal of Ukrainian armed formations from Lysichansk.

Yesterday they tried to cross from Verkhnekamenka to Seversk, but lost several phalanxes from the blows of the allied artillery and the Russian forces.

Subsequent attempts to break into our defenses were made through Belogorovka.

The reserve units of the Armed Forces of Ukraine are moving away and trying to find ways to escape from Novodruzhevka, Privolye and Shepilovo. They all leave for Seversk.

“According to sources, up to 5-7 thousand Ukrainians can be transferred to Seversk , ” Miroshnik said.

12 mercenaries captured in Lisichansk

More than 10 foreign mercenaries have reportedly been captured near Lisichansk.

Lugansk forces arrested more than 10 foreign mercenaries near Lisichansk trying to escape the besieged city. This was reported by Russian media, citing Lugansk Deputy Assistant Interior Minister Vitaly Kiselev.

“We caught 12 people near Lisichansk of different nationalities, different countries. “In the near future, I will tell you exactly how many of them and from which countries these mercenaries are,” says Kiselev.

The captured mercenaries also reportedly took part in the battles in Rubizhne and Severodonetsk.

Kiselev noted that foreign mercenaries, according to the Geneva Convention, are not entitled to the status of a fighter or a prisoner of war.

The Russian army killed 14 mercenaries

The Russian Defense Ministry said that the Ukrainian administration is trying to stop the chaotic flight of Ukrainian military units in the Lisichansk region.

According to the Russian YPAM:

In order to retain the personnel of the first battalion of the 72nd Mechanized Brigade of the Armed Forces of Ukraine in the area of the settlement Volcheyarovka, a “detachment” of the Nazi formation “Right Sector” was sent to these positions.

This unit was destroyed by Russian artillery.

Control of Ukrainian troops in the direction of Lysychansk is lost.

The commander of the 115th Mechanized Brigade of the Armed Forces of Ukraine lost control of his units, which led to the irreparable loss of 80% of the personnel and about 70% of the equipment of the 138th Battalion of this brigade during the battles.

On June 26, during the fighting, 3 km from the Lisichansk oil refinery, Russian units destroyed two groups of mercenaries carrying out a sabotage and reconnaissance operation with a total of 14 soldiers.

The first group was “international” and consisted of citizens of various European countries. The second – included only mercenaries from Georgia, who were part of the so-called “Georgian Legion”.

In the ranks of this formation fight mainly criminals.

The killed Georgian fighters are involved in the brutal torture and killing of Russian soldiers near Kyiv in March this year.

“The Russian Ministry of Defense has information about every mercenary involved in the abuse and killing of our soldiers. “We found them and punished them,” said Defense Ministry spokesman Lt. Gen. Igor Konashenkov.

Several videos at Source:

https://warnews247.gr/chaotikes-skines-sto-lisichansk-sklires-maches-roson-me-misthoforous-14-nekroi-kai-12-aichmalotoi-pano-apo-1000-nekroi-oukranoi/

Cheers

Robert

end

GLOBAL ISSUES AND COVID COMMENTARIES

Hepatitis should never occur in children. Now more than 900 cases have been reported and no doubt that these children have been vaccinated

a must read.

(Lorenz Duchamps/EpochTimes)

More Than 900 Cases Of Hepatitis Of Unknown Origin Reported In Children, WHO Says

WEDNESDAY, JUN 29, 2022 – 05:00 AM

Authored by Lorenz Duchamps via The Epoch Times (emphasis ours),